N-CSR

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED

SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-09277

Viking Mutual Funds

(Exact name of registrant as specified in charter)

|

1 Main Street North, Minot, ND |

|

58703 |

|

(Address of principal offices) |

|

(Zip code) |

Brent Wheeler and/or Kevin Flagstad, PO Box 500, Minot, ND 58702

(Name and address of agent for service)

Registrant’s telephone number, including area code: 701-852-5292

Date of fiscal year end: December 31st

Date of reporting period: December 31, 2017

Item 1. REPORTS TO STOCKHOLDERS.

VIKING MUTUAL FUNDS

Viking Tax-Free Fund for Montana

Viking Tax-Free Fund for North Dakota

Annual Report

December 31, 2017

|

|

|

|

Investment

Adviser |

Principal

Underwriter |

|

Transfer Agent |

Custodian |

|

Independent

Registered Public Accounting Firm

|

|

|

|

|

|

*The Funds are distributed through Integrity Funds Distributor, LLC. Member FINRA |

|

|

|

|

VIKING TAX-FREE FUND FOR MONTANA

VIKING TAX-FREE FUND FOR NORTH DAKOTA

DEAR SHAREHOLDERS:

Enclosed is the report of the operations for the Viking Tax-Free Fund for Montana (“Tax-Free Fund for MT”) and Viking Tax-Free Fund for North Dakota (“Tax-Free Fund for ND”) (each a “Fund”) for the year ended December 31, 2017. Each Fund’s portfolio and related financial statements are presented within for your review.

Economic Recap

The Federal Open Market Committee’s (“FOMC” or “Committee”) statement in mid-December noted that the labor market has continued to strengthen and that economic activity has been rising at a solid rate. The Committee also noted that job gains have been solid, and the unemployment rate declined further. Household spending has been expanding at a moderate rate, and growth in business fixed investment has picked up in recent quarters. The Committee continues to expect that, with gradual adjustments in the stance of monetary policy, economic activity will expand at a moderate pace and labor market conditions will remain strong. In view of realized and expected labor market conditions and inflation, the Committee decided to raise the target range for the federal funds rate to 1-1/4 to 1-1/2 %, the Committee's third raise of the year. The Committee expects that the federal funds rate is likely to remain, for some time, below levels that are expected to prevail in the longer run. However, the actual path of the federal funds rate will depend on the economic outlook as informed by incoming data.

Municipal Bond Market Recap

Returns were positive for the municipal market in the first and second quarters of 2017, after two consecutive quarters of negative returns to finish 2016. The Fed's increase in the funds rate in mid-March had no net impact on bond market performance in the first quarter as it was highly anticipated. Municipal market yields rose and then declined during the quarter, ending the period marginally lower than on December 31, 2016. The municipal market had doubts about the Trump Administration's ability to pass its growth initiatives in the short-term. Favorable factors persisted at the end of the first quarter with light supply and a muni/Treasury ratio that remained attractive. The municipal bond market continued to perform well in the second quarter as the Trump agenda faced an uphill battle. The lack of tax reform, as well as limited municipal supply and pent-up-demand propelled municipals in the first half of the year. Issuance in the first two quarters of the year came in at $171.9 billion nationally, a 15.9% decrease over the same period last year.

Returns were again positive for the municipal market in the third and fourth quarter, which marked four consecutive quarters of positive returns in 2017. Municipals continued to perform well as investors searched for relative safety in higher quality assets amid increasing tensions between the United States and North Korea, along with continued gridlock in Washington. The supply/demand dynamic continued to remain positive for municipals. Issuance for the third quarter came in at $77.9 billion nationally, a 26.3% decrease over the same period last year. However, issuance was significantly above average in the fourth quarter, more precisely December, as issuers feared the proposed tax bill in Congress would eliminate the tax-exempt status of private activity and advance refunding bonds. Though it didn’t go as far as eliminating both, it did eliminate the tax exempt status of municipal advance refunding bonds, which will likely decrease overall supply of municipals going forward. It also limits the amount of state and local taxes that households may deduct to $10,000. The robust supply in the fourth quarter was met with strong demand as investors expect the supply in early 2018 to be very light due to the large amount of issuance pulled forward into 2017. Issuance for the quarter came in at $129.2 billion nationally, a 31.1% increase over the same quarter last year. Total issuance nationally in 2017 was $385 billion a 5.7% decrease from 2016. State issuance in Montana was $915.6 million up 18.2% in 2017 versus 2016, while North Dakota issuance was $1.14 billion in 2017 a 42.6% increase over 2016.

Fund Performance and Outlook

In 2017, lower-rated investment grade muni bonds outperformed their higher-rated counterparts, while longer investment grade muni bonds outperformed their shorter counterparts. The yield curve flattened over the course of the year as the Fed raised the fed funds rate three times and hinted at further rate hikes in 2018. This caused rates on the very short end of the curve (i.e. 1-2 years) to increase at least 30 basis points while rates on the longer end of the curve (i.e. 20 years plus) decreased by at least 50 basis points. By maintaining an intermediate maturity structure the Montana and North Dakota Funds were able to capture roughly two-thirds of the price move in the yield curve by keeping the average weighted maturity of the portfolios under 10 years. The Funds' performance also benefited from a heavy weighting in AA and A rated bonds as those credits captured 80-100% of the upside price move in the MMD of their BBB rated equivalents.

Over the course of the year, the Portfolio Management Team (the “Team”) continued to maintain a shorter maturity structure than in past years and also made a concerted effort to purchase bonds with higher coupons when possible.

The Tax-Free Fund for MT and Tax-Free Fund for ND provided total returns for A shares of 3.77%* and 3.12%*, respectively (at net asset value with distributions reinvested) and for I shares of 4.03%* and 3.38%*, respectively for the year ended December 31, 2017 compared to the Funds’ benchmark, the Barclays Capital Municipal Bond Index which returned 5.45% and the Morningstar Muni Single State Intermediate Category which returned 3.59%.

Despite the continued relative scarcity of Montana and North Dakota municipal bonds throughout the period, each Fund was able to obtain an adequate supply of investment grade bonds of various maturities. Each Fund may also invest in non-rated bonds should we deem they are of investment grade equivalent. Although we refrain from making large bets on the direction of rates, we have taken the opportunity to shorten the Funds’ maturity structures over the last few years in anticipation of an eventual rise in rates. A shorter maturity structure should provide a somewhat greater degree of stability of each Fund’s share price should muni prices become volatile. The highest level of current income that is exempt from federal and each Fund’s state income taxes and is consistent with preservation of capital remains the investment objective of each Fund.

The current 3.8% Medicare surtax on investment income established by the Patient Protection and Affordable Care Act (municipals are exempt) combined with higher marginal tax rates at the federal and state levels boost the appeal of tax-exempt income. The federal marginal tax rate for taxpayers with adjusted gross incomes of $500,000 ($600,000 for married filing jointly) is 37.0%. The after-tax yield of a 10-year U.S. Treasury Note yielding 2.41% falls to approximately 1.43% at the 37.0% federal tax rate plus the 3.8% Medicare surtax.

Finally, we recommend that shareholders view their investment as long-term. As difficult as they may be, periods of panic (and euphoria) tend to be transitory in nature and it’s the long-term investors that may be rewarded with the long-term benefits of tax-free income and relatively low volatility that muni bonds have provided for decades.

If you would like more frequent updates, please visit the Fund’s website at www.integrityvikingfunds.com for daily prices along with pertinent Fund information.

Sincerely,

The Portfolio Management Team

The views expressed are those of The Portfolio Management Team of Viking Fund Management, LLC (“Viking Fund Management”, “VFM”, or the “Adviser”). The views are subject to change at any time in response to changing circumstances in the market and are not intended to predict or guarantee the future performance of any individual security, market sector, the markets generally, or any of the funds in the Integrity Viking family of funds.

*Performance does not include applicable front-end or contingent deferred sales charges, which would have reduced the performance. For Tax-Free Fund for MT Class A and I and Tax-Free Fund for ND Class A and I, the total annual fund operating expense ratio (before expense waivers and reimbursements and including acquired fund fees and expenses) as of the most recent fiscal year-end was 1.15%, 0.90%, 1.29% and 1.04%, respectively. The net annual fund operating expense ratio (after expense waivers and reimbursements and excluding acquired fund fees and expenses) as of the most recent fiscal year-end was 0.98%, 0.73%, 0.98% and 0.73%, respectively. The Funds’ investment adviser has contractually agreed to waive fees and reimburse expenses through April 29, 2018 so that total annual fund operating expenses after fee waivers and expense reimbursements (excluding taxes, brokerage fees, commissions, extraordinary and non-recurring expenses, and acquired fund fees and expenses) do not exceed 0.98%, 0.73%, 0.98% and 0.73%, respectively, of average daily net assets. This expense limitation agreement may only be terminated or modified prior to April 29, 2018 with the approval of the Fund’s Board of Trustees.

