N-CSRS

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED

SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-09277

VIKING MUTUAL FUNDS

(Exact name of registrant as specified in

charter)

|

1 Main Street North, Minot, ND |

|

58703 |

|

(Address of principal offices) |

|

(Zip code) |

Brent Wheeler and/or Kevin Flagstad, PO Box 500, Minot, ND 58702

(Name and address of agent for service)

Registrant’s telephone number, including area code: 701-852-5292

Date of fiscal year end: July 31st

Date of reporting period: January 31, 2020

Item 1. REPORT TO SHAREHOLDERS

Viking Mutual Funds

Kansas Municipal Fund

Maine Municipal Fund

Nebraska Municipal Fund

Oklahoma Municipal Fund

Viking Tax-Free Fund for Montana

Viking Tax-Free Fund for North Dakota

Semi-Annual Report | January 31, 2020

|

Investment

Adviser |

Principal

Underwriter |

|

Transfer Agent |

Custodian |

|

Independent

Registered Public Accounting Firm

|

|

*The Funds are distributed through Integrity Funds Distributor, LLC. Member FINRA

IMPORTANT NOTE: Beginning on January 1, 2021, as permitted by regulations adopted by the Securities and Exchange Commission, paper copies of the Integrity Viking Funds’ (the “Funds”) annual and semi-annual shareholder reports will no longer be sent by mail, unless you specifically request paper copies of the shareholder reports from the Funds or from your financial intermediary, such as a broker-dealer or bank. Instead, shareholder reports will be available on the Funds’ website (https://www.integrityvikingfunds.com/Documents), and you will be notified by mail each time a report is posted and provided with a website link to access the report.

If you hold Fund shares through a financial intermediary and you already elected to receive shareholder reports electronically through your financial intermediary, you will not be affected by this change and you need not take any action. You may elect to receive shareholder reports and other communications from the Funds electronically by notifying your financial intermediary.

You may elect to receive all future shareholder reports in paper free of charge. You can inform your financial intermediary that you wish to continue receiving paper copies of your shareholder reports, or if you are a direct investor, by calling the Funds at 800-601-5593. Your election to receive reports in paper will apply to all Funds you hold directly or through your financial intermediary, as applicable.

DEAR SHAREHOLDERS:

Enclosed is the report of the operations for the Kansas Municipal Fund, Maine Municipal Fund, Nebraska Municipal Fund, Oklahoma Municipal Fund, Viking Tax-Free Fund for Montana, and Viking Tax-Free Fund for North Dakota (each a “Fund”, and collectively the “Funds”) for the six months ended January 31, 2020. Each Fund’s portfolio and related financial statements are presented within for your review.

Economic Recap

During the six-month period, the U.S. economy continued to grow as economic activity rose at a moderate rate and the labor market remained strong as noted by the Federal Open Market Committee (“FOMC”) in their January 29th statement. However, the FOMC cited “implications of global developments” as well as muted inflation pressures as they lowered the federal funds rate twice during the period taking the fed funds target rate to 1-1/2 to 1-3/4 percent as of the end of January.

Municipal Bond Market Recap

During the six-month period, the municipal bond market posted strong returns, with five of the six months posting positive returns. Longer investment grade bonds performed best during the period, followed by intermediate, and finally shorter maturity bonds. Higher rated investment grade bonds performed in line with their lower rated, counterparts throughout the curve. Municipal bonds performed well as rates declined during the period on a dovish tone from the Federal Reserve. Other factors contributing to positive performance for municipal bonds was strong demand and persistent net negative issuance, in which more municipal bonds are maturing or being called than are being issued.

Fund Performance

The Kansas Municipal Fund, Maine Municipal Fund, Nebraska Municipal Fund, Oklahoma Municipal Fund, Viking Tax-Free Fund for Montana, and Viking Tax-Free Fund for North Dakota had total returns of 2.34%*, 1.84%*, 1.99%*, 2.29%*, 2.17%*, and 2.07%* for Class A shares and 2.47%*, 1.97%*, 2.22%*, 2.42%*, 2.30%*, and 2.10%* for Class I shares, respectively, during the semi-annual period ended January 31. This compares to the Bloomberg Barclays Capital Municipal Index’s return of 3.35% and the Morningstar Municipal Single State Intermediate Category which returned 2.37% for the period. The Funds underperformed the index during the period due to having a lower duration than the index. Additionally, the index is unmanaged and it is not possible to invest directly in an unmanaged index.

The current 3.8% Medicare surtax on investment income established by the Patient Protection and Affordable Care Act (municipals are exempt) combined with the high marginal tax rates at the federal and state levels boost the appeal of tax-exempt income. The federal marginal tax rate for taxpayers with adjusted gross incomes of $518,400 ($622,050 for married filing jointly) in 2020 is 37.0%. The after-tax yield of a 10-year U.S. Treasury Note yielding 1.52% falls to approximately 0.90% at the 37.0% federal tax rate plus the 3.8% Medicare surtax.

Finally, we recommend that shareholders view their investment as long-term. As difficult as they may be, periods of panic (and euphoria) tend to be transitory in nature and it’s the long-term investors that may be rewarded with the long-term benefits of tax-free income and relatively low volatility that muni bonds have provided for decades.

If you would like more frequent updates, please visit the Fund’s website at www.integrityvikingfunds.com for daily prices along with pertinent Fund information.

Sincerely,

The Portfolio Management Team

The views expressed are those of The Portfolio Management Team of Viking Fund Management, LLC (“Viking Fund Management”, “VFM”, or the “Adviser”). The views are subject to change at any time in response to changing circumstances in the market and are not intended to predict or guarantee the future performance of any individual security, market sector, the markets generally, or any of the funds in the Integrity Viking family of funds.

*Performance does not include applicable front-end or contingent deferred sales charges, which would have reduced the performance. For Kansas Municipal Fund, Maine Municipal Fund, Nebraska Municipal Fund, Oklahoma Municipal Fund, Viking Tax-Free Fund for Montana, and Viking Tax-Free Fund for North Dakota, the total annual fund operating expense ratio (before expense waivers and reimbursements and including acquired fund fees and expenses) as of the most recent fiscal year-end was 1.18%, 1.41%, 1.21%, 1.20%, 1.17%, and 1.32% respectively, for Class A, and 0.93%, 1.16%, 0.96%, 0.95%, 0.92%, and 1.09% respectively, for Class I. The net annual fund operating expense ratio (after expense waivers and reimbursements and excluding acquired fund fees and expenses) as of the most recent fiscal year-end was 0.98%, 0.98%, 0.98%, 0.98%, 0.98%, and 0.98%, respectively, for Class A and 0.73%, 0.73%, 0.73%, 0.73%, 0.73%, and 0.73%, respectively, for Class A. The Fund’s investment adviser has contractually agreed to waive fees and reimburse expenses through November 29, 2020 so that total annual fund operating expenses after fee waivers and expense reimbursements (excluding taxes, brokerage fees, commissions, extraordinary and non-recurring expenses, and acquired fund fees and expenses) do not exceed 0.98% for Class A and 0.73% for Class I of average daily net assets. This expense limitation agreement may only be terminated or modified prior to November 29, 2020 with the approval of the Fund’s Board of Trustees.

Performance data quoted above is historical. Past performance is no guarantee of future results. Current performance may be higher or lower than the performance data quoted. The principal value and investment return of an investment will fluctuate so that your shares, when redeemed, may be worth more or less than the original cost. You can obtain performance data current to the most recent month end (available within seven business days of the most recent month end) by calling 800-276-1262.

You should consider each Fund’s investment objectives, risks, charges, and expenses carefully before investing. For this and other important information, please obtain a Fund prospectus at no cost from your financial adviser and read it carefully before investing.

Bond prices and therefore the value of bond funds decline as interest rates rise. Because each Fund invests in securities of a single state, the Funds are more susceptible to factors adversely impacting the respective state than a municipal bond fund that does not concentrate its securities in a single state.

For investors subject to the alternative minimum tax, a portion of the each Fund’s dividends may be taxable. Distributions of capital gains are generally taxable.

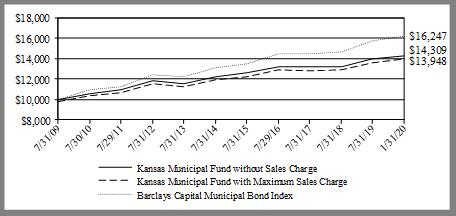

KANSAS MUNICIPAL FUND

PERFORMANCE (unaudited)

Comparison of change in value of a $10,000 investment

Average Annual Total Returns for the periods ended January 31, 2020

|

|

1 year |

3 year |

5 year |

10 year |

Since Inception* |

|

Class A Without sales charge |

6.46% |

3.58% |

2.53% |

3.30% |

4.08% |

|

Class A With sales charge (2.50%) |

3.80% |

2.73% |

2.02% |

3.04% |

3.99% |

|

Class I Without sales charge |

6.63% |

N/A |

N/A |

N/A |

3.82% |

|

* November 15, 1990 for Class A; November 1, 2017 for Class I |

|||||

The total annual fund operating expense ratio for class A and I (before expense waivers and reimbursements and including acquired fund fees and expenses) as of the most recent fiscal year-end was 1.18% and 0.93%, respectively. The net annual fund operating expense ratio (after expense waivers and reimbursements and excluding acquired fund fees and expenses) as of the most recent fiscal year-end was 0.98% and 0.73%, respectively. The Fund’s investment adviser has contractually agreed to waive fees and reimburse expenses through November 29, 2020 so that total annual fund operating expenses after fee waivers and expense reimbursements (excluding taxes, brokerage fees, commissions, extraordinary and non-recurring expenses, and acquired fund fees and expenses) do not exceed 0.98% and 0.73%, respectively, of average daily net assets. This expense limitation agreement may only be terminated or modified prior to November 29, 2020 with the approval of the Fund’s Board of Trustees.

