Use these links to rapidly review the document

TABLE OF CONTENTS

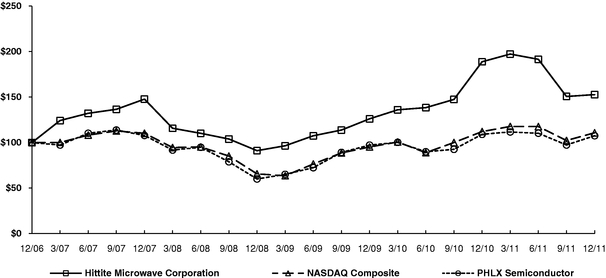

INDEX TO CONSOLIDATED FINANCIAL

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

| ý | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

For the Fiscal Year Ended December 31, 2011 |

||

or |

||

| o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

Commission File Number: 000-51448 |

||

HITTITE MICROWAVE CORPORATION

(Exact name of registrant as specified in its charter)

| DELAWARE (State or other jurisdiction of incorporation or organization) |

04-2854672 (I.R.S. Employer Identification No.) |

|

2 ELIZABETH DRIVE CHELMSFORD, MA 01824 (Address of principal executive offices) |

||

Telephone Number: (978) 250-3343 Securities registered pursuant to Section 12(b) of the Act: |

||

| Title of Each Class | Name of Each Exchange on Which Registered | |

| Common Stock, $.01 par value | The Nasdaq Stock Market, LLC (Nasdaq Global Select Market) |

|

Securities registered pursuant to Section 12(g) of the Act: |

||

| None. Title of each class |

||

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ý No o

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act. Yes o No ý

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ý No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ý No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See definition of "large accelerated filer," "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act.

| Large accelerated filer ý | Accelerated filer o | Non-accelerated filer o (Do not check if a smaller reporting company) |

Smaller reporting company o |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No ý

The aggregate market value of the voting and non-voting common equity held by non-affiliates as of June 30, 2011 was $1,914,498,773.

As of February 15, 2012 there were 31,448,089 common shares outstanding.

Documents Incorporated by Reference

Portions of the definitive Proxy Statement for the 2012 Annual Meeting of Shareholders to be filed with the Securities and Exchange Commission on or before April 29, 2012 are incorporated by reference in Part III of this Annual Report on Form 10-K.

HITTITE MICROWAVE CORPORATION

FORM 10-K

FOR THE FISCAL YEAR ENDED DECEMBER 31, 2011

INDEX

Our Company

We design and develop high performance integrated circuits (ICs), modules, subsystems and instrumentation for technically demanding radio frequency (RF) microwave and millimeterwave applications. As a result of our 27 years of experience and innovation, we have developed a deep knowledge of analog, digital and mixed-signal semiconductor technology, from the device level to the design and assembly of complete subsystems. Our fabless business model enables us to leverage our broad engineering, assembly and test capabilities and our intellectual property portfolio, including our semiconductor modeling expertise and library of proprietary circuit designs.

Industry Background

Growth in advanced electronic systems using RF, microwave and millimeterwave technology

Global demand for mobile communication services and for real-time access to diverse types of data continues to increase. This demand, coupled with the increasing capabilities and decreasing cost of computing devices, has led to rapid adoption of a wide variety of advanced electronic systems that rely on electromagnetic waves for high speed data transmission, reception or acquisition. These systems utilize a variety of data transmission technologies over a wide range of electromagnetic frequency bands, including RF, microwave and millimeterwave frequencies. These advanced electronic systems are integral to wireless networks such as cellular telephone, fixed wireless and satellite communication systems, as well as wired networks such as cable TV, broadband access and optical data networks. In addition, an increasing number of automotive, industrial, military, homeland security, scientific and medical applications use RF, microwave and millimeterwave technology to perform detection, measurement and imaging functions. All of these applications increase the demand for high speed networking equipment. The growth of advanced electronic systems using RF, microwave and millimeterwave technologies has accelerated demand for analog, digital and mixed-signal ICs, modules, subsystems and instrumentation that are optimized to provide high performance signal processing across the electromagnetic frequency spectrum.

The electromagnetic frequency spectrum

The terms RF, microwave and millimeterwave refer generally to electromagnetic waves that are propagated when an alternating current is applied to an antenna or conductor. The properties and uses of electromagnetic energy depend on its frequency. Each type of system typically uses a different frequency range, or band, of the frequency spectrum. For example:

- •

- Broadband access devices, cellular telephone systems, cable TV systems, global positioning system (GPS) equipment and

magnetic resonance imaging machines typically operate in what we refer to as the RF frequency band, between one megahertz and six gigahertz (GHz).

- •

- Direct broadcast satellite receivers, military electronic countermeasure systems and

point-to-point radio systems used in cellular backhaul applications commonly use frequencies in what we refer to as the microwave frequency band, between six GHz and

20 GHz.

- •

- Automotive collision avoidance systems, ground uplink and downlink stations used in satellite communications systems and many commercial and military radar systems operate in what we refer to as the millimeterwave frequency band, between 20 GHz and 110 GHz.

Access to specific bands of the frequency spectrum is limited due to spectrum capacity constraints. Frequency use is regulated globally by government agencies, which assign each type of communication service to one or more specific frequency bands. Growth in the volume of communications traffic, and

2

increasing demand for services such as multimedia that require higher data rates and consequently consume greater bandwidth, have resulted in more extensive use of the frequency spectrum.

Congestion of the limited available frequency bands is driving the telecommunications industry to develop more creative and efficient uses of available frequency spectrum. For example, some applications, such as newer 3G and 4G cellular telephone systems, have migrated to higher frequencies, which are inherently able to provide higher data transfer rates. Other applications, such as broadband wireless local loop applications, and cellular telephone systems being deployed in developing nations, take advantage of recently introduced modulation schemes to utilize lower frequency bands more efficiently. Still others, such as emerging ultra wide band systems, use new system architectures and complex modulation schemes to distribute data over the entire frequency spectrum. The implementation of these more complex system architectures and modulation schemes, and their distribution over a wider portion of the frequency spectrum, increase the technical challenges associated with the design and manufacture of ICs, modules, subsystems and instrumentation used in these systems.

Requirements of manufacturers of advanced electronic systems operating at RF, microwave and millimeterwave frequencies

The need for advanced electronic systems offering improved functionality, reliability and speed has intensified the challenges faced by original equipment manufacturers (OEMs) that design and develop these systems. Many OEMs do not have the IC design or semiconductor process expertise necessary to develop their own ICs, modules, subsystems and instrumentation for RF, microwave and millimeterwave applications. As a result, they increasingly look to qualified merchant suppliers to provide this expertise and these solutions and, in many cases, to design and manufacture custom products to meet their application-specific requirements.

Across all markets, OEMs seek semiconductor suppliers that provide technology that will enable them to differentiate their product offerings with respect to a number of criteria, including:

High performance. OEMs face continuously increasing competitive pressures to improve their products' overall system performance. As a result, OEMs require advanced semiconductor products that offer performance attributes such as higher power and linearity, lower noise, reduced power consumption, improved signal level and frequency accuracy and better isolation.

High reliability. OEMs seek suppliers with a demonstrated track record of delivering high quality products that will perform reliably for long periods of time under a variety of conditions. Manufacturers of advanced electronic systems used in certain commercial, military and aerospace applications have particularly stringent reliability requirements that mandate specialized design and manufacturing, quality assurance and testing processes.

