UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, DC 20549

FORM 10-Q

(Mark One)

| QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the quarterly period ended September 30, 2022

OR

| TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the transition period from ______ to _____

Commission File Number: 001-39965

(Exact Name of Registrant as Specified in its Charter)

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | ||||

| (Address of principal executive offices) | (Zip Code) | ||||

Registrant’s telephone number, including area code: (415 ) 369-8000

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||||||||||||

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes x No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ¨ | Accelerated filer | ¨ | |||||||||||

| x | Smaller reporting company | |||||||||||||

| Emerging growth company | ||||||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No x

As of November 4, 2022, the registrant had 48,047,496 shares of common stock outstanding.

Table of Contents

| Page | ||||||||

Item 1. | ||||||||

PART II. | ||||||||

1

SPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS

This Quarterly Report on Form 10-Q, or this Report, contains forward-looking statements that are based on our management’s beliefs and assumptions and on information currently available to our management. The forward-looking statements are contained principally in, but not limited to, the sections titled “Risk Factors,” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations.” Forward-looking statements include all statements that are not historical facts and can be identified by terms such as “anticipates,” “believes,” “could,” “seeks,” “estimates,” “expects,” “intends,” “may,” “plans,” “potential,” “predicts”, “projects,” “should,” “will,” “would” or similar expressions and the negatives of those terms. Forward-looking statements include, but are not limited to, statements about:

•our ability to attract new customers and expand sales to existing customers.

•our revenue growth rate may continue to decline in future periods;

•fluctuation in our performance, our history of net losses and expected increases in our expenses;

•competition and technological development in our markets and any decline in demand for our solutions or generally in our markets;

•adverse general economic and market conditions and spending on sales and marketing technology;

•our ability to expand our sales and marketing capabilities and otherwise manage our growth;

•the impact of the COVID-19 pandemic and future variants of the virus on our customer growth rate, which has declined in recent periods and may decline in future periods compared to 2021, as the impact of COVID-19 lessens and our customers and their users increasingly resume in-person marketing activities;

•disruptions, interruptions, outages or other issues with our technology or our use of third-party services, data connectors and data centers;

•the impact of the security incident involving ransomware that we experienced or any other cybersecurity-related attack, significant data breach or disruption of the information technology systems or networks on which we rely;

•our sales cycle, our international presence and our timing of revenue recognition from our sales;

•interoperability with other devices, systems and applications;

•compliance with data privacy, import and export controls, customs, sanctions and other laws and regulations;

•intellectual property matters, including any infringements of third-party intellectual property rights by us or infringement of our intellectual property rights by third parties; and

•the market for, trading price of and other matters associated with our common stock.

Forward-looking statements involve known and unknown risks, uncertainties and other factors that may cause our actual results, performance or achievements to be materially different from any future results, performance or achievements expressed or implied by the forward-looking statements. We discuss these risks in greater detail in the section entitled “Risk Factors” and elsewhere in this Report. Given these uncertainties, you should not place undue reliance on these forward-looking statements. Also, forward-looking statements represent our management’s beliefs and assumptions only as of the date of this Report. You should read this Report completely and with the understanding that our actual future results may be materially different from what we expect.

Except as required by law, we assume no obligation to update these forward-looking statements publicly, or to update the reasons actual results could differ materially from those anticipated in these forward-looking statements, even if new information becomes available in the future.

2

PART I—FINANCIAL INFORMATION

Item 1. Financial Statements.

ON24, Inc.

Condensed Consolidated Balance Sheets

(in thousands, except share and per share data)

(Unaudited)

| September 30, 2022 | December 31, 2021 | |||||||||||||

| Assets | ||||||||||||||

| Current assets | ||||||||||||||

| Cash and cash equivalents | $ | $ | ||||||||||||

| Marketable securities | ||||||||||||||

Accounts receivable, net of allowances and reserves of $ | ||||||||||||||

| Deferred contract acquisition costs, current | ||||||||||||||

| Prepaid expenses and other current assets | ||||||||||||||

| Total current assets | ||||||||||||||

| Property and equipment, net | ||||||||||||||

| Operating right-of-use assets | — | |||||||||||||

| Intangible asset, net | ||||||||||||||

| Deferred contract acquisition costs, non-current | ||||||||||||||

| Other long-term assets | ||||||||||||||

| Total assets | $ | $ | ||||||||||||

Liabilities and Stockholders’ Equity | ||||||||||||||

| Current liabilities | ||||||||||||||

| Accounts payable | $ | $ | ||||||||||||

| Accrued and other current liabilities | ||||||||||||||

| Deferred revenue | ||||||||||||||

| Finance lease liabilities, current | ||||||||||||||

Operating lease liabilities, current | — | |||||||||||||

| Total current liabilities | ||||||||||||||

| Finance lease liabilities, non-current | ||||||||||||||

| Operating lease liabilities, non-current | — | |||||||||||||

| Other long-term liabilities | ||||||||||||||

| Total liabilities | ||||||||||||||

Commitments and contingencies (See Note 10) | ||||||||||||||

Stockholders’ equity | ||||||||||||||

Common stock, $ | ||||||||||||||

| Additional paid-in capital | ||||||||||||||

| Accumulated deficit | ( | ( | ||||||||||||

Accumulated other comprehensive loss | ( | ( | ||||||||||||

Total stockholders’ equity | ||||||||||||||

Total liabilities and stockholders’ equity | $ | $ | ||||||||||||

See accompanying notes to condensed consolidated financial statements.

3

ON24, Inc.

Condensed Consolidated Statements of Operations

(in thousands, except share and per share amounts)

(Unaudited)

| Three Months Ended September 30, | Nine Months Ended September 30, | |||||||||||||||||||||||||

| 2022 | 2021 | 2022 | 2021 | |||||||||||||||||||||||

| Revenue: | ||||||||||||||||||||||||||

| Subscription and other platform | $ | $ | $ | $ | ||||||||||||||||||||||

| Professional services | ||||||||||||||||||||||||||

| Total revenue | ||||||||||||||||||||||||||

| Cost of revenue: | ||||||||||||||||||||||||||

| Subscription and other platform | ||||||||||||||||||||||||||

| Professional services | ||||||||||||||||||||||||||

| Total cost of revenue | ||||||||||||||||||||||||||

| Gross profit | ||||||||||||||||||||||||||

| Operating expenses: | ||||||||||||||||||||||||||

| Sales and marketing | ||||||||||||||||||||||||||

| Research and development | ||||||||||||||||||||||||||

| General and administrative | ||||||||||||||||||||||||||

| Total operating expenses | ||||||||||||||||||||||||||

Loss from operations | ( | ( | ( | ( | ||||||||||||||||||||||

| Interest expense | ||||||||||||||||||||||||||

| Other (income) expense, net | ( | ( | ||||||||||||||||||||||||

Loss before provision for (benefit from) income taxes | ( | ( | ( | ( | ||||||||||||||||||||||

Provision for (benefit from) income taxes | ( | ( | ||||||||||||||||||||||||

Net loss | ( | ( | ( | ( | ||||||||||||||||||||||

| Cumulative preferred dividends allocated to preferred stockholders | ( | |||||||||||||||||||||||||

Net loss attributable to common stockholders | $ | ( | $ | ( | $ | ( | $ | ( | ||||||||||||||||||

Net loss per share attributable to common stockholders: | ||||||||||||||||||||||||||

Basic and diluted | $ | ( | $ | ( | $ | ( | $ | ( | ||||||||||||||||||

Weighted-average shares used in computing net loss per share attributable to common stockholders: | ||||||||||||||||||||||||||

Basic and diluted | ||||||||||||||||||||||||||

See accompanying notes to condensed consolidated financial statements.

4

ON24, Inc.

Condensed Consolidated Statements of Comprehensive Loss

(in thousands)

(Unaudited)

| Three Months Ended September 30, | Nine Months Ended September 30, | |||||||||||||||||||||||||

| 2022 | 2021 | 2022 | 2021 | |||||||||||||||||||||||

Net loss | $ | ( | $ | ( | $ | ( | $ | ( | ||||||||||||||||||

| Other comprehensive income (loss) | ||||||||||||||||||||||||||

| Foreign currency translation adjustment, net of tax | ( | |||||||||||||||||||||||||

Unrealized gain (loss) on available for sale debt securities, net of tax | ( | ( | ( | |||||||||||||||||||||||

Total other comprehensive income (loss) | ( | |||||||||||||||||||||||||

Total comprehensive loss | $ | ( | $ | ( | $ | ( | $ | ( | ||||||||||||||||||

See accompanying notes to condensed consolidated financial statements.

