Exhibit 99.1

Exhibit 99.1

September 20, 2012

MasterCard Incorporated

2012 Investment Community Meeting

©2012 MasterCard. Proprietary.

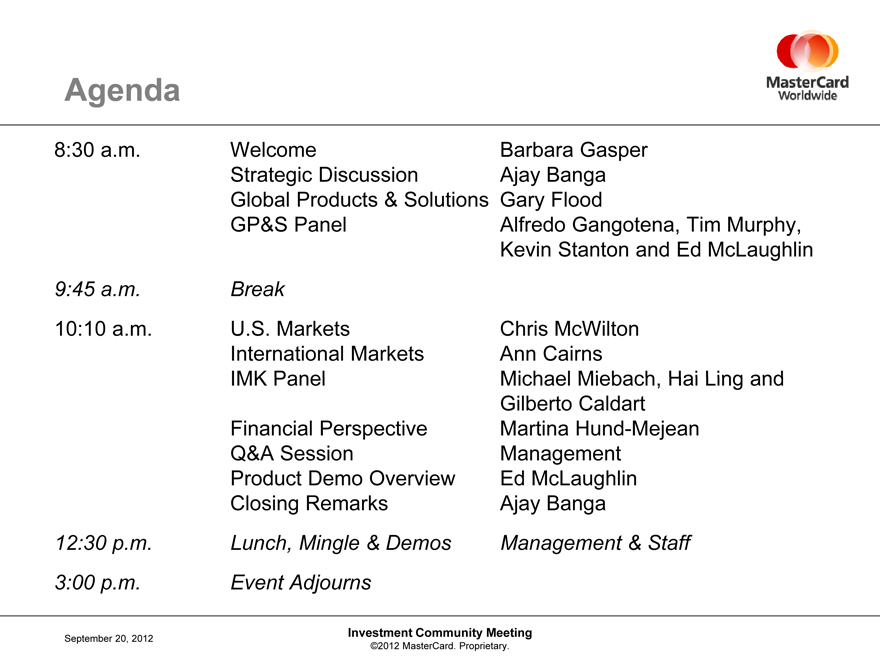

Agenda

Agenda

8:30 a.m.

Welcome

Strategic Discussion Global Products & Solutions GP&S Panel

Barbara Gasper Ajay Banga Gary Flood

Alfredo Gangotena, Tim Murphy, Kevin Stanton and Ed McLaughlin

9:45 a.m.

Break

10:10 a.m.

U.S. Markets International Markets IMK Panel

Chris McWilton Ann Cairns

Michael Miebach, Hai Ling and Gilberto Caldart

Financial Perspective Q&A Session Product Demo Overview Closing Remarks

Martina Hund-Mejean Management Ed McLaughlin Ajay Banga

12:30 p.m.

Lunch, Mingle & Demos

Management & Staff

3:00 p.m.

Event Adjourns

September 20, 2012

Investment Community Meeting

©2012 MasterCard. Proprietary.

|

|

Forward-Looking Statements

Today’s presentation may contain, in addition to historical information, forward looking statements within the meaning of the Private Securities Litigation Reform Act of 1995.

These forward-looking statements are based on our current assumptions, expectations and projections about future events which reflect the best judgment of management and involve a number of risks and uncertainties that could cause actual results to differ materially from those suggested by our comments today. You should review and consider the information contained in our filings with the SEC regarding these risks and uncertainties.

MasterCard disclaims any obligation to publicly update or revise any forward-looking statements or information provided during today’s presentations.

Any non-GAAP information contained in today’s presentations is reconciled to its GAAP equivalent in the Company’s periodic SEC filings.

September 20, 2012

Investment Community Meeting

©2012 MasterCard. Proprietary.

|

|

Ajay Banga

President and Chief Executive Officer September 20, 2012

Executing on the Strategy

2012 Investment Community Meeting

©2012 MasterCard. Proprietary.

|

|

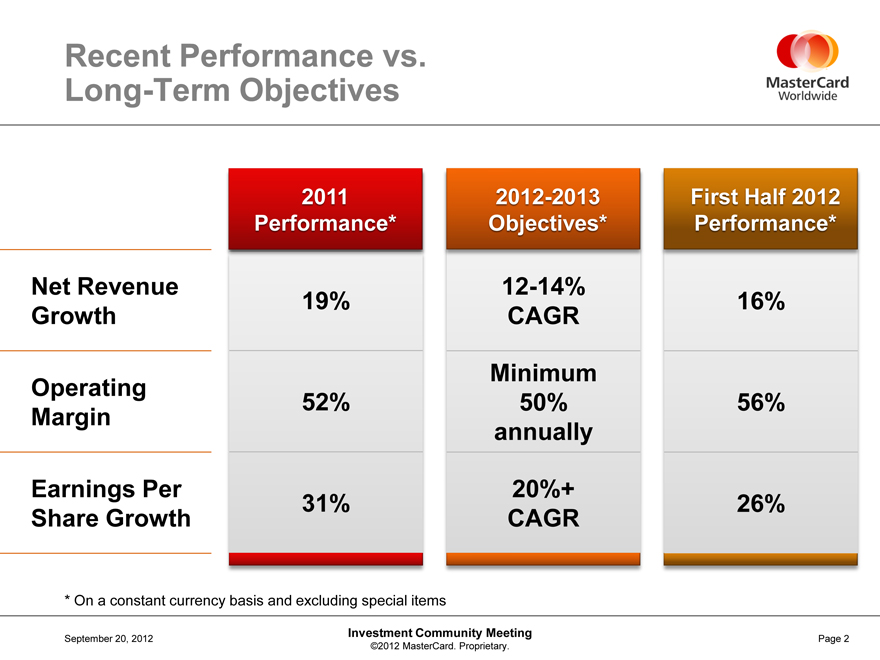

Recent Performance vs.

Long-Term Objectives

Net Revenue

Growth

Operating

Margin

Earnings Per

Share Growth

2011

Performance*

19%

52%

31%

2012-2013

Objectives*

12-14%

CAGR

Minimum

50%

annually

20%+

CAGR

First Half 2012

Performance*

16%

56%

26%

* On a constant currency basis and excluding special items

September 20, 2012

Investment Community Meeting

©2012 MasterCard. Proprietary.

Page 2

|

|

Three Drivers of Growth

Personal Consumption Expenditure

Cash & Check vs. Electronic Payments

MasterCard Share of Electronic Payments

September 20, 2012

Investment Community Meeting

©2012 MasterCard. Proprietary.

Page 3

|

|

Stakeholders

Consumers – B2B2C

Merchants – Value-added partner

Issuers – Complementary value propositions

Governments & Opinion Leaders – Local engagement

Solutions Driven by Data and Technology

September 20, 2012

Investment Community Meeting

©2012 MasterCard. Proprietary.

Page 4

|

|

Executing on the Strategy

GROW

Core Business

• Invest in Credit, Debit, Commercial and Prepaid products

• Win key deals

• Grow share

DIVERSIFY

Geographies & Customers

• Engage with non-traditional customers and governments

• Increase focus on emerging markets

BUILD

New Businesses

• Invest in e-Commerce and Mobile channels

• Invest in Information Services

Execute on Grow, Diversify, Build initiatives to gain share and grow the pie

Investment Community Meeting

©2012 MasterCard. Proprietary.

September 20, 2012

Page 5

|

|

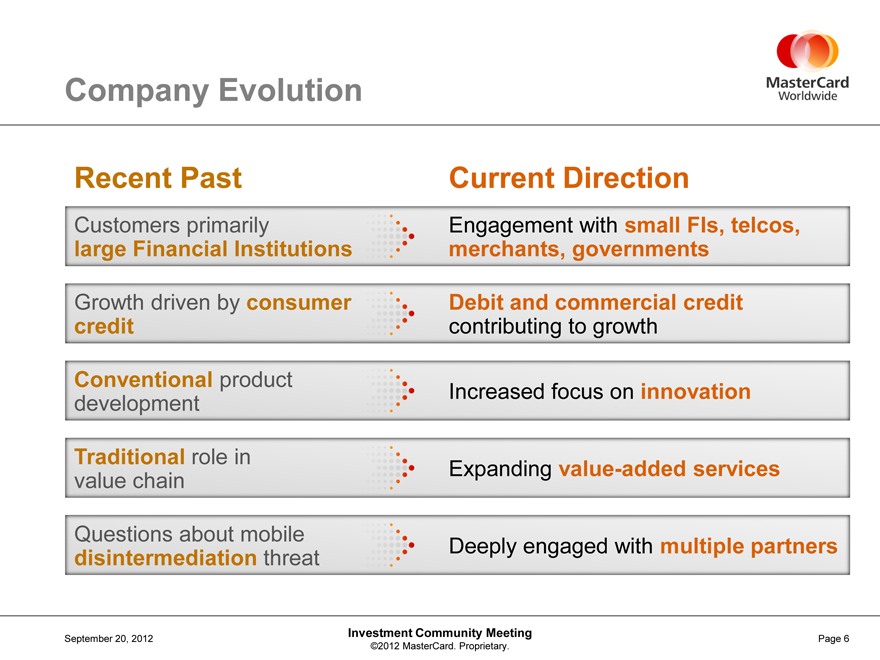

Company Evolution

Recent Past

Customers primarily

large Financial Institutions

Growth driven by consumer credit

Conventional product development

Traditional role in value chain

Questions about mobile disintermediation threat

Current Direction

Engagement with small FIs, telcos, merchants, governments

Debit and commercial credit contributing to growth

Increased focus on innovation

Expanding value-added services

Deeply engaged with multiple partners

Investment Community Meeting

©2012 MasterCard. Proprietary.

September 20, 2012

Page 6

|

|

Gary Flood

President, Global Products & Solutions

September 20, 2012

Driving Growth through Products & Solutions

2012 Investment Community Meeting

©2012 MasterCard. Proprietary.

|

|

Driving Growth

GROW

Core Businesses Faster than Market

DIVERSIFY

Customers and Geographies

BUILD

New, High-Growth Scalable Businesses

…capitalizing on:

Enormous Cash Conversion Opportunity

Evolving Industry Landscape

Investment Community Meeting

©2012 MasterCard. Proprietary.

September 20, 2012

Page 2

|

|

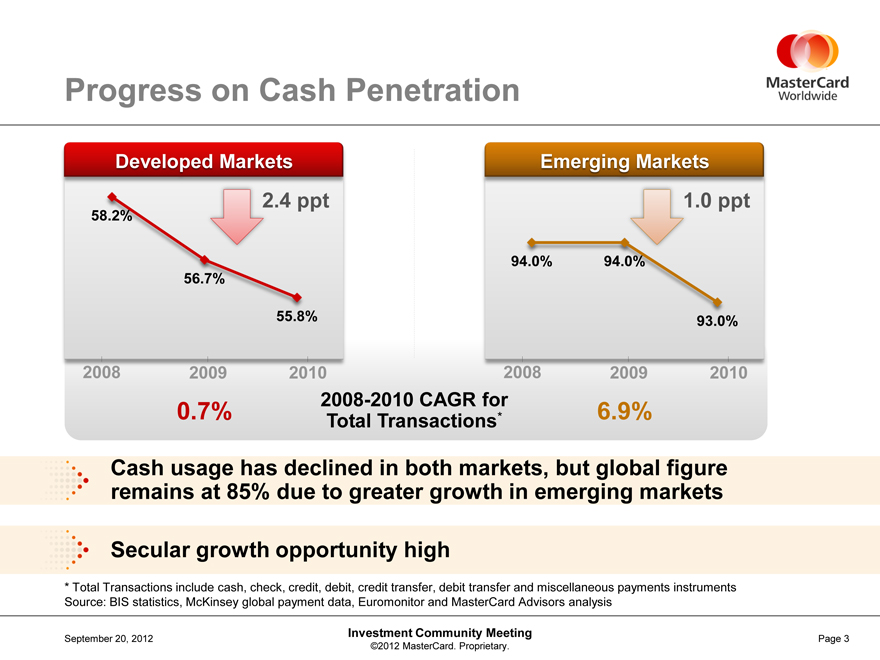

Progress on Cash Penetration

Developed Markets

Emerging Markets

2.4 ppt

58.2%

56.7%

55.8%

2008

2009

2010

1.0 ppt

94.0%

94.0%

93.0%

2008

2009

2010

2008-2010 CAGR for Total Transactions

0.7% *

6.9%

Cash usage has declined in both markets, but global figure remains at 85% due to greater growth in emerging markets

Secular growth opportunity high

* Total Transactions include cash, check, credit, debit, credit transfer, debit transfer and miscellaneous payments instruments Source: BIS statistics, McKinsey global payment data, Euromonitor and MasterCard Advisors analysis

Investment Community Meeting

©2012 MasterCard. Proprietary.

