UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

_______________________________

FORM 10-Q

QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | ||||||||

For the quarterly period ended | ||||||||

OR | ||||||||

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | ||||||||

For the transition period | from ________ to ________ | |||||||

Commission file number: 001-38855

___________________________________

(Exact name of registrant as specified in its charter)

| (State or Other Jurisdiction of Incorporation or Organization) | (I.R.S. Employer Identification No.) | ||||||||||

| (Address of Principal Executive Offices) | (Zip Code) | ||||||||||

Registrant’s telephone number, including area code: +1 212 401 8700

| No Changes | |||||||||||

| (Former name, former address and former fiscal year, if changed since last report) | |||||||||||

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||||||||||||

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| ☒ | Accelerated filer | ☐ | |||||||||

| Non-accelerated filer | ☐ | Smaller reporting company | |||||||||

| Emerging growth company | |||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

Indicate the number of shares outstanding of each of the issuer’s classes of common stock, as of the latest practicable date.

| Class | Outstanding at July 25, 2023 | ||||||||||

| Common Stock, $0.01 par value per share | shares | ||||||||||

Nasdaq, Inc.

Page | ||||||||

Part I. FINANCIAL INFORMATION | ||||||||

| Item 1. | ||||||||

| Item 2. | ||||||||

| Item 3. | ||||||||

| Item 4. | ||||||||

Part II. OTHER INFORMATION | ||||||||

| Item 1. | ||||||||

| Item 1A. | ||||||||

| Item 2. | ||||||||

| Item 3. | ||||||||

| Item 4. | ||||||||

| Item 5. | ||||||||

| Item 6. | ||||||||

i

About this Form 10-Q

Throughout this Form 10-Q, unless otherwise specified:

•“Nasdaq,” “we,” “us” and “our” refer to Nasdaq, Inc.

•“Nasdaq Baltic” refers to collectively, Nasdaq Tallinn AS, Nasdaq Riga, AS, and AB Nasdaq Vilnius.

•“Nasdaq BX” refers to the cash equity exchange operated by Nasdaq BX, Inc.

•“Nasdaq BX Options” refers to the options exchange operated by Nasdaq BX, Inc.

•“Nasdaq Clearing” refers to the clearing operations conducted by Nasdaq Clearing AB.

•“Nasdaq CXC” and “Nasdaq CX2” refer to the Canadian cash equity trading books operated by Nasdaq CXC Limited.

•“Nasdaq First North” refers to our alternative marketplaces for smaller companies and growth companies in the Nordic and Baltic regions.

•“Nasdaq GEMX” refers to the options exchange operated by Nasdaq GEMX, LLC.

•“Nasdaq ISE” refers to the options exchange operated by Nasdaq ISE, LLC.

•“Nasdaq MRX” refers to the options exchange operated by Nasdaq MRX, LLC.

•“Nasdaq Nordic” refers to collectively, Nasdaq Clearing AB, Nasdaq Stockholm AB, Nasdaq Copenhagen A/S, Nasdaq Helsinki Ltd, and Nasdaq Iceland hf.

•“Nasdaq PHLX” refers to the options exchange operated by Nasdaq PHLX LLC.

•“Nasdaq PSX” refers to the cash equity exchange operated by Nasdaq PHLX LLC.

•“The Nasdaq Options Market” refers to the options exchange operated by The Nasdaq Stock Market LLC.

•“The Nasdaq Stock Market” refers to the cash equity exchange and listing venue operated by The Nasdaq Stock Market LLC.

Nasdaq also provides as a tool for the reader the following list of abbreviations and acronyms that are used throughout this Quarterly Report on Form 10-Q.

2020 Credit Facility: $1.25 billion senior unsecured revolving credit facility, which was amended and restated by the 2022 Revolving Credit Agreement

2022 Revolving Credit Agreement: $1.25 billion senior unsecured revolving credit facility, which matures on December 16, 2027

2025 Notes: $500 million aggregate principal amount of 5.650% senior unsecured notes due June 28, 2025

2026 Notes: $500 million aggregate principal amount of 3.850% senior unsecured notes due June 30, 2026

2028 Notes: $1 billion aggregate principal amount of 5.350% senior unsecured notes due June 28, 2028

2029 Notes: €600 million aggregate principal amount of 1.75% senior unsecured notes due March 28, 2029

2030 Notes: €600 million aggregate principal amount of 0.875% senior unsecured notes due February 13, 2030

2031 Notes: $650 million aggregate principal amount of 1.650% senior unsecured notes due January 15, 2031

2032 Notes: €750 million aggregate principal amount of 4.500% senior unsecured notes due February 15, 2032

2033 Notes: €615 million aggregate principal amount of 0.900% senior unsecured notes due July 30, 2033

2034 Notes: $1.25 billion aggregate principal amount of 5.550% senior unsecured notes due February 15, 2034

2040 Notes: $650 million aggregate principal amount of 2.500% senior unsecured notes due December 21, 2040

2050 Notes: $500 million aggregate principal amount of 3.250% senior unsecured notes due April 28, 2050

2052 Notes: $550 million aggregate principal amount of 3.950% senior unsecured notes due March 7, 2052

2053 Notes: $750 million aggregate principal amount of 5.950% senior unsecured notes due August 15, 2053

2063 Notes: $750 million aggregate principal amount of 6.100% senior unsecured notes due June 28, 2063

ARR: Annualized Recurring Revenue

ASR: Accelerated Share Repurchase

AUM: Assets Under Management

CCP: Central Counterparty

CFTC: Commodity Futures Trading Commission

Equity Plan: Nasdaq Equity Incentive Plan

ESG: Environmental, Social and Governance

EMIR: European Market Infrastructure Regulation

ESPP: Nasdaq Employee Stock Purchase Plan

ETF: Exchange Traded Fund

ETP: Exchange Traded Product

Exchange Act: Securities Exchange Act of 1934, as amended

FINRA: Financial Industry Regulatory Authority

IPO: Initial Public Offering

NSCC: National Securities Clearing Corporation

OCC: The Options Clearing Corporation

OTC: Over-the-Counter

ii

PSU: Performance Share Unit

SaaS: Software as a Service

SEC: U.S. Securities and Exchange Commission

SERP: Supplemental Executive Retirement Plan

SFSA: Swedish Financial Supervisory Authority

SOFR: Secured Overnight Financing Rate

S&P: Standard & Poor’s

S&P 500: S&P 500 Stock Index

SPAC: Special Purpose Acquisition Company

TSR: Total Shareholder Return

U.S. GAAP: U.S. Generally Accepted Accounting Principles

U.S. Tape plans: U.S. cash equity and U.S. options industry data

NASDAQ, the NASDAQ logos, and other brand, service or product names or marks referred to in this report are trademarks or service marks, registered or otherwise, of Nasdaq, Inc. and/or its subsidiaries. FINRA and Trade Reporting Facility are registered trademarks of FINRA.

This Quarterly Report on Form 10-Q includes market share and industry data that we obtained from industry publications and surveys, reports of governmental agencies and internal company surveys. Industry publications and surveys generally state that the information they contain has been

obtained from sources believed to be reliable, but we cannot assure you that this information is accurate or complete. We have not independently verified any of the data from third-party sources nor have we ascertained the underlying economic assumptions relied upon therein. Statements as to our market position are based on the most currently available market data. For market comparison purposes, The Nasdaq Stock Market data in this Quarterly Report on Form 10-Q for IPOs is based on data generated internally by us; therefore, the data may not be comparable to other publicly-available IPO data. Data in this Quarterly Report on Form 10-Q for new listings of equity securities on The Nasdaq Stock Market is based on data generated internally by us, which includes issuers that switched from other listing venues, closed-end funds and ETPs. Data in this Quarterly Report on Form 10-Q for IPOs and new listings of equity securities on the Nasdaq Nordic and Nasdaq Baltic exchanges and Nasdaq First North also is based on data generated internally by us. IPOs and new listings data is presented as of period end. While we are not aware of any misstatements regarding industry data presented herein, our estimates involve risks and uncertainties and are subject to change based on various factors. We refer you to the "Risk Factors" section in our Form 10-K for the fiscal year ended December 31, 2022 that was filed with the SEC on February 23, 2023.