Performance data quoted above is historical. Past performance is no guarantee of future results. Current performance may be higher or lower than the performance data quoted. The principal value and investment return of an investment will fluctuate so that your shares, when redeemed, may be worth more or less than the original cost. You can obtain performance data current to the most recent month end (available within seven business days of the most recent month end) by calling 800-276-1262.

The table and graph above do not reflect the deduction of taxes that a shareholder would pay on Fund distributions and redemptions of Fund shares.

The graph comparing the Fund’s performance to a benchmark index provides you with a general sense of how the Fund performed. To put this information in context, it may be helpful to understand the special differences between the two. The Fund’s total return for the period shown appears with and without sales charges and includes Fund expenses and management fees. A securities index measures the performance of a theoretical portfolio. Unlike a fund, the index is unmanaged; there are no expenses that affect the results. In addition, few investors could purchase all of the securities to match the index. If they could, transaction costs and other expenses would be incurred. All Fund and benchmark returns include reinvested dividends. The results prior to August 1, 2009 were achieved while the Fund was managed by a different investment adviser. The current investment adviser may produce different investment results than those achieved by the previous investment adviser.

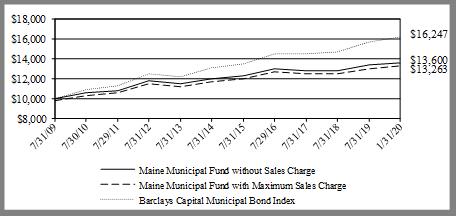

MAINE MUNICIPAL FUND

PERFORMANCE (unaudited)

Comparison of change in value of a $10,000 investment

Average Annual Total Returns for the periods ended January 31, 2020

|

|

1 year |

3 year |

5 year |

10 year |

Since Inception* |

|

Class A Without sales charge |

4.90% |

2.92% |

1.77% |

2.85% |

4.13% |

|

Class A With sales charge (2.50%) |

2.30% |

2.04% |

1.25% |

2.59% |

4.03% |

|

Class I Without sales charge |

5.06% |

N/A |

N/A |

N/A |

2.96% |

|

* December 5, 1991 for Class A; November 1, 2017 for Class I |

|||||

The total annual fund operating expense ratio for class A and I (before expense waivers and reimbursements and including acquired fund fees and expenses) as of the most recent fiscal year-end was 1.41% and 1.16%, respectively. The net annual fund operating expense ratio (after expense waivers and reimbursements and excluding acquired fund fees and expenses) as of the most recent fiscal year-end was 0.98% and 0.73%, respectively. The Fund’s investment adviser has contractually agreed to waive fees and reimburse expenses through November 29, 2020 so that total annual fund operating expenses after fee waivers and expense reimbursements (excluding taxes, brokerage fees, commissions, extraordinary and non-recurring expenses, and acquired fund fees and expenses) do not exceed 0.98% and 0.73%, respectively, of average daily net assets. This expense limitation agreement may only be terminated or modified prior to November 29, 2020 with the approval of the Fund’s Board of Trustees.

Performance data quoted above is historical. Past performance is no guarantee of future results. Current performance may be higher or lower than the performance data quoted. The principal value and investment return of an investment will fluctuate so that your shares, when redeemed, may be worth more or less than the original cost. You can obtain performance data current to the most recent month end (available within seven business days of the most recent month end) by calling 800-276-1262.

The table and graph above do not reflect the deduction of taxes that a shareholder would pay on Fund distributions and redemptions of Fund shares.

The graph comparing the Fund’s performance to a benchmark index provides you with a general sense of how the Fund performed. To put this information in context, it may be helpful to understand the special differences between the two. The Fund’s total return for the period shown appears with and without sales charges and includes Fund expenses and management fees. A securities index measures the performance of a theoretical portfolio. Unlike a fund, the index is unmanaged; there are no expenses that affect the results. In addition, few investors could purchase all of the securities to match the index. If they could, transaction costs and other expenses would be incurred. All Fund and benchmark returns include reinvested dividends. The results prior to August 1, 2009 were achieved while the Fund was managed by a different investment adviser. The current investment adviser may produce different investment results than those achieved by the previous investment adviser.

NEBRASKA MUNICIPAL FUND

PERFORMANCE (unaudited)

Comparison of change in value of a $10,000 investment

Average Annual Total Returns for the periods ended January 31, 2020

|

|

1 year |

3 year |

5 year |

10 year |

Since Inception* |

|

Class A Without sales charge |

5.85% |

3.73% |

2.43% |

3.34% |

3.62% |

|

Class A With sales charge (2.50%) |

3.25% |

2.87% |

1.92% |

3.07% |

3.52% |

|

Class I Without sales charge |

6.12% |

N/A |

N/A |

N/A |

3.69% |

|

* November 17, 1993 for Class A; November 1, 2017 for Class I |

|||||

The total annual fund operating expense ratio for class A and I (before expense waivers and reimbursements and including acquired fund fees and expenses) as of the most recent fiscal year-end was 1.21% and 0.96%, respectively. The net annual fund operating expense ratio (after expense waivers and reimbursements and excluding acquired fund fees and expenses) as of the most recent fiscal year-end was 0.98% and 0.73%, respectively. The Fund’s investment adviser has contractually agreed to waive fees and reimburse expenses through November 29, 2020 so that total annual fund operating expenses after fee waivers and expense reimbursements (excluding taxes, brokerage fees, commissions, extraordinary and non-recurring expenses, and acquired fund fees and expenses) do not exceed 0.98% and 0.73%, respectively, of average daily net assets. This expense limitation agreement may only be terminated or modified prior to November 29, 2020 with the approval of the Fund’s Board of Trustees.

Performance data quoted above is historical. Past performance is no guarantee of future results. Current performance may be higher or lower than the performance data quoted. The principal value and investment return of an investment will fluctuate so that your shares, when redeemed, may be worth more or less than the original cost. You can obtain performance data current to the most recent month end (available within seven business days of the most recent month end) by calling 800-276-1262.

The table and graph above do not reflect the deduction of taxes that a shareholder would pay on Fund distributions and redemptions of Fund shares.

The graph comparing the Fund’s performance to a benchmark index provides you with a general sense of how the Fund performed. To put this information in context, it may be helpful to understand the special differences between the two. The Fund’s total return for the period shown appears with and without sales charges and includes Fund expenses and management fees. A securities index measures the performance of a theoretical portfolio. Unlike a fund, the index is unmanaged; there are no expenses that affect the results. In addition, few investors could purchase all of the securities to match the index. If they could, transaction costs and other expenses would be incurred. All Fund and benchmark returns include reinvested dividends. The results prior to August 1, 2009 were achieved while the Fund was managed by a different investment adviser. The current investment adviser may produce different investment results than those achieved by the previous investment adviser.

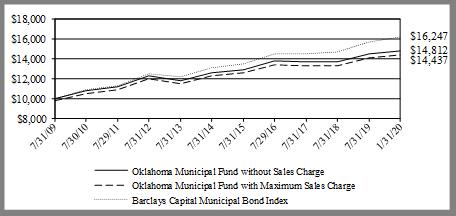

OKLAHOMA MUNICIPAL FUND

PERFORMANCE (unaudited)

Comparison of change in value of a $10,000 investment

Average Annual Total Returns for the periods ended January 31, 2020

|

|

1 year |

3 year |

5 year |

10 year |

Since Inception* |

|

Class A Without sales charge |

6.79% |

3.73% |

2.59% |

3.61% |

3.87% |

|

Class A With sales charge (2.50%) |

4.16% |

2.84% |

2.08% |

3.35% |

3.76% |

|

Class I Without sales charge |

7.05% |

N/A |

N/A |

N/A |

3.87% |

|

* September 25, 1996 for Class A; November 1, 2017 for Class I |

|||||

The total annual fund operating expense ratio for class A and I (before expense waivers and reimbursements and including acquired fund fees and expenses) as of the most recent fiscal year-end was 1.20% and 0.95%, respectively. The net annual fund operating expense ratio (after expense waivers and reimbursements and excluding acquired fund fees and expenses) as of the most recent fiscal year-end was 0.98%. and 0.73%, respectively The Fund’s investment adviser has contractually agreed to waive fees and reimburse expenses through November 29, 2020 so that total annual fund operating expenses after fee waivers and expense reimbursements (excluding taxes, brokerage fees, commissions, extraordinary and non-recurring expenses, and acquired fund fees and expenses) do not exceed 0.98% and 0.73%, respectively, of average daily net assets. This expense limitation agreement may only be terminated or modified prior to November 29, 2020 with the approval of the Fund’s Board of Trustees.