September 20, 2012

Page 3

|

|

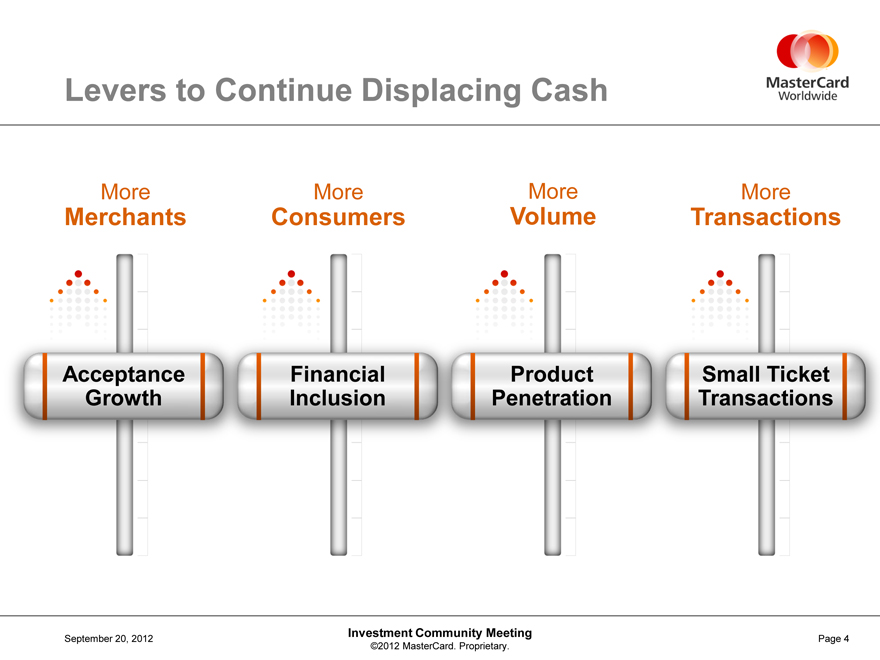

Levers to Continue Displacing Cash

More Merchants

Acceptance Growth

More Consumers

Financial Inclusion

More Volume

Product Penetration

More Transactions

Small Ticket Transactions

Investment Community Meeting

©2012 MasterCard. Proprietary.

September 20, 2012

Page 4

|

|

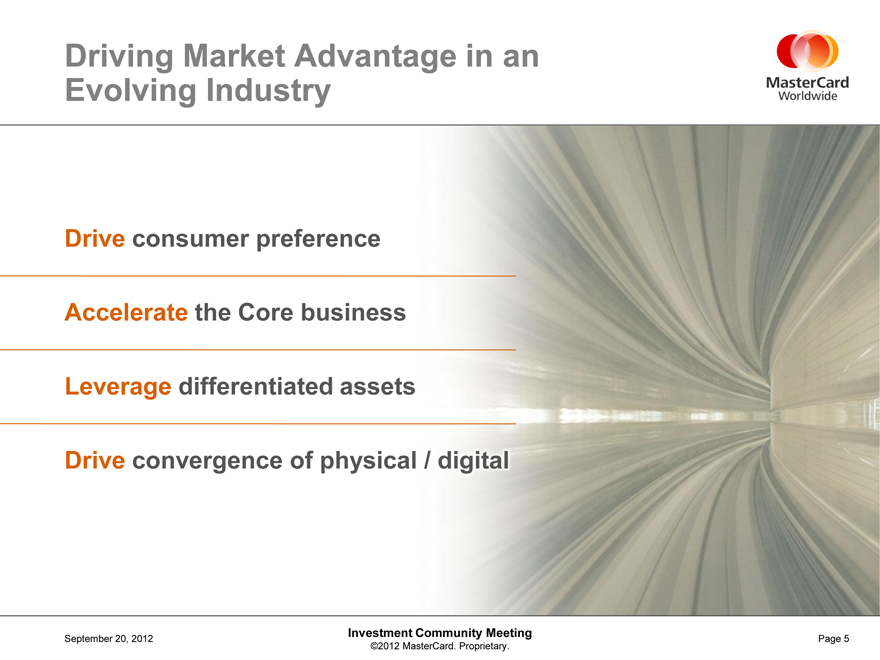

Driving Market Advantage in an Evolving Industry

Drive consumer preference

Accelerate the Core business

Leverage differentiated assets

Drive convergence of physical / digital

Investment Community Meeting

©2012 MasterCard. Proprietary.

September 20, 2012

Page 5

|

|

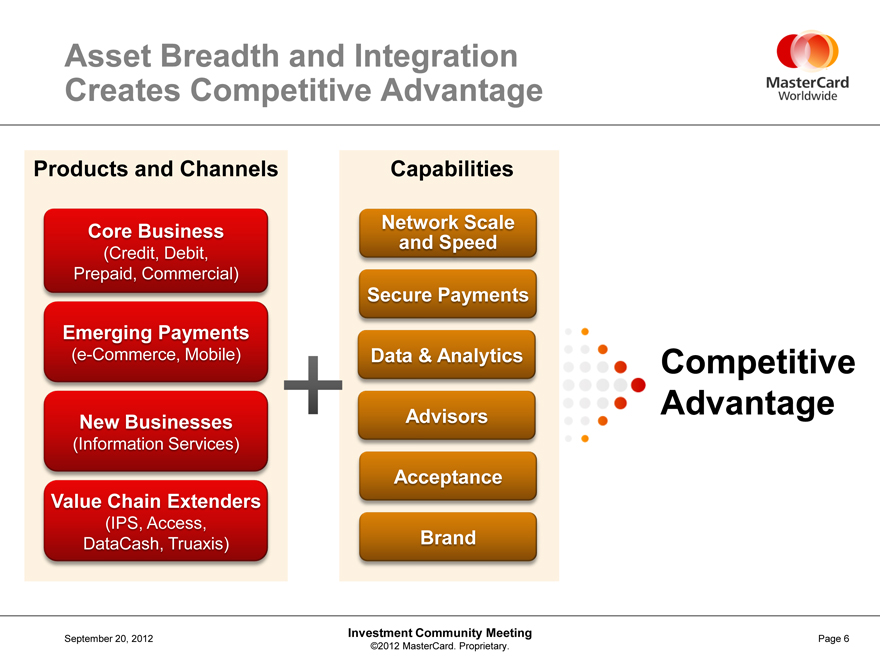

Asset Breadth and Integration

Creates Competitive Advantage

Products and Channels

Core Business

(Credit, Debit, Prepaid, Commercial)

Emerging Payments (e-Commerce, Mobile)

New Businesses (Information Services)

Value Chain Extenders (IPS, Access, DataCash, Truaxis)

Capabilities

Network Scale and Speed

Secure Payments

Data & Analytics

Advisors

Acceptance

Brand

Competitive Advantage

Investment Community Meeting

©2012 MasterCard. Proprietary.

September 20, 2012

Page 6

|

|

Alfredo Gangotena

Chief Marketing Officer

September 20, 2012

Brand Preference:

The Key to Business Growth

2012 Investment Community Meeting

©2012 MasterCard. Proprietary.

|

|

Marketing Strategic Focus

Transforming Consumer Insight Into Growth

From brand awareness to brand preference

Delivering a unique shopping experience

Return on investment

Investment Community Meeting

©2012 MasterCard. Proprietary.

September 20, 2012

Page 2

|

|

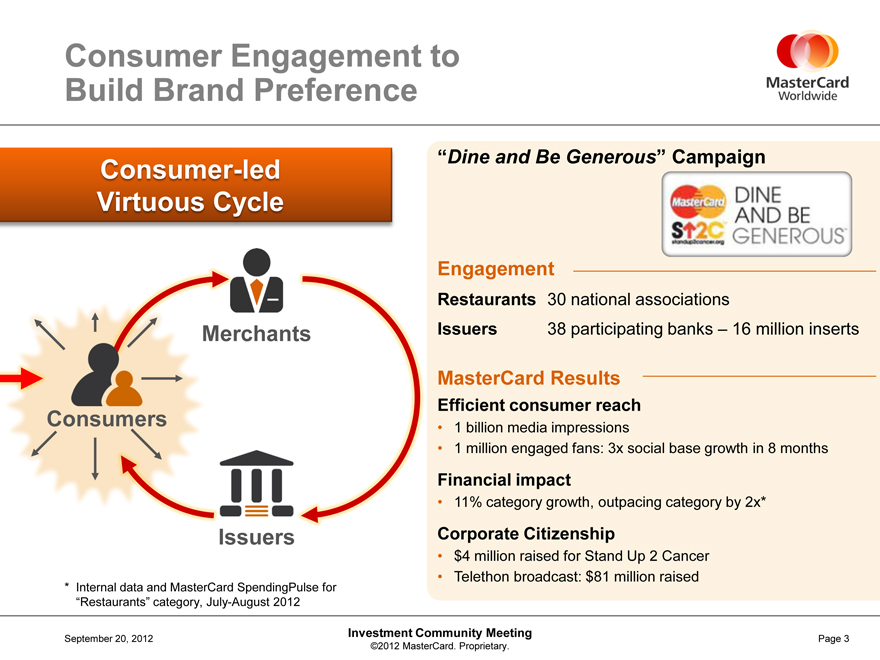

Consumer Engagement to Build Brand Preference

Consumer-led Virtuous Cycle

Merchants

Consumers

Issuers

Internal data and MasterCard SpendingPulse for “Restaurants” category, July-August 2012

“Dine and Be Generous” Campaign

Engagement

Restaurants 30 national associations

Issuers 38 participating banks – 16 million inserts

MasterCard Results

Efficient consumer reach

| 1 |

|

billion media impressions |

| 1 |

|

million engaged fans: 3x social base growth in 8 months |

Financial impact

11% category growth, outpacing category by 2x*

Corporate Citizenship

$4 million raised for Stand Up 2 Cancer

Telethon broadcast: $81 million raised

Investment Community Meeting

©2012 MasterCard. Proprietary.

September 20, 2012

Page 3

|

|

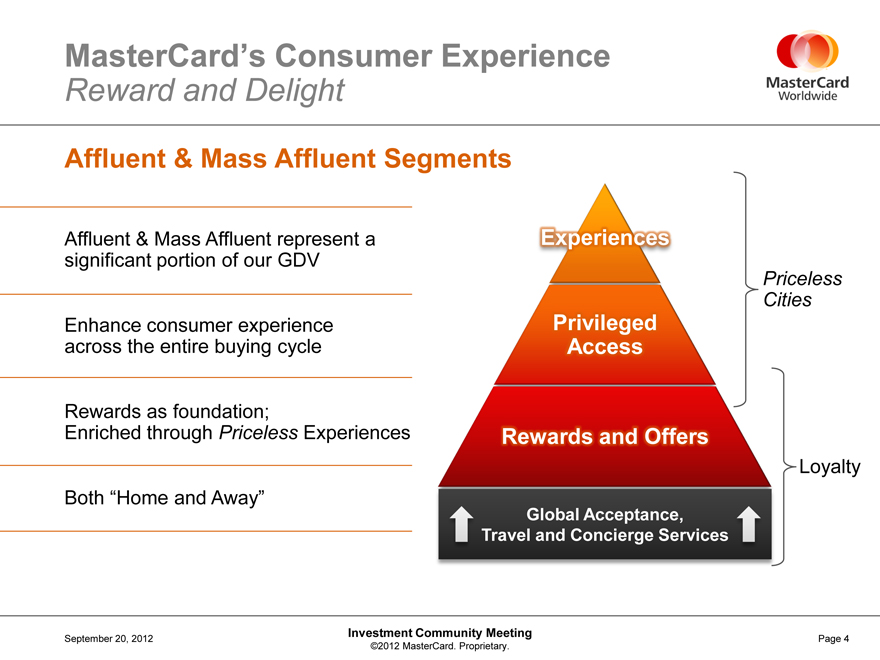

MasterCard’s Consumer Experience

Reward and Delight

Affluent & Mass Affluent Segments

Affluent & Mass Affluent represent a significant portion of our GDV

Enhance consumer experience across the entire buying cycle

Rewards as foundation; Enriched through Priceless Experiences

Both “Home and Away”

Experiences

Privileged Access

Priceless Cities

Rewards and Offers

Global Acceptance, Travel and Concierge Services

Loyalty

Investment Community Meeting

©2012 MasterCard. Proprietary.