Nasdaq intends to use its website, ir.nasdaq.com, as a means for disclosing material non-public information and for complying with SEC Regulation FD and other disclosure obligations.

iii

Forward-Looking Statements

The SEC encourages companies to disclose forward-looking information so that investors can better understand a company’s future prospects and make informed investment decisions. This Quarterly Report on Form 10-Q contains these types of statements. Words such as “may,” “will,” “could,” “should,” “anticipates,” “envisions,” “estimates,” “expects,” “projects,” “intends,” “plans,” “believes” and words or terms of similar substance used in connection with any discussion of future expectations as to industry and regulatory developments or business initiatives and strategies, future operating results or financial performance, and other future developments are intended to identify forward-looking statements. These include, among others, statements relating to:

•our strategic direction, including changes to our corporate structure;

•the integration of acquired businesses, including accounting decisions relating thereto;

•the scope, nature or impact of acquisitions, divestitures, investments, joint ventures or other transactional activities;

•the effective dates for, and expected benefits of, ongoing initiatives, including transactional activities and other strategic, restructuring, technology, ESG, de-leveraging and capital return initiatives;

•our products and services;

•the impact of pricing changes;

•tax matters;

•the cost and availability of liquidity and capital; and

•any litigation, or any regulatory or government investigation or action, to which we are or could become a party or which may affect us and any potential settlements of litigation, regulatory or governmental investigations or actions, including with respect to our CFTC investigation.

Forward-looking statements involve risks and uncertainties. Factors that could cause actual results to differ materially from those contemplated by the forward-looking statements include, among others, the following:

•our operating results may be lower than expected;

•our ability to successfully integrate acquired businesses or divest sold businesses or assets, including the fact that any integration or transition may be more difficult, time consuming or costly than expected, and we may be unable to realize synergies from business combinations, acquisitions, divestitures or other transactional activities;

•loss of significant trading and clearing volumes or values, fees, market share, listed companies, market data customers or other customers;

•our ability to develop and grow our non-trading businesses, including our technology, analytics, ESG and anti-financial crime offerings;

•our ability to keep up with rapid technological advances and adequately address cybersecurity risks;

•economic, political and market conditions and fluctuations, including inflation, interest rate and foreign currency risk inherent in U.S. and international operations, and geopolitical instability;

•the performance and reliability of our technology and technology of third parties on which we rely;

•any significant systems failures or errors in our operational processes;

•our ability to continue to generate cash and manage our indebtedness; and

•adverse changes that may occur in the litigation or regulatory areas, or in the securities markets generally, or increased regulatory oversight domestically or internationally.

Most of these factors are difficult to predict accurately and are generally beyond our control. You should consider the uncertainty and any risk related to forward-looking statements that we make. These risk factors are more fully described in the "Risk Factors" section in our Form 10-K filed with the SEC on February 23, 2023. You are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date of this report. You should carefully read this entire Quarterly Report on Form 10-Q, including “Part I. Item 2. Management’s Discussion and Analysis of Financial Condition and Results of Operations” and the condensed consolidated financial statements and the related notes. Except as required by the federal securities laws, we undertake no obligation to update any forward-looking statement, release publicly any revisions to any forward-looking statements or report the occurrence of unanticipated events. For any forward-looking statements contained in any document, we claim the protection of the safe harbor for forward-looking statements contained in the Private Securities Litigation Reform Act of 1995.

iv

PART I - FINANCIAL INFORMATION

Item 1. Financial Statements

Nasdaq, Inc.

Condensed Consolidated Balance Sheets

(in millions, except share and par value amounts)

| June 30, 2023 | December 31, 2022 | ||||||||||

| (unaudited) | |||||||||||

| Assets | |||||||||||

| Current assets: | |||||||||||

| Cash and cash equivalents | $ | $ | |||||||||

| Restricted cash and cash equivalents | |||||||||||

Default funds and margin deposits (including restricted cash and cash equivalents of $ | |||||||||||

| Financial investments | |||||||||||

| Receivables, net | |||||||||||

| Other current assets | |||||||||||

| Total current assets | |||||||||||

| Property and equipment, net | |||||||||||

| Goodwill | |||||||||||

| Intangible assets, net | |||||||||||

| Operating lease assets | |||||||||||

| Other non-current assets | |||||||||||

| Total assets | $ | $ | |||||||||

| Liabilities | |||||||||||

| Current liabilities: | |||||||||||

| Accounts payable and accrued expenses | $ | $ | |||||||||

| Section 31 fees payable to SEC | |||||||||||

| Accrued personnel costs | |||||||||||

| Deferred revenue | |||||||||||

| Other current liabilities | |||||||||||

| Default funds and margin deposits | |||||||||||

| Short-term debt | |||||||||||

| Total current liabilities | |||||||||||

| Long-term debt | |||||||||||

| Deferred tax liabilities, net | |||||||||||

| Operating lease liabilities | |||||||||||

| Other non-current liabilities | |||||||||||

| Total liabilities | |||||||||||

| Commitments and contingencies | |||||||||||

| Equity | |||||||||||

| Nasdaq stockholders’ equity: | |||||||||||

Common stock, $ | |||||||||||

| Additional paid-in capital | |||||||||||

Common stock in treasury, at cost: | ( | ( | |||||||||

| Accumulated other comprehensive loss | ( | ( | |||||||||

| Retained earnings | |||||||||||

| Total Nasdaq stockholders’ equity | |||||||||||

| Noncontrolling interests | |||||||||||

| Total equity | |||||||||||

| Total liabilities and equity | $ | $ | |||||||||

See accompanying notes to condensed consolidated financial statements.

1

Nasdaq, Inc.

Condensed Consolidated Statements of Income

(unaudited)

(in millions, except per share amounts)

| Three Months Ended June 30, | Six Months Ended June 30, | ||||||||||||||||||||||

| 2023 | 2022 | 2023 | 2022 | ||||||||||||||||||||

| Revenues: | |||||||||||||||||||||||

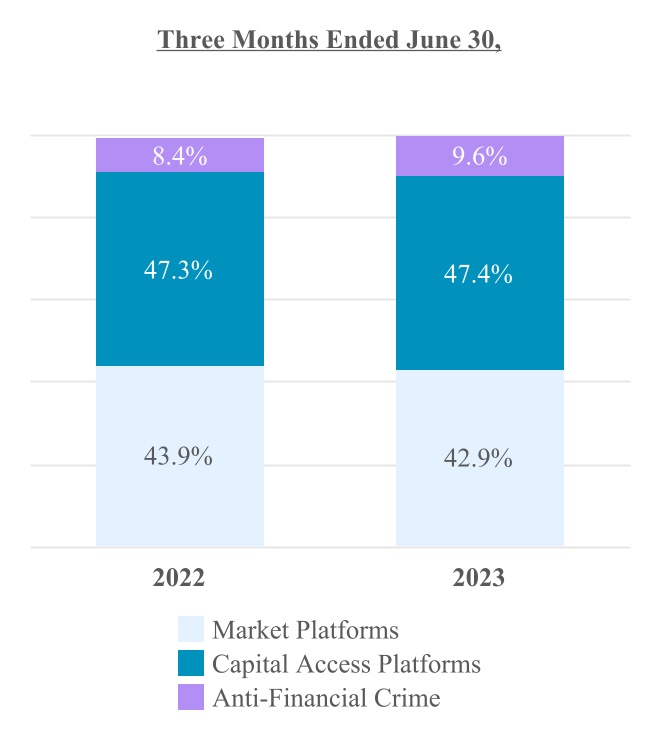

| Market Platforms | $ | $ | $ | $ | |||||||||||||||||||

| Capital Access Platforms | |||||||||||||||||||||||

| Anti-Financial Crime | |||||||||||||||||||||||

| Other revenues | |||||||||||||||||||||||

| Total revenues | |||||||||||||||||||||||

| Transaction-based expenses: | |||||||||||||||||||||||

| Transaction rebates | ( | ( | ( | ( | |||||||||||||||||||

| Brokerage, clearance and exchange fees | ( | ( | ( | ( | |||||||||||||||||||

| Revenues less transaction-based expenses | |||||||||||||||||||||||

| Operating expenses: | |||||||||||||||||||||||

| Compensation and benefits | |||||||||||||||||||||||

| Professional and contract services | |||||||||||||||||||||||

| Computer operations and data communications | |||||||||||||||||||||||

| Occupancy | |||||||||||||||||||||||

| General, administrative and other | |||||||||||||||||||||||

| Marketing and advertising | |||||||||||||||||||||||

| Depreciation and amortization | |||||||||||||||||||||||

| Regulatory | |||||||||||||||||||||||

| Merger and strategic initiatives | |||||||||||||||||||||||

| Restructuring charges | |||||||||||||||||||||||

| Total operating expenses | |||||||||||||||||||||||

| Operating income | |||||||||||||||||||||||

| Interest income | |||||||||||||||||||||||

| Interest expense | ( | ( | ( | ( | |||||||||||||||||||

| Other income (loss) | ( | ( | |||||||||||||||||||||

| Net income (loss) from unconsolidated investees | ( | ||||||||||||||||||||||

| Income before income taxes | |||||||||||||||||||||||

| Income tax provision | |||||||||||||||||||||||

| Net income | |||||||||||||||||||||||

| Net loss attributable to noncontrolling interests | |||||||||||||||||||||||

| Net income attributable to Nasdaq | $ | $ | $ | $ | |||||||||||||||||||

| Per share information: | |||||||||||||||||||||||

| Basic earnings per share | $ | $ | $ | $ | |||||||||||||||||||

| Diluted earnings per share | $ | $ | $ | $ | |||||||||||||||||||

| Cash dividends declared per common share | $ | $ | $ | $ | |||||||||||||||||||

See accompanying notes to condensed consolidated financial statements.

