485BPOS12/31/20220001141819false1.5825.334.344.997.698.0629.424.6049.4429.7900011418192023-04-302023-04-300001141819ck0001141819:S000068561Member2023-04-302023-04-300001141819ck0001141819:S000068561Memberck0001141819:C000219404Member2023-04-302023-04-300001141819ck0001141819:S000068561Memberck0001141819:C000219405Member2023-04-302023-04-30iso4217:USDxbrli:pure0001141819rr:AfterTaxesOnDistributionsMemberck0001141819:S000068561Memberck0001141819:C000219405Member2023-04-302023-04-300001141819ck0001141819:S000068561Memberck0001141819:C000219405Memberrr:AfterTaxesOnDistributionsAndSalesMember2023-04-302023-04-300001141819ck0001141819:MSCIUSREITIndexreflectsnodeductionforfeesexpensesortaxesIndexMemberck0001141819:S000068561Memberck0001141819:C000219405Member2023-04-302023-04-300001141819ck0001141819:MSCIUSREITIndexreflectsnodeductionforfeesexpensesortaxesIndexMemberck0001141819:S000068561Memberck0001141819:C000219404Member2023-04-302023-04-300001141819ck0001141819:S000068561Memberck0001141819:C000219405Memberck0001141819:MSCIUSAIMICoreRealEstateIndexreflectsnodeductionforfeesexpensesortaxesIndexMember2023-04-302023-04-300001141819ck0001141819:S000068561Memberck0001141819:MSCIUSAIMICoreRealEstateIndexreflectsnodeductionforfeesexpensesortaxesIndexMemberck0001141819:C000219404Member2023-04-302023-04-30

As filed with the Securities and Exchange Commission on April 26, 2023

1933 Act Registration File No. 333-62298

1940 Act File No. 811-10401

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-1A

| | | | | | | | | | | |

| REGISTRATION STATEMENT UNDER THE SECURITIES ACT OF 1933 | [X] |

Pre-Effective Amendment No. | | | [ ] |

Post-Effective Amendment No. | 832 | | [X] |

and/or

| | | | | | | | | | | |

| REGISTRATION STATEMENT UNDER THE INVESTMENT COMPANY ACT OF 1940 | [X] |

Amendment No. | 834 | | [X] |

TRUST FOR PROFESSIONAL MANAGERS

(Exact Name of Registrant as Specified in Charter)

615 East Michigan Street

Milwaukee, Wisconsin 53202

(Address of Principal Executive Offices) (Zip Code)

(Registrant’s Telephone Number, including Area Code) (414) 516-1514

Jay S. Fitton

U.S. Bank Global Fund Services

615 East Michigan Street, 2nd Floor

Milwaukee, Wisconsin 53202

(Name and Address of Agent for Service)

Copies to:

Carol A. Gehl, Esq.

Godfrey & Kahn, S.C.

833 East Michigan Street, Suite 1800

Milwaukee, Wisconsin 53202

(414) 273-3500

It is proposed that this filing will become effective (check appropriate box)

| | | | | | | | |

| [ ] | | Immediately upon filing pursuant to Rule 485(b). |

| [X] | | on April 30, 2023 pursuant to Rule 485(b). |

| [ ] | | 60 days after filing pursuant to Rule 485 (a)(1). |

| [ ] | | on (date) pursuant to Rule 485 (a)(1). |

| [ ] | | 75 days after filing pursuant to Rule 485 (a)(2). |

| [ ] | | on (date) pursuant to Rule 485 (a)(2). |

If appropriate, check the following box:

| | | | | | | | |

| [ ] | | This post-effective amendment designates a new effective date for a previously filed post-effective amendment. |

Explanatory Note: This Post-Effective Amendment No. 832 to the Registration Statement of Trust for Professional Managers is being filed to add the audited financial statements and certain related financial information for the fiscal year ended December 31, 2022 for the Terra Firma US Concentrated Realty Equity Fund, and to make other permissible changes under Rule 485(b).

Terra Firma US Concentrated Realty Equity Fund

Institutional Class Shares (TFRIX)

Open Class Shares (TFREX)

Prospectus

April 30, 2023

The U.S. Securities and Exchange Commission (the “SEC”) has not approved or disapproved of these securities or determined if this Prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

Terra Firma US Concentrated Realty Equity Fund

A series of Trust for Professional Managers (the “Trust”)

TABLE OF CONTENTS

| | | | | |

| SUMMARY SECTION | |

| INVESTMENT STRATEGIES, RISKS AND DISCLOSURE OF PORTFOLIO HOLDINGS | |

GENERAL INVESTMENT POLICIES OF THE FUND | |

PRINCIPAL RISKS OF INVESTING IN THE FUND | |

PORTFOLIO HOLDINGS INFORMATION | |

| MANAGEMENT OF THE FUND | |

THE ADVISER | |

PORTFOLIO MANAGERS | |

| SHAREHOLDER INFORMATION | |

CHOOSING A SHARE CLASS | |

DISTRIBUTION PLAN (RULE 12b-1 PLAN) | |

SHARE PRICE | |

HOW TO PURCHASE SHARES | |

HOW TO REDEEM SHARES | |

TOOLS TO COMBAT FREQUENT TRANSACTIONS | |

OTHER FUND POLICIES | |

| DISTRIBUTION OF FUND SHARES | |

THE DISTRIBUTOR | |

PAYMENTS TO FINANCIAL INTERMEDIARIES | |

| DISTRIBUTIONS AND TAXES | |

DISTRIBUTIONS | |

FEDERAL INCOME TAX CONSEQUENCES | |

| DERIVATIVE ACTIONS | |

| FINANCIAL HIGHLIGHTS | |

Summary Section

Investment Objectives

The primary investment objective of the Terra Firma US Concentrated Realty Equity Fund (the “Fund”) is long-term capital appreciation, with current income, including interest and dividends from portfolio securities, as a secondary objective.

Fees and Expenses of the Fund

This table describes the fees and expenses that you may pay if you buy, hold and sell shares of the Fund. You may pay other fees, such as brokerage commissions and other fees to financial intermediaries, which are not reflected in the table and example below.

| | | | | | | | |

Shareholder Fees (fees paid directly from your investment) | Institutional Class Shares | Open

Class Shares |

| None | None |

Annual Fund Operating Expenses (expenses that you pay each year as a percentage of the value of your investment) |

| Management Fees | 0.75% | 0.75% |

| Distribution and Service (12b-1) Fees | None | 0.25%1 |

| Other Expenses | 0.92% | 0.92% |

Total Annual Fund Operating Expenses2 | 1.67% | 1.92%1 |

| Fee Waiver and/or Expense Reimbursements | -0.67% | -0.67% |

Total Annual Fund Operating Expenses After Fee Waiver and/or Expense Reimbursement2 | 1.00% | 1.25%1 |

1 Please note that the Total Annual Fund Operating Expenses in the table above does not correlate to the Ratio of Expenses to Average Net Assets found within the “Financial Highlights” section of the Prospectus because the Fund only accrued Rule 12b-1 plan fees in the amount of 0.19% during the prior fiscal year.

2 Pursuant to an operating expense limitation agreement between the Fund’s investment adviser, Terra Firma Asset Management, LLC (the “Adviser”), and the Trust, on behalf of the Fund, the Adviser has agreed to waive its management fees and/or reimburse expenses of the Fund to ensure that Total Annual Fund Operating Expenses (excluding any front-end or contingent deferred loads, Rule 12b-1 plan fees, shareholder servicing plan fees, taxes, leverage expenses (i.e., any expenses incurred in connection with borrowings made by the Fund), interest (including interest incurred in connection with bank and custody overdrafts), brokerage commissions and other transactional expenses, acquired fund fees and expenses, dividends or interest expenses on short positions, expenses incurred in connection with any merger or reorganization, or extraordinary expenses such as litigation (collectively, “Excluded Expenses”)) for the Institutional Class shares and Open Class shares do not exceed 1.00% of the Fund’s average net assets, through at least May 1, 2030, and subject thereafter to annual re-approval of the agreement by the Trust’s Board of Trustees (the “Board of Trustees”). The operating expense limitation agreement may be terminated only by, or with the consent of, the Board of Trustees. The Adviser may request recoupment of previously waived fees and paid expenses from the Fund for up to three years from the date such fees and expenses were waived or paid, subject to the operating expense limitation agreement, if such reimbursements will not cause the Fund’s Total Annual Fund Operating Expenses, after recoupment has been taken into account, to exceed the lesser of: (1) the expense limitation in place at the time of the waiver and/or expense reimbursement; or (2) the expense limitation in place at the time of recoupment.

