Exhibit 1.2

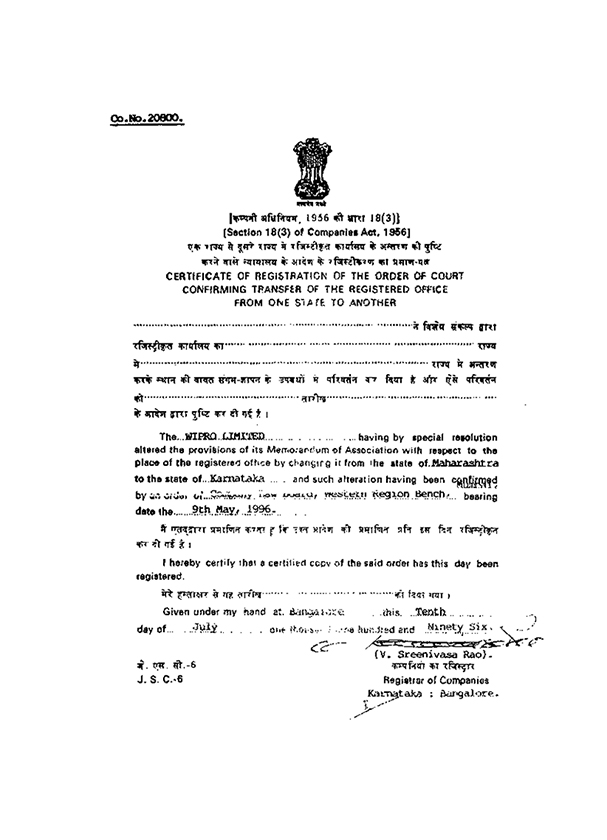

Co.No.20800.

[, 1956 18(3)]

(Section 18(3) of Companies Act, 1956)

CERTIFICATE OF REGISTRATION OF THE ORDER OF COURT

CONFIRMING TRANSFER OF THE REGISTERED OFFICE FROM ONE STATE TO ANOTHER

The WIPRO LIMITED having by special resolution altered the provisions of its Memorandum of

Association with respect to the place of the registered office by changing it from the state of Maharashtra to the state of Karnataka and such alteration having been confirmed by an order of Company Law Board, Western Region Bench, bearing date the

9th May, 1996.

I hereby certify that a certified copy of the said order has this day been registered.

Given under my hand at Bangalore this Tenth day of July one thousand hundred and Ninety Six.

(V. Sreenivasa Rao).

Registrar of Companies

Karnataka : Bangalore.

J.S.C.-6

FRESH CERTIFICATE OF INCORPORATION

CONSEQUENT ON

CHANGE OF NAME

No. 4713/GTA

IN THE OFFICE OF THE REGISTRAR OF COMPANIES

MAHARASHTRA, BOMBAY.

[Under the Companies Act, 1956 (1 of 1956)]

In the matter of *WIPRO PRODUCTS LIMITED.

I hereby certify that WIPRO PRODUCTS LIMITED, which

was originally incorporated on TWENTY NINTH day of December 1945 under the +INDIAN COMPANIES ACT, 1913, and under the name WIPRO PRODUCTS LIMITED having duly passed the necessary resolution in terms of Section 21/22(I) (a) /22(I) (b) of

Companies Act, 1956, and the approval of the Central Government signified in writing having been accorded thereto in the DEPARTMENT OF COMPANY AFFAIRS.

Regional

Director WESTERN REGION letter no. RD : 110(21)1/84 dated 31-3-1984 the name of the said company is this day changed to WIPRO LIMITED and this certificate is issued pursuant to Section 23(I) of the said Act.

Given under my hand at BOMBAY this day of TWENTY EIGHTH APRIL 1984 (One Thousand Nine Hundered EIGHTYFOUR).

Sd/-

(U. C. NAHTA)

Addl. Registrar of Companies,

Maharashtra, Bombay.

* Here give the name of the Company as existing prior to the change.

+ Here give the name of

the Act(s) under which the Company was originally registered and incorporated.

FRESH CERTIFICATE OF INCORPORATION

CONSEQUENT ON

CHANGE OF NAME

In the office of the Registrar of Companies, Maharashtra

(under the Companies Act, 1956 (1 of 1956)

In the matter of

*WESTERN INDIA VEGETABLE PRODUCTS LIMITED

I hereby certify the WESTERN INDIA VEGETABLE

PRODUCTS, LIMITED, which was originally incorporated on TWENTY NINTH day, DECEMBER 1945 under the @ INDIAN COMPANIES Act, 1913 and under the name WESTERN INDIA VEGETABLE PRODUCTS Limited having duly passed the necessary resolution in terms of

Section 21 of the Companies Act, 1956, and the approval of the Central Government signified in writing having been accorded thereto in the Regional Director, Company Law Board, Western Region, Bombay letter No. RD : 8(21) 5/77 dated 6/6/1977,

the name of the said company is this day changed to WIPRO PRODUCTS LIMITED and this certificate is issued pursuant to Section 23(1) of the said Act.

Given

under my hand at BOMBAY this SEVENTH day of JUNE 1977 (One thousand nine hundred and SEVENTY SEVEN).

Sd/-

(V. M. GODBOLE)

Asstt. Registrar of Companies,

Maharashtra, Bombay.

* Here give the name of the Company as existing prior to the change

@ Here give the name of the Act(s) under which the Company was originally registered and incorporated.

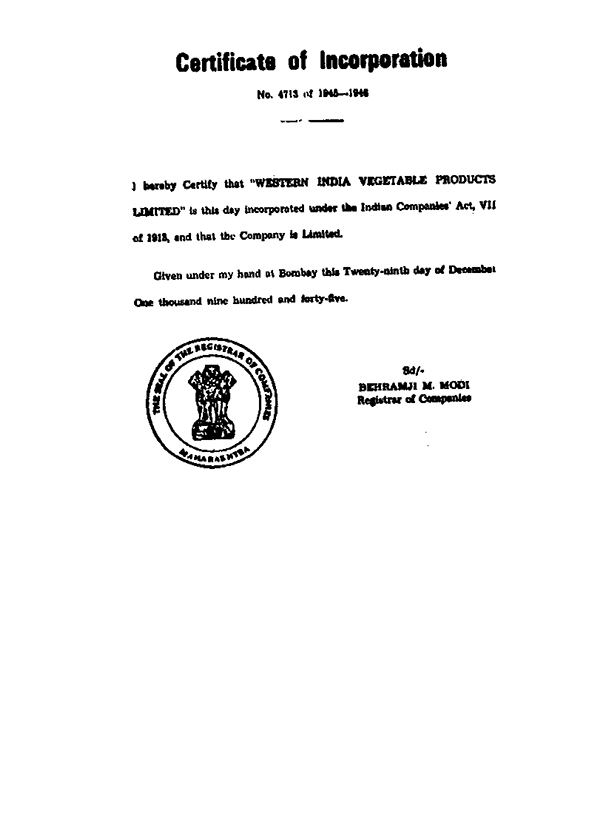

Certificate of Incorporation

No. 4713 of

1945—1946

I hereby Certify that “WESTERN INDIA VEGETABLE PRODUCTS LIMITED” is this day incorporated under the Indian Companies Act, VII of 1913, and

that the Company is Limited.

Given under my hand at Bombay this Twenty-ninth day of December One thousand nine hundred and forty-five.

Sd/-

BEHRAMJI M. MODI

Registrar of Companies

SECOND CERTIFICATE

pursuant to section 610(1)(b)

Certificate of Incorporation

Corporate Identity Number :

L32102KA1945PLC020800

*****

I hereby certify that M/s. WIPRO LIMITED which

was originally incorporated under the companies Act, 1913 on Twenty Ninth day of December One Thousand Nine Hundred and Forty Five and that the company is Limited

Given under my hand at Bangalore this 4th day of July

Two Thousand Thirteen.