Performance data quoted above is historical. Past performance is no guarantee of future results. Current performance may be higher or lower than the performance data quoted. The principal value and investment return of an investment will fluctuate so that your shares, when redeemed, may be worth more or less than the original cost. You can obtain performance data current to the most recent month end (available within seven business days of the most recent month end) by calling 800-276-1262.

The table and graph above do not reflect the deduction of taxes that a shareholder would pay on Fund distributions and redemptions of Fund shares.

The graph comparing the Fund’s performance to a benchmark index provides you with a general sense of how the Fund performed. To put this information in context, it may be helpful to understand the special differences between the two. The Fund’s total return for the period shown appears with and without sales charges and includes Fund expenses and management fees. A securities index measures the performance of a theoretical portfolio. Unlike a fund, the index is unmanaged; there are no expenses that affect the results. In addition, few investors could purchase all of the securities to match the index. If they could, transaction costs and other expenses would be incurred. All Fund and benchmark returns include reinvested dividends. The results prior to August 1, 2009 were achieved while the Fund was managed by a different investment adviser. The current investment adviser may produce different investment results than those achieved by the previous investment adviser.

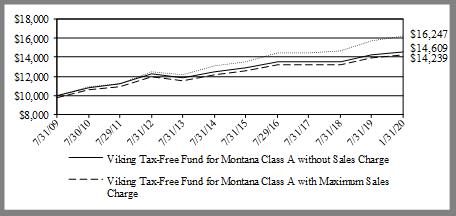

VIKING TAX-FREE FUND FOR MONTANA

PERFORMANCE (unaudited)

Comparison of change in value of a $10,000 investment

Average Annual Total Returns for the periods ended January 31, 2020

|

1 year |

3 year |

5 year |

10 year |

Since Inception* |

|

|

Class A Without sales charge |

6.25% |

3.64% |

2.42% |

3.43% |

3.83% |

|

Class A With sales charge (2.50%) |

3.64% |

2.78% |

1.89% |

3.17% |

3.70% |

|

Class I Without sales charge |

6.52% |

3.86% |

N/A |

N/A |

2.38% |

|

* August 3, 1999 for Class A; August 1, 2016 for Class I |

|||||

The total annual fund operating expense ratio for Class A and I (before expense waivers and reimbursements and including acquired fund fees and expenses) as of the most recent fiscal year-end was 1.17% and 0.92%, respectively. The net annual fund operating expense ratio (after expense waivers and reimbursements and excluding acquired fund fees and expenses) as of the most recent fiscal year-end was 0.98% and 0.73%, respectively. The Fund’s investment adviser has contractually agreed to waive fees and reimburse expenses through November 29, 2020 so that total annual fund operating expenses after fee waivers and expense reimbursements (excluding taxes, brokerage fees, commissions, extraordinary and non-recurring expenses, and acquired fund fees and expenses) do not exceed 0.98% and 0.73%, respectively, of average daily net assets. This expense limitation agreement may only be terminated or modified prior to November 29, 2020 with the approval of the Fund’s Board of Trustees.

Performance data quoted above is historical. Past performance is no guarantee of future results. Current performance may be higher or lower than the performance data quoted. The principal value and investment return of an investment will fluctuate so that your shares, when redeemed, may be worth more or less than the original cost. You can obtain performance data current to the most recent month end (available within seven business days of the most recent month end) by calling 800-276-1262.

The table and graph above do not reflect the deduction of taxes that a shareholder would pay on Fund distributions and redemptions of Fund shares.

The graph comparing the Fund’s performance to a benchmark index provides you with a general sense of how the Fund performed. To put this information in context, it may be helpful to understand the special differences between the two. The Fund’s total return for the period shown appears with and without sales charges and includes Fund expenses and management fees. A securities index measures the performance of a theoretical portfolio. Unlike a fund, the index is unmanaged; there are no expenses that affect the results. In addition, few investors could purchase all of the securities to match the index. If they could, transaction costs and other expenses would be incurred. All Fund and benchmark returns include reinvested dividends.

VIKING TAX-FREE FUND FOR NORTH DAKOTA

PERFORMANCE (unaudited)

Comparison of change in value of a $10,000 investment

Average Annual Total Returns for the periods ended January 31, 2020

|

|

1 year |

3 year |

5 year |

10 year |

Since Inception* |

|

Class A Without sales charge |

5.67% |

3.17% |

2.31% |

3.24% |

3.88% |

|

Class A With sales charge (2.50%) |

3.01% |

2.31% |

1.80% |

2.98% |

3.75% |

|

Class I Without sales charge |

5.83% |

3.43% |

N/A |

N/A |

2.11% |

|

* August 3, 1999 for Class A; August 1, 2016 for Class I |

|||||

The total annual fund operating expense ratio for class A and I (before expense waivers and reimbursements and including acquired fund fees and expenses) as of the most recent fiscal year-end was 1.32% and 1.09%, respectively. The net annual fund operating expense ratio (after expense waivers and reimbursements and excluding acquired fund fees and expenses) as of the most recent fiscal year-end was 0.98% and 0.73%, respectively. The Fund’s investment adviser has contractually agreed to waive fees and reimburse expenses through November 29, 2020 so that total annual fund operating expenses after fee waivers and expense reimbursements (excluding taxes, brokerage fees, commissions, extraordinary and non-recurring expenses, and acquired fund fees and expenses) do not exceed 0.98% and 0.73%, respectively, of average daily net assets. This expense limitation agreement may only be terminated or modified prior to November 29, 2020 with the approval of the Fund’s Board of Trustees.

Performance data quoted above is historical. Past performance is no guarantee of future results. Current performance may be higher or lower than the performance data quoted. The principal value and investment return of an investment will fluctuate so that your shares, when redeemed, may be worth more or less than the original cost. You can obtain performance data current to the most recent month end (available within seven business days of the most recent month end) by calling 800-276-1262.

The table and graph above do not reflect the deduction of taxes that a shareholder would pay on Fund distributions and redemptions of Fund shares.

The graph comparing the Fund’s performance to a benchmark index provides you with a general sense of how the Fund performed. To put this information in context, it may be helpful to understand the special differences between the two. The Fund’s total return for the period shown appears with and without sales charges and includes Fund expenses and management fees. A securities index measures the performance of a theoretical portfolio. Unlike a fund, the index is unmanaged; there are no expenses that affect the results. In addition, few investors could purchase all of the securities to match the index. If they could, transaction costs and other expenses would be incurred. All Fund and benchmark returns include reinvested dividends.

KANSAS MUNICIPAL FUND

PORTFOLIO MARKET SECTORS January 31, 2020 (unaudited)

|

General Obligation |

40.6% |

|

Health Care |

17.9% |

|

Utilities |

13.5% |

|

Other Revenue |

9.5% |

|

Pre-Refunded |

9.2% |

|

Cash Equivalents and Other |

5.3% |

|

Education |

2.6% |

|

Transportation |

1.4% |

|

100.0% |

Market sectors are breakdowns of the Fund’s portfolio holdings into specific investment classes.

These percentages are based on net assets and are subject to change.

SCHEDULE OF INVESTMENTS January 31, 2020 (unaudited)

|

Principal |

Fair |

|||

|

|

Amount |

|

Value |

|

|

MUNICIPAL BONDS (94.7%) |

||||

|

|

||||

|

Education (2.6%) |

||||

|

Johnson County Community College Foundation Inc 4.000% 11/15/2023 |

$ |

870,000 |

$ |

966,666 |

|

Kansas Development Finance Authority 5.000% 06/01/2027 |

250,000 |

264,055 |

||

|

Kansas Development Finance Authority 3.000% 10/01/2044 |

500,000 |

516,155 |

||

|

|

|

1,746,876 |

||

|

General Obligation (40.6%) |

||||

|

*Allen County Unified School District No 257 3.000% 09/01/2038 |

1,000,000 |

1,043,170 |

||

|

City of Bonner Springs KS 3.000% 09/01/2044 |

1,060,000 |

1,107,234 |

||

|

Bourbon County Unified School District No 234 Fort Scott 5.000% 09/01/2027 |

250,000 |

297,023 |

||

|

Bourbon County Unified School District No 234 Fort Scott 5.000% 09/01/2028 |

250,000 |

294,798 |

||

|

Bourbon County Unified School District No 234 Fort Scott 5.000% 09/01/2029 |

250,000 |

292,695 |

||

|

Bourbon County Unified School District No 234 Fort Scott 5.000% 09/01/2030 |

250,000 |

291,498 |

||

|

Bourbon County Unified School District No 234 Fort Scott 5.000% 09/01/2031 |

500,000 |

579,950 |

||

|

County of Clay KS 4.000% 10/01/2036 |

500,000 |

546,430 |

||

|

Douglas County Unified School District No 348 Baldwin City 4.000% 09/01/2030 |

250,000 |

285,437 |

||

|

*Franklin County Unified School District No 290 Ottawa 5.000% 09/01/2040 |

3,000,000 |

3,511,620 |

||

|

Geary County Unified School District No 475 4.000% 09/01/2033 |

350,000 |

394,706 |

||

|

Greenwood County Unified School District No 389 Eureka 4.000% 09/01/2021 |

150,000 |

156,285 |

||

|

City of Hillsboro KS 3.000% 09/01/2024 |

100,000 |

104,592 |

||

|

City of Hillsboro KS 3.000% 09/01/2027 |

225,000 |

236,183 |

||

|

City of Hillsboro KS 3.000% 09/01/2028 |

230,000 |

239,195 |

||

|

City of Hillsboro KS 3.000% 09/01/2029 |

240,000 |

247,346 |

||

|

Johnson & Miami Counties Unified School District No 230 Spring Hills 5.000% 09/01/2039 |