Example

This Example is intended to help you compare the costs of investing in the Fund with the cost of investing in other mutual funds. The Example assumes that you invest $10,000 in the Fund for the time periods indicated and then hold or redeem all of your shares at the end of those periods. The Example also assumes that your investment has a 5% return each year and that the Fund’s operating expenses remain the same. The operating expense limitation agreement discussed in the table above is reflected only through May 1, 2030. Although your actual costs may be higher or lower, based on these assumptions, your costs would be:

| | | | | | | | | | | | | | |

| One Year | Three Years | Five Years | Ten Years |

| Institutional Class | $102 | $318 | $552 | $1,498 |

| Open Class | $127 | $397 | $686 | $1,779 |

Portfolio Turnover

The Fund pays transaction costs, such as commissions, when it buys and sells securities (or “turns over” its portfolio). A higher portfolio turnover rate may indicate higher transaction costs and may result in higher taxes when Fund shares are held in a taxable account. These transaction costs, and potentially higher taxes, which are not reflected in the Total Annual Fund Operating Expenses or in the Example, affect the Fund’s performance. During the most recent fiscal year, the Fund’s portfolio turnover rate was 26% of the average value of its portfolio.

Principal Investment Strategies

Under normal circumstances, the Fund invests at least 80% of its assets in equity securities (including common, convertible and preferred stocks) of U.S. Realty Companies (as defined below), and synthetic instruments related to U.S. Realty Companies. Such synthetic instruments are investments that have economic characteristics similar to the Fund’s direct investments in U.S. Realty Companies and include warrants, rights, options and shares of exchange-traded funds (“ETFs”).

The portfolio managers conduct their own research to select the Fund’s investments, based on an analysis of macroeconomic factors, real estate sectors, and individual company attributes. Research on company level attributes may include analysis using numerical or financial measures such as earnings growth potential, price to net asset value (“NAV”) ratios, dividend yield, price to earnings ratios, among others. More qualitative factors at the company level may also include an assessment of the company’s overall business, growth strategy, quality of management, and quality of owned properties.

“Realty Companies” are real estate-related companies of any size and include real estate investment trusts (“REITs”), real estate operating or service companies and companies in the home building, lodging and hotel industries, as well as companies engaged in the natural resources and utility industries, and other companies whose investments, balance sheets or income statements are real estate-intensive (i.e., the company’s actual or anticipated revenues, profits, assets, services or products are related to real estate).

The Fund may invest in issuers of any market capitalization and securities of any maturity, and the Fund’s investments also may include securities purchased in initial public offerings (“IPOs”).

The Fund also may invest up to 20% of its assets in equity and fixed income and debt securities and instruments of companies or entities (which need not be U.S. Realty Companies), including, but not limited to, securities of non-U.S. companies and other investment companies.

The Fund’s investments in preferred stock and convertible and fixed income and debt securities may include securities which, at the time of purchase, are rated below “investment grade” by a nationally recognized statistical rating organization, or the unrated equivalent as determined by the portfolio managers (“junk bonds”).

In addition to purchasing options, the Fund may, but is not required to, write put and covered call options on securities and indexes, for hedging purposes or to seek to increase returns.

The Fund is classified as “non-diversified” under the Investment Company Act of 1940, as amended (the “1940 Act”), which means that it may invest a relatively high percentage of its assets in a limited number of issuers, when compared to a diversified fund.

Principal Risks

Before investing in the Fund, you should carefully consider your own investment goals, the amount of time you are willing to leave your money invested, and the amount of risk you are willing to take. Remember, in addition to possibly not achieving your investment goals, you could lose money by investing in the Fund. The principal risks of investing in the Fund are:

•Management Risk. The Adviser’s judgments about the attractiveness, value and potential appreciation of the Fund’s investments may prove to be incorrect and the investment strategies employed by the Adviser in selecting investments for the Fund may not result in an increase in the value of your investment or in overall performance equal to other similar investment vehicles having similar investment strategies.

•Recent Market Events Risk. U.S. and international markets have experienced significant periods of volatility in recent months and years due to a number of economic, political and global macro factors including rising inflation and the impact of the coronavirus (COVID-19) as a global pandemic, uncertainties regarding interest rates, rising inflation, trade tensions, and the threat of tariffs imposed by the U.S. and other countries. The recovery from COVID-19 is proceeding at slower than expected rates and may last for a prolonged period of time. As a result of continuing political tensions and armed conflicts, including the war between Ukraine and Russia, the U.S. and the European Union imposed sanctions on certain Russian individuals and companies, including certain financial institutions, and have limited certain exports and imports to and from Russia. The war has contributed to recent market volatility and may continue to do so. Continuing market volatility as a result of recent market conditions or other events may have an adverse effect on the performance of the Fund.

•General Market Risk. Certain securities selected for the Fund’s portfolio may be worth less than the price originally paid for them, or less than they were worth at an earlier time.

•Issuer Risk. The value of a security may decline for a number of reasons which directly relate to the issuer, such as management performance, financial leverage and reduced demand for the issuer’s goods or services, as well as the historical and prospective earnings of the issuer and the value of its assets or factors unrelated to the issuer’s value, such as investor perception.

•Real Estate-Related Securities Concentration Risk. The Fund’s investment portfolio is expected to be largely composed of securities of real estate-related companies. Consequently, the investment strategies of the Fund could lead to securities investment results that may be significantly different from investments in securities of companies in other industries and sectors, or in a more broad-based portfolio generally.

•Common Stock/Equity Securities Risk. Common stocks are susceptible to general stock market fluctuations and to volatile increases and decreases in value as market confidence in and perceptions of their issuers change.

•Preferred Securities Risk. There are various risks associated with investing in preferred securities. In addition, unlike common stock, participation in the growth of an issuer may be limited.

•Credit risk is the risk that a security held by the Fund will decline in price or the issuer of the security will fail to make dividend, interest or principal payments when due because the issuer experiences a decline in its financial status.

•Interest rate risk is the risk that securities will decline in value because of changes in market interest rates. When market interest rates rise, the market value of such securities generally will fall.

•Preferred securities may include provisions that permit the issuer, at its discretion, to defer or omit distributions for a stated period without any adverse consequences to the issuer.

•Preferred securities are generally subordinated to bonds and other debt instruments in an issuer’s capital structure in terms of having priority to corporate income, claims to corporate assets and

liquidation payments, and therefore will be subject to greater credit risk than more senior debt instruments.

•During periods of declining interest rates, an issuer may be able to exercise an option to call, or redeem its issue at par earlier than the scheduled maturity. If this occurs during a time of lower or declining interest rates, the Fund may have to reinvest the proceeds in lower yielding securities (and the Fund may not benefit from any increase in the value of its portfolio holdings as a result of declining interest rates).

•Certain preferred securities may be substantially less liquid than many other securities, such as common stocks or U.S. Government securities. Illiquid securities involve the risk that the securities will not be able to be sold at the time desired by the Fund or at prices approximating the value at which the Fund is carrying the securities on its books.

