Exhibit 10.1

LEASE

Arboretum Courtyard, L.L.C.,

a Delaware limited liability company,

Landlord

and

CATASYS, INC.,

a California corporation,

Tenant

for

Arboretum Courtyard

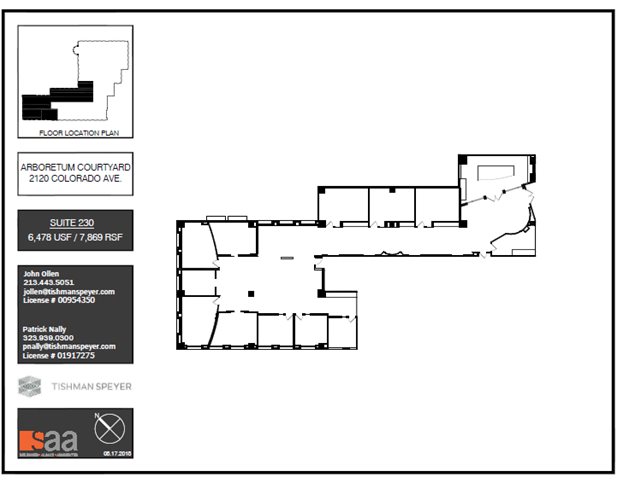

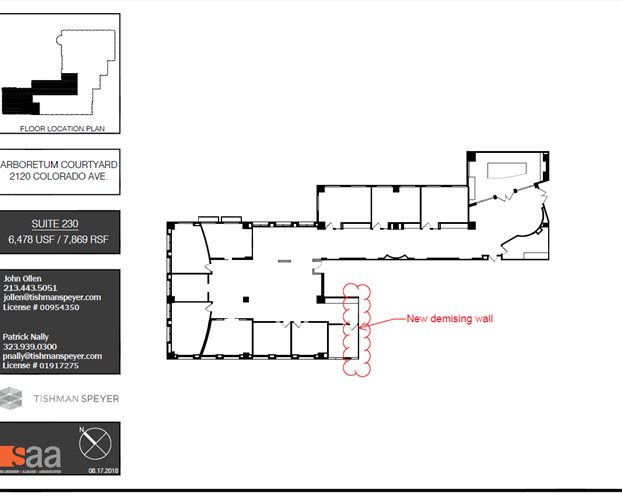

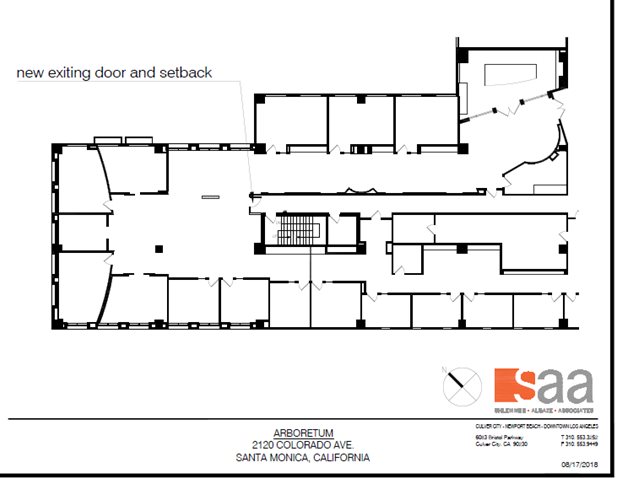

2120 Colorado Avenue, Suite 230

Santa Monica, California

September 28, 2018

|

789956.06/WLA 377061-00006/sb/sb |

|

Arboretum Courtyard [Catasys, Inc.] |

LEASE

THIS LEASE is made as of the 28th day of September, 2018 ("Effective Date"), between Arboretum Courtyard, L.L.C., a Delaware limited liability company ("Landlord"), and CATASYS, INC., a California corporation ("Tenant").

Landlord and Tenant hereby agree as follows:

ARTICLE 1

basic lease provisions

|

PREMISES |

A portion of the second (2nd) floor of the Building, commonly known as Suite 230, as more particularly shown on Exhibit A, attached hereto. |

|

|

BUILDING |

The building, fixtures, equipment and other improvements and appurtenances now located or hereafter erected, located or placed upon the land known as 2120 Colorado Avenue, Santa Monica, California. |

|

|

PROJECT |

That office building complex which is comprised collectively of the Building and that certain building located at 2150 Colorado Avenue, the land upon which such buildings are located, a subterranean parking garage located on such land, and all buildings and other improvements and plazas now or hereafter constructed on such land. |

|

|

COMMENCEMENT DATE |

The earlier to occur of (i) the date upon which Tenant first commences to conduct business in the Premises and (ii) the date that is thirty (30) days following the date upon which the Premises are Ready for Occupancy. The Premises are anticipated to be Ready for Occupancy on April 1, 2019. |

|

|

EXPIRATION DATE |

If the Commencement Date shall be the first day of a calendar month, then the day immediately preceding the fifth (5th) anniversary of the Lease Commencement Date; or, if the Commencement Date shall be other than the first day of a calendar month, then the last day of the month in which the fifth (5th) anniversary of the Commencement Date occurs. |

|

|

TERM |

The period commencing on the Commencement Date and ending on the Expiration Date. |

|

|

PERMITTED USES |

Executive and general offices, consistent with the character of the Building as a first-class office building. |

|

|

BASE YEAR |

Calendar year 2019. |

|

|

TENANT'S PROPORTIONATE SHARE |

5.3523%. |

|

|

AGREED AREA OF PROJECT |

147,022 rentable square feet |

|

|

AGREED AREA OF BUILDING |

86,656 rentable square feet, as mutually agreed by Landlord and Tenant. |

|

|

789956.06/WLA 377061-00006/sb/sb |

|

Arboretum Courtyard [Catasys, Inc.] |

|

AGREED AREA OF PREMISES |

7,869 rentable square feet, as mutually agreed by Landlord and Tenant. |

||||

|

FIXED RENT |

Months During |

Per Annum |

Per Month |

Monthly Fixed Rent Per Rentable Square Foot* |

|

|

1-12** |

$571,289.40 |

$47,607.45 |

$6.05 |

||

|

13-24 |

$591,284.52 |

$49,273.71 |

$6.26 |

||

|

25-36 |

$611,979.47 |

$50,998.29 |

$6.48 |

||

|

37-48 |

$633,398.75 |

$52,783.23 |

$6.71 |

||

|

49-Expiration Date |

$655,567.70 |

$54,630.64 |

$6.94 |

||

|

*The calculations of the monthly Fixed Rent Per Rentable Square Foot set forth above are approximate calculations based on a three and one half percent (3.5%) increase per annum and rounded to the nearest cent. Such approximations are provided for convenience only and the Per Annum and Per Month amounts set forth above shall control.

**Subject to the terms of Section 2.3(b), below. |

|||||

|

ADDITIONAL RENT |

All sums other than Fixed Rent payable by Tenant to Landlord under this Lease, including Tenant's Tax Payment, Tenant's Operating Payment, late charges, overtime or excess service charges, parking fees, damages, and interest and other costs related to Tenant's failure to perform any of its obligations under this Lease. |

||||

|

RENT |

Fixed Rent and Additional Rent, collectively. |

||||

|

INTEREST RATE |

The lesser of (i) three percent (3%) per annum above the then-current Base Rate, and (ii) the maximum rate permitted by applicable Requirements. |

||||

|

LETTER OF CREDIT |

$407,566.00. |

||||

|

PARKING |

Subject to the terms of Article 28 hereof. |

||||

|

TENANT'S ADDRESS FOR NOTICES |

Until Tenant commences business operations from the Premises:

Catasys, Inc. Los Angeles, CA 90025 |

||||

|

789956.06/WLA 377061-00006/sb/sb |

|

Arboretum Courtyard [Catasys, Inc.] |

|

Thereafter:

Catasys, Inc. 2120 Colorado Avenue, Suite 230

With copies to:

Loeb & Loeb LLP 10100 Santa Monica Blvd., Suite 2200 Los Angeles, California 90067 Attn: Thomas Hanley, Esq. |

|

|

LANDLORD'S ADDRESS FOR NOTICES |

Arboretum Courtyard, L.L.C. |

|

With copies to:

Tishman Speyer

and:

Tishman Speyer |

|

|

TENANT'S BROKER |

Jones Lang LaSalle, Inc. |

|

LANDLORD'S AGENT |

Tishman Speyer Properties, L.P. or any other person or entity designated at any time and from time to time by Landlord as Landlord's Agent. |

All capitalized terms used in this Lease without definition are defined in Exhibit B, attached hereto.

|

789956.06/WLA 377061-00006/sb/sb |

|

Arboretum Courtyard [Catasys, Inc.] |

ARTICLE 2

PREMISES; TERM; RENT

Section 2.1 Lease of Premises. Subject to the terms of this Lease, Landlord leases to Tenant and Tenant leases from Landlord the Premises for the Term. Landlord and Tenant hereby agree that the rentable square feet and usable square feet of the Premises, the rentable square feet of the office area of the Building and the rentable square feet of the Project have been agreed to by Landlord and Tenant and are as stipulated in Article 1 above. In addition, Landlord grants to Tenant the right to use, on a non-exclusive basis and in common with others, the Common Areas. Except in the event of an emergency or as otherwise specifically required pursuant to applicable Requirements or the terms of this Lease, Tenant shall be granted access to the Premises, the Building and the “Project Parking Facility,” as that term is defined in Article 28 below, twenty-four (24) hours per day, seven (7) days per week, every day of the year, during the Term, subject to all applicable Requirements, Landlord’s reasonable access control procedures, the Rules and Regulations and the terms of this Lease.

