UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington D.C. 20549

________________

FORM 10-Q

(Mark One)

OF THE SECURITIES EXCHANGE ACT OF 1934

For the quarterly period ended June 30, 2024

OR

OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from ____________ to ____________

Commission file number 001-15827

(Exact name of registrant as specified in its charter)

| State of | |||||||||||

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | ||||||||||

| (Address of principal executive offices) | (Zip code) | ||||||||||

Registrant’s telephone number, including area code: (800 )-VISTEON

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||||||

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ü No__

Indicate by check mark whether the registrant: has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ü No __

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer," "accelerated filer,” "smaller reporting company" and “emerging growth company" in Rule 12b-2 of the Exchange Act.

Emerging growth company ☐

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ü

Indicate by check mark whether the registrant has filed all documents and reports required to be filed by Sections 12, 13 or 15(d) of the Securities Exchange Act of 1934 subsequent to the distribution of securities under a plan confirmed by a court. Yes ü No ☐

As of July 18, 2024, the registrant had outstanding 27,606,858 shares of common stock.

Exhibit index located on page number 38.

1

Visteon Corporation and Subsidiaries

Index

| Page | ||||||||

| Condensed Consolidated Statements of Changes in Equity (Unaudited) | ||||||||

2

Part I

Financial Information

Item 1.Condensed Consolidated Financial Statements

VISTEON CORPORATION AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF COMPREHENSIVE INCOME (LOSS)

(In millions except per share amounts)

(Unaudited)

| Three Months Ended June 30, | Six Months Ended June 30, | ||||||||||||||||||||||

| 2024 | 2023 | 2024 | 2023 | ||||||||||||||||||||

Net sales | $ | $ | $ | $ | |||||||||||||||||||

Cost of sales | ( | ( | ( | ( | |||||||||||||||||||

Gross margin | |||||||||||||||||||||||

Selling, general and administrative expenses | ( | ( | ( | ( | |||||||||||||||||||

Restructuring, net | ( | ( | ( | ( | |||||||||||||||||||

Interest expense | ( | ( | ( | ( | |||||||||||||||||||

Interest income | |||||||||||||||||||||||

Equity in net income (loss) of non-consolidated affiliates | ( | ( | ( | ||||||||||||||||||||

Other income (expense), net | ( | ( | |||||||||||||||||||||

Income (loss) before income taxes | |||||||||||||||||||||||

Provision for income taxes | ( | ( | ( | ( | |||||||||||||||||||

Net income (loss) | |||||||||||||||||||||||

Less: Net (income) loss attributable to non-controlling interests | ( | ( | ( | ( | |||||||||||||||||||

Net income (loss) attributable to Visteon Corporation | $ | $ | $ | $ | |||||||||||||||||||

Comprehensive income (loss) | $ | $ | $ | $ | |||||||||||||||||||

| Less: Comprehensive (income) loss attributable to non-controlling interests | ( | ( | ( | ||||||||||||||||||||

Comprehensive income (loss) attributable to Visteon Corporation | $ | $ | $ | $ | |||||||||||||||||||

Basic earnings (loss) per share attributable to Visteon Corporation | $ | $ | $ | $ | |||||||||||||||||||

Diluted earnings (loss) per share attributable to Visteon Corporation | $ | $ | $ | $ | |||||||||||||||||||

See accompanying notes to the condensed consolidated financial statements.

3

VISTEON CORPORATION AND SUBSIDIARIES

CONDENSED CONSOLIDATED BALANCE SHEETS

(In millions)

| (Unaudited) | |||||||||||

| June 30, | December 31, | ||||||||||

| 2024 | 2023 | ||||||||||

| ASSETS | |||||||||||

Cash and equivalents | $ | $ | |||||||||

Restricted cash | |||||||||||

Accounts receivable, net | |||||||||||

Inventories, net | |||||||||||

Other current assets | |||||||||||

Total current assets | |||||||||||

Property and equipment, net | |||||||||||

Intangible assets, net | |||||||||||

Right-of-use assets | |||||||||||

Investments in non-consolidated affiliates | |||||||||||

Deferred tax assets | |||||||||||

Other non-current assets | |||||||||||

Total assets | $ | $ | |||||||||

| LIABILITIES AND EQUITY | |||||||||||

Short-term debt | $ | $ | |||||||||

Accounts payable | |||||||||||

Accrued employee liabilities | |||||||||||

Current lease liability | |||||||||||

Other current liabilities | |||||||||||

Total current liabilities | |||||||||||

Long-term debt, net | |||||||||||

Employee benefits | |||||||||||

Non-current lease liability | |||||||||||

Deferred tax liabilities | |||||||||||

Other non-current liabilities | |||||||||||

Stockholders’ equity: | |||||||||||

Preferred stock (par value | |||||||||||

Common stock (par value $ | |||||||||||

Additional paid-in capital | |||||||||||

Retained earnings | |||||||||||

Accumulated other comprehensive loss | ( | ( | |||||||||

Treasury stock | ( | ( | |||||||||

Total Visteon Corporation stockholders’ equity | |||||||||||

Non-controlling interests | |||||||||||

Total equity | |||||||||||

Total liabilities and equity | $ | $ | |||||||||

See accompanying notes to the condensed consolidated financial statements.

4

VISTEON CORPORATION AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS

(In millions)

(Unaudited)

| Six Months Ended June 30, | |||||||||||

| 2024 | 2023 | ||||||||||

Operating Activities | |||||||||||

Net income (loss) | $ | $ | |||||||||

Adjustments to reconcile net income (loss) to net cash provided from (used by) operating activities: | |||||||||||

Depreciation and amortization | |||||||||||

Non-cash stock-based compensation | |||||||||||

Equity in net loss (income) of non-consolidated affiliates, net of dividends remitted | |||||||||||

Other non-cash items | ( | ||||||||||

Changes in assets and liabilities: | |||||||||||

Accounts receivable | ( | ( | |||||||||

Inventories | ( | ||||||||||

Accounts payable | ( | ||||||||||

Other assets and other liabilities | ( | ( | |||||||||

Net cash provided from (used by) operating activities | |||||||||||

Investing Activities | |||||||||||

Capital expenditures, including intangibles | ( | ( | |||||||||

| Loan provided to non-consolidated affiliate | ( | ||||||||||

| Other | |||||||||||

Net cash used by investing activities | ( | ( | |||||||||

Financing Activities | |||||||||||

| Short-term debt, net | |||||||||||

| Principal repayment of term debt facility | ( | ( | |||||||||

| Dividends to non-controlling interests | ( | ||||||||||

| Repurchase of common stock | ( | ( | |||||||||

| Stock based compensation tax withholding payments | ( | ( | |||||||||

| Proceeds from the exercise of stock options | |||||||||||

Net cash used by financing activities | ( | ( | |||||||||

Effect of exchange rate changes on cash | ( | — | |||||||||

Net decrease in cash, equivalents, and restricted cash | ( | ( | |||||||||

Cash, equivalents, and restricted cash at beginning of the period | |||||||||||

Cash, equivalents, and restricted cash at end of the period | $ | $ | |||||||||

See accompanying notes to the condensed consolidated financial statements.

5

VISTEON CORPORATION AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF CHANGES IN EQUITY

(In millions)

(Unaudited)

| Total Visteon Corporation Stockholders' Equity | |||||||||||||||||||||||||||||||||||||||||||||||

| Common Stock | Additional Paid-In Capital | Retained Earnings | Accumulated Other Comprehensive Income (Loss) | Treasury Stock | Total Visteon Corporation Stockholders' Equity | Non-Controlling Interests | Total Equity | ||||||||||||||||||||||||||||||||||||||||

December 31, 2023 | $ | $ | $ | $ | ( | $ | ( | $ | $ | $ | |||||||||||||||||||||||||||||||||||||

| Net income (loss) | — | — | — | — | |||||||||||||||||||||||||||||||||||||||||||

| Other comprehensive income (loss) | — | — | — | ( | — | ( | ( | ( | |||||||||||||||||||||||||||||||||||||||

| Stock-based compensation, net | — | ( | — | — | — | ||||||||||||||||||||||||||||||||||||||||||

| Share repurchase | — | — | — | — | ( | ( | — | ( | |||||||||||||||||||||||||||||||||||||||

| Acquisition of non-controlling interest | — | — | — | — | — | — | ( | ( | |||||||||||||||||||||||||||||||||||||||