(SATYAJIT ROUL)

ASST. REGISTRAR OF COMPANIES,

KARNATAKA::BANGALORE.

| Government of India | ||||

| Special Adhesive | ||||

| Stamp of Rs. 45/- | ||||

| Sd/- | ||||

| Asstt. /Supdt. of Stamps, Bombay |

THE INDIAN COMPANIES ACT, 1913

MEMORANDUM OF ASSOCIATION

OF

WIPRO LIMITED

| 1. | The Name of the Company is WIPRO LIMITED. | Name of the Company | ||||||||

| 2. | The Registered Office of the Company will be situated in the State of Karnataka. | Registered Office | ||||||||

| 3. | The Objects for which the Company is established are the following: | Objects of the Company | ||||||||

| (a) | To purchase or otherwise acquire and take over any lands (whether freehold, leasehold, or otherwise) with or without buildings and plant, machinery, factory or factories or any other property for the purposes of the business of the Company. | |||||||||

| (b) | To carry on the business of extracting oil either by crushing or by chemical or any other processes from copra, cottonseed, linseed, castor-seed, ground-nuts or any other nut or seed or other oil bearing substance whatsoever. | |||||||||

| (c) | To manufacture and deal in hydrogenated oil, vegetable oils, vegetable ghee substitutes, vegetable products and butter-substitutes, glycerine, lubricating oils, greases, boiled oils, varnishes and all other kinds of oils, and oil preparations and products including bye-products of whatsoever description and kind and to carry on the business of manufacturers and dealers in all kinds of oils, oil seeds and oil products and the cultivation of oil-seeds and the business of buyers, sellers and dealers of oil seeds and oil-products including by-products. | |||||||||

| (c) | (i) | To carry on business as manufacturers, sellers, buyers, exporters, importers, and dealers of fluid power products of all types and kinds whether pneumatic or hydraulic and which are worked, propelled, and energised by fluids or gases and in particular the following pneumatic and hydraulic cylinders, air compressors, valves, hydraulic pumps, tools, regulators, filters, rotary tables, drill feeds, hydromotors, hydraulic and pneumatic equipments and all accessories and components required in connection therewith. | ||||||||

| (c) | (ii) | To carry on business as mechanical engineers, tool makers, brass and metal founders, mill-makers, mill-wrighters, machinists, metallurgists; to carry on business of machine operations like turning, boring, reaming, tapping, drilling, milling, shaping, cutting, grinding, honing, lapping, super finishing, buffing and to carry on and undertake processes like electro-plating, electro-forming, electro-etching, hardening, phosphating, nitriding, blackening, tempering, die-casting, shell-moulding, thermo-forming and all foundry operations and to buy, sell, manufacture, repair, convert, alter, let on hire and deal in machines, machine tools and hardware of all kinds. | ||||||||

| (c) | (iii) | To carry on the trade or business of manufacturing and distributing, chemists, and druggists, oil and colourmen, either wholesale or retail, together with all or any trades or business usually carried on in connection therewith and to prepare, manufacture, import, produce, buy, sell and deal in all kinds of raw materials, chemicals, compounds, synthetic products, salts, acids, mineral, vegetable, organic and inorganic alkalies, chemical and surgical materials and appliances and patent or proprietory medicines, pigments, varnishes, lacquers, manufacturing plants, chemicals, scientific, electrical, surgical and optical instruments and apparatus and other like articles and things and colour grinders, makers and dealers in proprietory articles of all kinds and of electrical, chemical, photographical, surgical and scientific apparatus and materials and to buy, sell, manufacture, refine, manipulate, import, export and deal in all substances and things capable of being used in by such business as aforesaid and required by any customers of or persons having dealings with the Company either by wholesale or retail. | ||||||||

| (c) | (iv) | To carry on business as exporters, sellers, dealers and buyers in all types and kinds of goods, articles and things. | ||||||||

| (c) | (v) | To carry on business in India and elsewhere as manufacturer, assembler, designer, builder, seller, buyer, exporter, importer, factors, agents, hirers and dealers of digital and analogue data processing devices and systems, electronic computers, mini and micro computers, micro-processors based devices and systems, electronic data processing equipment, central processing units, memories, peripherals of all kinds, data communication equipment control systems, remote control systems, software of all kinds, including machine oriented and problem oriented, software, data entry devices, data collecting systems, accounting and invoicing machines, intelligent terminals, controllers, media, solid state devices, integrated circuits, transistors, liquid crystals, liquid display systems, diodes, resistors, capacitors, transformers and all related and auxiliary items and accessories including all components of electronic hardware and appliance of any type and description. | ||||||||

| (c) | (vi) | To carry on research and development activities on all aspects related to the products business and objects of the Company. | ||||||||

| (d) | To construct, equip and maintain mills, factories, warehouses, godowns, jetties and wharves any other conveniences or erection suitable for any of the purpose of the Company. | |||||||||

| (e) | To erect, purchase or take on lease, or otherwise acquire any mills, factories, works, machinery, and any other real and personal property appertaining to the goodwill of, and any interest in the business of refining and hydrogenating vegetable and other oils and vegetable products. | |||||||||

| (f) | To carry on all or any of the business of soap and candle makers, tallow merchants, chemists, druggists, dry salters, oil-merchants, manufacturers of dyes, paints, chemicals and explosives and manufacturers of and dealers in pharmaceutical, chemical, medicinal and other preparations or compounds, perfumery and proprietary articles and photographic materials and derivatives and other similar articles of every description. | |||||||||

2

| (g) | To buy or otherwise acquire any oil or manure, mills or factories situate either in India, Ceylon or elsewhere and all property business and rights in connection therewith. | |||||||||

| (h) | To exchange, sell, convey, assign or let on lease or leases or otherwise deal with the whole or any part of the Company’s immoveable property, and to accept as consideration for, or in lieu thereof, other land or cash or Government securities, or securities guaranteed by Government or partly the one and partly the other or such other property or securities as may be determined by the Company, and to take back or reacquire any property so disposed of by re-purchasing or leasing the same for such price or prices or consideration and on such terms and conditions as may be agreed on. | |||||||||

| (i) | To sell or dispose of for cash, or on credit, or to contract for the sale and future delivery of, or to send for sale to any part of India or elsewhere, all the articles and things and also all other products or produce whatsoever of the company. | |||||||||

| (j) | To extend the business of the Company from time to time by purchasing or taking on lease or otherwise acquiring any lands (whether freehold, leasehold or otherwise) with or without buildings and machinery standing thereon situate in Bombay or any where in India, by erecting mills or other buildings on such lands; by purchasing or taking on lease or otherwise acquiring the business, goodwill and property of any private pressing or ginning factory or other factory situate anywhere in India; and by amalgamation with, or purchasing or otherwise acquiring the business goodwill, property and assets of any one or more Joint Stock Company or Companies carrying on any similar business anywhere in India. | |||||||||

| (k) | To extend the business of the Company by adding to, altering or enlarging from time to time all or any of the buildings, premises, plant and machinery for the time being the property of the Company; also by erecting new or additional buildings, on all or any of the lands and premises for the time being the property of the Company and also by expending from time to time such sums of money as may be in the opinion of the Directors necessary or expedient for the purposes of improving, adding to, altering, repairing, and maintaining the buildings, plant, machinery and property of the Company. | |||||||||

| (l) | To undertake the payment of all rents and the performance of all covenants, conditions and agreements contained in and reserved by any lease that may be granted or assigned to or be otherwise acquired by the Company. | |||||||||

| (m) | To purchase the reversion or reversions, or otherwise acquire the freehold of fee simple, of all or any part of the lands for the time being held under lease, or for an estate less than a freehold estate by the Company. | |||||||||

| (n) | To carry on any other trade or business whatsoever as can in the opinion of the Company be advantageously or conveniently carried on by the Company by way of extension of or in connection with any of the Company’s business or as calculated directly or indirectly to develop any branch of the Company’s business or to increase the value of or turn to account any of the Company’s assets property or rights and to acquire forests, forest products, timber and to establish saw mills and dal factories. | |||||||||

