Table of Contents

The information in this Preliminary Product Supplement and Preliminary Pricing Supplement is not complete and may be changed. We may not sell these Securities, until the Preliminary Product Supplement, Preliminary Pricing Supplement and the Prospectus (collectively, the “Offering Documents”) are delivered in final form. The Offering Documents are not an offer to sell these Securities, and we are not soliciting offers to buy these Securities, in any State where the offer or sale is not permitted.

|

|

SUBJECT TO COMPLETION PRELIMINARY PRICING SUPPLEMENT Filed Pursuant to Rule 424(b)(3) Registration Statement No. 333-178960 Dated May 15, 2012 |

UBS AG Fisher Enhanced Big Cap Growth Securities

Linked to the Russell 1000® Growth Index Total Return

UBS AG $[·] Securities Linked to the Russell 1000® Growth Index Total Return due on or about May 28, 2013

Investment Description

Fisher Enhanced Big Cap Growth Securities (the “Securities”) are unsubordinated, unsecured debt securities issued by UBS AG (“UBS”) with returns linked to the performance of the Russell 1000® Growth Index Total Return (the “underlying index”). The Securities are designed to replicate a leveraged, double-long position in the underlying index. At maturity, you will receive a cash payment per Security equal to $25.00 plus a return equal to (i) double the index return minus the index adjustment factor minus (ii) a redemption fee upon an early redemption, subject to the occurrence of a rebalance event. The Securities will be subject to automatic early redemption if the underlying index level during any trading day during the period from, but excluding, the trade date to, and including the final valuation date is less than the early redemption level (an “early redemption event”). The terms of the Securities may also be adjusted if the underlying index level during any trading day during the period from, but excluding, the trade date to, and including the final valuation date falls below the rebalance trigger (a “rebalance event”). Investors will not receive any interest payments during the term of the Securities. Investing in the Securities involves significant risks. In addition to being subject to the index adjustment factor, a redemption fee upon an early redemption and a principal amount reduction upon a rebalance event, you will participate in any negative performance of the underlying index on a two-times leveraged basis and may lose your entire investment in the Securities. You will have a loss on your investment if the index return is negative or not sufficiently positive to offset the effect of these fees and other reductions. Any payment on the Securities is subject to the creditworthiness of UBS. If UBS were to default on its payment obligations you may not receive any amounts owed to you under the Securities and you could lose your entire investment.

The Securities are intended for sophisticated investors. Accordingly, the Securities should be purchased only by knowledgeable investors who understand the potential consequences of investing in leveraged investments. Investors should actively and frequently monitor their investments in the Securities, even intraday.

Features

| q | Leveraged Exposure: The Securities provide an opportunity for leveraged participation in any positive index return, if held to maturity. However, the Securities do not guarantee any repayment of principal, and you will be exposed to a leveraged multiple of any negative index return and will also be subject to the index adjustment factor, a redemption fee upon an early redemption and a principal amount reduction upon a rebalance event. If the index return is positive, but the increase in the level of the underlying index is insufficient to offset these fees and other reductions, you will have a loss on your investment in the Securities. |

| q | Early Redemption Event: UBS will automatically call the Securities early if the underlying index level at any time during the period from, but excluding, the trade date to, and including the final valuation date is less than the early redemption level. An early redemption event caused by a breach of the early redemption level would likely result in the loss of a substantial portion, or all, of your principal amount. |

| q | Optional Early Redemption: You may also elect to have UBS redeem the Securities early during the optional redemption period provided you comply with the optional early redemption requirements detailed on page 7. |

| q | Rebalance Event: The terms of the Securities may also be adjusted if the underlying index level at any time at which a market disruption event is not occurring on any trading day is less than the rebalance trigger and an early redemption event has not occurred. A rebalance event will cause a deleveraging of the Securities, a principal reduction to be incurred and may adversely affect you. |

NOTICE TO INVESTORS: THE SECURITIES ARE SIGNIFICANTLY RISKIER THAN CONVENTIONAL DEBT INSTRUMENTS. THE ISSUER IS NOT NECESSARILY OBLIGATED TO REPAY THE FULL PRINCIPAL AMOUNT OF THE SECURITIES AT MATURITY, AND THE SECURITIES HAVE A LEVERAGE FACTOR WHICH DOUBLES THE MARKET RISK OF THE UNDERLYING INDEX. THIS LEVERAGE RISK IS IN ADDITION TO THE CREDIT RISK INHERENT IN PURCHASING A DEBT OBLIGATION OF UBS. YOU SHOULD NOT PURCHASE THE SECURITIES IF YOU DO NOT UNDERSTAND OR ARE NOT COMFORTABLE WITH THE SIGNIFICANT RISKS INVOLVED IN INVESTING IN THE SECURITIES.

YOU SHOULD CAREFULLY CONSIDER THE RISKS DESCRIBED UNDER “KEY RISKS” BEGINNING ON PAGE 13 AND UNDER “RISK FACTORS” BEGINNING ON PAGE PS-15 OF THE FISHER ENHANCED BIG CAP GROWTH SECURITIES PRODUCT SUPPLEMENT BEFORE PURCHASING ANY SECURITIES. EVENTS RELATING TO ANY OF THOSE RISKS, OR OTHER RISKS AND UNCERTAINTIES, COULD ADVERSELY EFFECT THE MARKET VALUE OF, AND THE RETURN ON, YOUR SECURITIES. YOU MAY LOSE SOME OR ALL OF YOUR INITIAL INVESTMENT IN THE SECURITIES.

Security Offering

These terms relate to the Securities we are offering. Each of the Securities offered hereby is linked to the Russell 1000® Growth Index Total Return. The starting level will be set on the trade date.

| Underlying Index | Starting Level |

Term | Trade Date | Settlement Date | Final Valuation Date |

Maturity Date | CUSIP / ISIN | |||||||

| Russell 1000® Growth Index Total Return |

· | 53 weeks | May 16, 2012 | May 21, 2012 | May 22, 2013 | May 28, 2013 | 90268U176/ US90268U1768 |

See “Additional Information about UBS and the Securities” on page 2. The Securities will have the terms set forth in the Fisher Enhanced Big Cap Growth Securities product supplement relating to the Securities, the accompanying prospectus and this preliminary pricing supplement. See “Key Risks” on page 13 and the more detailed “Risk Factors” beginning on page PS-15 of the Fisher Enhanced Big Cap Growth Securities product supplement (the “product supplement”) relating to the Securities for risks related to an investment in the Securities.

Neither the Securities and Exchange Commission nor any other regulatory body has approved or disapproved of these Securities or passed upon the adequacy or accuracy of this preliminary pricing supplement, or the accompanying product supplement, index supplement or prospectus. Any representation to the contrary is a criminal offense. The Securities are not deposit liabilities of UBS AG and are not FDIC insured.

| Offering of Securities | Price to Public | Underwriting Compensation | Proceeds to UBS AG | |||||||||

| Total | Per Security | Total | Per Security | Total | Per Security | |||||||

| Securities Linked to the Russell 1000® Growth Index Total Return Index |

· | $25.00 | $0.00 | $0.00 | · | $25.00 | ||||||

| UBS Securities LLC | UBS Investment Bank |

Table of Contents

Additional Information about UBS and the Securities

UBS has filed a registration statement (including a prospectus, as supplemented by an index supplement and a product supplement for the Securities) with the Securities and Exchange Commission, or SEC, for the offerings to which this preliminary pricing supplement relates. Before you invest, you should read these documents and any other documents relating to these offerings that UBS has filed with the SEC for more complete information about UBS and this offering. You may obtain these documents without cost by visiting EDGAR on the SEC web site at www.sec.gov. Our Central Index Key, or CIK, on the SEC web site is 0001114446. Alternatively, UBS will arrange to send you the prospectus, the index supplement and the product supplement if you so request by calling toll-free 877-387-2275.