Performance data quoted above is historical. Past performance is no guarantee of future results. Current performance may be higher or lower than the performance data quoted. The principal value and investment return of an investment will fluctuate so that your shares, when redeemed, may be worth more or less than the original cost. You can obtain performance data current to the most recent month end (available within seven business days of the most recent month end) by calling 800-276-1262.

You should consider the Fund’s investment objectives, risks, charges, and expenses carefully before investing. For this and other important information, please obtain a Fund prospectus at no cost from your financial adviser and read it carefully before investing.

Bond prices and therefore the value of bond funds decline as interest rates rise. Because the Fund invests in securities of a single state, the Fund is more susceptible to factors adversely impacting the respective state than a municipal bond fund that does not concentrate its securities in a single state.

For investors subject to the alternative minimum tax, a portion of the Fund’s dividends may be taxable. Distributions of capital gains are generally taxable.

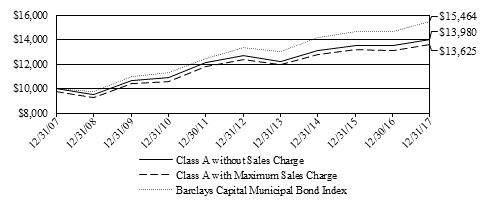

VIKING TAX-FREE FUND FOR MONTANA

PERFORMANCE (unaudited)

Comparison of change in value of a $10,000 investment

Average Annual Total Returns for the periods ended December 31, 2017

|

|

1 year |

3 year |

5 year |

10 year |

Since Inception* |

|

Class A Without sales charge |

3.77% |

2.16% |

1.90% |

3.41% |

3.87% |

|

Class A With sales charge (2.50%) |

1.13% |

1.31% |

1.38% |

3.14% |

3.72% |

|

Class I Without sales charge |

4.03% |

N/A |

N/A |

N/A |

0.41% |

|

* August 3, 1999 for Class A; August 1, 2016 Class I |

|||||

The total annual fund operating expense ratio for Class A and I (before expense waivers and reimbursements and including acquired fund fees and expenses) as of the most recent fiscal year-end was 1.15% and 0.90%, respectively. The net annual fund operating expense ratio (after expense waivers and reimbursements and excluding acquired fund fees and expenses) as of the most recent fiscal year-end was 0.98% and 0.73%, respectively. The Fund’s investment adviser has contractually agreed to waive fees and reimburse expenses through April 29, 2018 so that total annual fund operating expenses after fee waivers and expense reimbursements (excluding taxes, brokerage fees, commissions, extraordinary and non-recurring expenses, and acquired fund fees and expenses) do not exceed 0.98% and 0.73%, respectively, of average daily net assets. This expense limitation agreement may only be terminated or modified prior to April 29, 2018 with the approval of the Fund’s Board of Trustees.

Performance data quoted above is historical. Past performance is no guarantee of future results. Current performance may be higher or lower than the performance data quoted. The principal value and investment return of an investment will fluctuate so that your shares, when redeemed, may be worth more or less than the original cost. You can obtain performance data current to the most recent month end (available within seven business days of the most recent month end) by calling 800-276-1262.

The table and graph above do not reflect the deduction of taxes that a shareholder would pay on Fund distributions and redemptions of Fund shares.

The graph comparing the Fund’s performance to a benchmark index provides you with a general sense of how the Fund performed. To put this information in context, it may be helpful to understand the special differences between the two. The Fund’s total return for the period shown appears with and without sales charges and includes Fund expenses and management fees. A securities index measures the performance of a theoretical portfolio. Unlike a fund, the index is unmanaged; there are no expenses that affect the results. In addition, few investors could purchase all of the securities to match the index. If they could, transaction costs and other expenses would be incurred. All Fund and benchmark returns include reinvested dividends.

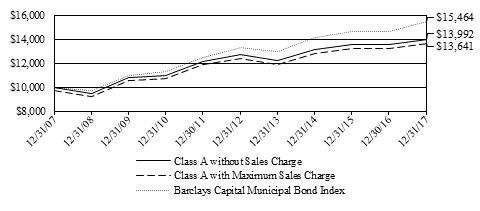

VIKING TAX-FREE FUND FOR NORTH DAKOTA

PERFORMANCE (unaudited)

Comparison of change in value of a $10,000 investment

Average Annual Total Returns for the periods ended December 31, 2017

|

|

1 year |

3 year |

5 year |

10 year |

Since Inception* |

|

Class A Without sales charge |

3.12% |

2.15% |

1.95% |

3.42% |

3.95% |

|

Class A With sales charge (2.50%) |

0.56% |

1.28% |

1.44% |

3.15% |

3.81% |

|

Class I Without sales charge |

3.38% |

N/A |

N/A |

N/A |

0.12% |

|

* August 3, 1999 for Class A; August 1, 2016 Class I |

|||||

The total annual fund operating expense ratio for class A and I (before expense waivers and reimbursements and including acquired fund fees and expenses) as of the most recent fiscal year-end was 1.29% and 1.04%, respectively. The net annual fund operating expense ratio (after expense waivers and reimbursements and excluding acquired fund fees and expenses) as of the most recent fiscal year-end was 0.98% and 0.73%, respectively. The Fund’s investment adviser has contractually agreed to waive fees and reimburse expenses through April 29, 2018 so that total annual fund operating expenses after fee waivers and expense reimbursements (excluding taxes, brokerage fees, commissions, extraordinary and non-recurring expenses, and acquired fund fees and expenses) do not exceed 0.98% and 0.73%, respectively, of average daily net assets. This expense limitation agreement may only be terminated or modified prior to April 29, 2018 with the approval of the Fund’s Board of Trustees.

Performance data quoted above is historical. Past performance is no guarantee of future results. Current performance may be higher or lower than the performance data quoted. The principal value and investment return of an investment will fluctuate so that your shares, when redeemed, may be worth more or less than the original cost. You can obtain performance data current to the most recent month end (available within seven business days of the most recent month end) by calling 800-276-1262.

The table and graph above do not reflect the deduction of taxes that a shareholder would pay on Fund distributions and redemptions of Fund shares.

The graph comparing the Fund’s performance to a benchmark index provides you with a general sense of how the Fund performed. To put this information in context, it may be helpful to understand the special differences between the two. The Fund’s total return for the period shown appears with and without sales charges and includes Fund expenses and management fees. A securities index measures the performance of a theoretical portfolio. Unlike a fund, the index is unmanaged; there are no expenses that affect the results. In addition, few investors could purchase all of the securities to match the index. If they could, transaction costs and other expenses would be incurred. All Fund and benchmark returns include reinvested dividends.

VIKING TAX-FREE FUND FOR MONTANA

PORTFOLIO MARKET SECTORS December 31, 2017

|

General Obligation |

43.0% |

|

Health Care |

17.8% |

|

Other Revenue |

9.3% |

|

Education |

8.3% |

|

Transportation |

7.3% |

|

Housing |

6.4% |

|

Utilities |

4.4% |

|

Cash Equivalents and Other |

3.5% |

|

100.0% |

Market sectors are breakdowns of the Fund’s portfolio holdings into specific investment classes.

These percentages are based on net assets.

