Use these links to rapidly review the document

TABLE OF CONTENTS

TABLE OF CONTENTS

Filed Pursuant to Rule 424(b)(3)

Registration No. 333-205004

Dear Crestwood Midstream Partners LP Unitholders:

On May 5, 2015, Crestwood Equity Partners LP ("CEQP"), Crestwood Equity GP LLC ("Equity GP"), which is the general partner of CEQP, CEQP ST SUB LLC, which is a wholly-owned subsidiary of CEQP ("MergerCo"), MGP GP, LLC ("MGP GP"), which is a wholly-owned subsidiary of CEQP, Crestwood Midstream Holdings LP ("Midstream Holdings"), Crestwood Midstream Partners LP ("Midstream"), Crestwood Midstream GP LLC ("Midstream GP"), which is the general partner of Midstream, and Crestwood Gas Services GP LLC ("CGS"), which is a wholly-owned subsidiary of Midstream GP, entered into an Agreement and Plan of Merger (the "merger agreement"). Pursuant to the merger agreement, MergerCo, Midstream Holdings and MGP GP will merge with and into Midstream (the "merger"), with Midstream surviving the merger as an indirect wholly-owned subsidiary of CEQP. Immediately following the effective time of the merger (the "effective time"), each issued and outstanding common unit representing a common limited partner interest of Midstream (collectively, the "Midstream common units"), except for any Midstream common units owned by CEQP, CGS or their respective subsidiaries, will be converted into the right to receive 2.75 common units representing limited partner interests in CEQP (the "CEQP common units") and each issued and outstanding unit representing preferred limited partner interests in Midstream (the "Midstream preferred units", and together with the Midstream common units, the "Midstream units"), except for any Midstream preferred units owned by CEQP or its subsidiaries, will be converted into the right to receive 2.75 preferred units representing limited partner interests in CEQP (the "CEQP preferred units"). No fractional CEQP common units or fractional CEQP preferred units will be issued in the merger, and holders of Midstream common units and Midstream preferred units will, instead, receive cash in lieu of fractional units, if any.

Pursuant to the merger agreement and Midstream's partnership agreement, a majority of the outstanding Midstream common units and Midstream preferred units (voting on an "as if converted" basis) voting together as a single class must vote in favor of the proposal in order for it to be approved. In connection with the merger agreement, CEQP entered into (i) a support agreement by and among CEQP, Midstream and CGS, pursuant to which, CEQP, which directly owns 7,137,841 Midstream common units, and CGS, which directly owns 21,597 Midstream common units, agreed to vote their respective Midstream common units in favor of the adoption of the merger agreement at any meeting of Midstream unitholders and (ii) a support agreement by and among CEQP, Midstream, Crestwood Holdings LLC, a Delaware limited liability company ("Holdings") and Crestwood Gas Services Holdings LLC, a Delaware limited liability company and wholly-owned subsidiary of Holdings ("CGS LLC,") pursuant to which, Holdings, which directly owns 2,497,071 Midstream common units, and CGS LLC, which directly owns 18,339,314 Midstream common units, agreed to vote their respective Midstream common units in favor of the adoption of the merger agreement at any meeting of Midstream unitholders. Pursuant to (i) a letter agreement regarding change of control election by and among CEQP, Midstream, CGS and GE Structured Finance, Inc. ("GE"), (ii) a letter agreement regarding change of control election by and among CEQP, Midstream, CGS and GSO COF II Holdings Partners LP ("GSO") and (iii) a letter agreement regarding change of control election by and among CEQP, Midstream, CGS, Magnetar Financial LLC ("Magnetar") and the preferred holders named therein (the "Magnetar preferred holders," and collectively with GE and GSO, the "preferred holders"), subject to the terms and conditions set forth in such letter agreements, each preferred holder expressed an intention to support the merger and agreed to elect to have all of the Midstream preferred units held of record by such preferred holder exchanged for CEQP preferred units upon the consummation of the merger in accordance with the terms of the merger agreement. Midstream has scheduled a special meeting of its unitholders to vote on the merger agreement and the merger on September 30, 2015 at 10:00 a.m., local time, at 700 Louisiana Street, Suite 2550, Houston, Texas 77002. Regardless of the number of units you own or whether you plan to attend the meeting, it is important that your units be represented and voted at the meeting. Voting instructions are set forth inside this proxy statement/prospectus.

The Conflicts Committee ("Midstream Conflicts Committee") of the Board of Directors of Midstream GP (the "Midstream Board") has determined unanimously that the merger agreement and the transactions contemplated thereby are advisable, fair and reasonable to and in the best interests of Midstream and the Midstream unaffiliated unitholders, and it approved the merger agreement, the execution, delivery and performance by Midstream of the merger agreement and the transactions contemplated thereby, which constituted "Special Approval" under Midstream's partnership agreement. The

Midstream Conflicts Committee also recommended that the Midstream Board approve the merger agreement, the execution, delivery and performance by Midstream of the merger agreement and the transactions contemplated thereby. The Midstream Board has determined unanimously that the merger agreement and the transactions contemplated thereby are fair and reasonable to and in the best interests of Midstream and the holders of Midstream units, approved the merger agreement, the execution, delivery and performance by Midstream of the merger agreement and the transactions contemplated thereby, directed that the merger agreement be submitted to the Midstream unitholders for approval at a special meeting of such unitholders for the purpose of approving the merger agreement and the merger and recommended that the holders of Midstream units approve the merger agreement and the merger and approve the proposal to adjourn the special meeting, if necessary, to solicit additional proxies if there are not sufficient votes to approve the merger agreement at the time of the special meeting.

This proxy statement/prospectus provides you with detailed information about the proposed merger and related matters. Midstream encourages you to read the entire document carefully. In particular, please read "Risk Factors" beginning on page 30 of this proxy statement/prospectus for a discussion of risks relevant to the merger and CEQP's business following the merger.

CEQP's common units are listed on the New York Stock Exchange ("NYSE") under the symbol "CEQP," and Midstream's common units are listed on the NYSE under the symbol "CMLP." The last reported sale price of CEQP's common units on the NYSE on August 26, 2015 was $2.67. The last reported sale price of Midstream common units on the NYSE on August 26, 2015 was $7.13.

![]()

Robert G. Phillips

President and Chief Executive Officer

Crestwood Midstream GP, LLC

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of the securities to be issued under this proxy statement/prospectus or has determined if this document is truthful or complete. Any representation to the contrary is a criminal offense.

All information in this document concerning CEQP has been furnished by CEQP. All information in this document concerning Midstream has been furnished by Midstream. CEQP has represented to Midstream, and Midstream has represented to CEQP, that the information furnished by and concerning it is true and correct in all material respects.

This proxy statement/prospectus is dated August 28, 2015 and is being first mailed to Midstream unitholders on or about September 1, 2015.

Houston, Texas

August 28, 2015

Notice of Special Meeting of Unitholders

To the Unitholders of Crestwood Midstream Partners LP:

A special meeting of unitholders of Crestwood Midstream Partners LP ("Midstream") will be held on September 30, 2015, at 10:00 a.m., local time, at 700 Louisiana Street, Suite 2550, Houston, Texas 77002, for the following purposes:

- •

- To consider and vote upon the approval of the Agreement and Plan of Merger dated as of May 5, 2015, by and among Crestwood

Equity Partners LP ("CEQP"), Crestwood Equity GP LLC ("Equity GP"), CEQP ST SUB LLC ("MergerCo"), MGP GP, LLC ("MGP GP"), Crestwood Midstream Holdings LP ("Midstream

Holdings"), Midstream, Crestwood Midstream GP LLC ("Midstream GP"), and Crestwood Gas Services GP LLC ("CGS"), as it may be amended from time to time (the "merger agreement"), and the merger

contemplated by the merger agreement (the "merger"); and

- •

- To consider and vote upon the proposal to adjourn the special meeting, if necessary, to solicit additional proxies if there are not

sufficient votes to approve the merger agreement at the time of the special meeting.

- •

- To transact such other business as may properly be presented at the meeting or any adjournments or postponements of the meeting.

Pursuant to the merger agreement and Midstream's partnership agreement, a majority of the outstanding common units representing limited partner interests in Midstream (the "Midstream common units") and the outstanding preferred units representing preferred limited partner interests in Midstream (the "Midstream preferred units," and together with the Midstream common units, the "Midstream units") (voting on an "as if converted" basis"), voting together as a single class, must vote in favor of the proposal in order for it to be approved. Failures to vote, abstentions and broker non-votes will have the same effect as a vote against the proposal for purposes of the vote by the Midstream unitholders required under the merger agreement and Midstream's partnership agreement.

