As filed with the Securities and Exchange Commission on August 30, 2022

Registration No. 333-257302

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

AMENDMENT NO. 8

to

FORM S-1

REGISTRATION STATEMENT UNDER THE SECURITIES ACT OF 1933

(Exact name of registrant as specified in its charter) |

| 2080 |

| ||

(State or Other Jurisdiction of |

| (Primary Standard Industrial |

| (IRS Employer |

Incorporation or Organization) |

| Classification Number) |

| Identification Number) |

New Momentum Corporation Singapore + |

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices) |

Leung Tin Lung David

President and Chief Executive Officer

New Momentum Corporation

150 Cecil Street, #08-01

Singapore 069543

+65 3105-4128

(Address, including zip code, and telephone number, including area code, of agent for service)

Copies to:

Thomas E. Puzzo, Esq.

Law Offices of Thomas E. Puzzo, PLLC

3823 44th Ave. NE

Seattle, Washington 98105

Telephone No.: (206) 522-2256

Approximate date of proposed sale to the public: As soon as practicable and from time to time after the effective date of this Registration Statement.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. ☒

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer | ☐ | Accelerated filer | ☐ |

☒ | Smaller reporting company | ||

Emerging growth company |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant Section 7(a)(2)(B) of the Exchange Act.

Calculation of Registration Fee

Title of Securities To Be Registered |

| Amount to be Registered |

|

| Proposed Maximum Offering Price Per Share |

|

| Proposed Maximum Aggregate Offering Price |

|

| Registration Fee |

| ||||

Common Stock, par value $0.001 per share, issuable pursuant to Investment Agreement (1) |

|

| 5,000,000 | (1) |

| $ | 1.000 | (3) |

| $ | 5,000,000 |

|

| $ | 545.50 |

|

Common Stock, par value $0.001 per share, issuable upon conversion of 10% Convertible Note (2) |

|

| 182,617 | (2) |

| $ | 1.00 | (3) |

| $ | 182,617 |

|

| $ | 19.92 |

|

Total |

|

| 5,182,617 | (3) |

| $ | 1.000 | (3) |

| $ | 5,182,617 |

|

| $ | 565.42 |

|

_____________

(1) | Represents the number of shares of common stock of the Registrant that we will put (“Put Shares”) to Strattner Alternative Credit Fund LP, a Delaware limited partnership (“Strattner”), pursuant to that certain Investment Agreement (the “Investment Agreement”) by and between Strattner and the Registrant, effective on April 16, 2021. In the event that adjustment provisions of the Investment Agreement require the Company to issue more shares than are being registered in this registration statement, for reasons other than those stated in Rule 416 of the Securities Act, the Company will file a new registration statement to register those additional shares. |

|

|

(2) | Represents the number of shares of common stock of the Registrant underlying that certain 10% Convertible Note (the “Note”), dated October 27, 2020, and made to EMA Financial, LLC. The Note is due July 27, 2021, and carries interest at a rate of 10% per annum. |

| |

(3) | This offering price has been estimated solely for the purpose of computing the registration fee in accordance with Rule 457(c) of the Securities Act on the basis of the average of the high and low prices of the common stock of the Company as reported on the Pink tier of the OTC Markets Group, Inc. on June 15, 2021. |

In the event of stock splits, stock dividends, or similar transactions involving the Registrant’s common stock, the number of Shares registered shall, unless otherwise expressly provided, automatically be deemed to cover the additional securities to be offered or issued pursuant to Rule 416 promulgated under the Securities Act of 1933, as amended (the “Securities Act”).

| 2 |

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, as amended, or until the Registration Statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

PRELIMINARY PROSPECTUS

SUBJECT TO COMPLETION ON AUGUST 30, 2022

NEW MOMENTUM CORPORATION

5,182,617 SHARES OF COMMON STOCK

This prospectus relates to the resale of shares of our common stock, par value $0.001 per share, by (i) Strattner Alternative Credit Fund LP (“Strattner”) of 5,000,000 Put Shares that we will put to Strattner pursuant to the Investment Agreement, and (ii) 182,617 shares of common stock underlying that certain 10% Convertible Note (the “Note”), dated October 27, 2020, and made to EMA Financial, LLC, a Delaware limited liability company (“EMA Financial”). Strattner and EMA Financial are collectively referred to herein as the “Selling Security Holders.” As used in this prospectus, references to the "Company", "we", "our", "us", and "New Momentum" refer to New Momentum Corporation and its subsidiaries, unless the context otherwise indicates.

The Investment Agreement with Strattner provides that Strattner is committed to purchase up to $5,000,000 of our common stock. We may draw on the facility from time to time, as and when we determine appropriate in accordance with the terms and conditions of the Investment Agreement.

The terms and conditions of the Note provide registration rights for the shares (the “Note Shares”) underlying the Note to EMA Financial.

The Selling Security Holders are “underwriters” within the meaning of the Securities Act in connection with the resale of our common stock under the Investment Agreement and the Note. No other underwriter or person has been engaged to facilitate the sale of shares of our common stock in this offering. This offering will terminate on October 22, 2022. The per share purchase price for the Put Shares shall be equal to 85% of volume weighted average price (“VWAP”) for the five (5) consecutive trading days including and immediately after the date on which the Company submits a put notice to Strattner.

The conversion price of the Note Shares is equal to the lower of: (i) the lowest closing price of the Common Stock during the preceding twenty (20) trading day period ending on the latest complete trading day prior to the Issue Date of this Note or (ii) 55% of the lowest trading price for the Common Stock on the Principal Market during the twenty (20) consecutive trading days including and immediately preceding the Conversion Date.

We will not receive any proceeds from the sale of the shares of common stock offered by the Selling Security Holders. We may receive proceeds of up to $5,000,000 from the sale of our Put Shares under the Investment Agreement. The proceeds will be used for working capital or general corporate purposes. We will bear all costs associated with this registration.

Our common stock is quoted on the OTCQB tier of the OTC Markets Group, Inc. (the “OTC Markets”) under the symbol “NNAX.” The shares of our common stock registered hereunder are being offered for sale by Selling Security Holders at prices established on the OTC Markets during the term of this offering. On May 5, 2022, the closing price of our common stock was $0.016 per share. These prices will fluctuate based on the demand for our common stock.

While our principal administrative offices are located in Singapore, the majority of our operations are conducted in Hong Kong, three of our subsidiaries are Hong Kong entities, and as such, we are subject to emerging legal and operational risks associated with having the majority of our operations in Hong Kong corporations and thereby subject to political and economic influence from China. These risks could result in a material change in our operations and/or the value of our common stock. These risks could also significantly limit or completely hinder our ability to offer or continue to offer securities to investors and cause the value of such securities to significantly decline or be worthless.

Recent statements and regulatory actions by the Chinese government, such as those related to data security, anti-monopoly concerns, entertainment, education, finance, real estate, video gaming, advertising, casino operations, social mores, healthcare and China’s extension of authority into Hong Kong, has or may impact our ability to conduct our business, accept foreign investments, or list on a U.S. or other foreign exchange. Under current regulatory conditions in China and Hong Kong, virtually no aspect of society is being left unaffected by these changes; therefore we expect that our business and operations will also be affected by China and/or Hong Kong regulatory actions in the future. For example, it travel or movement of peoples in China and/or Hong Kong is restricted, our business will be adversely effected. Furthermore, the policies of the Chinese government, including the implementation of the National Security Law in Hong Kong, recent legislative and government policy changes, including the redistribution of wealth, may impact our ability to operate with legal certainty.

