Exhibit 99.1

MEDIA CONTACT

Heather Worley, 214.932.6827

heather.worley@texascapitalbank.com

INVESTOR CONTACT

Myrna Vance, 214.932.6646

myrna.vance@texascapitalbank.com

TEXAS CAPITAL BANCSHARES ANNOUNCES OPERATING RESULTS FOR 2013

DALLAS – January 22, 2014 – Texas Capital Bancshares, Inc. (NASDAQ: TCBI), the parent company of Texas Capital Bank, announced earnings and operating results for the fourth quarter and full year of 2013.

| • | Net income decreased 9% on a linked quarter basis and decreased 3% from the fourth quarter of 2012 |

| • | EPS decreased 9% on a linked quarter basis and decreased 12% from the fourth quarter of 2012 |

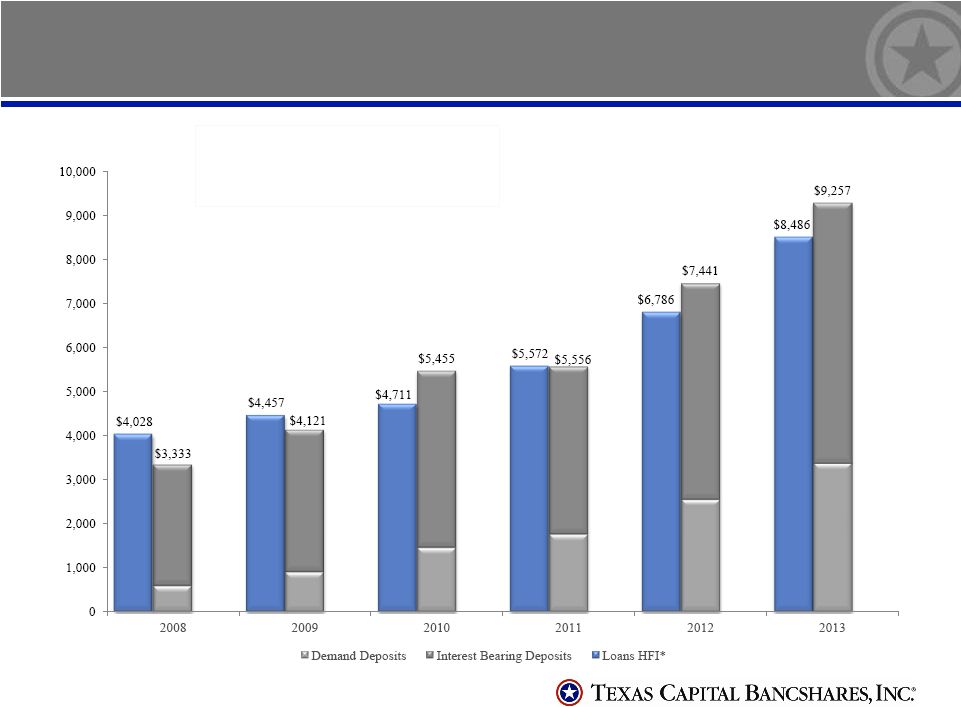

| • | Demand deposits increased 3% and total deposits increased 3% on a linked quarter basis, growing 32% and 24%, respectively, from the fourth quarter of 2012 |

| • | Loans held for investment, excluding mortgage finance, increased 5% and total loans increased 9% on a linked quarter basis, growing 25% and 13%, respectively, from the fourth quarter of 2012 |

“2013 has been an extraordinary year for Texas Capital as we continue to build our business consistent with our successful, long-standing model,” said Keith Cargill, CEO. “As we win top client-facing talent and the critically important people who deliver outstanding service, products and support, we build growing earnings power for the future. This is consistent with our upcoming capital raise to support our anticipated strong growth.”

FINANCIAL SUMMARY

(dollars and shares in thousands)

