Table of Contents

As filed with the Securities and Exchange Commission on October 16, 2020

Registration 333-249282

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form S-4/A

AMENDMENT NO.1

TO

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

PUGET ENERGY, INC.

(Exact name of registrant as specified in its charter)

| Washington | 6719 | 91-1969407 | ||

| (State or Other Jurisdiction of Incorporation or Organization) |

(Primary Standard Industrial Classification Code Number) |

(I.R.S. Employer Identification Number) |

355 110th Ave NE

Bellevue, Washington 98004

(425) 454-6363

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

Steve Secrist

Senior Vice President, General Counsel and Chief Ethics and Compliance Officer

Puget Energy, Inc.

355 110th Ave NE

Bellevue, Washington 98004

(425) 454-6363

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies to:

Andrew Bor

Perkins Coie LLP

1201 Third Avenue, Suite 4800

Seattle, Washington 98101-3099

(206) 359-8000

Approximate date of commencement of proposed sale to the public:

As soon as practicable after this Registration Statement becomes effective.

If the securities being registered on this Form are being offered in connection with the formation of a holding company and there is compliance with General Instruction G, check the following box. ☐

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☒ | Accelerated filer | ☐ | |||||

| Non-accelerated filer | ☐ | Smaller reporting company | ☐ | |||||

| Emerging growth company | ☐ | |||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 7(a)(2)(B) of the Securities Act. ☐

If applicable, place an X in the box to designate the appropriate rule provision relied upon in conducting this transaction:

Exchange Act Rule 13e-4(i) (Cross-Border Issuer Tender Offer) ☐

Exchange Act Rule 14d-1(d) (Cross-Border Third-Party Tender Offer) ☐

The registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until this Registration Statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

CALCULATION OF REGISTRATION FEE

|

| ||||||||

| Title of Each Class of Securities to be Registered |

Amount Registered |

Proposed Maximum Offering Price |

Proposed Maximum Aggregate Offering Price (1)(2) |

Amount of Registration Fee | ||||

| 4.100% Senior Secured Notes due 2030 |

$650,000,000 | 100% | $650,000,000 | $70,915.00(3) | ||||

|

| ||||||||

|

| ||||||||

| (1) | Estimated solely for the purpose of calculating the registration fee pursuant to Rule 457(f) under the Securities Act of 1933. |

| (2) | Equals the aggregate principal amount of the securities being registered. |

| (3) | Previously paid in connection with the filing of this Registration Statement. |

Table of Contents

P R O S P E C T U S

Puget Energy, Inc.

OFFER TO EXCHANGE ITS

4.100% Senior Secured Notes due 2030

that have been registered under the Securities Act of 1933, as amended

for any and all of its outstanding

4.100% Senior Secured Notes due 2030

that were issued and sold in a transaction

exempt from registration

under the Securities Act of 1933, as amended

Puget Energy, Inc., a Washington corporation, hereby offers to exchange, upon the terms and conditions set forth in this prospectus and the accompanying letter of transmittal, up to $650 million in aggregate principal amount of its 4.100% Senior Secured Notes due 2030, which we refer to as the “exchange notes,” for the same principal amount of its outstanding 4.100% Senior Secured Notes due 2030, which we refer to as the “original notes.” We refer to the original notes and the exchange notes, collectively, as the “Notes.” The original notes are and the exchange notes will be senior secured obligations and rank and will rank pari passu in right of payment with all of our existing and future senior secured indebtedness and will rank senior to all of our future subordinated indebtedness. Subject to certain exceptions, the Notes are and will be secured by a security interest in (i) substantially all of our assets, which for all practical purposes consists mainly of all of the issued and outstanding stock in our wholly owned operating subsidiary, Puget Sound Energy, Inc. (“PSE”) and (ii) all of our equity interests owned by our parent company, Puget Equico LLC (“Puget Equico”). These same assets also secure our obligations under our senior secured credit facility on an equal and ratable basis and may secure other obligations in the future on an equal and ratable basis.

The terms of the exchange notes are substantially identical to the terms of the original notes, except that the exchange notes will generally be freely transferable and do not contain certain terms with respect to registration rights and liquidated damages. We will issue the exchange notes under the indenture governing the original notes. For a description of the principal terms of the exchange notes, see “Description of Notes.”

The exchange offer will expire at 5:00 p.m. New York City time, on November 16, 2020, unless we extend the offer. At any time prior to the expiration date, you may withdraw your tender of any original notes; otherwise, such tender is irrevocable. We will receive no cash proceeds from the exchange offer.

The exchange notes constitute a new issue of securities for which there is no established trading market. Any original notes not tendered and accepted in the exchange offer will remain outstanding. To the extent original notes are tendered and accepted in the exchange offer, your ability to sell untendered, and tendered but unaccepted, original notes could be adversely affected. Following consummation of the exchange offer, the original notes will continue to be subject to their existing transfer restrictions and we will generally have no further obligations to provide for the registration of the original notes under the Securities Act of 1933, as amended, or the Securities Act. We cannot guarantee that an active trading market will develop or give assurances as to the liquidity of the trading market for either the original notes or the exchange notes. We do not intend to apply for listing of either the original notes or the exchange notes on any exchange or market.

Each broker-dealer that receives exchange notes for its own account pursuant to the exchange offer must acknowledge that it will deliver a prospectus in connection with any resale of its exchange notes. The letter of transmittal states that by so acknowledging and by delivering a prospectus, a broker-dealer will not be deemed to admit that it is an “underwriter” within the meaning of the Securities Act. This prospectus, as it may be amended or supplemented from time to time, may be used by a broker-dealer for a period of 180 days following the consummation of the exchange offer (or until such broker-dealer is no longer required to deliver a prospectus) in connection with resales of exchange notes received in exchange for notes where the notes were acquired by the broker-dealer as a result of market-making activities or other trading activities. See “Plan of Distribution.”

Investing in the exchange notes involves certain risks. Please read “Risk Factors” beginning on page 10 of this prospectus.

This prospectus and the letter of transmittal are first being mailed to all holders of the original notes on or about October 16, 2020.

Neither the Securities and Exchange Commission, or the SEC or the Commission, nor any state securities commission has approved or disapproved of the exchange notes or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

The date of this prospectus is October 16, 2020.

Table of Contents

You should rely only on the information provided in this prospectus or any prospectus supplement. We have not authorized anyone else to provide you with information different from that contained in this prospectus. We are offering to exchange original notes for exchange notes only in jurisdictions where such offer is permitted. You should not assume that the information in this prospectus or any prospectus supplement is accurate as of any other date other than the date on the front of these documents.

No dealer, salesperson or other person has been authorized to give any information or to make any representations other than those contained in this prospectus in connection with the exchange offer, and, if given or made, such information or representations must not be relied upon as having been authorized by Puget Energy. This prospectus does not constitute an offer of any securities other than those to which it relates or an offer or a solicitation by anyone in any jurisdiction in which such offer or solicitation is not authorized or in which the person making such offer or solicitation is not qualified to do so or to anyone to whom it is unlawful to make such offer or solicitation in such jurisdiction. Neither the delivery of this prospectus nor any sale made hereunder shall under any circumstance create an implication that there has been no change in the affairs of Puget Energy since the date hereof of this prospectus.

| Page | ||||

| ii | ||||

| 1 | ||||

| 10 | ||||

| 26 | ||||

| 27 | ||||

| 35 | ||||

| 36 | ||||

| 37 | ||||

| 38 | ||||

| 74 | ||||

| 104 | ||||

| 105 | ||||

| 106 | ||||

| 106 | ||||

| 106 | ||||

| F-1 | ||||

i

Table of Contents

This prospectus and the documents incorporated by reference into this prospectus contain “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. This act provides a “safe harbor” for forward-looking statements to encourage companies to provide prospective information about themselves so long as they identify these as forward-looking and provide meaningful cautionary language identifying important factors that could cause actual results to differ from the projected results. Words or phrases such as “anticipate,” “believe,” “continue,” “could,” “estimate,” “expect,” “future,” “intend,” “may,” “might,” “plan,” “potential,” “predict,” “project,” “should,” “will likely result,” or “will continue” or the negative of such terms or similar expressions are intended to identify certain of these forward-looking statements.