5

ON24, Inc.

Condensed Consolidated Statements of Convertible Preferred Stock and Stockholders’ Equity (Deficit)

(in thousands, except share amounts)

(Unaudited)

Convertible Preferred Stock | Redeemable convertible preferred stock | Common Stock | Additional paid-in capital | Accumulated Deficit | Accumulated other comprehensive income (loss) | Total stockholders' equity (deficit) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Shares | Amount | Shares | Amount | Shares | Amount | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Balance as of June 30, 2022 | $ | $ | $ | $ | $ | ( | $ | ( | $ | |||||||||||||||||||||||||||||||||||||||||||||||||||||

| Issuance of common stock upon exercise of stock options | — | — | — | — | — | — | — | |||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Issuance of common stock upon release of restricted stock units | — | — | — | — | — | — | — | — | — | |||||||||||||||||||||||||||||||||||||||||||||||||||||

| Stock-based compensation expense | — | — | — | — | — | — | — | — | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

Other comprehensive income | — | — | — | — | — | — | — | — | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Net loss | — | — | — | — | — | — | — | ( | — | ( | ||||||||||||||||||||||||||||||||||||||||||||||||||||

| Balance as of September 30, 2022 | $ | $ | $ | $ | $ | ( | $ | ( | $ | |||||||||||||||||||||||||||||||||||||||||||||||||||||

Convertible Preferred Stock | Redeemable convertible preferred stock | Common Stock | Additional paid-in capital | Accumulated Deficit | Accumulated other comprehensive income (loss) | Total stockholders' equity (deficit) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Shares | Amount | Shares | Amount | Shares | Amount | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Balance as of June 30, 2021 | $ | $ | $ | $ | $ | ( | $ | $ | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Issuance of common stock upon exercise of stock options | — | — | — | — | — | — | — | |||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Issuance of common stock upon release of restricted stock units | — | — | — | — | — | — | — | — | — | |||||||||||||||||||||||||||||||||||||||||||||||||||||

| Stock-based compensation expense | — | — | — | — | — | — | — | — | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

Other comprehensive income | — | — | — | — | — | — | — | — | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Net loss | — | — | — | — | — | — | — | ( | — | ( | ||||||||||||||||||||||||||||||||||||||||||||||||||||

| Balance as of September 30, 2021 | $ | $ | $ | $ | $ | ( | $ | $ | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

6

| Convertible Preferred Stock | Redeemable convertible preferred stock | Common Stock | Additional paid-in capital | Accumulated Deficit | Accumulated other comprehensive income (loss) | Total stockholders' equity (deficit) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Shares | Amount | Shares | Amount | Shares | Amount | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Balance as of December 31, 2021 | $ | $ | $ | $ | $ | ( | $ | ( | $ | |||||||||||||||||||||||||||||||||||||||||||||||||||||

| Repurchase of common stock | — | — | — | — | ( | — | ( | — | — | ( | ||||||||||||||||||||||||||||||||||||||||||||||||||||

| Issuance of common stock upon exercise of stock options | — | — | — | — | — | — | — | |||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Issuance of common stock upon release of restricted stock units | — | — | — | — | — | — | — | — | — | |||||||||||||||||||||||||||||||||||||||||||||||||||||

| Issuance of common stock under ESPP | — | — | — | — | — | — | — | |||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Payment for employee tax withholding upon net share settlement on equity awards | — | — | — | — | — | — | ( | — | — | ( | ||||||||||||||||||||||||||||||||||||||||||||||||||||

| Stock-based compensation expense | — | — | — | — | — | — | — | — | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Other comprehensive income (loss) | — | — | — | — | — | — | — | — | ( | ( | ||||||||||||||||||||||||||||||||||||||||||||||||||||

| Net loss | — | — | — | — | — | — | — | ( | — | ( | ||||||||||||||||||||||||||||||||||||||||||||||||||||

Balance as of September 30, 2022 | $ | $ | $ | $ | $ | ( | $ | ( | $ | |||||||||||||||||||||||||||||||||||||||||||||||||||||

| Convertible Preferred Stock | Redeemable convertible preferred stock | Common Stock | Additional paid-in capital | Accumulated Deficit | Accumulated other comprehensive income (loss) | Total stockholders' equity (deficit) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Shares | Amount | Shares | Amount | Shares | Amount | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Balance as of December 31, 2020 | $ | $ | $ | $ | $ | ( | $ | $ | ( | |||||||||||||||||||||||||||||||||||||||||||||||||||||

| Conversion of convertible preferred stock and redeemable convertible preferred stock to common stock upon initial public offering | ( | ( | ( | ( | — | — | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Issuance of common stock upon initial public offering, net of underwriting discounts and other offering costs | — | — | — | — | — | — | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Issuance of common stock upon exercise of stock options | — | — | — | — | — | — | — | |||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Issuance of common stock upon release of restricted stock units | — | — | — | — | — | — | — | — | — | |||||||||||||||||||||||||||||||||||||||||||||||||||||

| Payment for employee tax withholding upon net share settlement on equity awards | — | — | — | — | — | — | ( | — | — | ( | ||||||||||||||||||||||||||||||||||||||||||||||||||||

| Stock-based compensation expense | — | — | — | — | — | — | — | — | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Other comprehensive income (loss) | — | — | — | — | — | — | — | — | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Net loss | — | — | — | — | — | — | — | ( | — | ( | ||||||||||||||||||||||||||||||||||||||||||||||||||||

Balance as of September 30, 2021 | $ | $ | $ | $ | $ | ( | $ | $ | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

See accompanying notes to condensed consolidated financial statements.

7

ON24, Inc.

Condensed Consolidated Statements of Cash Flows

(In thousands)

(Unaudited)

| Nine Months Ended September 30, | ||||||||||||||

| 2022 | 2021 | |||||||||||||

| Cash flows from operating activities: | ||||||||||||||

Net loss | $ | ( | $ | ( | ||||||||||

Adjustments to reconcile net loss to net cash (used in) provided by operating activities: | ||||||||||||||

| Depreciation and amortization | ||||||||||||||

| Stock-based compensation expense | ||||||||||||||

| Amortization of deferred contract acquisition costs | ||||||||||||||

| Provision for allowance for doubtful accounts and billing reserve | ||||||||||||||

| Non-cash lease expense | ||||||||||||||

| Other | ( | |||||||||||||

| Changes in operating assets and liabilities: | ||||||||||||||

| Accounts receivable | ||||||||||||||

| Deferred contract acquisition costs | ( | ( | ||||||||||||

| Prepaid expenses and other assets | ( | ( | ||||||||||||

| Accounts payable | ( | |||||||||||||

| Accrued liabilities | ( | |||||||||||||

| Deferred revenue | ( | ( | ||||||||||||

| Other non-current liabilities | ( | ( | ||||||||||||

| Net cash (used in) provided by operating activities | ( | |||||||||||||

Cash flows from investing activities: | ||||||||||||||

| Purchase of property and equipment | ( | ( | ||||||||||||

Acquisition, net of cash acquired | ( | |||||||||||||

| Purchase of marketable securities | ( | ( | ||||||||||||

| Proceeds from maturities and paydowns of marketable securities | ||||||||||||||

| Net cash used in investing activities | ( | ( | ||||||||||||

Cash flows from financing activities: | ||||||||||||||

| Proceeds from initial public offering, net of underwriting discounts | ||||||||||||||

| Proceeds from exercise of stock options | ||||||||||||||

| Proceeds from issuance of common stock under ESPP | ||||||||||||||

| Payment of tax withholding obligations related to net share settlements on equity awards | ( | ( | ||||||||||||

| Payment for repurchase of common stock | ( | |||||||||||||

Repayment of equipment loans and borrowings | ( | ( | ||||||||||||

Repayment of finance lease obligations | ( | ( | ||||||||||||

Payment of offering costs | ( | |||||||||||||

| Net cash (used in) provided by financing activities | ( | |||||||||||||

| Effect of exchange rate changes on cash, cash equivalents and restricted cash | ||||||||||||||

Net (decrease) increase in cash, cash equivalents and restricted cash | ( | |||||||||||||

| Cash, cash equivalents and restricted cash, beginning of period | ||||||||||||||

| Cash, cash equivalents and restricted cash, end of period | $ | $ | ||||||||||||

Supplemental disclosures of cash flow information: | ||||||||||||||

| Cash paid for taxes, net of refunds | $ | $ | ||||||||||||

| Cash paid for interest | $ | $ | ||||||||||||

Reconciliation of cash, cash equivalents, and restricted cash to the condensed consolidated balance sheets: | ||||||||||||||

Cash and cash equivalents | $ | $ | ||||||||||||

Restricted cash included in other assets, non-current | ||||||||||||||

Total cash, cash equivalent, and restricted cash | $ | $ | ||||||||||||

8

ON24, Inc.