In connection with the merger agreement, CEQP entered into (i) a support agreement by and among CEQP, Midstream and CGS, pursuant to which, CEQP, which directly owns 7,137,841 Midstream common units, and CGS, which directly owns 21,597 Midstream common units, agreed to vote their respective Midstream common units in favor of the adoption of the merger agreement at any meeting of Midstream unitholders and (ii) a support agreement by and among CEQP, Midstream, Crestwood Holdings LLC, a Delaware limited liability company ("Holdings") and Crestwood Gas Services Holdings LLC, a Delaware limited liability company and wholly-owned subsidiary of Holdings ("CGS LLC,") pursuant to which, Holdings, which directly owns 2,497,071 Midstream common units, and CGS LLC, which directly owns 18,339,314 Midstream common units, agreed to vote their respective Midstream common units in favor of the adoption of the merger agreement at any meeting of Midstream unitholders. Pursuant to (i) a letter agreement regarding change of control election by and among CEQP, Midstream, CGS and GE Structured Finance, Inc. ("GE"), (ii) a letter agreement regarding change of control election by and among CEQP, Midstream, CGS and GSO COF II Holdings Partners LP ("GSO") and (iii) a letter agreement regarding change of control election by and among CEQP, Midstream, CGS, Magnetar Financial LLC ("Magnetar") and the preferred holders named therein (the "Magnetar preferred holders," and collectively with GE and GSO, the "preferred holders"), subject to the terms and conditions set forth in such letter agreements, each preferred holder expressed an intention to support the merger and agreed to elect to have all of the Midstream

preferred units held of record by such preferred holder exchanged for CEQP preferred units upon the consummation of the merger in accordance with the terms of the merger agreement.

The Conflicts Committee ("Midstream Conflicts Committee") of the Board of Directors of Midstream GP (the "Midstream Board") has determined unanimously that the merger agreement and the transactions contemplated thereby are advisable, fair and reasonable to and in the best interests of Midstream and the Midstream unaffiliated unitholders, and it approved the merger agreement, the execution, delivery and performance by Midstream of the merger agreement and the transactions contemplated thereby, which constituted "Special Approval" under Midstream's partnership agreement. The Midstream Conflicts Committee also recommended that the Midstream Board approve the merger agreement, the execution, delivery and performance by Midstream of the merger agreement and the transactions contemplated thereby. The Midstream Board has determined unanimously that the merger agreement and the transactions contemplated thereby are fair and reasonable to and in the best interests of Midstream and the holders of Midstream units, approved the merger agreement, the execution, delivery and performance by Midstream of the merger agreement and the transactions contemplated thereby, directed that the merger agreement be submitted to the Midstream unitholders for approval at a meeting of such unitholders for the purpose of approving the merger agreement and the merger and recommended that the holders of Midstream units approve the merger agreement and the merger and approve the proposal to adjourn the special meeting, if necessary, to solicit additional proxies if there are not sufficient votes to approve the merger agreement at the time of the special meeting.

Only unitholders of record at the close of business on August 24, 2015 are entitled to notice of and to vote at the meeting and any adjournments or postponements of the meeting. A list of unitholders entitled to vote at the meeting will be available for inspection at Midstream's offices in Houston, Texas for any purpose relevant to the meeting during normal business hours for a period of 10 days before the meeting and at the meeting.

YOUR VOTE IS IMPORTANT. WHETHER OR NOT YOU EXPECT TO ATTEND THE MEETING, PLEASE VOTE OR SUBMIT YOUR PROXY IN ONE OF THE FOLLOWING WAYS. If you hold your units in the name of a bank, broker or other nominee, you should follow the instructions provided by your bank, broker or nominee when voting your Midstream common units. If you hold your units in your own name, you may vote by:

- •

- using the toll-free telephone number shown on the proxy card;

- •

- using the Internet website shown on the proxy card; or

- •

- marking, signing, dating and promptly returning the enclosed proxy card in the postage-paid envelope. It requires no postage if mailed in the United States.

By order of the Board of Directors of Crestwood Midstream GP, LLC, as the general partner of Crestwood Midstream Partners LP.

![]()

Robert G. Phillips

President and Chief Executive Officer

Crestwood Midstream GP, LLC

IMPORTANT NOTE ABOUT THIS PROXY STATEMENT/PROSPECTUS

This proxy statement/prospectus, which forms part of a registration statement on Form S-4 filed with the Securities and Exchange Commission, which is referred to as the "SEC" or the "Commission," constitutes a proxy statement of Midstream under Section 14(a) of the Securities Exchange Act of 1934, as amended, which is referred to as the "Exchange Act," with respect to the solicitation of proxies for the special meeting of Midstream unitholders to, among other things, approve the merger agreement and the merger. This proxy statement/prospectus is also a prospectus of CEQP under Section 5 of the Securities Act of 1933, as amended, which is referred to as the "Securities Act," for CEQP units that will be issued to Midstream unitholders in the merger pursuant to the merger agreement.

As permitted under the rules of the SEC, this proxy statement/prospectus incorporates by reference important business and financial information about CEQP and Midstream from other documents filed with the SEC that are not included in or delivered with this proxy statement/prospectus. Please read "Where You Can Find More Information" beginning on page 148. You can obtain any of the documents incorporated by reference into this document from the SEC's website at http://www.sec.gov. This information is also available to you without charge upon your request in writing or by telephone from CEQP or Midstream, as the case may be, at the following addresses and telephone numbers:

| Crestwood Equity Partners LP 700 Louisiana Street, Suite 2550 Attention: Investor Relations Houston, Texas 77002 Telephone: (713) 380-3081 |

Crestwood Midstream Partners LP 700 Louisiana Street, Suite 2550 Attention: Investor Relations Houston, Texas 77002 Telephone: (713) 380-3081 |

Please note that copies of the documents provided to you will not include exhibits, unless the exhibits are specifically incorporated by reference into the documents or this proxy statement/prospectus.

You may obtain certain of these documents at CEQP's website, www.crestwoodlp.com, by selecting "Investors," and then selecting "Crestwood Equity Partners LP" and then selecting "SEC Filings," and at CMLP's website, www.crestwoodlp.com, by selecting "Investor Relations," and then selecting "Crestwood Midstream Partners LP" and then selecting "SEC Filings." Information contained on Midstream's and CEQP's websites is expressly not incorporated by reference into this proxy statement/prospectus.

In order to receive timely delivery of requested documents in advance of the Midstream special meeting of unitholders, your request should be received no later than September 22, 2015. If you request any documents, CEQP or Midstream will mail them to you by first class mail, or another equally prompt means, within one business day after receipt of your request.

CEQP and Midstream have not authorized anyone to give any information or make any representation about the merger, CEQP or Midstream that is different from, or in addition to, that contained in this proxy statement/prospectus or in any of the materials that have been incorporated by reference into this proxy statement/prospectus. Therefore, if anyone distributes this type of information, you should not rely on it. If you are in a jurisdiction where offers to exchange or sell, or solicitations of offers to exchange or purchase, the securities offered by this proxy statement/prospectus or the solicitation of proxies is unlawful, or you are a person to whom it is unlawful to direct these types of activities, then the offer presented in this proxy statement/prospectus does not extend to you. The information contained in this proxy statement/prospectus speaks only as of the date of this proxy statement/prospectus, or in the case of information in a document incorporated by reference, as of the date of such document, unless the information specifically indicates that another date applies. All information in this document concerning CEQP has been furnished by CEQP. All information in this document concerning Midstream has been furnished by Midstream. CEQP has represented to Midstream, and Midstream has represented to CEQP, that the information furnished by and concerning it is true and correct in all material respects.

i

ii

The following terms have the meanings set forth below for purposes of this proxy statement/prospectus, unless the context otherwise indicates:

- •

- "CEQP" means Crestwood Equity Partners LP, a Delaware limited partnership.

- •

- "CEQP Class A Unit" means units representing limited partner interests in CEQP having the rights and obligations specified with

respect to Class A Units in the CEQP Partnership Agreement

- •

- "CEQP common units" means common units representing limited partner interests in CEQP having the rights and obligations specified with

respect to Common Units in CEQP's partnership agreement.

- •

- "CEQP Conflicts Committee" means the Conflicts Committee of the Equity GP Board.

- •

- "CEQP LTIP" means the Crestwood Equity Partners LP Long Term Incentive Plan (formerly the Inergy Long Term Incentive Plan) as

Amended and Restated effective February 11, 2010.

