UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

(Mark One)

|

þ

|

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

For the fiscal year ended December 31, 2011

Or

|

o

|

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

For the transition period from ____________ to ______________

Commission file number 001-32521

|

NTS, Inc.

(formerly Xfone, Inc.)

|

|

(Exact name of registrant as specified in its charter)

|

|

Nevada

|

11-3618510

|

|

|

(State or other jurisdiction of

incorporation or organization)

|

(I.R.S. Employer

Identification No.)

|

5307 W Loop 289

Lubbock, Texas 79414

(Address of principal executive offices) (Zip Code)

806-771-5212

(Registrant’s telephone number, including area code)

Securities registered under Section 12(b) of the Act:

|

Title of each class registered:

|

Name of each exchange on which registered:

|

|

|

Common Stock

|

NYSE Amex LLC

|

|

|

Common Stock

|

Tel Aviv Stock Exchange Ltd.

|

Securities registered under Section 12(g) of the Act:

None.

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes o No þ

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No þ

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes þ No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

Yes þ No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. þ

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

|

Large accelerated filer o

|

Accelerated filer o

|

|

Non-accelerated filer o

(Do not check if smaller reporting company)

|

Smaller reporting company þ

|

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes o No þ

The aggregate market value of the common stock held by non-affiliates of the registrant, as of June 30, 2011, the last business day of the second fiscal quarter, was approximately $13,036,505 based on the closing price of $1.40 for the registrant’s common stock as reported on the NYSE Amex LLC. Shares of common stock held by each director, each officer and each person who owns 10% or more of the outstanding common stock have been excluded from this calculation in that such persons may be deemed to be affiliates. The determination of affiliate status is not necessarily conclusive and we have relied on information available to us regarding beneficial holder ownership as of the most recent practical date

prior to June 30, 2011.

As of March 28, 2012, there were 41,186,596 shares of our common stock issued and outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

None.

-1-

TABLE OF CONTENTS

|

Part I

|

||

|

Item 1.

|

Business

|

|

| 13 | ||

| 13 | ||

| 13 | ||

| 14 | ||

| 16 | ||

|

Part II

|

||

| 17 | ||

| 20 | ||

| 20 | ||

| 31 | ||

| 32 | ||

| 73 | ||

| 73 | ||

| 73 | ||

|

Part III

|

||

| 74 | ||

| 80 | ||

| 86 | ||

| 90 | ||

| 95 | ||

|

Part IV

|

||

| 97 | ||

| 104 |

-2-

PART I

ITEM 1. BUSINESS

General

As used in this Annual Report, references to “the Company”, “we”, “our”, “ours” and “us” refer to NTS, Inc. and consolidated subsidiaries, unless otherwise indicated or unless the context otherwise requires. References to “NTSI” refer to NTS, Inc. References to “NTSC” refer to NTS Communications, Inc. In addition, references to our “financial statements” are to our consolidated financial statements except as the context otherwise requires.

We prepare our financial statements in United States dollars and in accordance with generally accepted accounting principles as applied in the United States, referred to as U.S. GAAP. In this Annual Report, references to “$” and “dollars” are to United States dollars, “£”, “UKP”, or “GBP” are to British Pound Sterling, and references to “NIS” and “shekels” are to New Israeli Shekels.

Background

NTS, Inc. (f/k/a Xfone, Inc.)

NTS, Inc. was incorporated in the State of Nevada, U.S.A. in September 2000 as Xfone, Inc. We are a holding and managing company providing, through our subsidiaries, integrated communications services which include voice, video and data over our Fiber-To-The-Premise (“FTTP”) and other networks. As of summer 2010, we discontinued our operations in Israel and the United Kingdom. Our Board of Directors made a strategic decision to concentrate our operations in the U.S.; accordingly, in the summer of 2010 we disposed of our UK and Israeli operations. We currently have operations in Texas, Mississippi and Louisiana and we also serve customers in Arizona, Colorado, Kansas, New Mexico, and

Oklahoma.

On December 29, 2011, our shareholders approved an amendment (the “Amendment”) to NTSI’s Articles of Incorporation (the “Articles”) to change the name of the Company from Xfone, Inc. to NTS, Inc. and to increase the Company's authorized capital to 150,000,000 shares of common stock $0.001 par value per share (“Common Stock”). The Amendment became effective on February 1, 2012.

On February 2, 2012, our Common Stock began trading on the NYSE Amex LLC (“NYSE Amex”) and the Tel Aviv Stock Exchange Ltd. (“TASE”) under its new ticker symbol “NTS” (former ticker symbol: “XFN”)

On March 28, 2012, the closing price of our Common Stock was $0.59 (NYSE Amex) / NIS 2.149 (TASE).

Our principal executive offices are located at 5307 W. Loop 289, Lubbock, Texas 79414 and our telephone number is (806) 771-5212.

Our offices in Israel are located at 11 Rabbi Akiva Street, Modi'in Illit, 71919 and our telephone number there is + 972 08-6229582.

For our corporate website please visit www.ntscom.com. Our website is not part of this Annual Report.

-3-

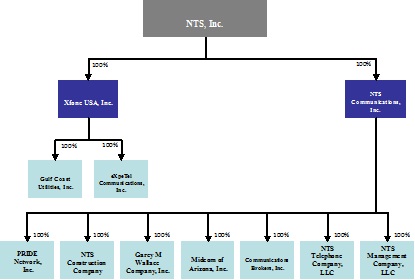

Our Organizational Structure

Following the sale of our UK and Israeli operations we have two wholly owned subsidiaries in the United States. These subsidiaries, and their consolidated subsidiaries, are shown in the following diagram:

Swiftnet Limited

On October 4, 2000, we acquired Swiftnet Limited (“Swiftnet”) which had a business plan to provide a comprehensive range of telecommunication services and products, integrated through one website. Swiftnet was incorporated in 1990 under the laws of the United Kingdom and is headquartered in London, England. Until 1999, the main revenues for Swiftnet were derived from messaging and fax broadcast services. During 2000, Swiftnet shifted its business focus to voice services by offering a comprehensive range of calling services to resellers and end customers. Utilizing automation and proprietary software packages, Swiftnet’s strategy is to grow without the need for heavy investments and with lower

expenses for operations and registration of new customers.

On January 29, 2010, we entered into an agreement with Abraham Keinan (our former Chairman of the Board of Directors and significant shareholder) and AMIT K LTD. (a company registered in England & Wales which at that time was wholly owned and controlled by Mr. Keinan) for the sale by us of the entire issued share capital of Swiftnet. The transaction closed on July 29, 2010.

Xfone 018 Ltd.

On April 15, 2004, we established an Israel based subsidiary, Xfone Communication Ltd., which changed its name to Xfone 018 Ltd. (“Xfone 018”) in March 2005. Headquartered in Petach Tikva, Israel, Xfone 018 is a telecommunications service provider that owns and operates its own facilities-based telecommunications switching system. Xfone 018 provides residential and business customers with international carrier services and Internet access services.

On August 31, 2010, we completed the disposition of our 69% interest in Xfone 018 pursuant to a certain agreement, dated May 14, 2010 (as amendment and supplement), by and between us, Newcall Ltd. (the former 26% minority owner of Xfone 018), Margo Pharma Ltd. (the former 5% minority owner of Xfone 018), and Marathon Telecom Ltd., the buyer of Xfone 018.

-4-

WS Telecom, Inc. / Xfone USA, Inc.

On May 28, 2004, we entered into an agreement and Plan of Merger to acquire WS Telecom, Inc., a Mississippi corporation, and its two wholly owned subsidiaries, eXpeTel Communications, Inc. and Gulf Coast Utilities, Inc., through the merger of WS Telecom with and into our wholly owned subsidiary Xfone USA, Inc (“Xfone USA”). On July 1, 2004, Xfone USA entered into a management agreement with WS Telecom which provided that Xfone USA provide management services to WS Telecom pending the consummation of the merger. The management agreement provided that all revenues generated from WS Telecom business operations would be assigned and transferred to Xfone USA. The term of the management agreement commenced

on July 1, 2004, and continued until the consummation of the merger on March 10, 2005.