Increased integration. Under constant pressure to offer their customers lower prices, OEMs seek to simplify their assembly operations and reduce their manufacturing costs by using more highly integrated components that combine multiple functions, thereby reducing design complexity, component count and system size.

Streamlined procurement processes. OEMs desiring to streamline their procurement processes seek suppliers with the proven ability to provide a broad range of products covering the full range of functions required for the design and manufacturing of high performance electronic systems that operate across the frequency spectrum.

Faster time to market. OEMs seek to shorten their product development cycles by outsourcing the highly specialized task of designing and manufacturing RF, microwave and millimeterwave

3

semiconductor products. Additionally, they select vendors that have strong manufacturing and product fulfillment capabilities and can meet short delivery lead time requirements.

An OEM's requirements may vary by market and application. In a particular application, an OEM may seek a highly integrated subsystem, while for another application the same OEM may prefer a single function IC that offers a specific performance attribute. A manufacturer of systems designed for consumer markets may require a supplier that can meet high volume manufacturing requirements, while that same manufacturer, when addressing military or aerospace markets, may require relatively low volumes of highly specialized, high value subsystems.

Challenges of developing ICs for manufacturers of advanced electronic systems

Advanced electronic systems typically rely upon a complex chain of analog and digital signals. Conversion of continuously varying real-world analog signals to binary digital form, and vice versa, and other signal transformations are known as signal processing functions. Semiconductor devices that combine analog and digital signal processing are referred to as mixed-signal ICs. The performance of an advanced electronic system depends substantially on the performance of the analog and mixed-signal ICs that provide its core functionality. Significant challenges are involved in designing and manufacturing analog and mixed-signal ICs that will operate satisfactorily at RF, microwave and millimeterwave frequencies, including the following:

RF, microwave and millimeterwave circuit design. RF, microwave and millimeterwave circuit design requires an understanding of complex electromagnetic and mathematical theory. Success in this field requires a combination of advanced scientific study and practical experience in implementing design techniques. Performance characteristics such as linearity and efficiency that are critical to electronic communications are more difficult to achieve at RF, microwave and millimeterwave frequencies. Unlike digital circuits, the performance of analog and mixed-signal circuits operating at these frequencies is affected by temperature, power supply and other external factors, as well as by the interaction of adjacent circuit elements. The design of an analog or mixed-signal circuit requires a sophisticated understanding of the complex interaction of all of these variables and the ability to predict, or model, the behavior of the IC under a variety of conditions.

Semiconductor device modeling. Creating an accurate device-level model of a semiconductor is fundamental to successful circuit design, particularly when the circuit is to be used at higher frequencies. The ability to predict the performance of a device manufactured using a particular process is necessary to enable a designer to modify the circuit design in order to meet the customer's requirements. Accurate device modeling requires the ability to measure and predict the behavior and interaction of the active and passive elements on a semiconductor under a range of conditions, including temperature, input power levels, frequency and voltage. Device modeling requires specialized skills and equipment, and engineers often develop proprietary methods to measure and validate the accuracy of their models. Because modeling is an iterative process, the accuracy, and thus the value, of device models increases with experience in using them over time.

Integration. Advances in gallium arsenide (GaAs) and silicon semiconductor technology have enabled higher degrees of integration in the design and manufacture of semiconductor devices. For example, analog and digital signal processing can now be combined on a single monolithic microwave integrated circuit (MMIC) or system on a chip (SOC). It has also become possible to combine multiple MMICs into a multi-chip module (MCM), which integrates multiple functions required by an advanced electronic system into a single compact package. Because MCMs can combine MMICs manufactured under different semiconductor process technologies, they can take advantage of the process technology that is best suited for each function. Higher degrees of integration can also be attained through the assembly of a number of MCMs into subsystems that provide greater functionality and can be more easily incorporated into an OEM's product.

4

The benefits of higher integration to an OEM can include superior performance, higher reliability, smaller form factor, lower parts count and simplified assembly processes. However, in order to deliver the benefits of higher integration to an OEM effectively, a semiconductor supplier must possess a broad range of engineering capabilities, including expertise in device modeling and the ability to optimize IC design and component interfaces based on system-level knowledge. The necessary capabilities also include the ability to manage the thermal, mechanical and package engineering issues that affect the performance of a highly integrated system, as well as the capability to perform more complex assembly and test operations.

As a result of all these factors, the knowledge and skills required to design integrated analog and mixed-signal devices operating at higher frequencies are highly specialized and can take many years to develop. We believe that a significant market opportunity exists for a supplier of high performance ICs, modules, subsystems and instruments optimized for RF, microwave and millimeterwave applications that can meet OEMs' diverse requirements.

Our Competitive Strengths

Our key competitive strengths as we address market opportunities include:

- •

- advanced RF, microwave and millimeterwave engineering capabilities;

- •

- ability to optimize circuit design and semiconductor process and packaging technologies to meet customers' application

requirements;

- •

- broad product portfolio, comprising 34 product lines;

- •

- diverse customer base, markets and applications;

- •

- multi-channel sales and support capabilities; and

- •

- our fabless business model.

Advanced RF, microwave and millimeterwave engineering capabilities. We have developed broad expertise in a number of disciplines that are critical to the design and manufacture of ICs, modules, subsystems and instruments for technically demanding RF, microwave and millimeterwave applications. These include:

- •

- analog, digital and mixed-signal IC design;

- •

- SOC design;

- •

- semiconductor device modeling;

- •

- RF, microwave and millimeterwave system, subsystem and instrument design;

- •

- mechanical, thermal and packaging engineering;

- •

- digital hardware and related software engineering;

- •

- automated test software engineering; and

- •

- manufacturing, process and quality engineering.

Our knowledge of analog and mixed-signal semiconductor technology, from the device level to the design and assembly of subsystems and instruments optimized for RF, microwave and millimeterwave applications, enables us to deliver high performance, high value products to our customers.

Ability to optimize circuit design and semiconductor process and packaging technologies to meet customers' application requirements. Based on customers' requirements, we select the foundry and semiconductor process that we believe will provide the best combination of performance attributes and form factor for use in that application. We also have expertise in a range of industry standard and proprietary packaging technologies. Our fabless business model and broad engineering expertise enable us to optimize our product designs using the semiconductor process and packaging technology that best address our customers' needs.

