UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-02405, 811-09739 and 811-21434

Name of Fund: BlackRock Balanced Capital Fund, Inc., Master Advantage Large Cap Core Portfolio of Master Large

Cap Series LLC and Master Total Return Portfolio of Master Bond LLC

Fund Address: 100 Bellevue Parkway, Wilmington, DE 19809

Name and address of agent for service: John M. Perlowski, Chief Executive Officer, BlackRock Balanced Capital

Fund, Inc., Master Advantage Large Cap Core Portfolio of Master Large Cap Series LLC and Master Total Return Portfolio of Master Bond LLC, 55 East 52nd Street, New York, NY 10055

Registrants’ telephone number, including area code: (800) 441-7762

Date of fiscal year end: 09/30/2018

Date of reporting period: 09/30/2018

Item 1 – Report to Stockholders

SEPTEMBER 30, 2018

| ANNUAL REPORT |

|

BlackRock Balanced Capital Fund, Inc.

| Not FDIC Insured § May Lose Value § No Bank Guarantee |

| 2 | T H I S P A G E I S N O T P A R T O F Y O U R F U N D R E P O R T |

| Page | ||||

| 2 | ||||

| Annual Report: |

||||

| 4 | ||||

| 7 | ||||

| 7 | ||||

| 8 | ||||

| 8 | ||||

| Fund Financial Statements: |

||||

| 9 | ||||

| 12 | ||||

| 13 | ||||

| 14 | ||||

| 15 | ||||

| 20 | ||||

| 28 | ||||

| 28 | ||||

| 29 | ||||

| Master Advantage Large Cap Core Portfolio Financial Statements: |

||||

| 30 | ||||

| 35 | ||||

| 36 | ||||

| 37 | ||||

| Master Advantage Large Cap Core Portfolio Financial Highlights |

38 | |||

| Master Advantage Large Cap Core Portfolio Notes to Financial Statements |

39 | |||

| Master Advantage Large Cap Core Portfolio Report of Independent Registered Public Accounting Firm |

45 | |||

| Director and Officer Information of Master Large Cap Series LLC |

46 | |||

| 49 | ||||

| Master Total Return Portfolio Consolidated Financial Statements: |

||||

| 50 | ||||

| 125 | ||||

| 126 | ||||

| 127 | ||||

| Master Total Return Portfolio Consolidated Financial Highlights |

128 | |||

| Master Total Return Portfolio Notes to Consolidated Financial Statements |

129 | |||

| Master Total Return Portfolio Report of Independent Registered Public Accounting Firm |

143 | |||

| 144 | ||||

| Director and Officer Information of the Fund and Master Total Return Portfolio |

147 | |||

| 150 | ||||

| 152 | ||||

| 3 |

| Fund Summary as of September 30, 2018 | BlackRock Balanced Capital Fund, Inc. |

Investment Objective

BlackRock Balanced Capital Fund, Inc.’s (the “Fund”) investment objective is to seek the highest total investment return through a fully managed investment policy utilizing equity, debt (including money market) and convertible securities.

Portfolio Management Commentary

How did the Fund perform?

For the 12-month period ended September 30, 2018, through its investments in Master Advantage Large Cap Core Portfolio of Master Large Cap Series LLC (the “equity allocation” or the “Master Advantage Large Cap Core Portfolio”) and Master Total Return Portfolio of Master Bond LLC (the “fixed income allocation” or the “Master Total Return Portfolio”) (collectively, the “Master Portfolios”), the Fund’s Institutional and Class K Shares outperformed the blended reference benchmark (60% Russell 1000® Index/40% Bloomberg Barclays U.S. Aggregate Bond Index) while Investor A Shares performed in line with the benchmark and Investor C and Class R Shares underperformed. For the same period, the Fund outperformed the fixed income portion of the benchmark, the Bloomberg Barclays U.S. Aggregate Bond Index, and underperformed the equity portion of the benchmark, the Russell 1000® Index.

What factors influenced performance?

The Fund combines top down macroeconomic views and bottom up security selection from the Master Advantage Large Cap Core Portfolio and Master Total Return Portfolio.

Tactical asset allocation supported Fund returns, with a cautious stance on U.S. bonds a notable driver of performance as bond yields moved higher over the period. A tilt toward Japanese equities also contributed to returns as Japanese equities outperformed, boosted by yen weakness. Within the equity allocation, the stock selection model had an overall positive impact on performance. Early in the period, stock selection insights capturing trends and sentiment across market participants were additive. Later in the period, insights that evaluate cash flow and asset efficiency contributed to results. Further, a signal that evaluates stocks based on key corporate events such as initial public offerings, CEO changes and revisions to forward guidance was a top performer. Within the fixed income allocation, exposure to non-agency mortgage-backed securities (“MBS”) and collateralized loan obligations, an overweight to municipal bonds, security selection within commercial mortgage-backed securities, and an allocation to high yield corporate bonds contributed positively to performance.

From a broad asset allocation perspective, a cautious stance on domestic stocks detracted from performance as U.S. equities advanced amid positive earnings momentum and supportive economic data. Within the equity allocation, some stock-specific events adversely affected performance during the period. Notably, an underweight position in Netflix Inc. detracted from performance after the company had a series of strong earnings reports. Elsewhere, several stock selection signals struggled. In particular, signals that seek to capture trends across consumer activity, such as foot traffic in brick and mortar retail locations, weighed on results. Additionally, an insight that uses online hiring activity as a measure of growth detracted. Traditional measures used to identify growth companies at attractive valuations also continued to struggle. In the fixed income allocation, positioning with respect to duration (and corresponding sensitivity to interest rate changes) detracted, as did positioning with respect to emerging market and investment grade credit. U.S. absolute return strategies and security selection within agency MBS also detracted from performance for the period.

Describe recent portfolio activity.

From a broad asset allocation perspective, the Fund favored stocks over bonds, while using the rise in bond yields at the turn of 2018 to reduce the magnitude of this overweight. Within equities, the Fund increased its conviction with respect to a relative value preference for international vs. U.S. stocks given expectations that the Fed would continue to withdraw stimulus more quickly than other economies. In the first and second quarters of 2018, the Fund held an overweight position in European equities, and brought this position down as prices moved higher on renewed dovishness from the European Central Bank. The Fund also reduced the magnitude of its underweight position in U.S. bonds, although it remained underweight. The Fund also ended the period with an overweight position in both the Australian dollar and the euro versus the U.S. dollar, given a view that Australian and European monetary policy would shift to become more hawkish, which should support both currencies. The Fund retained a preference for Japanese equities versus U.S. equities over the period.

The Master Advantage Large Cap Core Portfolio maintained a balanced allocation of risk across all major return drivers. However, there were a number of new stock selection insights that were added to the portfolio. These included a sentiment insight that captures longer-term trends in fundamentals based on text analysis of company executive conference calls and a signal that identifies stock price reversals based on recent performance. In addition, a stock selection model that evaluates companies on the basis of governance as well as the sustainability of their business practices from a social and environmental perspective was added during the period.

Within Master Total Return Portfolio, an underweight duration profile was maintained in the early part of the period and reduced during the first quarter of 2018. The portfolio was positioned with a focus on generating income through allocations to securitized assets, emerging market bonds and select corporate bonds. The spike in market volatility during the second half of the period led the portfolio to reduce risk in the corporate credit sector, while looking for more carry-oriented opportunities in higher quality assets within shorter-term Treasuries, securitized assets and select emerging markets. Toward the end of the period, the portfolio moved to an overweight duration position as the rise in interest rates provided an attractive entry point.

Describe portfolio positioning at period end.

The Fund maintained a preference for international developed stocks relative to domestic stocks at period end. In particular, the Fund held a tilt toward Japanese equities versus U.S. equities given a view that Japanese growth has been underappreciated by markets and that further tightening by the Fed would act as a headwind to U.S. equities. The Fund also held an underweight to U.S. bonds given an expectation for further global monetary policy tightening.

