Use these links to rapidly review the document

TABLE OF CONTENTS

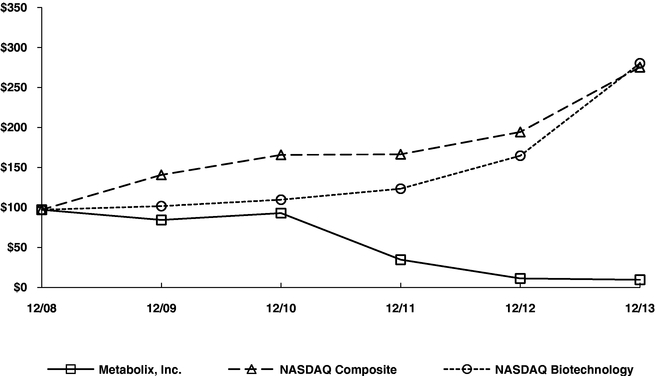

Index to Consolidated Financial Statements

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

ý |

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

|

For the fiscal year ended December 31, 2013; |

||

or |

||

o |

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

|

Commission File Number 001-33133

METABOLIX, INC.

(Exact name of registrant as specified in its charter)

| Delaware (State or other jurisdiction of incorporation or organization) |

04-3158289 (I.R.S. Employer Identification No.) |

|

21 Erie Street Cambridge, MA (Address of principal executive offices) |

02139 (Zip Code) |

(Registrant's telephone number, including area code): (617) 583-1700

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Name of exchange on which registered | |

|---|---|---|

| Common Stock, par value $.01 per share | The NASDAQ Stock Market LLC (NASDAQ Global Market) |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes o No ý

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No ý

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ý No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ý No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (Section 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of "large accelerated filer," "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act:

| Large accelerated filer o | Accelerated filer o | Non-accelerated filer o (Do not check if a smaller reporting company) |

Smaller reporting company ý |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of Act). Yes o No ý

The aggregate market value of the voting and non-voting common equity held by non-affiliates computed by reference to the price at which the common equity was last sold on the NASDAQ Global Market on June 30, 2013 was $34,313,662.

The number of shares outstanding of the registrant's common stock as of March 21, 2014 was 34,889,055.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the Registrant's definitive Proxy Statement to be filed with the Securities and Exchange Commission (the "Commission") pursuant to Regulation 14A in connection with the 2014 Annual Meeting of Stockholders to be held on May 20, 2014 are incorporated herein by reference into Part III of this report.

METABOLIX, INC.

ANNUAL REPORT ON FORM 10-K

For the Year Ended December 31, 2013

2

Forward Looking Statements

This annual report on Form 10-K contains "forward-looking statements" within the meaning of 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. In particular, statements contained in the Form 10-K, including but not limited to, statements regarding our future results of operations and financial position, business strategy and plan prospects, projected revenue or costs and objectives of management for future research, development or operations, are forward-looking statements. These statements relate to our future plans, objectives, expectations and intentions and may be identified by words such as "may," "will," "should," "expects," "plans," "anticipate," "intends," "target," "projects," "contemplates," "believe," "estimates," "predicts," "potential," and "continue," or similar words.

Although we believe that our expectations are based on reasonable assumptions within the limits of our knowledge of our business and operations, the forward-looking statements contained in this document are neither promises nor guarantees. Our business is subject to significant risk and uncertainties and there can be no assurance that our actual results will not differ materially from our expectations. These forward looking statements include, but are not limited to, statements concerning: future financial performance and position, plans and expectations that depend on the Company's ability to continue as a going concern, and management's strategy, plans and objectives for research and development, product development, industry collaborations, manufacturing and commercialization of current and future products, including the commercialization of our biopolymer products. Such forward-looking statements are subject to a number of risks and uncertainties that could cause actual results to differ materially from those anticipated including, without limitation, risks related to our limited cash resources, uncertainty about our ability to secure additional funding, dependence on establishing a manufacturing source for our products, risks related to the development and commercialization of new and uncertain technologies, risks associated with our protection and enforcement of our intellectual property rights, as well as other risks and uncertainties set forth below under the caption "Risk Factors" in Part I, Item 1A, of this report.

The forward-looking statements and risk factors presented in this document are made only as of the date hereof and we do not intend to update any of these risk factors or to publicly announce the results of any revisions to any of our forward-looking statements other than as required under the federal securities laws.

Unless the context otherwise requires, all references in this Annual Report on Form 10-K to "Metabolix," "we," "our," "us," "our company" or "the company" refer to Metabolix, Inc., a Delaware corporation and its subsidiaries.

Metabolix is an innovation-driven bioscience company focused on delivering sustainable solutions to the plastics and chemicals industries. We have core capabilities in microbial genetics, fermentation process engineering, chemical engineering, polymer science, plant genetics and botanical science, and we have assembled these capabilities in a way that has allowed us to integrate our biotechnology research with real world chemical engineering and industrial practice. In addition, we have created an extensive intellectual property portfolio to protect our innovations and, together with our technology, to serve as a valuable foundation for future industry collaborations.

Our targeted markets of plastics and chemicals offer substantial opportunity for innovation and value creation. Our strategy is based on the performance and differentiation of our materials. With proprietary biopolymer formulations we aim to address unmet needs of our customers and leverage the

3

distinctive properties of our PHAs to improve critical product qualities and enable our customers to enhance the value of their products and/or achieve savings through their value chain. As such, we are positioning our biopolymers as advanced specialty materials that offer a broad and attractive range of properties and processing options compared to other bioplastics or performance additives. In addition, we are also leveraging our technology to utilize renewable feedstocks to produce biobased industrial chemicals for high value applications as alternatives to the primary synthetic routes currently deployed by the chemical industry. We believe that a substantial global market opportunity exists to develop and commercialize our technology to produce advanced biopolymer and biobased industrial chemical products.

Metabolix was formed to leverage the ability of natural systems to produce complex biopolymers from renewable resources. We have focused on a family of biopolymers found in nature called polyhydroxyalkanoates ("PHAs"), which occur naturally in living organisms and are chemically similar to polyesters. We have demonstrated the production of PHAs at industrial scale to produce PHA biopolymers and PHA precursors to biobased industrial chemicals. We have also demonstrated the production of polyhydroxybutyrate ("PHB"), a subclass of PHAs, in agriculturally significant non-food crops.

PHA Biopolymers Platform

From 2004 through 2011, we developed and began commercialization of our PHA biopolymers through a technology alliance and subsequent commercial alliance with a wholly-owned subsidiary of Archer Daniels Midland Company ("ADM"), one of the largest agricultural processors in the world. Under the commercial alliance, ADM was responsible for resin manufacturing, and Metabolix was primarily responsible for product development, compounding, marketing and sales. Through this alliance, the companies established a joint venture company, Telles, LLC ("Telles"), to commercialize PHA biopolymer products.

After ADM terminated the Telles joint venture early in 2012, we retained significant rights and assets associated with the PHA biopolymers business, which we used to relaunch the business with a new business model and a restructured biopolymers team that retained core capabilities in technology, manufacturing and marketing. We hold exclusive rights to the Metabolix technology and intellectual property used in the joint venture. We acquired all of Telles's product inventory and compounding raw materials, all product certifications and all product trademarks including MirelTM and MveraTM, and we retained all co-funded pilot plant equipment in locations outside of the ADM commercial manufacturing facility in Clinton, Iowa. Today, we are focused on high value performance biopolymers and are in the process of identifying and securing the manufacturing capability needed to commercialize these products.