Section 2.2 Commencement Date. Upon the Effective Date, the terms and provisions hereof shall be fully binding on Landlord and Tenant. The Term of this Lease shall commence on the Commencement Date. Unless sooner terminated or extended as may be hereinafter provided, the Term shall end on the Expiration Date. If Landlord does not tender possession of the Premises to Tenant on or before any particular date, for any reason whatsoever, Landlord shall not be liable for any damage thereby, this Lease shall not be void or voidable thereby, and the Term shall not commence until the Commencement Date, subject to the terms of this Section 2.2 below. Landlord shall be deemed to have tendered possession of the Premises to Tenant upon the giving of notice by Landlord to Tenant stating that the Premises are vacant, in the condition required by this Lease and available for Tenant's occupancy. Except as set forth in Section 2.2, below, no failure to tender possession of the Premises to Tenant on or before any particular date shall affect any other obligations of Tenant hereunder. There shall be no postponement of the Commencement Date for (i) any delay in the tender of possession to Tenant which results from any Tenant Delay or (ii) any delays by Landlord in the performance of any punch list items relating to the construction of the Tenant Improvements. At any time during the Term, Landlord may deliver to Tenant a notice in the form as set forth in Exhibit G, attached hereto, as a confirmation only of the information set forth therein, which Tenant shall execute and return to Landlord within ten (10) days of receipt thereof; provided, however, Tenant's failure to execute and return such notice to Landlord within such time shall be conclusive upon Tenant that the information set forth in such notice is as specified therein.

Landlord shall use commercially reasonable efforts to cause the Premises to be Ready for Occupancy on or before April 1, 2019, provided that this Lease is fully executed and delivered by Landlord and Tenant on or before September 30, 2018.

Notwithstanding anything to the contrary set forth herein, but subject to the terms of this provision below, in the event that the Tenant Improvements are comprised of general office improvements, and Landlord fails to cause the Premises to be Ready for Occupancy on or before May 1, 2019 (the "Rent Credit Date") for any reason other than an Unavoidable Delay or a Tenant Delay, then Tenant shall be entitled to an abatement of one (1) day of Fixed Rent attributable to the Premises for the number of days commencing as of the day immediately following the Rent Credit Date and continuing through the date that the Premises are Ready for Occupancy. In the event that Tenant Improvements are not comprised of general office improvements, then the Rent Credit Date shall be July 1, 2019. In the event that Tenant is entitled to an abatement of Fixed Rent pursuant to the terms of this Section 2.2, such abatement of Fixed Rent shall be credited towards Tenant's obligation to pay Fixed Rent for the Premises commencing as of the day immediately following the expiration of the seventh (7th) month of the Term. Tenant's right to an abatement of Fixed Rent as set forth in this Section 2.2 shall be Tenant's sole and exclusive remedy at law or in equity for Landlord's failure to cause the Premises to be Ready for Occupancy on or prior to the Rent Credit Date. The Rent Credit Date shall be extended on a day-for-day basis to the extent of any Unavoidable Delay, any Tenant Delay or in the event that the Lease is not fully executed and delivered by Landlord and Tenant on or before September 30, 2018.

|

789956.06/WLA 377061-00006/sb/sb |

|

Arboretum Courtyard [Catasys, Inc.] |

Notwithstanding anything to the contrary set forth herein, in the event that Landlord fails to cause the Premises to be Ready for Occupancy on or before the date that is one (1) year following the full execution and delivery of this Lease (the "Outside Date") for any reason other than an Unavoidable Delay or a Tenant Delay, then, except as set forth above, the sole remedy of Tenant for such failure shall be the right to deliver a notice to Landlord (a "Election Notice") electing to terminate this Lease effective upon the date occurring ten (10) Business Days following receipt by Landlord of the Election Notice (the "Effective Termination Date"). The Election Notice must be delivered by Tenant to Landlord, if at all, not earlier than the Outside Date (as the same may be extended pursuant to the terms below) nor later than ten (10) Business Days after the Outside Date. In the event that Tenant fails to deliver to Landlord the Election Notice within ten (10) Business Days following the Outside Date, then Tenant shall be deemed to have waived its right to terminate the Lease pursuant to the terms of this Section 2.2. The Outside Date shall be extended to the extent of any Unavoidable Delay or any Tenant Delay. Upon any termination as set forth in this Section 2.2, Landlord and Tenant shall be relieved from any and all liability to each other resulting hereunder except that Landlord shall return to Tenant any prepaid rent or any Security Deposit (to the extent the same has been paid by Tenant to Landlord).

Section 2.3 Payment of Rent.

(a) In General. Tenant shall pay to Landlord, without notice or demand, and without any set-off, counterclaim, abatement or deduction whatsoever, except as may be expressly set forth in this Lease, in lawful money of the United States by wire transfer of funds, (i) Fixed Rent in equal monthly installments, in advance, on the first (1st) day of each month during the Term, commencing on the Commencement Date, and (ii) Additional Rent, at the times and in the manner set forth in this Lease.

(b) Abated Fixed Rent. Notwithstanding any provision to the contrary contained in the Lease, Tenant shall be entitled to an abatement of the entirety of the Fixed Rent due for the second (2nd) through sixth (6th) full calendar months of the initial Term (the "Fixed Rent Abatement Period"). The amount Fixed Rent abated under the terms of this Section 2.3(b) shall be referred to herein as the "Fixed Rent Abatement Amount". Landlord and Tenant acknowledge that Tenant's right (the "Fixed Rent Abatement Right") to receive Fixed Rent abatement during the Fixed Rent Abatement Period has been granted to Tenant as additional consideration for Tenant's agreement to enter into this Lease and comply with the terms and conditions otherwise required under this Lease. If there is an Event of Default by Tenant which remains uncured beyond all applicable notice and cure periods, or if this Lease is terminated for any reason other than in connection with a Landlord default, casualty or condemnation, then, in addition to any other remedies Landlord may have under this Lease, Landlord, at its option, may elect any or all of the following remedies: (i) Tenant's right to receive Fixed Rent abatement under this paragraph shall automatically be deemed terminated and of no further force or effect; or (ii) the unexpired portion of the Fixed Rent Abatement Period as of such Event of Default or termination shall be moved to the end of the initial Term, and Tenant shall immediately be obligated to begin paying Fixed Rent at the full amounts of the monthly installments therefor set forth above. The Fixed Rent Abatement Right set forth in this Section 2.3(b) shall be personal to the originally named Tenant hereunder (the "Original Tenant") and a Permitted Transferee Assignee (defined in Section 13.8(a), below) and shall not inure to the benefit of any other assignee, or any sublessee or other transferee of the Original Tenant's interest in this Lease. Tenant shall have the right by delivery of written notice to Landlord to convert any portion of the Fixed Rent Abatement Amount to the Tenant Improvement Allowance.

Section 2.4 First Month's Rent. Tenant shall pay one (1) month's Fixed Rent upon the execution of this Lease ("Advance Rent"). If the Commencement Date is on the first (1st) day of a month, the Advance Rent shall be credited towards the first (1st) month's Fixed Rent payment. If the Commencement Date is not the first (1st) day of a month, then on the Commencement Date Tenant shall pay Fixed Rent for the period from the Commencement Date through the last day of such month, and the Advance Rent shall be credited towards Fixed Rent for the next succeeding calendar month.

|

789956.06/WLA 377061-00006/sb/sb |

|

Arboretum Courtyard [Catasys, Inc.] |

Section 2.5 Renewal Term.

