Exhibit 99.1

ANNUAL INFORMATION FORM

For the Year Ended December 31, 2014

February 27, 2015

hydro One

TABLE OF CONTENTS

TABLE OF CONTENTS

| 2 | DEFINITIONS | |

| 7 | CORPORATE STRUCTURE | |

| 9 | FORWARD-LOOKING INFORMATION | |

| 15 | ABOUT HYDRO ONE | |

| 15 |

Our Mission and Vision | |

| 15 |

Our Strategy | |

| 17 |

Corporate Awards | |

| 19 | GENERAL DEVELOPMENT OF THE BUSINESS | |

| 19 | Electricity Sector Landscape | |

| 19 | OEB | |

| 19 | OPA and IESO | |

| 20 | 2013 Long-Term Energy Plan | |

| 20 | Recent Industry Activity | |

| 20 | Premier’s Advisory Council on Government Assets | |

| 21 | Customer Service Initiatives | |

| 21 | Distribution Sector Consolidation | |

| 23 | Regulated Price Plan Structure | |

| 23 | TOU Pricing Structure | |

| 25 | Procurement of New Generation | |

| 25 | Recent Developments at Hydro One | |

| 25 | Sustainable Electricity Company Designation | |

| 27 | OVERVIEW OF HYDRO ONE | |

| 29 | DESCRIPTION OF THE BUSINESS | |

| 29 | Our Business Segments | |

| 29 | Our Transmission Business | |

| 29 | Overview | |

| 30 | Transmission Planning | |

| 30 | Transmission Assets | |

| 30 | Transmission Stations | |

| 31 | Transmission Lines | |

| 31 | Network Operations | |

| 32 | Telecommunications Facilities | |

| 32 | Transmission Capital Expenditure Plans | |

| 33 | Major Transmission Capital Development Projects | |

| 35 | Transmission Projects at the Local Load Connection Level | |

| 36 | Transmission Sustainment | |

| 2014 ANNUAL INFORMATION FORM i |

| TABLE OF CONTENTS |

| 36 | Bruce to Milton Double Circuit Transmission Line | |

| 36 | NERC/NPCC | |

| 37 | NERC Critical Infrastructure Protection Standards | |

| 37 | Our Distribution Business | |

| 38 | Distribution Capital Expenditure Plans | |

| 39 | Distribution Assets | |

| 39 | Remote Communities | |

| 39 | Conservation and Demand Management | |

| 41 | Advanced Distribution System | |

| 42 | Smart Meters | |

| 44 | Our Telecommunications Business | |

| 44 | Other Business Particulars | |

| 44 | Employees | |

| 45 | Compensation | |

| 46 | Pension Plan | |

| 46 | Outsourcing Arrangements | |

| 47 | Environmental | |

| 47 | Health, Safety and Environmental Management System | |

| 48 | Permits and Approvals | |

| 48 | Regulation of Releases | |

| 48 | Hazardous Substances | |

| 48 | PCB | |

| 49 | Asbestos | |

| 49 | Herbicides | |

| 50 | Wood Preservatives | |

| 50 | Land Assessment and Remediation | |

| 51 | Electric and Magnetic Fields | |

| 51 | Health and Safety | |

| 52 | Insurance | |

| 52 | Legal Proceedings and Regulatory Actions | |

| 52 | Financial | |

| 53 | Cornerstone | |

| 55 | REGULATION | |

| 55 | The Statutory and Operating Framework | |

| 55 | Federal Framework | |

| 55 | Ontario Framework | |

| 56 | The Ontario Regulatory Process | |

| 56 | Contractual Arrangements, Codes and Licences | |

| 56 | Operating Agreement with the IESO | |

| 56 | Hydro One’s Relationships with Other Market Participants | |

| 57 | Electricity Industry Codes | |

| 57 | Electricity Industry Licences | |

| ii HYDRO ONE INC. |

| TABLE OF CONTENTS |

| 58 | Rate Orders and Related Issues for Hydro One’s Businesses | |

| 58 | Transmission | |

| 58 | Current Rate Orders and Review of the Existing Transmission Rate Structure | |