During 2012, we took key steps toward implementing the new business model for our PHA biopolymers business. We worked closely with our core customers to supply product from existing inventory as a bridge to new supply. We evaluated the potential applications for our biopolymer products and narrowed our market development focus to certain high value market segments: (i) performance additives, including film and bag applications; and (ii) functional biodegradation. In March 2012, we began directly recording product sales and shipping product from inventory to our customers. During the second half of 2012, we developed, sampled and launched a compostable film grade resin and, a polymeric modifier for polyvinyl chloride ("PVC"). We also established Metabolix GmbH, a subsidiary located in Cologne, Germany, to serve as a focal point for our commercial activities in Europe. This location is intended to enable us to directly access the European market, which is the largest for bioplastics.

During 2013, we continued to use existing biopolymer inventory as well as biobased and biodegradable polymers sourced from third parties to continue developing the market and to supply

4

new and existing customers. In the second half of 2013, we broadened our offering of film resins with the launch of Mvera B5010, a certified compostable resin for film and bag applications, and the launch of Mvera B5011, a certified compostable film resin for film and bag applications requiring transparency. We also launched I6003rp, a new polymeric modifier and processing aid for recycled PVC. Throughout 2013, we worked closely with customers developing applications using our materials.

During 2013 we also engaged in discussions and collaborations with potential customers and suppliers in Asia to expand our relationships there. In July 2013, we formalized a Memorandum of Understanding ("MOU") with Samsung Fine Chemicals, a company based in South Korea with complementary biopolymer products and complementary regional positioning to Metabolix. Under the MOU, we each fund our respective costs separately, but work together with the goal of expanding the global market for biodegradable polymers. Our MOU with Samsung also provides access to additional biodegradable polymers that we can use in resin formulations designed to deliver the best performance and value to targeted customer applications. The MOU is not a binding commitment and may be terminated at any time by either party without liability or obligations to the other party.

In 2014, we plan to increase our efforts in the areas of performance additives based on PHAs. We also expect to build on the performance, biodegradability and biobased content attributes of our PHA biopolymers as we continue to develop biobased and biodegradable resins for film and bag applications and for functional biodegradation applications based on PHAs and other biodegradable materials.

We will also continue to explore alternative options for biopolymer manufacturing with a supply chain properly sized to our business. In 2013, we conducted due diligence on several potential manufacturing sites, and we expect to select a site in 2014. Once our PHA supply chain is fully established, this captive capacity combined with access to additional biobased and biodegradable materials sourced from third parties, will allow us to continue formulating proprietary high-performance solutions for our target segments. However, our present capital resources are not sufficient to fund our planned operations for a twelve month period. We will, during 2014, require significant additional funding to continue our operations. Based on our current plans and projections, which remain subject to numerous uncertainties, we anticipate raising $50-60 million over the next 12-15 months. The timing, structure and vehicles for obtaining this financing are under consideration and it may be accomplished in stages. Although we cannot guarantee the availability of financing, our goal is to use this capital to build an intermediate scale specialty materials business based on PHA additives that serves as the foundation for our longer-range plans and the future growth of our business. Failure to receive additional funding will force us to delay, scale back or otherwise modify our business and manufacturing plans, sales and marketing efforts, research and development activities and other operations, and/or seek strategic alternatives.

Biobased Industrial Chemicals Platform.

For our second platform, we are developing C4 and C3 chemicals from biobased sources, as opposed to the fossil fuels that are used to produce most industrial chemicals today. Our process for creating biobased industrial C4 and C3 chemicals involves engineering metabolic pathways into microbes that, in a fermentation process, produce specific PHA structures that serve as precursors for these chemicals. Through our PHA technology, we are able to control the microbe biology to achieve high concentrations of specific PHAs that accumulate inside cells as they metabolize sugars. This intracellular accumulation of the biopolymers inside the microbes is a unique and differentiating aspect of our technology. When the fermentation is completed, we use a novel internally developed recovery process known as "FAST" (fast-acting, selective thermolysis) that converts the biopolymer directly to the target chemical using heat.

In the C4 program, we have produced biobased gamma butyrolactone ("GBL") at pilot scale and demonstrated a chemical profile that meets or exceeds the existing industrial specifications. In 2012, we

5

completed the preliminary design for a commercial scale plant to enable production of biobased GBL which, through an established conversion process, the biobased GBL can be further converted to biobased butanediol ("BDO"). This plan, which could be implemented under a potential future collaboration, includes specifications for all of the components of our fermentation and recovery process.

We believe that developing and commercializing biobased C3 chemicals could represent another attractive application of our technology. In 2012, after completing an analysis of the global market for acrylic acid, a C3 chemical, we continued scale up of fermentation and optimization of microbial strains to produce biobased C3 chemicals. We also successfully demonstrated recovery of acrylic acid from dried biomass using the "FAST" process in our Cambridge laboratory and provided sample quantities of dried biomass for conversion to biobased acrylic acid for customer evaluation. While significant work remains to be done, particularly around scale-up of the "FAST" process for commercial quantities of biobased acrylic acid, this is another opportunity that could be pursued under a potential future collaboration.

In 2013, we achieved three technical milestones in our biobased chemicals program. We demonstrated a process to efficiently recover ultra-high purity GBL from fermentation broth and showed that our C4 technology can be adapted to produce deuterated bio-GBL. We also demonstrated that our C3 and C4 microbial strains and fermentation processes are suitable for production of biobased chemicals based on second generation feedstocks, or cellulosic sugars.

While we believe that strategic alliances will be required to successfully commercialize C3 and C4 chemicals, there can be no assurance that we will be successful in establishing or maintaining suitable partnerships. We plan to continue seeking such alliances in 2014, with the goal to secure funding from potential partners to continue development of our biobased industrial chemical processes.

Crops Platform.

In our third technology platform, we are harnessing the renewable nature of plants to make renewable chemicals and bioenergy from crops. The focal point of our crop technology efforts is around PHB, the simplest member of the broad PHA family of biopolymers. While applications for PHAs have focused mainly on their use as biodegradable bioplastics, these polymers have a number of other unique features that will allow their use in other applications, such as the production of chemical intermediates and their use as value-added animal feeds. We are working to create proprietary systems to produce PHB in high concentration in the leaves of biomass crops or in the seeds of oilseed crops for these multiple applications. In doing this, we have been developing tools and intellectual property around enhancing the photosynthetic capacity of plants, a core capability for improved crop yield.

Our work in crops highlights our leading edge technical capabilities, and researchers at Metabolix have designed novel, multi-gene expression systems to increase production of PHB in plant tissue. The science behind this shift in metabolism is complex since the goal is to significantly increase production of PHB to be viable at industrial scale without impairing the ability of the plant to thrive in its natural environment. In 2011, Metabolix was awarded a $6 million grant by the U.S. Department of Energy ("DOE") to engineer switchgrass to produce 10 percent PHB, by weight, in the whole plant and to develop methods to thermally convert the PHB-containing biomass to crotonic acid and a higher density residual biomass fraction for production of bioenergy. During 2012 and 2013, Metabolix was awarded additional grants for leading-edge crop research targeting multi-gene expression and transformation of plants including important biofuel and food crops. Funding from these additional grants is expected to total approximately $1.6 million and will run through 2014.

