JANUARY 28, 2021

|

Summary Prospectus |

BlackRock Balanced Capital Fund, Inc. | Class K Shares

Class K: MKCPX

Before you invest, you may want to review the Fund’s

prospectus, which contains more information about the Fund and its risks. You can find the Fund’s prospectus (including amendments and supplements), reports to shareholders and other information about the Fund, including the Fund’s

statement of additional information, online at http://www.blackrock.com/prospectus. You can also get this information at no cost by calling (800) 537-4942 or by sending an e-mail request to

prospectus.request@blackrock.com, or from your financial professional. The Fund’s prospectus and statement of

additional information, both dated January 28, 2021, as amended and supplemented from time to time, are incorporated by reference into (legally made a part of) this Summary Prospectus.

This

Summary Prospectus contains information you should know before investing, including information about risks. Please read it before you invest and keep it for future reference.

The Securities and Exchange Commission has not approved or

disapproved these securities or passed upon the adequacy of this Summary Prospectus. Any representation to the contrary is a criminal offense.

Not FDIC Insured • May Lose Value • No Bank

Guarantee

Summary Prospectus

Key Facts About BlackRock Balanced Capital Fund, Inc.

Investment Objective

The investment objective of BlackRock Balanced Capital Fund,

Inc. (the “Fund”) is to seek the highest total investment return through a fully managed investment policy utilizing equity, debt (including money market) and convertible securities.

Fees and Expenses of the Fund

This table describes the fees and expenses that you may pay if

you buy, hold and sell Class K Shares of the Fund. You may pay other fees, such as brokerage commissions and other fees to your financial professional or your selected securities dealer, broker, investment adviser,

service provider or industry professional (including BlackRock Advisors, LLC (“BlackRock”) and its affiliates) (each, a “Financial Intermediary”), which are not reflected in the table and example below.

| Annual

Fund Operating Expenses (expenses that you pay each year as a percentage of the value of your investment) |

Class

K Shares |

| Management Fee1,2 | 0.42% |

| Distribution and/or Service (12b-1) Fees | None |

| Other Expenses | 0.06% |

| Acquired Fund Fees and Expenses3 | 0.27% |

| Total Annual Fund Operating Expenses3 | 0.75% |

| Fee Waivers and/or Expense Reimbursements1,2 | (0.25)% |

| Total Annual Fund Operating Expenses After Fee Waivers and/or Expense Reimbursements1,2 | 0.50% |

| 1 | As described in the “Management of the Fund” section of the Fund’s prospectus beginning on page 38, BlackRock has contractually agreed to waive its management fee by the amount of any management fees the Fund pays the manager of the Master Portfolios (defined below) indirectly through its investment in the Master Portfolios for as long as the Fund invests in the Master Portfolios. The contractual agreement may be terminated upon 90 days notice by a majority of the non-interested directors of the Fund or by a vote of a majority of the outstanding voting securities of the Fund. |

| 2 | As described in the “Management of the Fund” section of the Fund’s prospectus beginning on page 38, with the exception of the Fund’s investment in the Master Portfolios, BlackRock has contractually agreed to waive the management fee with respect to any portion of the Fund’s assets estimated to be attributable to investments in other equity and fixed-income mutual funds and exchange-traded funds managed by BlackRock or its affiliates that have a contractual management fee, through January 31, 2022. In addition, BlackRock has contractually agreed to waive its management fees by the amount of investment advisory fees the Fund pays to BlackRock indirectly through its investment in money market funds managed by BlackRock or its affiliates, through January 31, 2022. The contractual agreements may be terminated upon 90 days notice by a majority of the non-interested directors of the Fund or by a vote of a majority of the outstanding voting securities of the Fund. |

| 3 | The Total Annual Fund Operating Expenses do not correlate to the ratio of expenses to average net assets given in the Fund’s most recent annual report, which does not include Acquired Fund Fees and Expenses. |

Example:

This Example is intended to help you compare the cost of investing in the

Fund with the cost of investing in other mutual funds. The Example assumes that you invest $10,000 in the Fund for the time periods indicated and then redeem all of your shares at the end of those periods. The Example also assumes that your

investment has a 5% return each year and that the Fund’s operating expenses remain the same. Although your actual costs may be higher or lower, based on these assumptions your costs would be:

| 1 Year | 3 Years | 5 Years | 10 Years | |

| Class K Shares | $51 | $165 | $289 | $651 |

Portfolio Turnover:

The Total Return Portfolio (defined below) and the Core Portfolio (defined

below) pay transaction costs, such as commissions, when they buy and sell securities (or “turn over” their portfolios). A higher portfolio turnover rate may indicate higher transaction costs and may result in higher taxes when shares are

held in a taxable account. These costs, which are not reflected in annual fund operating expenses or in the Example, affect the performance of the Total Return Portfolio and the Core Portfolio. During the most recent fiscal year, the Fund’s

turnover rate was 0% of the average value of its portfolio, excluding transactions in the Master Portfolios (defined below). During the most recent

2

fiscal year, the Total Return Portfolio’s turnover rate was 556% of the

average value of its portfolio and the Core Portfolio’s turnover rate was 99% of the average value of its portfolio.