September 20, 2012

Page 4

|

|

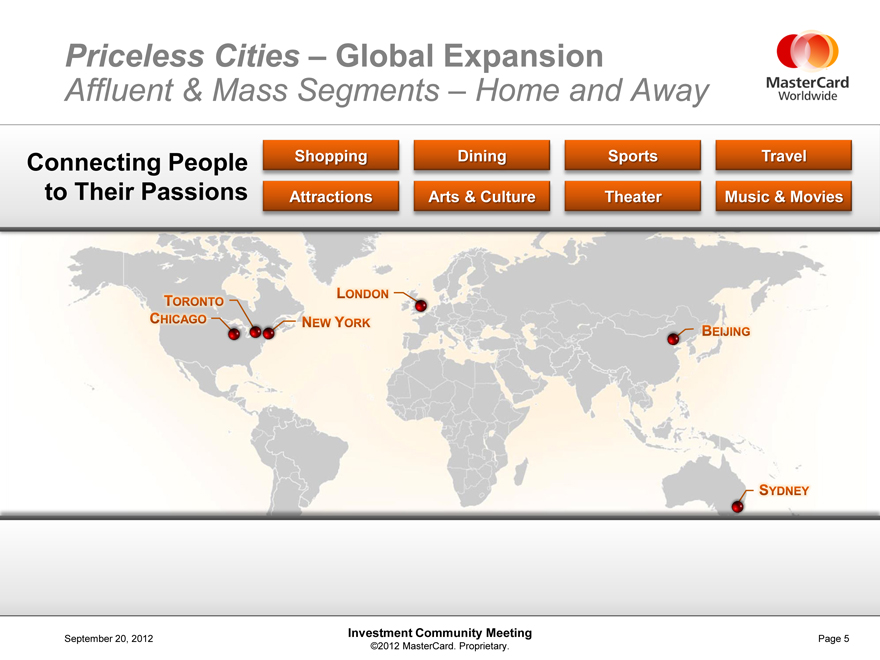

Priceless Cities – Global Expansion

Affluent & Mass Segments – Home and Away

Connecting People to Their Passions

Shopping Dining Sports Travel

Attractions Arts & Culture Theater Music & Movies

Toronto

Chicago

New York

London

Beijing

Sydney

Investment Community Meeting

©2012 MasterCard. Proprietary.

September 20, 2012

Page 5

|

|

Priceless Cities – Global Expansion

Affluent & Mass Segments – Home and Away

Connecting People to Their Passions

Shopping

Dining

Sports

Travel

Attractions

Arts & Culture

Theater

Music & Movies

Toronto

Chicago

Los Angeles

Mexico City

London

New York

Miami

Paris

Rio de Janeiro

Moscow

Istanbul

Singapore

Beijing

Sydney

A few of our participating partners

Investment Community Meeting

©2012 MasterCard. Proprietary.

September 20, 2012

Page 6

|

|

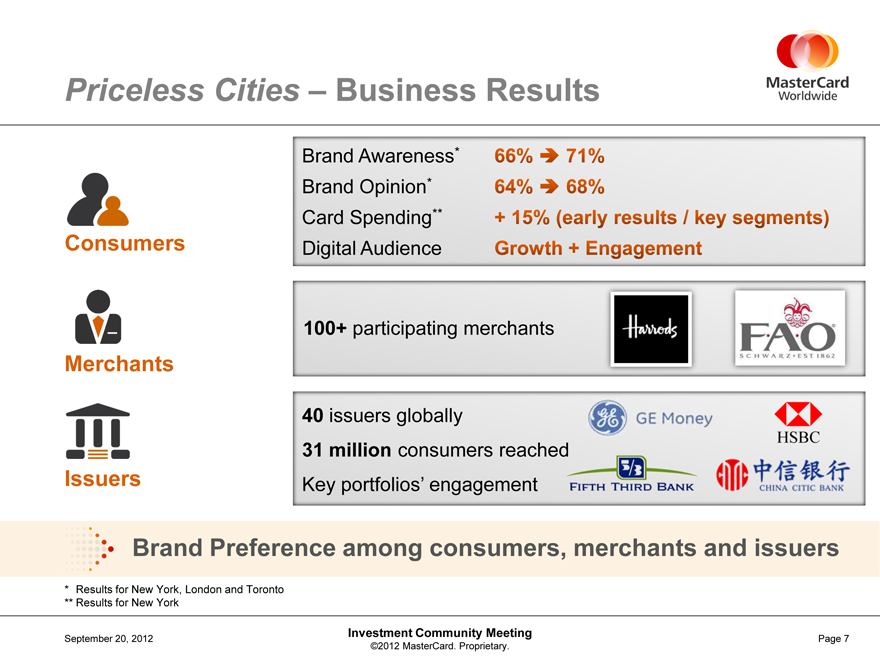

Priceless Cities– Business Results

Brand Awareness*

66% ® 71%

Brand Opinion*

64% ® 68%

Card Spending**

+ 15% (early results / key segments)

Digital Audience

Growth + Engagement

Consumers

Merchants

Issuers

100+ participating merchants

40 issuers globally

31 million consumers reached

Key portfolios’ engagement

Brand Preference among consumers, merchants and issuers

* Results for New York, London and Toronto

** Results for New York

Investment Community Meeting

©2012 MasterCard. Proprietary.

September 20, 2012

Page 7

|

|

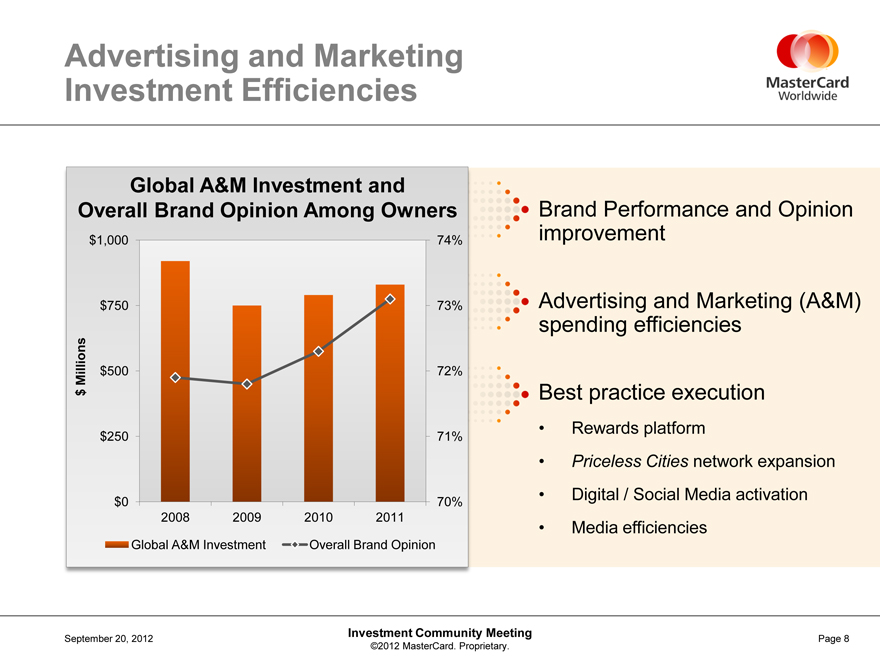

Advertising and Marketing

Investment Efficiencies

Global A&M Investment and Overall Brand Opinion Among Owners

Brand Performance and Opinion improvement

Advertising and Marketing (A&M) spending efficiencies

Best practice execution

• Rewards platform

• Priceless Cities network expansion

• Digital / Social Media activation

• Media efficiencies

$ Millions

$1,000

$750

$500

$250

$0

2008

2009

2010

2011

74%

73%

72%

71%

70%

Global A&M Investment

Overall Brand Opinion

Investment Community Meeting

©2012 MasterCard. Proprietary.

September 20, 2012

Page 8

|

|

Tim Murphy

Chief Product Officer

September 20, 2012

Accelerating Growth Faster than Market: Commercial

2012 Investment Community Meeting

©2012 MasterCard. Proprietary.

|

|

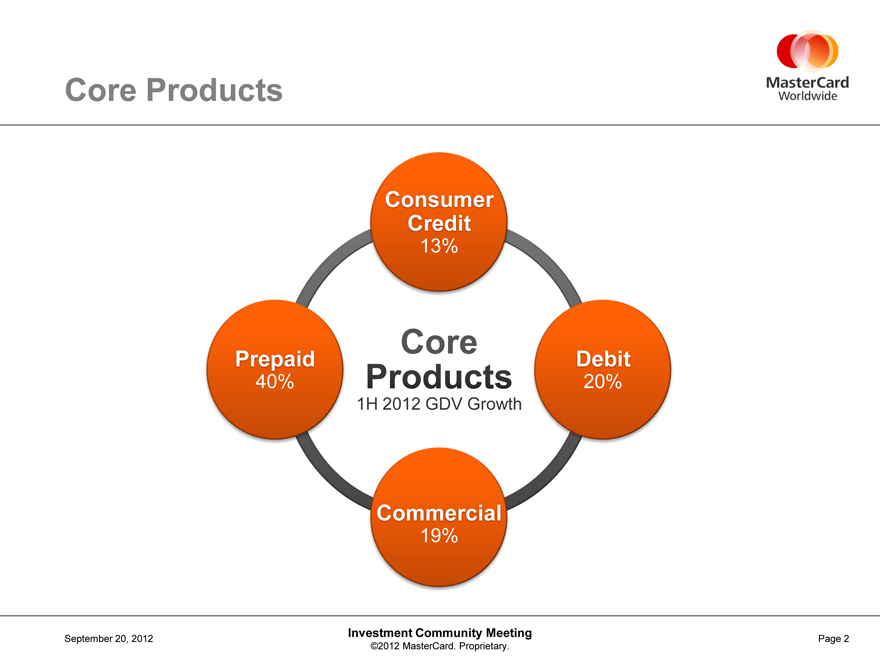

Core Products

Consumer Credit 13%

Core Products 1H 2012 GDV Growth

Debit 20%

Prepaid 40%

Commercial 19%

Investment Community Meeting

©2012 MasterCard. Proprietary.

September 20, 2012

Page 2

|

|

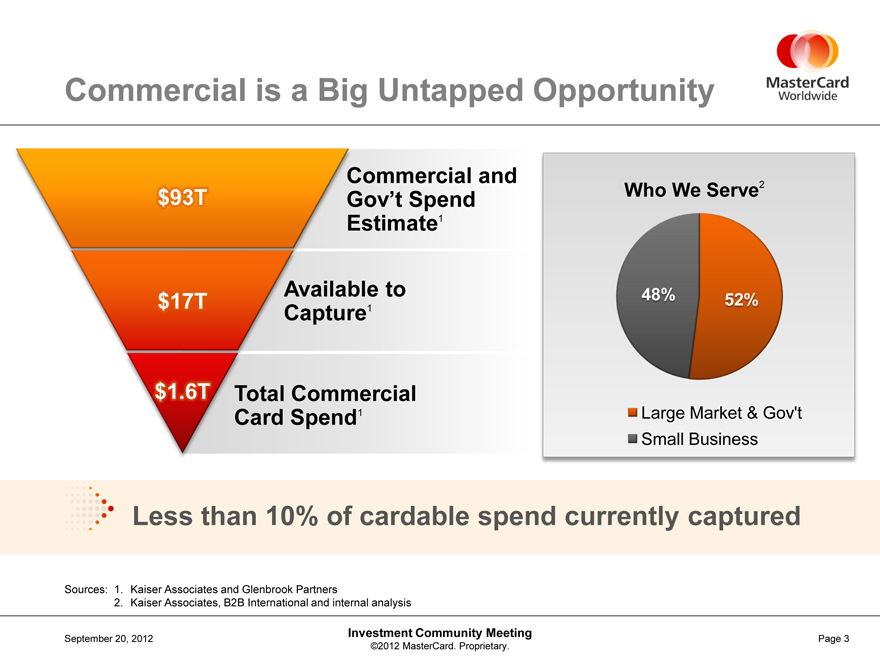

Commercial is a Big Untapped Opportunity

$93T

Commercial and Gov’t Spend

Estimate1

Available to Capture1

$17T

Total Commercial Card Spend1

$1.6T

Who We Serve2

Large Market & Gov’t

48%

52%

Small Business

Less than 10% of cardable spend currently captured

Sources:

1. Kaiser Associates and Glenbrook Partners

2. Kaiser Associates, B2B International and internal analysis

Investment Community Meeting

©2012 MasterCard. Proprietary.

September 20, 2012

Page 3

|

|

Investments in People

Deepen Relationships

…and with leading corporations around the world

Investment Community Meeting

©2012 MasterCard. Proprietary.