In 2014, we plan to continue to identify additional sources of grant funding while we advance research under our existing grants, focused primarily on increasing PHB production in switchgrass and developing a thermal conversion process to recover crotonic acid. We may also seek to establish

6

alliances with industry partners to commercially exploit this platform and the intellectual property we have gained in our work in this area. However, there can be no assurance that we will be successful in establishing or maintaining suitable partnerships.

Metabolix was formed in 1992 to leverage the ability of natural systems to produce complex polymers from renewable resources and to serve the growing needs of society for inherently biodegradable plastic materials and chemicals that do not deplete finite fossil resources.

Polymers are found in nature in a wide range of organisms including microbes, plants and animals. PHAs also naturally occur within certain organisms, including microbes. These microbes use PHA to store energy and consume it for food when needed. It is this characteristic that gives our PHA biopolymers their inherent biodegradability.

Though PHA polymers are found in nature, their production in wild-type bacterial strains is inefficient and costly for commercial purposes. In 1981, Imperial Chemical Industries ("ICI") developed a controlled fermentation process using a wild-type bacterial strain to produce a PHA copolymer that they introduced under the trade name Biopol. While a handful of applications were developed for Biopol, the cost to produce the polymer using the naturally occurring bacterial strains that were available at the time was prohibitively high and its performance properties were limited. Commercialization was not possible, but the Biopol assets remained largely intact and were eventually sold to Monsanto, Inc.

By the late 1980s, tools for genetic engineering had advanced significantly, and microbes were already being genetically designed to produce various products, such as protein drugs. At the Massachusetts Institute of Technology, Dr. Oliver Peoples, our Chief Scientific Officer, working in the lab of Dr. Anthony Sinskey, a member of our Board of Directors, identified the key genes required for the biosynthesis of our PHA biopolymers and invented and patented the first transgenic systems for their production. The use of genetically engineered production organisms, instead of wild-type strains, broadly expanded the number of compositions that could be made and enabled the tight level of control and high efficiency and productivity that are required for cost-effective industrial manufacturing.

Metabolix was formed to exploit these discoveries. In order to fully capture the opportunity, we acquired Monsanto's patent estate related to biobased plastics, which included the Biopol assets, in 2001. We have since fully developed an integrated manufacturing process using transgenic strains for fermentation and a proprietary recovery process. This integrated manufacturing process is available for use in commercial manufacturing going forward. We have also developed proprietary plastic formulation technology, and are developing a platform technology for co-producing plastics, chemicals and energy in crops such as switchgrass, oilseeds and sugarcane. In addition, we are applying our proprietary technologies to our industrial biobased chemicals platform.

Our Technology and Core Capabilities

We believe we have one of the most advanced capabilities to perform metabolic pathway engineering in the world and that we are skilled in our ability to integrate the biotechnology we develop into large scale industrial production processes. In particular, we believe that we have unique capabilities with respect to harnessing the metabolic pathways involved in the production of a wide range of bioplastic monomers and the ability to polymerize, accumulate and harvest these bioplastics from living cells. We are also developing key capabilities in the areas of biopolymer product development and customer focused technical support.

7

We have demonstrated that our technology and core capabilities enable us to:

- •

- design and engineer living organisms to perform a series of chemical reactions that convert a feedstock to an end product

in a highly efficient and reliable manner;

- •

- integrate those organisms into reliable, large scale industrial fermentation processes;

- •

- develop highly efficient recovery technology to separate the end product from the fermentation broth;

- •

- tailor the properties of our end product from that process to suit customer needs;

- •

- develop new applications and commercial opportunities for these products;

- •

- develop new formulations and compounds based on these products; and

- •

- provide sales and technical support to our customers who use these products.

Biology and Genetic Engineering

We have identified and chromosomally inserted into organisms a series of genes to produce several enzymatic proteins, and have done so in such a way that they are expressed to execute a series of reactions in a balanced manner to produce PHAs as the end-product of interest. This work is at the forefront of a scientific discipline referred to as "Synthetic Biology" which has become the focus of intense research and design activities. There have been many academic and venture-backed entrants in this general field, primarily targeting either advanced cellulosic ethanol or next generation biofuel technologies. We believe that we have advanced capabilities based on over 20 years of development taking early stage gene/pathway discovery through the entire value delivery chain through to implementation of that technology at commercial scale. In addition, we have developed core competencies in plant science, plant transformation and the development of advanced multigene expression technologies for introducing novel, multiple trait synthetic pathways into biomass plant crops.

Industrial Fermentation Process Engineering

We have tightly integrated our fermentation scale-up research capabilities with our genetic engineering capabilities to create a feedback loop where data from fermentation experiments can readily influence microbial design and where microbial engineering approaches can guide the fermentation group to structure the optimal protocols (recipes) for running fermentations. Based on this technology we have demonstrated the ability to produce a range of different biopolymers on a common fermentation platform.

Chemical Process Engineering

Another element of our product development process involves process chemistry and chemical engineering to separate the biopolymer from the biological cell material once fermentation is complete. We have a dedicated team that has developed a proprietary process for recovery of PHA biopolymer, and that process produces PHA biopolymer at a high level of purity without damaging the structure of the polymer and has operated effectively at a commercial scale. We have successfully demonstrated our ability to efficiently isolate the range of polymers necessary to meet and expand our range of target applications. These polymers can be routinely produced free from cell debris and processed into high quality resin pellets.

Our capabilities in fermentation and recovery for producing PHA biopolymers have been successfully translated to the development of biobased industrial chemicals. We have demonstrated

8

fermentation at pilot and industrial scale and recovered GBL using a proprietary thermolysis process in tonnage quantities. When fermentation is completed, our novel recovery process known as "FAST" (fast-acting, selective thermolysis) converts the biopolymers, poly-4-hydroxybutrate ("P4HB") for C4 chemicals and poly-3-hydroxyproprionate ("P3HP") for C3 chemicals, directly to GBL and acrylic acid, respectively. The FAST recovery process is a proprietary, low-cost, energy-efficient approach to recover high-purity biobased chemicals directly from dried or whole fermentation broth. Our FAST process has been demonstrated at both lab and tonnage pilot scale for C4 chemicals, and we have successfully demonstrated recovery of acrylic acid from dried biomass using the FAST process in our Cambridge laboratory. We believe our technology is differentiated and that it allows diversification of feedstock from existing fossil sources to renewable sources on a cost competitive basis. For chemicals, we can tailor products and purity levels to meet customer and market needs.

Polymer Science and Product Development

In the area of biopolymers, our product development process involves tailoring polymer properties and polymer blends to provide the desired end product properties and meet the processing requirements for specific customer applications. Our product development team has considerable expertise in polymer science and to date has developed advanced formulation and processing technology for a wide variety of customer applications and different processing methods. We will continue to work with customers to optimize formulations to conform to their commercial specifications as commercialization of our biopolymers expands.

In sum, we have successfully integrated capabilities in biology, genetics, fermentation process engineering, chemical engineering and polymer science to provide high value biobased and biodegradable plastic solutions to customers. We believe this integrated set of capabilities will be a source of competitive advantage. These same capabilities are being applied to our biobased chemicals and plant crop programs, where we have developed additional opportunities that we plan to advance through industry partnerships and/or government grants.

