UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

(Mark One)

[X] QUARTERLY REPORT UNDER SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the quarterly period ended July 31, 2020

[ ] TRANSITION REPORT UNDER SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from ________ to ________

Commission file number 001-36138

ADVAXIS, INC.

(Exact name of registrant as specified in its charter)

| Delaware | 02-0563870 | |

| (State or other jurisdiction of | (IRS Employer | |

| incorporation or organization) | Identification No.) |

| 305 College Road East, Princeton, NJ | 08540 | |

| (Address of principal executive offices) | (Zip Code) |

(609) 452-9813

(Registrant’s telephone number)

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||

| Common Stock | ADXS | Nasdaq Capital Market |

Indicate by check mark whether the registrant (1) has fled all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such fling requirements for the past 90 days. Yes [X] No [ ]

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes [X] No [ ]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large Accelerated Filer | [ ] | Accelerated Filer | [ ] | |

| Non-accelerated Filer | [X] | Smaller Reporting Company | [X] | |

| Emerging growth company | [ ] |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act.[ ]

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes [ ] No [X]

The number of shares of the registrant’s Common Stock, $0.001 par value, outstanding as of September 2, 2020 was 66,227,473.

TABLE OF CONTENTS

| Page No. | ||

| PART I | FINANCIAL INFORMATION | 5 |

| Item 1. | Financial Statements (unaudited) | 5 |

| Condensed Balance Sheets | 5 | |

| Condensed Statements of Operations | 6 | |

| Condensed Statements of Cash Flows | 7 | |

| Notes to the Condensed Financial Statements | 8 | |

| Item 2. | Management’s Discussion and Analysis of Financial Condition and Results of Operations | 22 |

| Item 3. | Quantitative and Qualitative Disclosures About Market Risk | 31 |

| Item 4. | Controls and Procedures | 31 |

| PART II | OTHER INFORMATION | 32 |

| Item 1. | Legal Proceedings | 32 |

| Item 1A. | Risk Factors | 32 |

| Item 6. | Exhibits | 33 |

| SIGNATURES | 34 | |

| 2 |

CAUTIONARY NOTE REGARDING FORWARD LOOKING-STATEMENTS

This quarterly report on Form 10-Q (“Form 10-Q”) includes statements that are, or may be deemed, “forward-looking statements.” In some cases, these forward-looking statements can be identified by the use of such terms as “believes,” “estimates,” “anticipates,” “expects,” “plans,” “intends,” “may,” “could,” “might,” “will,” “should,” “approximately” or, in each case, their negative or other variations thereon or comparable terminology, although not all forward-looking statements contain these words. They appear in a number of places throughout this Form 10-Q and include statements regarding our intentions, beliefs, projections, outlook, analyses or current expectations concerning, among other things, our ongoing and planned discovery and development of drug candidates, the strength and breadth of our intellectual property, our ongoing and planned preclinical studies and clinical trials, the timing of and our ability to make regulatory filings and obtain and maintain regulatory approvals for our product candidates, the degree of clinical utility of our product candidates, particularly in specific patient populations, expectations regarding clinical trial data, our results of operations, financial condition, our available cash, liquidity, prospects, growth and strategies, impacts of the ongoing coronavirus (COVID-19) pandemic, the length of time that we will be able to continue to fund our operating expenses and capital expenditures, our expected financing needs and sources of financing, the industry in which we operate and the trends that may affect our industry or us.

By their nature, forward-looking statements involve risks and uncertainties because they relate to events, competitive dynamics, and healthcare, regulatory and scientific developments and depend on the economic circumstances that may or may not occur in the future or may occur on longer or shorter timelines than anticipated. Although we believe that we have a reasonable basis for each forward-looking statement contained in this Form 10-Q, we caution you that forward-looking statements are not guarantees of future performance and that our actual results of operations, financial condition and liquidity, and the development of the industry in which we operate, may differ materially from the forward-looking statements contained in this Form 10-Q. In addition, even if our results of operations, financial condition and liquidity, and the development of the industry in which we operate, are consistent with the forward-looking statements contained in this Form 10-Q, they may not be predictive of results or developments in future periods.

Some of the factors that we believe could cause actual results to differ from those anticipated or predicted include:

| ● | the success and timing of our clinical trials, including patient accrual; | |

| ● | our ability to obtain and maintain regulatory approval or reimbursement of our product candidates for marketing; | |

| ● | our ability to obtain the appropriate labeling of our products under any regulatory approval; | |

| ● | our ability to develop and commercialize our products;

| |

| ● | potential effects of the COVID-19 pandemic on our business, financial condition, liquidity and results of operations, and our ability to continue operations in the same manner as previously conducted prior to the macroeconomic effects of the COVID-19 pandemic; | |

| ● | the successful development and implementation of our sales and marketing campaigns; | |

| ● | the change of key scientific or management personnel; | |

| ● | the size and growth of the potential markets for our product candidates and our ability to serve those markets; | |

| ● | our ability to successfully compete in the potential markets for our product candidates, if commercialized; |

| 3 |

| ● | regulatory developments in the United States and other countries; | |

| ● | the rate and degree of market acceptance of any of our product candidates; | |

| ● | new products, product candidates or new uses for existing products or technologies introduced or announced by our competitors and the timing of these introductions or announcements; | |

| ● | market conditions in the pharmaceutical and biotechnology sectors; | |

| ● | our available cash; | |

| ● | the accuracy of our estimates regarding expenses, future revenues, capital requirements and needs for additional financing; | |

| ● | our ability to obtain additional funding; | |

| ● | our ability to obtain and maintain intellectual property protection for our product candidates; | |

| ● | the success and timing of our preclinical studies, including IND enabling studies; | |

| ● | the ability of our product candidates to successfully perform in clinical trials and to resolve any clinical holds that may occur; | |

| ● | our ability to obtain and maintain approval of our product candidates for trial initiation; | |

| ● | our ability to manufacture and the performance of third-party manufacturers; | |

| ● | our ability to identify license and collaboration partners and to maintain existing relationships; | |

| ● | the performance of our clinical research organizations, clinical trial sponsors, clinical trial investigators and collaboration partners for any clinical trials we conduct; | |

| ● | any outcomes from our review of strategic transactions; and | |

| ● | our ability to successfully implement our strategy. |

Any forward-looking statements that we make in this Form 10-Q speak only as of the date of such statement, and we undertake no obligation to update such statements to reflect events or circumstances after the date of this Form 10-Q. You should also read carefully the factors described in the “Risk Factors” section of the Company’s annual report on Form 10-K for the fiscal year ended October 31, 2019, (as filed with the SEC on December 20, 2019, and amended by Amendment No. 1 thereto on Form 10-K/A filed on January 21, 2020 and by Amendment No. 2 thereto on Form 10-K/A filed on February 28, 2020, as so amended the “2019 Form 10-K/A”) as further supplemented by the risks and uncertainties discussed in Part II, Item 1A. Risk Factors in our Quarterly Report on Form 10-Q for the quarter ended April 30, 2020 (as filed with the SEC on June 11, 2020) to better understand the risks and uncertainties inherent in our business and underlying any forward-looking statements. As a result of these factors, we cannot assure you that the forward-looking statements in this Form 10-Q will prove to be accurate.

This Form 10-Q includes statistical and other industry and market data that we obtained from industry publications and research, surveys and studies conducted by third parties. Industry publications and third-party research, surveys and studies generally indicate that their information has been obtained from sources believed to be reliable, although they do not guarantee the accuracy or completeness of such information. While we believe these industry publications and third-party research, surveys and studies are reliable, we have not independently verified such data.

| 4 |

PART I - FINANCIAL INFORMATION

CONDENSED BALANCE SHEETS

(In thousands, except share and per share data)