| 59 | Bypass | |

| 59 | Competition | |

| 59 | Facilities Applications | |

| 60 | Distribution | |

| 60 | Current Rate Orders and Distribution Rate Structure | |

| 60 | Hydro One Networks Inc. | |

| 61 | Hydro One Brampton Networks Inc. | |

| 61 | Hydro One Remote Communities Inc. | |

| 62 | Rural and Remote Rate Protection | |

| 62 | Rate Protection and Determination of Direct Benefits to Accommodate | |

| Renewable Energy Generation Facilities | ||

| 62 | Ontario Clean Energy Benefit Act | |

| 63 | Connection Cost Responsibility | |

| 64 | RISK FACTORS | |

| 64 |

Ownership by the Province | |

| 65 |

Regulatory Risk | |

| 66 |

Risk of Natural and Other Unexpected Occurrences | |

| 66 |

First Nation and Métis Claims Risk | |

| 66 |

Risk from Transfer of Assets Located on Reserves | |

| 67 |

Risk Associated with Information Technology Infrastructure | |

| 67 |

Work Force Demographic Risk | |

| 67 |

Labour Relations Risk | |

| 68 |

Risk Associated with Arranging Debt Financing | |

| 68 |

Asset Condition | |

| 69 |

Environmental Risk | |

| 70 |

Pension Plan Risk | |

| 70 |

Risk Associated with Outsourcing Arrangements | |

| 70 |

Market and Credit Risk | |

| 71 |

Risk Associated with Transmission Projects | |

| 71 |

Risk from Provincial Ownership of Transmission Corridors | |

| 72 | DIVIDENDS | |

| 73 | DESCRIPTION OF CAPITAL STRUCTURE | |

| 74 | CREDIT RATINGS OF SECURITIES AND LIQUIDITY | |

| 75 | MARKET FOR SECURITIES | |

| 2014 ANNUAL INFORMATION FORM iii |

| TABLE OF CONTENTS

|

| 76 | DIRECTORS AND OFFICERS | |

| 76 | Directors | |

| 76 | Name and Municipality of Residence | |

| 83 | Information Regarding Certain Directors | |

| 84 | Executive Officers | |

| 84 | Name and Municipality of Residence | |

| 84 | Indebtedness of Directors and Executive Officers | |

| 85 | INTEREST OF MANAGEMENT AND OTHERS IN MATERIAL TRANSACTIONS | |

| 85 | Relationships with the Province and Other Parties | |

| 85 | Overview | |

| 85 | Transfer Orders | |

| 86 | Indemnities | |

| 87 | Payments in Lieu of Corporate Taxes | |

| 87 | Memorandum of Agreement | |

| 89 | TRUSTEES AND REGISTRARS | |

| 90 | MATERIAL CONTRACTS | |

| 93 | INTERESTS OF EXPERTS | |

| 94 | ADDITIONAL INFORMATION | |

| 95 | STATEMENT OF EXECUTIVE COMPENSATION | |

| 95 | Compensation Discussion and Analysis | |

| 95 | Overview | |

| 97 | Governance | |

| 97 | Composition of the CGHRC | |

| 97 | Committee Members Relevant and Direct Experience | |

| 99 | Compensation Policies and Practices Aligned to Risk Management | |

| 100 | Independent Consultant for the CGHRC | |

| 101 | ELEMENTS OF COMPENSATION | |

| 102 | Base Salary | |

| 103 | Performance-Based Compensation | |

| 103 | Fund Determination | |

| 104 | Fund Allocation | |

| 104 | Corporate Performance Measures and Targets | |

| 106 | Injury-Free Workplace | |

| 106 | Satisfying our Customers | |

| 107 | Continuous Improvement and Cost Effectiveness | |

| 108 | Maintaining a Commercial Culture | |

| 109 | Overall Performance for 2014 | |

| 109 | Individual Performance | |

| iv HYDRO ONE INC. |

| TABLE OF CONTENTS

|

| 112 | Benefits | |

| 113 | Role of NEOs in Determining Executive Compensation | |

| 114 | SUMMARY COMPENSATION TABLE | |

| 116 | Pension Plan Benefits | |

| 116 | Defined Benefit Pension Plan | |

| 119 | Termination and Change of Control Benefits | |

| 120 | Director Compensation | |

| 121 | Director Compensation Table | |

| 122 | APPOINTMENT OF AUDITOR | |

| 123 | AUDIT, FINANCE AND PENSION INVESTMENT COMMITTEE INFORMATION | |

| 123 | The Audit, Finance and Pension Investment Committee’s Charter | |

| 123 | Composition of the Audit, Finance and Pension Investment Committee | |

| 123 | Relevant Education and Experience | |

| 126 | Audit, Finance and Pension Investment Committee Oversight | |

| 126 | Pre-Approval Policies and Procedures | |

| 126 | External Auditor Service Fees | |

| 127 | CORPORATE GOVERNANCE DISCLOSURE | |

| 127 | Board of Directors | |

| 128 | Summary of Attendance of Directors | |

| 129 | Directors’ Board Memberships in Other Reporting Issuers | |

| 129 | Board Mandate | |

| 129 | Position Descriptions | |

| 129 | Committees of the Board (as at December 31, 2014) | |

| 129 | Audit, Finance and Pension Investment Committee | |

| 130 | Business Transformation Committee | |

| 130 | Corporate Governance and Human Resources Committee | |

| 130 | Health, Safety and Environment Committee | |

| 131 | Regulatory and Public Policy Committee | |

| 131 | Strategy Committee | |

| 131 | Orientation and Continuing Education | |

| 131 | Ethical Business Conduct | |

| 132 | Board, Committee and Director Assessments | |

| 133 | Board and Executive Composition | |

| 134 | APPENDIX “A” AUDIT, FINANCE AND PENSION INVESTMENT COMMITTEE MANDATE | |

| 147 | APPENDIX “B” HYDRO ONE INC. BOARD OF DIRECTORS MANDATE | |

| 150 | APPENDIX “C” HYDRO ONE TRANSMISSION AND DISTRIBUTION LICENCES | |

| 2014 ANNUAL INFORMATION FORM v |

EXCEPT WHERE OTHERWISE INDICATED,

ALL INFORMATION PRESENTED HEREIN IS

AS AT DECEMBER 31, 2014

2014 ANNUAL INFORMATION FORM 1

DEFINITIONS

DEFINITIONS

2 HYDRO ONE INC.

| DEFINITIONS

|

| For convenience, in this Annual Information Form:

| ||

|

“2010 LTEP” means “Ontario’s Long Term Energy Plan, Building Our Clean Energy Future”, announced by the Province on November 23, 2010;

| ||

|

“2013 LTEP” means “Ontario’s Long-Term Energy Plan, Achieving Balance”, announced by the Province on December 2, 2013;

| ||

|

“ADS” means the Advanced Distribution System;

| ||

|

“AIF” means this Annual Information Form;

| ||

|

“B2M LP” refers to B2M Limited Partnership;

| ||

|

“BES” means Bulk Electric System;

| ||

|

“Board” means the Board of Directors of Hydro One Inc.;

| ||

|

“Canadian GAAP” means Canadian Generally Accepted Accounting Principles per Part V of the Chartered Professional Accountants Canada Handbook;

| ||

|

“CDM” means conservation and demand management;

| ||

|

“CDM Code” means the CDM Code for Electricity Distributors;

| ||

|

“Council” means the Premier’s Advisory Council on Government Assets;

| ||

|

“DS” means a distribution station;

| ||

|

“DSC” means the Distribution System Code;

| ||

|

“EA” means the Environmental Assessment Act (Ontario);

| ||

|

“ECA” means an Electricity Conservation Agreement

| ||

|

“Electricity Act” means the Electricity Act, 1998, as amended;

| ||

|

“ESA” means an Environmental Site Assessment;

| ||

|

“ESR” means an Environmental Study Report;

| ||

|

“ETS” means Export Transmission Service;

| ||

|

“FERC” means the U.S. Federal Energy Regulatory Commission;

| ||

|

“First Nation” means a “band” as that term is defined in the Indian Act (Canada);

| ||

|

“FIT” means the feed-in-tariff program of the OPA;

| ||

|

“GEA” means the Green Energy and Green Economy Act, 2009 (Ontario);

| ||

|

“GTA” means the Greater Toronto Area;

| ||

|

“Hydro One”, “our company”, “we”, “us”, “our”, and “the company” refer to Hydro One Inc. and its subsidiaries and predecessors, except where the context requires otherwise;

|

| 2014 ANNUAL INFORMATION FORM 3 |

| DEFINITIONS

|

|

“IASB” refers to the International Accounting Standards Board;

| ||

|

“IESO” refers to the Independent Electricity System Operator, previously named the Independent Electricity Market Operator;

| ||

|

“IFRS” means International Financial Reporting Standards;

| ||

|

“Inergi Agreement” means the outsourcing service agreement with Inergi LP entered into on November 28, 2014 and commencing March 1, 2015;

| ||

|

“Intertie” means a transmission facility that physically connects adjacent transmission systems in different jurisdictions (e.g. provinces or countries) for the purpose of electrical power transfers;

| ||

|

“IPL” refers to an international power line;

| ||

|

“IPSP” means the Integrated Power System Plan developed by the OPA;

| ||

|

“IRM” means Incentive Regulation Mechanism;

| ||

|

“IT” means Information Technology;

| ||

|

“LDC” means a local distribution company;

| ||

|

“LRAM” means Lost Revenue Adjustment Mechanism;

| ||

|

“MAAD Application” means an application for a Merger Acquisition Amalgamation and Divestiture filed with the OEB;

| ||

|

“Market Rules” means the rules made under section 32 of the Electricity Act that are administered by the IESO;

| ||

|

“Micro FIT” means the micro feed-in-tariff program of the OPA;

| ||

|

“Ministry” or “Minister” means the Ontario Ministry of Energy or the Ontario Ministry of Energy and Infrastructure and, as applicable, its respective Minister;

| ||

|

“NEB” refers to the National Energy Board;

| ||

|

“NEB Act” means the National Energy Board Act, 1985 (Canada), as amended;

| ||

|

“NERC” means the North American Electric Reliability Corporation;

| ||

|

“NPCC” means the Northeast Power Coordinating Council Inc.;

| ||

|

“NYSE” means the New York Stock Exchange;

| ||

|

“OEB” refers to the Ontario Energy Board;

| ||

|

“OEB Act” means the Ontario Energy Board Act, 1998, as amended;

| ||

|

“OEFC” means the Ontario Electricity Financial Corporation;

| ||

|

“OGCC” means Hydro One’s Ontario Grid Control Centre located north of Toronto, Ontario;

|

| 4 HYDRO ONE INC. |

| DEFINITIONS

|

|

“OHSAS 18001” means Occupational Health and Safety Assessment Series 18001 standard;

| ||

|

“Ontario” refers to the Province of Ontario as a geographical area;

| ||

|

“OM&A” means Operation, Maintenance and Administration;

| ||

|

“OPA” refers to the Ontario Power Authority;

| ||

|

“Open Access” refers to the opening of Ontario’s wholesale and retail electricity markets to competition, which officially occurred on May 1, 2002;

| ||

|

“OPG” refers to Ontario Power Generation Inc.;

| ||

|

“PCB” means polychlorinated biphenyls;

| ||

|

“Province” refers to the Government of the Province of Ontario;

| ||

|

“PWU” refers to the Power Workers’ Union;

| ||

|

“Reserve” means a “reserve” as that term is defined in the Indian Act (Canada);

| ||

|

“ROE” refers to return on equity;

| ||

|

“RPP” refers to the regulated price plan structure for the cost of electricity supplied to low volume and designated customers;

| ||

|

“RRFE” means the Renewed Regulatory Framework for Electricity;

| ||

|

“RRP” means the Renewed Regulatory Framework for Electricity Distributors and Transmitters;

| ||

|

“RRRP” means Rural and Remote Electricity Rate Protection;

| ||

|

“SEC” means the United States Securities and Exchange Commission;

| ||

|

“Small FIT” means the small feed-in-tariff program of the OPA;

| ||

|

“Smart Grid Advisory Committee” means the committee created by the OEB on June 27, 2013;

| ||

|

“Society” refers to the Society of Energy Professionals;

| ||

|

“SS” refers to a switching station;

| ||

|

“TOU” refers to “time-of-use” rates;

| ||

|

“TS” refers to a transmission station;

| ||

|

“TSC” means the Transmission System Code;

| ||

|

“U.S.” means the United States of America; and

| ||

|

“U.S. GAAP” means United States Generally Accepted Accounting Principles.

|

| 2014 ANNUAL INFORMATION FORM 5 |

HYDRO ONE BRAMPTON NETWORKS INC. HYDRO ONE REMOTE COMMUNITIES INC. HYDRO ONE TELECOM INC. 6 HYDRO ONE INC.

| CORPORATE STRUCTURE |

CORPORATE STRUCTURE

Hydro One Inc. was incorporated as Ontario Hydro Services Company Inc. by Articles of Incorporation dated December 1, 1998, under the Business Corporations Act (Ontario). On May 1, 2000, we changed our name to Hydro One Inc.

