WELLS FARGO FUNDS TRUST

PART A

PROSPECTUS/INFORMATION STATEMENT

|

|

|

Prospectus/Information Statement

|

|

|

|

|

|

Important merger information

|

In November 2020, the Board of Trustees (the “Board”) of Wells Fargo Funds Trust (the “Trust”) approved the merger of Wells Fargo Diversified International Fund (the “Target Fund”) into Wells Fargo International Equity Fund (the “Acquiring Fund”), two funds within the same fund family. The merger does not require approval by Target Fund shareholders. We Are Not Asking You for a Proxy and You are Requested Not To Send Us a Proxy.

Please read the following information.

The enclosed document is a prospectus/information statement with information concerning the Target Fund and Acquiring Fund. As a shareholder of the Target Fund, you are being provided with this document to inform you of the principal aspects of the merger of your fund into the Acquiring Fund. We encourage you to read the full text of the enclosed prospectus/information statement.

What is happening?

The Board of the Target Fund believes that this merger will benefit current Target Fund shareholders. In the merger, the Target Fund will transfer all of its assets and liabilities to the Acquiring Fund in exchange for the same class of shares of the Acquiring Fund. The merger is expected to be a tax-free reorganization for U.S. federal income tax purposes. Immediately following the merger of your fund into the Acquiring Fund, you will hold shares of the Acquiring Fund with a dollar value equal to the dollar value of the Target Fund shares you previously held. The Target Fund and the Acquiring Fund are listed in the table below:

|

|

|

Target Fund

|

Acquiring Fund

|

|

Wells Fargo Diversified International Fund

|

Wells Fargo International Equity Fund

|

What do we believe are some key benefits of the fund merger?

Among the factors that Wells Fargo Funds Management, LLC considered in recommending the merger were the following:

| ■ |

Factoring in the waivers to which Wells Fargo Funds Management, LLC has contractually committed through February 28, 2022, the annual fund operating expenses after fee waivers of the Acquiring Fund are the same or lower compared to the Target Fund. |

| ■ |

Wells Fargo Funds Management, LLC serves as the investment manager of the Target Fund and the Acquiring Fund. |

| ■ |

Wells Capital Management Incorporated is the investment sub-advisor for the Target Fund and the Acquiring Fund. |

| ■ |

Both the Target Fund and the Acquiring Fund are managed by a team of portfolio managers and analysts from Wells Capital Management Incorporated’s [Fundamental Growth Equity team], under the leadership of Venkateshwar (Venk) Lal and Dale Winner, CFA. |

Why has the Board of Trustees approved the merger?

Among the factors the Board considered in approving the merger were the following:

| ■ |

The investment objective and principal investment strategy of the Target Fund is comparable to that of the Acquiring Fund. |

| ■ |

The merger will eliminate duplicative expenses and may reduce associated operating costs. |

| ■ |

Shareholders will not bear the Merger-related expenses (other than brokerage and transaction costs associated with the sale or purchase of portfolio securities in connection with the Merger). |

| ■ |

The merger is expected to be a tax-free reorganization for U.S. federal income tax purposes. |

Whom should I call with questions about the merger?

If you have any questions about the merger or related merger materials, please call your investment professional, trust officer, or the Wells Fargo Funds at 1-800-222-8222.

|

|

|

|

|

Wells Fargo Asset Management is a trade name used by the asset management businesses of Wells Fargo & Company. Wells Fargo Funds Management, LLC, a wholly owned subsidiary of Wells Fargo & Company, provides investment advisory and administrative services for Wells Fargo Funds. Other affiliates of Wells Fargo & Company provide subadvisory and other services for the funds. The funds are distributed by Wells Fargo Funds Distributor, LLC, Member FINRA, an affiliate of Wells Fargo & Company. |

|

|

|

|

© 2020 Wells Fargo Funds Management, LLC. All rights reserved.

|

www.wfam.com

|

WELLS FARGO FUNDS TRUST

525 MARKET STREET, 12TH FLOOR, SAN FRANCISCO, CA 94105

1.800.222.8222

December 30, 2020

Dear Shareholder,

On November 17, 19-20, 2020, the investment manager to the Wells Fargo Funds, Wells Fargo Funds Management, LLC (“Funds Management”), proposed to the Board of Trustees of Wells Fargo Funds Trust the merger outlined in the table below (the “Merger”). The Board of Trustees approved the Merger and the related Agreement and Plan of Reorganization.

|

|

|

Target Fund

|

Acquiring Fund

|

|

Wells Fargo Diversified International Fund

|

Wells Fargo International Equity Fund

|

This is a general summary of how the Merger will work:

| ■ |

The Target Fund will transfer all of its assets to the Acquiring Fund. |

| ■ |

The Acquiring Fund will assume all of the liabilities of the Target Fund. |

| ■ |

The Acquiring Fund will issue new shares that will be distributed to you in a dollar amount equal to the value of your Target Fund shares. |

| ■ |

You will become a shareholder of the Acquiring Fund and will have your investment managed in accordance with the Acquiring Fund’s investment strategies. |

| ■ |

You will not incur any sales charges or similar transaction charges as a result of the Merger. |

| ■ |

It is expected that the Merger will not be a taxable event to the Target Fund, the Acquiring Fund or their shareholders for U.S. federal income tax purposes. |

Details about the Target Fund’s and the Acquiring Fund’s investment objectives, principal investment strategies, management, past performance, principal risks, fees, and expenses, along with additional information about the Merger, are contained in the attached prospectus/information statement. Please read it carefully.

Thank you for choosing to invest with Wells Fargo Funds. We appreciate your confidence in us and remain committed to helping you meet your financial needs.

Sincerely,

Andrew Owen

President

Wells Fargo Funds

WELLS FARGO FUNDS TRUST

525 MARKET STREET, 12TH FLOOR, SAN FRANCISCO, CA 94105

1.800.222.8222

December 30, 2020

PROSPECTUS/INFORMATION STATEMENT

This prospectus/information statement contains information you should know before the completion of the merger (the “Merger”) of your Target Fund into the Acquiring Fund as set forth and defined in the table below, each of which is a series of Wells Fargo Funds Trust (the “Trust”), a registered open-end management investment company. The Merger will result in you receiving shares of the Acquiring Fund in exchange for your shares of the Target Fund.

|

|

|

Target Fund

|

Acquiring Fund

|

|

Wells Fargo Diversified International Fund

|

Wells Fargo International Equity Fund

|

The Target Fund and Acquiring Fund listed above are collectively referred to as the “Funds.”

Please read this prospectus/information statement carefully and retain it for future reference. Additional information concerning each Fund and the Merger has been filed with the Securities and Exchange Commission (the “SEC”).

The prospectuses, statements of additional information and annual reports of the Target Fund and the Acquiring Fund are incorporated into this document by reference and are legally deemed to be part of this prospectus/information statement. Copies of these documents pertaining to either the Target Fund or the Acquiring Fund are available upon request without charge by writing to Wells Fargo Funds, PO Box 219967, Kansas City, MO 64121-99676, calling 1.800.222.8222 or visiting the Wells Fargo Funds website at wfam.com.

You may also view or obtain these documents from the SEC: by phone at 1.800.SEC.0330 (duplicating fee required); in person or by mail at Public Reference Section, Securities and Exchange Commission, 100 F Street, N.E., Washington, D.C. 20549-0213 (duplicating fee required); by email at publicinfo@sec.gov (duplicating fee required); or by internet at www.sec.gov.

The SEC has not approved or disapproved these securities or determined if this prospectus/information statement is truthful or complete. Any representation to the contrary is a criminal offense.

The shares offered by this prospectus/information statement are not deposits of a bank, are not insured, endorsed or guaranteed by the FDIC or any government agency and involve investment risk, including possible loss of your original investment.