Principal Investment Strategies of the Fund

The Fund invests in equity securities (including common stock,

preferred stock, securities convertible into common stock, or securities or other instruments whose price is linked to the value of common stock) and fixed-income securities (including debt securities, convertible securities and short term

securities). The Fund may make investments directly in equity and fixed-income securities, indirectly through one or more funds that invest in such securities, or in a combination of securities and funds. Fund management shifts the allocation among

these securities types. The proportion the Fund invests in each category at any given time depends on Fund management’s view of how attractive that category appears relative to the others. This flexibility is the keystone of the Fund’s

investment strategy. The Fund intends to invest at least 25% of its assets in equity securities and at least 25% of its assets in senior fixed-income securities, such as U.S. government debt securities, corporate debt securities, and mortgage-backed

and asset-backed securities. The Fund primarily intends to invest in equity securities or other financial instruments that are components of, or have characteristics similar to, the securities included in the Russell 1000® Index (the “Russell 1000 Index”). The Russell 1000 Index is a capitalization-weighted index from a broad range of industries chosen for

market size, liquidity and industry group representation. The Fund may invest up to 30% of its net assets in securities of foreign issuers, of which 20% (as a percentage of the Fund’s net assets) may be in emerging markets issuers. Investments

in U.S. dollar-denominated securities of foreign issuers, excluding issuers from emerging markets, are permitted beyond the 30% limit. This means that the Fund may invest in such U.S. dollar-denominated securities of foreign issuers without limit.

The Fund may invest in debt securities of any duration or maturity. The Fund will invest primarily in fixed-income securities that are rated investment grade, but may also invest in fixed-income securities rated below investment grade or unrated

securities of equivalent credit quality. The Fund may use derivatives, including options, futures, swaps and forward contracts both to seek to increase the return of the Fund and to hedge (or protect) the value of its assets against adverse

movements in currency exchange rates, interest rates and movements in the securities markets. The Fund may also invest in indexed and inverse securities.

The Fund intends to invest a significant portion of its

fixed-income assets in the Master Total Return Portfolio (the “Total Return Portfolio”) of Master Bond LLC. The primary objective of the Total Return Portfolio is to realize a total return that exceeds that of the Bloomberg Barclays U.S.

Aggregate Bond Index. The Fund intends to invest a significant portion of its equity assets in the Master Advantage Large Cap Core Portfolio (the “Core Portfolio” and together with the Total Return Portfolio, the “Master

Portfolios”) of Master Large Cap Series LLC (“Master Large Cap LLC”). The investment objective of the Core Portfolio is to seek long-term capital growth. In other words, the Core Portfolio tries to choose investments that will

increase in value.

The Total Return Portfolio invests

primarily in a diversified portfolio of fixed-income securities, such as corporate bonds and notes, mortgage-backed and asset-backed securities, convertible securities, preferred securities and government debt obligations. The Core Portfolio

primarily intends to invest in equity securities, which include common stock, preferred stock and convertible securities, or other financial instruments that are components of, or have characteristics similar to, the securities included in the

Russell 1000 Index. The Core Portfolio primarily seeks to buy common stock and may also invest in preferred stock and convertible securities. From time to time, the Core Portfolio may invest in shares of companies through “new issues” or

initial public offerings (“IPOs”).

The Total

Return Portfolio may use derivatives, including, but not limited to, interest rate, total return and credit default swaps, options, futures, and options on futures and swaps, for hedging purposes, as well as to increase the return on its portfolio

investments. The Total Return Portfolio may also invest in credit-linked notes, credit-linked trust certificates, structured notes, or other instruments evidencing interests in special purpose vehicles, trusts, or other entities that hold or

represent interests in fixed-income securities. The Total Return Portfolio may also enter into reverse repurchase agreements and mortgage dollar rolls. The Core Portfolio may use derivatives, including options, futures, swaps (including, but not

limited to, total return swaps, some of which may be referred to as contracts for difference) and forward contracts, both to seek to increase the return of the Core Portfolio and to hedge (or protect) the value of its assets against adverse

movements in currency exchange rates, interest rates and movements in the securities markets. In order to manage cash flows into or out of the Core Portfolio effectively, the Core Portfolio may buy and sell financial futures contracts or options on

such contracts. Derivatives are financial instruments whose value is derived from another security, a currency or an index, including but not limited to the Russell 1000 Index. The use of options, futures, swaps and forward contracts can be

effective in protecting or enhancing the value of the Core Portfolio’s assets.

