UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

(Mark One)

| QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the Quarterly Period Ended September 30, 2024

or

| TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the transition period from to

Commission file number 1-15525

(Exact name of registrant as specified in its charter)

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |||||||||||||

(Address of principal executive offices and zip code)

(949 ) 250-2500

(Registrant's telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||||||

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of "large accelerated filer," "accelerated filer," "smaller reporting company," and "emerging growth company" in Rule 12b-2 of the Exchange Act.

| ☒ | Accelerated filer | ☐ | Non-accelerated filer | ☐ | Smaller reporting company | Emerging growth company | |||||||||||||||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

The number of shares outstanding of the registrant's common stock, $1.00 par value, as of October 31, 2024 was 589.8 million.

EDWARDS LIFESCIENCES CORPORATION

FORM 10-Q

For the quarterly period ended September 30, 2024

TABLE OF CONTENTS

Page Number | ||||||||

Item 6. | ||||||||

NOTE REGARDING FORWARD-LOOKING STATEMENTS

This report contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. We intend the forward-looking statements contained in this report to be covered by the safe harbor provisions of such Acts. Statements other than statements of historical or current fact in this report or referred to or incorporated by reference into this report are "forward-looking statements" for purposes of these safe harbor provisions. These statements can sometimes be identified by the use of the forward-looking words such as "may," "believe," "will," "expect," "project," "estimate," "should," "anticipate," "plan," "goal," "continue," "seek," "pro forma," "forecast," "intend," "guidance," "optimistic," "aspire," "confident," other forms of these words or similar words or expressions or the negatives thereof. Statements regarding past performance, efforts, or results about which inferences or assumptions may be made can also be forward-looking statements and are not indicative of future performance or results; these statements can be identified by the use of words such as "preliminary," "initial," "potential," "possible," "diligence," "industry-leading," "compliant," "indications," or "early feedback" or other forms of these words or similar words or expressions or the negatives thereof. These forward-looking statements are subject to substantial risks and uncertainties that could cause our results or future business, financial condition, results of operations or performance to differ materially from our historical results or experiences or those expressed or implied in any forward-looking statements contained in this report. These risks and uncertainties include, but are not limited to: our ability to complete or realize the anticipated benefits of the sale of our critical care product group; our ability to develop new products and avoid manufacturing and quality issues; risks related to our recent pending acquisitions, including our ability to close the transactions in a timely manner or at all; clinical trial or commercial results or new product approvals and therapy adoption; the impact of domestic and global conditions; competition in the markets in which we operate; our reliance on vendors, suppliers, and other third parties; damage, failure or interruption of our information technology systems; the impact of public health crises; consolidation in the healthcare industry; our ability to protect our intellectual property; our compliance with applicable regulations; our exposure to product liability claims; use of our products in unapproved circumstances; changes to reimbursement for our products; the impact of currency exchange rates; unanticipated actions by the United States Food and Drug Administration and other regulatory agencies; changes to tax laws; unexpected impacts or expenses of litigation or internal or government investigations; and other risks detailed under “Risk Factors” in our annual report on Form 10-K for the year ended December 31, 2023, as amended in this report, and as such risks and uncertainties may be further amended, supplemented or superseded from time to time by our subsequent reports on Forms 10-Q and 8-K we file with the United States Securities and Exchange Commission. These forward-looking statements speak only as of the date on which they are made and we do not undertake any obligation to update any forward-looking statement to reflect events or circumstances after the date of the statement. If we do update or correct one or more of these statements, investors and others should not conclude that we will make additional updates or corrections.

Unless otherwise indicated or otherwise required by the context, the terms "we," "our," "it," "its," "Company," "Edwards," and "Edwards Lifesciences" refer to Edwards Lifesciences Corporation and its subsidiaries.

Part I. Financial Information

Item 1. Financial Statements

EDWARDS LIFESCIENCES CORPORATION

CONSOLIDATED CONDENSED BALANCE SHEETS

(in millions, except par value; unaudited)

| September 30, 2024 | December 31, 2023 | ||||||||||

| ASSETS | |||||||||||

| Current assets | |||||||||||

| Cash and cash equivalents | $ | $ | |||||||||

| Short-term investments (Note 6) | |||||||||||

Accounts receivable, net of allowances of $ | |||||||||||

| Other receivables | |||||||||||

| Inventories (Note 2) | |||||||||||

| Prepaid expenses | |||||||||||

| Other current assets | |||||||||||

| Current assets of discontinued operations (Note 5) | |||||||||||

| Total current assets | |||||||||||

| Long-term investments (Note 6) | |||||||||||

| Property, plant, and equipment, net | |||||||||||

| Operating lease right-of-use assets | |||||||||||

| Goodwill | |||||||||||

| Other intangible assets, net | |||||||||||

| Deferred income taxes | |||||||||||

| Other assets (Note 2) | |||||||||||

| Non-current assets of discontinued operations (Note 5) | |||||||||||

| Total assets | $ | $ | |||||||||

| LIABILITIES AND STOCKHOLDERS' EQUITY | |||||||||||

| Current liabilities | |||||||||||

| Accounts payable | $ | $ | |||||||||

| Accrued and other liabilities (Note 2) | |||||||||||

| Operating lease liabilities | |||||||||||

| Current liabilities of discontinued operations (Note 5) | |||||||||||

| Total current liabilities | |||||||||||

| Long-term debt | |||||||||||

| Taxes payable | |||||||||||

| Operating lease liabilities | |||||||||||

| Uncertain tax positions | |||||||||||

| Litigation settlement accrual | |||||||||||

| Other liabilities | |||||||||||

| Non-current liabilities of discontinued operations (Note 5) | |||||||||||

| Total liabilities | |||||||||||

| Commitments and contingencies (Note 13) | |||||||||||

| Stockholders' equity | |||||||||||

Preferred stock, $ | |||||||||||

Common stock, $ | |||||||||||

| Additional paid-in capital | |||||||||||

| Retained earnings | |||||||||||

| Accumulated other comprehensive loss (Note 14) | ( | ( | |||||||||

Treasury stock, at cost, | ( | ( | |||||||||

| Total Edwards Lifesciences Corporation stockholders' equity | |||||||||||

| Noncontrolling interest | |||||||||||

| Total stockholders' equity | |||||||||||

| Total liabilities and equity | $ | $ | |||||||||

The accompanying notes are an integral part of these consolidated condensed financial statements.

1

EDWARDS LIFESCIENCES CORPORATION

CONSOLIDATED CONDENSED STATEMENTS OF OPERATIONS

(in millions, except per share information; unaudited)

| Three Months Ended September 30, | Nine Months Ended September 30, | ||||||||||||||||||||||

| 2024 | 2023 | 2024 | 2023 | ||||||||||||||||||||

| Net sales | $ | $ | $ | $ | |||||||||||||||||||

| Cost of sales | |||||||||||||||||||||||

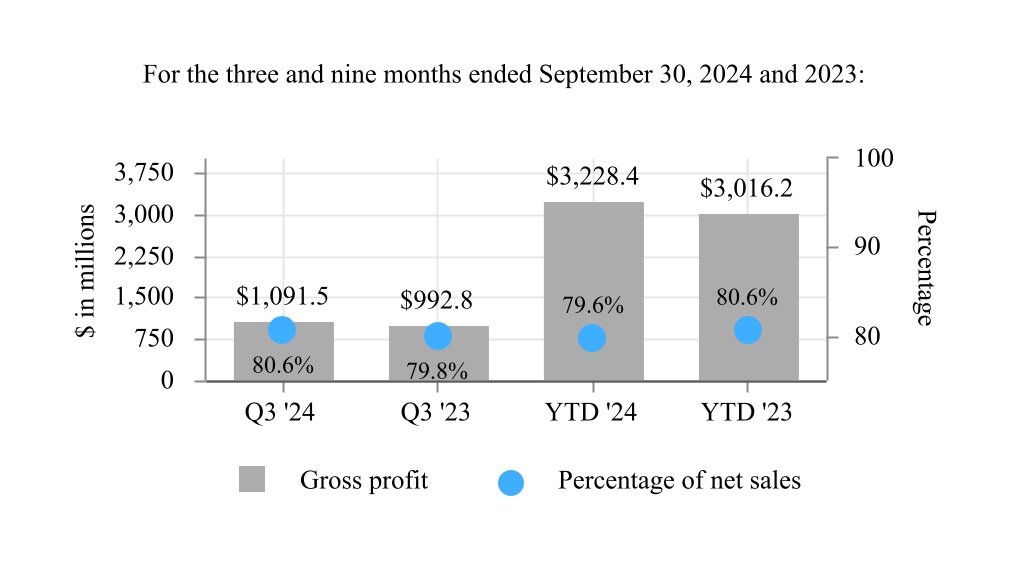

| Gross profit | |||||||||||||||||||||||

| Selling, general, and administrative expenses | |||||||||||||||||||||||

| Research and development expenses | |||||||||||||||||||||||

Intellectual property agreement and certain litigation expenses (Note 3) | |||||||||||||||||||||||