We are not a Chinese or Hong Kong operating company but a Nevada holding company with operations conducted by our subsidiaries in Hong Kong and Singapore, and this structure, as it related to our Hong Kong subsidiaries, involves unique risks to investors. Chinese regulatory authorities could disallow this structure, which would likely result in a material change in our operations and/or a material change in the value of the securities the subject of this offering, including the risk that disallowing this structure could cause the value of our securities to significantly decline or become worthless. For further description of such regulatory and structural risks, see “Risk Factors—Risks Related to Doing Business in the People’s Republic of China” on page 16.

| 3 |

Total Asia Associates PLT, our prior auditors, and the Company’s auditors, J&S Associate, are PCAOB-registered independent public accounting firms, based in Malaysia. Under the Holding Foreign Companies Accountable Act (the “HFCAA”), the PCAOB is permitted to inspect our independent public accounting firm. There is no guarantee that future audit reports will be prepared by auditors that are completely inspected by the PCAOB, and, as such, future investors may be deprived of such inspections, which could result in limitations or restrictions to our access of the U.S. capital markets. Furthermore, trading in our securities may be prohibited under the HFCAA, if the SEC subsequently determines our audit work is performed by auditors that the PCAOB is unable to inspect or investigate completely, and, as a result, our securities may be removed from quotation and further trading on the over-the-counter markets, where our shares of common stock are currently quoted. Furthermore, on June 22, 2021, the U.S. Senate passed the Accelerating Holding Foreign Companies Accountable Act, which, if enacted, would amend the HFCAA to reduce the number of non-inspection years from three to two years and, thus, would reduce the time before our securities may be prohibited from trading or be delisted. On December 2, 2021, the SEC adopted amendments to finalize rules implementing the HFCAA requiring the SEC to prohibit an issuer’s securities from trading on any U.S. securities exchange and on the over-the-counter market, if the auditor is not subject to PCAOB inspections for three consecutive years and this ultimately could result in our ordinary shares being delisted. On December 16, 2021, the PCAOB issued its HFCAA Determination Report to notify the SEC that it was unable to inspect or investigate completely registered public accounting firms headquartered in mainland China and in Hong Kong because of the positions taken by authorities in mainland China and Hong Kong. As stated above, our current auditors are based in Malaysia and the PCAOB is permitted to inspect and investigate them.

Our auditors are based in Malaysia and are subject to PCAOB inspection. It is not subject to the determinations announced by the PCAOB on December 16, 2021. However, in the event the Malaysian authorities subsequently take a position disallowing the PCAOB to inspect our auditors, then we would need to change our auditors to avoid having our securities delisted. Furthermore, due to the recent developments in connection with the implementation of the Holding Foreign Companies Accountable Act and the Accelerating the Holding Foreign Companies Accountable Act, we cannot assure you whether the SEC or other regulatory authorities would apply additional and more stringent criteria to us after considering the effectiveness of our auditors’ audit procedures and quality control procedures, adequacy of personnel and training, or sufficiency of resources, geographic reach or experience as it relates to the audit of our financial statements.

To the extent cash and/or assets of our business is in Hong Kong or our Hong Kong entities, such funds and/or assets may not be available to fund operations or for other use outside of Hong Kong due to interventions in or the imposition of restrictions and limitations on the ability of us or our subsidiaries by the PRC government to transfer cash and/or assets. For further discussion of our arrangement of how cash is transferred with our subsidiary, JJ Explorer, please see Note 8 (Related Party Transactions) to our unaudited financial statements for the fiscal quarter ended June 30, 2022 on page F-33. Our auditors are based in Malaysia and are subject to PCAOB inspection. It is not subject to the determinations announced by the PCAOB on December 16, 2021. However, in the event the Malaysian authorities subsequently take a position disallowing the PCAOB to inspect our auditors, then we would need to change our auditors to avoid having our securities delisted. Furthermore, due to the recent developments in connection with the implementation of the Holding Foreign Companies Accountable Act and the Accelerating the Holding Foreign Companies Accountable Act, we cannot assure you whether the SEC or other regulatory authorities would apply additional and more stringent criteria to us after considering the effectiveness of our auditors’ audit procedures and quality control procedures, adequacy of personnel and training, or sufficiency of resources, geographic reach or experience as it relates to the audit of our financial statements.

Our ability to pay dividends to our shareholders and to service any debt we may incur may depend upon dividends paid by our Hong Kong subsidiaries. Current Hong Kong regulations permit our Hong Kong Subsidiaries to pay dividends to us, only out of their accumulated profits, if any, determined in accordance with Hong Kong accounting standards and regulations. As of the date hereof, we have had no transactions that involved the transfer of cash or assets throughout our corporate structure and no transfers, dividends or distributions have been made to investors. Our Hong Kong subsidiaries have not transferred cash or other assets to New Momentum Corporation, including by way of dividends. New Momentum Corporation does not currently plan or anticipate transferring cash or other assets from our operations in Hong Kong to any non-Chinese entity.

We do not have any cash management policies that dictate how funds are transferred between New Momentum Corporation and its subsidiaries. To the extent cash and/or assets in our business in Hong Kong or in any of our Hong Kong subsidiaries, such funds and/or assets may not be available to fund operations or for other use outside of Hong Kong due to interventions in or the imposition of restrictions and limitations on the ability of you or your subsidiaries by the PRC government to transfer cash and/or assets.

Investing in our Common Stock involves a high degree of risk. See “Risk Factors” to read about factors you should consider before buying shares of our Common Stock.

NEITHER THE SECURITIES AND EXCHANGE COMMISSION NOR ANY STATE SECURITIES COMMISSION HAS APPROVED OR DISAPPROVED OF THESE SECURITIES OR DETERMINED IF THIS PROSPECTUS IS TRUTHFUL OR COMPLETE. ANY REPRESENTATION TO THE CONTRARY IS A CRIMINAL OFFENSE.

The information in this Prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission becomes effective. This Prospectus is not an offer to sell these securities and we are not soliciting an offer to buy these securities in any state where the offer or sale is not permitted or would be unlawful prior to registration or qualification under the securities laws of any such state.

The following table of contents has been designed to help you find information contained in this prospectus. We encourage you to read the entire prospectus.

| 4 |

TABLE OF CONTENTS

PART I - INFORMATION REQUIRED IN PROSPECTUS

| 5 |

| Table of Contents |

PROSPECTUS SUMMARY

You should read the following summary together with the more detailed information and the financial statements appearing elsewhere in this Prospectus. This Prospectus contains forward-looking statements that involve risks and uncertainties. Our actual results could differ materially from those anticipated in these forward-looking statements as a result of certain factors, including those set forth under “Risk Factors” and elsewhere in this Prospectus. Unless the context indicates or suggests otherwise, references to “we,” “our,” “us,” the “Company,” “New Momentum” or the “Registrant” refer to New Momentum Corporation, a Nevada corporation and its subsidiaries.

OUR COMPANY

Overview of New Momentum

We intend to develop travel services businesses, including “Gagfare,” an online ticketing platform that provides travelers a “Book Now, Pay Later” business model allowing travelers to secure the best fares and reserve flights well ahead of time. The Company intends to also become the driving force behind a bold new hospitality concept that takes nature lovers and intrepid travelers to exciting new and established destinations. The Company intends to curate a collection of boutique properties, each with a focus on diving, sustainability, conservation, and cultural authenticity, offering a thoroughly contemporary travel experience that is intrinsically linked to the destination, its heritage and its culture.

Our fiscal year-end date is December 31.

Our board of directors consists of one person: Leung Tin Lung David. Mr. Leung also serves as our sole officer, holding the offices of President, Secretary and Treasurer.