2

Nasdaq, Inc.

Condensed Consolidated Statements of Comprehensive Income

(unaudited)

(in millions)

| Three Months Ended June 30, | Six Months Ended June 30, | ||||||||||||||||||||||

| 2023 | 2022 | 2023 | 2022 | ||||||||||||||||||||

| Net income | $ | $ | $ | $ | |||||||||||||||||||

| Other comprehensive loss: | |||||||||||||||||||||||

| Foreign currency translation losses | ( | ( | ( | ( | |||||||||||||||||||

Income tax benefit (expense)(1) | ( | ( | |||||||||||||||||||||

| Foreign currency translation, net | ( | ( | ( | ( | |||||||||||||||||||

| Comprehensive income | |||||||||||||||||||||||

| Comprehensive loss attributable to noncontrolling interests | |||||||||||||||||||||||

| Comprehensive income attributable to Nasdaq | $ | $ | $ | $ | |||||||||||||||||||

____________

(1) Primarily relates to the tax effect of unrealized gains and losses on Euro denominated notes.

See accompanying notes to condensed consolidated financial statements.

3

Nasdaq, Inc.

Condensed Consolidated Statements of Changes in Stockholders' Equity

(unaudited)

(in millions)

| Three Months Ended June 30, | Six Months Ended June 30, | ||||||||||||||||||||||||||||||||||||||||||||||

| 2023 | 2022 | 2023 | 2022 | ||||||||||||||||||||||||||||||||||||||||||||

| Shares | $ | Shares | $ | Shares | $ | Shares | $ | ||||||||||||||||||||||||||||||||||||||||

| Common stock | |||||||||||||||||||||||||||||||||||||||||||||||

| Additional paid-in capital | |||||||||||||||||||||||||||||||||||||||||||||||

| Beginning balance | |||||||||||||||||||||||||||||||||||||||||||||||

| Share repurchase program | — | — | ( | ( | ( | ( | ( | ( | |||||||||||||||||||||||||||||||||||||||

ASR agreement | — | — | — | — | — | — | ( | ( | |||||||||||||||||||||||||||||||||||||||

| Share-based compensation | |||||||||||||||||||||||||||||||||||||||||||||||

| Other issuances of common stock, net | — | — | — | — | |||||||||||||||||||||||||||||||||||||||||||

| Ending balance | |||||||||||||||||||||||||||||||||||||||||||||||

| Common stock in treasury, at cost | |||||||||||||||||||||||||||||||||||||||||||||||

| Beginning balance | ( | ( | ( | ( | |||||||||||||||||||||||||||||||||||||||||||

| Other employee stock activity | ( | ( | — | ( | ( | ( | ( | ( | |||||||||||||||||||||||||||||||||||||||

| Ending balance | ( | ( | ( | ( | |||||||||||||||||||||||||||||||||||||||||||

| Accumulated other comprehensive loss | |||||||||||||||||||||||||||||||||||||||||||||||

| Beginning balance | ( | ( | ( | ( | |||||||||||||||||||||||||||||||||||||||||||

| Other comprehensive loss | ( | ( | ( | ( | |||||||||||||||||||||||||||||||||||||||||||

| Ending balance | ( | ( | ( | ( | |||||||||||||||||||||||||||||||||||||||||||

| Retained earnings | |||||||||||||||||||||||||||||||||||||||||||||||

| Beginning balance | |||||||||||||||||||||||||||||||||||||||||||||||

| Net income attributable to Nasdaq | |||||||||||||||||||||||||||||||||||||||||||||||

| Cash dividends declared per common share | ( | ( | ( | ( | |||||||||||||||||||||||||||||||||||||||||||

| Ending balance | |||||||||||||||||||||||||||||||||||||||||||||||

| Total Nasdaq stockholders’ equity | |||||||||||||||||||||||||||||||||||||||||||||||

| Noncontrolling interests | |||||||||||||||||||||||||||||||||||||||||||||||

| Beginning balance | |||||||||||||||||||||||||||||||||||||||||||||||

Net activity related to noncontrolling interests | — | — | ( | ( | |||||||||||||||||||||||||||||||||||||||||||

| Ending balance | |||||||||||||||||||||||||||||||||||||||||||||||

| Total Equity | $ | $ | $ | $ | |||||||||||||||||||||||||||||||||||||||||||

See accompanying notes to condensed consolidated financial statements.

4

Nasdaq, Inc.

Condensed Consolidated Statements of Cash Flows

(unaudited)

(in millions)

| Six Months Ended June 30, | |||||||||||

| 2023 | 2022 | ||||||||||

| Cash flows from operating activities: | |||||||||||

| Net income | $ | $ | |||||||||

| Adjustments to reconcile net income to net cash provided by operating activities: | |||||||||||

| Depreciation and amortization | |||||||||||

| Share-based compensation | |||||||||||

| Deferred income taxes | |||||||||||

| Extinguishment of debt and bridge fees | |||||||||||

| Non-cash restructuring charges | |||||||||||

| Net income from unconsolidated investees | ( | ( | |||||||||

| Operating lease asset impairments | |||||||||||

| Other reconciling items included in net income | |||||||||||

| Net change in operating assets and liabilities, net of effects of acquisitions: | |||||||||||

| Receivables, net | ( | ||||||||||

| Other assets | |||||||||||

| Accounts payable and accrued expenses | |||||||||||

| Section 31 fees payable to SEC | ( | ||||||||||

| Accrued personnel costs | ( | ( | |||||||||

| Deferred revenue | |||||||||||

| Other liabilities | ( | ( | |||||||||

| Net cash provided by operating activities | |||||||||||

| Cash flows from investing activities: | |||||||||||

| Purchases of securities | ( | ( | |||||||||

| Proceeds from sales and redemptions of securities | |||||||||||

| Acquisition of businesses, net of cash and cash equivalents acquired | ( | ||||||||||

| Purchases of property and equipment | ( | ( | |||||||||

Investments related to default funds and margin deposits, net(1) | ( | ( | |||||||||

| Other investing activities | |||||||||||

| Net cash used in investing activities | ( | ( | |||||||||

| Cash flows from financing activities: | |||||||||||

| Repayments of commercial paper, net | ( | ( | |||||||||

| Repayments of debt and credit commitment | ( | ||||||||||

| Payment of debt extinguishment cost and bridge fees | ( | ( | |||||||||

| Proceeds from issuances of debt, net of issuance costs | |||||||||||

| Repurchases of common stock | ( | ( | |||||||||

| ASR agreement | ( | ||||||||||

| Dividends paid | ( | ( | |||||||||

| Proceeds received from employee stock activity and other issuances | |||||||||||

| Payments related to employee shares withheld for taxes | ( | ( | |||||||||

| Default funds and margin deposits | |||||||||||

| Other financing activities | ( | ||||||||||

| Net cash provided by financing activities | |||||||||||

| Effect of exchange rate changes on cash and cash equivalents and restricted cash and cash equivalents | ( | ( | |||||||||

| Net increase in cash and cash equivalents and restricted cash and cash equivalents | |||||||||||

Cash and cash equivalents, restricted cash and cash equivalents at beginning of period | |||||||||||

| Cash and cash equivalents, restricted cash and cash equivalents at end of period | $ | $ | |||||||||

| Reconciliation of Cash, Cash Equivalents and Restricted Cash and Cash Equivalents | |||||||||||

| Cash and cash equivalents | $ | $ | |||||||||

| Restricted cash and cash equivalents | |||||||||||

| Restricted cash and cash equivalents (default funds and margin deposits) | |||||||||||

| Total | $ | $ | |||||||||

| Supplemental Disclosure Cash Flow Information | |||||||||||

| Interest paid | $ | $ | |||||||||

| Income taxes paid, net of refund | $ | $ | |||||||||

(1) Includes purchases and proceeds from sales and redemptions related to the default funds and margin deposits of our clearing operations. For further information, see "Default Fund Contributions and Margin Deposits," within Note 14, "Clearing Operations."

See accompanying notes to condensed consolidated financial statements.