| Change in fair value of contingent consideration liabilities (Note 9) | ( | ||||||||||||||||||||||

| Restructuring expenses (Note 4) | |||||||||||||||||||||||

| Other operating expenses, net | |||||||||||||||||||||||

| Operating income, net | |||||||||||||||||||||||

| Interest income, net | ( | ( | ( | ( | |||||||||||||||||||

| Other non-operating income, net | ( | ( | ( | ( | |||||||||||||||||||

| Income from continuing operations before provision for income taxes | |||||||||||||||||||||||

| Provision for income taxes | |||||||||||||||||||||||

| Net income from continuing operations | |||||||||||||||||||||||

| Income from discontinued operations, net of tax | |||||||||||||||||||||||

| Net income | |||||||||||||||||||||||

| Net loss attributable to noncontrolling interest | ( | ( | ( | ( | |||||||||||||||||||

| Net income attributable to Edwards Lifesciences Corporation | $ | $ | $ | $ | |||||||||||||||||||

Share information (Note 15) | |||||||||||||||||||||||

| Earnings per share: | |||||||||||||||||||||||

| Basic | |||||||||||||||||||||||

| Continuing operations | $ | $ | $ | $ | |||||||||||||||||||

| Discontinued operations | $ | $ | $ | $ | |||||||||||||||||||

| Basic earnings per share | $ | $ | $ | $ | |||||||||||||||||||

| Diluted | |||||||||||||||||||||||

| Continuing operations | $ | $ | $ | $ | |||||||||||||||||||

| Discontinued operations | $ | $ | $ | $ | |||||||||||||||||||

| Diluted earnings per share | $ | $ | $ | $ | |||||||||||||||||||

| Weighted-average number of common shares outstanding: | |||||||||||||||||||||||

| Basic | |||||||||||||||||||||||

| Diluted | |||||||||||||||||||||||

The accompanying notes are an integral part of these consolidated condensed financial statements.

2

EDWARDS LIFESCIENCES CORPORATION

CONSOLIDATED CONDENSED STATEMENTS OF COMPREHENSIVE INCOME

(in millions; unaudited)

| Three Months Ended September 30, | Nine Months Ended September 30, | ||||||||||||||||||||||

| 2024 | 2023 | 2024 | 2023 | ||||||||||||||||||||

| Net income | $ | $ | $ | $ | |||||||||||||||||||

Other comprehensive (loss) income, net of tax (Note 14): | |||||||||||||||||||||||

| Foreign currency translation adjustments | ( | ( | ( | ||||||||||||||||||||

Unrealized (loss) gain on hedges | ( | ( | |||||||||||||||||||||

Unrealized pension credits | |||||||||||||||||||||||

Unrealized gain on available-for-sale investments | |||||||||||||||||||||||

Other comprehensive (loss) income, net of tax | ( | ( | |||||||||||||||||||||

| Comprehensive income | |||||||||||||||||||||||

Comprehensive loss attributable to noncontrolling interest | ( | ( | ( | ( | |||||||||||||||||||

| Comprehensive income attributable to Edwards Lifesciences Corporation | $ | $ | $ | $ | |||||||||||||||||||

The accompanying notes are an integral part of these consolidated condensed financial statements.

3

EDWARDS LIFESCIENCES CORPORATION

CONSOLIDATED CONDENSED STATEMENTS OF CASH FLOWS

(in millions; unaudited)

| Nine Months Ended September 30, | |||||||||||

| 2024 | 2023 | ||||||||||

| Cash flows from operating activities | |||||||||||

| Net income | $ | $ | |||||||||

| Adjustments to reconcile net income to net cash provided by operating activities: | |||||||||||

| Depreciation and amortization | |||||||||||

| Non-cash operating lease cost | |||||||||||

| Stock-based compensation (Note 11) | |||||||||||

| Gain on sale of business (Note 5) | ( | ||||||||||

| Change in fair value of contingent consideration liabilities (Note 9) | ( | ||||||||||

| Deferred income taxes | ( | ( | |||||||||

| Gain on remeasurement of previously held interest upon acquisition (Note 8) | ( | ||||||||||

| Other | |||||||||||

| Changes in operating assets and liabilities: | |||||||||||

| Accounts and other receivables, net | ( | ||||||||||

| Inventories | ( | ( | |||||||||

| Accounts payable and accrued liabilities | |||||||||||

| Income taxes | |||||||||||

| Prepaid expenses and other current assets | ( | ||||||||||

| Intellectual property agreement accrual | ( | ( | |||||||||

| Long-term prepaid royalties (Note 3) | ( | ||||||||||

| Other | ( | ( | |||||||||

| Net cash provided by operating activities | |||||||||||

| Cash flows from investing activities | |||||||||||

| Capital expenditures | ( | ( | |||||||||

| Purchases of held-to-maturity investments (Note 6) | ( | ( | |||||||||

| Proceeds from held-to-maturity investments (Note 6) | |||||||||||

| Purchases of available-for-sale investments (Note 6) | ( | ( | |||||||||

| Proceeds from available-for-sale investments (Note 6) | |||||||||||

| Investments in intangible assets | ( | ( | |||||||||

| Proceeds from sale of business | |||||||||||

| Business combination, net of cash | ( | ( | |||||||||

| Payment for acquisition options (Note 7) | ( | ( | |||||||||

| Issuances of notes receivable | ( | ( | |||||||||

| Other | ( | ( | |||||||||

| Net cash provided by investing activities | |||||||||||

| Cash flows from financing activities | |||||||||||

| Purchases of treasury stock | ( | ( | |||||||||

| Equity forward contract related to accelerated share repurchase agreement (Note 12) | ( | ||||||||||

| Proceeds from stock plans | |||||||||||

| Other | ( | ( | |||||||||

| Net cash used in financing activities | ( | ( | |||||||||

| Effect of currency exchange rate changes on cash, cash equivalents, and restricted cash | ( | ||||||||||

| Net increase in cash, cash equivalents, and restricted cash | |||||||||||

| Cash, cash equivalents, and restricted cash at beginning of period | |||||||||||

| Cash, cash equivalents, and restricted cash at end of period (Note 2) | $ | $ | |||||||||

The accompanying notes are an integral part of these consolidated condensed financial statements.

4

EDWARDS LIFESCIENCES CORPORATION

CONSOLIDATED CONDENSED STATEMENTS OF STOCKHOLDERS' EQUITY

(in millions; unaudited)

| Common Stock | Treasury Stock | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Shares | Par Value | Shares | Amount | Additional Paid-in Capital | Retained Earnings | Accumulated Other Comprehensive Loss | Total Edwards Lifesciences Corporation Stockholders' Equity | Noncontrolling Interest | Total Stockholders' Equity | ||||||||||||||||||||||||||||||||||||||||||||||||||

| Balance at December 31, 2023 | $ | $ | ( | $ | $ | $ | ( | $ | $ | $ | |||||||||||||||||||||||||||||||||||||||||||||||||

| Net income | ( | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Other comprehensive gain, net of tax | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Common stock issued under stock plans | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Stock-based compensation expense | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Purchases of treasury stock | — | ( | ( | ( | |||||||||||||||||||||||||||||||||||||||||||||||||||||||

Balance at March 31, 2024 | $ | $ | ( | $ | $ | $ | ( | $ | $ | $ | |||||||||||||||||||||||||||||||||||||||||||||||||

| Net income | ( | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Other comprehensive gain, net of tax | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Common stock issued under equity plans | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Stock-based compensation expense | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Purchases of treasury stock | ( | ( | ( | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Balance at June 30, 2024 | $ | $ | ( | $ | $ | $ | ( | $ | $ | $ | |||||||||||||||||||||||||||||||||||||||||||||||||

| Net income | ( | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Other comprehensive loss, net of tax | ( | ( | ( | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Common stock issued under equity plans | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Stock-based compensation expense | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Purchases of treasury stock | ( | ( | ( | ( | |||||||||||||||||||||||||||||||||||||||||||||||||||||||

Balance at September 30, 2024 | $ | $ | ( | $ | $ | $ | ( | $ | $ | $ | |||||||||||||||||||||||||||||||||||||||||||||||||

The accompanying notes are an integral part of these consolidated condensed financial statements.