March 31, 2024 | $ | $ | $ | $ | ( | $ | ( | $ | $ | $ | |||||||||||||||||||||||||||||||||||||

| Net income (loss) | — | — | — | — | |||||||||||||||||||||||||||||||||||||||||||

| Other comprehensive income (loss) | — | — | — | ( | — | ( | ( | ( | |||||||||||||||||||||||||||||||||||||||

| Stock-based compensation, net | — | — | — | — | |||||||||||||||||||||||||||||||||||||||||||

| Dividends to non-controlling interest | — | — | — | — | — | — | ( | ( | |||||||||||||||||||||||||||||||||||||||

| June 30, 2024 | $ | $ | $ | $ | ( | $ | ( | $ | $ | $ | |||||||||||||||||||||||||||||||||||||

| Total Visteon Corporation Stockholders' Equity | |||||||||||||||||||||||||||||||||||||||||||||||

| Common Stock | Additional Paid-In Capital | Retained Earnings | Accumulated Other Comprehensive Income (Loss) | Treasury Stock | Total Visteon Corporation Stockholders' Equity | Non-Controlling Interests | Total Equity | ||||||||||||||||||||||||||||||||||||||||

December 31, 2022 | $ | $ | $ | $ | ( | $ | ( | $ | $ | $ | |||||||||||||||||||||||||||||||||||||

Net income (loss) | — | — | — | — | |||||||||||||||||||||||||||||||||||||||||||

Other comprehensive income (loss) | — | — | — | — | ( | ||||||||||||||||||||||||||||||||||||||||||

| Stock-based compensation, net | — | ( | — | — | ( | — | ( | ||||||||||||||||||||||||||||||||||||||||

| Dividends to non-controlling interest | — | — | — | — | — | — | (15) | (15) | |||||||||||||||||||||||||||||||||||||||

March 31, 2023 | $ | $ | $ | $ | ( | $ | ( | $ | $ | $ | |||||||||||||||||||||||||||||||||||||

| Net income (loss) | — | — | — | — | |||||||||||||||||||||||||||||||||||||||||||

| Other comprehensive income (loss) | — | — | — | ( | — | ( | ( | ( | |||||||||||||||||||||||||||||||||||||||

| Stock-based compensation, net | — | — | — | — | |||||||||||||||||||||||||||||||||||||||||||

| Share repurchase | — | — | — | — | ( | ( | — | ( | |||||||||||||||||||||||||||||||||||||||

| Dividends to non-controlling interest | — | — | — | — | — | — | ( | ( | |||||||||||||||||||||||||||||||||||||||

| June 30, 2023 | $ | $ | $ | $ | ( | $ | ( | $ | $ | $ | |||||||||||||||||||||||||||||||||||||

See accompanying notes to the condensed consolidated financial statements.

6

VISTEON CORPORATION AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(Unaudited)

NOTE 1. Summary of Significant Accounting Policies

Basis of Presentation - Interim Financial Statements

The condensed consolidated financial statements of Visteon Corporation and Subsidiaries (the "Company" or "Visteon") have been prepared in accordance with accounting principles generally accepted in the United States ("U.S. GAAP"). Certain information and footnote disclosures normally included in financial statements prepared in accordance with the rules and regulations of the United States Securities and Exchange Commission ("SEC") have been condensed or omitted pursuant to such rules and regulations. These interim condensed consolidated financial statements include all adjustments (consisting of normal recurring adjustments, except as otherwise disclosed) that management believes are necessary for a fair presentation of the results of operations, financial position, stockholders' equity, and cash flows of the Company for the interim periods presented. Interim results are not necessarily indicative of full-year results.

Use of Estimates: The preparation of financial statements in conformity with U.S. GAAP requires management to make estimates and assumptions that affect amounts reported herein. Considerable judgment is involved in making these determinations and the use of different estimates or assumptions could result in significantly different results. Management believes its assumptions and estimates are reasonable and appropriate. However, actual results could differ from those reported herein. Events and changes in circumstances arising after June 30, 2024 will be reflected in management's estimates in future periods.

Segment: The Company’s reportable segment is Electronics. The Electronics segment provides vehicle cockpit electronics products to customers, including digital instrument clusters, domain controllers with integrated advanced driver assistance systems ("ADAS"), displays, Android-based infotainment systems, and battery management systems. As the Company has one reportable segment, net sales, total assets, depreciation, amortization and capital expenditures are equal to consolidated results.

Accounts Receivable: Accounts receivable are stated at the invoiced amount, less an allowance for doubtful accounts for estimated amounts not expected to be collected, and do not bear interest.

The Company receives bank notes from certain customers in China to settle trade accounts receivable. The collection on such bank notes are included in operating cash flows based on the substance of the underlying transactions, which are operating in nature. The Company may hold such bank notes until maturity, exchange them with suppliers to settle liabilities, or sell them to third-party financial institutions in exchange for cash. The Company has entered into arrangements with financial institutions to sell certain bank notes, generally maturing within nine months. Bank notes are sold with recourse but qualify as a sale as all rights to the notes have passed to the financial institution. The Company redeemed $74 million of China bank notes during the three months ended June 30, 2024. Remaining amounts outstanding at third-party institutions related to sold bank notes will mature by December 31, 2024.

7

Business Combinations - Joint Venture - In August 2023, the FASB issued ASU 2023-05, "Joint Venture Formation (Subtopic 805-60) - Recognition and initial measurement." to provide decision-useful information to investors and other allocators of capital (collectively, investors) in a joint venture’s financial statements and to create consistency in presentation. The amendments in this ASU are effective for fiscal years beginning after January 1, 2025 and interim periods within those fiscal years. The Company is currently evaluating the impacts of the provisions of ASU 2023-05.

Disclosure Improvements - In October 2023, the FASB issued ASU 2023-06, "Disclosure Improvements (Release No. 33-10532)." The amendments in this update modify the disclosure or presentation requirements of a variety of topics in the codification. Certain of the amendments represent clarifications to or technical corrections of the current requirements. The amendments in this ASU are effective for the interim period June 30, 2027. The Company is currently evaluating the impacts of the provisions of ASU 2023-06.

Segment Reporting - In November 2023, the FASB issued ASU 2023-07, "Segment Reporting (Topic 280) - Improvements to Reportable Segment Disclosures" to improve reportable segment disclosure requirements, primarily through enhanced disclosures about significant segment expenses. The amendments in this ASU are effective for all public entities for fiscal years beginning after December 15, 2023 and interim periods within fiscal years beginning after December 15, 2024. The Company is currently evaluating the impacts of the provisions of ASU 2023-07.

Enhanced Income Tax Disclosures - In December 2023, the FASB issued ASU No. 2023-09 (“ASU 2023-09”), Income Taxes (Topic 740): Improvement to Income Tax Disclosures to enhance the transparency and decision usefulness of income tax disclosures. ASU 2023-09 is effective for annual periods beginning after December 15, 2024 on a prospective basis and early adoption is permitted. The Company is currently evaluating the potential effect of this accounting standard update on its consolidated financial statements and related disclosures.

8

NOTE 2. Non-Consolidated Affiliates

Investments in Affiliates

The Company's investments in non-consolidated equity method affiliates include the following:

| June 30, | December 31, | ||||||||||

| (In millions) | 2024 | 2023 | |||||||||

Yanfeng Visteon Investment Co., Ltd. ("YFVIC") ( | $ | $ | |||||||||

| Limited partnerships | |||||||||||

Other | |||||||||||

Total investments in non-consolidated affiliates | $ | $ | |||||||||

Variable Interest Entities

The Company evaluates whether joint ventures in which it has invested are Variable Interest Entities (“VIE”) at the start of each new venture and when a reconsideration event has occurred. The Company consolidates a VIE if it is determined to be the primary beneficiary of the VIE having both the power to direct the activities of the VIE that most significantly impact the entity’s economic performance and the obligation to absorb losses or the right to receive benefits from the VIE that could potentially be significant to the VIE.

The Company determined that YFVIC is a VIE. The Company holds a variable interest in YFVIC primarily related to its ownership interests and subordinated financial support. The Company and Yangfeng Automotive Trim Systems Co. Ltd. ("YF") each own 50 % of YFVIC and neither entity has the power to control the operations of YFVIC; therefore, the Company is not the primary beneficiary of YFVIC and does not consolidate the joint venture.

The Company's investments in YFVIC consists of the following:

| June 30, | December 31, | ||||||||||

| (In millions) | 2024 | 2023 | |||||||||

Payables due to YFVIC | $ | $ | |||||||||

Exposure to loss in YFVIC: | |||||||||||

Investment in YFVIC | $ | $ | |||||||||

Receivables due from YFVIC, net | |||||||||||

Loan receivable from YFVIC | |||||||||||

Maximum exposure to loss in YFVIC | $ | $ | |||||||||

During the second quarter of 2024, the Company extended a loan to YFVIC in the amount of $5 million, which is recorded in Other current assets.

Non-Consolidated affiliate Transactions

In 2018, the Company committed to make a $15 million investment in two entities principally focused on the automotive sector pursuant to limited partnership agreements. As a limited partner in each entity, the Company will periodically make capital contributions toward this total commitment amount. As of June 30, 2024, the Company has contributed a total of approximately $12 million toward the aggregate investment commitments. These limited partnerships are classified as equity method investments.

