U.S. SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

(Mark One)

For the year ended

For the transition period from ____ to____

Commission File Number:

(Formerly Uonlive Corp.)

(Exact name of registrant as specified in its charter)

| (State of Incorporation ) | (IRS Employer Identification No.) |

(Address of registrant’s principal executive offices)

Registrant’s telephone number, including

area code: +

Securities registered under Section 12(b) of the Act: None

Securities registered under Section 12(g) of the Act:

| Title of each class | Ticker Symbol |

Indicate by check mark if the registrant is a

well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨

Indicate by check mark if the registrant is not

required to file reports pursuant to Section 13 or Section 15(d) of the Act Yes ¨

Indicate by check mark whether the registrant

(1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding

12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such

filing requirements for the past 90 days.

Indicate by check mark whether the registrant

has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405

of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer | ¨ | x | |

| Accelerated filer | ¨ | Smaller reporting company | |

| Emerging growth company |

If an emerging growth company, indicate by check

mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting

standards provided pursuant to Section 13(a) of the Exchange Act.

Indicate by check mark whether the registrant

has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial

reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or

issued its audit report.

Indicate by check mark whether the registrant

is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨

As of June 30, 2022 (last business day of the

registrant’s most recently completed second fiscal quarter ), based upon the last reported trade on that date ($5.00 ),

the aggregate market value of the voting and non-voting common equity held by non-affiliates (for this purpose, all outstanding and issued

common stock minus stock held by the officers, directors and known holders of 10% or more of the Company’s common stock) was $

As of April 11, 2023, the registrant had shares of the issuer’s common stock, $0.001 par value outstanding.

EXPLANATORY NOTE

As used in this Annual Report, the terms “we,” “us,” “our,” and words of like import, and the “Company” refer to Kuber Resources Corporation and all of our subsidiaries unless the context otherwise indicates or the context otherwise requires.

FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K contains certain forward-looking statements (as such term is defined in Section 27A of the Securities Act of 1933, as amended (the “Securities Act”) and Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”)). The statements herein, which are not historical facts, reflect our current expectations and projections about the Company’s future results, performance, liquidity, financial condition, prospects and opportunities and are based upon information currently available to us and our management and our interpretation of what we believe to be significant factors affecting our business, including many assumptions about future events. Such forward-looking statements include statements regarding, among other things:

| ● | our ability to deliver, market and generate sales of our import services; |

| ● | our ability to develop and/or introduce new import services; |

| ● | our projected revenues, profitability and other financial metrics; |

| ● | our future financing plans; |

| ● | our anticipated needs for working capital; |

| ● | the anticipated trends in our industry; |

| ● | our ability to expand our sales and marketing capability; |

| ● | acquisitions of other companies or assets that we might undertake in the future; |

| ● | competition existing today or that will likely arise in the future; and |

| ● | other factors discussed elsewhere herein. |

Forward-looking statements, which involve assumptions and describe our plans, strategies, and expectations, are generally identifiable by use of the words “may,” “should,” “will,” “plan,” “could,” “target,” “contemplate,” “predict,” “potential,” “continue,” “expect,” “anticipate,” “estimate,” “believe,” “intend,” “seek,” or “project” or the negative of these words or other variations on these or similar words. Actual results, performance, liquidity, financial condition and results of operations, prospects and opportunities could differ materially from those expressed in, or implied by, these forward-looking statements because of various risks, uncertainties and other factors, including the ability to raise sufficient capital to continue the Company’s operations. These statements may be found under Part II, Item 7 “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” as well as elsewhere in this Annual Report on Form 10-K generally. Actual events or results may differ materially from those discussed in forward-looking statements as a result of various factors, including, without limitation, matters described in this Annual Report on Form 10-K.

In light of these risks and uncertainties, there can be no assurance that the forward-looking statements contained in this Annual Report on Form 10-K will in fact occur.

Potential investors should not place undue reliance on any forward-looking statements. Except as expressly required by the federal securities laws, there is no undertaking to publicly update or revise any forward-looking statements, whether as a result of new information, future events, changed circumstances or any other reason. Potential investors should not make an investment decision based solely on our projections, estimates or expectations.

The forward-looking statements in this Annual Report on Form 10-K represent our views as of the date of this Annual Report on Form 10-K. Such statements are presented only as some guide about future possibilities and do not represent assured events, and we anticipate that subsequent events and developments will cause our views to change. You should, therefore, not rely on these forward-looking statements as representing our views as of any date after the date of this Annual Report on Form 10-K.

This Annual Report on Form 10-K also contains estimates and other statistical data prepared by independent parties and by us relating to market size and growth and other data about our industry. These estimates and data involve a number of assumptions and limitations, and potential investors are cautioned not to give undue weight to these estimates and data. We have not independently verified the statistical and other industry data generated by independent parties and contained in this Annual Report on Form 10-K. In addition, projections, assumptions and estimates of our future performance and the future performance of the industries in which we operate are necessarily subject to a high degree of uncertainty and risk.

Except as required by law, we assume no obligation to update any forward-looking statements publicly, or to update the reasons actual results differing materially from those anticipated based on any forward-looking statements, even if new information becomes available in the future. Depending on the market for our stock and other conditional tests, a specific safe harbor under the Private Securities Litigation Reform Act of 1995 may be available to us. Notwithstanding the above, because Section 27A of the Securities Act and Section 21E of the Exchange Act expressly state that the safe harbor for forward-looking statements does not apply to companies that issue penny stock, the safe harbor for forward-looking statements may not be available to us at certain times as we may be considered to be an issuer of penny stock.

| 2 |

TABLE OF CONTENTS

| Item 1. | Business | 4 |

| Item 1A. | Risk Factors | 10 |

| Item 1B. | Unresolved Staff Comments | 10 |

| Item 2. | Properties | 10 |

| Item 3. | Legal Proceedings | 10 |

| Item 4. | Mine Safety Disclosures | 10 |

| Item 5. | Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities | 11 |

| Item 6. | Selected Financial Data | 14 |

| Item 7. | Management’s Discussion and Analysis of Financial Condition and Results of Operations | 14 |

| Item 7A. | Quantitative and Qualitative Disclosures About Market Risk | 15 |

| Item 8. | Financial Statements and Supplementary Data | 15 |

| Item 9. | Changes in and Disagreements With Accountants on Accounting and Financial Disclosure | 16 |

| Item 9A. | Controls and Procedures | 16 |

| Item 9B. | Other Information | 16 |

| Item 10. | Directors, Executive Officers and Corporate Governance | 17 |

| Item 11. | Executive Compensation | 19 |

| Item 12. | Security Ownership of Certain Beneficial Owners and Management and Related Stockholders Matters | 20 |

| Item 13. | Certain Relationships and Related transactions, and Director Independence | 22 |

| Item 14. | Principal Accounting Fees and Services | 23 |

| Item 15. | Exhibits, Financial Statement Schedules | 24 |

| Item 16. | Form 10-K Summary | 26 |

| 3 |

PART I

ITEM 1. BUSINESS

History of Our Company

We were incorporated in the State of Nevada on January 29, 1998 under the name Weston International Development Corporation to conduct any lawful business, to exercise any lawful purpose and power, and to engage in any lawful act or activity for which corporations may be organized under the General Corporation Laws of Nevada. On July 28, 1998, its name was changed to Txon International Development Corporation.

On August 14, 2000, pursuant to a share exchange agreement dated August 10, 2000, by and among Main Edge International Limited (“Main Edge”), Virtual Edge Limited (“Virtual Edge”), Richard Ford, Jeanie Hildebrand and Gary Lewis, we acquired from Main Edge all of the shares of Virtual Edge (the “Acquisition”) in exchange for an aggregate of 1,961,175 shares of our common stock, which shares equaled 75.16% of Txon International’s issued and outstanding shares after giving effect to the Acquisition. On September 15, 2000, Txon International Development Corporation changed its name to China World Trade Corporation (“CWTD”).

