Filed Pursuant to Rule 424(b)(3)

Registration Statement No. 333-178960

CALCULATION OF REGISTRATION FEE

|

| ||||

| Title of Each Class of Securities Offered |

Maximum Offering Price |

Amount of Registration Fee (1) | ||

| Relative Performance Securities Linked to the S&P 500® Index and the NYSE US 5 Year Treasury Futures Index due November 30, 2018 |

$2,230,000.00 | $287.22 | ||

|

| ||||

|

| ||||

| (1) | Calculated in accordance with Rule 457(r) of the Securities Act of 1933. |

|

|

FINAL PRICING SUPPLEMENT Filed Pursuant to Rule 424(b)(3) Registration Statement 333-178960 Dated November 25, 2013 |

|

UBS AG $2,230,000 Relative Performance Securities

Linked to the S&P 500® Index and the NYSE US 5 Year Treasury Futures Index due November 30, 2018

Investment Description

The UBS AG Relative Performance Securities (the “Securities”) are unsubordinated and unsecured debt obligations issued by UBS AG (“UBS”) with returns linked to the performance of the S&P 500® Index (the “long index”) relative to the NYSE US 5 Year Treasury Futures Index (the “short index”, and together with the long index, the “underlying indices”). If the performance of the long index is equal to or greater than the performance of the short index over the term of the Securities, as measured by the index returns of each underlying index from the trade date to the final valuation date, UBS will repay the principal amount of the Securities at maturity plus pay a return equal to the outperformance of the long index relative to the short index (the “relative return”) multiplied by the participation rate of 129.85%. If the long index underperforms the short index over the term of the Securities, you will be fully exposed to the underperformance of the long index relative to the short index, and UBS will repay less than the full principal amount of the Securities, if anything, resulting in a loss of principal that is proportionate to the negative relative return. Investing in the Securities involves significant risks. UBS will not pay any interest on the Securities. You may lose some or all of the principal amount of the Securities if the short index outperforms the long index over the term of the Securities. Any payment on the Securities is subject to the creditworthiness of UBS and is not, either directly or indirectly, an obligation of any third party. If UBS were to default on its payment obligations, you may not receive any amounts owed to you under the Securities and you could lose your entire investment.

NOTICE TO INVESTORS: THE SECURITIES ARE SIGNIFICANTLY RISKIER THAN CONVENTIONAL DEBT INSTRUMENTS. UBS IS NOT NECESSARILY OBLIGATED TO REPAY THE FULL PRINCIPAL AMOUNT OF THE SECURITIES AT MATURITY, AND THE SECURITIES WILL HAVE MARKET RISKS SIMILAR TO THE UNDERLYING INDICES, WHICH CAN RESULT IN THE LOSS OF SOME OR ALL OF YOUR INITIAL INVESTMENT IN THE SECURITIES. THIS MARKET RISK IS IN ADDITION TO THE CREDIT RISK INHERENT IN PURCHASING A DEBT OBLIGATION OF UBS. YOU SHOULD NOT PURCHASE THE SECURITIES IF YOU DO NOT UNDERSTAND OR ARE NOT COMFORTABLE WITH THE SIGNIFICANT RISKS INVOLVED IN INVESTING IN THE SECURITIES.

YOU SHOULD CAREFULLY CONSIDER THE RISKS DESCRIBED UNDER “KEY RISKS” BEGINNING ON PAGE 11 AND UNDER “RISK FACTORS” BEGINNING ON PAGE PS-15 OF THE RELATIVE PERFORMANCE SECURITIES PRODUCT SUPPLEMENT BEFORE PURCHASING ANY SECURITIES. EVENTS RELATING TO ANY OF THOSE RISKS, OR OTHER RISKS AND UNCERTAINTIES, COULD ADVERSELY AFFECT THE MARKET VALUE OF, AND THE RETURN ON YOUR SECURITIES. YOU MAY LOSE SOME OR ALL OF YOUR INVESTMENT IN THE SECURITIES.

Security Offering

These final terms relate to the Relative Performance Securities linked to the S&P 500® Index and the NYSE US 5 Year Treasury Futures Index. The Securities are offered at a minimum investment of $1,000, or 100 Securities at $10.00 per Security, and integral multiples of $10.00 in excess thereof.

| Offering | Long Index Bloomberg Symbol |

Long Index Initial Index Level |

Short Index Bloomberg Symbol |

Short Index Initial Index Level |

Participation Rate |

CUSIP | ISIN | |||||||

| Securities linked to the S&P 500® Index and the NYSE US 5 Year Treasury Futures Index | SPX | 1,802.48 | USTFIV | 163.08 | 129.85% | 90271R467 | US90271R4671 |

The estimated initial value of the Securities as of the trade date is $9.2650 for Securities linked to the relative performance between the S&P 500® Index and the NYSE US 5 Year Treasury Futures Index. The estimated initial value of the Securities was determined as of the close of the relevant markets on the date of this final pricing supplement by reference to UBS’ internal pricing models, inclusive of the internal funding rate. For more information about secondary market offers and the estimated initial value of the Securities, see “Key Risks — Fair value considerations” and “Key Risks — Limited or no secondary market and secondary market price considerations” on pages 11 and 12 of this final pricing supplement.

See “Additional Information about UBS and the Securities” on page 2. The Securities will have the terms specified in the Relative Performance Securities product supplement relating to the Securities, dated September 6, 2012 the accompanying prospectus and this final pricing supplement.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or passed upon the adequacy or accuracy of this final pricing supplement., the Relative Performance Securities product supplement or the accompanying prospectus. Any representation to the contrary is a criminal offense. The Securities are not deposit liabilities of UBS AG and are not FDIC insured.

| Price to Public | Underwriting Discount | Proceeds to UBS AG | ||||

| Per Security | $10.00 | $0.35 | $9.65 | |||

| Total | $2,230,000.00 | $78,050.00 | $2,151,950.00 |

| UBS Financial Services Inc. | UBS Investment Bank | |

| Final Pricing Supplement dated November 25, 2013 | ||

Additional Information about UBS and the Securities

UBS has filed a registration statement (including a prospectus, as supplemented by a product supplement for the Securities and an index supplement for various securities we may offer, including the Securities), with the Securities and Exchange Commission, or SEC, for the offering to which this final pricing supplement relates. Before you invest, you should read these documents and any other documents relating to this offering that UBS has filed with the SEC for more complete information about UBS and this offering. You may obtain these documents without cost by visiting EDGAR on the SEC website at www.sec.gov. Our Central Index Key, or CIK, on the SEC website is 0001114446. Alternatively, UBS will arrange to send you the prospectus and the Relative Performance Securities product supplement if you so request by calling toll-free 877-387-2275.

You may access these documents on the SEC website at www.sec.gov as follows:

| ¨ | Product supplement for Relative Performance Securities dated September 6, 2012: |

http://www.sec.gov/Archives/edgar/data/1114446/000119312512382603/d407568d424b2.htm

| ¨ | Index Supplement dated January 24, 2012: |

http://www.sec.gov/Archives/edgar/data/1114446/000119312512021889/d287369d424b2.htm

| ¨ | Prospectus dated January 11, 2012: |

http://www.sec.gov/Archives/edgar/data/1114446/000119312512008669/d279364d424b3.htm

References to “UBS,” “we,” “our” and “us” refer only to UBS AG and not to its consolidated subsidiaries. In this final pricing supplement, “Securities” refer to the Relative Performance Securities that are offered hereby, unless the context otherwise requires. Also, references to the “Relative Performance Securities product supplement” mean the UBS product supplement, dated September 6, 2012, references to the “index supplement” mean the UBS index supplement, dated January 24, 2012 and references to “accompanying prospectus” mean the UBS prospectus titled “Debt Securities and Warrants,” dated January 11, 2012.

