Use these links to rapidly review the document

TABLE OF CONTENTS

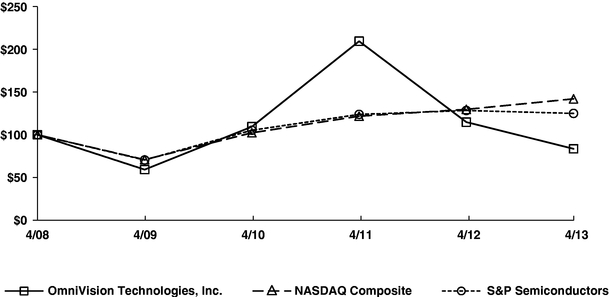

ITEM 8. FINANCIAL STATEMENTS AND SUPPLEMENTARY DATA

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

| (Mark One) | ||

ý |

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

|

For the fiscal year ended April 30, 2013 |

||

o |

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

|

For the transition period from to |

||

Commission file number: 0-29939 |

||

OMNIVISION TECHNOLOGIES, INC.

(Exact name of registrant as specified in its charter)

| Delaware | 77-0401990 | |

| (State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer Identification Number) |

|

4275 Burton Drive, Santa Clara, California 95054 (Address of principal executive offices) (Zip Code) |

||

Registrant's telephone number, including area code: (408) 567-3000 |

||

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Name of each exchange on which registered | |

|---|---|---|

| Common Stock, $0.001 par value (Including associated Preferred Stock Purchase Rights) |

The Nasdaq Stock Market LLC (Nasdaq Global Market) |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ý No o

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No ý

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ý No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ý No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained herein, and will not be contained, to the best of the Registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ý

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of "large accelerated filer," "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act.

| Large accelerated filer ý | Accelerated filer o | Non-accelerated filer o (Do not check if a smaller reporting company) |

Smaller reporting company o |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No ý

As of October 31, 2012, the last business day of Registrant's most recently completed second fiscal quarter, there were 53,541,659 shares of Registrant's common stock outstanding, and the aggregate market value of such shares held by non-affiliates of registrant (based upon the closing sale price of such shares on the NASDAQ Global Market on October 31, 2012 was approximately $765.6 million. Shares of Registrant's common stock held by the Registrant's executive `officers and directors and by each entity that owns five percent or more of Registrant's outstanding common stock have been excluded in that such persons may be deemed to be affiliates. This determination of affiliate status is not necessarily a conclusive determination for other purposes.

As of June 20, 2013, 54,657,293 shares of common stock of the Registrant were outstanding, exclusive of 20,599,187 shares of treasury stock.

DOCUMENTS INCORPORATED BY REFERENCE

The Registrant has incorporated by reference into Part III of this Annual Report on Form 10-K portions of its Proxy Statement for the 2013 Annual Meeting of Stockholders.

OMNIVISION TECHNOLOGIES, INC.

INDEX TO

ANNUAL REPORT ON FORM 10-K

FOR YEAR ENDED APRIL 30, 2013

2

The following information should be read in conjunction with our audited consolidated financial statements and the notes thereto included in Item 8 of this Annual Report on Form 10-K. This Annual Report on Form 10-K contains forward-looking statements, within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934, which involve risks and uncertainties. Forward-looking statements generally include words such as "anticipates," "believes," "expects," "intends," "may," "outlook," "plans," "seeks," "will" and words of similar import as well as the negative of those terms. In addition, any statements that refer to expectations, projections or other characterizations of future events or circumstances, including any underlying assumptions, are forward-looking statements. All forward-looking statements included in this Annual Report on Form 10-K, including, but not limited to, statements regarding our projected results of operations for future reporting periods, the continuing shift of our sales towards our OmniBSI-2 devices, the extent of future sales through original equipment manufacturers, or OEMs, and distributors, future growth trends and opportunities in certain markets, the capabilities of new products, our expectations regarding our customers' future actions, the timing of the production of our products, the continuing capabilities of our production system, the increasing competition in our industry, the effect of supply constraints, the ability of our suppliers to cost effectively expand to meet supply needs, the continued importance of the mobile phone market to our business, our expectations regarding market preferences with respect to image sensor technologies, the continued concentration of manufacturers in the mobile phone market, the further expansion of the smartphone segment within the mobile phone market, continued price competition and the consequent reduction in the average selling prices of our products, anticipated benefits of our joint ventures and alliances, the ability of our new products to mitigate declines in our average selling prices, the development of our business and manufacturing capacity, future expenses we expect to incur, our future investments, our future working capital requirements, the effect of a change in foreign currency exchange and market interest rates, the geographic distribution of our sales and end-users of our products, the continued improvement of general global and domestic economic conditions, our ability to improve our inventory turnover and to generate positive cash flow, the effects of adjustments to our tax positions and the sufficiency of our available cash, cash equivalents and short-term investments are based on current expectations and are subject to important factors that could cause actual results to differ materially from those projected in the forward-looking statements. Such important factors include, but are not limited to, those set forth in Part I under the caption "Item 1A. Risk Factors," beginning on page 16 of this Annual Report and elsewhere in this Annual Report and in other documents we file with the U.S. Securities and Exchange Commission, or SEC. All subsequent written and oral forward-looking statements by or attributable to us or persons acting on our behalf are expressly qualified in their entirety by such factors.

OmniVision, the OmniVision logo, OmniPixel and TrueFocus are registered trademarks of OmniVision Technologies, Inc., CameraChip, CameraCubeChip, OmniBSI, OmniBSI+, OmniBSI-2, OmniPixel2, OmniPixel3, OmniPixel3-HS, OmniQSP and SquareGA and ViV are trademarks of OmniVision Technologies, Inc. Wavefront Coded and Wavefront Coding are registered trademarks of OmniVision CDM Optics, Inc., a wholly-owned subsidiary of OmniVision Technologies, Inc.

Corporate Information

OmniVision Technologies, Inc., a Delaware corporation, was incorporated in May 1995 in California, and reincorporated in Delaware in March 2000. Our executive offices are located at 4275 Burton Drive, Santa Clara, California 95054 and our telephone number is (408) 567-3000. Copies of our Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Proxy Statement for our annual stockholders' meeting and Current Reports on Form 8-K, as well as any amendments to these reports, are available through our website as soon as reasonably practicable after we electronically file such documents with, or furnish them to, the SEC. Information about our company is available on the Internet at www.ovt.com. The information in, or that can be accessed through, our website is not part of this report.

3

Overview

We design, develop and market high-performance, highly integrated and cost-efficient semiconductor image-sensor devices. Our main products, image-sensing devices which we refer to as CameraChip™ image sensors, capture an image electronically and are used in a number of consumer and commercial mass-market applications. Our CameraChip image sensors are manufactured using the complementary metal oxide semiconductor, or CMOS, fabrication process and are predominantly single-chip solutions that integrate several distinct functions including image capture, image processing, color processing, signal conversion and output of a fully processed image or video stream. We have also integrated our CameraChip image sensors with wafer-level optics, which we refer to as CameraCubeChip™ imaging devices. Our CameraCubeChip imaging device is a small footprint, total camera solution that we believe will enable the further miniaturization of camera products. We believe that our highly integrated image sensors and imaging devices enable camera device manufacturers to build high quality camera products that are smaller, less complex, more reliable, more cost-effective and more power-efficient than cameras using traditional charge-coupled devices, or CCDs.

Current Economic Environment

We operate in a challenging economic environment that has undergone significant changes in technology and in patterns of global trade. We remain a leader in the development and marketing of image sensing devices based on the CMOS fabrication process and have benefited from the growing market demand for and acceptance of this technology.