On March 28, 2008, CWTD entered into a Share Exchange Agreement (the “Exchange Agreement”) by and among CWTD, William Tsang (“Tsang”), Uonlive Limited, a corporation organized and existing under the laws of the Hong Kong SAR of the People’s Republic of China (“Uonlive”), Tsun Sin Man Samuel, Chairman of Uonlive (“Tsun”), Hui Chi Kit, Chief Financial Officer of Uonlive (“Hui”), Parure Capital Limited, a corporation organized and existing under the laws of the British Virgin Islands and parent of Uonlive (“Parure Capital”). Upon closing of the share exchange transaction contemplated under the Exchange Agreement, Tsun and Hui transferred all of their share capital in Parure Capital to CWTD in exchange for an aggregate of 150,000,000 shares of common stock of the Registrant and 500,000 shares of Series A Convertible Preferred Stock of the Registrant, which is convertible after six months from the date of issuance into 100 shares of common stock of the Registrant, thus causing Parure Capital to become a direct wholly-owned subsidiary of the Registrant.

On July 2, 2008, the proposal to amend the articles of incorporation to change the name of the corporation to Uonlive Corporation was approved by the action of a majority of all shareholders entitled to vote on the record date and by CWTD’s Board of Directors. CWTD desired to change its name to truly reflect its new business as a holding company for Uonlive Limited, and possibly other companies that may be acquired in the future by the company (the “Company” or “Uonlive”).

On May 15, 2009, the Company approved the 1 for 100 reverse split of its common stock.

The Company initially ceased operations in early 2015. The Company has fully impaired all assets since the shutdown of its operations in 2015 and recorded the effects of this impairment as part of its discontinued operations.

On May 2, 2017, Parure Capital was struck off the BVI Register of Companies for non-payment of annual fees. Therefore, Parure Capital was no longer a subsidiary of the Company.

On June 15, 2018, the Eighth Judicial District Court of Nevada appointed Small Cap Compliance, LLC (“Custodian”) as custodian for Uonlive Corporations., proper notice having been given to the officers and directors of Uonlive Corporation. There was no opposition.

On June 20, 2018, the Custodian appointed Rhonda Keaveney as CEO, Secretary, Treasurer and Director of the Company.

On August 7, 2018, the Company filed a certificate of reinstatement with the state of Nevada.

On September 7, 2018, the Company authorized the issuance of 1,000,000 shares of Convertible Series B Preferred Stock. Each one Convertible Series B Preferred Stock was entitled to be converted into 1,000 shares of common stock. Also, each one Convertible Series B Preferred Stock was entitled to 1,000 votes of common stock. 150,000 shares of Convertible Series B Preferred Stock were issued to Chuang Fu Qu Kuai Lian Technology (Shenzhen) Limited giving Chuang Fu Qu Kuai Lian Technology (Shenzhen) Limited the voting control of the Company.

| 4 |

Also on September 7, 2018, Raymond Fu was appointed as President, Chief Executive Officer, Secretary, Treasurer and member of our Board of Directors of the Company and Rhonda Keaveney resigned as Chief Executive Officer, Treasurer, Secretary, and member from the Board of Directors.

On December 6, 2018, the Eighth Judicial District Court of Nevada discharged Small Cap Compliance, LLC as custodian for Uonlive Corporations.

On April 10, 2019, pursuant to an Acquisition Agreement, the Company contracted to acquire 80% of the issued and outstanding capital stock of Truly Organic Limited, a Hong Kong based company (“Truly Organic”), specializing in organic agriculture certification consulting in South East Asia. However, Truly Organic was unable to provide financial statements capable of being audited by a PCAOB independent public accountant, as required in the Acquisition Agreement. Therefore, such acquisition did not close.

On January 13, 2020, Edwin Lun, the existing secretary of the Board of Directors resigned. On January 13, 2020, the Board of Directors accepted his resignation. Also on January 13, 2020, (i) Timothy Chee Yau Lam was appointed and consented to act as the new secretary of the Board of Directors and a member of the Board of Directors of the Company, (ii) Kwok Fai Thomas Yip was appointed and consented to act as a member of the Board of Directors of the Company, and (iii) Chi Wai Michael Woo was appointed and consented to act as a member of the Board of Directors of the Company.

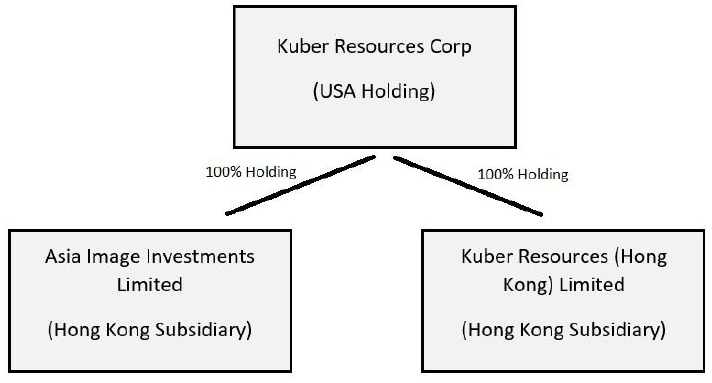

On March 2, 2020, pursuant to a Definitive Share Exchange Agreement, Uonlive Corporation (the “Company”) acquired 100% of the issued and outstanding capital stock of Asia Image Investing Limited (“Asia Image”), a Hong Kong based company, specializing in trade, distribution, and consulting in Hong Kong in the tea industry. The Company issued 100,000 shares of common stock, representing 4.8% of the Company’s outstanding shares of common stock, calculated post-issuance in exchange for the 100% issued and outstanding capital stock of Asia Image Investing Limited.

Corporate Structure

On March 2, 2020, the Company entered into a Definitive Share Agreement whereby Mr. Raymond Fu, the sole shareholder of Asia Image Investment Limited, relinquished all his shares in Asia Image and acquired 100,000 shares of the Company. Consequently, Asia Image became a wholly-owned subsidiary of the Company.

| 5 |

On October 27, 2020, the Company appointed AJSH & Co LLP , (now known as Mercurius & Associates LLP) a PCOAB registered firm as its independent registered accounting firm who performed the Company’s audit for the period ended December 31, 2019 and December 31, 2018.

AJSH & Co LLP, (now known as Mercurius & Associates LLP) also performed the audit for Asia Image Investment Limited for the periods ended December 31 2019, and December 31, 2018.

On November 7, 2022, the Company purchased from GRL21 Nominee Limited all the shares of Kuber Resources (Hong Kong) Limited for one Hong Kong dollar (HKD1.00). Accordingly, Kuber Resources (Hong Kong) Limited became a fully-owned subsidiary of the Company as at November 7, 2022. Kuber Resources (Hong Kong) Limited (previously known as Star Wise Limited) is a company incorporated in Hong Kong on October 21, 2022. It changed its name to Kuber (Resources (Hong Kong) Limited on 1 November 2022 and concurrently filed its notification of commencement of Business by Corporation on the same day. It had not traded and/or otherwise operated until after it had been purchased by the Company on November 7, 2022. The purpose of obtaining Kuber Resources (Hong Kong) Limited is to start an additional line of business outside of the international commodities trade currently undertaken by Asia Image Limited.

On December 8, 2022, Uonlive Corporation (the “Company”) filed Articles of Amendment (the “Articles of Amendment”) to its Articles of Incorporation, as amended, with the Secretary of Nevada to change the Company’s corporate name to Kuber Resources Corporation (the “Name Change”). In connection with the Name Change, the Company’s has changed its ticker symbol from “UOLI” to the new ticker symbol “KUBR” (the “Symbol Change”). There is no change in the CUSIP number of the Company’s common stock in connection with the Name Change and Symbol Change. As previously reported, the majority of issued and outstanding shares approved the Name Change and Symbol Change on September 15, 2022 by written consent.