Our goal is to build a commercially successful specialty biopolymers business, with attractive margins, based on the unique properties of our PHA biopolymers. At the same time, by advancing our biobased chemicals and plant crop programs, we aim to be a leader in discovering, developing and commercializing economically attractive, environmentally sustainable alternatives to petroleum-based chemicals. To achieve this goal, we are building a portfolio of programs that we believe will not only provide an attractive slate of commercial opportunities and create value for our business, but will also generate leading and competitive intellectual property positions in the field. However, our present capital resources are not sufficient to fund our planned operations for a twelve month period. We will, during 2014, require significant additional funding to continue our operations. Based on our current plans and projections, which remain subject to numerous uncertainties, we anticipate raising $50-60 million over the next 12-15 months. The timing, structure and vehicles for obtaining this level of financing are under consideration and may be accomplished in stages. Although we cannot guarantee the availability of financing, our goal is to use this capital to build an intermediate scale specialty materials business based on PHA additives that serves as the foundation for our longer-range plans and the future growth of our business. Failure to receive additional funding will force us to delay, scale back or otherwise modify our business and manufacturing plans, sales and marketing efforts, research and development activities, and other operations, and/or seek strategic alternatives. Key elements of our strategy include:

Creating a Product Portfolio of Proprietary Biopolymers and Biopolymer Formulations—Our strategy is to deliver solutions to customers in specialized market segments that can be served competitively by the distinctive properties of our biopolymers and biopolymer formulations. Our biopolymer products may

9

be biobased or biodegradable, or both, and will be used where their unique physical properties provide a competitive advantage. Through several years of interaction with customers, we have developed biopolymers and biopolymer formulations suitable for a variety of processing methods and applications. We are now focusing on developing biopolymers as performance additives or property modifiers (typically with loading in the range of one to ten percent in the end product application) for existing polymers such as PVC, PVC recyclate and PLA. In these high value applications our PHA technology may enhance processing, properties and performance of PVC and recycled PVC, as well as increase performance of PLA while retaining clarity, biobased properties and compostability of the resulting material. In addition, our technology may allow us to develop new formulations to extend the use of our biopolymers into uses such as latex applications.

Establishing a Supply Chain for PHA Biopolymers—We continue to evaluate a number of commercial scale PHA manufacturing options. This is a key element of the supply chain necessary to support our business strategy. While we evaluate these options, we are having PHAs toll produced at pilot scale to validate improvements in our technology and provide small quantities of our latest high performance PHA biopolymers for applications development with customers. We are also investigating a capital-efficient, intermediate-scale commercial production capability for PHA biopolymers. This approach would complement our commercial strategy, where we are focused on building a presence in key application spaces that are intended to demonstrate sufficient market demand to base-load a low cost, world-scale manufacturing facility for high performance PHA biopolymers.

Sourcing Complementary Biopolymers—Our biopolymers supply chain also includes the sourcing of several biobased or biodegradable polymers that are complementary to PHA, including PBAT, PBS and PLA, from third parties like Samsung and NatureWorks LLC. We use these complementary polymers to develop and market proprietary formulations and compounds for customers who are looking for biobased and/or biodegradable solutions in film, bag and functional biodegradation applications. This approach allows us to leverage the value of our existing inventory of PHA that we acquired from the Telles joint venture, while at the same time broadening our understanding of the unique performance enhancing benefits that can be gained by using PHAs as a performance enhancing additive or modifier in formulations based on other plastics.

Managing Existing Inventory—We expect to work closely with core customers to provide them with access to existing inventory acquired from Telles, as new PHA manufacturing and complementary polymer sourcing and the associated supply chain are established. We will also use some inventory as well as product from our pilot scale toll production to continue product development activities targeted at high value applications for our product.

Market Positioning and Technical Support—We have focused our technical and business development team to support existing customers and to educate and develop the prospective customer base for our biopolymer products. This team is focused on positioning our biopolymers as premium priced, specialty materials that are environmentally attractive alternatives to petroleum-based plastics and lower performance bioplastics. The focus of this effort is to build a pipeline of customers across a range of applications. It is our goal to establish customer relationships that will lead to a committed stream of demand for our biopolymers as we establish the supply chain for new PHA manufacturing.

Continuing Microbial Research and Process Development—We have identified opportunities to improve our PHA production strains and our fermentation and recovery processes. We believe that significant reductions in the operating and capital cost to manufacture our PHA biopolymers can occur as we successfully exploit these opportunities. We believe that our technology is robust and we expect to be able to successfully transfer these improvements to commercial scale production.

Extending Our Technology to Sustainable Production of Biobased Chemicals and Intermediates —We believe that our technology can be applied to produce important biobased commercial chemicals and

10

chemical intermediates through biological conversion of sustainable feedstocks such as sugars. Through our integrated bio-engineered chemicals program, we have conducted research into the development of sustainable solutions for chemicals and intermediates, including widely used C4 and C3 industrial chemicals. Our unique FAST process enables very efficient recovery of targeted molecules based on our PHA technology. We are seeking to establish strategic partnerships or other collaborations to advance these programs commercially.

Advancing Plant Crop Research—We believe that we are pioneering the technical process of introducing multigene traits into plant crops for the production of plastics and chemical intermediates directly in the plant. Our plant crop platform is currently in the research phase, with substantial funding provided by government grants. We are in the process of capturing intellectual property gained in our work in crops and expect to seek strategic partnerships or other collaborations to advance these programs commercially, while we continue work in plant crops under government grants.

Partnering our Programs—As appropriate, we may seek to leverage our technology and establish strategic partnerships with one or more industrial companies that can provide access to resources and infrastructure valuable for commercializing our plant crop and/or industrial chemicals platforms. These partnerships may take the form of large-scale strategic collaborations, or more limited collaborations with partners having complementary strengths, for example in biorefinery or chemical operations or in a relevant market space such as agriculture. We will also continue to seek funding through government grants or other government programs aimed at promoting development of biobased plastics and fuels.

Furthering our Leading and Competitive Intellectual Property Position—We have built a patent estate around our platform technologies and a variety of inventions relevant to the commercialization of PHA biopolymers, biobased chemicals and the production of bioplastics and biobased chemicals in plant crops. We continue to extend this patent estate within our core business as well as around other commercial opportunities in the area of biobased plastics, chemicals and plant crops. We have licensed our technology, and where appropriate, we will continue to license our intellectual property to others as a way to advance our business strategy or capitalize on our technology in fields outside our direct areas of interest.

Our targeted markets of plastics and chemicals offer substantial opportunity for innovation and value creation. These are very large markets facing substantial pressures to reduce energy consumption, greenhouse gas emissions and the overall impact on the environment. The limited long-term availability of fossil fuels and volatile oil prices are driving the demand for more sustainable and renewable alternatives in plastics and chemicals manufacturing.

The Plastics Market

The world's annual consumption of plastic materials has increased from around 5 million tons in the 1950s to nearly 240 million metric tons today and is estimated to be $0.5 trillion in size. Durability and lightweight properties, as well as a range of applications from packaging to engineering-grade automotive materials, continue to drive this exponential growth in the plastics market. However, a majority of plastics are made from fossil feedstocks, including crude oil and natural gas. As a result, plastic pricing is impacted by fluctuations in the cost of fossil feedstocks. A more concerning issue is that these fossil feedstock-based plastics do not biodegrade, instead congesting landfills and polluting the oceans. According to the U.S. Environmental Protection Agency, an estimated 32 million tons of plastic entered the U.S. municipal solid waste stream in 2011. It is estimated that 20-25 percent of landfill weight is plastics. In addition, every year approximately 45,000 tons of plastic waste ends up in the world's oceans.