Since the latter part of fiscal 2009, we have experienced fluctuations in our financial results due in part to changing macroeconomic conditions. As macroeconomic conditions have improved, our sales have also tended to improve and when macroeconomic uncertainties have returned, our sales have tended to be negatively impacted. In fiscal 2013, macroeconomic conditions appeared to gradually improve and our quarterly and annual sales also improved as compared to the similar prior year periods. Nevertheless, given the current economic environment and continuing uncertainties that exist, we remain cautious and we expect our customers to be cautious as well, which could affect our future results. If the economic recovery slows down or even dissipates, our business, financial condition, results of operations and cash flows could be materially and adversely affected.

Market Environment

We sell our products worldwide directly to OEMs, which include branded customers and contract manufacturers, and value added resellers, or VARs, and indirectly through distributors. In order to ensure that we address all available markets for our image sensors, we organize our marketing efforts into end-use market groups, each of which concentrates on a particular product or, in some cases, customers within a product group. Thus, we have marketing teams that address the mobile phone market, the entertainment market, the notebook and webcam market, the digital still camera, or DSC, market, the security and surveillance market, and the automotive and medical markets.

In the mobile phone market in particular, future revenues depend to a large extent on an extensive design win process where a particular mobile phone maker determines which image sensor to design into one or more specific models. The time lag between design win and volume shipments varies from as little as three months to as much as 12 months, which could cause an unexpected delay in generating revenues, especially during periods of product transitions. Design wins are also an important driver in the many other markets that we address. In some markets, such as automotive or medical applications, the time lag between a particular design win and revenue generation can be longer than one year.

The overwhelming majority of our sales depend on decisions by the engineering designers for manufacturers of products that incorporate image sensors to specify one of our products rather than one made by a competitor. In most cases, the decision to specify a particular image sensor requires

4

conforming other specifications of the product to the chosen image sensor and makes subsequent changes both difficult and expensive. Accordingly, the ability to produce and deliver reliable products in large quantities and in a timely manner is a key competitive differentiator. Since our inception, we have shipped more than 4.0 billion image sensors, including approximately 855 million in fiscal 2013. We believe that these quantities demonstrate the capabilities of our production system, including our sources of offshore fabrication.

We outsource the wafer fabrication and packaging of our image-sensor products to third parties. We outsource the color filter and micro-lens phases of production to VisEra Technologies Company, Ltd., or VisEra, our joint venture with Taiwan Semiconductor Manufacturing Company Limited, or TSMC. This approach allows us to focus our resources on the design, development, marketing and testing of our products and to significantly reduce our capital requirements.

To increase and enhance our production capabilities, we work closely with TSMC, our principal wafer supplier and one of the largest wafer fabrication companies in the world, to increase, as necessary, the number of its fabrication facilities at which our products can be produced. Our investments in VisEra and three other key back-end packaging suppliers are part of a broad strategy to ensure that we have sufficient back-end capacity for the processing of our image sensors in the various formats required by our customers. To enhance our CameraCubeChip production capabilities, we acquired from VisEra in October 2011 its CameraCubeChip production and assembly operations, which we had previously outsourced to them.

We currently perform the final testing of our packaged products at our own facility in China. As necessary, we will make further investments to expand our testing and production capacity, as well as our overall capability to design additional custom products for our customers.

Since our customers' end-user customers market and sell their products worldwide, our revenues by geographic location are not necessarily indicative of the geographic distribution of end-user sales, but rather indicate where the products and/or their components are manufactured or sourced. The revenues we report by geography are based on the country or region in which our customers issue their purchase orders to us.

Many of the products using our image sensors, such as mobile phones, entertainment applications such as tablets, notebooks and webcams, and DSCs, are consumer electronics goods. These mass-market camera devices generally have seasonal cycles which historically have caused the sales of our customers to fluctuate quarter-to-quarter. In addition, since a very large number of the manufacturers who use our products are located in China and Taiwan, the pattern of demand for our image sensors has been increasingly influenced by the timing of the extended lunar or Chinese New Year holiday, a period in which the factories which use our image sensors generally close. Consequently, demand for our image sensors has historically been stronger in the second and third quarters of our fiscal year and weaker in the first and fourth quarters of our fiscal year. Due to the macroeconomic uncertainties that have existed during the past several years, the seasonal cycle of our business has been less predictable. Beginning in fiscal 2013, our business started to recover and the seasonal cycle in our business became very pronounced. Nonetheless, given the current economic environment, we remain cautious toward our near-term business prospects and the return of the historical seasonal cycle of our business. Should the historical seasonal cycle return, we also believe that our fiscal 2014 seasonal cycle will be less pronounced when compared to fiscal 2013. While we believe that the market opportunities represented by mobile phones and entertainment applications such as tablets remain very large, the opportunities presented could be deferred because of the uncertainty surrounding the sustainability of the current global economic recovery.

We believe that, like the DSC market, mobile phone, tablet, notebook and webcam demand will not only continue to shift toward higher resolutions, but also will increasingly fragment into multiple market segments with differing product attributes. For example, we see the further expansion of the

5

smartphone segment within the mobile phone market. In addition, there is increased demand for customization, and several different interface standards are coming to maturity. All of these trends will require the development of a broader variety of products.

As the markets for image sensors have grown, we have experienced competition from manufacturers of CMOS and CCD image sensors. Our principal competitors in the market for CMOS image sensors include Aptina Imaging, Samsung, Sharp, Sony, STMicroelectronics and Toshiba. We expect to see continued price competition in the image-sensor market for mobile phones, entertainment devices, notebooks and webcams, security and surveillance systems, digital still and video cameras, automotive and medical imaging systems as those markets continue to grow. Although we believe that we currently compete effectively in those markets, our competitive position could be impaired by companies that have greater financial, technical, marketing, manufacturing and distribution resources, broader product lines, better access to large customer bases, greater name recognition, longer operating histories and more established strategic and financial relationships than we do. Such companies may be able to adapt more quickly to new or emerging technologies and customer requirements or devote greater resources to the promotion and sale of their products. Many of these competitors own and operate their own fabrication facilities, which in certain circumstances may give them the ability to price their products more aggressively than we can or may allow them to respond more rapidly than we can to changing market opportunities.

In addition, from time to time, other companies enter the CMOS image-sensor market by using obsolete and available manufacturing equipment. While these efforts have rarely had any long-term success, the new entrants do sometimes manage to gain market share in the short-term by pricing their products significantly below current market levels, which may put additional downward pressure on the prices that we can obtain for our products.

In common with many other semiconductor products and as a response to competitive pressures, the average selling prices, or ASPs, of image-sensor products have declined steadily since their introduction, and we expect ASPs to continue to decline in the future. Some of this ASP decline may be offset by the adoption of some of our newer and higher resolution products. We have also started to ship our CameraCubeChip products, which carries a higher ASP because of the added value from the attachment of wafer-level optics to our image sensors. Depending on the adoption rate and unit volume, we believe these products may also mitigate the rate of ASP decline. In order to maintain or grow our revenues, we need to increase the number of units we sell by a large enough amount to offset the effect of declining ASPs.

Separately, in order to maintain our gross margins, we and our suppliers must work continuously to lower our manufacturing costs and increase our production yields. Recently, we requested our suppliers to invest in additional equipment in connection with the production of our OmniBSI-2 products. Such investment resulted in higher product costs and lower gross margins for us in fiscal 2013. If we are unable to spread such added cost over larger unit sales or successfully negotiate lower prices with our suppliers, our gross margin may continue to stay at these lower levels for future periods as well. In addition, if we are unable to timely develop and introduce new products that can take advantage of smaller process geometries or new products that incorporate more advanced technology and include more advanced features that can be sold at higher ASPs, our gross margin may decline.