September 20, 2012

Page 4

|

|

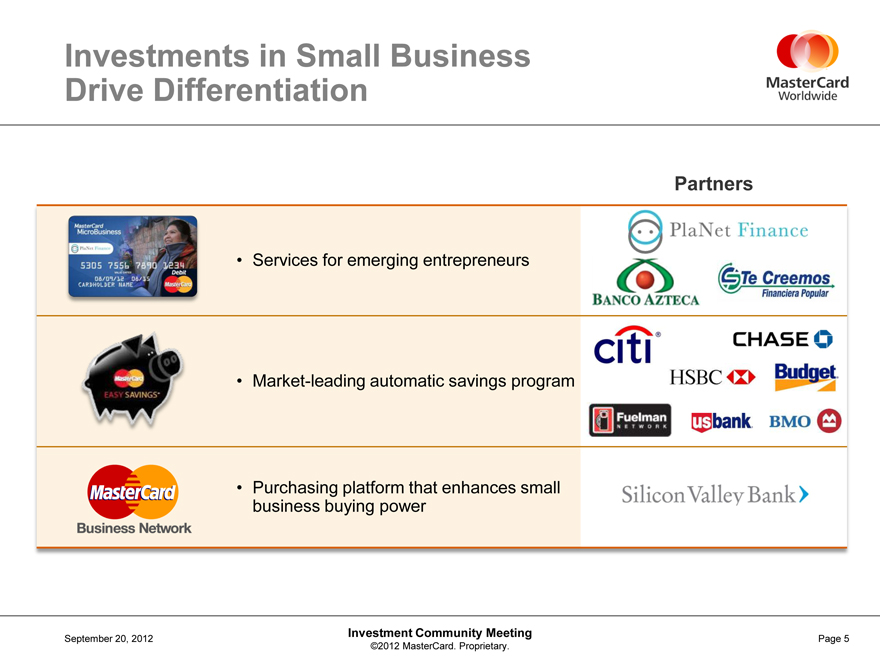

Investments in Small Business

Drive Differentiation

Services for emerging entrepreneurs

Market-leading automatic savings program

Purchasing platform that enhances small business buying power

Partners

Investment Community Meeting

©2012 MasterCard. Proprietary.

September 20, 2012

Page 5

|

|

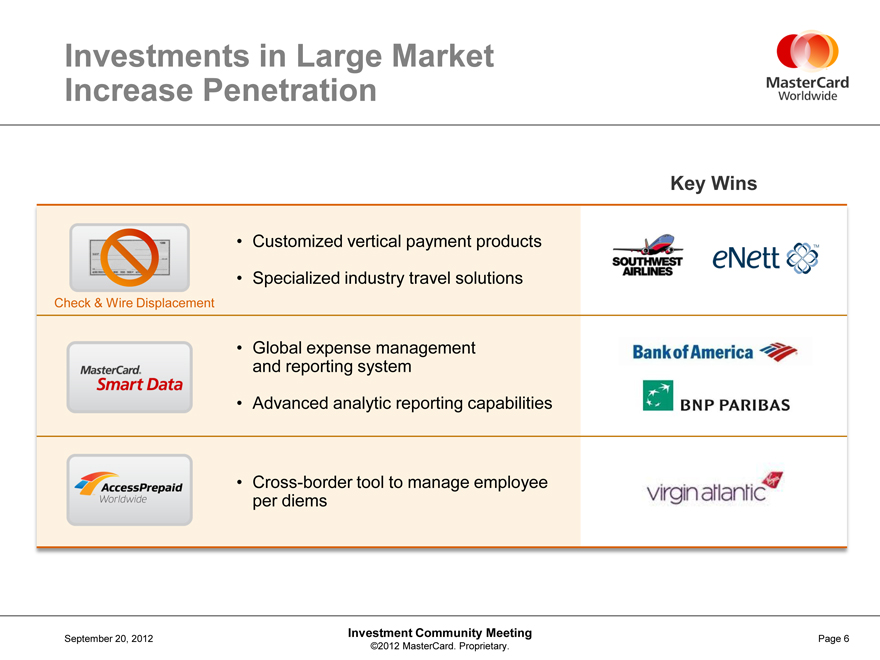

Investments in Large Market

Increase Penetration

Key Wins

Customized vertical payment products

Specialized industry travel solutions

Check & Wire Displacement

Global expense management and reporting system

Advanced analytic reporting capabilities

Cross-border tool to manage employee per diems

Investment Community Meeting

©2012 MasterCard. Proprietary.

September 20, 2012

Page 6

|

|

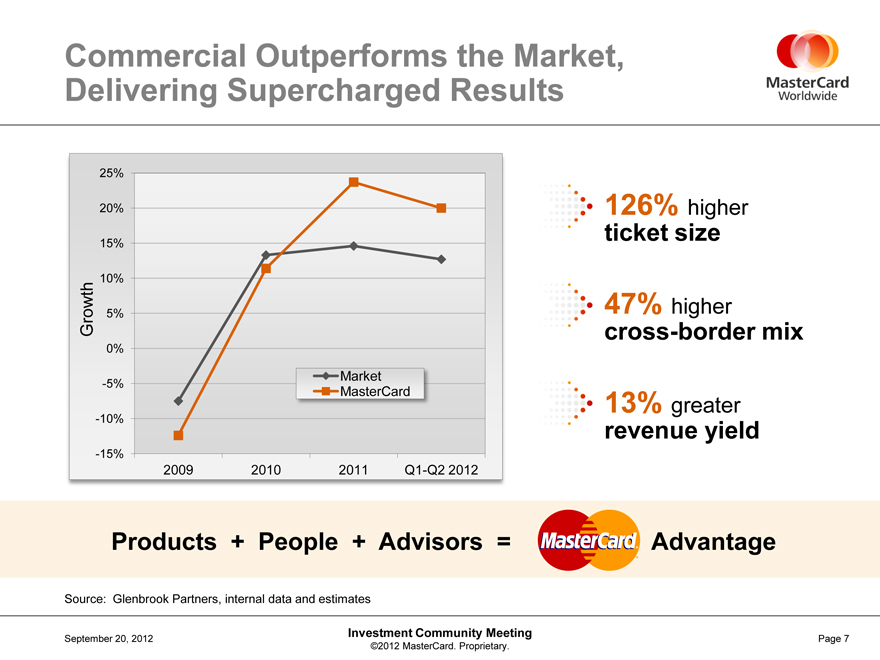

Commercial Outperforms the Market, Delivering Supercharged Results

Growth

25%

20%

15%

10%

5%

0%

-5%

-10%

-15%

2009

2010

2011

Q1-Q2 2012

Market

MasterCard

126% higher ticket size

47% higher cross-border mix

13% greater revenue yield

Products + People + Advisors = Advantage

Source: Glenbrook Partners, internal data and estimates

Investment Community Meeting

©2012 MasterCard. Proprietary.

September 20, 2012

Page 7

|

|

Kevin Stanton

President, MasterCard Advisors September 20, 2012

MasterCard Advisors:

Proven Currency, Force Multiplier, Game Changer

2012 Investment Community Meeting

©2012 MasterCard. Proprietary.

|

|

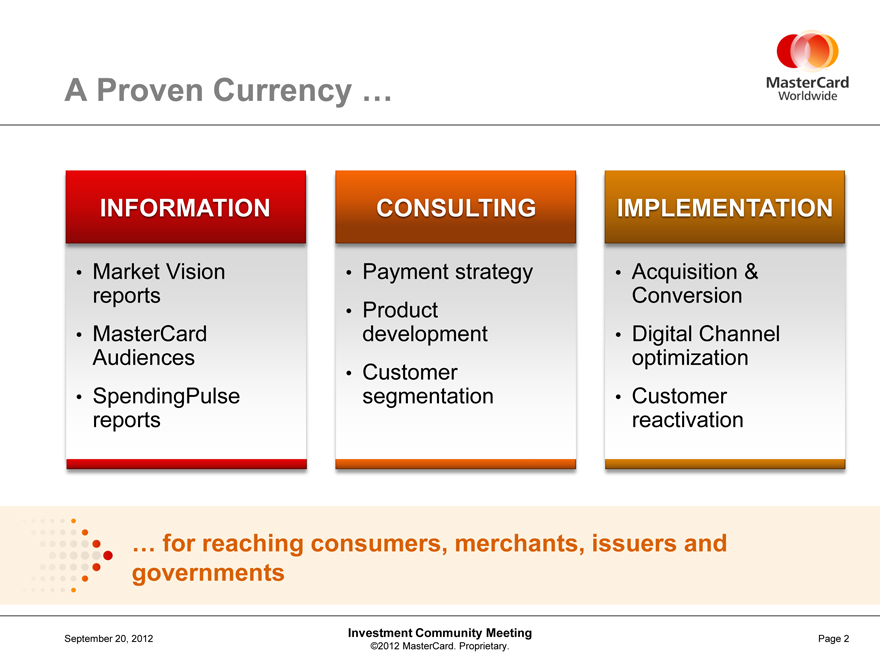

A Proven Currency

INFORMATION

Market Vision reports

MasterCard Audiences

SpendingPulse reports

CONSULTING

Payment strategy

Product development

Customer segmentation

IMPLEMENTATION

Acquisition & Conversion

Digital Channel optimization

Customer reactivation

… for reaching consumers, merchants, issuers and governments

Investment Community Meeting

©2012 MasterCard. Proprietary.

September 20, 2012

Page 2

|

|

A Force Multiplier …

DEAL

Credit Agreement

Debit Agreement

PRODUCT

Debit Five Steps

U.S. EMV Migration

MARKET

Sub-Saharan Programs

SEGMENT

Small Merchant

e-Commerce Authorization

Deutsche Telekom Mobile

U.S. Affluent Credit Reactivation

… to drive growth at the deal, product, market and segment level

Investment Community Meeting

©2012 MasterCard. Proprietary.

September 20, 2012

Page 3

|

|

A Game Changer …

… to drive new value and reach new customers

Investment Community Meeting

©2012 MasterCard. Proprietary.

September 20, 2012

Page 4

|

|

Ed McLaughlin

Chief Emerging Payments Officer

September 20, 2012

Convergence

2012 Investment Community Meeting

©2012 MasterCard. Proprietary.

|

|

Emerging Payments Growth Opportunity

Transforming the shopping experience

Expanding our reach to new consumers

Extending our network to new merchants

Leading the transition to digital

Investment Community Meeting

©2012 MasterCard. Proprietary.

September 20, 2012

Page 2

|

|

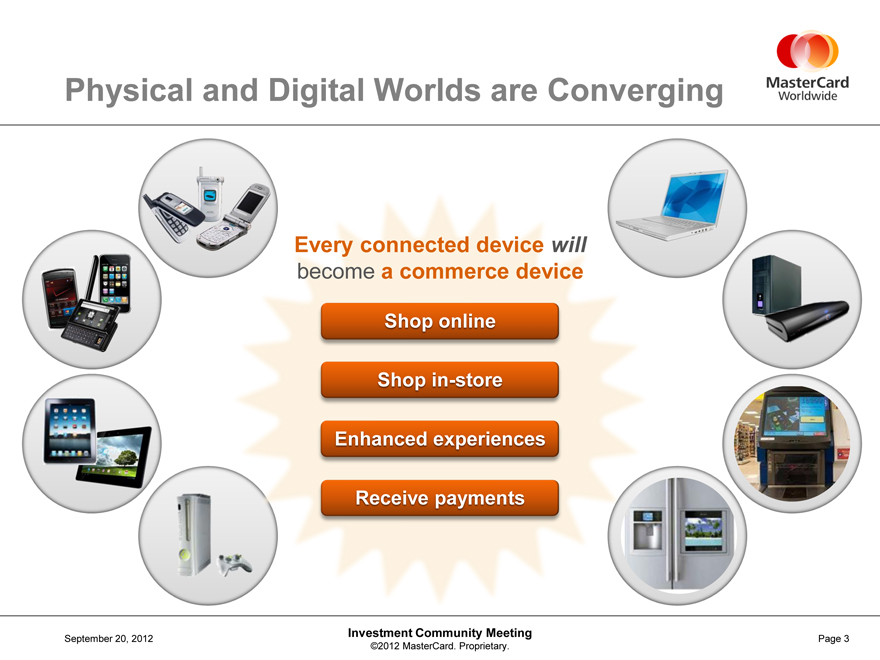

Physical and Digital Worlds are Converging

Every connected device will become a commerce device

Shop online

Shop in-store

Enhanced experiences

Receive payments

Investment Community Meeting

©2012 MasterCard. Proprietary.