The investment results of the fixed-income and equity portions

of the Fund’s portfolio will correspond directly to the investment results of (i) the Total Return Portfolio together with those of any fixed-income investments held directly by

3

the Fund and (ii) the Core Portfolio together with those of any equity

investments held directly by the Fund, respectively. For simplicity, this Prospectus uses the term “Fund” to include the underlying Total Return Portfolio and Core Portfolio in which the Fund invests.

The Fund may seek exposure to the investment returns of real

assets that trade in the commodity markets. The Fund may seek this exposure through its investment in the Total Return Portfolio and the Core Portfolio. Each of the Total Return Portfolio and the Core Portfolio may seek to provide exposure to the

investment returns of real assets that trade in the commodity markets through investment in commodity-linked derivative instruments and investment vehicles that exclusively invest in commodities such as precious metals, which are designed to provide

this exposure without direct investment in physical commodities.

Principal Risks of Investing in the Fund

Risk is inherent in all investing. The value of your

investment in the Fund, as well as the amount of return you receive on your investment, may fluctuate significantly from day to day and over time. You may lose part or all of your investment in the Fund or your investment may not perform as well as

other similar investments. The following is a summary description of principal risks of investing in the Fund and/or the Master Portfolios. References to the Fund in the description of risks below may include the Master Portfolios in which the Fund

invests, as applicable. The order of the below risk factors does not indicate the significance of any particular risk factor.

| ■ | Commodities Related Investments Risk — Exposure to the commodities markets may subject the Fund to greater volatility than investments in traditional securities. The value of commodity-linked derivative investments may be affected by changes in overall market movements, commodity index volatility, changes in interest rates, or factors affecting a particular industry or commodity, such as drought, floods, weather, embargoes, tariffs and international economic, political and regulatory developments. |

| ■ | Convertible Securities Risk — The market value of a convertible security performs like that of a regular debt security; that is, if market interest rates rise, the value of a convertible security usually falls. In addition, convertible securities are subject to the risk that the issuer will not be able to pay interest or dividends when due, and their market value may change based on changes in the issuer’s credit rating or the market’s perception of the issuer’s creditworthiness. Since it derives a portion of its value from the common stock into which it may be converted, a convertible security is also subject to the same types of market and issuer risks that apply to the underlying common stock. |

| ■ | Corporate Loans Risk — Commercial banks and other financial institutions or institutional investors make corporate loans to companies that need capital to grow or restructure. Borrowers generally pay interest on corporate loans at rates that change in response to changes in market interest rates such as the London Interbank Offered Rate (“LIBOR”) or the prime rates of U.S. banks. As a result, the value of corporate loan investments is generally less exposed to the adverse effects of shifts in market interest rates than investments that pay a fixed rate of interest. The market for corporate loans may be subject to irregular trading activity and wide bid/ask spreads. In addition, transactions in corporate loans may settle on a delayed basis. As a result, the proceeds from the sale of corporate loans may not be readily available to make additional investments or to meet the Fund’s redemption obligations. To the extent the extended settlement process gives rise to short-term liquidity needs, the Fund may hold additional cash, sell investments or temporarily borrow from banks and other lenders. |

| ■ | Debt Securities Risk — Debt securities, such as bonds, involve interest rate risk, credit risk, extension risk, and prepayment risk, among other things. |

| Interest Rate Risk — The market value of bonds and other fixed-income securities changes in response to interest rate changes and other factors. Interest rate risk is the risk that prices of bonds and other fixed-income securities will increase as interest rates fall and decrease as interest rates rise. | |

| The Fund may be subject to a greater risk of rising interest rates due to the current period of historically low rates. For example, if interest rates increase by 1%, assuming a current portfolio duration of ten years, and all other factors being equal, the value of the Fund’s investments would be expected to decrease by 10%. The magnitude of these fluctuations in the market price of bonds and other fixed-income securities is generally greater for those securities with longer maturities. Fluctuations in the market price of the Fund’s investments will not affect interest income derived from instruments already owned by the Fund, but will be reflected in the Fund’s net asset value. The Fund may lose money if short-term or long-term interest rates rise sharply in a manner not anticipated by Fund management. | |

| To the extent the Fund invests in debt securities that may be prepaid at the option of the obligor (such as mortgage-backed securities), the sensitivity of such securities to changes in interest rates may increase (to the detriment of the Fund) when interest rates rise. Moreover, because rates on certain floating rate debt securities typically reset |

