UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

(Mark One)

FORM 10-K

[X] ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2012

or

[ ] TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from ______________________________ to ___________________________________

Commission File Number: 0-26119

UONLIVE CORPORATION

(Exact name of registrant as specified in its charter)

|

Nevada |

87-0629754 |

|

(State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer Identification No.) |

5/F, Guangdong Finance Building, 88 Connaught Road West, Hong Kong

|

(Address of principal executive offices) |

(Zip Code) |

Registrant’s telephone number, including area code + (852) 2116-3560

Securities registered pursuant to Section 12(b) of the Act:

|

Title of each class |

Name of each exchange on which registered | |

Securities registered pursuant to section 12(g) of the Act:

Common Stock, par value $.001 per share

(Title of class)

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

☐ Yes ☒ No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

☐ Yes ☒ No

Note – Checking the box above will not relieve any registrant required to file reports pursuant to Section 13 or 15(d) of the Exchange Act from their obligations under those Sections.

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

☐ Yes ☒ No

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

☒ Yes ☐ No

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ☐ Yes ☒ No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

|

Large accelerated filer ☐ |

Accelerated filer ☐ |

|

Non-accelerated filer (Do not check if a smaller reporting company) ☐ |

Smaller reporting company ☒ |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). ☒ Yes ☐ No

State the aggregate market value of the voting and non-voting common equity held by non-affiliates computed by reference to the price at which the common equity was last sold, or the average bid and asked price of such common equity, as of the last business day of the registrant’s most recently completed second fiscal quarter.

Note.—If a determination as to whether a particular person or entity is an affiliate cannot be made without involving unreasonable effort and expense, the aggregate market value of the common stock held by non-affiliates may be calculated on the basis of assumptions reasonable under the circumstances, provided that the assumptions are set forth in this Form.

The aggregate market value of the voting and non-voting common equity held by non-affiliates June 30, 2012, computed by reference to the closing price of $0.34 on June 30, 2012 is $94,681.50.

APPLICABLE ONLY TO REGISTRANTS INVOLVED IN BANKRUPTCY

PROCEEDINGS DURING THE PRECEDING FIVE YEARS:

Indicate by check mark whether the registrant has filed all documents and reports required to be filed by Section 12, 13 or 15(d) of the Securities Exchange Act of 1934 subsequent to the distribution of securities under a plan confirmed by a court. ☐ Yes ☐ No

(APPLICABLE ONLY TO CORPORATE REGISTRANTS)

Indicate the number of shares outstanding of each of the registrant’s classes of common stock, as of the latest practicable date.

The number of shares of the issuer’s common stock, par value $.001 as of November 20, 2014 is 1,996,355.

DOCUMENTS INCORPORATED BY REFERENCE

List hereunder the following documents if incorporated by reference and the Part of the Form 10-K (e.g., Part I, Part II, etc.) into which the document is incorporated: (1) Any annual report to security holders; (2) Any proxy or information statement; and (3) Any prospectus filed pursuant to Rule 424(b) or (c) under the Securities Act of 1933. The listed documents should beclearly described for identification purposes (e.g., annual report to security holders for fiscal year ended December 24, 1980).

PART 1

Item 1. Business

CAUTIONARY STATEMENT REGARDING FORWARD LOOKING INFORMATION

This annual report on Form 10-K under the Securities Exchange Act of 1934, as amended, contains forward-looking statements that involve risks and uncertainties. Our actual results could differ significantly from those discussed herein. These include statements about our expectations, beliefs, intentions or strategies for the future, which we indicate by words or phrases such as "anticipate," "expect," "intend," "plan," "will," "we believe," "the Company believes," "management believes" and similar language, including those set forth in the discussion under "Business" and "Management's Discussion and Analysis of Financial Condition and Results of Operations," as well as those discussed elsewhere in this Form 10-K. We base our forward-looking statements on information currently available to us, and we assume no obligation to update them. Statements contained in this Form 10-K that are not historical facts are forward-looking statements.

History of Our Company

We were incorporated in the State of Nevada on January 29, 1998 under the name Txon International Development Corporation to conduct any lawful business, to exercise any lawful purpose and power, and to engage in any lawful act or activity for which corporations may be organized under the General Corporation Laws of Nevada.

On August 14, 2000, pursuant to a share exchange agreement dated August 10, 2000, by and among Main Edge International Limited (“Main Edge”), Virtual Edge Limited (“Virtual Edge”), Richard Ford, Jeanie Hildebrand and Gary Lewis, we acquired from Main Edge all of the shares of Virtual Edge (the “Acquisition”) in exchange for an aggregate of 1,961,175 shares of our common stock, which shares equaled 75.16% of Txon International’s issued and outstanding shares after giving effect to the Acquisition. On September 15, 2000, Txon International Development Corporation changed its name to China World Trade Corporation (“CWTD”).

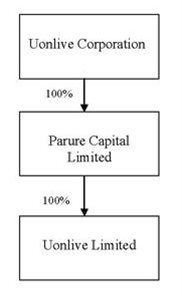

On March 28, 2008, CWTD entered into a Share Exchange Agreement (the “Exchange Agreement”) by and among CWTD, William Tsang (“Tsang”), Uonlive Limited, a corporation organized and existing under the laws of the Hong Kong SAR of the People’s Republic of China (“Uonlive”), Tsun Sin Man Samuel, Chairman of Uonlive (“Tsun”), Hui Chi Kit, Chief Financial Officer of Uonlive (“Hui”), Parure Capital Limited, a corporation organized and existing under the laws of the British Virgin Islands and parent of Uonlive (“Parure Capital”). Upon closing of the share exchange transaction contemplated under the Exchange Agreement, Tsun and Hui transferred all of their share capital in Parure Capital to CWTD in exchange for an aggregate of 150,000,000 shares of common stock of the Registrant and 500,000 shares of Series A Convertible Preferred Stock of the Registrant, which is convertible after six months from the date of issuance into 100 shares of common stock of the Registrant, thus causing Parure Capital to become a direct wholly-owned subsidiary of the Registrant.

On July 2, 2008, the proposal to amend the articles of incorporation to change the name of the corporation to Uonlive Corporation was approved by the action of a majority of all shareholders entitled to vote on the record date and by CWTD’s Board of Directors. CWTD desired to change its name to truly reflect its new business as a holding company for Uonlive Limited, and possibly other companies that may be acquired in the future by the company (the “Company” or “Uonlive”).

On May 15, 2009, the Company approved the 1 for 100 reverse split of its common stock.

The Company and subsidiaries are hereinafter collectively referred to as the “Company.”

Our mailing address is located at 5/F, Guangdong Finance Building, 88 Connaught Road West, Hong Kong.

Corporate Structure

Uonlive was, until December 31, 2011, an online multimedia company headquartered in Hong Kong SAR, China. The main business of Uonlive was operating an online radio station targetted at a younger audience.

During the first quarter of 2012, our management, after consulting the Board of Directors, decided to cease our operations because of minimal revenue and no improvement in developing the market for internet radio in Hong Kong.

As reflected in the accompanying financial statements, the Company has no source of revenues and needs additional cash resources to maintain its operations. The Company’s ability to continue as a going concern is dependent on its ability to raise additional capital or obtain necessary debt financing. These factors raise substantial doubt about our ability to continue as a going concern. As discussed elsewhere, our current business plan is to seek and identify a privately-held operating company desiring to become a publicly held company by combining with us through a reverse merger or acquisition type transaction. We cannot predict when, if ever, we will be successful in this venture and, accordingly, we may be required to cease operations at any time, if we do not have sufficient working capital to pay our operating costs for the next 12 months and we will require additional funds to pay our legal, accounting and other fees associated with our Company and its filing obligations under United States federal securities laws, as well as to pay our other accounts payable generated in the ordinary course of our business.