•Convertible Securities Risk. The market value of a convertible security tends to perform like that of a regular debt security so that, if market interest rates rise, the value of the convertible security falls. Investments in rights and warrants involve certain risks, including the possible lack of a liquid market for resale, price fluctuations and the failure of the price of the underlying security to reach a level at which the right or warrant can be prudently exercised, in which case the right or warrant may expire without being exercised and result in a loss of the Fund’s entire investment.

•Realty Companies, Real Estate Investments and REITs Risk. Since the Fund focuses its investments in Realty Companies, the Fund could lose money due to the performance of real estate-related securities even if securities markets generally are experiencing positive results. The performance of investments made by the Fund may be determined to a great extent by the current status of the real estate industry in general, or by other factors (such as interest rates and the availability of loan capital) that may affect the real estate industry, even if other industries would not be so affected. Consequently, the investment strategies of the Fund could lead to securities investment results that may be significantly different from investments in securities of other industries or sectors or in a more broad-based portfolio generally.

The risks related to investments in Realty Companies include, but are not limited to: adverse changes in general economic and local market conditions; adverse developments in employment; changes in supply or demand for similar or competing properties; unfavorable changes in applicable taxes, governmental regulations and interest rates; operating or development expenses; and lack of available financing.

Due to certain special considerations that apply to REITs, investments in REITs may carry additional risks not necessarily present in investments in other securities. REIT securities (including those trading on national exchanges) typically have trading volumes that are less than those of common stocks of non-Realty Companies traded on national exchanges, which may affect the Fund’s ability to trade or liquidate those securities. An investment in REITs may be adversely affected if the REIT fails to comply with applicable laws and regulations, including failing to qualify as a REIT under the Internal Revenue Code of 1986, as amended (the “Code”). A REIT generally is not taxed on income distributed to its shareholders if it complies with certain federal income tax requirements relating primarily to its organization, ownership, assets and income and, further, if it distributes at least 90% of its taxable income to shareholders each year. Under certain circumstances, a REIT may fail to qualify for pass-through treatment for tax purposes, which would subject the REIT to federal income taxes at the REIT level and adversely affect the value of the Fund’s investment in such REIT. The Fund generally will have no control over the operations and policies of a REIT, and the Fund generally will have no ability to cause a REIT to take the actions necessary to qualify as a REIT.

•Small and Mid Cap Companies Risk. Small and mid capitalization companies carry additional risks because their earnings tend to be less predictable, their share prices more volatile and their securities less liquid than larger, more established companies. The shares of small and mid capitalization companies tend to trade less frequently than those of larger companies, which can have an adverse

effect on the pricing of these securities and on the ability to sell these securities when the portfolio managers deem it appropriate.

•Non-Diversification Risk. The Fund’s NAV may be more vulnerable to changes in the market value of a single issuer or group of issuers and may be relatively more susceptible to adverse effects from any single corporate, industry, economic, market, political or regulatory occurrence than if the Fund’s investments consisted of securities issued by a larger number of issuers.

•Fixed-Income and Debt Securities Risk. The market value of a debt security may decline due to general market conditions that are not specifically related to a particular company, such as real or perceived adverse economic conditions, changes in the outlook for corporate earnings, changes in interest or currency rates or adverse investor sentiment generally. The debt securities market can be susceptible to increases in volatility and decreases in liquidity. Liquidity can decline unpredictably in response to overall economic conditions or credit tightening.

Prices of bonds and other debt securities tend to move inversely with changes in interest rates. Interest rate risk is usually greater for fixed-income securities with longer maturities or durations. A rise in interest rates (or the expectation of a rise in interest rates) may result in periods of volatility, decreased liquidity and increased redemptions, and, as a result, the Fund may have to liquidate portfolio securities at disadvantageous prices. Risks associated with rising interest rates are heightened given that the Federal Reserve has raised the federal funds rate several times in recent periods and may continue to increase rates in the future.

The Fund’s investments in lower-rated, higher-yielding securities (“junk bonds”) are subject to greater credit risk than its higher rated investments. Credit risk is the risk that the issuer will not make interest or principal payments, or will not make payments on a timely basis. Non-investment grade securities tend to be more volatile, less liquid and are considered speculative. If there is a decline, or perceived decline, in the credit quality of a debt security (or any guarantor of payment on such security), the security’s value could fall, potentially lowering the Fund’s share price. The prices of non-investment grade securities, unlike investment grade debt securities, may fluctuate unpredictably and not necessarily inversely with changes in interest rates. The market for these securities may be less liquid and therefore these securities may be harder to value or sell at an acceptable price, especially during times of market volatility or decline.

•Non-U.S. Securities Risk. The Fund’s performance will be influenced by political, social and economic factors affecting the non-U.S. countries and companies in which the Fund invests. Non-U.S. securities carry special risks, such as less developed or less efficient trading markets, political instability, a lack of company information, differing auditing and legal standards, and, potentially, less liquidity. In addition, investments denominated in currencies other than U.S. dollars may experience a decline in value, in U.S. dollar terms, due solely to fluctuations in currency exchange rates. Emerging market countries can generally have economic structures that are less diverse and mature, and political systems that are less stable, than those of developed countries. Investments in companies in emerging market countries may be subject to political, economic, legal, market and currency risks.

•Options Risk. Writing options on securities and indexes, including for hedging purposes, may increase volatility or reduce returns, perhaps substantially, particularly since most derivatives have a leverage component that provides investment exposure in excess of the amount invested, and may cause the Fund to experience losses greater than if the Fund had not engaged in such transactions. Writing options is subject to many of the risks of, and can be highly sensitive to changes in the value of, the related security or index. As such, a small commitment to written options could potentially have a relatively large impact on the Fund’s performance. Purchasing options will reduce returns by the amount of premiums paid for options that are not exercised. Over-the-counter options purchased on securities and indexes are subject to the risk of default by the counterparty and can be illiquid.

•Investment Companies and ETF Risk. Any investments in other investment companies and ETFs are subject to the risks of the investments of the investment companies and ETFs, as well as to the

general risks of investing in investment companies and ETFs. Fund shares will bear not only the Fund’s management fees and operating expenses, but also their proportional share of the management fees and operating expenses of any other investment companies and ETFs in which the Fund invests.

•Securities Selection Risk. Securities and other investments selected by the portfolio managers for the Fund may not perform to expectations. This could result in the Fund’s underperformance compared to other funds with similar investment objectives or strategies.

•Derivatives and Hedging Risk. Derivatives transactions, including those entered into for hedging purposes (i.e., seeking to protect Fund investments), may increase volatility, reduce returns, limit gains or magnify losses, perhaps substantially, particularly since most derivatives have a leverage component that provides investment exposure in excess of the amount invested. Forward currency contracts, structured products and other over-the-counter derivatives transactions are subject to the risk of default by the counterparty and can be illiquid. Changes in liquidity may result in significant, rapid and unpredictable changes in the prices for derivatives. These derivatives transactions, as well as the exchange-traded futures and options in which the Fund may invest, are subject to many of the risks of, and can be highly sensitive to changes in the value of the related currency or other reference asset. As such, a small investment could have a potentially large impact on the Fund’s performance. In fact, many derivatives may be subject to greater risks than those associated with investing directly in the underlying or other reference asset. Derivatives transactions incur costs, either explicitly or implicitly, which reduce returns, and costs of engaging in such transactions may outweigh any gains or any losses averted from hedging activities. Successful use of derivatives, whether for hedging or for other investment purposes, is subject to the portfolio managers’ ability to predict correctly movements in the direction of the relevant reference asset or market and, for hedging activities, correlation of the derivative instruments used with the investments seeking to be hedged. Use of derivatives transactions, even if entered into for hedging purposes, may cause the Fund to experience losses greater than if the Fund had not engaged in such transactions.

•IPO Shares Risk. The prices of securities purchased in IPOs can be very volatile. The effect of IPOs on the Fund’s performance depends on a variety of factors, including the number of IPOs the Fund invests in relative to the size of the Fund and whether and to what extent a security purchased in an IPO appreciates or depreciates in value. As the Fund’s asset base increases, IPOs may have a diminished effect on the Fund’s performance.