July 31, 2020 | October 31, 2019 | |||||||

(Unaudited) | ||||||||

| ASSETS | ||||||||

| Current Assets: | ||||||||

| Cash and cash equivalents | $ | 23,846 | $ | 32,363 | ||||

| Deferred expenses | 1,518 | 2,353 | ||||||

| Deferred offering costs | 644 | - | ||||||

| Prepaid expenses and other current assets | 1,291 | 1,433 | ||||||

| Total current assets | 27,299 | 36,149 | ||||||

| Property and equipment (net of accumulated depreciation) | 3,667 | 4,350 | ||||||

| Intangible assets (net of accumulated amortization) | 3,841 | 4,575 | ||||||

| Operating right-of-use asset (net of accumulated amortization) | 5,030 | - | ||||||

| Other assets | 182 | 183 | ||||||

| Total assets | $ | 40,019 | $ | 45,257 | ||||

| LIABILITIES AND STOCKHOLDERS’ EQUITY | ||||||||

| Current liabilities: | ||||||||

| Accounts payable | $ | 414 | $ | 976 | ||||

| Accrued expenses | 1,826 | 3,478 | ||||||

| Common stock warrant liability | 33 | 19 | ||||||

| Current portion of operating lease liability | 926 | - | ||||||

| Other current liabilities | 50 | 48 | ||||||

| Total current liabilities | 3,249 | 4,521 | ||||||

| Operating lease liability, net of current portion | 5,304 | - | ||||||

| Other liabilities | - | 1,205 | ||||||

| Total liabilities | 8,553 | 5,726 | ||||||

| Commitments and contingencies – Note 9 | ||||||||

| Stockholders’ equity: | ||||||||

| Preferred stock, $0.001 par value; 5,000,000 shares authorized; Series B Preferred Stock; 0 shares issued and outstanding at July 31, 2020 and October 31, 2019; Liquidation preference of $0 at July 31, 2020 and October 31, 2019 | - | - | ||||||

| Common stock - $0.001 par value; 170,000,000 shares authorized, 62,714,946 and 50,201,671 shares issued and outstanding at July 31, 2020 and October 31, 2019, respectively | 62 | 50 | ||||||

| Additional paid-in capital | 435,682 | 423,750 | ||||||

| Accumulated deficit | (404,278 | ) | (384,269 | ) | ||||

| Total stockholders’ equity | 31,466 | 39,531 | ||||||

| Total liabilities and stockholders’ equity | $ | 40,019 | $ | 45,257 |

The accompanying notes should be read in conjunction with the financial statements.

| 5 |

CONDENSED STATEMENTS OF OPERATIONS (Unaudited)

(In thousands, except share and per share data)

| Three Months Ended July 31, | Nine months ended July 31, | |||||||||||||||

| 2020 | 2019 | 2020 | 2019 | |||||||||||||

| Revenue | $ | - | $ | 6 | $ | 253 | $ | 20,883 | ||||||||

| Operating expenses: | ||||||||||||||||

| Research and development expenses | 3,458 | 7,060 | 12,239 | 19,735 | ||||||||||||

| General and administrative expenses | 2,384 | 3,076 | 8,063 | 8,834 | ||||||||||||

| Total operating expenses | 5,842 | 10,136 | 20,302 | 28,569 | ||||||||||||

| Loss from operations | (5,842 | ) | (10,130 | ) | (20,049 | ) | (7,686 | ) | ||||||||

| Other income (expense): | ||||||||||||||||

| Interest income, net | 7 | 95 | 108 | 354 | ||||||||||||

| Net changes in fair value of derivative liabilities | 7 | 177 | (16 | ) | 2,572 | |||||||||||

| Loss on shares issued in settlement of warrants | - | - | - | (1,607 | ) | |||||||||||

| Other expense | (1 | ) | - | (2 | ) | (7 | ) | |||||||||

| Net loss before benefit for income taxes | (5,829 | ) | (9,858 | ) | (19,959 | ) | (6,374 | ) | ||||||||

| Income tax expense | - | - | 50 | 50 | ||||||||||||

| Net loss | $ | (5,829 | ) | $ | (9,858 | ) | $ | (20,009 | ) | $ | (6,424 | ) | ||||

| Net loss per common share, basic and diluted | $ | (0.09 | ) | $ | (1.00 | ) | $ | (0.35 | ) | $ | (0.94 | ) | ||||

| Weighted average number of common shares outstanding, basic and diluted | 61,634,031 | 9,870,461 | 57,963,228 | 6,813,494 | ||||||||||||

The accompanying notes should be read in conjunction with the financial statements.

| 6 |

CONDENSED STATEMENTS OF CASH FLOWS (Unaudited)

(In thousands)

| Nine Months Ended July 31, | ||||||||

| 2020 | 2019 | |||||||

| OPERATING ACTIVITIES | ||||||||

| Net loss | $ | (20,009 | ) | $ | (6,424 | ) | ||

| Adjustments to reconcile net loss to net cash used in operating activities: | ||||||||

| Stock compensation | 708 | 1,565 | ||||||

| Employee stock purchase plan expense | 1 | 3 | ||||||

| Loss (gain) on change in value of warrants | 16 | (2,572 | ) | |||||

| Loss on shares issued in settlement of warrants | - | 1,607 | ||||||

| Loss on disposal of property and equipment | - | 290 | ||||||

| Abandonment of intangible assets | 892 | 625 | ||||||

| Depreciation expense | 683 | 848 | ||||||

| Amortization expense of intangible assets | 263 | 290 | ||||||

| Amortization of right-of-use asset | 553 | |||||||

| Change in operating assets and liabilities: | ||||||||

| Accounts receivable | - | 1,664 | ||||||

| Prepaid expenses and other current assets | 977 | (54 | ) | |||||

| Other assets | 1 | - | ||||||

| Accounts payable and accrued expenses | (2,251 | ) | (6,245 | ) | ||||

| Deferred revenue | 50 | (18,665 | ) | |||||

| Operating lease liabilities | (606 | ) | - | |||||

| Other liabilities | - | 39 | ||||||

| Net cash used in operating activities | (18,722 | ) | (27,029 | ) | ||||

| INVESTING ACTIVITIES | ||||||||

| Purchase of property and equipment | - | (54 | ) | |||||

| Proceeds from disposal of property and equipment | - | 8 | ||||||

| Cost of intangible assets | (421 | ) | (845 | ) | ||||

| Net cash used in investing activities | (421 | ) | (891 | ) | ||||

| FINANCING ACTIVITIES | ||||||||

| Net proceeds of issuance of common stock | 10,621 | 24,471 | ||||||

| Warrant exercise | - | 68 | ||||||

| Proceeds from employee stock purchase plan | 5 | 19 | ||||||

| Employee tax withholdings paid on equity awards | (2 | ) | (15 | ) | ||||

| Tax shares sold to pay for employee tax withholdings on equity awards | 2 | 14 | ||||||

| Net cash provided by financing activities | 10,626 | 24,557 | ||||||

| Net decrease in cash and cash equivalents | (8,517 | ) | (3,363 | ) | ||||

| Cash and cash equivalents at beginning of period | 32,363 | 45,118 | ||||||

| Cash and cash equivalents at end of period | $ | 23,846 | $ | 41,755 | ||||

| SUPPLEMENTAL CASH FLOW INFORMATION | ||||||||

| Cash paid for taxes | $ | 50 | $ | 50 | ||||

| SUPPLEMENTAL DISCLOSURE OF NON-CASH AND FINANCING ACTIVITIES | ||||||||

| Shares issued in settlement of warrants | - | 5,462 | ||||||

| Warrant liability reclassified into equity | 2 | 53 | ||||||

| Pre-funded warrant exercises | - | 1 | ||||||

| Commitment fee shares issued for equity line | 644 | - | ||||||

| Amounts accrued for offering costs | 37 | - | ||||||

The accompanying notes should be read in conjunction with the financial statements.

| 7 |

NOTES TO THE CONDENSED FINANCIAL STATEMENTS

(Unaudited)

1. NATURE OF OPERATIONS

Advaxis, Inc. (“Advaxis” or the “Company”) is a clinical-stage biotechnology company focused on the development and commercialization of proprietary Listeria monocytogenes (“Lm”)-based antigen delivery products. The Company is using its Lm platform directed against tumor-specific targets in order to engage the patient’s immune system to destroy tumor cells. Through a license from the University of Pennsylvania, Advaxis has exclusive access to this proprietary formulation of attenuated Lm called Lm TechnologyTM. Advaxis’ proprietary approach is designed to deploy a unique mechanism of action that redirects the immune system to attack cancer in three distinct ways:

| ● | Alerting and training the immune system by activating multiple pathways in Antigen-Presenting Cells (“APCs”) with the equivalent of multiple adjuvants; | |

| ● | Attacking the tumor by generating a strong, cancer-specific T cell response; and | |

| ● | Breaking down tumor protection through suppression of the protective cells in the tumor microenvironment (“TME”) that shields the tumor from the immune system. This enables the activated T cells to begin working to attack the tumor cells. |

Advaxis’ proprietary Lm platform technology has demonstrated clinical activity in several of its programs and has been dosed in over 470 patients across multiple clinical trials and in various tumor types. The Company believes that Lm Technology immunotherapies can complement and address significant unmet needs in the current oncology treatment landscape. Specifically, its product candidates have the potential to work synergistically with other immunotherapies, including checkpoint inhibitors, while having a generally well-tolerated safety profile.