5

Broad product portfolio. We offer a broad range of standard and custom ICs, modules, subsystems and instrumentation that perform a variety of functions across the RF, microwave and millimeterwave frequency bands. At December 31, 2011, we had more than 980 standard products which may be categorized for descriptive purposes into 34 functional product lines:

- •

- amplifiers

- •

- attenuators

- •

- automatic gain control

- •

- broadband time delays

- •

- clocks and timing

- •

- comparators

- •

- crosspoint switches

- •

- data converters

- •

- DC power conditioning

- •

- DC power management

- •

- dielectric resonator oscillators

- •

- filters-tunable

- •

- frequency dividers and detectors

- •

- frequency multipliers

- •

- high speed digital logic

- •

- IF signal processing

- •

- interface

- •

- limiting amplifiers

- •

- mixers and converters

- •

- modulators and demodulators

- •

- multiplexer / demultiplexer (mux / demux)

- •

- optical modulator drivers

- •

- passives

- •

- phase locked loops

- •

- phase locked loops with integrated voltage controlled oscillators

- •

- phase shifters

- •

- power detectors

- •

- sensors

- •

- signal generators/instrumentation

- •

- successive detection logarithmic video amplifiers

- •

- switches

- •

- transimpedance amplifiers

- •

- variable gain amplifiers

- •

- voltage controlled oscillators and phase locked oscillators

We offer our products in a wide variety of packaging formats, as well as in modules, subsystems and instrumentation, facilitating their use in a broad range of applications. We have the ability to rapidly design, prototype and commence volume production of our products, assisting our customers in meeting their time-to-market requirements. We introduced four new product lines in 2011, six in 2010, and four in 2009. We introduced 82 new standard products in 2011, 122 in 2010, and 83 in 2009, and also added custom products in comparable numbers during those years.

Diverse customer base, markets and applications. The diversity of our customers, markets and applications provides us with multiple long-term growth opportunities. In 2011, we sold our products to approximately 3,000 commercial and U.S. government customers for use in a variety of applications and markets worldwide. Our principal markets include:

| Automotive | • | telematics and GPS systems | ||

| • | collision avoidance, blind spot detection and intelligent cruise control | |||

| • | pre-collision sensors | |||

Broadband |

• |

cable TV and cable modems |

||

| • | direct broadcast satellite | |||

| • | fixed and mobile wireless networks |

6

Cellular Infrastructure |

• |

cellular telephone 3G and 4G base stations and repeaters |

||

| • | E911 and GPS location systems | |||

Fiber Optic |

• |

communications infrastructure |

||

| • | fiber optic test equipment | |||

| • | network data communications equipment | |||

Microwave and Millimeterwave Communications |

• |

high and low capacity point-to-point and point-to-multi-point radio systems |

||

| • | commercial very small aperture terminal (VSAT) systems | |||

| • | short range local area networks | |||

Military |

• |

communications systems |

||

| • | radar, guidance and electronic countermeasure systems | |||

| • | sensing and detection platforms | |||

Space |

• |

communication and imaging payloads |

||

| • | command, control and communications for commercial, scientific and military spacecraft | |||

Test and Measurement |

• |

medical and industrial imaging systems |

||

| • | homeland security systems | |||

| • | telecommunications test equipment | |||

| • | scientific and industrial equipment |

Many of our standard products are purchased by a variety of customers in different markets for use in numerous types of applications. We believe that the diversity of our customers, markets and applications helps to mitigate the impact on our business of fluctuations in demand from any particular customer or industry.

Multi-channel sales and support capabilities. Due to the technical nature of our products and markets, we utilize a multi-channel sales and support model that is intended to facilitate our customers' evaluation and selection of our products. Our sales and support channels include our direct sales force, our applications engineering staff, our worldwide network of independent sales representatives, a distributor and our website.

We have established flexible sales and support capabilities. For example:

- •

- We offer our customers and prospective customers comprehensive technical sales support and application engineering

services, provided by dedicated staff in local offices located in key geographies, to accelerate their understanding of our products' capabilities and how best to use them in their own system designs.

Our technical sales staff frequently visits customers at their engineering and manufacturing facilities to exchange design, product and production information.

- •

- We include in our product catalog detailed technical specifications, performance data, suggested design block diagrams and

recommended applications for our standard products.

- •

- We offer comprehensive on-line technical resources and tools to assist system designers and engineers in

specifying and using our products.

- •

- We offer qualified customers free samples of our products for evaluation purposes. To accelerate evaluation and design of our products, we offer versions mounted on printed circuit boards or in modular housings to facilitate their use in experimental prototypes.

7

We believe that our multi-channel approach to sales and technical support encourages the selection of our products, results in high customer satisfaction and leads to repeat sales.

Our fabless business model. We outsource wafer manufacturing to multiple third party fabricators and foundries. We believe that this fabless business model and our expertise in a wide range of semiconductor process technologies enables us to develop products using the technology most appropriate for our customers' applications. We believe that investing in our core design and engineering competencies, including advanced RF, microwave and millimeterwave circuit design, device modeling, system-level engineering and packaging engineering, while outsourcing the capital-intensive task of semiconductor fabrication, best enables us to meet the needs of our customers.

We design, develop and sell high performance analog, digital and mixed-signal ICs, modules, subsystems and instrumentation used in technically challenging RF, microwave and millimeterwave and fiber optic communications applications. We offer a broad range of radio frequency integrated circuits (RFICs), MMICs, MCMs, subsystems and instruments that perform a variety of signal processing functions and that operate across the RF, microwave, millimeterwave and visible light frequency spectrum. Our products are used in a wide range of wired and wireless communications applications, such as cellular base stations, microwave and millimeterwave radio systems, broadband wireless access systems and direct broadcast satellite systems. They are also used in detection, measurement and imaging applications including military communication, targeting, guidance and electronic countermeasure systems, commercial, scientific and military spacecraft, automotive collision avoidance systems, medical imaging systems and industrial test equipment. We also offer products designed for use in fiber optic communications systems and in high speed data/voice/video/networking applications.

We offer standard products and custom products. We develop standard products from our own specifications and offer them for sale through our direct sales organization and network of sales representatives, a distributor and our website. We currently offer more than 980 standard products across 34 product lines. Our strategy in developing standard products is to introduce high performance products that will be valued by customers for their ability to address technically challenging applications, rather than to offer commodity ICs for use in high volume applications where cost, rather than performance, is the highest priority. We believe that many of our standard products offer a combination of form factor, functionality and performance attributes that are not available from any other supplier. The standard products listed on our website generally are purchased by multiple customers for use in a variety of applications.

We also develop custom products to meet the specialized requirements of individual customers. Our custom products are not listed on our website and are sold by our direct sales force, which works with customers and prospective customers to have our products selected and designed into our customers' systems and programs. Our custom products generally are purchased by the customer for whom they were developed.

Our IC product lines

Our product lines include most of the functional circuit blocks required to create both receiver and transmitter subsystems for any RF, microwave or millimeterwave application.

Many of our products are designed to perform across numerous frequency bands, making them useful for diverse applications. We also offer products that optimize particular performance attributes required in specific applications. These products are offered in a variety of packaging formats, including

8

bare die, surface mount packages and connectorized modules. Our current product line offerings are as follows:

- •

- Amplifiers. Amplifiers boost the gain, or power, of a signal.

We offer a broad line of amplifiers, including:

- •

- gain blocks and drivers used throughout the receiver and

transmitter sections to boost signal level;

- •

- linear driver amplifiers used in transmitters or receivers where

distortion must be minimized to maintain signal fidelity;

- •

- power amplifiers used to increase the power level of the signal in

transmitter or high power level applications;

- •

- low noise amplifiers used in the first stage of a receiver, where

amplification with minimum distortion of an incoming signal having a low power level is required; and

- •

- wideband (distributed) amplifiers having more than an octave of operating

frequency bandwidth (that is, where the highest frequency is twice the lowest frequency), used in military, space and commercial systems where a wide range of frequencies need to be processed by one

subsystem.