| 2013 | 2012 | % Change | ||||||||||

| ANNUAL OPERATING RESULTS(1) |

||||||||||||

| Net Income |

$ | 121,046 | $ | 120,709 | 0 | % | ||||||

| Net Income Available to Common Shareholders |

$ | 113,652 | $ | 120,709 | (6 | )% | ||||||

| Diluted EPS |

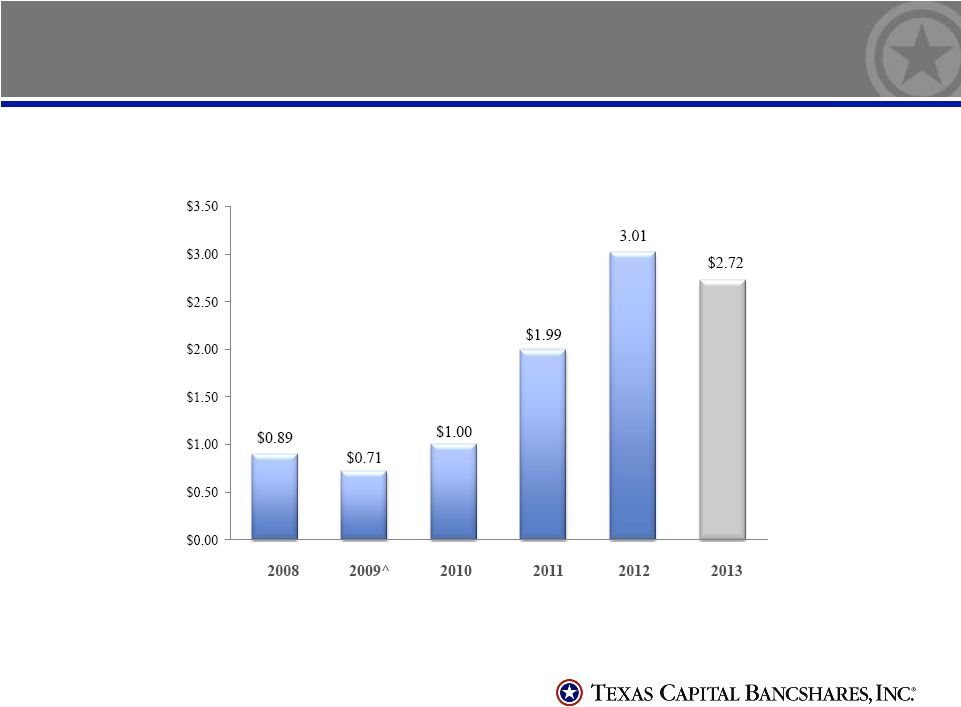

$ | 2.72 | $ | 3.01 | (10 | )% | ||||||

| ROA |

1.17 | % | 1.35 | % | ||||||||

| ROE |

12.82 | % | 16.93 | % | ||||||||

| Diluted Shares |

41,780 | 40,166 | ||||||||||

| QUARTERLY OPERATING RESULTS(1) |

||||||||||||

| Net Income |

$ | 30,356 | $ | 31,435 | (3 | )% | ||||||

| Net Income Available to Common Shareholders |

$ | 27,918 | $ | 31,435 | (11 | )% | ||||||

| Diluted EPS |

$ | .67 | $ | .76 | (12 | )% | ||||||

| ROA |

1.10 | % | 1.27 | % | ||||||||

| ROE |

11.94 | % | 15.35 | % | ||||||||

| Diluted Shares |

41,889 | 41,505 | ||||||||||

| BALANCE SHEET(1) |

||||||||||||

| Total Assets |

$ | 11,714,397 | $ | 10,540,542 | 11 | % | ||||||

| Demand Deposits |

3,347,567 | 2,535,375 | 32 | % | ||||||||

| Total Deposits |

9,257,379 | 7,440,804 | 24 | % | ||||||||

| Loans Held for Investment |

8,486,309 | 6,785,535 | 25 | % | ||||||||

| Loans Held for Investment, Mortgage Finance |

2,784,265 | 3,175,272 | (12 | )% | ||||||||

| Total Loans |

11,270,574 | 9,960,807 | 13 | % | ||||||||

| Stockholders’ Equity |

1,096,350 | 836,242 | 31 | % | ||||||||

| (1) | Operating results, assets and loans are reporting from continuing operations |

DETAILED FINANCIALS

Texas Capital Bancshares, Inc. reported net income from continuing operations of $121.0 million and net income available to common shareholders of $113.7 million for the year ended December 31, 2013 compared to $120.7 million for both net income from continuing operations and net income available to common shareholders for the year ended December 31, 2012. For the fourth quarter of 2013, net income from continuing operations was $30.4 million and net income available to common shareholders was $27.9 million, compared to $31.4 million for both net income from continuing operations and net income available to common shareholders for the same period in 2012. On a fully diluted basis, earnings per common share from continuing operations were $2.72 for the year ended December 31, 2013, compared to $3.01 for the same period in 2012. For the fourth quarter of 2013, diluted earnings per share was $.67 compared to $.76 for the same period in 2012. The discussion below relates only to continuing operations.

Return on average common equity was 12.82 percent and return on average assets was 1.17 percent for the year ended December 31, 2013, compared to 16.93 percent and 1.35 percent, respectively, for 2012. Return on average common equity was 11.94 percent and return on average assets was 1.10 percent for the fourth quarter of 2013, compared to 15.35 percent and 1.27 percent, respectively, for the fourth quarter of 2012.

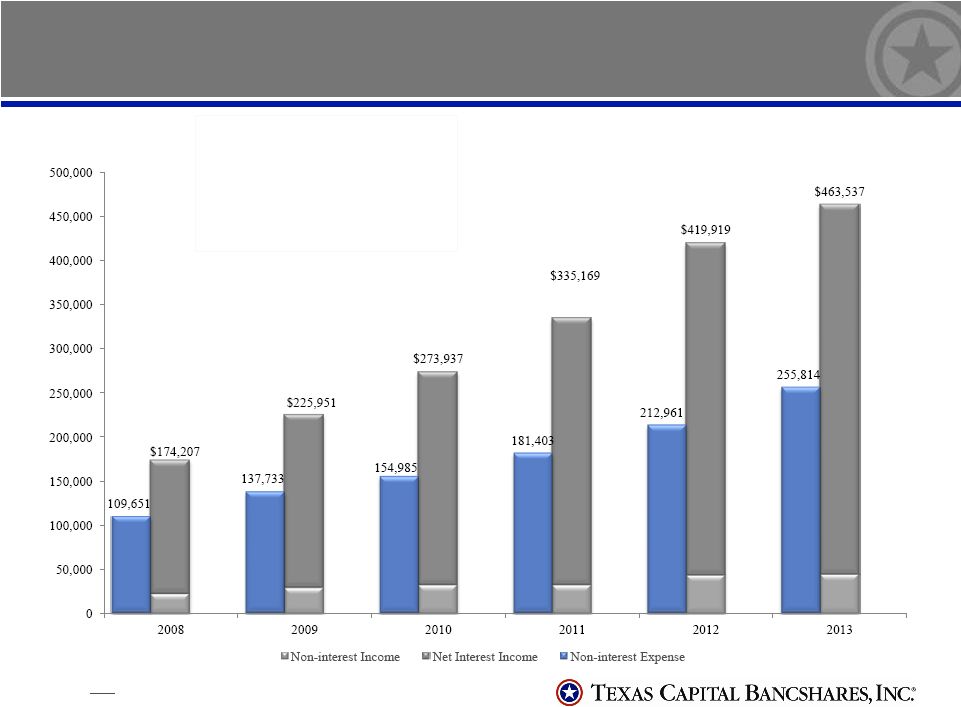

Net interest income was $111.5 million for the fourth quarter of 2013, compared to $108.8 million in the third quarter of 2013 and $101.2 million for the fourth quarter of 2012. For 2013, net interest income reached $419.5 million compared to $376.9 million in 2012. The net interest margin in the fourth quarter of 2013 was 4.21 percent, a 6 basis point decrease from the fourth quarter of 2012 and consistent with the third quarter of 2013. The year-to-date decrease in net interest margin is due to the growth in loans with lower yields offset with a reduction in the total cost of deposits and borrowed funds.

Average loans, excluding mortgage finance, for the year ended December 31, 2013 were $7.5 billion, an increase of $1.4 billion, or 23 percent, from 2012. Average mortgage finance loans for the year ended December 31, 2013 were $2.3 billion, consistent with 2012. Average loans, excluding mortgage finance, for the fourth quarter of 2013 were $8.1 billion, an increase of $1.4 billion, or 21 percent, from the fourth quarter of 2012 and an increase of $410.7 million, or 5 percent, from the third quarter of 2013. Average mortgage finance loans for the fourth quarter of 2013 decreased $419.4 million to $2.2 billion compared to the fourth quarter of 2012 and decreased $123.4 million from the third quarter of 2013.

Average total deposits for the fourth quarter of 2013 increased $2.2 billion from the fourth quarter of 2012 and increased $439.1 million from the third quarter of 2013. For the same periods, the average balance of demand deposits increased $932.5 million, or 40 percent, to $3.3 billion from $2.4 billion during the fourth quarter of 2012 and increased $164.7 million, or 5 percent, from the third quarter of 2013.