Xfone USA is an integrated telecommunications service provider that owns and operates its own facilities-based, telecommunications switching system and network. Xfone USA provides residential and business customers with high quality local, long distance and high-speed broadband Internet services. Xfone USA utilizes integrated multi-media offerings - combining digital voice and data services over broadband technologies to deliver services to customers throughout its service areas. Xfone USA is currently licensed to provide telecommunications services in Louisiana and Mississippi.

I-55 Internet Services, Inc.

On August 18, 2005, we entered into an Agreement and Plan of Merger to acquire I-55 Internet Services, Inc. (“I-55 Internet Services”), a Louisiana corporation, through the merger of I-55 Internet Services with and into our wholly owned subsidiary Xfone USA (the “I-55 Internet Services Merger”). The I-55 Internet Services Merger closed on March 31, 2006.

I-55 Internet Services provided Internet access and related services, such as installation of various networking equipment, website design, hosting and other Internet access installation services, throughout the Southeastern United States to individuals and businesses located predominantly in rural markets in Louisiana and Mississippi. These services are available throughout Louisiana and Mississippi. The Internet service offerings include dial-up, DSL, high speed dedicated Internet access, web services, email, the World Wide Web, Internet relay chat, file transfer protocol and Usenet news access to both residential and business customers. Xfone USA provides bundled services of voice and data (broadband Internet)

to customers throughout its service areas.

I-55 Telecommunications, LLC

On August 26, 2005, we entered into an Agreement and Plan of Merger to acquire I-55 Telecommunications, LLC (“I-55 Telecommunications”), a Louisiana corporation, through the merger of I-55 Telecommunications with and into our wholly owned subsidiary Xfone USA (the “I-55 Telecommunications Merger”). The I-55 Telecommunications Merger closed on March 31, 2006.

I-55 Telecommunications provided voice, data and related services throughout Louisiana and Mississippi to both individuals and businesses. Prior to the merger with and into Xfone USA, I-55 Telecommunications was a licensed facility based CLEC operating in Louisiana and Mississippi with a next generation class 5 carrier-switching platform. I-55 Telecommunications provided a complete package of local and long distance services to residential and business customers across both states. Utilizing the I-55 network footprint, Xfone USA expanded its On-Net (facilities) service area, through I-55 Telecommunications infrastructure, into New Orleans, Louisiana and surrounding areas, including Hammond, Louisiana.

Xfone USA maintains a retail sales presence in New Orleans and Hammond, Louisiana.

EBI Comm, Inc.

On January 1, 2006, Xfone USA, our wholly owned subsidiary, entered into an Agreement with EBI Comm, Inc. (“EBI”), a privately held Internet Service Provider, to purchase the assets of EBI. EBI provided a full range of Internet access options for both commercial and residential customers in north Mississippi. Based in Columbus, Mississippi, EBI’s services included Dial-up, DSL, T1 Dedicated Access and Web Hosting. The customer base, numbering approximately 1,500 Internet users at the time, is largely concentrated in the Golden Triangle area, which includes Columbus, West Point and Starkville, Mississippi. Acquired assets include the customer base and customer lists, trademarks and all related

intellectual property, fixed assets and all account receivables. The transaction was closed on January 25, 2008. The acquisition was not significant from an accounting perspective.

-5-

Canufly.net, Inc.

On January 10, 2006 (effective as of January 1, 2006), Xfone USA, our wholly owned subsidiary, entered into an Asset Purchase Agreement with Canufly.net, Inc. (“Canufly.net”), an Internet Service Provider based in Vicksburg, Mississippi, and its principal shareholder, Mr. Michael Nassour. Canufly.net provided residential and business customers with high-speed Internet services and utilized the facilities-based network of Xfone USA, as an alternative to BellSouth, to provide Internet connectivity to its customers. Canufly.net also provided Internet services through a small wireless application in certain areas in Vicksburg, Mississippi. The transaction was closed on January 24, 2006. The acquisition was

not significant from an accounting perspective.

Story Telecom

On May 10, 2006, we, Story Telecom, Inc., Story Telecom Limited, Story Telecom (Ireland) Limited, Nir Davison, and Trecastle Holdings Limited, a company owned and controlled by Mr. Davison, entered into a Stock Purchase Agreement. Pursuant to the Stock Purchase Agreement, we increased our ownership interest in Story Telecom from 39.2% to 69.6% in a cash transaction. The stock purchase pursuant to the Stock Purchase Agreement was completed on May 16, 2006. The transaction contemplated by the Stock Purchase Agreement was not significant from an accounting perspective.

Story Telecom, Inc., a telecommunication service provider, operated in the United Kingdom through its two wholly owned subsidiaries, Story Telecom Limited and Story Telecom (Ireland) Limited (which was dissolved on February 23, 2007). Following the acquisition, Story Telecom operated as a division of our operations in the United Kingdom.

On March 25, 2008, we purchased from Mr. Davison and Trecastle Holdings Limited, the shares of common stock of Story Telecom, Inc. that each party owned, respectively, pursuant to the terms of a Securities Purchase Agreement entered into between the parties on that date. Upon acquisition of the shares of common stock of Story Telecom, Inc. from Mr. Davison and Trecastle Holdings, Story Telecom, Inc. became our wholly owned subsidiary.

On January 29, 2010, we entered into an agreement with Abraham Keinan and AMIT K LTD. for the sale by us of the entire issued share capital of Story Telecom, Inc. and its subsidiary Story Telecom Limited. The transaction closed on July 29, 2010.

Equitalk.co.uk Limited

On May 25, 2006, we and the shareholders of Equitalk.co.uk Limited, a privately held telephone company based in the United Kingdom (“Equitalk”) entered into an Agreement relating to the sale and purchase of Equitalk (the “Equitalk Agreement”). The Equitalk Agreement provided for us to acquire Equitalk in a restricted Common Stock and warrant transaction. The acquisition was completed on July 3, 2006, and on that date Equitalk became our wholly owned subsidiary. Founded in December 1999, Equitalk, a VC-financed company, was the first fully automated e-telco in the United Kingdom. Equitalk provided both residential and business customers with low-cost IDA and CPS voice services, broadband and

teleconferencing.

On January 29, 2010, we entered into an agreement with Abraham Keinan and AMIT K LTD. for the sale by us of the entire issued share capital of Equitalk. The transaction closed on July 29, 2010.

Auracall Limited

On August 15, 2007, we, Swiftnet and Dan Kirschner entered into a definitive Share Purchase Agreement which was completed on the same date, pursuant to which Swiftnet purchased from Mr. Kirschner the 67.5% equity interest in Auracall Limited (“Auracall”) that he beneficially owned, thereby increasing Swiftnet’s ownership interest in Auracall from 32.5% to 100%. Swiftnet had acquired the initial 32.5% interest in Auracall through several transactions that occurred since October 16, 2001.

On January 29, 2010, we entered into an agreement with Abraham Keinan and AMIT K LTD. for the sale by us of the entire issued share capital of Auracall. The transaction closed on July 29, 2010.

-6-

NTS Communications, Inc.

On August 22, 2007, we entered into a Stock Purchase Agreement (the “NTSC Purchase Agreement”) with NTS Communications, Inc. (“NTSC”), a provider of integrated telecommunications solutions headquartered in Lubbock, Texas, and the owners of approximately 85% of the equity interests in NTSC, to acquire NTSC. Subsequently, all of the remaining shareholders of NTSC executed the NTSC Purchase Agreement, bringing the total percentage of equity interests in NTSC owned by NTSC shareholders that entered into the NTSC Purchase Agreement (the “NTSC Sellers”) to 100%. On February 14, 2008, we entered into a First Amendment to the NTSC Purchase Agreement to amend the agreement to

further extend the expiration date for the closing of our acquisition of NTSC. On February 26, 2008, we entered into a Second Amendment to the NTSC Purchase Agreement which amended, among other things, the definition and elements of Working Capital, as such term is defined in the NTSC Purchase Agreement, and increased the escrow amount. On April 25, 2008, we entered into a Third Amendment to the NTSC Purchase Agreement, pursuant to which we agreed to an extension of time for the calculation and payment of the post closing working capital adjustment under the NTSC Purchase Agreement.