Having the ability to forecast customer demand correctly and to prepare the appropriate level of inventory to meet this demand is also important in the semiconductor industry. In fiscal 2011, the entire semiconductor industry, including us, experienced supply constraints. Due to supply constraints, semiconductor companies were unable to meet the product demands of their customers and had to take certain actions such as allocating available products among their customers or, in some cases, increasing the prices of their products. This resulted in harm to customer relations, the loss of sales to customers and, in some cases, the loss of future business with those customers. We faced these same

6

challenges as we sought to meet our customers' demand for our products. Despite these challenges, through careful strategic planning relating to our products and the technologies that we delivered to market, we were able to achieve revenue growth and unit growth. If supply constraints were to happen again and we were unable to manage our products appropriately, our relations with our customers and their end-user customers may be harmed and we may be unable to achieve future sales growth, which could result in our revenues, gross margins and other financial results being materially and adversely affected. Conversely, an excess in inventory supply can also adversely affect our performance. During the second quarter of fiscal 2012, certain of our key customers unexpectedly cut back their orders. In addition to reducing our unit sales of our OmniBSI and OmniPixel3-HS based products and adversely affecting our revenues for the second and third quarters of fiscal 2012, the cutback also resulted in our inventories at the end of the second and third quarters of fiscal 2012 being higher than we intended them to be. During the fourth quarter of fiscal 2012 and during fiscal 2013, we significantly increased our OmniBSI-2 inventories as we prepared for anticipated increases in the sales of these products. Since our production capacity ramp is slower than our customers' production ramp schedule, we must build inventory to ensure we can meet our obligations to customers. However, since customer demand can be volatile, we may be unable to sell inventories that were built in excess of demand, or we may have to sell at lower prices to eliminate excess inventories. Under such circumstances, we may be required to record significant provisions for excess and obsolete inventories. This could materially and adversely affect our results of operations and financial condition. We expect the business environment to remain volatile in fiscal 2014, especially in the consumer-oriented product markets, which could continue to affect our ability to accurately forecast customer demand.

Given the rapidly changing nature of our technology, there can be no assurance that we will not encounter delays or other unexpected production yield issues with future products. In general, during the early stages of production, production yields and gross margins for new products are typically lower than those of established products. During production, we can also encounter unexpected manufacturing issues, such as unexpected back-end yield problems.

In addition, in preparation for new product introductions, we gradually decrease production of established products. Due to our 12-14 week production cycle, it is extremely difficult to predict precisely how many units of established products we will need. It is also difficult to accurately predict the speed of the ramp of new products. Given the current economic uncertainty, the visibility of our business outlook is extremely limited and forecasting is even more difficult than under normal market conditions. As a result, it is possible that we could suffer from shortages of certain products and build inventories in excess of demand for other products. We carefully consider the risk that our inventories may be in excess of expected future demand and record appropriate reserves. If, as sometimes happens, we are subsequently able to sell these reserved products, the sales have little or no associated cost and, consequently, they have a favorable impact on gross margins.

Technology

Image Sensor Technologies

In May 2008, we announced a new approach to CMOS image sensor design we call OmniBSI™ technology. OmniBSI technology is based on an idea called back side illumination, or BSI. All traditionally designed CMOS image sensors capture light on the front side of the chip, so the photo-sensitive portion has to share the surface of the image sensor with the metal wiring of the transistors in the imaging pixel and the metal wiring acts to limit the amount of image light that reaches the photo-sensitive portion of the image sensor. This type of pixel architecture is referred to as the front side illumination, or FSI, architecture. With our OmniBSI architecture, the image sensor receives light through the back side of the chip. As a result, there is no metal wiring to block the image light, and the entire backside of the image sensor can be photo-sensitive. Not only does this enable us to produce a superior image, it also permits the front of the chip surface area to be devoted entirely to processing,

7

and permits an increase in the number of metal layers, both of which result in greater functionality. Capturing light on the back side of the image sensor also allows us to reduce the distance the light has to travel to the imaging pixels, and thus provide a wider angle of light acceptance. Widening the angle of light acceptance in turn makes it possible to reduce the height of the camera module, and thus the height of the device which incorporates the camera module.

Since 2008, we have continued to refine our BSI technology. In February 2010, we announced our OmniBSI-2™ architecture built on the advanced 300 mm copper process at the facilities of TSMC. The OmniBSI-2 architecture represents our second-generation BSI technology and enables us to design imaging pixels as small as 1.1 µm in dimension. In January 2012, we introduced new image sensors based on OmniBSI+™, our improved 1.4 µm OmniBSI architecture. The OmniBSI+ architecture offers significant performance and image quality improvements over our original OmniBSI pixel architecture, and maintains a comparable cost structure.

CameraCubeChip Technology

In February 2009, we announced the introduction of our CameraCubeChip technology. This is a three-dimensional, reflowable, total camera solution that combines the full functionality of our CameraChip image sensors and wafer-level optics in one compact, small-footprint package. Our CameraCubeChip devices can be soldered directly to printed circuit boards, with no socket or insertion requirements. We believe our CameraCubeChip solution can streamline the mobile phone manufacturing process, thus resulting in lower cost and faster time-to-market for our customers. Although currently our customers primarily use our CameraCubeChip devices as secondary cameras in mobile handsets, going forward we anticipate that they will be used as the primary camera in mobile handsets.

Other Technologies

In March 2010, we acquired Aurora Systems, Inc., or Aurora, a privately-held company incorporated in California. Aurora is a supplier of liquid crystal on silicon, or LCOS, devices for use in mobile projection applications and high definition home theater projection systems. With the acquisition of Aurora, we acquired advanced image projection technology to capitalize on trends in the emerging video-projection consumer market.

In January 2013, we introduced a dual-camera video sharing technology that we call Video-in-Video, or ViV™. ViV allows for the combination of video feeds from both the front- and rear-facing cameras into a single video stream.

Product Design

Mixed Analog/Digital Circuit and CMOS Image Sensor Design

We have the in-house expertise to design complex analog and digital semiconductor circuits. This in-house expertise enables us to process video data in both analog and digital domains, which has allowed us to optimize each aspect of analog and digital chip design. We have also developed in-house expertise in the mixing of analog and digital signals in the same semiconductor design without suffering the common problems of interference from noise caused by heat or cross-talk. Our in-house semiconductor design engineers are skilled in the design of high speed, low power, and mixed analog/digital image sensors with advanced pixel cell structures. We use advanced design techniques to develop high-speed, highly integrated semiconductors which can be fabricated using standard CMOS processes. The result has been a combination of improved image quality coupled with a reduction in unwanted electrical noise.

8

Advanced Image Processing

We have developed a broad range of proprietary technologies for image processing. For example, we developed algorithms to produce high dynamic range images and to enable gesture-cognitive applications. We also put significant emphasis on low power consumption and high efficiency in our image signal processing.

Integrated Camera Solutions

We have also developed a significant level of in-house expertise in applied optical science with proprietary technologies to integrate our image sensors with wafer-level optics. We now offer total camera solutions which we market as CameraCubeChips, and are tailored to our customers' specific imaging requirements.