Forward-looking statements reflect our current expectations and involve risks and uncertainties that could cause actual results or outcomes to differ materially from those expressed. Our expectations, beliefs and projections are expressed in good faith and are believed by us and PSE, as applicable, to have a reasonable basis, including without limitation, management’s examination of historical operating trends, data contained in records and other data available from third parties. However, there can be no assurance that our expectations, beliefs or projections will be achieved or accomplished.

In addition to other factors and matters discussed elsewhere in this prospectus, some important factors that could cause our actual results or outcomes to differ materially from past results and those discussed in the forward-looking statements include:

| • | Governmental policies and regulatory actions, including those of the Federal Energy Regulatory Commission (FERC) and the Washington Utilities and Transportation Commission (Washington Commission), that may affect our ability to recover costs and earn a reasonable return, including but not limited to disallowance or delays in the recovery of capital investments and operating costs and discretion over allowed return on investment; |

| • | Changes in, adoption of and compliance with laws and regulations, including decisions and policies concerning the environment, climate change, greenhouse gas or other emissions or by products of electric generation (including coal ash or other substances), natural resources, and fish and wildlife (including the Endangered Species Act) as well as the risk of litigation arising from such matters, whether involving public or private claimants or regulatory investigative or enforcement measures; |

| • | Changes in tax law, related regulations or differing interpretation, or enforcement of applicable law by the Internal Revenue Service (IRS) or other taxing jurisdiction and PSE’s ability to recover costs in a timely manner arising from such changes; |

| • | Inability to realize deferred tax assets and use production tax credits (PTCs) due to insufficient future taxable income; |

| • | Accidents or natural disasters, such as hurricanes, windstorms, earthquakes, floods, fires and landslides, and other acts of God, terrorism, asset-based or cyber-based attacks, pandemic or similar significant events, which can interrupt service and lead to lost revenue, cause temporary supply disruptions and/or price spikes in the cost of fuel and raw materials and impose extraordinary costs; |

| • | The impact of widespread health developments, including the recent global coronavirus (COVID-19) pandemic, and responses to such developments (such as voluntary and mandatory quarantines, including government stay at home orders, as well as shut downs and other restrictions on travel, commercial, social and other activities) could materially and adversely affect, among other things, electric and natural gas demand, customers’ ability to pay, supply chains, availability of skilled work- force, contract counterparties, liquidity and financial markets; |

| • | Commodity price risks associated with procuring natural gas and power in wholesale markets from creditworthy counterparties; |

ii

Table of Contents

| • | Wholesale market disruption, which may result in a deterioration of market liquidity, increase the risk of counterparty default, affect the regulatory and legislative process in unpredictable ways, negatively affect wholesale energy prices and/or impede PSE’s ability to manage its energy portfolio risks and procure energy supply, affect the availability and access to capital and credit markets and/or impact delivery of energy to PSE from its suppliers; |

| • | Financial difficulties of other energy companies and related events, which may affect the regulatory and legislative process in unpredictable ways, adversely affect the availability of and access to capital and credit markets and/or impact delivery of energy to PSE from its suppliers; |

| • | The effect of wholesale market structures (including, but not limited to, regional market designs or transmission organizations) or other related federal initiatives; |

| • | PSE electric or natural gas distribution system failure, blackouts or large curtailments of transmission systems (whether PSE’s or others’), or failure of the interstate natural gas pipeline delivering to PSE’s system, all of which can affect PSE’s ability to deliver power or natural gas to its customers and generating facilities; |

| • | Electric plant generation and transmission system outages, which can have an adverse impact on PSE’s expenses with respect to repair costs, added costs to replace energy or higher costs associated with dispatching a more expensive generation resource; |

| • | The ability to restart generation following a regional transmission disruption; |

| • | The ability of a natural gas or electric plant to operate as intended; |

| • | Changes in climate or weather conditions in the Pacific Northwest, which could have effects on customer usage and PSE’s revenue and expenses; |

| • | Regional or national weather, which could impact PSE’s ability to procure adequate supplies of natural gas, fuel or purchased power to serve its customers and the cost of procuring such supplies; |

| • | Variable hydrological conditions, which can impact streamflow and PSE’s ability to generate electricity from hydroelectric facilities; |

| • | Variable wind conditions, which can impact PSE’s ability to generate electricity from the wind facilities; |

| • | The ability to renew contracts for electric and natural gas supply and the price of renewal; |

| • | Industrial, commercial and residential growth and demographic patterns in the service territories of PSE; |

| • | General economic conditions in the Pacific Northwest, which may impact customer consumption or affect PSE’s accounts receivable; |

| • | The loss of significant customers, changes in the business of significant customers or the condemnation of PSE’s facilities as a result of municipalization or other government action or negotiated settlement, which may result in changes in demand for PSE’s services; |

| • | The failure of information systems or the failure to secure information system data, which may impact the operations and cost of PSE’s customer service, generation, distribution and transmission; |

| • | Opposition and social activism that may hinder PSE’s ability to perform work or construct infrastructure; |

| • | Capital market conditions, including changes in the availability of capital and interest rate fluctuations; |

| • | Employee workforce factors including strikes; work stoppages; absences due to pandemics, accidents, natural disasters or other significant unforeseeable events; availability of qualified employees or the loss of a key executive; |

iii

Table of Contents

| • | The ability to obtain insurance coverage, the availability of insurance for certain specific losses, and the cost of such insurance; |

| • | The ability to maintain effective internal controls over financial reporting and operational processes; |

| • | Changes in our or PSE’s credit ratings, which may have an adverse impact on the availability and cost of capital for us or PSE generally; and |

| • | Deteriorating values of the equity, fixed income and other markets which could significantly impact the value of investments of PSE’s retirement plan, post-retirement medical benefit plan trusts and the funding of obligations thereunder. |

Any forward-looking statement speaks only as of the date on which such statement is made, and, except as required by law, we undertake no obligation to update any forward-looking statement to reflect events or circumstances after the date on which such statement is made or to reflect the occurrence of unanticipated events. New factors emerge from time to time and it is not possible for us to predict all such factors, nor can we assess the impact of any such factor on the business or the extent to which any factor, or combination of factors, may cause results to differ materially from those contained in any forward-looking statement. You are also advised to consult Item 1A—“Risk Factors” in our Annual Report on Form 10-K for the year ended December 31, 2019 and in our Quarterly Report on Form 10-Q for the quarter ended June 30, 2020 and any further disclosures we make on related subjects in our current reports on Form 8-K.

iv

Table of Contents

This section contains a general summary of certain of the information contained in this prospectus and does not include all of the information that may be important to you in making your investment decision. You should read this entire prospectus, including the “Risk Factors” section and the financial statements and notes to those statements contained in this prospectus before making an investment decision. See “Where You Can Find More Information.” As used herein, unless otherwise stated or indicated by context, references to “we,” “our” and “us” refer to Puget Energy, Inc. References to “PSE” are to Puget Sound Energy, Inc., our wholly owned subsidiary.