The Financial Industry Regulatory Authority (“FINRA”) announced the effectiveness of the Name Change and Symbol Change on December 9, 2022, which became effective in the market and for trading under the new name and ticker symbol on Monday, December 12, 2022.

The Name Change and Symbol Change do not affect the rights of the Company’s security holders. The Company’s common stock will continue to be quoted on OTC Markets. Following the Name Change, the stock certificates, which reflect the former name of the Company, will continue to be valid and need not be exchanged. Any certificates reflecting the Name Change will be issued in due course as old stock certificates are tendered for exchange or transfer to the Company’s transfer agent.

On December 19, 2022, Kuber Resources (Hong Kong) Limited entered into an consulting agreement with Wing Yeung Tong Medicine Manufactory Biotech Development Co., Limited to provide consulting services in Hong Kong.

Business Overview

Our main business is operating as an international trading platform with its main source of operations as a middle buyer of commodities and selling them to end buyers. There are two sectors of commodities that the Company focuses on; tea and precious metals.

We have experience in the China market and can leverage off that experience to bring together the various traditional products with customers using e-distribution channels. Our revenue streams are generated from the sale of such products throughout China.

We are expanding our business model by connecting traditional products through e-channels and using technological innovation as a driving force to connect end users to increase sales. The company intends to continuously expand the market share in the various products that it is involved in. It is committed to grow into one of the larger market players in the sphere.

| 6 |

We seek to grow our business by pursing the following strategies:

| • | Increasing our customer base by using various e-distribution channels |

| • | offering high quality traditional products for repeat business |

| • | Expanding our lead generation services enabling the business to better engage their customers |

| • | Building our own custom e-channel distribution channel |

| • | Creating cross-selling synergies between the various suit of products and services being sold to the customers |

| • | Using a scalable business model to eliminate certain barriers and rapid growth |

In 2022, as Covid-19 had affected the tea industry, our business focused more on the international trading of precious metal commodities. We developed a line of trading precious metals with suppliers in South America with the end buyers in Hong Kong, China.

Industry Overview

Tea Industry

The tea industry in China is a thriving market. The aggregate Revenue in the industry amounts to USD 92,684,000,000 of sales as at April 2020 and is expected to grow annually by 5.8%1.

Pursuant to statista.com, tea is the most consumed hot drink worldwide and the most consumed non-alcoholic beverage overall. It is especially important in Asia and Eastern Europe as well as in the United Kingdom. It serves the purpose of both caffeination and hydration. In China, tea has a much higher degree of prestige with upscale specialty products. Depending on the quality of the tea, a kilogram of tea in China can go for upwards of USD 100,0002.

1 Figures provided by Statista - https://www.statista.com/topics/4688/tea-industry-in-china/

2 See 1 above.

| 7 |

Given the prevalence of tea in China, combining it together with e-distribution channels can increase the industry growth and sales of the product.

Precious Metals Industry

The precious metals trade industry is a global business involving suppliers from different regions of the world, including South America, and buyers from various parts of the globe, such as Hong Kong. In this industry, suppliers from South America, particularly those in countries like Peru, Chile, and Colombia, are significant players in the trade of precious metals such as gold, silver, and platinum. These suppliers extract and refine the metals and sell them to international buyers, including those in Hong Kong, one of the world's major trade and financial centers. Hong Kong's end buyers include jewelers, bullion dealers, and investors who purchase precious metals both for their intrinsic value and as a store of value. This trade industry creates opportunities for both suppliers and buyers, contributing significantly to the global economy.

Our Strategy

We intend to modernize and enhance the experience of China products by distributing our products through e-distribution channels. In addition to tea and precious metals, the company plans on expanding into other areas to close the distribution gap between supplier and end buyer.

Our business objective is to generate revenues based on the sale of the products and to maintain and grow a customer base based upon our internal database.

Our target market is the China consumer market as well as corporate clients. Given the importance of tea culture within China, being a consumable, this product becomes a staple for meetings in board rooms and at home as an everyday product. As to precious metals, as there is a high demand for precious metals in China, Hong Kong being a trading hub is an excellent location for this business.

The Company seeks to leverage management’s experience to expand its consumer base, starting with corporate clients.

Potential competitors

There will be an abundance of competitors in the market, given the highly competitive environment we operate in, from both existing competitors and new market entrants. The Company’s competitors include Urban Tea Inc., Maiji (“麦吉”), Luosennina (“罗森尼娜”), NAYUKI (“奈雪的茶”), and Chayanyuese (“茶颜悦色”), all of which are located in the Hunan province. However, given that this is a consumable product that is used daily, the market should able to absorb all such products.

As to precious commodities trading in Hong Kong, we face significant competition from a variety of established companies in the region. Key players include industry leaders such as Chow Tai Fook and Luk Fook, both of which have extensive experience in the production and distribution of precious jewelry and metals on a global scale. Additionally, there are numerous multinational banks and financial institutions operating in the city, along with other specialized traders and dealers, who are also potential competitors in the industry. In order to succeed in this highly competitive market, our company must differentiate ourselves by providing exceptional customer service, offering innovative solutions, and building strong relationships with both our suppliers and buyers. By continually evolving and adapting to the changing market conditions, we are confident that we can maintain our position as a competitive player in the precious commodities trading industry in Hong Kong.

Products

Currently our tea plantation partners offer a wide range of tea drinks. The products are focused on not only their taste but also their aesthetic presentation and health benefits. Our products are currently being offered via our managed stores. The product is produced, packaged and ready for consumption by our tea plantation partners in China.

Our goal is to be a leading brand of tea beverages in each city in which we currently and intend to operate, by selling the finest quality tea beverages and related products, as well as complementary food offerings, and by providing each customer with a pleasant and comfortable environment. The current products being offered by our tea plantation partners are being sold in Fujian, in China.

The main product being sold is Yunnan Chi Tse Beeng Cha, which is a type of pu-er tea.

As to precious metals, in 2022, we have been importing tin ore and have contracts for copper ore.

Seasonality

The industry for the sale of tea-based beverages goes through a peak season from April to October, while the rest of the year is off-season. Moreover, seasonality includes adverse weather conditions and ordering during festive seasons, specifically Chinese New Year, where many of the factories may be closed. We have implemented a few measures to mitigate the impact of such seasonal fluctuations in sale, such as taking reserve stock to be sold during the off-season. As pu-er tea can be aged, keeping pu-er tea stock not only increases our inventory, but is also a good investment for later sales.

As to precious metals, shipping can take from 45 to 90 days from South America to Hong Kong depending on a variety of reasons and conditions, such as custom issues from the load port and quality issues of the cargoes at the discharge port.

| 8 |

Management, Culture and Training

We are guided by a philosophy that recognizes customer service and the importance of delivering optimal performance.

Passion for Tea. We seek to recruit, hire, train, retain and promote qualified, knowledgeable and enthusiastic business partners who share our passion for tea and strive to deliver an extraordinary retail experience to our customers.

| · | Extensive Training. We have specific training and certification requirements for potential business partners, including undergoing food handlers’ certification and foundational training. This process helps ensure that all team members educate our customers and execute our standards accurately and consistently. As team members progress to the assistant manager and manager levels, they undergo additional weeks of training in sales, operations and management. |

This philosophy extends to all types of trading and is applicable to precious metals trade.

Business and Strategic Partners

Currently, we are strategically aligned with Dongguan Gongxiang Tea Food Company Ltd, which is a tea plantation in Fujian that supplies the products mentioned above.

As to precious metals, we have strategically aligned with suppliers in South America.

Licenses, Permits and Government Regulations

PRC Legal System

The PRC legal system is a civil law system based on the PRC Constitution and is made up of written laws, regulations and directives. Unlike in the US where the law built partly upon decisions of common law cases, court cases in the PRC do not constitute binding precedents. The governmental directives are organized in the following hierarchy.