Products

Our main products, CameraChip image-sensing devices, are used to capture images electronically and are used in a number of consumer and commercial mass-market applications. Our image-sensor products have a variety of features, including:

| CMOS CameraChip image sensors | Color or black and white | |

Illumination Technique |

Front side illumination or back side illumination |

|

Resolutions |

CIF (352 × 288 pixels) to 16-megapixels (4,608 × 3,456 pixels) |

|

Output signal |

Analog and digital |

|

Operating voltage |

5 volt to 1.2 volt |

|

Optical lens/array size |

1/18 to 1/2.3 inch formats |

|

In addition, we design and develop another category of products which we refer to as CameraCubeChip imaging devices. They are image sensors with integrated wafer-level optics. We also supply companion chips used to connect our image sensors to various interfaces, including the universal serial bus, or USB, a connection which allows add-on devices to be connected to notebook and webcams and other industry standard interfaces such as the Mobile Industry Processor Interface, or MIPI, and low-voltage differential signaling, or LVDS. In addition, we provide companion digital signal processors, or DSP, that perform compression in standardized still photo and digital video formats.

We also design and develop standard software drivers for Linux, Mac OSX and Microsoft Windows, as well as for embedded operating systems such as Android, Blackberry OS, Symbian, Windows CE, Windows Embedded and Windows Mobile. These software drivers accept the image data being received from the USB, provide data decompression, if required, and manage interface protocols with the camera. We have designed these drivers for speed and flexibility and to allow easy customization of the user interface. We do not record any revenue from this software, which we provide to our customers as an element of customer support.

New Products

In May 2012, we introduced the OV16820 and OV16825, two 16-megapixel CMOS image sensors designed for the digital still and video camera markets and the high-end smartphone market, respectively. The two 1/2.3-inch image sensors are built on our 1.34-µm OmniBSI-2 pixel architecture.

9

They can operate at 30 FPS in full 16-megapixel resolution, at 60 FPS in 4K2K (3840 × 2160) resolution, and at 60 FPS in 1080p HD video mode. Additionally, the sensors support 16-megapixel burst photography.

In May 2012, we also introduced the OV2722, a 1/6-inch native 1080p HD CMOS image sensor based on our 1.4-µm OmniBSI+ pixel architecture. The OV2722 is designed specifically for ultra-portable applications where high performance and low profile are critical. It can fit inside camera modules with module height of less than 3-mm.

In May 2012, we also added the OVM7675 VGA CameraCubeChip to our portfolio of CameraCubeChip imaging devices. The OVM7675 has a module size of 2.9 × 2.9 × 2.3 mm and is designed to address the needs of front-facing camera applications in smartphones, tablets and notebooks. The OVM7675 is built on our OmniPixel3-HS pixel technology, and is capable of capturing VGA video at 30 FPS.

In May 2012, we introduced a fourth product, the OV12830, a 12-megapixel CMOS image sensor based on our 1.1-µm OmniBSI-2 pixel architecture. The 1/3.2-inch OV12830 is designed for high-end smartphones and tablets. To support high-speed photography and to minimize shutter lag from shot to shot, the OV12830 can operate at 24 FPS in full 12-megapixel resolution, and at 30 FPS in 16:9 aspect ratio 10-megapixel resolution. The OV12830 can also capture 1080p HD video at 60 FPS.

In August 2012, we introduced the OV7955, a NTSC analog and digital image sensor designed specifically for automotive applications. The OmniPixel3-HS based image sensor is suitable for rear-view, surround-view and blind spot detection systems.

In August 2012, we also introduced the OV5648, a 1/4-inch 5-megapixel CMOS image sensor based on our 1.4-µm OmniBSI+ pixel architecture. The OV5648 is capable of capturing high quality still images as well as 720p HD video at 60 FPS and 1080p HD video at 30 FPS.

In August 2012, we introduced a third product, the OV7695, our first VGA image sensor based on the OmniBSI+ pixel architecture. The 1/13-inch OV7695 is built on a 1.75-µm OmniBSI+ pixel architecture, and can capture VGA video at 30 FPS.

In October 2012, we introduced the OV480, a companion processor designed to enhance camera performance in wide field-of-view applications for automotive vision systems. The OV480 processor supports a wide range of OmniVision image sensors designed specifically for automotive applications.

In October 2012, we also introduced the OV5645, a system-on-chip 5-megapixel CMOS image sensor based on our 1.4-µm OmniBSI pixel architecture. The OV5645 offers 5-megapixel photography, 720p HD video at 60 FPS and 1080p HD video at 30 FPS. In addition, the OV5645 features a picture-in-picture architecture that allows for the attachment of a secondary camera to itself, thus enabling both cameras to communicate with the baseband processor via a single interface.

In October 2012, we introduced a third product, the OV8835, a 1/3.2-inch 8-megapixel CMOS image sensor based on an improved 1.4-µm OmniBSI-2 pixel architecture. The OV8835 can operate at 30 FPS for zero shutter lag high speed photograph. It is also capable of capturing full 1080p HD video at 30 FPS with electronic image stabilization, or EIS, or 720p HD video at 60 FPS with full horizontal field-of-view.

In October 2012, we also introduced a new CameraCubeChip imaging device, the OVM7695. It is a compact VGA CameraCubeChip with a module size of 2.4 × 2.4 × 2.3 mm. The OVM7695 is built on an optimized 1.75-µm OmniBSI+ pixel design, capable of capturing high-quality VGA video at 30 FPS.

In November 2012, we introduced the OV5656, a 5-megapixel CMOS image sensor based on our 1.75-µm OmniBSI+ pixel architecture. The 1/3.2-inch OV5656 is designed to address the needs of the

10

smartphone, tablet and digital video camera markets. The OV5656 offers full-resolution, high-speed photography at 30 FPS. It can also record 1080p HD video at 30 FPS with EIS, and 720p HD video at 60 FPS.

In January 2013, we introduced the OV4688, a 4-megapixel CMOS image sensor built on our 2-µm OmniBSI-2 pixel architecture. The 1/3-inch OV4688 captures full-resolution 4-megapixel HD video at 90 FPS, 1080p HD at 120 FPS with EIS, and 720p HD at 180 FPS. These features are designed for mobile applications that require high quality, fast frame rate HD video and photography.

In January 2013, we also introduced a LCOS chipset solution for HD pico projection systems. The chipset solution comprises the OVP7200, a single-chip color field sequential LCOS panel that displays native 720p HD video, and the OVP921, a companion chip that accepts video data from different signal inputs and provides advanced image processing. The LCOS chipset is designed for pico projection systems in mobile devices and head-up displays in automotive applications.

In April 2013, we introduced the OV9728, a 720p HD image sensor based on our 1.75-µm OmniBSI+ pixel architecture. The 1/6.5-inch OV9728 captures 720p HD video at 30 FPS or high quality cropped VGA video at 60 FPS. The OV9728 is designed specifically for front-facing camera applications in notebooks, tablets, smartphones, and smart TVs.

In April 2013, we also introduced the OV2724, a 1/6-inch 1080p HD image sensor based on our 1.34-µm OmniBSI-2 pixel architecture. The OV2724 captures 1080p HD video at 60 FPS with enhanced high dynamic range, and has the capability to reduce or eliminate common sources of image contamination, such as fixed pattern noise and smearing. The OV2724 is designed for front-facing camera applications in smartphones, tablets and notebooks.

Strategic Investments and Acquisitions

Joint Venture with TSMC

In October 2003, we entered into an agreement with TSMC, to form VisEra, a joint venture in Taiwan, for the purposes of providing certain manufacturing and automated final testing services related to CMOS image sensors. In August 2005, we and TSMC formed VisEra Holding Company, or VisEra Cayman, a company incorporated in the Cayman Islands, and VisEra became a subsidiary of VisEra Cayman. We and TSMC have equal interests in VisEra Cayman.