Our principal administrative offices are located at 150 Cecil Street, #08-01, Singapore 069543. Our website is www.gagfare.com. We do not incorporate the information on or accessible through our website into this Prospectus, and you should not consider any information on, or that can be accessed through, our websites a part of this Prospectus.

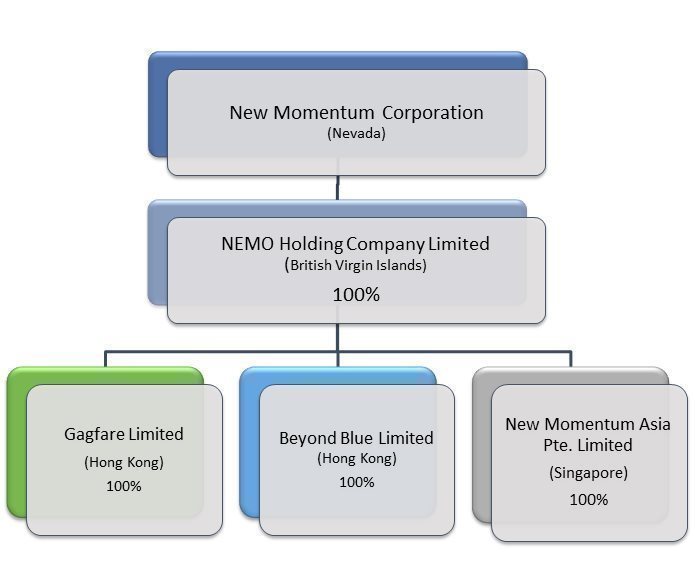

A summary diagram of our corporate structure is as follows:

| 6 |

| Table of Contents |

Recent Developments

Share Exchange Agreement

On July 6, 2020, the Company entered into a Share Exchange Agreement (the “Share Exchange Agreement”), by and among the Company, Nemo Holding Company Limited, a British Virgin Islands corporation (“Nemo Holding”), and the holders of common shares of Nemo Holding. The holders of the common stock of Nemo Holding consisted of 29 stockholders.

Under the terms and conditions of the Share Exchange Agreement, the Company offered, sold and issued 10,000,000 shares of common stock in consideration for all the issued and outstanding shares in Nemo Holding. Leung Tin Lung David, the Company’s sole officer and director, became the beneficial holder of 6,000,000 common shares, or 60%, of the issued and outstanding shares of Nemo Holding. The effect of the issuance of the 10,000,000 shares issued under the Share Exchange Agreement represents 10.8% of the issued and outstanding shares of common stock of the Company.

Immediately prior to the closing of the transactions under the Share Exchange Agreement, Mr. Leung was the holder of 233,813,213 shares of common stock, or 75.2%, of the issued and outstanding shares of common stock of the Company. Giving effect to the closing of the transactions under the Share Exchange Agreement, Mr. Leung acquired 6,000,000 shares of common stock of the Company, by virtue of his 60% beneficial ownership of Nemo Holding. The remaining 28 common shareholders of Nemo Holding acquired 4,000,000 shares of common stock under the Share Exchange Agreement, by virtue of their aggregate of 40% beneficial ownership of Nemo Holding.

As a result of the share exchange, Nemo Holding became a wholly-owned subsidiary of the Company.

The share exchange transaction with Nemo Holding was treated as a reverse acquisition, with Nemo Holding as the acquiror and the Company as the acquired party. Unless the context suggests otherwise, when we refer in this Form 8-K to business and financial information for periods prior to the consummation of the reverse acquisition, we are referring to the business and financial information of Nemo Holding.

Cooperation Agreement

Pursuant to Cooperation Agreement, dated February 1, 2016, by and between Gagfare Limited, a Hong Kong corporation and wholly owned subsidiary of the Company, and JJ Explorer Tours Limited, a Hong Kong corporation (“JJ Explorer”), controlled by our chief executive officer, JJ Explorer develops and maintains website and mobile application platforms the Company uses in the operation of its business in exchange for 50% of the net earnings the Company earns through its Gagfare website and mobile application platforms for a term of five years, to be expired on January 31, 2021. For the years ended December 31, 2021 and 2020, the Company did not pay or transfer any cash to JJ Explorer, because there were no net earnings during the reporting periods. Hence, no transfers, dividends, or distributions have been made to date, including the transfers to JJ Explorer during the reporting periods. For further discussion of our arrangement of how cash is transferred with JJ Explorer, please see Note 8 (Related Party Transactions) to our unaudited financial statements for the fiscal quarter ended June 30, 2022 on page F-33.

10% Convertible Note

On October 27, 2020, the Registrant offered and sold the Note, dated October 27, 2020, to EMA Financial for aggregate proceeds of $33,000. As of June 9, 2021, there was $35,000 in principal and $2,042 in interest due and owing under the Note. The Note is due July 27, 2021, and carries interest at a rate of 10% per annum. The conversion price of the Note Shares is equal to the lower of: (i) the lowest closing price of the Common Stock during the preceding twenty (20) trading day period ending on the latest complete trading day prior to the Issue Date of this Note or (ii) 55% of the lowest trading price for the Common Stock on the Principal Market during the twenty (20) consecutive trading days including and immediately preceding the Conversion Date. We will not receive any proceeds from the sale of the shares of common stock offered by EMA Financial. The terms and conditions of the Note provide registration rights for the Note Shares.

| 7 |

| Table of Contents |

Stock Purchase Agreement

On April 13, 2021, the Company entered into a Stock Purchase Agreement with Leung Tin Lung David, the Company’s sole director, President, and majority stockholder, pursuant to which the Company sold to Mr. Leung one share of Series A Preferred Stock in exchange for 169,000,000 shares of common stock of the Company. The Company subsequently canceled and returned to its authorized capital stock the 169,000,000 shares of common stock purchased from Mr. Leung. The holder of the one share of Series A Preferred Stock (i) has voting power equal to 110% of the total voting rights of the Company’s common stock, (ii) the right to appoint a designee to the board of directors, and (ii) requires the consent of the holder of the Series A Preferred Stock for any major corporate actions, including but not limited to changing the Articles of Incorporation or Bylaws of the Company, changing the business of the Company, issuing securities and or nominating a person as President or Chief Executive Office of the Company. As a result, Mr. Leung has controlling voting power in all matters submitted to our stockholders for approval including:

| · | The election of our board of directors; |

| · | The amendment of our Articles of Incorporation or bylaws; |

| · | The adoption of measures that could delay or prevent a change in control or impede a merger, takeover or other business combination involving us. |

As a result of his ownership and position, Mr. Leung is able to substantially influence all matters requiring stockholder approval, including the election of directors and approval of significant corporate transactions. Mr. Leung’s stock ownership may discourage a potential acquirer from making a tender offer or otherwise attempting to obtain control of us, which in turn could reduce our stock price or prevent our stockholders from realizing a premium over our stock price.

Investment Agreement with Strattner Alternative Credit Fund LP

On April 16, 2021, the Company entered into an Investment Agreement dated as of April 16, 2021 (the “Investment Agreement”) with Strattner. The Investment Agreement provides that, upon the terms and subject to the conditions set forth therein, Strattner is committed to purchase up to $5,000,000 (the “Total Commitment”) worth of the Company’s common stock, $0.001 par value, over the 36-month term of the Investment Agreement.

From time to time over the term of the Investment Agreement, commencing on the trading day immediately following the date on which the initial registration statement is declared effective by the Securities and Exchange Commission (the “Commission”), as further discussed below, the Company may, in its sole discretion, provide Strattner with draw down notices (each, a “Draw Down Notice”) to purchase a specified dollar amount of the Put Shares (the “Draw Down Amount”) over a 10 consecutive trading day period, commencing on the trading day specified in the applicable Draw Down Notice (the “Pricing Period”), with each draw down subject to the limitations discussed below. The maximum amount of Shares requested to be purchased pursuant to any single Draw Down Notice cannot exceed 200% of the average daily trading volume of the Company’s common stock for the ten trading days immediately preceding the date of the Draw Down Notice (the “Maximum Draw Down Amount”).