- •

- "CEQP Partnership Agreement Amendment" means the First Amendment to Fifth Amended and Restated Agreement of Limited Partnership of

CEQP in the form attached to the merger agreement as Annex A, as adopted by the Equity GP Board pursuant to the terms of the merger agreement.

- •

- "CEQP Phantom Units" means CEQP Phantom Units as defined in and awarded under Section 5 of the CEQP LTIP.

- •

- "CEQP preferred units" means preferred units representing limited partner interests in CEQP having the rights and obligations

specified with respect to Preferred Units in CEQP's partnership agreement, including any amendments thereto.

- •

- "CGS" means Crestwood Gas Services GP LLC, a Delaware limited liability company and wholly-owned subsidiary of

Midstream GP.

- •

- "CGS LLC" means Crestwood Gas Services Holdings LLC, a Delaware limited liability company and wholly-owned subsidiary of

Holdings.

- •

- "Common Merger Consideration" means the right of Midstream common unitholders, other than CEQP, CGS or their respective subsidiaries,

to exchange each Midstream common unit held by such unitholder into the right to receive 2.75 CEQP common units

- •

- "Crestwood Operations" means Crestwood Operations LLC, a Delaware limited liability company.

- •

- "Equity GP" means Crestwood Equity GP LLC, a Delaware limited liability company and the general partner of CEQP.

- •

- "Equity GP Board" means the board of directors of Equity GP.

- •

- "Holdings" means Crestwood Holdings LLC, a Delaware limited liability company.

- •

- "MergerCo" means CEQP ST SUB LLC, which is a wholly-owned subsidiary of CEQP.

- •

- "MGP GP" means MGP GP, LLC, a Delaware limited liability company and wholly-owned subsidiary of CEQP.

- •

- "Midstream" means Crestwood Midstream Partners LP, a Delaware limited partnership.

- •

- "Midstream Board" means the board of directors of Midstream GP.

1

- •

- "Midstream common units" means common units representing limited partner interests in Midstream having the rights and obligations

specified with respect to Common Units in Midstream's partnership agreement.

- •

- "Midstream Compensation Committee" means the Compensation Committee of the Midstream Board, consisting of David Wood and Warren

Gfeller.

- •

- "Midstream Conflicts Committee" means the Conflicts Committee of the Midstream Board.

- •

- "Midstream GP" means Crestwood Midstream GP LLC, a Delaware limited liability company and the general partner of Midstream.

- •

- "Midstream Holdings" means Crestwood Midstream Holdings LP.

- •

- "Midstream LTIP" means the Crestwood Midstream Partners LP Long Term Incentive Plan (formerly the Inergy Midstream, L.P.

Long Term Incentive Plan), effective December 21, 2011.

- •

- "Midstream phantom unit" means Midstream Phantom Units as defined in and awarded under Section 5 of the Midstream LTIP.

- •

- "Midstream preferred units" means units representing preferred limited partner interests in Midstream having the rights and

obligations specified with respect to Class A Preferred Units in Midstream's partnership agreement.

- •

- "Midstream Restricted Common Unit" means a Restricted Common Unit as defined in, and awarded under Section 6.1 of the Midstream

LTIP.

- •

- "Midstream unaffiliated unitholders" means the holders of Midstream common units and Midstream preferred units other than

(i) CEQP and affiliates of CEQP and (ii) the officers and directors of Midstream GP that are also officers or directors of Equity GP or affiliates of such officers and

directors.

- •

- "Midstream units" means Midstream common units and the Midstream preferred units.

- •

- "Preferred Merger Consideration" means the right of Midstream preferred unitholders, other than CEQP or its subsidiaries, to exchange

each Midstream preferred unit held by such unitholder into the right to receive 2.75 CEQP preferred units.

- •

- "Special Approval" under Midstream's partnership agreement means the approval of a majority of the members of the Midstream Conflicts Committee.

2

QUESTIONS AND ANSWERS ABOUT THE MERGER AND THE SPECIAL MEETING

Important Information and Risks. The following are brief answers to some questions that you may have regarding the proposed merger and the proposal being considered at the special meeting of Midstream unitholders. You should read and consider carefully the remainder of this proxy statement/prospectus, including the Risk Factors beginning on page 30 and the attached Annexes, because the information in this section does not provide all of the information that might be important to you. Additional important information and descriptions of risk factors are also contained in the documents incorporated by reference in this proxy statement/prospectus. Please read "Where You Can Find More Information" beginning on page 148.

- Q:

- Why am I receiving these materials?

- A:

- CEQP

and Midstream have agreed to combine by merging MergerCo, MGP GP and Midstream Holdings, with and into Midstream, with Midstream surviving the

merger. The merger cannot be completed without the approval of the holders of Midstream common units and Midstream preferred units (voting on an "as if converted" basis) voting together as a single

class.

- Q:

- Who is soliciting my proxy?

- A:

- Midstream GP,

on behalf of the Midstream Conflicts Committee and the Midstream Board, is sending you this proxy statement/prospectus in connection

with its solicitation of proxies for use at Midstream's special meeting of unitholders. Certain directors and officers of Midstream GP and certain employees of Crestwood Operations and its

affiliates who provide services to Midstream may also solicit proxies on Midstream's behalf by mail, telephone, fax or other electronic means, or in person.

- Q:

- What is the proposed transaction?

- A:

- CEQP and Midstream have agreed to combine by merging MergerCo, MGP GP and Midstream Holdings with and into Midstream, under the terms of a merger agreement that is described in this proxy statement/prospectus and attached as Annex A to this proxy statement/prospectus. As a result of the merger, each outstanding Midstream common unit, except for any Midstream common units owned by CEQP, CGS or their respective subsidiaries, will be converted into the right to receive 2.75 CEQP common units, and each outstanding Midstream preferred unit, except for any Midstream preferred units owned by CEQP or its subsidiaries, will be converted into the right to receive 2.75 CEQP preferred units.

The merger will become effective on the date and at the time that the certificate of merger is filed with the Secretary of State of the State of Delaware, or a later date and time if set forth in the certificate of merger. Throughout this proxy statement/prospectus, this is referred to as the "effective time" of the merger.

- Q:

- Why are CEQP and Midstream proposing the merger?

- A:

- CEQP and Midstream believe that the merger will benefit both CEQP and Midstream common unitholders by combining the two entities into a single partnership that is better positioned to compete in the marketplace.

Please read "The Merger—Recommendation of the Midstream Board and the Midstream Conflicts Committee's Reasons for the Merger" and "The Merger—CEQP's Reasons for the Merger."

3

- Q:

- What will happen to Midstream as a result of the merger?

- A:

- As

a result of the merger, MergerCo, MGP GP and Midstream Holdings will merge with and into Midstream, and Midstream will survive as an indirect

wholly-owned subsidiary of CEQP.

- Q:

- What will Midstream common unitholders and Midstream preferred unitholders receive in the

merger?

- A:

- If

the merger is completed, holders of Midstream common units (other than CEQP, CGS or their respective subsidiaries) will be entitled to receive 2.75 CEQP

common units in exchange for each Midstream common unit owned, and holders of Midstream preferred units (other than CEQP, CGS or their respective subsidiaries) will be entitled to receive 2.75 CEQP

preferred units in exchange for each Midstream preferred unit owned. This exchange ratio is fixed and will not be adjusted, regardless of any change in price of either CEQP common units or Midstream

common units prior to completion of the merger. If the exchange ratio would result in a Midstream unitholder or Midstream preferred unitholder being entitled to receive a fraction of a new CEQP common

unit or new CEQP preferred unit, that unitholder will receive cash from CEQP in lieu of such fractional interest in an amount equal to (A) with respect to a new CEQP common unit, the product of

(i) the closing sale price of the CEQP common units on the NYSE as reported by The Wall Street Journal on the trading day immediately preceding the date on which the effective time occurs and

(ii) the fraction of a new CEQP common unit that the holder would otherwise be entitled to receive pursuant to the merger agreement, and (B) with respect to a new CEQP preferred unit,

the product of (i) the closing sale price of the CEQP common units on the NYSE as reported by The Wall Street Journal on the trading day immediately preceding the date on which the effective

time occurs, (ii) the number of CEQP common units into which one new CEQP preferred unit would be convertible if the new CEQP preferred units were convertible as of the effective time at the

Conversion Rate (as such term is defined in the CEQP Partnership Agreement Amendment), and (iii) the fraction of a new CEQP preferred unit that such holder would otherwise be entitled to

receive pursuant to the merger agreement. For additional information regarding exchange procedures, please read "The Merger Agreement—Exchange of Certificates; Fractional Units."