You may access these documents on the SEC web site at www.sec.gov as follows:

| ¨ | Index Supplement dated January 24, 2012: |

http://www.sec.gov/Archives/edgar/data/1114446/000119312512021889/d287369d424b2.htm

| ¨ | Prospectus dated January 11, 2012: |

http://www.sec.gov/Archives/edgar/data/1114446/000119312512008669/d279364d424b3.htm

References to “UBS”, “we”, “our” and “us” refer only to UBS AG and not to its consolidated subsidiaries. In this document, “Fisher Enhanced Big Cap Growth Securities” or the “Securities” refer to the Securities that are offered hereby. References to the “Fisher Enhanced Big Cap Growth Securities product supplement” or “product supplement” mean the accompanying UBS product supplement, dated May 15, 2012, references to the “index supplement” mean the UBS Index Supplement, dated January 24, 2012 and references to “accompanying prospectus” mean the UBS prospectus titled “Debt Securities and Warrants”, dated January 11, 2012.

This preliminary pricing supplement, together with the documents listed above, contains the terms of the Securities and supersedes all other prior or contemporaneous oral statements as well as any other written materials including preliminary or indicative pricing terms, correspondence, trade ideas, structures for implementation, sample structures, brochures or other educational materials of ours. You should carefully consider, among other things, the matters set forth in “Key Risks” beginning on page 13 and in “Risk Factors” in the accompanying product supplement, as the Securities involve risks not associated with conventional debt securities. We urge you to consult your investment, legal, tax, accounting and other advisers before deciding to invest in the Securities.

Investor Suitability

The suitability considerations identified above are not exhaustive. Whether or not the Securities are a suitable investment for you will depend on your individual circumstances, and you should reach an investment decision only after you and your investment, legal, tax, accounting and other advisors have carefully considered the suitability of an investment in the Securities in light of your particular circumstances. You should also review carefully the “Key Risks” beginning on page 13 of this preliminary pricing supplement for risks related to an investment in the Securities.

2

Table of Contents

Indicative Terms

3

Table of Contents

4

Table of Contents

Determining Payment at Maturity or upon an Early Redemption

|

Determine starting level, early redemption level and rebalance trigger |

Trade Date | |||

|

Valuation Date | |||

| Early Redemption or Optional Early Redemption |

|

If the Securities are subject to an early redemption event, the valuation date will be that trading day on which the calculation agent is scheduled to complete the computation of the ending level, subject to the occurrence of an index constituent market disruption event as described under “General Terms of the Securities — Market Disruption Event — Index Constituent Market Disruption Event” beginning on page PS-28 in the accompanying product supplement.

For avoidance of doubt, if an early redemption event occurs on or after the redemption notice date or final valuation date, the applicable valuation date and ending level will be determined in accordance with the early redemption event provisions.

If the Securities are subject to an optional early redemption and an early redemption event has not occurred, the valuation date will be (i) the trading day on which the calculation agent determines that conditions in the second paragraph of the definition of ending level are satisfied, subject to the occurrence of an underlying index market disruption event as described under “General Terms of the Securities — Market Disruption Event — Underlying Index Market Disruption Event” beginning on page PS-27 of the accompanying product supplement and (ii) the following scheduled trading day in all other cases, subject to the occurrence of an index constituent market disruption event as described under “General Terms of the Securities — Market Disruption Event — Index Constituent Market Disruption Event” beginning on page PS-28 of the accompanying product supplement. | ||

|

|

||||

| Maturity Date |

|

With respect to the maturity date, the valuation date will be the final valuation date, or the following trading day if such day is not a trading day, subject to the occurrence of an underlying index market disruption event as described under “General Terms of the Securities — Market Disruption Event — Underlying Index Market Disruption Event” beginning on page PS-27 in the accompanying product supplement. |

If a rebalance event occurs, the terms of the Securities may also be adjusted. A rebalance event will cause a deleveraging of the Securities, a fee to be incurred and may adversely affect you.

The redemption amount, if any, you will receive at maturity or upon an early redemption will be calculated as follows:

An amount equal to the sum of (i) the principal amount plus (ii) (a) the principal amount multiplied by the leverage factor multiplied by the (b) index return minus the index adjustment factor minus (iii) the redemption fee for an early redemption.

Expressed as a formula:

Principal Amount + [Principal Amount x Leverage Factor x (Index Return – Index Adjustment Factor)] – Redemption Fee for an early redemption.

Any negative redemption amount will be deemed to be equal to zero. Therefore, your maximum loss under the Securities is your initial investment.

Upon the occurrence of an early redemption event, the redemption amount you receive is likely to be significantly less than your initial investment in the Securities and could be zero.

In addition to being subject to the index adjustment factor, a redemption fee upon an early redemption and a principal amount reduction upon a rebalance event, you will participate in any negative performance of the underlying index on a two-times leveraged basis and may lose your entire investment in the Securities. Any payment on the Securities, including any repayment of principal, is subject to the creditworthiness of UBS. If UBS were to default on its payment obligations, you may not receive any amounts owed to you under the Securities and you could lose your entire investment.

Any payment on the Securities, including any repayment of principal, is subject to the creditworthiness of UBS. If UBS were to default on its payment obligations, you may not receive any amounts owed to you under the Securities and you could lose your entire investment.

5

Table of Contents

Early Redemption

Early Redemption Event

The Securities will be automatically redeemed early if the underlying index level at any time at which a market disruption event is not occurring on any trading day during the observation period is less than the early redemption level.

If the Securities are redeemed pursuant to an early redemption event, you will receive on the applicable early redemption settlement date, a cash payment per Security equal to the redemption amount, calculated as of the applicable valuation date. After your Securities are redeemed pursuant to an early redemption event, no further amounts will be owed to you under the Securities.

For the avoidance of doubt, if an early redemption event occurs on or after the first averaging date on which the calculation agent commences determining ending level, the applicable valuation date and ending level will be determined in accordance with the early redemption event provisions, as described under “General Terms of the Securities — Early Redemption Event” on page PS-24 of the accompanying product supplement.

In addition, if an early redemption event occurs on or after the redemption notice date, the applicable valuation date and ending level will be determined in accordance with the early redemption event provisions.

The amount payable under the Securities upon an early redemption will be substantially less than your initial investment and may even be zero. In addition the redemption amount is reduced by an index adjustment factor , a redemption fee and, if applicable, a principal amount reduction upon a rebalance event that reduces the overall return (or increases the loss) of the Securities. Moreover, the occurrence of an early redemption event will cut-off your ability to participate in any recovery of the underlying index subsequent to the early termination event.

Early Redemption Event Ending Level Determination Schedule

This early redemption event ending level determination schedule is used to set the time interval for determining the index constituent VWAP upon an early redemption event. Generally, the first VWAP period begins at the time that the early redemption event occurs (the “event time”) and ends on the market close on the first day T. Any second VWAP period begins on the market open on day T+1 and ends at the time indicated in the chart below. The index constituent VWAP is determined by taking the weighted average of these volume weighted average prices.

| Event Time: Time (t) of day (T) when underlying (New York City time) |

First VWAP Period: Weight of VWAP (or closing level as |

Second VWAP Period: Weight of VWAP on Day T+1 and (New York City time) | ||

| Occurs after 09:30 a.m., but on or before 12:00 p.m. | 100% | 0% | ||

| Occurs after 12:00 p.m., but on or before 1:00 p.m. | 80% | 20% ending at 11:00 a.m. | ||

| Occurs after 1:00 p.m., but on or before 2:00 p.m. | 60% | 40% ending at 12:00 p.m. | ||

| Occurs after 2:00 p.m., but on or before 3:00 p.m. | 40% | 60% ending at 1:00 p.m. | ||

| Occurs after 3:00 p.m., but before 3:40 p.m. |

20% based on the closing level of the underlying index | 80% ending at 1:00 p.m. | ||

| Occurs on or after 3:40 p.m. | 0% | 100% ending at 2:00 p.m. |

Optional Early Redemption

You may elect an optional early redemption, in whole or in part, on any business day during the optional redemption period.

For the avoidance of doubt, if an early redemption event occurs on or after the redemption notice date, the applicable valuation date and ending level will be determined in accordance with the early redemption event provisions.

The “optional redemption period” means the period from, and including, the first business day following the settlement date to, and including the business day that is two scheduled trading days prior to the earlier of the final valuation date and the occurrence of an early redemption event. You may only elect to redeem your Securities during the optional redemption period.

You must comply with the redemption procedures described below in order to redeem your Securities.