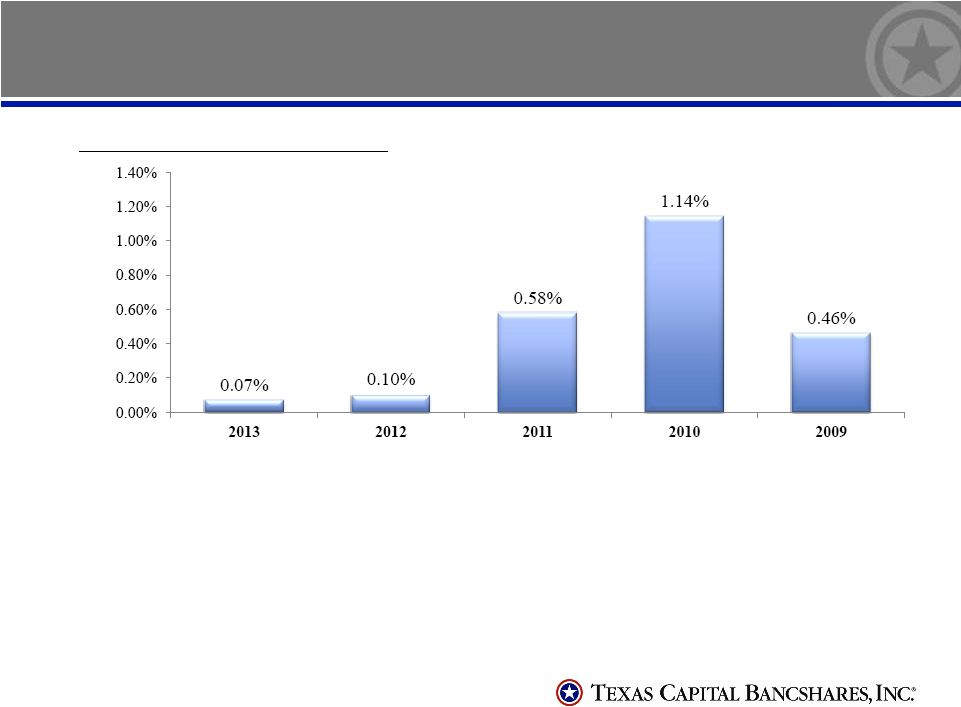

In the fourth quarter of 2013, we experienced decreases in the levels of non-performing assets. Credit costs, including the provision for credit losses and valuation charges related to other real estate owned (“OREO”) totaled $5.5 million in the fourth quarter of 2013 compared to $5.5 million in the fourth quarter of 2012 and $5.0 million in the third quarter of 2013. We recorded a $5.0 million provision for credit losses in the fourth quarter of 2013 compared to $4.5 million in the fourth quarter of 2012 and $5.0 million in the third quarter of 2013. For 2013, the total provision for credit losses was $19.0 million, an increase of 65 percent from $11.5 million in 2012. The substantial majority of the provision for the year ended December 31, 2013 was directly related to the significant growth in loans excluding mortgage finance loans during the year. Due to growth and improving credit quality, at December 31, 2013, the combined reserve decreased to 1.09 percent of loans excluding mortgage finance loans as compared to 1.15 percent at December 31, 2012 and 1.10 percent at September 30, 2013. In management’s opinion, the reserve is appropriate and is derived from consistent application of the methodology for establishing the adequacy of reserves for Texas Capital Bank’s loan portfolio. In the fourth quarter of 2013, net charge-offs were $1.3 million compared to net charge-offs of $3.5 million in the fourth quarter of 2012 and net charge-offs of $46,000 in the third quarter of 2013. For 2013, net charge-offs were $4.9 million, .07 percent of average loans, excluding mortgage finance loans, compared to $6.1 million and a ratio of .10 percent in 2012. Non-accrual loans were $32.4 million, or .38 percent of loans excluding mortgage finance loans as of December 31, 2013, $55.8 million, or .82 percent, as of December 31, 2012 and $35.7 million, or .44 percent, as of September 30, 2013. At December 31, 2013, total

2

OREO was $5.1 million compared to $16.0 million as of December 31, 2012, and $12.8 million as of September 30, 2013. The OREO balance of $5.1 million at December 31, 2013 does not have a valuation allowance. The valuation charge for OREO reflected in non-interest expense was $466,000 in the fourth quarter of 2013 compared to $955,000 in the fourth quarter of 2012 and none in the third quarter of 2013.

Non-interest income decreased $1.7 million during the fourth quarter of 2013, or 13 percent, compared to the same period of 2012 primarily related to a $1.6 million decrease in brokered loan fees as a result of declining mortgage finance volumes during the fourth quarter of 2013 as compared to the fourth of 2012.

Non-interest expense for the fourth quarter of 2013 increased $10.2 million, or 17 percent, to $70.3 million from $60.1 million in the fourth quarter of 2012. The increase is primarily related to an $11.8 million increase in salaries and employee benefits to $43.0 million for the fourth quarter of 2013 from $31.2 million for the same period in 2012, which was primarily due to general business growth and an increase in cost of incentives tied to stock price.

Stockholders’ equity increased by 31 percent from $836.2 million at December 31, 2012 to $1.1 billion at December 31, 2013, primarily due to the offering of 6.0 million preferred shares for net proceeds of $145.1 million in the first quarter of 2013 and retained income during 2013. The Bank is well capitalized under regulatory guidelines and at December 31, 2013, our ratio of tangible common equity to total tangible assets was 7.9 percent.

ABOUT TEXAS CAPITAL BANCSHARES, INC.

Texas Capital Bancshares, Inc. (NASDAQ®: TCBI), a member of the Russell 2000® Index and the S&P SmallCap 600®, is the parent company of Texas Capital Bank, a commercial bank that delivers highly personalized financial services to businesses and individual clients. Headquartered in Dallas, the bank has full-service locations in Austin, Dallas, Fort Worth, Houston and San Antonio.

This news release may be deemed to include forward-looking statements which are based on Texas Capital’s current estimates or expectations of future events or future results. Texas Capital is under no obligation, and expressly disclaims such obligation, to update, alter or revise its forward-looking statements, whether as a result of new information, future events, or otherwise. A number of factors, many of which are beyond Texas Capital’s control, could cause actual results to differ materially from future results expressed or implied by such forward-looking statements. These risks and uncertainties include, but are not limited to, the risk of adverse impacts from general economic conditions, competition, interest rate sensitivity and exposure to regulatory and legislative changes. These and other factors that could cause results to differ materially from those described in the forward-looking statements can be found in the prospectus supplements, the Annual Report on Form 10-K and other filings made by Texas Capital with the Securities and Exchange Commission (SEC).

3

TEXAS CAPITAL BANCSHARES, INC.