- Q:

- Where will my units trade after the merger?

- A:

- CEQP

common units will continue to trade on the NYSE under the symbol "CEQP." Midstream common units will no longer be publicly traded.

- Q:

- What will CEQP common unitholders receive in the merger?

- A:

- CEQP

common unitholders will simply retain the CEQP common units they currently own. They will not receive any additional CEQP common units in the merger.

- Q:

- What happens to my future distributions?

- A:

- Once the merger is completed and Midstream common units are exchanged for CEQP common units and Midstream preferred units are exchanged for CEQP preferred units, when distributions are approved and declared by Equity GP and paid by CEQP, former Midstream common unitholders and Midstream preferred unitholders will receive distributions on the CEQP common units and CEQP preferred units they receive in the merger in accordance with CEQP's partnership agreement, including the CEQP Partnership Agreement Amendment. Because the special meeting is scheduled to take place after the record dates for the distributions on both CEQP and Midstream units for the quarter ended June 30, 2015, which were declared and paid in August 2015, Midstream unitholders and Midstream preferred units will not receive second quarter

4

distributions for CEQP common units and CEQP preferred units received in the merger. For additional information, please read "Market Prices and Distribution Information."

Current CEQP common unitholders will continue to receive distributions on their common units in accordance with CEQP's partnership agreement and at the discretion of the Equity GP Board. For a description of the distribution provisions of CEQP's partnership agreement, please read "Comparison of the Rights of Midstream and CEQP Common Unitholders."

The current annualized distribution rate for each Midstream common unit is $1.64 (based on the quarterly distribution rate of $0.41 for each Midstream common unit paid on August 14, 2015 with respect to the second quarter of 2015). Based on the exchange ratio, the annualized distribution rate for each Midstream common unit exchanged for 2.75 CEQP common units would be approximately $1.5125 (based on the quarterly distribution rate of $0.1375 per CEQP common unit paid on August 14, 2015 with respect to the second quarter of 2015). Accordingly, based on current distribution rates and the 2.75 exchange ratio, a Midstream common unitholder would initially receive approximately 7.8% less in quarterly cash distributions on an annualized basis after giving effect to the merger. For additional information, please read "Comparative Per Unit Information" and "Market Prices and Distribution Information."

- Q:

- If I am a holder of Midstream common units represented by a unit certificate, should I send in my certificates representing Midstream

common units now?

- A:

- No.

After the merger is completed, holders of Midstream common units who hold their units in certificated form will receive written instructions for

exchanging their certificates representing Midstream common units. Please do not send in your certificates representing Midstream common units with your proxy card. If you own Midstream common units

in "street name," the merger consideration should be credited by your broker to your account within a few days following the closing date of the merger.

- Q:

- What constitutes a quorum?

- A:

- The

presence in person or by proxy at the special meeting of the holders of a majority of Midstream's outstanding common units and Midstream's outstanding

preferred units (on an "as if converted" basis), counted together as a single class, on the record date will constitute a quorum and will permit Midstream to conduct the proposed business at the

special meeting. Your units will be counted as present at the special meeting if you:

- •

- are present in person at the meeting; or

- •

- have submitted a properly executed proxy card or properly submitted your proxy by telephone or Internet.

Proxies received but marked as abstentions will be counted as units that are present and entitled to vote for purposes of determining the presence of a quorum. If an executed proxy is returned by a broker or other nominee holding units in "street name" indicating that the broker does not have discretionary authority as to certain units to vote on the proposals (a "broker non-vote"), such units will be considered present at the meeting for purposes of determining the presence of a quorum but cannot be included in the vote; therefore, broker non-votes have the same effect as a vote against the merger for purposes of the vote required under the merger agreement and Midstream's partnership agreement.

5

- Q:

- What is the vote required of Midstream common unitholders and Midstream preferred unitholders to approve the merger agreement and the

merger?

- A:

- Pursuant to the merger agreement and Midstream's partnership agreement, holders of a majority of the outstanding Midstream common units and Midstream outstanding preferred units (voting on an "as if converted" basis), voting together as a single class, must affirmatively vote in favor of the proposal in order for it to be approved. Failures to vote, abstentions and broker non-votes will have the same effect as a vote against the merger proposal for purposes of the vote required under the merger agreement and Midstream's partnership agreement. Your vote is important.

In connection with the merger agreement, CEQP entered into (i) a support agreement by and among CEQP, Midstream and CGS, pursuant to which, CEQP, which directly owns 7,137,841 Midstream common units, and CGS, which directly owns 21,597 Midstream common units, agreed to vote their respective Midstream common units in favor of the adoption of the merger agreement at any meeting of Midstream unitholders and (ii) a support agreement by and among CEQP, Midstream, Holdings and CGS LLC, pursuant to which, Holdings, which directly owns 2,497,071 Midstream common units, and CGS LLC, which directly owns 18,339,314 Midstream common units, agreed to vote their respective Midstream common units in favor of the adoption of the merger agreement at any meeting of Midstream unitholders. Pursuant to (i) a letter agreement regarding change of control election, by and among CEQP, Midstream, CGS and GE, a letter agreement regarding change of control election by and among CEQP, Midstream, CGS and GSO and (iii) a letter agreement regarding change of control election by and among CEQP, Midstream, CGS, Magnetar and the Magnetar preferred holders, pursuant to which, subject to the terms and conditions set forth in such letter agreements, each preferred holder expressed an intention to support the merger and agreed to elect to have all of the Midstream preferred units held of record by such preferred holder exchanged for CEQP preferred units upon the consummation of the merger in accordance with the terms of the merger agreement.

- Q:

- When do you expect the merger to be completed?

- A:

- A

number of conditions must be satisfied before CEQP and Midstream can complete the merger, including approval of the merger agreement and the merger by the

holders of Midstream units. Although CEQP and Midstream cannot be sure when all of the conditions to the merger will be satisfied, CEQP and Midstream expect to complete the merger as soon as

practicable following the Midstream special meeting (assuming the merger proposal is approved by the holders of Midstream units). For additional information, please read "The Merger

Agreement—Conditions to the Merger."

- Q:

- What is the recommendation of the Midstream Board?

- A:

- The Midstream Board recommends that you vote FOR the merger proposal.

On May 5, 2015, the Midstream Conflicts Committee determined unanimously that the merger agreement and the merger are advisable, fair and reasonable to and in the best interests of Midstream and the Midstream unaffiliated unitholders and recommended that the merger, the merger agreement and the transactions contemplated thereby be approved by the Midstream Board.

The Midstream Board determined that the merger agreement and merger are fair and reasonable to and in the best interests of Midstream and the Midstream unitholders, approved the merger agreement and the merger and recommended that the Midstream unitholders vote in favor of the merger proposal.

6

- Q:

- What are the expected U.S. federal income tax consequences to Midstream unitholders as a result of the transactions contemplated by

the merger agreement?

- A:

- It is anticipated that for U.S. federal income tax purposes no gain or loss should be recognized by Midstream unitholders solely as a result of the merger, other than gain resulting from either (i) any decrease in a Midstream unitholder's share of partnership liabilities pursuant to Section 752 of the Internal Revenue Code of 1986, as amended (the "Internal Revenue Code") or (ii) any cash received in lieu of any fractional new CEQP units.

Please read "Risk Factors—Tax Risks Related to the Merger" and "Material U.S. Federal Income Tax Consequences of the Merger—Tax Consequences of the Merger to Midstream and the Midstream Unitholders."

- Q:

- What are the expected U.S. federal income tax consequences for a Midstream unitholder of the ownership of CEQP common units after the

merger is completed?

- A:

- Each

Midstream unitholder who becomes a CEQP unitholder as a result of the merger will, as is the case for existing CEQP common unitholders, be allocated

such unitholder's distributive share of CEQP's income, gains, losses, deductions and credits. In addition to U.S. federal income taxes, such a holder will be subject to other taxes, including state

and local income taxes, unincorporated business taxes, and estate, inheritance or intangibles taxes that may be imposed by the various jurisdictions in which CEQP conducts business or owns property or

in which the unitholder is resident. Please read "U.S. Federal Income Tax Consequences of Ownership of CEQP Common Units."

- Q:

- Are Midstream unitholders entitled to appraisal rights?

- A:

- No.

Neither Midstream common unitholders nor Midstream preferred unitholders have appraisal rights under applicable law or contractual appraisal rights under

Midstream's partnership agreement or the merger agreement.