4

| only periodically, changes in prevailing interest rates (and particularly sudden and significant changes) can be expected to cause some fluctuations in the net asset value of the Fund to the extent that it invests in floating rate debt securities. | |

| These basic principles of bond prices also apply to U.S. Government securities. A security backed by the “full faith and credit” of the U.S. Government is guaranteed only as to its stated interest rate and face value at maturity, not its current market price. Just like other fixed-income securities, government-guaranteed securities will fluctuate in value when interest rates change. | |

| A general rise in interest rates has the potential to cause investors to move out of fixed-income securities on a large scale, which may increase redemptions from funds that hold large amounts of fixed-income securities. Heavy redemptions could cause the Fund to sell assets at inopportune times or at a loss or depressed value and could hurt the Fund’s performance. | |

| Credit Risk — Credit risk refers to the possibility that the issuer of a debt security (i.e., the borrower) will not be able to make payments of interest and principal when due. Changes in an issuer’s credit rating or the market’s perception of an issuer’s creditworthiness may also affect the value of the Fund’s investment in that issuer. The degree of credit risk depends on both the financial condition of the issuer and the terms of the obligation. | |

| Extension Risk — When interest rates rise, certain obligations will be paid off by the obligor more slowly than anticipated, causing the value of these obligations to fall. | |

| Prepayment Risk — When interest rates fall, certain obligations will be paid off by the obligor more quickly than originally anticipated, and the Fund may have to invest the proceeds in securities with lower yields. | |

| ■ | Derivatives Risk — The Fund’s use of derivatives may increase its costs, reduce the Fund’s returns and/or increase volatility. Derivatives involve significant risks, including: |

| Volatility Risk — Volatility is defined as the characteristic of a security, an index or a market to fluctuate significantly in price within a short time period. A risk of the Fund’s use of derivatives is that the fluctuations in their values may not correlate with the overall securities markets. | |

| Counterparty Risk — Derivatives are also subject to counterparty risk, which is the risk that the other party in the transaction will not fulfill its contractual obligation. | |

| Market and Illiquidity Risk — The possible lack of a liquid secondary market for derivatives and the resulting inability of the Fund to sell or otherwise close a derivatives position could expose the Fund to losses and could make derivatives more difficult for the Fund to value accurately. | |

| Valuation Risk — Valuation may be more difficult in times of market turmoil since many investors and market makers may be reluctant to purchase complex instruments or quote prices for them. | |

| Hedging Risk — Hedges are sometimes subject to imperfect matching between the derivative and the underlying security, and there can be no assurance that the Fund’s hedging transactions will be effective. The use of hedging may result in certain adverse tax consequences. | |

| Tax Risk — Certain aspects of the tax treatment of derivative instruments, including swap agreements and commodity-linked derivative instruments, are currently unclear and may be affected by changes in legislation, regulations or other legally binding authority. Such treatment may be less favorable than that given to a direct investment in an underlying asset and may adversely affect the timing, character and amount of income the Fund realizes from its investments. | |

| Regulatory Risk — Derivative contracts, including, without limitation, swaps, currency forwards and non-deliverable forwards, are subject to regulation under the Dodd-Frank Wall Street Reform and Consumer Protection Act (the “Dodd-Frank Act”) in the United States and under comparable regimes in Europe, Asia and other non-U.S. jurisdictions. Under the Dodd-Frank Act, certain derivatives are subject to margin requirements and swap dealers are required to collect margin from the Fund with respect to such derivatives. Specifically, regulations are now in effect that require swap dealers to post and collect variation margin (comprised of specified liquid instruments and subject to a required haircut) in connection with trading of over-the-counter (“OTC”) swaps with the Fund. Shares of investment companies (other than certain money market funds) may not be posted as collateral under these regulations. Requirements for posting of initial margin in connection with OTC swaps will be phased-in through at least 2021. In addition, regulations adopted by global prudential regulators that are now in effect require certain bank-regulated counterparties and certain of their affiliates to include in certain financial contracts, including many derivatives contracts, terms that delay or restrict the rights of counterparties, such as the Fund, to terminate such contracts, foreclose upon collateral, exercise other default rights or restrict transfers of credit support in the event that the counterparty and/or its affiliates are subject to certain types of resolution or insolvency proceedings. The implementation of these requirements with respect to derivatives, as well as regulations under the Dodd-Frank Act regarding clearing, mandatory trading and margining of other derivatives, may increase the costs and risks to the |