SCHEDULE OF INVESTMENTS December 31, 2017

|

|

|

|

|

|

|

|

|

Principal |

|

Fair |

|

|

Amount |

|

Value |

|

|

MUNICIPAL BONDS (96.5%) |

||||

|

|

||||

|

Education (8.3%) |

||||

|

Gallatin County School District No 44 Belgrade 3.500% 06/15/2028 |

$ |

575,000 |

$ |

609,000 |

|

Montana State Board of Regents 5.000% 11/15/2023 |

250,000 |

281,377 |

||

|

*Montana State Board of Regents 4.000% 05/15/2025 |

2,000,000 |

2,192,340 |

||

|

Montana State Board of Regents 4.000% 05/15/2026 |

1,145,000 |

1,242,817 |

||

|

Montana State Board of Regents 4.000% 11/15/2025 |

500,000 |

549,905 |

||

|

Montana State Board of Regents 5.000% 11/15/2025 |

500,000 |

589,150 |

||

|

Montana State Board of Regents 5.000% 11/15/2030 |

240,000 |

279,696 |

||

|

Montana State Board of Regents 5.000% 11/15/2024 |

200,000 |

239,504 |

||

|

University of Montana/Missoula MT 5.375% 05/15/2019 |

180,000 |

184,795 |

||

|

|

6,168,584 |

|||

|

General Obligation (43.0%) |

||||

|

City of Bozeman MT 4.000% 07/01/2028 |

540,000 |

612,095 |

||

|

City & County of Butte-Silver Bow MT 4.000% 07/01/2026 |

115,000 |

131,789 |

||

|

City & County of Butte-Silver Bow MT 4.000% 07/01/2028 |

215,000 |

243,349 |

||

|

City & County of Butte-Silver Bow MT 4.000% 07/01/2030 |

225,000 |

249,799 |

||

|

City & County of Butte-Silver Bow MT 4.000% 07/01/2032 |

240,000 |

262,704 |

||

|

City & County of Butte-Silver Bow MT 4.500% 07/01/2034 |

850,000 |

966,951 |

||

|

Cascade County Elementary School District No 1 Great Falls 5.000% 07/01/2027 |

1,120,000 |

1,405,096 |

||

|

Cascade County Elementary School District No 1 Great Falls 4.000% 07/01/2029 |

925,000 |

1,061,955 |

||

|

Cascade County Elementary School District No 1 Great Falls 4.000% 07/01/2030 |

935,000 |

1,064,002 |

||

|

Cascade County Elementary School District No 1 Great Falls 4.000% 07/01/2031 |

700,000 |

789,908 |

||

|

Cascade County High School District A Great Falls 4.000% 07/01/2028 |

610,000 |

705,678 |

||

|

Cascade County High School District A Great Falls 5.000% 07/01/2026 |

940,000 |

1,161,173 |

||

|

Cascade County High School District A Great Falls 5.000% 07/01/2027 |

1,110,000 |

1,392,550 |

||

|

Cascade County High School District A Great Falls 4.000% 07/01/2030 |

670,000 |

762,440 |

||

|

Flathead County High School District No 5 Kalispell 5.000% 01/01/2023 |

540,000 |

622,075 |

||

|

Gallatin County High School District No 7 Bozeman 5.000% 06/01/2023 |

495,000 |

575,769 |

||

|

Gallatin County High School District No 7 Bozeman 5.000% 12/01/2024 |

680,000 |

816,911 |

||

|

Gallatin County High School District No 7 Bozeman 5.000% 06/01/2025 |

565,000 |

685,108 |

||

|

Gallatin County School District No 72 Ophir 3.500% 07/01/2023 |

555,000 |

590,448 |

||

|

Gallatin County School District No 72 Ophir 3.750% 07/01/2024 |

645,000 |

687,480 |

||

|

Gallatin County School District No 72 Ophir 4.000% 07/01/2025 |

420,000 |

450,353 |

||

|

Gallatin County School District No 7 Bozeman 4.000% 12/01/2032 |

915,000 |

1,024,086 |

||

|

Gallatin County School District No 7 Bozeman 4.000% 12/01/2033 |

515,000 |

574,704 |

||

|

Gallatin County School District No 27 Monforton 4.250% 06/15/2026 |

415,000 |

472,361 |

||

|

Meagher County K-12 School District No 8 White Sulphur 4.000% 07/01/2028 |

475,000 |

547,143 |

||

|

County of Missoula MT 5.000% 07/01/2031 |

445,000 |

539,051 |

||

|

Missoula High School District No 1 4.000% 07/01/2032 |

$ |

275,000 |

$ |

304,312 |

|

Missoula High School District No 1 4.000% 07/01/2028 |

710,000 |

811,523 |

||

|

Missoula High School District No 1 5.000% 07/01/2027 |

290,000 |

361,549 |

||

|

Hellgate School District No 4 5.000% 06/15/2028 |

500,000 |

606,505 |

||

|

Hellgate School District No 4 5.000% 06/15/2029 |

500,000 |

602,505 |

||

|

Hellgate School District No 4 5.000% 06/15/2030 |

500,000 |

599,250 |

||

|

City of Missoula MT 4.000% 07/01/2026 |

350,000 |

401,306 |

||

|

City of Missoula MT 4.000% 07/01/2031 |

250,000 |

276,325 |

||

|

*Missoula County Elementary School District No 1 4.000% 07/01/2032 |

1,200,000 |

1,332,744 |

||

|

Missoula County Elementary School District No 1 4.000% 07/01/2033 |

750,000 |

826,035 |

||

|

State of Montana 4.000% 08/01/2023 |

385,000 |

436,736 |

||

|

State of Montana 4.000% 08/01/2026 |

855,000 |

975,187 |

||

|

State of Montana 4.000% 08/01/2027 |

480,000 |

541,282 |

||

|

State of Montana 5.000% 07/15/2025 |

200,000 |

218,020 |

||

|

County of Ravalli MT 4.250% 07/01/2027 |

150,000 |

154,281 |

||

|

County of Ravalli MT 4.350% 07/01/2028 |

155,000 |

160,293 |

||

|

County of Ravalli MT 4.400% 07/01/2029 |

165,000 |

170,494 |

||

|

County of Ravalli MT 4.250% 07/01/2030 |

755,000 |

835,294 |

||

|

Valley County K-12 School District No 1-A Glasgow/MT 4.250% 07/01/2031 |

450,000 |

507,159 |

||

|

Yellowstone County School District No 2 Billings 5.000% 06/15/2024 |

500,000 |

603,380 |

||

|

Yellowstone County School District No 2 Billings 5.000% 06/15/2026 |

515,000 |

618,870 |

||

|

Yellowstone County School District No 2 Billings 5.000% 06/15/2027 |

1,000,000 |

1,195,240 |

||

|

Yellowstone County School District No 2 Billings 5.000% 06/15/2031 |

350,000 |

414,631 |

||

|

Yellowstone County School District No 2 Billings 5.000% 06/15/2032 |

435,000 |

514,018 |

||

|

|

31,861,917 |

|||

|

Health Care (17.8%) |

||||

|

Montana Facility Finance Authority 4.500% 07/01/2023 |

250,000 |

253,750 |

||

|

Montana Facility Finance Authority 4.500% 07/01/2023 |

1,025,000 |

1,101,086 |

||

|

*Montana Facility Finance Authority 4.650% 07/01/2024 |

1,365,000 |

1,466,256 |

||

|

Montana Facility Finance Authority 4.750% 07/01/2025 |

380,000 |

408,257 |

||

|

Montana Facility Finance Authority 5.250% 06/01/2030 |

660,000 |

716,067 |

||

|

Montana Facility Finance Authority 5.125% 06/01/2026 |

1,000,000 |

1,091,490 |

||

|

Montana Facility Finance Authority 5.000% 07/01/2024 |

250,000 |

294,695 |

||

|

Montana Facility Finance Authority 4.750% 01/01/2040 |

705,000 |

739,087 |

||

|

Montana Facility Finance Authority 4.500% 01/01/2024 |

1,000,000 |

1,047,080 |

||

|

Montana Facility Finance Authority 5.000% 01/01/2024 |

400,000 |

424,852 |

||

|

Montana Facility Finance Authority 5.500% 01/01/2025 |

575,000 |

639,647 |

||

|

Montana Facility Finance Authority 5.750% 01/01/2031 |