The National People’s Congress of the PRC (“NPC”) and the Standing Committee of the NPC are empowered by the PRC Constitution to exercise the legislative power of the state. The NPC has the power to amend the PRC Constitution and to enact and amend primary laws governing the state organs and civil and criminal matters. The Standing Committee of the NPC is empowered to interpret, enact and amend laws other than those required to be enacted by the NPC.

The State Council of the PRC is the highest organ of state administration and has the power to enact administrative rules and regulations. Ministries and commissions under the State Council of the PRC are also vested with the power to issue orders, directives and regulations within the jurisdiction of their respective departments. Administrative rules, regulations, directives and orders promulgated by the State Council and its ministries and commissions must not be in conflict with the PRC Constitution or the national laws and, in the event that any conflict arises, the Standing Committee of the NPC has the power to annul such administrative rules, regulations, directives and orders.

At the regional level, the people’s congresses of provinces and municipalities and their standing committees may enact local rules and regulations and the people’s government may promulgate administrative rules and directives applicable to their own administrative area. These local laws and regulations may not be in conflict with the PRC Constitution, any national laws or any administrative rules and regulations promulgated by the State Council.

Rules, regulations or directives may be enacted or issued at the provincial or municipal level or by the State Council of the PRC or its ministries and commissions in the first instance for experimental purposes. After sufficient experience has been gained, the State Council may submit legislative proposals to be considered by the NPC or the Standing Committee of the NPC for enactment at the national level.

Governmental Regulations in Relation to the Company’s Businesses

Regulations Related to Retail

There are no separate mandatory legal provisions on the retail business model in the PRC. Companies and individual businesses may engage is the retail business as long as they have registered with the commerce departments in accordance with the laws such as the Regulation on Individual Industrial and Commercial Households and Administration of the Registration of Enterprises As Legal Persons, and include “retail” in the business scope on their business license.

| 9 |

Seasonality

We believe our operation and sales do not experience seasonality.

Off Balance Sheet Arrangements

We do not maintain off balance sheet arrangements.

Contractual Obligations and Commitments

As of December 31, 2022 and 2021, we did not have any contractual obligations.

Critical Accounting Policies

Our significant accounting policies are described in the notes to our financial statements for the years ended December 31, 2022 and 2021, and are included elsewhere in this registration statement.

Item 1A. RISK FACTORS

We are a smaller reporting company as defined by Rule 12b-2 of the Securities Exchange Act of 1934 and are not required to provide the information under this item.

ITEM 1B. UNRESOLVED STAFF COMMENTS

As a smaller reporting company, we are not required to provide the information pursuant to this Item.

ITEM 2. PROPERTIES

Our mailing address is 1113, Tower 2, Lippo Centre, 89 Queensway, Admiralty, Hong Kong.

ITEM 3. LEGAL PROCEEDINGS

From time to time, we may become involved in various lawsuits and legal proceedings, which arise in the ordinary course of business. However, litigation is subject to inherent uncertainties, and an adverse result in these or other matters may arise from time to time that may harm business. We are currently not aware of any such legal proceedings or claims that will have, individually or in the aggregate, a material adverse effect on our business, financial condition or operating results.

ITEM 4. MINE SAFETY DISCLOSURES

Not applicable.

| 10 |

Part II

ITEM 5. MARKET FOR REGISTRANTS COMMON EQUITY, RELATED STOCKHOLDERS MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES

Market Information

Our common stock is currently quoted on the OTC market "Pink Sheets" under the symbol KUBR. For the periods indicated, the following table sets forth the high and low bid prices per share of common stock. The below prices represent inter-dealer quotations without retail markup, markdown, or commission and may not necessarily represent actual transactions.

| Price Range | ||||||||

| Period | High | Low | ||||||

| Year ended December 31, 2022 | ||||||||

| First Quarter | $ | 4.50 | 4.50 | |||||

| Second Quarter | $ | 5.00 | 5.00 | |||||

| Third Quarter | $ | 5.75 | 5.75 | |||||

| Fourth Quarter | $ | 1.10 | 1.10 | |||||

| Year Ended December 31, 2021: | ||||||||

| First Quarter | $ | 18.00 | 18.00 | |||||

| Second Quarter | $ | 8.71 | 8.71 | |||||

| Third Quarter | $ | 5.05 | 5.05 | |||||

| Fourth Quarter | 4.95 | 4.95 | ||||||

Stockholders of Record

As of April 11, 2023, the Company has 150 recorded holders of our Common Stock. This number excludes any estimate by us of the number of beneficial owners of shares held in street name, the accuracy of which cannot be guaranteed.

Issuer Direct Corporation, One Glenwood Avenue, Suite 1001, Raleigh, NC 27603, is the transfer agent for our Common Stock.

Effective on August 11, 1993, the SEC adopted Rule 15g-9, which established the definition of a “penny stock,” for purposes relevant to the Company, as any equity security that has a market price of less than $5.00 per share or with an exercise price of less than $5.00 per share, subject to certain exceptions. For any transaction involving a penny stock, unless exempt, the rules require: (i) that a broker or dealer approve a person’s account for transactions in penny stocks; and (ii) that the broker or dealer receive from the investor a written agreement to the transaction, setting forth the identity and quantity of the penny stock to be purchased. In order to approve a person’s account for transactions in penny stocks, the broker or dealer must (i) obtain financial information and investment experience and objectives of the person; and (ii) make a reasonable determination that the transactions in penny stocks are suitable for that person and that person has sufficient knowledge and experience in financial matters to be capable of evaluating the risks of transactions in penny stocks. The broker or dealer must also deliver, prior to any transaction in a penny stock, a disclosure schedule prepared by the Commission relating to the penny stock market, which, in highlight form, (i) sets forth the basis on which the broker or dealer made the suitability determination; and (ii) states that the broker or dealer received a signed, written agreement from the investor prior to the transaction. Disclosure also has to be made about the risks of investing in penny stock in both public offerings and in secondary trading, and about commissions payable to both the broker-dealer and the registered representative, current quotations for the securities and the rights and remedies available to an investor in cases of fraud in penny stock transactions. Finally, monthly statements have to be sent disclosing recent price information for the penny stock held in the account and information on the limited market in penny stocks.

Common Stock

We are authorized to issue 1,000,000,000 common shares at a par value of $.001. As of December 31, 2022 and April 11, 2023 there are 132,606,355 and 132,612,342 common shares outstanding, respectively. Each holder of Common Stock shall be entitled to one vote per share.

Preferred Stock

We are authorized to issue 10,000,000 shares of preferred stock at a par value of $0.001. Out of the 10,000,000 shares of preferred stock, we are authorized to issue 2,000,000 shares of Series A Preferred Stock and 1,000,000 shares of Series B Preferred Stock.

| 11 |

Series A Preferred Shares

The following is a description of the material rights of our Series A Convertible Preferred Stock: Each share of Series A convertible Preferred Stock shall have a par value of $0.001 per share. The Series A Preferred Stock shall vote on any matter that may from time to time be submitted to the Company’s shareholders for a vote, on a one for one basis. If the Company effects a stock split which either increases or decreases the number of shares of Common Stock outstanding and entitled to vote, the voting rights of the Series A shall not be subject to adjustment unless specifically authorized.

Each share of Series A Convertible Preferred Stock shall be convertible into one share of Common Stock (“Conversion Ratio”), at the option of a Holder, at any time and from time to time, from and after the issuance of the Series A Preferred Stock.