(a) Renewal Term. The Original Tenant and a Permitted Transferee Assignee, as the case may be, shall have the right to renew the initial Term for all of the Premises for one renewal term of five (5) years (the “Renewal Term”) commencing on the day after the expiration of the initial Term (the “Renewal Term Commencement Date”) and ending on the day immediately preceding the fifth (5th) anniversary of the Renewal Term Commencement Date, unless the Renewal Term shall sooner terminate pursuant to any of the terms of this Lease or otherwise. The Renewal Term shall commence only if (i) Tenant notifies Landlord in writing (the “Exercise Notice”) of Tenant’s exercise of such renewal right not earlier than fourteen (14) months, and not later than nine (9) months, prior to the Expiration Date, (ii) at the time of the exercise of such right and immediately prior to the Renewal Term Commencement Date, no default by Tenant under this Lease shall have occurred and be continuing hereunder, (iii) Tenant occupies the entire Premises at the time the Exercise Notice is given and immediately prior to the Renewal Term Commencement Date, and (iv) Tenant exercises its renewal option, if at all, with respect to all of the Premises. Time is of the essence with respect to the giving of the Exercise Notice. The Renewal Term shall be upon all of the agreements, terms, covenants and conditions of this Lease, except that (a) the Rent for the Renewal Term shall be determined as provided in Section 2.5(b) below and (b) if Tenant exercises the renewal option set forth in this Section 2.5, then Tenant shall have no further right to renew the Term unless otherwise agreed to in writing by Landlord and Tenant. Upon the commencement of the Renewal Term, (1) the Renewal Term shall be added to and become part of the Term, (2) any reference to “this Lease”, to the “Term”, the “term of this Lease” or any similar expression shall be deemed to include the Renewal Term and (3) the expiration date of the Renewal Term shall become the Expiration Date. Any termination, cancellation or surrender of the entire interest of Tenant under this Lease at any time during the Term shall automatically terminate the renewal right set forth in this Section 2.5. The rights contained in this Section 2.5 shall be personal to Original Tenant and a Permitted Transferee Assignee, as the case may be, and may only be exercised by Original Tenant or a Permitted Transferee Assignee, as the case may be (and not any other assignee, or any sublessee or other transferee of Original Tenant’s interest in this Lease).

(b) Renewal Term Rent; Fair Market Value. The annual Rent payable during the Renewal Term shall be equal to the annual Fair Market Value (as hereinafter defined) of the Premises as of commencement of the Renewal Term (the “Calculation Date”). “Fair Market Value” shall mean the fair market annual rent (including additional rent and considering any “base year” or “expense stop” applicable thereto), taking into account all escalations, at which, as of the Calculation Date, tenants are leasing non-sublease, non-encumbered, non-equity, non-expansion space comparable in size, location and quality to the Premises for a term equal to the Renewal Term, in an arm’s-length transaction, which comparable space is located in the Project and/or in the Comparable Buildings, and which comparable transactions (collectively, the “Comparable Transactions”) are entered into within the six (6) month period immediately preceding Landlord’s delivery of the Rent Notice (as hereinafter defined) to Tenant, taking into consideration the following concessions (the “Concessions”): (i) rental abatement concessions, if any, being granted such tenants in connection with such comparable space; (ii) tenant improvements or allowances provided or to be provided for such comparable space, taking into account, and deducting the value of, the existing improvements in the Premises, such value to be based upon the age, condition, design, quality of finishes and layout of the improvements and the extent to which the same can be utilized by Tenant based upon the fact that the precise tenant improvements existing in the Premises are specifically suitable to Tenant; and (iii) other reasonable monetary concessions being granted such tenants in connection with such comparable space; provided, however, that in calculating the Fair Market Value, no consideration shall be given to (A) the fact that Landlord is or is not required to pay a real estate brokerage commission in connection with Tenant’s exercise of its right to lease the Premises during the Renewal Term or in connection with the Comparable Transactions or the fact that landlords are or are not paying real estate brokerage commissions in connection with such comparable space, and (B) any period of rental abatement, if any, granted to tenants in Comparable Transactions in connection with the design, permitting and construction of tenant improvements in such comparable spaces. The determination of Fair Market Value shall additionally include a determination (the “Financial Security Determination”) as to whether, and if so to what extent, Tenant must provide Landlord with financial security, such as a letter of credit or guaranty, for Tenant’s rent obligations in connection with Tenant’s lease of the Premises during the Renewal Term. In connection with the foregoing, as part of determining the Fair Market Rent, such determination shall be made by reviewing the extent of financial security then generally being imposed in Comparable Transactions from tenants of comparable financial condition and credit history to the then existing financial condition and credit history of Tenant (with appropriate adjustments to account for differences in the then-existing financial condition of Tenant and such other tenants). Landlord shall advise Tenant (the “Rent Notice”) of Landlord's determination of the Fair Market Value of the Premises for the Renewal Term at least forty-five (45) days prior to the Renewal Term Commencement Date. If Tenant timely disputes Landlord’s determination of Fair Market Value in accordance with Section 2.5(c) below, then the dispute shall be resolved by arbitration as provided in Section 2.5(c) below. If the Rent payable during the Renewal Term is not determined prior to the Renewal Term Commencement Date, then Tenant shall pay Rent in an amount equal to the Fair Market Value for the Premises as set forth in the Rent Notice (the "Interim Rent"). Upon final determination of the Rent for the Renewal Term, Tenant shall commence paying such Rent as so determined, and within ten (10) days after such determination Tenant shall pay any deficiency in prior payments of Rent or, if the Rent as so determined shall be less than the Interim Rent, Tenant shall be entitled to a credit against the next succeeding installments of Rent in an amount equal to the difference between each installment of Interim Rent and the Rent as so determined that should have been paid for such installment until the total amount of the over payment has been recouped.

|

789956.06/WLA 377061-00006/sb/sb |

|

Arboretum Courtyard [Catasys, Inc.] |

(c) Arbitration. If Tenant wishes to dispute Landlord’s determination of Fair Market Value of the Premises for the Renewal Term pursuant to Section 2.5(b) above, then Tenant shall give notice to Landlord of such dispute within thirty (30) days after delivery of the Rent Notice and such dispute thereafter shall be determined as follows:

(i) In its demand for arbitration, Tenant shall specify the name and address of the person to act as the arbitrator on Tenant’s behalf. The arbitrator shall be a real estate broker with at least ten (10) years full-time commercial brokerage experience who is familiar with the Fair Market Value of first-class office space in the Project and the Comparable Buildings. Failure on the part of Tenant to make the timely and proper demand for such arbitration where such failure continues for three (3) Business Days after Landlord delivers a notice to Tenant shall constitute a waiver of the right thereto and the Rent shall be as set forth in the Rent Notice. Within ten (10) Business Days after the service of the demand for arbitration, Landlord shall give notice to Tenant specifying the name and address of the person designated by Landlord to act as arbitrator on its behalf, which arbitrator shall be similarly qualified. If Landlord fails to notify Tenant of the appointment of its arbitrator within such ten (10) Business Day period, and such failure continues for three (3) Business Days after Tenant delivers a second notice to Landlord, then the arbitrator appointed by Tenant shall be the arbitrator to determine the Fair Market Value for the Premises.

(ii) If two arbitrators are chosen pursuant to Section 2.5(c)(i) above, the arbitrators so chosen shall meet within ten (10) Business Days after the second arbitrator is appointed and shall seek to reach agreement on Fair Market Value. If within twenty (20) Business Days after the second arbitrator is appointed the two arbitrators are unable to reach agreement on Fair Market Value then the two arbitrators shall appoint a third arbitrator, who shall be a competent and impartial person with qualifications similar to those required of the first two arbitrators pursuant to Section 2.5(c)(i) above. If the arbitrators are unable to agree upon such appointment within five (5) Business Days after expiration of such twenty (20) Business Day period, the third arbitrator shall be selected by the parties themselves. If the parties do not agree on the third arbitrator within five (5) Business Days after expiration of the foregoing five (5) Business Day period, then either party, on behalf of both, may request appointment of such a qualified person under the provisions of the American Arbitration Association, but subject to the instructions set forth in this Section 2.5(c). The third arbitrator shall decide the dispute, if it has not been previously resolved, by following the procedures set forth in Section 2.5(c)(iii) below. Each party shall pay the fees and expenses of its respective arbitrator and both shall share the fees and expenses of the third arbitrator. Attorneys’ fees and expenses of counsel and of witnesses for the respective parties shall be paid by the respective party engaging such counsel or calling such witnesses.