- Q:

- How do I vote my common units if I hold my common units in my own name?

- A:

- After

you have read this proxy statement/prospectus carefully, please respond by completing, signing and dating your proxy card and returning it in the

enclosed postage-paid envelope, or by submitting your proxy by telephone or the Internet as soon as possible in accordance with the instructions provided under "The Special Unitholder

Meeting—Voting Procedures—Voting by Midstream Unitholders" beginning on page 42.

- Q:

- If my Midstream common units are held in "street name" by my broker or other nominee, will my broker or other nominee vote my common

units for me?

- A:

- No. Your broker cannot vote your Midstream common units held in "street name" for or against the merger proposal unless you tell the broker or other nominee how you wish to vote. To tell your broker or other nominee how to vote, you should follow the directions that your broker or other nominee provides to you. Please note that you may not vote your Midstream common units held in "street name" by returning a proxy card directly to Midstream or by voting in person at the special meeting of Midstream unitholders unless you provide a "legal proxy," which you must obtain from your broker or other nominee. If you do not instruct your broker or other nominee on how to vote your Midstream common units, your broker or other nominee may not vote your Midstream common units, which will have the same effect as a vote against the merger for purposes of the vote required under the merger agreement and Midstream's partnership agreement. You should therefore provide your broker or other nominee with instructions as to how to vote your Midstream common units.

7

- Q:

- What if I do not vote?

- A:

- If

you do not vote in person or by proxy or if you abstain from voting, or a broker non-vote is made, it will have the same effect as a vote against the

merger proposal for purposes of the vote required under the merger agreement and Midstream's partnership agreement. If you sign and return your proxy card but do not indicate how you want to vote,

your proxy will be counted as a vote in favor of the merger proposal.

- Q:

- Who can attend and vote at the special meeting of Midstream unitholders?

- A:

- All

Midstream unitholders of record as of the close of business on August 24, 2015, the record date for the special meeting of Midstream unitholders,

are entitled to receive notice of and vote at the special meeting of Midstream unitholders.

- Q:

- When and where is the special meeting?

- A:

- The

special meeting will be held on September 30, 2015, at 10:00 a.m., local time, at 700 Louisiana Street, Suite 2550, Houston,

Texas 77002.

- Q:

- If I am planning to attend the special meeting in person, should I still vote by

proxy?

- A:

- Yes.

Whether or not you plan to attend the special meeting, you should vote by proxy. Your common units will not be voted if you do not vote by proxy and do

not vote in person at the special meeting.

- Q:

- Can I change my vote after I have submitted my proxy?

- A:

- Yes.

If you own your common units in your own name, you may revoke your proxy at any time prior to its exercise

by:

- •

- giving written notice of revocation to the chief executive officer of Midstream GP at or before the special meeting;

- •

- appearing and voting in person at the special meeting; or

- •

- properly completing and executing a later dated proxy and delivering it to the chief executive officer of Midstream GP at or before the special meeting.

Your presence without voting at the meeting will not automatically revoke your proxy, and any revocation during the meeting will not affect votes previously taken.

- Q:

- What should I do if I receive more than one set of voting materials for the special meeting of Midstream

unitholders?

- A:

- You

may receive more than one set of voting materials for the special meeting of Midstream unitholders and the materials may include multiple proxy cards or

voting instruction cards. For example, you will receive a separate voting instruction card for each brokerage account in which you hold units. If you are a holder of record registered in more than one

name, you will receive more than one proxy card. Please complete, sign, date and return each proxy card and voting instruction card that you receive according to the instructions on it.

- Q:

- Whom do I call if I have further questions about voting, the meeting or the

merger?

- A:

- Midstream unitholders may call Midstream's Investor Relations department at (713) 380-3081. If you would like additional copies, without charge, of this proxy statement/prospectus or if you have questions about the merger, including the procedures for voting your units, you should contact American Stock Transfer & Trust Company, LLC, which is assisting Midstream as tabulation agent in connection with the merger, at (800) 937-5449.

8

This summary highlights some of the information in this proxy statement/prospectus. It may not contain all of the information that is important to you. To understand the merger fully and for a more complete description of the terms of the merger, you should read carefully this document, the documents incorporated by reference, and the Annexes to this document, including the full text of the merger agreement included as Annex A. Please also read "Where You Can Find More Information."

The Merger Parties' Businesses (page 100)

Crestwood Equity Partners LP

CEQP, a Delaware limited partnership formed in 2004, is a master limited partnership (an "MLP") that develops, acquires, owns or controls, and operates primarily fee-based assets and operations within the energy midstream sector. Headquartered in Houston, Texas, CEQP provides broad-ranging infrastructure solutions across the value chain to service premier liquids-rich and crude oil shale plays across the United States. Its common units representing limited partner interests are listed on the NYSE under the symbol "CEQP."

CEQP owns and operates a diversified portfolio of crude oil and natural gas gathering, processing, storage and transportation assets that connect fundamental energy supply with energy demand across North America. CEQP's operating assets consist of a proprietary NGL supply and logistics business. Its other consolidated assets are owned by or through Midstream. CEQP's consolidated operating assets include:

- •

- natural gas facilities with approximately 2.5 billion cubic feet per day ("Bcf/d") of gathering capacity, 481 million

cubic feet per day ("MMcf/d") of processing capacity, 1.1 Bcf/d of firm transmission capacity, and 41 billion cubic feet ("Bcf") of certificated working gas storage capacity;

- •

- natural gas liquid ("NGL") facilities with approximately 24,000 barrels per day ("Bbls/d") of fractionation capacity and

2.8 million barrels of storage capacity;

- •

- crude oil facilities with approximately 125,000 Bbls/d of gathering capacity, approximately 1.1 million barrels of

storage capacity, 48,000 Bbls/d of transportation capacity and 160,000 Bbls/d of rail loading capacity; and

- •

- a fleet of transportation assets supporting its proprietary NGL supply and logistics business, including 8 truck and rail terminals and approximately 543 truck/trailer units and 1,600 rail units that can transport more than 294,000 Bbls/d of NGLs.

CEQP's principal executive offices are located at 700 Louisiana Street, Suite 2550, Houston, Texas 77002, and its telephone number is (832) 519-2200.

Crestwood Midstream Partners LP

Midstream, a Delaware limited partnership formed in 2004, is a growth-oriented MLP that develops, acquires, owns and operates primarily fee-based assets and operations within the energy midstream sector. Headquartered in Houston, Texas, it provides broad-ranging infrastructure solutions across the value chain to service premier liquids-rich and crude oil shale plays across the United States. Midstream's common units representing limited partner interests are listed on the NYSE under the symbol "CMLP."

9

Midstream owns and operates a diversified portfolio of crude oil and natural gas gathering, processing, storage and transportation assets that connect fundamental energy supply with energy demand across North America. Midstream's consolidated operating assets primarily include:

- •

- natural gas facilities with approximately 2.5 Bcf/d of gathering capacity, 481 MMcf/d of processing capacity,

1.1 Bcf/d of firm transmission capacity, and 41 Bcf of certificated working gas storage capacity;

- •

- NGL facilities with approximately 1.7 million barrels of storage capacity; and

- •

- crude oil facilities with approximately 125,000 Bbls/d of gathering capacity, approximately 1.1 million barrels of storage capacity, 48,000 Bbls/d of transportation capacity and 160,000 Bbls/d of rail loading capacity.

Midstream's principal executive offices are located at 700 Louisiana Street, Suite 2550, Houston, Texas 77002, and its telephone number is (832) 519-2200.