Business Plan

Our current business plan is to seek and identify a privately owned company which is looking to become a publicly listed company by combining their operation with us through a reverse merger. Private companies wishing to have their securities publicly traded may seek to merge or effect an exchange transaction with a shell company with a significant stockholder base. As a result of the merger or exchange transaction, the stockholders of the private company will hold a majority of the issued and outstanding shares of the shell company. Typically, the directors and officers of the private company become the directors and officers of the shell company. Often the name of the private company becomes the name of the shell company.

We have no capital and must depend on our controlling shareholders to provide us funding for our daily operation and expenses, including professional fee and fees charged by regulators, although they are under no obligation to do so. Mr. Hui Chi Kit is primarily tasked to investigate acquisition opportunities although we believe that business opportunities may also come to our attention from various sources, including our controlling shareholders, professional advisors such as attorneys and accountants, securities broker-dealers, venture capitalists, members of the financial community, and others who may present unsolicited proposals.

We cannot give assurance that we will successfully find a suitable candidate to implement its operation with us by a reverse merge. We also cannot give assurance that any acquisition, if occurs, will be on terms that are favorable to us or to our shareholders.

We do not propose to restrict our search for candidates in any particular geographical area of industry. Our management’s discretion in the selection of the business opportunities is unrestricted, subject to the availability of such opportunities, economic conditions, and other factors.

Any entity which has an interest in being acquired by, or merging into us, is expected to be an entity that desires to become a public company and establish a public trading market for its securities. In connection with such a merger or acquisition, it is anticipated that an amount of common stock constituting control of us would be issued by us.

Investigation and Selection of Business Opportunities

Certain types of business acquisition transactions may be completed without requiring us to first submit the transaction to our stockholders for their approval. If the proposed transaction is structured in such a fashion our stockholders (other than our controlling stockholders) will not be provided with financial or other information relating to the candidate prior to the completion of the transaction.

If a proposed business combination or business acquisition transaction is structured that requires our stockholder approval, and we are a reporting company, we will be required to provide our stockholders with information as applicable under Regulations 14A and 14C under the Exchange Act.

The analysis of business opportunities will be undertaken by or under the supervision of Mr.Hui Chi Kit, our Chief Financial Officer. In analyzing potential merger candidates, our management will consider, among other things, the following factors:

|

* |

Potential for future earnings and appreciation of value of securities; |

|

* |

Perception of how any particular business opportunity will be received by the investment community and by our stockholders; |

|

* |

Eligibility of a candidate, following the business combination, to qualify its securities for listing on a national exchange or on a national automated securities quotation system, such as NASDAQ. |

|

* |

Historical results of operations; |

|

* |

Liquidity and availability of capital resources; |

|

* |

Competitive position as compared to other companies of similar size and experience within the industry segment as well as within the industry as a whole; |

|

* |

Strength and diversity of existing management or management prospects that are scheduled for recruitment; |

|

* |

Amount of debt and contingent liabilities; and |

|

* |

The products and/or services and marketing concepts of the target company. |

There is no single factor that will be controlling in the selection of a business opportunity. Our management will attempt to analyze all factors appropriate to each opportunity and make a determination based upon reasonable measures and available data. Potentially available business opportunities may occur in many different industries and at various stages of development, all of which will make the task of comparative investigation and analysis of such business opportunities extremely difficult and complex. Because of our limited working capital available and limited personnel to perform due diligence and investigation we may not discover or adequately evaluate adverse facts about the business opportunity to be acquired.

We are unable to predict when we may participate in a business opportunity. Prior to making a decision to participate in a business transaction, we will generally request that we be provided with written materials regarding the business opportunity, including, but not limited to, a description of products, services and company history; financial information; available projections, with related assumptions upon which they are based; an explanation of proprietary products and services; evidence of existing patents, trademarks, or service marks, or rights thereto; present and proposed forms of compensation to management; a description of transactions between such company and its affiliates during the relevant periods; a description of present and required facilities; an analysis of risks and competitive conditions; audited financial statements, or if audited financial statements are not available, unaudited financial statements, together with reasonable assurance that audited financial statements would be able to be produced to comply with the requirements of a Current Report on Form 8-K to be filed with the Securities and Exchange Commission, upon consummation of the business combination.

We believe that various types of potential candidates might find a business combination with us to be attractive. These include candidates desiring to create a public market for their securities in order to enhance liquidity for current stockholders, candidates which have long-term plans for raising capital through public sale of securities and believe that the prior existence of a public market for their securities would be beneficial, and candidates which plan to acquire additional assets through issuance of securities rather than for cash, and believe that the development of a public market for their securities will be of assistance in that process.

Employees

The Company currently has two employees, namely our Chief Executive Officer, Samuel Tsun and our Chief Financial Officer, Hui Chi Kit. Management of the Company expects to use consultants, attorneys and accountants as necessary, and does not anticipate a need to engage any full-time employees so long as it is seeking and evaluating business opportunities. The need for employees and their availability will be addressed in connection with the decision whether or not to acquire or participate in specific business opportunities.

Item 1A. Rick Factors.

OUR INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM HAVE EXPRESSED THEIR CONCERN AS TO OUR ABILITY TO CONTINUE AS A GOING CONCERN.

As reflected in the accompanying financial statements, we have no source of revenues and need additional cash resources to maintain our operations. These factors raise substantial doubt about our ability to continue as a going concern. Our ability to continue as a going concern is dependent on our ability to raise additional capital or obtain necessary debt financing. As discussed, our current business plan is to seek and identify a privately-held operating company desiring to become a publicly held company by combining with us through a reverse merger or acquisition type transaction. We cannot predict when, if ever, we will be successful in this venture and, accordingly, we may be required to cease operations at any time, if we do not have sufficient working capital to pay our operating costs for the next 12 months and we will require additional funds to pay our legal, accounting and other fees associated with our company and our filing obligations under United States federal securities laws, as well as to pay our other accounts payable generated in the ordinary course of our business.

IT MAY BE DIFFICULT TO EFFECT SERVICE OF PROCESS AND ENFORCEMENT OF LEGAL JUDGMENTS UPON US AND OUR SOLE OFFICER AND DIRECTOR BECAUSE SHE RESIDES OUTSIDE THE UNITED STATES.

As our directors and officers reside in Hong Kong and PRC, service of process upon us and such director and officer may be difficult to effect within the United States.

WE HAVE NO PLAN TO DECLARE ANY DIVIDENDS TO SHAREHOLDERS IN THE NEAR FUTURE.

We currently intend to retain our future earnings, if any, to support our operations and to finance expansion. The declaration, and amount of any future dividends will be made at the discretion of the board of directors, and will depend upon, among other things, the results of our operations, cash flows and financial condition, operating and capital requirements, and other factors as the board of directors considers relevant. There is no assurance that future dividends will be paid, and, if dividends are paid, there is no assurance with respect to the amount of any such dividend.

“PENNY STOCK” RULES MAY MAKE BUYING OR SELLING OUR COMMON STOCK DIFFICULT.