|

789956.06/WLA 377061-00006/sb/sb |

|

Arboretum Courtyard [Catasys, Inc.] |

(iii) Fair Market Value shall be fixed by the third arbitrator in accordance with the following procedures. Concurrently with the appointment of the third arbitrator, each of the arbitrators selected by the parties shall state, in writing, his or her determination of the Fair Market Value supported by the reasons therefor. The third arbitrator shall have the right to consult experts and competent authorities for factual information or evidence pertaining to a determination of Fair Market Value, but any such determination shall be made in the presence of both parties with full right on their part to cross-examine. The third arbitrator shall conduct such hearings and investigations as he or she deems appropriate and shall, within thirty (30) days after being appointed, select which of the two proposed determinations most closely approximates his or her determination of Fair Market Value. The third arbitrator shall have no right to propose a middle ground or any modification of either of the two proposed determinations. The determination he or she chooses as that most closely approximating his or her determination of the Fair Market Value shall constitute the decision of the third arbitrator and shall be final and binding upon the parties. The third arbitrator shall render the decision in writing with counterpart copies to each party. The third arbitrator shall have no power to add to or modify the provisions of this Lease. Promptly following receipt of the third arbitrator’s decision, the parties shall enter into an amendment to this Lease, evidencing the extension of the Term for the Renewal Term and confirming the Rent for the Renewal Term, but the failure of the parties to do so shall not affect the effectiveness of the third arbitrator’s determination.

(iv) In the event of a failure, refusal or inability of any arbitrator to act, his or her successor shall be appointed by him or her, but in the case of the third arbitrator, his or her successor shall be appointed in the same manner as that set forth herein with respect to the appointment of the original third arbitrator.

ARTICLE 3

USE AND OCCUPANCY

Section 3.1 In General. Tenant shall use and occupy the Premises for the Permitted Uses and for no other purpose. Tenant shall not use or occupy or permit the use or occupancy of any part of the Premises in a manner constituting a Prohibited Use. Tenant further covenants and agrees that Tenant shall not use, or suffer or permit any person or persons to use, the Premises or any part thereof for any use or purpose contrary to the provisions of the Rules and Regulations set forth in Exhibit F, attached hereto, or in violation of any applicable Requirements. Tenant shall not do or permit anything to be done in or about the Premises, (including, without limitation, the installation or use of any Alterations (defined in Section 5.1, below), Equipment defined in Section 5.7, below) or any other furniture, fixture and equipment, in the Premises), which will in any way damage the reputation of the Building, be offensive or objectionable to Landlord or other occupants of the Building, or obstruct or interfere with the rights of other tenants or occupants of the Building, or injure or annoy them by reason of noise, odors, or vibrations. If Tenant uses the Premises for a purpose constituting a Prohibited Use, violating any Requirement or the terms of this Article 3, or causing the Building or Project to be in violation of any Requirement or the terms of this Article 3, then Tenant shall promptly discontinue such use upon notice of such violation. Tenant, at its expense, shall procure and at all times maintain and comply with the terms and conditions of all licenses and permits required for the lawful conduct of the Permitted Uses in the Premises.

|

789956.06/WLA 377061-00006/sb/sb |

|

Arboretum Courtyard [Catasys, Inc.] |

Section 3.2 Permitted Dogs. Notwithstanding any provision to the contrary in this Lease, Tenant shall be permitted during the initial Term and any Renewal Term to bring into the Premises fully-domesticated, fully-vaccinated, trained dogs owned by Tenant's employees as pets ("Permitted Dogs"), subject to the terms and conditions of this Section 3.2; provided, however, that Tenant shall be permitted to bring only two (2) Permitted Dogs on the Project at any one time. In no event shall Tenant permit any Dangerous Breeds (as defined below) or dogs weighing in excess of approximately one hundred twenty-five (125) pounds to enter the Premises, the Building or the Project. For the purposes herein, "Dangerous Breeds" shall mean the following breeds: Pit Bull Terrier, Rottweiler, Boxer, Chow, Presa Canario, German Shepherd, Alaskan Malamute, Husky and Doberman Pinscher. Landlord shall have the right, from time to time, to reasonably modify or add to the definition of Dangerous Breeds. All Permitted Dogs shall be strictly controlled at all times and shall not be permitted to foul, damage or otherwise mar any part of the Premises, the Building or the Project, or bark excessively or otherwise create a nuisance at the Project. The Permitted Dogs shall be on a leash at all times that they are not within the Premises, and shall not be allowed in the Project Parking Facility or in the Common Areas, except en route to and from the Premises. The Permitted Dogs shall be taken off the Project for their walks and shall not be permitted to excrete waste within the Premises, Building or Project. Upon Landlord's request at any time, and from time to time, Tenant shall provide Landlord with evidence of all current vaccinations and current flea treatment for Permitted Dogs. Tenant shall be responsible for any additional cleaning costs and all other costs which may arise from the presence of the Permitted Dogs in or on the Project in excess of the costs that would have been incurred had the Permitted Dogs not been allowed in or on the Project; and Tenant shall immediately remove any waste and excrement of any Permitted Dogs from the Project and properly clean the affected area. In no event shall any of the Permitted Dogs be kept in the Premises overnight. Tenant shall be responsible for, and shall indemnify, defend, protect and hold Landlord and the Indemnitees harmless from and against any and all Losses arising from, resulting from or connected with the acts or presence of the Permitted Dogs in the Premises or Building or on the Project (including, without limitation, bodily injury to persons in the Premises or Building or on the Project or property damage to the property of Landlord or any other tenant, subtenant, occupant, licensee or invitee of the Building or Project). Tenant shall provide Landlord with evidence reasonably satisfactory to Landlord that Tenant's insurance provided pursuant to Section 11.1 of this Lease covers dog-related injuries and damage. Tenant shall comply with all applicable Requirements associated with or governing the presence of the Permitted Dogs within the Premises or the Building or on the Project, and such presence shall not violate the certificate of occupancy for the Building. Notwithstanding the foregoing, Landlord shall have the right at any time to rescind Tenant's right to have any dogs in the Premises (other than seeing eye dogs, service dogs, assistance dogs, or emotional support dog in accordance with the Rules and Regulations and applicable Requirements), if (1) Tenant is in violation of one or more of the terms and conditions set forth in this Section 3.2 and fails to cure such violation within two (2) Business Days of receiving notice thereof from Landlord, or (2) Landlord has received three (3) or more complaints in any twelve (12)-month period from other tenants in the Building regarding any damage, disruption or nuisance caused by Tenant's Permitted Dogs in the Building or on the Project, which complaints are, in the Landlord's reasonable business judgment, are legitimate and not intended solely to harass or frustrate Tenant's use and occupancy of the Premises. If Tenant sublets all or any portion of the Premises (other than to a Permitted Transferee Assignee), then, as to such portion of the Premises sublet, upon such subletting and until the expiration of such sublease, the right to bring Tenant's Permitted Dogs into such portion of the Premises shall terminate and be of no further force or effect.

ARTICLE 4

CONDITION OF THE PREMISES

Tenant has inspected the Premises and agrees, except as otherwise specifically provided in the Tenant Work Letter, (a) to accept possession of the Premises in the condition existing on the Commencement Date "as is", and (b) that, except for the Tenant Improvement Allowance, Landlord has no obligation to perform any work, supply any materials, incur any expense or make any alterations or improvements to prepare the Premises for Tenant's occupancy. Tenant's occupancy of any part of the Premises shall be conclusive evidence, as against Tenant, that Landlord has Substantially Completed any work to be performed by Landlord under this Lease, Tenant has accepted possession of the Premises in its then current condition and at the time such possession was taken, the Premises, the Building and the Project were in a good and satisfactory condition as required by this Lease. Landlord shall deliver the Building Systems serving the Premises in good working order and condition.

ARTICLE 5

ALTERATIONS

Section 5.1 Tenant's Alterations.