In 2022, the Company made an investment in a private limited company focused on technology development for the automotive industry of $1 million. There have been no further contributions as of June 30, 2024.

A $6 million dividend was declared by a non-consolidated affiliate during the second quarter 2024, recorded as a current asset.

9

NOTE 3. Restructuring

Given the economically-sensitive and highly competitive nature of the automotive electronics industry, the Company continues to closely monitor current market factors and industry trends, taking actions as necessary which may include restructuring actions. However, there can be no assurance that any such actions will be sufficient to fully offset the impact of adverse factors on the Company or its results of operations, financial position and cash flows.

During the six months ended June 30, 2024 and 2023, the Company recorded $3 million and $2 million of net restructuring expense primarily related to employee severance, respectively.

Current restructuring actions include the following:

•During the six months ended June 30, 2024, the Company approved and recorded $3 million of net restructuring expense globally to improve efficiencies and rationalize the Company's footprint. As of June 30, 2024, $2 million remains accrued related to this action.

•During prior periods, the Company approved various restructuring programs to improve efficiencies across the organization. As of June 30, 2024, $2 million remains accrued related to these previously announced actions.

•As of June 30, 2024, the Company retained restructuring reserves as part of the Company's divestiture of the majority of its global Interiors business (the "Interiors Divestiture") and legacy operations of $3 million associated with completed programs for the fundamental reorganization of operations at facilities in Brazil and France.

Restructuring Reserves

The Company’s restructuring reserves and related activity are summarized below.

| (In millions) | |||||

| December 31, 2023 | $ | ||||

| Expense | |||||

| Utilization | ( | ||||

| March 31, 2024 | $ | ||||

| Expense | |||||

| Utilization | ( | ||||

| June 30, 2024 | $ | ||||

NOTE 4. Inventories

Inventories, net consist of the following components:

| June 30, | December 31, | ||||||||||

| (In millions) | 2024 | 2023 | |||||||||

Raw materials | $ | $ | |||||||||

Work-in-process | |||||||||||

Finished products | |||||||||||

| $ | $ | ||||||||||

10

NOTE 5. Goodwill and Other Intangible Assets

Intangible assets, net are comprised of the following:

| June 30, 2024 | December 31, 2023 | ||||||||||||||||||||||||||||||||||||||||

| (In millions) | Estimated Weighted Average Useful Life (years) | Gross Intangibles | Accumulated Amortization | Net Intangibles | Gross Intangibles | Accumulated Amortization | Net Intangibles | ||||||||||||||||||||||||||||||||||

| Definite-Lived: | |||||||||||||||||||||||||||||||||||||||||

| Developed technology | $ | $ | ( | $ | $ | $ | ( | $ | |||||||||||||||||||||||||||||||||

| Customer related | ( | ( | |||||||||||||||||||||||||||||||||||||||

| Capitalized software development | ( | ( | |||||||||||||||||||||||||||||||||||||||

| Other | ( | ( | |||||||||||||||||||||||||||||||||||||||

| Subtotal | ( | ( | |||||||||||||||||||||||||||||||||||||||

| Indefinite-Lived: | |||||||||||||||||||||||||||||||||||||||||

| Goodwill | — | — | |||||||||||||||||||||||||||||||||||||||

| Total | $ | $ | ( | $ | $ | $ | ( | $ | |||||||||||||||||||||||||||||||||

Capitalized software development consists of software development costs intended for integration into customer products.

NOTE 6. Other Assets

Other current assets are comprised of the following components:

| June 30, | December 31, | ||||||||||

| (In millions) | 2024 | 2023 | |||||||||

Recoverable taxes | $ | $ | |||||||||

Contractually reimbursable engineering costs | |||||||||||

Joint venture receivables | |||||||||||

Prepaid assets and deposits | |||||||||||

| Joint venture loan receivable | |||||||||||

| Contractual payments | |||||||||||

Other | |||||||||||

| $ | $ | ||||||||||

Other non-current assets are comprised of the following components:

| June 30, | December 31, | ||||||||||

| (In millions) | 2024 | 2023 | |||||||||

| Contractual payments | $ | $ | |||||||||

| Contractually reimbursable engineering costs | |||||||||||

| Recoverable taxes | |||||||||||

| Derivative financial instruments | |||||||||||

Other | |||||||||||

| $ | $ | ||||||||||

Current and non-current contractually reimbursable engineering costs are related to pre-production design and development costs incurred pursuant to long-term supply arrangements that are contractually guaranteed for reimbursement by customers.

11

The Company expects to receive cash reimbursement payments of $19 million during the remainder of 2024, $19 million in 2025, $8 million in 2026, $1 million in 2027, and $1 million in 2028 and beyond.

NOTE 7. Other Liabilities

Other current liabilities are summarized as follows:

| June 30, | December 31, | ||||||||||

| (In millions) | 2024 | 2023 | |||||||||

Deferred income | $ | $ | |||||||||

Product warranty and recall accruals | |||||||||||

Non-income taxes payable | |||||||||||

Income taxes payable | |||||||||||

Joint venture payable | |||||||||||

Royalty reserves | |||||||||||

Restructuring reserves | |||||||||||

Other | |||||||||||

| $ | $ | ||||||||||

Other non-current liabilities are summarized as follows:

| June 30, | December 31, | ||||||||||

| (In millions) | 2024 | 2023 | |||||||||

Product warranty and recall accruals | $ | $ | |||||||||

Deferred income | |||||||||||

Income tax reserves | |||||||||||

Derivative financial instruments | |||||||||||

| Restructuring reserves | |||||||||||

Other | |||||||||||

| $ | $ | ||||||||||

NOTE 8. Debt

The Company’s debt consists of the following:

| June 30, | December 31, | ||||||||||

| (In millions) | 2024 | 2023 | |||||||||

| Short-Term Debt: | |||||||||||

| Current Portion of long-term debt | $ | $ | |||||||||

| Long-Term Debt: | |||||||||||

| Term debt facility, net | $ | $ | |||||||||

On July 19, 2022 the Company entered into an amended and restated Credit Agreement which included a $350 million Term Facility and a $400 million Revolving Credit Facility. The amendment, among other things, changed the Credit Agreement from a LIBOR-based rate to a Secured Overnight Financing Rate ("SOFR") based rate and extended the Credit Agreement maturity date to July 19, 2027.

On June 28, 2023, the Company amended the existing Credit Agreement to, among other things, amend certain affirmative and negative covenants.

The Company has deferred costs of $2 million and $1 million related to these amendments to the Credit Agreement, which are recorded in Other non-current assets and Long-term debt, net, respectively. The deferred costs will be amortized over the term of the Credit Agreement.

12

Short-Term Debt

Terms of the amended credit facility require a quarterly principal payment equal to 1.25% of the original term debt balance. The first required payment was paid during the second quarter of 2023.

As of June 30, 2024, the Company has no other short-term borrowing, including at the Company's subsidiaries. The Company's subsidiaries have access to $147 million of capacity under short-term credit facilities.

Long-Term Debt

The Company has no outstanding borrowings on the Revolving Credit Facility as of June 30, 2024 and December 31, 2023.

Interest on the Term Facility loans and Revolving Credit Facility accrue interest at a rate equal to a SOFR-based rate plus an applicable margin of between % and 1.75 %, as determined by the Company's total gross leverage ratio. The Company can benefit from a 5 basis point decrease to the applicable margin due to a sustainability-linked pricing provision based on the Company's annual performance on reducing GHG emissions.

The Credit Agreement requires compliance with customary affirmative and negative covenants and contains customary events of default. The Revolving Credit Facility also requires that the Company maintain a total net leverage ratio no greater than 3.50 :1.00. During any period when the Company’s corporate and family ratings meet investment grade ratings, certain of the negative covenants are suspended.

The Revolving Credit Facility also provides $75 million availability for the issuance of letters of credit and a maximum of $20 million for swing line borrowings. Any amount of the facility utilized for letters of credit or swing line loans outstanding will reduce the amount available under the existing Revolving Credit Facility. The Company may request increases in the limits under the Credit Agreement and may request the addition of one or more term loan facilities. Outstanding borrowings may be prepaid without penalty (other than borrowings made for the purpose of reducing the effective interest rate margin or weighted average yield of the loans). There are mandatory prepayments of principle in connection with: (i) excess cash flow sweeps above certain leverage thresholds, (ii) certain asset sales or other dispositions, (iii) certain refinancing of indebtedness and (iv) over-advances under the Revolving Credit Facility. There are no excess cash flow sweeps required at the Company’s current leverage level.

All obligations under the Credit Agreement and obligations with respect to certain cash management services and swap transaction agreements between the Company and its lenders are unconditionally guaranteed by certain of the Company’s subsidiaries. Under the terms of the Credit Agreement, any amounts outstanding are secured by a first-priority perfected lien on substantially all property of the Company and the subsidiaries party to the security agreement, subject to certain limitations.