In the event of any liquidation, dissolution or winding up of the Corporation, either voluntary or involuntary, subject to the rights of any existing series of Preferred Stock or to the rights of any series of Preferred Stock which may from time to time hereafter come into existence, the holders of the Series A Preferred Stock shall be entitled to receive, prior and in preference to any distribution of any of the assets of the Corporation to the holders of Common Stock by reason of their ownership thereof, an amount per share equal to the price per share actually paid to the Corporation upon the initial issuance of the Series A Preferred Stock (each, the “the Original Issue Price”) for each share of Series A Preferred Stock then held by them, plus declared but unpaid dividends. Unless the Corporation can establish a different Original Issue Price in connection with a particular sale of Series A Preferred Stock, the Original issue price shall be $0.001 per share for the Series A Preferred Stock. If, upon the occurrence of any liquidation, dissolution or winding up of the Corporation, the assets and funds thus

Dividends

Dividends, if any, will be contingent upon our revenues and earnings, if any, capital requirements and financial conditions. The payment of dividends, if any, will be within the discretion of our board of directors. We intend to retain earnings, if any, for use in our business operations and accordingly, the board of directors does not anticipate declaring any dividends prior to an acquisition transaction, nor can there be any assurance that any dividends will be paid following any acquisition.

Series B Preferred Shares

As of March 1, 2021, we have issued 800,000 shares of Series B Preferred Shares, with $0.001 par value per share. 650,000 of those Series B Preferred Shares have been converted to common stock leaving 150,000 Series B Preferred Shares.

The following is a description of the material rights of our Series B Convertible Preferred Stock: Each share of Series B convertible Preferred Stock shall have a par value of $0.001 per share. The Series B Preferred Stock shall vote on any matter that may from time to time be submitted to the Company’s shareholders for a vote, on a 1,000 for one basis. If the Company effects a stock split which either increases or decreases the number of shares of Common Stock outstanding and entitled to vote, the voting rights of the Series A shall not be subject to adjustment unless specifically authorized.

Each share of Series B Convertible Preferred Stock shall be convertible into one thousand shares of Common Stock (“Conversion Ratio”), at the option of a Holder, at any time and from time to time, from and after the issuance of the Series B Preferred Stock.

In the event of any liquidation, dissolution or winding up of the Corporation, either voluntary or involuntary, subject to the rights of any existing series of Preferred Stock or to the rights of any series of Preferred Stock which may from time to time hereafter come into existence, the holders of the Series B Preferred Stock shall be entitled to receive, prior and in preference to any distribution of any of the assets of the Corporation to the holders of Common Stock by reason of their ownership thereof, an amount per share equal to the price per share actually paid to the Corporation upon the initial issuance of the Series B Preferred Stock (each, the “the Original Issue Price”) for each share of Series B Preferred Stock then held by them, plus declared but unpaid dividends. Unless the Corporation can establish a different Original Issue Price in connection with a particular sale of Series B Preferred Stock, the Original issue price shall be $0.001 per share for the Series B Preferred Stock. If, upon the occurrence of any liquidation, dissolution or winding up of the Corporation, the assets and funds thus

Dividends

Dividends, if any, will be contingent upon our revenues and earnings, if any, capital requirements and financial conditions. The payment of dividends, if any, will be within the discretion of our board of directors. We intend to retain earnings, if any, for use in our business operations and accordingly, the board of directors does not anticipate declaring any dividends prior to an acquisition transaction, nor can there be any assurance that any dividends will be paid following any acquisition.

Securities Authorized for Issuance under Equity Compensation Agreements

None.

| 12 |

Recent Sales of Unregistered Securities

During the years ended December 31, 2022 and 2021, we did not have sales of unregistered securities other than those already disclosed in the quarterly reports on Form 10-Q in the year of 2022 and current reports on Form 8-K.

Recent Purchases of Equity Securities by us and our Affiliated Purchasers

None.

Where You Can Find Additional Information

We are a reporting company and file annual, quarterly and current reports, proxy statements and other information with the SEC. For further information with respect to the Company, you may read and copy its reports, proxy statements and other information, at the SEC public reference rooms at 100 F. Street, N.E., Washington, D.C. 20549. You can request copies of these documents by writing to the SEC and paying a fee for the copying cost. Please call the SEC at 1-800-SEC-0330 for more information about the operation of the public reference rooms. The Company’s SEC filings are also available at the SEC’s web site at http://www.sec.gov.

| 13 |

ITEM 6. SELECTED FINANCIAL DATA

Not applicable to smaller reporting companies.

ITEM 7. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

Management’s Plan of Operation

The following discussion contains forward-looking statements. Forward-looking statements give our current expectations or forecasts of future events. You can identify these statements by the fact that they do not relate strictly to historical or current facts. They use of words such as “anticipate”, “estimate”, “expect”, “project”, “intend”, “plan”, “believe”, and other words and terms of similar meaning in connection with any discussion of future operating or financial performance. From time to time, we also may provide forward-looking statements in other materials we release to the public.

Overview

The Company’s current business objective is to seek operate in the tea and precious metals industry, including acting as a distributor and trader. We intend to use the Company’s limited personnel and financial resources in connection with such activities.

On November 7, 2022, the Company purchased from GRL21 Nominee Limited all the shares of Kuber Resources (Hong Kong) Limited for one Hong Kong dollar (HKD1.00). Accordingly, Kuber Resources (Hong Kong) Limited became a fully-owned subsidiary of the Company as at November 7, 2022. Kuber Resources (Hong Kong) Limited (previously known as Star Wise Limited) is a company incorporated in Hong Kong on October 21, 2022. It changed its name to Kuber (Resources (Hong Kong) Limited on 1 November 2022 and concurrently filed its notification of commencement of Business by Corporation on the same day. It had not traded and/or otherwise operated until after it had been purchased by the Company on November 7, 2022. The purpose of obtaining Kuber Resources (Hong Kong) Limited is to start an additional line of business outside of the international commodities trade currently undertaken by Asia Image Limited.

Results Of Operations

During The Year Ended December 31, 2022 As Compared To The Year Ended December 31, 2021

Revenue

For the year ended December 31, 2022 and 2021, the Company generated $1,562,629 and no revenue in the previous year , respectively.

Expenses

For the year ended December 31, 2022, the Company incurred $68,289 and $81,812 as total operating expenses, respectively. For the year ended December 31, 2022, operating expenses consisted of $59,557 in professional fees which primarily included audit and accounting fees. For the year ended December 31, 2021, the Company incurred $81,812 as total operating expenses which consists of $ 372,887 as professional fees which primarily includes fees audit and accounting expense. Mr. Raymond Fu, President, and Chief Executive Officer of the Company is also the indirect beneficial owner of Uonlive (Hong Kong) Limited. Also refer note no. 8.

Net Income (Loss)

For the years ended December 31, 2022 we incurred a net income of $758,130. For the years ended December 31, 2021 we incurred a net loss of $81,812. The increase in net income is due to ramp up of business activity during 2022 which was as a result of the Asia Image Acquisition.

| 14 |

Liquidity

Currently, we are relying on sales of our products. Currently, we pay costs associated with running a business on a day to day basis.

As of December 31, 2022, we had current assets of $1,255,948 which consists $109,187 cash on hand, $1,087,589 in advances to suppliers, $55,172 in loans to related parties, and $4,000 in prepaid expenses and current liabilities of $483,979. As of December 31, 2021, we had current assets of $56,085 which consists $52,279 cash on hand, and $3,806 prepaid expenses and current liabilities of $402,674.

To the extent that our capital resources are insufficient to meet current or planned operating requirements, we will seek additional funds through equity or debt financing, collaborative or other arrangements with corporate partners, licensees or others, and from other sources, which may have the effect of diluting the holdings of existing shareholders. The Company has no current arrangements with respect to, or sources of, such additional financing and we do not anticipate that existing shareholders will provide any portion of our future financing requirements.

No assurance can be given that additional financing will be available when needed or that such financing will be available on terms acceptable to the Company. If adequate funds are not available, we may be required to delay or terminate expenditures for certain of its programs that it would otherwise seek to develop and commercialize. This would have a material adverse effect on the Company.

Off-Balance Sheet Arrangements

As of December 31, 2022 and 2021, we did not have any off-balance sheet arrangements as defined in Item 303(a)(4)(ii) of Regulation S-K promulgated under the Securities Act of 1934.