5

| Fund of trading in these

instruments and, as a result, may affect returns to investors in the Fund. | |

| On October 28, 2020, the Securities and Exchange Commission adopted new regulations governing the use of derivatives by registered investment companies (“Rule 18f-4”). The Fund will be required to implement and comply with Rule 18f-4 by August 19, 2022. Once implemented, Rule 18f-4 will impose limits on the amount of derivatives a fund can enter into, eliminate the asset segregation framework currently used by funds to comply with Section 18 of the Investment Company Act of 1940, as amended, treat derivatives as senior securities so that a failure to comply with the limits would result in a statutory violation and require funds whose use of derivatives is more than a limited specified exposure amount to establish and maintain a comprehensive derivatives risk management program and appoint a derivatives risk manager. | |

| ■ | Emerging Markets Risk — Emerging markets are riskier than more developed markets because they tend to develop unevenly and may never fully develop. Investments in emerging markets may be considered speculative. Emerging markets are more likely to experience hyperinflation and currency devaluations, which adversely affect returns to U.S. investors. In addition, many emerging securities markets have far lower trading volumes and less liquidity than developed markets. |

| ■ | Equity Securities Risk — Stock markets are volatile. The price of equity securities fluctuates based on changes in a company’s financial condition and overall market and economic conditions. |

| ■ | Foreign Securities Risk — Foreign investments often involve special risks not present in U.S. investments that can increase the chances that the Fund will lose money. These risks include: |

| ■ | The Fund generally holds its foreign securities and cash in foreign banks and securities depositories, which may be recently organized or new to the foreign custody business and may be subject to only limited or no regulatory oversight. |

| ■ | Changes in foreign currency exchange rates can affect the value of the Fund’s portfolio. |

| ■ | The economies of certain foreign markets may not compare favorably with the economy of the United States with respect to such issues as growth of gross national product, reinvestment of capital, resources and balance of payments position. |

| ■ | The governments of certain countries may prohibit or impose substantial restrictions on foreign investments in their capital markets or in certain industries. |

| ■ | Many foreign governments do not supervise and regulate stock exchanges, brokers and the sale of securities to the same extent as does the United States and may not have laws to protect investors that are comparable to U.S. securities laws. |

| ■ | Settlement and clearance procedures in certain foreign markets may result in delays in payment for or delivery of securities not typically associated with settlement and clearance of U.S. investments. |

| ■ | The Fund’s claims to recover foreign withholding taxes may not be successful, and if the likelihood of recovery of foreign withholding taxes materially decreases, due to, for example, a change in tax regulation or approach in the foreign country, accruals in the Fund’s net asset value for such refunds may be written down partially or in full, which will adversely affect the Fund’s net asset value. |

| ■ | The European financial markets have recently experienced volatility and adverse trends due to concerns about economic downturns in, or rising government debt levels of, several European countries. These events may spread to other countries in Europe. These events may affect the value and liquidity of certain of the Fund’s investments. |

| ■ | High Portfolio Turnover Risk — The Fund may engage in active and frequent trading of its portfolio securities. High portfolio turnover (more than 100%) may result in increased transaction costs to the Fund, including brokerage commissions, dealer mark-ups and other transaction costs on the sale of the securities and on reinvestment in other securities. The sale of Fund portfolio securities may result in the realization and/or distribution to shareholders of higher capital gains or losses as compared to a fund with less active trading policies. These effects of higher than normal portfolio turnover may adversely affect Fund performance. In addition, investment in mortgage dollar rolls and participation in to-be-announced (“TBA”) transactions may significantly increase the Fund’s portfolio turnover rate. A TBA transaction is a method of trading mortgage-backed securities where the buyer and seller agree upon general trade parameters such as agency, settlement date, par amount, and price at the time the contract is entered into but the mortgage-backed securities are delivered in the future, generally 30 days later. |

| ■ | Indexed and Inverse Securities Risk — Indexed and inverse securities provide a potential return based on a particular index of value or interest rates. The Fund’s return on these securities will be subject to risk with respect to the value of the particular index. These securities are subject to leverage risk and correlation risk. Certain indexed and inverse securities have greater sensitivity to changes in interest rates or index levels than other |