The views expressed reflect the opinions of BlackRock as of the date of this report and are subject to change based on changes in market, economic or other conditions. These views are not intended to be a forecast of future events and are no guarantee of future results.

| 4 | 2 0 1 8 B L A C K R O C K A N N U A L R E P O R T T O S H A R E H O L D E R S |

| Fund Summary as of September 30, 2018 (continued) | BlackRock Balanced Capital Fund, Inc. |

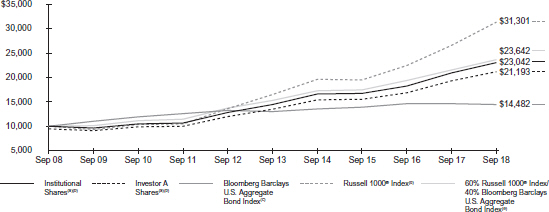

TOTAL RETURN BASED ON A $10,000 INVESTMENT

| (a) | Assuming maximum sales charges, if any, transaction costs and other operating expenses, including investment advisory and administration fees. Institutional Shares do not have a sales charge. |

| (b) | The Fund invests in equity securities (including common stock, preferred stock, securities convertible into common stock, or securities or other instruments whose price is linked to the value of common stock) and fixed-income securities (including debt securities, convertible securities and short term securities). |

| (c) | A widely recognized unmanaged market-weighted index, comprised of investment-grade corporate bonds rated BBB or better, mortgages and U.S. Treasury and U.S. Government agency issues with at least one year to maturity. |

| (d) | An index that measures the performance of the large cap segment of the U.S. equity universe. It is a subset of the Russell 3000® Index and includes approximately 1,000 of the largest securities based on a combination of their market capitalization and current index membership. The index represents approximately 92% of the total market capitalization of the Russell 3000® Index. |

| (e) | A customized weighted index comprised of the returns of the Russell 1000® Index (60%) and Bloomberg Barclays U.S. Aggregate Bond Index (40%). |

Performance Summary for the Period Ended September 30, 2018

| Average Annual Total Returns(a)(b) | |||||||||||||||||||||||||||||||||||

| 1 Year | 5 Years | 10 Years | |||||||||||||||||||||||||||||||||

| 6-Month Total Returns |

w/o sales charge |

w/ sales charge |

w/o sales charge |

w/ sales charge |

w/o sales charge |

w/ sales charge | |||||||||||||||||||||||||||||

| Institutional |

6.15 | % | 10.14 | % | N/A | 9.78 | % | N/A | 8.71 | % | N/A | ||||||||||||||||||||||||

| Investor A |

5.98 | 9.86 | 4.09 | % | 9.46 | 8.29 | % | 8.38 | 7.80 | % | |||||||||||||||||||||||||

| Investor C |

5.58 | 9.03 | 8.13 | 8.63 | 8.63 | 7.54 | 7.54 | ||||||||||||||||||||||||||||

| Class K |

6.19 | 10.18 | N/A | 9.79 | N/A | 8.71 | N/A | ||||||||||||||||||||||||||||

| Class R |

5.83 | 9.51 | N/A | 9.09 | N/A | 7.97 | N/A | ||||||||||||||||||||||||||||

| 60% Russell 1000® Index/40% Bloomberg Barclays U.S. Aggregate Bond Index |

6.58 | 9.90 | N/A | 9.06 | N/A | 8.99 | N/A | ||||||||||||||||||||||||||||

| Bloomberg Barclays U.S. Aggregate Bond Index |

(0.14 | ) | (1.22 | ) | N/A | 2.16 | N/A | 3.77 | N/A | ||||||||||||||||||||||||||

| Russell 1000® Index |

11.25 | 17.76 | N/A | 13.67 | N/A | 12.09 | N/A | ||||||||||||||||||||||||||||

| (a) | Assuming maximum sales charges, if any. Average annual total returns with and without sales charges reflect reductions for distribution and service fees. See “About Fund Performance” on page 8 for a detailed description of share classes, including any related sales charges and fees, and how performance was calculated for certain share classes. |

| (b) | The Fund invests in equity securities (including common stock, preferred stock, securities convertible into common stock, or securities or other instruments whose price is linked to the value of common stock) and fixed-income securities (including debt securities, convertible securities and short term securities). |

N/A — Not applicable as share class and index do not have a sales charge.

Past performance is not indicative of future results.

Performance results may include adjustments made for financial reporting purposes in accordance with U.S. generally accepted accounting principles.

Expense Example

| Actual | Hypothetical(b) | ||||||||||||||||||||||||||||||||||

| Beginning Account Value (04/01/18) |

Ending Account Value (09/30/18) |

Expenses Paid During the Period(a) |

Beginning Account Value (04/01/18) |

Ending Account Value (09/30/18) |

Expenses Paid During the Period(a) |

Annualized Expense Ratio | |||||||||||||||||||||||||||||

| Institutional |

$ | 1,000.00 | $ | 1,061.50 | $ | 2.95 | $ | 1,000.00 | $ | 1,022.07 | $ | 2.90 | 0.57 | % | |||||||||||||||||||||

| Investor A |

1,000.00 | 1,059.80 | 4.38 | 1,000.00 | 1,020.68 | 4.29 | 0.85 | ||||||||||||||||||||||||||||

| Investor C |

1,000.00 | 1,055.80 | 8.22 | 1,000.00 | 1,016.93 | 8.06 | 1.60 | ||||||||||||||||||||||||||||

| Class K |

1,000.00 | 1,061.90 | 2.65 | 1,000.00 | 1,022.36 | 2.60 | 0.52 | ||||||||||||||||||||||||||||

| Class R |

1,000.00 | 1,058.30 | 6.17 | 1,000.00 | 1,018.94 | 6.05 | 1.20 | ||||||||||||||||||||||||||||

| (a) | For each class of the Fund, expenses are equal to the annualized expense ratio for the class, multiplied by the average account value over the period, multiplied by 183/365 (to reflect the one-half year period shown). Because the Fund invests significantly in the Master Portfolios, the expense example reflects the net expenses of both the Fund and the Master Portfolios in which it invests. |

| (b) | Hypothetical 5% annual return before expenses is calculated by prorating the number of days in the most recent fiscal half year divided by 365. |

See “Disclosure of Expenses” on page 8 for further information on how expenses were calculated.

| F U N D S U M M A R Y | 5 |

| Fund Summary as of September 30, 2018 (continued) | BlackRock Balanced Capital Fund, Inc. |

Portfolio Information

| 6 | 2 0 1 8 B L A C K R O C K A N N U A L R E P O R T T O S H A R E H O L D E R S |

| The Benefits and Risks of Leveraging | BlackRock Balanced Capital Fund, Inc. |

The Master Total Return Portfolio may utilize leverage to seek to enhance returns and NAV. However, there is no guarantee that these objectives can be achieved in all interest rate environments.

The Master Total Return Portfolio may utilize leverage through a credit facility. In general, the concept of leveraging is based on the premise that the financing cost of leverage, which is based on short-term interest rates, is normally lower than the income earned by the Master Total Return Portfolio on its longer-term portfolio investments purchased with the proceeds from leverage. To the extent that the total assets of the Master Total Return Portfolio (including the assets obtained from leverage) are invested in higher-yielding portfolio investments, the Master Total Return Portfolio’s shareholders benefit from the incremental net income.

The interest earned on securities purchased with the proceeds from leverage is distributed to the Master Total Return Portfolio’s shareholders, and the value of these portfolio holdings is reflected in the Master Total Return Portfolio’s per share NAV. However, in order to benefit shareholders, the return on assets purchased with leverage proceeds must exceed the ongoing costs associated with the leverage. If interest and other ongoing costs of leverage exceed the Master Total Return Portfolio’s return on assets purchased with leverage proceeds, income to shareholders is lower than if the Master Total Return Portfolio had not used leverage.

Furthermore, the value of the Master Total Return Portfolio’s investments generally varies inversely with the direction of long-term interest rates, although other factors can also influence the value of portfolio investments. As a result, changes in interest rates can influence the Master Total Return Portfolio’s NAV positively or negatively in addition to the impact on the Master Total Return Portfolio’s performance from leverage. Changes in the direction of interest rates are difficult to predict accurately, and there is no assurance that the Master Total Return Portfolio’s leveraging strategy will be successful.