Puget Energy, Inc.

Overview

We are an energy services holding company incorporated in the state of Washington in 1999.

Substantially all of our operations are conducted through our subsidiary, PSE, a utility company. We also have a wholly-owned, non-regulated subsidiary, Puget LNG, LLC (“Puget LNG”), which was formed in 2016 and has the sole purpose of owning, developing and financing the non-regulated activity of a liquefied natural gas (LNG) facility at the Port of Tacoma, Washington.

We are an indirect wholly-owned subsidiary of Puget Holdings LLC (“Puget Holdings”). All of our common stock is indirectly owned by Puget Holdings. Puget Holdings is owned by a consortium of long-term infrastructure investors including the Canada Pension Plan Investment Board, the British Columbia Investment Management Corporation (BCI), the Alberta Investment Management Corporation (AIMCo), Ontario Municipal Employee Retirement System (OMERS) and PGGM Vermogensbeheer B.V. (collectively, the “Consortium”).

We are the direct parent company of PSE, the oldest and largest electric and natural gas utility headquartered in the state of Washington, primarily engaged in the business of electric transmission, distribution, generation and natural gas distribution. Our business strategy is to generate stable cash flows by offering reliable electric and natural gas service in a cost-effective manner through PSE.

PSE is a public utility incorporated in the state of Washington in 1960. PSE furnishes electric and natural gas services to residential and commercial customers within a service territory covering approximately 6,000 square miles, principally in the Puget Sound region of the state of Washington. At December 31, 2019, PSE had approximately 1,174,036 electric customers, of which approximately 88.0% were residential customers, 11.1% were commercial customers and 0.9% were industrial, transportation and other customers. At December 31, 2019, PSE had approximately 846,780 gas customers, of which approximately 93.0% were residential customers, 6.7% were commercial customers and 0.3% were industrial and transportation customers.

PSE is affected by various seasonal weather patterns and therefore, utility revenues and associated expenses are not generated evenly during the year. Energy usage varies seasonally and monthly, primarily as a result of weather conditions. PSE experiences its highest retail energy sales in the first and fourth quarters of the year. Sales of electricity to wholesale customers also vary by quarter and year depending principally upon fundamental market factors and weather conditions. PSE has a Purchased Gas Adjustment (“PGA”) mechanism in retail natural gas rates to recover variations in natural gas supply and transportation costs. PSE also has a Power Cost Adjustment (“PCA”) mechanism in retail electric rates to recover variations in electricity costs on a shared basis with customers.

Since substantially all of our operations are conducted through PSE, our primary source of funds for the repayment of our indebtedness is dividends paid by PSE, which is subject to numerous restrictions on its ability

1

Table of Contents

to pay dividends, some of which derive from state corporate law, PSE’s gas and electric mortgage indentures and its credit agreements, state regulations and commitments made to the Washington Commission in connection with the Washington Commission’s order approving our merger with Puget Holdings. See “Risk Factors – Risks Relating to Puget Energy’s Corporate Structure – As a holding company, we depend on PSE’s ability to pay dividends”.

Our executive office is located at 355 110th Ave NE, Bellevue, Washington 98004, and our mailing address is P.O. Box 97034, Bellevue, Washington, 98009-9734. Our telephone number is (425) 454-6363. Our website address is www.pugetenergy.com. Information found on our website is not incorporated into or otherwise part of this prospectus.

Summary of the Exchange Offer

In May 2020, we completed a private offering of the original notes. We received aggregate proceeds, before expenses, commissions and discounts, of $650,000,000 from the sale of the original notes.

In connection with the offering of original notes, we entered into a registration rights agreement with the initial purchasers of the original notes in which we agreed to use best efforts to cause an exchange offer registration statement of which this prospectus is a part to be declared effective by the SEC within 180 days of the issuance of the original notes as part of an exchange offer for the original notes. In an exchange offer, you are entitled to exchange your original notes for exchange notes, with substantially identical terms as the original notes. The exchange notes will be accepted for clearance through The Depository Trust Company, or the DTC, and Clearstream Banking SA, or Clearstream, or Euroclear Bank S.A./ N.V., as operator of the Euroclear System, or Euroclear, with a new CUSIP and ISIN number and common code. You should read the discussions under the headings “The Exchange Offer,” “Description of Notes,” and “Book-Entry; Delivery and Form” respectively, for more information about the exchange offer and exchange notes. After the exchange offer is completed, you will no longer be entitled to any exchange or, with limited exceptions, registration rights for your original notes.

| The Exchange Offer |

We are offering to exchange up to $650 million principal amount of the exchange notes for up to $650 million principal amount of the original notes. Original notes may only be exchanged in a principal amount of $2,000 or an integral multiple of $1,000 in excess thereof. |

| The terms of the exchange notes are identical in all material respects to those of the original notes, except the exchange notes will not be subject to transfer restrictions and holders of the exchange notes, with limited exceptions, will have no registration rights. Also, the exchange notes will not include provisions contained in the original notes that required payment of liquidated damages in the event we failed to satisfy our registration obligations with respect to the original notes. |

| Original notes that are not tendered for exchange will continue to be subject to transfer restrictions and, with limited exceptions, will not have registration rights. Therefore, the market for secondary resales of original notes that are not tendered for exchange is likely to be minimal. |

| We will issue registered exchange notes promptly after the expiration of the exchange offer. |

2

Table of Contents

| Expiration Date |

The exchange offer will expire at 5:00 p.m. New York City time, on November 16, 2020, unless we decide to extend the expiration date. Please read “The Exchange Offer—Extensions, Delay in Acceptance, Termination or Amendment” for more information about extending the expiration date. |

| Withdrawal of Tenders |

You may withdraw your tender of original notes at any time prior to the expiration date. We will return to you, without charge, promptly after the expiration or termination of the exchange offer any original notes that you tendered but that were not accepted for exchange. |

| Conditions to the Exchange Offer |

We will not be required to accept original notes for exchange if there is a question as to whether the exchange offer would be unlawful. |

| The exchange offer is not conditioned on any minimum aggregate principal amount of original notes being tendered. Please read “The Exchange Offer—Conditions to the Exchange Offer” for more information about the conditions to the exchange offer. |

| Procedures for Tendering Original Notes |

If your original notes are held through DTC and you wish to participate in the exchange offer, you may do so through DTC’s automated tender offer program. If you tender under this program, you will agree to be bound by the letter of transmittal that we are providing with this prospectus as though you had signed the letter of transmittal. By signing or agreeing to be bound by the letter of transmittal, you will represent to us that, among other things: |

| • | you are not our “affiliate,” as defined in Rule 405 under the Securities Act; |

| • | you are acquiring the exchange notes in the ordinary course of your business; |

| • | you do not intend to participate in the distribution of the original notes or the exchange notes; |

| • | if you are not a broker-dealer, you are not engaged in and do not intend to engage in the distribution of the exchange notes; and |

| • | if you are a broker-dealer or you are using the exchange offer to participate in the distribution of exchange notes, you agree and acknowledge that you could not, under Commission policy, rely on certain no-action letters, and you must comply with the registration and prospectus delivery requirements in connection with a secondary resale transaction. |

| Special Procedures for Beneficial Owner |

If you own a beneficial interest in original notes that are registered in the name of a broker, dealer, commercial bank, trust company or other nominee and you wish to tender the original notes in the exchange offer, please contact the registered holder as soon as possible and instruct the registered holder to tender on your behalf and to comply with our instructions described in this prospectus. |