September 20, 2012

Page 3

|

|

Consumers are Transacting Anywhere

Online, Offline, Physical, Digital

Receiving payroll and social benefits on mobile phone or card

Paying bills or merchants via SMS on a mobile phone

Accessing ATMs and merchants

Consumer Experiences

Emerging Market

Developed Market

Shopping on a mobile phone

Commuting with a PayPass enabled mobile phone

Dining with a physical card

Investment Community Meeting

©2012 MasterCard. Proprietary.

September 20, 2012

Page 4

|

|

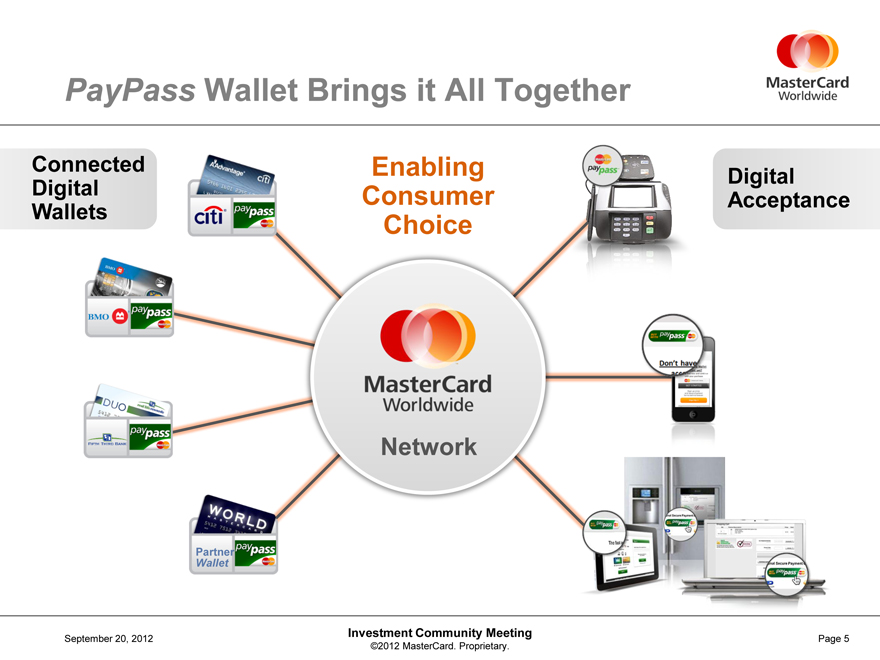

PayPass Wallet Brings it All Together

Connected Digital Wallets

Enabling Consumer Choice

Digital Acceptance

Network

Partner Wallet

Investment Community Meeting

©2012 MasterCard. Proprietary.

September 20, 2012

Page 5

Working with Partners

Working with Partners

September 20, 2012

Investment Community Meeting

©2012 MasterCard. Proprietary.

Page 6

|

|

Chris McWilton

President, U.S. Markets

September 20, 2012

Path to Partnership and Value:

U.S. Markets

2012 Investment Community Meeting

©2012 MasterCard. Proprietary.

|

|

Navigating the Regulatory and Legal Landscape

Maximizing market share/presence on debit cards

Enhancing debit value proposition

Continuing to solidify relationships and balance of ecosystem

Serving all stakeholders through an amicable resolution

Advocating on behalf of the consumer

Investment Community Meeting

©2012 MasterCard. Proprietary.

September 20, 2012

Page 2

|

|

Focused on Our Core Business

Differentiated product suite

Proven success in optimizing portfolio growth and management

Strong platform to optimize consumer engagement

Investment Community Meeting

©2012 MasterCard. Proprietary.

September 20, 2012

Page 3

|

|

Leading EMV Migration

Clear roadmap that addresses securing all channels

Creating the right dialogue as partners and counselors

Playing a key role in bringing the market together

Understanding product-specific implications to develop the right approach

Investment Community Meeting

©2012 MasterCard. Proprietary.

September 20, 2012

Page 4

|

|

Growing Merchant Relationships for Shared Value

Insights and tools to optimize, streamline and grow operations

Focus on programs that increase consumer preference and stickiness

Open new acceptance channels

Investment Community Meeting

©2012 MasterCard. Proprietary.

September 20, 2012

Page 5

|

|

Delivering Value and Growth to Governments

Strong programs and momentum

Government – reduced costs; greater efficiency

Recipient – greater access and empowerment

Investment Community Meeting

©2012 MasterCard. Proprietary.

September 20, 2012

Page 6

|

|

Staying True to Our Course

Investment Community Meeting

©2012 MasterCard. Proprietary.

September 20, 2012

Page 7

|

|

Ann Cairns

President, International Markets

September 20, 2012

International Markets:

Strength through Diversification

2012 Investment Community Meeting

©2012 MasterCard. Proprietary.

|

|

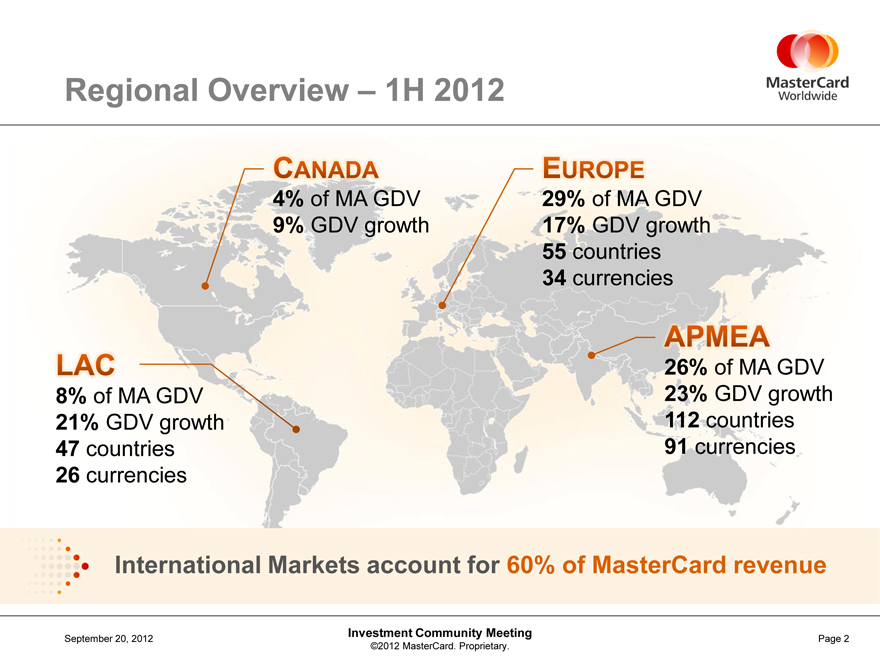

Regional Overview – 1H 2012

4% of MA GDV

9% GDV growth

29% of MA GDV

17% GDV growth

55 countries

34 currencies

8% of MA GDV

21% GDV growth

47 countries

26 currencies

26% of MA GDV

23% GDV growth

112 countries

91 currencies

International Markets account for 60% of MasterCard revenue

Investment Community Meeting

©2012 MasterCard. Proprietary.

September 20, 2012

Page 2

|

|

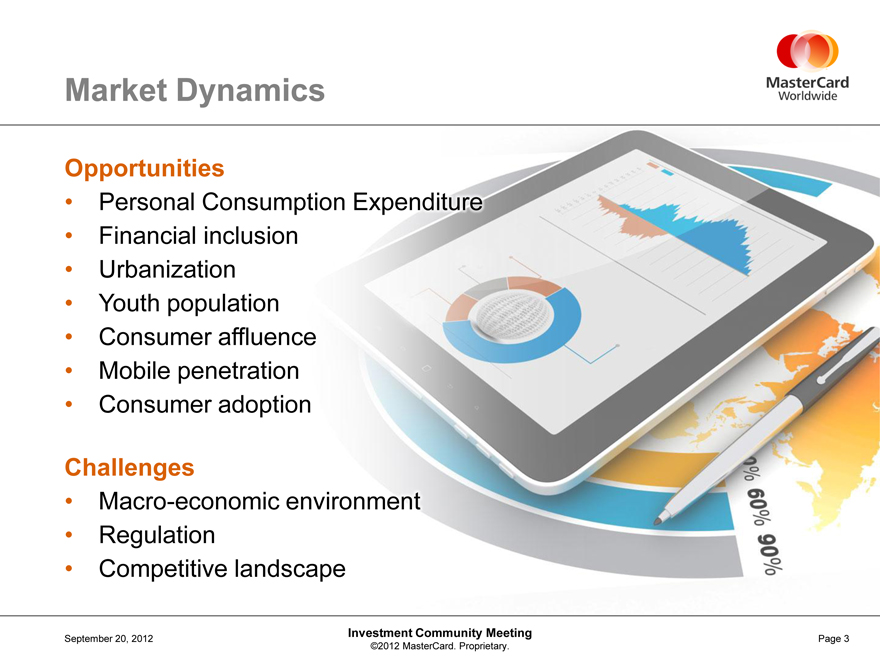

Market Dynamics

Opportunities

Personal Consumption Expenditure

Financial inclusion

Urbanization

Youth population

Consumer affluence

Mobile penetration

Consumer adoption

Challenges

Macro-economic environment

Regulation

Competitive landscape

Investment Community Meeting

©2012 MasterCard. Proprietary.

September 20, 2012

Page 3

|

|

Executing on Our Strategy

Invest and gain share in emerging and mature markets

Drive increased acceptance

Diversify with non-traditional partners

Engage with governments

Develop global and local strategic partnerships

Investment Community Meeting

©2012 MasterCard. Proprietary.

September 20, 2012

Page 4

|

|

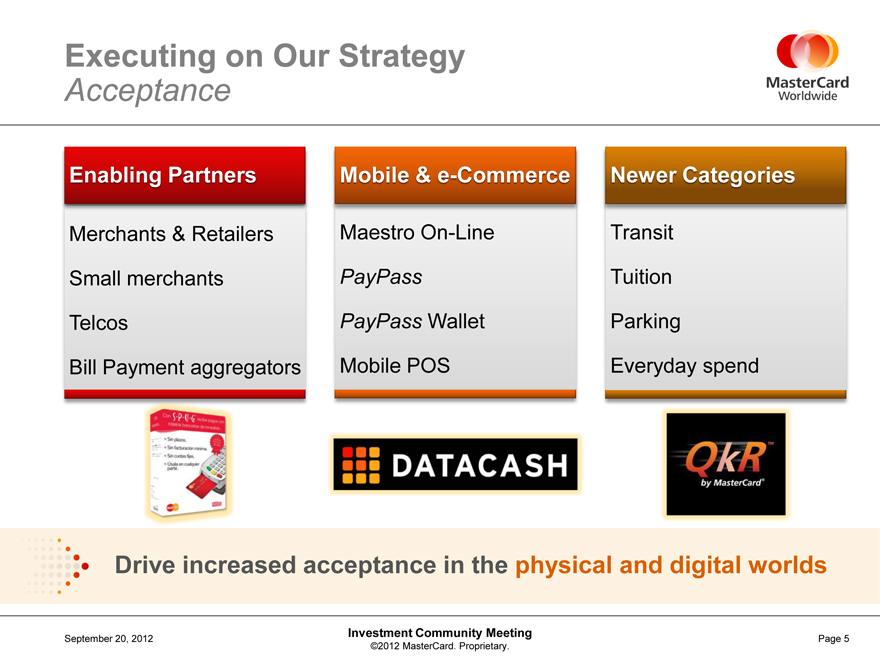

Executing on Our Strategy

Acceptance

Enabling Partners

Merchants & Retailers

Small merchants

Telcos

Bill Payment aggregators

Mobile & e-Commerce

Maestro On-Line

PayPass

PayPass Wallet

Mobile POS

Newer Categories

Transit

Tuition

Parking

Everyday spend

Drive increased acceptance in the physical and digital worlds

Investment Community Meeting

©2012 MasterCard. Proprietary.

September 20, 2012

Page 5

|

|

Executing on Our Strategy

Governments

Efficiency

Social benefits

T&E cards

Transit

Purchasing cards

ID cards

Financial Inclusion

Agricultural payments

Prepaid products

Mobile

Infrastructure

Education

Thought Leadership

Cost of Cash studies

Regulations

Tax collection

SpendingPulse

World Beyond Cash

South Africa

Brazil

India

Mexico

Partner to create a World Beyond Cash

Investment Community Meeting

©2012 MasterCard. Proprietary.