11

According to the Freedonia Group, global demand for biobased and biodegradable plastics will grow 19 percent annually to 950,000 metric tons in 2017. The Freedonia Group cites consumer preferences for more sustainable materials and improved performance of bioplastic resins and commodity plastics produced from biobased sources as the key factors driving this growth. Market research institute Ceresana predicts that the global bioplastics market will reach revenues of more than $5.8 billion in 2021, reflecting average annual growth rates of 18.9 percent. According to Ceresana, Europe was responsible for one-third of the market in 2013, followed by North America and Asia-Pacific. Strong growth is also predicted for South America as a result of production increases in Brazil. Through 2017, starch-based bioplastics and polylactic acid ("PLA") will account for the majority of bioplastic demand, followed by other biobased plastics, such as PHA/PHB, cellulose, polybutylene succinate ("PBS") and fossil fuel-based biodegradable plastics, representing approximately 40 percent of global bioplastic demand. Ceresana expects non-biodegradable plastics, such as polyethylene, made from renewable feedstocks to increase their market share from the 8 percent seen in 2010 to more than 48 percent of the bioplastics market by 2018.

According to Global Industry Analysts, Inc., the global market for PVC is approximately $70 billion based on an estimated 35 million metric tons produced annually. PVC is a versatile polymer used in a broad range of applications including construction materials, wire and cable, and medical disposables. Significant amounts of additives are added to PVC formulations (typically 20-40% of the formulation) to improve processing, plasticization and performance of PVC. For decades, low molecular weight phthalates have been used as performance additives to plasticize PVC. Research has shown that phthalates can migrate out of PVC over time, creating concerns about exposure to phthalates as well as deterioration in the properties of the PVC as it ages. We believe there is demonstrated market interest in biobased performance additives for PVC that can reduce or eliminate the use of phthalates while maintaining or improving the performance of PVC. According to a study on additives conducted by Freedonia, the total additives market for PVC is approximately 7 million MT per annum. Plasticizers represent approximately 72% of this market. Our market focus is on the property modifier additives segment that represents a market of 700 ktpa (kilo tonnes per annum) or approximately $3.5 billion annually according to the Freedonia study.

According to the German-based research firm nova-Institut, the global production of PLA is currently 180,000 tons per annum and is expected to reach 800,000 tons per annum by 2020.

The Chemicals Market

There are a large number of chemicals products which enable the manufacture of most industrial and consumer goods ranging from automobiles to food packaging. Major chemicals products include building block chemicals, such as ethylene and propylene, and specialty chemicals such as lubricating oil enhancers and pharmaceutical intermediates. The vast majority of chemicals produced today use non-renewable resources such as oil, natural gas or coal as their basic raw material.

Under the umbrella of the global chemicals market are conventional C4 and C3 industrial chemicals, with an estimated market of more than $10 billion annually.

The global C4 chemicals market is estimated at approximately $3 billion. C4 chemical products are used in a wide range of applications including engineering plastics, fabrics and fibers, personal care products and in semiconductor manufacturing. Conventional C4 chemicals are produced almost entirely from fossil-based hydrocarbons such as natural gas, oil or coal.

Global demand for C3 chemicals is estimated at greater than $8 billion per year based on sales of nine billion pounds annually with growth driven by increasing demand in Asia, including China and India. Conventional C3 chemicals, including crude acrylic acid, glacial acrylic acid and acrylates, are used in products such as superabsorbent polymers ("SAPs"), water treatment chemicals, coatings (decorative, automotive, and paper) and adhesives. Markets and Markets, a global market research and

12

consulting company, anticipates the global market for acrylic acid and its derivatives to grow to $14 billion by 2018.

Recent initiatives by the U.S. and European Union are fostering the growth in investment in the development of biobased chemicals. The governments of both the U.S. and the European Union are promoting the research and development of biobased chemicals as sustainable alternatives that reduce waste, create jobs, and drive innovation and growth. In Europe, governmental efforts have been met by private corporations to create the Biobased Industries Private Public Partnership (BBI), a pledge of billions of euros to bring biobased chemicals and fuels from the laboratory to marketplace. The 2014 Farm Bill recently signed into law in the U.S. includes important provisions for the continued growth of the biobased chemicals sector. For the first time, the Farm Bill has been expanded to support biobased chemicals, opening up the potential to fund important advances in sustainable alternatives to petroleum based chemicals. Government investment in these research efforts plays an important role in driving innovations in the development of biobased chemicals and encouraging continued public adoption of biobased and sustainable chemicals in consumer products.

Overview

Metabolix is engaged in product and market development of a biopolymer platform, based on technology developed by Metabolix and early commercialization efforts conducted through the Telles joint venture with ADM. Following the termination of our commercial alliance with ADM early in 2012, we restructured the biopolymers business, retaining a core team in our biopolymers group to provide continuity with technology, manufacturing process and markets. We worked closely with customers during this transition to understand their product needs and to match them to available inventory. In addition, we have held constructive discussions with various potential manufacturing partners for PHA biopolymers and expect to select a site in 2014 for intermediate scale commercial manufacturing. In 2014, in our biopolymers business we also expect to continue with a focused approach to performance additive applications, including high value film and bag applications, and functional biodegradation applications. However, failure to receive additional funding will force us to delay, scale back or otherwise modify our business and manufacturing plans, sales and marketing efforts, research and development activities and other operations, and/or seek strategic alternatives.

Former Alliance with Archer Daniels Midland Company

From 2004 through 2011, we developed and began commercialization of our PHA biopolymers through a technology alliance and subsequent commercial alliance with ADM Polymer Corporation, a wholly-owned subsidiary of ADM, one of the largest agricultural processors in the world. The Commercial Alliance Agreement between Metabolix and ADM Polymer specified the terms and structure of the alliance. The agreement governed the activities and obligations of the parties to commercialize PHA biopolymers, which have been marketed under the brand names Mirel™ and Mvera™. These activities included the establishment of a joint venture company, Telles, to market and sell PHA biopolymers, the construction of a manufacturing facility capable of producing 110 million pounds of material annually (the "Commercial Manufacturing Facility"), the licensing of technology to Telles and to ADM, and the conducting of various research, development, manufacturing, sales and marketing, compounding and administrative services by the parties.

On January 9, 2012, ADM notified us that it was terminating the commercial alliance effective February 8, 2012. ADM had undertaken a strategic review of its business investments and activities and made the decision to focus resources outside of Telles. As the basis for the decision, ADM indicated to us that the projected financial returns from the alliance were too uncertain.

13

Upon termination of the alliance, Metabolix intellectual property licenses to ADM Polymer and Telles ended, with Metabolix retaining all rights to its intellectual property. ADM retained its Commercial Manufacturing Facility located in Clinton, Iowa, previously used to produce PHA biopolymers for Telles.

After termination of the Commercial Alliance Agreement, the parties entered into a settlement agreement in which the parties agreed to specific terms related to the winding up and dissolution of Telles. Under this settlement agreement, we purchased certain assets of the joint venture for $2,982,000 including Telles's entire inventory, exclusive and perpetual rights to all of Telles's trademarks, and all product registrations, certifications and approvals for Telles's PHA biopolymers. We also retained all co-funded equipment previously acquired by Metabolix and situated at locations other than the Clinton, Iowa Commercial Manufacturing Facility.