815,000 |

912,580 |

||

|

Montana Facility Finance Authority 5.000% 06/01/2028 |

1,015,000 |

1,183,104 |

||

|

Montana Facility Finance Authority 5.000% 06/01/2029 |

915,000 |

1,068,034 |

||

|

*Montana Facility Finance Authority 5.000% 06/01/2022 |

1,100,000 |

1,101,331 |

||

|

County of Yellowstone MT 4.000% 10/01/2029 |

710,000 |

782,164 |

||

|

|

13,229,480 |

|||

|

Housing (6.4%) |

||||

|

Montana Board of Housing 2.650% 06/01/2021 |

125,000 |

126,769 |

||

|

Montana Board of Housing 2.650% 12/01/2021 |

280,000 |

282,520 |

||

|

Montana Board of Housing 3.000% 06/01/2023 |

155,000 |

158,418 |

||

|

Montana Board of Housing 3.000% 12/01/2023 |

80,000 |

82,100 |

||

|

Montana Board of Housing 3.150% 06/01/2024 |

325,000 |

332,930 |

||

|

Montana Board of Housing 3.150% 12/01/2024 |

115,000 |

117,255 |

||

|

Montana Board of Housing 3.350% 06/01/2025 |

145,000 |

147,561 |

||

|

Montana Board of Housing 3.875% 12/01/2023 |

180,000 |

194,843 |

||

|

Montana Board of Housing 4.050% 06/01/2024 |

160,000 |

174,040 |

||

|

Montana Board of Housing 4.050% 12/01/2024 |

450,000 |

486,149 |

||

|

Montana Board of Housing 4.650% 12/01/2028 |

250,000 |

269,010 |

||

|

Montana Board of Housing 5.050% 12/01/2024 |

20,000 |

20,228 |

||

|

Montana Board of Housing 5.300% 12/01/2029 |

105,000 |

106,218 |

||

|

*Montana Board of Housing 4.700% 12/01/2026 |

715,000 |

745,459 |

||

|

Montana Board of Housing 4.850% 06/01/2028 |

335,000 |

346,604 |

||

|

Montana Board of Housing 3.850% 06/01/2019 |

465,000 |

472,505 |

||

|

Montana Board of Housing 2.650% 06/01/2019 |

150,000 |

151,076 |

||

|

Montana Board of Housing 2.900% 06/01/2020 |

150,000 |

151,631 |

||

|

Montana Board of Housing 3.100% 06/01/2021 |

380,000 |

390,351 |

||

|

|

4,755,667 |

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Other Revenue (9.3%) |

||||

|

City of Billings MT 5.500% 07/01/2026 |

$ |

300,000 |

$ |

317,292 |

|

City of Billings MT 4.550% 07/01/2020 |

65,000 |

65,080 |

||

|

City of Billings MT 4.700% 07/01/2021 |

70,000 |

70,123 |

||

|

City of Billings MT 4.800% 07/01/2022 |

70,000 |

69,845 |

||

|

City of Billings MT 4.000% 07/01/2018 |

205,000 |

205,038 |

||

|

City of Billings MT 4.375% 07/01/2029 |

490,000 |

510,438 |

||

|

*City of Billings MT 5.000% 07/01/2033 |

900,000 |

944,199 |

||

|

City of Bozeman MT 4.950% 07/01/2028 |

200,000 |

208,368 |

||

|

City & County of Butte-Silver Bow MT 5.000% 07/01/2021 |

600,000 |

619,332 |

||

|

Gallatin County Rural Improvement District 5.500% 07/01/2025 |

600,000 |

601,506 |

||

|

*Gallatin County Rural Improvement District 6.000% 07/01/2030 |

1,000,000 |

1,003,940 |

||

|

City of Great Falls MT 5.550% 07/01/2029 |

275,000 |

289,218 |

||

|

City of Helena MT 4.625% 01/01/2024 |

270,000 |

278,635 |

||

|

City of Helena MT 5.000% 01/01/2029 |

175,000 |

181,249 |

||

|

Missoula Parking Commission 4.000% 10/01/2026 |

835,000 |

921,314 |

||

|

City of Missoula MT 5.125% 07/01/2026 |

125,000 |

127,143 |

||

|

Montana Facility Finance Authority 6.300% 10/01/2020 |

505,000 |

506,050 |

||

|

|

6,918,770 |

|||

|

Transportation (7.3%) |

||||

|

City of Billings MT Airport Revenue 4.500% 07/01/2018 |

800,000 |

807,504 |

||

|

City of Billings MT Airport Revenue 4.750% 07/01/2019 |

350,000 |

362,082 |

||

|

City of Billings MT Airport Revenue 5.000% 07/01/2020 |

235,000 |

247,949 |

||

|

Madison County Rural Improvement District 5.500% 07/01/2025 |

770,000 |

771,548 |

||

|

*Madison County Rural Improvement District 6.000% 07/01/2030 |

1,000,000 |

1,003,390 |

||

|

City of Missoula MT 4.750% 07/01/2027 |

200,000 |

200,568 |

||

|

City of Missoula MT 6.000% 07/01/2030 |

200,000 |

212,188 |

||

|

Missoula Special Improvement Districts/MT 4.600% 07/01/2024 |

100,000 |

100,193 |

||

|

Missoula Special Improvement Districts/MT 4.600% 07/01/2025 |

105,000 |

105,161 |

||

|

Missoula Special Improvement Districts/MT 5.400% 07/01/2029 |

370,000 |

385,422 |

||

|

Missoula Special Improvement Districts/MT 4.000% 07/01/2019 |

125,000 |

127,064 |

||

|

Missoula Special Improvement Districts/MT 4.625% 07/01/2023 |

240,000 |

248,873 |

||

|

Missoula Special Improvement Districts/MT 5.250% 07/01/2027 |

240,000 |

251,664 |

||

|

Missoula Special Improvement Districts/MT 5.500% 07/01/2031 |

235,000 |

245,977 |

||

|

Montana Department of Transportation 5.000% 06/01/2022 |

350,000 |

355,268 |

||

|

|

5,424,851 |

|||

|

Utilities (4.4%) |

||||

|

City of Billings MT 5.000% 07/01/2028 |

400,000 |

494,612 |

||

|

City of Billings MT 5.000% 07/01/2031 |

260,000 |

316,774 |

||

|

City of Billings MT Storm Sewer Revenue 4.000% 07/01/2025 |

215,000 |

238,848 |

||

|

City of Billings MT Storm Sewer Revenue 4.000% 07/01/2026 |

225,000 |

248,033 |

||

|

City of Billings MT Storm Sewer Revenue 4.000% 07/01/2028 |

250,000 |

279,960 |

||

|

City of Billings MT Storm Sewer Revenue 4.000% 07/01/2029 |

250,000 |

276,683 |

||

|

City of Dillon MT Water & Sewer System Revenue 4.000% 07/01/2033 |

250,000 |

276,958 |

||

|

*City of Forsyth MT 5.000% 05/01/2033 |

1,000,000 |

1,089,860 |

||

|

|

3,221,728 |

|||

|

|

||||

|

TOTAL MUNICPAL BONDS (COST: $68,869,593) |

$ |

71,580,997 |

||

|

|

||||

|

OTHER ASSETS LESS LIABILITIES (3.5%) |

|

2,604,745 |

||

|

|

||||

|

NET ASSETS (100.0%) |

$ |

74,185,742 |

||

|

|

||||

|

|

||||

|

*Indicates all or a portion of bonds are segregated by the custodian to cover when-issued purchases. |

||||

|

|

||||

|

|

||||

|

The accompanying notes are an integral part of these financial statements. |

||||

VIKING TAX-FREE FUND FOR NORTH DAKOTA

PORTFOLIO MARKET SECTORS December 31, 2017

|

Other Revenue |

19.9% |

|

General Obligation |

19.1% |

|

Education |

18.0% |

|

Health Care |

17.5% |

|

Utilities |

9.3% |

|

Housing |

8.9% |

|

Transportation |

6.3% |

|

Cash Equivalents and Other |

1.0% |

|

100.0% |

Market sectors are breakdowns of the Fund’s portfolio holdings into specific investment classes.

These percentages are based on net assets.

SCHEDULE OF INVESTMENTS December 31, 2017

|

|

|

|

|

|

|

|

|

Principal |

|

Fair |

|

|

Amount |

|

Value |

|

|

MUNICIPAL BONDS (99.0%) |

||||

|

|

||||

|

Education (18.0%) |

||||

|

Barnes County North Public School District Building Authority 4.000% 05/01/2022 |