The use of leverage also generally causes greater changes in the Master Total Return Portfolio’s NAV and dividend rates than comparable portfolios without leverage. In a declining market, leverage is likely to cause a greater decline in the NAV of the Master Total Return Portfolio’s shares than if the Master Total Return Portfolio was not leveraged. In addition, the Master Total Return Portfolio may be required to sell portfolio securities at inopportune times or at distressed values in order to comply with regulatory requirements applicable to the use of leverage or as required by the terms of the leverage instruments, which may cause the Master Total Return Portfolio to incur losses. The use of leverage may limit the Master Total Return Portfolio’s ability to invest in certain types of securities or use certain types of hedging strategies. The Master Total Return Portfolio incurs expenses in connection with the use of leverage, all of which are borne by the Master Total Return Portfolio’s shareholders and may reduce income.

Derivative Financial Instruments

The Fund and/or the Master Portfolios may invest in various derivative financial instruments. These instruments are used to obtain exposure to a security, commodity, index, market, and/or other assets without owning or taking physical custody of securities, commodities and/or other referenced assets or to manage market, equity, credit, interest rate, foreign currency exchange rate, commodity and/or other risks. Derivative financial instruments may give rise to a form of economic leverage and involve risks, including the imperfect correlation between the value of a derivative financial instrument and the underlying asset, possible default of the counterparty to the transaction or illiquidity of the instrument. The Fund and/or the Master Portfolios’ successful use of a derivative financial instrument depends on the investment adviser’s ability to predict pertinent market movements accurately, which cannot be assured. The use of these instruments may result in losses greater than if they had not been used, may limit the amount of appreciation the Fund and/or the Master Portfolios can realize on an investment and/or may result in lower distributions paid to shareholders. The Fund and/or the Master Portfolios’ investments in these instruments, if any, are discussed in detail in the Fund and the Master Portfolios’ Notes to Financial Statements.

| T H E B E N E F I T S A N D R I S K S O F L E V E R A G I N G / D E R I V A T I V E F I N A N C I A L I N S T R U M E N T S | 7 |

| About Fund Performance | BlackRock Balanced Capital Fund, Inc. |

Institutional and Class K Shares are not subject to any sales charge. These shares bear no ongoing distribution or service fees and are available only to certain eligible investors. Class K Shares performance shown prior to the January 25, 2018 inception date is that of Institutional Shares. The performance of the Fund’s Class K Shares would be substantially similar to Institutional Shares because Class K Shares and Institutional Shares invest in the same portfolio of securities and performance would only differ to the extent that Class K Shares and Institutional Shares have different expenses. The actual returns of Class K Shares would have been higher than those of the Institutional Shares because Class K Shares have lower expenses than the Institutional Shares.

Investor A Shares are subject to a maximum initial sales charge (front-end load) of 5.25% and a service fee of 0.25% per year (but no distribution fee). Certain redemptions of these shares may be subject to a contingent deferred sales charge (“CDSC”) where no initial sales charge was paid at the time of purchase. These shares are generally available through financial intermediaries. On December 27, 2017, the Fund’s issued and outstanding Investor B Shares converted into Investor A Shares with the same relative aggregate net asset value (“NAV”).

Investor C Shares are subject to a 1.00% CDSC if redeemed within one year of purchase. In addition, these shares are subject to a distribution fee of 0.75% per year and a service fee of 0.25% per year. These shares are generally available through financial intermediaries. Effective November 8, 2018, the Fund will adopt an automatic conversion feature whereby Investor C Shares will be automatically converted into Investor A Shares after a conversion period of approximately ten years, and, thereafter, investors will be subject to lower ongoing fees.

Class R Shares are not subject to any sales charge. These shares are subject to a distribution fee of 0.25% per year and a service fee of 0.25% per year. These shares are available only to certain employer-sponsored retirement plans.

Performance information reflects past performance and does not guarantee future results. The performance information for periods prior to February 2009 does not reflect any investment by the Fund in the Master Advantage Large Cap Core Portfolio. Current performance may be lower or higher than the performance data quoted. Refer to www.blackrock.com to obtain performance data current to the most recent month end. Performance results do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Figures shown in the performance tables on the previous pages assume reinvestment of all distributions, if any, at NAV on the ex-dividend dates. Investment return and principal value of shares will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. Distributions paid to each class of shares will vary because of the different levels of service, distribution and transfer agency fees applicable to each class, which are deducted from the income available to be paid to shareholders.

BlackRock Advisors, LLC (the “Manager”), the Fund’s investment adviser, has contractually and/or voluntarily agreed to waive and/or reimburse a portion of the Fund’s expenses. Without such waiver and/or reimbursement, the Fund’s performance would have been lower. The Manager is under no obligation to continue waiving and/or reimbursing its fees after the applicable termination date of such agreement. See Note 5 of the Notes to Financial Statements for additional information on waivers and/or reimbursements.

Shareholders of the Fund may incur the following charges: (a) transactional expenses, such as sales charges; and (b) operating expenses, including investment advisory fees, service and distribution fees, including 12b-1 fees, acquired fund fees and expenses and other fund expenses. The expense example shown on the page 5 (which is based on a hypothetical investment of $1,000 invested on April 1, 2018 and held through September 30, 2018) is intended to assist shareholders both in calculating expenses based on an investment in the Fund and in comparing these expenses with similar costs of investing in other mutual funds.

The expense example provides information about actual account values and actual expenses. In order to estimate the expenses a shareholder paid during the period covered by this report, shareholders can divide their account value by $1,000 and then multiply the result by the number corresponding to their share class under the heading entitled “Expenses Paid During the Period.”

The expense example also provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses. In order to assist shareholders in comparing the ongoing expenses of investing in the Fund and other funds, compare the 5% hypothetical examples with the 5% hypothetical examples that appear in shareholder reports of other funds.

The expenses shown in the expense example are intended to highlight shareholders’ ongoing costs only and do not reflect transactional expenses, such as sales charges, if any. Therefore, the hypothetical examples are useful in comparing ongoing expenses only, and will not help shareholders determine the relative total expenses of owning different funds. If these transactional expenses were included, shareholder expenses would have been higher.

| 8 | 2 0 1 8 B L A C K R O C K A N N U A L R E P O R T T O S H A R E H O L D E R S |

| September 30, 2018 |

BlackRock Balanced Capital Fund, Inc. (Percentages shown are based on Net Assets) |

| (a) | Annualized 7-day yield as of period end. |

| (b) | During the year ended September 30, 2018, investments in issuers considered to be affiliates of the Fund for purposes of Section 2(a)(3) of the Investment Company Act of 1940, as amended, and/or related parties of the Fund were as follows: |

| Affiliate |

Shares/ at 09/30/17 |

Shares/ Investment Value Purchased |

Shares/ Investment Value Sold |

Shares/ Investment Value Held at 09/30/18 |

Value at 09/30/18 |

Income | Net Realized Gain (Loss)(a) |

Change in Unrealized Appreciation (Depreciation) |

||||||||||||||||||||||||

| BlackRock Liquidity Funds, T-Fund, Institutional Class |

106,283,056 | — | (71,073,057 | )(b) | 35,209,999 | $ | 35,209,999 | $ | 586,089 | $ | 385 | $ | — | |||||||||||||||||||

| BlackRock Total Factor Fund, Class K |

— | 97,858 | — | 97,858 | 985,435 | — | 44,029 | (58,602 | ) | |||||||||||||||||||||||

| iShares Core U.S. Aggregate Bond ETF |

226,789 | 660,858 | (392,364 | ) | 495,283 | 52,262,262 | 1,307,602 | (722,905 | ) | (1,157,589 | ) | |||||||||||||||||||||

| iShares Edge MSCI Multifactor USA Index Fund |

— | 620,540 | (518,605 | ) | 101,935 | 3,427,055 | 134,581 | 433,935 | 138,632 | |||||||||||||||||||||||

| Master Advantage Large Cap Core Portfolio of Master Large Cap Series LLC |

$ | 614,070,118 | $ | 28,200,507 | (c)(d) | — | $ | 642,270,625 | 642,270,625 | 9,056,262 | 70,277,605 | 21,966,645 | ||||||||||||||||||||

| Master Total Return Portfolio of Master Bond LLC |

$ | 276,947,940 | $ | 72,984,229 | (c)(d) | — | $ | 349,932,169 | 349,932,169 | 12,273,346 | (5,774,754 | ) | (10,514,849 | ) | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||