6

Table of Contents

Redemption Procedures

To redeem your Securities pursuant to an optional early redemption, you must instruct your broker or other person through whom you hold your Securities to take the following steps through normal clearing system channels:

(i) deliver a notice of redemption, which is attached to this preliminary pricing supplement as Annex A, to UBS via email no later than 12:00 noon (New York City time) on the business day immediately preceding your desired redemption settlement date. We or our affiliate must acknowledge receipt in order for your confirmation to be effective;

(ii) deliver to us via facsimile by 5:00 p.m. (New York City time) on the same day the signed confirmation of redemption which is attached to this preliminary pricing supplement as Annex B. We or our affiliate must acknowledge receipt in order for your confirmation to be effective;

(iii) instruct your DTC custodian to book a delivery vs. payment trade with respect to your Securities on the redemption settlement date at a price equal to the redemption amount; and

(iv) cause your DTC custodian to deliver the trade as booked for settlement via DTC at or prior to 10:00 a.m. (New York City time) on the redemption settlement date.

All instructions given to participants from beneficial owners of Securities relating to the right to redeem their Securities will be irrevocable.

Different brokerage firms may have different deadlines for accepting instructions from their customers. Accordingly, as a beneficial owner of the Securities, you should consult the brokerage firm through which you own your interest for the relevant deadline. If your broker delivers your notice of redemption after 12:00 noon (New York City time), or your confirmation of redemption after 5:00 p.m. (New York City time), on the applicable business day, your notice will not be effective and your broker will need to complete all the required steps if you should wish to redeem your Securities on any subsequent redemption date. In addition, UBS may request a medallion signature guarantee or such assurances of delivery as it may deem necessary in its sole discretion. All instructions given to participants from beneficial owners of Securities relating to the right to redeem their Securities will be irrevocable.

The calculation agent will resolve any questions that may arise as to the validity of a notice of redemption and the timing of receipt of a notice of redemption or as to whether and when the required deliveries have been made. Notwithstanding the forgoing, the calculation agent may waive the notice of redemption and confirmation of redemption (but not the 2:00p.m. (New York City deadline) for the initial owner of beneficial interests in the Securities (so long as it and continues to have custodial arrangements satisfactory UBS Securities LLC). Any such requests should be e-mailed to UBS Securities LLC at OL-EarlyRedemption@ubs.com. Until UBS Securities LLC affirmatively responds to such a waiver such requests will be deemed null and void.

Rebalance Event

If the underlying index level at any time at which a market disruption event is not occurring on any trading day is less than the rebalance trigger and an early redemption event has not occurred (a “rebalance event” and the related trading day on which it occurs, the “rebalance date”):

(i) As of the occurrence of the rebalance event, the Securities will be adjusted such that they will provide 25% less index unit exposure to the underlying index relative to the day preceding the rebalance date;

(ii) the adjusted redemption amount (until and if another redemption event occurs) as of any given day (t) will be determined by a modified redemption amount formula; and

(iii) the calculation agent will compute adjusted redemption amountt and make adjustments to early redemption level and rebalance trigger as described under “General Terms of the Securities — Rebalance Event” on page PS-24.

Rebalance events can occur successively; that is the underlying index can fall to the rebalance trigger and be reset; the underlying index can then fall further to the reset rebalance trigger and the calculation agent will reset it again. There is no limit to the amount of rebalance events that can occur.

Notwithstanding the foregoing, if a rebalance event occurs on or after 2:00 p.m. (New York City time) on a given trading day and another rebalance event occurs after 2:00 p.m. (New York City time) on the following day the rebalance trigger is being set (or would have occurred based on that day’s recomputed rebalance trigger), that subsequent rebalancing event will be null and void.

In addition, if a rebalance event occurs (i) on or after the first averaging date with respect to the final valuation date on which the calculation agent commences determining the ending level, the rebalancing event will be null and void or (ii) with respect to any other valuation date on which the calculation agent commences determining ending level, the rebalancing event will be null and void, provided that this clause will apply only to Securities which are being redeemed in the case of an optional early termination.

A rebalance event will have the effect of deleveraging your Securities; that is, a constant percentage increase in the index level will have a lesser positive effect on the value of your Securities relative to before the rebalance event. This also means that you would not recover your investment even should the underlying index level increase back to its trade date level. In addition, each time a rebalance event occurs, there will be a 0.05% (5 basis point) reduction to the principal amount of your Securities. This reduction will reduce the amount of your return (or increase your loss) on the maturity date or on an early redemption settlement date.

7

Table of Contents

Hypothetical Examples of How the Securities Perform

The following examples illustrate the calculation of the redemption amount for a hypothetical offering of the Securities under various scenarios. Each example assumes the following terms:

| Term | 1 year | |

| Issue Price | $25.00 per Security | |

| Principal Amount | $25.00 per Security | |

| Leverage Factor | 2 | |

| Rebalance Trigger | 80% of the starting level | |

| Early Redemption Level | 70% of the starting level |

At Maturity

The following examples assume that the underlying index level never falls below the early redemption level at any time during the observation period and the Securities are redeemed at maturity. For purposes of these examples, we have assumed an index adjustment factor of 0.60% per annum per Security. The actual index adjustment factor will depend on the three month USD LIBOR over the interest rate period and upon the actual number of calendar days in the accrual period and may result in a substantially different index adjustment factor.

Example 1 — The Index Return is 5%

The following example illustrates the calculation of the index return and the redemption amount for hypothetical Securities with the following additional assumptions:

| Starting Level | 1000 | |

| Ending Level | 1050 | |

| Early Redemption Level | 700 (70% of the starting level) |

Given the above assumptions, the index return would be calculated as follows:

| Index Return |

= | Ending Level – Starting Level | = | 1050 – 1000 | = | 5% | ||||||||||||||||||||

| Starting Level | 1000 |

Given an index return of 5% and the leverage factor of 2, the redemption amount would be:

$25 + [$25 × Leverage Factor x (Index Return – Index Adjustment Factor)] – Redemption Fee =

$25 + [$25 × 2 x (5% - 0.60%)] - $0.00

= $27.20 per Security (a gain of 8.80%).

In this example, given an initial investment of $25.00, the total return on the Securities is 8.80% while the index return is 5%.

Example 2 — The Index Return is -5%

The following example illustrates the calculation of the index return and the redemption amount for hypothetical Securities with the following additional assumptions:

| Starting Level | 1000 | |

| Ending Level | 950 | |

| Early Redemption Level | 700 (70% of the starting level) |

Given the above assumptions, the index return would be calculated as follows:

| Index Return |

= | Ending Level – Starting Level | = | 950 – 1000 | = | -5% | ||||||||||||||||||||

| Starting Level | 1000 |

Given an index return of -5% and the leverage factor of 2, the payment at maturity would be:

$25 + [$25 × Leverage Factor x (Index Return – Index Adjustment Factor)] – Redemption Fee =

$25 + [$25 × 2 x (-5% - 0.60%)] - $0.00

= $22.20 per Security (a loss of 11.20%).

In this example, given an initial investment of $25.00, the total return on the Securities is -11.20% while the index return is -5%.

8

Table of Contents

Example 3 — The Index Return is 15%

The following example illustrates the calculation of the index return and the redemption amount for hypothetical Securities with the following additional assumptions:

| Starting Level | 1000 | |

| Ending Level | 1150 | |

| Early Redemption Level | 700 (70% of the starting level) |

Given the above assumptions, the index return would be calculated as follows:

| Index Return |

= | Ending Level – Starting Level | = | 1150 – 1000 | = | 15% | ||||||||||||||||||||

| Starting Level | 1000 |

Given an index return of 15% and the leverage factor of 2, the redemption amount would be:

$25 + [$25 × Leverage Factor x (Index Return – Index Adjustment Factor)] – Redemption Fee =

$25 + [$25 × 2 x (15% - 0.60%)] - $0.00

= $32.20 per Security (a gain of 28.80%).

In this example, given an initial investment of $25.00, the total return on the Securities is 28.80% while the index return is 15%.