Once presented with a Draw Down Notice, Strattner is required to purchase the number of Put Shares underlying the Draw Down Notice. The per share purchase price for the Shares subject to a Draw Down Notice shall be equal to 85% of the arithmetic average of the lowest VWAPs during the applicable Pricing Period Each purchase pursuant to a draw down shall reduce, on a dollar-for-dollar basis, the Total Commitment under the Investment Agreement.

| 8 |

| Table of Contents |

The Company is prohibited from issuing a Draw Down Notice if (i) the amount requested in such Draw Down Notice exceeds the Maximum Draw Down Amount, (ii) the sale of Shares pursuant to such Draw Down Notice would cause the Company to issue or sell or Strattner to acquire or purchase an aggregate dollar value of Shares that would exceed the Total Commitment, or (iii) the sale of Shares pursuant to the Draw Down Notice would cause the Company to sell or Strattner to purchase an aggregate number of shares of the Company’s common stock which would result in beneficial ownership by Strattner of more than 9.99% of the Company’s common stock (as calculated pursuant to Section 13(d) of the Securities Exchange Act of 1934, as amended, and the rules and regulations thereunder). The Company cannot make more than one draw down in any Pricing Period and must allow 10 days to elapse between the completion of the settlement of any one draw down and the commencement of a Pricing Period for any other draw down.

Additionally, the Company paid to Strattner a commitment fee equal in the form of 250,000 restricted shares of the Company’s common stock (the “Initial Commitment Shares”).

Registration Rights Agreement with Strattner Alternative Credit Fund LP

In connection with the execution of the Investment Agreement, on April 16, 2021, the Company and Strattner also entered into a Registration Rights Agreement (the “Registration Rights Agreement”). Pursuant to the Registration Rights Agreement, the Company has agreed to file an initial registration statement (“Registration Statement”) with the Commission to register an agreed upon number of Put Shares, on or prior to July 16, 2021 (the “Filing Deadline”) and have it declared effective on or before the 150th calendar day the Company has filed the Registration Rights Agreement (the “Effectiveness Deadline”).

If at any time all of the Registrable Securities (as defined in the Registration Rights Agreement) are not covered by the initial Registration Statement, the Company has agreed to file with the Commission one or more additional Registration Statements so as to cover all of the Registrable Securities not covered by such initial Registration Statement, in each case, as soon as practicable, but in no event later than the applicable filing deadline for such additional Registration Statements as provided in the Registration Rights Agreement.

Emerging risks for us being based in and having the majority of our operations in Hong Kong, China.

We are a Hong Kong, China-based company and we may face risks and uncertainties in doing business in China. In addition to the foregoing risks, we face various legal and operational risks and uncertainties arising from doing business in Hong Kong as summarized below and in “Risk Factors — Risks Relating to Doing Business in the People's Republic of China and Hong Kong” on page 19.

| · | The Peoples Republic of China (“PRC”) government has sovereignty of Hong Kong, and Hong Kong’s legislature adopts laws that are congruent with PRC government policies, laws and regulations. Because of the majority of our operations are in the Hong Kong, economic, political and legal developments in the PRC will significantly affect our business, financial condition, results of operations and prospects; For further discussion of this risk, see “Changes in the political and economic policies of the PRC government may materially and adversely affect our business, financial condition and results of operations and may result in our inability to sustain our growth and expansion strategies,” on page 19. |

|

|

|

| · | Government policies, laws and regulations in the PRC can change very quickly with little advance notice; For further discussion of this risk, see “Changes in the political and economic policies of the PRC government may materially and adversely affect our business, financial condition and results of operations and may result in our inability to sustain our growth and expansion strategies,” on page 19. |

|

|

|

| · | The PRC government may intervene or influence our operations in Hong Kong at any time and may exert more control over offerings conducted overseas and/or foreign investment in Hong Kong-based issuers, which could result in a material change in our operations and/or the value of our common stock, and could significantly limit or completely hinder our ability to offer or continue to offer securities to investors and cause the value of our common stock and other securities to significantly decline or be worthless; For further discussion of this risk, see “Because we have subsidiaries in Hong Kong, the PRC government has significant oversight and discretion over the conduct our business operations, may exert control over any offering of securities conducted overseas and/or foreign investment in China-based issuers, may intervene or influence our operations at any time, and may limit or completely hinder our ability to offer or continue to offer securities to investors, which could result in a material change in our operations and/or cause the value of such securities to significantly decline or be worthless, as the government deems appropriate to further regulatory, political and societal goals,” on page 19. |

|

|

|

| · | Changes in China’s economic, political or social conditions or government policies, especially over the movement of people and travel, could materially and adversely affect our business and results of operations; For further discussion of this risk, see “Changes in the political and economic policies of the PRC government may materially and adversely affect our business, financial condition and results of operations and may result in our inability to sustain our growth and expansion strategies,” on page 19. |

|

|

|

| · | The legal system in China embodies uncertainties which could limit the legal protections available to us or impose additional requirements and obligations on our business, which may materially and adversely affect our business, financial condition, and results of operations; For further discussion of this risk, see “Because we have subsidiaries in Hong Kong, the PRC government has significant oversight and discretion over the conduct our business operations, may exert control over any offering of securities conducted overseas and/or foreign investment in China-based issuers, may intervene or influence our operations at any time, and may limit or completely hinder our ability to offer or continue to offer securities to investors, which could result in a material change in our operations and/or cause the value of such securities to significantly decline or be worthless, as the government deems appropriate to further regulatory, political and societal goals,” on page 19. |

|

|

|

| · | The current tensions in international trade and rising political tensions, particularly between the United States and China, may adversely impact our business, financial condition, and results of operations; and For further discussion of this risk, see “Declines or disruptions in the travel industry could adversely affect our business and financial performance,” on page 15. |

|

|

|

| · | It may be difficult for overseas regulators to conduct investigations or collect evidence within China. For further discussion of this risk, see “It may be difficult for U.S. regulators, such as the Department of Justice, the SEC, and other authorities, to conduct investigation or collect evidence within China.,” on page 22. |

|

|

|

| · | To the extent cash and/or assets of our business is in Hong Kong or our Hong Kong entities, such funds and/or assets may not be available to fund operations or for other use outside of Hong Kong due to interventions in or the imposition of restrictions and limitations on the ability of us or our subsidiaries by the PRC government to transfer cash and/or assets. For further discussion of our arrangement of how cash is transferred with our subsidiary, JJ Explorer, please see Note 8 (Related Party Transactions) to our unaudited financial statements for the fiscal quarter ended June 30, 2022 on page F-33. |

|

|

|

| · | Because our holding company structure, which includes Hong Kong subsidiaries, creates restrictions on the payment of dividends or other cash payments, our ability to pay dividends or make other payments is limited.For further discussion of this risk, see “Because our holding company structure creates restrictions on the payment of dividends or other cash payments, our ability to pay dividends or make other payments is limited,” on page 21. |

|

|

|

| · | It is possible that PRC authorities could prevent our cash maintained in Hong Kong from leaving or the PRC could restrict the deployment of the cash into our business or for the payment of dividends. We rely on dividends from our Hong Kong subsidiary for our cash and financing requirements, such as the funds necessary to service any debt we may incur. Any such controls or restrictions may adversely affect our ability to finance our cash requirements, service debt or make dividend or other distributions to our shareholders. For further discussion of this risk, see “Our Hong Kong subsidiaries may be subject to restrictions on paying dividends or making other payments to us, which may restrict its ability to satisfy liquidity requirements, conduct business and pay dividends to holders of New Momentum Corporation’s common stock,” on page 21. |

|

|

|

| · | It is possible that PRC authorities could prevent our cash maintained in Hong Kong from leaving or the PRC could restrict the deployment of the cash into our business or for the payment of dividends. We rely on dividends from our Hong Kong subsidiary for our cash and financing requirements, such as the funds necessary to service any debt we may incur. Any such controls or restrictions may adversely affect our ability to finance our cash requirements, service debt or make dividend or other distributions to our shareholders. For further discussion of this risk, see “Governmental control of currency conversion may limit our ability to utilize revenues effectively and affect the value of your investment,” on page 21. |