Current Capabilities and Scope of our Operating Business in Biopolymers

Our biopolymers team has expertise in the key areas required to maintain and grow an operating business, as well as carrying forward the core knowledge of the biopolymer technology, manufacturing process and markets that we developed during our alliance with ADM. We have established a subsidiary located in Cologne, Germany to serve as a focal point for our commercial activities in Europe. We continue to work closely with customers to understand their needs and to match them to available inventory and newly developed products.

We plan to continue to build our supply chain through supply agreements that provide us access to biobased and/or biodegradable biopolymers, supplementing our remaining inventory of PHA material that was acquired from Telles. We are continuing pilot manufacturing of our proprietary PHA materials to develop and validate applications for high value PHAs in target markets of: (i) performance additives, including film and bag applications; and (ii) functional biodegradation. Our aim is to validate high value applications and secure commitments to base-load our commercial manufacturing facilities.

During 2013 we engaged in discussions and collaborations with potential customers and suppliers in Asia to expand our relationships there. In July 2013, we formalized a Memorandum of Understanding ("MOU") with Samsung Fine Chemicals, a company based in South Korea with a significant role in the biopolymers industry. Samsung is pursuing a similar strategy to Metabolix, offering a complementary product slate and complementary regional positioning. Metabolix is focused on the U.S. and Europe while Samsung has a strong market presence in Korea and across Asia. Metabolix has been working with Samsung on biodegradable polymers since early 2012. Under the MOU, we each fund our respective costs separately, but work together with the goal of expanding the global market for biodegradable polymers. Our MOU with Samsung provides access to additional biodegradable polymers that we can use in resin formulations designed to deliver the best performance and value to targeted customer applications. The MOU does not represent a legally binding commitment by either party, and it may be terminated at any time by either party without liability or obligations to the other party.

In 2012 we signed an agreement for demonstration scale production with Antibióticos SA, a toll manufacturer based in León, Spain, and began technology transfer. In 2013, Antibióticos entered a process for financial restructuring. It became apparent that Antibióticos is no longer a viable option for Metabolix due to a lack of progress in their financial restructuring. Therefore, we are no longer considering it as a manufacturing option and have instead shifted our focus to alternative sites.

In 2012 and 2013, we conducted due diligence on several potential PHA biopolymer manufacturing sites and expect to select a manufacturing site in 2014, properly sized to our business. When our PHA supply chain is fully established, this captive capacity will be combined with access to additional biobased and biodegradable materials sourced from third parties, which will allow us to continue formulating proprietary high-performance products for our target market segments.

14

Metabolix Biopolymers Business Strategy

| Customers and Markets | Focus on strategic customers and high value segments as foundation for business—initial areas of emphasis include performance additives, including for film and bags, and functional biodegradation. | |

Manufacturing Scale |

Initially targeting intermediate capacity of several kilotonnes annually, then expand capital investment and capacity according to demand. Ultimately establish one or more world-scale plants of 10-20 ktpa capacity according to demand. |

|

Business Partners |

Engage multiple partners with expertise in relevant application spaces, such as modified PVC, modified PLA, and latex coatings. |

|

Supply Chain |

Toll production of pilot scale quantities of our latest PHA products, together with sourcing of complementary biobased and/or biodegradable polymers for proprietary formulations and compounds. |

|

Technology Base |

Deploy state-of-the-art technology with improved yield and recovery processes. |

|

Value Chain |

Create integrated chain controlled by Metabolix, potentially with chemicals integration. |

Mirel biopolymers were produced successfully at industrial scale for two years under the joint venture with ADM. The product was produced at very high quality and in a targeted range of grades suited to different customer uses. Going forward, we see the potential to deploy our latest technology into industrial production at an initial scale that is matched to developing customer demand with the intention to add capacity in tandem with the growth outlook for our products. We marketed our Mirel and Mvera biopolymers for more than two years on behalf of Telles and gained traction during that time with over 50 customers. Going forward, we plan to focus our marketing and product development activities initially on providing high value material to customers in key application spaces based on the performance, biodegradability and biobased content attributes of our PHA biopolymers in the areas of: (i) performance additives, including film and bag applications, and (ii) functional biodegradation.

The Value Proposition of Metabolix Biopolymers

Our strategy is based on the performance of our materials. With proprietary biopolymer formulations we aim to address unmet needs of our customers and leverage the distinctive properties of our PHAs to improve critical product qualities and enable our customers to enhance the value of their products and/or achieve savings through their value chain.

As such, we are positioning our line of Mirel biopolymers as advanced specialty materials that offer a broad and attractive range of properties and processing options compared to other bioplastics. Our Mirel biopolymers can also be used to deliver biobased content in an end use application, as an additive or modifier to improve performance of other polymers including conventional plastics (e.g. PBAT, PVC) or other bioplastics (e.g., PLA and starch) and to deliver the required biodegradation profile of an end use product.

15

When compared with other performance additives and biodegradable plastics (whether biobased or petroleum based), we believe our Mirel biopolymers can be differentiated and offer unique benefits in end use applications based on the following factors:

Biobased Content—Our Mirel PHA biopolymers products are produced using fermentation which converts industrial sugar (a biobased feedstock) into PHA biopolymer. This biobased composition can be used in neat form, or can be combined with other polymers to make plastic formulations and compounds with targeted amounts of biocontent. This can be a key factor in an end use customer's material selection.

Biodegradability—Mirel biopolymers are available with a range of biodegradation profiles. For example, our PHA biopolymers will biodegrade due to the action of microbial agents in a wide variety of conditions, including home and industrial compost systems, soil, anaerobic environments such as those found in anaerobic digesters and septic systems, and marine and fresh water environments. The rate and extent of biodegradability will depend on the specific ingredients included in the particular Mirel biopolymer formulation, the size and shape of the articles made from our Mirel biopolymers as well as the specific end-of-life environment. However, like all bioplastics and organic matter, Mirel biopolymers are not designed to biodegrade in conventional, non-active landfills. Many plastics marketed as biodegradable only degrade in a controlled municipal industrial compost facility.

Performance Enhancement—Our PHA biopolymers possess a unique chemistry that can be used as an additive or modifier to improve the performance, properties and processing of other polymer materials including PVC, PVC recyclate, and PLA. While biobased content and biodegradability are not the drivers of enhanced performance, they are added benefits for end use applications where improved performance is required and biobased content and/or biodegradability is desired.

Physical Properties—Similar to petroleum-based plastic, Mirel biopolymers possess a particularly broad range of physical properties, varying from hard and stiff to soft and flexible.

Processability—Our biopolymers can be processed in many types of existing conventional polymer conversion processes that are currently being used for petroleum-based plastic.

Upper Service Temperature—Mirel biopolymers will withstand temperatures in excess of 100o C, i.e., the boiling point of water, an important threshold. Some formulations of Mirel biopolymers can withstand temperatures up to 130o C.

Resistance to Hydrolysis—While Mirel biopolymers will biodegrade in marine and fresh water environments through natural processes mediated by microbes, they are resistant to chemical hydrolysis with cold or hot water over the intended life span of the product. This is an important distinction with many other biodegradable polymers where the primary mechanism is hydrolysis followed by further microbial degradation of the residues.