| $ | 1,084,087,545 | $ | 23,357,880 | $ | 64,258,295 | $ | 10,374,237 | |||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||

| (a) | Includes net capital gain distributions, if applicable. |

| (b) | Represents net shares sold. |

| (c) | Inclusive of income, expense, realized and unrealized gains and losses allocated from the Master Portfolio. |

| (d) | Represents net shares/investment value purchased. |

Derivative Financial Instruments Outstanding as of Period End

Futures Contracts

| Description | Number of Contracts |

Expiration Date |

Notional Amount (000) |

Value/ Unrealized Appreciation (Depreciation) |

||||||||||||

| Long Contracts |

||||||||||||||||

| Nikkei 225 Index |

104 | 12/13/18 | $ | 22,078 | $ | 1,812,382 | ||||||||||

| TOPIX Index |

137 | 12/13/18 | 21,915 | 1,026,090 | ||||||||||||

| U.S. Treasury Notes (10 Year) |

129 | 12/19/18 | 15,323 | (200,752 | ) | |||||||||||

|

|

|

|||||||||||||||

| 2,637,720 | ||||||||||||||||

|

|

|

|||||||||||||||

| Short Contracts |

||||||||||||||||

| U.S. Ultra Treasury Bonds |

350 | 12/19/18 | 53,998 | 2,172,821 | ||||||||||||

| S&P 500 E-Mini Index |

80 | 12/21/18 | 11,676 | (34,776 | ) | |||||||||||

|

|

|

|||||||||||||||

| 2,138,045 | ||||||||||||||||

|

|

|

|||||||||||||||

| $ | 4,775,765 | |||||||||||||||

|

|

|

|||||||||||||||

| F U N D S C H E D U L E O F I N V E S T M E N T S | 9 |

| Schedule of Investments (continued) September 30, 2018 |

BlackRock Balanced Capital Fund, Inc. |

Forward Foreign Currency Exchange Contracts

| Currency Purchased |

Currency Sold |

Counterparty | Settlement Date |

Unrealized Appreciation (Depreciation) |

||||||||||||||

| AUD | 28,065,000 | USD | 20,277,684 | JPMorgan Chase Bank N.A. | 12/19/18 | $ | 22,321 | |||||||||||

| EUR | 24,600,000 | USD | 28,929,078 | Goldman Sachs International | 12/19/18 | (164,886 | ) | |||||||||||

|

|

|

|||||||||||||||||

| Net Unrealized Depreciation |

$ | (142,565 | ) | |||||||||||||||

|

|

|

|||||||||||||||||

Derivative Financial Instruments Categorized by Risk Exposure

As of period end, the fair values of derivative financial instruments located in the Statement of Assets and Liabilities were as follows:

| Assets — Derivative Financial Instruments | Commodity Contracts |

Credit Contracts |

Equity Contracts |

Foreign Currency Exchange Contracts |

Interest Rate Contracts |

Other Contracts |

Total | |||||||||||||||||||||||

| Futures contracts |

Net unrealized appreciation(a) | $ | — | $ | — | $ | 2,838,472 | $ | — | $ | 2,172,821 | $ | — | $ | 5,011,293 | |||||||||||||||

| Forward foreign currency exchange contracts |

Unrealized appreciation on forward foreign currency exchange contracts | — | — | — | 22,321 | — | — | 22,321 | ||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||

| $ | — | $ | — | $ | 2,838,472 | $ | 22,321 | $ | 2,172,821 | $ | — | $ | 5,033,614 | |||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||

| Liabilities — Derivative Financial Instruments |

||||||||||||||||||||||||||||||

| Futures contracts |

Net unrealized depreciation(a) | $ | — | $ | — | $ | 34,776 | $ | — | $ | 200,752 | $ | — | $ | 235,528 | |||||||||||||||

| Forward foreign currency exchange contracts |

Unrealized depreciation on forward foreign currency exchange contracts | — | — | — | 164,886 | — | — | 164,886 | ||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||

| $ | — | $ | — | $ | 34,776 | $ | 164,886 | $ | 200,752 | $ | — | $ | 400,414 | |||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||

| (a) | Includes cumulative appreciation (depreciation) on futures, if any, as reported in the Schedule of Investments. Only current day’s variation margin is reported within the Statement of Assets and Liabilities. |

For the year ended September 30, 2018, the effect of derivative financial instruments in the Statement of Operations were as follows:

| Net Realized Gain (Loss) from: | Commodity Contracts |

Credit Contracts |

Equity Contracts |

Foreign Currency Exchange Contracts |

Interest Rate Contracts |

Other Contracts |

Total | |||||||||||||||||||||

| Futures contracts |

$ | — | $ | — | $ | 3,533,895 | $ | — | $ | 1,414,941 | $ | — | $ | 4,948,836 | ||||||||||||||

| Forward foreign currency exchange contracts |

— | — | — | (441,753 | ) | — | — | (441,753 | ) | |||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| $ | — | $ | — | $ | 3,533,895 | $ | (441,753 | ) | $ | 1,414,941 | $ | — | $ | 4,507,083 | ||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Net Change in Unrealized Appreciation (Depreciation) on: |

||||||||||||||||||||||||||||

| Futures contracts |

$ | — | $ | — | $ | 1,538,155 | $ | — | $ | 1,574,222 | $ | — | $ | 3,112,377 | ||||||||||||||

| Forward foreign currency exchange contracts |

— | — | — | (142,565 | ) | — | — | (142,565 | ) | |||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| $ | — | $ | — | $ | 1,538,155 | $ | (142,565 | ) | $ | 1,574,222 | $ | — | $ | 2,969,812 | ||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

Average Quarterly Balances of Outstanding Derivative Financial Instruments

| Futures contracts: |

||||

| Average notional value of contracts — long |

$ | 75,568,903 | ||

| Average notional value of contracts — short |

$ | 86,544,320 | ||

| Forward foreign currency exchange contracts: |

||||

| Average amounts sold — in USD |

$ | 12,301,691 |

For more information about the Fund’s investment risks regarding derivative financial instruments, refer to the Notes to Financial Statements.

| 10 | 2 0 1 8 B L A C K R O C K A N N U A L R E P O R T T O S H A R E H O L D E R S |

| Schedule of Investments (continued) September 30, 2018 |

BlackRock Balanced Capital Fund, Inc. |

Derivative Financial Instruments – Offsetting as of Period End

The Fund’s derivative assets and liabilities (by type) were as follows:

| Assets | Liabilities | |||||||

| Derivative Financial Instruments: |

||||||||

| Futures contracts |

$ | 568,227 | $ | — | ||||

| Forward foreign currency exchange contracts |

22,321 | 164,886 | ||||||

|

|

|

|

|

|||||

| Total derivative assets and liabilities in the Statement of Assets and Liabilities |

$ | 590,548 | $ | 164,886 | ||||

|

|

|

|

|

|||||

| Derivatives not subject to a Master Netting Agreement or similar agreement (“MNA”) |

(568,227 | ) | — | |||||

|

|

|

|

|

|||||

| Total derivative assets and liabilities subject to an MNA |

$ | 22,321 | $ | 164,886 | ||||

|

|

|

|

|

|||||

The following table presents the Fund’s derivative assets and liabilities by counterparty net of amounts available for offset under an MNA and net of the related collateral received and pledged by the Fund:

| Counterparty |

Derivative Subject to an MNA

by |

Derivatives for Offset |

Non-cash Collateral Received |

Cash Collateral Received |

Net Amount of Derivative Assets(a) |

|||||||||||||||

| JPMorgan Chase Bank N.A |

$ | 22,321 | $ | — | $ | — | $ | — | $ | 22,321 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Counterparty | Derivative Liabilities Subject to an MNA by Counterparty |

Derivatives Available for Offset |

Non-cash Collateral Pledged |

Cash Collateral Pledged |

Net Amount of |

|||||||||||||||

| Goldman Sachs International |

$ | 164,886 | $ | — | $ | — | $ | — | $ | 164,886 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| (a) | Net amount represents the net amount receivable from the counterparty in the event of default. |

| (b) | Net amount represents the net amount payable due to the counterparty in the event of default. |

Fair Value Hierarchy as of Period End

Various inputs are used in determining the fair value of investments and derivative financial instruments. For more information about the Fund’s policy regarding valuation of investments and derivative financial instruments, refer to the Notes to Financial Statements.