This final pricing supplement, together with the documents listed above, contains the terms of the Securities and supersedes all other prior or contemporaneous oral statements as well as any other written materials including pricing terms, correspondence, trade ideas, structures for implementation, sample structures, brochures or other educational materials of ours. You should carefully consider, among other things, the matters set forth in “Key Risks” beginning on page 11 and in “Risk Factors” in the accompanying product supplement, as the Securities involve risks not associated with conventional debt securities. We urge you to consult your investment, legal, tax, accounting and other advisers before deciding to invest in the Securities.

UBS reserves the right to change the terms of, or reject any offer to purchase, the Securities prior to their issuance. In the event of any changes to the terms of the Securities, UBS will notify you and you will be asked to accept such changes in connection with your purchase. You may also choose to reject such changes in which case UBS may reject your offer to purchase.

2

Investor Suitability

The investor suitability considerations identified above are not exhaustive. Whether or not the Securities are a suitable investment for you will depend on your individual circumstances and you should reach an investment decision only after you and your investment, legal, tax, accounting and other advisors have carefully considered the suitability of an investment in the Securities in light of your particular circumstances. You should also review “Key Risks” beginning on page 11 of this final pricing supplement and the more detailed “Risk Factors” beginning on page PS-15 of the Relative Performance Securities product supplement for risks related to an investment in the Securities.

3

IF THE LONG INDEX RETURN IS LESS THAN THE SHORT INDEX RETURN, THE RELATIVE RETURN WILL BE NEGATIVE, AND YOU WILL LOSE SOME OR ALL OF YOUR INITIAL INVESTMENT AT MATURITY. THE RELATIVE RETURN WILL BE NEGATIVE IF, BETWEEN THE TRADE DATE AND THE FINAL VALUATION DATE, THE SHORT INDEX OUTPERFORMS THE LONG INDEX, WHICH WILL BE THE CASE IF: (A) BOTH UNDERLYING INDICES APPRECIATE BUT THE SHORT INDEX APPRECIATES BY A GREATER PERCENTAGE THAN THE PERCENTAGE THAT THE LONG INDEX APPRECIATES, (B) THE LONG INDEX DEPRECIATES WHILE THE SHORT INDEX REMAINS FLAT OR APPRECIATES, (C) THE LONG INDEX REMAINS FLAT WHILE THE SHORT INDEX APPRECIATES OR (D) BOTH UNDERLYING INDICES DEPRECIATE BUT THE LONG INDEX DEPRECIATES BY A GREATER PERCENTAGE THAN THE PERCENTAGE THAT THE SHORT INDEX DEPRECIATES.

INVESTING IN THE SECURITIES INVOLVES SIGNIFICANT RISKS. YOU MAY LOSE SOME OR ALL OF YOUR PRINCIPAL AMOUNT. ANY PAYMENT ON THE SECURITIES, INCLUDING ANY REPAYMENT OF PRINCIPAL, IS SUBJECT TO THE CREDITWORTHINESS OF UBS. IF UBS WERE TO DEFAULT ON ITS PAYMENT OBLIGATIONS, YOU MAY NOT RECEIVE ANY AMOUNTS OWED TO YOU UNDER THE SECURITIES AND YOU COULD LOSE YOUR ENTIRE INVESTMENT.

4

Hypothetical Examples of the Securities at Maturity

The examples below illustrate the payment at maturity for a $10.00 principal amount Security on a hypothetical offering of the Securities, with the following assumptions (the actual terms for each Security are specified on the first page of this final pricing supplement; amounts may have been rounded for ease of reference):

| Term: | Approximately 5 years | |

| Long Index Initial Index Level: | 1,600.00 | |

| Short Index Initial Index Level: | 160.00 | |

| Participation Rate: | 124.50% |

The examples below do not take into account any tax consequences from investing in the Securities.

Example 1: On the final valuation date, the long index closes at 2,000.00, which is 25% above the initial index level of 1,600.00, and the short index closes at 144.00, which is 10% below the initial index level of 160.00.

Step 1: Calculate the index return for each underlying index.

| Index |

Initial Index Level |

Final Index Level |

Index Return | |||

| S&P 500® Index (the long index) | 1,600.00 | 2,000.00 | 25%, which equals the long index return | |||

| NYSE US 5 Year Treasury Futures Index (the short index) | 160.00 | 144.00 | -10%, which equals the short index return |

The index returns set forth in the table above reflect the performance of each underlying index from the initial index level to the final index level, expressed as a percentage and calculated as follows:

Final Index Level – Initial Index Level

Initial Index Level

Step 2: Calculate the relative return.

A percentage equal to the long index return minus the short index return, calculated as follows:

Long Index Return – Short Index Return

25% – (-10%) = 35% Relative Return

Step 3: Calculate the payment at maturity.

Because the long index return is greater than the short index return, UBS will repay the principal amount plus pay a return equal to the relative return multiplied by the participation rate. Accordingly, the payment at maturity of $14.3575 per $10.00 principal amount Security would be calculated as follows:

$10.00 + ($10.00 × Relative Return × Participation Rate)

$10.00 + ($10.00 × 35% × 124.50%) = $14.3575

Example 2: On the final valuation date, the long index closes at 2,000.00, which is 25% above the initial index level of 1,600.00, and the short index closes at 200.00, which is 25% above the initial index level of 160.00.

Step 1: Calculate the index return for each underlying index.

| Index |

Initial Index Level |

Final Index Level |

Index Return | |||

| S&P 500® Index (the long index) | 1,600.00 | 2,000.00 | 25%, which equals the long index return | |||

| NYSE US 5 Year Treasury Futures Index (the short index) | 160.00 | 200.00 | 25%, which equals the short index return |

The index returns set forth in the table above reflect the performance of each underlying index from the initial index level to the final index level, expressed as a percentage and calculated as follows:

Final Index Level – Initial Index Level

Initial Index Level

Step 2: Calculate the relative return.

A percentage equal to the long index return minus the short index return, calculated as follows:

Long Index Return – Short Index Return

25% – 25% = 0% Relative Return

5

Step 3: Calculate the payment at maturity.

Because the long index return is equal to the short index return, UBS will repay the principal amount plus pay a return equal to the relative return multiplied by the participation rate. Accordingly, the payment at maturity of $10.00 per $10.00 principal amount Security would be calculated as follows:

$10.00 + ($10.00 × Relative Return × Participation Rate)

$10.00 + ($10.00 x 0% x 124.50%) = $10.00

Example 3: On the final valuation date, the long index closes at 1,760.00, which is 10% above the initial index level of 1,600.00, and the short index closes at 200.00, which is 25% above the initial index level of 160.00.

Step 1: Calculate the index return for each underlying index.

| Index |

Initial Index Level |

Final Index Level |

Index Return | |||

| S&P 500® Index (the long index) | 1,600.00 | 1,760.00 | 10%, which equals the long index return | |||

| NYSE US 5 Year Treasury Futures Index (the short index) | 160.00 | 200.00 | 25%, which equals the short index return |

The index returns set forth in the table above reflect the performance of each underlying index from the initial index level to the final index level, expressed as a percentage and calculated as follows:

Final Index Level – Initial Index Level

Initial Index Level

Step 2: Calculate the relative return.

A percentage equal to the long index return minus the short index return, calculated as follows:

Long Index Return – Short Index Return

10% – 25% = -15% Relative Return

Step 3: Calculate the payment at maturity.

Because the long index return is less than the short index return, UBS will repay less than the full principal amount at maturity, if anything, resulting in a loss of principal that is proportionate to the negative relative return. Accordingly, the payment at maturity of $8.50 per $10.00 principal amount Security would be calculated as follows:

the greater of (i) $10.00 + ($10.00 × Relative Return) and (ii) $0

= the greater of (i) $10.00 + ($10.00 x -15%) and (ii) $0

= the greater of (i) $8.50 and (ii) $0

Example 4: On the final valuation date, the long index closes at 1,200.00, which is 25% below the initial index level of 1,600.00, and the short index closes at 128.00, which is 20% below the initial index level of 160.00.