Going Concern and Management’s Plans

The Company has not yet commercialized any human products and the products that are being developed have not generated significant revenue. As a result, the Company has suffered recurring losses and requires significant cash resources to execute its business plans. These losses are expected to continue for an extended period of time. The aforementioned factors raise substantial doubt about the Company’s ability to continue as a going concern within one year from the date of filing. The accompanying financial statements have been prepared on a going concern basis, which contemplates the realization of assets and the satisfaction of liabilities in the normal course of business. The financial statements do not include any adjustments relating to the recoverability and classification of asset amounts or the classification of liabilities that might be necessary should the Company be unable to continue as a going concern within one year after the date the financial statements are issued.

Historically, the Company’s major sources of cash have been comprised of proceeds from various public and private offerings of its common stock, debt financings, clinical collaborations, option and warrant exercises, NOL tax sales, income earned on investments and grants and interest income. From October 2013 through July 31, 2020, the Company raised approximately $305.8 million in gross proceeds ($13.6 million in fiscal year 2020) from various public and private offerings of its common stock.

As of July 31, 2020, the Company had approximately $23.8 million in cash and cash equivalents. Although the Company expects to have sufficient capital to fund its obligations, as they become due, in the ordinary course of business until at least July 2021, the actual amount of cash that it will need to operate is subject to many factors. Over the past several months, the Company has taken steps to obtain additional financing, including the at-the-market (“ATM”) program and the equity line with Lincoln Park Capital. Due to the current state of the Company’s stock price and general market conditions, these programs have not been utilized to the fullest extent, thereby resulting in lower capital availability than anticipated. Management’s plans to mitigate an expected shortfall of capital and to support future operations include obtaining additional funds through partnerships or strategic or financing investors. The Company has reduced its operating expenses to $20.3 million for the nine months ended July 31, 2020 as compared to $28.6 million during the comparable prior period.

| 8 |

The Company recognizes it will need to raise additional capital in order to continue to execute its business plan in the future. There is no assurance that additional financing will be available when needed or that management will be able to obtain financing on terms acceptable to the Company or whether the Company will become profitable and generate positive operating cash flow. If the Company is unable to raise sufficient additional funds, it will have to scale back its operations.

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES AND BASIS OF PRESENTATION

Basis of Presentation/Estimates

The accompanying unaudited interim condensed financial statements and related notes have been prepared in accordance with accounting principles generally accepted in the United States of America (“U.S. GAAP”) for interim financial information, and in accordance with the rules and regulations of the Securities and Exchange Commission (“SEC”) with respect to Form 10-Q and Rule 10-01 of Regulation S-X. Accordingly, they do not include all of the information and footnotes required by U.S. GAAP for complete financial statements and the accompanying unaudited interim condensed balance sheet as of July 31, 2020 has been derived from the Company’s October 31, 2019 audited financial statements. In the opinion of management, the unaudited interim condensed financial statements furnished include all adjustments (consisting of normal recurring accruals) necessary for a fair statement of the results for the interim periods presented.

Operating results for interim periods are not necessarily indicative of the results to be expected for the full year. The preparation of financial statements in accordance with U.S. GAAP requires management to make estimates and assumptions that affect the reported amounts of assets, liabilities, revenues, expenses, and the related disclosures at the date of the financial statements and during the reporting period. Significant estimates include the timelines associated with revenue recognition on upfront payments received, fair value and recoverability of the carrying value of property and equipment and intangible assets, fair value of warrant liability, grant date fair value of options, deferred tax assets and any related valuation allowance and related disclosure of contingent assets and liabilities. On an on-going basis, the Company evaluates its estimates, based on historical experience and on various other assumptions that it believes to be reasonable under the circumstances. Actual results could materially differ from these estimates.

These unaudited interim condensed financial statements should be read in conjunction with the financial statements of the Company as of and for the fiscal year ended October 31, 2019 and notes thereto contained in the Company’s annual report on Form 10-K, as filed with the SEC on December 20, 2019, as amended by Amendment No. 1 thereto on Form 10-K/A filed on January 21, 2020 and by Amendment No. 2 thereto on Form 10-K/A filed on February 28, 2020.

Net Income (Loss) per Share

Basic net income or loss per common share is computed by dividing net income or loss available to common stockholders by the weighted average number of common shares outstanding during the period. Diluted earnings per share give effect to dilutive options, warrants, restricted stock units and other potential common stock outstanding during the period. In the case of a net loss, the impact of the potential common stock resulting from warrants, outstanding stock options and convertible debt are not included in the computation of diluted loss per share, as the effect would be anti-dilutive. In the case of net income, the impact of the potential common stock resulting from these instruments that have intrinsic value are included in the diluted earnings per share. The table sets forth the number of potential shares of common stock that have been excluded from diluted net loss per share (as of July 31, 2020, 327,338 warrants are included in the basic earnings per share computation because the exercise price is $0, and as of July 31, 2019, 13,079,000 pre-funded warrants are included in the basic earnings per share computation because the exercise price is nominal):

| As of July 31, | ||||||||

| 2020 | 2019 | |||||||

| Warrants | 5,070,888 | 18,301,804 | ||||||

| Stock options | 914,577 | 405,372 | ||||||

| Restricted stock units | 5,818 | 16,204 | ||||||

| Total | 5,991,283 | 18,723,380 | ||||||

| 9 |

Leases

Effective November 1, 2019, the Company adopted ASC Topic 842, Leases (“ASC 842”) using the modified retrospective transition approach by applying the new standard to all leases existing as of the date of initial application. Results and disclosure requirements for reporting periods beginning after November 1, 2019 are presented under ASC 842, while prior period amounts have not been adjusted and continue to be reported in accordance with the previous guidance in ASC 840, Leases.

At the inception of an arrangement, the Company determines whether an arrangement is or contains a lease based on the facts and circumstances present in the arrangement. An arrangement is or contains a lease if the arrangement conveys the right to control the use of an identified asset for a period of time in exchange for consideration. Most leases with a term greater than one year are recognized on the balance sheet as operating lease right-of-use assets and current and long-term operating lease liabilities, as applicable. The Company has elected not to recognize on the balance sheet leases with terms of 12 months or less. The Company typically only includes the initial lease term in its assessment of a lease arrangement. Options to extend a lease are not included in the Company’s assessment unless there is reasonable certainty that the Company will renew.

Operating lease liabilities and their corresponding right-of-use assets are recorded based on the present value of lease payments over the expected remaining lease term. Certain adjustments to the right-of-use asset may be required for items such as prepaid or accrued rent. The interest rate implicit in the Company’s leases is typically not readily determinable. As a result, the Company utilizes its incremental borrowing rate, which reflects the fixed rate at which the Company could borrow on a collateralized basis the amount of the lease payments in the same currency, for a similar term, in a similar economic environment. In transition to ASC 842, the Company utilized the remaining lease term of its leases in determining the appropriate incremental borrowing rates.

Recent Accounting Standards

Recently Adopted Accounting Standards

On November 1, 2019, the Company adopted Accounting Standards Update No. 2016-02, Leases (Topic 842) (ASU 2016-02), as amended, which establishes ASC 842 and supersedes the lease accounting guidance under ASC 840, and generally requires lessees to recognize operating and financing lease liabilities and corresponding right-of-use (ROU) assets on the balance sheet and to provide enhanced disclosures surrounding the amount, timing and uncertainty of cash flows arising from leasing arrangements. We adopted the new guidance using the modified retrospective transition approach by applying the new standard to all leases existing at the date of initial application and not restating comparative periods.

In adopting the new standard, the Company elected to utilize the available package of practical expedients permitted under the transition guidance within the new standard, which does not require the reassessment of the following: (i) whether existing or expired arrangements are or contain a lease, (ii) the lease classification of existing or expired leases, and (iii) whether previous initial direct costs would qualify for capitalization under the new lease standard. Additionally, the Company elected to combine lease and non-lease components and to exclude leases with a term of 12 months or less.

As of the November 1, 2019 effective date, the Company had identified one operating lease arrangement and one short-term lease in which it is a lessee. The adoption of ASC 842 resulted in the recognition of an operating lease liability and a right-of-use asset of approximately $6.8 million and $5.6 million, respectively, on the Company’s balance sheet relating to its leases, with the difference relating to reclassifications of the current accrued rent liability and the current lease incentive obligation of approximately $0.9 million and $0.3 million, respectively, as reductions to the right-of-use-asset for its operating lease. The adoption of the standard did not have a material effect on the Company’s condensed statements of operations or condensed statements of cash flows.