Notes to Condensed Consolidated Financial Statements (Unaudited)

Note 1. Description of Business and Significant Accounting Policies

Description of Business

ON24, Inc. and its subsidiaries (together, ON24 or the Company) provides a leading, cloud-based platform for digital engagement that enables businesses to convert customer engagement into revenue through interactive webinar experiences, virtual event experiences and multimedia content experiences. The Company’s platform offers a portfolio of interactive, personalized and content-rich digital experience products that creates and captures actionable, real-time data at scale from millions of professionals every month to provide businesses with buying signals and behavioral insights to efficiently convert prospects into customers. The Company was incorporated in the state of Delaware in January 1998 as NewsDirect, Inc. and in December 1998 changed its name to ON24, Inc. The Company is headquartered in San Francisco, California.

Initial Public Offering

On February 5, 2021, the Company closed its initial public offering (IPO) of 7,599,928 shares of its common stock at a public offering price of $50 per share for net proceeds of approximately $347.8 million, after deducting the underwriting discount of approximately $26.6 million and other offering costs of approximately $5.6 million. The shares of common stock sold in the IPO and the net proceeds from the IPO included the full exercise of the underwriters’ option to purchase additional shares.

Upon the closing of the IPO, all of the Company's outstanding shares of Class A-1 and Class A-2 convertible preferred stock and Class B and Class B-1 redeemable convertible preferred stock were automatically converted into an aggregate of 27,227,466 shares of common stock on a one -for-one basis.

Basis of Presentation

The accompanying condensed consolidated financial statements have been prepared in accordance with generally accepted accounting principles in the United States of America (U.S. GAAP) and applicable rules and regulations of the Securities and Exchange Commission (SEC) for interim financial reporting. Certain information and note disclosures included in the Company’s annual financial statements prepared in accordance with GAAP have been condensed or omitted pursuant to such rules and regulations. Therefore, these condensed consolidated financial statements should be read in conjunction with the consolidated financial statements and notes included in the Company’s annual report on Form 10-K for the year ended December 31, 2021. In the opinion of management, the condensed consolidated financial statements reflect all adjustments that are normal and recurring in nature and necessary for fair financial statement presentation. All intercompany transactions and balances have been eliminated in consolidation.

The results of operations for the three and nine months ended September 30, 2022 are not necessarily indicative of the operating results anticipated for the full year.

Use of Estimates

The preparation of condensed consolidated financial statements in conformity with U.S. GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the condensed consolidated financial statements and the reported amounts of revenue and expenses during the reporting period. Significant items subject to such estimates and assumptions include, but are not limited to, the estimated expected benefit period for deferred contract acquisition costs, the determination of standalone selling price for the Company’s performance obligations, the allowance for doubtful accounts and billing reserve, the useful lives of long-lived assets, the assumptions used to measure stock-based compensation, the valuation of deferred income tax assets and uncertain tax positions. Actual results could differ from those estimates.

9

Significant Accounting Policies

The Company’s significant accounting policies are disclosed in its Annual Report on Form 10-K for the year ended December 31, 2021. Other than the changes to the accounting policy for leases related to the adoption of ASC 842 on January 1, 2022 discussed below, there has been no material change to the Company’s significant accounting policies during the three and nine months ended September 30, 2022.

Leases

The Company determines if an arrangement is a lease at inception. Lease liabilities are recognized at the lease commencement date based on the present value of the future lease payments over the lease term. The interest rate used to determine the present value of the future lease payments is the Company's incremental borrowing rate because the interest rate implicit in its leases is not readily determinable. Right-of-use asset (ROU) asset is determined based on the lease liability initially established and reduced for any prepaid lease payments and any lease incentives received. The lease term to calculate the ROU asset and related lease liability may include options to extend or terminate the lease when the Company is reasonably certain that it will exercise the option.

Variable lease payments are expensed as incurred and are not included in the ROU assets and lease liabilities. Leases with an initial term of 12 months or less are not recognized on the balance sheet as ROU assets but expensed on a straight-line basis over the lease term.

Lease expense is recognized on a straight-line basis over the lease term. The Company accounts for lease components and non-lease components as a single lease component for its new or modified office facility operating leases entered into on or after January 1, 2022.

Recently Adopted Accounting Standards

In October 2021, the Financial Accounting Standards Board (FASB) issued ASU No. 2021-08, Business Combinations (Topic 805): Accounting for Contract Assets and Contract Liabilities from Contracts with Customers. ASU No. 2021-08 amended Topic 805 to require an acquirer to recognize and measure contract assets and liabilities acquired in a business combination to be in accordance with Topic 606, Revenue from Contracts with Customers. The Company early adopted this ASU on April 1, 2022. The adoption of this standard did not have a material impact on the Company’s consolidated financial statements.

In June 2016, FASB issued ASU No. 2016-13, Financial Instruments Topic 326: Credit Losses Measurement of Credit Losses on Financial Instruments, as amended, which requires an entity to measure all expected credit losses for financial instruments held at the reporting date based on historical experience, current conditions, and reasonable and supportable forecasts utilizing a new impairment model known as the current expected credit loss (CECL) model. The new guidance affects loans, debt securities, trade receivables, net investments in leases, off-balance-sheet credit exposures, reinsurance receivables, and any other financial assets not excluded from the scope that have the contractual right to receive cash. For public business entities, excluding entities eligible to be smaller reporting companies as defined by the SEC, ASU No. 2016-13, is effective for the annual periods in fiscal years beginning after December 15, 2019, and interim periods therein. For all other entities ASU No. 2016-13, is effective for fiscal years beginning after December 15, 2022, including interim periods within those fiscal year. The Company has elected to use the extended transition period that allows the Company to delay adoption of new or revised accounting pronouncements until such pronouncements are made applicable to private companies under the Jumpstart Our Business Startups Act of 2012. The Company is currently evaluating the impact of adopting this standard and does not expect the adoption to have a material impact on its consolidated financial statements.

In February 2016, the FASB issued ASU No. 2016-02, Leases (Topic 842), as amended, to supersede existing guidance on accounting for leases in Topic 840, Leases. Topic 842 generally requires lessees to recognize operating and financing lease liabilities and corresponding right-of-use assets on the balance sheet and to provide enhanced disclosures surrounding the amount, timing and uncertainty of cash flows arising from leasing arrangements.

The Company adopted the new lease standard effective January 1, 2022 on a modified retrospective basis using the effective date transition method, which applied the provisions of the new guidance at the effective date without adjusting the comparative periods presented. On the adoption date, the Company recognized on its condensed consolidated balance sheets $7.2 million of additional right-of-use assets, $9.6 million additional lease liabilities, and derecognized existing deferred rent and lease incentives totaling $2.4 million. The Company’s accounting for finance leases remained substantially unchanged.

10

The Company elected a number of the practical expedients permitted under the transition guidance within the new standard. This included the election to apply the practical expedient package upon transition, which comprised the following:

•The Company did not reassess whether expired or existing contracts are or contain a lease;

•The Company did not reassess the classification of existing leases; and

•The Company did not reassess the accounting treatment for initial direct costs.

The Company also elected to apply the hindsight practical expedient which allows the Company to use hindsight in determining the lease term.