- •

- Attenuators. Attenuators are used to reduce the power of a

signal in specific controlled amounts without distorting the signal quality. For example, to avoid overloading a base station's receiving circuitry as a mobile transmitter approaches a base station or

tower, an attenuator is used in the receiver to optimize the received signal for processing. Our portfolio of attenuators is classified into two types:

- •

- digital attenuators that provide control of the signal in response to a

digital logic input and deliver preprogrammed levels of attenuation according to the digital input; and

- •

- voltage variable attenuators that provide control of the signal in

response to an analog direct current (DC) voltage input and can deliver continuously varying, very fine to very large levels of attenuation.

- •

- Automatic gain control. Automatic gain control (AGC) is a

control technique employed in almost every transceiver. The average output signal of a transceiver is fed back to adjust the gain to an appropriate level for a range of input signal levels. An AGC

circuit uses a controller which can adjust the gain of the signal chain inversely proportionally to the error between desired and measured output signal amplitude or power. An AGC circuit usually

requires three separate, discrete ICs; a variable gain amplifier, a controller, and power level sensor. Typical applications for these products include microwave radio, cellular repeater/boosters,

military radios, VSAT, test equipment, sensors and WiMAX/LTE/4G systems.

- •

- Broadband time delays. Broadband time delays provide a highly

accurate and stable time delay for signals that are transmitted through them. The desired delay is controlled by either an analog or digital voltage and may be varied over a specified range. These

devices also feature internal circuitry to minimize delay variations with temperature changes or power supply changes. Our broadband time delay products are optimized for the synchronization of clock

and data signals or for timing compensation in optical communication and high speed data networking systems.

- •

- Clocks and timing. Clocks and timing products are vitally important in the generation and synchronization of signals in digital and RF/microwave systems to facilitate communication between the various system nodes. These synchronization signals often take the form of a clock signal which is a very stable, repeating pattern of 1s and 0s. Each node in the system operates

9

- •

- clock distribution products ensure that each section of the system

receives a good, stable copy of the primary reference clock; and

- •

- clock generators produce primary signal references, and are therefore

central to many communication systems.

- •

- Comparators. Comparators are devices that constantly monitor

signal levels at its inputs. The device generates a digital output signal based on the difference in amplitude of the input signal levels. Our high speed comparators are optimized for high speed

military, test equipment and industrial/medical equipment applications and exhibit low propagation dispersion, short minimum detectable pulse widths and low power consumption. Our comparator types

include clocked, latched and window.

- •

- Crosspoint switches. Crosspoint switches are used for routing

high speed signals across data and voice communications equipment backplanes. These devices are specified as N×M, with the first number (N) representing the number of inputs and the

last number (M) representing the number of output crosspoints. Any input signal may be routed from a given input port to any combination of output ports based on the appropriate condition of

the control signals. Our crosspoint switch products are optimized for driving and receiving high speed signals and are ideal for 10 GbE, 16G fibre channel and high speed data and wideband video

network applications.

- •

- Data converters. Data converters are used to convert signals

between analog and digital format. Our product line includes:

- •

- analog-to-digital converters (ADCs) convert analog

input voltages to a digital number which is proportional to the magnitude of the input voltage. Our standard ADC portfolio includes high performance, low power ADCs with up to 8 individual channels,

and ultra high speed ADC products with best in class linearity and low power consumption. Our ADCs are designed to meet the requirement of the most demanding high performance signal processing

applications; and

- •

- track-and-hold (T/H) amplifiers that sample a

continuously varying analog signal and convert it in a sequence of constant levels to eliminate signal variations for signal processing and conversion. Our T/H products are designed to provide

significant improvement in bandwidth and performance to wideband sampled signal systems.

- •

- DC power conditioning. A power conditioner supplies DC power

to an integrated circuit. Our power conditioner regulates the voltage level of a DC power supply, and removes unwanted noise and spurious products that can be detrimental to the performance of

integrated circuits. Our power conditioner products are optimized for frequency generation applications and provide up to four independent regulated outputs with excellent power supply rejection ratio

(PSRR).

- •

- DC power management. A power management device provides

appropriately regulated and filtered DC power supply voltages and currents to integrated circuits. The DC voltage and current outputs of the power management device are controlled within narrow limits

regardless of variations in the main power supplied to it. Our active bias controller is a complete biasing and monitoring solution and may be paired with many of our Class-A regime MMIC

amplifiers as well as those of our competitors, used in boosting the gain of a signal.

- •

- Dielectric resonator oscillators. An oscillator is a device that produces a frequency. A dielectric resonator oscillator (DRO) is a class of oscillator in which the output frequency is mechanically stabilized over a very narrow range by a resonating dielectric material. Our DRO products are

with this common clock signal in order to achieve synchronization. Our portfolio of clocks and timing products is classified into two types:

10

- •

- Filters-tunable. Tunable filters provide variable bandwidth

across a frequency range and are used in radio receivers, transmitters, test instrumentation, military, space and industrial applications to remove unwanted mixer image signals or undesirable local

oscillator harmonics, or may be used for baseband anti-alias protection. We offer four types of tunable filters:

- •

- band pass filters that offer user-selectable pass band

frequencies and cover the frequency spectrum from 1.0 to 37.0 GHz;

- •

- band reject filters that offer a user-selectable cutoff

frequency and cover frequency bands from 0.1 to 25 GHz;

- •

- low pass filters that offer a user-selectable cutoff frequency

and cover frequency bands from DC to 7.6 GHz; and

- •

- dual programmable low pass filters that are

6th order, fully calibrated and offer programmable bandwidth from 3.5 to 50.0 MHz.

- •

- Frequency dividers and detectors. Frequency dividers, also

called prescalers, and phase-frequency detectors are used in frequency generation circuits, to help process and distribute the carrier frequency of the system. We offer a full range of frequency

dividers and phase-frequency detectors. Our frequency dividers and detectors are used in military, space and commercial systems where very low noise is required or where a wide range of frequencies

need to be processed by one subsystem. Our dividers and detectors include:

- •

- dividers (prescaler) and counter that provide fixed division

ratios, including innovative divide-by-3 and divide-by-5 ratios, by dividing and digitizing a frequency without generating unwanted noise to enable the

synthesizer to lock on the desired output signal;

- •

- programmable divider that provide continuous integer division ratios from

1 to 32 in response to digital logic input; and

- •

- phase-frequency detectors that are used to detect the frequency and phase

of an input signal accurately, and can be combined with a divider to detect an incoming frequency and divide it by a predetermined factor.

- •

- Frequency multipliers. Frequency multipliers are used in

frequency generation circuits, or synthesizers, to increase by a predetermined factor the carrier frequency and to help distribute it throughout the system. We offer a full range of active and passive

frequency multiplier products, including:

- •

- active multipliers that utilize external DC power and integrate gain

and/or power amplification with frequency multiplier circuits (factors of 2, 3, 4, 8 or 16) to deliver output power levels the same as the input level or higher; and

- •

- passive multipliers, or frequency doublers that rely on a higher input

signal power level while utilizing no DC power, to deliver a signal that is two times the input frequency.