2,000,000 |

2,417,440 |

||

|

Johnson County Unified School District No 231 Gardner Edgerton 5.000% 10/01/2025 |

250,000 |

289,107 |

||

|

City of Junction City KS 5.000% 09/01/2025 |

5,000 |

5,003 |

||

|

Leavenworth County Unified School District No 453 4.000% 09/01/2037 |

650,000 |

732,654 |

||

|

Leavenworth County Unified School District No 464 4.000% 09/01/2031 |

500,000 |

570,150 |

||

|

County of Linn KS 3.000% 07/01/2036 |

1,100,000 |

1,158,872 |

||

|

Lyon County Unified School District No 253 Emporia 4.000% 09/01/2039 |

750,000 |

843,382 |

||

|

Lyon County Unified School District No 253 Emporia 4.000% 09/01/2048 |

1,000,000 |

1,109,150 |

||

|

Miami County Unified School District No 368 Paola 5.000% 09/01/2027 |

10,000 |

10,710 |

||

|

Neosho County Unified School District No 413 4.000% 09/01/2031 |

250,000 |

270,605 |

||

|

Rice County Unified School District No 444 4.000% 09/01/2031 |

710,000 |

837,736 |

||

|

Riley County Unified School District No 378 Riley 4.000% 09/01/2028 |

680,000 |

808,874 |

||

|

Riley County Unified School District No 383 Manhattan Ogden 4.000% 09/01/2039 |

1,000,000 |

1,136,480 |

||

|

County of Scott KS 5.000% 04/01/2032 |

500,000 |

601,655 |

||

|

Sedgwick County Unified School District No 261 Haysville 5.000% 11/01/2021 |

5,000 |

5,010 |

||

|

Sedgwick County Unified School District No 262 Valley Center 5.000% 09/01/2035 |

405,000 |

468,265 |

||

|

County of Seward KS 5.000% 08/01/2034 |

240,000 |

245,222 |

||

|

Seward County Unified School District No 480 Liberal 5.000% 09/01/2034 |

500,000 |

555,170 |

||

|

Seward County Unified School District No 480 Liberal 5.000% 09/01/2033 |

85,000 |

93,825 |

||

|

City of South Hutchinson KS 4.000% 10/01/2038 |

355,000 |

389,985 |

||

|

County of Thomas KS 3.000% 12/01/2047 |

1,000,000 |

1,025,010 |

||

|

City of Topeka KS 3.000% 08/15/2020 |

500,000 |

505,225 |

||

|

City of Topeka KS 3.000% 08/15/2021 |

1,000,000 |

1,030,590 |

||

|

City of Topeka KS 3.000% 08/15/2022 |

500,000 |

525,325 |

||

|

City of Wichita KS 4.500% 09/01/2022 |

150,000 |

150,075 |

||

|

City of Wichita KS 4.750% 09/01/2027 |

180,000 |

180,079 |

||

|

Wyandotte County Unified School District No 500 Kansas City 5.000% 09/01/2026 |

1,000,000 |

1,237,920 |

||

|

|

|

26,831,681 |

||

|

Health Care (17.9%) |

||||

|

Ashland Public Building Commission 5.000% 09/01/2030 |

1,020,000 |

1,121,908 |

||

|

Ashland Public Building Commission 5.000% 09/01/2035 |

500,000 |

544,670 |

||

|

Ashland Public Building Commission 5.000% 09/01/2032 |

550,000 |

616,649 |

||

|

Kansas Development Finance Authority 5.000% 03/01/2028 |

755,000 |

757,590 |

||

|

Kansas Development Finance Authority 4.125% 11/15/2027 |

100,000 |

108,269 |

||

|

City of Lawrence KS 5.000% 07/01/2043 |

1,500,000 |

1,813,590 |

||

|

City of Manhattan KS 5.000% 11/15/2023 |

250,000 |

278,110 |

||

|

City of Manhattan KS 5.000% 11/15/2024 |

250,000 |

278,267 |

||

|

City of Manhattan KS 5.000% 11/15/2029 |

500,000 |

550,770 |

||

|

City of Olathe KS 4.000% 09/01/2028 |

250,000 |

260,980 |

||

|

City of Olathe KS 4.000% 09/01/2030 |

295,000 |

306,962 |

||

|

University of Kansas Hospital Authority 4.000% 09/01/2040 |

500,000 |

544,085 |

||

|

University of Kansas Hospital Authority 5.000% 09/01/2035 |

500,000 |

582,500 |

||

|

University of Kansas Hospital Authority 4.000% 09/01/2048 |

1,000,000 |

1,111,240 |

||

|

University of Kansas Hospital Authority 5.000% 09/01/2048 |

2,000,000 |

2,442,940 |

||

|

University of Kansas Hospital Authority 3.000% 03/01/2041 |

500,000 |

511,265 |

||

|

|

11,829,795 |

|||

|

Other Revenue (9.5%) |

||||

|

Dickson County Public Building Commission 4.000% 08/01/2038 |

750,000 |

861,337 |

||

|

Johnson County Public Building Commission 4.000% 09/01/2022 |

405,000 |

436,987 |

||

|

Kansas Development Finance Authority 4.125% 05/01/2031 |

500,000 |

503,815 |

||

|

Kansas Development Finance Authority 3.000% 11/01/2033 |

1,000,000 |

1,062,740 |

||

|

City of Manhattan KS 5.000% 12/01/2026 |

395,000 |

395,932 |

||

|

City of Manhattan KS 4.500% 12/01/2025 |

500,000 |

515,025 |

||

|

*City of Manhattan KS 5.000% 12/01/2032 |

1,000,000 |

1,032,940 |

||

|

Topeka Public Building Commission 5.000% 06/01/2022 |

255,000 |

257,871 |

||

|

Washington County Public Building Commission 4.000% 09/01/2028 |

100,000 |

107,496 |

||

|

City of Wichita KS 4.000% 09/01/2038 |

1,000,000 |

1,104,520 |

||

|

|

6,278,663 |

|||

|

Pre-Refunded (9.2%) |

||||

|

Jackson County Unified School District No 336 Holton 5.000% 09/01/2029 |

135,000 |

149,614 |

||

|

Jackson County Unified School District No 336 Holton 5.000% 09/01/2034 |

140,000 |

155,155 |

||

|

Jackson County Unified School District No 336 Holton 5.000% 09/01/2029 |

115,000 |

127,418 |

||

|

Jackson County Unified School District No 336 Holton 5.000% 09/01/2034 |

110,000 |

121,878 |

||

|

Kansas Power Pool 5.000% 12/01/2031 |

750,000 |

775,208 |

||

|

Leavenworth County Unified School District No 458 5.000% 09/01/2029 |

500,000 |

572,200 |

||

|

Leavenworth County Unified School District No 469 4.000% 09/01/2030 |

320,000 |

343,994 |

||

|

Miami County Unified School District No 368 Paola 5.000% 09/01/2027 |

135,000 |

143,845 |

||

|

Miami County Unified School District No 368 Paola 5.000% 09/01/2027 |

105,000 |

111,896 |

||

|

City of Olathe KS 4.000% 09/01/2030 |

150,000 |

157,037 |

||

|

County of Seward KS 5.000% 08/01/2034 |

260,000 |

265,530 |

||

|

Seward County Unified School District No 480 Liberal 4.250% 09/01/2039 |

500,000 |

542,675 |

||

|

Seward County Unified School District No 480 Liberal 5.000% 09/01/2033 |

85,000 |

93,741 |

||

|

Seward County Unified School District No 480 Liberal 5.000% 09/01/2033 |

330,000 |

364,023 |

||

|

Washington County Public Building Commission 5.000% 09/01/2032 |

500,000 |

553,585 |

||

|

Washington County Public Building Commission 5.000% 09/01/2037 |

400,000 |

441,780 |

||

|

Washington County Public Building Commission 4.000% 09/01/2028 |

500,000 |

540,025 |

||

|

City of Wichita KS 5.000% 11/15/2029 |

300,000 |

320,841 |

||

|

Wyandotte County Unified School District No 202 Turner 5.000% 09/01/2025 |

250,000 |

285,530 |

||

|

|

6,065,975 |

|||

|

Transportation (1.4%) |

||||

|

State of Kansas Department of Transportation 5.000% 09/01/2033 |

500,000 |

598,740 |

||

|

State of Kansas Department of Transportation 5.000% 09/01/2035 |

250,000 |

298,565 |

||

|

|

897,305 |

|||

|

Utilities (13.5%) |

||||

|

*Kansas Municipal Energy Agency 5.750% 07/01/2038 |

1,000,000 |

1,136,690 |

||

|

Kansas Municipal Energy Agency 5.000% 04/01/2030 |

250,000 |

297,935 |

||

|

Kansas Municipal Energy Agency 5.000% 04/01/2032 |

500,000 |

589,405 |

||

|

Kansas Municipal Energy Agency 5.000% 04/01/2033 |

745,000 |

876,001 |

||

|

Kansas Municipal Energy Agency 5.000% 04/01/2038 |

1,000,000 |

1,161,330 |

||

|

Kansas Municipal Energy Agency 5.000% 04/01/2035 |

300,000 |

350,883 |

||

|

Kansas Power Pool 4.500% 12/01/2028 |

500,000 |

513,385 |

||

|

Kansas Power Pool 4.000% 12/01/2031 |

500,000 |

564,580 |

||

|

City of Topeka KS Combined Utility Revenue 4.000% 08/01/2023 |

500,000 |

551,920 |

||

|

Wyandotte County Kansas City Unified Government Utility System Revenue 5.000% 09/01/2036 |

250,000 |

264,822 |

||

|

*Wyandotte County Kansas City Unified Government Utility System Revenue 5.000% 09/01/2032 |

1,250,000 |

1,371,962 |

||

|

Wyandotte County Kansas City Unified Government Utility System Revenue 5.000% 09/01/2035 |

500,000 |

585,390 |

||

|

Wyandotte County Kansas City Unified Government Utility System Revenue 5.000% 09/01/2028 |

500,000 |

615,610 |

||

|

|

8,879,913 |

|||

|

|

||||

|

TOTAL MUNICIPAL BONDS (COST: $58,836,728) |

$ |

62,530,208 |

||

|

|

||||

|

OTHER ASSETS LESS LIABILITIES (5.3%) |

$ |

3,483,247 |

||

|

|

||||

|

NET ASSETS (100.0%) |

$ |

66,013,455 |

||

|

|

||||

|

*Indicates all or a portion of bonds are segregated by the custodian to cover when-issued or delayed-delivery purchases when they occur. As of January 31, 2020 there were no such purchases. |

||||

|

|

||||

|

|

||||

|

The accompanying notes are an integral part of these financial statements. |

||||

MAINE MUNICIPAL FUND

PORTFOLIO MARKET SECTORS January 31, 2020 (unaudited)

|

General Obligation |

29.3% |

|

Health Care |

21.7% |

|

Education |

18.7% |

|

Housing |

11.4% |

|

Utilities |

5.4% |

|

Cash Equivalents and Other |

4.1% |

|

Transportation |

3.8% |

|

Other Revenue |

3.8% |

|

Pre-Refunded |

1.8% |

|

100.0% |

Market sectors are breakdowns of the Fund’s portfolio holdings into specific investment classes.

These percentages are based on net assets.

SCHEDULE OF INVESTMENTS January 31, 2020 (unaudited)