Example 4 — The Index Return is -15%

The following example illustrates the calculation of the index return and the redemption amount for hypothetical Securities with the following additional assumptions:

| Starting Level | 1000 | |

| Ending Level | 850 | |

| Early Redemption Level | 700 (70% of the starting level) |

Given the above assumptions, the index return would be calculated as follows:

| Index Return |

= | Ending Level – Starting Level | = | 850 – 1000 | = | -15% | ||||||||||||||||||||

| Starting Level | 1000 |

Given an index return of -15% and the leverage factor of 2, the redemption amount would be:

$25 + [$25 × Leverage Factor x (Index Return – Index Adjustment Factor)] – Redemption Fee =

$25 + [$25 × 2 x (-15% - 0.60%)] - $0.00

= $17.20 per Security (a loss of 31.20%).

In this example, given an initial investment of $25.00, the total return on the Securities is -31.20% while the index return is -15%.

Accordingly, you could lose all or a substantial portion of your investment in your Securities. In addition to being subject to the index adjustment factor, a redemption fee upon an early redemption and a principal amount reduction upon a rebalance event, you will participate in any negative performance of the underlying index on a two-times leveraged basis.

Upon an Early Redemption Event

The following examples assume that the underlying index level falls below the early redemption level during the observation period and the Securities are redeemed early. The following examples also assume that the date upon which the early redemption event has occurred is also the same date that a rebalance event has occurred because the underlying index level was less than both the rebalance trigger (which was 800) and the early redemption level (which was 700) on the same trading day. The occurrence of an early redemption event on the same trading day as a rebalance event renders the rebalance event null and void and the total return on the Securities will be calculated as set forth in the following examples.

9

Table of Contents

Example 1 — The underlying index level falls below the early redemption level on the trading day that is the 90th calendar day of the term of the Securities.

The following example illustrates the calculation of the index return and the redemption amount for hypothetical Securities with the following additional assumptions:

| Starting Level | 1000 | |

| Ending Level | 600 | |

| Early Redemption Level | 700 (70% of the starting level) |

For purposes of this example, we have assumed a redemption fee of $0.0125 and an index adjustment factor of 0.60% per annum per Security (or 0.15% for the 90 calendar day period measured in this example). The actual index adjustment factor will depend upon the three month USD LIBOR over the accrual period and upon the actual number of calendar days in the accrual period and may result in substantially a different index adjustment factor.

Given the above assumptions, the index return would be calculated as follows:

| Index Return |

= | Ending Level – Starting Level | = | 600 – 1000 | = | -40% | ||||||||||||||||||

| Starting Level | 1000 |

Given an index return of -40% and the leverage factor of 2, the payment upon an early redemption would be:

$25 + [$25 × Leverage Factor x (Index Return – Index Adjustment Factor)] – Redemption Fee =

$25 + [$25 × 2 x (-40% - 0.15%)] - $0.0125

= $4.9125 per Security (a loss of 80.35%).

In this example, given an initial investment of $25.00, the total return on the Securities is -80.35% while the index return is -40%.

Example 2 — The underlying index level falls below the early redemption level on the trading day that is the 270th calendar day of the term of the Securities.

The following example illustrates the calculation of the index return and the redemption amount for hypothetical Securities with the following additional assumptions:

| Starting Level | 1000 | |

| Ending Level | 500 | |

| Early Redemption Level | 700 (70% of the starting level) |

For purposes of this example, we have assumed a redemption fee of $0.0125 and an index adjustment factor of 0.60% per annum per Security (or 0.45% for the 270 calendar day period measured in this example). The actual index adjustment factor will depend upon the three month USD LIBOR over the accrual period and upon the actual number of calendar days in the accrual period and may result in substantially a different index adjustment factor.

Given the above assumptions, the index return would be calculated as follows:

| Index Return |

= | Ending Level – Starting Level | = | 500 – 1000 | = | -50% | ||||||||||||||||||

| Starting Level | 1000 |

Given an index return of -50% and the leverage factor of 2, the payment upon an early redemption would be:

$25 + [$25 × Leverage Factor x (Index Return – Index Adjustment Factor)] – Redemption Fee =

$25 + [$25 × 2 x (-50% - 0.45%)] - $0.0125

= -$0.2375 per Security

Because the redemption amount cannot be negative, the payment upon early redemption will be $0.00 per Security, and investors will suffer a total loss of the initial investment of $25.00. In this example, the total return on the Securities is -100% while the index return is -50%

Accordingly, you could lose all or a substantial portion of your investment in your Securities. In addition to being subject to the index adjustment factor, a redemption fee upon an early redemption and a principal amount reduction upon a rebalance event, you will participate in any negative performance of the underlying index on a two-times leveraged basis.

Any payment on the Securities, including any repayment of principal, is subject to the creditworthiness of UBS. If UBS were to default on its payment obligations, you may not receive any amounts owed to you under the Securities and you could lose your entire investment.

10

Table of Contents

Upon a Rebalance Event

The following example assumes that on any trading day the underlying index level of the underlying index is less than the rebalance trigger and an early redemption event has not occurred during the observation period.

Example — The underlying index level falls below the rebalance trigger on the trading day that is the 90th calendar day of the term of the Securities on or prior to 2:00 p.m. on such trading day.

The following example illustrates the calculation of the adjusted index return and the rebalance redemption amount for hypothetical Securities with the following additional assumptions:

| Starting Level | 1000 | |

| Underlying Index Level on the day (t-1) (which is the day prior to a Rebalance Date) |

850 | |

| Reference Level on the day (t-1) |

17.5 | |

| Ending Level | 650 | |

| Closing level of the Underlying Index on the Rebalance Date |

800 | |

| Rebalance Trigger | 800 (80% of the starting level) | |

| Deleverage Factor | 0.75 |

For purposes of this example, we have assumed an index adjustment factor of 0.60% per annum per Security. The actual index adjustment factor will depend upon three month USD LIBOR over the accrual period and upon the actual number of calendar days in the accrual period and may result in a substantially different index adjustment factor.

Given the above assumptions, the effective leverage factor is then calculated as follows:

Effective Leverage Factort-1 = [($25 × Leverage Factor × Deleverage Factorn) / Starting Level] × (Underlying Index Levelt-1 / Reference Levelt-1) =

[($25 × 2 × 0.750) / 1000] × (850 / 17.5) = 2.4286

Given the above assumptions, the reference level is calculated as follows:

Reference Level = Reference Levelt-1 × (1 + Effective Leverage Factort-1 × (Underlying Index Levelt / Underlying Index Levelt-1-1)) – ($25 × Reduction Fee) =

17.5 × (1 + 2.4286 × (800 / 850 -1)) – (25 × 0.0005) = 14.9875

Given the above assumptions, and no further rebalance events, the redemption amount at maturity is calculated as follows. The Effective Leverage Factor must be recalculated as of the rebalance date to account for the deleveraging effect of the rebalance event.

As of the rebalance date, the effective leverage factor is recalculated as follows:

Effective Leverage Factort-1 = [($25 × Leverage Factor × Deleverage Factorn) / Starting Level] × (Underlying Index Levelt-1 / Reference Levelt-1)

[($25 × 2 × 0.751) / 1000] × (800 / 14.9875) = 2.0017

Given the assumptions above and assuming no additional rebalance events have occurred during the term of the Securities, the adjusted redemption amount at maturity can be calculated as follows:

Reference Levelt-1 × (1 + Effective Leverage Factor × (Underlying Index Levelt / Underlying Index Levelt-1-1) – ($25 × Leverage Factor × Index Adjustment Factor) – Redemption Fee =

14.9875 × (1 + 2.0017 × (650 / 800* -1) – ($25 × 2 × 0.006) – 0

= $9.0625 per Security (a loss of 63.75%).

In this example, given an initial investment of $25.00, the total return on the Securities is -63.75% while the index return is -35%.

11

Table of Contents

| * | Assumes constant value since the rebalance date |

Accordingly, you could lose all or a substantial portion of your investment in your Securities. In addition to being subject to the index adjustment factor, a redemption fee upon an early redemption and a principal amount reduction upon a rebalance event, you will participate in any negative performance of the underlying index on a two-times leveraged basis.

Any payment on the Securities, including any repayment of principal, is subject to the creditworthiness of UBS. If UBS were to default on its payment obligations, you may not receive any amounts owed to you under the Securities and you could lose your entire investment.