In addition, the Company elected the practical expedient related to short-term leases, which allows the Company not to recognize a ROU asset and lease liability for leases with an initial expected term of 12 months or less. The Company also elected to account for lease and non-lease components as a single lease component for operating facility leases.

Note 2. Revenue

Disaggregation of Revenue

The following table depicts the disaggregation of revenue by geographic region based on the shipping address of customers (in thousands):

| Three Months Ended September 30, | Nine Months Ended September 30, | |||||||||||||||||||||||||

| 2022 | 2021 | 2022 | 2021 | |||||||||||||||||||||||

| United States | $ | $ | $ | $ | ||||||||||||||||||||||

| EMEA | ||||||||||||||||||||||||||

| Other | ||||||||||||||||||||||||||

| Total revenue | $ | $ | $ | $ | ||||||||||||||||||||||

The following table summarizes the foreign countries which contributed 10% or more of the total revenue (in thousands):

| Three Months Ended September 30, | Nine Months Ended September 30, | |||||||||||||||||||||||||

| 2022 | 2021 | 2022 | 2021 | |||||||||||||||||||||||

| United Kingdom | * | * | * | % | ||||||||||||||||||||||

| * | Represent less than 10% of total revenue | ||||||||||

Contract Balances

11

Remaining Performance Obligations

The terms of the Company’s subscription agreements are primarily annual and, to a lesser extent, multi-year. The Company may bill for the full term in advance or on an annual, quarterly or monthly basis, depending on the terms of the agreement. As of September 30, 2022, the aggregate amount of the transaction price allocated to remaining performance obligations was $139.9 million, which consists of both billed consideration in the amount of $81.7 million and unbilled consideration in the amount of $58.2 million that the Company expects to recognize as revenue. As of September 30, 2022, the Company expects to recognize 80 % of its remaining performance obligations as revenue over the subsequent 12 months and the remainder thereafter.

Costs to Obtain a Contract

The Company capitalizes sales commissions and associated payroll taxes paid to internal sales personnel and third-party referral fees that are incremental costs resulting from obtaining a contract with a customer. These costs are recorded as deferred contract acquisition costs on the condensed consolidated balance sheets. The Company determines whether costs should be deferred based on its sales compensation plans and if the commissions are incremental and would not have occurred absent the customer contract.

Sales commissions paid upon the initial acquisition of a customer contract are amortized over an estimated period of benefit of five years as the Company specifically anticipates renewals of customer contracts and commissions paid on renewal contracts are not commensurate with commissions paid on new customer contracts. Sales commissions paid upon renewal of customer contracts are amortized over the contractual renewal term. Amortization is recognized on a straight-line basis commensurate with the pattern of revenue recognition. Sales commissions paid related to professional services are amortized over the expected service period. The Company determines the period of benefit for commissions paid for the acquisition of the initial customer contract by taking into consideration the initial estimated customer life and the technological life of its platform and related significant features. Amortization of deferred contract acquisition costs was $3.9 million and $11.9 million or the three and nine months ended September 30, 2022, respectively, and $3.8 million and $11.3 million for the three and nine months ended September 30, 2021, respectively. Amortization of deferred contract acquisition costs is included in sales and marketing expense in the condensed consolidated statements of operations.

The Company periodically reviews these deferred contract acquisition costs to determine whether events or changes in circumstances have occurred that could impact the period of benefit. The Company had no

12

Note 3. Marketable Securities

Marketable securities consisted of the following as of the periods presented (in thousands):

| September 30, 2022 | ||||||||||||||||||||||||||

Amortized Cost | Gross Unrealized Gains | Gross Unrealized Losses | Fair Value | |||||||||||||||||||||||

| Marketable Securities | ||||||||||||||||||||||||||

| U.S. Treasury securities | $ | $ | $ | ( | $ | |||||||||||||||||||||

| Certificates of deposit | ( | |||||||||||||||||||||||||

| Corporate debt securities | ( | |||||||||||||||||||||||||

| Commercial paper | ( | |||||||||||||||||||||||||

| Asset-backed securities | ( | |||||||||||||||||||||||||

| Total marketable securities | $ | $ | $ | ( | $ | |||||||||||||||||||||

| December 31, 2021 | ||||||||||||||||||||||||||

| Amortized Cost | Gross Unrealized Gains | Gross Unrealized Losses | Fair Value | |||||||||||||||||||||||

| Marketable Securities | ||||||||||||||||||||||||||

| U.S. Treasury securities | $ | $ | $ | ( | $ | |||||||||||||||||||||

| Certificates of deposit | ( | |||||||||||||||||||||||||

| Corporate debt securities | ( | |||||||||||||||||||||||||

| Commercial paper | ( | |||||||||||||||||||||||||

| Asset-backed securities | ( | |||||||||||||||||||||||||

| Total marketable securities | $ | $ | $ | ( | $ | |||||||||||||||||||||

The Company’s marketable securities have been classified as available for sale. All available for sale debt securities are available for use in current operations. Accordingly, they have been classified as current.

Marketable securities in an unrealized loss position consisted of the following as of the periods presented (in thousands):

| September 30, 2022 | ||||||||||||||||||||||||||||||||||||||

| Less Than 12 Months | 12 Months or More | Total | ||||||||||||||||||||||||||||||||||||

| Fair Value | Gross Unrealized Loss | Fair Value | Gross Unrealized Loss | Fair Value | Gross Unrealized Loss | |||||||||||||||||||||||||||||||||

| U.S. Treasury securities | $ | $ | ( | $ | $ | ( | $ | $ | ( | |||||||||||||||||||||||||||||

| Certificates of deposit | ( | ( | ||||||||||||||||||||||||||||||||||||

| Corporate debt securities | ( | ( | ( | |||||||||||||||||||||||||||||||||||

| Commercial paper | ( | ( | ||||||||||||||||||||||||||||||||||||

| Asset-backed securities | ( | ( | ||||||||||||||||||||||||||||||||||||

| Total | $ | $ | ( | $ | $ | ( | $ | $ | ( | |||||||||||||||||||||||||||||

13

| December 31, 2021 | ||||||||||||||||||||||||||||||||||||||

| Less Than 12 Months | 12 Months or More | Total | ||||||||||||||||||||||||||||||||||||

| Fair Value | Gross Unrealized Loss | Fair Value | Gross Unrealized Loss | Fair Value | Gross Unrealized Loss | |||||||||||||||||||||||||||||||||

| U.S. Treasury securities | $ | $ | ( | $ | $ | $ | $ | ( | ||||||||||||||||||||||||||||||

| Certificates of deposit | ( | ( | ||||||||||||||||||||||||||||||||||||

| Corporate debt securities | ( | ( | ||||||||||||||||||||||||||||||||||||

| Commercial paper | ( | ( | ||||||||||||||||||||||||||||||||||||

| Asset-backed securities | ( | ( | ||||||||||||||||||||||||||||||||||||

| Total | $ | $ | ( | $ | $ | $ | $ | ( | ||||||||||||||||||||||||||||||

The Company reviews the individual securities that have unrealized losses on a regular basis to evaluate whether any security has experienced other-than-temporary decline in fair value below amortized cost. The Company evaluates, among other factors, whether the Company has the intention to sell any of these marketable securities and whether it is more likely than not that the Company will be required to sell any securities before recovery of the amortized cost basis. Since the Company has the ability to hold its investments until maturity, and the decline in fair value was not due to any credit-related factor, no decline was deemed to be other-than-temporary.