•Cybersecurity Risk. With the increased use of technologies such as the Internet to conduct business, the Fund is susceptible to operational, information security, and related risks. Cyber incidents affecting the Fund or its service providers have the ability to cause disruptions and impact business operations, potentially resulting in financial losses, interference with the Fund’s ability to calculate its NAV, impediments to trading, the inability of shareholders to transact business, violations of applicable privacy and other laws, regulatory fines, penalties, reputational damage, reimbursement or other compensation costs, or additional compliance costs.

•Depositary Receipts Risk. American Depository Receipts (“ADRs”) and similar depositary receipts typically will be subject to certain of the risks associated with direct investments in the securities of non-U.S. companies because their values depend on the performance of the underlying non-U.S. securities. However, currency fluctuations will impact investments in depositary receipts differently than direct investments in non-U.S. dollar-denominated non-U.S. securities because a depositary receipt will not appreciate in value solely as a result of appreciation in the currency in which the underlying non-U.S. dollar security is denominated. The Fund may invest in depositary receipts through an unsponsored facility where the depositary issues the depositary receipts without an agreement with the company that issues the underlying securities. As a result, available information concerning the issuer may not be as current as for sponsored depositary receipts, and the prices of unsponsored depositary receipts may be more volatile than if such instruments were sponsored by the issuer.

•Emerging Market Risk. Emerging market countries generally have economic structures that are less diverse and mature, and political systems that are less stable, than those of developed countries. Investments in these countries may be subject to political, economic, legal, market and currency risks.

•ETF and Similar Products Risk. Shares of ETFs and similar products such as exchange-traded notes (“ETNs”) in which the Fund may invest may trade at prices that vary from their NAVs, sometimes significantly. The Fund’s investments in ETFs and similar products are subject to the risks of investments made by the ETFs and similar products, as well as to the general risks of investing in ETFs and similar products.

•Foreign Currency Risk. Investments denominated in currencies other than U.S. dollars may experience a decline in value, in U.S. dollar terms, due solely to fluctuations in currency exchange rates. The Fund’s investments could be adversely affected by delays in, or a refusal to grant, repatriation of funds or conversion of emerging market currencies.

•Monetary Policy, Political and Legislative Risk. Due to high levels of inflation, the Federal Reserve has raised short-term interest rates considerably over the last year and rate increases may continue throughout 2023. There is no way to be certain if the Federal Reserve will be able to limit inflation. Rate fluctuations may expose fixed-income and related markets to heightened volatility, interest rate sensitivity and reduced liquidity, which could cause the value of the Fund’s investments and share price to fall.

•Mortgage-Related and Asset-Backed Securities Risk. Mortgage-related securities are complex instruments, subject to both credit and prepayment risk, and may be more volatile and less liquid, and more difficult to price accurately, than more traditional debt securities. As with other interest-bearing securities, the prices of certain mortgage-related securities are inversely affected by changes in interest rates. However, although the value of a mortgage-related security may decline when interest rates rise, the converse is not necessarily true, since during periods of declining interest rates the mortgages underlying the security are more likely to be prepaid. The risks of asset-backed securities are similar to those of mortgage-related securities. However, asset-backed securities present certain risks that are not presented by mortgage-related securities. Primarily, these securities may provide the Fund with a less effective security interest in the related collateral than do mortgage-related securities.

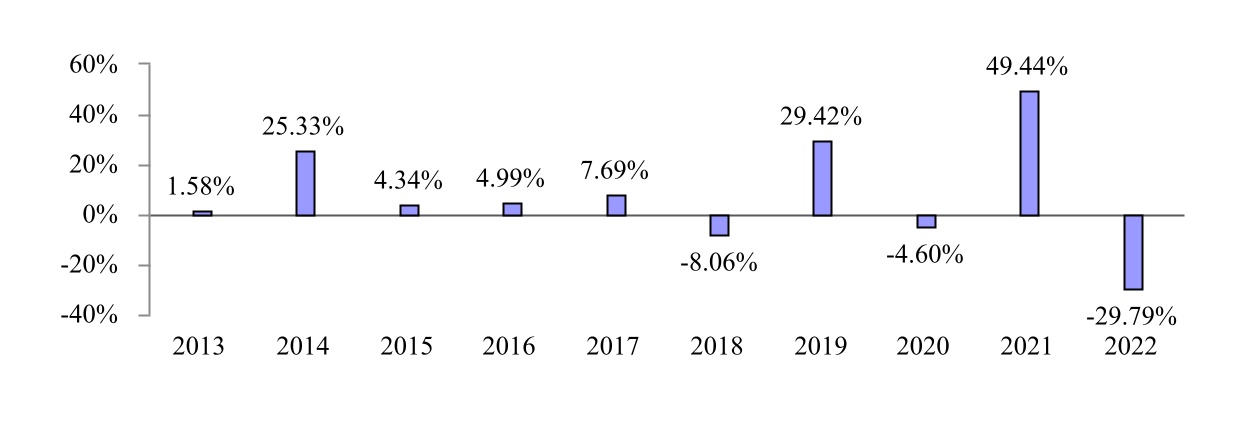

Performance

The bar chart demonstrates the risks of investing in the Fund by showing changes in the performance of the Fund’s Open Class shares from year to year. The Average Annual Total Returns table also demonstrates these risks by showing how the average annual returns for the Institutional Class and Open Class shares of the Fund for the one year, five years, ten years and since inception periods compare with those of a broad measure of market performance (the MSCI US REIT Index) and that of an index of large, mid and small capitalization companies engaged in the ownership, development and management of specific core property type real estate (the MSCI USA IMI Core Real Estate Index).

Performance data for the classes varies based on differences in their fee and expense structures. The performance figures for Institutional Class and Open Class shares reflect the historical performance of the then-existing shares (Institutional Shares and Open Shares) of the Lazard US Realty Equity Portfolio (the “Predecessor Portfolio”) (the predecessor to the Fund, for which Lazard Asset Management LLC served as the investment adviser), a series of The Lazard Funds, Inc., for periods from September 23, 2011 to June 19, 2020. The performance figures for Open Class shares also reflect the historical performance of the then-existing shares (Class A shares) of the predecessor fund to the Predecessor Portfolio, the Grubb & Ellis AGA U.S. Realty Fund (the “Predecessor Fund”) (for which Grubb & Ellis Alesco Global Advisors, LLC served as the investment adviser), for periods prior to September 23, 2011. Jay P. Leupp has served as a portfolio manager for the Fund, the Predecessor Portfolio and the Predecessor Fund since December 31, 2008. Christopher J. Hartung has served as a portfolio manager for the Fund and the Predecessor Portfolio since 2018.

The Fund’s past performance, before and after taxes, is not necessarily an indication of how the Fund will perform in the future. Updated performance information is available on the Fund’s website at www.terrafirmafunds.com or by calling the Fund toll-free at 1-844-40TERRA (1-844-408-3772).

Calendar Year Total Return for Open Class Shares as of December 31*

* The returns shown in the bar chart are for Open Shares of the Predecessor Portfolio (for periods prior to June 19, 2020). Institutional Class shares would have substantially similar annual returns because the shares were invested in the same portfolio of securities and the annual returns would differ only to the extent that the classes have different expenses. Performance for Institutional Class shares would be higher as expenses for Institutional Class shares are lower.