Trading in our securities will be subject to the “penny stock” rules. The SEC has adopted regulations that generally define a penny stock to be any equity security that has a market price of less than $5.00 per share, subject to certain exceptions. These rules require that any broker-dealer who recommends our securities to persons other than prior customers and accredited investors, must, prior to the sale, make a special written suitability determination for the purchaser and receive the purchaser’s written agreement to execute the transaction. Unless an exception is available, the regulations require the delivery, prior to any transaction involving a penny stock, of a disclosure schedule explaining the penny stock market and the risks associated with trading in the penny stock market. In addition, broker-dealers must disclose commissions payable to both the broker-dealer and the registered representative and current quotations for the securities they offer. The additional burdens imposed upon broker- dealers by such requirements may discourage broker-dealers from effecting transactions in our securities, which could severely limit the market price and liquidity of our securities. Broker-dealers who sell penny stocks to certain types of investors are required to comply with the Commission’s regulations concerning the transfer of penny stocks. These regulations require broker- dealers to:

|

● |

Make a suitability determination prior to selling a penny stock to the purchaser; |

|

● |

Receive the purchaser’s written consent to the transaction; and |

|

● |

Provide certain written disclosures to the purchaser. |

These requirements may restrict the ability of broker-dealers to sell our common stock and may affect your ability to resell our common stock.

LIMITED OPERATIONS MAKE POTENTIAL DIFFICULT TO ASSESS

We have limited financial resources and no operating activities. We will, in all likelihood, continue to sustain operating expenses without corresponding revenues, at least until the consummation of a business combination. Accordingly, we will most likely incur a net operating loss which will increase continuously until we can consummate a business combination with a target company. There is no assurance that we can identify such a target company and consummate such a business combination.

THERE ARE NO MINIMUM REQUIREMENTS FOR A BUSINESS COMBINATION

There can be no assurance that we will be successful in identifying and evaluating suitable business opportunities or in concluding a business combination. No particular industry or specific business within an industry has been selected for a target company. We have not established a specific length of operating history or a specified level of earnings, assets, net worth or other criteria which it will require a target company to have achieved, or without which we would not consider a business combination with such business entity. Accordingly, we may enter into a business combination with a business entity having no significant operating history, losses, limited or no potential for immediate earnings, limited assets, negative net worth or other negative characteristics. There is no assurance that we will be able to negotiate a business combination on terms favorable to us and our shareholders.

NO ASSURANCE OF SUCCESS OR PROFITABILITY

There is no assurance that we will find a favorable business opportunity. Even if we should become involved in a business opportunity, there is no assurance that it will generate revenues or profits, or that the market price of our outstanding shares will be increased thereby.

TYPE OF BUSINESS ACQUIRED

The business to be acquired may wish to avoid effecting its own public offering and the accompanying expense, delays, and uncertainties. Because of the Company’s limited capital, it is more likely than not that any acquisition by the Company will involve other parties whose primary interest is the acquisition of control of a publicly traded company. Moreover, any business target to be acquired may be currently unprofitable or present other negative factors.

LACK OF DIVERSIFICATION

Because of the limited financial resources that the Company has, it is unlikely that the Company will be able to diversify its acquisitions or operations. The Company’s probable inability to diversify its activities into more than one area will subject the Company to economic fluctuations within a particular business or industry and therefore increase the risks associated with the Company’s operations.

CONFLICTS OF INTEREST

The Company’s officers and directors have other business interests to which he/she currently devotes attention, and is expected to continue to do so. As a result, conflicts of interest may arise that can be resolved only through the exercise of judgment in a manner which is consistent with his/her fiduciary duties to the Company.

It is anticipated that the Company’s principal stockholders may actively negotiate or otherwise consent to the purchase of a portion of their common stock as a condition to, or in connection with, a proposed merger or acquisition transaction. In this process, the Company’s principal stockholders may consider their own personal pecuniary benefit rather than the best interest of other Company stockholders. Depending upon the nature of a proposed transaction, Company stockholders other than the principal stockholders may not be afforded the opportunity to approve or consent to a particular transaction.

NEED FOR ADDITIONAL FINANCING

We have very limited working capital funds, and such funds, may not be adequate to take advantage of any available business opportunities. Even if the Company’s currently available funds prove to be sufficient to pay for its operations until it is able to acquire an interest in, or complete a transaction with, a business opportunity, such funds will clearly not be sufficient to enable it to exploit the opportunity. Thus, the ultimate success of the Company will depend, in part, upon its availability to raise additional capital. In the event that the Company requires modest amounts of additional capital to fund its operations until it is able to complete a business acquisition or transaction, such funds, are expected to be provided by the principal stockholders. The Company has not investigated the availability, source, or terms that might govern the acquisition of the additional capital which is expected to be required in order to exploit a business opportunity, and will not do so until it has determined the level of need for such additional financing. There is no assurance that additional capital will be available from any source or, if available, that it can be obtained on terms acceptable to the Company. If not available, the Company’s operations will be limited to those that can be financed with its modest capital.

DEPENDENCE UPON OUTSIDE ADVISORS

To supplement the business experience of its officers and directors, the Company may be required to employ accountants, technical experts, appraisers, attorneys, or other consultants or advisors. The selection of any such advisors will be made by the Company’s officer, without any input by stockholders. Furthermore, it is anticipated that such persons may be engaged on an as-needed basis without a continuing fiduciary or other obligation to the Company. In the event the officer of the Company considers it necessary to hire outside advisors, he may elect to hire persons who are affiliates, if those affiliates are able to provide the required services.

THERE MAY BE A SCARCITY OF AND/OR SIGNIFICANT COMPETITION FOR BUSINESS OPPORTUNITES AND COMBINATIONS

The Company is and will continue to be an insignificant participant in the business of seeking mergers with and acquisitions of business entities. A large number of established and well-financed entities, including venture capital firms, are active in mergers and acquisitions of companies which may be merger or acquisition target candidates for the Company. Nearly all such entities have significantly greater financial resources, technical expertise and managerial capabilities than the Company and, consequently, the Company will be at a competitive disadvantage in identifying possible business opportunities and successfully completing a business combination. Moreover, the Company will also compete in seeking merger or acquisition candidates with other public shell companies, some of which may also have funds available for use by an acquisition candidate.

REPORTING REQUIREMENTS MAY DELAY OR PRECLUDE ACQUISITION

Pursuant to the requirements of Section 13 of the Exchange Act, the Company is required to provide certain information about significant acquisitions including audited financial statements of the acquired company. Obtaining audited financial statements are the economic responsibility of the target company. The additional time and costs that may be incurred by some potential target companies to prepare such financial statements may significantly delay or essentially preclude consummation of an otherwise desirable acquisition by the Company. Acquisition prospects that do not have or are unable to obtain the required audited statements may not be appropriate for acquisition so long as the reporting requirements of the Exchange Act are applicable. Notwithstanding a target company’s agreement to obtain audited financial statements within the required time frame, such audited financials may not be available to the Company at the time of effecting a business combination. In cases where audited financials are unavailable, the Company will have to rely upon unaudited information that has not been verified by outside auditors in making its decision to engage in a transaction with the business entity. This risk increases the prospect that a business combination with such a business entity might prove to be an unfavorable one for the Company.

LACK OF MARKET RESEARCH OR MARKETING ORGANIZATION

The Company has neither conducted, nor have others made available to it, market research indicating that demand exists for the transactions contemplated by the Company. In the event demand exists for a transaction of the type contemplated by the Company, there is no assurance the Company will be successful in completing any such business combination.

PROBABLE CHANGE IN CONTROL OF THE COMPANY AND/OR MANAGEMENT

In conjunction with completion of a business acquisition, it is anticipated that the Company will issue an amount of the Company’s authorized but unissued common stock that represents the greater majority of the voting power and equity of the Company, which will, in all likelihood, result in stockholders of a target company obtaining a controlling interest in the Company. The resulting change in control of the Company will likely result in removal of the present officers and director of the Company and a corresponding reduction in or elimination of her participation in the future affairs of the Company.