12

Table of Contents

Key Risks

An investment in the Securities involves significant risks. Some of the risks that apply to the offering of Securities are summarized here, but we urge you to read the more detailed explanation of risks relating to the Securities generally in the “Risk Factors” section beginning on page PS-15 of the Fisher Enhanced Big Cap Growth Securities product supplement. We also urge you to consult your investment, legal, tax, accounting and other advisors before you invest in the Securities.

| ¨ | Risk of loss and leveraged downside exposure — You can lose all or substantially all of your investment in the Securities. In addition to being subject to the index adjustment factor, a redemption fee upon an early redemption and possibly principal amount reduction upon a rebalance event, to the extent that the ending level declines below the starting level, your loss is doubled, and the return on the Securities will decline at a rate that will exceed the rate of decline of the underlying index or the index constituents. If the index return is positive, but the increase in the level of the underlying index is insufficient to offset the effect of these fees and other reductions, you will have a loss on your investment in the Securities |

| ¨ | Increased sensitivity to market risk — The return on the Securities is linked to the performance of the underlying index and indirectly linked to the value of the stocks (“index constituent stocks”) comprising the underlying index. Because your investment in the Securities contains a leverage component, changes in the level of the underlying index or intraday index will have a greater impact on the amount payable on your Securities. In particular, any decrease in the closing level of the underlying index or level of the intraday index as of the applicable valuation date will result in a significantly greater decrease in the amount payable under the Securities on the maturity date or on an early redemption settlement date. |

| ¨ | The index adjustment factor, redemption fee and possibly a principal amount reduction may have a negative effect on the return potential of the Securities — The calculation of the redemption amount includes an index adjustment factor and a redemption fee (upon an early redemption) that reduces the overall return (or increases your loss) on the Securities. In addition, upon a rebalance event you will suffer a reduction in principal. Therefore, if the index return is positive, but the increase in the level of the underlying index is insufficient to offset the effect of the index adjustment factor, the redemption fee or a principal amount reduction, if applicable, you will have a loss on your investment in the Securities. |

| ¨ | The Securities are subject to an automatic early redemption feature that may terminate your leveraged exposure to the underlying index — The Securities will be automatically redeemed early if the underlying index level at any time at which a market disruption event is not occurring on any trading day during the observation period is less than the early redemption level. If the Securities are redeemed early due to an early redemption event, you will receive a redemption amount that will likely be significantly less than the principal amount of your Securities and could be zero. You will not be entitled to any further payments after the early redemption settlement date, including any payment at maturity, even if the level of the underlying index increases substantially subsequent to the occurrence of the early redemption event. |

| ¨ | Whether an early redemption event or a rebalance event occurs and the value of your Securities upon an early redemption event are based on intraday levels of the underlying index — The underlying index level, which is used to determine whether an early redemption event or rebalance event has occurred on any trading day during the observation period, will be based on intraday levels of the intraday index. Therefore, because the intraday low levels may be less than or equal to the closing level of the underlying index, it is more likely that an early redemption event will occur than if the underlying index level were based solely on closing levels of the underlying index or the intraday index. Moreover, upon the occurrence of an early redemption event or, in some situations, an optional early redemption, the ending level and therefore the redemption amount of your securities will be based on the index constituent VWAP for a specified period following the occurrence of the early redemption event. |

| ¨ | Upon the occurrence of a rebalance event, the Securities will be deleveraged — A rebalance event will have the effect of deleveraging your Securities; that is, a constant percentage increase in the index level will have a lesser positive effect on the value of your Securities relative to before the rebalance event. This also means that you would not recover your investment even should the underlying index level increase back to its trade date level. In addition, each time a rebalance event occurs, there will be a 0.05% (5 basis point) reduction to the principal amount of your Securities. This reduction will reduce the amount of your return (or increase your loss) on the maturity date or on an early redemption settlement date. |

| ¨ | Your optional redemption election is irrevocable — You may elect to require UBS to redeem your Securities, in whole or in part, prior to the earlier of the final valuation date and the occurrence of an early redemption event. You will not be able to rescind your election to redeem your Securities after your confirmation of redemption is received by the redemption agent. Accordingly, you will be exposed to market risk in the event market conditions change after the redemption agent receives your offer and before the redemption amount is determined on the applicable valuation date. For the avoidance of doubt, if an early redemption event occurs on or after the redemption notice date, the applicable valuation date and ending level will be determined in accordance with the early redemption event provisions. |

| ¨ | Reinvestment risk — If the Securities are redeemed prior to maturity pursuant to an optional early redemption or early redemption event, there is no guarantee that you would be able to reinvest the proceeds from an investment in the Securities, if any, in a comparable investment with similar characteristics as the Securities. |

| ¨ | There may be little or no secondary market for the Securities — The Securities will not be listed or displayed on any securities exchange or any electronic communications network. There can be no assurance that a secondary market for the Securities will develop. UBS Securities LLC and other affiliates of UBS currently intend to make a market in the Securities, although they are not required to do so and may stop making a market at any time. If you sell your Securities prior to maturity, you may have to sell them at a substantial loss. |

13

Table of Contents

| ¨ | Owning the Securities is not the same as owning the index constituent stocks — Owning the Securities is not the same as owning the index constituent stocks. As a holder of the Securities, you will not have voting rights or rights to receive dividends directly or other distributions or other rights that holders of the index constituent stocks would have. |

| ¨ | The Securities will not bear interest — As a holder of the Securities, you will not receive any periodic coupon payments. The overall return you earn on your Securities may be lower than interest payments you would receive by investing in a conventional fixed-rate or floating-rate debt security having the same maturity date and issuance date as the Securities. |

| ¨ | Credit of UBS — The Securities are unsubordinated, unsecured debt obligations of the issuer, UBS, and are not, either directly or indirectly, an obligation of any third party. Any payment to be made on the Securities depends on the ability of UBS, to satisfy its obligations as they come due. As a result, the actual and perceived creditworthiness of UBS may affect the market value of the Securities and, in the event UBS were to default on its obligations, you may not receive any amounts owed to you under the terms of the Securities and you could lose your entire initial investment. |

| ¨ | Potential credit rating downgrade — According to public news sources, at least one nationally recognized statistical rating agency intends to reduce credit ratings of many financial institutions, including UBS. This reduction, depending on the degree of the downgrade, may push-up our funding costs and thereby impair our profitability. These potential reductions, which follow downgrades by other nationally recognized statistical rating agencies may adversely affect our economic prospects and therefore our ability to make any payments on the Securities. |

| ¨ | There may be little or no secondary market — The Securities will not be listed or displayed on any securities exchange or any electronic communications network. There can be no assurance that a secondary market for the Securities will develop. UBS Securities LLC and other affiliates of UBS may make a market in the Securities, although they are not required to do so and may stop making a market at any time. The price, if any, at which you may be able to sell your Securities prior to maturity could be at a substantial discount from the issue price and to the intrinsic value of the product; and as a result, you may suffer substantial losses. |

| ¨ | Price of Securities prior to maturity — The market price of the Securities will be influenced by many unpredictable and interrelated factors, including the level of the underlying index; the volatility of the underlying index; the dividend rate paid on any index constituent stocks; the time remaining to the maturity of the Securities; interest rates in the markets; geopolitical conditions and economic, financial, political and regulatory or judicial events; and the creditworthiness of UBS. |

| ¨ | Impact of fees on the secondary market price of the Securities — Generally, the price of the Securities in the secondary market is likely to be lower than the issue price to public since the issue price to public included, and the secondary market prices are likely to exclude, commissions, hedging costs or other compensation paid with respect to the Securities. |

| ¨ | Potential UBS impact on price — Trading or transactions by UBS or its affiliates in any index constituents and/or over-the-counter options, futures or other instruments with return linked to the performance of the underlying index or the index constituents, may adversely affect the index constituent VWAP, and level(s) of the underlying index and intraday index and, therefore, the market value of the Securities. |

| ¨ | Potential conflict of interest — UBS and its affiliates may engage in business with the issuers of index constituent stocks comprising the underlying index or intraday index, or trading activities related to the underlying index, intraday index or any index constituents, which may present a conflict between the interests of UBS and you, as a holder of the Securities. The calculation agent, an affiliate of the Issuer, will determine the payment at maturity of the Securities based on observed levels of the underlying index and the intraday index. The calculation agent can postpone the determination of the starting level, the ending level or the maturity date if a market disruption event occurs and is continuing on the trade date or applicable valuation date. |

| ¨ | Potentially inconsistent research, opinions or recommendations by UBS — UBS and its affiliates publish research from time to time on financial markets and other matters that may influence the value of the Securities, or express opinions or provide recommendations that are inconsistent with purchasing or holding the Securities. Any research, opinions or recommendations expressed by UBS or its affiliates may not be consistent with each other and may be modified from time to time without notice. Investors should make their own independent investigation of the merits of investing in the Securities and the underlying index to which the Securities are linked. |

| ¨ | UBS cannot control actions by the index sponsor and the index sponsor has no obligation to consider your interests — UBS and its affiliates are not affiliated with the index sponsor and have no ability to control or predict its actions, including any errors in or discontinuation of public disclosure regarding methods or policies relating to the calculation of the underlying index. The index sponsor is not involved in the offer of the Securities in any way and has no obligation to consider your interest as an owner of the Securities in taking any actions that might affect the market value of your Securities. |

| ¨ | Uncertain tax treatment – Significant aspects of the tax treatment of the Securities are uncertain. You should consult your own tax advisor about your tax situation. |