6

| securities, and the Fund’s investment in such instruments may decline significantly in value if interest rates or index levels move in a way Fund management does not anticipate. | |

| ■ | Investment Style Risk — Under certain market conditions, growth investments have performed better during the later stages of economic expansion and value investments have performed better during periods of economic recovery. Therefore, these investment styles may over time go in and out of favor. At times when the investment style used by the Fund is out of favor, the Fund may underperform other funds that use different investment styles. |

| ■ | Junk Bonds Risk — Although junk bonds generally pay higher rates of interest than investment grade bonds, junk bonds are high risk investments that are considered speculative and may cause income and principal losses for the Fund. |

| ■ | Leverage Risk — Some transactions may give rise to a form of economic leverage. These transactions may include, among others, derivatives, and may expose the Fund to greater risk and increase its costs. The use of leverage may cause the Fund to liquidate portfolio positions when it may not be advantageous to do so to satisfy its obligations or to meet any required asset segregation requirements. Increases and decreases in the value of the Fund’s portfolio will be magnified when the Fund uses leverage. |

| ■ | Market Risk and Selection Risk — Market risk is the risk that one or more markets in which the Fund invests will go down in value, including the possibility that the markets will go down sharply and unpredictably. The value of a security or other asset may decline due to changes in general market conditions, economic trends or events that are not specifically related to the issuer of the security or other asset, or factors that affect a particular issuer or issuers, exchange, country, group of countries, region, market, industry, group of industries, sector or asset class. Local, regional or global events such as war, acts of terrorism, the spread of infectious illness or other public health issues like pandemics or epidemics, recessions, or other events could have a significant impact on the Fund and its investments. Selection risk is the risk that the securities selected by Fund management will underperform the markets, the relevant indices or the securities selected by other funds with similar investment objectives and investment strategies. The Fund seeks to pursue its investment objective by using proprietary models that incorporate quantitative analysis and is subject to “Model Risk” as described in the “Details About the Fund” section of the Fund’s prospectus. This means you may lose money. |

| A recent outbreak of an infectious coronavirus has developed into a global pandemic that has resulted in numerous disruptions in the market and has had significant economic impact leaving general concern and uncertainty. The impact of this coronavirus, and other epidemics and pandemics that may arise in the future, could affect the economies of many nations, individual companies and the market in general ways that cannot necessarily be foreseen at the present time. | |

| ■ | Mid Cap Securities Risk — The securities of mid cap companies generally trade in lower volumes and are generally subject to greater and less predictable price changes than the securities of larger capitalization companies. |

| ■ | Money Market Securities Risk — If market conditions improve while the Fund has invested some or all of its assets in high quality money market securities, this strategy could result in reducing the potential gain from the market upswing, thus reducing the Fund’s opportunity to achieve its investment objective. |

| ■ | Mortgage- and Asset-Backed Securities Risks — Mortgage- and asset-backed securities represent interests in “pools” of mortgages or other assets, including consumer loans or receivables held in trust. Mortgage- and asset-backed securities are subject to credit, interest rate, prepayment and extension risks. These securities also are subject to risk of default on the underlying mortgage or asset, particularly during periods of economic downturn. Small movements in interest rates (both increases and decreases) may quickly and significantly reduce the value of certain mortgage-backed securities. |

| ■ | “New Issues” Risk — “New issues” are IPOs of equity securities. Securities issued in IPOs have no trading history, and information about the companies may be available for very limited periods. In addition, the prices of securities sold in IPOs may be highly volatile or may decline shortly after the initial public offering. |

| ■ | Preferred Securities Risk — Preferred securities may pay fixed or adjustable rates of return. Preferred securities are subject to issuer-specific and market risks applicable generally to equity securities. In addition, a company’s preferred securities generally pay dividends only after the company makes required payments to holders of its bonds and other debt. For this reason, the value of preferred securities will usually react more strongly than bonds and other debt to actual or perceived changes in the company’s financial condition or prospects. Preferred securities of smaller companies may be more vulnerable to adverse developments than preferred securities of larger companies. |

| ■ | Reverse Repurchase Agreements Risk — Reverse repurchase agreements involve the sale of securities held by the Fund with an agreement to repurchase the securities at an agreed-upon price, date and interest payment. Reverse repurchase agreements involve the risk that the other party may fail to return the securities in a timely manner or at all. The Fund could lose money if it is unable to recover the securities and the value of the collateral held by the |

7

| Fund, including the value of the investments made with cash collateral, is less than the value of the securities. These events could also trigger adverse tax consequences for the Fund. In addition, reverse repurchase agreements involve the risk that the interest income earned in the investment of the proceeds will be less than the interest expense. | |

| ■ | Sovereign Debt Risk — Sovereign debt instruments are subject to the risk that a governmental entity may delay or refuse to pay interest or repay principal on its sovereign debt, due, for example, to cash flow problems, insufficient foreign currency reserves, political considerations, the relative size of the governmental entity’s debt position in relation to the economy or the failure to put in place economic reforms required by the International Monetary Fund or other multilateral agencies. |

| ■ | Structured Notes Risk — Structured notes and other related instruments purchased by the Fund are generally privately negotiated debt obligations where the principal and/or interest is determined by reference to the performance of a specific asset, benchmark asset, market or interest rate (“reference measure”). The purchase of structured notes exposes the Fund to the credit risk of the issuer of the structured product. Structured notes may be leveraged, increasing the volatility of each structured note’s value relative to the change in the reference measure. Structured notes may also be less liquid and more difficult to price accurately than less complex securities and instruments or more traditional debt securities. |

| ■ | U.S. Government Issuer Risk — Treasury obligations may differ in their interest rates, maturities, times of issuance and other characteristics. Obligations of U.S. Government agencies and authorities are supported by varying degrees of credit but generally are not backed by the full faith and credit of the U.S. Government. No assurance can be given that the U.S. Government will provide financial support to its agencies and authorities if it is not obligated by law to do so. |