Relationship of CEQP and Midstream (page 102)

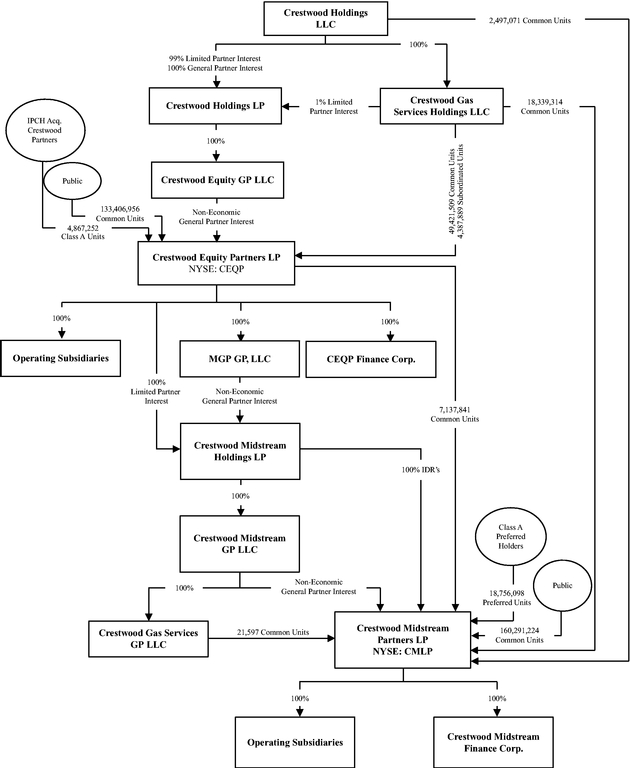

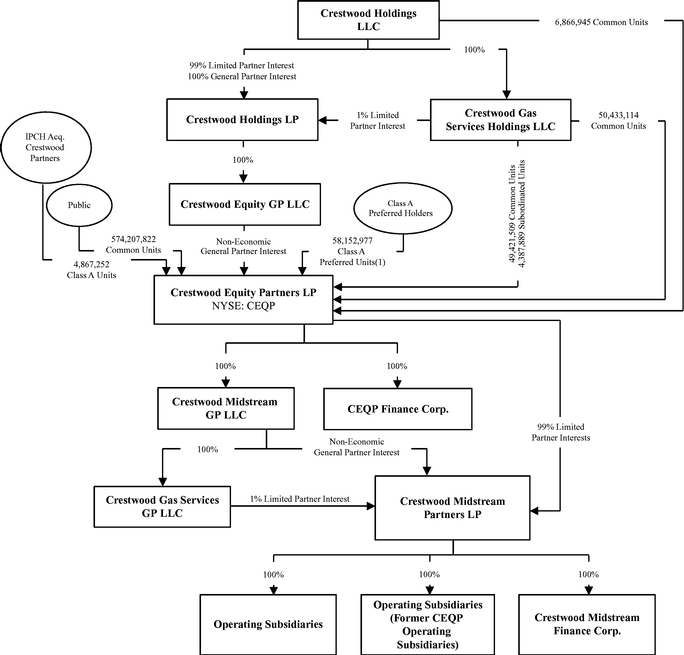

CEQP and Midstream are currently under common control. Midstream is currently owned 100% by its limited partners and its non-economic general partner, Midstream GP. Midstream was formed by CEQP in September 2004 for the purpose of holding certain of CEQP's midstream investments. Midstream GP and 100% of Midstream's IDRs are currently owned by Midstream Holdings, a wholly-owned subsidiary of CEQP. CEQP and CGS own collectively 7,159,438 of Midstream's outstanding common units.

As of August 27, 2015, Midstream's subsidiary, US Salt, had 96 employees, all of which are members of the United Steel Workers Union. Midstream does not otherwise have any employees. Midstream shares common management, general and administrative and overhead costs with CEQP. Midstream has an omnibus agreement with CEQP that requires it to reimburse CEQP for all shared costs incurred on its behalf, except for certain unit based compensation costs which are treated as capital transactions.

All of the executive officers and certain directors of Equity GP are executive officers and directors of Midstream GP. For information about the common executive officers and directors of Equity GP and Midstream GP, and the resulting interests of Midstream GP directors and officers in the merger, please read "Certain Relationships; Interests of Certain Persons in the Merger."

Structure of the Merger and Related Transactions (page 73)

Pursuant to the merger agreement, at the effective time of the merger, MergerCo, MGP GP and Midstream Holdings will merge with and into Midstream, with Midstream surviving the merger as an indirect wholly-owned subsidiary of CEQP. Immediately following the effective time of the merger, CEQP will contribute 100% of the equity interests of Crestwood Operations to Midstream in exchange for additional limited partner interests in Midstream, such that following the merger and the related transactions provided for in the merger agreement, Midstream GP will be a direct, wholly-owned subsidiary of CEQP and will continue to be the sole general partner of Midstream, and CEQP and CGS will own a 99.9% limited partner interest and a 0.1% limited partner interest, respectively, in Midstream. At the effective time, each outstanding common unit of Midstream held by Midstream unitholders, except for CEQP for any Midstream common units owned by CEQP, CGS or their respective affiliates will be converted into the right to receive 2.75 CEQP common units, and each outstanding preferred unit of Midstream held by Midstream unitholders, except for any Midstream preferred units owned by CEQP or its subsidiaries, will be converted into the right to receive 2.75 CEQP preferred units. This merger consideration represents a 17% premium to the closing price of Midstream common units based on the closing prices of Midstream common units and CEQP common

10

units on May 5, 2015, the last trading day before CEQP announced its initial proposal to acquire all of the Midstream common units owned by the public and the parties entered into the merger agreement.

In lieu of any fractional new CEQP common unit or new CEQP preferred unit, each holder of Midstream units who would otherwise be entitled to a fraction of a new CEQP common unit or new CEQP preferred unit will be paid in cash (without interest rounded up to the nearest whole cent) an amount equal to, (A) with respect to a new CEQP common unit, the product of (i) the closing sale price of the CEQP common units on the NYSE as reported by The Wall Street Journal on the trading day immediately preceding the date on which the effective time occurs and (ii) the fraction of a new CEQP common unit that the holder would otherwise be entitled to receive pursuant to the merger agreement, and (B) with respect to a new CEQP preferred unit, the product of (i) the closing sale price of the CEQP common units on the NYSE as reported by The Wall Street Journal on the trading day immediately preceding the date on which the effective time occurs, (ii) the number of CEQP common units into which one new CEQP preferred unit would be convertible if the new CEQP preferred units were convertible as of the effective time at the Conversion Rate (as such term is defined in the CEQP Partnership Agreement Amendment), and (iii) the fraction of a new CEQP preferred unit that such holder would otherwise be entitled to receive pursuant to the merger agreement. Any fractional CEQP common unit or CEQP preferred unit interest will not entitle its owner to vote or to have any rights as a CEQP unitholder with regard to such interest.

Once the merger is completed and the Midstream common units held by Midstream common unitholders (other than CEQP, CGS or their respective subsidiaries) are exchanged for CEQP common units and the Midstream preferred units held by Midstream preferred unitholders (other than CEQP or its subsidiaries) are exchanged for CEQP preferred units (and cash in lieu of fractional units, if applicable), when distributions are declared by the general partner of CEQP and paid by CEQP, former Midstream unitholders will receive distributions on their CEQP common units and CEQP preferred units in accordance with CEQP's partnership agreement, including the CEQP Partnership Agreement Amendment thereto. For a description of the distribution provisions of CEQP's partnership agreement, please read "Comparison of the Rights of CEQP and Midstream Unitholders."

As of May 5, 2015 there were 181,204,695 CEQP common units and 187,423,322 Midstream common units outstanding. Based on the 187,423,322 Midstream common units outstanding at such date that are owned by Midstream unitholders and eligible for exchange into CEQP common units pursuant to the merger agreement, CEQP expects to issue approximately 498.1 million CEQP common units in connection with the merger.

Based on the $6.82 closing price of CEQP common units on May 5, 2015 (the last full trading day before CEQP and Midstream entered into and announced the merger agreement), the exchange ratio of 2.75 CEQP common units for each outstanding Midstream common unit, and the approximate 153.5 million Midstream common units owned by Midstream unaffiliated unitholders, the value of the merger consideration to be received by such holders was approximately $2.9 billion, or $18.76 for each Midstream common unit.

Support Agreements and Letter Agreements Regarding Change of Control Election (page 71)

Pursuant to the merger agreement and Midstream's partnership agreement, a majority of the outstanding Midstream common units and Midstream preferred units (voting on an "as if converted" basis), voting together as a single class, must vote in favor of the proposal in order for it to be approved. In connection with the merger agreement, CEQP entered into (i) a support agreement by and among CEQP, Midstream and CGS, pursuant to which CEQP, which directly owns 7,137,841 Midstream common units, and CGS, which directly owns 21,597 Midstream common units, agreed to vote their respective Midstream common units in favor of the adoption of the merger agreement at any meeting of Midstream unitholders and (ii) a support agreement by and among CEQP, Midstream, Holdings and CGS LLC, pursuant to which Holdings, which directly owns 2,497,071 Midstream

11

common units, and CGS LLC, which directly owns 18,339,314 Midstream common units, agreed to vote their respective Midstream common units in favor of the adoption of the merger agreement at any meeting of Midstream unitholders. As a result, holders of a total of 27,995,823 Midstream common units, which represents 13.5% of the total outstanding Midstream common units and Midstream preferred units (on an "as if converted" basis), have agreed to vote in favor of the proposal. Pursuant to (i) a letter agreement regarding change of control election by and among CEQP, Midstream, CGS and GE, (ii) a letter agreement regarding change of control election by and among CEQP, Midstream, CGS and GSO and (iii) a letter agreement regarding change of control election by and among CEQP, Midstream, CGS, Magnetar and the Magnetar preferred holders, subject to the terms and conditions set forth in such letter agreements, each preferred holder stated that it expressed an intention to support the merger and agreed to elect to have all of the Midstream preferred units held of record by such preferred holder exchanged for CEQP preferred units upon the consummation of the merger in accordance with the terms of the merger agreement. These three preferred holders that have expressed an intention to support the merger pursuant to the letter agreements hold a total of 21,580,244 Midstream preferred units.