SELECTED FINANCIAL HIGHLIGHTS (UNAUDITED)

(Dollars in thousands except per share data)

| 4th Quarter 2013 |

3rd Quarter 2013 |

2nd Quarter 2013 |

1st Quarter 2013 |

4th Quarter 2012 |

||||||||||||||||

| CONSOLIDATED STATEMENT OF INCOME |

||||||||||||||||||||

| Interest income |

$ | 117,965 | $ | 115,217 | $ | 107,264 | $ | 104,179 | $ | 107,769 | ||||||||||

| Interest expense |

6,490 | 6,441 | 6,044 | 6,137 | 6,614 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net interest income |

111,475 | 108,776 | 101,220 | 98,042 | 101,155 | |||||||||||||||

| Provision for credit losses |

5,000 | 5,000 | 7,000 | 2,000 | 4,500 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net interest income after provision for credit losses |

106,475 | 103,776 | 94,220 | 96,042 | 96,655 | |||||||||||||||

| Non-interest income |

11,184 | 10,431 | 11,128 | 11,281 | 12,836 | |||||||||||||||

| Non-interest expense |

70,291 | 62,009 | 68,734 | 55,700 | 60,074 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Income from continuing operations before income taxes |

47,368 | 52,198 | 36,614 | 51,623 | 49,417 | |||||||||||||||

| Income tax expense |

17,012 | 18,724 | 12,542 | 18,479 | 17,982 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Income from continuing operations |

30,356 | 33,474 | 24,072 | 33,144 | 31,435 | |||||||||||||||

| Income (loss) from discontinued operations (after-tax) |

3 | 2 | 1 | (1 | ) | (6 | ) | |||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net income |

30,359 | 33,476 | 24,073 | 33,143 | 31,429 | |||||||||||||||

| Preferred stock dividends |

2,438 | 2,437 | 2,438 | 81 | – | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net income available to common shareholders |

$ | 27,921 | $ | 31,039 | $ | 21,635 | $ | 33,062 | $ | 31,429 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Diluted EPS from continuing operations |

$ | .67 | $ | .74 | $ | .52 | $ | .80 | $ | .76 | ||||||||||

| Diluted EPS |

$ | .67 | $ | .74 | $ | .52 | $ | .80 | $ | .76 | ||||||||||

| Diluted shares |

41,888,768 | 41,791,674 | 41,723,525 | 41,429,244 | 41,505,026 | |||||||||||||||

| CONSOLIDATED BALANCE SHEET DATA |

||||||||||||||||||||

| Total assets |

$ | 11,714,397 | $ | 10,797,448 | $ | 10,977,990 | $ | 10,020,565 | $ | 10,540,542 | ||||||||||

| Loans held for investment |

8,486,309 | 8,051,328 | 7,510,662 | 6,920,011 | 6,785,535 | |||||||||||||||

| Loans held for investment, mortgage finance |

2,784,265 | 2,262,085 | 2,838,234 | 2,577,830 | 3,175,272 | |||||||||||||||

| Securities |

63,214 | 67,815 | 75,861 | 87,527 | 100,195 | |||||||||||||||

| Demand deposits |

3,347,567 | 3,242,060 | 2,928,735 | 2,628,446 | 2,535,375 | |||||||||||||||

| Total deposits |

9,257,379 | 8,957,081 | 7,980,598 | 7,745,831 | 7,440,804 | |||||||||||||||

| Other borrowings |

1,025,630 | 449,724 | 1,634,630 | 938,134 | 1,947,161 | |||||||||||||||

| Subordinated notes |

111,000 | 111,000 | 111,000 | 111,000 | 111,000 | |||||||||||||||

| Long-term debt |

113,406 | 113,406 | 113,406 | 113,406 | 113,406 | |||||||||||||||

| Stockholders’ equity |

1,096,350 | 1,066,629 | 1,034,955 | 1,013,195 | 836,242 | |||||||||||||||

| End of period shares outstanding |

41,036,370 | 40,934,623 | 40,862,481 | 40,771,414 | 40,727,579 | |||||||||||||||

| Book value (excluding securities gains/losses) |

$ | 23.02 | $ | 22.35 | $ | 21.60 | $ | 21.10 | $ | 20.45 | ||||||||||

| Tangible book value (excluding securities gains/losses) |

$ | 22.50 | $ | 21.82 | $ | 21.08 | $ | 20.62 | $ | 19.96 | ||||||||||

| SELECTED FINANCIAL RATIOS |

||||||||||||||||||||

| Net interest margin |

4.21 | % | 4.21 | % | 4.19 | % | 4.27 | % | 4.27 | % | ||||||||||

| Return on average assets |

1.10 | % | 1.25 | % | 0.95 | % | 1.38 | % | 1.27 | % | ||||||||||

| Return on average common equity |

11.94 | % | 13.74 | % | 9.94 | % | 15.82 | % | 15.35 | % | ||||||||||

| Non-interest income to earning assets |

.42 | % | .40 | % | .46 | % | .49 | % | .54 | % | ||||||||||

| Efficiency ratio |

57.3 | % | 52.0 | % | 61.2 | % | 50.9 | % | 52.7 | % | ||||||||||

| Efficiency ratio (excluding OREO valuation/write-down) |

56.9 | % | 52.0 | % | 60.8 | % | 50.9 | % | 51.9 | % | ||||||||||

| Non-interest expense to earning assets |

2.65 | % | 2.40 | % | 2.84 | % | 2.42 | % | 2.53 | % | ||||||||||

| Non-interest expense to earning assets (excluding OREO valuation charge) |

2.63 | % | 2.40 | % | 2.83 | % | 2.42 | % | 2.49 | % | ||||||||||

| Tangible common equity to total tangible assets |

7.9 | % | 8.3 | % | 7.9 | % | 8.4 | % | 7.7 | % | ||||||||||

4

TEXAS CAPITAL BANCSHARES, INC.

CONSOLIDATED BALANCE SHEETS (UNAUDITED)

(Dollars in thousands)

