| SECURITIES AND EXCHANGE COMMISSION | ||

| Washington, D.C. 20549 | ||

| Form N-1A | ||

| REGISTRATION STATEMENT (NO. 2-14336) | ||

| UNDER THE SECURITIES ACT OF 1933 | [X] | |

| Pre-Effective Amendment No. | [ ] | |

| Post-Effective Amendment No. 128 | [X] | |

| and | ||

| REGISTRATION STATEMENT (NO. 811-00834) UNDER THE INVESTMENT COMPANY ACT | ||

| OF 1940 | ||

| Amendment No. 131 | [X] | |

| VANGUARD WINDSOR FUNDS | ||

| (Exact Name of Registrant as Specified in Declaration of Trust) | ||

| P.O. Box 2600, Valley Forge, PA 19482 | ||

| (Address of Principal Executive Office) | ||

| Registrant’s Telephone Number (610) 669-1000 | ||

| Heidi Stam, Esquire | ||

| P.O. Box 876 | ||

| Valley Forge, PA 19482 | ||

| Approximate Date of Proposed Public Offering: | ||

| It is proposed that this filing will become effective (check appropriate box) | ||

| [ ] | immediately upon filing pursuant to paragraph (b) | |

| [X] | on February 25, 2016 pursuant to paragraph (b) | |

| [ ] | 60 days after filing pursuant to paragraph (a)(1) | |

| [ ] | on (date) pursuant to paragraph (a)(1) | |

| [ ] | 75 days after filing pursuant to paragraph (a)(2) | |

| [ ] | on (date) pursuant to paragraph (a)(2) of rule 485 | |

| If appropriate, check the following box: | ||

| [ ] | This post-effective amendment designates a new effective date for a | |

| previously filed post-effective amendment. | ||

![]()

| Vanguard Windsor™ Fund |

| Prospectus |

| February 25, 2016 |

| Investor Shares & Admiral™ Shares |

| Vanguard Windsor Fund Investor Shares (VWNDX) |

| Vanguard Windsor Fund Admiral Shares (VWNEX) |

| This prospectus contains financial data for the Fund through the fiscal year ended October 31, 2015. |

| The Securities and Exchange Commission (SEC) has not approved or disapproved these securities or |

| passed upon the adequacy of this prospectus. Any representation to the contrary is a criminal offense. |

| Contents | |||

| Fund Summary | 1 | Investing With Vanguard | 23 |

| More on the Fund | 6 | Purchasing Shares | 23 |

| The Fund and Vanguard | 13 | Converting Shares | 26 |

| Investment Advisors | 14 | Redeeming Shares | 27 |

| Dividends, Capital Gains, and Taxes | 16 | Exchanging Shares | 31 |

| Share Price | 18 | Frequent-Trading Limitations | 31 |

| Financial Highlights | 20 | Other Rules You Should Know | 33 |

| Fund and Account Updates | 38 | ||

| Contacting Vanguard | 39 | ||

| Additional Information | 40 | ||

| Glossary of Investment Terms | 41 | ||

Fund Summary

Investment Objective

The Fund seeks to provide long-term capital appreciation and income.

Fees and Expenses

The following table describes the fees and expenses you may pay if you buy and hold Investor Shares or Admiral Shares of the Fund.

| Shareholder Fees | ||

| (Fees paid directly from your investment) | ||

| Investor Shares | Admiral Shares | |

| Sales Charge (Load) Imposed on Purchases | None | None |

| Purchase Fee | None | None |

| Sales Charge (Load) Imposed on Reinvested Dividends | None | None |

| Redemption Fee | None | None |

| Account Service Fee (for certain fund account balances below | $20/year | $20/year |

| $10,000) | ||

| Annual Fund Operating Expenses | ||

| (Expenses that you pay each year as a percentage of the value of your investment) | ||