OVERVIEW

This section summarizes the primary features and consequences of the Merger. This summary is qualified in its entirety by reference to the information contained elsewhere in this prospectus/information statement, in the Merger Statement of Additional Information (“Merger SAI”), in each Fund’s prospectus, in each Fund’s financial statements contained in its annual report, in each Fund’s Statement of Additional Information (“SAI”), and in the related Agreement and Plan of Reorganization (the “Plan”), a form of which is attached as Exhibit A hereto.

KEY FEATURES OF THE MERGER

The Plan sets forth the key features of the Merger covered thereby and generally provides for the following:

| ■ |

the transfer of all of the assets of the Target Fund to the Acquiring Fund in exchange for new shares of the Acquiring Fund; |

| ■ |

the assumption by the Acquiring Fund of all of the liabilities of the Target Fund; |

| ■ |

the liquidation of the Target Fund by distributing the shares of the Acquiring Fund to the Target Fund’s shareholders; and |

| ■ |

the assumption of the costs of the Merger by Wells Fargo Funds Management, LLC ( the “Manager” or “Funds Management”) or one of its affiliates. |

The Merger is scheduled to take place on or about March 26, 2021 (the “Closing Date”). For a more complete description of the Merger, see the section entitled “Merger Information - Agreement and Plan of Reorganization,” as well as Exhibit A.

REASONS FOR THE MERGER AND BOARD OF TRUSTEES APPROVAL

At a meeting held on November 17, 19-20, 2020, the Board of Trustees of the Trust (the “Board”), including a majority of Trustees who are not “interested persons” of the Target Fund, as that term is defined in the Investment Company Act of 1940, as amended (the “1940 Act”) (the “Independent Trustees”), considered and unanimously approved the Merger.

Prior to approving the Merger, the Board received the recommendation that the Merger be approved from the Manager. In recommending the approval of the Merger to the Board, the Manager noted that it considered various factors, including asset size, performance and profitability. The Manager indicated to the Board that the proposal to merge the Target Fund into the Acquiring Fund is intended to further rationalize the product offerings of the Wells Fargo fund family by combining funds with similar investment objectives and principal investment strategies.

Before approving the Merger, the Board reviewed, among other things, information about the Funds and the Merger. This included, among other things, a comparison of various factors, such as the relative sizes of the Funds, the performance records of the Funds, and the expenses of the Funds (including pro forma expense information of the Acquiring Fund following the Merger), as well as the similarities and differences between the Funds’ investment objectives, principal investment strategies and specific portfolio characteristics.

The Board, including all of the Independent Trustees, has concluded that the Merger would be in the best interests of the Target Fund, and that existing shareholders’ interests will not be diluted as a result of the Merger. Accordingly, the Board approved the Plan on behalf of the Target Fund’s shareholders and on behalf of the Acquiring Fund’s shareholders. For further information about the considerations of the Board, please see the section entitled “Board Considerations.”

In addition to the Merger, the Board also approved the reorganization of the Wells Fargo International Value Fund, another international equity fund in the fund family, into the Acquiring Fund (the “International Value Fund merger”). Unlike the Merger outlined here, the International Value Fund merger requires approval by International Value Fund shareholders in order to be completed. Completion of the Merger of the Target Fund is not contingent upon completion of the International Value Fund merger.

MERGER SUMMARY (OBJECTIVES, STRATEGIES, RISKS, PERFORMANCE, EXPENSE, MANAGEMENT AND TAX INFORMATION)

The following section provides a comparison of the Funds’ investment objectives, principal investment strategies, fundamental investment policies, risks, performance records, and expenses. It also provides information about what the management and share class structure of the Acquiring Fund will be after the Merger. The information below is only a summary; for more detailed information, please see the rest of this prospectus/information statement and each Fund’s prospectus(es) and SAI. In this section, percentages of a Fund’s “net assets” are measured as percentages of net assets plus

borrowings for investment purposes. References to “we” in the principal investment strategy discussion for a Fund generally refer to the Manager or the sub-adviser.

WELLS FARGO DIVERSIFIED INTERNATIONAL FUND INTO WELLS FARGO INTERNATIONAL EQUITY FUND

SHARE CLASS INFORMATION

The following table illustrates the share class of the Acquiring Fund you will receive in exchange for your Target Fund shares as a result of the Merger.

|

|

|

If you own this class of shares of the

Wells Fargo Diversified International Fund:

|

You will receive this class of shares of the

Wells Fargo International Equity Fund1:

|

|

Class A

|

Class A

|

|

Class C

|

Class C

|

|

Class R6

|

Class R6

|

|

Administrator Class

|

Administrator Class

|

|

Institutional Class

|

Institutional Class

|

| 1. |

The Acquiring Fund also offers Class R shares. This class is not involved in the Merger. |

The Acquiring Fund shares you will receive as a result of the Merger will have the same dollar value as your Target Fund shares as of the close of business on the business day immediately prior to the Merger.

The procedures for buying, selling and exchanging shares of the Funds are identical. For additional information see the section entitled “Buying, Selling and Exchanging Fund Shares.” Additional information on how you can buy, sell or exchange shares of each Fund is available in the Funds’ prospectuses and SAI. In addition, the distribution policies for the Funds are the same.

INVESTMENT OBJECTIVE AND STRATEGY COMPARISON

The following section compares the investment objectives, principal investment strategies and fundamental investment policies of the Funds. The investment objectives of the Funds may be changed without shareholder approval.

The Funds’ investment objectives are identical in that both Funds seek long-term capital appreciation.

The Funds’ principal investment strategies are similar in that both Funds focus at least 80% of their net assets in equity securities of foreign issuers. The primary difference is that the Target Fund, under normal circumstances, invests up to 20% of its total assets in emerging market equity securities, whereas the Acquiring Fund, under normal circumstances, invests up to 30% of its total assets in emerging market equity securities. In addition, the Acquiring Fund’s principal investment strategy is to invest in securities of at least three different countries including the U.S.

|

|

|

Wells Fargo Diversified International Fund

|

Wells Fargo International Equity Fund

|

|

INVESTMENT OBJECTIVES

|

INVESTMENT OBJECTIVES

|

|

The Fund seeks long-term capital appreciation.

|

The Fund seeks long-term capital appreciation.

|

|

PRINCIPAL INVESTMENT STRATEGIES

|

PRINCIPAL INVESTMENT STRATEGIES

|

|

Under normal circumstances, we invest: at least 80% of the Fund’s net assets in equity securities of foreign issuers; and up to 20% of the Fund’s total assets in emerging market equity securities.

|

Under normal circumstances, we invest: at least 80% of the Fund’s net assets in equity securities of foreign issuers; up to 30% of the Fund’s total assets in emerging market equity securities; and in securities of at least three different countries including the U.S.

|

|

|

|

Wells Fargo Diversified International Fund

|

Wells Fargo International Equity Fund

|

|

We invest principally in the equity securities of foreign issuers through the use of three different styles of international equity management: an international growth style, subadvised by Artisan Partners Limited Partnership; an international value style, sub-advised by LSV Asset Management; and an international blend style, sub-advised by Wells Capital Management Incorporated. We invest primarily in developed countries, but may invest in emerging market countries and may invest in equity securities of any market capitalization. Furthermore, we may use futures, options or participation notes to manage risk or to enhance return. We reserve the right to hedge the portfolio’s foreign currency exposure by purchasing or selling currency futures and foreign currency forward contracts. However, under normal circumstances, we will not engage in extensive foreign currency hedging. |

The types of securities in which we normally invest include common stock, preferred stock, rights, warrants and American Depositary Receipts (ADRs). We consider equity securities of foreign issuers (or foreign securities) to be equity securities: (1) issued by companies with their principal place of business or principal office or both, as determined in our reasonable discretion, in a country other than the U.S.; or (2) issued by companies for which the principal securities trading market is a country other than the U.S. We may use futures or forward foreign currency contracts to manage risk or to enhance return. |

|

Artisan Partners Limited Partnership (Artisan Partners)