- •

- High speed digital logic. High speed digital logic products are used to select, split, invert, route, multiply or delay high speed digital signals. High performance digital systems require these functions to route the signal throughout a digital backplane. Our high speed digital logic products can support digital signals with data rates of 13, 26 and 40 Gb/s, which makes them suitable for OC-48, OC-192 and OC-768 applications. These products include functions such as clock distribution, clock dividers, fanout buffers, flip-flops, XOR and NAND logic gates, NRZ to RZ converters, and selectors.

optimized for military, test equipment and industrial/medical equipment applications, and are characterized by their low phase noise, low temperature drift and robust packaging.

11

- •

- IF signal processing. In a receiver, intermediate frequency

(IF) signal processing involves the amplification and filtering of the desired signal after down conversion and prior to analog-to-digital conversion. In a transmitter, it

involves the amplification and filtering of the desired signal after digital-to-analog conversion and before upconversion to the RF or microwave frequency. Our IF signal IC

products include:

- •

- dual differential programmable low pass filters that support arbitrary

bandwidths from 3.5 MHz to 50 MHz, with very high accuracy; and

- •

- dual, differential digitally programmable, baseband variable gain

amplifiers that provide discrete gain level changes over a 40 dB range and high linearity performance.

- •

- Interface. Interface products are used in the digital or

analog control of integrated circuits. Our interface devices convert a serial or parallel logic input to a six bit wide complementary output, and can be used to simplify the control of digital

attenuators, digital phase shifters, digital variable gain amplifiers and switch matrices.

- •

- Limiting amplifiers. Limiting amplifiers increase the gain of

a digital signal, and have the feature of adding more gain to low level signals, and less gain to high level signals. Our limiting amplifier products are optimized for fiber optic communications and

feature low jitter and high data rate capability.

- •

- Mixers and converters. Mixers, upconverters and

downconverters are used to transform frequencies from a higher frequency input to a lower intermediate frequency, or vice versa, for easier processing of the signal. The input signal is combined with

a fixed carrier signal generated by a local oscillator (LO) to produce the higher or lower output frequency. Our standard mixer and converter products include:

- •

- mixers in a variety of types including single, double & triple

balanced mixers, sub-harmonic mixers, high IP3 mixers and I/Q mixers and image reject mixers, each utilizing our proprietary transformer circuit technology; and

- •

- converters including downconverter RFICs, I/Q downconverters / receivers,

I/Q upconverters / transmitters and sub-harmonic, which combine multiple functions such as LO drivers, gain blocks, low noise amplifiers and mixer circuits on a single IC or in a single

package.

- •

- Modulators and demodulators. Modulators are used in radio

transmitters to combine a digital information signal with an analog carrier signal generated by a local oscillator (LO). Demodulators are used in radio receivers to extract the digital information

signal from the analog carrier signal. Our modulators and demodulators address a variety of modulation schemes and feature high linearity, low noise and wide bandwidth. Our modulator and demodulator

products include:

- •

- bi-phase modulators based upon our double-balanced MMIC mixer

circuits and using a simple modulation format that supports low data rates;

- •

- demodulators that utilize analog and digital circuit techniques to

separate the in-phase and quadrature data from the received modulated signal;

- •

- direct quadrature modulators utilizing analog and digital circuit

techniques to support current and future high data rate modulation protocols; and

- •

- vector modulators used for error correction signal processing in high power wireless system amplifiers by enabling the variation of an incoming signal's phase and amplitude via a digital/analog dual control input.

12

- •

- Multiplexer / demultiplexer (Mux / Demux). A multiplexer

takes several separate parallel digital data streams as its input and combines them together into a serial data stream of a higher data rate. This allows multiple data streams to be carried from one

place to another over one physical link, which saves power, cost and printed circuit board area. At the receiving end of the data link a complementary demultiplexer performs the reverse operation,

taking a serial digital data bit stream at a higher rate as its input, and then breaking this data rate stream back down into several separate parallel lower data rate bit streams as its output. Our

multiplexer and demultiplexer products support analog or digital signals that operate at speeds of up to 45 Gb/s, which makes them suitable for OC-192 and OC-768 applications.

- •

- Optical modulator drivers. Optical modulator drivers are

ultra-wideband amplifiers that are optimized for driving laser modulators used in high speed fiber optic and time domain applications. Modulator driver amplifiers are optimized for operating with the

serial random high-speed digital signals. Our modulator drivers are ideal for 10G, 40G and 100G fiber optic applications both for short reach datacenter and long-haul for high

performance voltage outputs with excellent eye diagram quality. Our optical modulator driver family features very low power, low jitter, high SNR and high data rate capability.

- •

- Passives. Our passive product line consists of fixed

attenuators that operate at frequencies up to 50 GHz. Fixed attenuators, or pads, are used to accurately reduce the power level of a signal without distorting the signal's characteristics.

- •

- Phase locked loops. PLL integrated circuits are used in

conjunction with oscillators in signal generation circuitry to accurately select and stabilize the frequency of transmitted and received signals. Our PLL products are designed to minimize noise, allow

wide input bandwidth and provide advanced features. Our PLL products coupled with our VCO products can offer customers state-of-the-art signal generation

performance for the test and measurement, military and space markets.

- •

- Phase locked loops with integrated voltage controlled

oscillators. A PLL with integrated VCO produces an RF, microwave or millimeterwave frequency. Our PLL with integrated VCO products combine a fully integrated, low

noise VCO, with an advanced PLL integrated circuit. Our single-band, tri-band and wideband PLL with integrated VCO products are optimized for RF and microwave signal generation

applications, and exhibit low phase noise, low spurious products, low jitter and flexible programming capabilities.

- •

- Phase shifters. Phase shifters are used to change the phase

of an RF, microwave or millimeter wave signal while providing little or no amplitude change or distortion. High performance systems such as phased array radars, RF medical equipment, wide band

electronic warfare receivers, and time domain systems require tight design control over a signal's phase. These systems often rely on phase shifter components to maintain this control.

- •

- analog phase shifters provide continuous phase change as a function of

control voltage, often allowing over 360 degrees of phase shift; and

- •

- digital phase shifters provide discrete phase shift changes in response to a digital logic input, often in a combination of small and large phase steps.

13

- •

- Power detectors. Power detectors convert power levels of an

RF, microwave or millimeterwave signal to linear or logarithmic DC voltages that can be measured by simple digital circuitry.

- •

- Sensors. Our sensors use RF, microwave and millimeterwave

energy to detect, measure or form an image of an object. These sensor ICs integrate multiple circuit functions and are effectively subsystems on a chip. For example, we offer single chip sensors that

are used for range detection in multiple military and commercial applications.

- •

- Successive detection logarithmic video amplifiers

(SDLVAs). SDLVAs are a specialized form of power detector that operate by processing signals with much wider bandwidths, exhibiting a flatter frequency response

and providing a faster response to transient signals.

- •

- Switches. Switches are used to route signals from one or more

input paths to one or more output paths. Control of the selected input and output signal path is achieved via digital logic input. Our switches are designed to reduce signal loss, minimize noise and

interference, and operate at high frequencies and power levels. Our switch products provide the following functionality:

- •

- bypass, transfer and matrix switches that handle multiple inputs and

outputs while providing digital control, high isolation and low signal distortion and loss;

- •

- single pole multi-throw switches offering throw configurations of 3, 4, 6

and 8 while providing digital control, high isolation and low signal distortion and loss;

- •

- single pole double throw switches that offer a single input and two

outputs, while providing digital control, wide bandwidth, and low loss;

- •

- single pole double throw transmit/receive switches providing high power

handling of signals up to 10 watts of power with low distortion; and

- •

- single pole single throw switches that offer a single input and a single

output while providing digital control and high isolation or failsafe operation.