| Investor Shares | Admiral Shares | |

| Management Fees | 0.37% | 0.28% |

| 12b-1 Distribution Fee | None | None |

| Other Expenses | 0.02% | 0.01% |

| Total Annual Fund Operating Expenses | 0.39% | 0.29% |

Examples

The following examples are intended to help you compare the cost of investing in the Fund’s Investor Shares or Admiral Shares with the cost of investing in other mutual funds. They illustrate the hypothetical expenses that you would incur over various periods if you invested $10,000 in the Fund’s shares. These examples assume that the Shares provide a return of 5% each year and that total annual fund operating expenses remain as stated in the preceding table. You would incur these hypothetical expenses whether or not you redeem your investment at the end of the given period. Although your actual costs may be higher or lower, based on these assumptions your costs would be:

| 1 Year | 3 Years | 5 Years | 10 Years | |

| Investor Shares | $40 | $125 | $219 | $493 |

| Admiral Shares | $30 | $93 | $163 | $368 |

1

Portfolio Turnover

The Fund pays transaction costs, such as commissions, when it buys and sells securities (or “turns over” its portfolio). A higher portfolio turnover rate may indicate higher transaction costs and may result in more taxes when Fund shares are held in a taxable account. These costs, which are not reflected in annual fund operating expenses or in the previous expense examples, reduce the Fund’s performance. During the most recent fiscal year, the Fund’s portfolio turnover rate was 28% of the average value of its portfolio.

Principal Investment Strategies

The Fund invests mainly in large- and mid-capitalization companies whose stocks are considered by an advisor to be undervalued. Undervalued stocks are generally those that are out of favor with investors and that the advisor believes are trading at prices that are below average in relation to measures such as earnings and book value. The Fund uses multiple investment advisors.

Principal Risks

An investment in the Fund could lose money over short or even long periods. You should expect the Fund’s share price and total return to fluctuate within a wide range. The Fund is subject to the following risks, which could affect the Fund’s performance:

• Stock market risk, which is the chance that stock prices overall will decline. Stock markets tend to move in cycles, with periods of rising prices and periods of falling prices.

• Investment style risk, which is the chance that returns from large- and mid-capitalization value stocks will trail returns from the overall stock market. Large- and mid-cap stocks each tend to go through cycles of doing better—or worse—than other segments of the stock market or the stock market in general. These periods have, in the past, lasted for as long as several years. Historically, mid-cap stocks have been more volatile in price than large-cap stocks because, among other things, mid-size companies are more sensitive to changing economic conditions.

• Manager risk, which is the chance that poor security selection will cause the Fund to underperform relevant benchmarks or other funds with a similar investment objective. In addition, significant investment in the financial sector subjects the Fund to proportionately higher exposure to the risks of this sector.

An investment in the Fund is not a deposit of a bank and is not insured or guaranteed by the Federal Deposit Insurance Corporation or any other government agency.

2

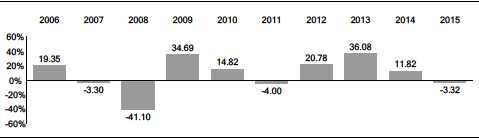

Annual Total Returns

The following bar chart and table are intended to help you understand the risks of investing in the Fund. The bar chart shows how the performance of the Fund‘s Investor Shares has varied from one calendar year to another over the periods shown. The table shows how the average annual total returns of the share classes presented compare with those of a relevant market index, which has investment characteristics similar to those of the Fund. Keep in mind that the Fund’s past performance (before and after taxes) does not indicate how the Fund will perform in the future. Updated performance information is available on our website at vanguard.com/performance or by calling Vanguard toll-free at 800-662-7447.

Annual Total Returns — Vanguard Windsor Fund Investor Shares

During the periods shown in the bar chart, the highest return for a calendar quarter was 18.93% (quarter ended September 30, 2009), and the lowest return for a quarter was –20.60% (quarter ended December 31, 2008).

| Average Annual Total Returns for Periods Ended December 31, 2015 | |||

| 1 Year | 5 Years | 10 Years | |

| Vanguard Windsor Fund Investor Shares | |||

| Return Before Taxes | –3.32% | 11.27% | 6.01% |

| Return After Taxes on Distributions | –5.10 | 10.38 | 5.13 |

| Return After Taxes on Distributions and Sale of Fund Shares | –0.36 | 9.00 | 4.85 |

| Vanguard Windsor Fund Admiral Shares | |||

| Return Before Taxes | –3.24% | 11.37% | 6.12% |

| Russell 1000 Value Index | |||

| (reflects no deduction for fees, expenses, or taxes) | –3.83% | 11.27% | 6.16% |