3

Table of Contents

| Guaranteed Delivery Procedures |

You must tender your original notes according to the guaranteed delivery procedures described in “The Exchange Offer—Guaranteed Delivery Procedures” if any of the following apply: |

| • | you wish to tender your original notes but they are not immediately available; |

| • | you cannot deliver your original notes, the letter of transmittal or any other required documents to the exchange agent prior to the expiration date; or |

| • | you cannot comply with the applicable procedures under DTC’s automated tender offer program prior to the expiration date. |

| Resales |

Except as indicated in this prospectus, we believe that the exchange notes may be offered for resale, resold and otherwise transferred without compliance with the registration and prospectus delivery requirements of the Securities Act provided that: |

| • | you are not our affiliate; |

| • | you are acquiring the exchange notes in the ordinary course of your business; |

| • | you do not intend to participate in the distribution of the original notes or the exchange notes; |

| • | if you are not a broker-dealer, you are not engaged in and do not intend to engage in the distribution of the exchange notes; and |

| • | if you are a broker-dealer or you are using the exchange offer to participate in the distribution of exchange notes, you agree and acknowledge that you could not, under Commission policy, rely on certain no-action letters, and you must comply with the registration and prospectus delivery requirements in connection with a secondary resale transaction. |

| Our belief is based on existing interpretations of the Securities Act by the SEC staff set forth in several no-action letters to third parties. We do not intend to seek our own no-action letter, and there is no assurance that the SEC staff would make a similar determination with respect to the exchange notes. If this interpretation is inapplicable, and you transfer any exchange notes without delivering a prospectus meeting the requirements of the Securities Act or without an exemption from such requirements, you may incur liability under the Securities Act. We do not assume, or indemnify holders against, such liability. |

| Each broker-dealer that is issued exchange notes for its own account in exchange for original notes that were acquired by the broker-dealer as a result of market-making activities or other trading activities must acknowledge that it will deliver a prospectus meeting the requirements of the Securities Act in connection with any resale of the exchange notes during the Exchange Offer Registration Period. See “Plan of Distribution.” |

4

Table of Contents

| United States Federal Income Tax Considerations |

The exchange of original notes for exchange notes will not be a taxable exchange for United States federal income tax purposes. Please see “Material United States Federal Income Tax Considerations.” |

| Use of Proceeds |

We will not receive any proceeds from the issuance of the exchange notes pursuant to the exchange offer. We will pay certain expenses incident to the exchange offer. See “The Exchange Offer—Transfer Taxes.” |

| Registration Rights |

If we fail to complete the exchange offer as required by the registration rights agreement, we may be obligated to pay additional interest to holders of the original notes. Please see “Description of Notes—Registration Rights; Additional Interest” for more information regarding your rights as a holder of the original notes. |

The Exchange Agent

We have appointed Wells Fargo Bank, National Association as exchange agent for the exchange offer. Please direct questions and requests for assistance, requests for additional copies of this prospectus or of the letter of transmittal and requests for the notice of guaranteed delivery to the exchange agent. As described in more detail under the caption “The Exchange Offer—Procedures for Tendering,” if you are not tendering under DTC’s automated tender offer program, you should send the letter of transmittal and any other required documents to the exchange agent as follows:

Wells Fargo Bank, National Association

| By Mail (Registered or Certified Mail Recommended), Overnight Courier or Hand: |

By Facsimile Transmission (for Eligible Institutions Only): |

Confirm Receipt of Tenders by Telephone: | ||

| Wells Fargo Bank, N.A. Corporate Trust Services 608 2nd Avenue South, 12th Floor Minneapolis, MN 55402 ATTN: Bondholder Communications |

(612) 667-6282 | (800) 344-5128 | ||

The Exchange Notes

| Issuer |

Puget Energy, Inc. |

| Notes Offered |

$650,000,000 aggregate principal amount of 4.100% Senior Secured Notes due 2030. |

| Maturity Date |

June 15, 2030. |

| Interest Payment Dates |

June 15 and December 15 of each year, beginning December 15, 2020. |

5

Table of Contents

| Optional Redemption |

At any time prior to March 15, 2030, we may, at our option, redeem the Notes in whole or in part, at any time, at a redemption price equal to the greater of (a) 100% of the principal amount of the Notes then outstanding to be redeemed, and (b) the sum of the present values of the remaining scheduled payments of principal and interest on the Notes being redeemed (not including any portion of such interest payments accrued to the date of redemption) discounted to the redemption date on a semiannual basis (assuming a 360-day year consisting of twelve 30-day months) at the Treasury Rate plus 50 basis points, plus in either case, accrued and unpaid interest, including additional interest, thereon to the date of redemption. |

| At any time on or after March 15, 2030, we may, at our option, redeem the Notes, in whole or in part, at 100% of the principal amount being redeemed plus accrued and unpaid interest thereon to but excluding the redemption date. |

| Ranking |

The Notes will be our senior secured obligations and will: |

| • | rank pari passu in right of payment, to the extent of the value of the Collateral (as described below) securing the Notes, with all of our existing and future senior secured indebtedness (as of March 31, 2020, our obligations under our senior secured credit facility, our term loans, our 6.500% Senior Secured Notes due 2020, our 6.000% Senior Secured Notes due 2021, our 5.625% Senior Secured Notes due 2022, and our 3.650% Senior Secured Notes due 2025 constitute our only other senior secured indebtedness); |

| • | be senior in right of payment to any of our future subordinated indebtedness; and |

| • | be structurally subordinated to all existing and future indebtedness and other liabilities (including trade payables) of our subsidiaries, including PSE. |

| As of June 30, 2020, we had approximately $2.2 billion of senior secured debt outstanding, and PSE had total long-term debt and current liabilities of approximately $5.1 billion, all of which would be structurally senior in right of payment to the Notes. |

| Guarantees |

The Notes will not be guaranteed by any of our subsidiaries or other affiliates. |

| Collateral |

Our obligations under the Notes will be secured by a security interest in substantially all of our assets and our equity interests owned by our direct parent company, Puget Equico, as provided in the indenture. The Collateral, consists mainly of all of the issued and outstanding stock in our wholly owned operating subsidiary, PSE, and our stock. These assets also secure our obligations under our senior secured credit facility, our term loans, and our existing senior secured notes on an equal and ratable basis and may secure other obligations in the |

6

Table of Contents

| future on an equal and ratable basis. See “Description of Notes—Security.” The Collateral will exclude certain of our assets as more specifically set forth in the Collateral Documents, as defined in the section entitled “Description of Notes—Definitions” in this prospectus, including without limitation, any lease, license, contract or agreement to which we are a party, and any of our rights or interest thereunder, if and to the extent that a security interest is prohibited by or in violation of (a) any law, rule or regulation applicable to us or (b) a term, provision or condition of any such lease, license, contract, property right or agreement (unless such law, rule, regulation, term, provision or condition would be rendered ineffective with respect to the creation of the security interest under the Collateral Documents pursuant to Sections 9-406, 9-407, 9-408 or 9-409 of the Uniform Commercial Code as in effect from time to time in the State of New York (or any successor provision or provisions) of any relevant jurisdiction or any other applicable law (including the U.S. Bankruptcy Code) or principles of equity. |

| Change of Control |

Upon the occurrence of a Change of Control Repurchase Event, as defined in the section entitled “Description of Notes—Definitions” in this prospectus, each holder of the Notes will have the right, at the holder’s option, to require us to repurchase all or any part of the holder’s Notes at a purchase price in cash equal to 101% of the principal thereof, plus accrued and unpaid interest, including additional interest, if any, to the date of such purchase in accordance with the procedures set forth in the indenture. See “Description of Notes—Purchase of Notes Upon Change of Control Repurchase Event.” |

| Events of Default |

For a discussion of events that will permit acceleration of the payment of the principal of and accrued interest on the Notes, see “Description of Notes—Events of Default.” |

| Further Issuances |

We may, from time to time, without notice to or the consent of the holders of the Notes, create and issue further Notes equal in rank and having the same maturity, payment terms, redemption features, CUSIP numbers and other terms as the Notes offered by this prospectus. These further Notes may be consolidated and form a single series with the Notes offered by this prospectus. |

| Issuer Obligations |

The obligations to pay the principal of, premium, if any, and interest on the Notes are solely our obligations, and none of Puget Equico (our direct parent company), the members of the Consortium, or any of our subsidiaries will guarantee or provide any credit support for our obligations on the Notes. |

| Covenants |

The indenture governing the Notes contains certain covenants that, among other things, restrict our ability to merge, consolidate or transfer or lease all or substantially all of our assets. These covenants are subject to important exceptions and qualifications as described in this prospectus under the caption “Description of Notes—Certain Covenants.” |

