Table of Contents

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| For the fiscal year ended December 31, 2005, or |

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| For the transition period from to |

Commission File No.: 001-16753

AMN HEALTHCARE SERVICES, INC.

(Exact Name of Registrant as Specified in Its Charter)

| Delaware | 06-1500476 | |

| (State or Other Jurisdiction of Incorporation or Organization) |

(I.R.S. Employer Identification No.) | |

| 12400 High Bluff Drive, Suite 100 San Diego, California |

92130 | |

| (Address of principal executive offices) | (Zip Code) | |

Registrant’s Telephone Number, Including Area Code: (866) 871-8519

Securities registered pursuant to Section 12(b) of the Act:

| Title of Each Class | Name of each exchange on which registered | |

| Common Stock, $0.01 par value |

New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act:

None.

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes þ No ¨

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act. Yes ¨ No þ

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes þ No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. þ

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See definition of “accelerated filer and large accelerated filer” in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer ¨ Accelerated filer þ Non-accelerated filer ¨

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No þ

The aggregate market value of the voting and non-voting common equity held by non-affiliates computed by reference to the price at which the common equity was last sold, or the average bid and asked price of such common equity, as of June 30, 2005 was $425,716,258 based on a closing sale price of $15.03 per share.

As of March 9, 2006, there were 32,130,241 shares of common stock, $0.01 par value, outstanding.

Documents Incorporated By Reference: Portions of the registrant’s definitive Proxy Statement for the annual meeting of shareholders to be held on April 12, 2006 have been incorporated by reference into Part II and Part III of this Form 10-K.

Table of Contents

| Item |

Page | |||

| PART I | ||||

| 1. |

Business | 1 | ||

| 1A. |

Risk Factors | 12 | ||

| 1B. |

Unresolved Staff Comments | 18 | ||

| 2. |

Properties | 18 | ||

| 3. |

Legal Proceedings | 18 | ||

| 4. |

19 | |||

| PART II | ||||

| 5. |

20 | |||

| 6. |

21 | |||

| 7. |

Management’s Discussion and Analysis of Financial Condition and Results of Operations |

23 | ||

| 7A. |

35 | |||

| 8. |

36 | |||

| 9. |

Changes In and Disagreements With Accountants on Accounting and Financial Disclosure |

65 | ||

| 9A. |

65 | |||

| 9B. |

67 | |||

| PART III | ||||

| 10. |

68 | |||

| 11. |

68 | |||

| 12. |

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters |

68 | ||

| 13. |

68 | |||

| 14. |

68 | |||

| PART IV | ||||

| 15. |

Exhibits and Financial Statement Schedules | 69 | ||

| Signatures | 75 | |||

i

Table of Contents

PART I

| Item 1. | Business |

Our Company

AMN Healthcare Services, Inc. “AMN”, is the largest temporary healthcare staffing company in the United States. As the leading nationwide provider of travel nurse staffing services and a leading provider of locum tenens (temporary physician staffing) and physician permanent placement services, we recruit physicians, nurses and allied health professionals, our “healthcare professionals,” nationally and internationally and place them on variable lengths of assignments and in permanent positions at acute-care hospitals, physician practice groups and other healthcare facilities throughout the United States. With the acquisition of The MHA Group, Inc., and its subsidiaries (“MHA”) on November 2, 2005, we expanded our service lines to include temporary and permanent physician staffing and clearly distinguished AMN as the largest healthcare staffing company.

Our staffing services are marketed to two distinct customer bases: (1) healthcare professionals and (2) hospital and healthcare facilities. We use a multi-brand recruiting strategy to enhance our ability to successfully attract nursing and allied healthcare professionals in the United States and internationally. We market our nurse and allied healthcare professional staffing to our healthcare professionals under recruitment brands including American Mobile Healthcare, Medical Express, NurseChoice InDemand, NursesRx, Preferred Healthcare Staffing, Thera Tech Staffing, Med Travelers, RN Demand, and O’Grady Peyton International. Each brand has distinct clinician focus, market strengths and brand reputation. We market our travel nursing services to hospitals and healthcare facilities under one brand, AMN Healthcare, as a single staffing provider with access to healthcare professionals from several recruitment brands. We market allied services to our clients under the brand names Thera Tech Staffing and Med Travelers, and we market long term nursing services to our clients under the brand name O’Grady Peyton International. We market our locum tenens and physician permanent placement services under the brand names Staff Care, Inc. and Merritt, Hawkins & Associates, respectively, to both healthcare professionals and hospital and healthcare facilities and physician staffing groups.

At the end of 2005, we had healthcare professionals on assignment at over 1,500 different healthcare facility clients. We provide services to acute-care and sub-acute healthcare facilities, physician groups, dialysis centers, clinics and schools. Our hospital and healthcare facility clients utilize our services to cost-effectively manage shortages in their staff due to a variety of circumstances such as attrition, new unit openings, seasonal patient census variations, the physician and nurse staffing shortage and other short and long-term staffing needs. In addition to providing continuity of care and quality patient care, we believe hospitals and healthcare facilities contract with us due to our skilled permanent and temporary healthcare professionals, our ability to meet their specific staffing needs, our flexible staffing assignment lengths, our reliable and superior customer service, our ability to offer a large national network of permanent and temporary healthcare professionals and our ability to provide temporary staffing solutions while we assist the client in filling physician permanent staffing needs.

Physicians, nurses and allied healthcare professionals join us on temporary assignments for a wide variety of reasons that include: seeking flexible work opportunities, exploring different areas of the country, building their clinical skills and resume by working at prestigious healthcare facilities, escaping the demands and political environment of working as a permanent staff and working through life and career transitions.

Our large number of hospital and healthcare facility clients provides us with the opportunity to offer temporary or permanent positions in all 50 states and in a variety of work environments and clinical settings. In addition, we provide our temporary healthcare professionals with an attractive benefits package that may include free or subsidized housing, free or reimbursed travel, competitive wages, professional development opportunities, a 401(k) plan, and health and professional liability insurance. We believe that we attract temporary healthcare professionals due to our long-standing reputation for providing a high level of service, our numerous job opportunities, our benefit packages, our innovative marketing programs and word-of-mouth referrals from our thousands of current and former healthcare professionals.

1

Table of Contents

Industry Overview

Total healthcare expenditures in the United States were estimated at $1.9 trillion during 2005, representing approximately 15.6% of the U.S. gross domestic product, and grew approximately 7% over 2004 according to the Centers for Medicare & Medicaid Services. Over the next decade, an aging U.S. population and advances in medical technology are expected to drive increases in hospital patient populations and the consumption of healthcare services. As a result, total healthcare expenditures are projected to increase to approximately $3.6 trillion by 2014.

The temporary healthcare staffing industry accounted for approximately $10.0 billion in revenue in 2005 according to estimates by The Staffing Industry Report, and is comprised of approximately 62% nurse staffing, 12% locum tenens, and the balance in allied health and other healthcare professional staffing. The temporary healthcare staffing industry was estimated to have grown at 2.5% in 2005 and has grown each year at a compound annual growth rate of approximately 9% since 1997, except during 2003 and 2004 when the industry declined on an annual basis. We believe that the decline during 2003 and 2004 reflected hospitals’ increased focus on internal nurse recruitment efforts, over-utilization of permanent labor staff and greater reliance on cost control efforts to reduce outsourced staffing solutions. In 2005, increased job turnover among permanent staff at the hospitals contributed to higher utilization of temporary nurses.