Contractual Obligations and Commitments

As of December 31, 2022 and 2021, we did not have any contractual obligations.

Critical Accounting Policies

Our significant accounting policies are described in the notes to our financial statements for the years ended December 31, 2022 and 2021, and are included elsewhere in this registration statement.

Going concern assumption .

As of December 31, 2022 and 2021, we had accumulated deficit of $3,285,836 and accumulated deficits of approximately $4,043,966, respectively. Our directors are of the opinion that the preparation of these financial statements is based on a going concern and its basis has been stated in Note 3 to the financial statements. Should there be any problem in the going concern of us, all the assets and liabilities have to be stated at net realizable values.

Off-Balance Sheet Arrangements

We had no off-balance sheet arrangements as of December 31, 2022 and 2021.

Seasonality

We believe our operation and sales do not experience seasonality.

Subsequent Events

ITEM 7A: QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK

Not applicable to smaller reporting companies.

ITEM 8: FINANCIAL STATEMENTS AND SUPPLEMENTARY DATA

The audited financial statements of the Company for the fiscal year ended December 31, 2022 and 2021 and the notes thereto are set forth on page F-1 through F-17 of this Annual Report. The Company’s financial statements have been prepared in accordance with accounting principles generally accepted in the U.S., or US GAAP, and pursuant to Regulation S-K as promulgated by the SEC. The financial statements have been prepared assuming the Company will continue as a going concern.

| 15 |

ITEM 9: CHANGES IN AND DISAGREEMENTS WITH ACCOUNTANTS ON ACCOUNTING AND FINANCIAL DISCLOSURE

None.

ITEM 9A: CONTROLS AND PROCEDURES

Evaluation of disclosure controls and procedures

Under the supervision and with the participation of our management, including our principal executive officer/principal financial officer, we conducted an evaluation of our disclosure controls and procedures, as such term is defined under Rule 13a-15(e) and Rule 15d-15(e) promulgated under the Exchange Act, as of December 31, 2022. Based on this evaluation, our principal executive officer and principal financial officer have concluded that our disclosure controls and procedures were effective to ensure that information required to be disclosed by us in the reports we file or submit under the Exchange Act is recorded, processed, summarized, and reported within the time periods specified in the SEC’s rules and forms and that our disclosure and controls are designed to ensure that information required to be disclosed by us in the reports that we file or submit under the Exchange Act is accumulated and communicated to our management, including our principal executive and principal financial officers, or persons performing similar functions, as appropriate to allow timely decisions regarding required disclosure.

Management’s Report on Internal Control over Financial Reporting

Management of the Company is responsible for establishing and maintaining effective internal control over financial reporting as defined in Rule 13a-15(f) under the Exchange Act. The Company’s internal control over financial reporting is designed to provide reasonable assurance to the Company’s management and Board of Directors regarding the preparation and fair presentation of published financial statements in accordance with US GAAP, including those policies and procedures that: (i) pertain to the maintenance of records that, in reasonable detail, accurately and fairly reflect the transactions and dispositions of the assets of the company, (ii) provide reasonable assurance that transactions are recorded as necessary to permit preparation of financial statements in accordance with US GAAP and that receipts and expenditures are being made only in accordance with authorizations of management and directors of the company, and (iii) provide reasonable assurance regarding prevention or timely detection of unauthorized acquisition, use, or disposition of the company’s assets that could have a material effect on the financial statements.

Management conducted an evaluation of the effectiveness of internal control over financial reporting based on the framework in Internal Control-Integrated Framework issued by the Committee of Sponsoring Organizations of the Treadway Commission. Management’s assessment included an evaluation of the design of our internal control over financial reporting and testing of the operational effectiveness of our internal control over financial reporting. Based on this evaluation, Management concluded the Company maintained effective internal control over financial reporting as of December 31, 2022.

Because of its inherent limitations, internal control over financial reporting may not prevent or detect misstatements. Therefore, even those systems determined to be effective can provide only reasonable assurance with respect to financial statement preparation and presentation.

Attestation Report of Registered Public Accounting Firm

This Annual Report on Form 10-K does not include an attestation report of our independent registered public accounting firm, regarding internal controls over financial reporting. Our internal control over financial reporting was not subject to such attestation as we are a smaller reporting company.

Changes in internal controls

There was no change in our internal controls over financial reporting that occurred during the period covered by this report, which has materially affected, or is reasonably likely to materially affect, our internal controls over financial reporting.

ITEM 9B. OTHER INFORMATION.

None.

| 16 |

PART III

ITEM 10. DIRECTORS, EXECUTIVE OFFICERS AND CORPORATE GOVERNANCE

Set forth below is information regarding our directors and executive officers as of the date of this Annual Report. The Board is comprised of only one class. All of the directors will serve until the next annual meeting of shareholders and until their successors are elected and qualified, or until their earlier death, retirement, resignation or removal. Officers are elected by and serve at the discretion of the Board. To date we have not had an annual meeting. There are no family relationships between any of our directors or executive officers.

| Name | Age | Position(s) | ||

| Raymond Fu | 54 | President, Treasurer, CEO, Secretary, Director | ||

| Timothy Lam Chee Yau | 38 | Secretary, Director | ||

| Michael Woo Chi Wai | 54 | Director | ||

| Shiu Chung Chan | 36 | Director | ||

| Hok Hin Mui | 32 | Director |

The following is a brief biography of each of our executive officers and directors:

FU, RAYMOND

Mr. Raymond Fu has more than 20 years of professional experience in operations, management and M&A in the finance industry. From 1993 until 2005, Mr Fu worked various roles at Triplenic Holdings Limited (now known as Fujian Group Limited (HKEX:181)), including as an executive director where he helped the group grow from a market value of 1 billion HKD to 300 billion HKD. From 2005 to present, Mr Fu has held his role as an executive director of Asia Image Investment Limited.

Mr Fu is also currently serving as the sole director and controlling shareholder of Uonlive (Hong Kong) Limited, a company incorporated in Hong Kong, since its incorporation on 22 May 2020. He is also the sole director and a shareholder of Chuang Fu Capital Equity CCI Capital Limited, a Hong Kong company, since its incorporation on 4 December 2018. Chuang Fu Capital Equity CCI Capital Limited is the sole shareholder of Chuang Fu Qu Kuai Technology (Shenzhen) Limited, a company incorporated in Shenzhen, China.

Mr. Fu has served in various public positions including President of the Lions Club and Honorary President of the New Territories Manufacturer's Association.

LAM, CHEE YAU TIMOTHY

Timothy was admitted as a lawyer in New South Wales, Australia in 2007. He is also admitted and a qualified lawyer in New Zealand and Hong Kong. Since 2019, he has been a Partner in a Hong Kong law firm and has experience across multiple jurisdictions including USA, Hong Kong, Australia, and China. Timothy has worked in both domestic and international firms in Australia and Hong Kong.

Timothy has a Bachelors in Arts (Philosophy), Bachelors in Law, Masters in Law (Corporate and Finance), Masters in Industrial Property, Masters in Applied Law (Commercial Litigation), Masters in Strategic Public Relations, Masters in Buddhist Studies and a Masters in Buddhist Counselling.

Timothy has advised and acted for multiple listed companies in Hong Kong and Australia. He has also advised listed company board members on their obligations and has also advised high level corporate and governmental staff as to their duties in their roles.