In June 2011, we entered into an agreement with VisEra to acquire from VisEra its CameraCubeChip production operations. We introduced the CameraCubeChip imaging devices near the end of fiscal 2009, and we had been outsourcing the production to VisEra. With the acquisition, we enhanced our CameraCubeChip production capabilities. See Note 5—"Long-Term Investments," Note 6—"Acquisition of Production Operations from VisEra," and Note 18—"Related Party Transactions" to our consolidated financial statements.

Acquisition of Aurora

In March 2010, we acquired Aurora. Aurora designed, marketed and sold LCOS-based microdisplay panels. These microdisplay panels are used for projection applications in consumer electronics, industrial, aerospace and mobile viewing platforms. We believe there is an emerging trend for video-projection applications in the consumer market. The advanced image projection technology we acquired through Aurora is intended to enable us to capitalize on this trend.

11

Acquisition of Kodak Patents

In March 2011, we acquired certain image-sensor related patents and patent applications from Eastman Kodak Company, or Kodak. In connection with the acquisition, we granted to Kodak world-wide, non-exclusive royalty-free licenses, without the right to sublicense, to use the purchased patents to manufacture and sell current image-sensor products and other Kodak products incorporating image sensors.

Industry Background

Image Sensor Technologies

Digital imaging enables the capture of still or moving images without the use of photographic or chemical-based films. The two most common electronic image sensors, both developed in the late 1960s, are CCD and CMOS image sensors. Both image sensors are silicon-based semiconductor devices that convert light to an electric charge for display or storage.

CMOS image sensors are typically less expensive to produce and consume significantly less power than CCDs. When originally introduced, the quality of CMOS image sensors lagged behind that of CCDs, but in recent years, advances in semiconductor manufacturing processes and design techniques have led to significant improvements in CMOS image sensor performance and image quality. Smaller circuits and better current control made it possible to design CMOS image sensors that provide image quality comparable to that of CCDs of comparable resolution. As a result, CMOS image sensors are now widely used in camera-equipped mobile phones, entertainment applications such as tablets, notebooks and webcams, DSCs, security and surveillance systems, and increasingly in automotive and medical applications, all areas where high image quality, low power consumption, small size and low cost are important considerations.

Most conventional CMOS image sensors operate on FSI technology, in which the image sensor captures light on the front side of the chip, so the photo-sensitive portion has to share the surface of the image sensor with the metal wiring of the transistors in the pixel. Currently, the most advanced CMOS image sensors operate on the BSI technology in which, as its name implies, the image sensor captures light on the back side of the chip. The advantages of BSI technology over conventional FSI technology are discussed in more detail under the sub-heading "Technology" on page 7 above.

CMOS Image Sensors versus CCD Image Sensors

One of the critical differences between CCD and CMOS image sensors is the way in which each processes an electrical charge, or a signal. Cameras employing CCDs require an additional integrated circuit called an analog-to-digital converter to convert a signal from analog to digital format. In contrast, image sensors based on the CMOS manufacturing process are able to integrate a number of functions on one device, enabling all of the conversion circuitry to be incorporated in a single image sensor chip. This high level of integration reduces the overall number of components and system complexity, and reduces the space required for them. We have seen multiple markets, such as security, automotive, as well as DSCs, transitioning away from CCDs, a process that we expect to continue.

Market Opportunity

Demand for CMOS image sensors for use in mobile phones continued to account for a substantial portion of our revenue in fiscal 2013. Other applications and markets that we are currently serving or that are developing include embedded applications for entertainment devices such as tablets, notebooks and webcams, security and surveillance, DSCs, and automotive and medical applications. As device manufacturers become increasingly aware of the numerous advantages associated with single chip CMOS image sensor solutions, such as high image quality, accelerated time to market, efficient design

12

and manufacturability, smaller size, lower power consumption and reduced cost, we believe these markets offer significant additional opportunities for mass-market applications for CMOS image sensors.

Customers

We sell directly to OEMs and VARs and indirectly through distributors. OEMs include branded camera device manufacturers and contract manufacturers. Often times, contract manufacturers and distributors serve multiple end-user customers in the consumer device markets, and end-user customers also engage multiple contract manufacturers and distributors. During fiscal 2013, we shipped approximately 855 million image sensors, an increase of 39.0% from approximately 615 million image sensors in fiscal 2012.

In fiscal 2013, we derived approximately 81.2% of our revenues from sales to OEMs and VARs and approximately 18.8% of our revenues from sales through distributors. The three OEM customers that accounted for 10% or more of our revenues in fiscal 2013 were LG Innotek Co., Ltd., Foxconn Technology Group, and Cowell Electronics Co., Ltd., which accounted for approximately 18.0%, 10.7%, and 10.3% of our revenues, respectively. The one distributor that accounted for 10% or more of our revenues in fiscal 2013 was World Peace Industrial Group, which accounted for approximately 11.7% of our revenues. No other OEM, VAR or distributor accounted for 10.0% or more of our fiscal 2012 revenues.

Sales and Marketing

We sell our products through a direct sales force and indirectly through distributors. As of April 30, 2013, our sales and marketing organization had a total of 182 full-time employees. We also had 12 independent distributors, 10 of which are located outside the United States.

Sales outside of the United States represented approximately 98.3%, 93.1% and 99.7% of our revenues in fiscal 2011, 2012 and 2013, respectively. We expect that sales outside of the United States will continue to account for a very large proportion of our revenues. We use distributors outside the United States principally to facilitate the logistics of the transactions in question and provide credit to end-user customers. These distributors also assume responsibility for collections, product returns and customer support. In addition to our standard product marketing, we also participate in tradeshows and other industry events to promote our imaging solutions.

Research and Development

We have designed the internal structure of our CMOS CameraChip and CameraCubeChip image sensors in a modular fashion. The major functions, such as image capture, image sensor control logic, color processing, analog output, digital output and programming control, are stand-alone circuits that we can rapidly modify for use in new product developments. We design circuit improvements so that we can transfer them readily to other CameraChip image sensor products to help reduce total development time and cost for new products. Our CameraCubeChip imaging devices also include integrated wafer-level optics. We developed our wafer-level optical technology with scalability and manufacturability in mind, enabling us to introduce a larger portfolio of CameraCubeChip products in the future. As of April 30, 2013, we had a total of 630 full-time employees engaged in research and development. Research, development and related expenses for fiscal 2011, 2012 and 2013 were approximately $88.5 million, $110.7 million and $113.2 million, respectively.

Intellectual Property

Our success and future revenue growth will depend, in part, on our ability to protect our intellectual property. We rely on a combination of patents, copyrights, trademarks and trade secrets, as

13

well as nondisclosure agreements and other methods, to protect various aspects of our CameraChip and CameraCubeChip image sensors. As of April 30, 2013, we have been issued 583 United States patents which expire between May 2013 and November 2031. We have also received 736 foreign patents which expire between January 2015 and December 2029. As of April 30, 2013, we have 248 additional United States patent applications pending, of which 13 have been allowed, and we have 855 foreign patent applications pending, of which 40 have been allowed.