5

EDWARDS LIFESCIENCES CORPORATION

CONSOLIDATED CONDENSED STATEMENTS OF STOCKHOLDERS' EQUITY

(in millions; unaudited)

| Common Stock | Treasury Stock | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Shares | Par Value | Shares | Amount | Additional Paid-in Capital | Retained Earnings | Accumulated Other Comprehensive Loss | Total Edwards Lifesciences, Inc. Stockholders' Equity | Noncontrolling Interest | Total Stockholders' Equity | ||||||||||||||||||||||||||||||||||||||||||||||||||

| Balance at December 31, 2022 | $ | $ | ( | $ | $ | $ | ( | $ | $ | $ | |||||||||||||||||||||||||||||||||||||||||||||||||

| Net income | — | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Other comprehensive loss, net of tax | ( | ( | ( | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Common stock issued under stock plans | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Stock-based compensation expense | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Purchases of treasury stock | ( | ( | ( | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Changes to noncontrolling interest | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Balance at March 31, 2023 | $ | $ | ( | $ | $ | $ | ( | $ | $ | $ | |||||||||||||||||||||||||||||||||||||||||||||||||

| Net income | ( | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Other comprehensive loss, net of tax | ( | ( | ( | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Common stock issued under equity plans | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Stock-based compensation expense | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Purchases of treasury stock | ( | ( | ( | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Changes to noncontrolling interest | ( | ( | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Balance at June 30, 2023 | $ | $ | ( | $ | $ | $ | ( | $ | $ | $ | |||||||||||||||||||||||||||||||||||||||||||||||||

| Net income | ( | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Other comprehensive loss, net of tax | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Common stock issued under equity plans | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Stock-based compensation expense | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Purchases of treasury stock | ( | ( | ( | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Balance at September 30, 2023 | $ | $ | ( | $ | $ | $ | ( | $ | $ | $ | |||||||||||||||||||||||||||||||||||||||||||||||||

The accompanying notes are an integral part of these consolidated condensed financial statements.

6

1. BASIS OF PRESENTATION

The accompanying interim consolidated condensed financial statements and related disclosures have been prepared pursuant to the rules and regulations of the Securities and Exchange Commission ("SEC") and should be read in conjunction with the consolidated financial statements and notes included in Edwards Lifesciences' Annual Report on Form 10-K for the year ended December 31, 2023. Certain information and footnote disclosures normally included in financial statements prepared in accordance with generally accepted accounting principles in the United States of America ("GAAP") have been condensed or omitted.

The consolidated condensed financial statements include the accounts of all wholly-owned subsidiaries and variable interest entities for which the Company is the primary beneficiary. The Company attributes the net income or losses of its consolidated variable interest entities to controlling and noncontrolling interests using the hypothetical liquidation at book value method. All intercompany accounts and transactions have been eliminated in consolidation.

On September 3, 2024, the Company sold its Critical Care product group ("Critical Care"). The historical results of Critical Care are reflected as discontinued operations in the Company's consolidated condensed financial statements for all periods presented. In addition, as a next step in the Company's disposal plan to exit businesses that are not focused on implantable medical innovations for structural heart disease, the historical results of a small non-core product group that the Company plans to sell are also included in discontinued operations. Unless otherwise indicated, the information in the notes to the consolidated condensed financial statements refer only to Edwards Lifesciences' continuing operations. For more information, see Note 5.

In the opinion of management, the unaudited interim consolidated condensed financial statements reflect all adjustments necessary for a fair statement of the results for the interim periods presented. All such adjustments, unless otherwise noted herein, are of a normal, recurring nature. The results of operations for the interim periods are not necessarily indicative of the results of operations to be expected for the full year.

There have been no material changes to the Company's significant accounting policies from those described in the Company's Annual Report on Form 10-K for the year ended December 31, 2023.

Recently Adopted Accounting Standards

In March 2023, the Financial Accounting Standards Board ("FASB") issued an amendment to the accounting guidance on investments in tax credit structures to allow entities to elect to account for their tax equity investments, regardless of the tax credit program from which the income tax credits are received, using the proportional amortization method if certain conditions are met. The guidance is effective for fiscal years beginning after December 15, 2023, including interim periods within those fiscal years. The Company adopted this guidance on January 1, 2024. The adoption of this guidance did not have a material impact on the Company's consolidated financial statements.

New Accounting Standards Not Yet Adopted

In November 2024, the FASB issued an amendment to the accounting guidance on income statement presentation to require disclosure, in the notes to the financial statements, of disaggregated information about certain costs and expenses, including purchases of inventory, employee compensation, and depreciation and amortization included in each relevant expense caption within continuing operations. The guidance is effective for fiscal years beginning after December 15, 2026, and interim periods beginning after December 15, 2027. The Company is currently evaluating the impact the guidance will have on its consolidated financial statements.

In March 2024, the SEC issued final climate-related disclosure rules that will require disclosure of material climate-related risks and material direct greenhouse gas emissions from operations owned or controlled (Scope 1) and/or material indirect greenhouse gas emissions from purchased energy consumed in owned or controlled operations (Scope 2). Additionally, the rules require disclosure in the notes to the financial statements of the effects of severe weather events and other natural conditions, subject to certain materiality thresholds. The new rules will be effective for annual reporting periods beginning in fiscal year 2025, except for the greenhouse gas emissions disclosures which will be effective for annual reporting periods beginning in fiscal year 2026. Subsequent to issuance, the rules became the subject of litigation, and the SEC has issued a stay

7

to allow the legal process to proceed. The Company is currently evaluating the disclosure impact the guidance will have on its consolidated financial statements.

In December 2023, the FASB issued an amendment to the accounting guidance on income taxes which requires entities to provide additional information in the rate reconciliation and additional disaggregated disclosures about income taxes paid. This guidance requires public entities to disclose in their rate reconciliation table additional categories of information about federal, state, and foreign income taxes and to provide more details about the reconciling items in some categories if the items meet a quantitative threshold. The guidance is effective for annual periods beginning after December 15, 2024. The Company does not expect the adoption of this guidance to impact its financial statements, but the guidance will impact its income tax disclosures.

In November 2023, the FASB issued an amendment to the accounting guidance on segment reporting. The amendments require disclosure of significant segment expenses and other segment items and requires entities to provide in interim periods all disclosures about a reportable segment's profit or loss and assets that are currently required annually. The amendment also requires disclosure of the title and position of the chief operating decision maker ("CODM") and an explanation of how the CODM uses the reported measure(s) of segment profit or loss in assessing segment performance and deciding how to allocate resources. The guidance is effective for fiscal years beginning after December 15, 2023, and interim periods within fiscal years beginning after December 15, 2024. Retrospective application is required, and early adoption is permitted. The Company is currently evaluating the impact the guidance will have on its consolidated financial statements.

2. OTHER CONSOLIDATED FINANCIAL STATEMENT DETAILS

Composition of Certain Financial Statement Captions

(in millions)

Components of selected captions in the consolidated condensed balance sheets consisted of the following:

| September 30, 2024 | December 31, 2023 | ||||||||||

| Inventories | |||||||||||

| Raw materials | $ | $ | |||||||||

| Work in process | |||||||||||

| Finished products | |||||||||||

| $ | $ | ||||||||||

At September 30, 2024 and December 31, 2023, $187.8 million and $164.6 million, respectively, of the Company's finished products inventories were held on consignment.