The acquisition closed on February 26, 2008. Upon closing of the acquisition, NTSC and its six wholly owned subsidiaries, NTS Construction Company, Garey M. Wallace Company, Inc., Midcom of Arizona, Inc., Communications Brokers, Inc., NTS Telephone Company, LLC, and NTS Management Company, LLC, became our wholly owned subsidiaries. On April 3, 2009, NTSC formed a seventh wholly owned subsidiary in Texas, called PRIDE Network, Inc.

On December 28, 2009, we and the NTSC Sellers entered into a certain General Release and Settlement Agreement (the “Settlement Agreement”) in order to resolve all issues related to the calculation and determination of the final purchase price as provided in Article II of the NTSC Purchase Agreement, including all issues which have been the subject of a proposed arbitration between the parties (hereinafter referred to as the “Disputed Issues”) by compromise and settlement and without resorting to potentially costly arbitration proceedings. Our financial statements have carried the full settlement amount. We do not expect to bear any additional expenses as a result of the

Settlement Agreement.

As consideration for this settlement, (i) the NTSC Sellers, their heirs, executors, administrators, agents, beneficiaries, successors and assigns, officers, directors, affiliates, employees, representatives, attorneys and insurers including those of affiliated companies, forever released and discharged us, including each of our subsidiaries, directors, officers, affiliates, employees, agents, representatives, attorneys, successors and assigns, and insurers, and their respective past and present officers, directors, employees, agents, and attorneys, of and from any and all manner of action and actions, causes and causes of action, claims, controversies, contracts, torts, debts, damages or demands whatsoever, in law

or in equity, that they have had, now have, or may in the future have, arising out of or related to the Disputed Issues; and (ii) we , including each of our directors, officers, affiliates, employees, agents, representatives, attorneys, successors and assigns, and insurers, and their respective past and present officers, directors, employees, agents, and attorneys forever released and discharged the NTSC Sellers, their heirs, executors, administrators, agents, beneficiaries, successors and assigns, officers, and directors, including those of affiliated companies, of and from any and all manner of action and actions, causes and causes of action, claims, controversies, contracts, torts, debts, damages or demands whatsoever, in law or in equity, that they have had, now have, or may in the future have, arising out of or related to the Disputed Issues.

NTSC is an integrated telecommunications service provider that owns and operates its own fiber optic and leased facilities-based, long haul and metropolitan telecommunications networks. NTSC provides business and residential customers with high quality broadband, managed data, video, local, and long distance services within its service areas. The company also provides long distance, data, and private line services to numerous communications carriers. NTSC is currently authorized to provide interexchange service in Arizona, Colorado, Kansas, Louisiana, New Mexico, Oklahoma, and Texas. NTSC is also authorized to provide local service only in Louisiana, New Mexico, and Texas, and video service only in

Louisiana and Texas.

Cybergate, Inc.

On November 26, 2008, Xfone USA entered into a Sale and Purchase Agreement (the “Agreement”) with Cybergate, Inc. (“Cybergate”), pursuant to which Cybergate agreed to sell to Xfone USA all of Cybergate’s assets, as set forth in the agreement (the “Assets”). Cybergate was a provider of Internet services, including Internet access, web and server hosting, data services and e-mail. Pursuant to the Agreement Xfone USA also agreed to assume certain of the liabilities of Cybergate. The Agreement and the closing of the sale and purchase have an effective date of November 1, 2008. The acquisition was not significant from an accounting

perspective.

CoBridge Telecom, LLC

On April 25, 2011, NTSC entered into an Asset Purchase Agreement (the “Agreement”) with CoBridge Telecom, LLC, (“CoBridge”), pursuant to which CoBridge agreed to sell NTSC all of CoBridge’s assets in and around the communities of Colorado City, Levelland, Littlefield, Morton, and Slaton Texas pursuant to the terms of that Agreement. CoBridge provided cable television service in those communities via coaxial cable facilities. As part of the transaction, NTSC also agreed to assume certain liabilities of CoBridge which are necessary to continue operation of the Assets. The sale and purchase closed on July 1, 2011. The acquisition is not significant from an accounting

perspective.

-7-

Reach Broadband

On September 16, 2011, NTSC entered into an Asset Purchase Agreement (the “Agreement”) with RB3, LLC, and Arklaoktex, LLC, each doing business as Reach Broadband (“Reach”), pursuant to which Reach agreed to sell NTSC all of Reach’s assets in and around the communities of Abernathy, Anton, Brownfield, Hale Center, Idalou, Levelland, Littlefield, Meadow, New Deal, O’Donnell, Olton, Reese, Ropesville, Shallowater, Smyer, Tahoka, and Wollforth Texas pursuant to the terms of the Agreement. Reach provided those communities with cable television service via coaxial cable facilities and Internet service via a wireless network. As part of the transaction, NTSC also agreed to assume

certain liabilities of Reach which are necessary to continue operation of the Assets. The sale and purchase closed on December 1, 2011, but is subject to a purchase price adjustment based on the number of Reach’s customers who failed to pay their accounts or cancelled service (offset by customers who convert to NTSC’s service in relevant markets) and actual transaction costs. The acquisition is not significant from an accounting perspective.

Our Principal Services and Their Markets

We provide through our subsidiaries the following telecommunication products / services:

Services provided by NTS Communications, Inc. and its subsidiaries

Retail Services

|

·

|

Local Services: NTSC delivers local telephony service to its customers through an “on-net” UNE-L connection, including voice mail, caller ID, forwarding, 3-way calling, blocking, and PBX services. In addition, NTSC sells “off-net” total service resale lines. NTSC provides UNE-L services in Lubbock, Abilene, Amarillo, Midland, Odessa, Pampa, Plainview, and Wichita Falls, Texas. NTSC provides local services via FTTP in Lubbock, Wolfforth, Levelland, Littlefield, Burkburnett, and Smyer, Texas. NTSC provides resold local services throughout Texas via its resale agreement with

AT&T.

|

|

·

|

Retail Long Distance Services: NTSC offers a full range of long distance services to its customers, including competitively priced switched long distance (including intrastate, interstate, and international), toll-free service, dedicated T-1 long distance and calling cards. The vast majority of its customers are concentrated in West Texas. A minority of its long distance customers are in Arizona, New Mexico, Oklahoma, Kansas, and Colorado.

|

|

·

|

Internet Data Services: NTSC provides broadband and dial-up Internet service in all of its Texas markets. Download speeds for broadband range from 500 Kilobits to 100 Megabits per second, depending on the end user’s distance from an NTSC collocation or the type of facilities used to deliver the service. NTSC also offers Web hosting and wide area networking solutions for business applications.

|

|

·

|

Fiber-Based Services (“Fiber to the Premise” or “FTTP”): As an integrated telecom provider, NTSC is capable of providing quality triple play (voice, digital video & data) on one bill at competitive prices to its FTTP customers. NTSC offers a full selection of video services, including basic cable, video on demand, HDTV and DVR. NTSC is a member of the National Cable Television Cooperative and as such obtains favorable programming rates from most major networks. NTSC provides FTTP service in Lubbock, Levelland, Littlefield, Brownfield, Burkburnett, Ropesville, Slaton, Smyer, Whitharral, and

Wolfforth, Texas.

|

|

·

|

Cable Television (CATV): In addition to providing video service via its FTTP network, NTSC offers CATV via a coaxial cable network in Anton, Brownfield, Colorado City, Hale Center, Idalou, Levelland, Littlefield, Meadow, Morton, New Deal, O’Donnell, Olton, Ropesville, Shallowater, Slaton, Smyer, Tahoka, and Wolfforth Texas. NTSC offers a wide selection of video services via its CATV offering basic cable, over 250 channels including premium sports and movie channels, and Pay Per View.

|

|

·

|

Customer Premise Equipment (“CPE”): NTSC resells a variety of CPE and CPE related services to its customers. Primarily, these sales involve NTSC acting as an authorized dealer for Toshiba phone systems. These systems are sold to customers either on a stand-alone basis, or in conjunction with the purchase of local, long distance, and/or data services from the company. In addition NTSC sells a variety of other electronics such as HD displays, surveillance equipment, paging systems, nurse call systems, routers switches and internetworking gear.

|

Wholesale Services

|

·

|

Private Line Services: NTSC offers aggregation and resale of leased fiber transport network from AT&T and other fiber network operators. This service is mostly provided for carrier customers that need direct network connectivity, as well as enterprises that require dedicated branch office connections. Services are generally offered under 1-year contracts for a fixed amount per month. NTSC provides private line service nationwide.

|

|

·

|

Wholesale Switched Termination Services: NTSC sells its wholesale-switched minutes to local telecom companies who do not have the volume to warrant attractive pricing from AT&T and other large carriers. NTSC provides multi-regional switched termination, switched toll free origination and wholesale Internet access services to various carrier customers. Services are generally offered for a fixed amount per minute. NTSC provides wholesale switched termination services to customers via network connections in NTSC POPs and switch sites.

|

-8-

Internet Based Customer Service

|

·

|

Our Internet based customer service (found at www.ntscom.com) includes full details on all our retail products and services.

|

NTS Communications owns and operates its own facilities-based telecommunications switching system.