(a) Tenant shall have the right, without Landlord’s prior written consent, but upon five (5) Business Days prior written notice to Landlord (which notice shall contain a description of the contemplated work), to make strictly cosmetic, non-structural additions and alterations, such as painting, wall coverings and floor coverings, to the Premises that (i) do not involve the expenditure of more than One Hundred Thousand and No/100 Dollars ($100,000.00) in the aggregate in any twelve (12) month period, and (ii) do not contain a Design Problem (defined below) (the foregoing additions and alterations described in this sentence are collectively referred to herein as “Decorative Alterations”). Except in connection with Decorative Alterations, Tenant shall not make any alterations, additions or other physical changes in or about the Premises (collectively, "Alterations"), without Landlord's prior consent, which consent shall not be unreasonably withheld, provided, that it shall be deemed reasonable for landlord to withhold its consent to any Alterations that contain a Design Problem. A "Design Problem" is defined as and will be deemed to exist if any Alterations (i) are structural or adversely affect any Building Systems, (ii) are visible from outside of the Premises, (iii) affect the certificate of occupancy issued for the Building or the Premises, and (iv) violate any Requirement.

|

789956.06/WLA 377061-00006/sb/sb |

|

Arboretum Courtyard [Catasys, Inc.] |

(b) Plans and Specifications. Prior to making any Alterations, Tenant, at its expense, shall (i) submit to Landlord for its approval, detailed plans and specifications ("Plans") of each proposed Alteration (other than Decorative Alterations), and with respect to any Alteration affecting any Building System, evidence that the Alteration has been designed by, or reviewed and approved by, Landlord's designated engineer for the affected Building System, (ii) obtain all permits, approvals and certificates required by any Governmental Authorities, (iii) furnish to Landlord duplicate original policies or certificates of worker's compensation (covering all persons to be employed by Tenant, and Tenant's contractors and subcontractors in connection with such Alteration) and commercial general liability (including property damage coverage) and business auto insurance and Builder's Risk coverage (as described in Article 11) all in such form, with such companies, for such periods and in such amounts as Landlord may reasonably require, naming Landlord, Landlord's Agent, any Lessor and any Mortgagee as additional insureds, and (iv) furnish to Landlord reasonably satisfactory evidence of Tenant's ability to complete and to fully pay for such Alterations (other than Decorative Alterations). Tenant shall give Landlord not less than five (5) Business Days' notice prior to performing any Decorative Alteration, which notice shall contain a description of such Decorative Alteration.

(c) Governmental Approvals. Tenant, at its expense, shall, as and when required, promptly obtain certificates of partial and final approval of such Alterations required by any Governmental Authority and shall furnish Landlord with copies thereof, together with "as-built" Plans for such Alterations prepared on an AutoCAD Computer Assisted Drafting and Design System (or such other system or medium as Landlord may reasonably accept), using naming conventions issued by the American Institute of Architects in June, 1990 (or such other naming conventions as Landlord may accept) and magnetic computer media of such record drawings and specifications translated in DFX format or another format acceptable to Landlord.

Section 5.2 Manner and Quality of Alterations. All Alterations shall be performed (a) in a good and workmanlike manner and free from defects, (b) substantially in accordance with the Plans, and by contractors reasonably by Landlord, provided that Tenant shall retain the contractors designated by Landlord to perform any structural, mechanical, electrical, plumbing, HVAC, life safety and sprinkler work, provided that their rates are competitive in the marketplace, (c) in compliance with all Requirements, the terms of this Lease and all construction procedures and regulations then prescribed by Landlord, and (d) at Tenant's expense. All materials and equipment shall be of first quality and at least equal to the applicable standards for the Building then established by Landlord, and no such materials or equipment (other than Tenant's Property) shall be subject to any lien or other encumbrance. Upon completion of any Alterations hereunder, Tenant shall provide Landlord with copies of all construction contracts, proof of payment for all labor and materials, and final unconditional waivers of lien from all contractors, subcontractors, materialmen, suppliers and others having lien rights with respect to such Alterations, in the form prescribed by California law. In addition, Tenant shall cause a Notice of Completion to be recorded in the Office of the Recorder of the county in which the Project is located in accordance with Section 8182 of the Civil Code of the State of California or any successor statute.

Section 5.3 Removal of Tenant's Property. Tenant's Property shall remain the property of Tenant and Tenant may remove the same at any time on or before the Expiration Date. On or before the Expiration Date, Tenant shall, unless otherwise directed by Landlord, at Tenant's expense, remove any Specialty Alterations and close up any slab penetrations in the Premises. Tenant shall repair and restore, in a good and workmanlike manner, any damage to the Premises, the Building or the Project caused by Tenant's removal of any Alterations or Tenant's Property or by the closing of any slab penetrations, and upon default thereof, Tenant shall reimburse Landlord for Landlord's cost of repairing and restoring such damage. Any Specialty Alterations or Tenant's Property not so removed shall be deemed abandoned and Landlord may retain or remove and dispose of same, and repair and restore any damage caused thereby, at Tenant's cost and without accountability to Tenant. All other Alterations shall become Landlord's property upon termination of this Lease.

|

789956.06/WLA 377061-00006/sb/sb |

|

Arboretum Courtyard [Catasys, Inc.] |

Section 5.4 Mechanic's Liens. Tenant, at its expense, shall discharge any lien or charge recorded or filed against the Project in connection with any work done or claimed to have been done by or on behalf of, or materials furnished or claimed to have been furnished to, Tenant, within fifteen (15) days after Tenant's receipt of notice thereof by payment, filing the bond required by law or otherwise in accordance with applicable Requirements.

Section 5.5 Labor Relations. Tenant shall not employ, or permit the employment of, any contractor, mechanic or laborer, or permit any materials to be delivered to or used in the Building, if, in Landlord's sole judgment, such employment, delivery or use will interfere or cause any conflict with other contractors, mechanics or laborers engaged in the construction, maintenance or operation of the Building by Landlord, Tenant or others. If such interference or conflict occurs based upon a good faith determination by Landlord, then upon Landlord's request, Tenant shall cause all contractors, mechanics or laborers causing such interference or conflict to leave the Building immediately.

Section 5.6 Tenant's Costs. Tenant shall pay to Landlord, upon demand, all reasonable out-of-pocket costs actually incurred by Landlord in connection with Tenant's Alterations, including costs incurred in connection with (a) Landlord's review of the Alterations (including review of requests for approval thereof) and (b) the provision of Building personnel during the performance of any Alteration, to operate elevators or otherwise to facilitate Tenant's Alterations. In addition, Tenant shall pay to Landlord, upon demand, an administrative fee in an amount equal to three percent (3%) of the total cost of any Alterations. At Landlord's request, Tenant shall deliver to Landlord reasonable supporting documentation evidencing the hard and soft costs incurred by Tenant in designing and constructing any Alterations.

Section 5.7 Tenant's Equipment. Tenant shall provide notice to Landlord prior to moving any heavy machinery, heavy equipment, freight, bulky matter or fixtures (collectively, "Equipment") into or out of the Building and shall pay to Landlord any costs actually incurred by Landlord in connection therewith. If such Equipment requires special handling, Tenant agrees (a) to employ only persons holding all necessary licenses to perform such work, (b) all work performed in connection therewith shall comply with all applicable Requirements and (c) such work shall be done only during hours designated by Landlord.

Section 5.8 Compliance. The approval of Plans, or consent by Landlord to the making of any Alterations, does not constitute Landlord's representation that such Plans or Alterations comply with any Requirements or the terms of Article 3 of this Lease (i.e., that the same shall not obstruct or interfere with the rights of other tenants or occupants of the Building, or injure or annoy them by reason of noise, odors, or vibrations). Landlord shall not be liable to Tenant or any other party in connection with Landlord's approval of any Plans, or Landlord's consent to Tenant's performing any Alterations, and Tenant's waiver and indemnity set forth in this Lease shall specifically apply to the Plans or Alterations. If any Alterations made by or on behalf of Tenant require Landlord to make any alterations or improvements to any part of the Building or Project in order to comply with any Requirements, Tenant shall pay all costs and expenses incurred by Landlord in connection with such alterations or improvements.

Section 5.9 Floor Load. Tenant shall not place a load upon any floor of the Premises that exceeds 100 pounds per square foot "live load". Landlord reserves the right to reasonably designate the position of all Equipment which Tenant wishes to place within the Premises, and to place limitations on the weight thereof.

|

789956.06/WLA 377061-00006/sb/sb |

|

Arboretum Courtyard [Catasys, Inc.] |

ARTICLE 6

REPAIRS

Section 6.1 Landlord's Repair and Maintenance. Landlord shall operate, maintain and, except as provided in Section 6.2 hereof, make all necessary repairs (both structural and nonstructural) to (i) the Base Building and (ii) the Common Areas, in conformance with standards applicable to Comparable Buildings. For purposes of this Lease, the “Base Building” shall include, but not be limited, to the following: (a) roof structure and membrane; (b) exterior walls and glass; (c) floor/ceiling slabs and other structural portions of the Building, including, without limitation, the foundation, curtain wall, exterior glass, and mullions, columns, beams, shafts (including elevator shafts); and (d) Building Systems.