Product Form—Our PHA biopolymers can be produced in pellet form (for further processing by customers), in densified form or as a blend with other biobased and/or biodegradable materials. We may also provide our biopolymers in other forms as may be determined by our customers.

Biobased and Biodegradability Certification

Mirel biopolymers in neat form have the advantage in the marketplace of being both biobased and biodegradable while having comparable functional properties to petroleum-based polymers. However, because there is sometimes confusion about the use of the terms "biobased" and "biodegradable" in the marketplace, we conform to following industry guidelines when making these claims.

16

We certify our biopolymer resin products individually based on their specific composition and formulation. We sell certain Mirel biopolymers that have received the Vinçotte certifications of "OK Biodegradability Soil" for natural soil biodegradability, "OK Biodegradability Water" for fresh water biodegradability, "OK Compost" for compostability in an industrial composting unit, and "OK Compost Home" for compostability in home composting systems. Vinçotte is the recognized European authority on materials inspection, certification, assessments and technical training. We believe that Mirel biopolymers are the only non-starch bioplastics to gain all four Vinçotte certifications. In addition to the Vinçotte certifications, certain Mirel biopolymers have been certified compostable by the Biodegradable Products Institute ("BPI"), an independent North American certifier of compostable material. BPI certification shows that Mirel biopolymers comply with the specifications established in the American Society for Testing and Materials standard ASTM D6400 for composting in a professionally managed composting facility. Our Mvera biopolymers are designed to be compostable and some have received the Vinçotte certification of "OK Compost" and/or the BPI certification for compostability in an industrial composting unit.

Regulatory Requirements

Some applications for which Mirel biopolymers may be suitable, such as food packaging, plastic-coated paper cups and lids for disposable cups, involve food contact, which, in the United States, is regulated by the U.S. Food and Drug Administration ("FDA"). The FDA process for food contact requires the submittal of a dossier, which is made up of a number of extraction studies conducted under specific guidelines.

Certain Mirel biopolymers, including Mirel F1005, F1006 and F3002, have been cleared for use in non-alcoholic food contact applications. The conditions of use range from frozen food storage to boiling water up to 100°C, including microwave reheating. These products are suitable for a wide range of food service and packaging applications including paper coatings, bags, cups, trays, squeeze bottles and injection molded parts like caps, closures and disposable items such as forks, spoons, knives, tubs, trays and hot cup lids. The clearance also includes products such as housewares, cosmetics and medical packaging.

Trends and Opportunities for Metabolix Biopolymers

Branded Products

The market for branded products and services with attributes of environmental responsibility and sustainability is an emerging business opportunity. We expect that by co-branding products that use Mirel and Mvera, Metabolix and its customers will be able to jointly promote environmental responsibility. We believe that producers are positioning products as environmentally responsible or superior to gain a competitive advantage as they believe consumer preferences are shifting. We believe the use of Mirel in branded products either directly or for packaging will facilitate and enhance our customers' efforts to exploit this trend.

Regulated Markets

Regulatory action, such as bans, taxes, subsidies, mandates and initiatives, to encourage substitution of renewable and sustainable materials for petroleum-based incumbents is increasing. It is notable that there are bans on single-use plastic bags being mandated in areas around the world. In the geographies where regulatory drivers exist, we expect that Metabolix biopolymers can meet requirements for biobased content or biodegradability and create a driver for the use of our biopolymers over conventional petroleum-based plastics. In addition, producers are now anticipating regulatory change and are initiating programs to introduce sustainable materials to their products prior to or in an attempt to forestall implementation of such regulation. We believe that as awareness of

17

practical and affordable biobased and biodegradable alternative grows, the pace of regulatory change may accelerate.

Market Segments for Metabolix Biopolymers

Although there are significant opportunities across many market segments, we are initially focusing on key application spaces based on the performance, biodegradability and biobased content attributes of our PHA biopolymers in the areas of: (i) performance additives, including film and bag applications, and (ii) functional biodegradation. These markets have the strongest need for materials that are biobased and biodegradable either for branding value, because of regulatory requirements or because biodegradability offers a useful property such as new end-of-life solutions like composting or anaerobic digestion. In addition, our biopolymers impart improved performance qualities when used as an additive and blended with other polymers including PVC and PLA. To approach these market segments, we expect to conduct certain focused product and market development activities, including working with potential customers to determine their specific needs, and we have begun the process of qualifying our material for certain customer applications. As new inventory becomes available, we expect that these activities will accelerate.

The performance profile of our biopolymer products is closely matched to the needs of the following market segments:

Performance Additives

We are developing PHA biopolymers as performance additives. Metabolix biopolymer resins are either miscible or highly compatible as a dispersed modifier with a broad range of biobased and petroleum-based materials and can improve a range of performance attributes such as impact strength, heat resistance, barrier properties, processability and plasticization through blending with these materials. We are initially focused on developing polymeric modifiers for PVC, a polymer with a diverse use pattern ranging from construction materials to medical applications and an estimated global demand of approximately 35 million metric tons per year. In PVC, a compounded product is typically formulated with about 20-40% performance additives used to improve the processability and performance of PVC products.

We are developing biobased polymeric modifiers for semi-rigid and flexible PVC compounds. We have shown that our polymeric modifiers can provide toughness, plasticization and permanence in addition to enhancing processing when added to PVC. We have also shown that our bioplastic polymeric modifiers have the potential to improve PVC toughness beyond that achievable with leading polymeric modifiers and at the same time serve as a non-migrating, non-phthalate high molecular weight plasticizer. We are now working with customers to identify suitable applications for the technology that may allow us to broaden the addressable market opportunity for our materials, beyond our traditional focus on those markets requiring biodegradation.

In 2012 we sampled and launched I6001, a polymeric modifier for PVC, and in 2013 we developed and launched I6003rp, a new polymeric modifier for recycled PVC, and worked with customers to identify suitable applications for this product where it can be used to upgrade the physical properties, processing, and value of PVC recyclates. In 2013, we also continued to develop polymeric modifiers based on our PHA technology suitable for enhancing the performance of targeted polymers. Future applications include toughening and enhanced ductility of polylactic acid (PLA) where the ability to address the inherent brittleness of this material could significantly expand the potential applications that can be served. We have shown that we can produce new PHA rubber modifiers that can improve the performance of PLA while retaining the clarity, biobased properties and compostability of the resulting material. We believe that Metabolix has the potential to develop a family of polymeric property modifiers that have improved functionality compared to current fossil derived materials while

18

also being biobased and biodegradable. In 2014, we expect to work with prospective customers to continue developing data supporting their applications of interest using PVC and PLA.

Film and Bag Applications

The compostable bag market is growing as brand owners and retailers are motivated by regulatory and consumer demand. Compostable bags are the single largest application use for compostable materials. The driver for this market is the ongoing need to reduce and eliminate organics (food scraps and yard waste) from municipal waste streams and landfills. Applications such as single-use retail bags, industrial can liners, kitchen compost bags and organic lawn and leaf bags have a strong need for the industrial compostability offered by our Mvera biopolymer products. In 2012, we developed and launched a certified film grade resin intended for use in bag and film applications where industrial composting is the desired final route of disposal. In 2013, we expanded our portfolio of products with the development and launch of two new compostable film grade resins, Mvera B5010 and Mvera B5011, a resin for producing transparent film and bags. We plan to continue to develop additional Mvera products suited to the needs of the marketplace for film and bag applications. Our innovative Mirel rubber modifiers also have the potential to expand the application space for PLA which may lead to new business opportunities. Their capability to modify and improve PLA demonstrates performance that is comparable to traditional non-renewable rubber modifiers without compromising the renewable nature of PLA or key features of clarity and compostability.