During the period of time shown in the bar chart, the highest quarterly return for the Open Class shares of the Fund was 17.83% for the quarter ended March 31, 2019, and the lowest quarterly return for Open Class shares of the Fund was -23.85% for the quarter ended March 31, 2020.

| | | | | | | | | | | | | | | | | | | | |

Average Annual Total Returns (for the Period Ended December 31, 2022) |

| Inception Date | One

Year | Five

Years | Ten

Years | Since Inception |

| Open Class Shares | 12/31/08 | | | | |

| Return Before Taxes | | -29.79% | 3.56% | 5.99% | 12.38% |

| Return After Taxes on Distributions | | -31.13% | 1.83% | 4.08% | 9.85% |

| Return After Taxes on Distributions and Sale of Fund Shares | | -16.91% | 2.53% | 4.28% | 9.57% |

| Institutional Class Shares | 9/26/11 | | | | |

| Return Before Taxes | | -29.69% | 3.82% | 6.26% | 9.14% |

MSCI US REIT Index (reflects no deduction for fees, expenses or taxes) | -24.51% | 3.69% | 6.48% | 8.50% |

| | | (Institutional Class) |

| -24.51% | 3.69% | 6.48% | 10.33% |

| | | | (Open Class) |

MSCI USA IMI Core Real Estate Index (reflects no deduction for fees, expenses or taxes) | -26.63% | 2.14% | 5.20% | 7.22% |

| | | (Institutional Class) |

| | -26.63% | 2.14% | 5.20% | 8.97% |

| | | | (Open Class) |

The MSCI USA IMI Core Real Estate Index has similar investment objectives to those of the Fund and is designed to represent the large, mid and small capitalization companies across U.S. equity markets engaged in the ownership, development, and management of specific core property type real estate.

After-tax returns are calculated using the highest historical individual federal marginal income tax rates and do not reflect the impact of state and local taxes. Actual after-tax returns depend on your tax situation and may differ from those shown. Furthermore, the after-tax returns shown are not relevant to shareholders who hold their shares through tax-deferred or other tax-advantaged arrangements, such as 401(k) plans or individual retirement accounts (“IRA”). After-tax returns are shown for Open Class shares only and after-tax returns for Institutional Class shares will vary. The Return After Taxes on Distributions and Sale of Fund Shares is higher than other return figures when a capital loss occurs upon the redemption of Fund shares.

Investment Adviser

Terra Firma Asset Management, LLC is the Fund’s investment adviser.

Portfolio Managers

Jay P. Leupp and Christopher J. Hartung are the Fund’s Portfolio Managers and are jointly and primarily responsible for the day-to-day management of the Fund. Mr. Leupp is a partner and co-founder of the Adviser, and Portfolio Manager of the Fund, the Predecessor Portfolio, and the Predecessor Fund since December 2008. Mr. Hartung is a partner and co-founder of the Adviser and Portfolio Manager of the Fund and the Predecessor Portfolio since September 2018.

Purchase and Sale of Fund Shares

You may purchase or redeem shares by mail (Terra Firma US Concentrated Realty Equity Fund, c/o U.S. Bank Global Fund Services, P.O. Box 701, Milwaukee, WI 53201-0701 (for regular mail) or 615 East Michigan Street, 3rd Floor, Milwaukee, WI 53202 (for overnight or express mail)), by wire transfer or by telephone at 1-844-40TERRA (1-844-408-3772), on any day the New York Stock Exchange (“NYSE”) is open for trading. Investors who wish to purchase or redeem Fund shares through a financial intermediary should contact the financial intermediary directly. The minimum initial and subsequent investment amounts are as follows:

| | | | | | | | |

| Minimum Investment Amount |

| Initial Investment | Subsequent Investments |

Institutional Class Shares | $0 for certain institutional investors as described under “Minimum Investment Amounts”; $10,000 for all other investors | $50 | |

Open Class Shares | $2,500 | | $50 | |

Tax Information

The Fund’s distributions will be taxed as ordinary income or long-term capital gains, unless you are investing through a tax-deferred or other tax-advantaged arrangement, such as a 401(k) plan or an IRA. You may be taxed later upon withdrawal of monies from tax-deferred arrangements.

Payments to Broker-Dealers and Other Financial Intermediaries

If you purchase Fund shares through a broker-dealer or other financial intermediary (such as a bank), the Fund and its related companies may pay the intermediary for the sale of Fund shares and related services. These payments may create conflicts of interest by influencing the broker-dealer or other intermediary and your salesperson to recommend the Fund over another investment. You may be required to pay commissions and/or other forms of compensation to the broker-dealer or other intermediaries for transactions in the Fund, which are not reflected in the fee table or expense example. Ask your adviser or visit your financial intermediary’s website for more information.

Investment Strategies, Risks and Disclosure of Portfolio Holdings

Investment Objectives

The primary investment objective of the Fund is long-term capital appreciation, with current income, including interest and dividends from portfolio securities, as a secondary objective.

Principal Investment Strategies

Under normal circumstances, the Fund invests at least 80% of its assets in equity securities (including common, convertible and preferred stocks) of US Realty Companies and synthetic instruments related to US Realty Companies. Such synthetic instruments are investments that have economic characteristics similar to the Fund’s direct investments in US Realty Companies and include warrants, rights, options and shares of ETFs.

The portfolio managers conduct their own research to select the Fund’s investments, based on an analysis of macroeconomic factors, real estate sectors, and individual company attributes. Research on company level attributes may include analysis using numerical or financial measures such as earnings growth potential, price to net asset value (“NAV”) ratios, dividend yield, price to earnings ratios, among others. More qualitative factors at the company level may also include an assessment of the company’s overall business, growth strategy, quality of management, and quality of owned properties.

“Realty Companies” are real estate-related companies of any size and include REITs, real estate operating or service companies and companies in the home building, lodging and hotel industries, as well as companies engaged in the natural resources and utility industries, and other companies whose investments, balance sheets or income statements are real estate-intensive (i.e., the company’s actual or anticipated revenues, profits, assets, services or products are related to real estate).

The portfolio managers may use macroeconomic analysis and property sector research, including US and international economic strength, the interest rate environment, broader stock market performance and property-level real estate trends as well as traditional supply and demand analysis to determine which investments to buy or sell.

The Fund considers a company to be “real estate-related” or “real estate-intensive” if at least fifty percent (50%) of the company’s actual or anticipated revenues, profits, assets, services or products are related to real estate including, but not limited to, the ownership, renting, leasing, construction, management, development or financing of commercial, industrial or residential real estate.

The Fund considers a company or issuer to be a “U.S. company” or “U.S. issuer” or a security to be “tied economically to the U.S.” if: (i) the company/issuer is organized under the laws of or domiciled in the U.S. or maintains its principal place of business in the U.S.; (ii) the security, or the security of such company/issuer, is traded principally in the U.S.; or (iii) during the most recent fiscal year of the company/issuer, the company/issuer derived at least 50% of its revenues or profits from goods produced or sold, investments made, or services performed in the U.S. or that has at least 50% of its assets in the U.S..

The Fund may invest in issuers of any market capitalization and securities of any maturity, and the Fund’s investments also may include securities purchased in IPOs.

The Fund also may invest up to 20% of its assets in equity and fixed income and debt securities and instruments of companies or entities (which need not be U.S. Realty Companies), including, but not limited to, securities of non-U.S. companies and other investment companies.

The Fund’s investments in preferred stock and convertible and fixed income and debt securities may include securities which, at the time of purchase, are rated below “investment grade” by an NRSRO, or the unrated equivalent as determined by the portfolio managers (“junk bonds”). The Fund may invest up to 20% of its assets in junk bonds.

The Fund may invest up to 5% of its assets in mortgage-related securities issued or guaranteed by U.S. issuers, including the U.S. government or one of its agencies or instrumentalities, or private issuers. The Fund is limited to investing in asset-backed securities issued by private issuers, and up to 5% of the Fund’s assets only.

In addition to purchasing options, the Fund may, but is not required to, write put and covered call options on securities and indexes, for hedging purposes or to seek to increase returns.

The Fund may invest in ETFs and similar products, which generally pursue a passive index-based strategy.