Artisan Partners employs a fundamental stock selection process to identify long-term growth opportunities to build a portfolio of non-U.S. growth companies of any market capitalization. Artisan Partners seeks to invest in companies within its preferred themes with sustainable growth characteristics at attractive valuations that do not fully reflect their long-term potential. Artisan Partners may sell a stock when Artisan Partners thinks the stock is approaching full valuation, the company exhibits deteriorating fundamentals, changing circumstances affect the original reasons for its purchase, or more attractive opportunities are identified. |

|

|

LSV Asset Management (LSV)

LSV invests in equity securities of foreign issuers which it believes are undervalued in the marketplace at the time of purchase and show recent positive signals, such as an appreciation in prices and increase in earnings. LSV believes that these securities have the potential to produce future returns if their future growth exceeds the market’s low expectations. LSV uses a quantitative investment model to make investment decisions for the Fund. The investment model ranks securities based on fundamental measures of value (such as the dividend yield) and indicators of near-term recovery (such as recent price appreciation). A stock is typically sold if the model indicates a decline in its ranking or if a stock’s relative portfolio weight has appreciated significantly (relative to the Fund’s benchmark). |

|

|

Wells Capital Management Incorporated (Wells Capital Management)

Wells Capital Management invests in equity securities of foreign issuers by using bottom-up stock selection, based on in-depth fundamental research as the cornerstone of its investment process. During each stage of the process, Wells Capital Management also considers the influence on the investment theses of top-down factors such as macroeconomic forecasts, real economic growth prospects, fiscal and monetary policy, currency issues, and demographic and political risks. The investment process seeks both growth and value opportunities. For growth investments, Wells Capital Management targets companies that it believes have strong business franchises, experienced and proven management, and accelerating cash flow growth rates. For value investments, Wells Capital Management targets companies that it believes are undervalued in the marketplace compared to their intrinsic value. Wells Capital Management may purchase securities across any market capitalization. Wells Capital Management may sell a stock if it achieves its investment objective for the position, if a stock’s fundamentals or price change significantly, if it changes its view of a country or sector, or if the stock no longer fits within the risk characteristics of the Fund’s portfolio. |

We use bottom-up stock selection, based on in-depth fundamental research as the cornerstone of our investment process. During each stage of the process, we also consider the influence on the investment theses of top-down factors such as macroeconomic forecasts, real economic growth prospects, fiscal and monetary policy, currency issues, and demographic and political risks. Sector and country weights result from rather than determine our stock-selection decisions. Our investment process seeks both growth and value opportunities. For growth investments, we target companies that we believe have strong business franchises, experienced and proven management, and accelerating cash flow growth rates. For value investments, we target companies that we believe are undervalued in the marketplace compared to their intrinsic value. Additionally, we seek to identify catalysts that will unlock value, which will then be recognized by the market. We may purchase securities across any market capitalization. We conduct ongoing review, research, and analysis of our portfolio holdings. We may sell a stock if it achieves our investment objective for the position, if a stock’s fundamentals or price change significantly, if we change our view of a country or sector, or if the stock no longer fits within the risk characteristics of the Fund’s portfolio. |

Except as noted above with respect to the Funds’ 80% policies, the fundamental investment policies of the Funds, which may only be changed with shareholder approval, are identical. For a comparative chart of the Funds’ fundamental investment policies, please see Exhibit B.

PRINCIPAL RISK COMPARISON

The principal risks of the Target Fund are similar, but not identical, to those of the Acquiring Fund due to the similarity of the Funds’ investment objectives and principal investment strategies, as noted above.

The table below compares the principal risk factors of the Target Fund with those of the Acquiring Fund. These risks are described in the section entitled “Risk Descriptions.”

|

|

|

Wells Fargo Diversified International Fund

|

Wells Fargo International Equity Fund

|

|

Derivatives Risk

|

Derivatives Risk

|

|

Emerging Markets Risk

|

Emerging Markets Risk

|

|

Equity Securities Risk

|

Equity Securities Risk

|

|

Foreign Currency Contracts Risk

|

Foreign Currency Contracts Risk

|

|

Foreign Investment Risk

|

Foreign Investment Risk

|

|

Futures Contracts Risk

|

Futures Contracts Risk

|

|

Growth/Value Investing Risk

|

Growth/Value Investing Risk

|

|

Management Risk

|

Management Risk

|

|

Market Risk

|

Market Risk

|

|

Multi-Manager Management Risk

|

Not subject to Multi-Manager Management Risk

|

|

Options Risk

|

Not subject to Options Risk

|

|

Participation Notes Risk

|

Not subject to Participation Notes Risk

|

|

Quantitative Model Risk

|

Not subject to Quantitative Model Risk

|

|

Smaller Company Securities Risk

|

Smaller Company Securities Risk

|

The Funds have other investment policies, practices and restrictions which, together with their related risks, are set forth in the Funds’ prospectuses and SAI.

FUND PERFORMANCE COMPARISON

The following bar charts and tables illustrate how each Fund’s returns have varied from year to year and compare each Fund’s returns with those of one or more broad-based securities indexes. Past performance (before and after taxes) is not necessarily an indication of future results. Current month-end performance information is available for the Funds on the Wells Fargo Funds website at wfam.com.

Calendar Year Total Returns for Class A Shares (%) for the Wells Fargo Diversified International Fund

|

|

|

|

Highest Quarter: 3rd Quarter 2010

|

+16.31%

|

|

Lowest Quarter: 3rd Quarter 2011

|

-20.73%

|

|

Year-to-date total return as of September 30, 2020 is -9.98%

|

|

|

|

|

|

|

|

Average Annual Total Returns for the periods ended 12/31/2019 (returns reflect applicable sales charges)

|

|

|

Inception Date of Share Class

|

1 Year

|

5 Year

|

10 Year

|

|

Class A (before taxes)

|

9/24/1997

|

14.38%

|

3.67%

|

4.93%

|

|

Class A (after taxes on distributions)

|

9/24/1997

|

14.08%

|

3.38%

|

4.60%

|

|

Class A (after taxes on distributions and the sale of Fund Shares)

|

9/24/1997

|

9.10%

|

2.98%

|

4.05%

|

|

Class C (before taxes)

|

4/1/1998

|

19.37%

|

4.12%

|

4.76%

|

|

Class R6 (before taxes)1

|

9/30/2015

|

21.84%

|

5.34%

|

5.87%

|

|

Administrator Class (before taxes)

|

11/8/1999

|

21.39%

|

5.02%

|

5.71%

|

|

Institutional Class (before taxes)

|

8/31/2006

|

21.72%

|

5.30%

|

5.95%

|

|

MSCI EAFE Index (Net) (reflects no deduction for fees, expenses, or taxes)

|

|

22.01%

|

5.67%

|

5.50%

|

| 1. |

Historical performance shown for the Class R6 shares prior to their inception reflects the performance of the Administrator Class shares, and includes the higher expenses applicable to Administrator Class shares. If these expenses had not been included, returns for Class R6 shares would be higher. |