We expect the temporary healthcare staffing industry to grow modestly in 2006 based on favorable economic conditions and an increase in hospital staff job openings and turnover. While this growth is expected to be positive and expand the opportunities available to healthcare professionals, the available supply of professionals is not expected to keep pace with the increase in demand.

Competition

The healthcare staffing industry is highly competitive. We compete in national, regional and local markets with full-service staffing companies and specialized temporary staffing agencies for both healthcare professionals and hospital and healthcare facility clients. We also compete with hospital systems that have developed their own recruitment departments and interim staffing pools to attract highly qualified healthcare professionals. We compete for these healthcare professionals on the basis of customer service and expertise, the quantity, diversity and quality of available assignments, compensation packages and, for our temporary nurses and allied healthcare professionals, the benefits that we provide to them while they are on assignment. We compete with other staffing companies for hospital and healthcare facility clients on the basis of the quality of our healthcare professionals, the timely availability of our professionals with requisite skills, the quality, breadth and price of our services, our customer service, our recruitment expertise and the geographic reach of our services.

We believe that larger, national firms enjoy distinct competitive advantages over smaller, local and regional competitors in the healthcare staffing industry. More established firms have a larger pool of available candidates, substantial word-of-mouth referral networks and more recognizable brand names, enabling them to attract a consistent flow of new applicants. Larger firms also generally have a deeper, more comprehensive infrastructure with a more established business framework and processes that provide the foundation for national recognition, such as the Joint Commission on Accreditation of Healthcare Organizations (JCAHO) staffing agency certification. The greater financial resources of these larger firms also make it relatively easier to provide payroll and housing services for its temporary healthcare professionals, which is cash flow intensive.

Some of our competitors in the temporary nurse and locum tenens staffing sector include Cross Country Healthcare, InteliStaf Healthcare, CHG Healthcare Services, Inc., On Assignment, and Medical Doctor Associates.

2

Table of Contents

Demand and Supply Drivers

Demand Drivers

| • | Demographics and Advances in Medicine and Technology. As the U.S. population ages and medical technology advances result in longer life expectancy, it is likely that chronic illnesses and hospital populations will continue to increase. We believe that these factors will increase the demand for both temporary and permanent healthcare professionals. In addition, enhanced healthcare technology has increased the demand for specialty physicians and nurses who are qualified to operate advanced medical equipment and perform complex medical procedures. |

| • | Increased Hospital Revenue Opportunity. Hospital and healthcare facilities’ primary revenue source is generated by physicians. By using permanent physician search and locum tenens services to fill vacancies quicker, hospitals and healthcare facilities can generate additional revenue. With more physicians on staff, healthcare facilities have a need for more nurses and allied healthcare professionals to support the increased patient census. |

| • | Shift to Flexible Staffing Models. Nurse wages comprise the largest percentage of hospitals’ labor expenses. Cost containment initiatives and a focus on cost-effective healthcare service delivery may lead more hospitals and other healthcare facilities to adopt adjustable staffing models that include utilization of flexible staffing resources such as temporary healthcare professionals. |

| • | Physician and Nursing Shortage. Most regions of the United States are experiencing a pronounced shortage of physicians and registered nurses. The Bureau of Labor Statistics projects that the incremental job openings for physicians and surgeons from 2002 to 2012 will be 114,000, an increase of 19.5% over ten years. The U.S. Department of Health and Human Services reported that the registered nurse workforce is expected to be 29% below projected requirements by 2020. Faced with increasing demand and tight supply for physicians and nurses, hospitals are utilizing more temporary physicians and nurses to meet staffing requirements. Factors contributing to the supply shortage of healthcare professionals include: |

| — | Changes in Physician and Nurse Population. Approximately 30% of all physicians are 55 years and older and approximately 38% are considering retirement in the next one to three years. The average age of a registered nurse was estimated to be 47 years old in 2004, an increase of 10.6% since 1996. |

| — | Shortage of Medical and Nursing Schools. As a result of a shortage of qualified faculty and limited availability of medical and nursing schools to prospective healthcare professionals, the number of medical school and nursing school graduates is well below the number of new healthcare professionals needed in order to eliminate the projected shortage. |

| — | Nurses Leaving Patient Care Environments for Less Stressful and More Flexible Careers. Career opportunities for nurses have expanded beyond the traditional bedside role. Pharmaceutical companies, insurance companies, HMOs and hospital service and supply companies increasingly offer nurses attractive positions which involve less demanding work schedules and more varied career progression and opportunity. |

| — | Physicians Leaving Practices Due to Increased Burdens of Malpractice Insurance and Medical Insurance Reimbursement. Physicians are increasingly concerned over reimbursement levels from insurance companies and government agencies and mounting claims billing restrictions and paperwork. In addition, malpractice premiums have been increasing over the last several years. |

3

Table of Contents

| • | Seasonality. Hospitals in regions that experience significant seasonal fluctuations in population, such as Florida or Arizona during the winter months, must be able to efficiently adjust their staffing levels to accommodate the change in patient census. Many of these hospitals utilize temporary healthcare professionals to satisfy these seasonal staffing needs. |

| • | State Legislation Requiring Healthcare Facilities to Utilize More Nurses. In response to concerns by nursing and consumer organizations over the quality of care provided in healthcare facilities and the increased workloads and pressures placed upon nurses, legislation has been introduced at both the federal and state level that is expected to increase the demand for nurses by requiring minimum nurse-to-patient ratios. Specifically, effective from January 2004, California hospitals have been required to staff units at government mandated nurse-to-patient ratios. New Jersey has enacted legislation requiring hospitals to post daily staffing information including nurse-to-patient ratios for each unit and shift, and to provide this information upon request by a member of the public. Illinois, Hawaii, Rhode Island, Florida, New Jersey and Iowa have also introduced legislation for minimum nurse-to-patient ratios in various healthcare settings. |

Supply Drivers

| • | Traditional Reasons for a Healthcare Professional to Work on a Temporary Assignment. Temporary staffing allows healthcare professionals to explore new areas of the United States, work at prestigious hospitals, learn new skills, manage work/life balance, build their resumes, try out different clinical settings, allow for a transitional period between permanent jobs and avoid unwanted workplace politics that may accompany a permanent position. Other benefits to temporary healthcare professionals could include free or subsidized housing, competitive wages, professional liability insurance coverage, professional development opportunities, health insurance and completion bonuses for some assignments. All of these opportunities have been constant supply drivers which continue to attract new healthcare professionals into our industry. |

| • | Word-of-Mouth Referrals. New applicants are often referred to staffing companies by other healthcare professionals who have taken temporary assignments with or been placed in a permanent position by the Company. Growth in the number of healthcare professionals who are working on temporary assignments or have been placed in permanent positions by a staffing agency, as well as the increased number of hospital and healthcare facilities that utilize temporary healthcare professionals, creates more opportunities for referrals. |