7

Table of Contents

Summary Consolidated Financial Information

The following summary consolidated financial information as of and for each of the three fiscal years in the periods ended December 31, 2019, 2018 and 2017 is derived from our audited consolidated financial statements. The results for the three months ended June 30, 2020 are not necessarily indicative of results for the full fiscal year or any future period. The results of the six month periods ended on June 30, 2020 and 2019 are unaudited. The summary consolidated financial information provided below should be read in conjunction with “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” “Use of Proceeds,” the consolidated financial statements, the related notes, and other financial information, included elsewhere in this prospectus.

| Fiscal Year Ended December 31, | Six Months Ended June 30, |

|||||||||||||||||||

| 2017 | 2018 | 2019 | 2019 | 2020 | ||||||||||||||||

| (dollars in thousands) | ||||||||||||||||||||

| Income statement data: |

||||||||||||||||||||

| Operating revenue |

3,460,276 | 3,346,496 | 3,401,130 | 1,785,769 | 1,697,809 | |||||||||||||||

| Operating expenses |

2,721,170 | 2,792,438 | 2,882,122 | 1,533,194 | 1,455,075 | |||||||||||||||

| Balance sheet and other data (at end of period): |

||||||||||||||||||||

| Cash and cash equivalents |

26,616 | 37,521 | 45,259 | 8,028 | 27,434 | |||||||||||||||

| Debt and preferred stock |

||||||||||||||||||||

| Shareholders’ equity |

3,750,030 | 3,860,758 | 4,000,299 | 3,924,066 | 4,033,738 | |||||||||||||||

| Cash flow statement data: |

||||||||||||||||||||

| Net cash from operating activities |

972,131 | 904,181 | 527,336 | 290,711 | 496,262 | |||||||||||||||

| Net cash from investing activities |

(1,040,330 | ) | (1,070,573 | ) | (952,479 | ) | (474,312 | ) | (438,373 | ) | ||||||||||

| Net cash from financing activities |

63,664 | 185,193 | 435,727 | 152,037 | (67,824 | ) | ||||||||||||||

| Other financial data: |

||||||||||||||||||||

| Capital expenditures |

(1,040,135 | ) | (1,072,670 | ) | (959,387 | ) | (470,335 | ) | (438,477 | ) | ||||||||||

| EBITDA(1) |

1,314,508 | 1,284,163 | 1,284,442 | 669,014 | 631,519 | |||||||||||||||

| (1) | EBITDA provides us with a measure of financial performance independent of items that are beyond the control of management in the short term, such as depreciation and amortization, taxation and interest expense, and unrealized gains or losses on derivative instruments. EBITDA measures our financial performance based on operational factors that management can influence in the short term, namely the cost structure and expenses of the organization. |

EBITDA has limitations as an analytical tool. Material limitations in making the adjustments to our net income (loss) to calculate EBITDA include, but are not limited to:

| • | the items excluded from the calculation of EBITDA generally represent income or expense items that may have a significant effect on our financial results; |

| • | items determined to be non-recurring in nature could, nevertheless, re-occur in the future; |

| • | EBITDA excludes certain tax payments that may represent a reduction in cash available to us; |

| • | EBITDA does not reflect any cash capital expenditure requirements for the assets being depreciated and amortized that may have to be replaced in the future; |

| • | EBITDA does not reflect changes in, or cash requirements for, our working capital needs; and |

8

Table of Contents

| • | EBITDA does not reflect the interest expense associated with, or the cash requirements necessary to service interest or principal payments on, our indebtedness. |

EBITDA is not an alternative to net income, income from continuing operations, or cash flows provided by or used in operating activities as calculated and presented in accordance with GAAP. You should not rely on EBITDA as a substitute for any such GAAP financial measure. We strongly urge you to review the reconciliation presented below, along with our consolidated statements of income, balance sheets, statements of comprehensive income and statements of cash flows. In addition, because EBITDA is not a measure of financial performance under GAAP and is susceptible to varying calculations, EBITDA as presented may differ from and may not be comparable to similarly titled measures used by other companies.

| Fiscal Year Ended December 31, | Six Months Ended June 30, |

|||||||||||||||||||

| 2017 | 2018 | 2019 | 2019 | 2020 | ||||||||||||||||

| (dollars in thousands) | ||||||||||||||||||||

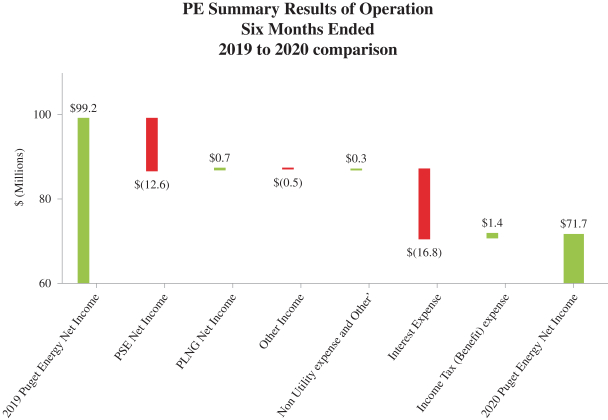

| Consolidated Net Income |

175,194 | 235,622 | 210,708 | 99,202 | 71,703 | |||||||||||||||

| Consolidated Puget Energy Interest Expense (excluding AFUDC) |

(354,802 | ) | (343,795 | ) | (356,638 | ) | (175,786 | ) | (195,677 | ) | ||||||||||

| Consolidated Puget Energy Income Tax Expense |

255,143 | 30,092 | 17,073 | 9,909 | 2,796 | |||||||||||||||

| Consolidated Puget Energy Depreciation & Amortization |

481,969 | 666,432 | 656,323 | 345,412 | 301,681 | |||||||||||||||

| Conservation Amortization |

121,216 | 111,714 | 96,571 | 53,315 | 47,714 | |||||||||||||||

| PSE AFUDC(1) |

10,826 | 13,695 | 14,559 | 6,920 | 7,557 | |||||||||||||||

| Cash Interest Income |

8,318 | 9,679 | 11,456 | 4,499 | 6,189 | |||||||||||||||

| EBITDA |

1,314,508 | 1,284,163 | 1,284,442 | 669,014 | 631,519 | |||||||||||||||

| (1) | Allowance for Funds Used During Construction is a regulatory non-cash return for financing capital projects before being placed in service. |

9

Table of Contents

You should carefully consider the following risks, as well as the other information contained in this prospectus, before exchanging the notes. The risks and uncertainties described below are not the only ones facing us. Additional risks and uncertainties not presently known or currently deemed immaterial may also impair our business operations and our ability to service the Notes.