8

| September 30, 2024 | December 31, 2023 | ||||||||||

| Other assets | |||||||||||

| Tax receivable (Note 16) | $ | $ | |||||||||

| Notes and other receivables | |||||||||||

| Acquisition options | |||||||||||

| Long-term prepaid royalties | |||||||||||

| Fair value of derivatives | |||||||||||

| Other long-term assets | |||||||||||

| $ | $ | ||||||||||

| Accrued and other liabilities | |||||||||||

| Employee compensation and withholdings | $ | $ | |||||||||

| Taxes payable (Note 5) | |||||||||||

| Property, payroll, and other taxes | |||||||||||

| Research and development accruals | |||||||||||

| Accrued rebates | |||||||||||

| Fair value of derivatives | |||||||||||

| Accrued marketing expenses | |||||||||||

| Legal and insurance | |||||||||||

| Litigation settlement | |||||||||||

| Accrued relocation costs | |||||||||||

| Accrued professional services | |||||||||||

| Accrued realignment reserves | |||||||||||

| Unfavorable contract liability | |||||||||||

| Other accrued liabilities | |||||||||||

| $ | $ | ||||||||||

Supplemental Cash Flow Information

(in millions)

| Nine Months Ended September 30, | |||||||||||

| 2024 | 2023 | ||||||||||

| Cash paid during the year for: | |||||||||||

Income taxes (a) (Note 16) | $ | $ | |||||||||

| Amounts included in the measurement of operating lease liabilities | $ | $ | |||||||||

| Non-cash investing and financing transactions: | |||||||||||

| Right-of-use assets obtained in exchange for new lease liabilities | $ | $ | |||||||||

| Capital expenditures accruals | $ | $ | |||||||||

______________________________________

(a) Includes cash paid for income taxes from discontinued operations of $29.7 million and $22.7 million for the nine months ended September 30, 2024 and 2023, respectively.

9

Cash, Cash Equivalents, and Restricted Cash

(in millions)

| September 30, 2024 | December 31, 2023 | |||||||||||||

| Continuing operations | ||||||||||||||

| Cash and cash equivalents | $ | $ | ||||||||||||

| Restricted cash included in other current assets | ||||||||||||||

| Restricted cash included in other assets | ||||||||||||||

| Total | $ | $ | ||||||||||||

| Discontinued operations | ||||||||||||||

| Cash and cash equivalents | $ | $ | ||||||||||||

| Total | $ | $ | ||||||||||||

| Total cash, cash equivalents, and restricted cash | $ | $ | ||||||||||||

Amounts included in restricted cash primarily represent funds placed in escrow related to litigation.

3. INTELLECTUAL PROPERTY AGREEMENT AND CERTAIN LITIGATION EXPENSES

4. RESTRUCTURING EXPENSES

In September 2024, the Company recorded an expense of $32.9 million related primarily to severance expenses associated with a global workforce realignment impacting approximately 360 employees. As of September 30, 2024, the Company's remaining severance obligations of $30.6 million are expected to be substantially paid within the next 12 months.

5. DISCONTINUED OPERATIONS

On June 3, 2024, the Company entered into a definitive agreement to sell its Critical Care product group ("Critical Care") to Becton, Dickinson and Company ("BD"). In addition, as a next step in the Company's disposal plan to exit businesses that are not focused on implantable medical innovations for structural heart disease, the Company has committed to a plan to sell a non-core product group, with the sale expected to occur within the next 12 months.

Critical Care and the aforementioned non-core product group (collectively, the "discontinued product groups") were historically reported in each of the Company's segments (United States, Europe, Japan, and Rest of World).

The Company concluded that the Critical Care product group met the criteria to be classified as held-for-sale in June 2024 and that the non-core product group met the criteria to be classified as held-for-sale in September 2024. The Company determined that, when considered together, the conditions for discontinued operations presentation had been met with respect to the discontinued product groups. A component of an entity is reported in discontinued operations after meeting the criteria for held-for-sale classification if the disposition represents a strategic shift that has (or will have) a major effect on the entity's operations and financial results. The Company analyzed the quantitative and qualitative factors relevant to the discontinued product groups, including their significance to the Company’s overall net income and total assets, and determined that those

10

conditions for discontinued operations presentation had been met. As such, the historical financial condition and results of the discontinued product groups have been reflected as discontinued operations in the Company's consolidated condensed financial statements. The assets and liabilities associated with discontinued product groups are classified as assets and liabilities of discontinued operations in the Company's consolidated condensed balance sheets. Prior period amounts have been adjusted to reflect the discontinued operations presentation.

On September 3, 2024, Critical Care was sold for $4.2 billion, which is subject to a further working capital adjustment, resulting in a gain of $3.3 billion which was included in Income from Discontinued Operations, net of tax.

In connection with the sale of Critical Care, the Company entered into a Transition Services Agreement ("TSA") to provide certain support services for up to 36 months from the closing date of the sale (with certain extension rights as provided therein). These support services may be in the areas of accounting, information technology, human resources, quality assurance, regulatory affairs, customer support, and global supply chain, among others. In connection with the TSA, the Company recognized an unfavorable contract liability of $115.1 million, which will be recognized over the TSA term.

In addition, Edwards and BD entered into other agreements to provide a framework for the ongoing activities between the Company and BD after the sale and until the end of the TSA including, but not limited to, interim operating model agreements to support the commercial operations until full transfer of all regulatory licenses to BD and completion of services under the TSA agreement, a manufacturing and supply agreement, and a quality agreement. Under these agreements, the Company will continue to provide certain services to BD during the term of these agreements including serving as an undisclosed selling and purchasing agent for the Critical Care business on behalf of BD for a period of up to 36 months.

As of September 30, 2024, the Company had a receivable of approximately $24.6 million from BD related to the services under the agreements. The Company recorded income from the TSA of $7.6

Details of Income from Discontinued Operations are as follows (in millions):

| Three Months Ended September 30, | Nine Months Ended September 30, | ||||||||||||||||||||||

| 2024 | 2023 | 2024 | 2023 | ||||||||||||||||||||

| Net sales | $ | $ | $ | $ | |||||||||||||||||||

| Cost of sales | |||||||||||||||||||||||

| Gross profit | |||||||||||||||||||||||

| Selling, general, and administrative expenses | |||||||||||||||||||||||

| Research and development expenses | |||||||||||||||||||||||

| Separation costs | |||||||||||||||||||||||

| Operating (loss) income, net | ( | ( | |||||||||||||||||||||

| Other non-operating (income) expense, net | ( | ( | |||||||||||||||||||||

| Income from discontinued operations before provision for income taxes | |||||||||||||||||||||||

| Provision for income taxes from discontinued operations | |||||||||||||||||||||||

| Net income from discontinued operations | |||||||||||||||||||||||

Separation costs related primarily to consulting, legal, tax, and other professional advisory services associated with the sale of Critical Care.

11

Details of assets and liabilities of discontinued operations are as follows (in millions):

| September 30, 2024 | December 31, 2023 | ||||||||||

| Cash and cash equivalents | $ | $ | |||||||||

| Accounts receivable, net of allowances | |||||||||||

| Other receivables | |||||||||||

| Inventories | |||||||||||

| Prepaid expenses | |||||||||||

| Other current assets | |||||||||||

| Total current assets of discontinued operations | $ | $ | |||||||||

| Property, plant, and equipment, net | |||||||||||

| Operating lease right-of-use assets | |||||||||||

| Goodwill | |||||||||||

| Other intangible assets, net | |||||||||||

| Deferred income taxes | |||||||||||

| Other assets | |||||||||||

| Total non-current assets of discontinued operations | $ | $ | |||||||||

| Accounts payable | $ | $ | |||||||||

| Accrued and other liabilities | |||||||||||

| Operating lease liabilities | |||||||||||

| Total current liabilities of discontinued operations | $ | $ | |||||||||

| Operating lease liabilities | |||||||||||

| Uncertain tax positions | |||||||||||

| Other liabilities | |||||||||||

| Total non-current liabilities of discontinued operations | $ | $ | |||||||||

Cash flows attributable to the Company's discontinued operations are included in the Company's consolidated condensed statements of cash flows. Significant non-cash operating and investing activities attributable to discontinued operations consisted of the following (in millions):

| Nine Months Ended September 30, | |||||||||||

| 2024 | 2023 | ||||||||||

| Depreciation and amortization | |||||||||||

| Stock-based compensation | |||||||||||

| Inventory write off | |||||||||||

| Capital expenditures | |||||||||||

12

6. INVESTMENTS

Debt Securities

Investments in debt securities at the end of each period were as follows (in millions):