The Fund may, but is not required to, enter into futures contracts and/or swap agreements in an effort to protect the Fund’s investments against a decline in the value of Fund investments that could occur following the effective date of a large redemption order and while the Fund is selling securities to meet the redemption request. Since, in this event, the redemption order is priced at the (higher) value of the Fund’s investments at the effective date of redemption, these transactions would seek to protect the value of Fund shares remaining outstanding from dilution or magnified losses resulting from the Fund selling securities to meet the redemption request while the value of such securities is declining. For the most part, this approach is anticipated to be utilized, if at all, if a significant percentage of Fund shares is redeemed on a single day, or in other similar circumstances.

The Fund is classified as “non-diversified” under the 1940 Act, which means that it may invest a relatively high percentage of its assets in a limited number of issuers, when compared to a diversified fund.

General Investment Policies of the Fund

Temporary Strategies; Cash or Similar Investments. For temporary defensive purposes, the Adviser may invest up to 100% of the Fund’s total assets in high-quality, short-term debt securities and money market instruments. For longer periods of time, the Fund may hold a substantial cash position. These short-term debt securities and money market instruments include shares of corporate and government money market mutual funds and U.S. Government securities. Taking a temporary defensive position in cash or holding a large cash position for an extended period of time may result in the Fund not achieving its investment objectives and may be inconsistent with the Fund’s principal investment strategies. Furthermore, a certain portion of the Fund’s assets may be held in reserves, typically invested in shares of a money market mutual fund. The reserve position provides flexibility in meeting redemptions, paying expenses and managing cash flows into the Fund. To the extent that the Fund invests in money market mutual funds for its cash position, there will be some duplication of expenses because the Fund would bear its pro rata portion of such money market funds’ management fees and operational expenses.

Change in Investment Objective. The Fund’s investment objectives may be changed without the approval of the Fund’s shareholders upon 60 days’ prior written notice to shareholders. The Fund may not make any change in its investment policy of investing at least 80% of its assets in equity securities of U.S. Realty Companies and synthetic investments related to U.S. Realty Companies without first changing the Fund’s name and providing shareholders with at least 60 days’ prior written notice, except the Fund may take temporary defensive positions as described in this Prospectus without changing the Fund’s name or providing notice to shareholders.

Principal Risks of Investing in the Fund

Before investing in the Fund, you should carefully consider your own investment goals, the amount of time you are willing to leave your money invested, and the amount of risk you are willing to take. Remember, in addition to possibly not achieving your investment goals, you could lose money by investing in the Fund. Each risk summarized below is considered a “principal risk” of investing in the Fund, unless stated otherwise, regardless of the order in which it appears. The Fund is subject to the following principal risks:

Management Risk. The ability of the Fund to meet its investment objectives is directly related to the Adviser’s investment strategies for the Fund. The value of your investment in the Fund may vary with the effectiveness of the Adviser’s research, analysis and asset allocation among portfolio securities. If the Adviser’s investment strategies do not produce the expected results, your investment could be diminished or even lost.

Market Risk. The Fund may incur losses due to declines in one or more markets in which it invests. These declines may be the result of, among other things, political, regulatory, market, economic or social developments affecting the relevant market(s). In addition, turbulence in financial markets and reduced liquidity in equity, credit and/or fixed income markets may negatively affect many issuers, which could adversely affect the Fund. Global economies and financial markets are increasingly interconnected, and conditions and events in one country, region or financial market may adversely impact issuers in a different country, region or financial market. These risks may be magnified if certain events or developments adversely interrupt the global supply chain; in these and other circumstances, such risks might affect companies worldwide. As a result, local, regional or global events such as war, acts of terrorism, the spread of infectious illness or other public health issues, recessions or other events could have a significant negative impact on global economic and market conditions.

Issuer Risk. The value of a security may decline for a number of reasons which directly relate to the issuer, such as management performance, financial leverage and reduced demand for the issuer’s goods or services, as well as the historical and prospective earnings of the issuer and the value of its assets or factors unrelated to the issuer’s value, such as investor perception.

Real Estate-Related Securities Concentration Risk. The Fund’s investment portfolio is expected to be largely composed of securities of real estate-related companies. Because the investment objectives and strategies of the Fund are focused principally on real estate-related securities, the Fund does not intend to diversify its investments among securities from issuers in other industries. Due to this investment strategy focus, the performance of investments made by the Fund may be determined to a great extent by the current status of the real estate industry in general, or on other factors (such as interest rates and the availability of loan capital) that may affect the real estate industry, even if other industries would not be so affected. Consequently, the investment strategies of the Fund could lead to securities investment results that may be significantly different from investments in securities of other industries or sectors (e.g., technology, financial services, retail or manufacturing) or in a more broad-based portfolio generally. The Fund could lose money due to the performance of real estate-related securities even if markets generally are experiencing positive results.

Common Stock/Equity Securities Risk. The Fund will be exposed to equity market risk through direct investments in equity securities, and its investment in other equity-linked instruments. Common stocks are susceptible to general stock market fluctuations and to volatile increases and decreases in value as market confidence in and perceptions of their issuers change.

Preferred Securities Risk. There are various risks associated with investing in preferred securities, including credit risk; interest rate risk; deferral and omission of distributions; subordination; call and reinvestment risk; limited liquidity; limited voting rights and special issuer redemption rights. In addition, unlike common stock, participation in the growth of an issuer may be limited.

•Credit risk is the risk that a security held by the Fund will decline in price or the issuer of the security will fail to make dividend, interest or principal payments when due because the issuer experiences a decline in its financial status.

•Interest rate risk is the risk that securities will decline in value because of changes in market interest rates. When market interest rates rise, the market value of such securities generally will fall. Securities with longer periods before maturity or effective durations may be more sensitive to interest rate changes.

•Preferred securities may include provisions that permit the issuer, at its discretion, to defer or omit distributions for a stated period without any adverse consequences to the issuer.

•Preferred securities are generally subordinated to bonds and other debt instruments in an issuer’s capital structure in terms of having priority to corporate income, claims to corporate assets and liquidation payments, and therefore will be subject to greater credit risk than more senior debt instruments.

•During periods of declining interest rates, an issuer may be able to exercise an option to call, or redeem, its issue at par earlier than the scheduled maturity, which is generally known as call risk. If this occurs during a time of lower or declining interest rates, the Fund may have to reinvest the proceeds in lower yielding securities (and the Fund may not benefit from any increase in the value of its portfolio holdings as a result of declining interest rates). This is known as reinvestment risk.

•Certain preferred securities may be substantially less liquid than many other securities, such as common stocks or U.S. Government securities. Illiquid securities involve the risk that the securities will not be able to be sold at the time desired by the Fund or at prices approximating the value at which the Fund is carrying the securities on its books.

•Generally, traditional preferred securities offer no voting rights with respect to the issuer unless preferred dividends have been in arrears for a specified number of periods, at which time the preferred security holders may elect a number of directors to the issuer’s board. Generally, once all the arrearages have been paid, the preferred security holders no longer have voting rights. Hybrid-preferred security holders generally have no voting rights.

•In certain varying circumstances, an issuer of preferred securities may redeem the securities prior to a specified date. For instance, for certain types of preferred securities, a redemption may be triggered by a change in U.S. federal income tax or securities laws. As with call provisions, a redemption by the issuer may negatively impact the return of the security held by the Fund.

Convertible Securities Risk. The market value of a convertible security tends to perform like that of a regular debt security so that, if market interest rates rise, the value of the convertible security falls. Investments in rights and warrants involve certain risks including the possible lack of a liquid market for resale, price fluctuations and the failure of the price of the underlying security to reach a level at which the right or warrant can be prudently exercised, in which case the right or warrant may expire without being exercised and result in a loss of the Fund’s entire investment.

Recent Market Events Risk. U.S. and international markets have experienced volatility in recent months and years due to a number of economic, political and global macro factors, including rising inflation and the impact of COVID‑19, which has resulted in a public health crisis, business interruptions, growth concerns in the U.S. and overseas, supply chain shortages and labor shortages. The recovery from COVID-19 is proceeding at slower than expected rates and may last for a prolonged period of time.