5

Nasdaq, Inc.

Notes to Condensed Consolidated Financial Statements

(Unaudited)

1. ORGANIZATION AND NATURE OF OPERATIONS

Nasdaq is a global technology company serving corporate clients, investment managers, banks, brokers, and exchange operators as they navigate and interact with the global capital markets and the broader financial system. We aspire to deliver world-leading platforms that improve the liquidity, transparency, and integrity of the global economy. Our diverse offering of data, analytics, software, exchange capabilities, and client-centric services enables clients to optimize and execute their business vision with confidence.

In September 2022, we announced a new organizational structure which aligns our businesses more closely with the foundational shifts that are driving the evolution of the global financial system. In order to amplify our strategy, we aligned the Company more closely with evolving client needs. As a result, our four previous business segments, Market Technology, Investment Intelligence, Corporate Platforms and Market Services, have been changed to align with our new corporate structure that now includes three business segments: Capital Access Platforms, Market Platforms, and Anti-Financial Crime.

Market Platforms

Our Market Platforms segment includes our Trading Services and Marketplace Technology businesses. Our Trading Services business primarily includes revenues from equity derivatives trading, cash equity trading, Nordic fixed income trading & clearing, Nordic commodities and U.S. Tape plans data. We operate multiple exchanges and other marketplace facilities across several asset classes, including derivatives, commodities, cash equity, debt, structured products and ETPs. In addition, in certain countries where we operate exchanges, we also provide clearing, settlement and central depository services. In June 2023, we entered into an agreement to sell our European energy trading and clearing business, subject to regulatory approval. Beginning in the third quarter of 2023, we will reflect revenues from this business in Other Revenues in the Condensed Consolidated Statements of Income for all periods, and in our Corporate segment for our segment disclosures.

Our transaction-based platforms provide market participants with the ability to access, process, display and integrate orders and quotes. The platforms allow the routing and execution of buy and sell orders as well as the reporting of transactions, providing fee-based revenues.

Our Trading Services business also includes our carbon removal offering through Puro.earth, a Finnish-based leading carbon crediting platform, in which Nasdaq holds a majority stake.

Our Marketplace Technology business includes our trade management services and our market technology businesses.

Trade management services provides market participants with a wide variety of alternatives for connecting to and accessing our markets for a fee. Our marketplaces may be accessed via a number of different protocols used for quoting, order entry, trade reporting and connectivity to various data feeds. We also provide colocation services to market participants, whereby we offer firms cabinet space and power to house their own equipment and servers within our data centers. Additionally, we offer a number of wireless connectivity offerings between select data centers using millimeter wave and microwave technology. In June 2022, we completed the wind-down of our Nordic broker services business.

Our market technology business is a leading global technology solutions provider and partner to exchanges, clearing organizations, central securities depositories, regulators, banks, brokers, buy-side firms and corporate businesses. Our solutions are utilized by leading markets in the U.S., Europe and Asia as well as emerging markets in the Middle East, Latin America, and Africa.

Capital Access Platforms

Our Capital Access Platforms segment includes our Data & Listing Services, Index and Workflow & Insights businesses.

Our Data business sells and distributes historical and real-time market data to the sell-side, the institutional investing community, retail online brokers, proprietary trading firms and other venues, as well as internet portals and data distributors. Our data products can enhance transparency of market activity within our exchanges and provide critical information to professional and non-professional investors globally. Additionally, our Nasdaq Cloud Data Service provides a flexible and efficient method of delivery for real-time exchange data and other financial information.

Our Listing Services business operates in the U.S. and Europe on a variety of listing platforms around the world to provide multiple global capital raising solutions for public companies. Our main listing markets are The Nasdaq Stock Market and the Nasdaq Nordic and Nasdaq Baltic exchanges. Through Nasdaq First North, our Nordic and Baltic operations also offer alternative marketplaces for smaller companies and growth companies.

As of June 30, 2023, there were 4,106 total listings on The Nasdaq Stock Market, including 547 ETPs. The combined market capitalization was approximately $24.6 trillion. In Europe, the Nasdaq Nordic and Nasdaq Baltic exchanges, together with Nasdaq First North, were home to 1,249 listed companies with a combined market capitalization of approximately $1.9 trillion.

6

Our Index business develops and licenses Nasdaq-branded indexes and financial products. We also license cash-settled options, futures and options on futures on our indexes. As of June 30, 2023, 386 ETPs listed on 26 exchanges in over 20 countries tracked a Nasdaq index and accounted for $418 billion in AUM.

Workflow & Insights includes our analytics and corporate solutions businesses. Our analytics business provides asset managers, investment consultants and institutional asset owners with information and analytics to make data-driven investment decisions, deploy their resources more productively, and provide liquidity solutions for private funds. Through our eVestment and Solovis solutions, we provide a suite of cloud-based solutions that help institutional investors and consultants conduct pre-investment due diligence, and monitor their portfolios post-investment. The eVestment platform also enables asset managers to efficiently distribute information about their firms and funds to asset owners and consultants worldwide.

Through our Solovis platform, endowments, foundations, pensions and family offices transform how they collect and aggregate investment data, analyze portfolio performance, model and predict future outcomes, and share meaningful portfolio insights with key stakeholders. The Nasdaq Fund Network and Nasdaq Data Link are additional platforms in our suite of investment data analytics offerings and data management tools.

Our corporate solutions business includes our Investor Relations Intelligence, ESG Solutions and Governance Solutions products, which serve both public and private companies and organizations. Our public company clients can be companies listed on our exchanges or other U.S. and global exchanges. Our private company clients include a diverse group of organizations ranging from family-owned companies, government organizations, law firms, privately held entities, and various non-profit organizations to hospitals and healthcare systems. We help organizations enhance their ability to understand and expand their global shareholder base, improve corporate governance, and navigate the evolving ESG landscape through our suite of advanced technology, analytics, reporting and consulting services. In June 2022, we acquired Metrio, a provider of ESG data collection, analytics and reporting services based in Montreal, Canada. We are integrating Metrio’s SaaS platform into our suite of ESG solutions.

Anti-Financial Crime

Our Anti-Financial Crime segment provides cloud-based anti-financial crime management solutions to help financial institutions detect, investigate, and report money laundering and financial fraud. This segment also includes Nasdaq Trade Surveillance, a SaaS solution designed for brokers and other market participants to assist them in complying with market rules, regulations and internal market surveillance policies, as well as Nasdaq Market Surveillance, a market surveillance solution for markets and regulators.

2. BASIS OF PRESENTATION AND PRINCIPLES OF CONSOLIDATION

The accompanying condensed consolidated financial statements reflect all adjustments which are, in the opinion of management, necessary for a fair statement of the results. These adjustments are of a normal recurring nature. All significant intercompany accounts and transactions have been eliminated in consolidation.

As permitted under U.S. GAAP, certain footnotes or other financial information can be condensed or omitted in the interim condensed consolidated financial statements. The information included in this Quarterly Report on Form 10-Q should be read in conjunction with the consolidated financial statements and accompanying notes included in Nasdaq’s Form 10-K. The year-end condensed balance sheet data was derived from the audited financial statements, but does not include all disclosures required by U.S. GAAP.

Accounting Estimates

In preparing our condensed consolidated financial statements, we make assumptions, judgments and estimates that can have a significant impact on our revenue, operating income and net income, as well as on the value of certain assets and liabilities in our Condensed Consolidated Balance Sheets. At least quarterly, we evaluate our assumptions, judgments and estimates, and make changes as deemed necessary.

Stock Split Effected in the Form of a Stock Dividend

On August 26, 2022, we effected a 3 -for-1 stock split of the Company's common stock in the form of a stock dividend to shareholders of record as of August 12, 2022. The par value per share of our common stock remains $0.01 per share. All references made with respect to a number of shares or per share amounts throughout this Quarterly Report on Form 10-Q have been retroactively adjusted to reflect the stock split.