Step 1: Calculate the index return for each underlying index.

| Index |

Initial Index Level |

Final Index Level |

Index Return | |||

| S&P 500® Index (the long index) | 1,600.00 | 1,200.00 | -25%, which equals the long index return | |||

| NYSE US 5 Year Treasury Futures Index (the short index) | 160.00 | 128.00 | -20%, which equals the short index return |

The index returns set forth in the table above reflect the performance of each underlying index from the initial index level to the final index level, expressed as a percentage and calculated as follows:

Final Index Level – Initial Index Level

Initial Index Level

Step 2: Calculate the relative return.

A percentage equal to the long index return minus the short index return, calculated as follows:

Long Index Return – Short Index Return

-25% – (-20%) = -5% Relative Return

6

Step 3: Calculate the payment at maturity.

Because the long index return is less than the short index return, UBS will repay less than the full principal amount at maturity, if anything, resulting in a loss of principal that is proportionate to the negative relative return. Accordingly, the payment at maturity of $9.50 per $10.00 principal amount Security would be calculated as follows:

the greater of (i) $10.00 + ($10.00 × Relative Return) and (ii) $0

= the greater of (i) $10.00 + ($10.00 x -5%) and (ii) $0

= the greater of (i) $9.50 and (ii) $0

Example 5: On the final valuation date, the long index closes at 1,520.00, which is 5% below the initial index level of 1,600.00, and the short index closes at 144.00, which is 10% below the initial index level of 160.00.

Step 1: Calculate the index return for each underlying index.

| Index |

Initial Index Level |

Final Index Level |

Index Return | |||

| S&P 500® Index (the long index) | 1,600.00 | 1,520.00 | -5%, which equals the long index return | |||

| NYSE US 5 Year Treasury Futures Index (the short index) | 160.00 | 144.00 | -10%, which equals the short index return |

The index returns set forth in the table above reflect the performance of each underlying index from the initial index level to the final index level, expressed as a percentage and calculated as follows:

Final Index Level – Initial Index Level

Initial Index Level

Step 2: Calculate the relative return.

A percentage equal to the long index return minus the short index return, calculated as follows:

Long Index Return – Short Index Return

-5% – (-10%) = 5% Relative Return

Step 3: Calculate the payment at maturity.

Because the long index return is greater than the short index return, UBS will repay the principal amount plus pay a return equal to the relative return multiplied by the participation rate. Accordingly, the payment at maturity of $10.6225 per $10.00 principal amount Security would be calculated as follows:

$10.00 + ($10.00 × Relative Return x Participation Rate)

$10.00 + ($10.00 × 5% x 124.50%) = $10.6225

Example 6 — On the final valuation date, the long index closes at 560.00, which is 65% below the index starting level of 1,600.00, and the short index closes at 240.00, which is 50% above the index starting level of 160.00.

Step 1: Calculate the index return for each Index.

| Index |

Initial Index Level |

Final Index Level |

Index Return | |||

| S&P 500® Index (the long index) | 1,600.00 | 560.00 | -65%, which equals the long index return | |||

| NYSE US 5 Year Treasury Futures Index (the short index) | 160.00 | 240.00 | 50%, which equals the short index return |

The index returns set forth in the table above reflect the performance of each index from the index starting level to the index ending level, expressed as a percentage and calculated as follows:

Index Ending Level – Index Starting Level

Index Starting Level

Step 2: Calculate the relative return.

A percentage equal to the long index return minus the short index return, calculated as follows:

Long Index Return – Short Index Return

-65% – 50% = -115% Relative Return

7

Step 3: Calculate the Payment at Maturity.

Because the long index return is less than the short index return, UBS will repay less than the full principal amount at maturity, if anything, resulting in a loss of principal that is proportionate to the negative relative return. Accordingly, the payment at maturity of $0 per $10.00 principal amount Security would be calculated as follows:

the greater of (i) $10.00 + ($10.00 × Relative Return) and (ii) $0

= the greater of (i) $10.00 + ($10.00 x -115%) and (ii) $0

= the greater of (i) -$1.50 and (ii) $0

INVESTING IN THE SECURITIES INVOLVES SIGNIFICANT RISKS. YOU MAY LOSE SOME OR ALL OF YOUR PRINCIPAL AMOUNT. ANY PAYMENT ON THE SECURITIES, INCLUDING ANY REPAYMENT OF PRINCIPAL, IS SUBJECT TO THE CREDITWORTHINESS OF UBS. IF UBS WERE TO DEFAULT ON ITS PAYMENT OBLIGATIONS, YOU MAY NOT RECEIVE ANY AMOUNTS OWED TO YOU UNDER THE SECURITIES AND YOU COULD LOSE YOUR ENTIRE INVESTMENT.

8

What Are the Tax Consequences of the Securities?

The United States federal income tax consequences of your investment in the Securities are uncertain. Some of these tax consequences are summarized below, but we urge you to read the more detailed discussion in “Supplemental U.S. Tax Considerations” beginning on page PS-32 of the Relative Performance Securities product supplement and discuss the tax consequences of your particular situation with your tax advisor.

There are no statutory provisions, regulations, published rulings or judicial decisions addressing the characterization for U.S. federal income tax purposes of securities with terms that are substantially the same as the Securities. Pursuant to the terms of the Securities, UBS and you agree, in the absence of a statutory, regulatory, administrative or judicial ruling to the contrary, to characterize your Securities as a pre-paid derivative contract with respect to the underlying indices. If your Securities are so treated, you should generally recognize capital gain or loss upon the sale or maturity of your Securities, which should be long-term if you hold your Securities for more than one year, in an amount equal to the difference between the amount you receive at such time and the amount you paid for your Securities.

In the opinion of our counsel, Cadwalader, Wickersham & Taft LLP, it would be reasonable to treat your Securities in the manner described above. However, because there is no authority that specifically addresses the tax treatment of the Securities, it is possible that your Securities could alternatively be treated for tax purposes in the manner described under “Supplemental U.S. Tax Considerations — Alternative Treatments” on page PS-33 of the product supplement.

The Internal Revenue Service, for example, might assert that you should be required to recognize taxable gain on any rebalancing or rollover of any underlying index, including each time a contract traded by the short index rolls. It is also possible that the Internal Revenue Service could assert that Section 1256 of the Internal Revenue Code should apply to all or the portion of your Securities that reflects the performance of regulated futures contracts. If Section 1256 were to supply to all or such portion of your Securities, gain or loss recognized with respect to such portion of your Securities would be treated as 60% long-term capital gain or loss and 40% short-term capital gain or loss, without regard to your holding period in the Securities. You would also be required to mark such portion of your Securities to market at the end of each year (i.e., recognize gain or loss as if the relevant portion of the Securities had been sold for fair market value). There may also be a risk that the Internal Revenue Service could assert that the Securities should not give rise to long-term capital gain or loss because the Securities offer exposure to a short investment strategy. Moreover, it is possible that the Internal Revenue Service could successfully assert that the underlying index itself is a “straddle” and that all gain (and certain losses) would be short-term capital gain or loss. The deductibility of capital losses is subject to limitations.

In 2007, the Internal Revenue Service released a notice that may affect the taxation of holders of the Securities. According to the notice, the Internal Revenue Service and the Treasury Department are actively considering whether the holder of an instrument similar to the Securities should be required to accrue ordinary income on a current basis, and they are seeking taxpayer comments on the subject. It is not possible to determine what guidance they will ultimately issue, if any. It is possible, however, that under such guidance, holders of the Securities will ultimately be required to accrue income currently and this could be applied on a retroactive basis. The Internal Revenue Service and the Treasury Department are also considering other relevant issues, including whether additional gain or loss from such instruments should be treated as ordinary or capital, whether foreign holders of such instruments should be subject to withholding tax on any deemed income accruals, and whether the special “constructive ownership rules” of Section 1260 of the Internal Revenue Code of 1986, as amended (the “Code”) should be applied to such instruments. Holders are urged to consult their tax advisors concerning the significance, and the potential impact, of the above considerations. Except to the extent otherwise required by law, UBS intends to treat your Securities for United States federal income tax purposes in accordance with the treatment described above and under “Supplemental U.S. Tax Considerations” beginning on page PS-32 of the Relative Performance Securities product supplement, unless and until such time as the Treasury Department and the Internal Revenue Service determine that some other treatment is more appropriate.