Our registered office and head office is located at 483 Bay Street, 8th Floor, South Tower, Toronto, Ontario, M5G 2P5.

The following are our principal subsidiaries, each of which is wholly owned by us and is incorporated under the laws of Ontario:

| — | Hydro One Networks Inc. – carries on all business relating to our ownership, operation and management of electricity transmission and distribution systems and facilities; |

| — | Hydro One Brampton Networks Inc. – carries on the business relating to our ownership, operation and management of electricity distribution systems and facilities in Brampton, Ontario; |

| — | Hydro One Remote Communities Inc. – carries on all business relating to our ownership, operation, maintenance and construction of generation and distribution assets used in the supply of electricity to remote communities throughout Northern Ontario; and |

| — | Hydro One Telecom Inc. – carries on all of our business relating to leasing dark fibre and providing lit telecommunications capacity to other telecommunication carriers, large corporations, government, healthcare, and education institutions. |

| 2014 ANNUAL INFORMATION FORM 7 |

FORWARD-LOOKING INFORMATION FORWARD-LOOKING INFORMATION 8 HYDRO ONE INC.

| FORWARD-LOOKING INFORMATION |

FORWARD-LOOKING INFORMATION

This AIF contains, and Hydro One’s oral and written public communications often contain, forward-looking statements that are based on current expectations, estimates, forecasts and projections about the business of Hydro One and the industry in which Hydro One operates and includes beliefs and assumptions made by the management of our company.

Such statements include, but are not limited to, statements about our strategy, including our strategic objectives; statements about the general development of our business, including statements related to distribution sector consolidation, the 2013 LTEP, the Council, and customer service initiatives; statements related to the OEB’s RPP and TOU pricing, including expectations regarding the exemption of TOU pricing for certain rural customers and the timeline for converting those customers to TOU pricing; statements related to the FIT program; expectations regarding connections of new generation to our transmission and distribution systems, including their cost and impact on our systems; expectations regarding future renewable energy generation, including the possibility of incurring capital expenditures related thereto; statements regarding current and future capital expenditures and capital development projects and other investment plans including expected benefits, completion and in-service dates and our ability to recover the costs related to such projects and to obtain environmental and other regulatory approvals in connection therewith; statements regarding the reliability of our distribution and transmission systems including equipment performance; statements about our transmission and distribution capacity; expectations regarding load growth and new generation; statements about our ongoing initiatives including the expected results and their completion dates; expectations regarding NERC/NPCC standards, expected timing of

required compliance/exceptions, the cost impact of their adoption, and possible recovery of these costs in rates; statements about smart meters; statements about CDM programs and targets; statements related to the buildout of an ADS for our distribution business, including future investments and the recoverability of those investments; statements related to the expiry of labour agreements, the attraction and retention of staff and the maintenance and development of the skills and competence of existing employees; statements regarding the Broader Public Sector Executive Compensation Act, 2014; statements about our outsourcing arrangements; expectations regarding environmental expenditures and other environmental matters including potential future costs related to PCBs, asbestos, herbicide and land assessment and remediation, our ability to recover such costs and the need for environmental approvals and assessments; statements relating to health and safety initiatives and opportunities; expectations related to amendments to electricity industry codes; statements regarding the RRFE; expectations regarding our operating agreement with the IESO; statements regarding our transmission and distribution rates and customer bill impacts resulting from our rate applications; statements related to our connection assets including recovery of costs related thereto; expectations regarding developments in the statutory and operating framework for electricity distribution and transmission in Ontario including changes to rates, rate orders, cost recovery, rates

| 2014 ANNUAL INFORMATION FORM 9 |

| FORWARD-LOOKING INFORMATION |

of return and rate structures in both our transmission and distribution businesses; expectations regarding the recoverability of our expenditures in future rates and the effects it may have; statements related to the filing and status of our applications to the OEB and the timing of decisions from the OEB; statements regarding the Ontario Clean Energy Benefit Act, 2010; statements relating to our relationship with the Province, including the possibility of the Province making declarations pursuant to our memorandum of agreement with them; statements relating to IT system failures or security breaches; expectations regarding workforce demographics; statements regarding our borrowing requirements; the estimated impact of changes in the forecasted long-term Government of Canada bond yield (used in determining our regulated rate of return) on our net income; expectations regarding anticipated expenditures associated with transferring assets located on Reserves and negotiation of rental terms; statements regarding provincial ownership of our transmission corridors; statements regarding future pension contributions and our pension plan; our expectation regarding our need for the OEFC indemnity associated with the original transfer orders; expectations regarding implementation of health and safety programs; statements regarding labour relations; and legal proceedings in which we are currently involved. Words such as “aim”, “could”, “would”, “expect”, “anticipate”, “intend”, “attempt”, “may”, “plan”, “will”, “believe”, “seek”, “estimate”, and variations of such words and similar expressions are intended to identify such forward-looking statements. These statements are not guarantees of future performance and involve assumptions and risks and uncertainties that are difficult to predict. Therefore, actual outcomes and results may differ materially from what is expressed, implied or forecasted in such forward-looking statements. Hydro One does not intend,

and Hydro One disclaims any obligation to update any forward-looking statements, except as required by law.

These forward-looking statements are based on a variety of factors and assumptions including, but not limited to: no unforeseen changes in the legislative and operating framework for Ontario’s electricity market; favourable decisions from the OEB and other regulatory bodies concerning outstanding rate and other applications; no delays in obtaining the required approvals; no unforeseen changes in rate orders or rate structures for our distribution and transmission businesses; no unfavourable changes in environmental regulation; continued use of U.S. GAAP; a stable regulatory environment; and no significant event occurring outside the ordinary course of business of our company. These assumptions are based on information currently available to Hydro One including information obtained by Hydro One from third-party sources. Actual results may differ materially from those predicted by such forward-looking statements. While Hydro One does not know what impact any of these differences may have, its business, results of operations, financial condition and its credit stability may be materially adversely affected. Factors that could cause actual results or outcomes to differ materially from the results expressed or implied by forward-looking statements include, among other things:

| — | the risks associated with being controlled by the Province including the possibility that the Province may make declarations pursuant to our memorandum of agreement with it, the Province could mandate the selling of all or part of our distribution business, as well as potential conflicts of interest that may arise between us, the Province and related parties; |

| 10 HYDRO ONE INC. |

| FORWARD-LOOKING INFORMATION |

| — | the risks associated with being subject to extensive regulation including risks associated with OEB action or inaction; |

| — | the timing and results of regulatory decisions regarding our revenue requirements, cost recovery and rates; |

| — | the risk that previously granted regulatory approvals may be subsequently challenged, appealed or overturned; |

| — | the risk to our facilities posed by severe weather conditions, natural disasters or catastrophic events and our limited insurance coverage for losses resulting from these events; |

| — | opposition to and delays or denials of the requisite approvals and accommodations for projects necessary to increase transmission and distribution capacity; |

| — | the risk that we may incur significant costs associated with transferring assets located on Reserves; |

| — | the risks associated with information system security, with maintaining a complex information technology system infrastructure, and with transitioning most of our financial and business processes to an integrated business and financial reporting system; |

| — | the risks related to our work force demographic and our potential inability to attract and retain qualified personnel; |

| — | the ability to negotiate appropriate collective agreements; |

| — | the risk of labour disputes; |

| — | the ability to maintain compliance with our licence requirements in the event of a labour dispute; |

| — | the risk that we are not able to arrange sufficient cost-effective financing to repay maturing debt and to fund capital expenditures and other obligations; |

| — | the risks associated with the execution of our capital and maintenance programs necessary to maintain the performance of our aging asset base; |

| — | the potential for substantial and currently undetermined or underestimated environmental costs and liabilities; |

| — | the risk that assumptions that form the basis of our recorded environmental liabilities and related regulatory assets may change; |

| — | the risk that future environmental expenditures are not recoverable in future electricity rates; |

| — | the risk that the presence or release of hazardous or harmful substances could lead to claims by third parties and/or governmental orders; |

| — | the risk that it may be determined that exposure to electric and magnetic fields emanating from power lines and other electric sources may cause health problems; |

| — | the potential impact of not being able to recover our pension costs; |

| — | future interest rates, investment returns, changes in benefits and changes in actuarial assumptions; |