|

Principal |

Fair |

|||

|

|

Amount |

|

Value |

|

|

MUNICIPAL BONDS (95.9%) |

||||

|

|

||||

|

Education (18.7%) |

||||

|

Maine Educational Loan Authority 4.450% 12/01/2025 |

$ |

100,000 |

$ |

102,709 |

|

*Maine Health & Higher Educational Facilities Authority 5.000% 07/01/2039 |

750,000 |

864,105 |

||

|

Maine Health & Higher Educational Facilities Authority 5.000% 07/01/2034 |

250,000 |

288,633 |

||

|

Maine Health & Higher Educational Facilities Authority 4.750% 07/01/2031 |

250,000 |

262,778 |

||

|

Maine Health & Higher Educational Facilities Authority 4.000% 07/01/2024 |

270,000 |

291,651 |

||

|

*Maine Health & Higher Educational Facilities Authority 5.000% 07/01/2026 |

940,000 |

1,166,944 |

||

|

|

2,976,820 |

|||

|

General Obligation (29.3%) |

||||

|

City of Auburn ME 4.500% 09/01/2022 |

100,000 |

109,371 |

||

|

Town of Bar Harbor ME 4.000% 10/15/2022 |

105,000 |

113,857 |

||

|

Town of Bar Harbor ME 4.000% 10/15/2023 |

140,000 |

156,122 |

||

|

City of Biddeford ME 4.000% 10/01/2026 |

250,000 |

298,010 |

||

|

Town of Brunswick ME 2.500% 11/01/2041 |

500,000 |

504,580 |

||

|

City of Lewiston ME 2.750% 03/15/2038 |

100,000 |

101,907 |

||

|

City of Lewiston ME 2.750% 03/15/2039 |

250,000 |

253,500 |

||

|

City of Lewiston ME 2.750% 03/15/2040 |

250,000 |

253,010 |

||

|

State of Maine 4.000% 06/01/2020 |

150,000 |

151,557 |

||

|

City of Portland ME 4.250% 05/01/2029 |

150,000 |

150,377 |

||

|

City of Portland ME 4.125% 10/01/2029 |

100,000 |

100,106 |

||

|

City of Portland ME 5.000% 08/01/2021 |

125,000 |

133,571 |

||

|

City of Portland ME 5.000% 08/01/2022 |

125,000 |

133,776 |

||

|

Regional School Unit No 26 3.000% 09/01/2044 |

475,000 |

495,463 |

||

|

City of Saco ME 4.000% 04/01/2028 |

100,000 |

100,551 |

||

|

Town of Scarborough ME 4.000% 11/01/2028 |

100,000 |

110,886 |

||

|

Maine School Administrative District No 51 4.000% 10/15/2029 |

100,000 |

113,062 |

||

|

*Maine School Administrative District No 28 4.000% 05/01/2036 |

500,000 |

574,970 |

||

|

City of Waterville ME 4.000% 07/01/2025 |

135,000 |

141,857 |

||

|

City of Waterville ME 4.000% 06/01/2024 |

115,000 |

130,221 |

||

|

Wells Ogunquit Community School District 3.000% 11/01/2023 |

400,000 |

430,248 |

||

|

Wells Ogunquit Community School District 4.000% 11/01/2024 |

100,000 |

115,339 |

||

|

|

4,672,341 |

|||

|

Health Care (21.7%) |

||||

|

Maine Health & Higher Educational Facilities Authority 4.500% 07/01/2031 |

190,000 |

192,681 |

||

|

Maine Health & Higher Educational Facilities Authority 5.250% 07/01/2023 |

190,000 |

193,697 |

||

|

Maine Health & Higher Educational Facilities Authority 5.000% 07/01/2020 |

250,000 |

254,420 |

||

|

Maine Health & Higher Educational Facilities Authority 5.000% 07/01/2040 |

250,000 |

254,120 |

||

|

*Maine Health & Higher Educational Facilities Authority 5.000% 07/01/2029 |

1,000,000 |

1,150,050 |

||

|

Maine Health & Higher Educational Facilities Authority 5.000% 07/01/2030 |

500,000 |

577,770 |

||

|

Maine Health & Higher Educational Facilities Authority 5.000% 07/01/2031 |

500,000 |

572,125 |

||

|

Maine Health & Higher Educational Facilities Authority 3.000% 07/01/2039 |

250,000 |

259,945 |

||

|

|

3,454,808 |

|||

|

Housing (11.4%) |

||||

|

Maine State Housing Authority 4.000% 11/15/2035 |

435,000 |

462,562 |

||

|

Maine State Housing Authority 3.000% 11/15/2036 |

400,000 |

412,380 |

||

|

*Maine State Housing Authority 4.000% 11/15/2044 |

500,000 |

536,515 |

||

|

Maine State Housing Authority 3.350% 11/15/2044 |

155,000 |

158,630 |

||

|

Maine State Housing Authority 5.000% 06/15/2024 |

250,000 |

253,942 |

||

|

|

1,824,029 |

|||

|

Other Revenue (3.8%) |

||||

|

Maine Governmental Facilities Authority 4.000% 10/01/2024 |

200,000 |

210,094 |

||

|

Maine Municipal Bond Bank 4.000% 11/01/2038 |

125,000 |

132,110 |

||

|

Maine Municipal Bond Bank 5.000% 11/01/2025 |

125,000 |

140,315 |

||

|

Maine Municipal Bond Bank 5.000% 11/01/2027 |

100,000 |

120,143 |

||

|

Maine Municipal Bond Bank 4.900% 11/01/2024 |

5,000 |

5,013 |

||

|

|

607,675 |

|||

|

Pre-Refunded (1.8%) |

||||

|

Town of Gorham ME 4.000% 10/01/2023 |

100,000 |

102,319 |

||

|

Maine Health & Higher Educational Facilities Authority 5.000% 07/01/2020 |

50,000 |

50,882 |

||

|

Maine Health & Higher Educational Facilities Authority 4.500% 07/01/2031 |

10,000 |

10,156 |

||

|

Maine Health & Higher Educational Facilities Authority 5.250% 07/01/2023 |

10,000 |

10,187 |

||

|

Maine Health & Higher Educational Facilities Authority 5.000% 07/01/2023 |

15,000 |

17,160 |

||

|

Regional School Unit No 1 Lower Kennebec Region School Unit 5.000% 02/01/2026 |

100,000 |

103,950 |

||

|

|

294,654 |

|||

|

Transportation (3.8%) |

||||

|

Maine Turnpike Authority 4.000% 07/01/2032 |

250,000 |

273,412 |

||

|

City of Portland ME General Airport Revenue 5.000% 07/01/2022 |

100,000 |

109,838 |

||

|

City of Portland ME General Airport Revenue 5.000% 07/01/2023 |

100,000 |

112,592 |

||

|

City of Portland ME General Airport Revenue 5.000% 07/01/2024 |

100,000 |

112,509 |

||

|

|

608,351 |

|||

|

Utilities (5.4%) |

||||

|

Kennebunk Light & Power District 5.000% 08/01/2022 |

315,000 |

316,273 |

||

|

Portland Water District 3.000% 11/01/2039 |

500,000 |

|

540,275 |

|

|

|

856,548 |

|||

|

|

||||

|

TOTAL MUNICIPAL BONDS (COST: $14,554,324) |

$ |

15,295,226 |

||

|

|

||||

|

OTHER ASSETS LESS LIABILITIES (4.1%) |

$ |

657,528 |

||

|

|

||||

|

NET ASSETS (100.0%) |

$ |

15,952,754 |

||

|

|

||||

|

*Indicates all or a portion of bonds are segregated by the custodian to cover when-issued or delayed-delivery purchases when they occur. As of July 31, 2018 there were no such purchases. |

||||

|

#When-issued purchase as of January 31, 2020 |

||||

|

|

||||

|

|

||||

|

The accompanying notes are an integral part of these financial statements. |

||||

NEBRASKA MUNICIPAL FUND

PORTFOLIO MARKET SECTORS January 31, 2020 (unaudited)

|

General Obligation |

34.3% |

|

Utilities |

25.3% |

|

Pre-Refunded |

23.9% |

|

Health Care |

6.0% |

|

Transportation |

3.6% |

|

Cash Equivalents and Other |

3.4% |

|

Housing |

2.1% |

|

Other Revenue |

0.9% |

|

Education |

0.5% |

|

100.0% |

Market sectors are breakdowns of the Fund’s portfolio holdings into specific investment classes.

These percentages are based on net assets and are subject to change.

SCHEDULE OF INVESTMENTS January 31, 2020 (unaudited)

|

Principal |

Fair |

|||

|

|

Amount |

|

Value |

|

|

MUNICIPAL BONDS (96.6%) |

||||

|

|

||||

|

Education (0.5%) |

||||

|

Nebraska Educational Health & Social Services Finance Authority 5.050% 09/01/2030 |