$ |

250,000 |

$ |

260,462 |

|

State Board of Higher Education of the State of North Dakota 4.000% 04/01/2025 |

415,000 |

469,552 |

||

|

State Board of Higher Education of the State of North Dakota 4.000% 04/01/2028 |

365,000 |

401,445 |

||

|

State Board of Higher Education of the State of North Dakota 4.000% 04/01/2026 |

435,000 |

482,519 |

||

|

State Board of Higher Education of the State of North Dakota 4.000% 04/01/2033 |

500,000 |

533,365 |

||

|

State Board of Higher Education of the State of North Dakota 5.000% 04/01/2026 |

500,000 |

607,545 |

||

|

State Board of Higher Education of the State of North Dakota 3.000% 08/01/2026 |

265,000 |

279,872 |

||

|

State Board of Higher Education of the State of North Dakota 3.000% 08/01/2027 |

275,000 |

285,082 |

||

|

State Board of Higher Education of the State of North Dakota 3.250% 08/01/2028 |

280,000 |

294,605 |

||

|

State Board of Higher Education of the State of North Dakota 3.250% 08/01/2029 |

290,000 |

300,649 |

||

|

State Board of Higher Education of the State of North Dakota 5.000% 04/01/2025 |

160,000 |

166,918 |

||

|

University of North Dakota 5.000% 04/01/2024 |

250,000 |

|

281,855 |

|

|

|

4,363,869 |

|||

|

General Obligation (19.1%) |

||||

|

City of Bismarck ND 3.000% 05/01/2023 |

500,000 |

518,100 |

||

|

Bismarck Public School District No 1 4.000% 05/01/2026 |

750,000 |

818,865 |

||

|

Dickinson Public School District No 1 4.000% 08/01/2034 |

400,000 |

430,800 |

||

|

City of Fargo ND 5.000% 05/01/2026 |

400,000 |

481,808 |

||

|

City of Fargo ND 4.000% 05/01/2023 |

300,000 |

323,514 |

||

|

City of Fargo ND 5.000% 05/01/2027 |

250,000 |

311,253 |

||

|

Mandan Public School District No 1 3.125% 08/01/2024 |

200,000 |

212,100 |

||

|

City of Minot ND Airport Revenue 3.500% 10/01/2025 |

570,000 |

601,413 |

||

|

City of Minot ND Airport Revenue 4.000% 10/01/2028 |

355,000 |

377,528 |

||

|

*West Fargo Public School District No 6 4.000% 05/01/2023 |

500,000 |

|

540,545 |

|

|

|

4,615,926 |

|||

|

Health Care (17.5%) |

||||

|

County of Burleigh ND 5.000% 07/01/2022 |

300,000 |

345,294 |

||

|

County of Burleigh ND 4.500% 07/01/2032 |

250,000 |

281,160 |

||

|

County of Burleigh ND 5.000% 07/01/2035 |

500,000 |

553,575 |

||

|

County of Burleigh ND 5.050% 11/01/2018 |

125,000 |

125,004 |

||

|

City of Fargo ND 5.500% 11/01/2020 |

500,000 |

555,560 |

||

|

City of Fargo ND 6.000% 11/01/2028 |

$ |

500,000 |

$ |

580,800 |

|

City of Grand Forks ND 5.000% 12/01/2022 |

500,000 |

551,625 |

||

|

City of Grand Forks ND 4.000% 12/01/2027 |

400,000 |

416,452 |

||

|

City of Grand Forks ND 5.000% 12/01/2032 |

250,000 |

267,352 |

||

|

City of Grand Forks ND 5.125% 12/01/2025 |

250,000 |

263,333 |

||

|

City of Grand Forks ND 3.000% 12/01/2020 |

135,000 |

133,796 |

||

|

City of Langdon ND 6.200% 01/01/2025 |

155,000 |

|

155,242 |

|

|

|

4,229,193 |

|||

|

Housing (8.9%) |

||||

|

North Dakota Housing Finance Agency 3.650% 01/01/2020 |

60,000 |

61,698 |

||

|

North Dakota Public Finance Authority 4.500% 06/01/2026 |

400,000 |

435,772 |

||

|

North Dakota Housing Finance Agency 2.900% 07/01/2020 |

300,000 |

305,535 |

||

|

North Dakota Housing Finance Agency 3.050% 07/01/2021 |

150,000 |

153,702 |

||

|

*North Dakota Housing Finance Agency 3.100% 01/01/2026 |

1,165,000 |

|

1,192,541 |

|

|

|

2,149,248 |

|||

|

Other Revenue (19.9%) |

||||

|

Bismarck Parks & Recreation District 3.500% 04/01/2025 |

280,000 |

286,580 |

||

|

Bismarck Parks & Recreation District 3.650% 04/01/2027 |

295,000 |

301,404 |

||

|

County of Burleigh ND Multi-County Sales Tax Revenue 4.000% 11/01/2032 |

400,000 |

419,132 |

||

|

City of Grand Forks ND 5.000% 12/15/2027 |

500,000 |

598,620 |

||

|

City of Grand Forks ND 5.000% 12/15/2028 |

250,000 |

296,900 |

||

|

Jamestown Park District/ND 4.000% 07/01/2033 |

345,000 |

363,996 |

||

|

City of Mandan ND 4.000% 09/01/2034 |

500,000 |

524,245 |

||

|

North Dakota Public Finance Authority 5.000% 06/01/2020 |

115,000 |

115,132 |

||

|

North Dakota Public Finance Authority 5.000% 06/01/2031 |

240,000 |

240,559 |

||

|

North Dakota Public Finance Authority 5.500% 10/01/2027 |

250,000 |

257,670 |

||

|

North Dakota Public Finance Authority 6.000% 06/01/2034 |

200,000 |

213,092 |

||

|

North Dakota Public Finance Authority 4.000% 06/01/2030 |

400,000 |

429,920 |

||

|

North Dakota Public Finance Authority 4.000% 06/01/2028 |

265,000 |

292,258 |

||

|

North Dakota Public Finance Authority 5.000% 06/01/2028 |

130,000 |

154,119 |

||

|

*County of Ward ND 3.000% 04/01/2022 |

300,000 |

|

308,235 |

|

|

|

4,801,862 |

|||

|

Transportation (6.3%) |

||||

|

Grand Forks Regional Airport Authority 4.600% 06/01/2024 |

350,000 |

364,178 |

||

|

Grand Forks Regional Airport Authority 5.000% 06/01/2029 |

500,000 |

523,880 |

||

|

Grand Forks Regional Airport Authority 4.500% 06/01/2028 |

230,000 |

250,383 |

||

|

Grand Forks Regional Airport Authority 4.500% 06/01/2028 |

370,000 |

|

396,388 |

|

|

|

1,534,829 |

|||

|

Utilities (9.3%) |

||||

|

City of Bismarck ND Water Revenue 3.000% 04/01/2021 |

495,000 |

505,157 |

||

|

*City of Bismarck ND Water Revenue 3.625% 04/01/2025 |

675,000 |

690,039 |

||

|

City of Bismarck ND Water Revenue 3.750% 04/01/2026 |

265,000 |

270,904 |

||

|

*County of McLean ND 4.875% 07/01/2026 |

750,000 |

|

794,490 |

|

|

|

2,260,590 |

|||

|

|

||||

|

TOTAL MUNICIPAL BONDS (COST: $22,904,702) |

$ |

23,955,517 |

||

|

|

||||

|

OTHER ASSETS LESS LIABILITIES (1.0%) |

|

242,063 |

||

|

|

||||

|

NET ASSETS (100.0%) |

$ |

24,197,580 |

||

|

|

||||

|

*Indicates all or a portion of bonds are segregated by the custodian to cover when-issued purchases. |

||||

|

|

||||

|

|

||||

|

The accompanying notes are an integral part of these financial statements. |

||||

FINANCIAL STATEMENTS

Statements of Assets and Liabilities December 31, 2017

|

Tax-Free |

Tax-Free |

|||

|

|

Fund for MT |

|

Fund for ND |

|

|

ASSETS |

||||

|

Investments in securities, at value |

$ |

71,580,997 |

$ |

23,955,517 |

|

Cash and cash equivalents |

1,586,107 |

64,606 |

||

|

Receivable for Fund shares sold |

52,202 |

0 |

||

|

Accrued interest receivable |

1,104,167 |

224,167 |

||

|

Prepaid expenses |

|

6,311 |

|

2,155 |

|

Total assets |

$ |

74,329,784 |

$ |

24,246,445 |

|

|

||||

|

LIABILITIES |

||||

|

Payable for Fund shares redeemed |

$ |

22,052 |

$ |

6,832 |

|

Dividends payable |

47,974 |

13,708 |

||

|

Trustees’ fees payable |

5,628 |

1,926 |

||

|

Payable to affiliates |

|

50,563 |

|

18,668 |

|

Accrued expenses |

17,825 |

7,731 |

||

|

Total liabilities |

$ |

144,042 |

$ |

48,865 |

|

|

||||

|

NET ASSETS |

$ |

74,185,742 |

$ |

24,197,580 |

|

|

||||

|

NET ASSETS ARE REPRESENTED BY: |

||||

|

Capital stock outstanding, $.001 par value, unlimited shares authorized |

$ |

74,303,442 |

$ |

24,036,254 |

|

Accumulated undistributed net realized gain (loss) on investments |

(2,835,199) |

(896,818) |

||

|

Accumulated undistributed net investment income (loss) |

6,095 |

7,329 |

||

|

Unrealized appreciation (depreciation) on investments |

|

2,711,404 |

|

1,050,815 |

|

|

||||

|

NET ASSETS |

$ |

74,185,742 |

$ |

24,197,580 |

|

|

||||

|

Net Assets - Class A |

$ |

68,989,647 |

$ |

23,548,110 |

|

Net Assets - Class I |

$ |

5,196,095 |

$ |

649,470 |

|

Shares outstanding - Class A |

6,841,126 |

2,294,538 |

||

|

Shares outstanding - Class I |

515,250 |

63,272 |

||

|

Net asset value per share - Class A* |

|

$10.08 |

|

$10.26 |

|

Net asset value per share - Class I |

|

$10.08 |

|

$10.26 |

|

Public offering price - Class A (sales charge of 2.50%) |

|

$10.34 |

|

$10.52 |

|

|

||||

|

*Redemption price per share is equal to net asset value less any applicable contingent deferred sales charge. |

||||

The accompanying notes are an integral part of these financial statements.