- •

- Transimpedance amplifiers. Transimpedance amplifiers are used

between devices which have very different levels of impedance or resistance. Our transimpedance amplifier provides a differential output voltage that is proportional to the current at its input, and

is optimized for photodiode and fiber optic data communication applications.

- •

- Variable gain amplifiers. Variable gain amplifiers (VGAs)

boost the gain or power of a signal and have the feature of allowing the user to set the gain or power to a specific level. Our analog and digital variable gain amplifiers utilize linear amplifiers,

high performance attenuators, and flexible driver interface circuitry.

- •

- Voltage controlled oscillators and phase locked oscillators (VCOs and

PLOs). An oscillator produces an RF, microwave or millimeterwave frequency. The output frequency of our voltage controlled oscillators (VCOs) can be varied by an

analog DC input control voltage. Our self-contained VCOs integrate all necessary circuitry on a single chip, so that no external components are required. We offer three types of MMIC

oscillators:

- •

- phase locked oscillators that offer integrated phase lock loop (PLL)

functionality for the VSAT market;

- •

- narrow band VCOs that offer narrower frequency tuning and lower phase

noise performance for microwave radio, test and measurement, military and space; and

- •

- wideband VCOs that offer octave tuning bandwidth for the test & measurement and military markets.

14

Modules, subsystems and instrumentation

Our highly integrated custom and standard modules and subsystems leverage our extensive portfolio of standard and custom ICs with our knowledge of RF, microwave and millimeterwave system design and our electrical, thermal and mechanical engineering expertise. Our modules and subsystems are mounted on either ceramic substrates or printed circuit boards in self-contained metal housings. Products include:

- •

- Signal generators / instrumentation consist of a family of synthesized

signal generators which are used by our customers in engineering, production and reliability screening applications. Our synthesized signal generators operate at frequencies up to 70 GHz, and are

designed to exhibit low phase noise, low spurious emissions, and high output power.

- •

- connectorized modules, which utilize ICs from our product lines, housed in

connectorized, hermetically sealed modules, for use in test and measurement equipment;

- •

- RF, microwave and millimeterwave receivers and synthesizers used in

military communication, targeting, guidance and countermeasure systems;

- •

- telecom and test equipment modules, such as our phase locked oscillator modules used in fiber optic test systems.

Technology

We consider the following technologies to be important in the design and manufacture of our products.

Semiconductor process technologies

We have expertise in designing RF, microwave and millimeterwave RFICs and MMICs using a variety of semiconductor manufacturing processes. Different processes produce devices that have characteristic performance attributes that are particularly suitable for specific applications. In choosing the foundry, semiconductor material and process technology to be used to manufacture a new product, we seek to optimize the match between the process technology and the desired performance parameters of the product.

Our products are manufactured using GaAs and silicon semiconductor processes, including SiGe, Bi-CMOS and CMOS. We continuously investigate advanced GaAs- and silicon-based processes that we believe may offer product performance advantages in RF, microwave and millimeterwave applications.

Packaging technologies

Interaction between an RF, microwave or millimeterwave semiconductor circuit and its package can significantly affect product performance, particularly at high frequencies. Characteristics such as the ability of the package to dissipate heat produced by the semiconductor, or to withstand vibration, shock, high temperature and humidity and other environmental conditions, are also critical in certain applications.

We carefully match the circuit design, semiconductor process and packaging technologies and, where necessary, develop new packaging technologies to ensure the product will perform as desired under the specified conditions. In this process, we use proprietary techniques to model the interaction between semiconductor and package, and our engineers make appropriate adjustments in the design of both the semiconductor and its package to take account of that interaction. We consider our expertise in package, design and modeling to be one of our core competencies and a key factor distinguishing us from our competitors.

15

We offer our products in a wide variety of packaging formats, ranging from bare die to surface mount plastic and ceramic packages and highly integrated, chassis-mounted connectorized subsystems. We offer plastic, ceramic and metal packaging formats, including many industry standard formats, as well as proprietary packaging technologies. Our microwave surface mount packages are offered in either a hermetically sealed format for military, space and high reliability commercial applications or a non-hermetically sealed format for commercial communications and sensor applications. Our highly integrated modules and subsystems are constructed utilizing a variety of formats including ceramic substrates or printed circuit boards mounted in self-contained metal housings.

When an application requires a standard packaging format, such as a product to be manufactured in large volumes using an industry standard plastic surface mount technology package, we outsource the packaging step in the manufacturing process to a third-party supplier. We typically perform the packaging of high value ceramic and metal package components in our own facility utilizing our automated wafer inspection, die attach and wire bond assembly equipment.

RoHS Directive

In response to environmental concerns, some customers and government agencies impose requirements for the elimination of hazardous substances, such as lead (which is widely used in soldering connections in the process of semiconductor packaging and assembly), from electronic equipment. For example, in 2003, the European Union (EU) adopted its Restrictions on Use of Hazardous Substances Directive (RoHS) Directive. Effective July 1, 2006, the RoHS Directive prohibits, with specified exceptions, the sale in the EU market of new electrical and electronic equipment containing more than agreed levels of lead or other hazardous materials. We have a program in place to meet these customer and governmental requirements, including the RoHS Directive, where applicable to us, by making available versions of our products that do not include lead or other hazardous substances.

Research and Development

We focus our research and development efforts on designing and introducing new and improved standard and custom products and on developing new semiconductor device modeling and advanced RF, microwave or millimeterwave circuit designs.

We have made significant investments in our core engineering capabilities, including semiconductor device modeling and advanced RF, microwave and millimeterwave circuit design. Recently, we expanded our digital software and hardware engineering capabilities to support our subsystem and instrumentation product development efforts. In the area of device modeling, we are expanding our library of device models that measure and predict the performance of a transistor within a given circuit design and packaging technology. This allows us to select the process technology that provides the best combination of performance attributes for use in a given application. Our circuit design efforts are focused on developing products that provide superior performance and reliability.

We have eight design centers, including our two primary design centers in Chelmsford, Massachusetts, and additional facilities in Cairo, Egypt; Colorado Springs, Colorado; Istanbul, Turkey; Ottawa, Ontario, Canada; Roanoke, Virginia; and Trondheim, Norway.

As part of our research and development strategy, we have and may continue to license intellectual property from third parties. For example, we use integrated circuit design and background intellectual property that we licensed from Northrop Grumman Space Technology sector in 2007 and from IBM in 2010 to further expand our millimeterwave products.

We continuously develop products using our own specifications, guided by input from our customers and market analysis, that combine technological innovation and general application. Our

16

team of experienced engineers also works closely with many of our customers to develop and introduce custom products that address the specific requirements of those customers.

Sales, Marketing and Support

We sell our products worldwide through multiple channels, including our worldwide direct sales force and applications engineering staff, our network of domestic and international independent sales representatives and our website. In addition, many of our standard products are available for sale in North America through our distributor, Future Electronics. Each of these sales channels is supported by our customer service and marketing organizations. We have sales and technical support staff in the United States, Canada, China, Finland, Germany, India, Japan, Korea, Norway, Sweden, Turkey, and the United Kingdom. We intend to expand our sales and support capabilities and our network of independent sales representatives in key regions domestically and internationally.

