PART II

Item 5. Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities

Market Information and Holders of Record. Our common stock is traded on the NASDAQ Capital Market under the symbol “PLUG.” As of April 28, 2021, there were approximately 974 record holders of our common stock. However, management believes that a significant number of shares are held by brokers in “street name” and that the number of beneficial stockholders of our common stock exceeds 670,867.

Dividend Policy. We have never declared or paid cash dividends on our common stock and do not anticipate paying cash dividends in the foreseeable future. Any future determination as to the payment of dividends will depend upon capital requirements and limitations imposed by our credit agreements, if any, and such other factors as our Board may consider.

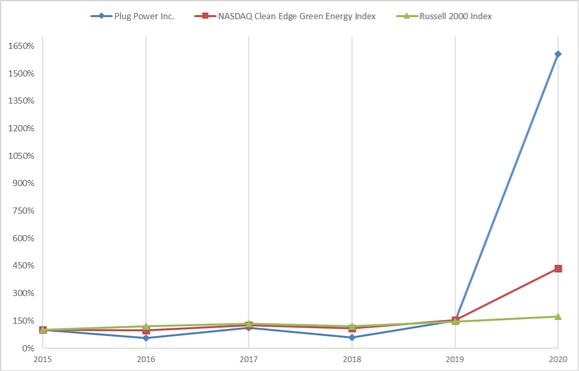

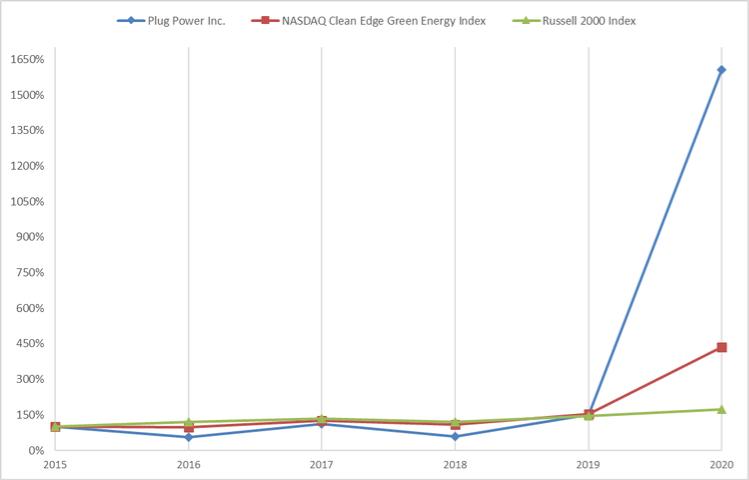

Five-Year Performance Graph. Below is a line graph comparing the percentage change in the cumulative total return of the Company’s common stock, based on the market price of the Company’s common stock, with the total return of companies included within the NASDAQ Clean Edge Green Energy Index (“CELS Index”) and the companies included within the Russell 2000 Index (“RUT Index”) for the period commencing December 31, 2015 and ending December 31, 2020. The calculation of the cumulative total return assumes a $100 investment in the Company’s common stock, the CELS Index and the RUT Index on December 31, 2015 and the reinvestment of all dividends, if any.

Index | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | ||||||||||||

Plug Power Inc. |

| $ | 100.00 |

| $ | 56.87 |

| $ | 111.85 |

| $ | 58.77 |

| $ | 149.76 |

| $ | 1,607.11 |

NASDAQ Clean Edge Green Energy Index | $ | 100.00 | $ | 96.38 | $ | 126.05 | $ | 109.45 | $ | 152.61 | $ | 434.93 | ||||||

Russell 2000 Index | $ | 100.00 | $ | 119.48 | $ | 135.18 | $ | 118.72 | $ | 146.15 | $ | 173.86 | ||||||

| ● | This graph and the accompanying text are not “soliciting material,” are not deemed filed with the SEC and are not to be incorporated by reference in any filing by us under the Securities Act or the Exchange Act, whether made before or after the date hereof and irrespective of any general incorporation language in any such filing. |

| ● | The stock price performance shown on the graph is not necessarily indicative of future price performance. |

| ● | Assuming the investment of $100 on December 31, 2015 and the reinvestment of dividends. The common stock price performance shown on the graph only reflects the change in our company’s common stock price relative to the noted indices and is not necessarily indicative of future price performance. |

34