Recent Legislation

Medicare Tax on Net Investment Income. Beginning in 2013, U.S. holders that are individuals, estates, and certain trusts will be subject to an additional 3.8% tax on all or a portion of their “net investment income,” which may include any gain realized with respect to the Securities, to the extent of their net investment income that when added to their other modified adjusted gross income, exceeds $200,000 for an unmarried individual, $250,000 for a married taxpayer filing a joint return (or a surviving spouse), or $125,000 for a married individual filing a separate return. U.S. holders should consult their tax advisors with respect to their consequences with respect to the 3.8% Medicare tax.

Specified Foreign Financial Assets. Under recently enacted legislation, individuals that own “specified foreign financial assets” may be required to file information with respect to such assets with their tax returns, especially if such assets are held outside the custody of a U.S. financial institution. You are urged to consult your tax adviser as to the application of this legislation to your ownership of the Securities.

Non U.S. Holders. Subject to Section 871(m) and FATCA (as discussed below), if you are not a United States holder, you should generally not be subject to United States withholding tax with respect to payments on your Securities or to generally applicable information reporting and backup withholding requirements with respect to payments on your Securities if you comply with certain certification and identification requirements as to your foreign status (by providing a fully completed and duly executed appropriate Internal Revenue Service Form W-8). Gain from the sale or exchange of a Security or settlement at maturity generally will not be subject to U.S. tax unless such gain is

9

effectively connected with a trade or business conducted by the non-U.S. holder in the United States or unless the non-U.S. holder is a non-resident alien individual and is present in the U.S. for 183 days or more during the taxable year of such sale, exchange or settlement and certain other conditions are satisfied.

Section 871(m) of the Code requires withholding (up to 30%, depending on the applicable treaty) on certain financial instruments to the extent that the payments or deemed payments on the financial instruments are contingent upon or determined by reference to U.S.-source dividends. Under proposed U.S. Treasury Department regulations, certain payments that are contingent upon or determined by reference to U.S. source dividends, including payments reflecting adjustments for extraordinary dividends, with respect to equity-linked instruments, including the Securities, may be treated as dividend equivalents. If enacted in their current form, the regulations may impose a withholding tax on payments made on the Securities on or after January 1, 2014 that are treated as dividend equivalents. In that case, we (or the applicable paying agent) would be entitled to withhold taxes without being required to pay any additional amounts with respect to amounts so withheld. Further, Non-U.S. Holders may be required to provide certifications prior to, or upon the sale, redemption or maturity of the Securities in order to minimize or avoid U.S. withholding taxes.

Foreign Account Tax Compliance Act. The Foreign Account Tax Compliance Act (“FATCA”) was enacted on March 18, 2010, and imposes a 30% U.S. withholding tax on “withholdable payments” (i.e., certain U.S. source payments, including interest (and OID), dividends, other fixed or determinable annual or periodical gain, profits, and income, and on the gross proceeds from a disposition of property of a type which can produce U.S. source interest or dividends) and “pass-thru payments” (i.e, certain payments attributable to withholdable payments) made to certain foreign financial institutions (and certain of their affiliates) unless the payee foreign financial institution agrees, among other things, to disclose the identity of any U.S. individual with an account of the institution (or the relevant affiliate) and to annually report certain information about such account. FATCA also requires withholding agents making withholdable payments to certain foreign entities that do not disclose the name, address, and taxpayer identification number of any substantial U.S. owners (or certify that they do not have any substantial United States owners) withhold tax at a rate of 30%. Under certain circumstances, a holder may be eligible for refunds or credits of such taxes.

Pursuant to final Treasury regulations published in the Federal Register on January 28, 2013, the withholding and reporting requirements will generally apply to certain withholdable payments made after December 31, 2013, certain gross proceeds on sale or disposition occurring after December 31, 2016, and certain pass-thru payments made after December 31, 2016. Pursuant to a recently issued Internal Revenue Service Notice, FATCA withholding on “withholdable payments” begins on July 1, 2014, and pursuant to this Notice, withholding tax under FATCA would not be imposed on payments pursuant to obligations that are outstanding on July 1, 2014 (and are not materially modified after June 30, 2014). If, however, withholding is required, we (and any paying agent) will not be required to pay additional amounts with respect to the amounts so withheld.

Significant aspects of the application of FATCA are not currently clear and the above description is based on proposed regulations and interim guidance. Investors should consult their own advisors about the application of FATCA, in particular if they may be classified as financial institutions under the FATCA rules.

PROSPECTIVE PURCHASERS OF SECURITIES SHOULD CONSULT THEIR TAX ADVISORS AS TO THE U.S. FEDERAL, STATE, LOCAL AND OTHER TAX CONSEQUENCES TO THEM OF THE PURCHASE, OWNERSHIP AND DISPOSITION OF THE SECURITIES.

10

Key Risks

An investment in the Securities involves significant risks. Some of the risks that apply to the Securities are summarized here, but we urge you to read the more detailed explanation of risks relating to the Securities generally in the “Risk Factors” section of the Relative Performance Securities product supplement. We also urge you to consult your investment, legal, tax, accounting and other advisers before you invest in the Securities.

| ¨ | Risk of loss — The Securities differ from ordinary debt securities in that UBS will not necessarily repay the full principal amount of the Securities. The return on the Securities at maturity is dependent on the relative return, which is the long index return minus the short index return. The outright performance levels of each underlying index are not individually relevant to the return on the Securities. You will not realize a positive return on your investment in the Securities unless the relative return is positive, whereas a negative relative return will result in the loss of some or all of your investment. A negative relative return will result any time that (i) both underlying indices appreciate but the short index appreciates by a greater percentage than the percentage that the long index appreciates, (ii) the long index depreciates while the short index remains flat or appreciates, (iii) the long index remains flat while the short index appreciates or (iv) both underlying indices depreciate but the long index depreciates by a greater percentage than the percentage that the short index depreciates. Consequently, you will lose some or all of your investment if the short index outperforms the long index over the term of the Securities. |

| ¨ | The participation rate applies only at maturity — You should be willing to hold your Securities to maturity. If you are able to sell your Securities prior to maturity in the secondary market, the price you receive will likely not reflect the full economic value of the participation rate or the Securities themselves and the return you realize may be less than the relative return even if such return is positive. You can receive the full benefit of the participation rate only if you hold your Securities to maturity. |

| ¨ | No interest payments — UBS will not pay any interest with respect to the Securities. |

| ¨ | Credit risk of UBS — The Securities are unsubordinated, unsecured debt obligations of UBS and are not, either directly or indirectly, an obligation of any third party. Any payment to be made on the Securities, including any repayment of principal, depends on the ability of UBS to satisfy its obligations as they come due. As a result, the actual and perceived creditworthiness of UBS may affect the market value of the Securities and, in the event UBS were to default on its obligations, you may not receive any amounts owed to you under the terms of the Securities and you could lose your entire initial investment. |

| ¨ | Market risk — The return on the Securities, which may be positive or negative, is directly linked to the performance of the long index relative to the short index and indirectly linked to the value of the stocks comprising the long index (“long index constituent stocks”) and the futures contracts comprising the short index (together with the long index constituent stocks, the “index components”) and will depend on whether, and the extent to which, the relative return is positive or negative. The levels of the underlying indices can rise or fall sharply due to factors specific to the underlying indices or the index components, such as price volatility, earnings, financial conditions, corporate, industry and regulatory developments, management changes and decisions and other events, as well as general market factors, such as general stock market or commodity market volatility and levels, interest rates and economic and political conditions. You may lose some or all of your principal amount if the relative return is negative. |