Uncertainties regarding inflation, interest rates, political events, the Russia-Ukraine conflict, rising government debt in the U.S. and trade tensions have also contributed to market volatility.

Additionally, a rise in protectionist trade policies, slowing global economic growth, risks associated with epidemic and pandemic diseases, risks associated with the United Kingdom’s departure from the European Union, the risk of trade disputes, and the possibility of changes to some international trade agreements, could affect the economies of many nations, including the United States, in ways that cannot necessarily be foreseen at the present time. Continuing market volatility as a result of recent market conditions or other events may have adverse effects on your account.

Realty Companies, Real Estate Investments and REITs Risk. The Fund could lose money due to the performance of real estate-related securities even if securities markets generally are experiencing positive results. The performance of investments made by the Fund may be determined to a great extent by the current status of the real estate industry in general, or by other factors (such as interest rates and the availability of loan capital) that may affect the real estate industry, even if other industries would not be so affected. Consequently, the investment strategies of the Fund could lead to securities investment results that may be significantly different from investments in securities of other industries or sectors or in a more broad-based portfolio generally.

The risks related to investments in Realty Companies and Real Estate Investments include, but are not limited to: adverse changes in general economic and local market conditions; adverse developments in employment; changes in supply or demand for similar or competing properties; unfavorable changes in applicable taxes, governmental regulations and interest rates; operating or development expenses; and lack of available financing.

REITs are subject to similar risks as Real Estate Investments and Realty Companies. Due to certain special considerations that apply to REITs, investments in REITs may carry additional risks not necessarily present in investments in other securities. REIT securities (including those trading on national exchanges) typically have trading volumes that are less than those of common stocks of other stocks traded on national exchanges, which may affect the Fund’s ability to trade or liquidate those securities. An investment in REITs may be adversely affected if the REIT fails to comply with applicable laws and regulations, including failing to qualify as a REIT under the Code. A REIT generally is not taxed on income distributed to its shareholders if it complies with certain federal income tax requirements relating primarily to its organization, ownership, assets and income and, further, if it distributes at least 90% of its taxable income to shareholders each year. Under certain circumstances, a REIT may fail to qualify for pass-through treatment for tax purposes, which would subject the REIT to federal income taxes at the REIT level and adversely affect the value of the Fund’s investment in such REIT. The Fund generally will have no control over the operations and policies of a REIT, and the Fund generally will have no ability to cause a REIT to take the actions necessary to qualify as a REIT.

Small and Mid Capitalization Companies Risk. Small and mid capitalization companies carry additional risks because their earnings tend to be less predictable, their share prices more volatile and their securities less liquid than larger, more established companies. The shares of small and mid capitalization companies tend to trade less frequently than those of larger companies, which can have an adverse effect on the pricing of these securities and on the ability to sell these securities when the portfolio managers deem it appropriate.

Non-Diversification Risk. The NAV of the Fund may be more vulnerable to changes in the market value of a single issuer or group of issuers and may be relatively more susceptible to adverse effects from any single corporate, industry, economic, market, political or regulatory occurrence than if the Fund’s investments consisted of securities issued by a larger number of issuers.

Fixed Income and Debt Securities Risk. The market value of a debt security may decline due to general market conditions that are not specifically related to a particular company, such as real or perceived adverse economic conditions, changes in the outlook for corporate earnings, changes in interest or currency rates or adverse investor sentiment generally. The debt securities market can be susceptible to increases in volatility and decreases in liquidity. Liquidity can decline unpredictably in response to overall economic conditions or credit tightening.

Prices of bonds and other debt securities tend to move inversely with changes in interest rates. Typically, a rise in rates will adversely affect debt securities and, accordingly, will cause the value of the Fund’s investments in these securities to decline. Interest rate risk is usually greater for fixed-income securities with longer maturities or durations. A rise in interest rates (or the expectation of a rise in interest rates) may result in periods of volatility, decreased liquidity and increased redemptions, and, as a result, the Fund may have to liquidate Fund securities at disadvantageous prices. Risks associated with rising interest rates are heightened given that the Federal Reserve has raised the federal funds rate several times in recent periods and may continue to increase rates in the near future. During periods of reduced market liquidity, the Fund may not be able to readily sell debt securities at prices at or near their perceived value. An unexpected increase in Fund redemption requests, including a single large request for a significant percentage of the Fund’s shares, which may be triggered by market turmoil or an increase in interest rates, could cause the Fund to sell its holdings at a loss or at undesirable prices and adversely affect the Fund’s share price and increase the Fund’s liquidity risk and/or Fund expenses. Economic and other developments can adversely affect debt securities markets.

The Fund’s investments in lower-rated, higher-yielding securities (“junk bonds”) are subject to greater credit risk than its higher rated investments. Credit risk is the risk that the issuer will not make interest or principal payments, or will not make payments on a timely basis. Non-investment grade securities tend to be more volatile, less liquid and are considered speculative. If there is a decline, or perceived decline, in the credit quality of a debt security (or any guarantor of payment on such security), the security’s value could fall, potentially lowering the Fund’s share price. The prices of non-investment grade securities, unlike investment grade debt securities, may fluctuate unpredictably and not necessarily inversely with changes in interest rates. The prices of high yield securities can fall in response to negative news about the issuer or its industry, or the economy in general to a greater extent than those of higher rated securities. The market for these securities may be less liquid and therefore these securities may be harder to value or sell at an acceptable price, especially during times of market volatility or decline.

Some fixed-income securities may give the issuer the option to call, or redeem, the securities before their maturity. If securities held by the Fund are called during a time of declining interest rates (which is typically the case when issuers exercise options to call outstanding securities), the Fund may have to reinvest the proceeds in an investment offering a lower yield (and the Fund may not fully benefit from any increase in the value of its portfolio holdings as a result of declining interest rates).

Adjustable rate securities provide the Fund with a certain degree of protection against rises in interest rates, although such securities will participate in any declines in interest rates as well. Certain adjustable rate securities, such as those with interest rates that fluctuate directly or indirectly based on multiples of a stated index, are designed to be highly sensitive to changes in interest rates and can subject the holders thereof to extreme reductions of yield and possibly loss of principal. Certain fixed-income securities may be issued at a discount from their face value (such as zero coupon securities) or purchased at a price less than their stated face amount or at a price less than their issue price plus the portion of “original issue discount” previously accrued thereon, i.e., purchased at a “market discount.” The amount of original issue discount and/or market discount on certain obligations may be significant, and accretion of market discount together with original issue discount will cause the Fund to realize income prior to the receipt of cash payments with respect to these securities.

Structured notes are privately negotiated debt instruments where the principal and/or interest is determined by reference to a specified asset, market or rate, or the differential performance of two assets or markets. Structured notes can have risks of both debt securities and derivative transactions.

Non-U.S. Securities Risk. The Fund’s performance will be influenced by political, social and economic factors affecting the non-U.S. countries and companies in which the Fund invests. Non-U.S. securities carry special risks, such as less developed or less efficient trading markets, political instability, a lack of company information, differing auditing and legal standards, and, potentially, less liquidity. Additionally, certain non- U.S. markets may rely heavily on particular industries and are more vulnerable to diplomatic developments, the imposition of economic sanctions against a particular country or countries, organizations, entities and/or individuals, changes in international trading patterns, trade barriers, and other protectionist or retaliatory measures. International trade barriers or economic sanctions against foreign countries, organizations, entities and/or individuals may adversely affect the Fund’s foreign holdings or exposures.