Management does not believe that any other recently issued, but not yet effective accounting pronouncements, if adopted, would have a material impact on the accompanying condensed financial statements.

| 10 |

3. PROPERTY AND EQUIPMENT

Property and equipment, net consists of the following (in thousands):

| July 31, 2020 | October 31, 2019 | |||||||

| Leasehold improvements | $ | 2,335 | $ | 2,335 | ||||

| Laboratory equipment | 3,405 | 3,405 | ||||||

| Furniture and fixtures | 744 | 744 | ||||||

| Computer equipment | 409 | 409 | ||||||

| Construction in progress | 83 | 83 | ||||||

| Total property and equipment | 6,976 | 6,976 | ||||||

| Accumulated depreciation and amortization | (3,309 | ) | (2,626 | ) | ||||

| Net property and equipment | $ | 3,667 | $ | 4,350 | ||||

Depreciation expense for the three months ended July 31, 2020 and 2019 was $0.2 million and $0.3 million, respectively. Depreciation expense for the nine months ended July 31, 2020 and 2019 was $0.7 million and $0.8 million, respectively.

4. INTANGIBLE ASSETS

Intangible assets, net consist of the following (in thousands):

| July 31, 2020 | October 31, 2019 | |||||||

| Patents | $ | 5,208 | $ | 5,833 | ||||

| Licenses | 777 | 777 | ||||||

| Software | 117 | 117 | ||||||

| Total intangibles | 6,102 | 6,727 | ||||||

| Accumulated amortization | (2,261 | ) | (2,152 | ) | ||||

| Intangible assets | $ | 3,841 | $ | 4,575 | ||||

The expirations of the existing patents range from 2020 to 2040 but the expirations can be extended based on market approval if granted and/or based on existing laws and regulations. Capitalized costs associated with patent applications that are abandoned without future value are charged to expense when the determination is made not to pursue the application. Patent applications having a net book value of $0.3 million were abandoned and were charged to research and development expenses in the statement of operations for each of the three months ended July 31, 2020 and 2019, respectively. Patent applications having a net book value of $0.9 million and $0.6 million were abandoned and were charged to research and development expenses in the statement of operations for the nine months ended July 31, 2020 and 2019, respectively. Amortization expense for intangible assets that was charged to general and administrative expense in the statement of operations aggregated $0.1 million for each of the three months ended July 31, 2020 and 2019, respectively. Amortization expense for intangible assets that was charged to general and administrative expense in the statement of operations aggregated $0.3 million for each of the nine months ended July 31, 2020 and 2019, respectively.

Management has reviewed its long-lived assets for impairment whenever events and circumstances indicate that the carrying value of an asset might not be recoverable. Net assets are recorded on the balance sheet for patents and licenses related to axalimogene filolisbac (AXAL), ADXS-HOT, ADXS-PSA and ADXS-HER2 and other products that are in development. However, if a competitor were to gain FDA approval for a treatment before us or if future clinical trials fail to meet the targeted endpoints, the Company would likely record an impairment related to these assets. In addition, if an application is rejected or fails to be issued, the Company would record an impairment of its estimated book value. Lastly, if the Company is unable to raise enough capital to continue funding its studies and developing its intellectual property, the Company would likely record an impairment to these assets.

| 11 |

At July 31, 2020, the estimated amortization expense by fiscal year based on the current carrying value of intangible assets is as follows (in thousands):

| Fiscal year ending October 31, | ||||

| 2020 (Remaining) | $ | 79 | ||

| 2021 | 309 | |||

| 2022 | 309 | |||

| 2023 | 309 | |||

| 2024 | 309 | |||

| Thereafter | 2,526 | |||

| Total | $ | 3,841 | ||

5. ACCRUED EXPENSES:

| July 31, 2020 | October 31, 2019 | |||||||

| Salaries and other compensation | $ | 743 | $ | 158 | ||||

| Vendors | 604 | 3,194 | ||||||

| Professional fees | 479 | 126 | ||||||

| Total accrued expenses | $ | 1,826 | $ | 3,478 | ||||

6. COMMON STOCK PURCHASE WARRANTS AND WARRANT LIABILITY

Warrants

As of July 31, 2020, there were outstanding warrants to purchase 5,398,226 shares of our common stock with exercise prices ranging from $0 to $281.25 per share. Information on the outstanding warrants is as follows:

| Exercise Price | Number of Shares Underlying Warrants | Expiration Date | Type of Financing | |||||||

| $ | - | 327,338 | July 2024 | July 2019 Public Offering | ||||||

| $ | 281.25 | 25 | N/A | Other warrants | ||||||

| $ | 0.372 | 70,863 | September 2024 | September 2018 Public Offering | ||||||

| $ | 1.25 | 5,000,000 | July 2025 | January 2020 Public Offering | ||||||

| Grand Total | 5,398,226 | |||||||||

As of October 31, 2019, there were outstanding warrants to purchase 432,142 shares of our common stock with exercise prices ranging from $0 to $281.25 per share. Information on the outstanding warrants is as follows:

| Exercise Price | Number of Shares Underlying Warrants | Expiration Date | Type of Financing | |||||||

| $ | - | 359,838 | July 2024 | July 2019 Public Offering | ||||||

| $ | 281.25 | 25 | N/A | Other Warrants | ||||||

| $ | 0.372 | 72,279 | September 2024 | September 2018 Public Offering | ||||||

| Grand Total | 432,142 | |||||||||

| 12 |

A summary of warrant activity was as follows (in thousands, except share and per share data):

| Shares | Weighted Average Exercise Price | Weighted Average Remaining Contractual Life In Years | Aggregate Intrinsic Value | |||||||||||||

| Outstanding and exercisable warrants at October 31, 2019 | 432,142 | $ | 0.08 | 4.76 | $ | 114,069 | ||||||||||

| Issued | 5,000,000 | 1.25 | ||||||||||||||

| Exercised * | (33,916 | ) | 0.02 | |||||||||||||

| Outstanding and exercisable warrants at July 31, 2020 | 5,398,226 | $ | 1.16 | 4.90 | $ | 204,596 | ||||||||||

* Includes the cashless exercise of 32,500 warrants that resulted in the issuance of 32,500 shares of common stock.

As of July 31, 2020, the Company had 5,327,363 of its total 5,398,226 outstanding warrants classified as equity (equity warrants). At October 31, 2019, the Company had 359,863 of its total 432,142 outstanding warrants classified as equity (equity warrants). At issuance, equity warrants are recorded at their relative fair values, using the relative fair value method, in the stockholders’ equity section of the balance sheet.

Warrant Liability

As of July 31, 2020, the Company had 70,863 of its total 5,398,226 outstanding warrants classified as liabilities (liability warrants). At October 31, 2019, the Company had 72,279 of its total 432,142 outstanding warrants classified as liabilities (liability warrants). These warrants contain a down round feature, except for exempt issuances as defined in the warrant agreement, in which the exercise price would immediately be reduced to match a dilutive issuance of common stock, options, convertible securities and changes in option price or rate of conversion. As of July 31, 2020, the down round feature was triggered three times and the exercise price of the warrants were reduced from $22.50 to $0.372. The warrants require liability classification as the warrant agreement requires the Company to maintain an effective registration statement and does not specify any circumstances under which settlement in other than cash would be permitted or required. As a result, net cash settlement is assumed and liability classification is warranted. For these liability warrants, the Company utilized the Monte Carlo simulation model to calculate the fair value of these warrants at issuance and at each subsequent reporting date.

In measuring the warrant liability at July 31, 2020 and October 31, 2019, the Company used the following inputs in its Monte Carlo simulation model:

| July 31, 2020 | October 31, 2019 | |||||||

| Exercise Price | $ | 0.372 | $ | 0.372 | ||||

| Stock Price | $ | 0.58 | $ | 0.32 | ||||

| Expected Term | 4.12 years | 4.87 years | ||||||

| Volatility % | 104.47 | % | 100.99 | % | ||||

| Risk Free Rate | 0.16 | % | 1.51 | % | ||||

7. SHARE BASED COMPENSATION

The following table summarizes share-based compensation expense included in the condensed statement of operations (in thousands):

| Three Months Ended July 31, | Nine Months Ended July 31, | |||||||||||||||

| 2020 | 2019 | 2020 | 2019 | |||||||||||||

| Research and development | $ | 79 | $ | 241 | $ | 233 | $ | 822 | ||||||||

| General and administrative | 176 | 223 | 475 | 743 | ||||||||||||

| Total | $ | 255 | $ | 464 | $ | 708 | $ | 1,565 | ||||||||

| 13 |

Restricted Stock Units (RSUs)

A summary of the Company’s RSU activity and related information for the nine months ended July 31, 2020 is as follows:

| Number of RSUs | Weighted-Average Grant Date Fair Value | |||||||

| Balance at October 31, 2019 | 14,706 | $ | 47.62 | |||||

| Vested | (8,608 | ) | 59.61 | |||||

| Cancelled | (280 | ) | 98.80 | |||||

| Balance at July 31, 2020 | 5,818 | $ | 27.40 | |||||

As of July 31, 2020, there was approximately $0.1 million of unrecognized compensation cost related to non-vested RSUs, which is expected to be recognized over a remaining weighted average vesting period of approximately 0.72 years.