FINANCIAL STATEMENTS

Statements of Operations For the year ended December 31, 2017

|

Tax-Free |

Tax-Free |

|||

|

|

Fund for MT |

|

Fund for ND |

|

|

INVESTMENT INCOME |

||||

|

Interest |

$ |

2,578,113 |

$ |

905,729 |

|

Total investment income |

$ |

2,578,113 |

$ |

905,729 |

|

|

||||

|

EXPENSES |

||||

|

Investment advisory fees |

$ |

380,620 |

$ |

130,406 |

|

Distribution (12b-1) fees - Class A |

181,174 |

63,977 |

||

|

Transfer agent fees |

97,347 |

37,295 |

||

|

Administrative service fees |

142,557 |

72,497 |

||

|

Professional fees |

18,472 |

8,118 |

||

|

Reports to shareholders |

3,264 |

1,764 |

||

|

License, fees, and registrations |

4,176 |

5,676 |

||

|

Audit fees |

13,843 |

4,733 |

||

|

Trustees’ fees |

5,628 |

1,926 |

||

|

Transfer agent out-of-pockets |

3,610 |

4,208 |

||

|

Custodian fees |

7,976 |

2,920 |

||

|

Legal fees |

5,424 |

1,852 |

||

|

Insurance expense |

2,439 |

846 |

||

|

Total expenses |

$ |

866,530 |

$ |

336,218 |

|

Less expenses waived or reimbursed (See Note 7) |

|

(129,647) |

|

(81,950) |

|

Total net expenses |

$ |

736,883 |

$ |

254,268 |

|

|

|

|

|

|

|

NET INVESTMENT INCOME (LOSS) |

$ |

1,841,230 |

$ |

651,461 |

|

|

||||

|

REALIZED AND UNREALIZED GAIN (LOSS) ON INVESTMENTS |

||||

|

Net realized gain (loss) from investment transactions |

$ |

(388,203) |

$ |

12,516 |

|

Net change in unrealized appreciation (depreciation) of investments |

|

1,446,092 |

|

155,303 |

|

Net realized and unrealized gain (loss) on investments |

$ |

1,057,889 |

$ |

167,819 |

|

|

||||

|

NET INCREASE (DECREASE) IN NET ASSETS RESULTING FROM OPERATIONS |

$ |

2,899,119 |

$ |

819,280 |

The accompanying notes are an integral part of these financial statements.

FINANCIAL STATEMENTS

Statements of Changes in Net Assets For the year ended December 31, 2017

|

Tax-Free |

Tax-Free |

|||

|

|

Fund for MT |

|

Fund for ND |

|

|

INCREASE (DECREASE) IN NET ASSETS FROM OPERATIONS |

||||

|

Net investment income (loss) |

$ |

1,841,230 |

$ |

651,461 |

|

Net realized gain (loss) from investment transactions |

|

(388,203) |

|

12,516 |

|

Net change in unrealized appreciation (depreciation) on investments |

|

1,446,092 |

|

155,303 |

|

Net increase (decrease) in net assets resulting from operations |

$ |

2,899,119 |

$ |

819,280 |

|

|

||||

|

DISTRIBUTIONS TO SHAREHOLDERS FROM |

||||

|

Net investment income - Class A |

$ |

(1,741,882) |

$ |

(636,887) |

|

Net investment income - Class I |

(96,666) |

(13,406) |

||

|

Total distributions |

$ |

(1,838,548) |

$ |

(650,293) |

|

|

||||

|

CAPITAL SHARE TRANSACTIONS |

||||

|

Proceeds from sale of shares - Class A |

$ |

6,992,434 |

$ |

3,014,897 |

|

Proceeds from sale of shares - Class I |

4,955,361 |

299,947 |

||

|

Proceeds from reinvested dividends - Class A |

1,174,851 |

479,025 |

||

|

Proceeds from reinvested dividends - Class I |

44,625 |

10,039 |

||

|

Cost of shares redeemed - Class A |

(16,067,897) |

(5,498,565) |

||

|

Cost of shares redeemed - Class I |

(665,065) |

(48,007) |

||

|

Net increase (decrease) in net assets resulting from capital share transactions |

$ |

(3,565,691) |

$ |

(1,742,664) |

|

|

||||

|

TOTAL INCREASE (DECREASE) IN NET ASSETS |

$ |

(2,505,120) |

$ |

(1,573,677) |

|

NET ASSETS, BEGINNING OF PERIOD |

$ |

76,690,862 |

$ |

25,771,257 |

|

NET ASSETS, END OF PERIOD |

$ |

74,185,742 |

$ |

24,197,580 |

|

|

||||

|

Accumulated undistributed net investment income |

$ |

6,095 |

$ |

7,329 |

The accompanying notes are an integral part of these financial statements.

FINANCIAL STATEMENTS

Statements of Changes in Net Assets For the year ended December 30, 2016

|

Tax-Free |

Tax-Free |

|||

|

|

Fund for MT |

|

Fund for ND |

|

|

INCREASE (DECREASE) IN NET ASSETS FROM OPERATIONS |

||||

|

Net investment income (loss) |

$ |

1,995,856 |

$ |

675,057 |

|

Net realized gain (loss) from investment transactions |

|

(551,409) |

|

(127,251) |

|

Net change in unrealized appreciation (depreciation) on investments |

|

(2,002,888) |

|

(578,191) |

|

Net increase (decrease) in net assets resulting from operations |

$ |

(558,441) |

$ |

(30,385) |

|

|

||||

|

DISTRIBUTIONS TO SHAREHOLDERS FROM |

||||

|

Net investment income - Class A |

$ |

(1,990,381) |

$ |

(670,541) |

|

Net investment income - Class I* |

(4,734) |

(3,295) |

||

|

Total distributions |

$ |

(1,995,115) |

$ |

(673,836) |

|

|

||||

|

CAPITAL SHARE TRANSACTIONS |

||||

|

Proceeds from sale of shares - Class A |

$ |

18,045,397 |

$ |

3,944,247 |

|

Proceeds from sale of shares - Class I* |

848,581 |

409,022 |

||

|

Proceeds from reinvested dividends - Class A |

1,327,137 |

524,042 |

||

|

Proceeds from reinvested dividends - Class I* |

4,633 |

2,349 |

||

|

Cost of shares redeemed - Class A |

(10,782,950) |

(4,439,248) |

||

|

Cost of shares redeemed - Class I* |

(9,529) |

(9,559) |

||

|

Net increase (decrease) in net assets resulting from capital share transactions |

$ |

9,433,269 |

$ |

430,853 |

|

|

||||

|

TOTAL INCREASE (DECREASE) IN NET ASSETS |

$ |

6,879,713 |

$ |

(273,368) |

|

NET ASSETS, BEGINNING OF PERIOD |

$ |

69,811,149 |

$ |

26,044,625 |

|

NET ASSETS, END OF PERIOD |

$ |

76,690,862 |

$ |

25,771,257 |

|

|

||||

|

Accumulated undistributed net investment income |

$ |

3,543 |

$ |

6,161 |

* Class I operations commenced on August 1, 2016.

The accompanying notes are an integral part of these financial statements.

NOTES TO FINANCIAL STATEMENTS

NOTE 1: Organization

Viking Mutual Funds (the “Trust”) was organized as a Delaware business trust on March 30, 1999 and commenced operations on August 3, 1999. The Trust is registered under the Investment Company Act of 1940 as an open-end management investment company and consists of multiple series (the “Funds”).

The Viking Tax-Free Fund for Montana (“Tax-Free Fund for MT”) and Viking Tax-Free Fund for North Dakota (“Tax-Free Fund for ND”), each a non-diversified Fund, seek the highest level of current income that is exempt from both federal and state income taxes and is consistent with preservation of capital.

On May 18, 2017, the Board of Trustees approved the reorganization of each series of the Integrity Managed Portfolios (Kansas Municipal Fund, Maine Municipal Fund, Nebraska Municipal Fund, New Hampshire Municipal Fund, and Oklahoma Municipal Fund) into the corresponding series of Viking Mutual Funds and the addition of I shares to each corresponding series. The reorganization was also approved by each Fund’s shareholders at a special meeting held on September 21, 2017. The reorganization occurred at the close of business on October 31, 2017.