7

3. REVENUE FROM CONTRACTS WITH CUSTOMERS

Disaggregation of Revenue

The following tables summarize the disaggregation of revenue by major product and service and by segment for the three and six months ended June 30, 2023 and 2022:

| Three Months Ended June 30, | |||||||||||

| 2023 | 2022 | ||||||||||

| (in millions) | |||||||||||

| Market Platforms | |||||||||||

| Trading Services, net | $ | $ | |||||||||

| Marketplace Technology | |||||||||||

| Capital Access Platforms | |||||||||||

| Data & Listing Services | |||||||||||

| Index | |||||||||||

| Workflow & Insights | |||||||||||

| Anti-Financial Crime | |||||||||||

| Other revenues | |||||||||||

| Revenues less transaction-based expenses | $ | $ | |||||||||

| Six Months Ended June 30, | |||||||||||

| 2023 | 2022 | ||||||||||

| (in millions) | |||||||||||

| Market Platforms | |||||||||||

| Trading Services, net | $ | $ | |||||||||

| Marketplace Technology | |||||||||||

| Capital Access Platforms | |||||||||||

| Data & Listing Services | |||||||||||

| Index | |||||||||||

| Workflow & Insights | |||||||||||

| Anti-Financial Crime | |||||||||||

| Other revenues | |||||||||||

| Revenues less transaction-based expenses | $ | $ | |||||||||

Substantially all revenues from the Capital Access Platforms and Anti-Financial Crime segments as well as our Marketplace Technology business were recognized over time for the three and six months ended June 30, 2023 and 2022. For the three and six months ended June 30, 2023 and 2022 approximately 92.9 93.8 7.1 6.2

Contract Balances

Substantially all of our revenues are considered to be revenues from contracts with customers. The related accounts receivable balances are recorded in our Condensed Consolidated Balance Sheets as receivables, which are net of allowance for doubtful accounts of $12 million as of June 30, 2023 and $15 million as of December 31, 2022. There were no material upward or downward adjustments to the allowance during the six months ended June 30, 2023. We do not have obligations for warranties, returns or refunds to customers.

For the majority of our contracts with customers, except for our market technology and listing services contracts, our performance obligations range from three months to three years and there is no significant variable consideration.

Deferred revenue is the only significant contract asset or liability as of June 30, 2023. Deferred revenue represents consideration received that is yet to be recognized as revenue for unsatisfied performance obligations. Deferred revenue primarily represents our contract liabilities related to our fees for Annual and Initial Listings, Workflow & Insights, Market Technology and Anti-Financial Crime contracts. See Note 7, “Deferred Revenue,” for our discussion on deferred revenue balances, activity, and expected timing of recognition.

We do not have a material amount of revenue recognized from performance obligations that were satisfied in prior periods. We do not provide disclosures about transaction price allocated to unsatisfied performance obligations if contract durations are less than one year. For our initial listings, the transaction price allocated to remaining performance obligations is included in deferred revenue. For our Market Technology, Anti-Financial Crime, and Workflow & Insights contracts, the portion of transaction price allocated to unsatisfied performance obligations is presented in the table below. To the extent consideration has been received, unsatisfied performance obligations would be included in the table below as well as deferred revenue.

The following table summarizes the amount of the transaction price allocated to performance obligations that are unsatisfied, for contract durations greater than one year, as of June 30, 2023:

| Market Technology | Anti-Financial Crime | Workflow & Insights | Total | ||||||||||||||||||||

| (in millions) | |||||||||||||||||||||||

| Remainder of 2023 | $ | $ | $ | $ | |||||||||||||||||||

| 2024 | |||||||||||||||||||||||

| 2025 | |||||||||||||||||||||||

| 2026 | |||||||||||||||||||||||

| 2027 | |||||||||||||||||||||||

| 2028+ | |||||||||||||||||||||||

| Total | $ | $ | $ | $ | |||||||||||||||||||

8

4. ACQUISITIONS

2023 Announced Acquisition

In June 2023, we entered into a definitive agreement to acquire Adenza Holdings, Inc., or Adenza, a provider of mission-critical risk management and regulatory software to the financial services industry, for $10.5 billion, comprised of $5.75 billion in cash and a fixed amount of 85.6 million shares of Nasdaq common stock, based on the volume-weighted average price per share over 15 consecutive trading days prior to signing. Nasdaq issued $5.0 billion of debt and entered into a $600 million term loan and will use the proceeds for the cash portion of the consideration. See “Financing of the Adenza Transaction” and “Acquisition Term Loan Agreement” of Note 8, “Debt Obligations,” for further discussion.

At the closing of the transaction, Nasdaq will issue the shares to Thoma Bravo, the sole shareholder of Adenza. These shares will represent approximately 14.9 % of the outstanding shares of Nasdaq as of the date of the merger agreement. As previously announced, at the closing of the transaction, Nasdaq and Thoma Bravo will enter into a stockholders' agreement providing for certain post-closing governance arrangements with respect to the Nasdaq shares to be received by Thoma Bravo in the transaction. For further discussion on the rights of common stockholders refer to “Common Stock” of Note 11, “Nasdaq Stockholders' Equity.” The closing of this transaction is subject to regulatory approvals and other customary closing conditions.

2022 Acquisition

In June 2022, we acquired Metrio, a provider of ESG data collection, analytics and reporting services based in Montreal, Canada. We are integrating Metrio’s SaaS platform into our suite of ESG solutions. Metrio is part of our Workflow & Insights business in our Capital Access Platforms segment.

Pro Forma Results and Acquisition-Related Costs

The condensed consolidated financial statements for the six months ended June 30, 2023 include the financial results of the 2022 acquisition from the date of the acquisition. Pro forma financial results have not been presented since this acquisition was not material to our financial results.

Acquisition-related costs for the transactions described above were expensed as incurred and are included in merger and strategic initiatives expense in the Condensed Consolidated Statements of Income. For the three and six months ended June 30, 2023 these costs primarily related to our planned acquisition of Adenza and mainly included fees for the transaction bridge financing, which was subsequently terminated, consulting and legal fees. Subject to the closing of the Adenza acquisition we expect to incur customary costs related to transaction advisors which will be included in merger and strategic initiatives expense in the Condensed Consolidated Statements of Income.

5. GOODWILL AND ACQUIRED INTANGIBLE ASSETS

Goodwill

The following table presents the changes in goodwill by business segment during the six months ended June 30, 2023:

| (in millions) | |||||

| Market Platforms | |||||

| Balance at December 31, 2022 | $ | ||||

| Foreign currency translation adjustments | ( | ||||

| Balance at June 30, 2023 | $ | ||||

| Capital Access Platforms | |||||

| Balance at December 31, 2022 | $ | ||||

| Foreign currency translation adjustments | ( | ||||

| Balance at June 30, 2023 | $ | ||||

| Anti-Financial Crime | |||||

| Balance at December 31, 2022 | $ | ||||

| Foreign currency translation adjustments | ( | ||||

| Balance at June 30, 2023 | $ | ||||

| Total | |||||

| Balance at December 31, 2022 | $ | ||||

| Foreign currency translation adjustments | ( | ||||

| Balance at June 30, 2023 | $ | ||||

Goodwill represents the excess of purchase price over the value assigned to the net assets, including identifiable intangible assets, of a business acquired. Goodwill is allocated to our reporting units based on the assignment of the fair values of each reporting unit of the acquired company. We test goodwill for impairment at the reporting unit level annually, or in interim periods if certain events occur indicating that the carrying amount may be impaired, such as changes in the business climate, poor indicators of operating performance or the sale or disposition of a significant portion of a reporting unit. There was no

9

Acquired Intangible Assets

The following table presents details of our total acquired intangible assets, both finite- and indefinite-lived:

| June 30, 2023 | December 31, 2022 | ||||||||||

| Finite-Lived Intangible Assets | (in millions) | ||||||||||

| Gross Amount | |||||||||||

| Technology | $ | $ | |||||||||

| Customer relationships | |||||||||||

| Trade names and other | |||||||||||

| Foreign currency translation adjustment | ( | ( | |||||||||

| Total gross amount | $ | $ | |||||||||

| Accumulated Amortization | |||||||||||

| Technology | $ | ( | $ | ( | |||||||

| Customer relationships | ( | ( | |||||||||

| Trade names and other | ( | ( | |||||||||

| Foreign currency translation adjustment | |||||||||||

| Total accumulated amortization | $ | ( | $ | ( | |||||||

| Net Amount | |||||||||||

| Technology | $ | $ | |||||||||

| Customer relationships | |||||||||||

| Trade names and other | |||||||||||

| Foreign currency translation adjustment | ( | ( | |||||||||

| Total finite-lived intangible assets | $ | $ | |||||||||

| Indefinite-Lived Intangible Assets | |||||||||||

| Exchange and clearing registrations | $ | $ | |||||||||

| Trade names | |||||||||||

| Licenses | |||||||||||

| Foreign currency translation adjustment | ( | ( | |||||||||

| Total indefinite-lived intangible assets | $ | $ | |||||||||

| Total intangible assets, net | $ | $ | |||||||||

There was no

The following table presents our amortization expense for acquired finite-lived intangible assets:

| Three Months Ended June 30, | |||||||||||

| 2023 | 2022 | ||||||||||

| (in millions) | |||||||||||

| Amortization expense | $ | $ | |||||||||

| Six Months Ended June 30, | |||||||||||

| 2023 | 2022 | ||||||||||

| (in millions) | |||||||||||

| Amortization expense | $ | $ | |||||||||

The table below presents the estimated future amortization expense (excluding the impact of foreign currency translation adjustments of $89 million as of June 30, 2023) of acquired finite-lived intangible assets as of June 30, 2023:

| (in millions) | |||||

| Remainder of 2023 | $ | ||||

| 2024 | |||||

| 2025 | |||||

| 2026 | |||||

| 2027 | |||||

| 2028+ | |||||

| Total | $ | ||||

6. INVESTMENTS

| June 30, 2023 | December 31, 2022 | ||||||||||

| (in millions) | |||||||||||

Financial investments | $ | $ | |||||||||

| Equity method investments | |||||||||||

| Equity securities | |||||||||||

Financial Investments

Financial investments are comprised of trading securities, primarily highly rated European government debt securities, of which $156 million as of June 30, 2023 and $161 million as of December 31, 2022 are assets primarily utilized to meet regulatory capital requirements, mainly for our clearing operations at Nasdaq Clearing.