The Company had no

The following summarizes the remaining contractual maturities of the Company’s marketable securities as of September 30, 2022 (in thousands):

Fair Value | |||||

| One year or less | $ | ||||

| Over one year through five years | |||||

| Total marketable securities | $ | ||||

Note 4. Fair Value Measurement

The following tables summarize the Company’s financial instruments recorded at fair value on a recurring basis by level within the fair value hierarchy as of the periods presented (in thousands):

| September 30, 2022 | |||||||||||||||||||||||

| Level 1 | Level 2 | Level 3 | Total | ||||||||||||||||||||

Cash and cash equivalent | |||||||||||||||||||||||

Cash equivalents - money market mutual funds | $ | $ | $ | $ | |||||||||||||||||||

| Cash equivalents - commercial paper | |||||||||||||||||||||||

| Marketable Securities | |||||||||||||||||||||||

| U.S. Treasury securities | |||||||||||||||||||||||

| Certificates of deposit | |||||||||||||||||||||||

| Corporate debt securities | |||||||||||||||||||||||

Commercial paper | |||||||||||||||||||||||

| Asset-backed securities | |||||||||||||||||||||||

| Total cash equivalents and marketable securities | $ | $ | $ | $ | |||||||||||||||||||

14

| December 31, 2021 | |||||||||||||||||||||||

| Level 1 | Level 2 | Level 3 | Total | ||||||||||||||||||||

Cash and cash equivalent | |||||||||||||||||||||||

| Cash equivalents - money market mutual funds | $ | $ | $ | $ | |||||||||||||||||||

| Marketable Securities | |||||||||||||||||||||||

| U.S. Treasury securities | |||||||||||||||||||||||

| Certificates of deposit | |||||||||||||||||||||||

| Corporate debt securities | |||||||||||||||||||||||

| Commercial paper | |||||||||||||||||||||||

| Asset-backed securities | |||||||||||||||||||||||

| Total cash equivalents and marketable securities | $ | $ | $ | $ | |||||||||||||||||||

As of September 30, 2022 and December 31, 2021, the Company classified its cash equivalents within level 1 or level 2 of the fair value hierarchy because they are valued using quoted market prices or alternative pricing sources and models utilizing observable market inputs. The Company classified its marketable securities within level 2 of the fair value hierarchy because they are valued using inputs other than quoted prices that are directly or indirectly observable in the market, including readily available pricing sources for the identical underlying security, which may not be actively traded.

Note 5. Balance Sheets Components

Prepaid Expenses and Other Current Assets

Prepaid expenses and other current assets consisted of the following as of the periods presented (in thousands):

| September 30, 2022 | December 31, 2021 | ||||||||||

| Prepaid expenses | $ | $ | |||||||||

| Other receivables | |||||||||||

| Other | |||||||||||

| Prepaid expenses and other current assets | $ | $ | |||||||||

Property and Equipment, Net

Property and equipment, net consisted of the following as of the periods presented (in thousands):

| September 30, 2022 | December 31, 2021 | ||||||||||

Computer, equipment and software(1) | $ | $ | |||||||||

| Furniture and fixtures | |||||||||||

| Leasehold improvements | |||||||||||

| Property and equipment, gross | |||||||||||

Less: Accumulated depreciation and amortization(2) | ( | ( | |||||||||

| Property and equipment, net | $ | $ | |||||||||

(1)Includes assets recorded under finance leases of $5.3

(2)Includes amount for assets recorded under finance leases of $3.6 million and $2.2 million as of September 30, 2022 and December 31, 2021, respectively.

Depreciation and amortization expense for property and equipment was $1.3 million and $3.7 million for the three and nine months ended September 30, 2022, respectively, and $1.1 million and $3.4 million for the three and nine months ended September 30, 2021, respectively.

15

The following table presents the property and equipment, net of depreciation and amortization, by geographic region as of the periods presented (in thousands):

| September 30, 2022 | December 31, 2021 | ||||||||||

| United States | $ | $ | |||||||||

| EMEA | |||||||||||

| Other | |||||||||||

| Total property and equipment, net | $ | $ | |||||||||

Accrued and Other Current Liabilities

Accrued and other current liabilities consisted of the following as of the periods presented (in thousands):

| September 30, 2022 | December 31, 2021 | ||||||||||

| Accrued compensation and benefits | $ | $ | |||||||||

| Accrued bonus and commissions | |||||||||||

| Other | |||||||||||

| Accrued and other current liabilities | $ | $ | |||||||||

Other Long-term Liabilities

Other long-term liabilities consisted of the following as of the periods presented (in thousands):

| September 30, 2022 | December 31, 2021 | ||||||||||

| Deferred rent liabilities | $ | $ | |||||||||

| Deferred revenue | |||||||||||

| Other | |||||||||||

| Other long-term liabilities | $ | $ | |||||||||

Note 6. Business Combination

In April 2022, the Company acquired Vibbio AS (Vibbio), a privately-held cloud video software company in Norway, for approximately $3.0 million in cash. The integration of Vibbio’s video capabilities across the ON24 platform is intended to allow customers to produce video content that creates more engagement, generates first-party data, and drives further personalization.

The purchase consideration was primarily allocated to developed technology intangible asset with an estimated fair value of $2.7 million at the acquisition date, which was valued using the cost to recreate method. The fair value of the remaining acquired tangible net assets was immaterial. The goodwill that was recorded represents the excess of the purchase consideration over the assets acquired and liabilities assumed relating to the acquisition and is immaterial.

The Company has not separately presented pro forma results reflecting the acquisition of Vibbio as the impacts were not material to the condensed consolidated financial statements.

16

Note 7. Intangible Assets

The Company’s acquired intangible asset subject to amortization was as follows (in thousands):

| September 30, 2022 | ||||||||||||||||||||

| Gross Carrying Amount | Accumulated Amortization | Net Carrying Amount | ||||||||||||||||||

| Developed technology | $ | $ | ( | $ | ||||||||||||||||

| Effect of foreign currency translation | ( | ( | ||||||||||||||||||

| Total | $ | $ | ( | $ | ||||||||||||||||

As of December 31, 2021, the Company had no intangible assets.

The intangible asset is amortized on a straight-line basis over its useful life of 4 years. As of September 30, 2022, the intangible asset had a remaining amortization period of 3.5 years.

The amortization expense for the three and nine months ended September 30, 2022 was $0.2 million and $0.3 million, respectively, and was included in research and development in the condensed consolidated statements of operations as the acquired technology will be used to enhance our existing product capabilities.

The estimated future amortization expense for the intangible asset is as follows (in thousands):

| Remainder of 2022 | $ | |||||||

| 2023 | ||||||||

| 2024 | ||||||||

| 2025 | ||||||||

| 2026 | ||||||||

| Total | $ | |||||||

Note 8. Leases

The Company entered into operating leases primarily for office facilities and finance leases primarily for computer and network equipment purchases. These leases have terms generally ranging from 3 years to 12 years. The Company’s lease agreements generally do not contain any material variable lease payments, residual value guarantees or restrictive covenants.

The balance sheet classification of the Company’s right-of-use assets and lease liabilities as of the period presented was as follows (in thousands):

| Leases | Classification | September 30, 2022 | ||||||||||||

| Non-Current Assets | ||||||||||||||

| Finance lease assets | $ | |||||||||||||

| Operating lease assets | Operating right-of-use asset | |||||||||||||

| Total leased assets | $ | |||||||||||||

| Current Liabilities | ||||||||||||||

| Finance | Finance lease liabilities, current | $ | ||||||||||||

| Operating | Operating lease liabilities, current | |||||||||||||

| Non-Current Liabilities | ||||||||||||||

| Finance | Finance lease liabilities | |||||||||||||

| Operating | Operating lease liabilities | |||||||||||||

| Total leased liabilities | $ | |||||||||||||

17

The components of lease cost were as follows (in thousands):

| Lease Cost | Classification | Three Months Ended September 30, 2022 | Nine Months Ended September 30, 2022 | |||||||||||||||||

| Finance lease cost | ||||||||||||||||||||

| Amortization of right-of-use assets | Depreciation and amortization | $ | $ | |||||||||||||||||

| Interest on finance lease liabilities | Interest expense | |||||||||||||||||||

| Operating lease cost | Selling, general and administrative expenses | |||||||||||||||||||

| Variable lease cost | Selling, general and administrative expenses | |||||||||||||||||||

| Total lease cost | $ | $ | ||||||||||||||||||

The undiscounted future lease payments under the lease liabilities as of September 30, 2022 were as follows (in thousands):

| Maturity of Lease Liabilities | Finance Lease | Operating Lease | ||||||||||||

| Remainder of 2022 | $ | $ | ||||||||||||

| 2023 | ||||||||||||||

| 2024 | ||||||||||||||

| 2025 | ||||||||||||||

| 2026 | ||||||||||||||

| Thereafter | ||||||||||||||

| Total lease payments | ||||||||||||||

| Less imputed interest | ( | ( | ||||||||||||

| Present value of lease liabilities | $ | $ | ||||||||||||

The undiscounted future lease payments as of December 31, 2021 prior to the Company’s adoption of the new lease standard were as follows (in thousands):

| Finance Lease | Operating Lease | |||||||||||||

| 2022 | $ | $ | ||||||||||||

| 2023 | ||||||||||||||

| 2024 | ||||||||||||||

| 2025 | ||||||||||||||

| Total payments | ||||||||||||||

| Less: Amount representing interest | ( | — | ||||||||||||

| Total payments, net of interest | $ | $ | ||||||||||||

Under ASC 840, the previous lease standard, rent expense, including common area maintenance charges, related to operating leases was $2.9 million, $2.8 million and $3.0 million, for 2021, 2020 and 2019, respectively.