| • | More Physicians Choosing Temporary Staffing Due to the Physician Shortage, Increased Reimbursement and Malpractice Concerns. Locum tenens provides physicians the opportunity to practice medicine without concern for malpractice costs or having to worry about insurance reimbursement. In addition, the current and expected physician shortage allows physicians to practice medicine with confidence that they can explore other clinical settings and be secure about future permanent employment. |

| • | More Nurses Choosing Traveling Due to the Nursing Shortage and Improving Economy. In times of nursing shortages and an improving economy, nurses with permanent jobs generally feel more secure about their employment prospects. They have a higher degree of confidence that they can leave their permanent position to take a travel assignment and have the ability to return to a permanent position in the future. Additionally, during a nursing shortage, permanent staff nurses are often required to assume greater responsibility and patient loads, work overtime and deal with increased pressures within the hospital. Consequently, many experienced nurses choose to leave their permanent employer and look for a more flexible and rewarding position. |

| • | Legislation Allowing Nurses to Become More Mobile. The Mutual Recognition Compact Legislation, promoted by the National Council of State Boards of Nursing, allows nurses to work more freely within states participating in the Compact Legislation without obtaining new state licenses. The recognition legislation began in 1999 and has been enacted in 20 states as of February 2006. |

4

Table of Contents

Growth Strategy

Our goal is to expand our leadership position within the healthcare staffing sector in the United States. The key components of our business strategy include:

| • | Strengthening and Expanding Our Relationships with Hospitals and Healthcare Facilities. We continue to strengthen and expand our existing relationships with our hospital and healthcare facility clients and to develop new relationships. Hospitals and healthcare facilities are seeking a strong business partner for outsourcing and recruiting who can fulfill the quantity, breadth and quality of their staffing needs and help them develop strategies for the most cost-effective staffing methods. In addition, over the last few years, hospitals and healthcare facilities have shown an interest in working with a limited number of vendors to increase efficiency. We believe that our size and proven ability to fill our clients’ staffing needs provide us with the opportunity to serve our client facilities that implement this vendor consolidation strategy. In addition, our recent acquisition of MHA has broadened the type of services we offer and will allow us to provide a more comprehensive staffing solution to our clients. Because we possess one of the largest national networks of available physician, nurse and allied health professionals, we are well positioned to offer our hospital and healthcare facility clients a wide spectrum of effective solutions to meet their staffing needs. |

| • | Expanding Our Network of Qualified Healthcare Professionals. Through our recruiting efforts both in the United States and internationally, we continue to expand our network of qualified healthcare professionals. We continue to build our supply of healthcare professionals through referrals from healthcare professionals who are currently working or have been placed by us in the past, as well as through advertising and internet sources. We have also conducted several research initiatives to assist us in segmenting the population of healthcare professionals and developed targeted advertising campaigns directed at these different segments. |

| • | Leveraging Our Business Model and Large Hospital and Healthcare Facility Client Base to Increase Productivity. We seek to increase our productivity through our proven multi-brand recruiting strategy, large network of healthcare professionals, established hospital and healthcare facility client relationships, proprietary information systems, innovative marketing and recruitment programs, training programs and centralized administrative support systems. Our multi-brand recruiting strategy for temporary nurses generally allows a recruiter in any of our nurse staffing brands to take advantage of all of our nationwide placement opportunities. In addition, our information systems and operational support and customer service personnel permit our recruiters to spend more time focused on the placement of our healthcare professionals. |

| • | Expanding Service Offerings Through New Staffing Solutions. In order to further enhance the growth in our business and improve our competitive position in the healthcare staffing sector, we continue to introduce new service offerings. As our hospital and healthcare facility clients’ needs change, we constantly explore what additional services we can provide to better serve them. During 2005, we introduced NurseChoice In Demand to address hospitals’ urgent need for registered nurses and, through our recent acquisition of MHA, we have significantly expanded and differentiated our service offerings by entering the physician staffing sector. |

| • | Providing Innovative Technology. We continue to be an innovation leader in healthcare staffing by providing on-line services and tools to both our hospital and healthcare facility clients and our healthcare professionals. Our on-line resource, Staffing Service Center, provides online resources for hospital and healthcare facility clients to streamline their communications and process flow to secure and manage staffing services. Another on-line resource, The Traveler Service Center, provides an on-line self-service resource for our healthcare professionals to track assignment information and complete key forms electronically. Both sites offer secure access and self-service features twenty-four hours a day, seven days a week. |

5

Table of Contents

| • | Building the Strongest Management Team to Optimize Our Business Model. In addition to a tenured senior sales and operations management team, we have continued to focus on training and professional development for all levels of management and have hired several additional experienced management members over the last few years. Our management team has been further broadened and strengthened through the addition of the MHA leadership team. |

| • | Capitalizing on Strategic Acquisition Opportunities. In order to enhance our competitive position, we will continue to selectively explore strategic acquisitions. After acquisitions, we have sought to leverage our hospital relationships and orders across our brands, integrate back-office functions and maintain brand differentiation for temporary healthcare professional recruitment purposes. While we intend to operate our recently acquired physician staffing businesses relatively separate from our nurse and allied businesses, we believe we have opportunities to cross-sell our comprehensive staffing solution to our hospital and healthcare facility clients and integrate certain back-office functions. |

Business Overview

Services Provided

Nurse and Allied Healthcare Staffing Segment

Hospitals and healthcare facilities generally obtain supplemental staffing for nurses and allied healthcare professionals from two external sources, local temporary (per diem) agencies and regional and national travel healthcare staffing companies. Per diem staffing involves the placement of locally based healthcare professionals on daily shift work on an as needed basis. Hospitals and healthcare facilities often give only a few hours notice of their per diem assignments, which require a quick turnaround from their staffing agencies of generally less than 24 hours. Travel staffing, on the other hand, has historically provided hospital and healthcare facilities with staffing solutions to address anticipated or longer-term staffing requirements, typically for 4 to 26 weeks. In contrast to per diem agencies, travel staffing companies select from a national (and in some cases international) skilled labor pool and provide pre-screened candidates to their hospital and healthcare facility clients, typically at a lower cost. Historically, we have focused on the travel segment of the temporary healthcare staffing industry for our nurse and allied healthcare professionals. In addition, we have expanded our service offerings to include assignment lengths of 2 weeks to 24 months placing both domestic and international healthcare professionals.

Nurses. We provide medical nurses, surgical nurses, specialty nurses, licensed practical or vocational nurses and advanced practice nurses in a wide range of specialties for travel assignments throughout the United States. We place our qualified nurse professionals with premier, nationally recognized hospitals and hospital systems. The majority of our assignments are in acute-care hospitals, including teaching institutions, trauma centers and community hospitals. Nurses comprise approximately 93% of the total nurse and allied health temporary healthcare professionals working for us. We typically place the majority of our nurses on 13-week assignments with hospitals and healthcare facilities under our AMN Healthcare brand. We also offer a longer-term staffing solution under our O’Grady Peyton International brand, typically 18 months, using our English speaking international nurses that we recruit primarily from foreign countries. During 2005, we launched a differentiated new service offering, NurseChoice InDemand, to address hospitals’ urgent need for registered nurses. NurseChoice InDemand is targeted to recruit and staff nurses who can begin assignments within one to two weeks in acute-care facilities in contrast to the three to five week lead time that may be required for travel nurses. Typical assignments are four to eight weeks and provide premium compensation packages to nurses.