FTTP Network Extensions / Stimulus Fundings

Levelland/Smyer, Texas

NTSC, through its wholly owned subsidiary, NTS Telephone Company, LLC, has extended its FTTP network to the nearby communities of Levelland (located approximately 30 miles west of Lubbock) and Smyer (approximately 15 miles west of Lubbock). These communities have added approximately 6,000 passings to the NTSC FTTP footprint and bring total FTTP passings to approximately 21,000. NTS Telephone Company has received approval from the Rural Utilities Service (“RUS”) for an $11.8 million, 17-year debt financing to complete this buildout. The RUS loan is non-recourse to NTSC and all other NTSC subsidiaries and interest is charged at the average rate of U.S. government

obligations. NTSC’s initial capital investment in the project was a $2.5 million equity contribution. NTSC provides voice, data, and video services for NTS Telephone Company and also provides billing, sales and marketing, back and front offices services to this subsidiary. NTSC receives a management fee from NTS Telephone Company equal to 15% of its revenues. NTSC began marketing its triple-play service in limited areas of Levelland in 2009 and construction was completed on April 8, 2010. NTSC will continue to work diligently to secure sales and complete installations in pursuit of its take rate goals.

Texas South Plains; Burkburnett and Iowa Park, Texas; St. Helena, Washington, and Tangipahoa Parishes in Southern Louisiana

In March 2010, we were notified that the applications of our wholly owned subsidiary, PRIDE Network, Inc. (“PRIDE Network”), for RUS funding from the U.S. Department of Agriculture under the Broadband Initiative Program for the FTTP build out of PRIDE Network’s projects in Texas, had been approved. PRIDE Network was selected to receive approximately $63.7 million in RUS funding for these projects, which will be split between loans of approximately $35.53 million and grants of approximately $28.14 million.

In September 2010, we were notified that another application of PRIDE Network for additional funding under the Broadband Initiative Program for the FTTP build out of its project in Louisiana has been approved. PRIDE Network was selected to receive approximately $36.2 million in additional RUS funding which will be split between a loan of approximately $18.46 million and a grant of approximately $17.74 million.

This funding is a significant milestone in our strategy to grow the FTTP business. The grants and loans will enable us to expand the rollout of our state-of-the-art FTTP infrastructure to bring broadband services to the Texas south plains, to the communities of Burkburnett and Iowa Park, Texas, and to St. Helena, Washington, and Tangipahoa Parishes in Southern Louisiana. Additionally, it is anticipated that these projects will help stimulate the economic growth of these communities by creating hundreds of new jobs associated with the network build out.

When completed, the PRIDE Network is expected to add 30,000 FTTP passings to the NTSC network bringing Company-wide FTTP passings to over 50,000. To date, we have established our FTTP network in Littlefield, Burkburnett, Brownfield and Whitharral, Texas, and started to record minimal revenues from these markets which will increase revenues from this project during 2012.

The fundings are contingent upon PRIDE Network meeting the terms of the loans, grants or loans/grants agreement.

-9-

Services provided by Xfone USA

|

·

|

Local Telephone Service: Using our own network in concentrated local areas throughout Mississippi and Louisiana and utilizing the underlying network of BellSouth Telecommunications, Inc. (the new ATT), outside of our local areas, we provide local dial tone and calling features, such as hunting, call forwarding and call waiting to both business and residential customers throughout Louisiana and Mississippi, including T-1 and PRI local telephone services to business customers.

|

|

·

|

Long Distance Service: We use our own network where available and QWEST, a nationwide long distance carrier, as our underlying long distance network provider. In conjunction with Local Telephone Services, we provide Long Distance Services to our residential and business customers. We provide two different categories of long distance services - Switched Services to both residential and small business customers, which include 1+ Outbound Service, Toll Free Inbound Service and Calling Card Service. For larger business customers we also provide Dedicated Services such as T-1 and PRI Services. Our long distance services are only available to customers who use our

local telephone services.

|

|

·

|

Internet/Data Service: We provide high-speed broadband Internet access to residential and business customers utilizing our own integrated digital data network and utilizing the broadband gateway network of the new ATT. Our DSL service provides up to 3 Mbps of streaming speed combined with Dynamic IP addresses, as well as multiple mailboxes and Web space. Our DSL services also include spam filter, instant messaging, pop-up blocking, web mail access, and parental controls. We also provide dial-up Internet access service for quick and dependable connection to the web. Our Internet/Data services are stand-alone products or are bundled with our voice services for

residential and business customers.

|

|

·

|

Customer Service: Customer Service is paramount at Xfone USA and is one of our major differentiating characteristics, thus tantamount to being one of our product offerings. Customers have been conditioned to accept poor customer service from the larger monopoly companies because they have never had any real choice in service providers, especially in the residential market. Our attentive customer service department is an additional “product offering” which sells - as well as retains - customers. The full scope of communications service entails network service, customer service, and repair service.

|

|

·

|

Customer Premise Equipment (“CPE”): Xfone USA also resells a variety of CPE and CPE related services to its customers. Primarily, these sales involve acting with NTSC as an authorized dealer for Toshiba phone systems. These systems are sold to customers either on a stand-alone basis, or in conjunction with the purchase of local, long distance, and/or data services from the company. In addition, the company sells a variety of other electronics such as HD displays, surveillance equipment, paging systems, nurse call systems, routers switches and internetworking gear.

|

Xfone USA owns and operates its own facilities-based telecommunications carrier class-switching platform.

Our Distribution and Marketing Methods

We use the following distribution methods to market our services:

|

·

|

We use full time, Account Executives “AE’s” to sell into Small, Mid-Market & Enterprise business customers in our fiber & legacy CLEC markets. Additionally, a subset of AE’s working within our PRIDE FTTU markets focus on selling directly to consumers. All AE’s carry quota’s which vary based on their responsibilities, titles and type of market assigned to them. AE’s receive a base salary paid bi-monthly in addition to any commissions that may have been earned under the specific compensation plan that AE falls under;

|

|

·

|

We actively pursue opportunities with other Carriers; ILEC’s, CLEC’s, ITSP’s, MSO’s and Agents who purchase wholesale Origination & Termination, Point to Point Circuits, Carrier Metro Ethernet, Long Haul, Dedicated Internet Access, Dark Fiber, Interconnect CPE & Internetworking equipment such as routers & switches directly from us and then resell these wholesale services & products at a mark-up to end-users under their own brand. This is strictly a “white labeled” offering and these entities generate their own invoices from call detail records CDR’s that we provide them. We call this division “National Accounts” and also refer to it

as “Carrier Wholesale”. Our National Account Managers are specialist and typically have over 20 years of experience;

|

|

·

|

We utilize traditional Agents & VAR’s that sell our services directly to end-users at our established prices; these agents receive an ongoing residual commission of approximately 5%-12% of the total monthly recurring charges “MRC’s” based on their individual contracts on collected revenues less any bad debt;

|

|

·

|

We have used and in the future may engage third party direct sales organizations (telesales and door-to-door) to register new customers when internal human capital is not available or when we want to target a specific service area aggressively for a period of time for the purpose of increase market share or a sales blitz around a new product offering;

|

|

·

|

We have retail and wholesale sales offices; employees at these sales offices receive annual salaries and commissions;

|

|

·

|

We deploy direct marketing resources including but not limited to: Internet/Social Networking, Advertising through newspaper, radio, television, outdoor boards, digital signage, direct mail campaigns, door hangers, community events and sponsorships, chambers affinity groups and alumni associations;

|

|

·

|

We attend telecommunications trade shows to network and to promote our products and services; and

|

|

·

|

We utilize the Internet as an additional distribution channel for our services.

|

-10-

Our Billing Practices

We charge our customers based on a monthly fixed amount or on actual usage by full or partial minutes. Our rates vary with distance, duration, time, type of call, and product or service provided, but are not dependent upon the facilities selected for the call transmission. The standard terms for our customers require either pre-payments or payments due as early as 16 or as late as 30 days from the date of the invoice. Our supplier’s standard terms are payment within 30 to 90 days from invoice date; however, some new suppliers ask for shorter payment terms.