3

| (o) | To carry on the business of tin makers, tin manufacturers, tin converters, colliery proprietors, coke manufacturers, miners, smelters, engineers, tin plate makers and iron founders in all their respective branches. | |||||||

| (p) | To acquire and take over the whole or any part of the business, property and liabilities of any person or persons, firm or corporation carrying on any business which this Company is authorised to carry on or possessed of any property or rights suitable for the purposes of the Company. | |||||||

| (q) | To generate, accumulate and supply electricity or other energy for running the Company’s mills, factories, plant and machinery and for other purposes of the business of the Company and to dispose of any surplus electricity or energy for any other purposes and on any terms and conditions and in any manner as the Company thinks expedient or convenient and for such purposes to acquire or construct, lay down, establish, fix and carry out all plant, powerhouse, cables, wires, lines, accumulators, transformers, lamps and works and to carry on the business of electricians and engineers and to do, execute and transact all such other works, acts, matters and things as the Company may think expedient or convenient in connection therewith. | |||||||

| (r) | To acquire, establish and provide or otherwise arrange for transport of any kinds for the purposes of the business of the Company and to construct any lines or works in connection therewith and work the same by steam, gas, oil, electricity or other fuel or power. | |||||||

| (s) | To manufacture or otherwise acquire and deal in containers and packing materials of any kinds including those made of glass, earthenware, metal, cardboard etc. | |||||||

| (t) | To sink wells and shafts, and to make, build and construct, lay down, acquire and maintain, reservoirs, water works, cisterns, tanks, culverts, filter-beds, main and other pipes, plant, machinery and appliances and to execute and do all other works and things expedient or convenient for obtaining, storing and delivering water for the purposes of the business of the Company and to dispose of any surplus water for any other purposes and on any terms and conditions and in any manner as the Company thinks expedient or convenient. | |||||||

| (u) | To apply for, purchase or otherwise acquire any patents, brevets d’invention, licences, concessions and the like conferring an exclusive or non-exclusive or limited right to use, any secret or other information as to any invention which may seem capable of being used for any of the purposes of the Company, or acquisition of which may seem to be expedient or convenient or calculated directly or indirectly to benefit this Company and to use, exercise, develop or grant licences in respect of or otherwise turn to account the property rights and information so acquired. | |||||||

| (v) | To purchase or otherwise acquire from time to time and to manufacture and deal in all such raw materials, stores, stock-in-trade, goods including finished goods, chattles and effects as may be necessary, expedient or convenient for any business for the time being carried on by the Company. | |||||||

| (w) | To pay all costs, charges and expenses incurred or sustained in or about the promotion and establishment of the Company, or which the Company shall consider to be preliminary including therein the cost of advertising, commissions for underwriting, brokerage, printing and stationery and expenses attendant upon the formation of agencies and local boards. | |||||||

4

| (x) | To enter into any partnership or any arrangement for sharing profits, union of interests, joint ventures, reciprocal concession or otherwise with any person or persons or corporation carrying on or engaged in or about to carry on or engage in, any business or enterprise which this Company is authorised to carry on or engage in, or any business or transaction capable of being conducted so as directly or indirectly to benefit or to be expedient for the purposes of this Company and to take or otherwise acquire and hold shares or stock in or securities of and to subsidise or otherwise assist any such Company and to sell, hold reissue with or without guarantee or otherwise deal with such shares, stock or securities. | |||||||

| (y) | To purchase or otherwise acquire all or any part of the business, property and liabilities of any person, company, society, or partnership formed for all or any of the purposes within the objects of this Company and to conduct and carry on or liquidate and wind up any such business. | |||||||

| (z) | To enter into any arrangement with any Government or authorities, supreme, municipal, local or otherwise that may seem conducive to the Company’s objects or any of them and to obtain from any such Government or authority any rights, privileges and concessions which the Company may think fit desirable or expedient to obtain and to carry out, exercise and comply with any such arrangements, rights, privileges and concessions. | |||||||

| (a1) | To provide for the welfare of person in the employment of the Company, or formerly engaged in any business acquired by the Company and the wives, widows, families or dependants of such persons by grants of money, pensions or other payments, and by establishing and supporting or aiding in the establishment and support of associations, institutions, funds, trusts, conveniences and by providing or subscribing towards places of instruction and recreation and hospitals, dispensaries, medical and other attendances and other assistance, as the Company shall think fit and to form, subscribe to or otherwise aid benevolent, religious, scientific, national, social, public, or other institutions or objects, or any exhibitions which shall have any moral or other claims to support or aid by the Company by reason of the locality of its operations or otherwise. | |||||||

| (a1) | (i) | To undertake, carry out, promote and sponsor rural development including any programme for promoting the social and economic welfare or uplift of the public in any rural area if the Directors consider it likely to promote and assist rural development and to give contributions to any recognised authority or institution and/or to incur any expenditure on any programme of rural development and to assist execution and promotion thereof either directly or through an independent agency or in other manner. Without prejudice to the generality of the foregoing, the words ‘rural area’ shall include such areas as may be regarded as rural areas under Section 35 CC of the Income-tax Act, 1961 or any other law relating to rural development for the time being in | ||||||

5

| force or as may be regarded by the Directors as rural areas and the Directors may at their discretion in order to implement any of the above mentioned objects or purposes transfer without consideration or at such fair or concessional value as the Directors may think fit and divest the ownership of any property of the Company to or in favour of any public or local body or authority or central or state government or any public institutions or trust established under any law for the time being in force or registered or approved by the central or state Government or any authority specified in that behalf. | ||||||||

| (a1) | (ii) | To undertake, carry out, promote and sponsor or assist any activity for the promotion and growth of the national economy and for discharging what the Directors may consider to be the social and moral responsibilities of the Company to the public or any section of the public as also any activity which the Directors consider likely to promote national welfare or the social, economic moral uplift of the public or any section of the public and by such means as the Directors may think fit and the Directors may without prejudice to the generality of the foregoing undertake, carry out, promote and sponsor any activity for publication of any books, literature, newspaper, etc. for organising lectures or seminars, likely to advance these objects or for giving merit awards, scholarships, loans or any other assistance to deserving students or other scholars or persons to enable them to prosecute their studies or academic pursuits or researches or for establishing, conducting or assisting any institution, fund, trust, etc. having any one of the aforesaid objects as one of its objects by giving donations or otherwise in any other manner and the Directors may at their discretion in order to implement any of the above mentioned objects or purposes transfer without consideration or at such fair or concessional values as the Director may think fit and divest the ownership of any property of the Company to or in favour of any public institutions or trusts established under any law for the time being in force or registered or approved by the central or state Government or any authority specified in that behalf. | ||||||

| (a2) |

From time to time to subscribe or contribute to any charitable, benevolent or useful object of a public character the support of which will, in the opinion of the Company, tend to increase its repute or popularity among its employees, its customers or the public. | |||||||

| (a3) |

To promote any company or companies for the purpose of acquiring all or any of the properties, rights and liabilities of this Company or for any other purpose which may seem directly or indirectly calculated to benefit this Company. |

|||||||

| (a4) |

Generally to purchase, take on lease or in exchange, hire or otherwise acquire any real and personal property and any rights or privileges which the Company may think necessary, expedient or convenient for the purpose of its business and in particular any lands, buildings, easements, machinery, plant and stock-in-trade. |

|||||||

| (a5) | To construct, maintain, alter, improve and enlarge any buildings or works necessary or convenient for the purposes of the Company. | |||||||

6

| (a6) | To construct, carry out, maintain, improve, manage, work, control, and superintend any roads, ways, tramways, railways, branches, or sidings, bridges, reservoirs, canals, docks, wharves, water-courses, hydraulic works, gas works, electric works, factories, mills, warehouses and other works and conveniences which may seem directly or indirectly conducive to any of the Company’s objects and contribute to subsidize or otherwise assist or take part in such maintenance, management working, control and superintendence. |

|||||||

| (a7) | To invest and deal with the moneys of the Company not immediately required in shares, stock, bonds, debentures obligations or other securities of any Company or association or in Government securities or in deposit with Banks or in any other instruments or commodities or in any other manner as may from time to time be determined. | |||||||

| (a8) | To lend money to such persons and on such terms as may seem expedient and in particular to customers and others having dealings with Company and to give any guarantee or indemnity as may seem expedient. | |||||||

| (a9) | To borrow or raise or secure the payment of money by mortgage or by the issue of debentures or debenture stock perpetual or otherwise, or in such other manner as the Company shall think fit and for the purposes aforesaid to charge all or any of the Company’s property or assets present and future including its uncalled and collaterally or further to secure any securities of the Company by a Trust Deed or other assurance and to redeem, purchase or pay off any such security. | |||||||