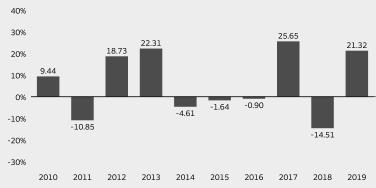

Calendar Year Total Returns for Class A Shares (%) for the Wells Fargo International Equity Fund

|

|

|

|

Highest Quarter: 3rd Quarter 2010

|

+17.95%

|

|

Lowest Quarter: 3rd Quarter 2011

|

-21.95%

|

|

Year-to-date total return as of September 30, 2020 is -10.29%

|

|

|

|

|

|

|

|

Average Annual Total Returns for the periods ended 12/31/2019 (returns reflect applicable sales charges)1

|

|

|

Inception Date of Share Class

|

1 Year

|

5 Year

|

10 Year

|

|

Class A (before taxes)

|

1/20/1998

|

8.42%

|

3.52%

|

4.36%

|

|

Class A (after taxes on distributions)

|

1/20/1998

|

8.05%

|

2.98%

|

3.88%

|

|

Class A (after taxes on distributions and the sale of Fund Shares)

|

1/20/1998

|

5.54%

|

2.77%

|

3.52%

|

|

Class C (before taxes)

|

3/6/1998

|

13.07%

|

3.97%

|

4.18%

|

|

Class R6 (before taxes)2

|

9/30/2015

|

15.39%

|

5.05%

|

5.23%

|

|

Administrator Class (before taxes)3

|

7/16/2010

|

15.09%

|

4.76%

|

4.99%

|

|

Institutional Class (before taxes)

|

3/9/1998

|

15.36%

|

5.03%

|

5.24%

|

|

MSCI ACWI ex USA Index (Net) (reflects no deduction for fees, expenses, or taxes)

|

|

21.51%

|

5.51%

|

4.97%

|

|

MSCI ACWI ex USA Value Index (Net) (reflects no deduction for fees, expenses, or taxes)

|

|

15.71%

|

3.65%

|

3.64%

|

| 1. |

Historical performance shown prior to July 19, 2010 is based on the performance of the Fund’s predecessor, Evergreen International Equity Fund. |

| 2. |

Historical performance shown for Class R6 shares prior to their inception reflects the performance of Institutional Class shares and includes the higher expenses applicable to Institutional Class shares. If these expenses had not been included, returns for Class R6 shares would be higher. |

| 3. |

Historical performance shown for the Administrator Class shares prior to their inception reflects the performance of the Institutional Class shares and has been adjusted to reflect the higher expenses applicable to the Administrator Class shares. |

SHAREHOLDER FEE AND FUND EXPENSE COMPARISON

This section compares the fees and expenses you pay if you buy, hold, and sell shares of the Target Fund and the Acquiring Fund.

For information about the share class of the Acquiring Fund that you will receive in connection with the Merger, please see the section entitled “Share Class Information” above.

The following table entitled “Shareholder Fees” allows you to compare the maximum sales charges of the Funds and includes a Pro Forma column that shows you what the sales charges will be assuming the Merger takes place. The sales charges for each class of shares of the Target Fund are identical to those of the class of shares of the Acquiring Fund. The Target Fund shareholders will not pay any front-end or deferred sales charges in connection with the Merger.

You may qualify for sales charge discounts if you and your family invest, or agree to invest in the future, at least $50,000 in the aggregate in specified classes of Wells Fargo Funds. More information about these and other discounts is available in the “Reductions and Waivers of Sales Charges” section of this prospectus/information statement and from your financial professional and in the Funds’ prospectuses.

The following table entitled “Annual Fund Operating Expenses” allows you to compare the annual operating expenses of the Funds. The total annual fund operating expenses for both Funds set forth in the following table are based on the actual expenses incurred for each Fund’s fiscal year ended October 31, 2019. The pro forma expense column shows you what the total annual fund operating expenses (before and after waiver) would have been for the Acquiring Fund for the twelve-month period ended April 30, 2020, assuming the Merger had taken place at the beginning of that period. The pro forma expenses below do not reflect the completion of the International Value Fund merger described earlier in the section entitled “Overview”. Should the Merger of the Target Fund and the International Value Fund merger occur, the combined pro forma expenses are not expected to be materially different than the expenses shown below. As noted earlier, the International Value Fund merger will not occur unless approved by International Value Fund shareholders. The Merger of the Target Fund is not contingent on consummation of the International Value Fund merger.

|

|

|

|

|

Shareholder Fees (fees paid directly from your investment)

|

|

|

Wells Fargo Diversified International Fund (Pre-Merger) |

Wells Fargo International Equity Fund (Pre-Merger) |

Wells Fargo International Equity Fund (Pro Forma) |

|

Class A

|

|

|

|

|

Maximum sales charge (load) imposed on purchases (as a percentage of the offering price)

|

5.75%

|

5.75%

|

5.75%

|

|

Maximum deferred sales charge (load) (as a percentage of the offering price)

|

None1

|

None1

|

None1

|

|

Class C

|

|

|

|

|

Maximum sales charge (load) imposed on purchases (as a percentage of the offering price)

|

None

|

None

|

None

|

|

Maximum deferred sales charge (load) (as a percentage of the offering price)

|

1.00%

|

1.00%

|

1.00%

|

|

Class R6

|

|

|

|

|

Maximum sales charge (load) imposed on purchases (as a percentage of the offering price)

|

None

|

None

|

None

|

|

Maximum deferred sales charge (load) (as a percentage of the offering price)

|

None

|

None

|

None

|

|

Administrator Class

|

|

|

|

|

Maximum sales charge (load) imposed on purchases (as a percentage of the offering price)

|

None

|

None

|

None

|

|

Maximum deferred sales charge (load) (as a percentage of the offering price)

|

None

|

None

|

None

|

|

Institutional Class

|

|

|

|

|

|

|

|

|

Shareholder Fees (fees paid directly from your investment)

|

|

|

Wells Fargo Diversified International Fund (Pre-Merger) |

Wells Fargo International Equity Fund (Pre-Merger) |

Wells Fargo International Equity Fund (Pro Forma) |

|

Maximum sales charge (load) imposed on purchases (as a percentage of the offering price)

|

None

|

None

|

None

|

|

Maximum deferred sales charge (load) (as a percentage of the offering price)

|

None

|

None

|

None

|

| 1. |

Investments of $1 million or more are not subject to a front-end sales charge, but will be subject to a deferred sales charge of 1.00% if you sell the shares within eighteen months from the date of purchase. |

|

|

|

|

|

Annual Fund Operating Expenses (expenses that you pay each year as a percentage of the value of your investment)

|

|

|

Wells Fargo Diversified International Fund (Pre-Merger)

|

Wells Fargo International Equity Fund (Pre-Merger)

|

Wells Fargo International Equity Fund (Pro Forma)