POSSIBLE DILUTION OF VALUE OF SHARES UPON BUSINESS COMBINATION

A business combination normally will involve the issuance of a significant number of additional shares. Depending upon the value of the assets acquired in such business combination, the per-share value of the Company’s common stock may increase or decrease, perhaps significantly.

ADDITIONAL RISKS—DOING BUSINESS IN A FOREIGN COUNTRY

The Company may effectuate a business combination with a merger target whose business operations or even headquarters, place of formation or primary place of business are located outside the United States of America. In such event, the Company may face the significant additional risks associated with doing business in that country. In addition to the language barriers, different presentations of financial information, different business practices, and other cultural differences and barriers that may make it difficult to evaluate such a merger target, ongoing business risks result from the international political situation, uncertain legal systems and applications of law, prejudice against foreigners, corrupt practices, uncertain economic policies and potential political and economic instability that may be exacerbated in various foreign countries.

TAXATION

Federal and state tax consequences will, in all likelihood, be major considerations in any business combination that the Company may undertake. Currently, such transactions typically may be structured so as to result in tax-free treatment to both companies, pursuant to various federal and state tax provisions. The Company intends to structure any business combination so as to minimize the federal and state tax consequences to both the Company and the target entity; however, there can be no assurance that such business combination will meet the statutory requirements of a tax-free reorganization or that the parties will obtain the intended tax-free treatment upon a transfer of stock or assets. A non-qualifying reorganization could result in the imposition of both federal and state taxes, which may have an adverse effect on both parties to the transaction.

Item 1B. Unresolved Staff Comments.

Not applicable.

Item 2. Properties

We presently maintain our mailing address at 5/F, Guangdong Finance Building, 88 Connaught Road West, Hong Kong. Other than this mailing address, we do not currently maintain any other office facilities, and do not anticipate the need for maintaining office facilities at any time in the foreseeable future. We pay no rent or other fees for the use of the mailing address as these offices are used virtually full-time by other businesses of the Company’s officers and directors.

It is likely that the Company will not establish an office until it has completed a business acquisition transaction, but it is not possible to predict what arrangements will actually be made with respect to future office facilities.

ITEM 3. LEGAL PROCEEDINGS.

The Company is not a party to any pending legal proceedings, and no such proceedings are known to be contemplated.

Item 4. Mine Safety Disclosures.

Not applicable.

PART II

Item 5. Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities.

Market for Common Equity and Related Stockholder Matters

Our common stock is currently quoted on a limited basis on the OTC Pink Limited Information tier of OTC Markets Group inter-dealer quotation and trading system under the symbol “UOLI.” The quotation of our common stock on the OTC Pink does not assure that a meaningful, consistent and liquid trading market currently exists. We cannot predict whether a more active market for our common stock will develop in the future. In the absence of an active trading market:

|

(1) |

Investors may have difficulty buying and selling or obtaining market quotation; |

|

(2) |

Market visibility for our common stock may be limited; and |

|

(3) |

A lack of visibility of our common stock may have a depressive effect on the market price for our common stock. |

The following table sets forth the range of bid prices of our common stock during the periods indicated. The prices reported represent prices between dealers, do not include markups, markdowns or commissions and do not necessarily represent actual transactions.

|

High |

Low |

||||||||

|

2012 |

First Quarter |

$ | 0.31 | $ | 0.27 | ||||

|

Second Quarter |

$ | 0.34 | $ | 0.31 | |||||

|

Third Quarter |

$ | 0.606 | $ | 0.34 | |||||

|

Fourth Quarter |

$ | 0.34 | $ | 0.34 | |||||

|

2011 |

First Quarter |

$ | 0.80 | $ | 0.16 | ||||

|

Second Quarter |

$ | 0.55 | $ | 0.55 | |||||

|

Third Quarter |

$ | 0.55 | $ | 0.37 | |||||

|

Fourth Quarter |

$ | 0.56 | $ | 0.32 | |||||

Our common shares are issued in registered form. Interwest Transfer Co., Inc., 1981 East 4800 South, Ste 100, Salt Lake City, UT 84111, Tel: (801) 272-9294, is the registrar and transfer agent for our common stock.

From January 1 to November 20, 2014, the highest and lowest prices of our common shares were $0.50 per share and $0.12 per share. On November 18, 2014, the closing price of our common stock was $0.12 per share.

As of November 20, 2014, there were 91 shareholders of record of 1,996,355 outstanding shares of common stock of the Company, not including approximately 5,000 holders of our shares in street name. Within the holders of record of our common stock are depositories such as Cede & Co. that hold shares of stock for brokerage firms, which, in turn, hold shares of stock for beneficial owners.

Dividends

We have not previously paid any cash dividends on our common stock and do not anticipate paying dividends on our common stock in the foreseeable future. It is the present intention of management to retain any earnings to provide funds for the operation and expansion of our business. Any future determination to pay dividends will be at the discretion of our board of directors and will depend on our results of operation, financial condition, contractual and legal restrictions and other factors the board of directors deem relevant.

Securities Authorized for Issuance under Equity Compensation Plans

As of December 31, 2012, we did not have any equity compensation plans.

Recent Sales of Unregistered Securities

We have not recorded any sales of unregistered securities during the reporting period.

Repurchase of Equity Securities by Issuer and Affiliated Purchasers

We have not repurchased any of our common stock and have no publicly announced repurchase plans or programs as of December 31, 2012.

Item 6. Selected Financial Data.

Not applicable.

Item 7. Management's Discussion and Analysis of Financial Condition and Results of Operations.

PRELIMINARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

This discussion contains forward-looking statements. The reader should understand that several factors govern whether any forward-looking statement contained herein will be or can be achieved. Any one of those factors could cause actual results to differ materially from those projected herein. These forward-looking statements include plans and objectives of management for future operations, including plans and objectives relating to the products and the future economic performance of the Company. Assumptions relating to the foregoing involve judgments with respect to, among other things, future economic, competitive and market conditions, future business decisions, and the time and money required to successfully complete development projects, all of which are difficult or impossible to predict accurately and many of which are beyond the control of the Company. Although the Company believes that the assumptions underlying the forward-looking statements contained herein are reasonable, any of those assumptions could prove inaccurate and, therefore, there can be no assurance that the results contemplated in any of the forward-looking statements contained herein will be realized. Based on actual experience and business development, the Company may alter its marketing, capital expenditure plans or other budgets, which may in turn affect the Company's results of operations. In light of the significant uncertainties inherent in the forward-looking statements included therein, the inclusion of any such statement should not be regarded as a representation by the Company or any other person that the objectives or plans of the Company will be achieved.

OVERVIEW

The predecessor of Uonlive Corporation was incorporated in the State of Nevada on January 29, 1998 under the name Txon International Development Corporation to conduct any lawful business, to exercise any lawful purpose and power, and to engage in any lawful act or activity for which corporations may be organized under the General Corporation Laws of Nevada. On August 1, 2008, the Company changed its name to Uonlive Corporation.

On March 28, 2008, the Company entered into the Exchange Agreement with Tsang William, Uonlive Limited, Tsun Samuel, Hui Chi Kit and Parure Capital Limited. Upon closing of the Share Exchange on March 31, 2008, Tsun and Hui delivered all of their share capital in Parure Capital to the Company in exchange for 150,000,000 shares of common stock of the Company and 500,000 shares of Series A Convertible Preferred Stock, resulting in Parure Capital becoming a wholly owned subsidiary of the Company and Uonlive becoming an indirect wholly owned subsidiary of the Company.