We have in the past been, currently are and may in the future be, subject to legal proceedings and claims with respect to our intellectual property, including such matters as trade secrets, patents, product liabilities and other actions arising out of the normal course of business. These claims may increase as our intellectual property portfolio becomes larger or more valuable. Intellectual property claims against us, and any resulting lawsuit, may cause us to incur significant expenses, subject us to liability for damages and invalidate our proprietary rights. Any potential intellectual property litigation against us would likely be time-consuming and expensive to resolve and would divert management's time and attention.

Manufacturing

Wafer Fabrication

Our semiconductor products are fabricated using standard CMOS processes, which permit us to engage independent wafer foundries to manufacture our semiconductors. We outsource our wafer manufacturing for image sensors to TSMC and Powerchip Technology Corporation, or PTC. Our image sensor products are currently fabricated using standard line geometry processes at 65 nm, 0.11 µm, 0.13 µm, 0.18 µm and 0.25 µm.

Color Filter Application

The majority of our fiscal 2013 image sensor sales were color image sensors, which, in addition to a micro-lens, require a color filter to be applied to the wafer before packaging. The color filter application uses a series of masks to place red, green and blue dyes on the individual pixels in an industry-standard Bayer pattern. In the final step, a micro lens is applied to each pixel. We outsource these manufacturing steps primarily to VisEra.

Wafer Probe Testing

After wafer fabrication, color filter application, if required, and micro-lens application, wafers are designated for either unpackaged or packaged deliveries. For unpackaged deliveries, referred to as chip-on-board, or COB, the wafers are tested using a process called wafer probe testing. The process identifies the good die on each wafer. We outsource wafer probe testing primarily to King Yuan Electronics Co., Ltd. and Tong Hsing Electronic Industries, Ltd., or Tong Hsing, an investee company. We then rely on Tong Hsing to prepare the good die as identified during the wafer probe testing for final delivery in a format referred to as reconstructed wafers.

Packaging

We support various packaging methods that are widely used for optical image sensor chips. In the case of chip scale packaged, or CSP, products, the wafers are packaged and then diced into chips. These packages have a glass lid to allow light to pass through to the image sensor array. We rely primarily on XinTec Inc., or XinTec, an investee company, for our CSP products. For other plastic and ceramic packaged products, the wafers are diced first and then packaged. We rely primarily on Lingsen Precision Industries Co., Ltd., or Lingsen, and Tong Hsing for such packaging services.

14

See Note 5—"Long-Term Investments" to our consolidated financial statements for a further description of our relationships with XinTec and Tong Hsing.

CameraCubeChip Assembly

We introduced our CameraCubeChip imaging devices near the end of fiscal 2009. To enhance our CameraCubeChip production capabilities, we acquired from VisEra in October 2011 its CameraCubeChip production operations, which we had previously outsourced to them.

Final Testing

High volume final product testing is a critical element in the production of our image sensors. Having this capability is a substantial barrier to entry for potential competitors. Production final testing instruments designed for conventional CMOS devices are not sufficient for testing image sensors, because an optical image must be captured and checked in addition to checking the standard logic and electrical functions. For our packaged products and CameraCubeChip imaging devices, we have installed high-throughput automated final test equipment built to our specifications at our testing facility in Shanghai, China. The final test equipment have automated handling capability, a lighting and lens system, a changeable image source and automated output sorting by functionality. The system is programmable so that testing criteria and methodology can be changed easily to accommodate new products or special testing requirements.

Product Quality Assurance

We focus on product quality through all stages of the design and manufacturing process. We submit all our designs to in-depth circuit simulation before we commit them to silicon. Before we commit a new product to production, we fabricate test wafers, package test chips and test the final product. We keep initial production runs to a minimum until sufficient products have completed the entire manufacturing and testing process and met the product specifications. It is only then that we will commit the product to full production runs.

We qualify each of our subcontractors through a series of industry standard environmental product stress tests, as well as through an audit and an analysis of the subcontractor's quality system and manufacturing capability. We also participate in quality and reliability monitoring through each stage of the production cycle by reviewing electrical parametric data from our foundries and other subcontractors.

Competition

We operate in an industry characterized by intense competition, rapid technological changes, evolving industry standards, declining ASPs and rapid product obsolescence. Our competition comes both from CMOS and CCD image sensor manufacturers:

- •

- CMOS Image Sensor Manufacturers. Image sensor

manufacturers using CMOS technology include a number of well established companies such as Aptina Imaging, Samsung, Sharp, Sony, STMicroelectronics and Toshiba.

- •

- CCD Image Sensor Manufacturers. Image sensor manufacturers using CCD technology include a number of well-established companies, particularly vertically integrated camcorder and high-resolution DSC manufacturers. Our main competition from CCD manufacturers comes from Panasonic, Sharp and Sony.

Our competitors include many large domestic and international companies that have greater presence in key markets, greater access to advanced wafer foundry capacity, substantially greater financial, technical, marketing, manufacturing, distribution and other resources, better access to large

15

customer bases, greater name recognition, longer operating histories and more established strategic and financial relationships than we do. As a result, they may be able to adapt more quickly to new or emerging technologies and customer requirements or devote greater resources to the promotion and sale of their products.

We believe that the principal factors affecting our competition in our markets include relationships with key OEMs that incorporate image sensors into mass-market applications, relationships with key distributors, relationships with semiconductor foundries and other participants in the semiconductor manufacturing chain, time to market, quality, total system design cost, product performance, customer support and supplier reputation. We believe that we compete effectively with respect to these factors.

Backlog

Sales are generally made pursuant to standard purchase orders. Our backlog includes only accepted customer orders with assigned shipment dates within the upcoming 12 months. As of April 30, 2012 and 2013, our backlog was approximately $237.8 million and $340.3 million, respectively. The increase in our backlog reflects, in part, an increase in product demand. Our current backlog is subject to cancellation or changes in delivery schedules, and may not necessarily be an indication of future revenue.

Employees

As of April 30, 2013, we had a total of 2,057 full-time employees, 413 located in the United States, and 1,644 in China, Germany, India, Japan, Norway, Singapore, South Korea, Taiwan and the United Kingdom. Our future success will depend, in part, on our ability to continue to attract, retain and motivate highly qualified technical and management personnel. None of our employees is represented by a collective bargaining agreement, and we have never experienced any material work stoppage. We believe that our employee relations are good.

Financial Information About Geographic Areas

For information about revenues and long-lived assets by geographic region/country, see Note 16—"Segment and Geographic Information" in Part II, Item 8 of this Form 10-K and "Management's Discussion and Analysis of Financial Condition and Results of Operations" in Part II, Item 7 of this Form 10-K.

Executive Officers of the Registrant

The following persons are our executive officers as of the filing date of this report:

Name

|

Age | Position | |||

|---|---|---|---|---|---|

Shaw Hong |

75 | Chief Executive Officer and Director | |||

Raymond Wu |

58 | President | |||

Anson Chan |

44 | Vice President of Finance and Chief Financial Officer | |||

Y. Vicky Chou |

50 | Senior Vice President of Global Management and General Counsel | |||

Ray Cisneros |

50 | Senior Vice President of Worldwide Sales and Sales Operations | |||

John Li |

45 | Vice President of System Technologies | |||

Howard Rhodes |

64 | Chief Technical Officer | |||

Henry Yang |

48 | Chief Operating Officer and Director | |||

Zille Hasnain |

58 | Vice President of Quality and Reliability | |||

Shaw Hong, one of our cofounders, has served as one of our directors and as our Chief Executive Officer since May 1995, and as our President from May 1995 to December 2012. Mr. Hong holds a

16

B.S. degree in electrical engineering from Jiao Tong University in China and an M.S. degree in electrical engineering from Oregon State University.