3

Actual after-tax returns depend on your tax situation and may differ from those shown in the preceding table. When after-tax returns are calculated, it is assumed that the shareholder was in the highest individual federal marginal income tax bracket at the time of each distribution of income or capital gains or upon redemption. State and local income taxes are not reflected in the calculations. Please note that after-tax returns are shown only for the Investor Shares and may differ for each share class. After-tax returns are not relevant for a shareholder who holds fund shares in a tax-deferred account, such as an individual retirement account or a 401(k) plan. Also, figures captioned Return After Taxes on Distributions and Sale of Fund Shares may be higher than other figures for the same period if a capital loss occurs upon redemption and results in an assumed tax deduction for the shareholder.

Investment Advisors

Pzena Investment Management, LLC (Pzena)

Wellington Management Company LLP (Wellington Management)

Portfolio Managers

Richard Pzena, Managing Principal and co-Chief Investment Officer of Pzena. He has co-managed a portion of the Fund since 2012.

John P. Goetz, Managing Principal and co-Chief Investment Officer of Pzena. He has co-managed a portion of the Fund since 2012.

Benjamin S. Silver, CFA, CPA, Principal, co-Director of Research, and Portfolio Manager at Pzena. He has co-managed a portion of the Fund since 2015.

James N. Mordy, Senior Managing Director and Equity Portfolio Manager at Wellington Management. He has managed a portion of the Fund since 2008.

Purchase and Sale of Fund Shares

You may purchase or redeem shares online through our website (vanguard.com), by mail (The Vanguard Group, P.O. Box 1110, Valley Forge, PA 19482-1110), or by telephone (800-662-2739). The minimum investment amount required to open and maintain a Fund account for Investor Shares or Admiral Shares is $3,000 or $50,000, respectively. The minimum investment amount required to add to an existing Fund account is generally $1. Institutional, financial intermediary, and Vanguard retail managed clients should contact Vanguard for information on special eligibility rules that may apply to them regarding Admiral Shares.

4

Tax Information

The Fund’s distributions may be taxable as ordinary income or capital gain. If you are investing through a tax-deferred retirement account, such as an IRA, special tax rules apply.

Payments to Financial Intermediaries

The Fund and its investment advisors do not pay financial intermediaries for sales of Fund shares.

5

More on the Fund

This prospectus describes the principal risks you would face as a Fund shareholder. It is important to keep in mind one of the main axioms of investing: generally, the higher the risk of losing money, the higher the potential reward. The reverse, also, is generally true: the lower the risk, the lower the potential reward. As you consider an investment in any mutual fund, you should take into account your personal tolerance for fluctuations in the securities markets. Look for this

symbol throughout the prospectus. It is used to mark detailed information about the more significant risks that you would confront as a Fund shareholder. To highlight terms and concepts important to mutual fund investors, we have provided Plain Talk® explanations along the way. Reading the prospectus will help you decide whether the Fund is the right investment for you. We suggest that you keep this prospectus for future reference.

symbol throughout the prospectus. It is used to mark detailed information about the more significant risks that you would confront as a Fund shareholder. To highlight terms and concepts important to mutual fund investors, we have provided Plain Talk® explanations along the way. Reading the prospectus will help you decide whether the Fund is the right investment for you. We suggest that you keep this prospectus for future reference.

Share Class Overview

The Fund offers two separate classes of shares: Investor Shares and Admiral Shares.