Directors and Executive Officers of CEQP Following the Merger (page 106)

The directors and executive officers of CEQP prior to the merger will continue as directors and executive officers of CEQP after the merger.

Market Prices of CEQP Common Units and Midstream Common Units Prior to Announcing the Proposed Merger (page 29)

CEQP's common units are traded on the NYSE under the ticker symbol "CEQP." Midstream's common units are traded on the NYSE under the ticker symbol "CMLP." The following table shows the closing prices of CEQP common units and Midstream common units on May 5, 2015.

Date/Period

|

CEQP Common Units |

Midstream Common Units |

|||||

|---|---|---|---|---|---|---|---|

May 5, 2015 |

$ | 6.82 | $ | 16.00 | |||

The Special Unitholder Meeting (page 41)

Where and when: The Midstream special unitholder meeting will take place at 700 Louisiana Street, Suite 2550, Houston, Texas 77002 on September 30, 2015 at 10:00 a.m., local time.

What you are being asked to vote on: At the Midstream meeting, Midstream unitholders will vote on the approval of the merger agreement and the merger the proposal to adjourn the special meeting, if necessary, to solicit additional proxies if there are not sufficient votes to approve the merger agreement at the time of the special meeting. Midstream unitholders also may be asked to consider other matters as may properly come before the meeting. At this time, Midstream knows of no other matters that will be presented for the consideration of its unitholders at the meeting.

Who may vote: You may vote at the Midstream meeting if you owned Midstream common units or Midstream preferred units at the close of business on the record date, August 24, 2015. On that date, there were 188,306,968 Midstream common units outstanding. You may cast one vote for each outstanding Midstream common unit or Midstream preferred unit, as applicable, that you owned on the record date.

What vote is needed: Under the merger agreement and Midstream's partnership agreement, holders of a majority of the outstanding Midstream common units and Midstream preferred units (voting on an "as if converted" basis), voting together as a single class must affirmatively vote in favor of the proposal in order for it to be approved. CEQP, CGS, Holdings and CGS LLC have agreed to

12

vote any Midstream common units owned by them or their subsidiaries in favor of adoption of the merger agreement and the merger at any meeting of Midstream unitholders. Each of CEQP, CGS, Holdings and CGS LLC currently directly owns 7,137,841, 21,597, 2,497,071 and 18,339,314 Midstream common units, respectively (representing approximately 14.9% of the outstanding Midstream common units). Pursuant to (i) a letter agreement regarding change of control election by and among CEQP, Midstream, CGS and GE, (ii) a letter agreement regarding change of control election by and among CEQP, Midstream, CGS and GSO and (iii) a letter agreement regarding change of control election by and among CEQP, Midstream, CGS and the preferred holders, subject to the terms and conditions set forth in such letter agreements, each preferred holder expressed an intention to support the merger and agreed to elect to have all of the Midstream preferred units held of record by such preferred holder exchanged for CEQP preferred units upon the consummation of the merger in accordance with the terms of the merger agreement.

Under Midstream's partnership agreement, to approve the proposal to adjourn the special meeting, if necessary, to solicit additional proxies if there are not sufficient votes to approve the merger agreement at the time of the special meeting, holders of a majority of the outstanding Midstream common units present and entitled to vote at the meeting must affirmatively vote in favor of the proposal in order for it to be approved.

Recommendation to Midstream Unitholders (page 54)

The members of the Midstream Conflicts Committee considered the benefits of the merger and the related transactions as well as the associated risks and determined unanimously that the merger agreement and the merger are advisable, fair and reasonable to, and in the best interests of, Midstream and the Midstream unaffiliated unitholders. The Midstream Conflicts Committee also recommended that the merger agreement and the merger be approved by the Midstream Board. The Midstream Board has also approved the merger agreement and the merger and recommends that the Midstream unitholders vote to approve the merger agreement and the merger.

Midstream unitholders are urged to review carefully the background and reasons for the merger described under "The Merger" and the risks associated with the merger described under "Risk Factors."

Midstream's Reasons for the Merger (page 54)

The Midstream Conflicts Committee considered many factors in making its determination and recommendation that the merger agreement and the merger are fair and reasonable to and in the best interests of Midstream and the Midstream unaffiliated unitholders and has approved the merger agreement and recommended that the Midstream Board approve the merger agreement, the execution, delivery and performance by Midstream of the merger agreement and the transactions contemplated thereby. Based upon, among other things, the recommendation of Midstream Conflicts Committee, the Midstream Board has determined unanimously that the merger agreement and the transactions contemplated thereby are fair and reasonable to and in the best interests of Midstream and the holders of Midstream units, approved the merger agreement, the execution, delivery and performance by Midstream of the merger agreement and the transactions contemplated thereby, directed that the merger agreement be submitted to the Midstream unitholders for approval at a special meeting of such unitholders for the purpose of approving the merger agreement and the merger and recommends that the holders of Midstream units vote "FOR" the merger agreement and the merger.

In the course of reaching its decision to approve the merger agreement and the transactions contemplated by the merger agreement, the Midstream Conflicts Committee considered a number of factors in its deliberations. For a more complete discussion of these factors, see "The Merger—Recommendation of the Midstream Board and the Midstream Conflicts Committee's Reasons for the Merger."

13

Overall, the Midstream Conflicts Committee believed that the advantages of the merger outweighed the negative factors.

Opinion of the Midstream Conflicts Committee's Financial Advisor (page 56)

At the request of the Midstream Conflicts Committee at a meeting of the Midstream Conflicts Committee held on May 5, 2015, Tudor, Pickering, Holt & Co. Advisors, LLC ("TPH") rendered its oral opinion to the Midstream Conflicts Committee that, as of May 5, 2015, based upon and subject to the assumptions, qualifications, limitations and other matters considered by TPH in connection with the preparation of its opinion, the Common Merger Consideration to be received by the Unaffiliated Common Unitholders in the merger pursuant to the merger agreement was fair, from a financial point of view, to the Unaffiliated Common Unitholders. TPH subsequently confirmed its oral opinion in writing dated May 5, 2015 to the Midstream Conflicts Committee. In the sections of this proxy statement/prospectus regarding TPH's opinion and related analyses, references to the "Unaffiliated Common Unitholders" means the holders of Midstream common units other than (i) CEQP and its affiliates and (ii) the officers and directors of Midstream GP that are also officers or directors of Equity GP or affiliates of such officers and directors, and references to the "Transaction" means the merger and the related transactions contemplated by the merger agreement.

TPH's opinion was directed to the Midstream Conflicts Committee (in its capacity as such), and only addressed the fairness from a financial point of view, as of the date of the opinion, to the Unaffiliated Common Unitholders of the Common Merger Consideration to be received by the Unaffiliated Common Unitholders in the merger pursuant to the merger agreement. TPH's opinion did not address any other term or aspect of the merger agreement or the Transaction. The full text of the TPH written opinion, dated May 5, 2015, which describes the assumptions made, procedures followed, matters considered, and qualifications and limitations of the review undertaken by TPH in rendering its opinion, is attached as Annex B to this proxy statement/prospectus. The summary of TPH's opinion set forth in this proxy statement/prospectus is qualified in its entirety by reference to the full text of the opinion. However, neither TPH's written opinion nor the summary of its opinion and the related analyses set forth in this proxy statement/prospectus are intended to be, and they do not constitute, a recommendation as to how the Midstream Conflicts Committee or the board of directors of Midstream GP, Midstream GP, any holder of securities in Midstream or any other person should act or vote with respect to any matter relating to the merger, the Transaction or any other matter.

Certain Relationships; Interests of Certain Persons in the Merger (page 102)

CEQP and its general partner are effectively controlled by First Reserve, through its subsidiary Holdings. Given that CEQP effectively owns and control's Midstream's general partner, First Reserve effectively controls Midstream as well as CEQP.