| December 31, 2013 |

December 31, 2012 |

% Change |

||||||||||

| Assets |

||||||||||||

| Cash and due from banks |

$ | 92,484 | $ | 111,938 | (17 | )% | ||||||

| Interest-bearing deposits |

61,337 | 94,410 | (35 | )% | ||||||||

| Federal funds sold |

90 | — | 100 | % | ||||||||

| Securities, available-for-sale |

63,214 | 100,195 | (37 | )% | ||||||||

| Loans held for sale from discontinued operations |

294 | 302 | (3 | )% | ||||||||

| Loans held for investment, mortgage finance |

2,784,265 | 3,175,272 | (12 | )% | ||||||||

| Loans held for investment (net of unearned income) |

8,486,309 | 6,785,535 | 25 | % | ||||||||

| Less: Allowance for loan losses |

87,604 | 74,337 | 18 | % | ||||||||

|

|

|

|

|

|

|

|||||||

| Loans held for investment, net |

11,182,970 | 9,886,470 | 13 | % | ||||||||

| Premises and equipment, net |

11,482 | 11,445 | (0 | )% | ||||||||

| Accrued interest receivable and other assets |

281,534 | 316,201 | (11 | )% | ||||||||

| Goodwill and intangibles, net |

21,286 | 19,883 | 7 | % | ||||||||

|

|

|

|

|

|

|

|||||||

| Total assets |

$ | 11,714,691 | $ | 10,540,844 | 11 | % | ||||||

|

|

|

|

|

|

|

|||||||

| Liabilities and Stockholders’ Equity |

||||||||||||

| Liabilities: |

||||||||||||

| Deposits: |

||||||||||||

| Non-interest bearing |

$ | 3,347,567 | $ | 2,535,375 | 32 | % | ||||||

| Interest bearing |

5,579,505 | 4,576,120 | 22 | % | ||||||||

| Interest bearing in foreign branches |

330,307 | 329,309 | 0 | % | ||||||||

|

|

|

|

|

|

|

|||||||

| Total deposits |

9,257,379 | 7,440,804 | 24 | % | ||||||||

| Accrued interest payable |

749 | 650 | 15 | % | ||||||||

| Other liabilities |

110,177 | 91,581 | 20 | % | ||||||||

| Federal funds purchased |

148,650 | 273,179 | (46 | )% | ||||||||

| Repurchase agreements |

21,954 | 23,936 | (8 | )% | ||||||||

| Other borrowings |

855,026 | 1,650,046 | (48 | )% | ||||||||

| Subordinated notes |

111,000 | 111,000 | — | |||||||||

| Trust preferred subordinated debentures |

113,406 | 113,406 | — | |||||||||

|

|

|

|

|

|

|

|||||||

| Total liabilities |

10,618,341 | 9,704,602 | 9 | % | ||||||||

| Stockholders’ equity: |

||||||||||||

| Preferred stock, $.01 par value, $1,000 liquidation value: |

||||||||||||

| Authorized shares – 10,000,000 |

||||||||||||

| Issued shares |

150,000 | — | 100 | % | ||||||||

| Common stock, $.01 par value: |

||||||||||||

| Authorized shares – 100,000,000 |

||||||||||||

| Issued shares – 41,036,787 and 40,727,996 at December 31, 2013 and 2012, respectively |

410 | 407 | 1 | % | ||||||||

| Additional paid-in capital |

448,208 | 450,116 | (0 | )% | ||||||||

| Retained earnings |

496,112 | 382,455 | 30 | % | ||||||||

| Treasury stock (shares at cost: 417 at December 31, 2013 and 2012) |

(8 | ) | (8 | ) | — | |||||||

| Accumulated other comprehensive income, net of taxes |

1,628 | 3,272 | (50 | )% | ||||||||

|

|

|

|

|

|

|

|||||||

| Total stockholders’ equity |

1,096,350 | 836,242 | 31 | % | ||||||||

|

|

|

|

|

|

|

|||||||

| Total liabilities and stockholders’ equity |

$ | 11,714,691 | $ | 10,540,844 | 11 | % | ||||||

|

|

|

|

|

|

|

|||||||

5

TEXAS CAPITAL BANCSHARES, INC.

CONSOLIDATED STATEMENTS OF INCOME (UNAUDITED)

(Dollars in thousands except per share data)

| Three Months Ended December 31 |

Year Ended December 31 |

|||||||||||||||

| 2013 | 2012 | 2013 | 2012 | |||||||||||||

| Interest income |

||||||||||||||||

| Interest and fees on loans |

$ | 117,261 | $ | 106,653 | $ | 441,314 | $ | 393,548 | ||||||||

| Securities |

621 | 1,053 | 3,015 | 4,688 | ||||||||||||

| Federal funds sold |

24 | 6 | 65 | 13 | ||||||||||||

| Deposits in other banks |

59 | 57 | 231 | 208 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total interest income |

117,965 | 107,769 | 444,625 | 398,457 | ||||||||||||

| Interest expense |

||||||||||||||||

| Deposits |

3,858 | 3,312 | 14,030 | 13,644 | ||||||||||||

| Federal funds purchased |

116 | 190 | 686 | 979 | ||||||||||||

| Repurchase agreements |

5 | 3 | 18 | 13 | ||||||||||||

| Other borrowings |

40 | 615 | 515 | 2,149 | ||||||||||||

| Subordinated notes |

1,840 | 1,829 | 7,327 | 2,037 | ||||||||||||

| Trust preferred subordinated debentures |

631 | 665 | 2,536 | 2,756 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total interest expense |

6,490 | 6,614 | 25,112 | 21,578 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Net interest income |

111,475 | 101,155 | 419,513 | 376,879 | ||||||||||||

| Provision for credit losses |

5,000 | 4,500 | 19,000 | 11,500 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Net interest income after provision for credit losses |

106,475 | 96,655 | 400,513 | 365,379 | ||||||||||||

| Non-interest income |

||||||||||||||||

| Service charges on deposit accounts |

1,674 | 1,693 | 6,783 | 6,605 | ||||||||||||

| Trust fee income |

1,250 | 1,260 | 5,023 | 4,822 | ||||||||||||

| Bank owned life insurance (BOLI) income |

533 | 510 | 1,917 | 2,168 | ||||||||||||

| Brokered loan fees |

3,380 | 4,978 | 16,980 | 17,596 | ||||||||||||

| Swap fees |

1,904 | 2,093 | 5,520 | 4,909 | ||||||||||||

| Other |

2,443 | 2,302 | 7,801 | 6,940 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total non-interest income |

11,184 | 12,836 | 44,024 | 43,040 | ||||||||||||

| Non-interest expense |

||||||||||||||||

| Salaries and employee benefits |

43,008 | 31,198 | 157,752 | 121,456 | ||||||||||||

| Net occupancy expense |

4,487 | 3,916 | 16,821 | 14,852 | ||||||||||||

| Marketing |

4,183 | 3,980 | 16,203 | 13,449 | ||||||||||||

| Legal and professional |

5,520 | 5,320 | 18,104 | 17,557 | ||||||||||||

| Communications and technology |

3,597 | 3,070 | 13,762 | 11,158 | ||||||||||||

| FDIC insurance assessment |

1,923 | 1,071 | 8,057 | 5,568 | ||||||||||||

| Allowance and other carrying costs for OREO |

609 | 1,369 | 1,788 | 9,075 | ||||||||||||

| Litigation settlement expense |

— | 4,000 | — | 4,000 | ||||||||||||

| Other |

6,964 | 6,150 | 24,247 | 22,729 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total non-interest expense |

70,291 | 60,074 | 256,734 | 219,844 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Income from continuing operations before income taxes |

47,368 | 49,417 | 187,803 | 188,575 | ||||||||||||

| Income tax expense |

17,012 | 17,982 | 66,757 | 67,866 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Income from continuing operations |

30,356 | 31,435 | 121,046 | 120,709 | ||||||||||||

| Loss from discontinued operations (after-tax) |

3 | (6 | ) | 5 | (37 | ) | ||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Net income |

30,359 | 31,429 | 121,051 | 120,672 | ||||||||||||

| Preferred stock dividends |

2,438 | — | 7,394 | — | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Net income available to common shareholders |

$ | 27,921 | $ | 31,429 | $ | 113,657 | $ | 120,672 | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Basic earnings per common share: |

||||||||||||||||

| Income from continuing operations |

$ | .68 | $ | .78 | $ | 2.78 | $ | 3.09 | ||||||||

| Net income |

$ | .68 | $ | .78 | $ | 2.78 | $ | 3.09 | ||||||||

| Diluted earnings per common share: |

||||||||||||||||

| Income from continuing operations |

$ | .67 | $ | .76 | $ | 2.72 | $ | 3.01 | ||||||||

| Net income |

$ | .67 | $ | .76 | $ | 2.72 | $ | 3.00 | ||||||||

6

TEXAS CAPITAL BANCSHARES, INC.