14

Table of Contents

Russell 1000® Growth Index Total Return and Russell 1000® Growth Index

We have derived all information contained in this preliminary pricing supplement regarding the Russell 1000® Growth Index Total Return and the Russell 1000® Growth Index (each, a “Russell 1000 Growth Index), including, without limitation, its make-up, method of calculation and changes in its components, from publicly available information. Such information reflects the policies of, and is subject to change by Russell Investments, a subsidiary of Russell Investment Group (the “index sponsor”). UBS has not conducted any independent review or due diligence of any publicly available information with respect to the underlying index or the intraday index. You should make your own investigation into the underlying index and intraday index.

The Russell 1000 Growth Indexes are a sub-group of the Russell 1000® Index and measure the composite price performance of stocks of 1,000 companies (the “Russell 1000® component stocks”) incorporated in the U.S. and its territories. All 1,000 stocks are traded on a major U.S. exchange and are the 1,000 largest securities that form the Russell 3000® Index. The Russell 3000® Index is composed of the 3,000 largest U.S. companies as determined by market capitalization and represents approximately 98% of the U.S. equity market. The Russell 1000® Index consists of the largest 1,000 companies included in the Russell 3000 Index and represents approximately 92% of the total market capitalization of the U.S. equity market. The Russell 1000® Index is designed to track the performance of the large-capitalization segment of the U.S. equity market.

Two versions of the Russell 1000® Growth Index are calculated — a price return index, the Russell 1000® Growth Index, and a total return index, the Russell 1000® Growth Index Total Return. The price return index is ordinarily calculated without regard to cash dividends on Russell 1000® Growth Index securities. The total return index reinvests cash dividends on the ex-date. Both the price return and total return index reinvest extraordinary cash distributions.

Selection of stocks underlying the Russell 1000® Growth Index.

To be eligible for inclusion in the Russell 1000® Index, and, consequently, the Russell 1000 Growth Indexes, a company’s stocks must be listed on the last trading day in May of a given year and Russell Investments must have access to documentation verifying the company’s eligibility for inclusion. Eligible initial public offerings are added to Russell U.S. Indices at the end of each calendar quarter, based on total market capitalization rankings within the market-adjusted capitalization breaks established during the most recent reconstitution. To be added to any Russell U.S. index during a quarter outside of reconstitution, initial public offerings must meet additional eligibility criteria.

Only companies that are determined to be part of the U.S. equity market are eligible for inclusion in the Russell 1000 Growth Indexes. All securities eligible for inclusion must trade on a major U.S. exchange. Bulletin board, pink sheet or over-the-counter traded securities are not eligible for inclusion. Stocks must have a close price at or above $1.00 on their primary exchange or on another major U.S. exchange on the last trading day in May to be considered eligible for inclusion. The following companies are specifically excluded from the Russell 1000 Growth Indexes: (i) companies with a total market capitalization less than $30 Million; (ii) companies with only a small portion of their shares available in the marketplace; (iii) royalty trusts, limited liability companies, closed-end investment companies (business development companies are eligible), blank check companies, special purpose acquisition companies and limited partnerships. In addition, preferred and convertible preferred stock, redeemable shares, participating preferred stock, warrants, rights and trust receipts are not eligible for inclusion.

Russell Investments uses a “non-linear probability” method to assign stocks to the growth and value style indices. The term “probability” is used to indicate the degree of certainty that a stock is value or growth based on its relative book-to-price (B/P) ratio, I/B/E/S forecast medium-term growth (2 year) and sales per share historical growth (5 year). This method allows stocks to be represented as having both growth and value characteristics, while preserving the additive nature of the indices.

The process for assigning growth and value weights is applied separately to the stocks in the Russell 1000® Index. The stocks in the Russell 1000® Index are ranked by their adjusted book-to-price ratio (B/P), their I/B/E/S forecast medium-term growth (2 year) and sales per share historical growth (5 year). These rankings are converted to standardized units and combined to produce a Composite Value Score (CVS). Stocks are then ranked by their CVS, and a probability algorithm is applied to the CVS distribution to assign growth and value weights to each stock. In general, stocks with a lower CVS are considered growth, stocks with a higher CVS are considered value, and stocks with a CVS in the middle range are considered to have both growth and value characteristics, and are weighted proportionately in the growth and value index. Stocks are always fully represented by the combination of their growth and value weights, e.g., a stock that is given a 20% weight in a Russell value index will have an 80% weight in the same Russell growth index.

The growth and value probabilities will always sum to 100%. Hence, the sum of a stock’s market capitalization in the growth and value index will always equal its market capitalization in the Russell 1000® Index.

The quartile breaks are calculated such that approximately 25% of the available market capitalization lies in each quartile. Stocks at the median are divided 50% in each style index. Stocks below the first quartile are 100% in the growth index. Stocks above the third quartile are 100% in the value index. Stocks falling between the first and third quartile breaks are in both indexes to varying degrees depending on how far they are above or below the median and how close they are to the first or third quartile breaks.

Roughly 70% of the available market capitalization is classified as all growth or all value. The remaining 30% have some portion of their market value in either the value or growth index, depending on their relative distance from the median value score. Note that there is a small position cutoff rule. If a stock’s weight is more than 95% in one style index, its weight is increased to 100% in the index. This rule eliminates many small weightings and makes passive management easier.

15

Table of Contents

The Russell 1000 Growth Indexes, along with the Russell 1000® Index, are reconstituted annually to reflect changes in the marketplace. The list of companies is ranked based on May 31 total market capitalization, with the actual reconstitution effective on the first trading day following the final Friday of June each year. Changes in the constituents are preannounced and subject to change if any corporate activity occurs or if any new information is received prior to release.

Capitalization Adjustments.

The Russell 1000® Growth Indexes are float-adjusted and market-capitalization weighted. The current Russell 1000 Growth Index values are calculated by adding the market values of the Russell 1000® Index’s component stocks, which are derived by multiplying the price of each stock by the number of available shares, to arrive at the total market capitalization of the 1,000 stocks. The total market capitalization is then divided by a divisor, which represents the “adjusted” capitalization of the Russell 1000 Growth Indexes on the base date of December 31, 1978. To calculate the Russell 1000 Growth Indexes, last sale prices will be used for exchange-traded stocks. If a component stock is not open for trading, the most recently traded price for that security will be used in calculating the Russell 1000 Growth Indexes. In order to provide continuity for the Russell 1000 Growth Index’s values, the divisor is adjusted periodically to reflect events including changes in the number of common shares outstanding for Russell 1000® component stocks, company additions or deletions, corporate restructurings and other capitalization changes.

Available shares are assumed to be shares available for trading. Exclusion of capitalization held by other listed companies and large holdings of private investors (10% or more) is based on information recorded in corporate filings with the Securities and Exchange Commission. Other sources are used in cases of missing or questionable data.