Performance Information

The information shows you how the Fund’s performance has

varied year by year and provides some indication of the risks of investing in the Fund. Class K Shares commenced operations on January 25, 2018. As a result, the returns shown below for Class K Shares prior to January 25, 2018 are those of the

Fund’s Institutional Shares, which are not offered in this prospectus. The performance of Class K Shares would be substantially similar to Institutional Shares because Class K Shares and Institutional Shares are invested in the same portfolio

of securities and performance would differ only to the extent that Institutional Shares and Class K Shares have different expenses. The actual returns of Class K Shares would have been higher than those of Institutional Shares because Class K Shares

have lower expenses than Institutional Shares. The table compares the Fund’s performance to that of the Russell 1000® Index, the Bloomberg

Barclays U.S. Aggregate Bond Index and a customized weighted index comprised of the returns of the Russell 1000® Index (60%) and the Bloomberg

Barclays U.S. Aggregate Bond Index (40%), which are relevant to the Fund because they have characteristics similar to the Fund’s investment strategies. To the extent that dividends and distributions have been paid by the Fund, the performance

information for the Fund in the chart and table assumes reinvestment of the dividends and distributions. As with all such investments, past performance (before and after taxes) is not an indication of future results. The table includes all

applicable fees. If the Fund’s investment manager and its affiliates had not waived or reimbursed certain Fund expenses during these periods, the Fund’s returns would have been lower. Updated information on the Fund’s performance,

including its current net asset value, can be obtained by visiting http://www.blackrock.com or can be obtained by phone at (800) 882-0052.

8

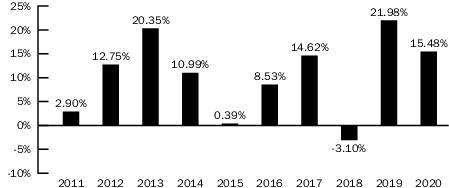

Class K Shares

ANNUAL TOTAL RETURNS

BlackRock Balanced Capital Fund, Inc.

As of 12/31

As of 12/31

During the ten-year

period shown in the bar chart, the highest return for a quarter was 15.52% (quarter ended June 30, 2020) and the lowest return for a quarter was -12.99% (quarter ended March 31, 2020).

| As

of 12/31/20 Average Annual Total Returns |

1 Year | 5 Years | 10 Years |

| BlackRock Balanced Capital Fund — Class K Shares | |||

| Return Before Taxes | 15.48% | 11.17% | 10.20% |

| Return After Taxes on Distributions | 13.94% | 8.71% | 7.87% |

| Return After Taxes on Distributions and Sale of Fund Shares | 9.62% | 8.10% | 7.49% |

| Russell

1000® Index (Reflects no deduction for fees, expenses or taxes) |

20.96% | 15.60% | 14.01% |

| Bloomberg

Barclays U.S. Aggregate Bond Index (Reflects no deduction for fees, expenses or taxes) |

7.51% | 4.44% | 3.84% |

| 60%

Russell 1000® Index/40% Bloomberg Barclays U.S. Aggregate Bond Index (Reflects no deduction for fees, expenses or taxes) |

16.29% | 11.35% | 10.11% |

After-tax returns are calculated using the historical highest

individual federal marginal income tax rates and do not reflect the impact of state and local taxes. Actual after-tax returns depend on the investor’s tax situation and may differ from those shown, and the after-tax returns shown are not

relevant to investors who hold their shares through tax-deferred arrangements, such as 401(k) plans or individual retirement accounts.

Investment Manager

The Fund’s investment manager is BlackRock Advisors, LLC

(previously defined as “BlackRock”).

Portfolio Managers

The asset allocation of the equity and fixed-income portions

of the Fund’s portfolio is managed by Philip Green.

| Name | Portfolio

Manager of the Fund Since |

Title |

| Philip Green | 2006 | Managing Director of BlackRock, Inc. |

The Total Return Portfolio in which the Fund invests a

portion of its assets is managed by a team of investment professionals comprised of Rick Rieder, Bob Miller and David Rogal.