The following tables summarize the Fund’s investments and derivative financial instruments categorized in the disclosure hierarchy:

| Level 1 | Level 2 | Level 3 | Total | |||||||||||||

| Assets: |

||||||||||||||||

| Investments: |

||||||||||||||||

| Investment Companies(a) |

$ | 91,884,751 | $ | — | $ | — | $ | 91,884,751 | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Investments Valued at NAV(b) |

992,202,794 | |||||||||||||||

|

|

|

|||||||||||||||

| Total Investments |

$ | 1,084,087,545 | ||||||||||||||

|

|

|

|||||||||||||||

| Derivative Financial Instruments(c) |

||||||||||||||||

| Assets: |

||||||||||||||||

| Equity contracts |

$ | 2,838,472 | $ | — | $ | — | $ | 2,838,472 | ||||||||

| Foreign currency exchange contracts |

— | 22,321 | — | 22,321 | ||||||||||||

| Interest rate contracts |

2,172,821 | — | — | 2,172,821 | ||||||||||||

| Liabilities: |

||||||||||||||||

| Equity contracts |

(34,776 | ) | — | — | (34,776 | ) | ||||||||||

| Foreign currency exchange contracts |

— | (164,886 | ) | — | (164,886 | ) | ||||||||||

| Interest rate contracts |

(200,752 | ) | — | — | (200,752 | ) | ||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| $ | 4,775,765 | $ | (142,565 | ) | — | $ | 4,633,200 | |||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| (a) | See above Schedule of Investments for values in each security type. |

| (b) | As of September 30, 2018, certain investments of the Fund were fair valued using NAV per share or its equivalent as no quoted market value is available and therefore have been excluded from the fair value hierarchy. |

| (c) | Derivative financial instruments are futures contracts and forward foreign currency exchange contracts, which are valued at the unrealized appreciation (depreciation) on the instrument. |

During the year ended September 30, 2018, there were no transfers between levels.

See notes to financial statements.

| F U N D S C H E D U L E O F I N V E S T M E N T S | 11 |

Statement of Assets and Liabilities

September 30, 2018

| BlackRock Balanced Capital |

||||

| ASSETS |

||||

| Investments at value — affiliated (cost — $1,011,892,750) |

$ | 1,084,087,545 | ||

| Cash pledged for futures contracts |

2,544,991 | |||

| Foreign currency at value (cost — $2,915,698) |

2,888,604 | |||

| Receivables: |

||||

| Capital shares sold |

1,302,551 | |||

| Dividends — affiliated |

60,017 | |||

| Variation margin on futures contracts |

568,227 | |||

| Unrealized appreciation on forward foreign currency exchange contracts |

22,321 | |||

| Deferred offering costs |

7,030 | |||

| Prepaid expenses |

51,535 | |||

|

|

|

|||

| Total assets |

1,091,532,821 | |||

|

|

|

|||

| LIABILITIES |

||||

| Payables: |

||||

| Board realignment and consolidation |

35,138 | |||

| Capital shares redeemed |

7,964,686 | |||

| Investment advisory fees |

118,457 | |||

| Offering costs |

16,683 | |||

| Officer’s fees |

5,939 | |||

| Other accrued expenses |

148,783 | |||

| Other affiliates |

35,116 | |||

| Service and distribution fees |

198,027 | |||

| Transfer agent fees |

231,200 | |||

| Unrealized depreciation on forward foreign currency exchange contracts |

164,886 | |||

|

|

|

|||

| Total liabilities |

8,918,915 | |||

|

|

|

|||

| NET ASSETS |

$ | 1,082,613,906 | ||

|

|

|

|||

| NET ASSETS CONSIST OF |

||||

| Paid-in capital |

$ | 929,650,748 | ||

| Undistributed net investment income |

4,320,444 | |||

| Accumulated net realized gain |

71,841,814 | |||

| Net unrealized appreciation (depreciation) |

76,800,900 | |||

|

|

|

|||

| NET ASSETS |

$ | 1,082,613,906 | ||

|

|

|

|||

| NET ASSET VALUE |

||||

| Institutional — Based on net assets of $427,510,797 and 17,851,290 shares outstanding, 400 million shares authorized, $0.10 par value |

$ | 23.95 | ||

|

|

|

|||

| Investor A — Based on net assets of $528,701,177 and 22,162,643 shares outstanding, 200 million shares authorized, $0.10 par value |

$ | 23.86 | ||

|

|

|

|||

| Investor C — Based on net assets of $103,755,756 and 4,990,694 shares outstanding, 200 million shares authorized, $0.10 par value |

$ | 20.79 | ||

|

|

|

|||

| Class K — Based on net assets of $8,283,024 and 345,899 shares outstanding, 2 billion shares authorized, $0.10 par value |

$ | 23.95 | ||

|

|

|

|||

| Class R — Based on net assets of $14,363,152 and 652,973 shares outstanding, 500 million shares authorized, $0.10 par value |

$ | 22.00 | ||

|

|

|

|||

See notes to financial statements.

| 12 | 2 0 1 8 B L A C K R O C K A N N U A L R E P O R T T O S H A R E H O L D E R S |

Year Ended September 30, 2018

| BlackRock Balanced Capital Fund, Inc. |

||||

| INVESTMENT INCOME |

| |||

| Dividends — unaffiliated |

$ | 79,774 | ||

| Dividends — affiliated |

2,028,272 | |||

| Other income |

26,215 | |||

| Net investment income allocated from the affiliated Master Portfolios: |

||||

| Interest — unaffiliated |

13,143,741 | |||

| Dividends — unaffiliated |

11,765,659 | |||

| Dividends — affiliated |

289,538 | |||

| Securities lending income — affiliated — net |

22,395 | |||

| Other income |

1,421 | |||

| Foreign taxes withheld |

(16,296 | ) | ||

| Total expenses |

(3,885,153 | ) | ||

| Fees waived |

8,303 | |||

|

|

|

|||

| Total investment income |

23,463,869 | |||

|

|

|

|||

| FUND EXPENSES |

| |||

| Investment advisory |

4,524,665 | |||

| Service and distribution — class specific |

2,404,214 | |||

| Transfer agent — class specific |

1,046,902 | |||

| Registration |

109,458 | |||

| Professional |

103,180 | |||

| Printing |

72,721 | |||

| Board realignment and consolidation |

35,138 | |||

| Officer |

28,212 | |||

| Offering |

27,215 | |||

| Custodian |

15,621 | |||

| Accounting services |

1,939 | |||

| Miscellaneous |

32,685 | |||

|

|

|

|||

| Total expenses |

8,401,950 | |||

| Less fees waived and/or reimbursed by the Manager |

(3,071,580 | ) | ||

|

|

|

|||

| Total expenses after fees waived and/or reimbursed |

5,330,370 | |||

|

|

|

|||

| Net investment income |

18,133,499 | |||

|

|

|

|||

| REALIZED AND UNREALIZED GAIN (LOSS) |

| |||

| Net realized gain from: |

||||

| Investments — unaffiliated |

145,192 | |||

| Investments — affiliated |

(288,970 | ) | ||

| Capital gain distributions from investment companies — affiliated |

44,414 | |||

| Foreign currency translations |

3,792 | |||

| Forward foreign currency exchange contracts |

(441,753 | ) | ||

| Futures contracts |

4,948,836 | |||

| Net realized gain from investments, borrowed bonds, payments by affiliate, foreign currency transactions, forward foreign currency exchange contracts, futures contracts, options written and swaps allocated from the affiliated Master Portfolios |

64,502,851 | |||

|

|

|

|||

| 68,914,362 | ||||

|

|

|

|||

| Net change in unrealized appreciation (depreciation) on: |

||||

| Investments — unaffiliated |

(366,392 | ) | ||

| Investments — affiliated |

(1,077,559 | ) | ||

| Futures contracts |

3,112,377 | |||

| Forward foreign currency exchange contracts |

(142,565 | ) | ||

| Foreign currency translations |

19,682 | |||

| Net change in unrealized appreciation (depreciation) on investments, borrowed bonds, foreign currency translations, forward foreign currency exchange contracts, futures contracts, options written, short sales and swaps allocated from the affiliated Master Portfolios |