Permissions under Hong Kong Law and PRC Law

We are currently not required to obtain permission from any of the PRC authorities to operate and issue our common stock to foreign investors. In addition, we and our subsidiaries are not required to obtain permission or approval from the Hong Kong and PRC authorities, including China Securities Regulatory Commission (“CSRC”), Cyberspace Administration of China (“CAC”) and/or any other entity that is required to approve our operations other than the standard annual check with local administration bureau. This is subject to the uncertainty of different interpretation and implementation of the rules and regulations in the PRC that could be potentially adverse to us, which may take place quickly with little advance notice.

Recently, the General Office of the Central Committee of the Communist Party of China and the General Office of the State Council jointly issued the Opinions on Severe and Lawful Crackdown on Illegal Securities Activities, which was available to the public on July 6, 2021. These opinions emphasized the need to strengthen the administration over illegal securities activities and the supervision on overseas listings by China-based companies. The PRC government also initiated a series of regulatory actions and statements to regulate business operations in China with little advance notice, including cracking down on illegal activities in the securities market, enhancing supervision over China-based companies listed overseas using variable interest entity structure, adopting new measures to extend the scope of cybersecurity reviews, and expanding the efforts in anti-monopoly enforcement. Since these statements and regulatory actions are new, it is highly uncertain how soon legislative or administrative regulation making bodies will respond and what existing or new laws or regulations or detailed implementations and interpretations will be modified or promulgated, if any, and the potential impact such modified or new laws and regulations will have on our daily business operation, the ability to accept foreign investments and list on a U.S. exchange. On July 10, 2021, the State Internet Information Office issued the Measures of Cybersecurity Review (Revised Draft for Comments, not yet effective), which requires operators with personal information of more than 1 million users who want to list abroad to file a cybersecurity review with the Office of Cybersecurity Review. As of the date of this prospectus, our Company and its subsidiaries have not been involved in any investigations on cybersecurity review initiated by any PRC regulatory authority, nor has any of them received any inquiry, notice or sanction. We do not believe that our existing business will require such regulatory review. As of the date of this prospectus, our Company its subsidiaries have not received any inquiry, notice, warning or sanctions regarding our planned overseas listing from the China Securities Regulatory Commission or any other PRC governmental authorities.

We have received all requisite permissions and approvals to operate our business. If PRC authorities reinterpret PRC laws to apply to Hong Kong companies, our Hong Kong subsidiaries may become subject permits, to the laws and regulations of the PRC governing businesses. We may also become subject to foreign exchange regulations that might limit our ability to convert foreign currency into Renminbi or Hong Kong Dollars, acquire any PRC companies, establish VIEs in the PRC, or make dividend payments from any subsidiary entities operating in the PRC and/or Hong Kong to us. If we do not receive or fail to maintain all requisite permits, permissions and approvals to operate our business, we would have to cease our operations in Hong Kong and you could lose your entire investment.

If either Hong Kong or PRC authorities reinterpret PRC laws to apply to Hong Kong companies, it is possible that Hong Kong or PRC authorities could determine that we are not allowed to operate our business in Hong Kong for failure to have requisite permits, permissions or approvals (which do not exist as of today), in which case we would have to cease our operations in Hong Kong and you could lose your entire investment.

If we inadvertently conclude that such permits, permissions or approvals are not required, Hong Kong or PRC authorities could assess us a monetary penalty, which as of today would be for an unknown amount, or determine that we are not allowed to operate our business in Hong Kong for failure to obtain requisite permits, permissions or approvals (which do not exist as of today), in which case we would have to cease our operations in Hong Kong and you could lose your entire investment.

If either Hong Kong or PRC authorities change applicable laws or regulations to apply to Hong Kong companies, and we are required to obtain new permits, permissions or approvals (which do not exist as of today), it is possible that Hong Kong or PRC authorities could determine that we are not granted such permits, permissions or approvals and, therefore, not allowed to operate our business in Hong Kong, in which case we would have to cease our operations in Hong Kong and you could lose your entire investment.

| 9 |

| Table of Contents |

The PRC National Security Law

On June 30, 2020, the PRC government’s National People’s Congress Standing Committee passed a national security law (the “National Security Law”) for the Hong Kong Special Administrative Region (“Hong Kong”). The National Security Law criminalizes, and otherwise gives the PRC government board broad powers to find unlawful, a broad variety of political crimes, including separatism, and collusion with a foreign country or with external elements to endanger national security in relation to the Hong Kong. The PRC government can, at its or the Hong Kong government’s discretion, exercise jurisdiction over alleged violations of the law and prosecute and adjudicate the cases in mainland China. The law can apply to alleged violations committed by anyone, anywhere in the world, including in the United States. We do not believe that we violate or have violated the National Security Law, but in light of the PRC government’s current and rapidly changing policies regarding PRC and Hong businesses operations, our business operations could in the future be subject to the National Security Law, if the PRC or Hong Kong government believes that it should. Additionally, regulations announced by the Cyberspace Administration of China the ("CAC") on January 4, 2022, The Cybersecurity Review Measures (2021) (the “Measures”), became effective on February 15, 2022. According to the Measures, to go public abroad, an online platform operator that possesses the personal information of more than 1,000,000 users must seek cybersecurity review from the Office of Cybersecurity Review. Currently, we have not been involved in any investigations on cybersecurity review initiated by the CAC or related governmental regulatory authorities, and we have not received any inquiry, notice, warning, or sanction in such respect. We have been advised by Hong Kong counsel, Tasman C.H. Tam, that the CAC does not apply to our operations in Hong Kong because we do not possess an amount of information in our business operations that would trigger the CAC; and the kind of data processed in our operations does not relate to national security. We have not obtained a legal opinion, and instead relied on legal advice from local counsel, because no legal opinion was required in order for us to rely on such advice.

Transfers of Cash to and from Our Hong Kong Subsidiaries, and to our U.S Investors.

New Momentum Corporation is a Nevada holding company with no operations of its own. We conduct our operations in Hong Kong primarily through our subsidiaries in Hong Kong. We may rely on dividends to be paid by our Hong Kong subsidiaries to fund our cash and financing requirements, including the funds necessary to pay dividends and other cash distributions to our shareholders, to service any debt we may incur and to pay our operating expenses. If our Hong Kong subsidiaries incur debt on their own behalf in the future, the instruments governing the debt may restrict their ability to pay dividends or make other distributions to us. For further discussion of our arrangement of how cash is transferred with our subsidiary, JJ Explorer, please see Note 8 (Related Party Transactions) to our unaudited financial statements for the fiscal quarter ended June 30, 2022 on page F-33.