| September 30, 2024 | December 31, 2023 | ||||||||||||||||||||||||||||||||||||||||||||||

| Held-to-maturity | Amortized Cost | Gross Unrealized Gains | Gross Unrealized Losses | Fair Value | Amortized Cost | Gross Unrealized Gains | Gross Unrealized Losses | Fair Value | |||||||||||||||||||||||||||||||||||||||

| Bank time deposits | $ | $ | $ | $ | $ | $ | $ | $ | |||||||||||||||||||||||||||||||||||||||

| Available-for-sale | |||||||||||||||||||||||||||||||||||||||||||||||

| Bank time deposits | $ | $ | $ | $ | $ | $ | $ | $ | |||||||||||||||||||||||||||||||||||||||

| Commercial paper | |||||||||||||||||||||||||||||||||||||||||||||||

| U.S. government and agency securities | ( | ( | |||||||||||||||||||||||||||||||||||||||||||||

| Asset-backed securities | ( | ( | |||||||||||||||||||||||||||||||||||||||||||||

| Corporate debt securities | ( | ( | |||||||||||||||||||||||||||||||||||||||||||||

| Municipal securities | ( | ( | |||||||||||||||||||||||||||||||||||||||||||||

| Total | $ | $ | $ | ( | $ | $ | $ | $ | ( | $ | |||||||||||||||||||||||||||||||||||||

The cost and fair value of investments in debt securities, by contractual maturity, as of September 30, 2024, were as follows:

| Held-to-Maturity | Available-for-Sale | ||||||||||||||||||||||

| Amortized Cost | Fair Value | Amortized Cost | Fair Value | ||||||||||||||||||||

| (in millions) | |||||||||||||||||||||||

| Due in 1 year or less | $ | $ | $ | $ | |||||||||||||||||||

| Due after 1 year through 5 years | |||||||||||||||||||||||

Instruments not due at a single maturity date (a) | |||||||||||||||||||||||

| $ | $ | $ | $ | ||||||||||||||||||||

_______________________________________

(a) Consists of mortgage-backed and asset-backed securities.

Actual maturities may differ from the contractual maturities due to call or prepayment rights.

The following tables present gross unrealized losses and fair values for those investments that were in an unrealized loss position as of September 30, 2024 and December 31, 2023, aggregated by investment category and the length of time that individual securities have been in a continuous loss position (in millions):

| September 30, 2024 | |||||||||||||||||||||||||||||||||||

| Less than 12 Months | 12 Months or Greater | Total | |||||||||||||||||||||||||||||||||

| Fair Value | Gross Unrealized Losses | Fair Value | Gross Unrealized Losses | Fair Value | Gross Unrealized Losses | ||||||||||||||||||||||||||||||

| U.S. government and agency securities | $ | $ | $ | $ | ( | $ | $ | ( | |||||||||||||||||||||||||||

| Asset-backed securities | ( | ( | ( | ||||||||||||||||||||||||||||||||

| Corporate debt securities | ( | ( | |||||||||||||||||||||||||||||||||

| Municipal securities | ( | ( | |||||||||||||||||||||||||||||||||

| $ | $ | ( | $ | $ | ( | $ | $ | ( | |||||||||||||||||||||||||||

13

| December 31, 2023 | |||||||||||||||||||||||||||||||||||

| Less than 12 Months | 12 Months or Greater | Total | |||||||||||||||||||||||||||||||||

| Fair Value | Gross Unrealized Losses | Fair Value | Gross Unrealized Losses | Fair Value | Gross Unrealized Losses | ||||||||||||||||||||||||||||||

| U.S. government and agency securities | $ | $ | $ | $ | ( | $ | $ | ( | |||||||||||||||||||||||||||

| Asset-backed securities | ( | ( | ( | ||||||||||||||||||||||||||||||||

| Corporate debt securities | ( | ( | ( | ||||||||||||||||||||||||||||||||

| Municipal securities | ( | ( | |||||||||||||||||||||||||||||||||

| $ | $ | ( | $ | $ | ( | $ | $ | ( | |||||||||||||||||||||||||||

The Company reviews its investments in debt securities to determine if there has been an other-than-temporary decline in fair value. Consideration is given to 1) the financial condition and near-term prospects of the issuer, including the credit quality of the security's issuer, 2) the Company's intent to sell the security, and 3) whether it is more likely than not the Company will have to sell the security before recovery of its amortized cost. The unrealized losses on the debt securities were largely due to changes in interest rates, not credit quality, and as of September 30, 2024, the Company did not intend to sell the securities, and it was not more likely than not that it will be required to sell the securities before recovery of the unrealized losses, and, therefore, the unrealized losses are considered temporary.

Investments in Unconsolidated Entities

The Company has a number of equity investments in unconsolidated entities. These investments are recorded in Long-term Investments on the consolidated condensed balance sheets, and are as follows:

| September 30, 2024 | December 31, 2023 | ||||||||||

| (in millions) | |||||||||||

| Equity method investments | |||||||||||

| Carrying value of equity method investments | $ | $ | |||||||||

| Equity securities | |||||||||||

| Carrying value of marketable equity securities | |||||||||||

| Carrying value of non-marketable equity securities | |||||||||||

| Total investments in unconsolidated entities | $ | $ | |||||||||

The Company makes equity investments in limited liability companies that invest in qualified community development entities ("CDEs") through the New Markets Tax Credit ("NMTC") program. The NMTC program provides federal tax incentives to investors to make investments in distressed communities and promotes economic improvements through the development of successful businesses in these communities. The NMTC is equal to 39 % of the qualified investment and is taken over seven years . These limited liability companies are variable interest entities ("VIEs"). The Company determined that it is not the primary beneficiary of the VIEs because it does not have the power to direct the activities that most significantly impact the economic performance of the VIEs and, therefore, the Company does not consolidate these entities. Instead, the NMTC investments are accounted for as equity method investments.

Marketable equity securities consist of investments with readily determinable fair values over which we do not own a controlling interest or exercise significant influence. Non-marketable equity securities consist of investments in privately held companies without readily determinable fair values, and are reported at cost minus impairment, if any, plus or minus changes resulting from observable price changes in orderly transactions for the identical or similar investment of the same issuer. The Company recorded an upward adjustment of $0.5 million and a downward adjustment of $2.4 million during the nine months ended September 30, 2024 based on observable price changes. As of September 30, 2024, the Company had recorded cumulative upward adjustments of $9.3 million based on observable price changes, and cumulative downward adjustments of $5.5 million due to impairments and observable price changes.

14

7. INVESTMENTS IN VARIABLE INTEREST ENTITIES

The Company reviews its investments in other entities to determine whether the Company is the primary beneficiary of a VIE. The Company would be the primary beneficiary of the VIE, and would be required to consolidate the VIE, if it has the power to direct the significant activities of the entity and the obligation to absorb losses or receive benefits from the entity that may be significant to the VIE. The Company's maximum loss exposure to variable interest entities, prior to the exercise of options to acquire the entities, is limited to its investment in the variable interest entities, which include equity investments, options to acquire, and promissory notes.

Consolidated VIEs

In February 2023, the Company acquired a majority equity interest in a medical technology company pursuant to a preferred stock purchase agreement, and amended and restated a previous option agreement to acquire the remaining equity interest. Edwards concluded that it is the primary beneficiary and consolidated the VIE. The total assets and liabilities of the Company's consolidated VIE was $258.1 million and $26.7 million, respectively, as of September 30, 2024, and were $272.1 million and $31.5 million, respectively, as of December 31, 2023. The assets of the VIE can only be used to settle obligations of the VIE and general creditors have no recourse to the Company.

Unconsolidated VIEs

Edwards has relationships with various VIEs that it does not consolidate as Edwards lacks the power to direct the activities that significantly impact the economic success of these entities.

In June 2022, the Company entered into a convertible promissory note and amended its existing warrant agreement with a medical device company. Under the convertible promissory note agreement, the Company agreed to loan the medical device company up to $47.5 million, of which $42.5 million had been advanced as of September 30, 2024. The remaining $5.0 million was advanced in October 2024. In addition, in 2019, the Company paid $35.0 million for an option to acquire the medical device company. The option and the note receivable are included in Other Assets on the consolidated balance sheets.