Timothy is a Member of the Hong Kong Law Society, a Member of the NSW Law Society, a Governor to the Board of the Children’s Cancer Foundation and a Fellow of the Hong Kong Institute of Directors. He has acted on multiple boards in private companies in Australia and Hong Kong.

| 17 |

WOO, CHI WAI MICHAEL

Michael is a consultant and has over 20 years of specialized experience working for international financial institutions and large corporate enterprises. His experience spans across working for various listed companies in multi-jurisdictions including the USA, Singapore, Hong Kong, Australia and China. From 1997 to 1999, Michael joined the Australian listed company Zhongxiang Construction Group (ASX:CIH) as a deputy manager of project financing. In 2003 to 2008, Michael joined Hong Kong First Asia Financial Group (now known as National Investment Limited HKEX:1227) as a partner of the global capital markets team. From 2009 to 2013, Michael Joined the China Minmetals Securities as the International Capital Markets Operations Director. From 2017 to 2019, Michael joined the HSBC Financial Group Co., Ltd as a Chief Strategy Officer. He has been involved in multiple large-scale deals which include raising over 1 billion dollars’ worth of capital. He has also experience in managing companies at various levels including acting as a director for various company boards.

CHAN, SHIU CHUNG

Shiu Chung obtained a Bachelor of Arts in Japanese Studies from the University of Hong Kong in 2011, and obtained a Masters of Business Administration in International Business from the University of Greenwich in 2019.

Shiu Chung is currently also currently the General Manager for Emperio Securities and Assets Management Ltd in Hong Kong.

MUI, HOK HIN

Hok Hin obtained a Bachelor of Economic and Finance from the University of Hong Kong in 2013. He has experience in asset management and is currently a trader in the Sunrich Asset Management Limited Group in Hong Kong.

Committees of the Board of Directors

Our board of directors has not established any committees, including an audit committee, a compensation committee, a nominating committee or any committee performing a similar function. The functions of those committees are being undertaken by our Board as a whole. Because we only recently (March 2023) appointed two independent directors, the establishment of committees of the Board of Directors has not yet been undertaken.

Code of Ethics

We have not adopted a code of business conduct and ethics that applies to our directors, officers and all employees.

Family Relationships

There are no family relationships among the directors and executive officers of the Company.

Directors’ Compensation

We have not paid any cash compensation to members of our Board of Directors.

The Company will reimburse its directors for reasonable expenses in connection with attendance at board and committee meetings. Directors will also be eligible to receive stock options offered by our company from time to time. No options have been granted to any director.

Involvement in Certain Legal Proceedings

To the best of our knowledge, our sole director or any executive officers have not, during the past ten years:

| ● | been convicted in a criminal proceeding or been subject to a pending criminal proceeding (excluding traffic violations and other minor offenses); |

| ● | had any bankruptcy petition filed by or against the business or property of the person, or of any partnership, corporation or business association of which he was a general partner or executive officer, either at the time of the bankruptcy filing or within two years prior to that time; |

| ● | been subject to any order, judgment, or decree, not subsequently reversed, suspended or vacated, of any court of competent jurisdiction or federal or state authority, permanently or temporarily enjoining, barring, suspending or otherwise limiting, his involvement in any type of business, securities, futures, commodities, investment, banking, savings and loan, or insurance activities, or to be associated with persons engaged in any such activity; |

| 18 |

| ● | been found by a court of competent jurisdiction in a civil action or by the SEC or the Commodity Futures Trading Commission to have violated a federal or state securities or commodities law, and the judgment has not been reversed, suspended, or vacated; |

| ● | been the subject of, or a party to, any federal or state judicial or administrative order, judgment, decree, or finding, not subsequently reversed, suspended or vacated (not including any settlement of a civil proceeding among private litigants), relating to an alleged violation of any federal or state securities or commodities law or regulation, any law or regulation respecting financial institutions or insurance companies including, but not limited to, a temporary or permanent injunction, order of disgorgement or restitution, civil money penalty or temporary or permanent cease-and-desist order, or removal or prohibition order, or any law or regulation prohibiting mail or wire fraud or fraud in connection with any business entity; or |

| ● | been the subject of, or a party to, any sanction or order, not subsequently reversed, suspended or vacated, of any self-regulatory organization (as defined in Section 3(a)(26) of the Exchange Act), any registered entity (as defined in Section 1(a)(29) of the Commodity Exchange Act), or any equivalent exchange, association, entity or organization that has disciplinary authority over its members or persons associated with a member. |

Corporate Governance

The business and affairs of the Company are managed by the Board of Directors. In addition to the contact information in this Annual Report, each stockholder will be given specific information on how he/she can direct communications to the officers and directors of the Company at our annual stockholders meetings. All communications from stockholders are relayed to the board of member.

Role in Risk Oversight

Our sole director is primarily responsible for overseeing our risk management processes. The Board receives and reviews periodic reports from management, auditors, legal counsel, and others, as considered appropriate regarding our company’s assessment of risks. The sole director focuses on the most significant risks facing our company and our company’s general risk management strategy, and also ensures that risks undertaken by our company are consistent with the board’s appetite for risk. While the sole director oversees our company’s risk management, management is responsible for day-to-day risk management processes.

Compliance with Section 16(a) of the Exchange Act

Section 16(a) of the Exchange Act, requires our directors, officers and persons who own more than 10% of our common stock to file with the SEC initial reports of ownership and reports of changes in ownership of common stock and other of our equity securities. To our knowledge, based solely on review of the copies of such reports furnished to us, all Section 16(a) filings applicable to officers, directors and greater than 10% shareholders were not timely made during year 2022.

ITEM 11. EXECUTIVE COMPENSATION

No executive compensation was paid during the years ended December 31, 2022 and 2021. The Company has no employment agreement with any of its officers and directors.

Agreements with Named Executive Officers

On March 2, 2020, the Company entered into a Definitive Share Agreement whereby Mr. Raymond Fu, the sole shareholder of Asia Image Investment Limited, and the an officer and director of the Company, relinquished all his shares in Asia Image and acquired 100,000 shares of the Company. Consequently, Asia Image became a wholly-owned subsidiary of the Company.

Pension, Retirement or Similar Benefit Plans

There are no arrangements or plans in which we provide pension, retirement or similar benefits for directors or executive officers. We have no material bonus or profit sharing plans pursuant to which cash or non-cash compensation is or may be paid to our directors or executive officers, except that stock options may be granted at the discretion of the board of directors or a committee thereof.

| 19 |

Compensation of Directors

For the years ended December 31, 2022 and 2021, we have not paid compensation to any of our directors.

Outstanding Equity Awards

There were no equity awards outstanding as of the end of the year ending December 31, 2022.

Compensation Policies and Practices as They Relate to the Company’s Risk Management

We believe that our current compensation policies and practices for all employees, including executive officers, do not create risks that are reasonably likely to have a material adverse effect on us.

Equity Compensation Plan

The Company currently does not have any equity compensation plans; however, the Company is currently deliberating on implementing an equity compensation plan.

Directors’ and Officers’ Liability Insurance

The Company currently does not have insurance for directors and officers against liability; however, the Company is in the process of investigating the availability of such insurance.

Change of Control Compensatory Plans

As of December 31, 2022, we had no pension plans or compensatory plans or other arrangements which provide compensation in the event of termination of employment or change in control of us.

ITEM 12. SECURITY OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND MANAGEMENT RELATED STOCKHOLDERS MATTERS

The following table sets forth as of April 11, 2023 the number of shares of the Company’s common stock and preferred stock owned on record or beneficially by each person known to be the beneficial owner of 5% or more of the issued and outstanding shares of the Company’s voting stock, and by each of the Company’s directors and executive officers and by all its directors and executive officers as a group. As of April 11, 2023 there were 132,612,342 common shares issued and outstanding.