| (a10) | Upon any issue of shares, debentures or other securities of the Company to employ broker-commission agents and underwriters and to provide its remuneration of such reasons for their services by payment in cash, or by the issue of shares debentures or other securities of the Company, or by the granting of options, to take the same, or in any other manner allowed by law. | |||||||

| (a11) | To draw, make, accept endorse, discount, execute, and issue promissory notes, bills of exchange, hundles, bills of lading, warrants, debentures and other negotiable or transferable instruments. | |||||||

| (a12) | To undertake and execute any trusts the undertaking whereof may seem desirable or expedient, and either gratuitously or otherwise. | |||||||

| (a13) | To sell or dispose of the undertaking of the Company or any part thereof in such manner and for such consideration as the Company may think fit and in particular for shares (fully or partly paid-up) debentures, debenture stock or securities of any other Company whether promoted by the Company for the purpose or not and to improve, manage, develop, exchange, lease, dispose of, turn to account or otherwise deal with all or any part of the property and rights of the Company. | |||||||

| (a14) | To adopt such means of making known the production of the Company as may seem expedient or convenient and in particular by advertising in the press by circulars, by purchase and exhibition of works of art or interest, by publication of books and periodicals and by granting prizes, rewards and donations. | |||||||

| (a15) | To establish and maintain local registers, agencies and branch places of business and procure the Company to be registered or recognized and carry on business in any part of the world. | |||||||

7

| (a16) | To sell, improve, manage, develop, exchange, enfranchise, lease, mortgage, dispose of, turn to account or otherwise deal with all or any part of the property and rights of the Company. | |||||||

| (a17) | To place, to reserve or to distribute as dividend or bonus among the members or otherwise to apply as the Company may from time to time think fit, any moneys of the company including moneys received by way of premium on shares or debentures issued at a premium by the Company and any moneys received in respect of dividends accrued on forfeited shares and also moneys arising from the sale by the Company of forfeited shares or from unclaimed dividends. | |||||||

| (a18) | To distribute any of the Company’s property among the members in specie or kind. | |||||||

| (a19) | To do all or any of the above things in any part of the world and either as principals, agents, trustees or otherwise and either alone or in conjunction with others and by or through agents, sub-contractors, trustees or otherwise. | |||||||

| (a20) | To do all such other things as are incidental or the Company may think expedient or conducive to the attainment of the above objects or any of them. | |||||||

| (a21) | To carry on the business of leasing and hire purchase and to acquire, to provide on lease or to provide on hire purchase basis, all types of industrial and office plant, equipment, machinery, vehicles, buildings and real estate, required for manufacturing, processing, transportation, and trading businesses and other commercial and service businesses. | |||||||

| (a22, a23 and a24 Amended vide resolution passed by members at the Annual General Meeting held on July 21, 2005) | (a22) | To undertake and carry on the business of providing all kinds of information technology based and enabled services in India and internationally, electronic remote processing services, eServices, including all types of Internet-based/ Web enabled services, transaction processing, fulfillment services, business support services including but not limited to providing financial and related services of all kinds and description including billing services, processing services, database services, data entry business-marketing services, business information and management services, training and consultancy services to businesses, organizations, concerns, firms, corporations, trusts, local bodies, states, governments and other entities; to establish and operate service processing centers for providing services for back office and processing requirements, marketing, sales, credit collection services for companies engaged in the business of remote processing and IT enabled services from a place of business in India or elsewhere, contacting & communicating to and on behalf of overseas customers by voice, data image, letters using dedicated international private lines; and to handle business process management, remote help desk management; remote management; remote customer interaction, customer relationship management and customer servicing through call centers, email based activities and letter/fax based communication, knowledge storage and management, data management, warehousing, search, integration and analysis for financial and non financial data. | ||||||

8

| (a23) | To act as information technology consultants and to operate a high technology data processing center for providing information processing, analysis, development, accounting and business information and data to customers in India and internationally; to carry on the business of gathering, collating, compiling, processing, analyzing, distributing, selling, publishing data and information and including conduct of studies and research, and marketing of information and services and providing access to information regarding financial operations and management, financial services, investment services business and commercial operations, financial status, creditworthiness and rating, consumer responses and management of businesses of all kinds and descriptions by whatever name called. | |||||||

| (a24) | To carry on the business as Internet service provider and undertake any and all kinds of Internet/web based activities and transactions; to design, develop, sell, provide, maintain, market, buy, import, export, sell and license computer software, hardware, computer systems and programs products, services and to give out computer machine time and to carry on the business of collecting, collating, storing, devising other systems including software programs and systems. | |||||||

| (Amended vide Special Resolution by way of Postal Ballot held on June 25, 2008) | (a25) | To design, develop, fabricate, manufacture, operate, install, maintain, and assemble, export from and Import, sell or otherwise deal in all kinds of end to end solutions including equipments, for water treatment including but not limited to ultra pure water, waste water treatment, water reuse and desalination and related activities. | ||||||

|

(a26) |

To design, develop, fabricate, manufacture, assemble, operate, maintain, export from and import, sell or otherwise deal in and to act as consultant, designer, supplier, manufacturer, importer or exporter of every goods and services including equipments in connection with all types of renewal energy systems, food and agricultural processing systems such as but not limited to Biofuel, wind energy, solar energy, geo-thermal energy systems, filing, sealing, coding, marking/labeling and packaging machinery and equipment, agricultural tools/implements, machinery and equipment, agricultural product processing including food processing project and equipment not limited to such purposes as power generation, water heating, sorting, grading, washing, cutting, slicing, mixing, waxing, distillation, fermentation, filteration, drying, concentration, heat exchangers, mixing, pasteurization systems, etc made of all types of steel and other special metals / non metals for all types of applications and user industries and to deliver these plant, equipment, machinery and services anywhere in the world. |

|||||||

| AND it is hereby declared that the word Company in this clause shall be deemed to include any partnership or other body of persons whether incorporated or not and whether domiciled in India or elsewhere and the intention is that the objects specified in each sub-clause or paragraph of this Clause shall except where otherwise expressed such sub-clause or paragraph, be in no ways limited or restricted by reference to or inference from the terms of any other sub-clause or paragraph or the name of the Company but may be carried out in as full and ample a manner and construed in as wide a sense as if each of the said sub-clause or paragraphs defines the objects of a separate distinct and independent company. | ||||||||

9

| Members Liability limited | 4. | The liability of the members is limited | ||

| Capital (Amended vide pursuant to the orders of High Court of Karnataka, in the company petition nos. 291 and 292 of 2013) | 5. | “The Authorized Share Capital of the company is Rs. 610,00,00,000/- (Rupees Six Hundred and Ten Crore Only) divided into 291,75,00,000 (two hundred and ninety one crores seventy five lakhs) Equity Shares of Rs. 2/- (Rupees two only) each, 2,50,00,000 (Two Crore Fifty lakhs) preference shares of Rs. 10/- (Rupees ten only) each and 1,50,000 (One lakh Fifty Thousand) 10% optionally convertible Cumulative Preference shares of Rs. 100/- each, with power to increase and reduce or consolidate or sub-divide the capital of the Company and to divide the shares in the Capital for the time being into several classes and to attach thereto respectively such preferential, deferred, qualified or special rights, privileges or conditions as may be determined by or accordance with the Articles of Association of the Company for the time being and to verify, modify or abrogate any such rights, privileges or conditions in such manner as may for the time being be permitted by the Act or provided by the Articles of Association of the Company for the time being.”. | ||

9-1

We, the several persons, whose names and addresses are subscribed thereto, are desirous of being formed into a Company in pursuance of this Memorandum of Association and we respectively agree to take the number of shares in the Capital of the Company set opposite to our respective names.

| Names |

Address and description of subscribers |

Number of Shares taken by each subscriber |

Witness | |||

| Sd. R M. Chinoy | Radio House, Apollo Bunder, Fort, Bombay, Director, Indian Radio & Cable Communication Co., Ltd. | 50 | Sd. N. P. Vansia | |||

| Sd. Pranlal Devkaran Nanjee | 17, Elphinstone Circle, Fort, Bombay, Banker. | 100 | Sd. N. P. Vansia | |||

| Sd. Behram N. Karanjia | 17-19, Bomanji Master Road, Kalba-devi Road, Bombay-2 General Merchant. | 50 | Sd. N. P. Vansia | |||

| Sd. Ratansey Karsondas Vissanji | 9, Wallace Street Fort, Bombay, Director, Wallace Flour Mills, Ltd. | 50 | Sd. N. P. Vansia | |||

| Sd. Dewjee Tokarsee Mooljee | 17, Bazargate Street, Fort, Bombay General Merchant. | 50 | Sd. N. P. Vansia | |||

| Sd. Ratilal Mulji Gandhi | C/o Messrs R Ratilal & Co. Teju Kaya Building, Chinch Bunder Road, Bombay-9 General Merchant | 100 | Sd. N. P. Vansia | |||

| Sd. Mohamed Husein Hasham Premji | Botawala Building, 8, Elphinstone Circle, Fort, Bombay, General Merchant |

100 | Sd. N. P. Vansia | |||

| Sd. Gangaram Vallabhji | Botawala Building, 8, Elphinstone Circle, Fort Bombay, Merchant |

50 | Sd. N. P. Vansia | |||

Dated the 21st day of December 1945.