|

|

Class A

|

|

|

|

|

Management Fees

|

0.85%

|

0.85%

|

0.85%

|

|

Distribution (12b-1) Fees

|

0.00%

|

0.00%

|

0.00%

|

|

Other Expenses

|

0.92%

|

0.59%

|

0.59%

|

|

Acquired Fund Fees and Expenses

|

0.00%

|

0.01%

|

0.00%

|

|

Total Annual Fund Operating Expenses

|

1.77%

|

1.45%

|

1.44%

|

|

Fee Waivers

|

(0.42)%

|

(0.30)%

|

(0.30)%

|

|

Total Annual Fund Operating Expenses After Fee Waivers1

|

1.35%

|

1.15%

|

1.14%

|

|

Class C

|

|

|

|

|

Management Fees

|

0.85%

|

0.85%

|

0.85%

|

|

Distribution (12b-1) Fees

|

0.75%

|

0.75%

|

0.75%

|

|

Other Expenses

|

0.92%

|

0.59%

|

0.59%

|

|

Acquired Fund Fees and Expenses

|

0.00%

|

0.01%

|

0.00%

|

|

Total Annual Fund Operating Expenses

|

2.52%

|

2.20%

|

2.19%

|

|

Fee Waivers

|

(0.42)%

|

(0.30)%

|

(0.30)%

|

|

Total Annual Fund Operating Expenses After Fee Waivers1

|

2.10%

|

1.90%

|

1.89%

|

|

Class R6

|

|

|

|

|

Management Fees

|

0.85%

|

0.85%

|

0.85%

|

|

Distribution (12b-1) Fees

|

0.00%

|

0.00%

|

0.00%

|

|

Other Expenses

|

0.49%

|

0.16%

|

0.16%

|

|

Acquired Fund Fees and Expenses

|

0.00%

|

0.01%

|

0.00%

|

|

Total Annual Fund Operating Expenses

|

1.34%

|

1.02%

|

1.01%

|

|

Fee Waivers

|

(0.45)%

|

(0.22)%

|

(0.22)%

|

|

Total Annual Fund Operating Expenses After Fee Waivers1

|

0.89%

|

0.80%

|

0.79%

|

|

Administrator Class

|

|

|

|

|

Management Fees

|

0.85%

|

0.85%

|

0.85%

|

|

Distribution (12b-1) Fees

|

0.00%

|

0.00%

|

0.00%

|

|

Other Expenses

|

0.84%

|

0.51%

|

0.51%

|

|

Acquired Fund Fees and Expenses

|

0.00%

|

0.01%

|

0.00%

|

|

Total Annual Fund Operating Expenses

|

1.69%

|

1.37%

|

1.36%

|

|

Fee Waivers

|

(0.44)%

|

(0.22)%

|

(0.22)%

|

|

Total Annual Fund Operating Expenses After Fee Waivers1

|

1.25%

|

1.15%

|

1.14%

|

|

|

|

|

|

Annual Fund Operating Expenses (expenses that you pay each year as a percentage of the value of your investment)

|

|

|

Wells Fargo Diversified International Fund (Pre-Merger)

|

Wells Fargo International Equity Fund (Pre-Merger)

|

Wells Fargo International Equity Fund (Pro Forma)

|

|

Institutional Class

|

|

|

|

|

Management Fees

|

0.85%

|

0.85%

|

0.85%

|

|

Distribution (12b-1) Fees

|

0.00%

|

0.00%

|

0.00%

|

|

Other Expenses

|

0.59%

|

0.26%

|

0.26%

|

|

Acquired Fund Fees and Expenses

|

0.00%

|

0.01%

|

0.00%

|

|

Total Annual Fund Operating Expenses

|

1.44%

|

1.12%

|

1.11%

|

|

Fee Waivers

|

(0.45)%

|

(0.27)%

|

(0.27)%

|

|

Total Annual Fund Operating Expenses After Fee Waivers1

|

0.99%

|

0.85%

|

0.84%

|

| 1. |

Effective upon the closing of the Merger, the Manager has contractually committed through February 28, 2022, to waive fees and/or reimburse expenses to the extent necessary to cap the Fund’s Total Annual Fund Operating Expenses After Fee Waivers at the amounts shown above. Brokerage commissions, stamp duty fees, interest, taxes, acquired fund fees and expenses (if any), and extraordinary expenses are excluded from the expense cap. Prior to or after the commitment expiration date, the cap may be increased or the commitment to maintain the cap may be terminated only with the approval of the Funds Trust Board. |

Examples of Fund Expenses

The examples below are intended to help you compare the costs of investing in the Target Fund with the costs of investing in the Acquiring Fund, both before and after the Merger, and are for illustration only. The examples assume a $10,000 initial investment, 5% annual total return, and that operating expenses remain the same, as in the tables above. To the extent that the Manager is waiving fees or reimbursing expenses, the examples assume that such waivers or reimbursements will only be in place through the date noted above. Although your actual costs may be higher or lower, based on these assumptions, your costs would be:

|

|

|

|

|

|

Wells Fargo Diversified International Fund (Pre-Merger)

|

|

Assuming you sold your shares, you would pay:

|

After 1 Year

|

After 3 Years

|

After 5 Years

|

After 10 Years

|

|

Class A

|

$705

|

$1,062

|

$1,442

|

$2,506

|

|

Class C

|

$313

|

$745

|

$1,303

|

$2,824

|

|

Class R6

|

$91

|

$380

|

$691

|

$1,573

|

|

Administrator Class

|

$127

|

$490

|

$876

|

$1,961

|

|

Institutional Class

|

$101

|

$411

|

$744

|

$1,685

|

|

Assuming you held your shares, you would pay:

|

|

|

|

|

|

Class C

|

$213

|

$745

|

$1,303

|

$2,824

|

|

|

|

|

|

|

Wells Fargo International Equity Fund (Pre-Merger)

|

|

Assuming you sold your shares, you would pay:

|

After 1 year

|

After 3 Years

|

After 5 Years

|

After 10 Years

|

|

Class A

|

$685

|

$950

|

$1,266

|

$2,160

|

|

Class C

|

$293

|

$629

|

$1,123

|

$2,486

|

|

Class R6

|

$82

|

$280

|

$519

|

$1,207

|

|

Administrator Class

|

$117

|

$389

|

$707

|

$1,607

|

|

Institutional Class

|

$87

|

$301

|

$563

|

$1,313

|

|

Assuming you held your shares, you would pay:

|

|

|

|

|

|

Class C

|

$193

|

$629

|

$1,123

|

$2,486

|

|

|

|

|

|

|

Wells Fargo International Equity Fund (Pro Forma)

|

|

Assuming you sold your shares, you would pay:

|

After 1 year

|

After 3 Years

|

After 5 Years

|

After 10 Years

|

|

Class A

|

$685

|

$947

|

$1,261

|

$2,150

|

|

|

|

|

|

|

Wells Fargo International Equity Fund (Pro Forma)

|

|

Assuming you sold your shares, you would pay:

|

After 1 year

|

After 3 Years

|

After 5 Years

|

After 10 Years

|

|

Class C

|

$292

|

$626

|

$1,118

|

$2,475

|

|

Class R6

|

$81

|

$277

|

$514

|

$1,195

|

|

Administrator Class

|

$116

|

$386

|

$702

|

$1,596

|

|

Institutional Class

|

$86

|

$298

|

$558

|

$1,302

|

|

Assuming you held your shares, you would pay:

|

|

|

|

|

|

Class C

|

$192

|

$626

|

$1,118

|

$2,475

|

Each Fund has a shareholder servicing fee of up to 0.25% for Class A, Class C and Administrator Class shares. Class R6 and Institutional Class shares do not pay a shareholder servicing fee.

FUND MANAGEMENT INFORMATION

The following table identifies the manager and sub-adviser for the Acquiring Fund. The manager and sub-adviser of the Target Fund and Acquiring Fund are the same. Further information about the management of the Acquiring Fund can be found under the section entitled “Management of the Funds.”

|

|

|

Wells Fargo International Equity Fund

|

|

Investment Manager

|

Wells Fargo Funds Management, LLC

|

|

Investment Sub-adviser

|

Wells Capital Management Incorporated

|

|

Portfolio Manager, Title/Managed Since

|

Venkateshwar (Venk) Lal, Portfolio Manager / 2017

Dale A. Winner, CFA, Portfolio Manager / 2012

|

TAX INFORMATION

It is expected that the Merger will qualify as a tax-free “reorganization” for U.S. federal income tax purposes under Section 368(a) of the Internal Revenue Code of 1986, as amended. A receipt of an opinion substantially to that effect from Troutman Pepper Hamilton Sanders LLP, tax counsel to the Acquiring Fund, is a condition to the obligation of the Funds to consummate the Merger. As a tax-free reorganization, the Merger will not be taxable to the Acquiring Fund, the Target Fund or their shareholders for U.S. federal income tax purposes. Even though the Merger is expected to be tax-free, because the Merger will end the tax year of the Target Fund, the Merger may accelerate taxable distributions from the Target Fund to its shareholders.

The cost basis and holding period of the Target Fund shares will carry over to the shares of the Acquiring Fund you receive as a result of the Merger, in each case for U.S. federal income tax purposes. At any time prior to the consummation of the Merger, a shareholder may redeem shares, usually resulting in recognition of a gain or loss for U.S. federal income tax purposes to the redeeming shareholder if the shareholder holds the shares in a taxable account.