SUMMARY OF LOAN LOSS EXPERIENCE

(Dollars in thousands)

| 4th Quarter 2013 |

3rd Quarter 2013 |

2nd Quarter 2013 |

1st Quarter 2013 |

4th Quarter 2012 |

||||||||||||||||

| Reserve for loan losses: |

||||||||||||||||||||

| Beginning balance |

$ | 84,006 | $ | 79,428 | $ | 75,000 | $ | 74,337 | $ | 73,722 | ||||||||||

| Loans charged-off: |

||||||||||||||||||||

| Commercial |

1,605 | 496 | 2,826 | 1,648 | 4,044 | |||||||||||||||

| Real estate – term |

— | 13 | 26 | 105 | — | |||||||||||||||

| Consumer |

— | — | 26 | 19 | — | |||||||||||||||

| Leases |

— | 2 | — | — | 34 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total loans charged-off |

1,605 | 511 | 2,878 | 1,772 | 4,078 | |||||||||||||||

| Recoveries: |

||||||||||||||||||||

| Commercial |

225 | 233 | 348 | 397 | 350 | |||||||||||||||

| Real estate – term |

60 | 195 | 7 | 8 | 226 | |||||||||||||||

| Consumer |

9 | 19 | 15 | 30 | 7 | |||||||||||||||

| Leases |

43 | 18 | 140 | 121 | 21 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total recoveries |

337 | 465 | 510 | 556 | 604 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net charge-offs |

1,268 | 46 | 2,368 | 1,216 | 3,474 | |||||||||||||||

| Provision for loan losses |

4,866 | 4,624 | 6,796 | 1,879 | 4,089 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Ending balance |

$ | 87,604 | $ | 84,006 | $ | 79,428 | $ | 75,000 | $ | 74,337 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Reserve for off-balance sheet credit losses: |

||||||||||||||||||||

| Beginning balance |

$ | 4,556 | $ | 4,180 | $ | 3,976 | $ | 3,855 | $ | 3,444 | ||||||||||

| Provision for off-balance sheet credit losses |

134 | 376 | 204 | 121 | 411 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Ending balance |

$ | 4,690 | $ | 4,556 | $ | 4,180 | $ | 3,976 | $ | 3,855 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total reserves for credit losses |

$ | 92,294 | $ | 88,562 | $ | 83,608 | $ | 78,976 | $ | 78,192 | ||||||||||

| Total provision for credit losses |

$ | 5,000 | $ | 5,000 | $ | 7,000 | $ | 2,000 | $ | 4,500 | ||||||||||

| Reserve to loans |

.78 | % | .81 | % | .77 | % | .79 | % | .75 | % | ||||||||||

| Reserve to loans excluding mortgage finance loans(2) |

1.03 | % | 1.04 | % | 1.06 | % | 1.08 | % | 1.10 | % | ||||||||||

| Reserve to average loans |

.84 | % | .83 | % | .83 | % | .81 | % | .88 | % | ||||||||||

| Reserve to average loans excluding mortgage finance loans(2) |

1.08 | % | 1.09 | % | 1.11 | % | 1.10 | % | 1.12 | % | ||||||||||

| Net charge-offs to average loans(1) |

.05 | % | .00 | % | .10 | % | .05 | % | .15 | % | ||||||||||

| Net charge-offs to average loans excluding mortgage

finance |

.06 | % | .00 | % | .13 | % | .07 | % | .21 | % | ||||||||||

| Net charge-offs to average loans for last twelve months(1) |

.05 | % | .07 | % | .09 | % | .07 | % | .07 | % | ||||||||||

| Net charge-offs to average loans, excluding mortgage finance loans, for last twelve months(1)(2) |

.07 | % | .10 | % | .12 | % | .10 | % | .10 | % | ||||||||||

| Total provision for credit losses to average loans(1) |

.19 | % | .20 | % | .29 | % | .09 | % | .19 | % | ||||||||||

| Total provision for credit losses to average loans excluding mortgage finance loans(1)(2) |

.24 | % | .26 | % | .39 | % | .12 | % | .27 | % | ||||||||||

| Combined reserves for credit losses to loans |

.82 | % | .86 | % | .81 | % | .83 | % | .78 | % | ||||||||||

| Combined reserves for credit losses to loans, excluding mortgage finance loans(2) |

1.09 | % | 1.10 | % | 1.11 | % | 1.14 | % | 1.15 | % | ||||||||||

| Non-performing assets (NPAs): |

||||||||||||||||||||

| Non-accrual loans |

$ | 32,375 | $ | 35,737 | $ | 38,450 | $ | 43,424 | $ | 55,833 | ||||||||||

| Other real estate owned (OREO) (4) |

5,110 | 12,805 | 13,053 | 14,426 | 15,991 | |||||||||||||||

| Other repossessed assets |

— | — | 19 | — | 42 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total |

$ | 37,485 | $ | 48,542 | $ | 51,522 | $ | 57,850 | $ | 71,866 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

7

| Non-accrual loans to loans |

.29 | % | .35 | % | .37 | % | .46 | % | .56 | % | ||||||||||

| Non-accrual loans to loans excluding mortgage finance loans(2) |

.38 | % | .44 | % | .51 | % | .63 | % | .82 | % | ||||||||||

| Total NPAs to loans plus OREO |

.33 | % | .47 | % | .50 | % | .61 | % | .72 | % | ||||||||||

| Total NPAs to loans excluding mortgage finance loans plus OREO(2) |

.44 | % | .60 | % | .68 | % | .83 | % | 1.06 | % | ||||||||||

| Total NPAs to earning assets |

.33 | % | .47 | % | .49 | % | .60 | % | .71 | % | ||||||||||

| Reserve for loan losses to non-accrual loans |

2.7x | 2.4x | 2.1x | 1.7x | 1.3x | |||||||||||||||

| Restructured loans |

$ | 1,935 | $ | 4,691 | $ | 4,765 | $ | 11,755 | $ | 10,407 | ||||||||||

| Loans past due 90 days and still accruing(3) |

$ | 9,325 | $ | 7,510 | $ | 7,633 | $ | 12,614 | $ | 3,674 | ||||||||||

| Loans past due 90 days to loans |

.08 | % | .07 | % | .07 | % | .13 | % | .04 | % | ||||||||||

| Loans past due 90 days to loans excluding mortgage finance loans(2) |

.11 | % | .09 | % | .10 | % | .18 | % | .05 | % |

| (1) | Interim period ratios are annualized. |

| (2) | Mortgage finance loans were previously classified as loans held for sale but have been reclassified as loans held for investment. The indicated ratios are presented with and excluding the mortgage finance loans because the risk profile of our mortgage finance loans is different than our other loans held for investment. No provision for credit losses is allocated to these loans based on the internal risk grade assigned. |

| (3) | At December 31, 2013, loans past due 90 days and still accruing includes premium finance loans of $3.8 million. These loans are primarily secured by obligations of insurance carriers to refund premiums on cancelled insurance policies. The refund of premiums from the insurance carriers can take 180 days or longer from the cancellation date. |

| (4) | At December 31, 2013, there is no valuation allowance recorded against the OREO balance. |

8

TEXAS CAPITAL BANCSHARES, INC.