11,451,796 | |||

|

|

|

|||

| 12,997,339 | ||||

|

|

|

|||

| Net realized and unrealized gain |

81,911,701 | |||

|

|

|

|||

| NET INCREASE IN NET ASSETS RESULTING FROM OPERATIONS |

$ | 100,045,200 | ||

|

|

|

|||

See notes to financial statements.

| F U N D F I N A N C I A L S T A T E M E N T S | 13 |

Statements of Changes in Net Assets

| BlackRock Balanced Capital Fund, Inc. | ||||||||

| Year Ended September 30, | ||||||||

| 2018 | 2017 | |||||||

| INCREASE (DECREASE) IN NET ASSETS |

||||||||

| OPERATIONS |

||||||||

| Net investment income |

$ | 18,133,499 | $ | 14,299,404 | ||||

| Net realized gain |

68,914,362 | 169,911,456 | ||||||

| Net change in unrealized appreciation (depreciation) |

12,997,339 | (45,529,106 | ) | |||||

|

|

|

|

|

|||||

| Net increase in net assets resulting from operations |

100,045,200 | 138,681,754 | ||||||

|

|

|

|

|

|||||

| DISTRIBUTIONS TO SHAREHOLDERS(a) |

||||||||

| From net investment income: |

||||||||

| Institutional |

(7,864,574 | ) | (5,977,896 | ) | ||||

| Investor A |

(8,476,532 | ) | (7,033,433 | ) | ||||

| Investor C |

(1,161,720 | ) | (826,230 | ) | ||||

| Class K |

(77,270 | ) | — | |||||

| Class R |

(219,925 | ) | (162,510 | ) | ||||

| From net realized gain: |

||||||||

| Institutional |

(63,775,655 | ) | (11,650,226 | ) | ||||

| Investor A |

(80,979,483 | ) | (16,359,474 | ) | ||||

| Investor B |

(5,569 | ) | (13,851 | ) | ||||

| Investor C |

(17,905,020 | ) | (4,424,571 | ) | ||||

| Class R |

(2,623,088 | ) | (455,657 | ) | ||||

|

|

|

|

|

|||||

| Decrease in net assets resulting from distributions to shareholders |

(183,088,836 | ) | (46,903,848 | ) | ||||

|

|

|

|

|

|||||

| CAPITAL SHARE TRANSACTIONS |

||||||||

| Net increase (decrease) in net assets derived from capital share transactions |

113,852,254 | (11,429,619 | ) | |||||

|

|

|

|

|

|||||

| NET ASSETS |

||||||||

| Total increase in net assets |

30,808,618 | 80,348,287 | ||||||

| Beginning of year |

1,051,805,288 | 971,457,001 | ||||||

|

|

|

|

|

|||||

| End of year |

$ | 1,082,613,906 | $ | 1,051,805,288 | ||||

|

|

|

|

|

|||||

| Undistributed net investment income, end of year |

$ | 4,320,444 | $ | 4,457,519 | ||||

|

|

|

|

|

|||||

| (a) | Distributions for annual periods determined in accordance with U.S. federal income tax regulations. |

See notes to financial statements.

| 14 | 2 0 1 8 B L A C K R O C K A N N U A L R E P O R T T O S H A R E H O L D E R S |

(For a share outstanding throughout each period)

| BlackRock Balanced Capital Fund, Inc. | ||||||||||||||||||||

| Institutional | ||||||||||||||||||||

| Year Ended September 30, | ||||||||||||||||||||

| 2018 | 2017 | 2016 | 2015 | 2014 | ||||||||||||||||

| Net asset value, beginning of year |

$ | 26.09 | $ | 23.86 | $ | 23.09 | $ | 26.07 | $ | 25.16 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net investment income(a) |

0.47 | 0.41 | 0.38 | 0.37 | 0.48 | |||||||||||||||

| Net realized and unrealized gain (loss) |

1.89 | 3.01 | 1.64 | (0.03 | ) | 3.05 | ||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net increase from investment operations |

2.36 | 3.42 | 2.02 | 0.34 | 3.53 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Distributions:(b) | ||||||||||||||||||||

| From net investment income |

(0.47 | ) | (0.40 | ) | (0.41 | ) | (0.43 | ) | (0.56 | ) | ||||||||||

| From net realized gain |

(4.03 | ) | (0.79 | ) | (0.84 | ) | (2.89 | ) | (2.06 | ) | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total distributions |

(4.50 | ) | (1.19 | ) | (1.25 | ) | (3.32 | ) | (2.62 | ) | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net asset value, end of year |

$ | 23.95 | $ | 26.09 | $ | 23.86 | $ | 23.09 | $ | 26.07 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total Return(c) |

||||||||||||||||||||

| Based on net asset value |

10.14 | % | 14.83 | %(d) | 8.93 | %(d) | 0.82 | % | 14.77 | % | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Ratios to Average Net Assets(e) |

||||||||||||||||||||

| Total expenses(f) |

0.91 | % | 0.93 | % | 0.94 | % | 0.92 | % | 0.95 | % | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total expenses after fees waived and/or reimbursed(f) |

0.62 | % | 0.62 | % | 0.63 | % | 0.59 | % | 0.63 | % | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net investment income(f) |

1.97 | % | 1.67 | % | 1.64 | % | 1.52 | % | 1.88 | % | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Supplemental Data |

||||||||||||||||||||

| Net assets, end of year (000) |

$ | 427,511 | $ | 395,850 | $ | 348,430 | $ | 341,225 | $ | 348,345 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Portfolio turnover rate of the Fund(g) |

140 | % | 109 | % | — | — | — | |||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Portfolio turnover rate of the Master Total Return Portfolio(h) |

734 | % | 806 | % | 841 | % | 1,015 | % | 750 | % | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Portfolio turnover rate of the Master Advantage Large Cap Core Portfolio |

148 | % | 130 | % | 39 | % | 41 | % | 40 | % | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| (a) | Based on average shares outstanding. |

| (b) | Distributions for annual periods determined in accordance with U.S. federal income tax regulations. |

| (c) | Where applicable, assumes the reinvestment of distributions. |

| (d) | Includes proceeds received from a settlement of litigation, which had no impact on the Fund’s total return. |

| (e) | Includes the Fund’s share of the Master Portfolios’ allocated expenses and/or net investment income. |

| (f) | Excludes expenses incurred indirectly as a result of investments in underlying funds as follows: |

| Year Ended September 30, | ||||||||||||||||||||||||||||||||||||||||

| 2018 | 2017 | 2016 | 2015 | 2014 | ||||||||||||||||||||||||||||||||||||

| Investments in underlying funds |

0.01 | % | 0.01 | % | 0.01 | % | — | — | ||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||||||

| (g) | Excludes transactions in the Master Portfolios. |

| (h) | Includes mortgage dollar roll transactions. Additional information regarding portfolio turnover rate is as follows: |

| Year Ended September 30, | ||||||||||||||||||||||||||||||||||||||||

| 2018 | 2017 | 2016 | 2015 | 2014 | ||||||||||||||||||||||||||||||||||||

| Portfolio turnover rate (excluding mortgage dollar roll transactions) |

350 | % | 540 | % | 598 | % | 725 | % | 529 | % | ||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||||||

See notes to financial statements.

| F U N D F I N A N C I A L H I G H L I G H T S | 15 |

Financial Highlights (continued)

(For a share outstanding throughout each period)

| BlackRock Balanced Capital Fund, Inc. (continued) | ||||||||||||||||||||

| Investor A | ||||||||||||||||||||

| Year Ended September 30, | ||||||||||||||||||||

| 2018 | 2017 | 2016 | 2015 | 2014 | ||||||||||||||||

| Net asset value, beginning of year |

$ | 26.00 | $ | 23.78 | $ | 23.03 | $ | 26.00 | $ | 25.11 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net investment income(a) |