| — | the potential that we may incur significant expenses to replace some or all of the functions currently outsourced if our agreements with Inergi LP or Brookfield Johnson Controls Canada LP are terminated or expire before a new service provider is selected; |

| 2014 ANNUAL INFORMATION FORM 11 |

| FORWARD-LOOKING INFORMATION |

| — | the risks of counter-party default on our outstanding derivative contracts; |

| — | the risks associated with changes in interest rates or discount rates; |

| — | the risks associated with changes in the forecast long-term Government of Canada bond yield; |

| — | changes in the electricity industry requiring changes to investment needs not foreseen in long-term rate forecasting; |

| — | the risk that unexpected capital expenditures may be needed to support renewable generation or resolve unforeseen technical issues; |

| — | the risk that we will be unable to source the materials necessary to support our work programs; |

| — | the risk that load or consumption could fall below projected levels; |

| — | unanticipated changes in our costs; |

| — | the impact of the 2013 LTEP on our company and the costs and expenses arising therefrom; |

| — | the impact of the ownership by the Province of lands underlying our transmission system; |

| — | the inability to prepare financial statements using U.S. GAAP, or IFRS, as applicable; |

| — | actions taken by the Province resulting from the review of Ontario’s electricity sector by the Ontario Distribution Sector Review Panel; and |

| — | the impact of increased competition on our transmission business. |

Hydro One cautions you that the above list of factors is not exclusive. Some of these and other factors are discussed in more detail under “Risk Factors” in this AIF and you should review such section in detail.

In addition, Hydro One cautions you that forward-looking statements provided in this AIF concerning potential future expenditures are provided in order to provide context to the nature of some of our future plans and may not be appropriate for other purposes.

| 12 HYDRO ONE INC. |

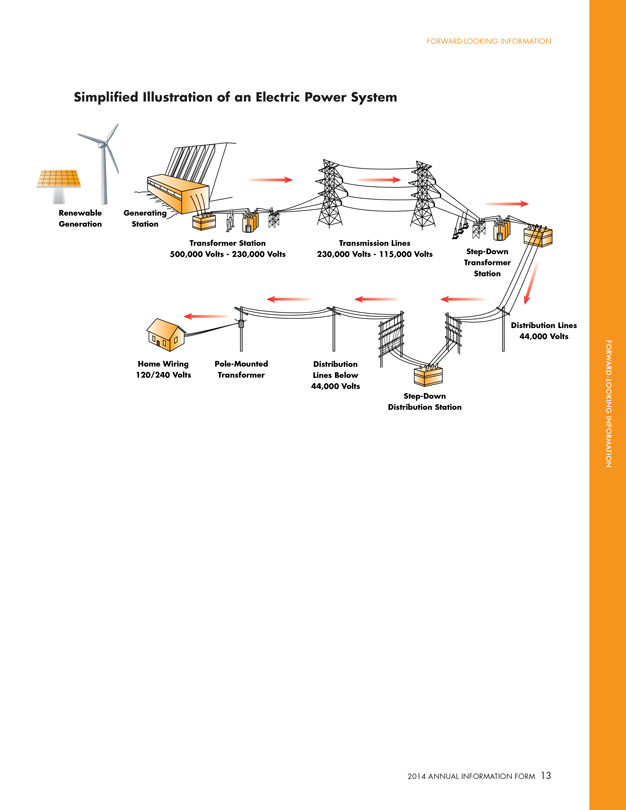

FORWARD-LOOKING INFORMATION

Simplified Illustration of an Electric

Power System

Renewable Generation

Generating Station

Transformer Station 500,000 Volts - 230,000 Volts

Transmission Lines 230,000 Volts - 115,000 Volts

Step-Down Transformer Station

Distribution Lines 44,000 Volts

Step-Down Distribution Station

Distribution Lines Below 44,000 Volts

Pole-Mounted Transformer

Home Wiring 120/240 Volts

2014 ANNUAL INFORMATION FORM 13

FORWARD-LOOKING INFORMATION

ABOUT HYDRO ONE

ABOUT HYDRO ONE

14 HYDRO ONE INC.

| ABOUT HYDRO ONE |

ABOUT HYDRO ONE

Hydro One is wholly owned by the Province, and our transmission and distribution businesses are regulated by the OEB. Our industry, including our company, is governed within the broad legislative framework of the Electricity Act and the OEB Act.

Our AIF provides material information about us and our business in the context of historical and future developments. Our AIF describes our company and our operations, risks and other factors that impact our business.

Our Mission and Vision

Our mission and vision are driven by our values: health and safety, excellence, stewardship and innovation. We live our values every day in everything we do and they represent what is most important to us.

As stewards of the Province’s electricity grid, our core role is to provide safe, reliable and cost-effective electricity transmission and distribution and to connect clean and renewable sources of generation to Ontario’s electricity grid.

Our Strategy

Our corporate strategy builds on our strong commitment to the Province and is shaped by our values. It lays out a set of objectives to position our company to achieve our mission and vision which is to be an innovative and trusted company delivering electricity safely, reliably and efficiently to create value for our customers. Our values represent our core beliefs:

| — | Health and safety: Nothing is more important than the health and safety of our employees, those who work on our property, and the public. |

| — | Excellence: We achieve excellence through continuous training, ensuring we are prepared and equipped to deliver high-quality and affordable service, with integrity. |

| — | Stewardship: We invest in our assets and people to build a safe, environmentally sustainable electricity network in a commercial manner. |

| — | Innovation: We innovate through new processes, people and technology to allow us to find better ways to meet the needs of our customers. |

We have eight strategic objectives that are inextricably linked. They drive the fulfillment of our mission and vision and ensure we remain focused on achieving our corporate goal of providing safe, reliable and affordable service to our customers, today and tomorrow, while increasing enterprise value for our shareholder.

Creating an injury-free workplace and maintaining public safety. Health and safety must be integrated into all that we do as we continue to reinforce that nothing is more important than the health and safety of our employees. We will continue to create a passion for preventing injury, staying safe and keeping each other safe. We will invest in building a culture of accountability to continue our drive to zero injuries in the workplace. In addition, we will continue to strengthen our already strong safety culture through our Journey to Zero initiative and our successful certification to the OHSAS 18001 standard.

Satisfying our customers. We exist to serve our customers, and serving our customers means reducing costs, improving customer service and meeting their expectations regarding reliable power supply. We will continue to focus our efforts

| 2014 ANNUAL INFORMATION FORM 15 |

| ABOUT HYDRO ONE |

to improve our relationship with customers and to improve our customers’ satisfaction with us. We will meet our commitments, make customers our focus in all planning discussions, communicate effectively, coordinate across our company, and maximize opportunities to improve our corporate image and every customer interaction. We will develop and deliver targeted customer segment strategies, products and delivery channels that will respond to their unique needs.

Continuous innovation. Innovation represents one of our values and is critical to achieving our mission and vision. We have been using innovation and technology to build the foundation of our company as the utility of the future. Over the next two decades, we will continue to build on that foundation to improve the reliability and efficiency of our transmission and distribution systems and provide our customers with more capability to manage their power costs. The development of the ADS is a key element in our investment in innovation, as are the investments we have made, through our Cornerstone project, in next generation business tools to enable us to implement leading industry practices and increase productivity.

Building and maintaining reliable, affordable transmission and distribution systems. Our transmission strategy is to provide a robust and reliable provincial grid that accommodates Ontario’s emerging generation profile, manages an aging asset base and meets demand requirements through prudent expansion and effective maintenance. Our distribution strategy is focused on continuing to meet the challenge of providing reliable, affordable service to our customers in a wide range of geographical regions and climate zones; incorporating ADS technology to provide greater visibility; and

increased control and improved customer service. We will meet customer expectations regarding reliability, in part through our investment planning process, which starts with the identification of asset and customer needs.

Protecting and sustaining the environment for future generations. Consistent with our value of stewardship, we play a central role in reducing Ontario’s carbon footprint through the delivery of clean and renewable energy and through measures that allow our customers to manage and reduce their energy use.

Championing people and culture. We believe our primary strength is the capability of our people. In order to sustain this advantage, we will continue to address the issues of corporate culture, labour demographics, diversity, development of critical core competencies, and skill and knowledge retention. We will continue to develop a culture of accountability and trust as a key component to fostering employee engagement. Our labour strategy is to consolidate and clarify our collective agreements, increase flexibility and reduce costs and maintain a progressive relationship with our unions.