CONSOLIDATED STATEMENT OF INCOME (UNAUDITED)

(Dollars in thousands)

| 4th Quarter 2013 |

3rd Quarter 2013 |

2nd Quarter 2013 |

1st Quarter 2013 |

4th Quarter 2012 |

||||||||||||||||

| Interest income |

||||||||||||||||||||

| Interest and fees on loans |

$ | 117,261 | $ | 114,453 | $ | 106,418 | $ | 103,182 | $ | 106,653 | ||||||||||

| Securities |

621 | 682 | 773 | 939 | 1,053 | |||||||||||||||

| Federal funds sold |

24 | 22 | 13 | 6 | 6 | |||||||||||||||

| Deposits in other banks |

59 | 60 | 60 | 52 | 57 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total interest income |

117,965 | 115,217 | 107,264 | 104,179 | 107,769 | |||||||||||||||

| Interest expense |

||||||||||||||||||||

| Deposits |

3,858 | 3,699 | 3,228 | 3,245 | 3,312 | |||||||||||||||

| Federal funds purchased |

116 | 152 | 206 | 212 | 190 | |||||||||||||||

| Repurchase agreements |

5 | 4 | 5 | 4 | 3 | |||||||||||||||

| Other borrowings |

40 | 119 | 143 | 213 | 615 | |||||||||||||||

| Subordinated notes |

1,840 | 1,829 | 1,829 | 1,829 | 1,829 | |||||||||||||||

| Trust preferred subordinated debentures |

631 | 638 | 633 | 634 | 665 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total interest expense |

6,490 | 6,441 | 6,044 | 6,137 | 6,614 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net interest income |

111,475 | 108,776 | 101,220 | 98,042 | 101,155 | |||||||||||||||

| Provision for credit losses |

5,000 | 5,000 | 7,000 | 2,000 | 4,500 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net interest income after provision for credit losses |

106,475 | 103,776 | 94,220 | 96,042 | 96,655 | |||||||||||||||

| Non-interest income |

||||||||||||||||||||

| Service charges on deposit accounts |

1,674 | 1,659 | 1,749 | 1,701 | 1,693 | |||||||||||||||

| Trust fee income |

1,250 | 1,263 | 1,269 | 1,241 | 1,260 | |||||||||||||||

| Bank owned life insurance (BOLI) income |

533 | 423 | 463 | 498 | 510 | |||||||||||||||

| Brokered loan fees |

3,380 | 4,078 | 4,778 | 4,744 | 4,978 | |||||||||||||||

| Swap fees |

1,904 | 983 | 981 | 1,652 | 2,093 | |||||||||||||||

| Other |

2,443 | 2,025 | 1,888 | 1,445 | 2,302 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total non-interest income |

11,184 | 10,431 | 11,128 | 11,281 | 12,836 | |||||||||||||||

| Non-interest expense |

||||||||||||||||||||

| Salaries and employee benefits |

43,008 | 36,012 | 45,191 | 33,541 | 31,198 | |||||||||||||||

| Net occupancy expense |

4,487 | 4,342 | 4,135 | 3,857 | 3,916 | |||||||||||||||

| Marketing |

4,183 | 3,974 | 4,074 | 3,972 | 3,980 | |||||||||||||||

| Legal and professional |

5,520 | 3,937 | 4,707 | 3,940 | 5,320 | |||||||||||||||

| Communications and technology |

3,597 | 3,696 | 3,347 | 3,122 | 3,070 | |||||||||||||||

| FDIC insurance assessment |

1,923 | 4,357 | 699 | 1,078 | 1,071 | |||||||||||||||

| Allowance and other carrying costs for OREO |

609 | 267 | 482 | 430 | 1,369 | |||||||||||||||

| Litigation settlement expense |

— | (908 | ) | — | — | 4,000 | ||||||||||||||

| Other |

6,964 | 6,332 | 6,099 | 5,760 | 6,150 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total non-interest expense |

70,291 | 62,009 | 68,734 | 55,700 | 60,074 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Income from continuing operations before income taxes |

47,368 | 52,198 | 36,614 | 51,623 | 49,417 | |||||||||||||||

| Income tax expense |

17,012 | 18,724 | 12,542 | 18,479 | 17,982 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Income from continuing operations |

30,356 | 33,474 | 24,072 | 33,144 | 31,435 | |||||||||||||||

| Income (loss) from discontinued operations (after-tax) |

3 | 2 | 1 | (1 | ) | (6 | ) | |||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net income |

30,359 | 33,476 | 24,073 | 33,143 | 31,429 | |||||||||||||||

| Preferred stock dividends |

2,438 | 2,437 | 2,438 | 81 | — | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net income available to common shareholders |

$ | 27,921 | $ | 31,039 | $ | 21,635 | $ | 33,062 | $ | 31,429 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

9

TEXAS CAPITAL BANCSHARES, INC.

QUARTERLY FINANCIAL SUMMARY – UNAUDITED

Consolidated Daily Average Balances, Average Yields and Rates

Continuing Operations

(Dollars in thousands)

| 4th Quarter 2013 | 3rd Quarter 2013 | 2nd Quarter 2013 | 1st Quarter 2013 | 4th Quarter 2012 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Average Balance |

Revenue/ Expense (1) |

Yield/ Rate |

Average Balance |

Revenue/ Expense (1) |

Yield/ Rate |

Average Balance |

Revenue/ Expense (1) |

Yield/ Rate |

Average Balance |

Revenue/ Expense (1) |

Yield/ Rate |

Average Balance |

Revenue/ Expense (1) |

Yield/ Rate |

||||||||||||||||||||||||||||||||||||||||||||||

| Assets |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Securities – Taxable |