Section 6.2 Tenant's Repair and Maintenance. Tenant shall promptly, at its expense and in compliance with Article 5 including, without limitation, the requirement that any repairs affecting any Building System be reviewed and approved by Landlord's designated engineer for the affected Building System, make all nonstructural repairs to the Premises and the fixtures, equipment and appurtenances therein (including all electrical, plumbing, heating, ventilation and air conditioning, sprinklers and life safety systems in and serving the Premises from the point of connection to the Building Systems) (collectively, "Tenant Fixtures") as and when needed to preserve the Premises in good working order and condition, except for reasonable wear and tear and damage which is Landlord's obligation to repair pursuant to the express provisions of this Lease. All damage to the Building or to any portion thereof, or to any Tenant Fixtures, requiring structural or nonstructural repair caused by or resulting from any act, omission, neglect or improper conduct of a Tenant Party or the moving of Tenant's Property or Equipment into, within or out of the Premises by a Tenant Party, shall be repaired at Tenant's expense by (i) Tenant, if the required repairs are nonstructural in nature and do not affect any Building System, or (ii) Landlord, if the required repairs are structural in nature, involve replacement of exterior window glass or affect any Building System. All Tenant repairs shall be of good quality utilizing new construction materials.

Section 6.3 Reserved Rights. Landlord reserves the right to make all changes, alterations, additions, improvements, repairs or replacements to the Building and/or the Project, including the Building Systems, including changing the arrangement or location of entrances or passageways, doors and doorways, corridors, elevators, stairs, toilets or other Common Areas (collectively, "Work of Improvement"), as Landlord deems necessary or desirable, and to take all materials into the Premises required for the performance of such Work of Improvement, provided that (a) the level of any Building service shall not decrease in any material respect from the level required of Landlord in this Lease as a result thereof (other than temporary changes in the level of such services during the performance of any such Work of Improvement), (b) Tenant is not deprived of access to the Premises, and (c) any Work of Improvement does not otherwise materially and adversely impact Tenant’s rights under this Lease. Landlord shall use reasonable efforts to minimize interference with Tenant's use and occupancy of the Premises during the performance of such Work of Improvement. There shall be no Rent abatement or allowance to Tenant for a diminution of rental value, no actual or constructive eviction of Tenant, in whole or in part, no relief from any of Tenant's other obligations under this Lease, and no liability on the part of Landlord by reason of inconvenience, annoyance or injury to business arising from Landlord, Tenant or others performing, or failing to perform, any Work of Improvement.

ARTICLE 7

INCREASES IN TAXES AND OPERATING EXPENSES

Section 7.1 Definitions. For the purposes of this Article 7, the following terms shall have the meanings set forth below:

(a) "Assessed Valuation" shall mean the amount for which the Project is assessed by the County Assessor of Los Angeles, California, for the purpose of imposition of Taxes.

|

789956.06/WLA 377061-00006/sb/sb |

|

Arboretum Courtyard [Catasys, Inc.] |

(b) "Base Operating Expenses" shall mean the Operating Expenses for the Base Year.

(c) "Base Taxes" shall mean the Taxes payable for the Base Year.

(d) "Comparison Year" shall mean each calendar year commencing subsequent to the Base Year in which all or any portion of the Term falls, through and including the calendar year in which the Term expires.

(e) "Operating Expenses" shall mean the aggregate of all costs and expenses paid or incurred by or on behalf of Landlord in connection with the ownership, operation, repair and maintenance of the Project, including the rental value (at customary market rates) of Landlord's Building office and capital improvements incurred after the Base Year only if such capital improvement either (i) is reasonably intended to result in a reduction in Operating Expenses (as for example, a labor-saving improvement), provided the amount included in Operating Expenses in any Comparison Year shall not exceed an amount equal to the savings reasonably anticipated to result from the installation and operation of such improvement, and/or (ii) is made during any Comparison Year in compliance with Requirements, except for such capital improvements to remedy a condition existing prior to the date hereof, which a federal, state, or municipal Governmental Authority, if it had knowledge of such condition prior to the date hereof, would have then required to be remedied pursuant to the then-current Requirements in their form existing as of the date hereof. Such capital improvements shall be amortized (with interest at the Base Rate) on a straight-line basis over such period as Landlord shall reasonably determine in accordance with sound real estate management and accounting principles consistently applied, and the amount included in Operating Expenses in any Comparison Year shall be equal to the annual amortized amount. Operating Expenses shall not include any Excluded Expenses. If during all or part of the Base Year or any Comparison Year, Landlord shall not furnish any particular item(s) of work or service (which would otherwise constitute an Operating Expense) to any occupable portions of the Project for any reason, then, for purposes of computing Operating Expenses for such period, the amount included in Operating Expenses for such period shall be increased by an amount equal to the costs and expenses that would have been reasonably incurred by Landlord during such period if Landlord had furnished such item(s) of work or service to such portion of the Project. Landlord shall exclude from Operating Expenses for the Base Year any non-recurring items. If Landlord eliminates from Operating Expenses for any Comparison Year a recurring category of expenses previously included in Operating Expenses for the Base Year, Landlord may subtract such category from Operating Expenses for the Base Year commencing with such Comparison Year. Without limiting the generality of the foregoing, if Landlord eliminates from Operating Expenses for any Comparison Year any particular type of insurance included in Operating Expenses for the Base Year, or if Landlord reduces the level of insurance coverage during any Comparison Year from that carried during the Base Year, then Landlord may adjust the amount of any insurance premium included in Operating Expenses for the Base Year to equal that amount which Landlord reasonably estimates it would have incurred had Landlord maintained similar types and levels of insurance during the Base Year as maintained by Landlord during such Comparison Year. In determining the amount of Operating Expenses for the Base Year or any Comparison Year, if less than ninety-five percent (95%) of the Project rentable area is occupied by tenants at any time during any such Base Year or Comparison Year, Operating Expenses that vary based on occupancy shall be determined for such Base Year or Comparison Year to be an amount equal to the like expenses which would normally be expected to be incurred had such occupancy been ninety-five percent (95%) throughout the Base Year or such Comparison Year.

Notwithstanding any provision to the contrary set forth herein, Landlord shall (a) not collect or be entitled to collect Operating Expenses from all of the tenants in the Building in an amount in excess of one hundred percent (100%) of the Operating Expenses actually paid by Landlord in connection with the operation of the Building; and (b) make no profit from Landlord's collections of Operating Expenses.

(f) "Statement" shall mean a statement containing a comparison of (i) Base Taxes and the Taxes for any Comparison Year, or (ii) Base Operating Expenses and the Operating Expenses for any Comparison Year.

|

789956.06/WLA 377061-00006/sb/sb |

|

Arboretum Courtyard [Catasys, Inc.] |

(g) "Taxes" shall mean (i) all real estate taxes, assessments, sewer and water rents, rates and charges and other governmental levies, impositions or charges, whether general, special, ordinary, extraordinary, foreseen or unforeseen (including transit taxes, leasehold taxes or taxes based upon the receipt of rent, including gross receipts or sales taxes applicable to the receipt of rent), which may be assessed, levied or imposed upon all or any part of the Project, and (ii) all expenses (including reasonable attorneys' fees and disbursements and experts' and other witnesses' fees) incurred in contesting any of the foregoing or the Assessed Valuation of the Project. Taxes shall not include (x) interest or penalties incurred by Landlord as a result of Landlord's late payment of Taxes, or (y) franchise, transfer, gift, inheritance, estate or net income taxes imposed upon Landlord. If Landlord elects to pay any assessment in annual installments, then (i) such assessment shall be deemed to have been so divided and to be payable in the maximum number of installments permitted by law, and (ii) there shall be deemed included in Taxes for each Comparison Year the installments of such assessment becoming payable during such Comparison Year, together with interest payable during such Comparison Year on such installments and on all installments thereafter becoming due as provided by law, all as if such assessment had been so divided. If at any time the methods of taxation prevailing on the Effective Date shall be altered so that in lieu of or as an addition to the whole or any part of Taxes, there shall be assessed, levied or imposed (1) a tax, assessment, levy, imposition or charge based on the income or rents received from the Project whether or not wholly or partially as a capital levy or otherwise, (2) a tax, assessment, levy, imposition or charge measured by or based in whole or in part upon all or any part of the Project and imposed upon Landlord, (3) a license fee measured by the rents, or (4) any other tax, assessment, levy, imposition, charge or license fee however described or imposed, including business improvement district impositions, then all such taxes, assessments, levies, impositions, charges or license fees or the part thereof so measured or based shall be deemed to be Taxes.

Section 7.2 Tenant's Tax Payment.