As of July 31, 2020, the aggregate intrinsic value of non-vested RSU’s was approximately $3,000.

Employee Stock Awards

Common Stock issued to executives and employees related to vested incentive retention awards, employment inducements, management purchases and employee excellence awards totaled 0 shares and 408 shares during the three months ended July 31, 2020 and 2019, respectively. Total stock compensation expense associated with employee awards for the three months ended July 31, 2020 and 2019 was approximately $40,000 and $0.2 million, respectively

Common Stock issued to executives and employees related to vested incentive retention awards, employment inducements, management purchases and employee excellence awards totaled 8,608 shares and 10,947 shares during the nine months ended July 31, 2020 and 2019, respectively. Total stock compensation expense associated with employee awards for the nine months ended July 31, 2020 and 2019 was approximately $0.1 million and $0.7 million, respectively.

Stock Options

A summary of changes in the stock option plan for the nine months ended July 31, 2020 is as follows:

| Number of Options | Weighted-Average Exercise Price | |||||||

| Outstanding at October 31, 2019: | 560,490 | $ | 71.56 | |||||

| Granted | 450,000 | 0.66 | ||||||

| Canceled or expired | (95,913 | ) | 58.21 | |||||

| Outstanding at July 31, 2020 | 914,577 | 38.08 | ||||||

| Vested and Exercisable at July 31, 2020 | 266,380 | $ | 125.14 | |||||

During the nine months end July 31, 2020, the Company granted options to purchase 385,000 and 65,000 shares of its common stock to employees and directors, respectively. The stock options have a ten-year term, vest over three years, and have an exercise price of $0.66.

Total compensation cost related to the Company’s outstanding stock options, recognized in the statement of operations for the three months ended July 31, 2020 and 2019 was approximately $0.2 million and $0.3 million, respectively. For the nine months ended July 31, 2020 and 2019, compensation cost related to the Company’s outstanding stock options was approximately $0.6 million and $0.9 million, respectively.

As of July 31, 2020, there was approximately $0.8 million of unrecognized compensation cost related to non-vested stock option awards, which is expected to be recognized over a remaining weighted average vesting period of 1.37 years.

| 14 |

As of July 31, 2020, the aggregate intrinsic value of vested and exercisable options was $0 and the aggregate intrinsic value of non-vested options was approximately $42,000.

In determining the fair value of the stock options granted during the nine months ended July 31, 2020, the Company used the following inputs in its Black Scholes Merton model:

Nine Months Ended | ||||

| Expected Term | 5.50-6.50 years | |||

| Expected Volatility | 100.27-105.21 | % | ||

| Expected Dividends | 0 | % | ||

| Risk Free Interest Rate | 0.36-0.52 | % | ||

Employee Stock Purchase Plan

During the nine months ended July 31, 2020 and 2019, the Company issued 11,148 and 4,585 shares, respectively, that were purchased under the 2018 Employee Stock Purchase Plan (“ESPP”).

8. COLLABORATION AND LICENSING AGREEMENTS

OS Therapies LLC

On September 4, 2018, the Company entered into a development, license and supply agreement with OS Therapies (“OST”) for the use of ADXS31-164, also known as ADXS-HER2, for evaluation in the treatment of osteosarcoma in humans. Under the terms of the license agreement, as amended, OST will be responsible for the conduct and funding of a clinical study evaluating ADXS-HER2 in recurrent, completely resected osteosarcoma. Under the most recent amendment to the licensing agreement, OST agrees to pay Advaxis $25,000 per month (“Monthly Payment”) starting on April 30, 2020 until it achieves its funding milestone of $2,337,500. Upon receipt of the first Monthly Payment, Advaxis will initiate the transfer of the intellectual property and licensing rights of ADXS31-164, which were licensed pursuant to the Penn Agreement, back to the University of Pennsylvania. Contemporaneously, OST will enter negotiations with the University of Pennsylvania to establish a licensing agreement for ADXS31-164 to OST for clinical and commercial development of the ADXS31-164 technology.

Provided that OST meets its ongoing obligation to make its Monthly Payments to Advaxis for six consecutive months, Advaxis agrees to transfer, and OST agrees to take full ownership of, the IND application for ADXS31-164 in its entirety to OST, along with agreements and promises contained therein, as well as all obligations associated with this IND or any HER2 product/program development. Until OST makes its Monthly Payments to Advaxis for six consecutive months, Advaxis will continue to bear the costs of the regulatory filing services related to the IND application for ADXS31-164.

Within five business days of achieving the funding milestone of $2,337,500 for the performance of the Children’s Oncology Group study (knowns as the “License Commencement Date”), OST will make a non-refundable and non-creditable payment to Advaxis of $1,550,000 less the cumulative Monthly Payments previously made (the “License Commencement Payment”). Within five days following the License Commencement Date, Advaxis will provide existing drug supply “as is” to OST, and until the drug supply is supplied to OST, Advaxis will bear the storage costs for the drug product. Pursuant to the agreement, the Company is also to receive sales-based milestone payments and royalties on future product sales. In addition, the Company and OST will establish a Joint Steering Committee to oversee the R&D activities.

The promises to (1) Maintain the HER2 product until transfer to OST, (2) Provide the IND application ownership for ADX321-164 to OST, (3) Participate in the Joint Steering Committee, (4) Transfer of IP & licensing rights of ADXS31-164 and related Patents, and (5) Provide Clinical Drug Supply represent one combined performance obligation for revenue recognition purposes. The Company concluded that the transfer of the IP and licensing rights provides OST with a functional, or “right to use,” license, and thus the Company will recognize the upfront fees of $1,550,000 from the license at a point in time. The revenue from the transfer of the license cannot be recognized until the transfer of the corresponding IP to OST has occurred and OST has the ability to benefit from the right to use the license. As the right to use the license begins when OST makes the upfront payment within five days of the License Commencement Date and the IP transfers to OST at that time, the upfront fees from the license will be recognized upon the transfer of the intellectual property to OST.

Since OST is making $25,000 monthly payments that will be creditable against the $1,550,000, the Company will receive payments prior to the performance of the single distinct performance obligation. Due to this, the Company will defer any of the monthly payments until the IP and licensing rights are transferred to OST. However, if OST terminates the contract, which they are able to do with 60-day notice, the Company would recognize any of the $25,000 monthly payments received when the contract terminates. As of July 31, 2020, OST has made payments totaling $50,000 and this has been recorded as other liabilities in the condensed balance sheet.

Elanco Animal Health (formerly Aratana Therapeutics)

During the fiscal year ended October 31, 2018, the USDA’s Center for Veterinary Biologics granted Aratana conditional approval for its canine osteosarcoma vaccine using Advaxis’ technology. During the three months ended July 31, 2020 and 2019, Advaxis recognized royalty revenue totaling $0 and $6,000, respectively, from Aratana’s sales of the canine osteosarcoma vaccine. During the nine months ended July 31, 2020 and 2019, Advaxis recognized royalty revenue totaling approximately $3,000 and $8,000, respectively, from Aratana’s sales of the canine osteosarcoma vaccine. On July 16, 2019, Aratana announced their shareholders approved a merger agreement with Elanco Animal Health (“Elanco”) whereby Elanco will be the majority shareholder of Aratana. All of the terms of the Aratana Agreement remain in effect.

Global BioPharma Inc.

On December 9, 2013, the Company entered into an exclusive licensing agreement for the development and commercialization of axalimogene filolisbac with Global BioPharma, Inc. (“GBP”), a Taiwanese based biotech company funded by a group of investors led by Taiwan Biotech Co., Ltd (TBC). During each of the nine months ended July 31, 2020 and 2019, the Company recorded $0.3 million in revenue for the annual license fee renewal. Since Advaxis has no significant obligation to perform after the license transfer and has provided GBP with the right to use its intellectual property, performance is satisfied when the license renews.

| 15 |

9. COMMITMENTS AND CONTINGENCIES

Legal Proceedings

Stendhal

On September 19, 2018, Stendhal filed a Demand for Arbitration before the International Centre for Dispute Resolution (Case No. 01-18-0003-5013) relating to the Co-development and Commercialization Agreement with Especificos Stendhal SA de CV (the “Stendhal Agreement”). In the demand, Stendhal alleged that (i) the Company breached the Stendhal Agreement when it made certain statements regarding its AIM2CERV program, (ii) that Stendhal was subsequently entitled to terminate the Agreement for cause, which it did so at the time and (iii) that the Company owes Stendhal damages pursuant to the terms of the Stendhal Agreement. Stendhal is seeking to recover $3 million paid to the Company in 2017 as support payments for the AIM2CERV clinical trial along with approximately $0.3 million in expenses incurred. Stendhal is also seeking fees associated with the arbitration and interest. The Company has answered Stendhal’s Demand for Arbitration and denied that it breached the Stendhal Agreement. The Company also alleges that Stendhal breached its obligations to the Company by, among other things, failing to make support payments that became due in 2018 and that Stendhal therefore owes the Company $3 million. Advaxis is also seeking fees associated with the arbitration and interest.