Maintaining a commercial culture that increases value for our shareholder. For the delivery component of a customer bill, we are committed to maintaining total annual bill impacts for an average residential customer at or below the rate of inflation, and delivering income and dividends to our shareholder. We will pursue growth opportunities through LDC consolidation to increase the enterprise value of our company by leveraging our existing assets, technologies, capabilities, unparalleled experience in LDC acquisitions and our distribution and transmission footprint.

| 16 HYDRO ONE INC. |

| ABOUT HYDRO ONE |

Achieving productivity improvements and cost-effectiveness. To achieve our mission and vision, we must constantly strive for productivity through efficiency and effective management of costs. Productivity is key to meeting our other strategic objectives and, in particular, to achieving value for our customers and our shareholder.

Corporate Awards

In 2014, Hydro One was one of the six LDCs honoured by the State of New Jersey in recognition of our support in the recovery efforts from Hurricane Sandy. Additionally, we were presented with the Utility Analytics Institute’s 2014 Innovation Award in Grid Analytics for the creation and implementation of an asset analytics application tool.

In 2013, we were presented with the OHSAS 18001 Standard award from the Occupational Health and Safety Assessment Series for Hydro One’s commitment to continual health and safety improvement. Further, in 2014, we successfully completed our first annual Surveillance Audit required for our company to maintain our certification under the OHSAS 18001 Standard.

| 2014 ANNUAL INFORMATION FORM 17 |

GENERAL DEVELOPMENT OF THE BUSINESS

GENERAL DEVELOPMENT OF THE

BUSINESS

18 HYDRO ONE INC.

| GENERAL DEVELOPMENT OF THE BUSINESS |

GENERAL DEVELOPMENT OF THE BUSINESS

The following is a description of our company’s business and how it has developed, with a particular emphasis on the past three years. In this section, we will describe the electricity sector landscape, as well as recent industry activity, and recent developments.

| Electricity Sector Landscape | ||

| As a participant in the Ontario electricity sector, our company is affected by the following key parties in the electricity sector in Ontario. | ||

|

OEB |

||

| The OEB is the principal regulator of Ontario’s electricity industry. It is an independent adjudicative tribunal that regulates Ontario’s electricity sector in the public interest, and ensures an adequate level of consumer protection in the energy market. The OEB licenses all participants in the electricity sector, including the IESO, generators, transmitters, distributors, wholesalers and retailers. The OEB’s mandate and authority come from the OEB Act, the Electricity Act, and a number of other provincial statutes.

|

| |

|

OPA and IESO |

||

| The OPA was created in 2004 by virtue of an amendment to the Electricity Act, as a non-profit corporation without share capital, licensed and regulated by the OEB. Part II.1 of the Electricity Act defined its objects and the OPA had a mandate to ensure the adequacy and efficiency of electricity supply in Ontario through planning of electricity supply and demand.

The IESO is the system controller of Ontario’s electricity system. The IESO manages the reliability of Ontario’s power system, forecasts the demand and supply of electricity and co-ordinates emergency preparedness for Ontario’s electricity system. The IESO also operates the wholesale electricity market, while ensuring fair competition through market surveillance.

The OPA and the IESO were amalgamated effective January 1, 2015.

|

|

| 2014 ANNUAL INFORMATION FORM 19 |

| GENERAL DEVELOPMENT OF THE BUSINESS |

2013 Long-Term Energy Plan

On December 2, 2013, the Province released its updated Long-Term Energy Plan, the 2013 LTEP, replacing the 2010 LTEP. The 2013 LTEP sets out the Province’s plan of action for the energy sector, including strategies for mitigating increases in electricity rates; continued renewable energy procurement; nuclear refurbishment; enhanced regional planning with respect to energy infrastructure; transmission enhancements; encouraging Aboriginal participation in energy development, transmission and conservation projects; and the expansion of natural gas infrastructure. The plans are guided by the goal of balancing five core principles: cost-effectiveness, reliability, clean energy, community engagement, and CDM. Pursuant to the 2013 LTEP, the Province “will encourage OPG and Hydro One to explore new business lines and opportunities inside and outside Ontario. These opportunities will help leverage existing areas of expertise and grow revenues for the benefit of Ontarians”. The Province expects Hydro One to begin planning for a new Northwest bulk transmission line, west of Thunder Bay (the “North West Bulk Transmission Line Project”), with the project scope to be recommended by the OPA. On October 1, 2014, Hydro One received correspondence from the OPA requesting that the project commence development according to the scope and timing contained within the letter. Subsequently, the Company applied to the OEB for a variance account to track the project’s development costs for future recovery. The application is now in the interrogatory phase.

Recent Industry Activity

Premier’s Advisory Council on Government Assets

On April 11, 2014, the Province announced the appointment of the Premier’s Advisory Council on Government Assets to provide the Province with

recommendations designed to maximize the value of certain provincially owned assets, one of which being the Company. The objective of the review is to advise the Province on how to best maximize value from its assets. The Council’s Terms of Reference provided guidance indicating that it would give preference to continued ownership of government assets, but would consider mergers, acquisitions and divestments if there is a strong business case, and would enhance value to taxpayers of the Province.

The interim report released on November 19, 2014, noted the Company’s transmission business is a well-run entity with some opportunities to deliver savings on the operating side and on capital expenditures, and recommended that the Province maintain its ownership of the Company’s transmission business. The interim report noted that Ontario’s local electricity distribution system is an unnecessarily cluttered and fragmented system with too many entities, some of which are highly inefficient, unable to adapt to the changing environment and lack capital to modernize or consolidate.

Consequently, the Council recommended that the Company’s transmission and distribution businesses be separated, and that Hydro One Networks Inc.’s distribution business and Hydro One Brampton Networks Inc. be used to spur industry consolidation. The Council also recommended that the Province reduce its interest in our Company’s distribution business by bringing in private sector investment.

The Province has now asked the Council to build on its work by entering phase two, which includes the Council receiving and discussing written ideas related to encouraging consolidation and to Hydro One Brampton Networks Inc. and Hydro One Networks Inc.’s distribution business, and

| 20 HYDRO ONE INC. |

| GENERAL DEVELOPMENT OF THE BUSINESS |

finalizing its recommendations to the Province. We understand that the Province is specifically considering the sale of Hydro One Brampton Networks Inc., as well as the distribution business of Hydro One Networks Inc.

Customer Service Initiatives

During 2014, we focused tremendous effort on serving our customers and building stronger relationships. Through a series of three teletownhalls, we spoke to more than 60,000 customers from across Ontario and received their feedback on how we serve them and their ideas on making it easier to do business with Hydro One. To further improve our customer service performance culture, we have recently announced two initiatives: our draft customer commitments and a third party expert Customer Service Advisory Panel. Our customer commitments will form the basis of our promises to our customers, and the Customer Service Advisory Panel will provide advice and hold us accountable to the promises we make to our customers. Once our customer commitments are finalized with input received from our customers, our employees and our Customer Service Advisory Panel, we will develop a public scorecard and will report on our performance as a transparent, accountable and customer focused organization. Service levels of our billing system and at our call centre are now better than they were before we implemented our new billing system and we have set new targets that, when achieved, will put us among the best in the business.

Distribution Sector Consolidation

In 2009, the transfer tax exemption applicable when publicly owned utilities sell electricity distribution assets to other publicly-owned utilities in Ontario was made permanent by the Province. In April 2012, the Province announced it was launching a comprehensive review of Ontario’s

electricity sector to explore options to improve efficiencies, including LDC consolidation. As a result, the Province created the Ontario Distribution Sector Review Panel (the “Panel”). In December 2012, the Panel released its report, “Renewing Ontario’s Electricity Distribution Sector: Putting the Consumer First,” with recommendations for electricity sector consolidation. This report recommended that the 73 LDCs comprising the focus of the report be consolidated into eight to 12 larger regional electricity distributors within a two-year timeframe. Specifically, it recommended there be two regional distributors in northern Ontario and between six and 10 regional distributors in southern Ontario with a minimum of 400,000 customers each. Given our company’s position as the largest LDC, the report recommended that Hydro One Networks Inc. be given unambiguous direction to lead and engage in the discussion of the merger of distribution assets with the appropriate interested utilities on a commercial basis. The Minister subsequently indicated he was supportive of voluntary consolidation and expects all LDCs to pursue innovative partnerships and transformative initiatives that will result in electricity ratepayer savings.