September 20, 2012

Page 6

|

|

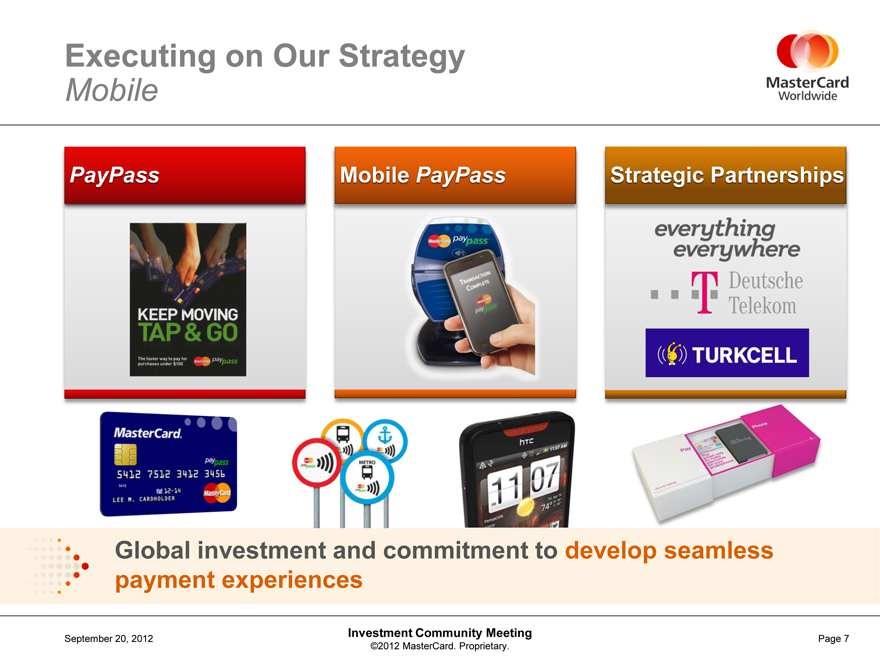

Executing on Our Strategy

Mobile

PayPass

Mobile PayPass

Strategic Partnerships

Global investment and commitment to develop seamless payment experiences

Investment Community Meeting

©2012 MasterCard. Proprietary.

September 20, 2012

Page 7

|

|

International Markets

Panel Discussion

Michael Miebach

President, Middle East & Africa

Expanding in Emerging Markets:

Partnering with Governments

Hai Ling

President, Greater China

China: Partnering with Major

Local Players

Gilberto Caldart

President, South Latin America

Brazil: Innovative Growth Engine

Investment Community Meeting

©2012 MasterCard. Proprietary.

September 20, 2012

Page 8

|

|

September 20, 2012

IMK Panel

2012 Investment Community Meeting

©2012 MasterCard. Proprietary.

|

|

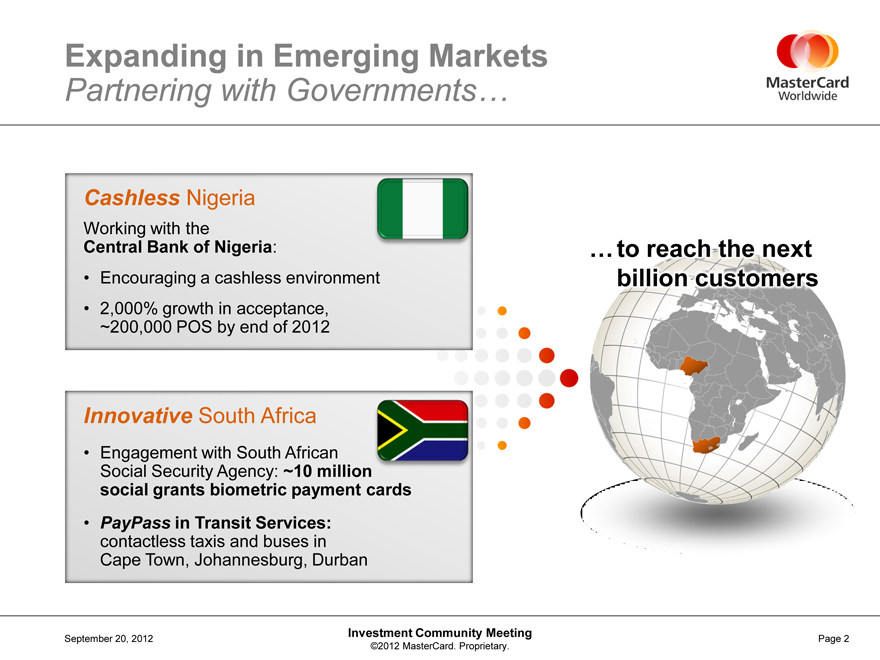

Expanding in Emerging Markets

Partnering with Governments…

… to reach the next billion customers

Cashless Nigeria

Working with the Central Bank of Nigeria:

• Encouraging a cashless environment

2,000% growth in acceptance, ~200,000 POS by end of 2012

Innovative South Africa

Engagement with South African Social Security Agency: ~10 million social grants biometric payment cards

PayPass in Transit Services: contactless taxis and buses in Cape Town, Johannesburg, Durban

Investment Community Meeting

©2012 MasterCard. Proprietary.

September 20, 2012

Page 2

|

|

China

Partnering with Major Local Players

MasterCard is special in Chinese: Everything is Attainable

Significant Market Opportunity

World’s 2nd largest economy, expected to grow at 7% - 8% (2011 GDP = $7.3 trillion)

Rapid urbanization: 67% of population will be urban by 2020 (900 million)

Sizable emerging middle class:

Income US$10,000 – US$60,000

Size ~ 300 million

2nd highest number of High Net Worth individuals in Asia

Local Strategic Partnerships

Investment Community Meeting

©2012 MasterCard. Proprietary.

September 20, 2012

Page 3

|

|

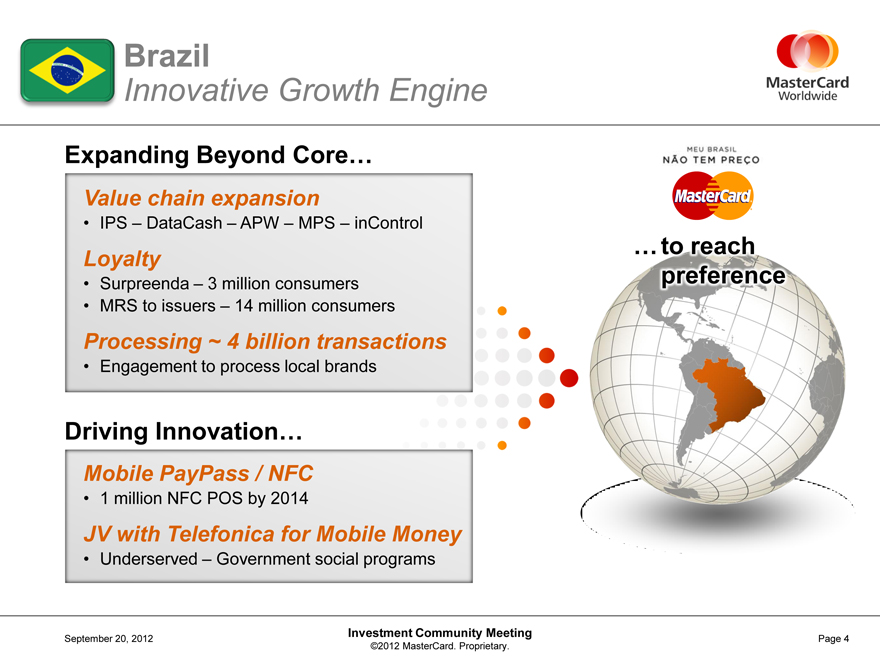

Brazil

Innovative Growth Engine

… to reach preference

Expanding Beyond Core…

Value chain expansion

IPS – DataCash – APW – MPS – inControl

Loyalty

Surpreenda – 3 million consumers

MRS to issuers – 14 million consumers

Processing ~ 4 billion transactions

Engagement to process local brands

Driving Innovation…

Mobile PayPass / NFC

| 1 |

|

million NFC POS by 2014 |

JV with Telefonica for Mobile Money

Underserved – Government social programs

Investment Community Meeting

©2012 MasterCard. Proprietary.

September 20, 2012

Page 4

|

|

Martina Hund-Mejean

Chief Financial Officer

September 20, 2012

Financial Perspective

2012 Investment Community Meeting

©2012 MasterCard. Proprietary.

|

|

Topics for Today

2012 Outlook

Approach to FX Hedging

Capital Structure Considerations

Long-Term Growth Opportunity

Long-Term Performance Targets

Investment Community Meeting

©2012 MasterCard. Proprietary.

September 20, 2012

Page 2

|

|

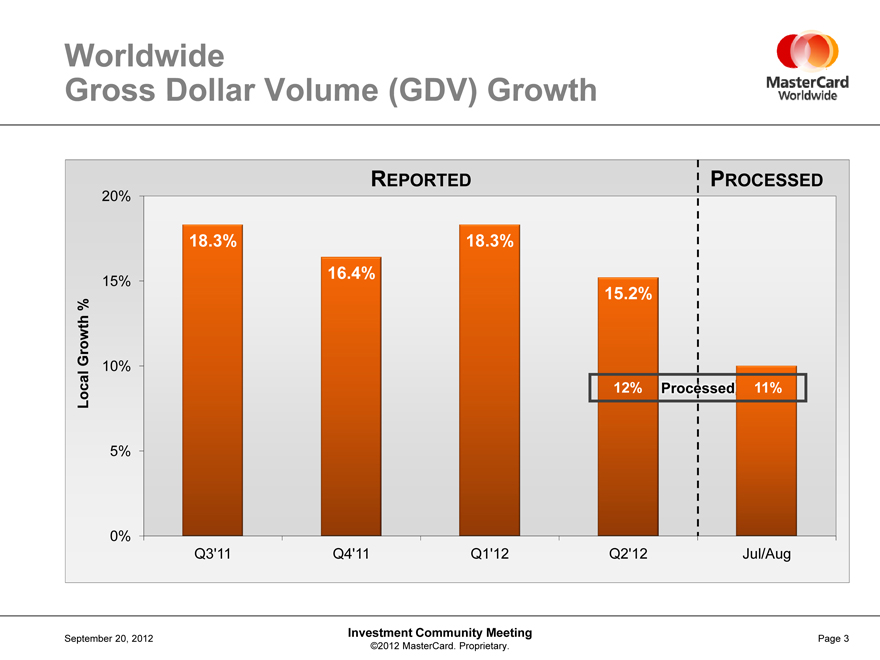

Worldwide

Gross Dollar Volume (GDV) Growth

REPORTED PROCESSED

18.3% 18.3%

16.4% 15.2%

Local Growth %

12% Processed 11%

0% 5% 10% 15% 20%

Q3’11 Q4’11 Q1’12 Q2’12 Jul/Aug

September 20, 2012

Investment Community Meeting

©2012 MasterCard. Proprietary.

Page 3

|

|

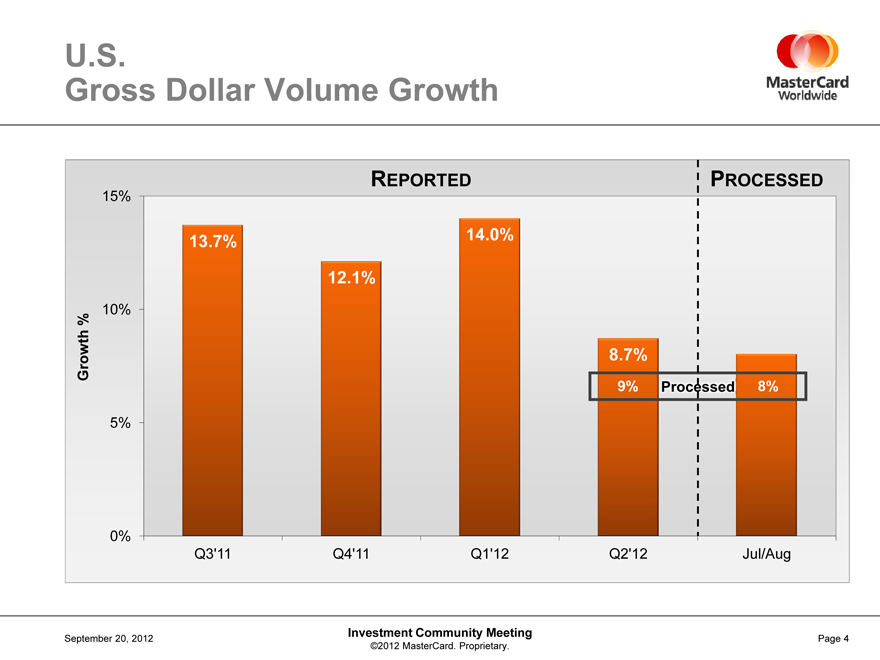

U.S.