9A

THE COMPANIES ACT, 2013

COMPANY LIMITED BY SHARES

(INCORPORATED UNDER THE COMPANIES ACT, 1913)

ARTICLES OF ASSOCIATION

OF

WIPRO LIMITED

1

The following regulations comprised in these Articles of Association were adopted pursuant to members’ resolution passed at the Annual General Meeting held on July 23, 2014 in substitution for and to the entire exclusion of, the regulations contained in the existing Articles of Association of the Company.

ARTICLES OF ASSOCIATION

OF

WIPRO LIMITED

I. CONSTITUTION OF THE COMPANY

| Table F not to apply | 1 | Wipro Limited is established with Limited Liability in accordance with and subject to the provisions of the Indian Companies Act, 1913, but none of the Regulations contained in the Table marked F in Schedule I to the Companies Act, 2013, shall be applicable to the Company except so far as the said Act or any modification there otherwise expressly provides. | ||||||

| Company to be governed by these Articles |

The Regulations for management of the Company and for the observance of the members shall be such as are contained in these Articles. | |||||||

| II. INTERPRETATION | ||||||||

| Interpretation Clause | 2 |

(a) |

In the interpretation of these Articles, the following words and expressions shall have the following meanings, unless repugnant to the subject or context. | |||||

| “Alter” | (i) | ‘Alter’ and ‘Alteration’ shall include the making of additions and omissions. | ||||||

| “Auditors” | (ii) | ‘Auditors’ means those Auditors appointed under the said Act. | ||||||

| “A Company” | (iii) | A Company means a company as defined under Section 2(20) of the Act. | ||||||

| “Board” | (iv) | ‘Board’ means the Directors of the Company collectively, and shall include a committee thereof. | ||||||

| “Body Corporate or Corporation” | (v) | ‘Body Corporate’ or’ Corporation’ includes a company incorporated outside India but does not include, (1) a Co-operative Society registered under any law relating to Co-operative Societies, (2) any other body corporate which the Central Government may by notification in the Official Gazette specify in that behalf. | ||||||

2

| “The Company” or “This Company” | (vi) | The Company’ or This Company’ means Wipro Limited established as aforesaid. | ||

| “The Companies Act 2013”

“The said Act” or “The Act” |

(vii) | ‘The Companies Act, 2013’, The said Act’, or The act’ and reference to any section or provision thereof respectively means and includes the Companies Act, 2013 (Act No. 18 of 2013) and any statutory modification thereof for the time being in force, and reference to the section or provision of the said Act or such statutory modification. | ||

| “Debenture” | (viii) | ‘Debenture’ includes Debenture stock, bonds or any other instrument of a Company evidencing a debt, whether constituting a charge on the assets of the company or not. | ||

| “Directors” | (ix) | ‘Directors’ means a director appointed to the Board of the company. | ||

| “Dividend” | (x) | ‘Dividend’ shall include interim dividend. | ||

| “Document” | (xi) | ‘Document’ includes summons, notice, requisition, order, declaration, form and register, whether issued, sent or kept in pursuance of this Act or under any other law for the time being in force or otherwise, maintained on paper or in electronic form. | ||

| “Executor” or “Administrator” | (xii) | “Executor” or “Administrator” means a person who has obtained probate or Letters of Administration, as the case may be, from a competent Court, and shall include the holder of a Succession Certificate authorising the holder thereof to negotiate or transfer the share or shares of the deceased members, and shall also include the holder of a Certificate granted by the Administrator-General of any State in India. | ||

3

| “Financial Statements” | (xiii) | “Financial Statements means: | ||||

| (i) | a balance sheet as at the end of the financial year; | |||||

| (ii) | a profit and loss account, or in the case of a company carrying on any activity not for profit, an income and expenditure account for the financial year; | |||||

| (iii) | cash flow statement for the financial year; | |||||

| (iv) | a statement of changes in equity, if applicable; and | |||||

| (v) | any explanatory note annexed to, or forming part of, any document referred to in sub-clause (i) to sub-clause (iv) | |||||

| “In writing” | (xiv) | “In writing” or “Written” shall include e-mail, and any other form of electronic transmission. | ||||

| “Independent Director” | (xv) | “Independent Director” shall have the meaning ascribed to it in the Act. | ||||

| “Key Managerial Personnel” | (xvi) | “Key Managerial Personnel” means the Chief executive officer or the managing director; the company secretary; whole-time director; chief financial officer; and such other officer as may be notified from time to time in the Rules. | ||||

| “Month” | (xvii) | “Month” means calendar month. | ||||

| “National Holiday” | (xviii) | “National Holiday” means the day declared as national holiday by the Central Government. | ||||

| “Office” | (xix) | ‘Office” means the Registered Office for the time being of the Company. | ||||

4

| “Ordinary & Special Resolution” |

(xx) | “Ordinary Resolution” and “Special Resolution” shall have the meanings assigned to these terms by Section 114 of the Act. | ||||

| “Rules” |

(xxi) | “Rules” means any rule made pursuant to section 469 of the Act or such other provisions pursuant to which the Central Government is empowered to make rules, and shall include such rules as may be amended from time to time. | ||||

| “Secretary” |

(xxii) | “Secretary” is a Key Managerial Person appointed by the Directors to perform any of the duties of a Company Secretary. | ||||

| “Shareholders ‘or Members” |

(xxiii) | “Shareholders” or “Members” means the duly registered holder from time to time of the shares of the Company, and shall include beneficial owners whose names are entered as a beneficial owner in the records of a depository. | ||||

| “The Seal” |

(xxiv) | “The Seal” means the common seal of the Company for the time being. | ||||

| “These presents” |

(b) | “These presents” means and includes the Memorandum and this Articles of Association. | ||||

| Singular Number |

(c) | Words importing the singular number include, where the context admits or requires, the plural number and vice versa. | ||||

| Gender |

(d) | Words importing the masculine gender also include the feminine gender. | ||||

| Persons |

(e) | Words importing persons shall, where the context requires, include bodies corporate and companies as well as individuals. | ||||

5

| Words and expressions defined in the Companies Act, 2013 |

(f) | Subject as aforesaid, any words and expressions defined in the said Act as modified up to the date on which these Articles become binding on the Company shall, except where the subject or context otherwise requires, bear the same meanings in these Articles. | ||||

| Marginal Notes and other Headings | (g) | The marginal notes and the headings given in these Articles shall not affect the construction hereof. | ||||

| Copies of the Memorandum and Articles to be Furnished | 3 | The Company shall, on being so required by a Member, send to him within seven days of the requirement and subject to the payment of a fee of Rs. 100/- or such other fee as may be specified in the Rules for each copy of the documents specified in Section 17 of the said Act. | ||||

| III. SHARE CAPITAL, VARIATION OF RIGHTS & BUY BACK | ||||||

| Capital and shares | 4 | The Authorised Share Capital of the Company shall be such amount and be divided into such shares as may from time to time, be provided in clause V of Memorandum of Association. with power to Board of Directors to reclassify, subdivide, consolidate and increase and with power from time to time, to issue any shares of the original capital or any new capital with and subject to any preferential, qualified or special rights, privileges, or conditions may be, thought fit and upon the sub-division of shares to apportion the right to participate in profits, in any manner as between the shares resulting from sub-division.