Allied Health Professionals. We also provide allied health professionals under our Med Travelers and Thera Tech Staffing brands to acute-care hospitals and other healthcare facilities such as skilled nursing facilities, rehabilitation clinics and schools. Allied health professionals include such disciplines as physical therapists, surgical technologists, respiratory therapists, medical and radiology technologists, dialysis technicians, speech pathologists and rehabilitation assistants. Allied health professionals comprise approximately 7% of the total nurse and allied health temporary healthcare professionals working for us.

6

Table of Contents

Physician Staffing Segment

Hospitals, physician groups and healthcare facilities generally obtain physicians from two sources, permanent hire and outsourced temporary physician staffing. We provide both temporary and permanent physician staffing services.

Locum Tenens. We place physicians of all specialties on a temporary basis (locum tenens) under our Staff Care brand as independent contractors with all types of healthcare organizations throughout the United States, including hospitals, medical groups, occupational medical clinics, individual practitioners, networks, psychiatric facilities, government institutions, and managed care entities. Physicians are recruited nationwide and typically placed on multi-week contracts. While assignments can range from a few days up to one year, the average is 8 weeks in duration. The locum tenens business comprises approximately 84% of our total physician staffing segment based on revenue.

Permanent Placement. We provide permanent physician placement services under our Merritt, Hawkins & Associates brand to medical facilities throughout the United States. Our broad specialty offerings include over 40 specialist and sub-specialist opportunities. Permanent physician placement comprises approximately 16% of our total physician staffing segment based on revenue.

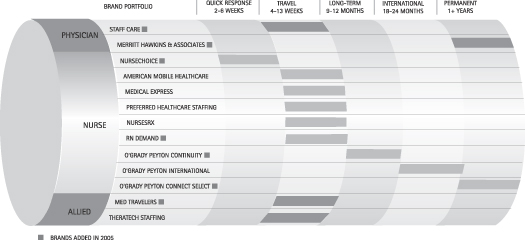

Offering Comprehensive Healthcare Staffing Solutions

We employ a focused marketing strategy for our hospital and healthcare facility clients and market and administer the majority of our nursing services under the single corporate brand of AMN Healthcare. Our physician, allied and international staffing services are marketed to our hospital and healthcare facility clients under their respective brands.

The following chart depicts our comprehensive healthcare staffing capabilities and focus on critical staffing needs:

National Presence and Diversified Hospital and Healthcare Facility Client Base

We offer our healthcare professionals nationwide placement opportunities and provide staffing solutions to our hospital and healthcare facility clients that are located throughout the United States. We typically generate revenue in all 50 states. During 2005, the largest percentages of our revenue were concentrated in California, Arizona, Florida, New York, North Carolina and Massachusetts. Our physician permanent placement market has

7

Table of Contents

significant growth potential due to the increasing demand for physicians and the ability to cross-sell permanent placement services through our temporary service relationships. Our physician permanent placement brand, Merritt Hawkins & Associates has conducted over 30,000 physician search assignments since its founding and has worked in all 50 states.

We had temporary healthcare professionals on assignment at over 1,500 different healthcare facility clients at the end of 2005. The majority of our temporary healthcare professional assignments are at acute-care hospitals. In addition to acute-care hospitals, we provide services to sub-acute healthcare facilities, physician groups, dialysis centers, clinics and schools. Our clients include hospitals and healthcare systems such as Georgetown University Hospital, HCA, NYU Medical Center, Stanford Health Care, UCLA Medical Center and The University of Chicago Hospitals. No single client healthcare system comprised more than 10% of revenue and no single client facility comprised more than 3% of revenue for the year ended December 31, 2005.

Our Business Model

We have developed and continually refined our business model to achieve greater levels of productivity and efficiency. Our model is designed to optimize the communication with, and service to, both our healthcare professionals and our hospital and healthcare facility clients.

Marketing and Recruitment of New Healthcare Professionals

We believe that physician, nursing and allied health professionals are attracted to us because of our customer service and relationship-oriented approach, our competitive compensation and benefits package, and our large and diverse offering of work assignments that provide the opportunity to work at numerous attractive locations throughout the United States. We believe that our multi-brand recruiting strategy makes us more effective at reaching a larger number of healthcare professionals.

Screening, Licensing and Quality Management

Through our quality management and assurance departments, we screen all candidates prior to placement, and we continue to evaluate our temporary healthcare professionals after they are placed to ensure adequate performance and manage risk, as well as to determine feasibility for future placements. Our internal processes are designed to ensure that our healthcare professionals have the appropriate experience, credentials and skills for the assignments that they accept. Our experience has shown us that well-matched placements result in satisfied healthcare professionals and healthcare facility clients.

Sales, Marketing and Account Management

We market our nursing services to hospitals and healthcare facilities generally under one corporate brand name, AMN Healthcare, a single staffing provider with several recruitment sources of healthcare professionals. We utilize a team approach to service our hospital and healthcare facility clients. This team includes the Regional Client Service Director, Hospital Account Manager, Quality Management, and Clinical Liaison. We market our temporary and permanent physician placement services under the brand names Staff Care, Inc. and Merritt, Hawkins and Associates, respectively. We have a large base of professionals marketing our physician staffing services to our clients who make thousands of client contacts each month.

Placement

For the nurse and allied healthcare staffing segment, generally, orders are entered into our information network by our hospital account managers and are available to the recruiters at all of our recruitment brands.

8

Table of Contents

The hospital account managers develop a relationship with the healthcare facility, arrange telephone interviews between the temporary healthcare professional and the hospital, and confirm offers and placements with the hospital or healthcare facility. At the same time, our recruiters seek to develop and maintain strong and lasting relationships with our healthcare professionals.

In the case of our international temporary healthcare professionals, the recruiters and placement coordinators at our O’Grady Peyton International brand, including those located in the United Kingdom, Australia and South Africa, assist candidates in preparing for the United States nursing examination and subsequently obtaining a U.S. nursing license. These recruiters and other staff also assist our international temporary healthcare professionals to obtain petitions to become lawful permanent residents prior to their arrival in the United States. Our international temporary healthcare professionals are typically placed on longer-term, 18-month assignments as a result of our substantial investment in bringing them to work in the United States. Near completion of the 18-month assignment, our recruiters will work with these temporary healthcare professionals to explore their options for new assignments.

For the physician staffing segment, orders for temporary physicians or permanent placement requests are generated by our national marketing team. Our national presence and infrastructure enable us to provide physicians with a variety of attractive client locations, perquisites and opportunities for career development. Our recruiters and account representatives work together using proprietary information systems to fill orders and schedule physicians on temporary assignments. Our permanent placement recruiters work closely with our clients and marketing team to recruit and fill permanent placement requests. We also have the ability to cross-sell our permanent placement and temporary placement services to our clients.

Housing and Support Services

We offer substantially all of our temporary healthcare professionals free or subsidized housing while on assignment. For our nurse and allied placements, housing expenses are typically included in the hourly or weekly fees that we charge to our hospital and healthcare facility clients. For our locum tenens placements, housing costs are typically billed separately. We negotiate contracts with national property management and furniture rental companies to leverage our size and obtain more favorable pricing and terms.