The following types of shares are considered unavailable and are removed from total market capitalization to arrive at free float or available market capitalization:

| ¨ | ESOP or LESOP shares that comprise 10% or more of the shares outstanding are adjusted; |

| ¨ | Corporate cross-owned shares — shares held by another member of a Russell index (including Russell global indexes) are considered cross-owned shares, and all such shares will be adjusted regardless of percentage held; |

| ¨ | Large private and corporate shares — large private and corporate holdings are defined as those shares held by an individual, a group of individuals acting together or a corporation not in the index that own 10% or more of the shares outstanding. However, not to be included in this class are institutional holdings, which are: investment companies, partnerships, insurance companies, mutual funds, banks or venture capital firms unless these firms have a direct relationship to the company, such as board representation, in which case they are considered strategic holdings and are included with the officers/directors group; |

| ¨ | Unlisted share classes — classes of common stock that are not traded on a U.S. securities exchange; |

| ¨ | Initial public offering lock-ups — shares locked-up during an initial public offering are not available to the public and will be excluded from the market value at the time the initial public offering enters the index; and |

| ¨ | Government holdings: |

| ¨ | Direct government holders — holdings listed as “government of” are considered unavailable and will be removed entirely from available shares; |

| ¨ | Indirect government holders — shares held by government investment boards and/or investment arms will be treated similar to large private holdings and removed if the holding is greater than 10%; and |

| ¨ | Government pensions — holdings by government pension plans are considered institutional holdings and will not be removed from available shares. |

Corporate Actions Affecting the Russell 1000® Growth Index.

The following summarizes the types of Russell 1000® Growth Index maintenance adjustments and indicates whether or not an index adjustment is required:

| ¨ | “No Replacement” Rule — Securities that leave the Russell 1000® Growth Index, between reconstitution dates, for any reason (e.g., mergers, acquisitions or other similar corporate activity) are not replaced. Thus, the number of securities in the Russell 1000® Growth Index over the past year will fluctuate according to corporate activity. |

| ¨ | Rule for Deletions — When a stock is acquired, delisted, or moves to the pink sheets or bulletin boards on the floor of a U.S. securities exchange, the stock is deleted from the index at the close on the effective date or when the stock is no longer trading on the exchange. |

| ¨ | When acquisitions or mergers take place within the Russell 1000® Growth Index, the stock’s capitalization moves to the acquiring stock, hence, mergers have no effect on the index total capitalization. Shares are updated for the acquiring stock at the time the transaction is final. |

| ¨ | Rule for Additions — The only additions between reconstitution dates are as a result of spin-offs and initial public offerings. Spin-off companies are added to the parent company’s index and capitalization tier of membership, if the spin-off is large enough. To be eligible, the spun-off company’s total market capitalization must be greater than the market-adjusted total market capitalization of the smallest security in the Russell 3000E Index at the latest reconstitution. |

16

Table of Contents

Updates to Share Capital Affecting the Russell 1000® Growth Index.

Each month, the Russell 1000® Growth Index is updated for changes to shares outstanding as companies report changes in share capital to the Securities and Exchange Commission. Effective April 30, 2002, only cumulative changes to shares outstanding greater than 5% will be reflected in the Russell 1000® Growth Index. This does not affect treatment of major corporate events, which are effective on the ex-date.

License Agreement between Russell Investments and UBS.

Russell Investments and UBS have entered into a non-exclusive license agreement providing for the license to UBS, and certain of its affiliated or subsidiary companies, in exchange for a fee, of the right to use the Russell 1000® Growth Index, which is owned and published by Russell Investments, in connection with the securities.

The license agreement between Russell Investments and UBS provides that the following language must be set forth in this index supplement:

The securities are not sponsored, endorsed, sold or promoted by Russell Investments. Russell Investments makes no representation or warranty, express or implied, to the owners of the securities or any member of the public regarding the advisability of investing in securities generally or in the securities particularly or the ability of the Russell 1000® Growth Index to track general stock market performance or a segment of the same. Russell Investments’ publication of the Russell 1000® Growth Index in no way suggests or implies an opinion by Russell Investments as to the advisability of investment in any or all of the securities upon which the Russell 1000® Growth Index is based. Russell Investments’ only relationship to UBS is the licensing of certain trademarks and trade names of Russell Investments and of the Russell 1000® Growth Index, which is determined, composed and calculated by Russell Investments without regard to UBS or the securities. Russell Investments is not responsible for and has not reviewed the securities nor any associated literature or publications and Russell Investments makes no representation or warranty express or implied as to their accuracy or completeness, or otherwise. Russell Investments reserves the right, at any time and without notice, to alter, amend, terminate or in any way change the Russell 1000® Growth Index. Russell Investments has no obligation or liability in connection with the administration, marketing or trading of the securities.

RUSSELL INVESTMENTS DOES NOT GUARANTEE THE ACCURACY AND/OR THE COMPLETENESS OF THE RUSSELL 1000® GROWTH INDEX OR ANY DATA INCLUDED THEREIN AND RUSSELL INVESTMENTS SHALL HAVE NO LIABILITY FOR ANY ERRORS, OMISSIONS, OR INTERRUPTIONS THEREIN. RUSSELL INVESTMENTS MAKES NO WARRANTY, EXPRESS OR IMPLIED, AS TO RESULTS TO BE OBTAINED BY UBS, INVESTORS, OWNERS OF THE SECURITIES, OR ANY OTHER PERSON OR ENTITY FROM THE USE OF THE RUSSELL 1000® GROWTH INDEX OR ANY DATA INCLUDED THEREIN. RUSSELL INVESTMENTS MAKES NO EXPRESS OR IMPLIED WARRANTIES, AND EXPRESSLY DISCLAIMS ALL WARRANTIES OF MERCHANTABILITY OR FITNESS FOR A PARTICULAR PURPOSE OR USE WITH RESPECT TO THE RUSSELL 1000® GROWTH INDEX OR ANY DATA INCLUDED THEREIN. WITHOUT LIMITING ANY OF THE FOREGOING, IN NO EVENT SHALL RUSSELL INVESTMENTS HAVE ANY LIABILITY FOR ANY SPECIAL, PUNITIVE, INDIRECT, OR CONSEQUENTIAL DAMAGES (INCLUDING LOST PROFITS), EVEN IF NOTIFIED OF THE POSSIBILITY OF SUCH DAMAGES.

The “Russell 1000® Index” is a trademark of Russell Investments and has been licensed for use by UBS. The securities are not sponsored, endorsed, sold or promoted by Russell Investments and Russell Investments makes no representation regarding the advisability of investing in the securities.

Information from outside sources is not incorporated by reference in, and should not be considered part of, this preliminary pricing supplement or any accompanying prospectus. UBS has not conducted any independent review or due diligence of any publicly available information with respect to the underlying index.

17

Table of Contents

Historical Information

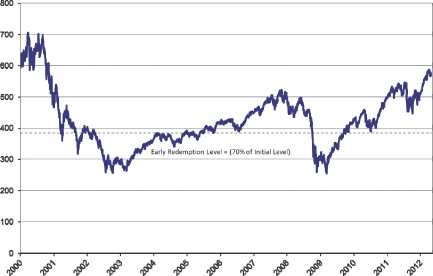

The following table sets forth the quarterly high and low closing levels for the Russell 1000® Growth Index Total Return, as reported by Bloomberg Professional® service (“Bloomberg”), without independent verification. UBS has not undertaken an independent review or due diligence of any publically available information obtained from Bloomberg. The closing level of the Russell 1000® Growth Index Total Return on May 11, 2012 was 563.08. The historical levels of the underlying index should not be taken as an indication of future performance.