Raymond Wu, one of our cofounders, has served as our President since December 2012. From 2006 to 2012, Mr. Wu served as President of EU3C USA, Inc., a consumer electronics company. Prior to August 2006, Mr. Wu served as one of our directors since May 1995, and as our Executive Vice President since October 1999. Prior to October 1999, Mr. Wu was the head of our sales department and our engineering department. Mr. Wu received a B.S. degree in electrical engineering from Chung-Yuan University in Taiwan and an M.S. degree in electrical engineering from Wayne State University.

Anson Chan has served as our Vice President of Finance and Chief Financial Officer since October 2008 at which time he assumed the additional position of Chief Financial Officer. From February 2007 to present, Mr. Chan has served as our Vice President of Finance. From July 2006 to February 2007, Mr. Chan served as our Vice President of Business Strategy. From September 1997 to July 2006, Mr. Chan served in various positions with PricewaterhouseCoopers, LLP, a public accounting firm, most recently as a Senior Manager. Mr. Chan holds a B.S. degree in economics and a B.S. degree in engineering from the University of Pennsylvania and an M.B.A. degree in business strategy and operations management from the University of Chicago. Mr. Chan is also a Certified Public Accountant licensed in the State of California.

Y. Vicky Chou has served as our Senior Vice President of Global Management and General Counsel since February 2012. From August 2009 to February 2012, Ms. Chou served as our Vice President of Global Management and General Counsel. From June 2003 to August 2009, Ms. Chou served as our Vice President of Legal and General Counsel. From February 2003 to June 2003, Ms. Chou served as our Corporate Counsel. From August 1999 to January 2003, Ms. Chou was an attorney at Heller Ehrman White & McAuliffe LLP. From June 1997 to July 1999, Ms. Chou was an attorney/corporate specialist at Coudert Brothers LLP. Ms. Chou received a B.S. degree in anthropology from Temple University, an M.B.A. degree from St. Joseph's University and a J.D. degree from Santa Clara University.

Ray Cisneros has served as our Senior Vice President of Worldwide Sales and Sales Operations since February 2012. From August 2009 to February 20012, Mr. Cisneros served as our Vice President of Worldwide Sales. From September 2006 to August 2009, Mr. Cisneros served as our Vice President of Sales. From December 2004 to September 2006, Mr. Cisneros served as our Director of Sales and Marketing for North American Sales. Prior to December 2004, Mr. Cisneros held various sales positions since joining our company in October 2002 including key account management, regional management and sales operations roles. Prior to joining our company, Mr. Cisneros held various senior management positions in the area of sales and marketing for companies in the fiber optics and semiconductor industries, including Sagitta, Inc., a provider of manufacturing equipment solutions for the fiber-optics industry, UMC, a semiconductor foundry, and Novellus Systems, Inc., a provider of manufacturing equipment for the semiconductor industry. Mr. Cisneros holds a B.S. in Metallurgical Engineering from Illinois Institute of Technology and an M.B.A. from Golden Gate University.

John Li has served as our Vice President of System Technologies since August 2009. From November 2004 to August 2009, Mr. Li served as our Senior Director of Applications Engineering. Prior to November 2004, Mr. Li held various senior engineering positions subsequent to joining our company in February 1997. Prior to joining our company, Mr. Li held various electrical engineering positions with companies in the semiconductor and electronics industries, including HuaKo Electronics Co. Ltd in Hong Kong, a manufacturer of semiconductor devices, and Fudan University in China. Mr. Li specialized in electrical engineering while attending Fudan University.

17

Dr. Howard Rhodes has served as our Chief Technical Officer since February 2012. From August 2005 to February 2012, Dr. Rhodes served as our Vice President of Process Engineering. Dr. Rhodes served as our Senior Director of Process Engineering from September 2004 to August 2005. Prior to joining OmniVision, Dr. Rhodes worked at Micron Technology, Inc., a provider of semiconductor solutions, from 1988 to 2004 as Director of Imager Engineering, and at Kodak Research Labs, a division of Eastman Kodak Company, an imaging company, from 1980 to 1988 as Process Integration Engineer where he was in charge of process development and process integration for high speed visible and IR sensitive CCD products. Dr. Rhodes earned his B.S., M.S, and Ph.D. degrees in Solid State Physics from the University of Illinois.

Dr. Henry Yang has served as our Chief Operating Officer since February 2012. In addition, Dr. Yang has served as one of our directors since his appointment in February 2010. From February 2007 to February 2012, Dr. Yang served as our Vice President of Engineering. From February 2003 to January 2007, Dr. Yang served as our Director of Engineering. Prior to February 2003, Dr. Yang held various engineering positions since joining our company in April 1996. Dr. Yang holds B.E., M.E. and Ph.D. degrees in Electrical Engineering from the Tsinghua University in China.

Zille Hasnain has served as our Vice President of Quality and Reliability since February 2012. Prior to joining OmniVision, Mr. Hasnain served as Senior Director of Quality Assurance and Customer Support from 1983 to January 2012 at Micron Technology, Inc., a provider of semiconductor solutions, where he worked to ensure all Micron DRAM, Flash and CMOS image sensor products met quality and reliability expectations when entering high volume shipments. Mr. Hasnain holds an M.B.A. in Business Administration with an emphasis on Quantitative Analysis from Washington State University.

This Annual Report on Form 10-K, including Management's Discussion and Analysis of Financial Condition and Results of Operations, contains forward-looking statements. These forward-looking statements are subject to substantial risks and uncertainties that could cause our future business, financial condition or results of operations to differ materially from our historical results or currently anticipated results, including those set forth below.

Risks Related to Our Business

For the majority of our revenues, we depend on a few key customers and, the loss of one or more of our key customers, or their key end-user customers, could significantly reduce our revenues.

A relatively small number of OEMs, VARs and distributors account for a significant portion of our revenues. Some of these OEMs, VARs and distributors are major producers of mobile phones, including smartphones, for some of the largest companies in the mobile phone industry and may rely upon one or more key end-user customers for a significant portion of their revenue. Any material delay, alteration, cancellation or reduction of purchase orders from or change in the purchasing patterns of one or more of our major customers or distributors, or their key end-user customers, could result in our failure to achieve our revenue forecast for a particular period. For example, in our second quarter of fiscal 2012, we experienced an unexpected cutback in orders from certain of our key customers. This reduced the unit sales of our OmniBSI and OmniPixel3-HS based products and adversely affected our revenue for that quarter. In addition, if we are unable to retain one or more of our largest OEM, VAR or distributor customers, if we are unable to maintain our current level of revenues from one or more of these significant customers, if our OEM, VAR or distributor customers are unable to retain one or more of their key end-user customers, or if we are unable to attract new customers to replace the revenue lost from such customers, our business and results of operation would be impaired, and our stock price could decrease, potentially significantly. Such a delay, alteration, cancellation or reduction of purchase orders, a change in purchasing patterns or our inability to retain

18

a key customer or several of our smaller customers could be caused by, among other things, failure to meet our customers', including their key end-user customers', demand for our products or to timely develop and introduce new products that meet the needs of our customers, including their key end-user customers, and that are efficiently and successfully integrated into their products. In fiscal 2012 and 2013, approximately 52.0% and 57.7%, respectively, of our revenues came from sales to our top five customers. In addition, in fiscal 2013, three OEM customers accounted for approximately 39.0% of our revenues, and one distributor customer accounted for approximately 11.7% of our revenues. Our business, financial condition, results of operations and cash flows will continue to depend significantly on our ability to retain our current key customers and to attract new customers, as well as on the financial condition and success of our OEMs, VARs and distributors, including their ability to retain their key end-user customers and attract new customers.