| ¨ | Fair value considerations. |

| ¨ | The issue price you pay for the Securities exceeds their estimated initial value — The issue price you pay for the Securities exceeds their estimated initial value as of the trade date due to the inclusion in the issue price of the underwriting discount, hedging costs, issuance costs and projected profits. As of the close of the relevant markets on the trade date, we have determined the estimated initial value of the Securities by reference to our internal pricing models and it is set forth in this final pricing supplement. The pricing models used to determine the estimated initial value of the Securities incorporate certain variables, including the price, volatility and expected dividends on the constituent stocks of the underlying indices, prevailing interest rates, the term of the Securities and our internal funding rate. Our internal funding rate is typically lower than the rate we would pay to issue conventional fixed or floating rate debt securities of a similar term. The underwriting discount, hedging costs, issuance costs, projected profits and the difference in rates will reduce the economic value of the Securities to you. Due to these factors, the estimated initial value of the Securities as of the trade date is less than the issue price you pay for the Securities. |

| ¨ | The estimated initial value is a theoretical price; the actual price that you may be able to sell your Securities in any secondary market (if any) at any time after the trade date may differ from the estimated initial value — The value of your Securities at any time will vary based on many factors, including the factors described above and in “— Market risk” above and is impossible to predict. Furthermore, the pricing models that we use are proprietary and rely in part on certain assumptions about future events, which may prove to be incorrect. As a result, after the trade date, if you attempt to sell the Securities in the secondary market, the actual value you would receive may differ, perhaps materially, from the estimated initial value of the Securities determined by reference to our internal pricing models. The estimated initial value of the Securities does not represent a minimum or maximum price at which we or any of our affiliates would be willing to purchase your Securities in any secondary market at any time. |

| ¨ | Our actual profits may be greater or less than the differential between the estimated initial value and the issue price of the Securities as of the trade date — We may determine the economic terms of the Securities, as well as hedge our obligations, at least in part, prior to the trade date. In addition, there may be ongoing costs to us to maintain and/or adjust any hedges and such hedges are often imperfect. Therefore, our actual profits (or potentially, losses) in issuing the Securities cannot be determined as of the trade date and any such differential between the estimated initial value and the issue price of the Securities as of the trade date does not reflect our actual profits. Ultimately, our actual profits will be known only at the maturity of the Securities. |

11

| ¨ | Limited or no secondary market and secondary market price considerations. |

| ¨ | There may be little or no secondary market for the Securities — The Securities will not be listed or displayed on any securities exchange or any electronic communications network. There can be no assurance that a secondary market for the Securities will develop. UBS Securities LLC and its affiliates may make a market in the Securities, although they are not required to do so and may stop making a market at any time. If you are able to sell your Securities prior to maturity, you may have to sell them at a substantial loss. The estimated initial value of the Securities does not represent a minimum or maximum price at which we or any of our affiliates would be willing to purchase your Securities in any secondary market at any time. |

| ¨ | The price at which UBS Securities LLC and its affiliates may offer to buy the Securities in the secondary market (if any) may be greater than UBS’ valuation of the Securities at that time, greater than any other secondary market prices provided by unaffiliated dealers (if any) and, depending on your broker, greater than the valuation provided on your customer account statements — For a limited period of time following the issuance of the Securities, UBS Securities LLC or its affiliates may offer to buy or sell such Securities at a price that exceeds (i) our valuation of the Securities at that time based on our internal pricing models, (ii) any secondary market prices provided by unaffiliated dealers (if any) and (iii) depending on your broker, the valuation provided on customer account statements. The price that UBS Securities LLC may initially offer to buy such Securities following issuance will exceed the valuations indicated by our internal pricing models due to the inclusion for a limited period of time of the aggregate value of the underwriting discount, hedging costs, issuance costs and theoretical projected trading profit. The portion of such amounts included in our price will decline to zero on a straight line basis over a period ending no later than the date specified under “Supplemental Plan of Distribution (Conflicts of Interest); Secondary Market (if any).” Thereafter, if UBS Securities LLC or an affiliate makes secondary markets in the Securities, it will do so at prices that reflect our estimated value determined by reference to our internal pricing models at that time. The temporary positive differential relative to our internal pricing models arises from requests from and arrangements made by UBS Securities LLC with the selling agents of structured debt securities such as the Securities. As described above, UBS Securities LLC and its affiliates are not required to make a market for the Securities and may stop making a market at any time. The price at which UBS Securities LLC or an affiliate may make secondary markets at any time (if at all) will also reflect its then current bid-ask spread for similar sized trades of structured debt securities. UBS Financial Services Inc. and UBS Securities LLC reflect this temporary positive differential on their customer statements. Investors should inquire as to the valuation provided on customer account statements provided by unaffiliated dealers. |

| ¨ | Price of Securities prior to maturity — The market price of the Securities will be influenced by many unpredictable and interrelated factors, including the levels of the underlying indices; the correlation between the underlying indices; the volatility of the underlying indices; the dividend rate paid on the underlying indices’ constituent stocks; the time remaining to the maturity of the Securities; interest rates in the markets; geopolitical conditions and economic, financial, political, force majeure and regulatory or judicial events; the creditworthiness of UBS and the then current bid-ask spread for the Securities. |

| ¨ | Impact of fees and the use of internal funding rates rather than secondary market credit spreads on secondary market prices — All other things being equal, the use of the internal funding rates described above under “— Fair value considerations” as well as the inclusion in the issue price of the underwriting discount, hedging costs, issuance costs and any projected profits are, subject to the temporary mitigating effect of UBS Securities LLC’s and its affiliates’ market making premium, expected to reduce the price at which you may be able to sell the Securities in any secondary market. |

| ¨ | The payment at maturity on your Securities is not based on the levels of the underlying indices at any time other than the final valuation date — The final index levels and the relative return will be based solely on the closing levels of the underlying indices on the final valuation date (subject to adjustments as described in the product supplement). Therefore, if the level of one or both of the underlying indices moves precipitously on the final valuation date to negatively impact the relative return, the payment at maturity on your Securities, if any, may be significantly less than it would otherwise have been had the payment at maturity been linked to the levels of the underlying indices at a time prior to such movement. Although the level of one or both of the underlying indices on the maturity date or at other times during the life of your Securities may reflect greater outperformance of the long index relative to the short index than on the final valuation date, you will not benefit from the level of the underlying indices at any time other than the final valuation date. |

| ¨ | The Securities do not represent an investment in a basket of the underlying indices — The Securities do NOT represent an investment in a basket of the underlying indices. If the short index return exceeds the long index return, the relative return will be negative and you will lose some or all of your principal, regardless of the outright performance of each of the underlying indices. The benefit to you of any increase in the level of the long index may be offset or negated entirely by increases in the level of the short index. You will not benefit from any increase in the level of the short index, regardless of the performance of the long index. In addition, a decline in the level of the short index may not benefit you unless the long index declines by a lesser amount as the return on the Securities is dependent on the relative performance of the underlying indices. |

| ¨ | You will not have rights in the 5 year treasury futures — The short index reflects the returns available by maintaining a rolling position in 5 year U.S. Treasury Notes futures contracts (the “5 year Treasury futures” and each, a “5 year Treasury futures contract”). At any given time, the short index is comprised of a single 5 year Treasury futures contract that is either the contract closest to expiration (the “near month futures contract”), or the next 5 year Treasury futures contract scheduled to expire immediately following the near month futures contract (the “far month futures contract”). The short index maintains its exposure to 5 year Treasury futures by closing out its position in the expiring near month futures contract and establishing a new position in the far month futures contract, a process referred to as “rolling.” Sale prices for contracts with later expiration dates that are higher or lower than the sale prices for contracts expiring earlier could significantly affect the level of the short index, and therefore, the payment at maturity. Further, any roll yield |