Each Fund in the Trust currently offers both Class A and Class I shares. Tax-Free Fund for MT Class A and Tax-Free Fund for North Dakota Class A are sold with an initial sales charge of 2.50% and a distribution fee of up to 0.25% on an annual basis. Class I shares are sold without sales charge or distribution fee. The two classes of shares represent interest in each Fund’s same portfolio of investments, have the same rights, and are generally identical in all respects except that each class bears its separate distribution and certain other class expenses and has exclusive voting rights with respect to any matter on which a separate vote of any class is required.

Each Fund is an investment company and, accordingly, follows the investment company accounting and reporting guidance of the Financial Accounting Standards Board (FASB) Accounting Standard Codification Topic 946 Financial Services – Investment Companies.

NOTE 2: Summary of Significant Accounting Policies

Investment security valuation—Securities for which quotations are not readily available are valued at fair value using a matrix system as determined by the Funds’ administrative services agent, Integrity Fund Services, LLC (“Integrity Fund Services” or “IFS”). The matrix system has been developed based on procedures approved by the Board of Trustees and includes consideration of the following: yields or prices of municipal bonds of comparable quality; type of issue, coupon, maturity, and rating; indications as to value from dealers; and general market conditions. Because the market value of securities can only be established by agreement between parties in a sales transaction, and because of the uncertainty inherent in the valuation process, the fair values as determined may differ from the values that would have been used had a readily available market for the securities existed. Shares of a registered investment company, including money market funds, that are not traded on an exchange are valued at the investment company’s net asset value per share. Refer to Note 3 for further disclosures related to the inputs used to value the Funds’ investments.

When-issued securities—The Funds may purchase securities on a when-issued basis. Payment and delivery may take place after the customary settlement period for that security. The price of the underlying securities and the date when the securities will be delivered and paid for are fixed at the time the transaction is negotiated. The value of the securities purchased on a when-issued basis are identified as such in each Fund’s Schedule of Investments. With respect to purchase commitments, the Funds identify securities to be segregated by the custodian in its records with a value at least equal to the amount of the commitment. Losses may arise due to changes in the value of the underlying securities, if the counterparty does not perform under the contract terms, or if the issuer does not issue the securities due to political, economic, or other factors. There were no when-issued securities as of December 31, 2017.

Contingent deferred sales charge—Investments in Class A shares of $1 million or more may be subject to a 1.00% contingent deferred sales charge (“CDSC”) if redeemed within 24 months of purchase (excluding shares purchased with reinvested dividends and/or distributions).

Federal and state income taxes—Each Fund is a separate taxpayer for federal income tax purposes. Each Fund’s policy is to comply with the requirements of the Internal Revenue Code that are applicable to regulated investment companies and to distribute substantially all of its net investment income and any net realized gain on investments to its shareholders; therefore, no provision for income taxes is required.

As of and during the year ended December 31, 2017, the Funds did not have a liability for any unrecognized tax benefits. The Funds recognize interest and penalties, if any, related to unrecognized tax benefits as income tax expense in the Statements of Operations. During the year, the Funds did not incur any interest or penalties.

For all open tax years and all major taxing jurisdictions, management of the Funds has concluded that there are no significant uncertain tax positions that would require recognition in the financial statements. Open tax years are those that are open for examination by taxing authorities. Furthermore, management of the Funds is also not aware of any tax positions for which it is reasonably possible that the total amounts of unrecognized tax benefits will significantly change in the next twelve months.

Premiums and discounts—Premiums and discounts on municipal securities are accreted and amortized using the effective yield method over the lives of the respective securities for financial reporting purposes.

Cash and cash equivalents—The Funds consider investments in an FDIC insured interest bearing savings account to be cash. The Fund maintains cash balances, which, at times, may exceed federally insured limits. The Fund maintains these balances with a high quality financial institution.

Security transactions, investment income, expenses and distributions—Income and expenses are recorded on the accrual basis. Investment transactions are accounted for on the trade date. Realized gains and losses are reported on the specific identification basis. Interest income and estimated expenses are accrued daily. The Funds declare dividends from net investment income daily and pay such dividends monthly. Capital gains, when available, are distributed at least annually. Dividends are reinvested in additional shares of the Funds at net asset value or paid in cash. Distributions to shareholders are recorded on the ex-dividend date. Income and capital gain distributions are determined in accordance with federal income tax regulations and may differ from net investment income and realized gains determined in accordance with accounting principles generally accepted in the United States of America. These differences are primarily due to differing treatment of market discount. In addition, other amounts have been reclassified within the composition of net assets to more appropriately conform financial accounting to tax basis treatment.

Use of estimates—The financial statements have been prepared in accordance with accounting principles generally accepted in the United States of America (“GAAP”), which requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the reporting period. Actual results could differ from those estimates.

Common expenses—Common expenses of the Trust are allocated among the Funds within the Trust based on relative net assets of each Fund or the nature of the services performed and the relative applicability to each Fund.

NOTE 3: Fair Value Measurements

Various inputs are used in determining the value of the Funds' investments. These inputs are summarized in three broad levels: Level 1 inputs are based on quoted prices in active markets for identical securities. Level 2 inputs are based on significant observable inputs (including quoted prices for similar securities, interest rates, prepayment speeds, credit risk, etc.). Level 3 inputs are based on significant unobservable inputs (including each Fund's own assumptions in determining the fair value of investments). The following is a summary of the inputs used to value the Funds’ investments as of December 31, 2017:

|

|

Level 1 |

Level 2 |

Level 3 |

Total |

|||||||||

|

Tax-Free Fund for MT |

Municipal Bonds |

$ |

0 |

$ |

71,580,997 |

$ |

0 |

$ |

71,580,997 |

||||

|

Total |

$ |

0 |

$ |

71,580,997 |

$ |

0 |

$ |

71,580,997 |

|||||

|

|

|||||||||||||

|

Tax-Free Fund for ND |

Municipal Bonds |

$ |

0 |

$ |

23,955,517 |

$ |

0 |

$ |

23,955,517 |

||||

|

Total |

$ |

0 |

$ |

23,955,517 |

$ |

0 |

$ |

23,955,517 |

Please refer to the Schedule of Investments for sector classification. The Funds did not hold any Level 3 assets during the year ended December 31, 2017. There were no transfers into or out of Level 1 or Level 2 during the year ended December 31, 2017. The Funds consider transfers into or out of Level 1 and Level 2 as of the end of the reporting period. The Funds did not hold any derivative instruments at any time during the year ended December 31, 2017.

NOTE 4: Investment Transactions

Purchases and sales of investment securities (excluding short-term securities) for the year ended December 31, 2017, were as follows:

|

Tax-Free Fund for MT |

Tax-Free Fund for ND |

||

|

Purchases |

$15,070,725 |

$2,828,521 |

|

|

Sales |

$19,120,448 |

$4,381,945 |

NOTE 5: Capital Share Transactions

|

Year Ended 12/31/17: |

Tax-Free |

Tax-Free |

||

|

Class A |

Fund for MT |

Fund for ND |

||

|

Shares sold |

695,195 |

292,668 |

||

|

Shares issued from reinvestments |

116,868 |

46,603 |

||

|

Shares redeemed |

(1,597,587) |

(534,065) |

||

|

Net increase (decrease) |

(785,524) |

(194,794) |

||

|

Class I |

||||

|

Shares sold |

494,381 |

29,066 |

||

|

Shares issued from reinvestments |

4,433 |

976 |

||

|

Shares redeemed |

(66,028) |

(4,661) |

||

|

Net increase (decrease) |

432,786 |

25,381 |

||

|

|

|

|

|

|

|

Year Ended 12/30/16: |

Tax-Free |

Tax-Free |

||

|

Class A |

Fund for MT |

Fund for ND |

||

|

Shares sold |

1,749,393 |

374,263 |

||

|

Shares issued from reinvestments |

129,262 |

49,843 |

||

|

Shares redeemed |

(1,058,209) |

(422,651) |

||

|

Net increase (decrease) |

820,446 |

1,455 |

||

|

Class I |

||||

|

Shares sold |

82,963 |

38,603 |

||

|

Shares issued from reinvestments |

462 |

227 |

||

|

Shares redeemed |

(961) |

(939) |

||

|

Net increase (decrease) |

82,464 |

37,891 |

NOTE 6: Income Tax Information

At December 31, 2017, the net unrealized appreciation (depreciation) based on the cost of investments for federal income tax purposes was as follows:

|

|

Tax-Free Fund for MT |

|

Tax-Free Fund for ND |

|

Investments at cost |

$68,863,605 |

|

$22,897,373 |

|

Unrealized appreciation |

$2,770,982 |

|

$1,063,954 |

|

Unrealized depreciation |

(53,590) |

|

(5,810) |

|

Net unrealized appreciation (depreciation) |

$2,717,392* |

|

$1,058,144* |

*Differences between financial reporting-basis and tax-basis unrealized appreciation/(depreciation) are due to differing treatment of market discount.