As the utility sector began to assess the impact of the Panel’s recommendations, Hydro One was an active participant in the competitive sale process of several LDCs. Hydro One was the successful proponent in three acquisitions in 2014: Norfolk Power Inc. (“Norfolk Power”), Woodstock Hydro Holdings Inc. (“Woodstock Hydro”), and Haldimand County Utilities Inc. (“Haldimand Hydro”).

In April 2013, Hydro One entered into an agreement with the Corporation of Norfolk County (“Norfolk County”) to purchase all the outstanding shares of Norfolk Power for approximately

| 2014 ANNUAL INFORMATION FORM 21 |

| GENERAL DEVELOPMENT OF THE BUSINESS |

$93 million, subject to OEB approval. On July 3, 2014, the OEB issued its Decisions and Order for our company to acquire all of the outstanding shares of Norfolk Power and for the transfer of Norfolk Power Distribution Inc.’s (the distribution company of Norfolk Power) distribution system to Hydro One Networks Inc.

In August 2014, we completed the Norfolk Power acquisition transaction. The total purchase price for Norfolk Power, net of the long-term debt assumed and adjusted for preliminary working capital and other closing adjustments was approximately $68 million.

In May 2014, we entered into an agreement with the City of Woodstock to purchase all outstanding shares of Woodstock Hydro for approximately $46 million, subject to OEB approval. Hydro One will pay the City of Woodstock approximately $29 million, being the enterprise value of Woodstock Hydro, net of Woodstock Hydro’s existing debt of approximately $17 million. Woodstock Hydro is the holding company which owns Woodstock Hydro Services Inc., a local distribution company serving the City of Woodstock. Hydro One filed its MAAD

Application on July 9, 2014 seeking OEB approval of the acquisition of Woodstock Hydro. An oral hearing for this application was held in January 2015.

In June 2014, we entered into an agreement with Haldimand County to purchase all of the outstanding shares of Haldimand Hydro for approximately $75 million, subject to OEB approval. Hydro One will pay Haldimand County approximately $65 million, being the enterprise value of Haldimand Hydro, net of Haldimand Hydro’s existing debt of approximately $10 million. Haldimand Hydro is the holding company which owns Haldimand County Hydro Inc., a local distribution company, and Haldimand County Energy Inc., a non-rate-regulated telecom company. Hydro One filed its MAAD Application on July 31, 2014 seeking OEB approval of the acquisition of Haldimand Hydro.

We intend to continue to consider growth opportunities through LDC consolidation by leveraging our existing assets, technologies, capabilities, unparalleled experience in LDC acquisitions and our distribution footprint.

| 22 HYDRO ONE INC. |

| GENERAL DEVELOPMENT OF THE BUSINESS |

Regulated Price Plan Structure

On April 1, 2005, the OEB implemented the RPP. The RPP regulates only the commodity price of electricity and does not affect the rates charged for transmission and distribution of electricity. Prices are developed using the RPP Manual methodology involving two essential steps; forecasting the total RPP supply cost for twelve months and establishing prices to recover the

forecast supply cost for RPP consumers over the period. The price structures are designed to make their consumption weighted average price equal to the average supply cost. There are two price structures: tiered pricing and TOU pricing. A consumer with an average load profile will pay the same average price under either price structure.

|

RPP Pricing (per kWh)

|

||||

|

Winter (Nov. 1, 2013 – April 30, 2014)

|

Lower Tier Price

|

8.3 cents

| ||

|

Upper Tier Price

|

9.7 cents | |||

|

Summer (May 1, 2014 – Oct. 31, 2014)

|

Lower Tier Price |

8.6 cents | ||

|

Upper Tier Price

|

10.1 cents | |||

|

Winter (Nov. 1, 2014 – April 30, 2015)

|

Lower Tier Price

|

8.8 cents

| ||

|

Upper Tier Price

|

10.3 cents |

TOU Pricing Structure

TOU pricing structure is for consumers with eligible smart meters. One of the OEB’s goals through TOU pricing is to provide an incentive for consumers to shift some consumption away from periods of high total consumption (called “on-peak”) to periods of low demand (called “off-peak”). On August 4, 2010, the OEB issued its final determination to mandate TOU pricing for RPP customers. All eligible Hydro One distribution customers were migrated to TOU billing as of June 2011, except certain customers located in very

rural and very sparsely populated areas. On December 1, 2014, Hydro One filed a request for a five year exemption extension for 120,000 hard-to-reach customers and requested permission to migrate an additional 50,000 customers back to tiered pricing as it is not economically feasible to consistently provide actual readings from these meters. An interim Decision dated December 18, 2014, has granted the exemption until June 30, 2015 or until a final Decision has been issued. Below is a chart outlining the TOU periods and the prices.

| 2014 ANNUAL INFORMATION FORM 23 |

| GENERAL DEVELOPMENT OF THE BUSINESS |

RPP Pricing (per kWh) –TOU Prices

|

Winter (Nov. 1, 2013 – April 30, 2014) |

Off-peak Price 7pm – 7am Weekdays, Weekends and Holidays

|

7.2 cents | ||

| Mid-peak Price 11am – 5pm Weekdays

|

10.9 cents | |||

|

On-peak Price 7am – 11am, 5pm – 7pm Weekdays

|

12.9 cents | |||

| Summer (May 1, 2014 – Oct. 31, 2014) |

Off-peak Price 7 pm – 7 am Weekdays, Weekends and Holidays

|

7.5 cents | ||

|

Mid-peak Price 7 am – 11 am, 5 pm – 7 pm Weekdays

|

11.2 cents | |||

|

On-peak Price 11 am – 5 pm Weekdays

|

13.5 cents | |||

|

Winter (Nov. 1, 2014 – April 30, 2015) |

Off-peak Price 7 pm – 7 am Weekdays, Weekends and Holidays

|

7.7 cents | ||

|

Mid-peak Price 11 am – 5 pm Weekdays

|

11.4 cents | |||

|

On-peak Price 7 am – 11 am, 5 pm – 7 pm Weekdays

|

14.0 cents |

New RPP prices are computed at six-month intervals and are the result of an integrated consideration of rebasing and true-ups.

| 24 HYDRO ONE INC. |

| GENERAL DEVELOPMENT OF THE BUSINESS |

Procurement of New Generation

Pursuant to a directive from the Province, the OPA set up the FIT program for procurement of renewable generation. The program is currently divided into three streams:

| — | Micro FIT (projects up to 10 kW); |

| — | Small FIT (projects between 10 kW and generally up to 500 kW depending on connection voltage); and |

| — | Large Renewable Procurement (competitive bids for projects generally greater than 500 kW) – this program has not been finalized. |

All such projects may result in connection to Hydro One Networks Inc.’s distribution or transmission systems. Under the FIT program, the OPA has entered into contracts or conditional contracts with generation proponents pursuant to which the OPA will pay a fixed rate for power produced over a specified period of time. Hydro One continues to connect projects for which there are firm contracts.

In May 2013, the Province announced that it would make 900 MW of new capacity available between 2013 and 2018 for the Small FIT and Micro FIT programs. The Province has set annual procurement targets, from 2014 onwards, of 150 MW for Small FIT generation and 50 MW for Micro FIT generation. The Province is working with the OPA to develop a competitive process for renewable energy generation projects above 500 kW which is expected to launch in 2015.

Recent Developments at Hydro One

Sustainable Electricity Company Designation

In January 2015, Hydro One Networks Inc. was designated a “Sustainable Electricity Company”. The Sustainable Electricity Company™ brand mark is a designation established by the Canadian Electricity Association. Companies that wish to use the Sustainable Electricity Company™ brand mark must commit to core subjects, issues and related actions and expectations contained in the standard that are deemed applicable and significant to the company and its stakeholders. The brand mark is granted for five years, with the option for renewal thereafter. The use of the Sustainable Electricity Company™ brand mark demonstrates Hydro One’s commitment to responsible environmental, social and economic practices, and to the principles of sustainable development.

| 2014 ANNUAL INFORMATION FORM 25 |

| OVERVIEW OF HYDRO ONE |

OVERVIEW OF HYDRO ONE

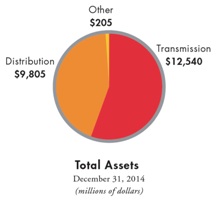

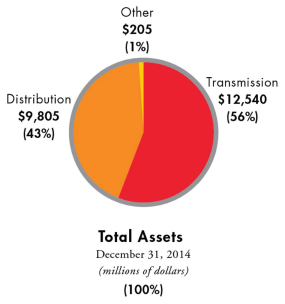

We are the largest electricity transmission and distribution company in Ontario. We own and operate substantially all of Ontario’s electricity transmission system, accounting for approximately 97% of Ontario’s transmission capacity based on revenue approved by the OEB.