12

| generated from rolling may also impact the level of the short index. Investing in the Securities is not equivalent to investing directly in a succession of 5 year Treasury futures, and you will not have rights that investors in 5 year Treasury futures may have. |

| ¨ | Owning the Securities is not the same as owning the long index constituent stocks — Owning the Securities is not the same as owning the long index constituent stocks. As a holder of the Securities, you will not have voting rights or rights to receive dividends or other distributions or other rights that holders of stocks included in the long index would have. |

| ¨ | No assurance that the investment view implicit in the Securities will be successful — It is impossible to predict whether and the extent to which the level of the underlying indices will rise or fall. There can be no assurance that the level of the long index will outperform short index. The final index levels of the underlying indices will be influenced by complex and interrelated political, economic, financial and other factors that affect the index components. You should be willing to accept the risks associated with the relevant markets tracked by the underlying indices in general and the index components in particular, and the risk of losing some or all of your initial investment. |

| ¨ | Changes that affect the underlying indices will affect the market value of your Securities and the amount you will receive at maturity of your Securities — The policies of any sponsor of the underlying indices (an “index sponsor”) concerning the calculation of the underlying indices, additions, deletions or substitutions of the index components and the manner in which changes affecting the index components, the issuers of the long index constituent stocks (such as stock dividends, reorganizations or mergers) or the futures contracts comprising the short index (such as prolonged changes in market value, significantly decreased liquidity or if any such futures contract ceases to exist) are reflected in the underlying indices, could affect the levels of the underlying indices and, therefore, could affect the amount payable on your Securities at maturity and the market value of your Securities prior to maturity. The amount payable on the Securities and their market value could also be affected if an index sponsor changes these policies, for example by changing the manner in which it calculates the long index or short index, or if an index sponsor discontinues or suspends calculation or publication of any of the underlying indices, in which case it may become difficult to determine the market value of the Securities. If events such as these occur, or if the final index level is not available because of a market disruption event or for any other reason, and no successor index is selected, the calculation agent — which initially will be UBS Securities LLC, an affiliate of UBS — may determine the final index level — and thus the amount payable at maturity — in a manner it considers appropriate. |

| ¨ | Historical and hypothetical back-tested performance of the short index should not be taken as an indication of the future performance of the short index — It is impossible to predict whether the underlying indices will rise or fall. The actual future performance of the underlying indices may bear little relation to the historical or hypothetical back-tested levels of the underlying indices. Any information regarding the performance of the short index prior to August 11, 2010 is hypothetical and back-tested. Any back-tested index levels are based solely on back-tested simulation, are derived with the benefit of hindsight and are provided for illustrative purposes only. They represent a calculation of the past performance of the short index based on its methodology and certain data, assumptions and estimates, not all of which may be specified herein, and which may be different from the data, assumptions and estimates that someone else might use to calculate the short index. Simulation based on different assumptions or for a different historical period may produce different results. Any hypothetical back-tested or historical index levels should not be taken as an indication of the future performance of the short index. Any upward or downward trend in the hypothetical back-tested index levels or the historical index levels during any period is not an indication that such index level is more or less likely to increase or decrease in the future. |

| ¨ | UBS cannot control actions by the index sponsors and the index sponsors have no obligation to consider your interests — UBS and its affiliates are not affiliated with the index sponsors and have no ability to control or predict their actions, including any errors in or discontinuation of public disclosure regarding methods or policies relating to the calculation of the underlying indices. The index sponsors are not involved in the Securities offering in any way and have no obligation to consider your interest as an owner of the Securities in taking any actions that might affect the market value of your Securities. |

| ¨ | The underlying indices reflect price return, not total return — The return on your Securities is based on the performances of the underlying indices, which reflect the changes in the market prices of the long index constituent stocks and futures contracts comprising the short index. It is not, however, linked to a “total return” index or strategy, which, in addition to reflecting those price returns, would also reflect dividends paid on the long index constituent stocks. The return on your Securities will not include such a total return feature or dividend component. |

| ¨ | Potential UBS impact on price — Trading or transactions by UBS or its affiliates in the long index constituent stocks and/or over-the-counter options, futures or other instruments with returns linked to the performance of one or both of the underlying indices may adversely affect the performance and, therefore, the market value of the Securities. |

| ¨ | Potential conflict of interest — UBS and its affiliates may engage in business related to the underlying indices, the long index constituent stocks or the futures contracts comprising the short index, which may present a conflict between the obligations of UBS and you, as a holder of the Securities. The calculation agent, an affiliate of UBS, will determine the relative return and the payment at maturity based on the closing level of the long index in relation to the closing level of the short index on the final valuation date. The calculation agent can postpone the determination of the relative return or the maturity date if a market disruption event occurs and is continuing on the final valuation date. As UBS determines the economic terms of the Securities, including the participation rate and such terms include hedging costs, issuance costs and projected profits, the Securities represent a package of economic terms. There are other potential conflicts of interest insofar as an investor could potentially get better economic terms if that investor entered into exchange-traded and/or OTC derivatives or other instruments with third parties, assuming that such instruments were available and the investor had the ability to assemble and enter into such instruments. |

13

| ¨ | Potentially inconsistent research, opinions or recommendations by UBS — UBS and its affiliates publish research from time to time on financial markets, commodity markets and other matters that may influence the value of the Securities, or express opinions or provide recommendations that are inconsistent with purchasing or holding the Securities. Any research, opinions or recommendations expressed by UBS or its affiliates may not be consistent with each other and may be modified from time to time without notice. Investors should make their own independent investigation of the merits of investing in the Securities and the underlying indices to which the Securities are linked. |

| ¨ | Dealer incentives — UBS and its affiliates act in various capacities with respect to the Securities. We and our affiliates may act as a principal, agent or dealer in connection with the sale of the Securities. Such affiliates, including the sales representatives, will derive compensation from the distribution of the Securities and such compensation may serve as an incentive to sell these Securities instead of other investments. We will pay total underwriting compensation in an amount equal to the underwriting discount listed on the cover hereof per Security to any of our affiliates acting as agents or dealers in connection with the distribution of the Securities. Given that UBS Securities LLC and its affiliates temporarily maintain a market making premium, it may have the effect of discouraging UBS Securities LLC and its affiliates from recommending sale of your Securities in the secondary market. |

| ¨ | Uncertain tax treatment — Significant aspects of the tax treatment of the Securities are uncertain. You should consult your tax advisor about your own tax situation. See “What Are the Tax Consequences of the Securities” beginning on page 9. |

14

S&P 500® Index

We have derived all information contained in this final pricing supplement regarding the S&P 500® Index, including without limitation, its make-up, method of calculation and changes in its components from publicly available information. Such information reflects the policies of, and is subject to change by Standard & Poor’s Financial Services LLC, a subsidiary of The McGraw-Hill Companies, Inc. (“S&P”). UBS has not conducted any independent review or due diligence of any publicly available information with respect to the S&P 500® Index.

S&P has no obligation to continue to publish the S&P 500® Index, and may discontinue publication of the S&P 500® Index at any time. The S&P 500® Index is determined, comprised and calculated by S&P without regard to the Securities.

The S&P 500® Index is published by S&P. As discussed more fully in the index supplement under the heading “Underlying Indices and Underlying Index Publishers — S&P 500® Index”, the S&P 500® Index is intended to provide an indication of the pattern of common stock price movement. The calculation of the value of the S&P 500® Index is based on the relative value of the aggregate market value of the common stock of 500 companies as of a particular time compared to the aggregate average market value of the common stocks of 500 similar companies during the base period of the years 1941 through 1943. Ten main groups of companies comprise the S&P 500® Index, with the number of companies included in each group as of September 30, 2013 indicated below: Consumer Discretionary (83); Consumer Staples (40); Energy (43); Financials (81); Health Care (55); Industrials (63); Information Technology (67); Materials (31); Telecommunications Services (6) and Utilities (31).

Information from outside sources is not incorporated by reference in, and should not be considered part of, this final pricing supplement or any accompanying prospectus. UBS has not conducted any independent review or due diligence of any publicly available information with respect to the S&P 500® Index.