$ |

250,000 |

$ |

266,250 |

|

|

||||

|

General Obligation (34.3%) |

||||

|

Plattsmouth School District 3.000% 12/15/2039 |

1,000,000 |

1,024,350 |

||

|

#Ponca Public Schools 3.000% 12/15/2026 |

355,000 |

384,483 |

||

|

Fremont School District 1.100% 12/15/2020 |

100,000 |

100,104 |

||

|

*Omaha School District 5.000% 12/15/2029 |

1,630,000 |

2,046,253 |

||

|

Omaha School District 3.000% 12/15/2042 |

1,000,000 |

1,049,500 |

||

|

Elkhorn School District 4.000% 12/15/2034 |

300,000 |

336,372 |

||

|

Elkhorn School District 4.000% 12/15/2030 |

500,000 |

577,355 |

||

|

Elkhorn School District 4.000% 12/15/2034 |

500,000 |

586,965 |

||

|

Elkhorn School District 4.000% 12/15/2037 |

300,000 |

353,652 |

||

|

Elkhorn School District 5.000% 06/15/2022 |

475,000 |

519,617 |

||

|

Douglas County School District No 59/NE 3.500% 06/15/2043 |

500,000 |

521,475 |

||

|

Westside Community Schools 5.000% 12/01/2038 |

235,000 |

268,676 |

||

|

Westside Community Schools 5.000% 12/01/2039 |

250,000 |

285,375 |

||

|

Hall County Airport Authority 5.000% 07/15/2030 |

410,000 |

436,306 |

||

|

Hall County Airport Authority 5.000% 07/15/2031 |

435,000 |

458,725 |

||

|

County of Kearney NE 4.000% 06/01/2024 |

350,000 |

390,628 |

||

|

Knox County School District N0 576 4.000% 12/15/2038 |

590,000 |

636,634 |

||

|

Lancaster County School District 001 5.000% 01/15/2023 |

750,000 |

839,715 |

||

|

City of Lincoln NE 3.000% 12/01/2039 |

685,000 |

726,532 |

||

|

Superior Public Schools 1.450% 12/15/2022 |

340,000 |

342,921 |

||

|

City of Omaha NE 4.000% 04/15/2037 |

500,000 |

582,850 |

||

|

City of Omaha NE 5.000% 04/15/2027 |

955,000 |

1,191,143 |

||

|

City of Omaha NE 5.000% 04/15/2028 |

500,000 |

620,225 |

||

|

City of Omaha NE 3.750% 01/15/2038 |

500,000 |

548,090 |

||

|

Polk County School District No 19 3.000% 06/15/2039 |

455,000 |

464,919 |

||

|

Gretna Public Schools 5.000% 12/15/2035 |

250,000 |

297,222 |

||

|

Sarpy County School District No 1 3.500% 12/15/2035 |

250,000 |

268,707 |

||

|

Scotts Bluff County School District No 32 5.000% 12/01/2031 |

250,000 |

300,002 |

||

|

City of Sidney NE 4.000% 12/15/2036 |

1,250,000 |

1,307,075 |

||

|

|

17,465,871 |

|||

|

Health Care (6.0%) |

||||

|

Douglas County Hospital Authority No 2 5.000% 05/15/2027 |

200,000 |

245,216 |

||

|

Lincoln County Hospital Authority No 1 5.000% 11/01/2023 |

250,000 |

268,003 |

||

|

Lincoln County Hospital Authority No 1 5.000% 11/01/2024 |

250,000 |

268,185 |

||

|

Lincoln County Hospital Authority No 1 5.000% 11/01/2025 |

250,000 |

268,617 |

||

|

Lincoln County Hospital Authority No 1 5.000% 11/01/2032 |

250,000 |

263,157 |

||

|

Madison County Hospital Authority No 1 5.000% 07/01/2031 |

500,000 |

576,375 |

||

|

Madison County Hospital Authority No 1 5.000% 07/01/2032 |

335,000 |

385,320 |

||

|

Madison County Hospital Authority No 1 5.000% 07/01/2033 |

450,000 |

516,807 |

||

|

Madison County Hospital Authority No 1 5.000% 07/01/2034 |

215,000 |

247,583 |

||

|

|

3,039,263 |

|||

|

Housing (2.1%) |

||||

|

Nebraska Investment Finance Authority 3.850% 03/01/2038 |

515,000 |

544,139 |

||

|

#Nebraska Investment Finance Authority 3.450% 09/01/2033 |

500,000 |

542,360 |

||

|

|

1,086,499 |

|||

|

Other Revenue (0.9%) |

||||

|

Papillion Municipal Facilities Corp 3.000% 12/15/2034 |

435,000 |

|

453,370 |

|

|

|

||||

|

Pre-refunded (23.9%) |

||||

|

County of Douglas NE 5.500% 07/01/2030 |

350,000 |

356,811 |

||

|

*County of Douglas NE 5.875% 07/01/2040 |

1,500,000 |

1,531,455 |

||

|

Grand Island Public Schools 5.000% 12/15/2033 |

500,000 |

596,710 |

||

|

Grand Island Public Schools 5.000% 12/15/2039 |

500,000 |

596,710 |

||

|

*City of Lincoln NE Electric System Revenue 5.000% 09/01/2037 |

1,000,000 |

1,095,560 |

||

|

City of Lincoln NE 5.500% 08/15/2031 |

500,000 |

522,925 |

||

|

West Haymarket Joint Public Agency 5.000% 12/15/2042 |

750,000 |

807,555 |

||

|

*City of Omaha NE 5.000% 02/01/2027 |

1,000,000 |

1,083,580 |

||

|

Papio Missouri River Natural Resource District 4.000% 12/15/2030 |

1,000,000 |

1,011,180 |

||

|

University of Nebraska 5.000% 07/01/2035 |

1,500,000 |

1,792,245 |

||

|

University of Nebraska 5.000% 05/15/2035 |

500,000 |

601,865 |

||

|

University of Nebraska 5.000% 05/15/2033 |

250,000 |

301,080 |

||

|

University of Nebraska 4.500% 05/15/2030 |

250,000 |

252,565 |

||

|

University of Nebraska 5.000% 05/15/2035 |

275,000 |

278,217 |

||

|

University of Nebraska 5.000% 07/01/2042 |

1,000,000 |

1,070,610 |

||

|

University of Nebraska 5.000% 07/01/2038 |

250,000 |

273,690 |

||

|

|

12,172,758 |

|||

|

Transportation (3.6%) |

||||

|

Omaha Airport Authority 5.000% 12/15/2027 |

500,000 |

621,935 |

||

|

Omaha Airport Authority 5.000% 12/15/2036 |

1,000,000 |

1,203,360 |

||

|

|

1,825,295 |

|||

|

Utilities (25.3%) |

||||

|

*Central Plains Energy Project 5.000% 09/01/2027 |

2,000,000 |

2,159,580 |

||

|

Central Plains Energy Project 5.250% 09/01/2037 |

500,000 |

542,110 |

||

|

Central Plains Energy Project 5.000% 09/01/2042 |

500,000 |

543,465 |

||

|

City of Columbus NE Combined Revenue 4.000% 12/15/2032 |

100,000 |

114,499 |

||

|

City of Grand Island NE Sewer System Revenue 5.000% 09/15/2026 |

250,000 |

287,985 |

||

|

City of Hastings NE Combined Utility Revenue 4.000% 10/15/2032 |

500,000 |

534,530 |

||

|

City of Lincoln NE Solid Waste Management Revenue 4.000% 08/01/2025 |

275,000 |

307,689 |

||

|

City of Lincoln NE Solid Waste Management Revenue 4.000% 08/01/2027 |

400,000 |

445,336 |

||

|

Metropolitan Utilities District of Omaha 4.000% 12/15/2026 |

250,000 |

272,967 |

||

|

Municipal Energy Agency of Nebraska 5.000% 04/01/2030 |

500,000 |

545,105 |

||

|

Municipal Energy Agency of Nebraska 5.000% 04/01/2032 |

100,000 |

108,573 |

||

|

Nebraska Public Power District 5.000% 01/01/2041 |

250,000 |

295,668 |

||

|

*Nebraska Public Power District 5.000% 01/01/2036 |

2,355,000 |

2,792,583 |

||

|

Nebraska Public Power District 5.000% 01/01/2030 |

500,000 |

541,935 |

||

|

City of Omaha NE Sewer Revenue 5.000% 11/15/2029 |

250,000 |

293,708 |

||

|

City of Omaha NE Sewer Revenue 5.000% 11/15/2030 |

250,000 |

295,645 |

||

|

City of Omaha NE Sewer Revenue 5.000% 11/15/2031 |

500,000 |

587,870 |

||

|

City of Omaha NE Sewer Revenue 4.000% 04/01/2035 |

250,000 |

280,922 |

||

|

City of Omaha NE Sewer Revenue 1.050% 04/01/2020 |

250,000 |

250,077 |

||

|

Omaha Public Power District Nebraska City Station Unit 2 5.000% 02/01/2032 |

250,000 |

294,505 |

||

|

Omaha Public Power District Nebraska City Station Unit 2 5.000% 02/01/2031 |

445,000 |

539,732 |

||

|

Omaha Public Power District Nebraska City Station Unit 2 4.000% 02/01/2032 |

400,000 |

453,240 |

||

|

Omaha Public Power District Nebraska City Station Unit 2 4.000% 02/01/2035 |

365,000 |

411,359 |

||

|

|

12,899,083 |

|||

|

|

||||

|

TOTAL MUNICIPAL BONDS (COST: $46,502,931) |

$ |

49,208,389 |

||

|

|

||||

|

OTHER ASSETS LESS LIABILITIES (3.4%) |

$ |

1,709,114 |

||

|

|

||||

|

NET ASSETS (100.0%) |

$ |

50,917,503 |

||

|

|

||||

|

*Indicates all or a portion of bonds are segregated by the custodian to cover when-issued or delayed-delivery purchases when they occur. |

||||

|

#When-issued purchase as of January 31, 2020. |

||||

|

|

||||

|

|

||||

|

The accompanying notes are an integral part of these financial statements. |

||||

OKLAHOMA MUNICIPAL FUND

PORTFOLIO MARKET SECTORS January 31, 2020 (unaudited)

|

Other Revenue |

27.3% |

|

Utilities |

18.8% |

|

Transportation |

12.3% |

|

Education |

12.2% |

|

General Obligation |

9.0% |

|

Health Care |

7.0% |

|

Pre-Refunded |

6.5% |

|

Cash Equivalents and Other |

5.2% |

|

Housing |

1.7% |

|

100.0% |

Market sectors are breakdowns of the Fund’s portfolio holdings into specific investment classes.

These percentages are based on net assets and are subject to change.

SCHEDULE OF INVESTMENTS January 31, 2020 (unaudited)