The weighted-average lease term and discount rate as of September 30, 2022 were as follows:

| Finance Lease | Operating Lease | |||||||||||||

| Weighted-average remaining lease term | ||||||||||||||

| Weighted-average discount rate | % | % | ||||||||||||

18

Supplemental cash flow information was as follows (in thousands):

| Nine Months Ended September 30, 2022 | ||||||||

| Cash paid for amounts included in the measurement of lease liabilities: | ||||||||

| Operating cash flows used by operating leases | $ | |||||||

| Financing cash used by finance leases | ||||||||

| Right of use assets obtained in exchange for new lease liabilities: | ||||||||

| Operating leases - adoption | ||||||||

| Operating leases - nine months ended September 30, 2022 | ||||||||

| Finance leases | ||||||||

Note 9. Credit Facility

In September 2021, the Company amended its revolving line of credit with a financial institution effective August 2021, which increased the Company's borrowing capacity to a maximum of $50.0 million with a letter of credit sublimit of $4.0 million and a credit card sublimit of $1.0 million. The amendment allows the Company to borrow up to $50.0 million if the Company maintains at least $100.0 million on deposit at the institution. If such deposit is less than $100.0 million, the Company may borrow up to the lesser of $50.0 million or an amount determined by the Company's trailing five months of recurring revenue, annualized renewal rate and annualized monthly churn rate, as defined by the agreement. As of September 30, 2022, the Company did not draw down on its line of credit and has a borrowing capacity of $50.0 million. The terms of the agreement permit voluntary prepayment without premium or penalty. The revolving credit facility matures in August 2024 and is secured by substantially all of the Company’s assets. The outstanding principal balance on the revolving line of credit, if any, is due at maturity. The Company is required to pay quarterly in arrears a commitment fee of 0.15 % per annum on the undrawn portion available under the revolving line of credit. As of September 30, 2022, the Company had an outstanding standby letter of credit of $1.2 million as a guarantee for a leased space.

Interest on the revolving credit facility is payable monthly in arrears at a rate equal to the lender’s prime referenced rate as defined in the agreement. Prior to this amendment, interest on the revolving line of credit was the prime rate, as published by the Wall Street Journal (Prime Rate), plus 0.75 % effective July 31, 2020, and Prime Rate plus 0.50 % prior to July 31, 2020. The prime referenced rate was 6.25 % as of September 30, 2022 and 3.25 % as of September 30, 2021.

The revolving credit facility is subject to certain restrictions and financial covenants, including the requirement of maintaining a minimum debt to EBITDA ratio when the Company’s current portion of the total borrowing exceeds $5.0 million and the Company fails to maintain $100.0 million in deposits. In addition, the revolving line of credit agreement restricts the Company from paying dividends without prior approval from the financing institution. The Company was not subject to the financial covenants as of September 30, 2022.

Note 10. Commitment and Contingencies

Purchase Obligations

The Company has non-cancelable purchase commitments of $3.7 million as of September 30, 2022, primarily related to software license fees and co-location facilities and services, of which $0.9 million is expected to be paid in remainder of 2022, $2.6 million in 2023 and $0.2 million in 2024.

Contingencies

The Company has agreed to indemnify its directors and executive officers for costs associated with any fees, expenses, judgments, fines, and settlement amounts incurred by any of these persons in any action or proceeding to which any of those persons is, or is threatened to be, made a party by reason of the person’s service as a director or officer, including any action by the Company, arising out of that person’s services as the Company’s director or officer or that person’s services provided to any other company or enterprise at the Company’s request. The Company maintains director and officer insurance coverage that may enable the Company to recover a portion of any future amounts paid.

FASB ASC 450-20, Contingencies, sets forth the rules for accounting for uncertain tax positions for taxes not based on income. When a loss contingency exists, the likelihood of the incurrence of the liability can range from probable to remote. The Company believes it is reasonably possible that a loss will result from the sales and use tax assessments in the range of zero to $0.4 million. The Company has not

19

Legal Proceedings

The Company, its Chief Executive Officer, its Chief Financial Officer, certain current and former members of its Board of Directors and the underwriters that participated in the Company’s IPO are named as defendants in a consolidated putative class action, captioned In re ON24, Inc. Securities Litigation, 4:21-cv-08578-YGR (filed in November 2021), that is currently pending in the United States District Court for the Northern District of California. The consolidated complaint purports to assert claims under Sections 11 and 15 of the Securities Act of 1933 on behalf of all persons and entities that purchased, or otherwise acquired, the Company’s common stock issued in connection with the Company’s IPO. The complaint alleges that the Company’s registration statement and prospectus contained untrue statements of material fact and/or omitted material facts about ON24’s growth and customer base. Plaintiff seeks, among other things, an award of damages and attorneys’ fees and costs. Defendants filed a motion to dismiss the complaint in May 2022, which is currently pending. The Company believes the allegations in the consolidated complaint are without merit. The Company is unable to reasonably estimate a possible loss or range of possible loss, if any, arising from this matter at this early stage. Accordingly, no accrued litigation expense has been recorded in the accompanying condensed consolidated financial statements.

In June 2022, a shareholder derivative complaint, captioned Banks v. Sharan, et al., Case No. 3:22-cv-03861, was filed by a purported shareholder in the United States District Court for the Northern District of California. The complaint names as defendants the Company’s Chief Executive Officer, the Company’s Chief Financial Officer, and certain current and former members of the Company’s board of directors, and names the Company as a nominal defendant. The complaint purports to assert claims on the Company’s behalf against the individual defendants for breach of fiduciary duty and alleged violations of Sections 10(b) and 21D of the Securities Exchange Act of 1934. The complaint is based on allegations that are substantially similar to those in the putative class action filed in the United States District Court for the Northern District of California, described above. The complaint seeks, among other things, an award of damages on behalf of the Company, corporate governance reforms, and attorneys’ fees and costs. In September 2022, the plaintiff voluntarily dismissed the complaint without prejudice.

In the ordinary course of business, the Company may be subject from time to time to various proceedings, lawsuits, disputes or claims. Although the Company cannot predict with assurance the outcome of any litigation, the Company does not believe there are currently any actions, other than those described in the prior paragraph, that if resolved unfavorably, would have a material impact on its financial condition, results of operations or cash flows.

Note 11. Stockholders’ Equity and Equity Incentive Plan

Preferred Stock

The Company’s amended and restated certificate of incorporation authorized the issuance of 10,000,000 shares of undesignated preferred stock with a par value of $0.0001 per share. The Company’s board of directors is authorized to designate the rights, preferences, privileges and restrictions of the preferred stock from time to time.

Common Stock

The Company’s amended and restated certificate of incorporation authorized the issuance of 500,000,000 shares of common stock, $0.0001 par value per share. Holders of common stock are entitled to one vote per share.

Common Stock Reserved for Future Issuance

As of September 30, 2022, the Company had the following shares of common stock reserved for future issuance under its equity incentive plan and employee share purchase plan:

| Stock options outstanding | |||||

| Restricted stock units outstanding | |||||

Remaining shares available for future grant under 2021 Equity Incentive Plan(1) | |||||

Remaining shares available for future issuance under ESPP(2) | |||||

| Total shares of common stock reserved as of September 30, 2022 | |||||

(1)Includes the automatic annual increase of 2,386,367 additional shares under 2021 Equity Incentive Plan on January 1, 2022.

(2)Includes the automatic annual increase of 477,273 additional shares under ESPP on January 1, 2021.