0.40 | 0.34 | 0.31 | 0.30 | 0.40 | |||||||||||||||

| Net realized and unrealized gain (loss) |

1.89 | 3.01 | 1.62 | (0.02 | ) | 3.03 | ||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net increase from investment operations |

2.29 | 3.35 | 1.93 | 0.28 | 3.43 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Distributions:(b) | ||||||||||||||||||||

| From net investment income |

(0.40 | ) | (0.34 | ) | (0.34 | ) | (0.36 | ) | (0.48 | ) | ||||||||||

| From net realized gain |

(4.03 | ) | (0.79 | ) | (0.84 | ) | (2.89 | ) | (2.06 | ) | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total distributions |

(4.43 | ) | (1.13 | ) | (1.18 | ) | (3.25 | ) | (2.54 | ) | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net asset value, end of year |

$ | 23.86 | $ | 26.00 | $ | 23.78 | $ | 23.03 | $ | 26.00 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total Return(c) |

||||||||||||||||||||

| Based on net asset value |

9.86 | % | 14.52 | %(d) | 8.57 | %(d) | 0.57 | % | 14.39 | % | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Ratios to Average Net Assets(e) |

||||||||||||||||||||

| Total expenses(f) |

1.20 | % | 1.21 | % | 1.22 | % | 1.20 | % | 1.25 | % | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total expenses after fees waived and/or reimbursed(f) |

0.91 | % | 0.90 | % | 0.91 | % | 0.88 | % | 0.92 | % | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net investment income(f) |

1.68 | % | 1.38 | % | 1.35 | % | 1.23 | % | 1.58 | % | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Supplemental Data |

||||||||||||||||||||

| Net assets, end of year (000) |

$ | 528,701 | $ | 535,542 | $ | 491,889 | $ | 461,642 | $ | 476,919 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Portfolio turnover rate of the Fund(g) |

140 | % | 109 | % | — | — | — | |||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Portfolio turnover rate of the Master Total Return Portfolio(h) |

734 | % | 806 | % | 841 | % | 1,015 | % | 750 | % | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Portfolio turnover rate of the Master Advantage Large Cap Core Portfolio |

148 | % | 130 | % | 39 | % | 41 | % | 40 | % | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| (a) | Based on average shares outstanding. |

| (b) | Distributions for annual periods determined in accordance with U.S. federal income tax regulations. |

| (c) | Where applicable, excludes the effects of any sales charges and assumes the reinvestment of distributions. |

| (d) | Includes proceeds received from a settlement of litigation, which had no impact on the Fund’s total return. |

| (e) | Includes the Fund’s share of the Master Portfolios’ allocated expenses and/or net investment income. |

| (f) | Excludes expenses incurred indirectly as a result of investments in underlying funds as follows: |

| Year Ended September 30, | ||||||||||||||||||||||||||||||||||||||||

| 2018 | 2017 | 2016 | 2015 | 2014 | ||||||||||||||||||||||||||||||||||||

| Investments in underlying funds |

0.01 | % | 0.01 | % | 0.01 | % | — | — | ||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||||||

| (g) | Excludes transactions in the Master Portfolios. |

| (h) | Includes mortgage dollar roll transactions. Additional information regarding portfolio turnover rate is as follows: |

| Year Ended September 30, | ||||||||||||||||||||||||||||||||||||||||

| 2018 | 2017 | 2016 | 2015 | 2014 | ||||||||||||||||||||||||||||||||||||

| Portfolio turnover rate (excluding mortgage dollar roll transactions) |

350 | % | 540 | % | 598 | % | 725 | % | 529 | % | ||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||||||

See notes to financial statements.

| 16 | 2 0 1 8 B L A C K R O C K A N N U A L R E P O R T T O S H A R E H O L D E R S |

Financial Highlights (continued)

(For a share outstanding throughout each period)

| BlackRock Balanced Capital Fund, Inc. (continued) | ||||||||||||||||||||

| Investor C | ||||||||||||||||||||

| Year Ended September 30, | ||||||||||||||||||||

| 2018 | 2017 | 2016 | 2015 | 2014 | ||||||||||||||||

| Net asset value, beginning of year |

$ | 23.21 | $ | 21.34 | $ | 20.80 | $ | 23.80 | $ | 23.20 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net investment income(a) |

0.19 | 0.14 | 0.12 | 0.10 | 0.19 | |||||||||||||||

| Net realized and unrealized gain (loss) |

1.67 | 2.68 | 1.47 | (0.01 | ) | 2.79 | ||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net increase from investment operations |

1.86 | 2.82 | 1.59 | 0.09 | 2.98 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Distributions:(b) | ||||||||||||||||||||

| From net investment income |

(0.25 | ) | (0.16 | ) | (0.21 | ) | (0.20 | ) | (0.32 | ) | ||||||||||

| From net realized gain |

(4.03 | ) | (0.79 | ) | (0.84 | ) | (2.89 | ) | (2.06 | ) | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total distributions |

(4.28 | ) | (0.95 | ) | (1.05 | ) | (3.09 | ) | (2.38 | ) | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net asset value, end of year |

$ | 20.79 | $ | 23.21 | $ | 21.34 | $ | 20.80 | $ | 23.80 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total Return(c) |

||||||||||||||||||||

| Based on net asset value |

9.03 | % | 13.62 | %(d) | 7.78 | %(d) | (0.21 | )% | 13.51 | % | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Ratios to Average Net Assets(e) |

||||||||||||||||||||

| Total expenses(f) |

1.95 | % | 1.97 | % | 1.98 | % | 1.97 | % | 2.02 | % | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total expenses after fees waived and/or reimbursed(f) |

1.66 | % | 1.66 | % | 1.67 | % | 1.65 | % | 1.69 | % | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net investment income(f) |

0.93 | % | 0.63 | % | 0.60 | % | 0.47 | % | 0.81 | % | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Supplemental Data |

||||||||||||||||||||

| Net assets, end of year (000) |

$ | 103,756 | $ | 104,113 | $ | 117,651 | $ | 86,397 | $ | 74,908 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Portfolio turnover rate of the Fund(g) |

140 | % | 109 | % | — | — | — | |||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Portfolio turnover rate of the Master Total Return Portfolio(h) |

734 | % | 806 | % | 841 | % | 1,015 | % | 750 | % | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Portfolio turnover rate of the Master Advantage Large Cap Core Portfolio |

148 | % | 130 | % | 39 | % | 41 | % | 40 | % | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| (a) | Based on average shares outstanding. |

| (b) | Distributions for annual periods determined in accordance with U.S. federal income tax regulations. |

| (c) | Where applicable, excludes the effects of any sales charges and assumes the reinvestment of distributions. |

| (d) | Includes proceeds received from a settlement of litigation, which had no impact on the Fund’s total return. |

| (e) | Includes the Fund’s share of the Master Portfolios’ allocated expenses and/or net investment income. |

| (f) | Excludes expenses incurred indirectly as a result of investments in underlying funds as follows: |

| Year Ended September 30, | ||||||||||||||||||||||||||||||||||||||||

| 2018 | 2017 | 2016 | 2015 | 2014 | ||||||||||||||||||||||||||||||||||||

| Investments in underlying funds |

0.01 | % | 0.01 | % | 0.01 | % | — | — | ||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||||||

| (g) | Excludes transactions in the Master Portfolios. |

| (h) | Includes mortgage dollar roll transactions. Additional information regarding portfolio turnover rate is as follows: |

| Year Ended September 30, | ||||||||||||||||||||||||||||||||||||||||

| 2018 | 2017 | 2016 | 2015 | 2014 | ||||||||||||||||||||||||||||||||||||

| Portfolio turnover rate (excluding mortgage dollar roll transactions) |

350 | % | 540 | % | 598 | % | 725 | % | 529 | % | ||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||||||

See notes to financial statements.

| F U N D F I N A N C I A L H I G H L I G H T S | 17 |

Financial Highlights (continued)