Gross Dollar Volume Growth

REPORTED PROCESSED

13.7% 14.0%

12.1%

0% 5% 10% 15%

Growth % 8.7%

9% Processed 8%

Q3’11 Q4’11 Q1’12 Q2’12 Jul/Aug

September 20, 2012

Investment Community Meeting

©2012 MasterCard. Proprietary.

Page 4

|

|

Rest of World

Gross Dollar Volume Growth

REPORTED PROCESSED

25% 20% 15% 10% 5% 0%

20.6% 20.6%

18.6% 18.6%

Local Growth % 15% Processed 14%

Q3’11 Q4’11 Q1’12 Q2’12 Jul/Aug

September 20, 2012

Investment Community Meeting

©2012 MasterCard. Proprietary.

Page 5

|

|

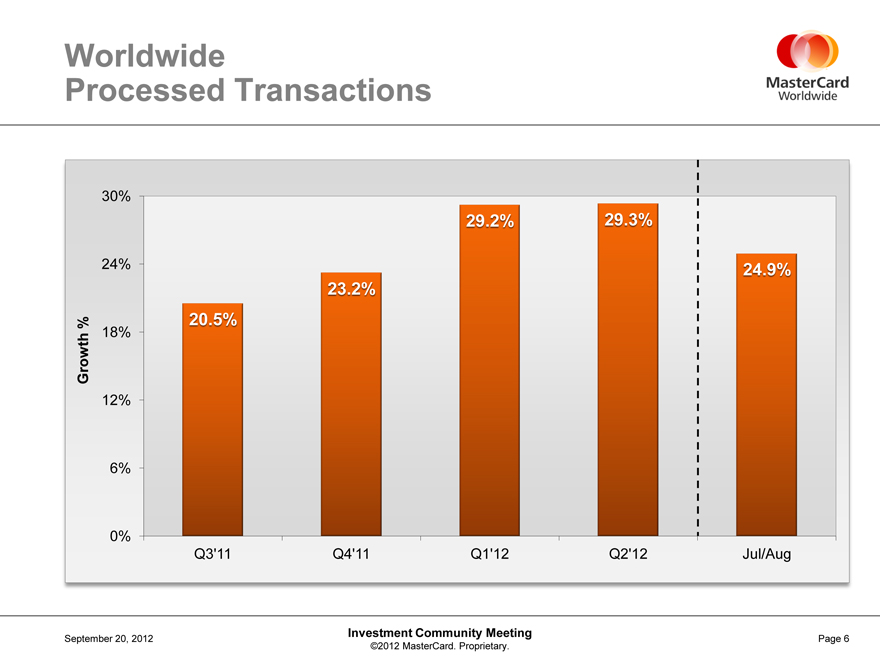

Worldwide

Processed Transactions

30%

24%

18%

12%

6%

0%

20.5%

23.2%

29.2%

29.3%

24.9%

Q3’11 Q4’11 Q1’12 Q2’12 Jul/Aug

Growth %

Investment Community Meeting

©2012 MasterCard. Proprietary.

September 20, 2012

Page 6

|

|

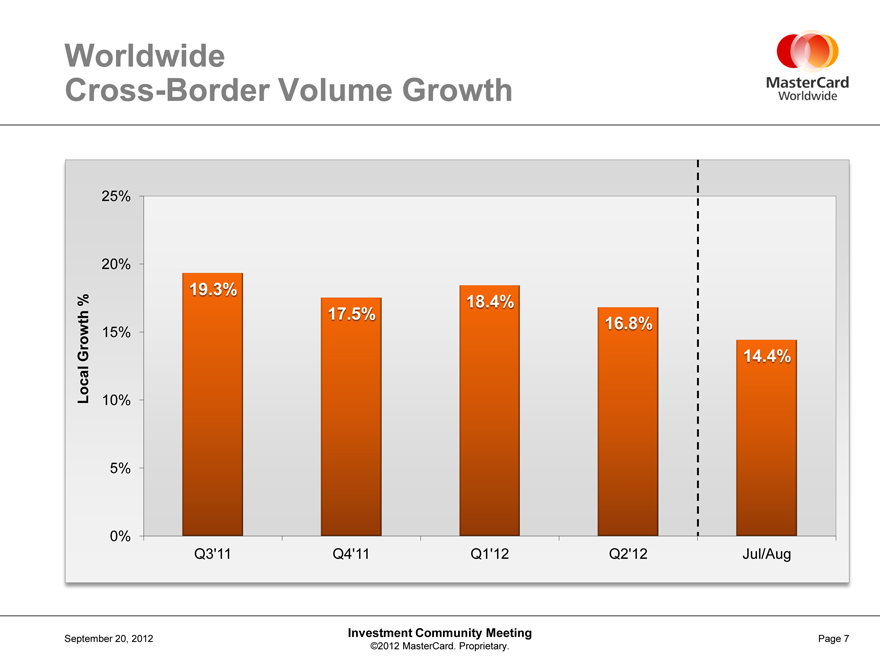

Worldwide

Cross-Border Volume Growth

Local Growth %

25%

20%

15%

10%

5%

0%

19.3%

17.5%

18.4%

16.8%

14.4%

Q3’11 Q4’11 Q1’12 Q2’12 Jul/Aug

Investment Community Meeting

©2012 MasterCard. Proprietary.

September 20, 2012

Page 7

|

|

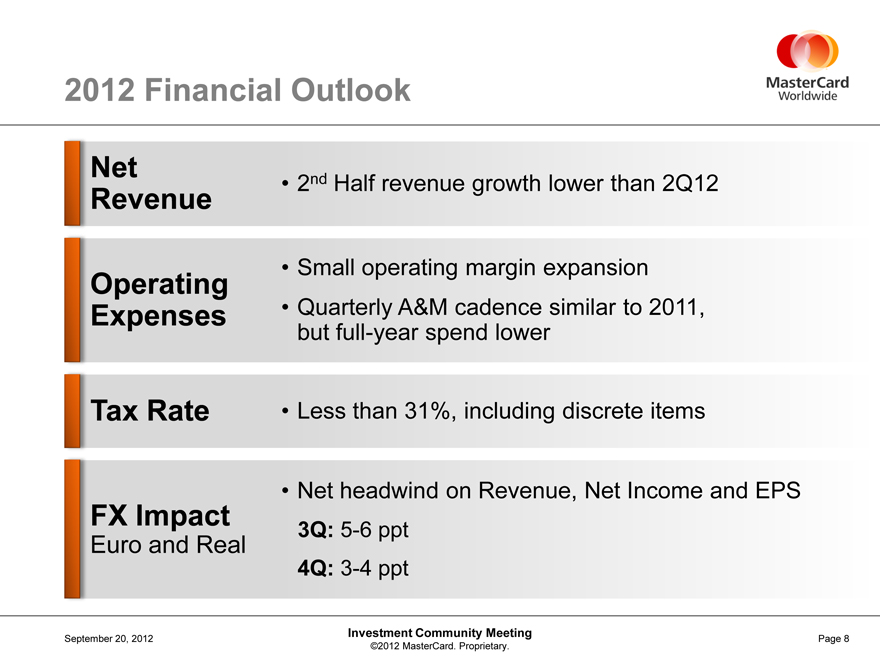

2012 Financial Outlook

Net Revenue

Operating Expenses

Tax Rate

FX Impact

Euro and Real

2nd Half revenue growth lower than 2Q12

Small operating margin expansion

Quarterly A&M cadence similar to 2011, but full-year spend lower

Less than 31%, including discrete items

Net headwind on Revenue, Net Income and EPS

3Q: 5-6 ppt

4Q: 3-4 ppt

Investment Community Meeting

©2012 MasterCard. Proprietary.

September 20, 2012

Page 8

|

|

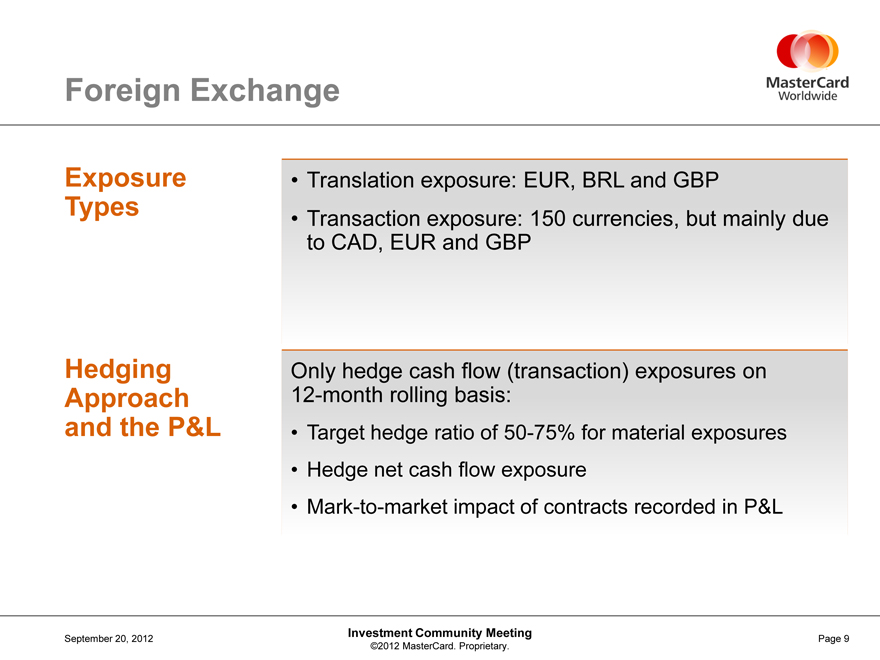

Foreign Exchange

Exposure Types

Translation exposure: EUR, BRL and GBP

Transaction exposure: 150 currencies, but mainly due to CAD, EUR and GBP

Hedging Approach and the P&L

Only hedge cash flow (transaction) exposures on 12-month rolling basis:

Target hedge ratio of 50-75% for material exposures

Hedge net cash flow exposure

Mark-to-market impact of contracts recorded in P&L

Investment Community Meeting

©2012 MasterCard. Proprietary.

September 20, 2012

Page 9

|

|

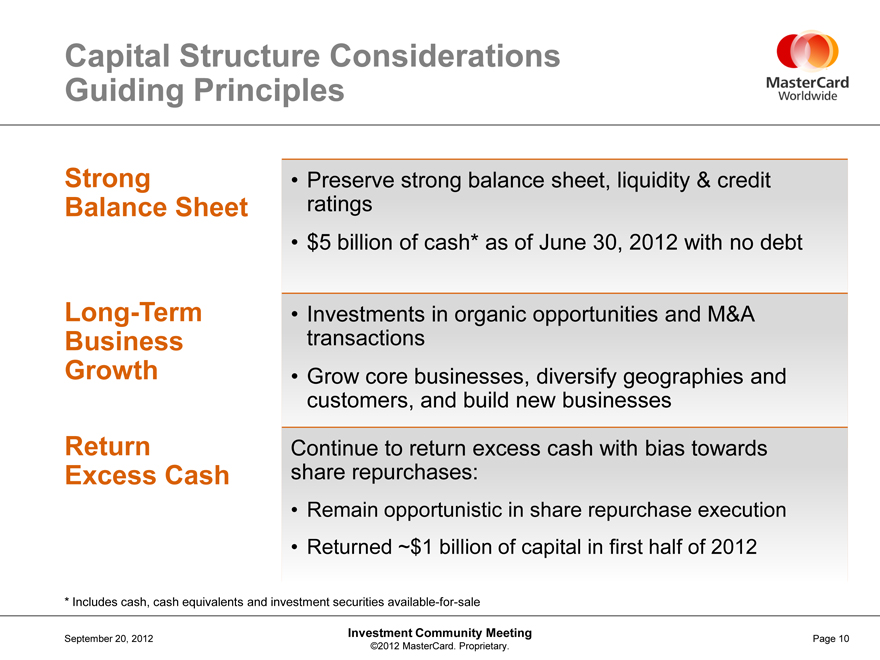

Capital Structure Considerations

Guiding Principles

Strong Balance Sheet

Preserve strong balance sheet, liquidity & credit ratings

$5 billion of cash* as of June 30, 2012 with no debt

Long-Term Business Growth

Investments in organic opportunities and M&A transactions

Grow core businesses, diversify geographies and customers, and build new businesses

Return Excess Cash

Continue to return excess cash with bias towards share repurchases:

Remain opportunistic in share repurchase execution

Returned ~$1 billion of capital in first half of 2012

* Includes cash, cash equivalents and investment securities available-for-sale

Investment Community Meeting

©2012 MasterCard. Proprietary.