|

Principal |

Fair |

|||

|

|

Amount |

|

Value |

|

|

MUNICIPAL BONDS (94.8%) |

||||

|

|

||||

|

Education (12.2%) |

||||

|

Oklahoma Agricultural & Mechanical Colleges 4.400% 08/01/2039 |

$ |

630,000 |

$ |

637,913 |

|

*Oklahoma City Community College/OK 4.375% 07/01/2030 |

750,000 |

760,080 |

||

|

Oklahoma Development Finance Authority 5.000% 06/01/2039 |

500,000 |

574,505 |

||

|

Oklahoma Development Finance Authority 5.000% 06/01/2029 |

250,000 |

292,955 |

||

|

Oklahoma Development Finance Authority 5.000% 06/01/2034 |

500,000 |

577,085 |

||

|

Oklahoma Development Finance Authority 5.000% 06/01/2039 |

500,000 |

572,690 |

||

|

Oklahoma Development Finance Authority 4.000% 08/01/2030 |

280,000 |

310,736 |

||

|

Oklahoma Development Finance Authority 4.000% 08/01/2031 |

290,000 |

320,166 |

||

|

Oklahoma Development Finance Authority 4.000% 08/01/2032 |

305,000 |

335,890 |

||

|

Oklahoma Development Finance Authority 4.000% 08/01/2033 |

315,000 |

346,043 |

||

|

Oklahoma State University 5.000% 08/01/2032 |

250,000 |

320,383 |

||

|

University of Oklahoma/The 5.000% 07/01/2037 |

290,000 |

308,583 |

||

|

University of Oklahoma/The 5.000% 07/01/2036 |

500,000 |

588,640 |

||

|

University of Oklahoma/The 4.000% 07/01/2040 |

650,000 |

716,677 |

||

|

University of Oklahoma/The 5.000% 07/01/2038 |

500,000 |

588,405 |

||

|

|

7,250,751 |

|||

|

General Obligation (9.0%) |

||||

|

City of Broken Arrow OK 4.000% 12/01/2037 |

605,000 |

686,082 |

||

|

City of Broken Arrow OK 4.000% 12/01/2038 |

610,000 |

689,758 |

||

|

City of Broken Arrow OK 2.000% 12/01/2021 |

500,000 |

508,110 |

||

|

City of Broken Arrow OK 4.000% 12/01/2020 |

655,000 |

669,489 |

||

|

City of Broken Arrow OK 4.125% 08/01/2031 |

180,000 |

188,008 |

||

|

City of Broken Arrow OK 3.125% 12/01/2035 |

575,000 |

614,842 |

||

|

City of Lawton OK 2.000% 12/01/2022 |

500,000 |

512,400 |

||

|

City of Midwest City OK 3.000% 06/01/2041 |

500,000 |

521,955 |

||

|

City of Nichols Hills OK 4.000% 07/01/2022 |

650,000 |

692,829 |

||

|

City of Perkins OK 3.000% 06/01/2033 |

125,000 |

135,643 |

||

|

City of Perkins OK 3.000% 06/01/2034 |

115,000 |

124,680 |

||

|

|

5,343,796 |

|||

|

Health Care (7.0%) |

||||

|

Oklahoma Development Finance Authority 5.000% 08/15/2025 |

350,000 |

426,482 |

||

|

Oklahoma Development Finance Authority 5.000% 08/15/2029 |

250,000 |

295,335 |

||

|

Oklahoma Development Finance Authority 4.000% 08/15/2038 |

250,000 |

273,520 |

||

|

Oklahoma Development Finance Authority 5.000% 08/15/2029 |

345,000 |

429,277 |

||

|

Oklahoma Development Finance Authority 5.000% 08/15/2033 |

175,000 |

210,663 |

||

|

Oklahoma Development Finance Authority 4.000% 08/15/2048 |

825,000 |

907,261 |

||

|

Oklahoma Development Finance Authority 5.000% 07/01/2035 |

250,000 |

277,900 |

||

|

Tulsa County Industrial Authority 4.600% 02/01/2035 |

250,000 |

250,000 |

||

|

Tulsa County Industrial Authority 3.000% 02/01/2021 |

270,000 |

275,252 |

||

|

Tulsa County Industrial Authority 3.000% 02/01/2022 |

320,000 |

332,122 |

||

|

Tulsa County Industrial Authority 3.000% 02/01/2037 |

500,000 |

511,910 |

||

|

|

4,189,722 |

|||

|

Housing (1.7%) |

||||

|

Oklahoma Housing Finance Agency 3.000% 09/01/2039 |

1,000,000 |

|

1,035,050 |

|

|

|

||||

|

Other Revenue (27.3%) |

||||

|

Bryan County School Finance Authority 4.000% 12/01/2028 |

385,000 |

461,931 |

||

|

Bryan County School Finance Authority 4.000% 12/01/2029 |

415,000 |

503,802 |

||

|

Bryan County School Finance Authority 4.000% 12/01/2030 |

435,000 |

523,992 |

||

|

Caddo County Governmental Building Authority 5.000% 09/01/2040 |

1,010,000 |

1,193,881 |

||

|

Elk City Industrial Authority 3.000% 05/01/2034 |

1,050,000 |

1,099,497 |

||

|

Elk City Industrial Authority 3.000% 05/01/2039 |

425,000 |

432,306 |

||

|

Goldsby Public Works Authority 3.000% 08/01/2021 |

165,000 |

167,376 |

||

|

Grady County School Finance Authority 5.000% 09/01/2032 |

370,000 |

462,596 |

||

|

Kingfisher County Educational Facilities Authority 3.000% 03/01/2033 |

250,000 |

263,757 |

||

|

Leflore County Public Facility Authority 3.000% 12/01/2032 |

500,000 |

537,015 |

||

|

McClain County Economic Development Authority 4.000% 09/01/2021 |

400,000 |

417,144 |

||

|

City of Oklahoma City OK 5.000% 03/01/2032 |

250,000 |

250,975 |

||

|

City of Oklahoma City OK 5.000% 03/01/2034 |

500,000 |

501,675 |

||

|

City of Oklahoma City OK 5.000% 03/01/2033 |

250,000 |

250,872 |

||

|

Oklahoma City Public Property Authority 5.000% 10/01/2027 |

350,000 |

425,712 |

||

|

Oklahoma City Public Property Authority 5.000% 10/01/2028 |

400,000 |

484,320 |

||

|

Oklahoma City Public Property Authority 5.000% 10/01/2029 |

625,000 |

752,556 |

||

|

Oklahoma City Public Property Authority 5.000% 10/01/2036 |

230,000 |

272,334 |

||

|

Oklahoma City Public Property Authority 5.000% 10/01/2039 |

835,000 |

979,789 |

||

|