The Authorised Share Capital of the Company shall be such amount and be divided into such shares as may from time to time, be provided in clause V of Memorandum of Association. with power to Board of Directors to reclassify, subdivide, consolidate and increase and with power from time to time, to issue any shares of the original capital or any | ||||

6

| new capital with and subject to any preferential, qualified or special rights, privileges, or conditions may be, thought fit and upon the sub-division of shares to apportion the right to participate in profits, in any manner as between the shares resulting from sub-division. | ||||||||||||

| If and whenever the capital of the Company is divided into shares of different classes, the tights of any such class may be varied, modified, affected, extended, abrogated or surrendered as provided by the said Act or by Articles of Association or by the terms of issue, but not further or otherwise. | ||||||||||||

| Provisions of Section 43, 47 of the Act to apply | 5 | The provisions of Section 43, 47 of the Act in so far as the same may be applicable to issue of share capital shall be observed by the Company. | ||||||||||

| Restrictions on Allotment | 6 | The Directors shall have regard to the restrictions on the allotment of shares imposed by Section 39 and 40 of the said Act so far as those restrictions are binding on the Company. | ||||||||||

| Commission for placing shares | 7. | (1) | (i) | The Company may at any time pay a commission to any person in consideration of his subscribing, or agreeing to subscribe (whether absolutely or conditionally) for any shares in or debentures of the Company or procuring or agreeing to procure subscription (whether absolute or conditional) for any shares in or debentures of the Company and the provisions of Section 40 of the said Act shall be observed and complied with. Such commission shall not exceed the maximum permissible rate as prescribed in the Rules. Such commission may be paid in cash or by the allotment of Securities. | ||||||||

7

| (ii) | Company shall not pay any commission to any underwriter on securities which are not offered to public for subscription. | |||||||

| (iii) | The number of shares or debentures which persons have agreed to for commission to subscribe absolutely or conditionally is disclosed in the manner aforesaid. | |||||||

| (2) | Nothing in this clause shall affect the power of the Company to pay such brokerage as it may consider reasonable. | |||||||

| (3) | A Vendor to, promoter of, other person who receives payment in shares, debentures or money from the Company shall have and shall be deemed always to have had power to apply any part of the shares, debentures or money so received in payment of any commission the payment of which, if made directly by the Company, would have been legal under this Articles. | |||||||

| (4) | The commission may be paid or satisfied (subject to the provisions of the Act and these Articles) in cash or in share, debentures or debenture stock of the Company, (whether fully paid or otherwise) or in any combination thereof. | |||||||

| Company not to give financial assistance for purchase of its own shares | 8. | Except as provided by the Act, the Company shall not, except by reduction of capital under the provision of Sections 66 or Section 242 of the said Act, buy its own shares nor give, whether directly or indirectly, and whether by means of a loan, guarantee, provision of security or otherwise any financial assistance for the purpose of or in connection with a purchase or subscription made or to be made by any person of or for any shares in the Company or in its holding company. | ||||||

| Provided that nothing in this Article shall be taken to prohibit: | ||||||||

8

| 8.1 | (i) | the provision of money in accordance with any scheme approved by the Company through Special Resolution and in accordance with the requirements specified in the relevant Rules, for the purchase of, or subscription for, fully paid up Shares in the Company, if the purchase of, or the subscription for the Shares held by trustees for the benefit of the employees or such Shares held by the employee of the Company; | ||||

| (ii) | the giving of loans by the Company to persons in the employment of the Company other than its Directors or Key Managerial Personnel, for an amount not exceeding their salary or wages for a period of six months with a view to enabling them to purchase or subscribe for fully paid up Shares in the Company to be held by them by way of beneficial ownership.

Nothing in this clause shall affect the right of the Company to redeem any shares issued under Section 55. | |||||

| Buy back of Shares | 8.2 | Notwithstanding what is stated in Articles 8.1 above, in the event it is permitted by the Law and subject to such conditions, approvals or consents as may be laid down for the purpose, the Company shall have the power to buy-back its own shares, whether or not there is any consequent reduction of Capital. If and to the extent permitted by Law, the Company shall also have the power to re-issue the shares so bought back. | ||||

| Issue of Securities at a Premium | 9 | The Company shall have power to issue Securities at a premium and shall duly comply with the provision of Sections 52 of the said Act. | ||||

9

| Issue of redeemable preference shares | 10 | The Company may, subject to the provisions of Section 55 of the said Act, issue preference shares which are liable to be redeemed and may redeem such shares in any manner provided in the said section and may issue shares up to the nominal amount of the shares redeemed or to be redeemed. Where the Company has issued redeemable preference shares the provisions of the said section shall be complied with. The manner in which such shares shall be redeemed, shall be as provided by Article 80 unless the terms of issue otherwise provide. | ||||

| IV. SHARES AND SHAREHOLDERS | ||||||

| Register of Members | 11 | (1) | The Company shall cause to be kept and maintained the following registers namely: | |||

| (a) Register of members indicating separately for each class of equity and preference shares held by each member residing in India or outside India; | ||||||

| (b) Register of debenture-holders; and | ||||||

| (c) Register of any other security holders: | ||||||

| (d) including an index in respect of each of the registers to be maintained in accordance with Section 88 of the Act. | ||||||

| (2) | The Company shall also comply with the provisions of Sections 92 of the Act as to filing Annual Returns. | |||||

| (3) | The Company shall duly comply with the provisions of Section 94 of the Act in regard to keeping of the Registers, Indexes, copies of Annual Returns and giving inspection thereof and furnishing copies thereof. | |||||

10

| Shares to be numbered progressively | 12 | The shares in the capital shall be numbered progressively according to their several classes. | ||||

| Shares at the disposal of the Directors | 13 | Subject to the provisions of the said Act and these Articles, the shares in the capital of the Company for the time being (including any shares forming part of any increased capital of the Company) shall be under the control of the Directors who may issue, allot or otherwise dispose of the same or any one of them to such persons on such proportion and on such terms and conditions and either at a premium or at par or (subject to compliance with the provisions of Section 54 of the Act) at a discount and at such times as they may from time to time think fit and proper and with the sanction of the Company in General Meeting to give to any person the option to call for or be allotted shares of any class of the Company either at par or at premium or subject aforesaid at a discount during such time and for such consideration and such option being exercisable at such times as the Directors think fit and may allot and issue shares in the capital of the Company in lieu of services rendered to the Company or in the conduct of its business; and any shares which may be so allotted may be issued as fully paid up shares and if so issued shall be deemed to be fully paid up shares. | ||||

| Every share transferable etc. | 14 | (1) | The shares or other interest of any member in the Company shall be movable property transferable in the manner provided by the Articles of the Company. | |||

| (2) | Each share in the Company having a share capital shall be distinguished by its appropriate number. | |||||

11

| (3) | Certificates of Shares : | |||||

| A certificate under the Seal of the Company specifying any shares held by any Member shall be prima facie evidence of the title of the Member to such shares. | ||||||

| Application of premiums received on issue of shares | 15 | (1) | Where the Company issues shares at a premium, whether for cash or otherwise, a sum equal to the aggregate amount of the value of the premiums on those Shares shall be transferred to an amount to be called “the securities premium account”, and the provisions of the Act relating to the reduction of the Share Capital of a company shall except as provided in this clause, apply as if the securities premium account were paid-up share capital of the Company. | |||

| (2) | The securities premium account may be applied by the Company for the purposes permissible pursuant to the Act | |||||

| Further issue of capital | 16 | The Company shall comply with the provisions of Section 62 of the Act with regard to increasing the subscribed capital of the Company. | ||||

| 17 | If and whenever as the result of issue of new shares or any consolidation or subdivision of shares, any shares become held by members in fractions the Directors shall subject to the provisions of the Act and the Articles and to the directions of the Company in general meeting, if any, sell those shares which members hold in fractions for the best price reasonably obtainable and shall pay and distribute to and amongst the members entitled to such shares in due proportion, the net proceeds of the sale thereof. For the purpose of giving effect to any such sale the Directors may authorise any person to transfer the shares sold to the purchaser thereof comprised in any such transfer and he shall not be bound to see to the application of the purchase money nor shall his title to the shares be effected by any irregularity or invalidity in the proceedings in reference to the sale. | |||||

12

| Acceptance of shares | 18 | An application signed by or on behalf of an applicant for shares in the Company followed by an allotment of shares therein, shall be an acceptance of shares within the meaning of these Articles;. The Directors shall comply with the provisions of Sections 39 and 40 of the Act so far as applicable. | ||||

| Deposit and call etc. to be a debt payable immediately | 19 | The money (if any) which the Directors shall, on the allotment of any shares being made by them, require or direct to be paid by way of deposits, calls or otherwise in respect of any shares allotted by them, shall, immediately on the inscription of the name in the Register of Members as the holder of such shares, become a debt due to and recoverable by the Company from the allottee thereof, and shall be paid by him accordingly. | ||||

| Calls on shares of the same class to be made on uniform basis Calls on shares of the same class to be made on uniform basis | 20 | Where any calls for further share capital are made on shares, such calls shall be made on a uniform basis on all shares, falling under the same class.