Other

The Company has a $7 million letter of credit facility, whereby the Company is required to maintain a cash collateral account equal to 103 % (110 % for non-U.S. dollar denominated letters) of the aggregate stated amount of issued letters of credit and must reimburse any amounts drawn under issued letters of credit. The Company had $4 million and $2 million of outstanding letters of credit issued under this facility secured by restricted cash, as of June 30, 2024 and December 31, 2023, respectively. Additionally, the Company had $2 million of locally issued bank guarantees and letters of credit as of June 30, 2024 and December 31, 2023, to support various tax appeals, customs arrangements and other obligations at its local affiliates.

13

NOTE 9. Employee Benefit Plans

The Company's net periodic benefit costs for all defined benefit plans for the three month periods ended June 30, 2024 and 2023 were as follows:

| U.S. Plans | Non-U.S. Plans | ||||||||||||||||||||||

| (In millions) | 2024 | 2023 | 2024 | 2023 | |||||||||||||||||||

Costs Recognized in Income: | |||||||||||||||||||||||

Pension service (cost): | |||||||||||||||||||||||

Service cost | $ | $ | $ | ( | $ | ( | |||||||||||||||||

Pension financing benefits (cost): | |||||||||||||||||||||||

Interest cost | $ | ( | $ | ( | $ | ( | $ | ( | |||||||||||||||

| Expected return on plan assets | |||||||||||||||||||||||

Amortization of losses and other | — | — | — | — | |||||||||||||||||||

| Total pension financing benefits: | — | ||||||||||||||||||||||

| Net pension benefit (cost) | $ | $ | $ | — | $ | ( | |||||||||||||||||

The Company's net periodic benefit costs for all defined benefit plans for the six month periods ended June 30, 2024 and 2023 were as follows:

| U.S. Plans | Non-U.S. Plans | ||||||||||||||||||||||

| (In millions) | 2024 | 2023 | 2024 | 2023 | |||||||||||||||||||

Costs Recognized in Income: | |||||||||||||||||||||||

Pension service (cost): | |||||||||||||||||||||||

Service cost | $ | $ | $ | ( | $ | ( | |||||||||||||||||

Pension financing benefits (costs): | |||||||||||||||||||||||

Interest cost | $ | ( | $ | ( | $ | ( | $ | ( | |||||||||||||||

| Expected return on plan assets | |||||||||||||||||||||||

Amortization of losses and other | — | — | — | ||||||||||||||||||||

| Total pension financing benefits: | — | — | |||||||||||||||||||||

| Net pension benefit (cost) | $ | $ | $ | ( | $ | ( | |||||||||||||||||

Pension financing benefits are classified as Other income (expense), net on the Company's condensed consolidated statements of comprehensive income.

14

NOTE 10. Income Taxes

During the six-month period ended June 30, 2024, the Company recorded a provision for income tax of $44 million. This reflects (i) income tax expense in countries where the Company is profitable, (ii) where they have accrued withholding taxes, and (iii) where they are unable to record a tax benefit for pretax losses and/or recognize expense for pretax income due to valuation allowances. Pretax losses in jurisdictions where valuation allowances are maintained and, consequently, no income tax benefits are recognized, totaled $18 million and $20 million for the six-month periods ended June 30, 2024 and 2023, respectively, resulting in an increase in the Company's effective tax rate in those years.

The Company's provision for income taxes in interim periods is computed by applying an estimated annual effective tax rate against income before income taxes, excluding equity in net income of non-consolidated affiliates for the period. Effective tax rates vary from period-to-period as separate calculations are performed for those countries where the Company's operations are profitable and whose results continue to be tax-effected, and for those countries where full valuation allowances exist and are maintained.

In the fourth quarter of 2023, the Company released $313 million of valuation allowance against its U.S. net deferred tax assets reflecting the amount more likely than not to be realized. The Company continues to carefully assess all available positive and negative evidence closely monitoring current and projected financial performance as the realization of net deferred tax assets is dependent on the Company’s ability to generate sufficient future taxable income during periods prior to the expiration of tax attributes to fully utilize these assets.

The Organization for Economic Cooperation and Development (the "OECD"), Pillar Two initiative introduced a 15% global minimum tax applied on a country-by-country basis and for which many jurisdictions have now committed to an effective enactment date starting January 1, 2024. The Company has incorporated the estimated annual effect of these new rules and the impact on the Company's effective tax rate is not material. The Company will continue to evaluate and to monitor for any changes in these new rules as well as any other changes in domestic and international tax rules and regulations.

15

NOTE 11. Stockholders’ Equity and Non-controlling Interests

Non-Controlling Interests

The Company's non-controlling interests are as follows:

| June 30, | December 31, | ||||||||||

| (In millions) | 2024 | 2023 | |||||||||

| Shanghai Visteon Automotive Electronics, Co., Ltd. | $ | $ | |||||||||

| Yanfeng Visteon Automotive Electronics Co., Ltd. | |||||||||||

Changchun Visteon FAWAY Automotive Electronics, Co., Ltd. | |||||||||||

Other | |||||||||||

| $ | $ | ||||||||||

During the six months ended June 30, 2024, the Company paid approximately $1 million to buy-out the shares of a minority joint venture partner in Tunisia.

16

Accumulated Other Comprehensive Income (Loss)

Changes in Accumulated other comprehensive income (loss) (“AOCI”) and reclassifications out of AOCI by component include:

| Three Months Ended June 30, | Six Months Ended June 30, | ||||||||||||||||||||||

| (In millions) | 2024 | 2023 | 2024 | 2023 | |||||||||||||||||||

Changes in AOCI: | |||||||||||||||||||||||

Beginning balance | $ | ( | $ | ( | $ | ( | $ | ( | |||||||||||||||

Other comprehensive income (loss) before reclassification, net of tax | ( | ( | ( | ( | |||||||||||||||||||

Amounts reclassified from AOCI | |||||||||||||||||||||||

Ending balance | $ | ( | $ | ( | $ | ( | $ | ( | |||||||||||||||

Changes in AOCI by Component: | |||||||||||||||||||||||

Foreign currency translation adjustments | |||||||||||||||||||||||

Beginning balance | $ | ( | $ | ( | $ | ( | $ | ( | |||||||||||||||

Other comprehensive income (loss) before reclassification, net of tax | ( | ( | ( | ||||||||||||||||||||

Ending balance | ( | ( | ( | ( | |||||||||||||||||||

Net investment hedge | |||||||||||||||||||||||

Beginning balance | |||||||||||||||||||||||

Other comprehensive income (loss) before reclassification, net of tax | ( | ( | |||||||||||||||||||||

Amounts reclassified from AOCI | |||||||||||||||||||||||

Ending balance | |||||||||||||||||||||||

Benefit plans | |||||||||||||||||||||||

Beginning balance | ( | ( | ( | ( | |||||||||||||||||||

Other comprehensive income (loss) before reclassification, net of tax | |||||||||||||||||||||||

| Amounts reclassified from AOCI | ( | ||||||||||||||||||||||

Ending balance | ( | ( | ( | ( | |||||||||||||||||||

Unrealized hedging gain (loss) | |||||||||||||||||||||||

Beginning balance | |||||||||||||||||||||||

Other comprehensive income (loss) before reclassification, net of tax | ( | ( | |||||||||||||||||||||

| Amounts reclassified from AOCI | |||||||||||||||||||||||

Ending balance | |||||||||||||||||||||||

Total AOCI | $ | ( | $ | ( | $ | ( | $ | ( | |||||||||||||||

Share Repurchase Program

On March 2, 2023 the Company's board of directors authorized a share repurchase program of $300 million of common stock through December 31, 2026. Under this program, the Company will repurchase shares at the prevailing market prices pursuant to specified share price and daily volume limits. During the three months ended June 30, 2024, the Company did not purchase any shares related to this program. As of June 30, 2024, the Company has repurchased 953,840 shares at an average price of $132.01 related to this program. Excise taxes incurred due to purchases under the program totaled less than $1 million during the six months ended June 30, 2024.

17

NOTE 12. Earnings Per Share

Basic earnings per share is calculated by dividing net income attributable to Visteon by the weighted average number of shares of common stock outstanding. Diluted earnings per share is calculated by dividing net income by the weighted average number of common and potentially dilutive common shares outstanding. Performance based share units are considered contingently issuable shares and are included in the computation of diluted earnings per share based on the number of shares that would be issuable if the reporting date were the end of the contingency period and if the result would be dilutive.