As a result, 495,566 post reverse split shares of the Company’s common stock were outstanding immediately prior to the closing of the Share Exchange, and 1,995,659 shares of the Company’s common stock were outstanding immediately after the closing of the Share Exchange. In addition, 500,000 shares of Series A Convertible Preferred Stock were outstanding immediately after the closing of the Share Exchange. Of these shares, approximately 263,559 shares represented the Company’s “public float” prior to and after the Share Exchange. The 1,500,000 shares of common stock and 500,000 shares of Series A Convertible Preferred Stock issued in the Share Exchange were issued in reliance upon an exemption from registration pursuant to Regulation S under the Securities Act of 1933, as amended (the “Securities Act”). The shares in the public float will continue to represent the shares of the Company’s common stock held for resale without further registration by the holders thereof. After the Share Exchange, Uonlive becomes our operating subsidiary.

On May 19, 2009, we approved a 1:100 reverse stock split (the “Reverse Split”) of our common stock and an amendment to our Articles of Incorporation to effectuate the Reverse Split.

The Company’s main business was operating an online radio station, targeting younger listening audience.

On or about January 2013, the Company made a decision to cease business operation due to insufficient revenue generated from the online radio business. The Company had been losing customers and audience because of higher broadband charges in the area.

Our current business plan is to seek and identify a privately owned company which is looking to become a publicly listed company by combining their operation with us through a reverse merger.

Results of Operations

Revenue

Revenue for the fiscal year ended December 31, 2012 were $0 as compared to $15,415 for the fiscal year ended December 31, 2011. No revenue was reported for the fiscal year ended 2012 due to the Company ceasing operations (as discussed above) and the resulting classification of operations, assets and liabilities associated with the discontinued operations under accounting principles generally accepted in the United States of America (“GAAP”). We anticipate not receiving any revenue for so long as operations have ceased.

Operating Expenses

Operating expenses for the fiscal year ended December 31, 2012 were $175,137 compared to $512,801 for the fiscal year ended December 31, 2011. Operating expenses mainly represented the consulting, legal and audit expenses associated with listing on the OTC Bulletin Board. The decrease was primarily due to the termination of staff and IT services and maintenance. We expect to incur an annual expense of approximately $100,000 for the maintaining the shell company.

Net Loss

We had net loss of $175,137for the fiscal year ended December 31, 2012 as compared to net loss of $539,106 for the fiscal year ended December 31, 2011, primarily due to the decrease in operating expenses as described above.

Comprehensive Loss

Comprehensive loss for the fiscal year ended December 31, 2012 was $182,197 compared to $544,922 for the fiscal year ended December 31, 2011. The decrease in net loss was a result of the decrease in operating expenses.

Liquidity and Capital Resources

During the fiscal year ended December 31, 2012, net cash used in operating activities was $108,075, which included a net loss of $175,137 compared to $517,162 and $539,106 for the same period in 2011, and net-off by depreciation of approximately $12,959, impairment loss on plant and equipment of $11,432 and an increase in accounts payable and accrued liabilities of $42,671. Net cash provided by financing activities accounted for $87,657 and $528,054 for the fiscal year ended December 31, 2012 and 2011 respectively, which was an amount due to a shareholder.

Cash Requirements

As reflected in the accompanying financial statements, the Company has no stabilized source of revenues and needs additional cash resources to maintain its operations. These factors raise substantial doubt about our ability to continue as a going concern. The Company’s ability to continue as a going concern is dependent on its ability to raise additional capital or obtain necessary debt financing. As discussed elsewhere, our current business plan is to seek and identify a privately-held operating company desiring to become a publicly held company by combining with us through a reverse merger or acquisition type transaction. We cannot predict when, if ever, we will be successful in this venture and, accordingly, we may be required to cease and terminate our business plan to seek potential companies willing to merge with us, if we do not have sufficient working capital to pay our operating costs for the next 12 months and we will require additional funds to pay our legal, accounting and other fees associated with our Company and its filing obligations under federal securities laws, as well as to pay our other accounts payable generated in the ordinary course of our business.

We have no commitments from any party to provide such funds to us. If we are unable to obtain additional capital as necessary until such time as we are able to conclude a business combination, we will be unable to satisfy our obligations and otherwise continue to meet our reporting obligations under federal securities laws. In that event, our stock would no longer be quoted on the OTC Bulletin Board and our ability to consummate a reverse merger or acquisition type transaction upon terms and conditions which would be beneficial to our existing stockholders would be adversely affected.

We currently plan to satisfy our cash requirements for the next 12 months by borrowing from our majority shareholders and we believe we can satisfy our cash requirements so long as we are able to obtain financing from these shareholders. We currently expect that money borrowed will be used during the next 12 months to satisfy our operating costs, professional fees and for general corporate purposes. We have also been exploring alternative financing sources.

Based upon a twelve-month work plan, it is anticipated that such a work plan would require approximately $100,000 of financing, designed to fund various commitments and business operations.

We will use our limited personnel and financial resources in connection with seeking new business opportunities. It may be expected that entering into a reverse merger or acquisition type transaction will involve the issuance of a substantial number of restricted shares of common stock. If such additional restricted shares of common stock are issued, our shareholders will experience a dilution in their ownership interest and a change in control may be expected to occur.

In connection with the plan to seek new business opportunities, we may seek to raise funds from the sale of restricted stock or debt securities. We have no agreements to issue any debt or equity securities and cannot predict whether equity or debt financing will become available at acceptable terms, if at all.

There are no limitations in our certificate of incorporation restricting our ability to borrow funds or raise funds through the issuance of restricted common stock to effect a reverse merger or acquisition type transaction. Our limited resources and lack of recent operating history may make it difficult to borrow funds or raise capital.

Such inability to borrow funds or raise funds through the issuance of restricted common stock required to effect or facilitate a reverse merger or acquisition type transaction may have a material adverse effect on our financial condition and future prospects, including the ability to complete a reverse merger or acquisition type transaction. To the extent that debt financing ultimately proves to be available, any borrowing will subject us to various risks traditionally associated with indebtedness, including the risks of interest rate fluctuations and insufficiency of cash flow to pay principal and interest.

Off-Balance Sheet Arrangements

We currently do not have any off-balance sheet arrangements.

Recent Accounting Pronouncements

We continue to assess the effects of recently issued accounting standards. The impact of all recently adopted and issued accounting standards has been disclosed in the Footnotes to the financial statements.

Critical Accounting Policies and Estimates

We are a shell company and, as such, we do not employ critical accounting estimates. Should we resume operations we will employ critical accounting estimates and will make any and all disclosures that are necessary and appropriate.

Item 7A. Quantitative and Qualitative Disclosures About Market Risk.

Not applicable.

Item 8. Financial Statements and Supplementary Data.

UONLIVE CORPORATION

INDEX TO CONSOLIDATED FINANCIAL STATEMENTS

|

Page | |

|

Report of Independent Registered Public Accounting Firm |

F-2 |

|

Consolidated Balance Sheets |

F-3 |

|

Consolidated Statements of Operations And Comprehensive Loss |

F-4 |

|

Consolidated Statements of Cash Flows |

F-5 |

|

Consolidated Statements of Changes in Stockholders’ Deficit |

F-6 |

|

Notes to Consolidated Financial Statements |

F-7 – F-16 |

|

REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

The Board of Directors and Stockholders of

Uonlive Corporation

We have audited the accompanying consolidated balance sheets of Uonlive Corporation and its subsidiaries (“the Company”) as of December 31, 2012 and 2011, the related consolidated statements of operations and comprehensive loss, cash flows and changes in stockholders’ deficit for the years ended December 31, 2012 and 2011. These financial statements are the responsibility of the Company’s management. Our responsibility is to express an opinion on these financial statements based on our audits

We conducted our audits in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audits to obtain reasonable assurance about whether the financial statements are free of material misstatement. The Company is not required to have, nor were we engaged to perform, an audit of its internal control over financial reporting. Our audits included consideration of internal control over financial reporting as a basis for designing audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Company’s internal control over financial reporting. Accordingly, we express no such opinion. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. An audit also includes assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. We believe that our audits provide a reasonable basis for our opinion.