Divisions

We operate the following divisions:

|

·

|

Customer Service Division - We operate a live customer service center that operates 24 hours a day, 7 days a week.

|

|

·

|

Operations Division - Our Operations Division provides the following operational functions to our business: (a) 24 hour/7 day a week technical support; (b) inter-company network; (c) hardware and software installations; and (d) operating switch and other platforms.

|

|

·

|

Administration Division - Our Administration Division provides the billing, collection, credit control, and customer support aspects of our business.

|

|

·

|

Marketing Division - Our Marketing Division is responsible for our marketing and selling campaigns that target potential and existing retail customers.

|

Geographic Markets

Our primary geographic markets are Texas, Mississippi and Louisiana, United States. However, we also serve customers in Arizona, Colorado, Kansas, New Mexico, and Oklahoma.

Competitive Business Conditions

NTSC operates in a highly competitive environment which is generally characterized by the dominance of the Incumbent Local Exchange Carrier (ILEC). With respect to its primary Texas markets, the dominant ILEC is either AT&T (formerly Southwestern Bell Telephone Company) or Windstream Communications. NTSC also competes with the Incumbent Cable TV Provider (ICTVP) in markets where that carrier provides voice, data and/or video services. In its core Texas markets, the ICTVP is SuddenLink Communications, Time Warner Communications, or other smaller operators. Within these same core markets, NTSC also competes with a variety of widely dispersed smaller Competitive Local

Exchange Carriers (CLEC). With respect to its data and long distance products, the company competes with various national and regional players including AT&T, Verizon, Suddenlink, Qwest, Level 3 and others.

Xfone USA also operates in highly competitive markets in Mississippi and Louisiana. In these markets Xfone USA competes against the dominant ILEC, AT&T (formerly BellSouth Telecommunications), as well as many smaller CLECs.

Principal Suppliers

In fiscal year 2011, our principal supplier of telephone routing and switching services constituted 61% of our costs of revenues.

We are dependent on several of our suppliers, including those that provide significant hardware and software products and support. However, these suppliers are required to provide us with services in accordance with the relevant regulations and their licenses to operate as a telecommunications provider in the relevant jurisdictions.

-11-

Major Customers

We have four major types of customers:

|

·

|

Residential - Pre-subscribed customers, including for local, long distance, internet and cable television services.

|

|

·

|

Commercial - We serve small to complex business customers within our service areas.

|

|

·

|

Governmental agencies - We provide various governmental entities a broad range of services, including local, long distance, internet, managed data, and private line services.

|

|

·

|

Resellers & Wholesale - We provide resellers and other carriers with various switched and non-switched voice and data services on a wholesale basis. We also provide long haul transport, metro access, and switched termination services to a variety of communications companies throughout the United States.

|

We are not dependant upon any major customer. However, our revenues are dependent upon certain factors, including: price competition; access provided to our services by other telecom companies and the prices for that access; demand for our services; economic conditions in our markets; and our ability to market our services.

Patents and Trademarks

The Mark, “NTS Communications” related to the provision of telephone telecommunications services in the United States, was registered by the USPTO on September 4, 1984, and has been renewed through the year 2014.

The Mark, “NTS Communications (with design)” related to the provision of telephone communications services in the United States, was registered by the USPTO on October 12, 1993, and has been renewed through the year 2013.

The Mark, “NTS-ONLINE (with design)” related to the provision of web hosting was registered by the USPTO on August 15, 2000, and has been renewed through the year 2020.

On February 6, 2007, NTSC filed an application with the USPTO to register the Mark, “NTS-ONLINE” related to the provision of expanded telecom services, web hosting services, and domain name services. The application also seeks to eliminate the design associated with the mark. On May 27, 2008, the USPTO issued a Notice of Allowance. NTSC’s Statement of Use was accepted by the USPTO on January 3, 2009. The mark was registered by the USPTO on February 10, 2009.

The Mark, “EXPETEL” related to the provision of telephone communications services in the United States, was registered by the USPTO on April 12, 2005.

The Mark, “XFONE” related to the provision of telephone communications services and multiple user dial-up and dedicated access to the Internet in the United States, was registered by the USPTO on July 15, 2008.

On January 9, 2004, we received notification from the Trademarks Registry Office of Great Britain that as of August 8, 2003, our trademark, “XFONE”, was registered by that government agency.

We do not have any other patents or registered trademarks.

Regulatory Matters

We provide our services in certain States, each of which may have different regulations, standards and controls related to licensing, telecommunications, import/export, currency and trade. We believe that we are in substantial compliance with these laws and regulations.

Xfone USA is currently licensed as a CLEC and an Inter-exchange Carrier to provide local telephone and long distance services in the states of Louisiana and Mississippi. During fiscal 2008, Xfone USA was also licensed in Alabama, Florida, and Georgia, however, we withdrew these licenses during the first quarter of fiscal 2009. Internet and data services provided by Xfone USA are not regulated services.

-12-

On February 14, 2008, NTSI and NTSC received domestic and international Section 214 authorization from the United States Federal Communications Commission to transfer control of NTSC to NTSI.

NTSC has certain domestic and international Section 214 authority, which authorizes NTSC to provide long distance service in the United States.

NTSC is a registered re-seller of long-distance services in the states of Arizona, Colorado, Kansas, New Mexico, Oklahoma and Texas. NTSC is also registered to provide local services in Louisiana, New Mexico and Texas. Further, in Texas, NTSC has the authority to provide local telecommunications services throughout the state of Texas, and has authorization to provide video services in designated areas within Lubbock, , Anton, Brownfield, Burkburnett, Colorado City, Hale Center, Idalou, Levelland, Littlefield, Meadow, Morton, New Deal, O’Donnell, Olton, Ropesville, Shallowater, Slaton, Smyer, Tahoka, Whitharral, Wichita Falls, Wilson, and Wolfforth. In addition, NTSC has entered into

9-1-1 Emergency Service Agreements with the applicable 9-1-1 entities in the markets it serves.

NTSC also has authority to provide video services in certain communities in the following Parishes in the state of Louisiana: Livingston, St. Helena, St. Tammany, Tangipahoa, and Washington.

On May 19, 2008 a petition was filed with the Federal Communications Commission (In the Matter of NTS Communications, Inc., Petition for Extension of Waiver of Section 76.1204(a)(1) of the Commission’s Rules, CS Docket No. 97-80). This Petition seeks a two-year extension of the relief previously granted from Commission Rules banning the use of integrated set-top boxes by cable service providers. The original waiver, granted on July 23, 2007, expired on July 1, 2008. The May 19, 2008 petition is currently pending.