Historical Information

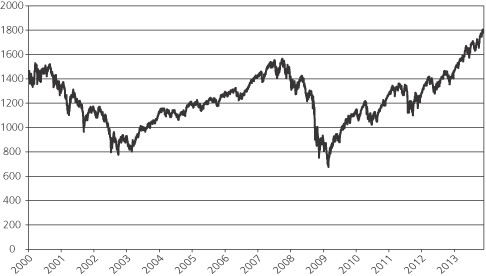

The following table sets forth the quarterly high and low closing levels for the S&P 500® Index, based on the daily closing level as reported by Bloomberg Professional service (“Bloomberg”), without independent verification. UBS has not conducted any independent review or due diligence of publicly available information obtained from Bloomberg. The closing level of the S&P 500® Index on November 25, 2013 was 1,802.48. Past performance of the underlying index is not indicative of the future performance of the underlying index.

| Quarter Begin | Quarter End | Quarterly High | Quarterly Low | Quarterly Close | ||||

| 1/2/2009 | 3/31/2009 | 934.70 | 676.53 | 797.87 | ||||

| 4/1/2009 | 6/30/2009 | 946.21 | 811.08 | 919.32 | ||||

| 7/1/2009 | 9/30/2009 | 1,071.66 | 879.13 | 1,057.08 | ||||

| 10/1/2009 | 12/31/2009 | 1,127.78 | 1,025.21 | 1,115.10 | ||||

| 1/4/2010 | 3/31/2010 | 1,174.17 | 1,056.74 | 1,169.43 | ||||

| 4/1/2010 | 6/30/2010 | 1,217.28 | 1,030.71 | 1,030.71 | ||||

| 7/1/2010 | 9/30/2010 | 1,148.67 | 1,022.58 | 1,141.20 | ||||

| 10/1/2010 | 12/31/2010 | 1,259.78 | 1,137.03 | 1,257.64 | ||||

| 1/3/2011 | 3/31/2011 | 1,343.01 | 1,256.88 | 1,325.83 | ||||

| 4/1/2011 | 6/30/2011 | 1,363.61 | 1,265.42 | 1,320.64 | ||||

| 7/1/2011 | 9/30/2011 | 1,353.22 | 1,119.46 | 1,131.42 | ||||

| 10/3/2011 | 12/30/2011 | 1,285.09 | 1,099.23 | 1,257.60 | ||||

| 1/3/2012 | 3/30/2012 | 1,416.51 | 1,277.06 | 1,408.47 | ||||

| 4/2/2012 | 6/30/2012 | 1,419.04 | 1,278.04 | 1,362.16 | ||||

| 7/2/2012 | 9/28/2012 | 1,465.77 | 1,334.76 | 1,440.67 | ||||

| 10/1/2012 | 12/31/2012 | 1,461.40 | 1,353.33 | 1,426.19 | ||||

| 1/2/2013 | 3/29/2013 | 1,569.19 | 1,457.15 | 1,569.19 | ||||

| 4/1/2013 | 6/28/2013 | 1,669.16 | 1,541.61 | 1,606.28 | ||||

| 7/1/2013 | 9/30/2013 | 1,725.52 | 1,614.08 | 1,681.55 | ||||

| 10/1/2013* | 11/25/2013* | 1,804.76 | 1,655.45 | 1,802.48 |

| * | As of the date of this final pricing supplement, available information for the fourth calendar quarter of 2013 includes data for the period from October 1, 2013 through November 25, 2013. Accordingly, the “Quarterly High,” “Quarterly Low” and “Quarterly Close” data indicated are for this shortened period only and do not reflect complete data for the fourth calendar quarter of 2013. |

15

The graph below illustrates the performance of the S&P 500® Index from January 3, 2000 through November 25, 2013, based on information from Bloomberg. Past performance of the underlying index is not indicative of the future performance of the underlying index.

PAST PERFORMANCE IS NOT INDICATIVE OF FUTURE RESULTS.

16

NYSE US 5 Year Treasury Futures Index

The NYSE US 5 Year Treasury Futures Index is a one-security futures index that aims to replicate the returns of maintaining a continuous rolling long position in 5 year US Treasury Notes futures contracts (the “5 year Treasury futures” and each, a “5 year Treasury futures contract”). The short index is maintained and calculated by NYSE Arca (the “short index sponsor”) and is denominated in U.S. dollars. The level of the short index is deemed to have been 100 on February 26, 1999, which is referred to as the “index commencement date”. The short index sponsor began calculating the short index on August 11, 2010. 5 year Treasury futures are legally binding agreements for the buying or selling of U.S. Treasury notes at a fixed price for physical settlement on a future date. Each 5 year Treasury futures contract has a face value of $100,000 and requires the delivery of a U.S. Treasury bond with an original maturity term of no more than five years and three months and a remaining maturity of no less than four years and two months as of the first day of the delivery month. 5 year Treasury futures are traded on the Chicago Board of Trade (“CBOT”). The closing prices of 5 year Treasury futures are calculated by CBOT and reported on Bloomberg under symbol “FV”. As used herein, an “index business day” means any day that CBOT is scheduled to be open for trading.

At any given time, the short index is comprised of a single 5 year Treasury futures contract that is either the contract closest to expiration (the “near month futures contract”) or the next 5 year Treasury futures contract scheduled to expire immediately following the near month futures contract (the “far month futures contract”). The short index maintains its exposure to 5 year Treasury futures by closing out its position in the expiring near month futures contract and establishing a new position in the far month futures contract, a process referred to as “rolling.” The roll takes place through a rebalance that is effective for the last trading day of the month prior to that in which the near month futures contract expires each quarter. The short index rebalance consists of the notional value of the near month futures contract being reinvested into the far month futures contract. The roll occurs at the settlement prices of both the near month futures contracts and the far month futures contracts on the second to last trading day of the month prior to that of the near month futures contract’s expiration.

The opening level of the short index is calculated using the current last trade of the futures contract held in the short index or in the case of futures contracts that have a non-traded status, the previous day’s settlement price. The opening level of the short index will be the first published index level for the day. The short index sponsor calculates and maintains intraday real-time index levels which are published to the US Consolidated Tape B under the index symbol USTFIV between the hours of 8:00 AM and 6:00 PM ET each trading day that is an index business day; however, the short index is not calculated on days that either A) the CBOT is closed for regular session trading or B) the NYSE is closed for equity trading. On days that the CBOT is closed and the NYSE open, the exchange publishes out a static previous index close during equity trading hours. NYSE Arca calculates and publishes an official closing index value on each trading day between approximately 3:00 PM and 4:00 PM ET. The short index is fixed at that official close (to two decimal places) for the remainder of the day. The official index close is calculated based off of the CBOT 5 year Futures Contract’s settlement price which is determined and disseminated shortly after the end of the core trading session at 3 PM ET.

Calculation of the Short Index

The level of the short index is deemed to have been 100 on February 26, 1999, which we refer to as the “index commencement date”.

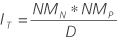

On any given index business day, the level of the short index is equal to:

where:

“IT” means the index level of the short index on Day T;

“T” means the day of calculation;

“NMN” means the number of contracts of the near month futures in the short index; and

“NMP” means, for an intraday calculation, the last trade of the 5 year Treasury futures contract and, for a closing calculation, the settlement price of the 5 year Treasury futures contract; and

“D” means the index divisor, which is fixed at 1,000,000

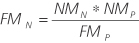

The short index is rebalanced and rolled into the far month futures contract using the following formula:

17

where:

“FMn” means number of new far month futures contracts to be held in the short index after the rebalancing;

“NMN” means the number of near month futures contracts held in the short index before the rebalancing; and

“NMP” means the settlement price of the far month futures contract on the trading day preceding the effective date of the rebalancing.

Exceptional Market Conditions and Corrections

NYSE Arca retains the right to delay the publication of the opening levels of the short index. Furthermore, NYSE Arca retains the right to suspend the publication of the level of the short index if it believes that circumstances prevent the proper calculation of the short index. These circumstances include, but are not limited to, the CBOT being closed for US Treasury Futures trading or the relevant index-held futures contract being in a suspended or halted state. If trades or futures settlement prices are cancelled or revised, the short index will be recalculated at the discretion of NYSE Arca.

Announcement Policy

Changes to the short index, its component futures contract or its rules will be announced by an index announcement which will be distributed via e-mail and/or the website of NYSE Euronext. As a rule the announcement periods that are mentioned underneath will be applied. However, urgent treatments or late notices may require the NYSE Arca to deviate from the standard timing.