Our direct sales force and applications engineers provide our customers with technical assistance regarding the selection and use of our products. We believe that maintaining a close relationship with our customers and providing them with technical support improves their level of satisfaction and enables us to anticipate and influence their future product needs. We provide ongoing technical training to our distributor and sales representatives to keep them informed of our existing and new products. Our website also provides our customers with on-line tools and technical resources to help them select and use our products.

We maintain an internal marketing organization that is responsible for the production and dissemination of sales and advertising materials, such as product announcements, press releases, brochures, magazine articles, advertisements and cover features in trade journals and other publications and our product selection guide both in print and e-media. We participate in public relations and promotional events, including industry tradeshows and technical conferences. Our marketing organization is also responsible for the content and maintenance of our website.

Manufacturing

We design and develop our proprietary products and utilize third-party foundries to manufacture the semiconductors used in our products. In some cases, we use third-party suppliers to assemble our products. Outsourcing many of our manufacturing and assembly activities, rather than investing heavily in capital-intensive production facilities, provides us with the flexibility to respond to new market opportunities, simplifies our operations and significantly reduces our capital requirements.

We currently utilize a wide range of semiconductor processes to develop and manufacture our products, although each of our foundries tends to use a particular process technology in the production of its semiconductor wafers. Based on the requirements of a particular product, we choose the foundry and semiconductor process that we believe will provide the best combination of performance attributes for use in that product. For most of our products, we use a single foundry for the production of the semiconductor wafer. Our foundries are Cobham, CREE, Global Communications Semiconductors, IBM, Tower/Jazz Semiconductor, Northrop Grumman, Taiwan Semiconductor Manufacturing Company (TSMC), Telefunken Semiconductor, TriQuint Semiconductor, United Monolithic Semiconductors (UMS) and WIN Semiconductors. We are actively engaged with these and other foundries to develop device models and intellectual property which can be included in our future production or research and development programs. Because the quality and reliability of our products is critical, we carefully qualify each of our foundries and processes before applying the technology to a production program.

For most of our products, the production process begins with a GaAs or silicon semiconductor substrate, or wafer. The foundry that we select to manufacture a particular product utilizes a set of masks that are generated from our proprietary circuit layout designs. Completed wafers or die are shipped by the foundry to us or to our third-party packaging vendors. Depending on the application,

17

the integrated circuit may be sold as bare die or assembled into an injection molded plastic package or a ceramic or metal package or housing, using a wide variety of packaging technologies. Standard plastic packaged parts are assembled by third-party suppliers located primarily in Asia and the United States, while packaging of high value package components is performed primarily at our Chelmsford facility. We utilize contract manufacturers to produce complex printed circuit board assemblies for certain military and commercial subsystems and instruments. Following the assembly process, we perform a final test for validation, inspection and quality assurance purposes on all finished products before they are shipped to our customers.

Our Chelmsford manufacturing facility contains class 100K clean rooms certified for commercial, military and space level product manufacturing. Our networked material requirements planning documentation and test data acquisition systems enable us to track materials throughout our suppliers and our own facility, as well as schedule production activities and shipments based on customer demand. We utilize automated and manual test stations for each of our numerous package types, driven by proprietary test equipment configurations and software. Our manual and automatic hybrid assembly equipment includes die shear and bond pull inspection equipment, die inspect/pick, die/substrate attach and wire bond functions. We are capable of testing our products from DC up to 110 GHz, utilizing our automated and semi-automated RF, microwave and millimeterwave equipment.

We conduct environmental screening on production material, including tests such as temperature cycling and temperature shock, constant acceleration, mechanical vibration and shock, liquid and ambient burn-in, fine and gross hermetic leak test and particle impact noise detection. Our reliability test equipment includes high temperature life-test equipment, highly accelerated stress test and infrared reflow testing and acoustic sonic scanning, as well as field emission scanning electron microscope (SEM) and energy dispersive spectroscopy (EDS) capability.

Quality Assurance

We are committed to maintaining the highest level of quality in our products. Our objective is that our products meet all of our customer requirements, are delivered on-time and function reliably throughout their useful lives. As part of our total quality assurance program, our quality management system has been certified to ISO 9001 since 1997 and is ISO 9001:2008 certified. The ISO 9001:2008 standards provide models for quality assurance in design and development, production, installation and servicing. This level of quality certification is required by many of our customers. Recently, we expanded our quality initiatives and certifications to include S20.20 electrostatic discharge (ESD) management system certification and AS-9100 aerospace certification. These certifications evidence the fact that our operating policies and procedures satisfy industry requirements for our products' ESD protection and aerospace manufacturing controls. Many of our customers involved in the manufacture of systems used in military and aerospace applications have particularly stringent reliability requirements that mandate specialized manufacturing, quality assurance and testing processes. To meet these specialized needs, we have processes in place to manufacture parts to the requirements of MIL-PRF-38543/38535.

Competition

The markets for our products are extremely competitive, and are characterized by rapid technological change and continuously evolving customer requirements. We compete primarily with other suppliers of high performance analog and mixed-signal semiconductor components used in RF, microwave and millimeterwave applications. These competitors include large, diversified semiconductor manufacturers with broad product lines, such as Avago and Analog Devices, with whom we compete in a number of our markets. We also compete in specific markets or product categories with a large number of semiconductor manufacturers such as Eudyna, Linear Technology, NEC, RFMD, Skyworks, TriQuint Semiconductor and UMS. We also encounter competition from manufacturers of advanced

18

electronic systems that also manufacture semiconductor components internally. Some of these competitors, such as NEC, are also our customers. Additionally, in certain product categories we compete with semiconductor manufacturers from which we also obtain foundry services, such as TriQuint Semiconductor and UMS.

Many of our existing competitors have significantly greater financial, technical, manufacturing and marketing resources than we do and might be perceived by prospective customers to offer financial and operational stability superior to ours. This is particularly true of competitors in the markets for silicon-based products. We expect competition in our markets to intensify, as new competitors enter the RF, microwave and millimeterwave component market, existing competitors merge or form alliances, and new technologies emerge.

Intellectual Property

We seek to protect our proprietary technology under United States and foreign laws affording protection for trade secrets, and to seek United States and foreign patent, copyright and trademark protection of our products and developments where appropriate. We rely on trade secrets, patents, technical know-how and other unpatented proprietary information relating to our product development and manufacturing activities. We seek to protect our trade secrets and proprietary information, in part, by requiring our employees to enter into agreements providing for the maintenance of confidentiality and the assignment of rights to inventions made by them while employed by us. We also enter into non-disclosure agreements with our consultants, semiconductor foundries and other suppliers to protect our confidential information delivered to them.

We believe that while the protection afforded by trade secret, patent, copyright and trademark laws may provide some advantages, our ability to maintain our competitive position is largely determined by such factors as the technical and creative skills of our personnel, new product developments, and frequent product enhancements. There can be no assurance that our confidentiality agreements with employees, consultants and other parties will not be breached, that we will have adequate remedies for any breach or that our trade secrets and other proprietary information will not otherwise become known. There also can be no assurance that others will not independently develop technologies that are similar or superior to our technology or reverse engineer our products. Additionally, the laws of countries in which we operate may afford little or no protection to our intellectual property rights.