(a) If the Taxes payable for any Comparison Year exceed the Base Taxes, Tenant shall pay to Landlord Tenant's Proportionate Share of such excess ("Tenant's Tax Payment"). For each Comparison Year, Landlord shall furnish to Tenant a statement setting forth Landlord's reasonable estimate of Tenant's Tax Payment for such Comparison Year (the "Tax Estimate"). Tenant shall pay to Landlord on the first (1st) day of each month during such Comparison Year an amount equal to 1/12 of the Tax Estimate for such Comparison Year. If Landlord furnishes a Tax Estimate for a Comparison Year subsequent to the commencement thereof, then (i) until the first (1st) day of the month following the month in which the Tax Estimate is furnished to Tenant, Tenant shall pay to Landlord on the first (1st) day of each month an amount equal to the monthly sum payable by Tenant to Landlord under this Section 7.2 during the last month of the preceding Comparison Year, (ii) promptly after the Tax Estimate is furnished to Tenant or together therewith, Landlord shall give notice to Tenant stating whether the installments of Tenant's Tax Estimate previously made for such Comparison Year were greater or less than the installments of Tenant's Tax Estimate to be made for such Comparison Year in accordance with the Tax Estimate, and (x) if there shall be a deficiency, Tenant shall pay the amount thereof within ten (10) Business Days after demand therefor, or (y) if there shall have been an overpayment, Landlord shall credit the amount thereof against subsequent payments of Rent due hereunder, and (iii) on the first (1st) day of the month following the month in which the Tax Estimate is furnished to Tenant, and on the first (1st) day of each month thereafter throughout the remainder of such Comparison Year, Tenant shall pay to Landlord an amount equal to 1/12 of the Tax Estimate. Landlord shall have the right, upon not less than thirty (30) days prior written notice to Tenant, to reasonably adjust the Tax Estimate from time to time during any Comparison Year.

(b) As soon as reasonably practicable after Landlord has determined the Taxes for a Comparison Year, Landlord shall furnish to Tenant a Statement for such Comparison Year. If the Statement shall show that the sums paid by Tenant under Section 7.2(a) exceeded the actual amount of Tenant's Tax Payment for such Comparison Year, Landlord shall credit the amount of such excess against subsequent payments of Rent due hereunder or if no further payments of Rent are due hereunder, Landlord shall refund such amounts directly to Tenant. If the Statement for such Comparison Year shall show that the sums so paid by Tenant were less than Tenant's Tax Payment for such Comparison Year, Tenant shall pay the amount of such deficiency within ten (10) Business Days after delivery of the Statement to Tenant. The provisions of this Section 7.2 shall survive the expiration or earlier termination of the Term.

|

789956.06/WLA 377061-00006/sb/sb |

|

Arboretum Courtyard [Catasys, Inc.] |

(c) Only Landlord may institute proceedings to reduce the Assessed Valuation of the Project and the filings of any such proceeding by Tenant without Landlord's consent shall constitute an Event of Default. If the Taxes payable for the Base Year are reduced, the Base Taxes shall be correspondingly revised, the Additional Rent previously paid or payable on account of Tenant's Tax Payment hereunder for all Comparison Years shall be recomputed on the basis of such reduction, and Tenant shall pay to Landlord within ten (10) Business Days after being billed therefor, any deficiency between the amount of such Additional Rent previously computed and paid by Tenant to Landlord, and the amount due as a result of such recomputations. If Landlord receives a refund of Taxes for any Comparison Year, Landlord shall credit against subsequent payments of Rent due hereunder, an amount equal to Tenant's Proportionate Share of the refund, net of any expenses incurred by Landlord in achieving such refund, which amount shall not exceed Tenant's Tax Payment paid for such Comparison Year. Landlord shall not be obligated to file any application or institute any proceeding seeking a reduction in Taxes or the Assessed Valuation. The benefit of any exemption or abatement relating to all or any part of the Project shall accrue solely to the benefit of Landlord and Taxes shall be computed without taking into account any such exemption or abatement.

(d) Tenant shall be responsible for any applicable occupancy or rent tax now in effect or hereafter enacted and, if such tax is payable by Landlord, Tenant shall promptly pay such amounts to Landlord, upon Landlord's demand.

(e) Tenant shall be obligated to make Tenant's Tax Payment regardless of whether Tenant may be exempt from the payment of any Taxes as the result of any reduction, abatement or exemption from Taxes granted or agreed to by any Governmental Authority, or by reason of Tenant's diplomatic or other tax-exempt status.

Section 7.3 Tenant's Operating Payment.

(a) If the Operating Expenses payable for any Comparison Year exceed the Base Operating Expenses, Tenant shall pay to Landlord Tenant's Proportionate Share of such excess ("Tenant's Operating Payment"). For each Comparison Year, Landlord shall furnish to Tenant a statement setting forth Landlord's reasonable estimate of Tenant's Operating Payment for such Comparison Year (the "Expense Estimate"). Tenant shall pay to Landlord on the first (1st) day of each month during such Comparison Year an amount equal to 1/12 of the Expense Estimate. If Landlord furnishes an Expense Estimate for a Comparison Year subsequent to the commencement thereof, then (i) until the first (1st) day of the month following the month in which the Expense Estimate is furnished to Tenant, Tenant shall pay to Landlord on the first (1st) day of each month an amount equal to the monthly sum payable by Tenant to Landlord under this Section 7.3 during the last month of the preceding Comparison Year, (ii) promptly after the Expense Estimate is furnished to Tenant or together therewith, Landlord shall give notice to Tenant stating whether the installments of Tenant's Operating Payment previously made for such Comparison Year were greater or less than the installments of Tenant's Operating Payment to be made for such Comparison Year in accordance with the Expense Estimate, and (x) if there shall be a deficiency, Tenant shall pay the amount thereof within ten (10) Business Days after demand therefor, or (y) if there shall have been an overpayment, Landlord shall credit the amount thereof against subsequent payments of Rent due hereunder, and (iii) on the first (1st) day of the month following the month in which the Expense Estimate is furnished to Tenant, and on the first (1st) day of each month thereafter throughout the remainder of such Comparison Year, Tenant shall pay to Landlord an amount equal to 1/12 of the Expense Estimate. Landlord shall have the right, upon not less than thirty (30) days prior written notice to Tenant, to reasonably adjust the Expense Estimate from time to time during any Comparison Year.

(b) On or before May 1st of each Comparison Year, Landlord shall furnish to Tenant a Statement for the immediately preceding Comparison Year. If the Statement shows that the sums paid by Tenant under Section 7.3(a) exceeded the actual amount of Tenant's Operating Payment for such Comparison Year, Landlord shall credit the amount of such excess against subsequent payments of Rent due hereunder or if no further payments of Rent are due hereunder, Landlord shall refund such amounts directly to Tenant. If the Statement shows that the sums so paid by Tenant were less than Tenant's Operating Payment for such Comparison Year, Tenant shall pay the amount of such deficiency within ten (10) Business Days after delivery of the Statement to Tenant. The failure of Landlord to timely furnish the Statement for any Comparison Year shall not prejudice Landlord or Tenant from enforcing its rights under this Article 7. The provisions of this Section 7.3 shall survive the expiration or earlier termination of the Term.

|

789956.06/WLA 377061-00006/sb/sb |

|

Arboretum Courtyard [Catasys, Inc.] |

Section 7.4 Non-Waiver; Disputes. (a) Landlord's failure to render any Statement on a timely basis with respect to any Comparison Year shall not prejudice Landlord's right to thereafter render a Statement with respect to such Comparison Year or any subsequent Comparison Year, nor shall the rendering of a Statement prejudice Landlord's right to thereafter render a corrected Statement for that Comparison Year. Notwithstanding the foregoing, Tenant shall not be responsible for Taxes or Operating Expenses attributable to any Comparison Year which are first billed to Tenant more than eighteen (18) months after the expiration of the Term, provided that in any event Tenant shall be responsible for Taxes and Operating Expenses levied by any governmental authority or by any public utility companies at any time following the expiration of the Term which are attributable to any Comparison Year (provided that Landlord delivers to Tenant any such bill for such amounts within one (1) calendar year following Landlord’s receipt of the bill therefor).