Functional Biodegradation

Our biopolymers are unique biobased materials for applications requiring functional biodegradation. Since PHAs are produced naturally in living organisms such as microbes, our PHA biopolymers can be biodegraded by similar microbes present in ambient environments such as soil and water. Our biopolymers can also be formulated or compounded with other biodegradable biopolymers to provide customers with new product performance and biodegradation profiles.

Soil compostable films and parts in horticulture and agriculture—The soil biodegradability profile of PHA makes our products uniquely suited for resin products with horticultural and agricultural uses. Applications such as plant pots, vine clips, sod netting and agricultural film have a strong need for the soil biodegradability functionality offered by certain of our Mirel biopolymer resin grades. In these applications, the natural biodegradation process for Mirel biopolymers in the soil can provide a sustainable alternative to conventional plastics and save costs related to labor and disposal of conventional plastics.

Marine and aquatic degradable films and parts—The biobased composition combined with marine degradation properties of Mirel biopolymers are unmatched in the industry. Mirel biopolymer resins degrade in the marine environment due to microbial activity. Metabolix has worked on several projects with government agencies and universities to validate the use of Mirel biopolymers in shoreline applications.

Studies have noted that the world's oceans show increasing levels of persistent plastic particles of a size ingestible by marine creatures at the bottom of the food chain. Larger plastic items are also accumulating in substantial quantities in certain parts of the ocean, and marine birds and mammals have been found dead from ingesting or getting tangled in plastic debris. Mirel biopolymers allow brand owners the opportunity to offer a product that will biodegrade if inadvertently released into the environment or in applications where in-situ marine degradation is a key attribute (e.g., erosion control).

Water treatment—Metabolix has worked with customers to develop pond water and aquarium water treatment systems based on the biodegradation and microbial activity of our biopolymers.

19

Latex coatings—A unique form of our PHA biopolymers may be used as a biobased and biodegradable coating for paper and cardboard. If development of this product is successful, it has the potential for applications such as repulpable coated corrugated cardboard.

Additional applications—Metabolix has worked with customers on a variety of additional applications where biodegradation of the polymer is a performance requirement.

Industry Landscape

The plastics market is large, with many established players. The market has grown around the chemical processing of oil and natural gas, and is concentrated in the conventional, non-biodegradable petroleum-based segment.

Established companies in this segment include Dow Chemical, DuPont, BASF, Ineos, LyondellBasell, SABIC and Mitsubishi Chemical, among many others. The price of conventional petroleum-based plastic is volatile, as it is dependent on petroleum as a key manufacturing input. In addition, the non-biodegradability of conventional petroleum-based plastics makes them persistent in and harmful to the environment and creates significant waste.

A few companies, such as DuPont, DSM, Arkema and Braskem, have taken steps toward plastics based on renewable resources and are commercializing conventional plastics that use building blocks derived from renewable resources as components. However, these products are generally not biodegradable. Other producers of petroleum-based plastics, including BASF and Samsung, now produce certain petrochemical grades that are biodegradable in industrial compost environments, but are otherwise persistent in the environment and are still subject to the volatility of oil and natural gas prices.

Our most comparable competitors are in the biodegradable, renewable resource based plastic segment, within which there are three distinct technologies: PHA, PLA and starch-based biodegradables. Just as a wide variety of different petroleum-based plastics now serve the needs of the market; we believe that these three product classes are more complementary than competitive. We believe that of these three product classes, Mirel biopolymers offer a broad range of properties and processing options, and will address a large proportion of opportunities as an environmentally attractive yet functionally equivalent alternative to conventional petroleum-based plastics. Unlike PLA and most starch-based biodegradables, Mirel biopolymers can:

- •

- biodegrade in natural soil and water environments, including the marine environment;

- •

- biodegrade in industrial or home composts;

- •

- remain functional in a wide range of temperature settings; and

- •

- not break down in everyday use.

Companies active in the PHA plastics segment include Kaneka, Tianan, Tianjin Green Biomaterials, EcoMann, Meredian, and a minor producer in Brazil. The key players in PLA and starch-based biodegradable plastics include NatureWorks, Mitsui Chemical, Teijin, Novamont and Biome. Our PHA biopolymers can be blended with many of these materials to improve their performance and other characteristics. In addition, there are companies that compound blends of various materials, including bioplastics.

20

Summarized below is an overview of the industry landscape for conventional, biobased and biodegradable polymers.

Biodegradability

|

Based on Petroleum | Based on Renewable Resources | ||

|---|---|---|---|---|

| Biodegradable | Synthetic Biodegradable: BASF (EcoflexTM, EcovioTM) Dupont (BiomaxTM) ShowaDenko (BionolleTM) Mitsubishi Chemical (GS Pla) Samsung (PBAT, PBS) Zhejiang Hisun (PBAT) |

PHA: Metabolix Kaneka (PHBH) Tianan (PHBV) Tianjin (SoGreenTM) EcoMann (EM) Meredian (Nodax PHA) |

||

PLA: NatureWorks (IngeoTM) Mitsui Chemical (LaceaTM) Starch-based: Novamont (Mater-BiTM) Biome |

||||

Non-biodegradable |

Conventional petroleum-based plastics |

Dupont (SoronaTM (~30% biobased) Dow Chemical (Soybean Polyurethanes) Arkema (Nylon 11) Braskem (polyethylene) |

Biobased Industrial Chemicals Platform

The combined global market for conventional C4 and C3 industrial chemicals is estimated at more than $10 billion annually. These fundamental building block industrial chemicals have application to a broad range of industrial and consumer products. We view this market as attractive both commercially and technologically for the development and deployment of our PHA fermentation and FAST recovery technologies. We believe our technology can be used to produce these chemicals from renewable feedstocks cost effectively as high value, biobased replacements in the industry supply chain for conventional chemicals produced with oil priced at or above $90 per barrel.

Our objective is to develop and commercialize biobased industrial chemicals starting with C4 and then C3 through partnerships with industry leaders. Our business strategy is to form strategic alliances where our partners contribute fermentation and manufacturing capabilities, access to market channels in the value chain and related assets, and Metabolix contributes intellectual property, proprietary technology and process engineering capabilities to enable commercialization of a new source of supply for competitive, cost-effective biobased industrial chemicals targeted to high value applications to meet rising global market demand.

In our biobased industrial chemicals platform, our C4 program is most advanced in development toward commercialization. We have developed our proprietary fermentation and FAST recovery processes to produce biobased gamma-butyrolactone ("GBL") at industrial scale. Through an established synthetic route, our biobased GBL can be converted to biobased butanediol ("BDO"), the workhorse of the C4 industry value chain that enables access to broad segments of the market.

We have also demonstrated that our technology is directly applicable to the manufacture of biobased acrylic acid, the primary industrial chemical in the C3 industry value chain. We have focused initially on engineering production strains for fermentation and validating our FAST recovery process for production of biobased acrylic acid.

21

Market for C4 and C3 Industrial Chemicals