In April 2021, the Company entered into a promissory note agreement, a preferred stock purchase agreement, and an option agreement with a privately-held medical device company (the "Investee"). The secured promissory note provides for borrowings up to $45.0 million. At both September 30, 2024 and December 31, 2023, the Company had advanced $30.0 42.8 million and $39.3 million, respectively, in the Investee's preferred equity securities (included in Long-term Investments) and had paid $20.9 million and $13.1 million, respectively, for an option to acquire the Investee (included in Other Assets). Pursuant to the agreements, the Company may be required to invest up to an additional $3.0 million in the Investee's preferred equity securities and up to an additional $6.6 million for the option to acquire the Investee.

In March 2023, the Company agreed to pay a medical device company up to $45.0 million as consideration for an option

to acquire that medical device company, of which $30.0 million had been paid as of September 30, 2024. Also, in March 2023, Edwards advanced $5.0 million to the medical device company under a convertible promissory note. In addition, as of September 30, 2024 and December 31, 2023, the Company had invested $3.5 million and $3.3 million, respectively, in the medical device company's preferred equity securities. The option and the note are included in Other Assets on the consolidated balance sheets, and the equity investment is included in Long-term Investments. In July 2024, the Company exercised its option to acquire the medical device company and the transaction closed in October 2024. For more information, see Note 18.

In addition, Edwards has made equity investments through the NMTC program in limited liability companies that are considered VIEs. For more information, see Note 6.

8. BUSINESS COMBINATIONS

Endotronix, Inc.

On August 19, 2024, the Company acquired all the remaining outstanding shares of Endotronix, Inc. ("Endotronix"). Endotronix is a developer of an implantable sensor for management of heart failure patients. The acquisition was completed primarily to expand the Company's structural heart portfolio into a new therapeutic area to address the large unmet needs of patients suffering from heart failure.

15

Prior to the acquisition date, the Company had previously paid $60.0 million for an option to acquire Endotronix, which was historically recorded in Other Assets using the measurement alternative for fair value, and had an existing preferred stock investment in Endotronix of $10.0 million, which represented an ownership interest in Endotronix of approximately 7 % (collectively, the "previously held equity interest"). In July 2024, the Company exercised its option to acquire the remaining equity interest in Endotronix which was accounted for as a step acquisition in accordance with Accounting Standards Codification Topic 805, "Business Combinations." Accordingly, the Company allocated the purchase price of the acquired company to the net tangible assets and intangible assets acquired based upon their preliminary estimated fair values. The Company remeasured the previously held equity interest to its fair value, as of the date of acquisition. The Company considered multiple factors in determining the fair value of the previously held equity interest, including, (i) the price negotiated with the selling shareholders for the remaining 93 % interest in Endotronix and (ii) an income approach valuation model. As a result of the remeasurement of the previously held equity interest, the Company recognized a gain of $24.6 million in Other income, net in the third quarter of 2024.

The purchase consideration for the acquisition of Endotronix was $798.8 million, which consisted of cash consideration of $649.1 million (net of cash acquired of $1.2 million), the fair value of the Company's previously held equity interest of $94.6 million, and the settlement of pre-existing relationships of $53.1 million. In addition, the Company agreed to pay an additional $2.0 million in a pre-specified milestone-driven payment that is dependent on the receipt of CE Mark approval for the CorPASS before June 30, 2025. The Company recognized a $2.0 million contingent consideration liability for the estimated fair value of the contingent milestone payments. The fair value of the contingent milestone payment will be remeasured each quarter, with changes in the fair value recognized within operating expenses on the consolidated statements of operations.

In connection with the acquisition of Endotronix, the Company placed $35.0 million of the cash consideration paid at closing into escrow to satisfy any claims for indemnification made in accordance with the merger agreement and for purchase price adjustments. Acquisition-related costs of $5.6 million were recorded in Selling, General, and Administrative Expenses during the nine months ended September 30, 2024.

The following table summarizes the fair value of consideration transferred and the fair values of the assets acquired and liabilities assumed (in millions):

| Cash consideration paid at closing | $ | ||||||||||

| Settlement of pre-existing relationships | |||||||||||

| Fair value of previously held equity interest | |||||||||||

| Fair value of contingent consideration | |||||||||||

| Total purchase price | |||||||||||

| Less: cash acquired | ( | ||||||||||

| Total purchase price, net of cash acquired | $ | ||||||||||

| Current assets | $ | ||||||||||

| Property and equipment, net | |||||||||||

| Goodwill | |||||||||||

| In-process research and development | |||||||||||

| Developed technology | |||||||||||

| Operating lease right-of-use assets | |||||||||||

| Other assets | |||||||||||

| Liabilities assumed | ( | ||||||||||

| Deferred tax liabilities | ( | ||||||||||

| Net assets acquired | |||||||||||

| Less: cash acquired | ( | ||||||||||

| Total purchase price, net of cash acquired | $ | ||||||||||

The above purchase price allocation is preliminary and subject to revision for a one-year measurement period following the date of acquisition as additional information about the fair value of individual assets and liabilities becomes available. The preliminary measurement of intangible assets, goodwill, and deferred income taxes are subject to change. A change in the estimated fair value of the net assets acquired will change the amount of the purchase price allocable to goodwill.

16

Goodwill includes Endotronix's assembled workforce and expected synergies the Company believes will result from the acquisition. Goodwill was assigned to the Company’s United States segment and is not deductible for tax purposes. The fair value of the developed technology was determined using the income approach. This approach determines fair value based on cash flow projections which are discounted to present value using a risk-adjusted rate of return. The discount rate used to determine the fair value of the developed technology was 15.5 %. The fair value of the IPR&D was also determined using the income approach. IPR&D has been capitalized at fair value as an intangible asset with an indefinite life and will be assessed for impairment in subsequent periods. The discount rate used to determine the fair value of the IPR&D was 18.0 %. Completion of successful design developments, bench testing, pre-clinical studies and human clinical studies are required prior to selling any product. The risks and uncertainties associated with completing development within a reasonable period of time include those related to the design, development, and manufacturability of the product, the success of pre-clinical and clinical studies, and the timing of regulatory approvals. The valuation assumed $47.1 million of additional research and development expenditures would be incurred prior to the date of product introduction. In the valuation, net cash inflows were modeled to commence in the United States in 2027 and in Japan and Europe in 2028. Upon completion of development, the underlying research and development asset will be amortized over its estimated useful life.

The results of operations for Endotronix have been included in the accompanying consolidated financial statements from the date of acquisition. Pro forma results have not been presented as the results of Endotronix are not material in relation to the consolidated financial statements of Edwards Lifesciences.

JC Medical, Inc.

On July 22, 2024, the Company acquired all the outstanding shares of JC Medical, Inc. ("JC Medical") for purchase consideration of $116.3 million, net of cash acquired. In addition, the Company agreed to pay up to an additional $200.0 million in pre-specified milestone-driven payments over the next 12 years. The Company recognized a $1.8 million contingent consideration liability for the estimated fair value of the contingent milestone payments. The fair value of the contingent milestone payments will be remeasured each quarter, with changes in the fair value recognized within operating expenses on the consolidated statements of operations.

The Company placed $12.0 million of the cash consideration paid at closing into escrow to satisfy any claims for indemnification made in accordance with the merger agreement. Any funds remaining 15 months after the acquisition date will be disbursed to JC Medical's former shareholders. Acquisition-related costs of $1.6 million were recorded in Selling, General, and Administrative Expenses during the nine months ended September 30, 2024.

JC Medical, Inc. is a structural heart company that is primarily engaged in the design and development of transcatheter valve replacement products for the minimally invasive treatment of structural heart disease. The acquisition was completed primarily to expand the Company's TAVR portfolio to enable the treatment of patients with aortic regurgitation. The acquisition was accounted for as a business combination. Tangible and intangible assets acquired were recorded based on their estimated fair values at the acquisition date. The excess of the purchase price over the fair value of net assets acquired was recorded to goodwill.