Employees

As of December 31, 2011, we had 469 full-time employees, compared with 402 full-time employees at December 31, 2010. We have never experienced a work stoppage, and none of our employees is subject to a collective bargaining agreement. We believe that our current relations with our employees are good.

19

Executive Officers and Directors of the Registrant

The following table sets forth certain information regarding our executive officers, other vice president-level officers and directors.

Name

|

Age | Position | |||

|---|---|---|---|---|---|

Stephen G. Daly |

46 | Chairman of the Board, President and Chief Executive Officer | |||

William W. Boecke |

60 |

Vice President, Chief Financial Officer and Treasurer |

|||

Everett N. Cole III |

50 |

Vice President of Hybrid Manufacturing(1) |

|||

William D. Hannabach |

49 |

Vice President of Global Operations |

|||

Norman G. Hildreth, Jr. |

48 |

Vice President |

|||

Dong Hyun (Thomas) Hwang |

48 |

Vice President of Sales |

|||

Brian J. Jablonski |

52 |

Vice President of Operations(1) |

|||

Michael A. Olson |

51 |

Vice President |

|||

Antonio Visconti |

51 |

Vice President |

|||

Ernest L. Godshalk |

66 |

Director(2) |

|||

Rick D. Hess |

58 |

Director(3) |

|||

Adrienne M. Markham |

60 |

Director(4) |

|||

Brian P. McAloon |

61 |

Director(5) |

|||

Cosmo S. Trapani |

73 |

Director(6) |

|||

Franklin Weigold |

73 |

Director(7) |

|||

- (1)

- Our

Vice President of Hybrid Manufacturing and Vice President of Operations are not executive officers. They are included pursuant to Item 401(c) of

Regulation S-K as persons who are expected to make significant contributions to our business.

- (2)

- Chairman

of the Audit Committee and member of the Compensation Committee

- (3)

- Chairman

of the Nominating and Corporate Governance Committee and member of the Audit Committee

- (4)

- Chairman

of the Compensation Committee and member of the Nominating and Corporate Governance Committee

- (5)

- Member

of the Compensation and Nominating and Corporate Governance Committees

- (6)

- Member

of the Audit and Compensation Committees

- (7)

- Lead Director and member of the Nominating and Corporate Governance Committee. Our Lead Director is a non-employee director, appointed by the Board, whose responsibilities are to preside over Board meetings in the absence of the Chairman and lead executive sessions of the Board (i.e., sessions without management present); to act as a liaison between the independent directors and the Chief Executive Officer, and facilitate discussions among the independent directors on key issues and concerns outside of Board meetings (without limiting the ability of any independent director to communicate directly with the Chairman); and to work with the Chairman to set an appropriate calendar of Board meetings and develop the agendas for Board meetings. Our Lead Director has no role in the management or operations of the Company, does not establish Company policy or strategy and, except as directed by the Board, does not act as a spokesman for the Company.

20

Stephen G. Daly has served as our President since January 2004, as our Chief Executive Officer since December 2004 and as our Chairman since December 2005. Since joining Hittite in 1996, Mr. Daly has held various positions, including Director of Marketing, Director of Sales, Principal Sales Engineer and Applications Engineer. From 1992 to 1996, Mr. Daly held sales management positions at Alpha Industries and M/A-COM, which are RF and microwave semiconductor companies. From 1988 to 1992, Mr. Daly held various microwave design engineering positions at Raytheon's Missile Systems Division and Special Microwave Device Operations Division. Mr. Daly received a B.S. in Electrical Engineering from Northeastern University.

William W. Boecke has served as our Chief Financial Officer and Treasurer since March 2001. From 1997 to 2001, Mr. Boecke served as Vice President, Corporate Controller of PRI Automation, Inc., a supplier of semiconductor manufacturing automation systems. From 1991 to 1997, Mr. Boecke served as Director of Finance of LTX Corporation, a developer of automated semiconductor test equipment. Mr. Boecke received a B.S. from St. John's University and an M.B.A. from Boston College, and is a Certified Public Accountant.

Everett N. Cole III has served as our Vice President of Hybrid Manufacturing since January 2010. From October 1997 to January 2010, Mr. Cole served as our Director of Quality. From 1985 until joining Hittite in 1997, Mr. Cole held various quality engineering positions at Raytheon's Missile Systems Division. Mr. Cole received a B.S. in Electrical Engineering from the University of Lowell and an M.S. in Manufacturing Management Science from the University of Massachusetts at Lowell.

William D. Hannabach has served as our Vice President of Global Operations since January 2010. Since joining Hittite in February 2005, Mr. Hannabach has held various positions, including Director of Operations and Director of Programs. From 2003 to 2005, Mr. Hannabach was a Global Supply Chain Strategy Program Manager at GE Healthcare. From 2000 to 2003, Mr. Hannabach was the Director of Project Management at the Surface Mount Division of Universal Instruments, a capital equipment manufacturer for the printed wire board industry. From 1985 to 2000, Mr. Hannabach held various program and operations management positions at Lockheed Martin Corporation and GE Aerospace. Mr. Hannabach received a B.S. in Mechanical Engineering from The Pennsylvania State University and an M.B.A. from Boston University.

Norman G. Hildreth, Jr. has served as Vice President since January 2010, managing research and development engineering. From January 2004 to January 2010, Mr. Hildreth served as our Vice President of Sales and Marketing, and from February 2002 to January 2004, he served as our Director of Product Development. He was employed by Sirenza Microdevices, a designer and supplier of RF components, from August 2000 to February 2002, as Vice President, Wireless Products, and Director of Fixed Wireless Products. From February 1992 to August 2000, Mr. Hildreth held various positions at Hittite including Director of Marketing, Director of Sales, Engineering Sales Manager and Senior Engineer. From 1985 to 1992 he held design engineering positions at Adams-Russell, M/A-Com and ST Olektron. Mr. Hildreth received a B.S. in Electrical Engineering from the University of Massachusetts at Dartmouth.

Dong Hyun (Thomas) Hwang has served as our Vice President of Sales since January 2010. Since joining Hittite in January 2002, Mr. Hwang has held various positions, including Asia-Pacific Regional Sales Manager and Director of Sales. From 1997 to 2002, Mr. Hwang served as Country Manager for Korea for M/A-COM. Mr. Hwang received a B.S in Electrical Engineering from Lehigh University and an M.S. in Electrical Engineering from Lehigh University.

Brian J. Jablonski has served as our Vice President of Operations since December 2005. From May 2004 to December 2005, Mr. Jablonski served as our Director of Operations. From 2003 until joining Hittite in 2004, Mr. Jablonski served as a Capital Planning Manager at Allegro Microsystems Corp., a supplier of advanced mixed signal power IC semiconductors. From 2000 to 2003, he served as

21

Materials Manager at M/A-Com and as the Director of Operations at Trebia Networks, a developer of storage networking applications. From 1986 to 2000, he served in a number of management positions, including Director of Materials, for Unitrode Integrated Circuits, a manufacturer of analog and mixed signal integrated circuits. Mr. Jablonski received a B.S. in Industrial Management from Northeastern University and an M.B.A. from New Hampshire College.