Temporary Healthcare Professional Compensation

During 2005, approximately 94% of our working temporary healthcare professional employees were compensated directly by us, while approximately 6% were paid directly by the hospital or healthcare facility client.

Temporary Healthcare Professional Benefits

In our effort to attract and retain highly qualified temporary healthcare professionals, we offer a variety of benefits. These benefits may include: travel reimbursement; group medical, dental and life insurance; referral bonuses; completion bonuses; 401(k) plan and dependent care and medical reimbursement; and free continuing education.

Hospital Billing

To accommodate the needs of our hospital clients, for temporary healthcare professional staffing, we offer two types of billing: hours and days worked contracts and flat fee contracts. During 2005, we billed approximately 94% of working nurse and allied healthcare professionals based on hours and days worked contracts and approximately 6% based on flat rate contracts, and we billed substantially all of the working temporary physicians based on hours and days worked contracts.

9

Table of Contents

Hours and Days Worked Contracts. Under hours and days worked contracts, the temporary healthcare professional is either our employee for payroll and benefits purposes or an independent contractor paid directly by us on behalf of the hospital and healthcare facility clients. Under this arrangement, we bill our hospital and healthcare facility clients at an hourly or daily rate that effectively includes reimbursement for recruitment fees, compensation and benefits for the temporary healthcare professional and any applicable employer taxes. Housing or travel expenses are either included in the rate or billed separately. Overtime, shift differential and holiday hours worked are typically billed at a premium rate. In turn, we pay the temporary healthcare professional’s wages or contracted fees, housing and travel costs and benefits. Providing payroll services is a value-added and convenient service that hospitals and healthcare facilities generally expect from their supplemental staffing sources.

Flat Rate Contracts. With flat rate contracts, the temporary healthcare professional is compensated directly by the hospital or healthcare facility. We bill the hospital a “flat” weekly rate that includes reimbursement for recruitment fees, temporary healthcare professional benefits and typically housing expenses, which may be billed separately.

Information Systems

Our primary management information and communications systems are centralized and controlled in our corporate headquarters in San Diego, CA for nursing and in the MHA headquarters in Irving, TX for physicians. Our financial and payroll systems are centralized at these headquarters and our operational reporting is standardized at all of our offices.

We have developed and currently operate proprietary information systems that include integrated processes for healthcare professional and healthcare facility contract management, matching of healthcare professionals with clients and assignments, healthcare professional file submissions for placements, quality management tracking, controlling compensation packages and managing healthcare facility contract and billing terms. These systems provide our staff with fast, detailed information regarding individual healthcare professionals and hospital and healthcare facility clients.

Risk Management

We have developed an integrated risk management program that focuses on loss analysis, education and assessment in an effort to reduce our operational costs and risk exposure. We regularly analyze our losses on professional liability claims and workers compensation claims to identify trends. This allows us to focus our resources on those areas that may have the greatest impact on us and adjust our sales and operational approach to these areas. We have also developed educational materials for distribution to our temporary healthcare professionals that are targeted to address specific work-injury risks and documentation of clinical events.

In addition to our proactive measures, we engage in a peer review process of any incidents involving our temporary nurses and allied healthcare professionals. Upon notification of a nurse or allied healthcare professional’s involvement in an incident that may result in liability for us, our corporate team of registered nurses reviews the healthcare professional’s actions. Our peer review committee makes a prompt determination regarding whether the healthcare professional will continue the assignment and whether we will place him/her on future assignments. We also rely on our hospital and healthcare facility clients and the state professional associations’ investigation of incidents in determining continued and future assignments.

Regulation

The healthcare industry is subject to extensive and complex federal and state laws and regulations related to professional licensure, conduct of operations, payment for services and payment for referrals. Our business, however, is not directly impacted by or subject to the extensive and complex laws and regulations that generally

10

Table of Contents

govern the healthcare industry. The laws and regulations that are applicable to our hospital and healthcare facility clients could indirectly impact our business to a certain extent, but because we provide services on a contract basis and are paid directly by our hospital and healthcare facility clients, we do not have any direct Medicare or managed care reimbursement risk.

Some states require state licensure for businesses that employ, assign and/or place healthcare personnel to provide healthcare services at hospitals and other healthcare facilities. We are currently licensed in states that require such licenses and take measures to ensure compliance with all material state licensure requirements. In addition, we received our JCAHO Corporate Certification for AMN Healthcare and the nurse and allied brands of American Mobile Healthcare, Medical Express, NursesRx, Preferred Healthcare Staffing and Thera Tech Staffing based on a review of our compliance with national standards during the second quarter of 2005. We were the first healthcare staffing firm in the country to receive the prestigious JCAHO Certification as a corporate system with multiple staffing sites.

Most of the temporary healthcare professionals that we employ or independently contract with are required to be individually licensed or certified under applicable state laws. We take prudent steps to ensure that our healthcare professionals possess all necessary licenses and certifications.

We recruit nurses from Canada for placement in the United States. Canadian nurses can come to the United States on TN Visas under the North American Free Trade Agreement. TN Visas are renewable, one-year temporary work visas, which generally allow entrance into the United States provided the nurse presents at the border proof of waiting employment in the United States, evidence of the necessary healthcare practice licenses and a visa credentials assessment from the Commission on Graduates of Foreign Nursing Schools.

With respect to our recruitment of international temporary healthcare professionals through our O’Grady Peyton International brand, we must comply with certain United States immigration law requirements, including the Illegal Immigration Reform and Immigrant Responsibility Act of 1996. We primarily bring healthcare professionals to the United States as immigrants, or lawful permanent residents (commonly referred to as “green card” holders). We screen foreign healthcare professionals and assist them in preparing for the national nursing examination and subsequently obtaining a U.S. nursing license. We file petitions with the United States Citizenship and Immigration Service for a healthcare professional to become a permanent resident of the United States or obtain necessary work visas. Generally, such petitions are accompanied by proof that the healthcare professional has either passed the Commission on Graduates of Foreign Nursing Schools Examination or holds a full and unrestricted state license to practice professional nursing, as well as a contract between us and the healthcare professional demonstrating that there is a bona fide job offer.

Employees

As of December 31, 2005, we had approximately 1,700 corporate employees. During the fourth quarter of 2005, we had an average of over 6,500 nurse and allied healthcare professionals working on assignment. Since our acquisition of MHA on November 2, 2005 through December 31, 2005, days filled by our physician independent contractors totaled 29,570. Days filled is calculated by dividing the physician independent contractor hours filled during the period by 8 hours.

Additional Information

We maintain a corporate website at www.amnhealthcare.com/investors. Our Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K and amendments to these reports, are made available, free of charge, through this website as soon as reasonably practicable after being filed with or furnished to the Securities and Exchange Commission. The information found on our website is not part of this or any other report we file with or furnish to the Securities and Exchange Commission.