Effect of Probable Governmental Regulations

As an ETC (Eligible Telecommunications Carrier), there are numerous actions proposed at both the state and federal level including the FCC’s recent Order Reforming USF and Intercarrier Compensation, which could limit NTSC and Xfone USA’s future access to reimbursement from various Universal Service Funds (“USF”). NTSC currently only receives minimal reimbursement from USF for its provision of Lifeline and LinkUp services while Xfone USA received significant support for services provided in high cost areas of Mississippi. These measures could limit NTSC and Xfone USA’s ability to obtain reimbursement for services provided in high cost areas. The Order does attempt

to eliminate the artificial distinctions between VoIP and other types of traffic and may open the door to new markets for our wholesale switched services. At this time, in our opinion, it does not appear that the Order will have a material impact on NTSC or Xfone USA’s operations. We are still reviewing the Order and awaiting final rules from the FCC and state regulators. We anticipate that parts of the Order will be challenged in court and could be overturned. Therefore, the final impact of the Order is not clear and we will continue to monitor developments carefully. In areas where it has not deployed its own last mile facilities, NTSC and Xfone USA continue to rely on AT&T for access to high cap interoffice and last mile copper loop facilities. AT&T’s obligation to provide these facilities is created by the Federal

Telecommunications Act of 1996 and corresponding regulations of the FCC and memorialized in interconnection agreements between NTSC and Xfone USA and Incumbent Local Exchange Carriers. Should laws or regulations be changed to limit and or eliminate competitive access to these essential facilities, our business could be adversely affected.

Employees

We currently have 308 employees in the United States and 2 employees in Israel.

ITEM 1A. RISK FACTORS

Not applicable.

ITEM 1B. UNRESOLVED STAFF COMMENTS

Not applicable.

ITEM 2. PROPERTIES

Principal Executive Offices

Our principal executive offices are located at 5307 W. Loop 289, Lubbock, Texas 79414, USA.

-13-

Material Properties in the U.S

Real Property Owned by NTSC and subsidiaries

Our video headend and operations center is located at 8902 Alcove Avenue, Wolfforth, Texas 79382. This is a single story 3,500 sq. ft. building built in 2004. The building is used for equipment storage warehouse, office space, and the video and data headend. A satellite farm is located adjacent to the building. The building sits on two fenced acres within a ten acre lot.

Our retail and Toshiba sales offices, is located in the Metro Tower, which is a 20-story building located at 1220 Broadway, Lubbock, Texas 79401. The building also houses local switching, local provisioning and outside technicians. Each floor of the building measures approximately 5,000 sq. ft. We lease office space in the building to various businesses including many technology and telecommunications companies. We also lease roof space to companies to house communications antennas.

We own a 7,700 sq. ft. single story building at 601 College Avenue, Levelland, Texas, 79336. The building houses our operations in Levelland.

We own a 3,000 sq. ft. single story building at 510 West 7th, Littlefield, Texas, 79339. The building houses our operations in Littlefield.

We own a 3,087 sq. ft. building at 312 E. 3rd, Burkburnett, Texas 76354. The building houses our operations in Burkburnett.

We own a 416 sq. ft. building at 770 W. 1-20 North 208, Colorado City, Texas 79512. The building houses NTSC’s equipment in Colorado City.

We own a 1,463 sq. ft. building at 704 W. Highway St, Iowa Park, Texas 76367. The building houses PRIDE Network’s operations in Iowa Park.

We own a 3,750 sq. ft. building at 321 W. Broadway, Brownfield, Texas 79316. The building houses PRIDE Network’s operations in Brownfield.

We also own properties in a number of communities that house offices and cable head end equipment for our traditional cable television network in a number of communities: Abernathy, Brownfield, Hale Center, Idalou, O’Donnell and Tahoka, Texas.

Real Property Leased through NTSC and subsidiaries

|

·

|

Our corporate offices, Network Control Center, Customer Care, and Internet help desk are located at 5307 W. Loop 289, Lubbock, TX, measuring 45,072 sq. ft. on three floors with annual triple net base rent of $518,328. The lease expires July 31, 2013 and contains three options for five year renewal terms. We believe the building has sufficient space for our operations.

|

|

·

|

Point of Presence (“POP”) site and fiber node located at 201 E Main, Ste. 104, El Paso Texas, measuring 950 sq. ft. (including 850 linear feet of conduit) with annual rent of $54,070. The lease expires on March 31, 2015 and contains no option to renew.

|

|

·

|

POP, switch site and fiber node located at 500 Chestnut, Suite 936, Abilene, TX, measuring 4,763 sq. ft. (including roof space for one (1) GPS antenna) with annual rent of $49,896. The lease expires on December 31, 2013 and contains two options for three year renewal terms.

|

|

·

|

POP located at 201 Robert S. Kerr, Suite 1070, Oklahoma City, OK, measuring 1,092 sq. ft. with annual rent of $18,564.00. The lease expires on April 30, 2014.

|

|

·

|

Equipment room located at 8212 Ithaca, Room W-12, Lubbock, TX, of approximately 16 sq. ft. of wall space with annual rent of $480. The lease is on a month-to-month term.

|

|

·

|

Local sales and technician offices located at 4214 Kell, Suite 104 Wichita Falls, TX, measuring 2,400 sq. ft. with annual rent of $39,600. The lease expires in August 2014 and has options to renew for one additional 36 month terms.

|

|

·

|

POP, switch site, and fiber node located at Petroleum Building, 203 W. 8th Street Suite 102, Amarillo, TX, measuring 4,276 sq. ft. with annual rent of $62,998.44. The lease is expires on June 30, 2016, and has options to renew for two additional 5 year terms.

|

-14-

|

·

|

POP, switch site, and fiber node located at 710 Lamar Street, Suite 10-25, Wichita Falls, TX, measuring approximately 890 sq. ft., 380 feet of conduit, antenna roof space, plus 200 sq. ft. to house a gas generator at 714 Travis, 6th Floor, Wichita Falls. Annual rent for both spaces totals $17,033.40. The lease expires April 30, 2015 and has one option for a five year renewal term.

|

|

·

|

POP and switch site located at 4316 Bryan, Dallas, TX, measuring 3,816 sq. ft. with annual base rent of $196,860. The lease expires on October 31, 2012 and has two options for renewal terms of three years.

|

|

·

|

POP and fiber node located at 415 Wall St., Midland, TX, measuring approximately 100 sq. ft. with annual rent of $10,800. The lease expires on October 31, 2016.

|

|

·

|

We also lease property that is used to house the equipment, offices, and facilities necessary for the operation of our traditional cable television network in the following communities: Abernathy, Anton, Brownfield, Colorado City, Hale Center, Idalou, Levelland, Opdyke, Littlefield, Lubbock, Meadow, New Deal, Olton, Ropesville, Shallowater, Slaton, Smyer, Tahoka, and Wolfforth, Texas.

|

Easements and Private Rights of Way through NTSC and subsidiaries

|

·

|

Perpetual Construction and Utility Easement from Benny Judah for facility hut at 10508 Topeka, Lubbock, Texas, 79424.

|

Israeli Office

Our Israeli office is located at 11 Rabbi Akiva Street, Modi'in Illit, Israel, measuring 516 sq. ft. The monthly rent (including municipal rate) is NIS 2,230 (approximately $583). The lease expires June 3, 2014.

Our offices are in good condition and are sufficient to conduct our operations.

We do not intend to renovate, improve or develop any properties; however, from time to time we improve leased office space in order to comply with local legislation and to provide an office environment necessary to conduct business in the markets in which we operate. We are not subject to competitive conditions for property. We have no policy with respect to investments in real estate or interests in real estate and no policy with respect to investments in real estate mortgages. We have no policy with respect to investments in securities of or interests in persons primarily engaged in real estate activities.

ITEM 3. LEGAL PROCEEDINGS

Eliezer Tzur et al. vs. 012 Telecom Ltd. et al.

On January 19, 2010, Eliezer Tzur et al. (the “Petitioners”) filed a request to approve a claim as a class action (the “Class Action Request”) against Xfone 018 Ltd. (“Xfone 018”), our former 69% Israel-based subsidiary, and four other Israeli telecom companies, all of which are entities unrelated to us (collectively with Xfone 018, the “Defendants”), in the District Court in Petach Tikva, Israel (the “Israeli Court”). The Petitioners’ claim alleges that the Defendants have not fully fulfilled their alleged legal requirement to bear the cost of telephone calls by customers to the Defendants’ respective technical support numbers. One

of the Petitioners, Mr. Eli Sharvit (“Mr. Sharvit”), seeks damages from Xfone 018 for the cost such telephone calls allegedly made by him during the 5.5-year period preceding the filing of the Class Action Request, which he assessed at NIS 54.45 (approximately $14). The Class Action Request, to the extent it pertains to Xfone 018, states total damages of NIS 7,500,000 (approximately $1,962,836) which reflects the Petitioners’ estimation of damages caused to all customers that (pursuant to the Class Action Request) allegedly called Xfone 018’s technical support number during a certain period defined in the Class Action Request.