Investments in non-U.S. companies include ADRs and similar investments, including European Depositary Receipts (“EDRs”) and Global Depositary Receipts (“GDRs”), dollar-denominated foreign securities and securities purchased directly on foreign exchanges. ADRs, EDRs and GDRs are depositary receipts for non-U.S. company stocks that are not themselves listed on a U.S. exchange, and are issued by a bank and held in trust at that bank, and that entitle the owner of such depositary receipts to any capital gains or dividends from the foreign company stocks underlying the depositary receipts. ADRs are U.S. dollar denominated. EDRs and GDRs are typically U.S. dollar denominated but may be denominated in a foreign currency.

Options Risk. Writing options on securities and indexes, including for hedging purposes, may increase volatility or reduce returns, perhaps substantially, particularly since most derivatives have a leverage component that provides investment exposure in excess of the amount invested, and may cause the Fund to experience losses greater than if the Fund had not engaged in such transactions. Writing options is subject to many of the risks of, and can be highly sensitive to changes in the value of, the related security or index. As such, a small commitment to written options could potentially have a relatively large impact on the Fund’s performance. Purchasing options will reduce returns by the amount of premiums paid for options that are not exercised. Over- the-counter options purchased on securities and indexes are subject to the risk of default by the counterparty and can be illiquid.

Investment Companies and ETF Risk. The Fund may invest in shares of other investment companies, including ETFs. The Fund limits its investments in securities issued by other investment companies in accordance with the 1940 Act. With certain exceptions, Section 12(d)(1) of the 1940 Act precludes the Fund from acquiring (i) more than 3% of the total outstanding shares of another investment company; (ii) shares of another investment company having an aggregate value in excess of 5% of the value of the total assets of the Fund; or (iii) shares of another registered investment company and all other investment companies having an aggregate value in excess of 10% of the value of the total assets of the Fund (such limits do not apply to investments in money market funds). However, Section 12(d)(1)(F) of the 1940 Act provides that the provisions of paragraph 12(d)(1) shall not apply to securities purchased or otherwise acquired by the Fund if: (i) immediately after such purchase or acquisition not more than 3% of the total outstanding shares of such investment company is owned by the Fund and all affiliated persons of the Fund; and (ii) the Fund has not offered or sold, and is not proposing to offer or sell its shares through a principal underwriter or otherwise at a public offering price that includes a sales load of more than 1 1/2%.

The Fund may also rely on Rule 12d1-4 of the 1940 Act, which provides an exemption from Section 12(d)(1) that allows the Fund to invest all of its assets in other registered funds, including ETFs, if the Fund satisfies certain conditions specified in the Rule, including, among other conditions, that the Fund

and its advisory group will not control (individually or in the aggregate) an acquired fund (e.g., hold more than 25% of the outstanding voting securities of an acquired fund that is a registered open-end management investment company).

Derivatives and Hedging Risk. Derivatives transactions, including those entered into for hedging purposes (i.e., seeking to protect Fund investments), may increase volatility, reduce returns, limit gains or magnify losses, perhaps substantially, particularly since most derivatives have a leverage component that provides investment exposure in excess of the amount invested. Over-the-counter swap agreements, forward currency contracts, writing or purchasing over-the-counter options on securities (including options on ETFs and ETNs), indexes and currencies and other over-the-counter derivatives transactions are subject to the risk of default by the counterparty and can be illiquid. Changes in liquidity may result in significant, rapid and unpredictable changes in the prices for derivatives. These derivatives transactions, as well as the exchange-traded futures and options in which the Fund may invest, are subject to many of the risks of, and can be highly sensitive to changes in the value of, the related index, commodity, interest rate, currency, security or other reference asset. As such, a small investment could have a potentially large impact on the Fund’s performance. Purchasing options will reduce returns by the amount of premiums paid for options that are not exercised. In fact, many derivatives may be subject to greater risks than those associated with investing directly in the underlying or other reference asset.

Derivatives transactions incur costs, either explicitly or implicitly, which reduce returns, and costs of engaging in such transactions may outweigh any gains or any losses averted from hedging activities. Successful use of derivatives, whether for hedging or for other investment purposes, is subject to the portfolio managers’ ability to predict correctly movements in the direction of the relevant reference asset or market and, for hedging activities, correlation of the derivative instruments used with the investments seeking to be hedged. Use of derivatives transactions, even when entered into for hedging purposes, may cause the Fund to experience losses greater than if the Fund had not engaged in such transactions.

The regulation of the U.S. and non-U.S. derivatives markets has undergone substantial change in recent years and such change may continue. In particular, new Rule 18f-4 under the 1940 Act (the “Derivatives Rule”), adopted by the SEC on October 28, 2020, replaces the asset segregation regime of Investment Company Act Release No. 10666 (Release 10666) with a new framework for the use of derivatives by registered funds. The Fund’s treatment of derivatives may change following the implementation of the Derivatives Rule.

IPO Shares Risk. The prices of securities purchased in IPOs can be very volatile. The effect of IPOs on the Fund’s performance depends on a variety of factors, including the number of IPOs the Fund invests in relative to the size of the Fund and whether and to what extent a security purchased in an IPO appreciates or depreciates in value. As the Fund’s asset base increases, IPOs may have a diminished effect on the Fund’s performance.

Cybersecurity Risk. With the increased use of technologies such as the Internet to conduct business, the Fund is susceptible to operational, information security, and related risks. In general, cyber incidents can result from deliberate attacks or unintentional events. Cyber attacks include, but are not limited to, gaining unauthorized access to digital systems (e.g., through “hacking” or malicious software coding) for purposes of misappropriating assets or sensitive information, corrupting data, or causing operational disruption. Cyber attacks may also be carried out in a manner that does not require gaining unauthorized access, such as causing denial-of-service attacks on websites (i.e., efforts to make network services unavailable to intended users). Cyber incidents affecting the Fund or its service providers have the ability to cause disruptions and impact business operations, potentially resulting in financial losses, interference with the Fund’s ability to calculate its NAV, impediments to trading, the inability of shareholders to transact business, violations of applicable privacy and other laws, regulatory fines, penalties, reputational damage, reimbursement or other compensation costs, or additional compliance costs. Similar adverse

consequences could result from cyber incidents affecting issuers of securities in which the Fund invests, counterparties with which the Fund engages in transactions, governmental and other regulatory authorities, exchange and other financial market operators, banks, brokers, dealers, insurance companies and other financial institutions (including financial intermediaries and service providers for shareholders) and other parties. In addition, substantial costs may be incurred in order to prevent any cyber incidents in the future. While the Fund’s service providers have established business continuity plans in the event of, and risk management systems to prevent, such cyber incidents, there are inherent limitations in such plans and systems including the possibility that certain risks have not been identified. Furthermore, the Fund cannot control the cyber security plans and systems put in place by its service providers or any other third parties whose operations may affect the Fund or its shareholders. As a result, the Fund and its shareholders could be negatively impacted.

Depositary Receipts Risk. ADRs and similar depositary receipts typically will be subject to certain of the risks associated with direct investments in the securities of non-U.S. companies, because their values depend on the performance of the underlying non-U.S. securities. However, currency fluctuations will impact investments in depositary receipts differently than direct investments in non-U.S. dollar-denominated non-U.S. securities, because a depositary receipt will not appreciate in value solely as a result of appreciation in the currency in which the underlying non-U.S. dollar security is denominated. Certain countries may limit the ability to convert depositary receipts into the underlying non-U.S. securities and vice versa, which may cause the securities of the non-U.S. company to trade at a discount or premium to the market price of the related depositary receipt. The Fund may invest in depositary receipts through an unsponsored facility where the depositary issues the depositary receipts without an agreement with the company that issues the underlying securities. Holders of unsponsored depositary receipts generally bear all the costs of such facilities, and the depositary of an unsponsored facility frequently is under no obligation to distribute shareholder communications received from the issuer of the deposited security or to pass through voting rights to the holders of the depositary receipts with respect to the deposited securities. As a result, available information concerning the issuer may not be as current as for sponsored depositary receipts, and the prices of unsponsored depositary receipts may be more volatile than if such instruments were sponsored by the issuer.