The table below provides details underlying the calculations of basic and diluted earnings per share:

| Three Months Ended June 30, | Six Months Ended June 30, | ||||||||||||||||||||||

| (In millions, except per share amounts) | 2024 | 2023 | 2024 | 2023 | |||||||||||||||||||

Numerator: | |||||||||||||||||||||||

Net income (loss) attributable to Visteon | $ | $ | $ | $ | |||||||||||||||||||

Denominator: | |||||||||||||||||||||||

Average common stock outstanding - basic | |||||||||||||||||||||||

Dilutive effect of performance based share units and other | |||||||||||||||||||||||

Diluted shares | |||||||||||||||||||||||

Basic and Diluted Per Share Data: | |||||||||||||||||||||||

Basic earnings (loss) per share attributable to Visteon | $ | $ | $ | $ | |||||||||||||||||||

Diluted earnings (loss) per share attributable to Visteon: | $ | $ | $ | $ | |||||||||||||||||||

NOTE 13. Fair Value Measurements and Financial Instruments

Fair Value Measurements

The Company uses a three-level fair value hierarchy that categorizes assets and liabilities measured at fair value based on the observability of the inputs utilized in the valuation. The fair value hierarchy gives the highest priority to the quoted prices in active markets for identical assets and liabilities and lowest priority to unobservable inputs.

•Level 1 – Financial assets and liabilities whose values are based on unadjusted quoted market prices for identical assets and liabilities in an active market that the Company has the ability to access.

•Level 2 – Financial assets and liabilities whose values are based on quoted prices in markets that are not active or model inputs that are observable for substantially the full term of the asset or liability.

•Level 3 – Financial assets and liabilities whose values are based on prices or valuation techniques that require inputs that are both unobservable and significant to the overall fair value measurement.

Items Measured at Fair Value on a Recurring Basis

The Company is exposed to various market risks including, but not limited to, changes in foreign currency exchange rates and market interest rates. The Company manages these risks, in part, through the use of derivative financial instruments. The use of derivative financial instruments creates exposure to credit loss in the event of nonperformance by the counterparty to the derivative financial instruments. The Company limits this exposure by entering into agreements including master netting arrangements directly with a variety of major highly rated financial institutions that are expected to fully satisfy their obligations under the contracts. Additionally, the Company’s ability to utilize derivatives to manage risks is dependent on credit and market conditions. The Company presents its derivative positions and any related material collateral under master netting arrangements that provide for the net settlement of contracts, by counterparty, in the event of default or termination. There is no cash collateral on any of these derivatives.

Derivative financial instruments are measured at fair value on a recurring basis under an income approach using industry-standard models that consider various assumptions, including time value, volatility factors, current market and contractual prices for the underlying, and non-performance risk. Substantially all of these assumptions are observable in the marketplace

18

throughout the full term of the instrument or may derived from observable data. Accordingly, the Company's currency instruments are classified as Level 2, "Other Observable Inputs" in the fair value hierarchy.

Cross Currency Swaps: The Company has executed cross-currency swap transactions intended to mitigate the variability of the U.S. dollar value of its investment in certain of its non-U.S. entities. These swaps are designated as net investment hedges and the Company has elected to assess hedge effectiveness under the spot method. Accordingly, changes in the fair value of the swaps are recorded as a cumulative translation adjustment in AOCI in the Consolidated Balance Sheet.

As of June 30, 2024 and December 31, 2023 the Company had cross-currency swaps with aggregate notional amounts of $200 million intended to mitigate the variability of U.S. dollar value investment in certain of its non-U.S. entities. These swaps are designated as net investment hedges. There was no ineffectiveness associated with such derivatives as of June 30, 2024 and December 31, 2023. The fair value of these derivatives is a non-current liability of $5 million and $15 million as of June 30, 2024 and December 31, 2023, respectively. A gain of approximately $4 million is expected to be reclassified out of accumulated other comprehensive income into earnings within the next 12 months.

Interest Rate Swaps: The Company utilizes interest rate swap instruments to manage its exposure and to mitigate the impact of interest rate variability. The swaps are designated as cash flow hedges, accordingly, the effective portion of the changes in fair value is recognized in accumulated other comprehensive income. Subsequently, the accumulated gains and losses recorded in equity are reclassified to income in the period during which the hedged exposure impacts earnings.

As of June 30, 2024 and December 31, 2023 the Company had interest rate swaps with aggregate notional amounts of $250 million. The fair value of these derivatives is a non-current asset of $11 million and $7 million as of June 30, 2024 and December 31, 2023, respectively. As of June 30, 2024, a loss of approximately $7 million is expected to be reclassified out of accumulated other comprehensive income into earnings within the next 12 months.

Financial Statement Presentation

Gains and losses on derivative financial instruments for the three and six months ended June 30, 2024 and 2023 are as follows:

| Recorded Income (Loss) into AOCI, net of tax | Reclassified from AOCI into Income (Loss) | ||||||||||||||||||||||

| (In millions) | 2024 | 2023 | 2024 | 2023 | |||||||||||||||||||

| Three months ended June 30, | |||||||||||||||||||||||

Interest rate risk - Interest expense, net: | |||||||||||||||||||||||

| Interest rate swaps | ( | ( | |||||||||||||||||||||

Net investment hedges | ( | — | — | ||||||||||||||||||||

| $ | $ | — | $ | ( | $ | ( | |||||||||||||||||

| Six months ended June 30, | |||||||||||||||||||||||

Interest rate risk - Interest expense, net: | |||||||||||||||||||||||

Interest rate swaps | ( | ( | ( | ( | |||||||||||||||||||

Net investment hedges | ( | — | — | ||||||||||||||||||||

| $ | $ | ( | $ | ( | $ | ( | |||||||||||||||||

Items Not Carried at Fair Value

The Company's fair value of debt was $327 million and $328 million as of June 30, 2024 and December 31, 2023, respectively. Fair value estimates were based on the current rates offered to the Company for debt of the same remaining maturities. Accordingly, the Company's debt fair value disclosures are classified as Level 2 in the fair value hierarchy.

19

Concentrations of Credit Risk

Financial instruments including cash equivalents, derivative contracts, and accounts receivable, expose the Company to counterparty credit risk for non-performance. The Company’s counterparties for cash equivalents and derivative contracts are banks and financial institutions that meet the Company’s credit rating requirements. The Company’s counterparties for derivative contracts are substantial investment and commercial banks with significant experience using such derivatives. The Company manages its credit risk pursuant to written policies that specify minimum counterparty credit profile and by limiting the concentration of credit exposure amongst its multiple counterparties.

The Company's credit risk with any single customer does not exceed ten percent of total accounts receivable except for GM, Ford, and Nissan/Renault and their affiliates. GM represents 16 % and 15 % of the Company's balance as of June 30, 2024 and December 31, 2023, respectively. Ford represents 13 % and 16 % of the Company's balance as of June 30, 2024 and December 31, 2023, respectively. Nissan/Renault represents 10 % and 9 % of the Company's balance as of June 30, 2024 and December 31, 2023, respectively.

NOTE 14. Commitments and Contingencies

Litigation and Claims

In 2003, the Local Development Finance Authority of the Charter Township of Van Buren, Michigan issued approximately $28 million in bonds finally maturing in 2032, the proceeds of which were used at least in part to assist in the development of the Company’s U.S. headquarters located in the Township. During January 2010, the Company and the Township entered into a settlement agreement (the “Settlement Agreement”) that, among other things, reduced the taxable value of the headquarters property to current market value and also provided that the Company would negotiate in good faith with the Township if the property tax payments were inadequate to permit the Township to meet its payment obligations with respect to the bonds. On December 9, 2019, the Township commenced litigation against the Company in Michigan’s Wayne County Circuit Court. On June 27, 2023, Visteon and the Township entered into a Settlement and Mutual Release Agreement pursuant to which Visteon, without admitting wrongdoing, will pay the Township $12 million. Payment was made in two equal installments, the first on July 3, 2023 and the second on July 1, 2024. The second payment is classified as a current liability as of June 30, 2024. The litigation commenced in Michigan’s Wayne County Circuit Court and has been dismissed with prejudice.

The Company's operations in Brazil are subject to highly complex labor, tax, customs and other laws. While the Company believes that it is in compliance with such laws, it is periodically engaged in litigation regarding the application of these laws. The Company maintained accruals of $7 million for claims aggregating $47 million in Brazil as of June 30, 2024. The amounts accrued represent claims that are deemed probable of loss and are reasonably estimable based on the Company's assessment of the claims and prior experience with similar matters.

While the Company believes its accruals for litigation and claims are adequate, the final amounts required to resolve such matters could differ materially from recorded estimates and the Company's results of operations and cash flows could be materially affected.

Product Warranty and Recall

Amounts accrued for product warranty and recall claims are based on management’s best estimates of the amounts that will ultimately be required to settle such items. The Company’s estimates for product warranty and recall obligations are developed with support from its sales, engineering, quality and legal functions and include due consideration of contractual arrangements, past experience, current claims and related information, production changes, industry and regulatory developments, and various other considerations. The Company can provide no assurances that it will not experience material claims in the future or that it will not incur significant costs to defend or settle such claims beyond the amounts accrued or beyond what the Company may recover from its suppliers.