From October 21-23, 2019, an evidentiary hearing for the arbitration was conducted. On April 1, 2020, the Arbitrator issued a final award denying Stendhal’s claim in full. The Arbitrator found that the Company had not repudiated the Agreement and did not owe Stendhal damages, fees, or interest associated with the arbitration. The Arbitrator also denied the Company’s claim that Stendhal breached its obligations to the Company. The parties were ordered to bear their own attorneys’ fees and evenly split administrative fees and expenses for the arbitration.

10. LEASES

Operating Leases

The Company leases its corporate office and manufacturing facility in Princeton, New Jersey under an operating lease that expires in November 2025. The Company has the option to renew the lease term for two additional five-year terms. The renewal periods were not included the lease term for purposes of determining the lease liability or right-of-use asset. The Company has provided a security deposit of approximately $182,000, which is recorded as Other Assets in the condensed balance sheet.

The Company identified and assessed the following significant assumptions in recognizing its right-of-use assets and corresponding lease liabilities:

| ● | As the Company does not have sufficient insight to determine an implicit rate, the Company estimated the incremental borrowing rate in calculating the present value of the lease payments. The Company utilized a synthetic credit rating model to determine a benchmark for its incremental borrowing rate for its leases. The benchmark rate was adjusted to arrive at an appropriate discount rate for the lease. | |

| ● | Since the Company elected to account for each lease component and its associated non-lease components as a single combined component, all contract consideration was allocated to the combined lease component. | |

| ● | Renewal option periods have not been included in the determination of the lease terms as they are not deemed reasonably certain of exercise. | |

| ● | Variable lease payments, such as common area maintenance, real estate taxes, and property insurance are not included in the determination of the lease’s right-of-use asset or lease liability. |

| 16 |

Supplemental balance sheet information related to leases as of July 31, 2020 was as follows (in thousands):

| Operating Leases: | ||||

| Operating lease right-of-use assets | $ | 5,030 | ||

| Operating lease liability | $ | 926 | ||

| Operating lease liability, net of current portion | 5,304 | |||

| Total operating lease liabilities | $ | 6,230 |

Supplemental lease expense related to leases was as follows (in thousands):

| Lease Cost (in thousands) | Statements of Operations Classification | For the Three Months Ended July 31, 2020 | For the Nine Months Ended July 31, 2020 | |||||||

| Operating lease cost | General and administrative | 290 | 869 | |||||||

| Short-term lease cost | General and administrative | 83 | 249 | |||||||

| Variable lease cost | General and administrative | $ | 108 | $ | 282 | |||||

| Total lease expense | $ | 481 | $ | 1,400 | ||||||

Other information related to leases where the Company is the lessee is as follows:

| For the Nine Months Ended July 31, 2020 | ||||

| Weighted-average remaining lease term | 5.3 years | |||

| Weighted-average discount rate | 6.5 | % | ||

Supplemental cash flow information related to operating leases was as follows:

| For the Three Months Ended July 31, 2020 | For the Nine Months Ended July 31, 2020 | |||||||

| Cash paid for operating lease liabilities | $ | 311 | $ | 922 | ||||

Future minimum lease payments under non-cancellable leases as of July 31, 2020 were as follows:

| Fiscal Year ending October 31, | ||||

| 2020 (Remaining) | $ | 311 | ||

| 2021 | 1,318 | |||

| 2022 | 1,369 | |||

| 2023 | 1,395 | |||

| 2024 | 1,419 | |||

| Thereafter | 1,564 | |||

| Total minimum lease payments | 7,376 | |||

| Less: Imputed interest | (1,146 | ) | ||

| Total | $ | 6,230 | ||

Under ASC 840, future minimum payments under the Company’s operating lease were as follows (in thousands):

| Fiscal Year ending October 31, | ||||

| 2020 | $ | 1,233 | ||

| 2021 | 1,318 | |||

| 2022 | 1,369 | |||

| 2023 | 1,395 | |||

| 2024 | 1,419 | |||

| Thereafter | 1,564 | |||

| Total | $ | 8,298 | ||

Under ASC 840, rent expense for each of the years ended October 31, 2019 and 2018 was approximately $1.2 million.

| 17 |

11. STOCKHOLDERS’ EQUITY

A summary of the changes in stockholders’ equity for the three and nine months ended July 31, 2020 and 2019 is presented below (in thousands, except share data):

| Preferred Stock | Common Stock | Additional Paid-In | Accumulated | Total Shareholders’ | ||||||||||||||||||||||||

| Shares | Amount | Shares | Amount | Capital | Deficit | Equity | ||||||||||||||||||||||

| Balance at November 1, 2018 | - | $ | - | 4,634,189 | $ | 5 | $ | 391,703 | $ | (367,657 | ) | $ | 24,051 | |||||||||||||||

| Stock based compensation | - | - | 9,811 | - | 622 | - | 622 | |||||||||||||||||||||

| Tax withholdings paid on equity awards | - | - | - | - | (11 | ) | - | (11 | ) | |||||||||||||||||||

| Tax shares sold to pay for tax withholdings on equity awards | - | - | - | - | 11 | - | 11 | |||||||||||||||||||||

| Issuance of shares to employees under ESPP Plan | - | - | 2,007 | - | 9 | - | 9 | |||||||||||||||||||||

| ESPP Expense | - | - | - | - | 1 | 1 | ||||||||||||||||||||||

| Net Income | - | - | - | - | 12,817 | 12,817 | ||||||||||||||||||||||

| Balance at January 31, 2019 | - | $ | - | 4,646,007 | $ | 5 | $ | 392,335 | $ | (354,840 | ) | $ | 37,500 | |||||||||||||||

| Stock based compensation | - | - | 693 | - | 479 | - | 479 | |||||||||||||||||||||

| Tax withholdings paid on equity awards | - | - | - | - | (3 | ) | - | (3 | ) | |||||||||||||||||||

| Tax shares sold to pay for tax withholdings on equity awards | - | - | - | - | 3 | - | 3 | |||||||||||||||||||||

| Issuance of shares to employees under ESPP Plan | - | - | 1,505 | - | 7 | - | 7 | |||||||||||||||||||||

| Warrant exercises | - | - | 15,300 | - | 68 | - | 68 | |||||||||||||||||||||

| Warrant liability reclassified into equity | - | - | - | - | 53 | - | 53 | |||||||||||||||||||||

| ESPP Expense | - | - | - | - | 1 | 1 | ||||||||||||||||||||||

| Shares issued in settlement of warrants | - | - | 856,865 | 1 | 5,462 | - | 5,463 | |||||||||||||||||||||

| Advaxis public offerings, net of offering costs | - | - | 2,500,000 | 2 | 8,980 | - | 8,982 | |||||||||||||||||||||

| Net Loss | - | - | - | - | - | (9,383 | ) | (9,383 | ) | |||||||||||||||||||

| Balance at April 30, 2019 | - | $ | - | 8,020,370 | $ | 8 | $ | 407,385 | $ | (364,223 | ) | $ | 43,170 | |||||||||||||||

| Stock based compensation | 408 | - | 464 | - | 464 | |||||||||||||||||||||||

| Tax withholdings paid on equity awards | - | - | - | - | 1 | - | (1 | ) | ||||||||||||||||||||

| Tax shares sold to pay for tax withholdings on equity awards | - | - | - | - | (1 | ) | - | 1 | ||||||||||||||||||||

| Issuance of shares to employees under ESPP Plan | - | - | 1,073 | - | 3 | - | 3 | |||||||||||||||||||||

| Shares issued in settlement of warrants | - | - | 577,000 | 1 | - | - | 1 | |||||||||||||||||||||

| Advaxis public offerings, net of offering costs | - | - | 10,650,000 | 11 | 15,478 | - | 15,489 | |||||||||||||||||||||

| Net Loss | - | - | - | - | - | (9,858 | ) | (9,858 | ) | |||||||||||||||||||

| Balance at July 31, 2019 | - | $ | - | 19,248,851 | $ | 20 | $ | 423,330 | $ | (374,081 | ) | $ | 49,269 | |||||||||||||||