17

The following table summarizes the fair value of consideration transferred and the fair values of the assets acquired and liabilities assumed (in millions):

| Cash consideration paid at closing | $ | ||||||||||

| Fair value of contingent consideration | |||||||||||

| Total purchase price | |||||||||||

| Less: cash acquired | ( | ||||||||||

| Total purchase price, net of cash acquired | $ | ||||||||||

| Current assets | $ | ||||||||||

| Property and equipment, net | |||||||||||

| Goodwill | |||||||||||

| In-process research and development | |||||||||||

| Current liabilities assumed | ( | ||||||||||

| Deferred tax liabilities | ( | ||||||||||

| Net assets acquired | |||||||||||

| Less: cash acquired | ( | ||||||||||

| Total purchase price, net of cash acquired | $ | ||||||||||

The above purchase price allocation is preliminary and subject to revision for a one-year measurement period following the date of acquisition as additional information about the fair value of individual assets and liabilities becomes available. The preliminary measurement of intangible assets, goodwill, and deferred income taxes are subject to change. A change in the estimated fair value of the net assets acquired will change the amount of the purchase price allocable to goodwill.

Goodwill includes JC Medical's assembled workforce and expected synergies the Company believes will result from the acquisition. Goodwill was assigned to the Company’s United States segment and is not deductible for tax purposes. IPR&D has been capitalized at fair value as an intangible asset with an indefinite life and will be assessed for impairment in subsequent periods. The fair value of the IPR&D was determined using the income approach. This approach determines fair value based on cash flow projections which are discounted to present value using a risk-adjusted rate of return. The discount rate used to determine the fair value of the IPR&D was 15.0 %. Completion of successful design developments, bench testing, pre-clinical studies and human clinical studies are required prior to selling any product. The risks and uncertainties associated with completing development within a reasonable period of time include those related to the design, development, and manufacturability of the product, the success of pre-clinical and clinical studies, and the timing of regulatory approvals. The valuation assumed $55.8 million of additional research and development expenditures would be incurred prior to the date of product introduction. In the valuation, net cash inflows were modeled to commence in the United States in 2028 and Europe in 2029. Upon completion of development, the underlying research and development asset will be amortized over its estimated useful life.

The results of operations for JC Medical have been included in the accompanying consolidated financial statements from the date of acquisition. Pro forma results have not been presented as the results of JC Medical are not material in relation to the consolidated financial statements of Edwards Lifesciences.

9. FAIR VALUE MEASUREMENTS

Fair value is defined as the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants. The Company prioritizes the inputs used to determine fair values in one of the following three categories:

Level 1—Quoted market prices in active markets for identical assets or liabilities.

Level 2—Inputs, other than quoted prices in active markets, that are observable, either directly or indirectly.

Level 3—Unobservable inputs that are not corroborated by market data.

18

In certain cases, the inputs used to measure fair value may fall into different levels of the fair value hierarchy. In such cases, the level in the fair value hierarchy within which the fair value measurement in its entirety falls has been determined based on the lowest level input that is significant to the fair value measurement in its entirety.

The consolidated condensed financial statements include financial instruments for which the fair market value of such instruments may differ from amounts reflected on a historical cost basis. Financial instruments of the Company consist of cash deposits, accounts and other receivables, investments, accounts payable, certain accrued liabilities, and borrowings under a revolving credit agreement. The carrying value of these financial instruments generally approximates fair value due to their short-term nature. Financial instruments also include notes payable. As of September 30, 2024, the fair value of the notes payable, based on Level 2 inputs, was $600.0 million.

Assets and Liabilities Measured at Fair Value on a Recurring Basis

The following table summarizes the Company's financial instruments which are measured at fair value on a recurring basis (in millions):

| September 30, 2024 | Level 1 | Level 2 | Level 3 | Total | |||||||||||||||||||

| Assets | |||||||||||||||||||||||

| Cash equivalents | $ | $ | $ | $ | |||||||||||||||||||

| Available-for-sale investments: | |||||||||||||||||||||||

Bank time deposits | |||||||||||||||||||||||

Corporate debt securities | |||||||||||||||||||||||

Asset-backed securities | |||||||||||||||||||||||

| United States government and agency securities | |||||||||||||||||||||||

Commercial paper | |||||||||||||||||||||||

Municipal securities | |||||||||||||||||||||||

| Equity investments in unconsolidated entities | |||||||||||||||||||||||

| Investments held for deferred compensation plans | |||||||||||||||||||||||

| Derivatives | |||||||||||||||||||||||

| $ | $ | $ | $ | ||||||||||||||||||||

| Liabilities | |||||||||||||||||||||||

| Derivatives | $ | $ | $ | $ | |||||||||||||||||||

| Contingent consideration liabilities | |||||||||||||||||||||||

| Other | |||||||||||||||||||||||

| $ | $ | $ | $ | ||||||||||||||||||||

| December 31, 2023 | |||||||||||||||||||||||

| Assets | |||||||||||||||||||||||

| Cash equivalents | $ | $ | $ | $ | |||||||||||||||||||

| Available-for-sale investments: | |||||||||||||||||||||||

Corporate debt securities | |||||||||||||||||||||||

Asset-backed securities | |||||||||||||||||||||||

| United States government and agency securities | |||||||||||||||||||||||

Municipal securities | |||||||||||||||||||||||

| Investments held for deferred compensation plans | |||||||||||||||||||||||

| Derivatives | |||||||||||||||||||||||

| $ | $ | $ | $ | ||||||||||||||||||||

| Liabilities | |||||||||||||||||||||||

| Derivatives | $ | $ | $ | $ | |||||||||||||||||||

| Other | |||||||||||||||||||||||

| $ | $ | $ | $ | ||||||||||||||||||||

19

Cash Equivalents and Available-for-sale Investments

Cash equivalents included money market funds for the periods presented above. The Company estimates the fair values of its money market funds based on quoted prices in active markets for identical assets. The Company estimates the fair values of its corporate debt securities, asset-backed securities, commercial paper, United States and foreign government and agency securities, and municipal securities by taking into consideration valuations obtained from third-party pricing services. The pricing services use industry standard valuation models, including both income and market-based approaches, for which all significant inputs are observable, either directly or indirectly, to estimate fair value. These inputs include reported trades and broker-dealer quotes on the same or similar securities, benchmark yields, credit spreads, prepayment and default projections based on historical data, and other observable inputs. The Company independently reviews and validates the pricing received from the third-party pricing service by comparing the prices to prices reported by a secondary pricing source. The Company’s validation procedures have not resulted in an adjustment to the pricing received from the pricing service.

Deferred Compensation Plans

The Company holds investments related to its deferred compensation plans. The investments are in a variety of stock, bond and money market mutual funds. The fair values of these investments are based on quoted market prices.

Derivative Instruments

The Company uses derivative financial instruments in the form of foreign currency forward exchange contracts and cross-currency swap contracts to manage foreign currency exposures. All derivative instruments are recognized on the balance sheet at their fair value, which was measured using quoted foreign exchange rates, interest rates, yield curves, and cross-currency swap basis rates. The estimates presented herein are not necessarily indicative of the amounts that the Company could realize in a current market exchange.

Contingent Consideration Liabilities

Certain of the Company's acquisitions involve contingent consideration arrangements. Payment of additional consideration is contingent upon the acquired company reaching certain performance milestones, such as attaining specified sales levels or obtaining regulatory approvals. These contingent consideration liabilities are measured at estimated fair value using either a probability weighted discounted cash flow analysis or a Monte Carlo simulation model, both of which consider significant unobservable inputs. These inputs include (1) the discount rate used to present value the projected cash flows

(ranging from 0.0 % to 11.7 %; with a weighted average of 5.6 %), (2) the probability of milestone achievement (ranging from 60 % to 100 %; with a weighted average of 80.9 %), (3) the projected payment dates (ranging from 2025 to 2032; with a weighted average of 2029), and (4) the volatility of future revenue (27 %). The weighted average of each of the above inputs was determined based on the relative fair value of each obligation. The use of different assumptions could have a material effect on the estimated fair value amounts.