RISKS RELATING TO THE EXCHANGE OFFER

Because there is no public market for the exchange notes, you may not be able to sell your exchange notes.

The exchange notes will be registered under the Securities Act, but will constitute a new issue of securities with no established trading market. There can be no assurance as to:

| • | The liquidity of any trading market that may develop; |

| • | The ability of holders to sell their exchange notes; or |

| • | The price at which the holders would be able to sell their exchange notes. |

The exchange notes will not be listed on any exchange or market. If a trading market were to develop, the exchange notes might trade at higher or lower prices than their principal amount or purchase price, depending on many factors, including prevailing interest rates, the market for similar securities and our financial performance.

Any market-making activity in the exchange notes will be subject to the limits imposed by the Securities Act and the Exchange Act. There can be no assurance that an active trading market will exist for the exchange notes or that any trading market that does develop will be liquid.

In addition, any original note holder who tenders in the exchange offer for the purpose of participating in a distribution of the exchange notes may be deemed to have received restricted securities and, if so, will be required to comply with the registration and prospectus delivery requirements of the Securities Act in connection with any resale transaction.

Your original notes will not be accepted for exchange if you fail to follow the exchange offer procedures.

We will issue exchange notes pursuant to the exchange offer only after a timely receipt of your original notes, a properly completed and duly executed letter of transmittal and all other required documents. Therefore, if you want to tender your original notes, please allow sufficient time to ensure timely delivery. If we do not receive your original notes, letter of transmittal and other required documents by the expiration date of the exchange offer, we will not accept your original notes for exchange. We are under no duty to give notification of defects or irregularities with respect to the tenders of original notes for exchange. If there are defects or irregularities with respect to your tender of original notes, we may not accept your original notes for exchange.

If you do not exchange your original notes, your original notes will continue to be subject to the existing transfer restrictions and you may be unable to sell your outstanding original notes.

We did not register the original notes and do not intend to do so following the exchange offer. Original notes that are not tendered will therefore continue to be subject to the existing transfer restrictions and may be transferred only in limited circumstances under applicable securities laws. If you do not exchange your original notes, you will lose your right, except in limited circumstances, to have your original notes registered under the federal securities laws. As a result, if you hold original notes after the exchange offer, you may be unable to sell your original notes and the value of the original notes may decline. We have no obligation, except in limited circumstances, and do not currently intend, to file an additional registration statement to cover the resale of original notes that did not tender in the exchange offer or to re-offer to exchange the exchange notes for original notes following the expiration of the exchange offer.

10

Table of Contents

RISKS RELATED TO COVID-19

PSE faces risks related to health epidemics such as the novel Coronavirus (COVID-19) and other outbreaks that could have a material adverse impact on our business and results of operations.

The recent outbreak of the COVID-19 has adversely impacted economic activity and conditions worldwide. We cannot predict the degree that the continued spread of COVID-19 and efforts to contain the virus (including, but not limited to, voluntary and mandatory quarantines, restrictions on travel, limiting gatherings of people, and reduced operations and extended closures of many businesses and institutions) could materially impact our results of operations, financial condition and ongoing operations. The impacts include but are not limited to:

| • | impacting customer demand for electricity and natural gas by our customers, particularly from commercial and industrial customers; |

| • | reducing the availability and productivity of our employees; |

| • | causing us to experience an increase in costs as a result of our emergency measures, delayed payments from our customers and uncollectible accounts; |

| • | causing delays and disruptions in the availability of and timely delivery of materials and components used in our operations; |

| • | causing a deterioration in our financial metrics or the business environment that impacts our credit ratings; |

| • | causing significant disruption in the financial markets which could have a negative impact on our ability to access capital in the future and cost of capital; |

| • | resulting in our inability to meet the requirements of the covenants in our existing credit facilities, including covenants regarding the ratio of total debt to total capitalization; and |

| • | disrupting our ability to meet customer requirements and potentially significantly increase response costs. |

RISKS RELATING TO PUGET ENERGY’S CORPORATE STRUCTURE

As a holding company, we depend on PSE’s ability to pay dividends.

As a holding company with no significant operations of our own, the primary source of funds for the repayment of debt and other expenses, as well as payment of dividends to our shareholder, is cash dividends PSE pays to us. PSE is a separate and distinct legal entity and has no obligation to pay any amounts to us, whether by dividends, loans or other payments. The ability of PSE to pay dividends or make distributions to us, and accordingly, our ability to pay dividends or repay debt or other expenses, will depend on PSE’s earnings, capital requirements and general financial condition. If we do not receive adequate distributions from PSE, we may not be able to meet our obligations or pay dividends.

The payment of dividends by PSE to us is restricted by provisions of certain covenants applicable to long- term debt contained in PSE’s electric and natural gas mortgage indentures. In addition, beginning February 2009, pursuant to the terms of the Washington Commission merger order, PSE may not declare or pay dividends if PSE’s common equity ratio calculated on a regulatory basis is 44.0% or below, except to the extent a lower equity ratio is ordered by the Washington Commission. Also, pursuant to the merger order, PSE’s ability to declare or make any distribution is limited by its’ corporate credit/issuer rating and EBITDA to interest ratio. The common equity ratio, calculated on a regulatory basis, was 48.4% at December 31, 2019 and the EBITDA to interest expense was 5.3 to 1.0 for the twelve-months ended December 31, 2019.

PSE’s ability to pay dividends is also limited by the terms of its credit facilities, pursuant to which PSE is not permitted to pay dividends during any Event of Default (as defined in the facilities), or if the payment of dividends would result in an Event of Default, such as failure to comply with certain financial covenants.

11

Table of Contents

The Notes will be structurally subordinated to claims of creditors of PSE and our other subsidiaries.

The Notes will be structurally subordinated to indebtedness and other liabilities of PSE and our other subsidiaries. Any right that we have pursuant to our equity interest in PSE and Puget LNG to receive any assets of PSE or Puget LNG upon the liquidation or reorganization of PSE or Puget LNG, and the consequent rights of holders of the Notes to realize proceeds from the sale of their assets, will be effectively subordinated to the claims of PSE’s or Puget LNG’s creditors, including any trade creditors, debt holders, secured creditors, taxing authorities and guarantee holders. Accordingly, in the event of a bankruptcy, liquidation or reorganization of PSE or Puget LNG, PSE or Puget LNG, as the case may be, will pay the holders of their indebtedness and any of their trade creditors and any other creditors referenced above before they will be able to distribute any of their assets to us on account of our equity interest in PSE or Puget LNG. The security interest in the pledged stock of PSE will not alter the effective subordination of the Notes to the claims of creditors of PSE.

RISKS RELATING TO PSE’S BUSINESS

The actions of regulators can significantly affect PSE’s earnings, liquidity and business activities.

The rates that PSE is allowed to charge for its services are the single most important item influencing its financial position, results of operations and liquidity. PSE is highly regulated and the rates that it charges its wholesale and retail customers are determined by both the Washington Commission and the FERC.

PSE is also subject to the regulatory authority of the Washington Commission with respect to accounting, operations, the issuance of securities and certain other matters, and the regulatory authority of the FERC with respect to the transmission of electric energy, the sale of electric energy at the wholesale level, accounting and certain other matters. In addition, proceedings with the Washington Commission typically involve multiple stakeholder parties, including consumer advocacy groups and various consumers of energy, who have differing concerns but who have the common objective of limiting rate increases or decreasing rates. Policies and regulatory actions by these regulators could have a material impact on PSE’s financial position, results of operations and liquidity.