20

The following table provides a rollforward of changes in the product warranty and recall claims liability:

| Six Months Ended June 30, | |||||||||||

| (In millions) | 2024 | 2023 | |||||||||

| Beginning balance | $ | $ | |||||||||

| Provisions | |||||||||||

Changes in estimates | ( | — | |||||||||

| Currency/other | ( | ||||||||||

| Settlements | ( | ( | |||||||||

| Ending balance | $ | $ | |||||||||

Guarantees and Commitments

As part of 2015 divestitures involving the Company's former climate and interiors businesses, the Company continues to provide lease guarantees to divested Climate and Interiors entities. As of June 30, 2024, the Company has $1 million and $2 million of outstanding guarantees, related to the divested Climate and Interiors entities, respectively. The guarantees represent the maximum potential amount that the Company could be required to pay under the guarantees in the event of default by the guaranteed parties. The guarantees will generally cease upon expiration of current lease agreement which expire in 2026 and 2024 for the Climate and Interiors entities, respectively.

Other Contingent Matters

Various legal actions, governmental investigations and proceedings and claims are pending or may be instituted or asserted in the future against the Company, including those arising out of alleged defects in the Company’s products; governmental regulations relating to safety; employment-related matters; customer, supplier and other contractual relationships; intellectual property rights; product warranties; customs and international trade regulations; product recalls; product liability claims; and environmental matters. Some of the foregoing matters may involve compensatory, punitive or antitrust or other treble damage claims in very large amounts, or demands for recall campaigns, environmental remediation programs, sanctions, or other relief which, if granted, would require very large expenditures. The Company enters into agreements that contain indemnification provisions in the normal course of business for which the risks are considered nominal and impracticable to estimate.

Contingencies are subject to many uncertainties, and the outcome of individual litigated matters is not predictable with assurance. Reserves have been established by the Company for matters discussed in the immediately foregoing paragraphs where losses are deemed probable and reasonably estimable. It is possible, however, that some of the matters discussed in the foregoing paragraphs could be decided unfavorably to the Company and could require the Company to pay damages or make other expenditures in amounts, or a range of amounts, that cannot be estimated as of June 30, 2024 and that are in excess of established reserves. The Company does not reasonably expect, except as otherwise described herein, based on its analysis, that any adverse outcome from such matters would have a material effect on the Company’s financial condition, results of operations or cash flows, although such an outcome is possible.

21

NOTE 15. Revenue Recognition and Geographical Information

Financial Information by Geographic Region

Disaggregated net sales by geographical market and product lines is as follows:

| Three Months Ended June 30, | Six Months Ended June 30, | ||||||||||||||||||||||

| (In millions) | 2024 | 2023 | 2024 | 2023 | |||||||||||||||||||

| Geographical Markets | |||||||||||||||||||||||

| Americas | $ | $ | $ | $ | |||||||||||||||||||

| Europe | |||||||||||||||||||||||

| China Domestic | |||||||||||||||||||||||

| China Export | |||||||||||||||||||||||

| Other Asia-Pacific | |||||||||||||||||||||||

| Eliminations | ( | ( | ( | ( | |||||||||||||||||||

| $ | $ | $ | $ | ||||||||||||||||||||

| Three Months Ended June 30, | Six Months Ended June 30, | ||||||||||||||||||||||

| (In millions) | 2024 | 2023 | 2024 | 2023 | |||||||||||||||||||

| Product Lines | |||||||||||||||||||||||

| Instrument clusters | $ | $ | $ | $ | |||||||||||||||||||

| Cockpit domain controller | |||||||||||||||||||||||

| Body and electrification electronics | |||||||||||||||||||||||

| Infotainment | |||||||||||||||||||||||

| Information displays | |||||||||||||||||||||||

| Other | |||||||||||||||||||||||

| $ | $ | $ | $ | ||||||||||||||||||||

22

Item 2.Management's Discussion and Analysis of Financial Condition and Results of Operations

Management’s Discussion and Analysis (“MD&A”) is intended to help the reader understand the results of operations, financial condition, and cash flows of Visteon Corporation (“Visteon” or the “Company”). MD&A is provided as a supplement to, and should be read in conjunction with, the Company’s Annual Report on Form 10-K for the fiscal year ended December 31, 2023 filed with the Securities and Exchange Commission on February 20, 2024 and the financial statements and accompanying notes to the financial statements included elsewhere herein.

Executive Summary

Strategic Priorities

Visteon is a global automotive technology company serving the mobility industry, dedicated to creating more enjoyable, connected, and safe driving experiences. Our platforms leverage proven, scalable hardware and software solutions that enable the digital, electric and autonomous evolution of our global automotive customers. The automotive mobility market is expected to grow faster than underlying vehicle production volumes as the vehicle shifts from analog to digital and towards device and cloud connected, electric vehicles, and vehicles with more advanced safety features.

The Company has laid out the following strategic priorities:

•Technology Innovation - The Company is an established global leader in cockpit electronics and is positioned to provide solutions as the industry transitions to the next generation automotive cockpit experience. The cockpit is becoming fully digital, connected, automated, learning, and voice enabled. Visteon's broad portfolio of cockpit electronics technology, the industry's first wireless battery management system, and the development of safety technology integrated into its domain controllers positions Visteon to support these macro trends in the automotive industry.

•Long-Term Growth - The Company has continued to win business at a rate that exceeds current sales levels by demonstrating product quality, technical and development capability, new product innovation, reliability, timeliness, product design, manufacturing capability, and flexibility, as well as overall customer service.

•Balanced Capital Allocation with a Strong Balance Sheet - The Company continues to maintain a strong balance sheet to withstand near-term industry volatility and support a balanced capital allocation framework. The Company is primarily focused on allocating capital to high-returning organic initiatives that increase internal capabilities, pursuing attractive inorganic opportunities, and returning capital to shareholders. In March 2023, the Company announced a $300 million share repurchase program maturing at the end of 2026. The Company has repurchased $126 million of Company common stock under this program.

23

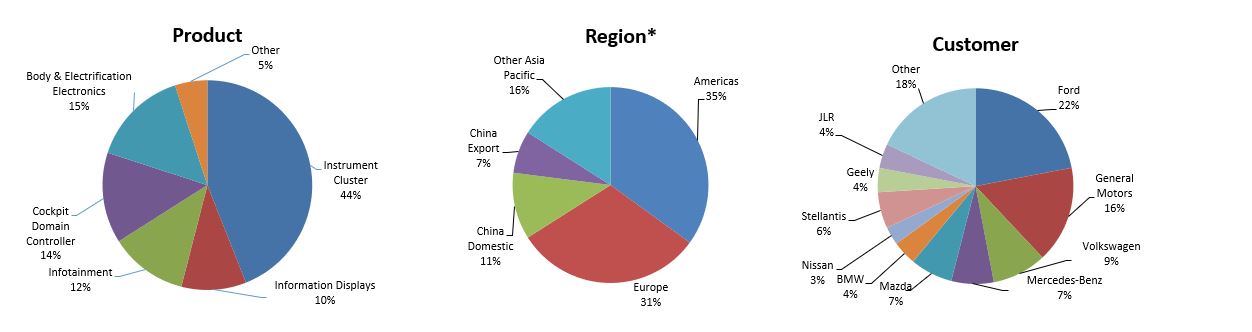

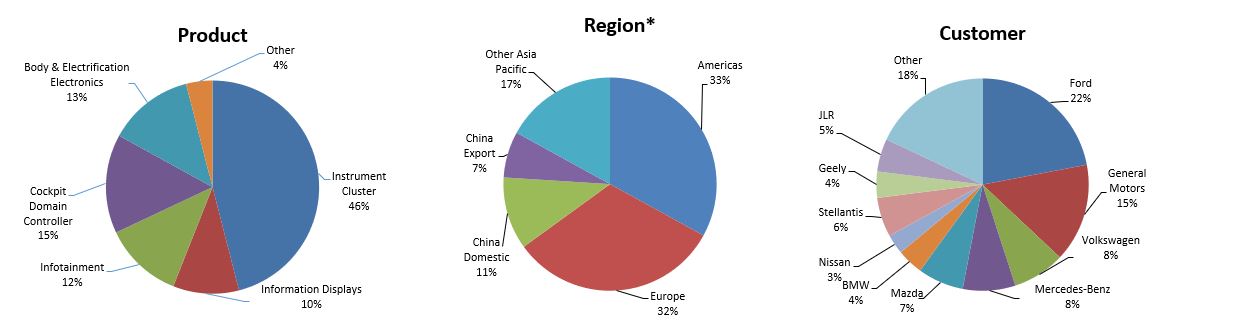

Financial Results

The pie charts below highlight the net sales breakdown for Visteon for the three and six months ended June 30, 2024.