On February 22, 2011, Xfone 018 and Mr. Sharvit entered into a settlement agreement, which following the instructions of the Israeli Court was supplemented on May 3, 2011 and amended on July 18, 2011 and on March 21, 2012 (the “Settlement Agreement”). Pursuant to the Settlement Agreement, Xfone 018 agreed to compensate its current and past registered customers of international calling services (the “Services”) who called its telephone service center from July 4, 2004 until February 21, 2010, due to a problem in the Services, and were charged for such calls (the “Compensation”). The Compensation includes a right for a single, up to ten minutes, free of charge, international call

to one landline destination around the world, and shall be valid for a period of six months. In addition, Xfone 018 agreed to pay Mr. Sharvit a one-time special reward in the amount of NIS 10,000 (approximately $2,617) (the “Reward”). Xfone 018 further agreed to pay Mr. Sharvit attorneys' fee for professional services in the amount of NIS 40,000 (approximately $10,468) plus VAT (the “Attorneys Fee”). In return, Mr. Sharvit and the members of the Represented Group (as defined in the Settlement Agreement) agreed to waive any and all claims in connection with the Class Action Request. As required by Israeli law in such cases, the Settlement Agreement is subject to the approval of the Israeli Court. An internal court deliberation with respect to the Class Action Request has been scheduled by the Israeli Court for May 26, 2012. It is expected that the Israeli Court

will consider Xfone 018 and Mr. Sharvit's request to approve the Settlement Agreement before said date.

-15-

On May 14, 2010, we entered into an agreement (including any amendment and supplement thereto, the “Agreement”) with Marathon Telecom Ltd. for the sale of our majority (69%) holdings in Xfone 018. Pursuant to Section 10 of the Agreement, we are fully and exclusively liable for any and all amounts, payments or expenses which will be incurred by Xfone 018 as a result of the Class Action Request. Section 10 of the Agreement provides that we shall bear any and all expenses or financial costs which are entailed by conducting the defense on behalf of Xfone 018 and/or the financial results thereof, including pursuant to a judgment or settlement (it was agreed that in the event that Xfone 018 will be

obligated to provide services at a reduced price, we shall bear only the cost of such services). Section 10 of the Agreement further provides that the defense by Xfone 018 shall be performed in full cooperation with us and with mutual assistance. It is agreed between us and Xfone 018 that subject to and upon the approval of the Settlement Agreement by the Israeli Court, we shall bear and/or pay: (i) the costs of the Compensation; (ii) the Reward; (iii) the Attorneys Fee; and (iv) Xfone 018 attorneys' fees for professional services in connection with the Class Action Request, estimated at approximately NIS 75,000 (approximately $19,628).

In the event the Settlement Agreement is not approved by the Israeli Court, Xfone 018 intends to vigorously defend the Class Action Request.

Danny Jay & Stephanie Tollison vs. NTS Communications, Inc.

On December 20, 2010, NTSC received a demand letter from Danny J. and Stephanie Tollison (the “Petitioners”) claiming $3 million in damages stemming from the search of Mr. Tollison’s home and his wife’s business by the FBI. The Petitioners alleged that the search was effected because of incorrect information provided by NTSC to the FBI pursuant to a subpoena. The investigation was dropped when the FBI was unable to find what they were looking for and identified another suspect.

On July 19, 2011 the Petitioners filed suit in 350th District Court of Taylor County, Texas seeking $5 million in economic and non-economic damages and asserting breach of contract, negligence, gross negligence, defamation, libel, invasion of privacy, and intentional infliction of emotional distress claims. On NTSC’s request due to questions of federal law, the case had been moved to the United States District Court for the Northern District of Texas and was scheduled for trial on April 1, 2013. However, in February on reconsideration, the federal judge denied NTSC’s request and remanded the case to the District Court of Taylor County where it awaits scheduling. NTSC’s insurance carrier has

agreed to defend the suit and has referred the matter to its counsel. NTSC anticipates that its insurance carrier will cover all costs and damages without any liability to NTSC.

ITEM 4. Mine Safety Disclosures

Not Applicable.

-16-

PART II

ITEM 5. MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES

On February 2, 2012, our Common Stock began trading on the NYSE Amex and the Tel Aviv Stock Exchange (“TASE”) under its new ticker symbol “NTS” (former ticker symbol: “XFN”).

On March 28, 2012, the closing price of our Common Stock was $0.59 (NYSE Amex) / NIS 2.149 (TASE).

Below is the market information pertaining to the range of the high and low closing price of our Common Stock for each quarter in 2011 and 2010. The quotations reflect inter-dealer prices, without retail markup, markdown or commission and may not represent actual transactions.

|

Period

|

Low

|

High

|

||||

|

2011

|

||||||

|

Fourth Quarter

|

$

|

0.30

|

$

|

0.68

|

||

|

Third Quarter

|

$

|

0.42

|

$

|

1.27

|

||

|

Second Quarter

|

$

|

0.99

|

$

|

1.44

|

||

|

First Quarter

|

$

|

1.20

|

$

|

1.84

|

||

|

2010

|

||||||

|

Fourth Quarter

|

$

|

1.08

|

$

|

1.49

|

||

|

Third Quarter

|

$

|

1.04

|

$

|

1.30

|

||

|

Second Quarter

|

$

|

0.99

|

$

|

1.49

|

||

|

First Quarter

|

$

|

0.60

|

$

|

1.85

|

The source of the above information is http://www.nysenet.com.

Holders

On March 28, 2012, there were 248 holders of record of our Common Stock.

Dividends

We have not declared or paid cash dividends on our Common Stock in the last several years. We currently intend to retain future earnings, if any, to operate and expand our business, and we do not anticipate paying cash dividends on our Common Stock in the foreseeable future. Any payment of cash dividends in the future will be at the discretion of our Board of Directors and will depend upon our results of operations, earnings, capital requirements, contractual restrictions and other factors deemed relevant by our Board of Directors.

On March 23, 2010, we entered into a Securities Purchase Agreement (the “Burlingame Agreement”) with an existing shareholder, Burlingame Equity Investors, LP (“Burlingame”), pursuant to which Burlingame agreed to purchase from us and we agreed to sell and issue to Burlingame certain securities for an aggregate purchase price of $6,000,000. Among these securities, a Senior Promissory Note (as amended on May 2, 2011, the “Note”) in the aggregate principal amount of $3,500,000, maturing on March 22, 2013. According to the Burlingame Agreement and so long as the Note remains outstanding, we agreed that we shall not declare or pay any dividends or make any distributions to any

holder(s) of our Common Stock without the approval of Burlingame.

-17-

On October 6, 2011, we entered into a term loan, guarantee and security agreement (the “ICON Agreement”) between the following: (1) ICON Agent, LLC, acting as agent for the Lenders, ICON Equipment and Corporation Infrastructure Fund Fourteen, L.P. and Hardwood Partners, LLC.; (2) we, as Guarantor; (3) Xfone USA, Inc., NTS Communications, Inc., Gulf Coast Utilities, Inc., eXpeTel Communications, Inc., NTS Construction Company, Garey M. Wallace Company, Inc., Midcom of Arizona, Inc., Communications Brokers, Inc., and N.T.S. Management Company, LLC, acting as Borrowers and Guarantors; and (4) PRIDE Network, Inc., and NTS Telephone Company, LLC. The principal amount of the loan extended

pursuant to the ICON Agreement was $7,500,000 bearing interest of 12.75% payable in 60 consecutive monthly installments with the first 12 monthly payments being payments of accrued interest only. According to the ICON Agreement, until all obligations under the ICON Agreement are paid in full, we agreed that we shall not declare or pay any dividend or incur any liability to make any other payment or distribution of cash or other property or assets on or in respect of our stock (including common stock, options, warrants, membership interests, general or limited partnership interests, participation or other equivalents).