The amounts and percentages of our Common Stock beneficially owned are reported on the basis of SEC rules governing the determination of beneficial ownership of securities. Under the SEC rules, a person is deemed to be a “beneficial owner” of a security if that person has or shares “voting power,” which includes the power to vote or to direct the voting of such security, or “investment power,” which includes the power to dispose of or to direct the disposition of such security. A person is also deemed to be a beneficial owner of any securities of which that person has the right to acquire beneficial ownership within 60 days through the exercise of any stock option, warrant or other right. Under these rules, more than one person may be deemed a beneficial owner of the same securities and a person may be deemed to be a beneficial owner of securities as to which such person has no economic interest. Unless otherwise indicated, each of the shareholders named in the table below, or his or her family members, has sole voting and investment power with respect to such shares of our Common Stock. Except as otherwise indicated, the address of each of the shareholders listed below is: 1113, Tower 2, Lippo Center, 89 Queensway, Hong Kong, Hong Kong 000000.

| 20 |

In computing the number of shares of Common Stock beneficially owned by a person and the percentage ownership of that person, we deemed to be outstanding all shares of Common Stock as held by that person or entity that are currently exercisable or that will become exercisable within 60 days of April 11, 2023.

List of Common stockholder

| Name of Shareholder | Affiliation with Company |

Number of Common Shares |

Percent of Class | Note |

| Raymond Fu | President / CEO/ Secretary / Treasurer / Director | 5,000 | *% | 1,3 |

| Uonlive (Hong Kong) Limited | N/A | 116,587,211 | 87.9% | 1 |

List of Preference Shareholders-

| Name of Shareholder | Affiliation with Company |

Number of Shares |

Holding % | Nature of Preference shares |

Notes |

| Dragon Ace Global Limited | N/A | 250,000 | 21.37% | Series A | 2 |

| Standford Global Capital Limited | N/A | 250,000 | 21.37% | Series A | 3 |

| Chuang Fu Qu Kuai Lian Technology (Shenzhen) Limited | N/A | 150,000 | 12.82% | Series B | 4 |

| Uonlive (Hong Kong) Limited | 520,000 | 44.44% | Series A | 1,3 |

*less than 1%

1 Raymond Fu is the direct beneficial owner of 5,000 common shares and indirect beneficial owner of 116,587,211 of common stock of the Company and 520,000 Series A preferred shares through Uonlive (Hong Kong) Limited, of which Raymond Fu is the indirect beneficial owner of 99% of its share capital.

2. Chi Hung Tsang, is the control person of Dragon Ace Global Limited and has dispositive voting control thereof; its business address is 5/F Guangdong Finance Building 88, Connaught Road West Hong Kong, Hong Kong.

3. Chi Hung Tsang, is the control person of Standford and has dispositive voting control thereof; its business address is 5/F Guangdong Finance Building 88, Connaught Road West Hong Kong, Hong Kong.

4. Zhong Jia Ping, is a Director of Chuang Fu Qu Kuai Lian Technology (Shenzhen) Limited and has dispositive voting control thereof.

There are no other persons known by us who owns beneficially 5% or more of our common stock as of April 11, 2023.

| 21 |

ITEM 13. CERTAIN RELATIONSHIPS AND RELATED TRANSACTIONS, AND DIRECTOR INDEPENDENCE

Other than compensation agreements and other arrangements described in “Management,” and our transactions described below, since our inception there has not been, nor is there currently proposed, any transaction or series of similar transactions to which we were or will be a party:

| ● | in which the amount involved exceeded or will exceed $120,000; and |

| ● | in which any current director, executive officer, holder of 5% or more of our shares of Common Stock on an as-converted basis or any member of their immediate family had or will have a direct or indirect material interest. |

Related parties payable

On March 02, 2020, the Company entered into a Definitive Share Agreement whereby Raymond Fu, the sole shareholder of Asia Image Investment Limited (“Asia Image”), relinquished all his shares in Asia Image and acquired 100,000 shares of the Company. Consequently, Asia Image became a wholly-owned subsidiary of the Company.

On May 26, 2020 and October 10, 2020, the Company issued 650,000 (Series B Convertible Preferred Stock) and 520,000 (Series A Convertible Preferred Stock) Convertible Preferred Stock to Uonlive (Hong Kong) Limited for the provision of management services valued at $54,586 and $ 290,990 respectively. Mr. Raymond Fu, President, and Chief Executive Officer of the Company is also the indirect beneficial owner of Uonlive (Hong Kong) Limited.

Loan Payable-Related Party

As of December 31, 2022 and 2021 the Company has a loan payable of $77,785 and $170,712 to Mr. Raymond Fu, President and Chief Executive Officer of the Company, respectively. This loan is unsecured, non-interest bearing and it is repayable on demand.

Note Payable-Related Party

As of December 31, 2022 and 2021 the Company has a note payable of and $0 and $167,554 to Mr. Raymond Fu, President and Chief Executive Officer of the Company. This note is unsecured, non-interest bearing and it is repayable on demand.

Director Independence

Our Board of Directors will periodically review relationships that directors have with the Company to determine whether the directors are independent. Directors are considered “independent” as long as they do not accept any consulting, advisory or other compensatory fee (other than director fees) from the Company, are not an affiliated person of the Company or its subsidiaries (e.g., an officer or a greater-than-ten-percent stockholder) and are independent within the meaning of applicable laws, regulations. In this latter regard, the Board of Directors will use the Nasdaq listing rules (specifically, Section 5605(a)(2) of such rules) as a benchmark for determining which, if any, of its directors are independent, solely in order to comply with applicable SEC disclosure rules. However, this is for disclosure purposes only.

Our Board of Directors has determined, after considering all the relevant facts and circumstances, that Shiu Chung Chan and Hok Hin Mui are independent directors, as “independence” is defined by the listing standards of Nasdaq, and by the Securities and Exchange Commission, or SEC, because they have no relationship with us that would interfere with their exercise of independent judgment in carrying out their responsibilities as a director. Mr. Fu, Mr. Lam, and Mr. Woo are not “independent” as defined by the listing standards.

| 22 |

ITEM 14. PRICINPAL ACCOUNTING FEES AND SERVICES

Audit Fees

For the Company’s fiscal years ended December 31, 2022 and 2021, we were billed approximately $37,000 and $34,000 for professional services rendered for the audit and review of our financial statements.

Audit Related Fees

There were no fees for audit related services for the years ended December 31, 2022 and 2021.

Tax Fees

For the Company’s fiscal years ended December 31, 2022 and 2021, there were no fees for professional services rendered for tax compliance, tax advice, and tax planning.

All Other Fees

The Company did not incur any other fees related to services rendered by our principal accountant for the fiscal years ended December 31, 2022 and 2021.

Effective May 6, 2003, the SEC adopted rules that require that before our independent registered public accounting firm is engaged by us to render any auditing or permitted non-audit related service, the engagement be:

| ● | approved by our audit committee; or |

| ● | entered into pursuant to preapproval policies and procedures established by the audit committee, provided the policies and procedures are detailed as to the particular service, the audit committee is informed of each service, and such policies and procedures do not include delegation of the audit committee’s responsibilities to management. |

We do not have an audit committee. Our board of directors preapproves all services provided by our independent registered public accounting firm. However, all of the above services and fees were reviewed and approved by the board for the respective services were rendered.

| 23 |

ITEM 15. FINANCIAL STATEMENTS AND EXHIBITS

| Report of Independent Registered Public Accounting Firm | F-1 |

| Consolidated Balance Sheets as of December 31, 2022 and December 31, 2021 | F-3 |

| Consolidated Statements of Operations for the Years Ended December 31, 2022 and December 31, 2021 | F-4 |

| Consolidated Statements of Changes in Stockholders’ Equity for the Years Ended December 31, 2022 and December 31, 2021 | F-5 |

| Consolidated Statements of Cash Flows for the Years Ended December 31, 2022 and December 31, 2021 | F-6 |

| Notes to the Consolidated Financial Statements | F-7 |

(a) FINANCIAL STATEMENTS. The following financial statements are included in this report:

| 24 |

(b) EXHIBITS. The following exhibits are included as part of this report:

| 25 |

ITEM 16. FORM 10-K SUMMARY

None.

| 26 |

Report of Independent Registered Public Accounting

Firm (PCAOB ID

Report of Independent Registered Public Accounting Firm

To the Shareholders and Board of Directors of Kuber Resources Corporation

Opinion on the Financial Statements