The tax character of distributions paid was as follows:

|

|

Tax-Free Fund for MT |

|

Tax-Free Fund for ND |

||||

|

|

Year |

|

Year |

|

Year |

|

Year |

|

|

Ended 12/31/17 |

|

Ended 12/30/16 |

|

Ended 12/31/17 |

|

Ended 12/30/16 |

|

Tax-exempt income |

$1,838,548 |

|

$1,995,115 |

|

$650,293 |

|

$673,836 |

As of December 31, 2017, the components of accumulated earnings/(deficit) on a tax basis were as follows:

|

|

Tax-Free Fund for MT |

|

Tax-Free Fund for ND |

|

Undistributed tax-exempt income |

$107 |

|

$0 |

|

Accumulated capital and other (losses) |

(2,835,199) |

|

(896,818) |

|

Unrealized appreciation/(depreciation)* |

2,717,392 |

|

1,058,144 |

|

Total accumulated earnings/(deficit) |

($117,700) |

|

($161,326) |

*Differences between financial reporting-basis and tax-basis unrealized appreciation/(depreciation) are due to differing treatment of market discount.

The tax components of distributable earnings are determined in accordance with income tax regulations which may differ from the composition of net assets reported under GAAP. Accordingly, for the year ended December 31, 2017, certain differences were reclassified in the Tax-Free Fund for MT as follows: and accumulated net investment income to accumulated realized gains (losses) of $130 due to market discount on the sale of bonds.

Under the Regulated Investment Company Modernization Act of 2010 (“Act”), funds are permitted to carry forward capital losses incurred in taxable years beginning after December 22, 2010 for an unlimited period of time. The short-term and long-term character of such losses are retained rather than being treated as short-term as under previous law. Pre-enactment losses are eligible to be carried forward for a maximum period of eight years. Pursuant to the Act, post-enactment capital losses must be utilized before pre-enactment capital losses. As a result, pre-enactment capital loss carryforwards may be more likely to expire unused. The Funds’ capital loss carryforward amounts as of December 29, 2016 are as follows:

|

|

Tax-Free Fund for MT |

|

Tax-Free Fund for ND |

|

Expires in 2018 |

$106,551 |

|

$75,200 |

|

Non-expiring short-term losses |

$1,701,122 |

|

$536,257 |

|

Non-expiring long-term losses |

$1,027,526 |

|

$285,361 |

|

Total Capital Loss Carryforwards |

$2,835,199 |

|

$896,818 |

Tax-Free Fund for ND utilized $12,516 of capital loss carryforwards against current year capital gains.

NOTE 7: Investment Advisory Fees and Other Transactions with Affiliates

Viking Fund Management (“VFM”), the Funds’ investment adviser; Integrity Funds Distributor, LLC (“Integrity Funds Distributor” or “IFD”), the Funds’ underwriter and distributor; and Integrity Fund Services, the Funds’ transfer, accounting, and administrative services agent; are subsidiaries of Corridor Investors, LLC (“Corridor Investors” or “Corridor”), the Funds’ sponsor. A Trustee of the Funds is also a Governor of Corridor.

VFM provides investment advisory and management services to the Funds. The Investment Advisory Agreement (the “Advisory Agreement”) provides for fees to be computed at an annual rate of 0.50% of each Fund’s average daily net assets. VFM has contractually agreed to pay all the expenses of the Funds (other than extraordinary or non-recurring expenses, taxes, brokerage fees, commissions, and acquired fund fees and expenses) until April 29, 2019 so that the net annual operating expenses do not exceed 0.98% and 0.73% for Class A and I, respectively. After this date, the expense limitations may be terminated or revised. There are no recoupment provisions in place for waived/reimbursed fees. VFM and the affiliated service providers agreed to waive the affiliated service provider’s fees before waiving VFM’s management fee for the period January 1, 2017 through May 12, 2017. VFM and affiliated service providers may also voluntarily waive fees or reimburse expenses not required under the advisory or other contracts from time to time. During the year ended December 31, 2017 there were no voluntary waivers. An expense limitation lowers expense ratios and increases returns to investors. Certain Officers of the Funds are also Officers and Governors of VFM.

|

Year Ended 12/31/17 |

Payable 12/31/17 |

||||||

|

Advisory Fees* |

Advisory Fees Waived |

Advisory Fees* |

|||||

|

Tax-Free Fund for MT |

$ |

267,672 |

$ |

112,948 |

$ |

18,987 |

|

|

Tax-Free Fund for ND |

$ |

60,519 |

$ |

69,887 |

$ |

3,208 |

|

*After waivers.

IFD serves as the principal underwriter and distributor for the Funds and receives sales charges deducted from Fund share sales proceeds and CDSC from applicable Fund share redemptions. Also, the Funds have adopted a distribution plan for each class of shares as allowed by Rule 12b-1 of the 1940 Act. Distribution plans permit the Funds to reimburse its principal underwriter for costs related to selling shares of the Funds and for various other services. These costs, which consist primarily of commissions and service fees to broker-dealers who sell shares of the Funds, are paid by shareholders through expenses called “Distribution Plan expenses.” The Class A shares currently pay an annual distribution fee of up to 0.25% of the average daily net assets. Certain Officers of the Funds are also Officers and Governors of IFD.

|

Year Ended 12/31/17 |

Payable 12/31/17 |

||||||||||||||

|

Sales |

|

Distribution |

Distribution |

Sales |

|

Distribution |

|||||||||

|

Charges |

CDSC |

Fees* |

Fees Waived |

Charges |

CDSC |

Fees* |

|||||||||

|

Tax-Free Fund for MT - A |

$ |

87,838 |

$ |

0 |

$ |

181,174 |

$ |

0 |

$ |

0 |

$ |

0 |

$ |

13,678 |

|

|

Tax-Free Fund for ND - A |

$ |

41,511 |

$ |

0 |

$ |

63,977 |

$ |

0 |

$ |

0 |

$ |

0 |

$ |

4,756 |

|

*After waivers.

IFS acts as the Funds’ transfer agent for a monthly variable fee equal to 0.12% of the average daily net assets on an annual basis for the first $0 to $200 million and at a lower rate in excess of $200 million and an additional fee of $500 per month for each additional share class plus reimbursement of out-of-pocket expenses and sub-transfer agent out-of-pocket expenses. Sub-transfer agent out-of-pocket expenses are included in the transfer agent fees below and in the transfer agent out-of-pocket balance on the Statements of Operations. IFS also acts as the Funds’ administrative services agent for a monthly fee equal to the sum of a fixed fee of $2,000 and a variable fee equal to 0.14% of the Funds’ average daily net assets on an annual basis for the first $0 to $200 million and at a lower rate in excess of $200 million plus reimbursement of out-of-pocket expenses. Certain Officers of the Funds are also Officers and Governors of IFS.

|

Year Ended 12/31/17 |

Payable 12/31/17 |

||||||||||||

|

Transfer |

Transfer |

Admin. |

Admin. |

Transfer |

Admin. |

||||||||

|

Agency |

Agency |

Service |

Service |

Agency |

Service |

||||||||

|

Fees* |

Fees Waived |

Fees* |

Fees Waived |

Fees* |

Fees* |

||||||||

|

Tax-Free Fund for MT |

$ |

94,170 |

$ |

6,787 |

$ |

132,645 |

$ |

9,912 |

$ |

6,832 |

$ |

11,066 |

|

|

Tax-Free Fund for ND |

$ |

37,407 |

$ |

4,096 |

$ |

64,530 |

$ |

7,967 |

$ |

5,109 |

$ |

5,595 |

|

|

* After waivers. |

|||||||||||||

NOTE 8: Principal Risks

The Funds invest primarily in municipal securities from a specific state. The Funds may also invest in municipal securities of U.S. territories and possessions (such as Puerto Rico, the U.S. Virgin Islands, and Guam). Each Fund is therefore more susceptible to political, economic, legislative, or regulatory factors adversely affecting issuers of municipal securities in its specific state or U.S. territories and possessions.

Interest rate risk is the risk that bond prices will decline in value because of changes in interest rates. There is normally an inverse relationship between the fair value of securities sensitive to prevailing interest rates and actual changes in interest rates. The longer the average maturity of each Fund’s portfolio, the greater its interest rate risk.

NOTE 9: Subsequent Events