Oklahoma Development Finance Authority 4.000% 06/01/2038 |

725,000 |

835,425 |

||

|

Oklahoma Capitol Improvement Authority 5.000% 07/01/2035 |

530,000 |

676,465 |

||

|

Oklahoma Capitol Improvement Authority 4.000% 07/01/2045 |

500,000 |

571,665 |

||

|

Oklahoma Capitol Improvement Authority 4.000% 07/01/2043 |

500,000 |

548,605 |

||

|

Okmulgee County Governmental Building Authority 4.250% 12/01/2035 |

500,000 |

542,585 |

||

|

Ottawa County Educational Facilities Authority 4.000% 09/01/2022 |

990,000 |

1,059,419 |

||

|

Sand Springs Municipal Authority 4.250% 01/01/2035 |

250,000 |

269,437 |

||

|

Sand Springs Municipal Authority 4.000% 01/01/2036 |

500,000 |

534,695 |

||

|

Tahlequah Public Facilities Authority 4.000% 04/01/2023 |

550,000 |

598,779 |

||

|

Wagoner County School Development Authority 4.000% 09/01/2027 |

500,000 |

586,500 |

||

|

|

16,205,105 |

|||

|

Pre-refunded (6.5%) |

||||

|

Collinsville Municipal Authority 5.000% 03/01/2035 |

275,000 |

276,037 |

||

|

Collinsville Municipal Authority 5.000% 03/01/2040 |

250,000 |

250,942 |

||

|

*Grand River Dam Authority 5.250% 06/01/2040 |

2,000,000 |

2,027,240 |

||

|

Oklahoma Development Finance Authority 5.000% 02/15/2042 |

250,000 |

270,715 |

||

|

Oklahoma Turnpike Authority 5.000% 01/01/2030 |

250,000 |

259,732 |

||

|

Oklahoma Water Resources Board 4.000% 04/01/2025 |

150,000 |

160,489 |

||

|

Pawnee County Public Programs Authority 4.875% 02/01/2030 |

145,000 |

145,000 |

||

|

*Rogers County Industrial Development Authority 4.900% 04/01/2035 |

500,000 |

503,365 |

||

|

|

3,893,520 |

|||

|

Transportation (12.3%) |

||||

|

Oklahoma Capitol Improvement Authority 4.000% 10/01/2024 |

800,000 |

846,272 |

||

|

Oklahoma Capitol Improvement Authority 4.000% 10/01/2025 |

1,000,000 |

1,057,780 |

||

|

Oklahoma Turnpike Authority 5.000% 01/01/2028 |

250,000 |

259,182 |

||

|

Oklahoma Turnpike Authority 4.000% 01/01/2042 |

1,000,000 |

1,131,510 |

||

|

Oklahoma Turnpike Authority 4.000% 01/01/2038 |

100,000 |

113,989 |

||

|

Tulsa Airports Improvement Trust 5.000% 06/01/2023 |

420,000 |

442,844 |

||

|

Tulsa Airports Improvement Trust 5.000% 06/01/2024 |

230,000 |

242,310 |

||

|

Tulsa Airports Improvement Trust 5.250% 06/01/2025 |

245,000 |

258,855 |

||

|

Tulsa Airports Improvement Trust 5.250% 06/01/2026 |

360,000 |

380,207 |

||

|

Tulsa Airports Improvement Trust 4.000% 06/01/2035 |

1,355,000 |

1,518,548 |

||

|

Tulsa Airports Improvement Trust 4.000% 06/01/2036 |

145,000 |

161,843 |

||

|

#Tulsa Airports Improvement Trust 5.000% 06/01/2027 |

300,000 |

370,692 |

||

|

Tulsa Parking Authority 4.000% 07/01/2025 |

500,000 |

521,615 |

||

|

|

7,305,647 |

|||

|

Utilities (18.8%) |

||||

|

Clinton Public Works Authority 4.000% 12/01/2034 |

750,000 |

818,700 |

||

|

Clinton Public Works Authority 4.000% 12/01/2039 |

500,000 |

542,595 |

||

|

Coweta Public Works Authority 4.000% 08/01/2032 |

1,000,000 |

1,118,740 |

||

|

Edmond Public Works Authority 5.000% 07/01/2032 |

500,000 |

621,625 |

||

|

Glenpool Utility Services Authority 5.100% 12/01/2035 |

250,000 |

257,985 |

||

|

Miami Special Utility Authority 4.000% 12/01/2036 |

500,000 |

564,755 |

||

|

*Midwest City Municipal Authority 5.000% 03/01/2025 |

2,000,000 |

2,095,220 |

||

|

Oklahoma City Water Utilities Trust 5.000% 07/01/2031 |

250,000 |

265,432 |

||

|

Oklahoma City Water Utilities Trust 5.000% 07/01/2034 |

100,000 |

118,652 |

||

|

Oklahoma City Water Utilities Trust 4.000% 07/01/2039 |

175,000 |

192,761 |

||

|

*Oklahoma Municipal Power Authority 5.750% 01/01/2024 |

370,000 |

429,056 |

||

|

Oklahoma Municipal Power Authority 5.000% 01/01/2021 |

250,000 |

258,725 |

||

|

Oklahoma Water Resources Board 5.000% 04/01/2032 |

140,000 |

152,513 |

||

|

Oklahoma Water Resources Board 5.000% 10/01/2029 |

250,000 |

295,895 |

||

|

Oklahoma Water Resources Board 5.000% 10/01/2033 |

500,000 |

584,975 |

||

|

Oklahoma Water Resources Board 4.000% 10/01/2043 |

830,000 |

945,868 |

||

|

Oklahoma Water Resources Board 4.000% 10/01/2048 |

850,000 |

960,321 |

||

|

Sallisaw Municipal Authority 4.450% 01/01/2028 |

100,000 |

100,280 |

||

|

Sapulpa Municipal Authority 5.000% 04/01/2028 |

750,000 |

840,232 |

||

|

|

11,164,330 |

|||

|

|

||||

|

TOTAL MUNICIPAL BONDS (COST: $53,290,542) |

$ |

56,387,921 |

||

|

|

||||

|

OTHER ASSETS LESS LIABILITIES (5.2%) |

$ |

3,075,308 |

||

|

|

||||

|

NET ASSETS (100.0%) |

$ |

59,463,229 |

||

|

|

||||

|

*Indicates all or a portion of bonds are segregated by the custodian to cover when-issued or delayed-delivery purchases when they occur. As of January 31, 2019 there were no such purchases. |

||||

|

#When-issued purchase as of July 31, 2020 |

||||

|

|

||||

|

|

||||

|

The accompanying notes are an integral part of these financial statements. |

||||

VIKING TAX-FREE FUND FOR MONTANA

PORTFOLIO MARKET SECTORS January 31, 2020 (unaudited)

|

General Obligation |

42.9% |

|