Three Months Ended June 30, 2024

Six Months Ended June 30, 2024

*Regional net sales are based on the geographic region where sales originate and not where customer is located (excludes inter-regional eliminations).

Global Automotive Market Conditions and Production Levels

Automotive industry production has been turbulent in recent years with impacts from the COVID-19 pandemic, worldwide semiconductor and other supply related shortages, a UAW strike, increased geopolitical challenges, and the industry transition to electric vehicles. Industry vehicle volumes increased in 2022 and again in 2023 as the worldwide semiconductor and other supply related shortages have eased. However, industry production volumes are expected to decline approximately 1 million units which equates to approximately 90 million units produced in 2024, which is below recent industry production levels that peaked in 2017. Risks related to vehicle affordability, economic uncertainty, potential geopolitical challenges, and customer market share changes create ongoing uncertainties. The magnitude of the impact on the financial statements, results of operations, and cash flows will be dependent on plant production schedules, supply chain impacts, global economic impacts, and electric vehicle adoption.

24

Results of Operations - Three Months Ended June 30, 2024 and 2023

The Company's consolidated results of operations for the three months ended June 30, 2024 and 2023 were as follows:

| Three Months Ended June 30, | |||||||||||||||||

| (In millions) | 2024 | 2023 | Change | ||||||||||||||

| Net sales | $ | 1,014 | $ | 983 | $ | 31 | |||||||||||

| Cost of sales | (867) | (879) | 12 | ||||||||||||||

| Gross margin | 147 | 104 | 43 | ||||||||||||||

| Selling, general and administrative expenses | (49) | (52) | 3 | ||||||||||||||

| Restructuring, net | (1) | (1) | — | ||||||||||||||

| Interest, net | — | (3) | 3 | ||||||||||||||

| Equity in net income of non-consolidated affiliates | — | (2) | 2 | ||||||||||||||

| Other income (expense), net | 3 | (10) | 13 | ||||||||||||||

| Provision for income taxes | (25) | (13) | (12) | ||||||||||||||

| Net income (loss) | 75 | 23 | 52 | ||||||||||||||

| Less: Net (income) loss attributable to non-controlling interests | (4) | (3) | (1) | ||||||||||||||

| Net income (loss) attributable to Visteon Corporation | $ | 71 | $ | 20 | $ | 51 | |||||||||||

| Adjusted EBITDA* | $ | 136 | $ | 90 | $ | 46 | |||||||||||

* Adjusted EBITDA is a Non-GAAP financial measure, as further discussed below. | |||||||||||||||||

Net Sales, Cost of Sales and Gross Margin

| (In millions) | Net Sales | Cost of Sales | Gross Margin | ||||||||||||||

| Three months ended June 30, 2023 | $ | 983 | $ | (879) | $ | 104 | |||||||||||

| Volume, mix, and net new business | 102 | (81) | 21 | ||||||||||||||

| Currency | (14) | 10 | (4) | ||||||||||||||

| Customer pricing | (33) | — | (33) | ||||||||||||||

| Engineering costs, net * | — | 12 | 12 | ||||||||||||||

| Cost performance, design changes and other | (24) | 71 | 47 | ||||||||||||||

| Three months ended June 30, 2024 | $ | 1,014 | $ | (867) | $ | 147 | |||||||||||

| *Excludes the impact of currency. | |||||||||||||||||

Net sales for the three months ended June 30, 2024 totaled $1,014 million, representing an increase of $31 million compared with the same period of 2023. Volumes and net new business increased net sales by $102 million due to market outperformance as a result of recent product launches partially offset by lower customer vehicle production volumes. Customer pricing decreased net sales by $33 million as a result of lower customer recoveries due to improving supply chain dynamics and annual price reductions. Currency decreased net sales by $14 million, primarily attributable to the Chinese renminbi and Japanese yen. Cost performance, design changes and other decreased net sales by $24 million, primarily as a result of the non-recurrence of certain prior year commercial one-time items.

Cost of sales decreased by $12 million for the three months ended June 30, 2024 compared with the same period in 2023. Volume, mix and net new business increased cost of sales by $81 million. Net engineering costs, excluding currency, decreased cost of sales by $12 million. Foreign currency decreased cost of sales by $10 million, primarily attributable to the Mexican peso and Chinese renminbi, partially offset by the Brazilian real. Favorable cost performance, design changes, and other decreased cost of sales by $71 million primarily due to improving supply chain dynamics, manufacturing efficiencies, and the non-recurrence of a prior year product recall charge of $15 million.

25

A summary of net engineering costs is shown below:

| Three Months Ended June 30, | |||||||||||

| (In millions) | 2024 | 2023 | |||||||||

| Gross engineering costs | $ | (81) | $ | (91) | |||||||

| Engineering recoveries | 31 | 29 | |||||||||

| Engineering costs, net | $ | (50) | $ | (62) | |||||||

Gross engineering costs relate to forward model program development and advanced engineering activities and exclude contractually reimbursable engineering costs. Net engineering costs of $50 million for the three months ended June 30, 2024, including the impacts of currency, were $12 million lower than the same period of 2023. This decrease is primarily related to increased 2023 costs incurred related to the timing engineering project expenses.

Selling, General and Administrative Expenses

Selling, general, and administrative expenses were $49 million and $52 million, during the three months ended June 30, 2024 and 2023, respectively. The decrease is primarily due to reduced bad debt expense.

Restructuring

During the three months ended June 30, 2024 and 2023, the Company recorded $1 million of restructuring expense primarily related to employee severance.

Interest, Net

Interest, net, for each of the three months ended June 30, 2024 and 2023 was zero and expense of $3 million, respectively. The decrease in interest expense is primarily due to higher interest income on cash balances.

Equity in Net Income of Non-Consolidated Affiliates

Equity in net income of non-consolidated affiliates was zero and a loss of $2 million for the three months ended June 30, 2024 and 2023, respectively. The decreased loss is primarily due to operational improvements at an affiliate.

Other Income (Expense), Net

Other income, net was $3 million for the three-month period ending June 30, 2024 was primarily due to net pension financing benefits.

Other expense, net was $10 million for the three-month period ending June 30, 2023 was primarily related to the 2023 Van Buren litigation settlement partially offset by net pension financing benefits.

Income Taxes

The Company's provision for income taxes of $25 million for the three months ended June 30, 2024 represents an increase of $12 million compared with $13 million in the same period of 2023. The increase in tax expense is primarily attributable to the overall increase in net income, including changes in the mix of earnings and differing tax rates between jurisdictions, partially offset by $3 million year-over-year decrease related to uncertain tax positions.

Adjusted EBITDA

The Company defines Adjusted EBITDA as net income attributable to the Company adjusted to eliminate the impact of depreciation and amortization, non-cash stock-based compensation expense, provision for income taxes, net interest expense, net income attributable to non-controlling interests, restructuring expense, equity in net income of non-consolidated affiliates, and other gains and losses not reflective of the Company's ongoing operations.

Adjusted EBITDA is presented as a supplemental measure of the Company's financial performance that management believes is useful to investors because the excluded items may vary significantly in timing or amounts and/or may obscure trends useful in evaluating and comparing the Company's operating activities across reporting periods. Not all companies use identical

26

calculations and, accordingly, the Company's presentation of Adjusted EBITDA may not be comparable to other similarly titled measures of other companies. Adjusted EBITDA is not a recognized term under U.S. GAAP and does not purport to be a substitute for net income as an indicator of operating performance or cash flows from operating activities as a measure of liquidity. Adjusted EBITDA has limitations as an analytical tool and is not intended to be a measure of cash flow available for management's discretionary use, as it does not consider certain cash requirements such as interest payments, tax payments, and debt service requirements. The Company uses Adjusted EBITDA as a factor in incentive compensation decisions and to evaluate the effectiveness of the Company's business strategies. In addition, the Company's credit agreements use measures similar to Adjusted EBITDA to measure compliance with certain covenants.