Based on assets, our transmission system is one of the largest in North America and our distribution system is the largest in Ontario. We have three reportable segments: (1) our transmission business; (2) our distribution business; and (3) our other business.

Our transmission business, which represented approximately $12.5 billion of our total assets of $22.5 billion as at December 31, 2014, being approximately 56% of our total assets, transmits electricity through a high-voltage network from generators to our own distribution networks, to LDCs, and to transmission-connected companies. We also own and operate facilities that interconnect our transmission system with systems in neighbouring provinces and states.

Our distribution business, which represented approximately $9.8 billion of our total assets of $22.5 billion as at December 31, 2014, being approximately 43% of our total assets, distributes electricity through our low-voltage distribution system to municipalities and to rural areas. Customers of our distribution business include LDCs, customers with loads exceeding 5 MW, and rural and urban customers.

Hydro One Brampton Networks Inc. is our urban distribution company serving customers in the City of Brampton, Ontario. We also operate, through our subsidiary Hydro One Remote Communities Inc., small, regulated generation and distribution systems in remote communities across Northern Ontario that are not connected to Ontario’s electricity grid.

Our other business segment is primarily represented by the operations of Hydro One Telecom Inc. This subsidiary markets dark and lit fibre-optic capacity to telecommunications carriers and commercial customers with broadband network requirements. The assets of this segment constituted approximately $0.2 billion of our total assets of $22.5 billion as at December 31, 2014, being approximately 1% of our total assets.

| 2014 ANNUAL INFORMATION FORM 27 |

| DESCRIPTION OF THE BUSINESS |

DESCRIPTION OF THE BUSINESS

Our Business Segments

Our Transmission Business

Overview

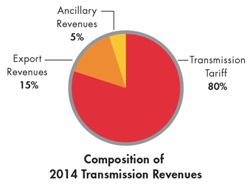

Our transmission system operates at 500 kV, 230 kV and 115 kV and transmits electricity to customers consisting of 46 LDCs, our own distribution businesses and 90 transmission-connected companies. Electricity is also delivered to utilities in other jurisdictions through Interties. Electricity is supplied by generators, both within and outside Ontario, of which 113 in Ontario are connected directly to the transmission grid. Our transmission system serves approximately five million customers, directly or indirectly, and transported approximately 139.8 TWh of energy throughout Ontario in 2014. Revenues from our transmission business accounted for approximately 24% of our total revenues in 2014 and approximately 25% and 26% of our total revenues in 2013 and 2012, respectively.

Our transmission system forms an integrated transmission grid that can be divided into two categories based on function. The bulk system operates primarily at 500 kV or 230 kV over relatively long distances and links major sources of generation to transmission stations and larger area load centres. The area supply system operates at 230 kV or 115 kV and links the bulk system to local generators and loads, such as LDCs, industrial customers and our own retail distribution operations. Transmission stations located near load centres step down the high voltage to the level required for retail distribution systems or end-use customers connected directly to our transmission system.

Our transmission system is interconnected with the North American eastern system that is comprised of virtually all of the electric utilities east of the Continental Divide. Our transmission business owns and operates 26 Interties at 345 kV, 230 kV and 115 kV levels with New York (7), Quebec (11), Michigan (4), Manitoba (3) and Minnesota (1).

Through these 26 Interties, the IESO, in its report “Ontario Transmission System” dated November 27, 2014, estimates that, in the summer, with all transmission elements in service, the theoretical maximum capability for exports is up to 5,960 MW and for imports is up to 6,631 MW; in the winter, the theoretical maximum capability for exports is 6,295 MW and for imports is 6,963 MW respectively. In operation, the actual import and export capabilities may be restricted significantly by limitations within our or another jurisdiction’s transmission networks, unscheduled power flows between interconnected systems and local load and generation patterns.

Our transmission system is relatively free of restrictions in its ability to supply electricity to major load centres from generating sources located across Ontario, although there are certain short duration periods when the transmission constraints restrict economical utilization of generation. A 500 kV system serves as the transmission “backbone” around the GTA with 500 kV connections to Northern Ontario, Ottawa, London and the major generating facilities in Ontario. As new generation projects are assessed in Ontario, the impact on the transmission system is assessed and where required, transmission investment plans are initiated in a timely manner.

| 2014 ANNUAL INFORMATION FORM 29 |

| DESCRIPTION OF THE BUSINESS |

This section on our transmission business consists of five topics:

| 1. | Transmission Planning |

| 2. | Transmission Assets |

| 3. | Transmission Capital Expenditure Plans |

| 4. | NERC/NPCC |

| 5. | NERC Critical Infrastructure Protection Standards |

1. Transmission Planning

Hydro One develops transmission plans for new transmission facilities and for refurbishment and replacement of existing transmission facilities, as required. The plans for new facilities identify proposed equipment, configuration, routing and resulting capacities for network, local area and connection/transformation investments. We consult with customers to determine the need, timing and technical solutions for new connection/ transformation facilities. We also consult with affected communities, stakeholders and First Nations and Métis communities whose rights may be potentially impacted as part of the project development process for new or upgraded transmission lines.

The need for additional network and local area capabilities is determined in consultation with the OPA (which plans future generation and CDM programs) and customers and in response to governmental policy and direction. The need for short-term and long-term solutions may also be highlighted in the reliability reports issued by the IESO. The IESO assesses the system impact of proposed facilities based on requests by Hydro One, as required by the Market Rules. Projects involving new transmission lines longer than two kilometres are subject to the OEB’s leave-to-construct approval. The EA approval requirements for a “transmission line” or “transmission station” are prescribed in Ontario Regulation 116/01 made under the EA. Whether or not a particular

project is subject to class environmental or an individual environmental assessment approval is dependent on that particular project.

Hydro One’s plans to maintain, refurbish or replace existing facilities are developed on the basis of maintenance standards, asset condition assessments and end-of-life criteria specific to each type of equipment. Priorities are assigned to each type of investment based on the risks that it mitigates. These investment plans are also included in our rate filings submitted to the OEB.

2. Transmission Assets

Our transmission assets can be divided into four functional categories:

| A. | Transmission Stations, |

| B. | Transmission Lines, |

| C. | Network Operations, and |

| D. | Telecommunications Facilities. |

A. Transmission Stations

Transmission station facilities are used for the delivery of power, voltage transformation and switching, and serve as connection points for both customers and generators.

Transmission stations can be broadly classified into two categories. The first category consists of

| 30 HYDRO ONE INC. |

| DESCRIPTION OF THE BUSINESS

|

terminal stations, including switchyards located at generating facilities, which are used mainly for switching and voltage transformation between the 500 kV, 230 kV, and 115 kV systems. The second category consists of customer supply stations, which are transmission stations that deliver power from the transmission system to wholesale customers. Currently, most transmission stations used for customer supply consist of paired circuits and step-down transformers that are meant to ensure that the failure of any one element will not result in a permanent loss of supply. For smaller or remote loads, a simpler station design with a single transformer or a single circuit is used.

Our transmission system includes 290 transmission stations whose components may include high voltage power transformers, power circuit breakers, high voltage switches, capacitor and reactor banks, protection and control systems, metering and monitoring systems together with site infrastructures such as buildings and security systems.

B. Transmission Lines

Our transmission lines are classified into bulk power transmission lines and area supply lines. Bulk power transmission lines are main lines delivering power from generating stations or interconnections to receiving terminal stations. Bulk power transmission lines are part of the integrated transmission network and generally operate at 500 kV or 230 kV, with a few at 115 kV. Area supply lines take power from the transmission network at the receiving stations and transmit it to customer supply transmission stations at customer load centres. The usual voltage levels of area supply lines are 230 kV or 115 kV. All of these lines are overhead except for approximately 271 circuit kilometres of underground cables in urban areas.

The transmission system includes approximately 29,000 circuit kilometres of high voltage lines whose major components consist of cables, conductors, wood or steel support structures, foundations, insulators, connecting hardware and grounding systems.

C. Network Operations

All of our transmission assets and many of our sub-transmission assets are managed from one central location, the OGCC. As owners and operators of the largest portion of the Ontario transmission network, we have the responsibility under the Electricity Act to ensure that our assets are operated in a safe and reliable manner which optimizes connection performance to our customers.