11

Table of Contents

| Item 1A. | Risk Factors |

The following risk factors should be read carefully in connection with evaluating us and the forward-looking statements contained in this Annual Report on Form 10-K. Any of the following risks could materially adversely affect our company, operating results, financial condition and the actual outcome of matters as to which forward- looking statements are made in this Annual Report on Form 10-K. Certain statements in “Risk Factors” constitute “forward-looking statements.” Our actual results could differ materially from those projected in the forward-looking statements as a result of certain factors and uncertainties set forth below and elsewhere in this Annual Report on Form 10-K. See “Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations—Special Note Regarding Forward-Looking Statements.”

If we are unable to continue to recruit and retain healthcare professionals for our healthcare staffing business at reasonable costs, it could increase our operating costs and negatively impact our business.

We rely significantly on our ability to recruit and retain healthcare professionals who possess the skills, experience and licenses necessary to meet the requirements of our hospital, healthcare facility clients and physician practice groups. We compete for healthcare staffing personnel with other temporary healthcare staffing companies and with hospitals, healthcare facilities and physician practice groups based on the quantity, diversity and quality of assignments offered, compensation packages and the benefits that we provide to our healthcare professionals. We rely on our human capital intensive, relationship-oriented approach and national infrastructure to enable us to compete in the permanent physician staffing business. We must continually evaluate and expand our temporary and permanent healthcare professional network to keep pace with the needs of our hospital, healthcare facility clients and physician practice groups.

Currently, there is a shortage of qualified nurses, physicians and certain allied healthcare professionals in the United States, significant competition exists for these personnel, and salaries and benefits have risen. We may be unable to continue to increase the number of temporary and permanent healthcare professionals that we recruit, decreasing the potential for growth of our business. Our ability to recruit and retain temporary and permanent healthcare professionals depends on several factors, including our ability to provide our healthcare professionals with assignments and placements that they view as attractive and to provide our temporary healthcare professionals with competitive wages and benefits, including health insurance and housing. We cannot assure you that we will be successful in any of these areas as the costs of attracting healthcare professionals and providing them with attractive benefit packages may be higher than we anticipate, or we may be unable to pass these costs on to our hospital and healthcare facility clients. If we are unable to increase the rates that we charge our hospital and healthcare facility clients to cover these costs, our profitability could decline. Moreover, if we are unable to recruit temporary and permanent healthcare professionals, the quality of our services to our hospital and healthcare facility clients may decline and, as a result, we could lose clients.

Our operations may deteriorate if we are unable to continue to attract, develop and retain our sales and operations personnel.

Our success is dependent upon the performance of our sales and operations personnel. The number of individuals who meet our qualifications for these positions is limited, and we may experience difficulty in attracting qualified candidates. In addition, we commit substantial resources to the training, development and support of our personnel. Competition for qualified sales personnel in the line of business in which we operate is strong, and there is a risk that we may not be able to retain our sales personnel after we have expended the time and expense to recruit and train them.

12

Table of Contents

We operate in a highly competitive market and our success depends on our ability to remain competitive in obtaining and retaining hospital, healthcare facility and physician practice group clients and demonstrating the value of our services.

The temporary healthcare staffing business is highly competitive. We compete in national, regional and local markets with full-service staffing companies, specialized temporary staffing agencies and hospital systems that have developed their own interim staffing pools. Some of our large competitors in the temporary nurse and locum tenens staffing sectors include Cross Country Healthcare, InteliStaf Healthcare, CHG Healthcare Services, Inc., On Assignment, and Medical Doctor Associates.

We believe that the primary competitive factors in obtaining and retaining hospital, healthcare facility and physician practice group clients are identifying qualified healthcare professionals for specific job requirements, providing qualified employees in a timely manner, pricing services competitively and effectively monitoring employees’ job performance. Competition for hospital, healthcare facility and physician practice group clients and temporary and permanent healthcare professionals may increase in the future due to these factors or a shortage of qualified healthcare professionals in the marketplace and, as a result, we may not be able to remain competitive. To the extent competitors seek to gain or retain market share by reducing prices or increasing marketing expenditures, we could lose revenue or clients and our margins could decline, which could seriously harm our operating results and cause the price of our stock to decline. In addition, the development of alternative recruitment channels could lead our clients to bypass our services, which would also cause revenue and margins to decline.

Our business depends upon our ability to secure and fill new orders from our hospital, healthcare facility and physician practice group clients because our temporary healthcare staffing business does not have long-term, exclusive or guaranteed contracts with them, and economic conditions may adversely impact the number of new orders and contracts we receive.

We generally do not have long-term, exclusive or guaranteed order contracts for temporary healthcare staffing with our hospital, healthcare facility and physician practice group clients. The success of our business is dependent upon our ability to continually secure new contracts and orders from hospitals, healthcare facilities and physician practice groups and to fill those orders with our temporary healthcare professionals. Our hospital, healthcare facility and physician practice group clients are free to award contracts and place orders with our competitors and choose to use temporary healthcare professionals that our competitors offer them. Therefore, we must maintain positive relationships with our hospital, healthcare facility and physician practice group clients. If we fail to maintain positive relationships with our hospital, healthcare facility and physician practice group clients or are unable to provide a cost-effective staffing solution, we may be unable to generate new temporary healthcare professional orders and our business may be adversely affected.

Some hospitals and healthcare facility clients choose to outsource this contract and order function to staffing associations owned by member healthcare facilities or companies with vendor management services that may act as intermediaries with our client facilities. These organizations may impact our ability to obtain new clients and maintain our existing client relationships by impeding our ability to access and contract directly with healthcare facility clients. Additionally, we may experience pricing pressure or incremental fees from these organizations that may negatively impact our revenue and profitability.

Depressed economic conditions, such as increasing unemployment rates and low job growth, could also negatively influence our ability to secure new orders and contracts from clients. In times of economic downturn, permanent healthcare facility staff may be more inclined to work overtime and less likely to leave their positions, resulting in fewer available vacancies and less demand for our services. Fewer placement opportunities for our temporary healthcare professionals impairs our ability to recruit and place both temporary and permanent placement healthcare professionals and our revenues and profitability may decline as a result of this constricted demand and supply.

13

Table of Contents

The demand for our services, and therefore the profitability of our business, may be adversely affected by changes in the staffing needs due to fluctuations in hospital admissions or staffing preferences of our healthcare facility clients.

The temporary healthcare staffing industry grew from 1996 through 2002, declined in early 2003 and stabilized and grew modestly from late 2003 through 2005. Demand for our temporary healthcare staffing services is affected by the staffing needs and preferences of our healthcare facility clients, as well as by fluctuations in patient occupancy at our client healthcare facilities due to economic factors and seasonal fluctuations that are beyond our control.

Hospitals in certain geographical regions experience significant seasonal fluctuations in admissions, and must be able to adjust their staffing levels to accommodate the change in patient census. Our healthcare facility clients may choose to use temporary staff, additional overtime from their permanent staff or add new permanent staff in order to accommodate changes in their staffing needs. Many healthcare facilities will utilize temporary healthcare professionals to accommodate an increase in hospital admissions. Alternatively, if hospital admissions decrease, the demand for our temporary healthcare professionals may decline as healthcare facility clients typically will reduce their use of temporary staff before reducing the workload or undertaking layoffs of their regular employees. In addition, we may experience more competitive pricing pressure during periods of patient occupancy and hospital admission downturns, negatively impacting our revenue and profitability.