For net capital losses realized in taxable years beginning before January 1, 2011, U.S. federal income tax law permits registered investment companies (“RICs”), such as the Funds, to carry forward a net capital loss to offset its capital gain, if any, realized during the eight years following the year of the loss. For net capital losses realized in taxable years beginning on or after January 1, 2011, a Fund is permitted to carry forward a net capital loss to offset its capital gain indefinitely. The Target Fund may be presently entitled to significant net capital loss carryforwards for U.S. federal income tax purposes, as detailed in “Material U.S. Federal Income Tax Consequences of the Merger.”

Before the Closing Date, the Target Fund expects to sell a substantial portion of its portfolio securities in connection with repositioning its portfolio in anticipation of the Merger. These transactions will result in additional transaction costs to the Target Fund and may result in increased taxable distributions to shareholders of the Target Fund. In addition, it is expected that the Acquiring Fund may experience transaction costs immediately following the Merger in connection with reacquiring certain securities previously held by the Target Fund but which are unable to be transferred directly to the Acquiring Fund due to certain jurisdictional restrictions on transfers. Potential transaction costs are estimated to be approximately $122K. This estimate of transaction costs is predicated on an assumption that the Target Fund is expected to sell approximately 64% of its portfolio. Transaction costs are dependent on market conditions and actual securities traded; costs could be higher or lower for securities based on liquidity. We expect the transition to occur over a two week period to take advantage of market liquidity and minimize trading costs. Understanding that there is a cost to trading, the

portfolio management teams and traders will make every effort to minimize transaction costs. These potential transactions are estimated to result in possible net realized gains of $4.8 million. However, given the Fund’s current undistributed losses, these gains may be able to be offset. The actual tax impact of such sales will depend on the difference between the price at which such portfolio assets are sold and the Target Fund’s basis in such assets. Any net realized capital gain from sales that occur prior to the Merger will be distributed to the Target Fund’s shareholders as capital gain distributions (to the extent of the excess of net long-term capital gain over net short-term capital loss) and/or ordinary dividends (to the extent of the excess of net short-term capital gain over net long-term capital loss) during or with respect to the year of sale (after reduction by any available capital loss carryforwards), and such distributions will be taxable to shareholders. This portfolio turnover would be in addition to the portfolio turnover that would be experienced by the Acquiring Fund following the Merger in connection with its normal investment operations. In addition, it is expected that the Target Fund may hold a larger amount of cash during this period in connection with repositioning its portfolio. As a result, the Fund may not be invested pursuant to its principal investment strategies.

Certain other U.S. federal income tax consequences are discussed below under “Material U.S. Federal Income Tax Consequences of the Merger.”

RISK DESCRIPTIONS

An investment in the Acquiring Fund is subject to certain risks. There is no assurance that the return of the Acquiring Fund will be positive or that the Acquiring Fund will meet its investment objective. An investment in the Acquiring Fund is not a deposit of Wells Fargo Bank, N.A. or its affiliates; is not insured, or guaranteed by the Federal Deposit Insurance Corporation or any other government agency; and is subject to investment risks, including possible loss of your original investment. Like most investments, your investment in the Acquiring Fund could result in a loss of money. The following provides additional information regarding the various risks (in alphabetical order) of investing in the Acquiring Fund as referenced in the section entitled “Merger Summary - Principal Risk Comparison”.

Derivatives Risk. The use of derivatives, such as futures, options and swap agreements, presents risks different from, and possibly greater than, the risks associated with investing directly in traditional securities. The use of derivatives can lead to losses because of adverse movements in the price or value of the derivatives’ underlying assets, indexes or rates and the derivatives themselves, which may be magnified by certain features of the derivatives. These risks are heightened when derivatives are used to enhance a Fund’s return or as a substitute for a position or security, rather than solely to hedge (or mitigate) the risk of a position or security held by the Fund. The success of a derivative strategy will be affected by the portfolio manager’s ability to assess and predict market or economic developments and their impact on the derivatives’ underlying assets, indexes or reference rates, as well as the derivatives themselves. Certain derivative instruments may become illiquid and, as a result, may be difficult to sell when the portfolio manager believes it would be appropriate to do so. Certain derivatives create leverage, which can magnify the impact of a decline in the value of their underlying assets, indexes or reference rates, and increase the volatility of the Fund’s net asset value. Certain derivatives (e.g., over-the-counter swaps) are also subject to the risk that the counterparty to the derivative contract will be unwilling or unable to fulfill its contractual obligations, which may cause a Fund to lose money, suffer delays or incur costs arising from holding or selling an underlying asset. Changes in laws or regulations may make the use of derivatives more costly, may limit the availability of derivatives, or may otherwise adversely affect the use, value or performance of derivatives.

Emerging Markets Risk. Emerging market securities typically present even greater exposure to the risks described under “Foreign Investment Risk” and may be particularly sensitive to global economic conditions. For example, emerging market countries are typically more dependent on exports and are, therefore, more vulnerable to recessions in other countries. Emerging markets tend to have less developed legal and financial systems and a smaller market capitalization than markets in developed countries. Some emerging markets are subject to greater political instability. Additionally, emerging markets may have more volatile currencies and be more sensitive than developed markets to a variety of economic factors, including inflation. Emerging market securities are also typically less liquid than securities of developed countries and could be difficult to sell, particularly during a market downturn.

Equity Securities Risk. The values of equity securities may experience periods of substantial price volatility and may decline significantly over short time periods. In general, the values of equity securities are more volatile than those of debt securities. Equity securities fluctuate in value and price in response to factors specific to the issuer of the security, such as management performance, financial condition, and market demand for the issuer’s products or services, as well as factors unrelated to the fundamental condition of the issuer, including general market, economic and political conditions. Investing in equity securities poses risks specific to an issuer, as well as to the particular type of company

issuing the equity securities. For example, investing in the equity securities of small- or mid-capitalization companies can involve greater risk than is customarily associated with investing in stocks of larger, more-established companies. Different parts of a market, industry and sector may react differently to adverse issuer, market, regulatory, political, and economic developments. Negative news or a poor outlook for a particular industry can cause the share prices of securities of companies in that industry to decline.

Foreign Currency Contracts Risk. A Fund that enters into forwards or other foreign currency contracts, which are a type of derivative, is subject to the risk that the portfolio manager may be incorrect in his or her judgment of future exchange rate changes. The Fund’s gains from positions in foreign currency contracts may accelerate and/or lead to recharacterization of the Fund’s income or gains and its distributions to shareholders. The Fund’s losses from such positions may also lead to recharacterization of the Fund’s income and its distributions to shareholders and may cause a return of capital to Fund shareholders.

Foreign Investment Risk. Foreign investments may be subject to lower liquidity, greater price volatility and risks related to adverse political, regulatory, market or economic developments. Foreign companies may be subject to significantly higher levels of taxation than U.S. companies, including potentially confiscatory levels of taxation, thereby reducing the earnings potential of such foreign companies. Foreign investments may involve exposure to changes in foreign currency exchange rates. Such changes may reduce the U.S. dollar value of the investments. Foreign investments may be subject to additional risks, such as potentially higher withholding and other taxes, and may also be subject to greater trade settlement, custodial, and other operational risks than domestic investments. Certain foreign markets may also be characterized by less stringent investor protection and disclosure standards.

Futures Contracts Risk. A Fund that uses futures contracts, which are a type of derivative, is subject to the risk of loss caused by unanticipated market movements. In addition, there may at times be an imperfect correlation between the movement in the prices of futures contracts and the value of their underlying instruments or indexes, and there may at times not be a liquid secondary market for certain futures contracts.

Growth/Value Investing Risk. Securities that exhibit certain characteristics, such as growth characteristics or value characteristics, tend to perform differently and shift into and out of favor with investors depending on changes in market and economic sentiment and conditions. As a result, a Fund’s performance may at times be worse than the performance of other mutual funds that invest more broadly or in securities that exhibit different characteristics.