| Quarter Begin | Quarter End | Quarterly High | Quarterly Low | Quarterly Close | ||||

| 1/2/2008 | 3/31/2008 | 495.37 | 435.37 | 451.27 | ||||

| 4/1/2008 | 6/30/2008 | 496.91 | 456.61 | 456.91 | ||||

| 7/1/2008 | 9/30/2008 | 460.17 | 383.49 | 400.58 | ||||

| 10/1/2008 | 12/31/2008 | 395.26 | 259.15 | 309.30 | ||||

| 1/2/2009 | 3/31/2009 | 324.37 | 254.91 | 296.56 | ||||

| 4/1/2009 | 6/30/2009 | 353.53 | 300.60 | 344.96 | ||||

| 7/1/2009 | 9/30/2009 | 396.28 | 332.15 | 393.16 | ||||

| 10/1/2009 | 12/31/2009 | 429.07 | 382.64 | 424.38 | ||||

| 1/4/2010 | 3/31/2010 | 446.32 | 401.73 | 444.10 | ||||

| 4/1/2010 | 6/30/2010 | 460.18 | 391.94 | 391.94 | ||||

| 7/1/2010 | 9/30/2010 | 444.91 | 389.59 | 442.90 | ||||

| 10/1/2010 | 12/31/2010 | 496.69 | 440.35 | 495.30 | ||||

| 1/3/2011 | 3/31/2011 | 532.63 | 496.09 | 525.17 | ||||

| 4/1/2011 | 6/30/2011 | 542.76 | 504.11 | 529.15 | ||||

| 7/1/2011 | 9/30/2011 | 546.10 | 453.08 | 459.64 | ||||

| 10/3/2011 | 12/30/2011 | 521.64 | 446.75 | 508.39 | ||||

| 1/3/2012 | 3/30/2012 | 586.08 | 515.43 | 583.07 | ||||

| 4/2/2012* | 5/11/2012* | 588.12 | 562.95 | 563.08 |

| * | As of the date of this preliminary pricing supplement, available information for the second calendar quarter of 2012 includes data for the period from April 2, 2012 through May 11, 2012. Accordingly, the “Quarterly High,” “Quarterly Low” and “Quarterly Close” data indicated are for this shortened period only and do not reflect complete data for the second calendar quarter of 2012. |

The graph below illustrates the performance of the underlying index from January 3, 2000 through May 11, 2012, based on information from Bloomberg. The dotted line represents a hypothetical early redemption level of 394.16, which is equal to 70% of the closing level of the underlying index on May 11, 2012. The actual early redemption level will be based on the closing level of the underlying index on the trade date. Past performance of the underlying index is not indicative of the future performance of the underlying index.

18

Table of Contents

Historical Information

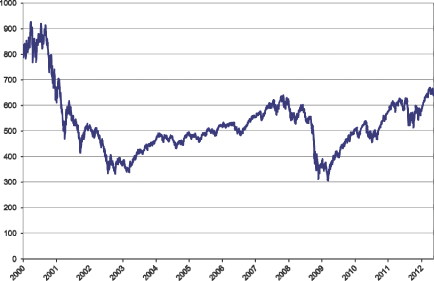

The following table sets forth the quarterly high and low closing levels for the Russell 1000® Growth Index, as reported by Bloomberg Professional® service (“Bloomberg”), without independent verification. UBS has not undertaken an independent review or due diligence of any publically available information obtained from Bloomberg. The closing level of the Russell 1000® Growth Index on May 11, 2012 was 639.93. The historical levels of the intraday index should not be taken as an indication of future performance.

| Quarter Begin | Quarter End | Quarterly High | Quarterly Low | Quarterly Close | ||||

| 1/2/2008 | 3/31/2008 | 603.27 | 528.73 | 547.93 | ||||

| 4/1/2008 | 6/30/2008 | 601.89 | 553.07 | 553.07 | ||||

| 7/1/2008 | 9/30/2008 | 555.83 | 462.66 | 483.28 | ||||

| 10/1/2008 | 12/31/2008 | 476.75 | 311.83 | 371.18 | ||||

| 1/2/2009 | 3/31/2009 | 389.26 | 304.75 | 354.15 | ||||

| 4/1/2009 | 6/30/2009 | 420.43 | 358.87 | 410.05 | ||||

| 7/1/2009 | 9/30/2009 | 469.23 | 394.77 | 465.38 | ||||

| 10/1/2009 | 12/31/2009 | 505.82 | 452.91 | 500.22 | ||||

| 1/4/2010 | 3/31/2010 | 524.09 | 473.03 | 521.38 | ||||

| 4/1/2010 | 6/30/2010 | 540.02 | 458.26 | 458.26 | ||||

| 7/1/2010 | 9/30/2010 | 518.19 | 455.50 | 515.80 | ||||

| 10/1/2010 | 12/31/2010 | 576.30 | 512.80 | 574.67 | ||||

| 1/3/2011 | 3/31/2011 | 616.77 | 573.79 | 607.18 | ||||

| 4/1/2011 | 6/30/2011 | 627.13 | 580.90 | 609.52 | ||||

| 7/1/2011 | 9/30/2011 | 628.94 | 520.79 | 527.38 | ||||

| 10/3/2011 | 12/30/2011 | 598.07 | 512.58 | 580.88 | ||||

| 1/3/2012 | 3/30/2012 | 667.37 | 588.93 | 663.73 | ||||

| 4/2/2012* | 5/11/2012* | 669.45 | 639.93 | 639.93 |

| * | As of the date of this preliminary pricing supplement, available information for the second calendar quarter of 2012 includes data for the period from April 2, 2012 through May 11, 2012. Accordingly, the “Quarterly High,” “Quarterly Low” and “Quarterly Close” data indicated are for this shortened period only and do not reflect complete data for the second calendar quarter of 2012. |

The graph below illustrates the performance of the intraday index from January 3, 2000 through May 11, 2012, based on information from Bloomberg. Past performance of the intraday index is not indicative of the future performance of the intraday index.

19

Table of Contents

What Are the Tax Consequences of the Securities?

The United States federal income tax consequences of your investment in the Securities are uncertain. Some of these tax consequences are summarized below, but we urge you to read the more detailed discussion in “Supplemental U.S. Tax Considerations” on page PS-33 of the Fisher Enhanced Big Cap Growth Securities product supplement and discuss the tax consequences of your particular situation with your tax advisor.

There are no statutory provisions, regulations, published rulings or judicial decisions addressing the characterization for U.S. federal income tax purposes of securities with terms that are substantially the same as the Securities. Accordingly, the tax treatment of the Securities is uncertain. Pursuant to the terms of the Securities, UBS and you agree, in the absence of a statutory, regulatory, administrative or judicial ruling to the contrary, to characterize your Securities as a pre-paid derivative contract with respect to the underlying index. If your Securities are so treated, you should generally not accrue any income with respect to the Securities prior to sale, exchange or maturity of the Securities and you should generally recognize capital gain or loss upon the sale, exchange or maturity of your Securities in an amount equal to the difference between the amount you receive at such time and the amount you paid for your Securities. Such gain or loss should be long-term capital gain or loss if you have held your Securities for more than one year.

In the opinion of our counsel, Cadwalader, Wickersham & Taft LLP, it would be reasonable to treat your Securities in the manner described above. However, because there is no authority that specifically addresses the tax treatment of the Securities, it is possible that your Securities could alternatively be treated for tax purposes in the manner described under “Supplemental U.S. Tax Considerations — Alternative Treatments” on page PS-34 of the product supplement.

In 2007, the Internal Revenue Service released a notice that may affect the taxation of holders of the Securities. According to the notice, the Internal Revenue Service and the Treasury Department are actively considering whether the holder of an instrument similar to the Securities should be required to accrue ordinary income on a current basis, and they are seeking taxpayer comments on the subject. It is not possible to determine what guidance they will ultimately issue, if any. It is possible, however, that under such guidance, holders of the Securities will ultimately be required to accrue income currently and this could be applied on a retroactive basis. The Internal Revenue Service and the Treasury Department are also considering other relevant issues, including whether additional gain or loss from such instruments should be treated as ordinary or capital, whether foreign holders of such instruments should be subject to withholding tax on any deemed income accruals, and whether the special “constructive ownership rules” of Section 1260 of the Internal Revenue Code of 1986, as amended (the “Code”) above should be applied to such instruments. Holders are urged to consult their tax advisors concerning the significance, and the potential impact, of the above considerations. Except to the extent otherwise required by law, UBS intends to treat your Securities for United States federal income tax purposes in accordance with the treatment described above and under “Supplemental U.S. Tax Considerations” on page PS-33 of the product supplement, unless and until such time as the Treasury Department and Internal Revenue Service determine that some other treatment is more appropriate.

Moreover, in 2007, legislation was introduced in Congress that, if it had been enacted, would have required holders of Securities purchased after the bill was enacted to accrue interest income over the term of the Securities despite the fact that there will be no interest payments over the term of the Securities. It is not possible to predict whether a similar or identical bill will be enacted in the future, or whether any such bill would affect the tax treatment of your Securities.