(b) Within one hundred eighty (180) days after receipt of a Statement by Tenant, Tenant or an agent of Tenant may, after reasonable notice to Landlord, inspect Landlord’s records at Landlord’s offices in Los Angeles. Each Statement sent to Tenant shall be conclusively binding upon Tenant unless Tenant (i) pays to Landlord when due the amount set forth in such Statement, without prejudice to Tenant's right to dispute such Statement, and (ii) within one hundred eighty (180) days after such Statement is sent, sends a notice to Landlord objecting to such Statement and specifying the reasons therefor. Tenant agrees that Tenant will not employ, in connection with any dispute under this Lease, any person or entity who is to be compensated, in whole or in part, on a contingency fee basis. If the parties are unable to resolve any dispute as to the correctness of such Statement within thirty (30) days following such notice of objection, either party may refer the issues raised to a nationally recognized public accounting firm selected by Landlord and reasonably acceptable to Tenant, and the decision of such accountants shall be conclusively binding upon Landlord and Tenant. In connection therewith, Tenant and such accountants shall execute and deliver to Landlord a confidentiality agreement, in form and substance reasonably satisfactory to Landlord, whereby such parties agree not to disclose to any third party any of the information obtained in connection with such review. Tenant shall pay the fees and expenses relating to such procedure, unless such accountants determine that Landlord overstated Operating Expenses by more than five percent (5%) for such Comparison Year, in which case Landlord shall pay such fees and expenses. Except as provided in this Section 7.4, Tenant shall have no right whatsoever to dispute, by judicial proceeding or otherwise, the accuracy of any Statement.

Section 7.5 Proration. If the Commencement Date is not January 1, and provided that the Commencement Date does not occur in the Base Year, Tenant's Tax Payment and Tenant's Operating Payment for the Comparison Year in which the Commencement Date occurs shall be apportioned on the basis of the number of days in the year from the Commencement Date to the following December 31. If the Expiration Date occurs on a date other than December 31st, Tenant's Tax Payment and Tenant's Operating Payment for the Comparison Year in which such Expiration Date occurs shall be apportioned on the basis of the number of days in the period from January 1st to the Expiration Date. Upon the expiration or earlier termination of this Lease, any Additional Rent under this Article 7 shall be adjusted or paid within thirty (30) days after submission of the Statement for the last Comparison Year.

Section 7.6 No Reduction in Rent. In no event shall any decrease in Operating Expenses or Taxes in any Comparison Year below the Base Operating Expenses or Base Taxes, as the case may be, result in a reduction in the Fixed Rent or any component of Additional Rent payable hereunder.

|

789956.06/WLA 377061-00006/sb/sb |

|

Arboretum Courtyard [Catasys, Inc.] |

Section 7.7 Allocation of Operating Expenses and Taxes. Landlord shall have the right, from time to time, to equitably allocate some or all of the Operating Expenses and/or Taxes for the Project among different portions or occupants of the Project and/or the Building (the “Cost Pools”), in Landlord’s discretion. Such Cost Pools may include, but shall not be limited to, the office space tenants of the Project and/or the Building, and the retail space tenants of the Project and/or the Building. The Operating Expenses and/or Taxes allocable to each such Cost Pool shall be allocated to such Cost Pool and charged to the tenants within such Cost Pool in an equitable manner. The parties acknowledge that the Building is a part of a multi-building project and that the costs and expenses incurred in connection with the Project should be shared between the tenants of the Building and the tenants of the other buildings in the Project. Accordingly, Operating Expenses and Taxes are determined annually for the Project as a whole, and a portion of the Operating Expenses and Taxes, which portion shall be determined by Landlord on an equitable basis, shall be allocated to the tenants of the Building (as opposed to the tenants of any other buildings in the Project) and such portion shall be the Operating Expenses and Taxes for purposes of this Lease. Such portion of Operating Expenses and Taxes allocated to the tenants of the Building shall include all Operating Expenses and Taxes attributable solely to the Building and an equitable portion of the Operating Expenses and Taxes attributable to the Project as a whole.

ARTICLE 8

REQUIREMENTS OF LAW

Section 8.1 Compliance with Requirements.

(a) Tenant's Compliance. Tenant, at its expense, shall comply with all Requirements applicable to the Premises and/or Tenant's use or occupancy thereof; provided, however, that Tenant shall not be obligated to comply with any Requirements requiring any structural alterations to the Building unless the application of such Requirements arises from (i) the specific manner and/or nature of Tenant's use or occupancy of the Premises, as distinct from general office use, (ii) the Tenant Improvements or Alterations made by Tenant, or (iii) a breach by Tenant of any provisions of this Lease. Any repairs or alterations required for compliance with applicable Requirements shall be made at Tenant's expense (1) by Tenant in compliance with Article 5 if such repairs or alterations are nonstructural and do not affect any Building System, and to the extent such repairs or alterations do not affect areas outside the Premises, or (2) by Landlord if such repairs or alterations are structural or affect any Building System, or to the extent such repairs or alterations affect areas outside the Premises. If Tenant obtains knowledge of any failure to comply with any Requirements applicable to the Premises, Tenant shall give Landlord prompt notice thereof.

(b) Hazardous Materials. Tenant shall not cause or permit (i) any Hazardous Materials to be brought onto the Project, (ii) the storage or use of Hazardous Materials in or about the Building or Premises (subject to the second sentence of this Section 8.1(b)), or (iii) the escape, disposal or release of any Hazardous Materials within or in the vicinity of the Project. Nothing herein shall be deemed to prevent Tenant's use of any Hazardous Materials customarily used in the ordinary course of office work, provided such use is in accordance with all Requirements. Tenant shall be responsible, at its expense, for all matters directly or indirectly based on, or arising or resulting from the presence of Hazardous Materials at the Project which is caused or permitted by a Tenant Party. Tenant shall provide to Landlord copies of all communications received by Tenant with respect to any Requirements relating to Hazardous Materials, and/or any claims made in connection therewith. Landlord or its agents may perform environmental inspections of the Premises at any time, subject to the provisions of Section 14.1 below. Subject to and as set forth in items (r) and (s) of the definition of “Excluded Expenses” set forth in Exhibit B attached hereto, any costs incurred by Landlord in connection with any Pre-Existing Hazardous Materials (as defined in item (r) of Exhibit B) and any other Hazardous Materials brought into the Building or onto the Project after the date of this Lease by Landlord, the Indemnitees, any tenant (other than Tenant), or any other third party shall be specifically excluded from Operating Expenses. Landlord covenants that during the Term, Landlord shall comply with all Requirements relating to Hazardous Materials in accordance with, and as required by, the terms of Article 8 of this Lease.

(c) Landlord's Compliance. Landlord shall comply with (or cause to be complied with) all Requirements applicable to the Base Building and the Common Areas which are not the obligation of Tenant, to the extent that non-compliance would (i) prohibit Tenant from obtaining or maintaining a certificate of occupancy for the Premises, (ii) unreasonably and materially affect the safety of Tenant's employees or create a significant health hazard for Tenant's employees, or (iii) materially impair Tenant's use and occupancy of the Premises for the Permitted Uses. All costs incurred by Landlord in connection with this Section 8.1(c) shall be included in Operating Expenses to the extent permitted under Section 7.1 of this Lease.

|

789956.06/WLA 377061-00006/sb/sb |

|

Arboretum Courtyard [Catasys, Inc.] |

(d) Landlord's Insurance. Tenant shall not cause or permit any action or condition that would (i) invalidate or conflict with Landlord's insurance policies or be inconsistent with the recommendations of any of the issuers of such policies, (ii) violate applicable rules, regulations and guidelines of the Fire Department, Fire Insurance Rating Organization or any other authority having jurisdiction over the Building or Project, (iii) cause an increase in the premiums of insurance for the Building or Project over that payable with respect to Comparable Buildings, or (iv) result in Landlord's insurance companies' refusing to insure the Building or Project or any property therein in amounts and against risks as reasonably determined by Landlord. If insurance premiums increase as a result of Tenant's failure to comply with the provisions of this Section 8.1, Tenant shall promptly cure such failure and shall reimburse Landlord for the increased insurance premiums paid by Landlord as a result of such failure by Tenant.

Section 8.2 Fire and Life Safety. Tenant shall maintain in good order and repair the sprinkler, fire-alarm and life-safety system in the Premises in accordance with this Lease including, without limitation, the provisions of Section 6.2 respecting any repairs affecting any Building System, the Rules and Regulations and all Requirements, if and to the extent such system has not been installed in the Premises prior to the Commencement Date. If the Fire Insurance Rating Organization or any Governmental Authority or any of Landlord's insurers requires or recommends any modifications and/or alterations be made or any additional equipment be supplied in connection with the sprinkler system or fire alarm and life-safety system serving the Building by reason of Tenant's business, any Alterations performed by Tenant or the location of the partitions, Tenant's Property, or other contents of the Premises, Landlord (to the extent outside of the Premises) or Tenant (to the extent within the Premises) shall make such modifications and/or Alterations, and supply such additional equipment, in either case at Tenant's expense.