$ | 50,281 | $ | 480 | 3.79 | % | $ | 54,838 | $ | 522 | 3.78 | % | $ | 60,063 | $ | 594 | 3.97 | % | $ | 71,220 | $ | 729 | 4.15 | % | $ | 78,182 | $ | 811 | 4.13 | % | ||||||||||||||||||||||||||||||

| Securities – Non-taxable(2) |

14,786 | 217 | 5.82 | % | 16,879 | 246 | 5.78 | % | 18,843 | 275 | 5.85 | % | 22,174 | 323 | 5.91 | % | 25,301 | 372 | 5.85 | % | ||||||||||||||||||||||||||||||||||||||||

| Federal funds sold and securities purchased under resale agreements |

59,409 | 24 | 0.16 | % | 78,896 | 22 | 0.11 | % | 54,448 | 13 | 0.10 | % | 24,785 | 6 | 0.10 | % | 21,617 | 6 | 0.11 | % | ||||||||||||||||||||||||||||||||||||||||

| Deposits in other banks |

99,185 | 59 | 0.24 | % | 88,717 | 60 | 0.27 | % | 91,177 | 60 | 0.26 | % | 78,718 | 52 | 0.27 | % | 69,886 | 57 | 0.32 | % | ||||||||||||||||||||||||||||||||||||||||

| Loans held for investment, mortgage finance loans |

2,238,730 | 20,236 | 3.59 | % | 2,362,118 | 22,547 | 3.79 | % | 2,406,246 | 22,440 | 3.74 | % | 2,362,646 | 22,641 | 3.89 | % | 2,658,092 | 26,440 | 3.96 | % | ||||||||||||||||||||||||||||||||||||||||

| Loans held for investment |

8,142,569 | 97,025 | 4.73 | % | 7,731,901 | 91,906 | 4.72 | % | 7,152,323 | 83,978 | 4.71 | % | 6,842,766 | 80,541 | 4.77 | % | 6,662,817 | 80,213 | 4.79 | % | ||||||||||||||||||||||||||||||||||||||||

| Less reserve for loan losses |

84,009 | — | — | 79,551 | — | — | 75,006 | — | — | 74,442 | — | — | 73,912 | — | — | |||||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||||||

| Loans, net of reserve |

10,297,290 | 117,261 | 4.52 | % | 10,014,468 | 114,453 | 4.53 | % | 9,483,563 | 106,418 | 4.50 | % | 9,130,970 | 103,182 | 4.58 | % | 9,246,997 | 106,653 | 4.59 | % | ||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||||||

| Total earning assets |

10,520,951 | 118,041 | 4.45 | % | 10,253,798 | 115,303 | 4.46 | % | 9,708,094 | 107,360 | 4.44 | % | 9,327,867 | 104,292 | 4.53 | % | 9,441,983 | 107,899 | 4.55 | % | ||||||||||||||||||||||||||||||||||||||||

| Cash and other assets |

378,315 | 383,968 | 402,898 | 401,692 | 427,299 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||||||||||||||||||||||||||

| Total assets |

$ | 10,899,266 | $ | 10,637,766 | $ | 10,110,992 | $ | 9,729,559 | $ | 9,869,282 | ||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||||||||||||||||||||||||||

| Liabilities and Stockholders’ Equity |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Transaction deposits |

$ | 787,720 | $ | 76 | 0.04 | % | $ | 794,630 | $ | 102 | 0.05 | % | $ | 1,051,199 | $ | 233 | 0.09 | % | $ | 1,003,735 | $ | 253 | 0.10 | % | $ | 941,947 | $ | 244 | 0.10 | % | ||||||||||||||||||||||||||||||

| Savings deposits |

4,365,746 | 3,079 | 0.28 | % | 4,057,792 | 2,863 | 0.28 | % | 3,340,420 | 2,292 | 0.28 | % | 3,246,675 | 2,297 | 0.29 | % | 2,933,904 | 2,299 | 0.31 | % | ||||||||||||||||||||||||||||||||||||||||

| Time deposits |

385,546 | 394 | 0.41 | % | 402,920 | 414 | 0.41 | % | 397,868 | 407 | 0.41 | % | 403,113 | 414 | 0.42 | % | 423,685 | 448 | 0.42 | % | ||||||||||||||||||||||||||||||||||||||||

| Deposits in foreign branches |

348,240 | 309 | 0.35 | % | 357,532 | 320 | 0.36 | % | 340,713 | 296 | 0.35 | % | 335,265 | 281 | 0.34 | % | 362,580 | 321 | 0.35 | % | ||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||||||

| Total interest bearing deposits |

5,887,252 | 3,858 | 0.26 | % | 5,612,874 | 3,699 | 0.26 | % | 5,130,200 | 3,228 | 0.25 | % | 4,988,788 | 3,245 | 0.26 | % | 4,662,116 | 3,312 | 0.28 | % | ||||||||||||||||||||||||||||||||||||||||

| Other borrowings |

314,018 | 161 | 0.20 | % | 539,767 | 275 | 0.20 | % | 727,158 | 354 | 0.20 | % | 1,041,573 | 429 | 0.17 | % | 1,725,129 | 808 | 0.19 | % | ||||||||||||||||||||||||||||||||||||||||

| Subordinated notes |

111,000 | 1,840 | 6.58 | % | 111,000 | 1,829 | 6.54 | % | 111,000 | 1,829 | 6.61 | % | 111,000 | 1,829 | 6.68 | % | 111,000 | 1,829 | 6.56 | % | ||||||||||||||||||||||||||||||||||||||||

| Trust preferred subordinated debentures |

113,406 | 631 | 2.21 | % | 113,406 | 638 | 2.23 | % | 113,406 | 633 | 2.24 | % | 113,406 | 634 | 2.27 | % | 113,406 | 665 | 2.33 | % | ||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||||||

| Total interest bearing liabilities |

6,425,676 | 6,490 | 0.40 | % | 6,377,047 | 6,441 | 0.40 | % | 6,081,764 | 6,044 | 0.40 | % | 6,254,767 | 6,137 | 0.40 | % | 6,611,651 | 6,614 | 0.40 | % | ||||||||||||||||||||||||||||||||||||||||

| Demand deposits |

3,289,307 | 3,124,602 | 2,914,341 | 2,529,927 | 2,356,758 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Other liabilities |

106,461 | 89,640 | 91,608 | 90,538 | 86,308 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Stockholders’ equity |

1,077,822 | 1,046,477 | 1,023,279 | 854,327 | 814,565 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||||||||||||||||||||||||||

| Total liabilities and stockholders’ equity |

$ | 10,899,266 | $ | 10,637,766 | $ | 10,110,992 | $ | 9,729,559 | $ | 9,869,282 | ||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||||||||||||||||||||||||||

| Net interest income |

$ | 111,551 | $ | 108,862 | $ | 101,316 | $ | 98,155 | $ | 101,285 | ||||||||||||||||||||||||||||||||||||||||||||||||||

| Net interest margin |

4.21 | % | 4.21 | % | 4.19 | % | 4.27 | % | 4.27 | % | ||||||||||||||||||||||||||||||||||||||||||||||||||

| (1) | The loan averages include loans on which the accrual of interest has been discontinued and are stated net of unearned income. |

| (2) | Taxable equivalent rates used where applicable. |

10