We face intense competition in our markets from CMOS and CCD image-sensor manufacturers, and if we are unable to compete successfully we may not be able to maintain or grow our business.

The image-sensor market is intensely competitive, and we expect competition in this industry to continue to increase. This competition has resulted in rapid technological change, evolving standards, reductions in product selling prices and rapid product obsolescence. If we are unable to successfully meet these competitive challenges, we may be unable to maintain and grow our business. Any inability on our part to compete successfully would also adversely affect our results of operations and impair our financial condition.

Our image-sensor products face competition from other companies that sell CMOS image sensors and from companies that sell CCD image sensors. Many of our competitors have longer operating histories, greater presence in key markets, greater name recognition, larger customer bases, more established strategic and financial relationships and significantly greater financial, sales and marketing, distribution, technical and other resources than we do. Many of them also have their own manufacturing facilities, which may give them a competitive advantage. As a result, they may be able to adapt more quickly to new or emerging technologies and customer requirements or devote greater resources to the promotion and sale of their products. Our competitors include established CMOS image-sensor manufacturers such as Aptina Imaging, Samsung, Sharp, Sony, STMicroelectronics and Toshiba as well as CCD image-sensor manufacturers such as Panasonic, Sharp and Sony. Many of these competitors own and operate their own fabrication facilities, which in certain circumstances may give them the ability to price their products more aggressively than we can, respond more rapidly than we can to changing market opportunities or more easily meet increased demands for their products. In addition, we compete with a large number of smaller CMOS manufacturers that has required, and in the future may require, us to reduce our prices. For instance, we have seen increased competition in the markets for VGA image-sensor products with resulting pressures on product pricing. Downward pressure on pricing could result both in decreased revenues and lower gross margins, which would adversely affect our profitability. From time to time, other companies enter the CMOS image-sensor market by using obsolete and available manufacturing equipment. These new entrants gain market share in the short term by pricing their products significantly below current market levels, which puts additional downward pressure on the prices we can obtain for our products.

Our competitors may acquire or enter into strategic or commercial agreements or arrangements with foundries or providers of color filter application, wafer probe testing, assembly or packaging services. These strategic arrangements between our competitors and third party service providers could involve preferential or exclusive arrangements for our competitors. Such strategic alliances could impair our ability to secure sufficient capacity from foundries and service providers to meet our demand for wafer manufacturing, color filter application, wafer probe testing, assembly or packaging services, adversely affecting our ability to meet customer demand for our products. In addition, competitors may enter into exclusive relationships with distributors, which could reduce available distribution channels

19

for our products and impair our ability to sell our products and grow our business. Further, some of our customers could also become developers of image sensors, and this could potentially adversely affect our results of operations, business and prospects.

The development of new and more complex products can increase our cost of revenue and adversely affect our gross margins.

A key component of our future success is the continued development of new and innovative products and technologies. These new products and technologies are often times very complex and may require additional equipment and resources to develop and manufacture. In addition, for these new products, we may initially experience lower production yields than our other more established products. These new products and technologies also often have a higher cost structure than our existing products and technologies because we must devote more time and effort to developing the products and technologies and our suppliers and manufacturers may incur additional costs by acquiring new equipment or components in order to meet our design specification and capacity requirements. As our product mix shifts to include a higher volume of these new products and technologies, our gross margins may be lower than in comparable historical periods. For example, our OmniBSI-2 products have very different production requirements when compared to our previous generation products and we had to request our suppliers to install new equipment and tooling, which increased the production costs for these new products. Because we experienced increased sales of our OmniBSI-2 products in fiscal 2013, and expect these products to constitute a significant percentage of our total sales in fiscal 2014, we anticipate that our gross margins will remain at lower levels than we have experienced historically, before our introduction of OmniBSI-2. If we are unable to sufficiently increase our ASPs to offset these higher production costs, increase our yields or lower the costs associated with the development and manufacture of these new products and technologies, our gross margins could continue to be negatively affected.

Reductions in our average selling prices may lower our revenues and, as a result, may reduce our gross margins.

We have experienced and expect to continue to experience pressure to reduce the selling prices of our products, and our ASPs have generally declined over time as a result. Competition in our product markets is intense and as competition continues to intensify, we anticipate that these pricing pressures will increase. Although we experienced an increase in our ASPs for the three months ended April 30, 2013 as a result of favorable product mix, we expect that the ASPs for many of our products will continue to decline over time. Unless we can increase unit sales sufficiently to offset these declines in our ASPs, our revenues will decline. Reductions in our ASPs have adversely affected our gross margins, and unless we can reduce manufacturing costs to compensate, additional reductions in our ASPs will continue to adversely affect our gross margins and could materially and adversely affect our operating results and impair our financial condition. Historically we have increased and are likely to continue to increase our research, development and related expenses in the long-term to continue the development of new image-sensor products that can be sold at higher selling prices and/or manufactured at lower cost. If we are unable to timely introduce new products that incorporate more advanced technology and include more advanced features that can be sold at higher ASPs, or if we are unable to successfully develop more cost-effective technologies, our financial results could be adversely affected.

Sales of our image-sensor products for mobile phones, including smartphones, account for a large portion of our revenues, and any decline in sales to the mobile phone market or failure of this market and other emerging markets to continue to grow as expected could adversely affect our results of operations.

Sales to the mobile phone market, including smartphones, account for a large portion of our revenues. Although we can only estimate the percentages of our products that are used in the mobile

20

phone market due to the significant number of our image-sensor products that are sold to module makers or through distributors and VARs, we believe that the mobile phone market accounted for approximately 56% and 59% of our revenues in fiscal 2012 and 2013, respectively. We expect that revenues from sales of our image-sensor products to the mobile phone market will continue to account for a significant portion of our revenues during fiscal 2014 and beyond. Any factors adversely affecting the demand for our image sensors in this market could cause our business to suffer and adversely affect our financial condition, operating results and cash flows. The digital image-sensor market for mobile phones is extremely competitive, and we expect to face increased competition in this market in the future. In addition, we continue to believe the market for mobile phones is also relatively concentrated and the top five producers account for approximately 66% of the annual sales of these products. If we do not continue to achieve design wins with key mobile phone manufacturers or if we experience a cutback in orders from our key customers, such as the cutback we experienced in our second quarter of fiscal 2012, our market share or revenues could decrease. The mobile phone image-sensor market is also subject to rapid technological change. In order to compete successfully in this market, we will have to correctly forecast customer demand for technological improvements and be able to deliver such products on a timely basis at competitive prices. If we fail to correctly forecast customer demand and timely deliver products at competitive prices, our results of operations, business and prospects would be materially and adversely affected. In the past, we have experienced problems accurately forecasting customer demand in our target markets. In addition, current domestic and global economic conditions could negatively affect the mobile phone market if consumers and/or businesses defer purchases in this market in response to tighter credit, negative financial news, and/or decreased corporate or consumer spending.

We also expect that image sensors will become more important in the notebook and webcam, entertainment, security, medical and automotive industries. As image sensors begin to fill a greater role in these other markets, the challenges and risks that we face in these other markets could increase and could be similar to some of the challenges and risks that we face in the mobile phone market. If our sales to the mobile phone market and other emerging markets do not increase and/or the mobile phone market and other emerging markets do not grow as expected, our results of operations, business and prospects would be materially adversely affected.

If we do not forecast customer demand correctly, our business could be impaired and our stock price may decline.