Management Risk. Investment decisions, techniques, analyses or models implemented by a Fund’s manager or sub-adviser in seeking to achieve the Fund’s investment objective may not produce the returns expected, may cause the Fund’s shares to lose value or may cause the Fund to underperform other funds with similar investment objectives.

Market Risk. The values of, and/or the income generated by, securities held by a Fund may decline due to general market conditions or other factors, including those directly involving the issuers of such securities. Securities markets are volatile and may decline significantly in response to adverse issuer, regulatory, political, or economic developments. Different sectors of the market and different security types may react differently to such developments. Political, geopolitical, natural and other events, including war, terrorism, trade disputes, government shutdowns, market closures, natural and environmental disasters, epidemics, pandemics and other public health crises and related events have led, and in the future may lead, to economic uncertainty, decreased economic activity, increased market volatility and other disruptive effects on U.S. and global economies and markets. Such events may have significant adverse direct or indirect effects on a Fund and its investments. In addition, economies and financial markets throughout the world are becoming increasingly interconnected, which increases the likelihood that events or conditions in one country or region will adversely impact markets or issuers in other countries or regions.

Smaller Company Securities Risk. Securities of companies with smaller market capitalizations tend to be more volatile and less liquid than those of larger companies. Smaller companies may have no or relatively short operating histories, limited financial resources or may have recently become public companies. Some of these companies have aggressive capital structures, including high debt levels, or are involved in rapidly growing or changing industries and/or new technologies.

MANAGEMENT OF THE FUNDS

The following provides additional information regarding the manager and sub-adviser of the Acquiring Fund as referenced in the section entitled “Merger Summary” and also provides expenses related to the operation of the

Acquiring Fund. The Manager and sub-adviser of the Target Fund are the same as the Manager and sub-adviser of its Acquiring Fund.

MANAGER

Funds Management, headquartered at 525 Market Street, San Francisco, CA 94105, provides advisory and fund-level administrative services to the Acquiring Fund pursuant to an investment management agreement. Funds Management is a wholly owned subsidiary of Wells Fargo & Company, a publicly traded diversified financial services company that provides banking, insurance, investment, mortgage and consumer financial services. Funds Management is a registered investment adviser that provides advisory services for registered mutual funds, closed-end funds and other funds and accounts. Funds Management is a part of Wells Fargo Asset Management, the trade name used by the asset management businesses of Wells Fargo & Company.

SUB-ADVISER

Wells Capital Management Incorporated, an affiliate of Funds Management and an indirect wholly owned subsidiary of Wells Fargo, located at 525 Market Street, San Francisco, California 94105, is the sub-adviser for the Acquiring Fund. Wells Capital is responsible for the day-to-day investment management activities of the Acquiring Fund. Wells Capital is a registered investment adviser that provides investment advisory services for registered mutual funds, company retirement plans, foundations, endowments, trust companies, and high net-worth individuals.

MANAGEMENT AND SUB-ADVISORY FEES

As compensation for the investment management services Funds Management provides to both the Target Fund and the Acquiring Fund, Funds Management is entitled to receive a monthly fee at the annual rates indicated below, as a percentage of both the Target Fund’s and the Acquiring Fund’s average daily net assets. As noted below, the management fee schedule for the Target Fund is identical to the management fee schedule for the Acquiring Fund.

|

|

|

|

Fund

|

|

Fee

|

|

Wells Fargo Diversified International Fund

Wells Fargo International Equity Fund

|

First $500M

Next $500M

Next $1B

Next $2B

Next $1B

Next $5B

Over $10B |

0.850%

0.800%

0.750%

0.725%

0.700%

0.690%

0.680% |

For providing investment sub-advisory services to both the Target Fund and the Acquiring Fund, Wells Capital Management is entitled to receive monthly fees at the annual rates indicated below, which are stated as a percentage of both the Target Fund and the Acquiring Fund’s average daily net assets. Wells Capital Management is compensated for its services by Funds Management from the fees Funds Management receives for its services as investment manager to both the Target Fund and the Acquiring Fund.

|

|

|

|

|

Fund

|

Sub-Adviser

|

Fee

|

|

|

Wells Fargo Diversified International Fund

|

Artisan Partners

|

First $50M

Next $200M

Over $250M

|

0.800%

0.600%

0.500%

|

|

|

LSV

|

First $150M

Next $350M

Next $250M

Next $250M

Over $1B

|

0.350%

0.400%

0.350%

0.325%

0.300%

|

|

|

Wells Capital Management

|

First $200M

Over $200M

|

0.450%

0.400%

|

|

Wells Fargo International Equity Fund

|

Wells Capital Management

|

First $200M

Over $200M

|

0.450%

0.400%

|

For the Acquiring Fund’s most recent fiscal year, the management fee paid to Funds Management, net of any applicable waivers and reimbursement was as follows:

|

|

|

Fund

|

As a % of average daily net assets

|

|

Wells Fargo International Equity Fund

|

0.85%

|

For a discussion regarding the basis for the approval of the Acquiring Fund’s Management Agreement and Sub-Advisory Agreement by the Board, please see the shareholder report for the six months ended October 31, 2019.

MULTI-MANAGER ARRANGEMENT

The Funds and Funds Management have obtained an exemptive order from the SEC that permits Funds Management, subject to the approval of the Funds Trust Board, to select certain sub-advisers and enter into or amend sub-advisory agreements with them, without obtaining shareholder approval. The SEC order extends to sub-advisers that are not otherwise affiliated with Funds Management or the Funds, as well as sub-advisers that are wholly-owned subsidiaries of Funds Management or of a company that wholly owns Funds Management (“Multi-Manager Sub-Advisers”).

Pursuant to the order, Funds Management, with the approval of the Funds Trust Board, may hire or replace Multi-Manager Sub-Advisers for each Fund that is eligible to rely on the order. Funds Management, subject to the Funds Trust Board’s oversight, has the responsibility to oversee Multi-Manager Sub-Advisers and to recommend their hiring, termination and replacement. If a new sub-adviser is hired for a Fund pursuant to the order, the Fund is required to notify shareholders within 90 days. The Funds are not required to disclose the individual fees that Funds Management pays to a Multi-Manager Sub-Adviser.

ADDITIONAL INFORMATION REGARDING THE EXPENSES OF THE FUNDS

The Acquiring Fund pays Funds Management a class-level administrative fee. The class-level administrative fee is applied on a class-by-class basis and at rates that differ among classes. Funds Management provides or obtains transfer agency services for the Acquiring Fund as part of its class-level administrative service, and the administrative fee paid on a class-by-class basis is intended in part to compensate Funds Management for providing or obtaining those transfer agency services. The Acquiring Fund’s SAI contains more information regarding the administration and transfer agency service fees borne by the Acquiring Fund.

MERGER INFORMATION

BOARD CONSIDERATIONS

At a regular Board meeting held on November 17, 19-20, 2020 (the “Meeting”), the Board, all of the members of which are Independent Trustees, considered the Merger. In advance of the Meeting, Funds Management provided extensive background materials and analyses to the Board. These materials included the rationale for the proposed Merger, as well as information on the investment objectives and principal investment strategies of both the Target Fund and the Acquiring Fund; their respective fee arrangements, operating expense ratios, asset sizes, risk profiles and investment performance; and analyses of certain tax information, transaction cost information and the projected benefits of the Merger. Representatives of Funds Management presented these materials and responded to questions at the Meeting.