The inclusion of a new Futures Contract through a Rebalance or Roll will be announced at least 3 trading days before the actual inclusion or effective date. Barring exception, a period of at least three months should pass between the date a proposed change is published and the date this comes into effect. Exceptions can be made if the change is not in conflict with the interests of an affected party.

Disclaimer

UBS has entered into a license agreement with NYSE Euronext, in exchange for a fee, whereby we are permitted to use the index in connection with the sale of the Securities.

The “NYSE US 5 Year Treasury Futures Index” is a service mark of NYSE Euronext or its affiliates (“NYSE Euronext”) and will be used with the permission of NYSE Euronext. NYSE Euronext in no way sponsors, endorses, or is otherwise involved in the transactions specified and described in this document (“Transaction”). NYSE Euronext makes no representations or warranties regarding UBS or the ability of the NYSE US 5 Year Treasury Futures Index to track general market performance.”

NYSE EURONEXT MAKES NO EXPRESS OR IMPLIED WARRANTIES, AND HEREBY EXPRESSLY DISCLAIMS ALL WARRANTIES OF MERCHANTABILITY OR FITNESS FOR A PARTICULAR PURPOSE WITH RESPECT TO THE NYSE US 5 YEAR TREASURY FUTURES INDEX OR ANY DATA INCLUDED THEREIN. IN NO EVENT SHALL NYSE EURONEXT HAVE ANY LIABILITY FOR ANY SPECIAL, PUNITIVE, INDIRECT, OR CONSEQUENTIAL DAMAGES (INCLUDING LOST PROFITS), EVEN IF NOTIFIED OF THE POSSIBILITY OF SUCH DAMAGES.

Hypothetical Historical and Historical Performance of the Short Index

The level of the short index is deemed to have been 100 on February 26, 1999, which is referred to as the “index commencement date”. The short index sponsor began calculating the short index on August 11, 2010. Therefore, the historical information, including such information provided in the table and graph below, for the period from February 26, 1999 until August 11, 2010, is an historical estimate by the short index sponsor using available data as an illustration of how the short index would have performed during the period had the short index sponsor begun calculating the short index on the index commencement date using the methodology it currently uses. This data does not reflect actual performance, nor was a contemporaneous investment model run of the short index. Historical information for the period from and after August 11, 2010 is based on the actual performance of the short index.

All calculations of historical information are based on information obtained from various third party independent and public sources. UBS has not independently verified the information extracted from these sources.

18

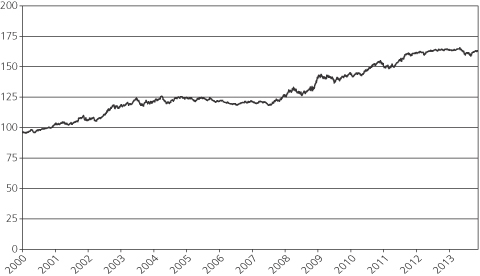

The following table and graph illustrate the performance of the short index from the index commencement date to November 25, 2013. Neither the estimated historical performance of the short index (for the period from February 26, 1999 until August 11, 2010) nor the actual historical performance of the short index (from the period after August 11, 2010) should be taken as an indication of future performance; no assurance can be given as to the closing level on any day during the term of the Securities, including on the final valuation date. We cannot give you assurance that the performance of the NYSE 5 Year Treasury Futures index will be less than the performance of the S&P 500® index, and therefore we cannot assure you of the return of any of your initial investment.

| Date |

Level of the Short index | |

| February 26, 1999 | 100.00 | |

| December 31, 1999 | 96.67 | |

| December 29, 2000 | 102.54 | |

| December 31, 2001 | 106.63 | |

| December 31, 2002 | 118.88 | |

| December 31, 2003 | 121.65 | |

| December 31, 2004 | 124.30 | |

| December 30, 2005 | 122.07 | |

| December 29, 2006 | 120.49 | |

| December 31, 2007 | 126.52 | |

| December 31, 2008 | 141.98 | |

| December 31, 2009 | 141.67 | |

| December 31, 2010 | 150.15 | |

| December 30, 2011 | 161.62 | |

| December 31, 2012 | 164.17 | |

| November 25, 2013 | 163.08 |

PAST PERFORMANCE IS NOT INDICATIVE OF FUTURE RESULTS.

19

Supplemental Plan of Distribution (Conflicts of Interest); Secondary Markets (if any)

We have agreed to sell to UBS Financial Services Inc. and certain of its affiliates, together the “Agents,” and the Agents have agreed to purchase, all of the Securities at the issue price less the underwriting discount indicated on the cover of this final pricing supplement, the document filed pursuant to Rule 424(b) containing the final pricing terms of the Securities. The Securities will be issued pursuant to a distribution agreement substantially in the form attached as an exhibit to the registration statement of which the accompanying prospectus forms a part. The Agents intend to resell the offered Securities at the original issue price to the public. The Agents may resell the Securities to securities dealers (“Dealers”) at a discount from the original issue price to the public up to the underwriting discount indicated on the cover of this final pricing supplement.

Conflicts of Interest — Each of UBS Securities LLC and UBS Financial Services Inc. is an affiliate of UBS and, as such, has a “conflict of interest” in this offering within the meaning of FINRA Rule 5121. In addition, UBS will receive the net proceeds (excluding the underwriting discount) from the initial public offering of the Securities, thus creating an additional conflict of interest within the meaning of Rule 5121. Consequently, the offering is being conducted in compliance with the provisions of Rule 5121. Neither UBS Securities LLC nor UBS Financial Services Inc. is permitted to sell Securities in this offering to an account over which it exercises discretionary authority without the prior specific written approval of the account holder.

UBS Securities LLC and its affiliates may offer to buy or sell the Securities in the secondary market (if any) at prices greater than UBS’ internal valuation — The value of the Securities at any time will vary based on many factors that cannot be predicted. However, the price (not including UBS Securities LLC or any affiliate’s customary bid-ask spreads) at which UBS Securities LLC or any affiliate would offer to buy or sell the Securities immediately after the trade date in the secondary market is expected to exceed the estimated initial value of the Securities as determined by reference to our internal pricing models. The amount of the excess will decline to zero on a straight line basis over a period ending no later than 12 months after the trade date, provided that UBS Securities LLC may shorten the period based on various factors, including the magnitude of purchases and other negotiated provisions with selling agents. Notwithstanding the foregoing, UBS Securities LLC and its affiliates are not required to make a market for the Securities and may stop making a market at any time. For more information about secondary market offers and the estimated initial value of the Securities, see “Key Risks — Fair value considerations” and “Key Risks — Limited or no secondary market and secondary market price considerations” on pages 11 and 12 of this final pricing supplement.

Structured Product Categorization

To help investors identify appropriate Structured Products (“Structured Products”), UBS organizes its Structured Products into four categories: Protection Strategies, Optimization Strategies, Performance Strategies and Leverage Strategies. The Securities are classified by UBS as a Performance Strategy for this purpose. The description below is intended to describe generally the four categories of Structured Products and the types of principal repayment features that may be offered on those products. This description should not be relied upon as a description of any particular Structured Product.

| ¨ | Protection Strategies are structured to complement and provide the potential to outperform traditional fixed income instruments. These Structured Products are generally designed for investors with low to moderate risk tolerances, but who can tolerate downside market risk prior to maturity. |

| ¨ | Optimization Strategies provide the opportunity to enhance market returns or yields and can be structured with full downside market exposure or with buffered or contingent downside market exposure. These structured products are generally designed for investors who can tolerate downside market risk. |

| ¨ | Performance Strategies provide efficient access to markets and can be structured with full downside market exposure or with buffered or contingent downside market exposure. These structured products are generally designed for investors who can tolerate downside market risk. |

| ¨ | Leverage Strategies provide leveraged exposure to the performance of an underlying asset. These Structured Products are generally designed for investors with high risk tolerances. |

In order to benefit from any type of principal repayment feature, investors must hold the Securities to maturity.

Classification of Structured Products into categories is for informational purposes only and is not intended to guarantee particular results or performance.

20