Explanation: - For the purpose of this provision shares of the same nominal value on which different amounts have been paid up shall not be deemed to fall under the same class. | ||||

| Return of allotment | 21 | The Directors shall cause to be made the returns as to all allotments from time to time made in accordance with the provisions of Section 39 of the said Act. | ||||

| Installments on shares to be duly paid | 22 | If, by the conditions of allotment of any shares the whole or part of the amount or issue price thereof shall be payable by installments, every such installment shall, when, due, be paid to the Company by the person who for the time being and from time to time shall be of the shares or his legal representative. | ||||

13

| Liability of Members | 23 | Every member, or his executors or administrators or other representative, shall pay to the Company the portion of the capital represented by his share or shares, which may, for the time being, remain unpaid thereon, in such amounts, at such time or times, and in such manner, as the Directors shall, from time to time, in accordance with the Company’s regulations, require or fix for the payment thereof. | ||||

| Liability of Joint holders | 24 | If any share stands in the names of two or more persons all the joint-holders of the share shall be severally as well as jointly liable for the payment of all deposits, installments, and calls due in respect of such shares, and for all incidents thereof according to the Company’s regulations; but the persons first named in the Register shall, as regards service of notice, and all other matters connected with the Company, except the transfer of the share and any other matter by the said Act or herein otherwise provided, be deemed the sole holder thereof. | ||||

| Registered holder only the owner of the shares | 25 | Save as herein or by laws otherwise expressly provided, the Company shall be entitled to treat the registered holder of any share as the absolute owner thereof, and accordingly shall not, except as ordered by a Court of competent jurisdiction, or as by statute required, be bound to recognize any benami trusts whatsoever or equitable, contingent, future, partial or other claim to or interest in such share on the part of any other person whether or not it shall have express or implied notice thereof; the Directors shall, however be at liberty, at their sole discretion, to register any share in the joint names of any two or more persons, and the survivor or survivors of them. | ||||

14

| V. CERTIFICATES | ||||||||

| Certificate of shares | 26 | Subject to any statutory or other requirement having the force of law governing the issue and signatures to and sealing of certificate to shares and applicable to this Company for the time being in force the certificate of title to shares and the duplicate thereof when necessary shall be issued under the seal of the Company which shall be affixed in the presence of and signed by (1) two Directors or persons acting on behalf of the Directors under a duly registered power of attorney and (2) the Secretary or some other person appointed by the Board for the purpose; a Director may sign a share certificate by affixing signature thereon by means of any machine, equipment or other mechanical means such as engraving in metal or lithography but not by means of a rubber stamp, provided that the Director shall be responsible for the safe custody of such machine, equipment or other materials used for the purpose. | ||||||

| Members’ right to Certificates | 27 | (1) | (i) | Every member shall be entitled without payment to the certificate for all the Shares of each class or denomination registered in his name, or if the Board, so approve (upon paying such fees as the Board may from time to time determine) to several certificates, each for one or of such Shares and the Company shall complete such certificate within two months after the allotment or such period as may be determined at the time of the issue of such capital whichever is longer or within one month after registration of the transfer thereof as provided by Section 56 of the Act. Every certificate of shares shall have its distinctive number and be issued under the Seal of the Company and shall specify the number and denoting number of the shares in respect of which it is issued and the | ||||

15

| amount paid thereon and shall be in such form as the Board shall prescribe or approve provided that in respect of share or shares held jointly by several persons, the Company shall not be bound to issue more than one certificate and the delivery of a certificate for a share or shares to one of several joint-holders shall be deemed to be sufficient delivery to all. | ||||

| May be delivered to any one of Joint-holders | (ii) | A certificate of shares registered in the names of two or more persons, unless otherwise directed by them in writing, may be delivered to any one of them on behalf of them all. | ||

| Shares in Depository form | (2) (iii) | Notwithstanding anything contained herein, the Company shall be entitled to dematerialise its shares, debentures and other securities pursuant to the Depositories Act, 1996 and to offer its shares, debentures and other securities for subscription in a dematerialised form. | ||

| (iii) | Notwithstanding anything contained herein, the Company shall be entitled to treat the person whose names appear in the register of members as a holder of any share or whose names appear as beneficial owners of shares in the records of the Depository, as the absolute owner thereof and accordingly shall not (except as ordered by a Court of competent jurisdiction or as required by law) be bound to recognise any benami trust or equity or equitable contingent or other claim to or interest in such share on the part of any other person whether or not it shall have express or implied notice thereof. | |||

| (iii) | Notwithstanding anything contained herein, in the case of transfer of shares or other marketable securities where the Company has not issued any Certificates and where such shares or other marketable securities are being held in | |||

16

| an electronic and fungible form, the provisions of the Depositories Act, 1996 shall apply. Further, the provisions relating to progressive numbering shall not apply to the shares of the Company which have been dematerialised. | ||||

| Issue of new certificate in place of one defaced, lost or destroyed | 28 | If any certificate be worn out, defaced, destroyed or lost or if there be no further space on the back thereof for endorsement of transfer, then upon production thereof to the Board, they, may order the same to be cancelled, and may issue a new certificate in lieu thereof and if any certificate be lost or destroyed then upon proof thereof to the satisfaction of the Board and on such indemnity as the Board deem adequate being given, a new certificate in lieu thereof shall be given to the party entitled to such lost or destroyed certificate. A sum not exceeding Rs. 50/- shall be paid to the Company for every certificate issued under this clause, as the Board may fix from time to time, provided that no fee shall be charged for issue of new certificate in replacement of those which are old, worn, decrepit out or where the cages on the reverse for recording transfers have been fully utilised. | ||

| Board may waive fees | 29 | The Board may waive payment of any fee generally or in any particular case. | ||

| Endorsement on certificate | 30 | Every endorsement upon the certificate of any share in favour of any transferee thereof shall be signed by such person for the time being authorised by the Board in that behalf. | ||

| Board to comply with Rules | 31 | The Board shall comply with requirements prescribed by any Rules made pursuant to the said Act; relating to the issue and execution of share certificates. | ||

17

| VI. CALLS ON SHARES

| ||||||

| Directors may make calls

Calls may be made by installments |

32 | Subject to the provisions of Section 49 of the said Act, the Board may, from time to time, by means of resolution passed at its meetings make such calls as they may think fit upon the members in respect of moneys unpaid on the share held by them respectively and not by the conditions of allotment thereof made payable at fixed times, and each member shall pay the amount of every call so made on him to the persons and at the times and place appointed by the Board. A call may be made payable by installments. | ||||

| Call to date from resolution | 33 | A call shall be deemed to have been made at the time when the resolution of the Board authorising such call was passed and may be made payable by members on a subsequent date to be specified by Directors. | ||||

| Notice of call | 34 | Fourteen day’s notice at least of every call made payable otherwise than on allotment shall be given by the Company in the manner hereinafter provided for the giving of notices specifying the time and place of payment, and the person to whom such call shall be paid. Provided that before the time for payment of such call the Board may by notice given in the manner hereinafter provided revoke the same. The Board may, from time to time at their discretion, extend the time fixed for the payment of any call, and may extend such time as to all or any of the members who, the Board may deem fairly entitled to such extension; but no member shall be entitled to any such extension, except as a matter of grace and favour. | ||||

| Provisions applicable to installments | 35 | If by the terms of issue of any share or otherwise any amount is payable at any fixed time or by installments at fixed times, whether on account of the share or by way of premium, every such | ||||