New Momentum Corporation is permitted under the Nevada laws to provide funding to our subsidiaries in Hong Kong through loans or capital contributions without restrictions on the amount of the funds, subject to satisfaction of applicable government registration, approval and filing requirements. Our Hong Kong subsidiaries are also permitted under the laws of Hong Kong to provide funding to our other subsidiaries through dividend distribution without restrictions on the amount of the funds. As of the date of this prospectus, there has been no dividends or distributions among the holding company or the subsidiaries.

We currently intend to retain all available funds and future earnings, if any, for the operation and expansion of our business and do not anticipate declaring or paying any dividends in the foreseeable future. Any future determination related to our dividend policy will be made at the discretion of our board of directors after considering our financial condition, results of operations, capital requirements, contractual requirements, business prospects and other factors the board of directors deems relevant, and subject to the restrictions contained in any future financing instruments.

Subject to the Nevada Revised Statutes and our Bylaws, our board of directors may authorize and declare a dividend to shareholders at such time and of such an amount as they think fit if they are satisfied, on reasonable grounds, that immediately following the dividend the value of our assets will exceed our liabilities and we will be able to pay our debts as they become due. There is no further Nevada statutory restriction on the amount of funds which may be distributed by us by dividend.

Under the current practice of the Inland Revenue Department of Hong Kong, no tax is payable in Hong Kong in respect of dividends paid by us. The laws and regulations of the PRC do not currently have any material impact on transfer of cash from New Momentum Corporation to its subsidiaries. There are no restrictions or limitation under the laws of Hong Kong imposed on the conversion of HK dollar into foreign currencies and the remittance of currencies out of Hong Kong or across borders and to U.S investors.

Current PRC regulations permit PRC subsidiaries to pay dividends to Hong Kong subsidiaries only out of their accumulated profits, if any, determined in accordance with Chinese accounting standards and regulations. In addition, each of our subsidiaries in China is required to set aside at least 10% of its after-tax profits each year, if any, to fund a statutory reserve until such reserve reaches 50% of its registered capital. Each of such entity in China is also required to further set aside a portion of its after-tax profits to fund the employee welfare fund, although the amount to be set aside, if any, is determined at the discretion of its board of directors. Although the statutory reserves can be used, among other ways, to increase the registered capital and eliminate future losses in excess of retained earnings of the respective companies, the reserve funds are not distributable as cash dividends except in the event of liquidation. As of the date of this prospectus, we do not have any PRC subsidiaries.

The PRC government also imposes controls on the conversion of RMB into foreign currencies and the remittance of currencies out of the PRC. Therefore, we may experience difficulties in completing the administrative procedures necessary to obtain and remit foreign currency for the payment of dividends from our profits, if any. Furthermore, if our subsidiaries in the PRC incur debt on their own in the future, the instruments governing the debt may restrict their ability to pay dividends or make other payments. If we or our subsidiaries are unable to receive all of the revenues from our operations, we may be unable to pay dividends on our common stock.

Cash dividends, if any, on our common stock will be paid in U.S. dollars. If we are considered a PRC tax resident enterprise for tax purposes, any dividends we pay to our overseas shareholders may be regarded as China-sourced income and as a result may be subject to PRC withholding tax at a rate of up to 10.0%.

In order for us to pay dividends to our shareholders, we will rely on payments made from our Hong Kong subsidiary to New Momentum Corporation. If in the future we have PRC subsidiaries, certain payments from such PRC subsidiaries to Hong Kong subsidiaries will be subject to PRC taxes, including business taxes and VAT. As of the date of this prospectus, we do not have any PRC subsidiaries and our Hong Kong subsidiary has not made any transfers or distributions.

Pursuant to Arrangement between Mainland China and the Hong Kong Special Administrative Region for the Avoidance of Double Taxation and Tax Evasion on Income, or the Double Tax Avoidance Arrangement, the 10% withholding tax rate may be lowered to 5% if a Hong Kong resident enterprise owns no less than 25% of a PRC entity. However, the 5% withholding tax rate does not automatically apply and certain requirements must be satisfied, including, without limitation, that (a) the Hong Kong entity must be the beneficial owner of the relevant dividends; and (b) the Hong Kong entity must directly hold no less than 25% share ownership in the PRC entity during the 12 consecutive months preceding its receipt of the dividends. In current practice, a Hong Kong entity must obtain a tax resident certificate from the Hong Kong tax authority to apply for the 5% lower PRC withholding tax rate. As the Hong Kong tax authority will issue such a tax resident certificate on a case-by-case basis, we cannot assure you that we will be able to obtain the tax resident certificate from the relevant Hong Kong tax authority and enjoy the preferential withholding tax rate of 5% under the Double Taxation Arrangement with respect to dividends to be paid by a PRC subsidiary to its immediate holding company. As of the date of this prospectus, we do not have a PRC subsidiary. In the event that we acquire or form a PRC subsidiary in the future and such PRC subsidiary desires to declare and pay dividends to our Hong Kong subsidiary, our Hong Kong subsidiary will be required to apply for the tax resident certificate from the relevant Hong Kong tax authority. In such event, we plan to inform the investors through SEC filings, such as a current report on Form 8-K, prior to such actions. See “Risk Factors – Risk Factors Relating to Doing Business in the People's Republic of China and Hong Kong” on Page 19.

For further discussion of this risk, see “Changes in the political and economic policies of the PRC government may materially and adversely affect our business, financial condition and results of operations and may result in our inability to sustain our growth and expansion strategies,” on page 19.

| 10 |

| Table of Contents |

We are a “Smaller Reporting Company”

We are a “smaller reporting company,” meaning that we are not an investment company, an asset-backed issuer, or a majority-owned subsidiary of a parent company that is not a smaller reporting company and have (i) a public float of less than $250 million or (ii) annual revenues of less than $100 million during the most recently completed fiscal year and no public float, or a public float of less than $700 million. As a “smaller reporting company,” the disclosure we will be required to provide in our SEC filings are less than it would be if we were not considered a “smaller reporting company.” Specifically, “smaller reporting companies” are able to provide simplified executive compensation disclosures in their filings; are exempt from the provisions of Section 404(b) of the Sarbanes-Oxley Act of 2002 requiring that independent registered public accounting firms provide an attestation report on the effectiveness of internal control over financial reporting; are not required to conduct say-on-pay and frequency votes until annual meetings; and have certain other decreased disclosure obligations in their SEC filings, including, among other things, being permitted to provide two years of audited financial statements in annual reports rather than three years. Decreased disclosures in our SEC filings due to our status as a “smaller reporting company” may make it harder for investors to analyze the Company’s results of operations and financial prospects.

Emerging Growth Company

We are an ‘‘emerging growth company’’ within the meaning of the federal securities laws. For as long as we are an emerging growth company, we will not be required to comply with the requirements that are applicable to other public companies that are not “emerging growth companies” including, but not limited to, not being required to comply with the auditor attestation requirements of Section 404 of the Sarbanes-Oxley Act, the reduced disclosure obligations regarding executive compensation in our periodic reports and proxy statements and the exemptions from the requirements of holding a nonbinding advisory vote on executive compensation and shareholder approval of any golden parachute payments not previously approved. We intend to take advantage of these reporting exemptions until we are no longer an emerging growth company. For a description of the qualifications and other requirements applicable to emerging growth companies and certain elections that we have made due to our status as an emerging growth company, see “Risk Factors—Risks Related to this Offering and our Common Stock – We are an ‘emerging growth company’ and we cannot be certain if the reduced disclosure requirements applicable to emerging growth companies will make our common stock less attractive to investors” on page 8 of this prospectus.

Our fiscal year end is December 31. Our audited financial statements for the year ended December 31, 2021, were prepared assuming that we will continue our operations as a going concern. Our accumulated loss for the period from March 15, 2016 (inception) to the fiscal quarter ended September 30, 2021 was $4,716,695. For the nine months ended September 30, 2021, we earned revenues of $968,271, from ticketing sales, with the cost of such revenue being $964,540.