The reconciliation of net income (loss) attributable to Visteon to Adjusted EBITDA for the three months ended June 30, 2024 and 2023, is as follows:

| Three Months Ended June 30, | |||||||||||||||||

| (In millions) | 2024 | 2023 | Change | ||||||||||||||

| Net income (loss) attributable to Visteon Corporation | $ | 71 | $ | 20 | $ | 51 | |||||||||||

| Depreciation and amortization | 24 | 26 | (2) | ||||||||||||||

| Non-cash, stock-based compensation expense | 11 | 9 | 2 | ||||||||||||||

| Provision for income taxes | 25 | 13 | 12 | ||||||||||||||

| Restructuring, net | 1 | 1 | — | ||||||||||||||

| Interest expense, net | — | 3 | (3) | ||||||||||||||

| Net income attributable to non-controlling interests | 4 | 3 | 1 | ||||||||||||||

| Equity in net income of non-consolidated affiliates | — | 2 | (2) | ||||||||||||||

| Other | — | 13 | (13) | ||||||||||||||

| Adjusted EBITDA | $ | 136 | $ | 90 | $ | 46 | |||||||||||

Adjusted EBITDA was $136 million for the three months ended June 30, 2024, representing an increase of $46 million when compared to $90 million for the same period of 2023. Volume and new business increased Adjusted EBITDA by $21 million due to market outperformance as a result of recent product launches partially offset by lower customer vehicle production volumes. Foreign currency decreased Adjusted EBITDA by $4 million primarily attributable to the Brazilian real and Japanese yen, partially offset by the Mexican peso. Net engineering costs, excluding currency, increased Adjusted EBITDA by $12 million. Warranty increased Adjusted EBITDA by $16 million, primarily related to the non-recurrence of a prior year charge of $15 million related to a product recall. Favorable cost performance, design changes and other actions, partially offset by customer pricing and certain commercial items increased Adjusted EBITDA by $1 million.

27

Results of Operations - Six Months Ended June 30, 2024 and 2023

The Company's consolidated results of operations for the six months ended June 30, 2024 and 2023 were as follows:

| Six Months Ended June 30, | |||||||||||||||||

| (In millions) | 2024 | 2023 | Change | ||||||||||||||

| Net sales | $ | 1,947 | $ | 1,950 | $ | (3) | |||||||||||

| Cost of sales | (1,681) | (1,736) | 55 | ||||||||||||||

| Gross margin | 266 | 214 | 52 | ||||||||||||||

| Selling, general and administrative expenses | (101) | (104) | 3 | ||||||||||||||

| Restructuring, net | (3) | (2) | (1) | ||||||||||||||

| Interest, net | — | (6) | 6 | ||||||||||||||

| Equity in net income of non-consolidated affiliates | (4) | (7) | 3 | ||||||||||||||

| Other income (expense), net | 5 | (7) | 12 | ||||||||||||||

| Provision for income taxes | (44) | (27) | (17) | ||||||||||||||

| Net income (loss) | 119 | 61 | 58 | ||||||||||||||

| Less: Net (income) loss attributable to non-controlling interests | (6) | (7) | 1 | ||||||||||||||

| Net income (loss) attributable to Visteon Corporation | $ | 113 | $ | 54 | $ | 59 | |||||||||||

| Adjusted EBITDA* | $ | 238 | $ | 189 | $ | 49 | |||||||||||

* Adjusted EBITDA is a Non-GAAP financial measure, as further discussed below. | |||||||||||||||||

Net Sales, Cost of Sales and Gross Margin

| (In millions) | Net Sales | Cost of Sales | Gross Margin | ||||||||||||||

| Six Months Ended June 30, 2023 | $ | 1,950 | $ | (1,736) | $ | 214 | |||||||||||

| Volume, mix, and net new business | 112 | (88) | 24 | ||||||||||||||

| Currency | (19) | 12 | (7) | ||||||||||||||

| Customer pricing | (72) | — | (72) | ||||||||||||||

| Engineering costs, net * | — | 8 | 8 | ||||||||||||||

| Cost performance, design changes and other | (24) | 123 | 99 | ||||||||||||||

| Six Months Ended June 30, 2024 | $ | 1,947 | $ | (1,681) | $ | 266 | |||||||||||

| *Excludes the impact of currency. | |||||||||||||||||

Net sales for the six months ended June 30, 2024 totaled $1,947 million, representing a decrease of $3 million compared with the same period of 2023. Volumes and net new business increased net sales by $112 million due to market outperformance as a result of recent product launches partially offset by lower customer vehicle production volumes. Customer pricing decreased net sales by $72 million as a result of lower customer recoveries due to improving supply chain dynamics and annual price reductions. Currency decreased net sales by $19 million primarily attributable to the Chinese renminbi and Japanese yen. Cost performance, design changes and other decreased net sales by $24 million, primarily as a result of the non-recurrence of certain prior year commercial one-time items.

Cost of sales decreased by $55 million for the six months ended June 30, 2024 compared with the same period in 2023. Volume, mix, and net new business increased cost of sales by $88 million. Net engineering costs, excluding currency, decreased cost of sales by $8 million. Foreign currency decreased cost of sales by $12 million primarily attributable to the Chinese renminbi and Japanese yen, partially offset by the Brazilian real. Favorable cost performance, design changes and other decreased cost of sales by $123 million primarily due to improving supply chain dynamics, manufacturing efficiencies, and a non-recurrence of a prior year product recall charge of $15 million.

28

A summary of net engineering costs is shown below:

| Six Months Ended June 30, | |||||||||||

| (In millions) | 2024 | 2023 | |||||||||

| Gross engineering costs | $ | (164) | $ | (174) | |||||||

| Engineering recoveries | 54 | 56 | |||||||||

| Engineering costs, net | $ | (110) | $ | (118) | |||||||

Gross engineering costs relate to forward model program development and advanced engineering activities and exclude contractually reimbursable engineering costs. Net engineering costs of $110 million for the six months ended June 30, 2024, including the impacts of currency, were $8 million lower than the same period of 2023. This decrease is primarily related to increased 2023 costs incurred related to the timing engineering project expenses.

Selling, General and Administrative Expenses

Selling, general, and administrative expenses were $101 million and $104 million for the six months ended June 30, 2024 and 2023, respectively. The decrease is primarily due to reduced bad debt expense.

Restructuring

During the six months ended June 30, 2024 and 2023, the Company recorded $3 million and $2 million, respectively, of restructuring expense, primarily related to employee severance.

Interest, Net

Interest, net, for the six months ended June 30, 2024 and 2023 was zero and expense of $6 million, respectively. The decrease in interest expense is primarily due to higher interest income on cash balances.

Equity in Net Income of Non-Consolidated Affiliates

Equity in net income of non-consolidated affiliates was a loss of $4 million and a loss of $7 million for the six months ended June 30, 2024 and 2023, respectively. The decreased loss is primarily due to the non-recurrence of certain operational and non-operational charges in 2023 combined with operational improvements at an affiliate during 2024.

Other Income (Expense), Net

Other income, net was $5 million for the six-month period ending June 30, 2024 is primarily due to net pension financing benefits.

Other expense, net was $7 million for the six-month period ending June 30, 2023 due to the 2023 Van Buren litigation settlement partially offset by net pension financing benefits.

Income Taxes

The Company's provision for income taxes of $44 million for the six months ended June 30, 2024 represents an increase of $17 million compared with $27 million in the same period of 2023. The increase in tax expense is primarily attributable to the overall increase in net income, including changes in the mix of earnings and differing tax rates between jurisdictions, partially offset by $3 million year-over-year decrease related to uncertain tax positions.

Adjusted EBITDA

The Company defines Adjusted EBITDA as net income attributable to the Company adjusted to eliminate the impact of depreciation and amortization, non-cash stock-based compensation expense, provision for income taxes, net interest expense, net income attributable to non-controlling interests, restructuring expense, equity in net income of non-consolidated affiliates, and other gains and losses not reflective of the Company's ongoing operations.

Adjusted EBITDA is presented as a supplemental measure of the Company's financial performance that management believes is useful to investors because the excluded items may vary significantly in timing or amounts and/or may obscure trends useful in evaluating and comparing the Company's operating activities across reporting periods. Not all companies use identical

29

calculations and, accordingly, the Company's presentation of Adjusted EBITDA may not be comparable to other similarly titled measures of other companies. Adjusted EBITDA is not a recognized term under U.S. GAAP and does not purport to be a substitute for net income as an indicator of operating performance or cash flows from operating activities as a measure of liquidity. Adjusted EBITDA has limitations as an analytical tool and is not intended to be a measure of cash flow available for management's discretionary use, as it does not consider certain cash requirements such as interest payments, tax payments, and debt service requirements. The Company uses Adjusted EBITDA as a factor in incentive compensation decisions and to evaluate the effectiveness of the Company's business strategies. In addition, the Company's credit agreements use measures similar to Adjusted EBITDA to measure compliance with certain covenants.

The reconciliation of net income (loss) attributable to Visteon to Adjusted EBITDA for the six months ended June 30, 2024 and 2023, is as follows:

| Six Months Ended June 30, | |||||||||||||||||

| (In millions) | 2024 | 2023 | Change | ||||||||||||||

| Net income (loss) attributable to Visteon Corporation | $ | 113 | $ | 54 | $ | 59 | |||||||||||

| Depreciation and amortization | 46 | 55 | (9) | ||||||||||||||

| Provision for income taxes | 44 | 27 | 17 | ||||||||||||||

| Non-cash, stock-based compensation expense | 21 | 17 | 4 | ||||||||||||||

| Interest, net | — | 6 | (6) | ||||||||||||||

| Net income (loss) attributable to non-controlling interests | 6 | 7 | (1) | ||||||||||||||