PSE’s recovery of costs is subject to regulatory review and its operating income may be adversely affected if its costs are disallowed.

The Washington Commission determines the rates PSE may charge to its electric retail customers based, in part, on historic costs during a particular test year, adjusted for certain normalizing adjustments. Power costs on the other hand, are normalized for market, weather and hydrological conditions projected to occur during the applicable rate year, the ensuing twelve-month period after rates become effective. The Washington Commission determines the rates PSE may charge to its natural gas customers based on historic costs during a particular test year. Natural gas costs are adjusted through the PGA mechanism, as discussed previously. If in a specific year PSE’s costs are higher than the amounts used by the Washington Commission to determine the rates, revenue may not be sufficient to permit PSE to earn its allowed return or to cover its costs. In addition, the Washington Commission has the authority to determine what level of expense and investment is reasonable and prudent in providing electric and natural gas service. If the Washington Commission decides that part of PSE’s costs do not meet the standard, those costs may be disallowed partially or entirely and not recovered in rates. For the aforementioned reasons, the rates authorized by the Washington Commission may not be sufficient to earn the allowed return or recover the costs incurred by PSE in a given period.

PSE is currently subject to a Washington Commission order that requires PSE to share its excess earnings above the authorized rate of return with customers.

The Washington Commission previously approved an electric and natural gas decoupling mechanism for the recovery of its delivery-system and fixed production costs, along with a rate plan and earnings sharing mechanism that requires PSE and its customers to share in any earnings in excess of the authorized rate of return

12

Table of Contents

of 7.39%. The earnings test is done for each service (electric/natural gas) separately, so PSE would be obligated to share the earnings for one service exceeding the authorized rate of return, even if the other service did not exceed the authorized rate of return.

The PCA mechanism, by which variations in PSE’s power costs are apportioned between PSE and its customers pursuant to a graduated scale, could result in significant increases in PSE’s expenses if power costs are significantly higher than the baseline rate.

PSE has a PCA mechanism that provides for recovery of power costs from customers or refunding of power cost savings to customers, as those costs vary from the “power cost baseline” level of power costs which are set, in part, based on normalized assumptions about weather and hydrological conditions. Excess power costs or power cost savings will be apportioned between PSE and its customers pursuant to the graduated scale set forth in the PCA mechanism and will trigger a surcharge or refund when the cumulative deferral trigger is reached. As a result, if power costs are significantly higher than the baseline rate, PSE’s expenses could significantly increase.

PSE may be unable to acquire energy supply resources to meet projected customer needs or may fail to successfully integrate such acquisitions.

PSE projects that future energy needs will exceed current purchased and PSE-controlled power resources. As part of PSE’s business strategy, it plans to acquire additional electric generation and delivery infrastructure to meet customer needs. If PSE cannot acquire additional energy supply resources at a reasonable cost, it may be required to purchase additional power in the open market at a cost that could significantly increase its expenses thus reducing earnings and cash flows. Additionally, PSE may not be able to timely recover some or all of those increased expenses through ratemaking. While PSE expects to identify the benefits of new energy supply resources prior to their acquisition and integration, it may not be able to achieve the expected benefits of such energy supply sources.

PSE’s cash flow and earnings could be adversely affected by potential high prices and volatile markets for purchased power, increased customer demand for energy, recurrence of low availability of hydroelectric resources, outages of its generating facilities or a failure to deliver on the part of its suppliers.

The utility business involves many operating risks. If PSE’s operating expenses, including the cost of purchased power and natural gas, significantly exceed the levels recovered from retail customers, its cash flow and earnings would be negatively affected. Factors which could cause PSE’s purchased power and natural gas costs to be higher than anticipated include, but are not limited to, high prices in western wholesale markets during periods when PSE has insufficient energy resources to meet its energy supply needs and/or purchases in wholesale markets of high volumes of energy at prices above the amount recovered in retail rates due to:

| • | Below normal levels of generation by PSE-owned hydroelectric resources due to low streamflow conditions or precipitation; |

| • | Extended outages of any of PSE-owned generating facilities or the transmission lines that deliver energy to load centers, or the effects of large-scale natural disasters on a substantial portion of distribution infrastructure; and |

| • | Failure of a counterparty to deliver capacity or energy purchased by PSE. |

PSE’s electric generating facilities are subject to operational risks that could result in unscheduled plant outages, unanticipated operation and maintenance expenses and increased power purchase costs.

PSE owns and operates coal, natural gas-fired, hydroelectric, and wind-powered generating facilities. Operation of electric generating facilities involves risks that can adversely affect energy output and efficiency levels or increase expenditures, including:

| • | Facility shutdowns due to a breakdown or failure of equipment or processes; |

13

Table of Contents

| • | Volatility in prices for fuel and fuel transportation; |

| • | Disruptions in the delivery of fuel and lack of adequate inventories; |

| • | Regulatory compliance obligations and related costs, including any required environmental remediation, and any new laws and regulations that necessitate significant investments in our generating facilities; |

| • | Labor disputes; |

| • | Operator error or safety related stoppages; |

| • | Terrorist or other attacks (both cyber-based and/or asset-based); and |

| • | Catastrophic events such as fires, explosions or acts of nature. |

Cyber-attacks, including cyber-terrorism or other information technology security breaches, or information technology failures may disrupt business operations, increase costs, lead to the disclosure of confidential information and damage PSE’s reputation.

Security breaches of PSE’s information technology infrastructure, including cyber-attacks and cyber- terrorism, or other failures of PSE’s information technology infrastructure could lead to disruptions of PSE’s production and distribution operations, and otherwise adversely impact PSE’s ability to safely and effectively operate electric and natural gas systems and serve customers. In addition, an attack on or failure of information technology systems could result in the unauthorized release of customer, employee or Company data that is crucial to PSE’s operational security or could adversely affect PSE’s ability to deliver and collect on customer bills. Such security breaches of PSE’s information technology infrastructure could adversely affect our operations and business reputation, diminish customer confidence, subject PSE to financial liability or increased regulation, expose PSE to fines or material legal claims and liability and adversely affect our financial results. PSE has implemented preventive, detective and remediation measures to manage these risks, and maintains cyber risk insurance to mitigate the effects of these events. Nevertheless, these may not effectively protect all of PSE’s systems all of the time. To the extent that the occurrence of any of these cyber- events is not fully covered by insurance, it could adversely affect PSE’s financial condition and results of operations.

Natural disasters and catastrophic events, including terrorist acts, may adversely affect PSE’s business.

Events such as fires, earthquakes, explosions, floods, tornadoes, terrorist acts, and other similar occurrences, could damage PSE’s operational assets, including utility facilities, information technology infrastructure, distributed generation assets and pipeline assets. Such events could likewise damage the operational assets of PSE’s suppliers or customers. These events could disrupt PSE’s ability to meet customer requirements, significantly increase PSE’s response costs, and significantly decrease PSE’s revenues.

Unanticipated events or a combination of events, failure in resources needed to respond to events, or a slow or inadequate response to events may have an adverse impact on PSE’s operations, financial condition, and results of operations. The availability of insurance covering catastrophic events, sabotage and terrorism may be limited or may result in higher deductibles, higher premiums, and more restrictive policy terms.

PSE is subject to the commodity price, delivery and credit risks associated with the energy markets.