Due to the uncertainty of our ability to meet our current operating and capital expenses, our independent auditors have included a going concern opinion in their report on our audited financial statements for the period ended December 31, 2021. The notes to our financial statements contain additional disclosure describing the circumstances leading to the issuance of a going concern opinion by our auditors.

THE OFFERING

This Prospectus relates to the resale of up to 5,182,617 shares of our Common Stock, issuable to Strattner, pursuant to that certain Investment Agreement (the “Investment Agreement”), dated April 16, 2021, by and between the Company and to Strattner, and 182,617 shares of common stock underlying that certain 10% Convertible Note (the “note”), dated October 27, 2020, and made to EMA Financial.

The Offering

Common Stock offered by Selling Security Holders: |

| This Prospectus relates to the resale of 5,000,000 shares of our Common Stock, issuable to the Selling Security Holders. |

| ||

Common Stock outstanding before the Offering: |

| 176,168,548 shares of Common Stock as of the date of this Prospectus. |

| ||

Common Stock outstanding after the Offering: |

| 181,168,548 shares of Common Stock (1) |

| ||

Terms of the Offering: |

| The Selling Security Holders will determine when and how it will sell the Common Stock offered in this Prospectus. The prices at which the Selling Security Holders may sell the shares of Common Stock in this Offering will be determined by the prevailing market price for the shares of Common Stock or in negotiated transactions. |

| ||

Termination of the Offering |

| The Offering will conclude upon such time as all of the Common Stock has been sold pursuant to the Registration Statement. |

| ||

Trading Market |

| Our Common Stock is subject to quotation on the OTC Markets under the symbol “NNAX.” |

| ||

Use of proceeds |

| The Company is not selling any shares of the Common Stock covered by this Prospectus. As such, we will not receive any of the Offering proceeds from the registration of the shares of Common Stock covered by this Prospectus. See “Use of Proceeds.” |

| ||

Risk Factors |

| The Common Stock offered hereby involves a high degree of risk and should not be purchased by investors who cannot afford the loss of his/her/its entire investment. See “Risk Factors”. |

(1) This total reflects the number of shares of Common Stock that will be outstanding assuming that the Selling Security Holders purchase all of the 5,000,000 shares of our common stock under the Investment Agreement.

| 11 |

| Table of Contents |

SUMMARY FINANCIAL INFORMATION

The tables and information below are derived from our audited financial statements for the fiscal year ended December 31, 2021, and our unaudited financial statements for the fiscal quarter ended June 30, 2022. Our working capital deficit as at June 30, 2022 was $(355,718).

|

| For the Fiscal Year December 31, 2021 |

| |

|

|

|

| |

Financial Summary (Audited) |

|

|

| |

Cash and Deposits |

| $ | 15,609 |

|

Total Assets |

|

| 76,150 |

|

Total Liabilities |

|

| 384,249 |

|

Total Stockholder’s Equity (Deficit) |

| $ | (308,099 | ) |

|

| For the Fiscal Year ended December 31, 2021 |

| |

|

|

|

| |

Consolidated Statements of Expenses and Net Loss |

|

|

| |

Total Operating Expenses |

| $ | 295,409 |

|

Net Loss for the Period |

| $ | (287,763 | ) |

|

| For the Fiscal Quarter June 30, 2022 |

| |

|

|

|

| |

Financial Summary (Unaudited) |

|

|

| |

Cash and Deposits |

| $ | 70,507 |

|

Total Assets |

|

| 117,597 |

|

Total Liabilities |

|

| 473,315 |

|

Total Stockholder’s Equity (Deficit) |

| $ | 355,718 |

|

|

| For the Fiscal Quarter ended June 30, 2022 |

| |

|

|

|

| |

Consolidated Statements of Expenses and Net Loss |

|

|

| |

Total Operating Expenses |

| $ | 30,431 |

|

Net Loss for the Period |

| $ | (29,124 | ) |

| 12 |

| Table of Contents |

RISK FACTORS

An investment in our common stock involves a number of very significant risks. You should carefully consider the following known material risks and uncertainties in addition to other information in this prospectus in evaluating our company and its business before purchasing shares of our company’s common stock. You could lose all or part of your investment due to any of these risks.

RISKS RELATING TO OUR COMPANY

Our auditors have expressed substantial doubt about our ability to continue as a going concern.

Our audited financial statements for the period from March 15, 2016 (inception) through December 31, 2021 were prepared assuming that we will continue our operations as a going concern. Our wholly-owned subsidiary, Nemo Holding Company Limited, was incorporated on April 16, 2016, and does not have a history of earnings. As a result, our independent accountants in their audit report have expressed substantial doubt about our ability to continue as a going concern. Continued operations are dependent on our ability to complete equity or debt financings or generate profitable operations. Such financings may not be available or may not be available on reasonable terms. Our financial statements do not include any adjustments that may result from the outcome of this uncertainty.

If our estimates related to future expenditures are erroneous or inaccurate, our business will fail and you could lose your entire investment.

Our success is dependent in part upon the accuracy of our management’s estimates of our future cost expenditures for legal and accounting services (including those we expect to incur as a publicly reporting company), for website marketing and development expenses, and for administrative expenses, which management estimates to be approximately $10,000,000 over the next twelve months. If such estimates are erroneous or inaccurate, or if we encounter unforeseen costs, we may not be able to carry out our business plan, which could result in the failure of our business and the loss of your entire investment.

If we are not able to develop our business as anticipated, we may not be able to generate revenues or achieve profitability and you may lose your investment.

Our wholly-owned subsidiary, Nemo Holding Company Limited, was incorporated on April 16, 2020, and our net loss for the period from inception (March 15, 2016) to June 30, 2022 was $(4,690,647). We have few customers, and we have not earned substantive revenues to date. Our business prospects are difficult to predict because of our limited operating history, and unproven business strategy. Our primary business activities will be focused on the commercialization of licensing our New Momentum brand. Although we believe that our business plan has significant profit potential, we may not attain profitable operations and our management may not succeed in realizing our business objectives. If we are not able to develop out business as anticipated, we may not be able to generate revenues or achieve profitability and you may lose your entire investment.

Potential disputes related to the existing agreement pursuant to which we purchased the intellectual property rights underlying our business could result in the loss of rights that are material to our business.

The acquisition of the intellectual property of New Momentum, by way of the Share Exchange Agreement, by and among the Company, New Momentum Corporation, and the holders of common stock of New Momentum, is of critical importance to our business and involves complex legal, business, and scientific issues. Although we have clear title to and no restrictions to use our intellectual property, disputes may arise regarding the Share Exchange Agreement, including but not limited to, the breaches of representations or other interpretation-related issues. If disputes over intellectual property that we have acquired under the Share Exchange Agreement prevent or impair our ability to maintain our current intellectual property, we may be unable to successfully develop and commercialize our business.

| 13 |

| Table of Contents |

We expect to suffer losses in the immediate future that may cause us to curtail or discontinue our operations.

We expect to incur operating losses in future periods. These losses will occur because we do not yet have substantive revenues to offset the expenses associated with the development of brand and our business operations, generally. We cannot guarantee that we will ever be successful in generating revenues in the future. We recognize that if we are unable to generate revenues, we will not be able to earn profits or continue operations. There is no history upon which to base any assumption as to the likelihood that we will prove successful, and we can provide investors with no assurance that we will generate any operating revenues or ever achieve profitable operations. If we are unsuccessful in addressing these risks, our business will almost certainly fail.