Equity Method Investments

We record our estimated pro-rata share of earnings or losses each reporting period and record any dividends as a reduction in the investment balance. As of June 30, 2023 and 2022, our equity method investments primarily included our 40.0

The carrying amounts of our equity method investments are included in other non-current assets in the Condensed Consolidated Balance Sheets. No

10

Net income (loss) recognized from our equity interest in the earnings and losses of these equity method investments, primarily OCC and Nasdaq Private Market, LLC or NPM, was $(11 ) million and $9 million for the three months ended June 30, 2023 and 2022, respectively, and $3 million and $15 million for the six months ended June 30, 2023 and 2022, respectively.

Equity Securities

The carrying amounts of our equity securities are included in other non-current assets in the Condensed Consolidated Balance Sheets. We elected the measurement alternative for substantially all of our equity securities as they do not have a readily determinable fair value. No material adjustments were made to the carrying value of our equity securities for the three and six months ended June 30, 2023 and 2022. As of June 30, 2023 and December 31, 2022, our equity securities primarily represent various strategic investments made through our corporate venture program.

7. DEFERRED REVENUE

Deferred revenue represents consideration received that is yet to be recognized as revenue. The changes in our deferred revenue during the six months ended June 30, 2023 are reflected in the following table:

Balance at December 31, 2022 | Additions | Revenue Recognized | Adjustments | Balance at June 30, 2023 | |||||||||||||

| (in millions) | |||||||||||||||||

| Market Platforms: | |||||||||||||||||

| Market Technology | $ | $ | $ | ( | $ | ( | $ | ||||||||||

| Capital Access Platforms: | |||||||||||||||||

| Initial Listings | ( | ||||||||||||||||

| Annual Listings | ( | ( | |||||||||||||||

| Workflow & Insights | ( | ||||||||||||||||

| Anti-Financial Crime | ( | ||||||||||||||||

| Other | ( | ||||||||||||||||

| Total | $ | $ | $ | ( | $ | ( | $ | ||||||||||

In the above table:

•Additions primarily reflect deferred revenue billed in the current period, net of recognition.

•Revenue recognized includes revenue recognized during the current period that was included in the beginning balance.

•Adjustments reflect foreign currency translation adjustments.

As of June 30, 2023, we estimate that our deferred revenue will be recognized in the following years:

Fiscal year ended: | 2023 | 2024 | 2025 | 2026 | 2027 | 2028+ | Total | ||||||||||||||||

| (in millions) | |||||||||||||||||||||||

| Market Platforms: | |||||||||||||||||||||||

| Market Technology | $ | $ | $ | $ | $ | $ | $ | ||||||||||||||||

| Capital Access Platforms: | |||||||||||||||||||||||

| Initial Listings | |||||||||||||||||||||||

| Annual Listings | |||||||||||||||||||||||

| Workflow & Insights | |||||||||||||||||||||||

| Anti-Financial Crime | |||||||||||||||||||||||

| Other | |||||||||||||||||||||||

| Total | $ | $ | $ | $ | $ | $ | $ | ||||||||||||||||

In the above table, the amounts shown under the column for 2023 represent the remaining six months of 2023.

11

8. DEBT OBLIGATIONS

The following table presents the carrying amounts of our debt outstanding, net of unamortized debt issuance costs:

| June 30, 2023 | December 31, 2022 | ||||||||||

| (in millions) | |||||||||||

| Short-term debt: | |||||||||||

| Commercial paper | $ | $ | |||||||||

| Long-term debt - senior unsecured notes: | |||||||||||

2025 Notes, $ | |||||||||||

2026 Notes, $ | |||||||||||

2028 Notes, $ due June 28, 2028 | |||||||||||

2029 Notes, € | |||||||||||

2030 Notes, € | |||||||||||

2031 Notes, $ | |||||||||||

2032 Notes, € | |||||||||||

2033 Notes, € | |||||||||||

2034 Notes $ | |||||||||||

2040 Notes, $ | |||||||||||

2050 Notes, $ | |||||||||||

2052 Notes, $ | |||||||||||

2053 Notes, $ | |||||||||||

2063 Notes, $ | |||||||||||

| 2022 Revolving Credit Agreement | ( | ( | |||||||||

| Total long-term debt | $ | $ | |||||||||

| Total debt obligations | $ | $ | |||||||||

Commercial Paper Program

Our U.S. dollar commercial paper program is supported by our 2022 Revolving Credit Agreement, which provides liquidity support for the repayment of commercial paper issued through this program. See “2022 Revolving Credit Agreement” below for further discussion. The effective interest rate of commercial paper issuances fluctuates as short-term interest rates and demand fluctuate. The fluctuation of these rates may impact our interest expense.

As of June 30, 2023, commercial paper notes in the table above reflect the aggregate principal amount, less the unamortized discount, which is being accreted through interest expense over the life of the applicable notes. The original maturities of these notes range from 70 days to 91 days and as of June 30, 2023, the weighted-average maturity is 16 days with a weighted-average effective interest rate of 5.28 % per annum.

Senior Unsecured Notes

Our 2040 Notes were issued at par. All of our other outstanding senior unsecured notes were issued at a discount. As a result of the discount, the proceeds received from each issuance were less than the aggregate principal amount. As of June 30, 2023, the amounts in the table above reflect the aggregate principal amount, less the unamortized debt discount and the unamortized debt issuance costs, which are being accreted through interest expense over the life of the applicable notes. The accretion of these costs is immaterial for the six months ended June 30, 2023. Our Euro denominated notes are adjusted for the impact of foreign currency translation. Our senior unsecured notes are general unsecured obligations which rank equally with all of our existing and future unsubordinated obligations and are not guaranteed by any of our subsidiaries. The senior unsecured notes were issued under indentures that, among other things, limit our ability to consolidate, merge or sell all or substantially all of our assets, create liens, and enter into sale and leaseback transactions. The senior unsecured notes may be redeemed by Nasdaq at any time, subject to a make-whole amount.

Upon a change of control triggering event (as defined in the various supplemental indentures governing the applicable notes), the terms require us to repurchase all or part of each holder’s notes for cash equal to 101 % of the aggregate principal amount purchased plus accrued and unpaid interest, if any.

The 2029 Notes, 2030 Notes, 2032 Notes and 2033 Notes pay interest annually. All other notes pay interest semi-annually. The U.S senior unsecured notes coupon rates may vary with Nasdaq’s debt rating, to the extent Nasdaq is downgraded below investment grade, up to an upward rate adjustment not to exceed 2 %.

Net Investment Hedge

Our Euro denominated notes have been designated as a hedge of our net investment in certain foreign subsidiaries to mitigate the foreign exchange risk associated with certain investments in these subsidiaries. Accordingly, the remeasurement of these notes is recorded in accumulated other comprehensive loss within Nasdaq's stockholders’ equity in the Condensed Consolidated Balance Sheets. As of June 30, 2023, the impact of the translation of our Euro denominated notes was $39 million.

12

Financing of the Adenza Transaction

Senior Unsecured Notes

In June 2023, Nasdaq issued a series of six notes for total proceeds of $5,016 million, net of debt issuance costs, with various maturity dates ranging from 2025 to 2063. The net proceeds from these notes will be used to finance the majority of the cash consideration due in connection with the Adenza acquisition. The notes issued in connection with the Adenza financing (the 2025 Notes, 2028 Notes, the 2032 Notes, the 2034 Notes, the 2053 Notes and the 2063 Notes) are subject to a special mandatory redemption feature pursuant to which we will be required to redeem all of the outstanding notes at a redemption price equal to 101 % of the aggregate principal amount of all the notes, plus accrued and unpaid interest, in the event that either Nasdaq notifies the trustee in respect of such notes that Nasdaq will no longer pursue the Adenza acquisition or that the closing of the Adenza acquisition does not occur on or before the later of (i) the date that is five business days after September 10, 2024 and (ii) the date that is five business days after any later date to which the seller and Nasdaq mutually agree to extend. For further discussion of the Adenza acquisition, see “2023 Announced Acquisition,” of Note 4, “Acquisitions.”