The Independent Trustees reviewed and discussed these materials and analyses with Funds Management and among themselves. The Independent Trustees were assisted in their evaluation of the Merger by independent legal counsel, with whom they met separately and from whom they received separate legal advice. After such review, discussion and evaluation, the Board unanimously approved the Plan for the Merger at the Meeting. In its deliberations, the Board considered that some of the projected benefits of the Merger would accrue to Funds Management and its affiliates, in addition to those that would accrue to the shareholders of the Target Fund and the Acquiring Fund. In this regard, the Board noted that Funds Management and its affiliates are likely to benefit from the elimination of duplicative expenses and the reduction of other associated operational costs resulting from the consolidation of funds with identical objectives and similar strategies. The Board took into account these benefits, among others, in the context of focusing on Fund shareholder benefits and evaluating the Merger overall, and determined that merging the Target Fund into the Acquiring Fund would be in the best interests of both Funds. The Board further determined that the interests of the shareholders of both the Target Fund and the Acquiring Fund would not be diluted as a result of the Merger.

In approving the Plan, the Board did not identify any particular information or consideration that was all-important or controlling, and each Trustee likely attributed different weights to various factors.

The Board approved the Merger for the following reasons:

Overall Basis For Approval. The Board considered a number of factors in determining that the Merger would be in the best interests of the Target Fund. After taking into account the Funds’ identical investment objectives and the extent to which their strategies overlap, the Board considered that the Merger would result in a fund that has experienced consistent outflows being merged into a fund with stronger short-term performance and lower gross and net expense ratios for each share class. The Board also considered Funds Management’s view that the Acquiring Fund is well positioned to perform in light of anticipated market style shifts. The Board also reviewed Funds Management’s assessment of other possible options for the Target Fund, including liquidation and whether there were other viable merger candidates among the Wells Fargo Fund family.

Portfolio Management. The Board considered information regarding the qualifications, background, tenure and responsibilities of the personnel who will be primarily responsible for the day-to-day portfolio management of the Acquiring Fund after the Merger. The Board considered that the Target Fund has three investment sub-advisers, including Wells Capital Management, an affiliate of Funds Management, and that Wells Capital Management is the only investment sub-adviser for the Acquiring Fund.

The Board considered that the investment objectives of the Target Fund and Acquiring Fund – to seek long-term capital appreciation – are identical. The Board considered the principal investment strategy similarities and differences described below. To the extent the principal investment strategies of the Acquiring Fund differ from those of the Target Fund, as described in the section entitled “Merger Summary (Objectives, Strategies, Risks, Performance, Expense, Management and Tax Information) – Investment Objective and Strategy Comparison” above and under Compatible Objectives and Investment Strategies below, the Board considered those differences as part of its overall determination that participating in the Merger would be in the best interests of the Target Fund.

The Board noted that the Acquiring Fund’s contractual management fee schedule and effective management fee rate are equal to those of the Target Fund, and that Funds Management agreed (contingent upon the closing of the Merger) to waive fees and/or reimburse expenses for each share class of the Acquiring Fund through February 28, 2022, to ensure that net expenses paid by each share class of the Acquiring Fund after the Merger are lower than those currently paid by each corresponding share class of the Target Fund, and that, thereafter, such a cap may not be raised or removed without Board approval.

The Board considered that the contractual sub-advisory fee rate schedule with respect to the Acquiring Fund provides for a lower effective sub-advisory fee rate than the aggregate sub-advisory fee rate paid in connection with the Target Fund, and that the effective sub-advisory fee rate to be paid in connection with the management of the Acquiring Fund after the Merger will be lower than that currently paid in connection with the management of the Target Fund. The Board noted that, given the affiliation between Wells Capital Management and Funds Management, the overall compensation retained by Funds Management and its affiliates on a combined basis will exceed that retained under the current arrangement with LSV Asset Management and Artisan Partners Limited Partnership serving as investment sub-advisers to the Target Fund, alongside Wells Capital Management.

Greater Potential Economies Of Scale And Viability. The Board also considered that shareholders of both the Target Fund and the Acquiring Fund may benefit from the potential for greater economies of scale and viability in the future by consolidating the Target Fund into a fund with a higher Morningstar rating and better short-term performance that is expected by Funds Management to have greater potential for asset growth and viability following the Merger.

Compatible Objectives And Investment Strategies. As described in the section entitled “Merger Summary (Objectives, Strategies, Risks, Performance, Expense, Management and Tax Information) - Investment Objective and Strategy Comparison” above, the Board considered that the investment objective of the Target Fund – to seek long-term capital appreciation – is identical to that of the Acquiring Fund.

The Acquiring Fund and the Target Fund have similar principal investment strategies, although the Funds’ strategies and holdings diverge with respect to their allocations to emerging market investments. In this regard, the Board noted that, under normal circumstances, the Target Fund invests (i) at least 80% of its net assets in equity securities of foreign issuers, and (ii) up to 20% of its total assets in emerging market equity securities, while the Acquiring Fund invests (i) at least 80% of its net assets in equity securities of foreign issuers, (ii) up to 30% of its total assets in emerging market equity securities, and (iii) in securities of at least three different countries, including the U.S.

The Board also considered that the Target Fund and Acquiring Fund pursue both value- and growth-oriented investment strategies, while the Target Fund also utilizes an international blend strategy to pursue its investment objectives.

The Board considered the holdings of the Target Fund and the Acquiring Fund and noted the degree to which the characteristics of their overall holdings are consistent, and the degree to which the Target Fund’s individual holdings are compatible with the Acquiring Fund’s investment strategy. In this regard, the Board considered that Funds Management intends that approximately one-third of the Target Fund’s historic assets be transferred to the Acquiring Fund in the Merger.

The Board noted that both Funds may invest across any market capitalization and use derivatives to manage risk or enhance return. In addition, the Board noted that the Target Fund, through multiple sub-advisers, relies on fundamental and bottom-up stock selection, as well as a quantitative model, to execute its investment strategies, while the Acquiring Fund relies on bottom-up stock selection, based on in-depth fundamental research conducted by a single sub-adviser, to employ its investment strategy.

The Board also considered transaction costs and other related fees with respect to the Merger, as well as the tax implications.

Comparative Performance. The Board reviewed the performance of the Target Fund relative to that of the Acquiring Fund, and noted that the Acquiring Fund (Institutional Class) had outperformed the Target Fund for the one-year period ended September 30, 2020, while the Target Fund had outperformed the Acquiring Fund for the three-, five- and ten-year periods ended September 30, 2020. The Board considered the Funds’ short- and long-term performance and Funds Management’s assessment of the relative positioning of each Fund in light of anticipated style shifts. In reviewing comparative performance, the Board considered the similarities and differences between the Funds’ investment objectives and principal investment strategies. Shareholders should consult the chart in the section entitled “Merger Summary (Objectives, Strategies, Risks, Performance, Expense, Management and Tax Information) - Fund Performance Comparison” for more detailed performance information, including information about each Funds’ performance relative to that of its primary benchmark index. Of course, past performance is not predictive of future results.

Gross And Net Operating Expense Ratios Of The Funds. The Board noted that the pro forma combined gross operating expense ratio for each share class of the Acquiring Fund is lower than that of each corresponding share class of the Target Fund based on average net assets for the six-month period ended September 30, 2020. The Board also considered that the pro forma combined net operating expense ratio of each share class of the Acquiring Fund will be lower than that of each corresponding share class of the Target Fund, after giving effect to the Merger and taking into account fee waiver and expense reimbursement commitments by Funds Management.

In this regard, the Board noted that Funds Management has agreed (contingent upon the completion of the Merger) to maintain the Acquiring Fund’s pro forma net operating expense ratio cap through February 28, 2022, and that, thereafter, the cap may not be raised without Board approval. Thus, Target Fund and Acquiring Fund shareholders are assured that they will not experience an increase in their net operating expense ratios until February 28, 2022, at the earliest. Shareholders should consult the section entitled “Merger Summary (Objectives, Strategies, Risks, Performance, Expense, Management and Tax Information) - Shareholder Fee and Fund Expense Comparison” for more detailed gross and net operating expense ratio information.