In our opinion, the consolidated financial statements referred to above present fairly, in all material respects, the financial position of the Company as of December 31, 2012 and 2011, and the results of its operations and its cash flows for the years then ended, in conformity with accounting principles generally accepted in the United States of America.

The accompanying consolidated financial statements have been prepared assuming that the Company will continue as a going concern. As discussed in Note 2 to the consolidated financial statements, the Company has incurred continuous losses and capital deficit, all of which raise substantial doubt about its ability to continue as a going concern. These consolidated financial statements do not include any adjustments that might result from the outcome of this uncertainty.

/s/ HKCMCPA Company Limited

HKCMCPA Company Limited

Certified Public Accountants

Hong Kong, China

November 21, 2014

Unit 602, 6/F., Hoseinee House, 69 Wyndham Street, Central, Hong Kong

|

Tel: (852) 2573 2296 |

Fax: (852) 2384 2022 |

http://www.hkcmcpa.us |

UONLIVE CORPORATION

CONSOLIDATED BALANCE SHEETS

AS OF DECEMBER 31, 2012 AND 2011

(Currency expressed in United States Dollars (“US$”), except for number of shares)

|

As of December 31, |

||||||||

|

2012 |

2011 |

|||||||

|

ASSETS |

||||||||

|

Current assets: |

||||||||

|

Cash and cash equivalents |

$ | 1,017 | $ | 21,402 | ||||

|

Non-current assets: |

||||||||

|

Plant and equipment, net |

- | 24,356 | ||||||

|

TOTAL ASSETS |

$ | 1,017 | $ | 45,758 | ||||

|

LIABILITIES AND STOCKHOLDERS’ DEFICIT |

||||||||

|

Current liabilities: |

||||||||

|

Accounts payable and accrued liabilities |

$ | 63,000 | $ | 20,329 | ||||

|

Amount due to a shareholder |

3,111,087 | 3,016,673 | ||||||

|

Total current liabilities |

3,174,087 | 3,037,002 | ||||||

|

Long-term liabilities: |

||||||||

|

Note payable to a shareholder |

167,672 | 167,301 | ||||||

|

Total liabilities |

3,341,759 | 3,204,303 | ||||||

|

Stockholders’ deficit: |

||||||||

|

Series A, Convertible preferred stock, $0.001 par value; 10,000,000 shares authorized, 500,000 shares issued and outstanding, respectively |

500 | 500 | ||||||

|

Common stock, $0.001 par value; 200,000,000 shares authorized; 1,996,355 shares issued and outstanding, respectively |

1,996 | 1,996 | ||||||

|

Additional paid-in capital |

197,570 | 197,570 | ||||||

|

Accumulated deficit |

(3,531,854 | ) | (3,356,717 | ) | ||||

|

Accumulated other comprehensive loss |

(8,954 | ) | (1,894 | ) | ||||

|

Total stockholders’ deficit |

(3,340,742 | ) | (3,158,545 | ) | ||||

|

TOTAL LIABILITIES AND STOCKHOLDERS’ DEFICIT |

$ | 1,017 | $ | 45,758 | ||||

See accompanying notes to consolidated financial statements.

UONLIVE CORPORATION

CONSOLIDATED STATEMENTS OF OPERATIONS AND COMPREHENSIVE LOSS

FOR THE YEARS ENDED DECEMBER 31, 2012 AND 2011

(Currency expressed in United States Dollars (“US$”), except for number of shares)

|

Years ended December 31, |

||||||||

|

2012 |

2011 |

|||||||

|

Revenues, net: |

||||||||

|

- Related party |

$ | - | $ | 15,415 | ||||

|

Cost of revenue (exclusive of depreciation) |

- | (41,720 | ) | |||||

|

Gross loss |

- | (26,305 | ) | |||||

|

Operating expenses: |

||||||||

|

Sales and marketing |

- | 6,147 | ||||||

|

Consulting and professional fee |

33,008 | 32,857 | ||||||

|

General and administrative |

142,129 | 473,797 | ||||||

|

|

||||||||

|

Total operating expenses |

175,137 | 512,801 | ||||||

|

LOSS BEFORE INCOME TAXES |

(175,137 | ) | (539,106 | ) | ||||

|

Income tax expense |

- | - | ||||||

|

NET LOSS |

$ | (175,137 | ) | $ | (539,106 | ) | ||

|

Other comprehensive income: |

||||||||

|

- Foreign currency translation loss |

(7,060 | ) | (5,816 | ) | ||||

|

COMPREHENSIVE LOSS |

$ | (182,197 | ) | $ | (544,922 | ) | ||

|

Net loss per share – Basic and diluted |

$ |

(0.09 |

) | $ | (0.27 | ) | ||

|

Weighted average common shares outstanding – Basic and diluted |

1,996,355 | 1,996,355 | ||||||

See accompanying notes to consolidated financial statements.

UONLIVE CORPORATION

CONSOLIDATED STATEMENTS OF CASH FLOWS

FOR THE YEARS ENDED DECEMBER 31, 2012 AND 2011

(Currency expressed in United States Dollars (“US$”))

|

Years ended December 31, |

||||||||

|

2012 |

2011 |

|||||||

|

Cash flow from operating activities: |

||||||||

|

Net loss |

$ | (175,137 | ) | $ | (539,106 | ) | ||

|

Adjustments to reconcile net loss to net cash used in operating activities: |

||||||||

|

Depreciation of plant and equipment |

12,959 | 14,773 | ||||||

|

Impairment loss on plant and equipment |

11,432 | - | ||||||

|

Changes in operating assets and liabilities: |

||||||||

|

Accounts receivable, related party |

- | 3,854 | ||||||

|

Deposits and other receivables |

- | 3,326 | ||||||

|

Accounts payable and accrued liabilities |

42,671 | (9 | ) | |||||

|

Net cash used in operating activities |

(108,075 | ) | (517,162 | ) | ||||

|

Cash flows from investing activities: |

||||||||

|

Purchase of plant and equipment |

- | (5,894 | ) | |||||

|

Net cash used in investing activities |

- | (5,894 | ) | |||||

|

Cash flows from financing activities: |

||||||||

|

Advances from a shareholder |

87,657 | 528,054 | ||||||

|

Net cash provided by financing activities |

87,657 | 528,054 | ||||||

|

Effect of exchange rate change on cash and cash equivalents |

33 | 37 | ||||||

|

NET CHANGE IN CASH AND CASH EQUIVALENTS |

(20,385 | ) | 5,035 | |||||

|

CASH AND CASH EQUIVALENTS, BEGINNING OF YEAR |

21,402 | 16,367 | ||||||

|

CASH AND CASH EQUIVALENTS, END OF YEAR |

$ | 1,017 | $ | 21,402 | ||||

|

SUPPLEMENTAL DISCLOSURE OF CASH FLOW INFORMATION |

||||||||

|

Cash paid for income taxes |

$ | - | $ | - | ||||

|

Cash paid for interest |

$ | - | $ | - | ||||

See accompanying notes to consolidated financial statements.