(For a share outstanding throughout each period)

| BlackRock Balanced Capital Fund, Inc. (continued) |

||||

| Class K | ||||

| Period from 01/25/18(a) to 09/30/18 |

||||

| Net asset value, beginning of period |

$ | 23.61 | ||

|

|

|

|||

| Net investment income(b) |

0.33 | |||

| Net realized and unrealized gain |

0.25 | |||

|

|

|

|||

| Net increase from investment operations |

0.58 | |||

|

|

|

|||

| Distributions from net investment income |

(0.24 | ) | ||

|

|

|

|||

| Net asset value, end of period |

$ | 23.95 | ||

|

|

|

|||

| Total Return(c) |

||||

| Based on net asset value |

2.46 | %(d) | ||

|

|

|

|||

| Ratios to Average Net Assets(e) |

||||

| Total expenses(f) |

0.81 | %(g) | ||

|

|

|

|||

| Total expenses after fees waived and/or reimbursed(f) |

0.51 | %(g) | ||

|

|

|

|||

| Net investment income(f) |

2.07 | %(g) | ||

|

|

|

|||

| Supplemental Data |

||||

| Net assets, end of period (000) |

$ | 8,283 | ||

|

|

|

|||

| Portfolio turnover rate of the Fund(h)(i) |

140 | % | ||

|

|

|

|||

| Portfolio turnover rate of the Master Total Return Portfolio(h)(j) |

734 | % | ||

|

|

|

|||

| Portfolio turnover rate of the Master Advantage Large Cap Core Portfolio(h) |

148 | % | ||

|

|

|

|||

| (a) | Commencement of operations. |

| (b) | Based on average shares outstanding. |

| (c) | Where applicable, assumes the reinvestment of distributions. |

| (d) | Aggregate total return. |

| (e) | Includes the Fund’s share of the Master Portfolio’s allocated expenses and/or net investment income. |

| (f) | Excludes expenses incurred indirectly as a result of investments in underlying funds as follows: |

| Period from 01/25/18(a) to 09/30/18 | |||||

| Investments in underlying funds |

0.01 | % | |||

|

|

|

||||

| (g) | Annualized. |

| (h) | Portfolio turnover rate is representative for the entire year. |

| (i) | Excludes transactions in the Master Portfolios. |

| (j) | Includes mortgage dollar roll transactions. Additional information regarding portfolio turnover rate is as follows: |

| Period from 01/25/18(a) to 09/30/18 | |||||

| Portfolio turnover rate (excluding mortgage dollar roll transactions)(h) |

350 | % | |||

|

|

|

||||

See notes to financial statements.

| 18 | 2 0 1 8 B L A C K R O C K A N N U A L R E P O R T T O S H A R E H O L D E R S |

Financial Highlights (continued)

(For a share outstanding throughout each period)

| BlackRock Balanced Capital Fund, Inc. (continued) | ||||||||||||||||||||

| Class R | ||||||||||||||||||||

| Year Ended September 30, | ||||||||||||||||||||

| 2018 | 2017 | 2016 | 2015 | 2014 | ||||||||||||||||

| Net asset value, beginning of year |

$ | 24.30 | $ | 22.31 | $ | 21.70 | $ | 24.68 | $ | 23.96 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net investment income(a) |

0.29 | 0.24 | 0.22 | 0.21 | 0.30 | |||||||||||||||

| Net realized and unrealized gain (loss) |

1.77 | 2.81 | 1.52 | (0.02 | ) | 2.89 | ||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net increase from investment operations |

2.06 | 3.05 | 1.74 | 0.19 | 3.19 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Distributions:(b) | ||||||||||||||||||||

| From net investment income |

(0.33 | ) | (0.27 | ) | (0.29 | ) | (0.28 | ) | (0.41 | ) | ||||||||||

| From net realized gain |

(4.03 | ) | (0.79 | ) | (0.84 | ) | (2.89 | ) | (2.06 | ) | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total distributions |

(4.36 | ) | (1.06 | ) | (1.13 | ) | (3.17 | ) | (2.47 | ) | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net asset value, end of year |

$ | 22.00 | $ | 24.30 | $ | 22.31 | $ | 21.70 | $ | 24.68 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total Return(c) |

||||||||||||||||||||

| Based on net asset value |

9.51 | % | 14.11 | %(d) | 8.15 | %(d) | 0.23 | % | 14.03 | % | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Ratios to Average Net Assets(e) |

||||||||||||||||||||

| Total expenses(f) |

1.55 | % | 1.56 | % | 1.58 | % | 1.53 | % | 1.59 | % | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total expenses after fees waived and/or reimbursed(f) |

1.26 | % | 1.25 | % | 1.27 | % | 1.21 | % | 1.27 | % | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net investment income(f) |

1.33 | % | 1.04 | % | 0.99 | % | 0.91 | % | 1.23 | % | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Supplemental Data |

||||||||||||||||||||

| Net assets, end of year (000) |

$ | 14,363 | $ | 16,257 | $ | 12,731 | $ | 10,448 | $ | 9,322 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Portfolio turnover rate of the Fund(g) |

140 | % | 109 | % | — | — | — | |||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Portfolio turnover rate of the Master Total Return Portfolio(h) |

734 | % | 806 | % | 841 | % | 1,015 | % | 750 | % | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Portfolio turnover rate of the Master Advantage Large Cap Core Portfolio |

148 | % | 130 | % | 39 | % | 41 | % | 40 | % | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| (a) | Based on average shares outstanding. |

| (b) | Distributions for annual periods determined in accordance with U.S. federal income tax regulations. |

| (c) | Where applicable, assumes the reinvestment of distributions. |

| (d) | Includes proceeds received from a settlement of litigation, which had no impact on the Fund’s total return. |

| (e) | Includes the Fund’s share of the Master Portfolios’ allocated expenses and/or net investment income. |

| (f) | Excludes expenses incurred indirectly as a result of investments in underlying funds as follows: |

| Year Ended September 30, | ||||||||||||||||||||||||||||||||||||||||

| 2018 | 2017 | 2016 | 2015 | 2014 | ||||||||||||||||||||||||||||||||||||

| Investments in underlying funds |

0.01 | % | 0.01 | % | 0.01 | % | — | — | ||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||||||

| (g) | Excludes transactions in the Master Portfolios. |

| (h) | Includes mortgage dollar roll transactions. Additional information regarding portfolio turnover rate is as follows: |

| Year Ended September 30, | ||||||||||||||||||||||||||||||||||||||||

| 2018 | 2017 | 2016 | 2015 | 2014 | ||||||||||||||||||||||||||||||||||||

| Portfolio turnover rate (excluding mortgage dollar roll transactions) |

350 | % | 540 | % | 598 | % | 725 | % | 529 | % | ||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||||||

See notes to financial statements.

| F U N D F I N A N C I A L H I G H L I G H T S | 19 |

| Notes to Financial Statements | BlackRock Balanced Capital Fund, Inc. |

| 1. | ORGANIZATION |

BlackRock Balanced Capital Fund, Inc. (the “Fund”) is registered under the Investment Company Act of 1940, as amended (the “1940 Act”), as an open-end management investment company. The Fund is classified as diversified. The Fund is organized as a Maryland corporation. The Fund seeks to achieve its investment objective by investing directly in equity and fixed-income securities, indirectly through one or more funds that invest in such securities, or in a combination of securities and funds. The Fund intends to invest a significant portion of its fixed-income assets in Master Total Return Portfolio (the “Master Total Return Portfolio”) of Master Bond LLC, a mutual fund that has an investment objective and strategy consistent with that of the fixed-income portion of the Fund. The Fund intends to invest a significant portion of its equity assets in Master Advantage Large Cap Core Portfolio (the “Master Advantage Large Cap Core Portfolio”) of Master Large Cap Series LLC, a mutual fund that has an investment objective and strategy consistent with that of the equity portion of the Fund. Master Total Return Portfolio and Master Advantage Large Cap Core Portfolio, both affiliates of the Fund, are collectively referred to as the “Master Portfolios.” The value of the Fund’s investment in the Master Portfolios reflects the Fund’s proportionate interest in the net assets of the Master Portfolios. The performance of the Fund is directly affected by the performance of the Master Portfolios as well as the Fund’s direct investments. At September 30, 2018, the percentages of the Master Advantage Large Cap Core Portfolio and Master Total Return Portfolio owned by the Fund were 20.7% and 2.7%, respectively. The financial statements of the Master Portfolios, including the Schedules of Investments, are included elsewhere in this report and should be read in conjunction with the Fund’s financial statements.