We may not be able to execute our business plan or stay in business without additional funding.

Our ability to generate future operating revenues depends in part on whether we can obtain the financing necessary to implement our business plan. We will likely require additional financing through the issuance of debt and/or equity in order to establish profitable operations, and such financing may not be forthcoming. As widely reported, the global and domestic financial markets have been extremely volatile in recent months. If such conditions and constraints continue or if there is no investor appetite to finance our specific business, we may not be able to acquire additional financing through credit markets or equity markets. Even if additional financing is available, it may not be available on terms favorable to us. At this time, we have not identified or secured sources of additional financing. Our failure to secure additional financing when it becomes required will have an adverse effect on our ability to remain in business.

Any significant disruption in our website and mobile application presence or services could result in a loss of customers.

Our plans call for our customers to access our service through our website, www.gagfare.com and our mobile applications. Our reputation and ability to attract, retain and serve our customers will be dependent upon the reliable performance of our website, network infrastructure and fulfillment processes (how we deliver services purchased by our customers). Prolonged or frequent interruptions in any of these systems could make our website unavailable or unusable, which could diminish the overall attractiveness of our subscription service to existing and potential customers.

Our servers will likely be vulnerable to computer viruses, physical or electronic break-ins and similar disruptions, which could lead to interruptions and delays in our service and operations and loss, misuse or theft of data. It is likely that our website will periodically experience directed attacks intended to cause a disruption in service, which is not uncommon for web-based businesses. Any attempts by hackers to disrupt our website service or our internal systems, if successful, could harm our business, be expensive to remedy and damage our reputation. Efforts to prevent hackers from entering our computer systems are expensive to implement and may limit the functionality of our services. Any significant disruption to our website or internal computer systems could result in a loss of subscribers and adversely affect our business and results of operations.

Our connections to the airline booking systems may be interrupted and causing delays or unavailability to search and book the flight tickets, which may affect the user experiences and trust significantly.

Technology changes rapidly in our business and if we fail to anticipate or successfully implement new technologies or the manner in which use our products and services, the quality, timeliness and competitiveness of our products and services will suffer.

Rapid technology changes in our industry require us to anticipate, sometimes years in advance, which technologies we must implement and take advantage of in order to make our products and services competitive in the market. Therefore, we must start our product development with a range of technical development goals that we hope to be able to achieve. We may not be able to achieve these goals, or our competition may be able to achieve them more quickly and effectively than we can. In either case, our products and services may be technologically inferior to our competitors’, less appealing to consumers, or both. If we cannot achieve our technology goals within the original development schedule of our products and services, then we may delay their release until these technology goals can be achieved, which may delay or reduce revenue and increase our development expenses. Alternatively, we may increase the resources employed in research and development in an attempt to accelerate our development of new technologies, either to preserve our product or service launch schedule or to keep up with our competition, which would increase our development expenses. Any such failure to adapt to, and appropriately allocate resources among, emerging technologies would harm our competitive position, reduce our market share and significantly increase the time we take to bring our product to market.

| 14 |

| Table of Contents |

Our potential customers will require a high degree of reliability in the delivery of our services, and if we cannot meet their expectations for any reason, demand for our products and services will suffer.

Our success depends in large part on our ability to assure generally error-free services, uninterrupted operation of our network and software infrastructure, and a satisfactory experience for our customers’ end users when they use Internet-based communications services. To achieve these objectives, we depend on the quality, performance and scalability of our products and services, the responsiveness of our technical support and the capacity, reliability and security of our network operations. We also depend on third parties over which we have no control. For example, our ability to serve our customers is based solely on our network access agreement with one service provider and on that service provider’s ability to provide reliable Internet access. Due to the high level of performance required for critical communications traffic, any failure to deliver a satisfactory experience to end users, whether or not caused by our own failures could reduce demand for our products and services.

If we fail to promote and maintain our brand in an effective and cost-efficient way, our business and results of operations may be harmed.

We believe that developing and maintaining awareness of our brand effectively is critical to attracting new and retaining existing customers. Successful promotion of our brand and our ability to attract customers depends largely on the effectiveness of our marketing efforts and the success of the channels we use to promote our services. It is likely that our future marketing efforts will require us to incur significant additional expenses. These efforts may not result in increased revenues in the immediate future or at all and, even if they do, any increases in revenues may not offset the expenses incurred. If we fail to successfully promote and maintain our brand while incurring substantial expenses, our results of operations and financial condition would be adversely affected, which may impair our ability to grow our business.

Declines or disruptions in the travel industry could adversely affect our business and financial performance.

Our financial results and prospects are almost entirely dependent upon the sale of travel services. Travel, including accommodation (including hotels, motels, resorts, homes, apartments and other unique places to stay), rental car and airline ticket reservations, is significantly dependent on discretionary spending levels. As a result, sales of travel services tend to decline during general economic downturns and recessions and times of political or economic uncertainty as consumers engage in less discretionary spending, are concerned about unemployment or inflation, have reduced access to credit or experience other concerns or effects that reduce their ability or willingness to travel.

Perceived or actual adverse economic conditions, including slow, slowing or negative economic growth, high or rising unemployment rates, inflation and weakening currencies, and concerns over government responses such as higher taxes or tariffs, increased interest rates and reduced government spending, could impair consumer spending and adversely affect travel demand.

These and other macro-economic uncertainties, such as oil prices, geopolitical tensions and differing central bank monetary policies, have led to significant volatility in the exchange rates between the U.S. Dollar and the Euro, the British Pound Sterling and other currencies. Significant fluctuations in foreign currency exchange rates, stock markets and oil prices can also impact consumer travel behavior. For example, although lower oil prices may lead to increased travel activity as consumers have more discretionary funds and airline fares decrease, declines in oil prices may be indicative of broader macro-economic weakness, which in turn could negatively affect the travel industry, our business and results of operations. Conversely, higher oil prices may result in higher airfares and decreased travel activity, which can negatively affect our business and results of operations.

The uncertainty of macro-economic factors and their impact on consumer behavior, which may differ across regions, makes it more difficult to forecast industry and consumer trends and the timing and degree of their impact on our markets and business, which in turn could adversely affect our ability to effectively manage our business and adversely affect our results of operations.

| 15 |

| Table of Contents |

In addition, events beyond our control, such as oil prices, stock market volatility, terrorist attacks, unusual or extreme weather or natural disasters such as earthquakes, hurricanes, tsunamis, floods, fires, droughts and volcanic eruptions, travel-related health concerns including pandemics and epidemics such as coronaviruses, Ebola and Zika, political instability, changes in economic conditions, wars and regional hostilities, imposition of taxes, tariffs or surcharges by regulatory authorities, changes in trade policies or trade disputes, changes in immigration policies, travel-related accidents or increased focus on the environmental impact of travel, have previously and may in the future disrupt travel, limit the ability or willingness of travelers to visit certain locations or otherwise result in declines in travel demand and adversely affect our business and results of operations. Because these events or concerns, and the full impact of their effects, are largely unpredictable, they can dramatically and suddenly affect travel behavior by consumers, and therefore demand for our services and our relationships with travel service providers and other partners, any of which can adversely affect our business and results of operations. Certain jurisdictions, particularly in Europe, are considering regulations intended to address the issue of “overtourism,” including by restricting access to city centers or popular tourist destinations or limiting accommodation offerings in surrounding areas, such as by restricting construction of new hotels or the renting of homes or apartments. Such regulations could adversely affect travel to, or our ability to offer accommodations in, such markets, which could negatively impact our business, growth and results of operations. The United States has implemented or proposed, or is considering, various travel restrictions and actions that could affect U.S. trade policy or practices, which could also adversely affect travel to or from the United States.