UONLIVE CORPORATION

CONSOLIDATED STATEMENTS OF CHANGES IN STOCKHOLDERS’ DEFICIT

FOR THE YEARS ENDED DECEMBER 31, 2012 AND 2011

(Currency expressed in United States Dollars (“US$”), except for number of shares)

|

Series A, Convertible preferred stock |

Common stock |

Additional |

Accumulated other |

Total |

||||||||||||||||||||||||||||

| No. of | No. of | paid | Accumulated | comprehensive | stockholders’ | |||||||||||||||||||||||||||

|

shares |

Amount |

shares |

Amount |

in capital | deficit | (loss) income | deficit | |||||||||||||||||||||||||

|

Balance as of January 1, 2011 |

500,000 | $ | 500 | 1,996,355 | $ | 1,996 | $ | 197,570 | $ | (2,817,611 | ) | $ | 3,922 | $ | (2,613,623 | ) | ||||||||||||||||

|

Net loss for the year |

- | - | - | - | - | (539,106 | ) | - | (539,106 | ) | ||||||||||||||||||||||

|

Foreign currency translation adjustment |

- | - | - | - | - | - | (5,816 | ) | (5,816 | ) | ||||||||||||||||||||||

|

Balance as of December 31, 2011 |

500,000 | $ | 500 | 1,996,355 | $ | 1,996 | $ | 197,570 | $ | (3,356,717 | ) | $ | (1,894 | ) | $ | (3,158,545 | ) | |||||||||||||||

|

Net loss for the year |

- | - | - | - | - | (175,137 | ) | - | (175,137 | ) | ||||||||||||||||||||||

|

Foreign currency translation adjustment |

- | - | - | - | - | - | (7,060 | ) | (7,060 | ) | ||||||||||||||||||||||

|

Balance as of December 31, 2012 |

500,000 | $ | 500 | 1,996,355 | $ | 1,996 | $ | 197,570 | $ | (3,531,854 | ) | $ | (8,954 | ) | $ | (3,340,742 | ) | |||||||||||||||

See accompanying notes to consolidated financial statements.

UONLIVE CORPORATION

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

FOR THE YEARS ENDED DECEMBER 31, 2012 AND 2011

(Currency expressed in United States Dollars (“US$”), except for number of shares)

|

1. |

DESCRIPTION OF BUSINESS AND ORGANIZATION |

Uonlive Corporation (“UOLI” or the “Company”) was incorporated under the laws of the State of Nevada on January 29, 1998 as Weston International Development Corporation. On July 28, 1998, its name was changed to Txon International Development Corporation. On September 15, 2000, the Company changed its name to China World Trade Corporation. On July 2, 2008, the Company further changed its name to Uonlive Corporation.

UOLI, through its subsidiaries, previously engaged in the provision of online multimedia and advertising service and the operation of online radio stations in Hong Kong.

Since 2012, the Company ceased its operation and became a shell company with no or nominal operations. The Company is actively considering various acquisition targets and other business opportunities. The Company hopes to acquire one or more operating businesses or consummate a business opportunity within the next twelve months.

UOLI and its subsidiaries are hereinafter collectively referred to as “the Company”.

|

2. |

GOING CONCERN UNCERTAINTIES |

These consolidated financial statements have been prepared assuming that the Company will continue as a going concern, which contemplates the realization of assets and the discharge of liabilities in the normal course of business for the foreseeable future.

For the year ended December 31, 2012, the Company has incurred a net loss of $175,137 and experienced negative operating cash flows of $108,075 with an accumulated deficit of $3,531,854 as of that date. The continuation of the Company is dependent upon the continuing financial support of its shareholders. Management believes this funding will continue, and is also actively seeking new investors. Management believes the existing stockholders will provide the additional cash to meet the Company’s obligations as they become due. However, there is no assurance that the Company will be successful in securing sufficient funds to sustain the operations.

These and other factors raise substantial doubt about the Company’s ability to continue as a going concern. These consolidated financial statements do not include any adjustments to reflect the possible future effects on the recoverability and classification of assets or the amounts and classification of liabilities that may result in the Company not being able to continue as a going concern.

|

3. |

SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES |

|

● |

Basis of presentation |

These accompanying consolidated financial statements have been prepared in accordance with generally accepted accounting principles in the United States of America.

|

● |

Shell company |

The Company has ceased all of its business and is currently considered as a shell company.

UONLIVE CORPORATION

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

FOR THE YEARS ENDED DECEMBER 31, 2012 AND 2011

(Currency expressed in United States Dollars (“US$”), except for number of shares)

|

● |

Use of estimates |

In preparing these consolidated financial statements, management makes estimates and assumptions that affect the reported amounts of assets and liabilities in the balance sheets and revenues and expenses during the years reported. Actual results may differ from these estimates.

|

● |

Basis of consolidation |

The consolidated financial statements include the accounts of UOLI and its subsidiaries. All significant inter-company balances and transactions within the Company have been eliminated upon consolidation.

|

● |

Cash and cash equivalents |

Cash and cash equivalents are carried at cost and represent cash on hand, demand deposits placed with banks or other financial institutions and all highly liquid investments with an original maturity of three months or less as of the purchase date of such investments.

|

● |

Accounts receivable |

Accounts receivable consist primarily of trade receivables. Accounts receivable are recognized and carried at original invoiced amount less an allowance for any uncollectible accounts. Management reviews and adjusts this allowance periodically based on historical experience, current economic climate as well as its evaluation of the collectibility of outstanding accounts. The Company evaluates the credit risks of its customers utilizing historical data and estimates of future performance. For the years ended December 31, 2012 and 2011, the Company did not provide an allowance for doubtful accounts, nor have been any write-offs.

|

● |

Plant and equipment |

Plant and equipment are stated at cost less accumulated depreciation and accumulated impairment losses, if any. Depreciation is calculated on the straight-line basis over the following expected useful lives from the date on which they become fully operational:

|

Expected useful life | ||

|

Furniture, fittings and office equipment |

5 years | |

|

Computer and broadcasting equipment |

5 years |

Expenditure for maintenance and repairs is expensed as incurred. The gain or loss on the disposal of plant and equipment is the difference between the net sales proceeds and the carrying amount of the relevant assets and is recognized in the statement of operations.

|

● |

Impairment of long-lived assets |

Long-lived assets primarily include plant and equipment. In accordance with the Financial Accounting Standards Board (“FASB”) Accounting Standards Codification (“ASC”) Topic 360-10-5, “Impairment or Disposal of Long-Lived Assets”, the Company reviews its long-lived assets for impairment whenever events or changes in business circumstances indicate that the carrying amount of the assets may not be fully recoverable or that the useful lives are no longer appropriate. If the total of the expected undiscounted future net cash flows is less than the carrying amount of the asset, a loss is recognized for the difference between the fair value and carrying amount of the asset.

|

● |

Revenue recognition |

The Company derives revenues from the sale of advertising airtime to customers. Revenue is recognized when the following four revenue criteria are met: persuasive evidence of an arrangement exists, delivery has occurred, the selling price is fixed or determinable, and collectibility is reasonably assured, as defined by ASC Topic 605, “Revenue Recognition”. No revenue was generated in the year ended December 31, 2012.