| 18 |

| Preferred Stock | Common Stock | Additional Paid-In | Accumulated | Total Shareholders’ | ||||||||||||||||||||||||

| Shares | Amount | Shares | Amount | Capital | Deficit | Equity | ||||||||||||||||||||||

| Balance at November 1, 2019 | - | $ | - | 50,201,671 | $ | 50 | $ | 423,750 | $ | (384,269 | ) | $ | 39,531 | |||||||||||||||

| Stock based compensation | - | - | 2,957 | - | 242 | - | 242 | |||||||||||||||||||||

| Advaxis public offerings, net of offering costs | - | - | 10,000,000 | 10 | 9,618 | - | 9,628 | |||||||||||||||||||||

| Warrant exercises | - | - | 26,416 | - | 2 | - | 2 | |||||||||||||||||||||

| Issuance of shares to employees under ESPP Plan | - | - | 5,555 | - | 2 | - | 2 | |||||||||||||||||||||

| Net Income | - | - | - | - | - | (7,857 | ) | (7,857 | ) | |||||||||||||||||||

| Balance at January 31, 2020 | - | $ | - | 60,236,599 | $ | 60 | $ | 433,614 | $ | (392,126 | ) | $ | 41,548 | |||||||||||||||

| Stock based compensation | - | - | 5,651 | - | 210 | - | 210 | |||||||||||||||||||||

| Warrant exercises | - | - | 7,500 | - | - | - | - | |||||||||||||||||||||

| Issuance of shares to employees under ESPP Plan | - | - | 2,694 | - | 2 | - | 2 | |||||||||||||||||||||

| Net Income | - | - | - | - | - | (6,323 | ) | (6,323 | ) | |||||||||||||||||||

| Balance at April 30, 2020 | - | $ | - | 60,252,444 | $ | 60 | $ | 433,826 | $ | (398,449 | ) | $ | 35,437 | |||||||||||||||

| Stock based compensation | - | - | - | - | 255 | - | 255 | |||||||||||||||||||||

| Tax withholdings paid on equity awards | - | - | - | - | (1 | ) | - | (1 | ) | |||||||||||||||||||

| Tax shares sold to pay for tax withholdings on equity awards | - | - | - | - | 1 | - | 1 | |||||||||||||||||||||

| Issuance of shares to employees under ESPP Plan | - | - | 2,899 | - | 2 | - | 2 | |||||||||||||||||||||

| At-the-market shares issued, net of offering costs | - | - | 1,375,337 | 1 | 956 | - | 957 | |||||||||||||||||||||

| Commitment fee shares issued for equity line | - | - | 1,084,266 | 1 | 643 | - | 644 | |||||||||||||||||||||

| Net Income | - | - | - | - | - | (5,829 | ) | (5,829 | ) | |||||||||||||||||||

| Balance at July 31, 2020 | - | $ | - | 62,714,946 | $ | 62 | $ | 435,682 | $ | (404,278 | ) | $ | 31,466 | |||||||||||||||

On February 21, 2019, the Company’s stockholders voted to approve an amendment to the Company’s Amended and Restated Certificate of Incorporation (the “Certificate of Incorporation”) increase the number of authorized shares of common stock from 95,000,000 to 170,000,000 and also voted to approve an amendment to the Certificate of Incorporation allow the Company to execute a reverse stock split of common stock at the discretion of the Board of Directors. The amendment to increase the number of authorized shares of common stock became effective upon filing of the amendment with the Secretary of State of the State of Delaware on February 28, 2019. Additionally, on March 29, 2019, the Company executed a 1 for 15 reverse stock split.

In April 2019, the Company issued 2,500,000 shares of the Company’s common stock in a public offering at $4.00 per share, less underwriting discounts and commissions. The net proceeds to the Company from the transaction was approximately $9 million.

In July 2019, the Company closed on an underwritten public offering of 10,650,000 shares of its common stock, pre-funded warrants to purchase 13,656,000 shares of common stock and warrants to purchase up to 17,142,000 shares of common stock at a public offering price of $1.20, for gross proceeds of $17.0 million. Each share of common stock or pre-funded warrant was sold together in a fixed combination with a warrant to purchase 0.75 shares of common stock. The pre-funded warrants are exercisable immediately, do not expire and have an exercise price of $0.001 per share. The warrants are exercisable immediately, expire five years from the date of issuance, have an exercise price of $2.80 per share and are subject to anti-dilution and other adjustments for certain stock splits, stock dividends, or recapitalizations. The warrants also provide that if during the period of time between the date that is the earlier of (i) 30 days after issuance and (ii) if the common stock trades an aggregate of more than 35,000,000 shares after the pricing of the offering, and ending 15 months after issuance, the weighted-average price of common stock immediately prior to the exercise date is lower than the then-applicable exercise price per share, each Common Warrant may be exercised, at the option of the holder, on a cashless basis for one share of Common Stock. After deducting the underwriting discounts and commissions and other offering expenses, the net proceeds from the offering were approximately $15.5 million.

| 19 |

In January 2020, the Company closed on a public offering of 10,000,000 shares of its common stock at a public offering price of $1.05, for gross proceeds of $10.5 million. In addition, the Company also undertook a concurrent private placement of warrants to purchase up to 5,000,000 shares of common stock. The warrants have an exercise price per share of $1.25, are exercisable during the period beginning on the six-month anniversary of the date of its issuance (the “Initial Exercise Date”) and will expire on the fifth anniversary of the Initial Exercise Date. The warrants contain a change of control provision whereby if the change of control is within the Company’s control, the warrants could be settled in cash based on the Black-Scholes value of the warrants at the option of the warrant holder. The warrants also provide that if there is no effective registration statement registering, or no current prospectus available for, the issuance or resale of the warrant shares, the warrants may be exercised via a cashless exercise. After deducting the underwriting discounts and commissions and other offering expenses, the net proceeds from the offering were approximately $9.6 million.

At the Annual Meeting of Stockholders of the Company held on May 4, 2020, the stockholders ratified and approved an amendment to the Company’s 2015 Incentive Plan to increase the aggregate number of shares of common stock authorized for issuance under such Plan from 877,744 shares to 6,000,000 shares.

In May 2020, the Company entered into a sales agreement related to an ATM equity offering program pursuant to which the Company may sell, from time to time, common stock with an aggregate offering price of up to $40 million through A.G.P./Alliance Global Partners, as sales agent. From May 2020 to July 2020, the Company sold 1,375,337 shares of its common stock under the ATM program for $1.085 million, or an average of $0.79 per share, and received net proceeds of $0.957 million, net of commissions of $35,000.

Lincoln Park Purchase Agreement

On July 30, 2020, the Company entered into a Purchase Agreement (the “Purchase Agreement”) and a Registration Rights Agreement (the “Registration Rights Agreement”) with Lincoln Park Capital Fund, LLC (“Lincoln Park”). Over the 36-month term of the Purchase Agreement, the Company has the right, but not the obligation, from time to time, to sell to Lincoln Park up to an aggregate amount of $20,000,000 of shares of common stock, in its sole discretion and subject to certain conditions, including that the closing price of its common stock is not below $0.10 per share, to direct Lincoln Park to purchase up to 1,000,000 shares (the “Regular Purchase Share Limit”) of its Common Stock (each such purchase, a “Regular Purchase”). Lincoln Park’s maximum obligation under any single Regular Purchase will not exceed $1,000,000, unless the parties mutually agree to increase the maximum amount of such Regular Purchase. The purchase price for shares of Common Stock to be purchased by Lincoln Park under a Regular Purchase will be the equal to the lower of (in each case, subject to the adjustments described in the Purchase Agreement): (i) the lowest sale price for the Company’s common stock on the applicable purchase date, and (ii) the arithmetic average of the three lowest sale prices for the Company’s common stock during the ten trading days prior to the purchase date.

As consideration for entering into the Purchase Agreement, the Company issued 1,084,266 shares of common stock to Lincoln Park as a commitment fee. The shares were valued at approximately $0.6 million and were recorded as deferred offering expenses in the condensed balance sheet. The deferred charges will be charged against paid-in capital upon future proceeds from the sale of common stock under the Lincoln Park Purchase Agreement.

12. FAIR VALUE

The authoritative guidance for fair value measurements defines fair value as the exchange price that would be received for an asset or paid to transfer a liability (an exit price) in the principal or the most advantageous market for the asset or liability in an orderly transaction between market participants on the measurement date. Market participants are buyers and sellers in the principal market that are (i) independent, (ii) knowledgeable, (iii) able to transact, and (iv) willing to transact. The guidance describes a fair value hierarchy based on the levels of inputs, of which the first two are considered observable and the last unobservable, that may be used to measure fair value which are the following:

| 20 |

● Level 1 — Quoted prices in active markets for identical assets or liabilities.