The following tables summarize the changes in fair value of Level 3 financial instruments measured at fair value on a recurring basis (in millions):

| Contingent Consideration | Other | Total | |||||||||||||||

Balance at December 31, 2023 | $ | $ | $ | ||||||||||||||

| Additions | |||||||||||||||||

| Payments | |||||||||||||||||

| ( | ( | ||||||||||||||||

| Balance at September 30, 2024 | $ | $ | $ | ||||||||||||||

| Contingent Consideration | Other | Total | |||||||||||||||

Balance at December 31, 2022 | $ | $ | $ | ||||||||||||||

| ( | ( | ( | |||||||||||||||

| Balance at September 30, 2023 | $ | $ | $ | ||||||||||||||

20

10. DERIVATIVE INSTRUMENTS AND HEDGING ACTIVITIES

The Company uses derivative financial instruments to manage its currency exchange rate risk and its interest rate risk as summarized below. Notional amounts are stated in United States dollar equivalents at spot exchange rates at the respective dates. The Company does not enter into these arrangements for trading or speculation purposes.

| Notional Amount | |||||||||||

| September 30, 2024 | December 31, 2023 | ||||||||||

| (in millions) | |||||||||||

| Foreign currency forward exchange contracts | $ | $ | |||||||||

| Cross-currency swap contracts | |||||||||||

Derivative financial instruments involve credit risk in the event the counterparty should default. It is the Company's policy to execute such instruments with global financial institutions that the Company believes to be creditworthy. The Company diversifies its derivative financial instruments among counterparties to minimize exposure to any one of these entities. The Company also uses International Swap Dealers Association master-netting agreements. The master-netting agreements provide for the net settlement of all contracts through a single payment in a single currency in the event of default, as defined by the agreements.

The Company uses foreign currency forward exchange contracts and cross-currency swap contracts to manage its exposure to changes in currency exchange rates from (a) future cash flows associated with intercompany transactions and certain local currency expenses expected to occur within approximately one year (designated as cash flow hedges), (b) its net investment in certain foreign subsidiaries (designated as net investment hedges) and (c) foreign currency denominated assets or liabilities (designated as fair value hedges). The Company also uses foreign currency forward exchange contracts that are not designated as hedging instruments to offset the transaction gains and losses associated with revaluation of certain assets and liabilities denominated in currencies other than their functional currencies (resulting principally from intercompany and local currency transactions).

All derivative financial instruments are recognized at fair value in the consolidated condensed balance sheets. For each derivative instrument that is designated as a fair value hedge, the gain or loss on the derivative included in the assessment of hedge effectiveness is recognized immediately to earnings and offsets the loss or gain on the underlying hedged item. The Company reports in Accumulated Other Comprehensive Loss the gain or loss on derivative financial instruments that are designated, and that qualify, as cash flow hedges. The Company reclassifies these gains and losses into earnings in the same line item and in the same period in which the underlying hedged transactions affect earnings. Changes in the fair value of net investment hedges are reported in Accumulated Other Comprehensive Loss as a part of the cumulative translation adjustment and would be reclassified into earnings if the underlying net investment is sold or substantially liquidated. The portion of the change in fair value related to components excluded from the hedge effectiveness assessment are amortized into earnings over the life of the derivative. The gains and losses on derivative financial instruments for which the Company does not elect hedge accounting treatment are recognized in the consolidated statements of operations in each period based upon the change in the fair value of the derivative financial instrument. Cash flows from net investment hedges are reported as investing activities in the consolidated statements of cash flows, and cash flows from all other derivative financial instruments are reported as operating activities.

21

The following table presents the location and fair value amounts of derivative instruments reported in the consolidated condensed balance sheets (in millions):

| Fair Value | ||||||||||||||||||||

| Derivatives designated as hedging instruments | Balance Sheet Location | September 30, 2024 | December 31, 2023 | |||||||||||||||||

| Foreign currency contracts | Other current assets | $ | $ | |||||||||||||||||

| Cross-currency swap contracts | Other assets | $ | $ | |||||||||||||||||

| Foreign currency contracts | Accrued and other liabilities | $ | $ | |||||||||||||||||

| Derivatives not designated as hedging instruments | ||||||||||||||||||||

| Liabilities | ||||||||||||||||||||

| Foreign currency contracts | Accrued and other liabilities | $ | $ | |||||||||||||||||

The following table presents the effect of master-netting agreements and rights of offset on the consolidated condensed balance sheets (in millions):

| Gross Amounts Not Offset in the Consolidated Balance Sheet | |||||||||||||||||||||||||||||||||||

| Gross Amounts Offset in the Consolidated Balance Sheet | |||||||||||||||||||||||||||||||||||

| Net Amounts Presented in the Consolidated Balance Sheet | |||||||||||||||||||||||||||||||||||

| September 30, 2024 | Gross Amounts | Financial Instruments | Cash Collateral Received | Net Amount | |||||||||||||||||||||||||||||||

| Derivative assets | |||||||||||||||||||||||||||||||||||

| Foreign currency contracts | $ | $ | $ | $ | ( | $ | $ | ||||||||||||||||||||||||||||

| Cross-currency swap contracts | $ | $ | $ | $ | $ | $ | |||||||||||||||||||||||||||||

| Derivative liabilities | |||||||||||||||||||||||||||||||||||

| Foreign currency contracts | $ | $ | $ | $ | ( | $ | $ | ||||||||||||||||||||||||||||

| December 31, 2023 | |||||||||||||||||||||||||||||||||||

| Derivative assets | |||||||||||||||||||||||||||||||||||

| Foreign currency contracts | $ | $ | $ | $ | ( | $ | $ | ||||||||||||||||||||||||||||

| Cross-currency swap contracts | $ | $ | $ | $ | $ | $ | |||||||||||||||||||||||||||||

| Derivative liabilities | |||||||||||||||||||||||||||||||||||

| Foreign currency contracts | $ | $ | $ | $ | ( | $ | $ | ||||||||||||||||||||||||||||

The following tables present the effect of derivative and non-derivative hedging instruments on the consolidated condensed statements of operations and consolidated condensed statements of comprehensive income (in millions):

| Amount of Gain or (Loss) Recognized in Other Comprehensive Income on Derivative (Effective Portion) | ||||||||||||||||||||||||||

| Three Months Ended September 30, | Nine Months Ended September 30, | |||||||||||||||||||||||||

| 2024 | 2023 | 2024 | 2023 | |||||||||||||||||||||||

| Cash flow hedges | ||||||||||||||||||||||||||

| Foreign currency contracts | $ | ( | $ | $ | $ | |||||||||||||||||||||

| Net investment hedges | ||||||||||||||||||||||||||

| Cross-currency swap contracts | $ | ( | $ | $ | ( | $ | ( | |||||||||||||||||||

The cross-currency swap contracts have an expiration date of June 15, 2028. At the maturity of the cross-currency swap contracts, the Company will deliver the notional amount of €257.2 million and will receive $300.0 million from the counterparties. The Company receives semi-annual interest payments from the counterparties based on a fixed interest rate until maturity of the agreements.

22

The following tables present the effect of derivative instruments on the consolidated condensed statements of operations (in millions):

| Location and Amount of Gain or (Loss) Recognized in Income | |||||||||||||||||||||||||||||||||||

| Three Months Ended September 30, 2024 | Nine Months Ended September 30, 2024 | ||||||||||||||||||||||||||||||||||

| Cost of sales | Interest income, net | Other non-operating income, net | Cost of sales | Interest income, net | Other non-operating income, net | ||||||||||||||||||||||||||||||

| Total amounts presented in the consolidated condensed statements of operations | $ | ( | $ | $ | $ | ( | $ | $ | |||||||||||||||||||||||||||

| The effects of fair value hedges: | |||||||||||||||||||||||||||||||||||

| Foreign currency contracts: | |||||||||||||||||||||||||||||||||||

| Hedged items | $ | $ | $ | $ | $ | $ | ( | ||||||||||||||||||||||||||||

| Derivatives designated as hedging instruments | $ | $ | $ | $ | $ | $ | |||||||||||||||||||||||||||||

| Amount excluded from effectiveness testing (amortized) | $ | $ | $ | $ | $ | $ | |||||||||||||||||||||||||||||

| The effects of cash flow hedges: | |||||||||||||||||||||||||||||||||||

| Foreign currency contracts: | |||||||||||||||||||||||||||||||||||

| Amount of gain (loss) reclassified from accumulated other comprehensive loss into income | $ | $ | $ | $ | $ | $ | |||||||||||||||||||||||||||||

| The effects of net investment hedges: | |||||||||||||||||||||||||||||||||||

| Cross currency swap contracts: | |||||||||||||||||||||||||||||||||||

| Amount excluded from effectiveness testing | $ | $ | $ | $ | $ | $ | |||||||||||||||||||||||||||||

| The effects of non-designated hedges: | |||||||||||||||||||||||||||||||||||

| Foreign currency contracts | $ | $ | $ | ( | $ | $ | $ | ||||||||||||||||||||||||||||