20

Grant Activities

Stock Options

A summary of stock option activity under the Company’s equity incentive plans and related information is as follows:

| Options Outstanding | |||||||||||||||||||||||

Number of Shares | Weighted- Average Exercise Price | Weighted- Average Remaining Contractual Life (in years) | Aggregate Intrinsic Value (in thousands) | ||||||||||||||||||||

Balance as of December 31, 2021 | $ | ||||||||||||||||||||||

| Granted | |||||||||||||||||||||||

| Exercised | ( | $ | |||||||||||||||||||||

| Cancelled and forfeited | ( | ||||||||||||||||||||||

Balance as of September 30, 2022 | $ | $ | |||||||||||||||||||||

| Vested and exercisable | $ | $ | |||||||||||||||||||||

Restricted Stock Units

A summary of RSU activity under the Company’s equity incentive plans and related information is as follows:

| RSUs Outstanding | |||||||||||

Number of Shares | Weighted-Average Grant Date Fair Value | ||||||||||

Unvested balance as of December 31, 2021 | $ | ||||||||||

| Granted | |||||||||||

| Vested | ( | ||||||||||

| Cancelled and forfeited | ( | ||||||||||

Unvested balance as of September 30, 2022 | $ | ||||||||||

The total fair value of RSUs vested in the three and nine months ended September 30, 2022 was $4.9 million and $15.7 million, respectively. The total fair value of RSUs vested in the three and nine months ended September 30, 2021 was $0.6

The Company also had 187,500 performance-based RSUs that were vested during the nine months ended September 30, 2021.

21

Stock -Based Compensation

The stock-based compensation expense by line item in the accompanying condensed consolidated statements of operations is summarized as follows (in thousands):

| Three Months Ended September 30, | Nine Months Ended September 30, | ||||||||||||||||||||||

| 2022 | 2021 | 2022 | 2021 | ||||||||||||||||||||

| Cost of revenue | |||||||||||||||||||||||

| Subscription and other platform | $ | $ | $ | $ | |||||||||||||||||||

| Professional services | |||||||||||||||||||||||

| Total cost of revenue | |||||||||||||||||||||||

| Sales and marketing | |||||||||||||||||||||||

| Research and development | |||||||||||||||||||||||

| General and administrative | |||||||||||||||||||||||

| Total stock-based compensation expense | $ | $ | $ | $ | |||||||||||||||||||

As of September 30, 2022, unrecognized stock-based compensation expense by award type and their weighted-average recognition periods are as follows (in thousands, except years):

| Stock Option | RSU | ESPP | |||||||||||||||

| Unrecognized stock-based compensation expense | $ | $ | $ | ||||||||||||||

| Weighted-average amortization period | |||||||||||||||||

Repurchase of Common Stock

In December 2021, the Company’s Board of Directors authorized a $50.0 million share repurchase program. The timing and number of shares repurchased under the program will depend on a variety of factors, including stock price, trading volume, and general business and market conditions. The share repurchase program may be modified, suspended or discontinued at any time at the Company’s discretion.

When the Company has repurchased shares under the program, it reduced the common stock component of stockholder’s equity by the par value of the repurchased shares. The excess of the repurchase price over par value of the shares was charged to additional paid in capital as the Company is in an accumulated deficit position. All repurchased shares were retired and became authorized and unissued shares.

As of September 30, 2022, the Company had $21.0 million available for future share buybacks under the repurchase program. The following table presents certain information regarding shares repurchased under the program during the period presented:

| Nine Months Ended September 30, 2022 | |||||

| Number of shares repurchased | |||||

| Average price per share (including commissions) | $ | ||||

| Total repurchase costs (in millions) | $ | ||||

The Company did not repurchase shares during the three months ended September 30, 2022.

22

12. Other (Income) Expense, Net

Other (income) expense, net consisted of the following for the periods presented (in thousands):

| Three Months Ended September 30, | Nine Months Ended September 30, | |||||||||||||||||||||||||

| 2022 | 2021 | 2022 | 2021 | |||||||||||||||||||||||

| Interest income | $ | ( | $ | ( | $ | ( | $ | ( | ||||||||||||||||||

| Amortization (accretion) on marketable securities | ( | ( | ||||||||||||||||||||||||

| Foreign currency losses | ||||||||||||||||||||||||||

| Other | ( | ( | ( | ( | ||||||||||||||||||||||

| Other (income) expense, net | $ | ( | $ | $ | ( | $ | ||||||||||||||||||||

Note 13. Income Taxes

The Company’s provision for (benefit from) income taxes were as follows (in thousands):

| Three Months Ended September 30, | Nine Months Ended September 30, | ||||||||||||||||||||||

| 2022 | 2021 | 2022 | 2021 | ||||||||||||||||||||

Provision for (benefit from) income taxes | $ | $ | ( | $ | $ | ( | |||||||||||||||||

The Company’s provision for (benefit from) income taxes for interim periods is determined using an estimate of its annual effective tax rate, adjusted for discrete items, if any. The Company updates its estimate of the annual effective tax rate and makes a year-to-date adjustment to the provision quarterly. Provision for (benefit from) income taxes for the three and nine months ended September 30, 2022 changed by $0.1 million and $0.2 million, respectively, compared to the three and nine months ended September 30, 2021. The change in provision for (benefit from) income taxes was primarily driven by the tax shortfalls associated with stock-based compensation benefit in a foreign jurisdiction.

The Company regularly performs an assessment of the likelihood of realizing benefits of its deferred tax assets. As of September 30, 2022, the Company recorded a valuation allowance against its U.S. deferred tax assets based on available evidence. However, if there are favorable changes to actual operating results or to projections of future income, the Company may determine that it is more likely than not that such deferred tax assets may be realizable.

Utilization of net operating loss carryforwards, tax credits and other attributes may be subject to future annual limitations due to the ownership change limitations provided by Section 382 of the Internal Revenue Code and similar state provisions.

In August 2022, the Inflation Reduction Act of 2022 was signed into the U.S. law, which implements a new alternative minimum tax for some large corporations, an excise tax on stock buybacks, and significant tax incentives for energy and climate initiatives, among other provisions. The Company does not expect the Inflation Reduction Act to have a material impact on its consolidated financial statements.

Note 14. Net Loss Per Share Attributable to Common Stockholders

The following tables set forth the computation of basic and diluted net loss per share attributable to common stockholders for the periods presented (in thousands, except share and per share data):

| Three Months Ended September 30, | Nine Months Ended September 30, | |||||||||||||||||||||||||

| 2022 | 2021 | 2022 | 2021 | |||||||||||||||||||||||

Net loss | $ | ( | $ | ( | $ | ( | $ | ( | ||||||||||||||||||

| Cumulative preferred dividends allocated to preferred stockholders | ( | |||||||||||||||||||||||||

Net loss attributable to common stockholders | $ | ( | $ | ( | $ | ( | $ | ( | ||||||||||||||||||

Net loss per share of common stock, basic and diluted | $ | ( | $ | ( | $ | ( | $ | ( | ||||||||||||||||||

Weighted-average common stock outstanding, basic and diluted | ||||||||||||||||||||||||||

23

The following table sets forth the potential shares of common stock that were excluded from the computation of diluted net loss per share attributable to common stockholders for the periods presented because including them would have been antidilutive:

| Three Months Ended September 30, | Nine Months Ended September 30, | |||||||||||||||||||||||||

| 2022 | 2021 | 2022 | 2021 | |||||||||||||||||||||||

| Stock options | ||||||||||||||||||||||||||

| Restricted stock units | ||||||||||||||||||||||||||

| ESPP purchase rights | ||||||||||||||||||||||||||

| Total antidilutive securities | ||||||||||||||||||||||||||

Note 15. Related Party Transactions

16. Restructuring

In the third quarter of 2022, the Company initiated a strategic cost reduction plan, which included a reduction of the Company’s global full-time employee headcount as of June 30, 2022 through voluntary and involuntary headcount reductions. As of September 30, 2022, the Company’s full-time headcount decreased by approximately 6 % from June 30, 2022. Additionally, the Company incurred restructuring costs of $1.1 million during the third quarter of 2022, primarily related to severance and one-time termination benefits. The Company expects to incur additional restructuring costs of $1.0 million to $1.3 million in the fourth quarter of 2022 for such activities.