UONLIVE CORPORATION

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

FOR THE YEARS ENDED DECEMBER 31, 2012 AND 2011

(Currency expressed in United States Dollars (“US$”), except for number of shares)

|

● |

Cost of revenue |

Cost of revenue included IT service cost for maintenance and operating the online radio domain and rent charge of radio studio in Hong Kong. No cost of revenue was generated in the year ended December 31, 2012.

|

● |

Income taxes |

Income taxes are determined in accordance with the provisions of ASC Topic 740, “Income Taxes” (“ASC 740”). Under this method, deferred tax assets and liabilities are recognized for the future tax consequences attributable to differences between the financial statement carrying amounts of existing assets and liabilities and their respective tax basis. Deferred tax assets and liabilities are measured using enacted income tax rates expected to apply to taxable income in the years in which those temporary differences are expected to be recovered or settled. Any effect on deferred tax assets and liabilities of a change in tax rates is recognized in income in the period that includes the enactment date.

ASC 740 prescribes a comprehensive model for how companies should recognize, measure, present, and disclose in their financial statements uncertain tax positions taken or expected to be taken on a tax return. Under ASC 740, tax positions must initially be recognized in the financial statements when it is more likely than not the position will be sustained upon examination by the tax authorities. Such tax positions must initially and subsequently be measured as the largest amount of tax benefit that has a greater than 50% likelihood of being realized upon ultimate settlement with the tax authority assuming full knowledge of the position and relevant facts.

For the years ended December 31, 2012 and 2011, the Company did not have any interest and penalties associated with tax positions. As of December 31, 2012, the Company did not have any significant unrecognized uncertain tax positions.

The Company is subject to Hong Kong tax jurisdiction. The Company files tax returns that are subject to examination by the foreign tax authority. For the year ended December 31, 2012, the Company filed and cleared a 2011 tax return with its local tax authority.

|

● |

Net loss per share |

The Company calculates net loss per share in accordance with ASC Topic 260, “Earnings per Share.” Basic net loss per share is computed by dividing net loss by the weighted-average number of common share outstanding during the period. Diluted net loss per share is computed similar to basic net loss per share except that the denominator is increased to include the number of additional common share that would have been outstanding if the potential common share equivalents had been issued and if the additional common shares were dilutive.

|

● |

Comprehensive income or loss |

ASC Topic 220, “Comprehensive Income” establishes standards for reporting and display of comprehensive income or loss, its components and accumulated balances. Comprehensive income as defined includes all changes in equity during a period from non-owner sources. Accumulated comprehensive income or loss consists of changes in unrealized gains and losses on foreign currency translation. This comprehensive income or loss is not included in the computation of income tax expense or benefit.

UONLIVE CORPORATION

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

FOR THE YEARS ENDED DECEMBER 31, 2012 AND 2011

(Currency expressed in United States Dollars (“US$”), except for number of shares)

|

● |

Foreign currencies translation |

Transactions denominated in currencies other than the functional currency are translated into the functional currency at the exchange rates prevailing at the dates of the transaction. Monetary assets and liabilities denominated in currencies other than the functional currency are translated into the functional currency using the applicable exchange rates at the balance sheet dates. The resulting exchange differences are recorded in the consolidated statement of operations.

The reporting currency of the Company is the United States Dollars ("US$") and the accompanying consolidated financial statements have been expressed in US$. In addition, the Company’s subsidiary in Hong Kong maintain its books and record in its local currency, Hong Kong Dollars ("HK$"), which is its functional currency and the primary currency of the economic environment in which their operations are conducted.

In general, for consolidation purposes, assets and liabilities of its subsidiaries whose functional currency is not US$ are translated into US$, in accordance with ASC Topic 830-30, “Translation of Financial Statement”, using the exchange rate on the balance sheet date. Revenues and expenses are translated at average rates prevailing during the period. The gains and losses resulting from translation of financial statements of foreign subsidiaries are recorded as a separate component of accumulated other comprehensive income within the statements of changes in stockholders’ deficit.

Translation of amounts from HK$ into US$1 has been made at the following exchange rates for the respective year:

|

2012 |

2011 |

|||||||

|

Year-end HK$:US$1 exchange rate |

7.7519 | 7.7691 | ||||||

|

Annual average HK$:US$1 exchange rate |

7.7575 | 7.7851 | ||||||

|

● |

Segment reporting |

ASC Topic 280, “Segment Reporting” establishes standards for reporting information about operating segments on a basis consistent with the Company’s internal organization structure as well as information about geographical areas, business segments and major customers in financial statements. For the years ended December 31, 2012 and 2011, the Company operates in one reportable segment in Hong Kong.

|

● |

Related parties |

For the purposes of these financial statements, parties are considered to be related if one party has the ability, directly or indirectly, to control the party or exercise significant influence over the party in making financial and operating decisions, or vice versa, or where the Company and the party are subject to common control or common significant influence. Related parties may be individuals or other entities.

|

● |

Fair value of financial instruments |

The carrying value of the Company’s financial instruments: cash and cash equivalents, accounts receivable, deposits and other receivables, accounts payable and accrued liabilities and amount due to a shareholder approximate at their fair values because of the short-term nature of these financial instruments.

The Company also follows the guidance of the ASC Topic 820-10, “Fair Value Measurements and Disclosures” ("ASC 820-10"), with respect to financial assets and liabilities that are measured at fair value. ASC 820-10 establishes a three-tier fair value hierarchy that prioritizes the inputs used in measuring fair value as follows:

|

Level 1 : Inputs are based upon unadjusted quoted prices for identical instruments traded in active markets; |

UONLIVE CORPORATION

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

FOR THE YEARS ENDED DECEMBER 31, 2012 AND 2011

(Currency expressed in United States Dollars (“US$”), except for number of shares)

|

Level 2 : Inputs, other than the quoted prices in active markets, that are observable either directly or indirectly; and; and |

|

Level 3 : Inputs are generally unobservable and typically reflect management’s estimates of assumptions that market participants would use in pricing the asset or liability. The fair values are therefore determined using model-based techniques, including option pricing models and discounted cash flow models. |

Fair value estimates are made at a specific point in time based on relevant market information about the financial instrument. These estimates are subjective in nature and involve uncertainties and matters of significant judgment and, therefore, cannot be determined with precision. Changes in assumptions could significantly affect the estimates.

|

● |

Recent accounting pronouncements |

The Company has reviewed all recently issued, but not yet effective, accounting pronouncements and does not believe the future adoption of any such pronouncements may be expected to cause a material impact on its financial condition or the results of its operations, as follows:

In June 2011, the Financial Accounting Standards Board (“FASB”) issued ASU No. 2011-05, “ Comprehensive Income (Topic 220): Presentation of Comprehensive Income ” (“ASU 2011-05”). ASU 2011-05 eliminates the option to report other comprehensive income and its components in the statement of changes in equity. ASU 2011-05 requires that all non-owner changes in stockholders’ equity be presented in either a single continuous statement of comprehensive income or in two separate but consecutive statements. This new guidance is to be applied retrospectively. The Company adopted this ASU by presenting the comparative components of comprehensive income within our consolidated financial statements of operation and comprehensive income.

In September 2011, the FASB issued ASU No. 2011-08, “Intangibles - Goodwill and Other (Topic 350): Testing Goodwill for Impairment”(“ASU 2011-08”). This ASU is intended to simplify how entities test goodwill for impairment and permits an entity to first assess qualitative factors to determine whether it is “more likely than not” that the fair value of a reporting unit is less than its carrying amount as a basis for determining whether it is necessary to perform the two-step goodwill impairment test described in Topic 350. ASU 2011-08 is effective for annual and interim goodwill impairment tests performed for fiscal years beginning after December 15, 2011. The adoption of these changes had no impact on the Company’s consolidated financial statements.