Acquisition Term Loan Agreement

In June 2023, in connection with the financing of the Adenza acquisition, we entered into a term loan credit agreement, or the Acquisition Term Loan Agreement. The Acquisition Term Loan Agreement provides us with the ability to borrow up to $600 million to finance a portion of the cash consideration for the Adenza acquisition, for repayment of certain debt of Adenza and its subsidiaries, and to pay fees, costs and expenses related to the transaction.

Under the Acquisition Term Loan Agreement, borrowings bear interest on the principal amount outstanding at a variable interest rate based on either the SOFR or the base rate (or other applicable rate with respect to non-dollar borrowings), plus an applicable margin that varies with Nasdaq's credit rating. As of June 30, 2023, no amounts were outstanding.

Credit Facilities

2022 Revolving Credit Agreement

In December 2020, Nasdaq entered into the 2020 Credit Facility, which replaced a former credit facility and consists of a $1.25 billion five-year revolving credit facility (with sublimits for non-dollar borrowings, swingline borrowings and letters of credit). We amended and restated the 2020 Credit Facility in December 2022 with a new maturity date of December 16, 2027. Nasdaq intends to use funds available under the 2022 Revolving Credit Agreement for general corporate purposes and to provide liquidity support for the repayment of commercial paper issued through the commercial paper program. Nasdaq is permitted to repay borrowings under our 2022 Revolving Credit Agreement at any time in whole or in part, without penalty.

As of June 30, 2023, no amounts were outstanding on the 2022 Revolving Credit Agreement. The $(5 ) million balance represents unamortized debt issuance costs which are being accreted through interest expense over the life of the credit facility.

Borrowings under the revolving credit facility and swingline borrowings bear interest on the principal amount outstanding at a variable interest rate based on either the SOFR (or a successor rate to SOFR), the base rate (as defined in the 2022 credit agreement), or other applicable rate with respect to non-dollar borrowings, plus an applicable margin that varies with Nasdaq’s debt rating. We are charged commitment fees of 0.100 % to 0.250 %, depending on our credit rating, whether or not amounts have been borrowed. These commitment fees are included in interest expense and were not material for the three and six months ended June 30, 2023 and 2022.

The 2022 Revolving Credit Agreement contains financial and operating covenants. Financial covenants include a maximum leverage ratio. Operating covenants include, among other things, limitations on Nasdaq’s ability to incur additional indebtedness, grant liens on assets, dispose of assets and make certain restricted payments. The facility also contains customary affirmative covenants, including access to financial statements, notice of defaults and certain other material events, maintenance of properties and insurance, and customary events of default, including cross-defaults to our material indebtedness.

The 2022 Revolving Credit Agreement includes an option for Nasdaq to increase the available aggregate amount by up to $750 million, subject to the consent of the lenders funding the increase and certain other conditions.

Other Credit Facilities

Certain of our European subsidiaries have several other credit facilities, which are available in multiple currencies, primarily to support our Nasdaq Clearing operations in Europe, as well as to provide a cash pool credit line for one subsidiary. These credit facilities, in aggregate, totaled $178 million as of June 30, 2023 and $184 million as of December 31, 2022 in available liquidity, none one-year term. The amounts borrowed under these various credit facilities bear interest on the principal amount outstanding at a variable interest rate based on a base rate (as defined in the applicable credit agreement), plus an applicable margin. We are charged commitment fees (as defined in the applicable credit agreement), whether or not amounts have been borrowed. These commitment fees are included in interest expense and were not material for the three and six months ended June 30, 2023 and 2022.

These facilities include customary affirmative and negative operating covenants and events of default.

Debt Covenants

As of June 30, 2023, we were in compliance with the covenants of all of our debt obligations.

13

9. RETIREMENT PLANS

Defined Contribution Savings Plan

We sponsor a 401(k) plan, which is a voluntary defined contribution savings plan, for U.S. employees. Employees are immediately eligible to make contributions to the plan and are also eligible for an employer contribution match at an amount equal to 100.0 6.0 The following table presents the savings plan expense for the three and six months ended June 30, 2023 and 2022, which is included in compensation and benefits expense in the Condensed Consolidated Statements of Income:

| Three Months Ended June 30, | Six Months Ended June 30, | ||||||||||||||||||||||

| 2023 | 2022 | 2023 | 2022 | ||||||||||||||||||||

| (in millions) | |||||||||||||||||||||||

Savings Plan expense | $ | $ | $ | $ | |||||||||||||||||||

Pension and Supplemental Executive Retirement Plans

We maintain non-contributory, defined-benefit pension plans, non-qualified SERPs for certain senior executives and other post-retirement benefit plans for eligible employees in the U.S. Our pension plans and SERPs are frozen. Future service and salary for all participants do not count toward an accrual of benefits under the pension plans and SERPs. Most employees outside the U.S. are covered by local retirement plans or by applicable social laws. Benefits under social laws are generally expensed in the periods in which the costs are incurred. The following table presents the total expense for these plans for the three and six months ended June 30, 2023 and 2022, which is included in compensation and benefits expense in the Condensed Consolidated Statements of Income:

| Three Months Ended June 30, | Six Months Ended June 30, | ||||||||||||||||||||||

| 2023 | 2022 | 2023 | 2022 | ||||||||||||||||||||

| (in millions) | |||||||||||||||||||||||

Retirement Plans expense | $ | $ | $ | $ | |||||||||||||||||||

Nonqualified Deferred Compensation Plan

10. SHARE-BASED COMPENSATION

We have a share-based compensation program for employees and non-employee directors. Share-based awards granted under this program include restricted stock (consisting of restricted stock units), PSUs and stock options. For accounting purposes, we consider PSUs to be a form of restricted stock. Generally, annual employee awards are granted on April 1st of each year.

Summary of Share-Based Compensation Expense

The following table presents the total share-based compensation expense resulting from equity awards and the 15.0

| Three Months Ended June 30, | Six Months Ended June 30, | ||||||||||||||||||||||

| 2023 | 2022 | 2023 | 2022 | ||||||||||||||||||||

| (in millions) | |||||||||||||||||||||||

| Share-based compensation expense before income taxes | $ | $ | $ | $ | |||||||||||||||||||

Common Shares Available Under Our Equity Plan

As of June 30, 2023, we had approximately 24.7 million shares of common stock authorized for future issuance under our Equity Plan.

Restricted Stock

We grant restricted stock to most employees. The grant date fair value of restricted stock awards is based on the closing stock price at the date of grant less the present value of future cash dividends. Restricted stock awards granted to employees below the manager level generally vest 33 % on the first anniversary of the grant date, 33 % on the second anniversary of the grant date, and the remainder on the third anniversary of the grant date. Restricted stock awards granted to employees at or above the manager level generally vest 33 % on the second anniversary of the grant date, 33 % on the third anniversary of the grant date, and the remainder on the fourth anniversary of the grant date.

Summary of Restricted Stock Activity

The following table summarizes our restricted stock activity for the six months ended June 30, 2023:

| Restricted Stock | |||||||||||

| Number of Awards | Weighted-Average Grant Date Fair Value | ||||||||||

| Unvested at December 31, 2022 | $ | ||||||||||

| Granted | |||||||||||

| Vested | ( | ||||||||||

| Forfeited | ( | ||||||||||

| Unvested at June 30, 2023 | $ | ||||||||||

As of June 30, 2023, $144 million of total unrecognized compensation cost related to restricted stock is expected to be recognized over a weighted-average period of 1.9 years.

14

PSUs

We grant three-year PSUs to certain eligible employees. PSUs are based on performance measures that impact the amount of shares that each recipient will receive upon vesting. Each eligible individual receives PSUs, subject to the satisfaction of applicable market performance conditions, with a three-year cumulative performance period that vest at the end of the performance period and which settle in shares of our common stock. Compensation cost is recognized over the three-year performance period, taking into account an estimated forfeiture rate, regardless of whether the market condition is satisfied, provided that the requisite service period has been completed. Performance will be determined by comparing Nasdaq’s TSR to two peer groups, each weighted 50.0 %. The first peer group consists of exchange companies, and the second peer group consists of all companies in the S&P 500. Nasdaq’s relative performance ranking against each of these groups will determine the final number of shares delivered to each individual under the program. The award issuance under this program will be between 0.0 % and 200.0 % of the number of PSUs granted and will be determined by Nasdaq’s overall performance against both peer groups. However, if Nasdaq’s TSR is negative for the three-year performance period, regardless of TSR ranking, the award issuance will not exceed 100.0 % of the number of PSUs granted. We estimate the fair value of PSUs granted under the three-year PSU program using the Monte Carlo simulation model, as these awards contain a market condition.