18

| amount or installments shall be payable as if it were a call duly made by the Board and of which due notice had been given, and all the provisions herein contained in respect of calls shall relate to such amount or installments accordingly. | ||||||

| When interest on call or installment payable | 36 | If the sum payable in respect of any call or such other amount or installments be not paid on or before the day appointed for payment thereof or any extension thereof as aforesaid, the holder for the time being of the share, in respect of which the call shall have been made, or such amount or installment shall be due, shall pay interest for the same, from the day appointed for the payment thereof to the time of actual payment at such rate not exceeding ten per cent per annum, as shall from time to time be fixed by the Board. Nothing in this Article shall however, be deemed to make it compulsory on the Board to demand or recover any such interest, and the payment of such interest, wholly or in part, may be waived by the Board if they think fit so to do. | ||||

| Money due to members from the Company may be applied in payment of call or installment | 37 | Any money due from the Company to a member may, without the consent and notwithstanding the objection of such member, be applied by the Company in or towards the payment of any money due from him to the Company for calls or otherwise. | ||||

| Part payment on account to call etc. not to preclude forfeiture | 38 | Neither a judgement nor a decree in favour of the Company for calls of other moneys due in respect of any shares nor any part-payment or satisfaction thereunder nor the receipt by the Company of a portion of any money which shall from time to time be due from any member to the Company in respect of his shares, either by way of principal or interest, nor any indulgence granted by the Company in respect of payment of any such money, shall preclude the forfeiture of such shares as hereinafter provided. | ||||

19

| Proof on trial on of suit on money on shares | 39 | On the trial or hearing of any action or suit brought by the Company against any member or his legal representatives to recover any moneys claimed to be due to the Company for any call or other sum in respect of his shares, it shall be sufficient to prove that the name of the member in respect of whose shares the money is sought to be recovered, appears entered on the Register of Members as the holder, or one of the holders, at or subsequent to the date at which the money sought to be recovered is alleged to have become due, on the shares in respect of which such money is sought to be recovered, and that the amount claimed is not entered as paid in the books of the Company or the Register of Members and that the resolution making the call is duly recorded in the minute book, and that notice of such call was duly given to the member or his legal representatives sued in pursuance of these presents; and it shall not be necessary to prove the appointment of the Directors who made such call, not that a quorum of Directors was present at the meeting of the Board at which such call was made, nor that the meeting at which such call was made duly convened or constituted, nor any other matter whatsoever, but the proof of the matters aforesaid shall be conclusive evidence of the debts, and the same shall be recovered by the Company against the member or his representatives from whom the same is sought to be recovered unless it shall be proved, on behalf of such member or his representatives against the Company that the name of such member was improperly inserted in the register, or that the money sought to be recovered has actually been paid. | ||||

20

| Payment of unpaid share capital in advance

Interest may be paid thereon

Repayment of such advances

Priority of payment in case of winding up |

40 | (1) | The Board may, if they think fit, subject to the provisions of Section 50 of the Act receive from any member willing to advance the same, either in money or money’s worth the whole or any part of the amount remaining unpaid on the shares held by him beyond the sum actually called up and upon the moneys so paid or satisfied in advance, or so much thereof, as from time to time and at any time thereafter exceeds the amount of the calls then made upon and due respect of the shares on account of which such advances have been made, the Company may pay or allow interest at such rate as the member paying such advance and the Board agree upon; provided always that if at any time after the payment of any such money the rate of interest so agreed to be paid to any such member appears to the Board to be excessive, it shall be lawful for the Board from time to time to repay to such member so much of money as shall then exceed the amount of the calls made upon such shares, unless there be an express agreement to the contrary; and after such repayment such member shall be liable to pay, and such advance had been made, provided also that if at any time after the payment of any money so paid in advance, the Company shall go into liquidation, either voluntary or otherwise, before the full amount of the money so advanced shall have become due by the member to the Company for installments or calls, or any other manner, the member making such advance shall be entitled (as between himself and the other members) to receive back from the Company the full balance of such moneys rightly due to him by the Company in priority to any payment to members on account of capital. | |||

21

| No right to vote | (2) | The member making such advance shall not, however, be entitled to any voting rights in respect of the moneys so advanced by him until the same would, but for such payment, become presently payable. | ||||||

| VII. FORFEITURE OF AND LIEN ON SHARES | ||||||||

| If call or installment not paid notice to be given to member | 41 | If any member fails to pay any money due from him in respect of any call made or amount or installment as provided in Article 35 on or before the day appointed for payment of the same, or any such extension thereof as aforesaid or any interest due on such call or amount or installment or any expenses that may have been incurred thereon, the Directors or any person authorised by them for the purpose may, at any time thereafter, during such time as such money remains unpaid, or a judgement or a decree in respect thereof remains unsatisfied in whole or in part, serve a notice in the manner hereinafter provided for the serving of notices on such member or any of his legal representatives or any of the persons entitled to the share by transmission, requiring payment of the money payable in respect of such share, together with such interest and all expenses (legal or otherwise) incurred by the Company by reason of such non-payment. | ||||||

| Term of notice | 42 | The notice shall name a day (not earlier than the expiration of fourteen days from the date of the notice) and a place or places on or before and at which the money due as aforesaid is to be paid. The notice may also state that in the event of the non-payment of such money at or before the time and the place appointed, the shares in respect of which the same owed will be liable to be forfeited. | ||||||

22

| In default of payment shares may be forfeited | 43 | If the requirements of any such notice as aforesaid are not complied with, every or any share in respect of which the notice is given may, at any time thereafter before payment of all calls or amounts or installments, interest and expenses due in respect thereof, be forfeited by a resolution of the Board to that effect. Such forfeiture shall include all dividends and bonuses declared in respect of the forfeited shares and not actually paid before the forfeiture. | ||||||

| Notice of forfeiture

Entry of forfeiture in register of members |

44 | When any share shall have been so forfeited, notice of the forfeiture shall be given to the member in whose name it stood immediately prior to the forfeiture or to any of his legal representatives, or to any of the persons entitled to the share by transmission and an entry of the forfeiture, with the date thereof, shall forthwith be made in the Register of Members. The provisions of this Article are, however, directory only and no forfeiture shall in any manner be invalidated by any omission or neglect to give such notice or to make such entry as aforesaid. | ||||||

| Forfeited shares to become property of the

Company and may be sold etc. |

45 | Any share so forfeited shall be deemed to be the property of the Company and the Board may sell, re-allot or otherwise dispose of the same, either to the original holder thereof or to any other persons, and either by public auction or by private sale and upon such terms and in such manner as the Directors shall think fit. | ||||||

| Forfeiture may be remitted or annulled | 46 | In the meantime, and until any share so forfeited shall be sold, re-allotted or otherwise dealt with as aforesaid, the forfeiture thereof may at the discretion and by a resolution of the Board, be remitted or annulled as a matter of grace and favour but not as of right, upon such terms and conditions as they think fit. | ||||||

23

| Members still liable to pay money due notwithstanding the forfeiture | 47 | Any member whose shares have been forfeited shall, notwithstanding the forfeiture, remain liable to pay and shall forthwith pay to the Company all calls, amounts, installments, interest expenses owing upon or in respect of such shares at the time of the forfeiture, together with interest thereon, from the time of the forfeiture until payment, at the rates, not exceeding ten percent per annum as the Board may determine, in the same manner in all respects as if the shares had not been forfeited, without any. deduction or allowance for the value of the shares at the time to the forfeiture and the Board may enforce the payment thereof if they think fit (but without being under any obligation so to do) without entitling such member or his representative to any remission of such forfeiture or to any compensation for the same, unless the Directors shall think fit to make such compensation, which they shall have full power to do, in such manner and on such terms on behalf of the Company as they shall think fit. | ||||||

| Effect of forfeiture | 48 | The forfeiture of a share shall involve the extinction of all interest in and of all claims and demands against the Company of the member in respect of the share and ail other right of the member incident to the share except only such of those rights as by these Article are expressly saved. | ||||||

| Surrender of shares | 49 | The Directors may, subject to the provision of the Act, accept a surrender of any share from or by any member desirous of surrendering those on such terms as they think fit. | ||||||

24