The ability of our hospital, healthcare facility and physician practice group clients to retain and increase the productivity of their permanent staff may affect the demand for our services.

If our hospital, healthcare facility and physician practice group clients retain and increase the productivity of their permanent staff, their need for our services may decline. Higher permanent staff retention rates and increased productivity of permanent staff members could result in increased efficiencies, thereby reducing the demand for both our temporary staffing and permanent placement services, which could negatively impact our revenue and profitability.

We operate in a regulated industry and changes in regulations or violations of regulations may result in increased costs or sanctions that could reduce revenue and profitability and may impact our ability to grow and operate our business.

The healthcare industry is subject to extensive and complex federal and state laws and regulations related to professional licensure, conduct of operations, costs and payment for services and payment for referrals.

Our business is generally not subject to the extensive and complex laws that apply to our hospital, healthcare facility and physician practice group clients, including laws related to Medicare, Medicaid and other federal and state healthcare programs. However, these laws and regulations could indirectly affect the demand or the prices paid for our services. For example, our hospital, healthcare facility and physician practice group clients could suffer civil and criminal penalties and be excluded from participating in Medicare, Medicaid and other healthcare programs if they fail to comply with the laws and regulations applicable to their businesses.

In addition, our hospital, healthcare facility and physician practice group clients could receive reduced reimbursements, or be excluded from coverage, because of a change in the rates or conditions set by federal or state governments. In turn, violations of or changes to these laws and regulations that adversely affect our hospital, healthcare facility and physician practice group clients could also adversely affect the prices and demand for our services. For example, legislation in Massachusetts limited the hourly rate paid to temporary nursing agencies for registered nurses, licensed practical nurses and certified nurses aides. While we are exempt from this regulation, in part, similar regulations may be enacted in other states in which we operate, and as a result revenue and margins could decrease. Furthermore, third party payers, such as health maintenance organizations, increasingly challenge the prices charged for medical care. Failure by hospitals, healthcare

14

Table of Contents

facilities and physician practice groups to obtain full reimbursement from those third party payers could reduce the demand or the price paid for our services.

We are also subject to certain laws and regulations applicable to healthcare staffing agencies and general temporary staffing services. Like all employers, we must also comply with various laws and regulations relating to pay practices, workers compensation and immigration. As we continue to grow, we believe that we are more likely to be a target of challenges to our pay practices, such as challenges to our employee classifications under the Fair Labor Standards Act. There is a risk that we could be subject to payment of additional wages, insurance and employment and payroll related taxes if certain of our corporate employees classified as exempt from overtime and minimum wage requirements are re-classified as non-exempt from overtime and minimum wage requirements. Because of the nature of our business, the impact of these laws and regulations may have a more pronounced effect on our business. These laws and regulations may also impede our ability to grow our operations.

We primarily draw our supply of healthcare professionals from the United States, but international supply channels have represented a small but growing temporary nurse supply source. Our ability to recruit healthcare professionals through these foreign supply channels may be impacted by government legislation limiting the number of immigrant visas that can be issued.

Additionally, we have incurred and will continue to incur additional legal and accounting expenses related to compliance with corporate governance and disclosure standards implemented by the Sarbanes-Oxley Act of 2002, the rules of the New York Stock Exchange and regulations of the Securities and Exchange Commission. Regulations promulgated in connection with Section 404 of the Sarbanes-Oxley Act of 2002 require an annual and quarterly review by management and evaluation of our internal control systems, in addition to an annual auditor attestation of the effectiveness of these systems, which commenced with our fiscal year ended on December 31, 2004 (exclusive of our recent acquisition of The MHA Group, Inc.). In addition, as of December 31, 2006, we will need to certify the sufficiency of the internal control systems of MHA. If we fail to comply with these laws and regulations, damages, civil and criminal penalties, injunctions and cease and desist orders may be imposed, which would negatively impact our business and operations. The increase in costs necessitated by compliance with the laws and regulations affecting our business reduces our overall profitability, and reduces the assets and resources available for utilization in the expansion of our business operations.

Our profitability is impacted by our ability to leverage our cost structure.

We have technology, operations and human capital infrastructures to support our existing business and contemplated growth. In the event that our business does not grow at the rate that we had anticipated, our inability to reduce these costs would impair our profitability. Additionally, if we are not able to capitalize on this infrastructure our earnings growth rate will be impacted.

The variation in pricing of the healthcare facility contracts under which we place temporary and permanent healthcare professionals impacts our profitability.

The pricing of our contracts with hospitals, healthcare facilities and physician practice groups may vary depending on circumstances, including geographic location, economic conditions and supply and demand factors. These pricing variables impact our gross margin and could result in decreased profitability if we are unable to renew existing accounts on economically favorable terms.

15

Table of Contents

We may not be able to successfully implement our strategic growth, acquisition and integration strategies.

An effective growth management strategy is necessary to organically grow our current operations, and if we do not successfully execute on this growth strategy, our profitability could decline. We continue to explore strategic acquisition opportunities to supplement our organic growth strategy. Acquisitions involve significant risks and uncertainties, including difficulties integrating acquired personnel and other corporate cultures into our business, the potential loss of key employees or customers of acquired companies, the assumption of liabilities and exposure to unforeseen liabilities of acquired companies and the diversion of management attention from existing operations. We may not be able to fully integrate the operations of the acquired businesses with our own in an efficient and cost-effective manner. Acquisitions may also require significant expenditures of cash and other resources and assumption of debt that may ultimately negatively impact our overall financial performance. In particular, we are still in the process of integrating our recent MHA acquisition.

Difficulties in maintaining our management information and communications systems may result in increased costs that reduce our profitability.

Our ability to deliver our staffing services to our hospital, healthcare facility and physician practice group clients and manage our internal systems depends to a large extent upon our access to and the performance of our management information and communications systems. These systems also maintain accounting and financial information, which we depend upon to fulfill our financial reporting obligations. If these systems do not adequately support our operations, these systems are damaged or if we are required to incur significant additional costs to repair, maintain or expand these systems, our business and financial results could be materially adversely affected. Although we have risk mitigation measures, these systems, and our access to these systems, are not impervious to floods, fire, storms, or other natural disasters, and the loss of systems information could result in disruption to our business.

The challenge to the classification of certain of our healthcare professionals as independent contractors could adversely impact our profitability.

Although there is a long-standing industry standard to treat physicians as independent contractors, there is a risk we could be subject to additional wage and insurance claims, employment and payroll-related taxes if federal or state taxing authorities re-classify our independent contractor physicians as employees, which would significantly reduce our profitability. In addition, many states have laws which prohibit non-physician owned companies from employing physicians which we refer to as the “corporate practice of medicine.” If our independent contractor physicians are classified as employees, we would be in violation of state laws that prohibit the corporate practice of medicine, which would have a substantial negative impact on our profitability.

The impact of medical malpractice and other claims asserted against us could subject us to substantial liabilities.