Securities Authorized For Issuance under Equity Compensation Plans

Equity Compensation Plan Information

as of December 31, 2011

|

Plan category

|

Number of Securities to be Issued upon Exercise of Outstanding Options, Warrants and Rights

|

Weighted Average Exercise Price of Outstanding Options, Warrants and Rights

|

Number of Securities Remaining Available for Future Issuance under the Plan

|

||||||

|

Compensation plans approved by security holders(1) (2) (3)

|

9,344,856

|

$

|

1.63

|

5,019,739

|

|||||

|

Compensation plans not approved by security holders

|

-

|

-

|

-

|

||||||

|

Total

|

9,344,856

|

$

|

1.63

|

5,019,739

|

|||||

(1) Represents the number of shares authorized for issuance under our 2004 Stock Option Plan (the “2004 Plan”) and 2007 Stock Incentive Plan (the “2007 Plan”).

(2) On November 24, 2004, our Board approved and adopted the principal items forming our 2004 Plan. On November 1, 2005, the 2004 Plan was approved by the Board and on March 13, 2006 by our shareholders, at a Special Meeting. Under the 2004 Plan, the Plan Administrator is authorized to grant options to acquire up to a total of 5,500,000 shares of our Common Stock underlying such options. The purpose of the 2004 Plan is to retain the services of valued key employees and consultants of the Company and such other persons as the Plan Administrator (as defined in the 2004 Plan) shall select, and to encourage such persons to acquire a greater proprietary interest in the Company, thereby strengthening their incentive to

achieve the objectives of the shareholders of the Company, and to serve as an aid and inducement in the hiring of new employees and to provide an equity incentive to consultants and other persons selected by the Plan Administrator.

(3) On October 28, 2007, our Board adopted and approved the 2007 Plan which is designated for the benefit of employees, directors and consultants of the Company and its affiliates. On December 17, 2007, our shareholders approved this plan at the Annual Meeting of stockholders. The 2007 Plan authorizes the issuance of awards for up to a total of 8,000,000 shares of our Common Stock underlying such awards. The purpose of the 2007 Plan is to promote the best interests of the Company, and its shareholders by (i) assisting the Company and its affiliates in the recruitment and/or retention of persons with ability and initiative, (ii) providing an incentive to such persons to contribute to the growth and success of the

Company’s businesses by affording such persons equity participation in the Company, and (iii) associating the interests of such persons with those of the Company and its affiliates and shareholders.

Recent Grants under our 2004 Plan and 2007 Plan

I. On February 15, 2010, we granted the following options to directors, officers and employees under and subject to our 2007 Plan:

Guy Nissenson, our Chairman of the Board, President and Chief Executive Officer was granted options to purchase 1,500,000 shares of our Common Stock, fully vested, exercisable at $1.10 per share and expiring five years from the date of grant.

Niv Krikov, our Treasurer, Chief Financial Officer and director was granted options to purchase 400,000 shares of our Common Stock, exercisable at $1.10 per share and expiring seven years from the grant date. 25% of the options vested 12 months from the date of grant. The remaining 75% of the options shall vest over four years in equal quarterly installments beginning 15 months from the date of grant. In the event of a change of control of the Company, any unvested and outstanding portion of the options shall immediately and fully vest.

-18-

The grant of these options was recommended by our Compensation Committee and approved by our Board.

An aggregate of 1,372,500 options to purchase shares of our Common Stock were granted to other employees of the Company and its subsidiaries. Each such option is exercisable at $1.10 per share and expiring seven years from the date of grant. Of these options, 85,000 options were fully vested on the date of grant. 25% of the remaining 1,287,500 options vested 12 months from the date of grant. The remaining 75% of the options shall vest over four years in equal quarterly installments beginning 15 months from the date of grant. Additionally, 125,000 of the options will immediately and fully vest in the event of a change in control of the Company. On March 22, 2010, 69,500 of these options were

exercised.

II. On September 20, 2010, we granted the following options to directors and employees under and subject to our 2007 Plan:

Each of Mr. Itzhak Almog, a former director, and Messrs Shemer S. Schwarz, Israel Singer and Arie Rosenfeld, members of our Board, was granted options to purchase 90,000 shares of our Common Stock, on the following terms: exercise price - $1.22, vesting - 10,000 options per month until all options are vested after nine months from date of grant, expiration date - five years from the date of grant.

The grant of these options was recommended by our Compensation Committee and approved by our Board.

An aggregate of 135,000 options to purchase shares of our Common Stock were granted to other employees of the Company and its subsidiaries. Each such option is exercisable at $1.22 per share and expiring seven years from the date of grant. 25% of the options vested 12 months from the date of grant. The remaining 75% of the options shall vest over four years in equal quarterly installments beginning 15 months from the date of grant.

III. On November 2, 2011, in connection with the consummation of our Rights Offering, we granted the following options to directors, officers and employees under and subject to our 2004 Plan and 2007 Plan:

Mr. Nissenson was granted, under and subject to our 2004 Plan, options to purchase 1,642,379 shares of our Common Stock, fully vested, exercisable at $1.10 per share and expiring five years from the date of grant.

Mr. Krikov was granted, under and subject to our 2007 Plan, options to purchase 391,212 shares of our Common Stock, exercisable at $1.10 per share and expiring seven years from the date of grant. 37.5% of the options vested on the date of grant. The remaining 62.5% of the options shall vest in equal installments over a period of ten quarters with the first quarterly installment vesting on November 14, 2011. In the event of a change of control of the Company, any unvested and outstanding portion of the options shall immediately and fully vest.

Each of Messrs Almog, Schwarz, Singer and Rosenfeld was granted, under and subject to our 2007 Plan, options to purchase 76,581 shares of our Common Stock, fully vested, at an exercise price of $1.10 per share and with expiration date of November 2, 2018.

Mr. Almog was granted, under and subject to our 2004 Plan, options to purchase 348 shares of our Common Stock, fully vested, at an exercise price of $1.10 per share and with expiration date of November 2, 2018.

Mr. Singer was granted, under and subject to our 2004 Plan, options to purchase 1,122 shares of our Common Stock, fully vested, at an exercise price of $1.10 per share and with expiration date of November 2, 2018.

An aggregate of 1,274,277 options to purchase shares of our Common Stock were granted, under and subject to our 2007 Plan, to other employees of the Company and its subsidiaries. Each such option is exercisable at $1.10 per share and expiring seven years from the date of grant. Of these options, 565,011 options were fully vested on the date of grant. The remaining 709,266 of the options shall vest in quarterly installments until September 2014.

An aggregate of 113,113 options to purchase shares of our Common Stock were granted, under and subject to our 2004 Plan, to other employees of our subsidiaries. Each such option is exercisable at $1.10 per share and expiring seven years from the date of grant. All of these options were fully vested on the date of grant.

IV. On December 15, 2011, we granted the following options to Timothy M. Farrar, member of our Board, under and subject to our 2007 Plan:

Options to purchase 90,000 shares of our Common Stock on the following terms: exercise price - $1.22, vesting - 10,000 options per month, beginning on January 15, 2012 and until all options are vested after nine months from date of grant, expiration date - five years from the date of grant.

-19-

Options to purchase 76,581 shares of our Common Stock, fully vested, exercisable at $1.10 per share and expiring seven years from the date of grant.

Recent Sales of Unregistered Securities

None.

Issuances Subsequent to Fiscal 2011

None.

Private Placements Subsequent to Fiscal 2011

None.

ITEM 6. SELECTED FINANCIAL DATA

Not applicable.

ITEM 7. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

FORWARD-LOOKING STATEMENTS

The information set forth in this Management's Discussion and Analysis of Financial Condition and Results of Operations (“MD&A”) contains certain “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933, as amended, Section 21E of the Securities Exchange Act of 1934, as amended, and the Private Securities Litigation Reform Act of 1995, including, among others (i) expected changes in NTS, Inc.'s (referred to herein as the "Company", or "NTSI", "we", "our", "ours" and "us") revenues and profitability, (ii) prospective business opportunities and (iii) our strategy for financing our business. Forward-looking statements are statements