● Level 2— Inputs other than Level 1 that are observable, either directly or indirectly, such as quoted prices for similar assets or liabilities; quoted prices in markets that are not active; or other inputs that are observable or corroborated by observable market data or substantially the full term of the assets or liabilities.

● Level 3 — Unobservable inputs that are supported by little or no market activity and that are significant to the value of the assets or liabilities.

The following table provides the assets and liabilities carried at fair value measured on a recurring basis as of July 31, 2020 and October 31, 2019 (in thousands):

| July 31, 2020 | Level 1 | Level 2 | Level 3 | Total | ||||||||||||

| Common stock warrant liability, warrants exercisable at $0.372 through September 2024 | - | - | $ | 33 | $ | 33 | ||||||||||

| October 31, 2019 | Level 1 | Level 2 | Level 3 | Total | ||||||||||||

| Common stock warrant liability, warrants exercisable at $0.372 through September 2024 | - | - | $ | 19 | $ | 19 | ||||||||||

The following table sets forth a summary of the changes in the fair value of the Company’s warrant liabilities:

For the Ended | ||||

| Beginning balance | $ | 19 | ||

| Warrant exercises | (2 | ) | ||

| Change in fair value | 16 | |||

| Ending Balance | $ | 33 | ||

13. Subsequent Events

On August 3, 2020, Lincoln Park purchased 3,510,527 shares of common stock for gross proceeds of approximately $2 million. The net proceeds to the Company from the transaction was approximately $1.9 million.

On September 4, 2020, the Company and Molly Henderson, Executive Vice President and Chief Financial Officer, announced that Ms. Henderson is stepping down as Chief Financial Officer effective September 25, 2020.

| 21 |

Item 2. Management’s Discussion and Analysis of Financial Condition and Results of Operations

The following discussion and analysis contains forward-looking statements about our plans and expectations of what may happen in the future. Forward-looking statements are based on a number of assumptions and estimates that are inherently subject to significant risks and uncertainties, and our results could differ materially from the results anticipated by our forward-looking statements as a result of many known or unknown factors, including, but not limited to, those factors discussed below in Part II Item 1A. “Risk Factors” of this Form 10-Q. See also the “Special Cautionary Notice Regarding Forward-Looking Statements” set forth at the beginning of this report.

You should read the following discussion and analysis in conjunction with the unaudited financial statements, and the related footnotes thereto, appearing elsewhere in this report, and in conjunction with management’s discussion and analysis and the audited financial statements included in our annual report on Form 10-K for the fiscal year ended October 31, 2019, as filed with the SEC on December 20, 2019, as amended by Amendment No. 1 thereto on Form 10-K/A filed on January 21, 2020 and by Amendment No. 2 thereto on Form 10-K/A filed on February 28, 2020 (the “2019 Form 10-K/A”). In addition, we intend to use our media and investor relations website (www.advaxis.com/investor-relations), SEC filings, press releases, public conference calls and webcasts to communicate with the public about Advaxis, its services and other issues.

Overview

Advaxis, Inc. (“we” or “Advaxis”) is a clinical-stage biotechnology company focused on the development and commercialization of proprietary Listeria monocytogenes (“Lm”)-based antigen delivery products. We are using our Lm platform directed against tumor-specific targets in order to engage the patient’s immune system to destroy tumor cells. Through a license from the University of Pennsylvania, we have exclusive access to this proprietary formulation of attenuated Lm called Lm TechnologyTM. Our proprietary approach is designed to deploy a unique mechanism of action that redirects the immune system to attack cancer in three distinct ways:

| ● | Alerting and training the immune system by activating multiple pathways in Antigen-Presenting Cells (“APCs”) with the equivalent of multiple adjuvants; | |

| ● | Attacking the tumor by generating a strong, cancer-specific T cell response; and | |

| ● | Breaking down tumor protection through suppression of the protective cells in the tumor microenvironment (“TME”) that shields the tumor from the immune system. This enables the activated T cells to begin working to attack the tumor cells. |

Our proprietary Lm platform technology has demonstrated clinical activity in several of our programs and has been dosed in over 470 patients across multiple clinical trials and in various tumor types. We believe that Lm Technology immunotherapies can complement and address significant unmet needs in the current oncology treatment landscape. Specifically, our product candidates have the potential to work synergistically with other immunotherapies, including checkpoint inhibitors, while having a generally well-tolerated safety profile.

Recent Developments

On March 11, 2020, the World Health Organization declared the coronavirus (COVID-19) a pandemic, and on March 13, 2020, the United States declared a national emergency with respect to COVID-19. The pandemic has resulted in government-imposed quarantines, travel restrictions, business and school closures and other public health safety measures, many of which remain in effect to varying degrees. We continue to monitor the COVID-19 pandemic and take steps intended to mitigate the potential risks to our workforce and our operations. The COVID-19 pandemic has, and may continue to, directly or indirectly affect the pace of enrollment in our clinical trials as patients may avoid or may not be able to travel to healthcare facilities and physicians’ offices unless due to a health emergency and clinical trial staff can no longer get to the clinic. Nonetheless, thus far, the COVID-19 pandemic has not had a significant impact on the business. However, we remain in contact with the clinical sites in our study and are in discussion with additional sites to combat any potential impact in enrollment. We are unable to determine or predict the extent, duration or scope of the overall impact of the COVID-19 pandemic on our business, operations, financial condition or liquidity.

| 22 |

Strategic Transactions

As a matter of course, we are reviewing strategic transactions and alternatives and there can be no assurance that we will be successful in identifying or completing any strategic transactions, that any such strategic transaction will result in additional value for our stockholders or that the process will not have an adverse impact on our business. These transactions could include, but are not limited to, collaboration agreements, co-development agreements, strategic mergers, reverse mergers, the issuance or buyback of public shares, or the purchase or sale of specific assets, in addition to other potential actions aimed at increasing stockholder value. There can be no assurance that the review of strategic transactions will result in the identification or consummation of any transaction. Our Board of Directors may also determine that our most effective strategy is to continue to effectuate our current business plan. Any potential transaction would be dependent upon a number of factors that may be beyond our control, including, but not limited to, market conditions, industry trends, the interest of third parties in our business and the availability of financing to potential buyers on reasonable terms. No decision has been made with respect to any transaction.

The Advaxis Corporate Strategy

Our strategy is to advance the Lm Technology platform and leverage its unique capabilities to design and develop an array of cancer treatments. We are currently conducting or have conducted clinical studies of Lm Technology immunotherapies in HPV-associated cancers (including cervical and head and neck), prostate cancer, non-small cell lung cancer and other solid tumor types. We are working with, or are in the process of identifying, collaborators for our programs.

Moving forward, we expect that we will continue to invest in our core clinical program areas and will also remain opportunistic in evaluating Investigator Sponsored Trials (“ISTs”) as well as licensing opportunities. The Lm Technology platform is protected by a range of patents, covering both product and process, some of which we believe can be maintained into 2040.

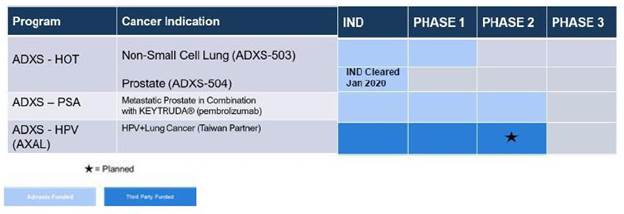

Advaxis Pipeline of Product Candidates

Disease focused hotspot/ ‘off the shelf’ neoantigen therapies (ADXS-HOT)

We are creating a new group of immunotherapy constructs for major solid tumor cancers that combines our optimized Lm Technology vector with promising targets designed to generate potent anti-cancer immunity. The ADXS-HOT program is a series of novel cancer immunotherapies that will target somatic mutations, or hotspots, cancer testis antigens, or CTAs, and oncofetal antigens, or OFAs. These three types of targets form the basis of the ADXS-HOT program because they are designed to be more capable of generating potent, tumor specific, and high strength killer T cells, versus more traditional over-expressed native sequence tumor associated antigens. Most hotspot mutations and OFA/CTA proteins play critical roles in oncogenesis; targeting both at once could significantly impair cancer proliferation. The ADXS-HOT products will combine many of the potential high avidity targets that are expressed in all patients with the target disease into one “off-the-shelf,” ready to administer treatment. We believe the ADXS-HOT technology has a strong intellectual property, or IP, position, with potential protection into 2040, and an IP filing strategy providing for broad coverage opportunities across multiple disease platforms and combination therapies.

| 23 |