September 20, 2012

Page 10

|

|

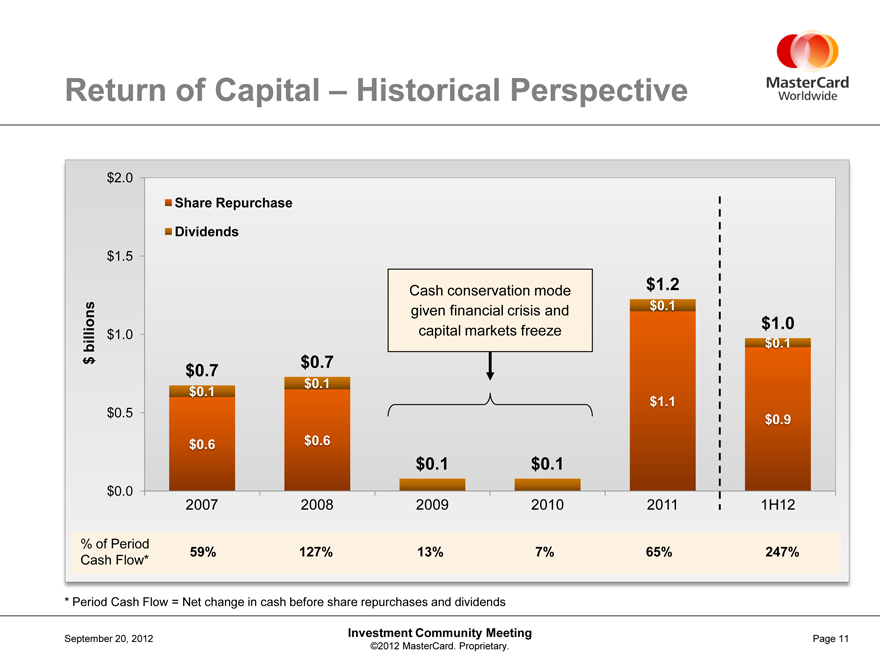

Return of Capital – Historical Perspective

Share Repurchase

Dividends

Cash conservation mode given financial crisis and capital markets freeze

$ billions

$2.0

$1.5

$1.2

$0.1

$1.0

$1.0

$0.1

$0.7

$0.7

$0.1

$0.1

$0.5

$1.1

$0.9

$0.6

$0.6

$0.1

$0.1

$0.0

2007 2008 2009 2010 2011 1H12

% of Period

Cash Flow*

59%

127%

13%

7%

65%

247%

* Period Cash Flow = Net change in cash before share repurchases and dividends

Investment Community Meeting

©2012 MasterCard. Proprietary.

September 20, 2012

Page 11

|

|

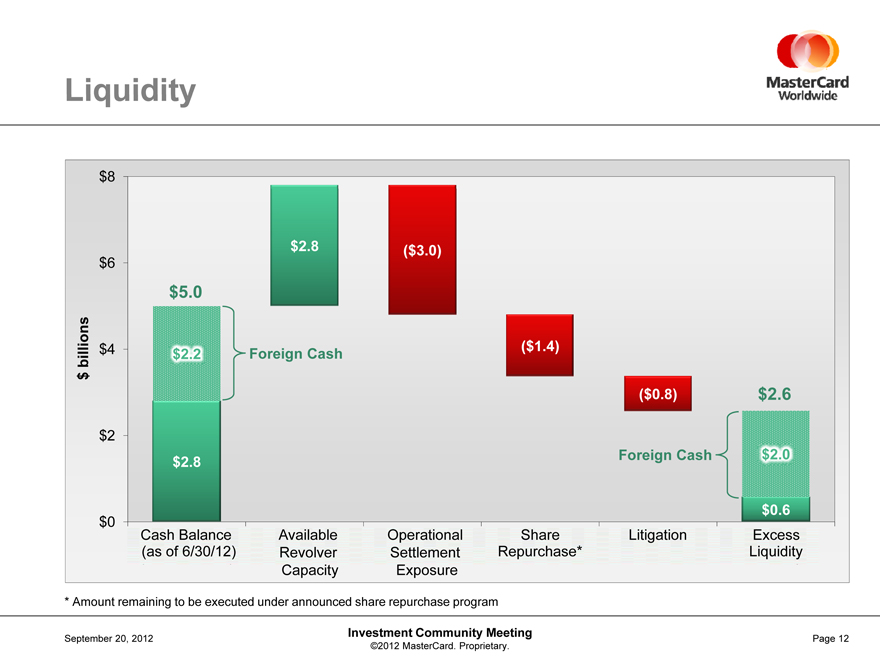

Liquidity

$8

$2.8

($3.0)

$6

$5.0

$4 ($1.4)

$ billions

$2.2

Foreign Cash

($0.8) $2.6

$2

Foreign Cash

$2.0

$2.8

$0.6

$0

Cash Balance

(as of 6/30/12)

Available Revolver…

Operational Settlement…

Share Repurchase*

Litigation

Excess Liquidity

* Amount remaining to be executed under announced share repurchase program

Investment Community Meeting

©2012 MasterCard. Proprietary.

September 20, 2012

Page 12

|

|

Execution against Business and Financial Objectives

$6,714

$5,538

$4,992

$5,099

$4,068

$3,326

Net Revenue

($ millions)

13%

19%

20%

4%

10%

19%

Constant Currency Growth

2006 2007 2008 2009 2010 2011

$18.70

$14.05

$9.45

$11.19

$7.58

$3.37

$ Earnings Per Share*

Constant Currency Growth

43% 121% 23% 21% 26% 31%

2006 2007 2008 2009 2010 2011

* Excluding special items

Investment Community Meeting

©2012 MasterCard. Proprietary.

September 20, 2012

Page 13

|

|

Three Drivers of Growth

Personal Consumption Expenditure

Cash & Check vs. Electronic Payments

MasterCard Share of Electronic Payments

Investment Community Meeting

©2012 MasterCard. Proprietary.

September 20, 2012

Page 14

|

|

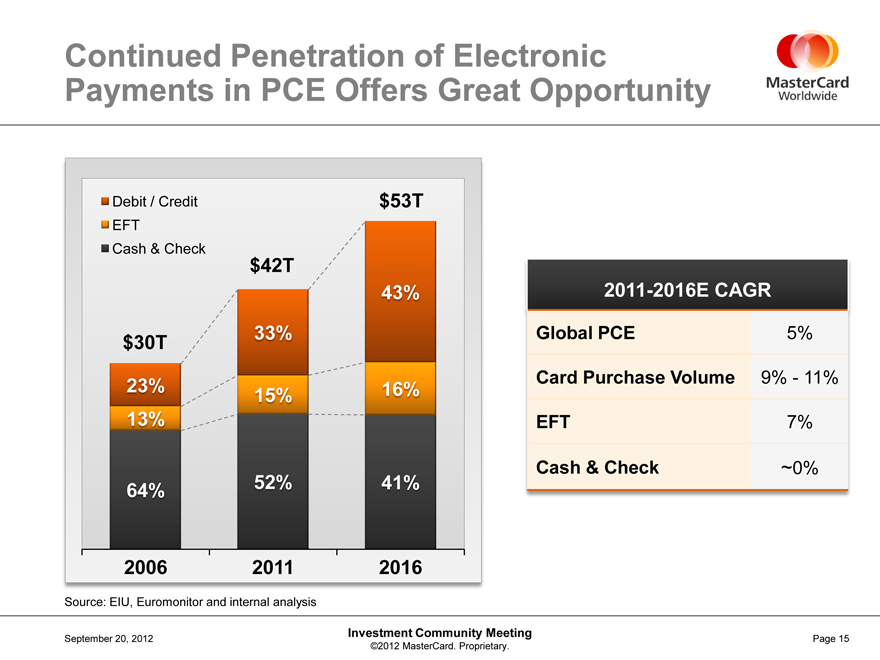

Continued Penetration of Electronic Payments in PCE Offers Great Opportunity

Debit / Credit

EFT

Cash & Check

$53T

$42T

43%

33%

$30T

2011-2016E CAGR

Global PCE 5%

Card Purchase Volume 9%—11%

Cash & Check ~0%

23%

15%

16%

13%

EFT

7%

64% 52% 41%

2006 2011 2016

Source: EIU, Euromonitor and internal analysis

Investment Community Meeting

©2012 MasterCard. Proprietary.

September 20, 2012

Page 15

|

|

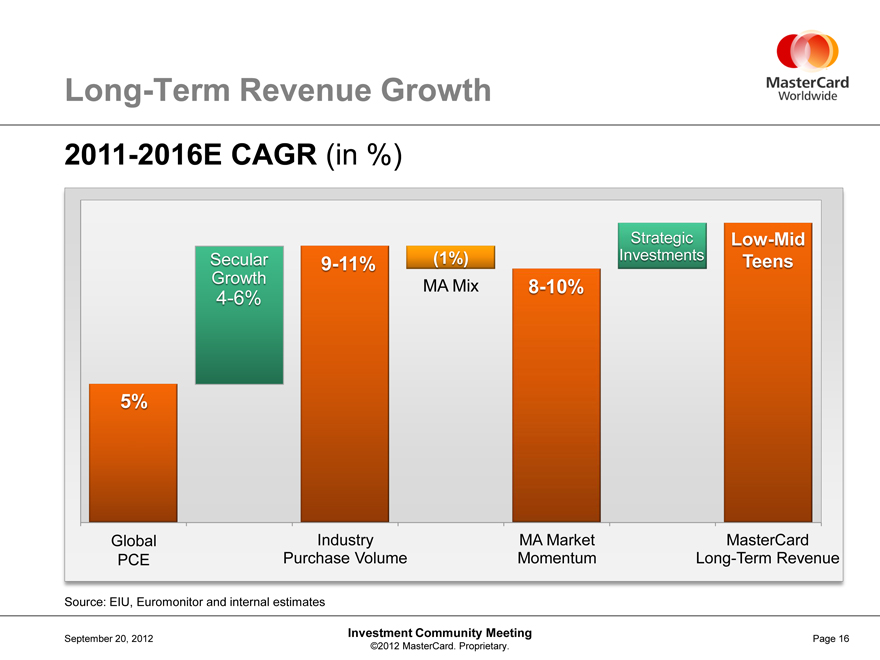

Long-Term Revenue Growth

2011-2016E CAGR (in %)

Strategic Growth 4-6%

Low-Mid Teens

Secular Investments

9-11%

(1%)

MA Mix

8-10%

5%

Global PCE

Industry Purchase Volume

MA Market Momentum

MasterCard Long-Term Revenue

Source: EIU, Euromonitor and internal estimates

Investment Community Meeting

©2012 MasterCard. Proprietary.

September 20, 2012

Page 16

|

|

Longer-Term

2013 – 2015 Performance Objectives*

Net Revenue Growth

11-14% CAGR

Operating Margin

Minimum 50% annually

Earnings Per Share Growth Rate

At least 20% CAGR

* On a constant currency basis and excluding future acquisitions

Investment Community Meeting

©2012 MasterCard. Proprietary.

September 20, 2012

Page 17

|

|

Investing in Our Strategy

GROW

Core Business

DIVERSIFY

Geographies & Customers

BUILD

New Businesses

Credit

Government sector

e-Commerce

Debit

Non-traditional customers

Mobile

Commercial

Information services

Emerging markets

Prepaid

Acquisitions and partnerships

Wide variety of investment opportunities to gain share and grow the pie

Investment Community Meeting

©2012 MasterCard. Proprietary.

September 20, 2012

Page 18

|

|

September 20, 2012

Question & Answer Session

2012 Investment Community Meeting

©2012 MasterCard. Proprietary.

Ed McLaughlin

Ed McLaughlin

Chief Emerging Payments Officer

September 20, 2012

Product Demo Overview

2012 Investment Community Meeting

©2012 MasterCard. Proprietary.

|

|

Ajay Banga

President and Chief Executive Officer

September 20, 2012

Closing Comments

2012 Investment Community Meeting

©2012 MasterCard. Proprietary.

|

|

Final Thoughts

Execute through the Grow, Diversify, Build roadmap

Capitalize on opportunities and address challenges

Invest to drive growth through innovation

Deliver on our commitments

Investment Community Meeting

©2012 MasterCard. Proprietary.

September 20, 2012

Page 2

|

|

MasterCard

Worldwide

The Heart of Commerce™