9

| Name | Portfolio

Manager of the Total Return Portfolio Since |

Title |

| Rick Rieder | 2010 | Managing

Director of BlackRock, Inc., BlackRock’s Chief Investment Officer of Global Fixed Income, Head of the Fundamental Fixed Income business, Head of the Global Allocation Investment Team, member of BlackRock’s Executive Sub-Committee on Investments, member of BlackRock’s Global Operating Committee, and Chairman of the firm-wide BlackRock Investment Council. |

| Bob Miller | 2011 | Managing Director of BlackRock, Inc. |

| David Rogal | 2017 | Managing Director of BlackRock, Inc. |

The Core Portfolio in which the Fund invests a portion of its

assets is managed by Raffaele Savi, Travis Cooke, CFA, and Richard Mathieson.

| Name | Portfolio

Manager of the Core Portfolio Since |

Title |

| Raffaele Savi | 2017 | Managing Director of BlackRock, Inc. |

| Travis Cooke, CFA | 2017 | Managing Director of BlackRock, Inc. |

| Richard Mathieson | 2017 | Managing Director of BlackRock, Inc. |

Purchase and Sale of Fund Shares

Class K Shares of the Fund are available only to (i) certain

employee benefit plans, such as health savings accounts, and certain employer-sponsored retirement plans (not including SEP IRAs, SIMPLE IRAs and SARSEPs) (collectively, “Employer-Sponsored Retirement Plans”), (ii) collective trust

funds, investment companies and other pooled investment vehicles, each of which may purchase shares of the Fund through a Financial Intermediary that has entered into an agreement with the Fund’s distributor to purchase such shares, (iii)

“Institutional Investors,” which include, but are not limited to, endowments, foundations, family offices, banks and bank trusts, local, city, and state governmental institutions, corporations and insurance company separate accounts,

each of which may purchase shares of the Fund through a Financial Intermediary that has entered into an agreement with the Fund’s distributor to purchase such shares, (iv) clients of private banks that purchase shares of the Fund through a

Financial Intermediary that has entered into an agreement with the Fund’s distributor to sell such shares, (v) fee-based advisory platforms of a Financial Intermediary that (a) has specifically acknowledged in a written agreement with the

Fund’s distributor and/or its affiliate(s) that the Financial Intermediary shall offer such shares to fee-based advisory clients through an omnibus account held at the Fund or (b) transacts in the Fund’s shares through another

intermediary that has executed such an agreement and (vi) any other investors who met the eligibility criteria for BlackRock Shares or Class K Shares prior to August 15, 2016 and have continually held Class K Shares of the Fund in the same account

since August 15, 2016.

You may purchase or redeem shares

of the Fund each day the New York Stock Exchange is open. Purchase orders may also be placed by calling (800) 537-4942, by mail (c/o BlackRock, P.O. Box 9819, Providence, Rhode Island 02940-8019), or online at www.blackrock.com. Institutional

Investors are subject to a $5 million minimum initial investment requirement. Other investors, including Employer-Sponsored Retirement Plans, have no minimum initial investment requirement. There is no minimum investment amount for additional

purchases.

Tax Information

Different income tax rules apply depending on whether you are

invested through a qualified tax-exempt plan described in section 401(a) of the Internal Revenue Code of 1986, as amended. If you are invested through such a plan (and Fund shares are not “debt-financed property” to the plan), then the

dividends paid by the Fund and the gain realized from a redemption or exchange of Fund shares will generally not be subject to U.S. federal income taxes until you withdraw or receive distributions from the plan. If you are not invested through such

a plan, then the Fund’s dividends and gain from a redemption or exchange may be subject to U.S. federal income taxes and may be taxed as ordinary income or capital gains, unless you are a tax-exempt investor.

10

Payments to Broker/Dealers and Other Financial

Intermediaries

If you purchase shares of the Fund through a Financial

Intermediary,, the Fund and BlackRock Investments, LLC, the Fund’s distributor, or its affiliates may pay the Financial Intermediary for the sale of Fund shares and related services. These payments may create a conflict of interest by

influencing the Financial Intermediary and your individual financial professional to recommend the Fund over another investment.

Class K Shares are only available through a Financial

Intermediary if the Financial Intermediary will not receive from Fund assets, or the Fund’s distributor’s or an affiliate’s resources, any commission payments, shareholder servicing fees (including sub-transfer agent and networking

fees), or distribution fees (including Rule 12b-1 fees) with respect to assets invested in Class K Shares.

Ask your individual financial professional or visit your

Financial Intermediary’s website for more information.

11

INVESTMENT COMPANY ACT FILE # 811-02405

SPRO-BC-K-0121