In connection with matching PSE’s energy needs and available resources, PSE engages in wholesale sales and purchases of electric capacity and energy and, accordingly, is subject to commodity price risk, delivery risk, credit risk and other risks associated with these activities. Credit risk includes the risk that counterparties owing PSE money or energy will breach their obligations for delivery of energy supply or contractually required payments related to PSE’s energy supply portfolio. Should the counterparties to these arrangements fail to perform, PSE may be forced to enter into alternative arrangements. In that event, PSE’s financial results could be adversely affected. Although PSE takes into account the expected probability of default by counterparties, the actual exposure to a default by a particular counterparty could be greater than predicted.

14

Table of Contents

Costs of compliance with environmental, climate change and endangered species laws are significant and the costs of compliance with new and emerging laws and regulations and the incurrence of associated liabilities could adversely affect PSE’s results of operations.

PSE’s operations are subject to extensive federal, state and local laws and regulations relating to environmental issues, including air emissions and climate change, endangered species protection, remediation of contamination, avian protection, waste handling and disposal, decommissioning, water protection and siting new facilities. To fulfill these legal requirements, PSE must spend significant sums of money to comply with these measures including resource planning, remediation, monitoring, analysis, mitigation measures, pollution control equipment and emissions related abatement and fees. New environmental laws and regulations affecting PSE’s operations may be adopted, and new interpretations of existing laws and regulations could be adopted or become applicable to PSE or its facilities. Compliance with these or other future regulations could require significant expenditures by PSE and adversely affect PSE financially. In addition, PSE may not be able to recover all of its costs for such expenditures through electric and natural gas rates, in a timely manner, at current levels in the future.

Under current law, PSE is also generally responsible for any on-site liabilities associated with the environmental condition of the facilities that it currently owns or operates or has previously owned or operated. The occurrence of a material environmental liability or new regulations governing such liability could result in substantial future costs and have a material adverse effect on PSE’s results of operations and financial condition.

Specific to climate change, Washington State has adopted both renewable portfolio standards and GHG legislation, including the Clean Energy Infrastructure Act, and PSE anticipates compliance with these requirements and the EPA set CO2 emission standards with specific state goals.

PSE’s inability to adequately develop or acquire the necessary infrastructure to comply with new and emerging laws and regulations could have a material adverse impact on our business and results of operations.

Potential changes in regulatory standards, impacts of new and existing laws and regulations, including environmental laws and regulations, and the need to obtain various regulatory approvals create uncertainty surrounding our energy resource portfolio. The current abundance of low, stably priced natural gas, together with environmental, regulatory, and other concerns surrounding coal-fired generation resources, fossil fuel infrastructure bans, and energy resource portfolio requirements, including those related to renewables development and energy efficiency measures, create strategic challenges as to the appropriate generation portfolio and fuel diversification mix.

In expressing concerns about the environmental and climate-related impacts from continued extraction, transportation, delivery and combustion of fossil fuels, environmental advocacy groups and other third parties have in recent years undertaken greater efforts to oppose the permitting and construction of fossil fuel infrastructure projects. These efforts may increase in scope and frequency depending on a number of variables, including the future course of Municipal, State and Federal environmental regulation and the increasing financial resources devoted to these opposition activities. PSE cannot predict the effect that any such opposition may have on our ability to develop and construct fossil fuel infrastructure projects in the future.

PSE’s operating results fluctuate on a seasonal and quarterly basis and can be impacted by various impacts of climate change.

PSE’s business is seasonal and weather patterns can have a material impact on its revenue, expenses and operating results. Demand for electricity is greater in the winter months associated with heating. Accordingly, PSE’s operations have historically generated less revenue and income when weather conditions are milder in winter. In the event that PSE experiences unusually mild winters, its results of operations and financial condition could be adversely affected. PSE’s hydroelectric resources are also dependent on snow conditions in the Pacific Northwest.

15

Table of Contents

PSE may be adversely affected by extreme events in which PSE is not able to promptly respond, repair and restore the electric and natural gas infrastructure system.

PSE must maintain an emergency planning and training program to allow PSE to quickly respond to extreme events. Without emergency planning, PSE is subject to availability of outside contractors during an extreme event which may impact the quality of service provided to PSE’s customers and also require significant expenditures by PSE. In addition, a slow or ineffective response to extreme events may have an adverse effect on earnings as customers may be without electricity and natural gas for an extended period of time.

PSE depends on its work force and third party vendors to perform certain important services and may be negatively affected by its inability to attract and retain professional and technical employees or the unavailability of vendors.

PSE is subject to workforce factors, including but not limited to loss or retirement of key personnel and availability of qualified personnel. PSE’s ability to implement a workforce succession plan is dependent upon PSE’s ability to employ and retain skilled professional and technical workers. Without a skilled workforce, PSE’s ability to provide quality service to PSE’s customers and to meet regulatory requirements could affect PSE’s earnings. Also, the costs associated with attracting and retaining qualified employees could reduce earnings and cash flows.

PSE continues to be concerned about the availability of skilled workers for special complex utility functions. PSE also hires third party vendors to perform a variety of normal business functions, such as power plant maintenance, data warehousing and management, electric transmission, electric and natural gas distribution construction and maintenance, certain billing and metering processes, call center overflow and credit and collections. The unavailability of skilled workers or unavailability of such vendors could adversely affect the quality and cost of PSE’s natural gas and electric service and accordingly PSE’s results of operations.

Potential municipalization may adversely affect PSE’s financial condition.

PSE may be adversely affected if we experience a loss in the number of our customers due to municipalization or other related government action. When a town or city in PSE’s service territory establishes its own municipal-owned utility, it acquires PSE’s assets and takes over the delivery of energy services that PSE provides. Although PSE is compensated in connection with the town or city’s acquisition of its assets, any such loss of customers and related revenue could negatively affect PSE’s future financial condition.

Technological developments may have an adverse impact on PSE’s financial condition.

Advances in power generation, energy efficiency and other alternative energy technologies, such as solar generation, could lead to more wide-spread use of these technologies, thereby reducing customer demand for the energy supplied by PSE which could negatively impact PSE’s revenue and financial condition.

RISKS RELATING TO OUR AND PSE’S BUSINESS

Challenges relating to the construction or future operation of the Tacoma LNG facility could adversely affect Puget Energy and PSE’s operations.

PSE and our subsidiary, Puget LNG, currently are constructing the Tacoma LNG facility at the Port of Tacoma, a jointly owned facility intended to provide peak-shaving services to PSE’s natural gas customers, and to provide LNG as fuel primarily to the maritime market. Puget LNG has entered into one fuel supply agreement with a maritime customer, and is marketing the facility’s expected output to other potential customers. Scheduled to be completed in 2021, delays in the facility’s construction and operation or in its ability to timely deliver fuel to customers could expose Puget LNG to damages under one or more fuel supply contracts, which could unfavorably impact our return on investment.

16

Table of Contents

Puget Energy’s and PSE’s businesses are dependent on their ability to successfully access capital.

We rely, and PSE relies, on access to internally generated funds, bank borrowings through multi-year committed credit facilities and short-term money markets as sources of liquidity and longer-term debt markets to fund PSE’s utility construction program and other capital expenditure requirements of PSE. If we or PSE are unable to access capital on reasonable terms, our ability to pursue improvements or acquisitions, including generating capacity, which may be necessary for future growth, could be adversely affected. Capital and credit market disruptions, a downgrade of our or PSE’s credit rating or the imposition of restrictions on borrowings under our or PSE’s credit facilities in the event of a deterioration of financial ratios, may increase our and PSE’s cost of borrowing or adversely affect the ability to access one or more financial markets.

The amount of Puget Energy’s and PSE’s debt could adversely affect its liquidity and results of operations.