Accordingly, the OGCC is the controlling authority for our company’s transmission network and for large portions of the sub-transmission network. The OGCC is an operating centre that monitors and controls our transmission and sub-transmission networks via the Network Management System. With this computer system, the OGCC remotely monitors and operates transmission equipment, responds to alarms and contingencies, and can restore and reroute interrupted power.

| 2014 ANNUAL INFORMATION FORM 31 |

| DESCRIPTION OF THE BUSINESS

|

The OGCC reviews, approves, performs and/or authorizes all switching and control actions on our transmission system and sub-transmission system assets. The OGCC also provides the dispatch function across the entire company for transmission and distribution assets. The OGCC coordinates all planned transmission and sub-transmission equipment outages with stakeholders and customers. Additionally, the OGCC is responsible for notifying affected customers of any planned distribution outages. For forced distribution outages, the OGCC creates outage tickets which contain all the relevant information for the outage, dispatches field crews, communicates estimated time of repair and confirms outage restoration with the Hydro One distribution customer.

The OGCC is fully supported by onsite customer service, engineering, operations technology, training, process and business planning staff. There is a fully functional back-up facility which would be staffed in the event of an evacuation of the OGCC.

D. Telecommunications Facilities

Our telecommunications requirements include services necessary for protection and operation of the power system as well as voice and administrative data. Power system protection

and control, and voice communications required for control and restoration of transmission and distribution assets have very stringent reliability and security requirements which must continue to be met during prolonged blackout conditions. These telecommunications requirements are vital to meeting our transmission reliability compliance obligations, ensuring the protection of our assets and ensuring efficient and rapid restoration following contingencies. These requirements are met through the use of our own facilities and services acquired from other telecommunications service providers. The reliability and availability of telecommunication services used in the protection and operation of our transmission system are vital to meeting our interconnection obligations, ensuring the protection of our assets and ensuring the reliability of our transmission system. Historically, if telecommunications service providers were not able or willing to provide the required services at an appropriate cost, we installed our own telecommunication facilities. These owned facilities include systems constructed using various communication technologies such as fibre optic and metallic cables, wireless transmission and power line carrier equipment.

3. Transmission Capital Expenditure Plans

Transmission Capital Expenditure Plans consist of four segments:

| A. | Major Transmission Capital Development Projects, |

| B. | Transmission Projects at the Local Load Connection Level, |

| C. | Transmission Sustainment, and |

| D. | Bruce to Milton Double Circuit Transmission Line. |

Capital expenditures for the transmission portion of our business for 2015 are estimated to be approximately $900 million net overall. Our capital investment plan is designed to address

| 32 HYDRO ONE INC. |

| DESCRIPTION OF THE BUSINESS

|

Ontario’s changing generation profile, accommodate load growth in areas throughout Ontario and support the expected increase in renewable energy generation in furtherance of the GEA as discussed below. Additionally, this plan seeks to sustain or improve our transmission reliability performance, which is in the top quartile ranking in Canada for transmission systems of 115 kV and 230 kV. This plan also furthers our ongoing objective of sustaining the performance of aging assets through refurbishment programs and end-of-life asset replacements.

In February 2011, the Minister issued a directive to the OEB, which in turn issued a decision and order on February 28, 2011, to amend the transmission licence of Hydro One Networks Inc. to develop and seek approval for the following projects the scope and timing of which shall be in accordance with the recommendations of the OPA (see “Regulation – Transmission – Facilities Applications”):

| 1. | upgrade one or more existing transmission lines west of London (see “Major Transmission Capital Development Projects – Lambton to Longwood Transmission Upgrade”); and |

| 2. | build a new transmission line west of London. |

Hydro One Networks Inc. has completed the upgrade of the Lambton to Longwood transmission lines. This work was placed in service in September 2014. The OPA has not yet provided Hydro One Networks Inc. with any recommendations related to the build of a new transmission line west of London.

To enable the Province’s expectations contained in the 2013 LTEP, the Minister issued a directive to the OEB dated November 27, 2013, and the OEB in turn issued a decision and order on January 9, 2014, to amend the transmission licence of Hydro

One Networks Inc. to develop and seek approval for the Northwest Bulk Transmission Line Project. The scope and timing of the Northwest Bulk Transmission Line Project shall be in accordance with the recommendations of the OPA. On October 1, 2014, Hydro One received a letter from the OPA recommending scope and timing for this project. The Province also expects Hydro One and Infrastructure Ontario to work together to explore ways to ensure that the Northwest Bulk Transmission Line Project is developed and delivered in a cost-effective manner and results in value for Ontario electricity customers. These discussions are currently underway.

Hydro One is also pursuing a number of additional projects as part of our company’s transmission investments. These projects, together with those noted above, will require various approvals, including, but not limited to, OEB approvals and EA approvals.

A. Major Transmission Capital Development Projects

Set out below are our current major transmission capital development projects for which we have obtained or are actively seeking the requisite approvals. The major transmission system capital development projects described below are at different stages of development and may not

| 2014 ANNUAL INFORMATION FORM 33 |

| DESCRIPTION OF THE BUSINESS

|

proceed to construction if requisite approvals are not obtained or if anticipated generation does not materialize.

| — | Toronto Midtown Transmission Reinforcement Project |

Supply to the midtown Toronto area is currently provided by three 115 kV circuits between Leaside TS and Wiltshire TS. These circuits supply Bridgman TS and Dufferin TS from Leaside TS and also provide load transfer capability between the Leaside TS and Manby TS. This project will replace a section of aging cable and is expected to provide additional capacity by adding one 115 kV circuit between Leaside TS and Bridgman TS. Hydro One Networks Inc. has obtained all the requisite approvals for this project and construction work is underway. The planned in-service date for the project is estimated to be late in 2015.

| — | Rebuild Hearn SS |

The existing 115 kV Hearn SS was identified by our company as due for refurbishment. The project was placed partially in service in December 2013 with the remaining work expected to be completed in 2015.

| — | Upgrade 115 kV Switch Yards at Manby TS, Leaside TS, Hawthorne TS & Allanburg TS |

To allow the incorporation of new renewable generation in the Toronto, Ottawa and Niagara areas, the short circuit capability at each of Manby TS, Leaside TS, Hawthorne TS and Allanburg TS 115 kV yards will be increased from the existing 40 kA to 50 kA by replacing the 115 kV breakers. The upgrades at Allanburg TS and Leaside TS were completed in December 2014. All breakers at Manby TS and Hawthorne TS have been replaced and the planned in-service dates for the additional station work are mid-2016 and mid-2015 respectively.

| — | Niagara Reinforcement Project |

This project comprises the construction of 76 kilometres of 230 kV line from our Allanburg TS in the Niagara area to our Middleport TS in the Hamilton area. The Niagara Reinforcement Project is designed to relieve transmission bottlenecks that limit transfer of Niagara area generation and imports from New York State. The Niagara Reinforcement Project status is considered substantially on time, with the exception that some project work has been delayed due to access issues created by a blockade related to aboriginal land claims on a section of the line. As a result, the OEB concluded that the project deserves special regulatory treatment and in its ruling of August 2007, the OEB determined that interest capitalized against this project could be expensed and recovered as a period cost from January 1, 2007. It is anticipated that the remaining construction of the project will take approximately two months to complete once a land settlement agreement has been concluded between the Province, the federal government, and the Six Nations.

| — | Lambton to Longwood Transmission Upgrade |

This upgrade involves the reconductoring of approximately 70 kilometres of 230 kV double circuit transmission line in southwestern Ontario

| 34 HYDRO ONE INC. |

| DESCRIPTION OF THE BUSINESS

|

between Lambton TS and Longwood TS with a higher capacity related conductor. The upgrade will enable the connection of approximately 300-500 MW of additional renewable generation in the area west of London. The project was approved for construction in November 2012, and placed in service in September 2014.

| — | Clarington TS (formerly Oshawa Area TS) Project |

In October 2011, the OPA requested that Hydro One develop an implementation plan and initiate work on the installation of additional autotransformer capacity at our proposed Clarington TS. In 2012, Hydro One commenced planning and environmental studies, and a draft ESR was made available for review on November 15, 2012. On closing of the review period, multiple third party requests had been submitted to the Ministry of the Environment to escalate the EA approval from a class environmental assessment to a more comprehensive individual environmental assessment. On January 2, 2014, the Minister of Environment issued a decision on the requests and ruled that an individual environmental assessment is not required for the project and advised that Hydro One can proceed with the project, subject to certain conditions. The final ESR was submitted to the Ministry of the Environment on January 16, 2014. Hydro One began construction in July 2014, and the planned in-service date is 2017.

| — | Guelph Area Transmission Refurbishment Project |