In considering the recommendation of the Midstream Board with respect to the merger, Midstream unitholders should be aware that certain of the executive officers and directors of Midstream GP have interests in the transaction that differ from, or are in addition to, the interests of Midstream unitholders generally, including:

- •

- All of the directors and executive officers of Midstream GP will receive continued indemnification for their actions as

directors and executive officers.

- •

- Certain directors of Midstream GP, none of whom is a member of the Midstream Conflicts Committee, own CEQP common units.

- •

- Some of Midstream GP's directors, none of whom is a member of the Midstream Conflicts Committee, also serve as executive officers of Equity GP, have certain duties to the limited partners of CEQP and are compensated, in part, based on the performance of CEQP.

14

Each of the executive officers and directors of Equity GP is currently expected to remain an executive officer and director of Equity GP following the merger. The persons who will be elected as additional executive officers or directors of Equity GP following the merger have not yet been determined.

Robert G. Phillips, Alvin Bledsoe, Michael G. France, Warren H. Gfeller, John J. Sherman and David M. Wood, who are directors of Midstream GP, also serve as directors of Equity GP.

The Merger Agreement (page 73)

The merger agreement is attached to this proxy statement/prospectus as Annex A and is incorporated by reference into this document. You are encouraged to read the merger agreement because it is the legal document that governs the merger.

Material U.S. Federal Income Tax Consequences of the Merger (page 128)

Tax matters associated with the merger are complicated. The U.S. federal income tax consequences of the merger to a Midstream unitholder will depend on such unitholder's specific tax situation. The tax discussions in this proxy statement/prospectus focus on the U.S. federal income tax consequences generally applicable to individuals who are residents or citizens of the United States that hold Midstream units as capital assets, and these discussions have only limited application to other unitholders, including those subject to special tax treatment. Midstream unitholders are urged to consult their tax advisors for a full understanding of the U.S. federal, state, local and foreign tax consequences of the merger that will be applicable to them.

Midstream expects to receive an opinion from Vinson & Elkins LLP to the effect that no gain or loss should be recognized by Midstream unitholders to the extent new CEQP units are received as a result of the merger, other than gain resulting from either (i) any decrease in partnership liabilities pursuant to Section 752 of the Internal Revenue Code, or (ii) any cash received in lieu of any fractional new CEQP units. CEQP also expects to receive an opinion from Vinson & Elkins LLP to the effect that no gain or loss should be recognized by CEQP unitholders as a result of the merger (other than gain resulting from any decrease in partnership liabilities pursuant to Section 752 of the Internal Revenue Code). Opinions of counsel, however, are subject to certain limitations and are not binding on the Internal Revenue Service, "IRS" and no assurance can be given that the IRS would not successfully assert a contrary position regarding the merger and the opinions of counsel.

Please read "Material U.S. Federal Income Tax Consequences of the Merger" beginning on page 128 for a more complete discussion of the U.S. federal income tax consequences of the merger.

Other Information Related to the Merger

No Dissenters' or Appraisal Rights (page 70)

Neither Midstream common unitholders nor Midstream preferred unitholders have dissenters' or appraisal rights under applicable Delaware law or contractual appraisal rights under Midstream's partnership agreement or the merger agreement.

Antitrust and Regulatory Matters (page 70)

The merger is subject to both state and federal antitrust laws. Under the rules applicable to partnerships, no filing is required under the Hart-Scott-Rodino Antitrust Improvements Act of 1976 (the "HSR Act"). However, CEQP or Midstream may receive inquiries or requests for information concerning the proposed merger and related transactions from the Federal Trade Commission ("FTC"), the Antitrust Division of the Department of Justice ("DOJ"), or individual states, and the FTC or DOJ could take such action under the antitrust laws as it deems necessary or desirable in the public interest.

15

Listing of Common Units to be Issued in the Merger (page 70)

CEQP expects to obtain approval to list on the NYSE the CEQP common units to be issued pursuant to the merger agreement, which approval is a condition to the merger.

Accounting Treatment of the Merger (page 70)

The proposed merger will be accounted for in accordance with Financial Accounting Standards Board Accounting Standards Codification 810, Consolidations—Overall—Changes in Parent's Ownership Interest in a Subsidiary. Because CEQP controls Midstream both before and after the merger and related transactions, the changes in CEQP's ownership interest in Midstream will be accounted for as an equity transaction and no gain or loss will be recognized in CEQP's consolidated statements of operations resulting from the merger. The proposed merger represents CEQP's acquisition of the noncontrolling interests in Midstream.

Comparison of the Rights of CEQP and Midstream Unitholders (page 107)

Midstream common unitholders will own CEQP common units following the completion of the merger, and their rights associated with CEQP common units will be governed by, in addition to Delaware law, CEQP's partnership agreement, which differs in a number of respects from Midstream's partnership agreement.

As a condition to closing of transactions contemplated under the merger agreement, the parties have agreed to execute and deliver (i) the CEQP Partnership Agreement Amendment to CEQP's partnership agreement to create the CEQP preferred units, (ii) a Registration Rights Agreement intended to give the holders of CEQP preferred units substantially the same rights as they currently have with respect to their Midstream preferred units under a corresponding agreement with Midstream; and (iii) a Board Representation and Standstill Agreement intended to give the holders of CEQP preferred units substantially the same rights as they currently have with respect to their Midstream preferred units under a corresponding agreement with Midstream. After giving effect to these transactions, the CEQP preferred units will constitute Substantially Equivalent Units (as defined in Midstream's partnership agreement). Please read "Comparison of the Rights of CEQP And Midstream Unitholders" for a more complete discussion of the rights of Midstream and CEQP unitholders.

Pending Litigation (page 70)

On May 20, 2015, Lawrence G. Farber, a purported unitholder of Midstream, filed a complaint in the Southern District of the United States, Houston Division, as a putative class action on behalf of the Midstream unitholders, captioned Lawrence G. Farber, individually and on behalf of all others similarly situated v. Crestwood Midstream Partners LP, Crestwood Midstream GP, LLC, Robert G. Phillips, Alvin Bledsoe, Michael G. France, Philip D. Gettig, Warren H. Gfeller, David Lumpkins, John J. Sherman, David Wood, Crestwood Equity Partners LP, Crestwood Equity GP LLC, CEQP ST Sub LLC, MGP GP, LLC, Crestwood Midstream Holdings LP, and Crestwood Gas Services GP, LLC, Civil Action No. 4:15-cv-1367. This complaint alleges, among other things, that Midstream GP breached its fiduciary duties, certain individual defendants have breached their fiduciary duties of loyalty and due care, and that other defendants have aided and abetted such breaches. On July 6, 2015, the plaintiff in such lawsuit filed an amended complaint, which further alleges that the named defendants violated Sections 14(a) and 20(a) of the Securities Exchange Act of 1934 and Rule 14a-9 promulgated thereunder by disseminating a false and materially misleading proxy statement in connection with the merger. The plaintiff seeks to enjoin the merger unless and until such alleged breaches have been cured.

On July 21, 2015, Isaac Aron, another purported unitholder of Midstream, filed a complaint in the Southern District of the United States, Houston Division, as a putative class action on behalf of the Midstream unitholders, captioned Isaac Aron, individually and on behalf of all others similarly situated

16

v. Robert G. Phillips, Alvin Bledsoe, Michael G. France, Philip D. Gettig, Warren H. Gfeller, David Lumpkins, John J. Sherman, David Wood, Crestwood Midstream Partners LP, Crestwood Midstream Holdings LP, Crestwood Midstream GP LLC, Crestwood Gas Services GP, LLC, Crestwood Equity Partners LP, Crestwood Equity GP LLC, CEQP ST SUB LLC and MGP GP, LLC, Civil Action No. 4:15-cv-2101. The complaint alleges, among other things, that Midstream GP and certain individual defendants violated Sections 14(a) and 20(a) of the Securities Exchange Act of 1934 and Rule 14a-9 promulgated thereunder by disseminating a false and materially misleading proxy statement in connection with the merger. The plaintiff seeks to enjoin the merger unless and until certain information is disclosed to Midstream unitholders.

On August 10, 2015, the Kenneth C. Halter Trust, another purported unitholder of Midstream, by and through its trustee, filed a complaint in the Delaware Court of Chancery seeking to inspect and make copies and extracts of certain books and records of Midstream for the purpose of investigating possible mismanagement and alleged breaches of Midstream's partnership agreement by the Midstream Board in connection with merger.