Grants of PSUs that were issued in 2020 with a three-year performance period exceeded the applicable performance parameters. As a result, an additional 764,748 units above the original target were granted in the first quarter of 2023 and were fully vested upon issuance.

The following weighted-average assumptions were used to determine the weighted-average fair values of the outstanding PSU awards granted under the three-year PSU program during the six months ended June 30, 2023 and 2022:

| Grant date | April 3, 2023 | April 1, 2022 | |||||||||

| Weighted-average risk-free interest rate | % | % | |||||||||

Expected volatility | % | % | |||||||||

| Weighted-average grant date share price | $ | $ | |||||||||

| Weighted-average fair value at grant date | $ | $ | |||||||||

In the table above, the risk-free interest rate for periods within the expected life of the award is based on the U.S. Treasury yield curve in effect at the time of grant; and we use historic volatility for PSU awards issued under the three-year PSU program, as implied volatility data could not be obtained for all the companies in the peer groups used for relative performance measurement within the program.

In addition, the annual dividend assumption utilized in the Monte Carlo simulation model is based on Nasdaq’s dividend yield at the date of grant.

Summary of PSU Activity

The following table summarizes our PSU activity for the six months ended June 30, 2023:

| PSUs | |||||||||||

| Number of Awards | Weighted-Average Grant Date Fair Value | ||||||||||

| Unvested at December 31, 2022 | $ | ||||||||||

| Granted | |||||||||||

| Vested | ( | ||||||||||

| Forfeited | ( | ||||||||||

| Unvested at June 30, 2023 | $ | ||||||||||

In the table above, the granted amount also includes additional awards granted based on overachievement of performance parameters.

As of June 30, 2023, total unrecognized compensation cost related to the PSU program is $63 million and is expected to be recognized over a weighted-average period of 1.6 years.

Stock Options

We had no stock option activity for the six months ended June 30, 2023. A summary of our outstanding and exercisable stock options at June 30, 2023 is as follows:

Number of Stock Options | Weighted-Average Exercise Price | Weighted- Average Remaining Contractual Term (in years) | Aggregate Intrinsic Value (in millions) | |||||||||||

| Outstanding at June 30, 2023 | $ | $ | ||||||||||||

| Exercisable at June 30, 2023 | $ | $ | ||||||||||||

As of June 30, 2023, the aggregate pre-tax intrinsic value of the outstanding and exercisable stock options in the above table was $22 million and represents the difference between our closing stock price on June 30, 2023 of $49.85 and the exercise price, times the number of shares that would have been received by the option holder had the option holder exercised the stock options on that date. This amount can change based on the fair market value of our common stock. As of June 30, 2022, 0.8 million outstanding stock options were exercisable and the weighted-average exercise price was $22.23 .

15

ESPP

We have an ESPP under which approximately 11.7 million shares of our common stock were available for future issuance as of June 30, 2023. Under our ESPP, employees may purchase shares having a value not exceeding 10.0 % of their annual compensation, subject to applicable annual Internal Revenue Service limitations. We record compensation expense related to the 15.0 % discount that is given to our employees.

11. NASDAQ STOCKHOLDERS' EQUITY

Common Stock

As of June 30, 2023, 900,000,000 shares of our common stock were authorized, 514,060,903 shares were issued and 491,274,775 shares were outstanding. As of December 31, 2022, 900,000,000 shares of our common stock were authorized, 513,157,630 shares were issued and 491,592,491 shares were outstanding. The holders of common stock are entitled to one 5.0

Common Stock in Treasury, at Cost

We account for the purchase of treasury stock under the cost method with the shares of stock repurchased reflected as a reduction to Nasdaq stockholders’ equity and included in common stock in treasury, at cost in the Condensed Consolidated Balance Sheets. Shares repurchased under our share repurchase program are currently retired and canceled and are therefore not included in the common stock in treasury balance. If treasury shares are reissued, they are recorded at the average cost of the treasury shares acquired. We held 22,786,128 shares of common stock in treasury as of June 30, 2023 and 21,565,139 shares as of December 31, 2022, most of which are related to shares of our common stock withheld for the settlement of employee tax withholding obligations arising from the vesting of restricted stock and PSUs.

Share Repurchase Program

As of June 30, 2023, the remaining aggregate authorized amount under the existing share repurchase program was $491 million.

These repurchases may be made from time to time at prevailing market prices in open market purchases, privately-negotiated transactions, block purchase techniques, an accelerated share repurchase program or otherwise, as determined by our management. The repurchases are primarily funded from existing cash balances. The share repurchase program may be suspended, modified or discontinued at any time, and has no defined expiration date.

The following is a summary of our share repurchase activity, reported based on settlement date, for the six months ended June 30, 2023:

| Six Months Ended June 30, 2023 | ||||||||

| Number of shares of common stock repurchased | ||||||||

Average price paid per share | $ | |||||||

Total purchase price (in millions) | $ | |||||||

In the table above, the number of shares of common stock repurchased excludes an aggregate of 1,220,989 shares withheld upon the vesting of restricted stock and PSUs for the six months ended June 30, 2023.

As discussed above in “Common Stock in Treasury, at Cost,” shares repurchased under our share repurchase program are currently retired and cancelled.

Preferred Stock

Our certificate of incorporation authorizes the issuance of 30,000,000 0.01 no

Cash Dividends on Common Stock

During the first six months of 2023, our board of directors declared and paid the following cash dividends:

| Declaration Date | Dividend Per Common Share | Record Date | Total Amount Paid | Payment Date | ||||||||||||||||||||||

| (in millions) | ||||||||||||||||||||||||||

| January 24, 2023 | $ | March 17, 2023 | $ | March 31, 2023 | ||||||||||||||||||||||

| April 18, 2023 | June 16, 2023 | June 30, 2023 | ||||||||||||||||||||||||

| $ | ||||||||||||||||||||||||||

The total amount paid of $206 million was recorded in retained earnings within Nasdaq's stockholders' equity in the Condensed Consolidated Balance Sheets at June 30, 2023.

In July 2023, the board of directors approved a regular quarterly cash dividend of $0.22 per share on our outstanding common stock. The dividend is payable on September 29, 2023 to shareholders of record at the close of business on September 15, 2023. The estimated aggregate payment of this dividend is $108 million. Future declarations of quarterly dividends and the establishment of future record and payment dates are subject to approval by the board of directors.

The board of directors maintains a dividend policy with the intention to provide stockholders with regular and increasing dividends as earnings and cash flows increase.

16

12. EARNINGS PER SHARE

The following table sets forth the computation of basic and diluted earnings per share:

| Three Months Ended June 30, | |||||||||||

| 2023 | 2022 | ||||||||||

| Numerator: | (in millions, except share and per share amounts) | ||||||||||

| Net income attributable to common shareholders | $ | $ | |||||||||

| Denominator: | |||||||||||

| Weighted-average common shares outstanding for basic earnings per share | |||||||||||

| Weighted-average effect of dilutive securities - Employee equity awards | |||||||||||

| Weighted-average common shares outstanding for diluted earnings per share | |||||||||||

| Basic and diluted earnings per share: | |||||||||||

| Basic earnings per share | $ | $ | |||||||||

| Diluted earnings per share | $ | $ | |||||||||

| Six Months Ended June 30, | |||||||||||

| 2023 | 2022 | ||||||||||

| Numerator: | (in millions, except share and per share amounts) | ||||||||||

| Net income attributable to common shareholders | $ | $ | |||||||||

| Denominator: | |||||||||||

| Weighted-average common shares outstanding for basic earnings per share | |||||||||||

| Weighted-average effect of dilutive securities - Employee equity awards | |||||||||||

| Weighted-average common shares outstanding for diluted earnings per share | |||||||||||

| Basic and diluted earnings per share: | |||||||||||

| Basic earnings per share | $ | $ | |||||||||

| Diluted earnings per share | $ | $ | |||||||||

13. FAIR VALUE OF FINANCIAL INSTRUMENTS

The following tables present our financial assets and financial liabilities that were measured at fair value on a recurring basis as of June 30, 2023 and December 31, 2022.

| June 30, 2023 | |||||||||||||||||||||||

Total | Level 1 | Level 2 | Level 3 | ||||||||||||||||||||

(in millions) | |||||||||||||||||||||||