The following table summarizes the restructuring costs in our condensed consolidated statements of operations for the three and nine months ended September 30, 2022 (in thousands):

| Cost of revenue | |||||

| Subscription and other platform | $ | ||||

| Professional services | |||||

| Total cost of revenue | |||||

| Sales and marketing | |||||

| Research and development | |||||

| General and administrative | |||||

| Total restructuring costs | $ | ||||

The Company paid restructuring costs of $0.5 0.6 million and is included in accrued and other current liabilities on the condensed consolidated balance sheets.

24

Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations.

You should read the following discussion and analysis of our financial condition and results of operations together with the condensed consolidated financial statements and related notes included elsewhere in this Report on Form 10-Q. This discussion contains forward-looking statements based upon current expectations that involve risks and uncertainties. Our actual results may differ materially from those anticipated in these forward-looking statements as a result of various factors, including those discussed in the section titled “Risk Factors” and in other parts of this Report on Form 10-Q.

Overview

We provide a leading, cloud-based platform for digital engagement that delivers insights for revenue growth through interactive webinar experiences, virtual event experiences and multimedia content experiences. Our platform’s portfolio of interactive, personalized and content-rich digital experience products creates and captures actionable, real-time data at scale from millions of professionals every month to provide businesses with buying signals and behavioral insights to efficiently convert prospects into customers.

Similar to what has taken place in the business-to-consumer (B2C) market, our platform for digital engagement empowers business-to-business (B2B) companies with insights to better personalize their engagement. Large social media platforms have been successful at leveraging experiences and insights of consumers on their platforms to enable B2C companies to effectively understand their potential consumers. While these have been effective in the B2C market, B2B companies often lack deep insights about prospective customers to effectively understand and engage them.

Businesses today primarily use automated solutions, such as digital advertising and email, for marketing. While these automated solutions reach large numbers of prospective customers, they have generally failed to deepen customer engagement because they were designed with the simple purpose of pushing marketing messages in one direction—from the business to the prospective customer. For businesses to succeed, we believe their sales and marketing strategies must evolve from the era of automation to the era of engagement. Our platform provides an innovative way both to scale digital marketing and deepen prospective customer engagement. We believe our opportunity to help businesses convert digital engagement into revenue will continue to grow as industries modernize their sales and marketing processes.

We sell subscriptions to our platform’s experience products that are backed by analytics and our ecosystem of third-party integrations. Before 2013, we offered services and licensed software for managing webinars and virtual events primarily on a per event basis. In 2013, we transitioned to be a software-as-a-service company with the release of ON24 Elite and ON24 Virtual Conference as cloud-based subscription products. Substantially all of our customers subscribe to ON24 Elite, which enables customers to seamlessly broadcast video-based content and drive real-time interactivity in a single immersive experience. Our customers can host multiple tracks of their webinar experiences as a large-scale virtual event experience using ON24 Virtual Conference.

In 2018, we launched two complementary experience products, ON24 Engagement Hub and ON24 Target, to provide our customers with a system for digital engagement, offering customers the ability to curate and disseminate rich, multimedia content experiences. In addition to our products, we also provide professional services such as experience management, monitoring and premium support services, which provide the opportunity for recurring revenue, as well as implementation and other services.

In 2021, we launched ON24 Breakouts, which expanded the functionality and interactivity of webinars built with ON24 Elite. For example, breakouts enable attendees and presenters to network with each other face-to-face, sales teams to connect immediately with prospects and subject matter experts to offer two-way communication to support customer education and training.

In 2021, we also launched ON24 Go Live, which provides a new self-service virtual event solution for companies to stand up live-streaming video events faster and easier. Organizations can build a complete end-to-end external or internal event ranging from roadshows, customer conferences, virtual pop-ups, town halls, and company meetings, using pre-built templates and an easy-to-use and engaging interface.

We recently launched ON24 Forums that joins our portfolio of experience products and unifies engagement and data. ON24 Forums provides a new way to moderate interactive discussions and drive immediate action with audiences. For example, it enables audiences to participate in face-to-face, two-way video discussions.

In April 2022, we acquired Vibbio AS (Vibbio), a video software company in Norway. The integration of Vibbio’s video capabilities across the ON24 platform is intended to allow customers to produce video content that creates more engagement, generates first-party data, and drives further personalization.

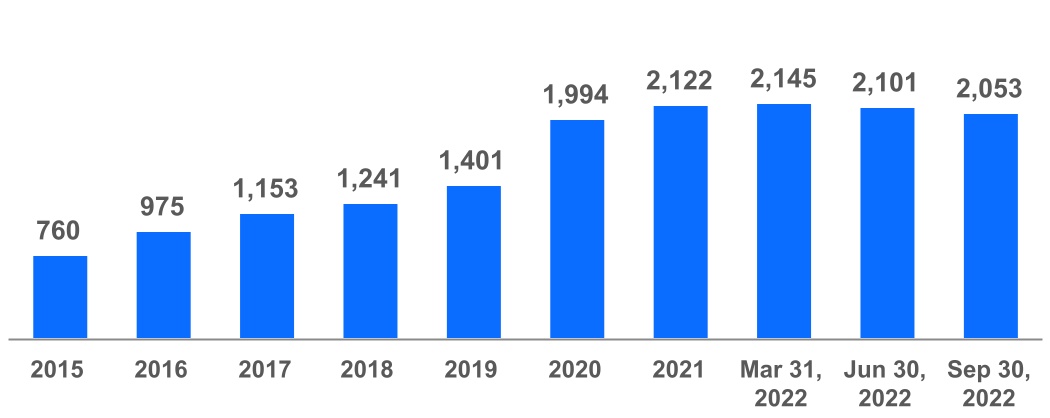

We deliver our platform products as cloud-based subscriptions that are easy to use and purpose-built for sales and marketing professionals. As of September 30, 2022, we had 2,053 customers.

25

Prior to developing our current cloud-based subscription model, we generated revenue from our Legacy offering, which primarily consisted of fully managed events and associated services. In connection with shifting to our current data-driven, cloud-based subscription model, we stopped selling our Legacy offering to new customers in 2018 and stopped selling it to all customers in 2020.

Our revenue was $47.6 million and $144.3 million for the third quarter and first nine months of 2022, respectively, compared to $49.4 million and $151.6 million for the same periods of 2021, representing a period-over-period decrease of 4% and 5%. We had a net loss of $14.4 million and $46.1 million for the third quarter and first nine months of 2022, respectively, compared to $9.4 million and $14.7 million for the same periods of 2021.

COVID-19 Update

The continued spread of COVID-19, any future variants that may be more transmissible and have more severe symptoms than current variants, may extend the impact of COVID-19 on our business. The impact of these variants cannot be predicted at this time and could depend on numerous factors, including vaccination rates among the population, the effectiveness of COVID-19 vaccines against emerging variants, and any new measures that may be introduced by governments or other parties in response to an increase in COVID-19 cases.

During the COVID-19 pandemic, digital became the primary way for people to connect, work, learn and be entertained, and for businesses to engage with customers. The imperative to optimize digital sales and marketing investments to drive revenue conversion has become increasingly important as businesses have accelerated digital transformation initiatives in response to the COVID-19 pandemic, resulting in increased usage of our subscription and other platforms, especially during the height of the COVID-19 pandemic in 2020 and early 2021.

There is no assurance that we will experience in future periods the same level of accelerated growth we experienced in 2020, and to a lesser extent in 2021. For example, our revenue recently decreased by 4% and 5% in the third quarter and first nine months of 2022, respectively, compared to the same periods in 2021. Our revenue growth rate also declined in 2021 compared to 2020. We may continue to face declines in our revenue in future periods as the impact of COVID-19 continues to lessen. If the effects of the COVID-19 pandemic continue to subside, our customers and their users may increasingly resume in-person marketing activities in a way that decreases usage of our platform. The extent of the impact of COVID-19 on our business and financial performance may be influenced by a number of factors, many of which we cannot control, including the emergence of recent and any future variants of the virus, future spikes of COVID-19 infections resulting in additional preventative and mitigative measures, the severity of the economic decline attributable to or influenced by the COVID-19 pandemic, the timing and nature of a potential economic recovery, the impact on our customers and our sales cycles, and our ability to generate new business leads. For additional details, see the section titled “Risk Factors.”

Key Factors Affecting Our Performance

Acquiring New Customers