In recent years, our hospital, healthcare facility and physician practice group clients are subject to a number of legal actions alleging malpractice or related legal theories. Because our temporary and permanent healthcare professionals provide medical care and we provide credentialing of these healthcare professionals, claims may be brought against us and our healthcare professionals relating to the recruitment and qualification of these healthcare professionals and the quality of medical care provided by our temporary healthcare professionals while on assignment or after placement at our hospital, healthcare facility and physician practice group clients. We and the healthcare professional are at times named in these lawsuits regardless of our contractual obligations, the competency of the healthcare professional, the standard of care provided by the healthcare professional or the quality of service that we provided. In some instances, we are required to indemnify hospital, healthcare facility and physician practice group clients contractually against some or all of these potential legal actions. Also, because some of our temporary healthcare professionals are our employees, we may be subject to various employment claims and contractual disputes regarding the terms of a temporary healthcare professional’s employment.

16

Table of Contents

Because we are in the business of placing our temporary healthcare professionals in the workplaces of other companies, we are subject to possible claims by our temporary healthcare professionals alleging discrimination, sexual harassment and other similar activities by our hospital and healthcare facility clients. We maintain a policy for employment practices coverage. However, the cost of defending such claims, even if groundless, could be substantial and the associated negative publicity could adversely affect our ability to attract, retain and place qualified individuals in the future.

We maintain various types of insurance coverage, including professional liability, workers compensation and employment practices, through insurance carriers, and we also self-insure for these claims through accruals for retention reserves. We may experience increased insurance costs and reserve accruals and may not be able to pass on all or any portion of increased insurance costs to our hospital, healthcare facility and physician practice group clients, thereby reducing our profitability. Our insurance coverage and reserve accruals may not be sufficient to cover all claims against us, and we may be exposed to substantial liabilities.

Terrorist threats or attacks may disrupt or adversely affect our business operations.

Our business operations may be interrupted or adversely impacted in the United States and abroad in the event of a terrorist attack or heightened security alerts. Our temporary healthcare professionals may become reluctant to travel and may decline assignments based upon the perceived risk of terrorist activity, which would reduce our revenue and profitability. In addition, terrorist activity or threats may impede our access to our management and information systems resulting in loss of revenue. We do not maintain insurance coverage against terrorist attacks.

If we are unable to carry out our business strategy our profitability could be negatively impacted.

Our success is dependent on our ability to execute our business strategy, which necessarily involves the successful operation of a number of integral components and business objectives. Our ability to execute these business objectives is dependent upon a sufficient cash flow and capital structure to support the business. If we are unable to access credit on commercially reasonable terms or our cash flow is significantly impaired, our profitability could be negatively impacted.

The loss of key officers and management personnel could adversely affect our ability to remain competitive.

We believe that the success of our business strategy and our ability to operate profitably depends on the continued employment of our senior management team. We have employment agreements only with Steven C. Francis, our Executive Chairman, Susan R. Nowakowski, our President and Chief Executive Officer, and two non-executive officers. If these individuals or members of our senior management team become unable or unwilling to continue in their present positions, our business and financial results could be materially adversely affected.

We have a substantial amount of goodwill on our balance sheet that may have the effect of decreasing our earnings or increasing our losses in the event that we are required to recognize an impairment to goodwill.

As of December 31, 2005, we had $240.8 million of unamortized goodwill on our balance sheet, which represents the excess of the total purchase price of our acquisitions over the fair value of the net assets acquired. At December 31, 2005, goodwill represented 38.9% of our total assets.

SFAS No. 142, Goodwill and Other Intangible Assets requires that goodwill not be amortized but rather that it be reviewed annually for impairment. In the event impairment is identified, a charge to earnings would be recorded. Although an impairment charge to earnings for goodwill would not affect our cash flow, it would

17

Table of Contents

decrease our earnings or increase our losses, as the case may be, and our stock price could be adversely affected. We have reviewed our goodwill for impairment in accordance with the provisions of SFAS No. 142, and have not identified any impairment to goodwill.

We have a substantial accrual for self-insured retentions on our balance sheet, and any significant adverse adjustments in these accruals may have the effect of decreasing our earnings or increasing our losses.

We maintain accruals for self-insured retentions for professional liability, health insurance and workers compensation on our balance sheet. Increases to these accruals do not immediately affect our cash flow, but a significant increase to these self-insured retention accruals may decrease our earnings or increase our losses, as the case may be. We determine the adequacy of our self-insured retention accruals by evaluating our historical experience and trends, related to both insurance claims and payments, information provided to us by our insurance brokers and third party administrators, as well as industry experience and trends. If such information indicates that our accruals are overstated or understated, we reduce or provide for additional accruals, as appropriate.

| Item 1B. | Unresolved Staff Comments |

None.

| Item 2. | Properties |

We believe that our leased space is adequate for our current needs. In addition, we believe that adequate space can be obtained to meet our foreseeable business needs. In accordance with, and as required by, the terms of our New Credit Agreement, we have pledged substantially all of our assets and properties to our lenders under our New Credit Agreement to secure our obligations thereunder. Our principal leases as of December 31, 2005 are identified in the chart below:

| Location |

Square Feet | |

| San Diego, California (corporate headquarters) |

175,672 | |

| Irving, Texas |

125,909 | |

| Huntersville, North Carolina |

30,870 | |

| Ft. Lauderdale, Florida |

25,408 | |

| Westminster, Colorado |

19,427 | |

| Salt Lake City, Utah |

13,347 | |

| Atlanta, Georgia |

13,302 | |

| Irvine, California |

6,165 | |

| Savannah, Georgia |

4,780 | |

| London (United Kingdom) |

3,391 | |

| Sydney (Australia) |

2,788 | |

| Birmingham (United Kingdom) |

2,300 |

| Item 3. | Legal Proceedings |

We are subject to various claims and legal actions in the ordinary course of our business. Some of these matters include professional liability, tax, payroll and employee-related matters and inquiries and investigations by governmental agencies regarding our employment practices. We are not aware of any pending or threatened litigation that we believe is reasonably likely to have a material adverse effect on our results of operations, financial position or liquidity.

18

Table of Contents

Our hospital and healthcare facility clients may also become subject to claims, governmental inquiries and investigations and legal actions to which we may become a party relating to services provided by our professionals. From time to time, and depending upon the particular facts and circumstances, we may be subject to indemnification obligations under our contracts with our hospital and healthcare facility clients relating to these matters. At this time, we are not aware of any such pending or threatened litigation that we believe is reasonably likely to have a material adverse effect on our results of operations, financial position or liquidity.

| Item 4. | Submission of Matters to a Vote of Security Holders |

No matters were submitted to a vote of security holders during the fourth quarter of fiscal 2005.

19

Table of Contents

PART II

| Item 5. | Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities |

Our common stock has traded on the New York Stock Exchange under the symbol “AHS” since our initial public offering on November 13, 2001. Prior to that time, there was no public trading market for our common stock. The following table sets forth, for the periods indicated, the high and low sales prices reported by the New York Stock Exchange.

| Sales Price | ||||||

| High |

Low | |||||

| Year Ended December 31, 2004 |

||||||

| First Quarter |

$ | 21.56 | $ | 17.00 | ||

| Second Quarter |

$ | 18.58 | $ | 14.49 | ||

| Third Quarter |

$ | 15.35 | $ | 11.26 | ||

| Fourth Quarter |

$ | 16.66 | $ | 10.70 | ||

| Year Ended December 31, 2005 |

||||||

| First Quarter |