Both share classes offered by the Fund have the same investment objective, strategies, and policies. However, different share classes have different expenses; as a result, their investment performances will differ.

| Plain Talk About Fund Expenses |

| All mutual funds have operating expenses. These expenses, which are deducted |

| from a fund’s gross income, are expressed as a percentage of the net assets of |

| the fund. Assuming that operating expenses remain as stated in the Fees and |

| Expenses section, Vanguard Windsor Fund’s expense ratios would be as follows: |

| for Investor Shares, 0.39%, or $3.90 per $1,000 of average net assets; for |

| Admiral Shares, 0.29%, or $2.90 per $1,000 of average net assets. The average |

| expense ratio for multi-cap value funds in 2014 was 1.18%, or $11.80 per $1,000 |

| of average net assets (derived from data provided by Lipper, a Thomson Reuters |

| Company, which reports on the mutual fund industry). |

| Plain Talk About Costs of Investing |

| Costs are an important consideration in choosing a mutual fund. That is because |

| you, as a shareholder, pay a proportionate share of the costs of operating a fund, |

| plus any transaction costs incurred when the fund buys or sells securities. These |

| costs can erode a substantial portion of the gross income or the capital |

| appreciation a fund achieves. Even seemingly small differences in expenses can, |

| over time, have a dramatic effect on a fund‘s performance. |

6

The following sections explain the principal investment strategies and policies that the Fund uses in pursuit of its objective. The Fund‘s board of trustees, which oversees the Fund‘s management, may change investment strategies or policies in the interest of shareholders without a shareholder vote, unless those strategies or policies are designated as fundamental.

Market Exposure

The Fund invests mainly in large- and mid-capitalization companies (although the advisors will occasionally select companies with lower market capitalizations) whose stocks are considered by an advisor to be undervalued. Undervalued stocks are generally those that are out of favor with investors and that the advisor believes are trading at prices that are below average in relation to measures such as earnings and book value.

Stocks of publicly traded companies and funds that invest in stocks are often classified according to market value, or market capitalization. These classifications typically include small-cap, mid-cap, and large-cap. It is important to understand that, for both companies and stock funds, market-capitalization ranges change over time. Also, interpretations of size vary, and there are no “official” definitions of small-, mid-, and large-cap, even among Vanguard fund advisors. The asset-weighted median market capitalization of the Fund’s stock holdings as of October 31, 2015, was $32 billion.

The Fund is subject to stock market risk, which is the chance that stock prices overall will decline. Stock markets tend to move in cycles, with periods of rising prices and periods of falling prices.

To illustrate the volatility of stock prices, the following table shows the best, worst, and average annual total returns for the U.S. stock market over various periods as measured by the S&P 500 Index, a widely used barometer of U.S. stock market activity. Total returns consist of dividend income plus change in market price. Note that the returns shown do not include the costs of buying and selling stocks or other expenses that a real-world investment portfolio would incur.

| U.S. Stock Market Returns | ||||

| (1926–2015) | ||||

| 1 Year | 5 Years | 10 Years | 20 Years | |

| Best | 54.2% | 28.6% | 19.9% | 17.8% |

| Worst | –43.1 | –12.4 | –1.4 | 3.1 |

| Average | 11.9 | 10.0 | 10.4 | 11.1 |

7

The table covers all of the rolling 1-, 5-, 10-, and 20-year periods from 1926 through 2015. You can see, for example, that although the average annual return on common stocks for all of the 5-year periods was 10%, average annual returns for individual 5-year periods ranged from –12.4% (from 1928 through 1932) to 28.6% (from 1995 through 1999). These average annual returns reflect past performance of common stocks; you should not regard them as an indication of future performance of either the stock market as a whole or the Fund in particular.

| Plain Talk About Growth Funds and Value Funds |

| Growth investing and value investing are two styles employed by stock-fund |

| managers. Growth funds generally focus on stocks of companies believed to |

| have above-average potential for growth in revenue, earnings, cash flow, or other |

| similar criteria. These stocks typically have low dividend yields and above-average |

| prices in relation to measures such as earnings and book value. Value funds |

| typically emphasize stocks whose prices are below average in relation to those |

| measures; these stocks often have above-average dividend yields. Value stocks |

| also may remain undervalued by the market for long periods of time. Growth and |

| value stocks have historically produced similar long-term returns, though each |

| style has periods when it outperforms the other. |

The Fund is subject to investment style risk, which is the chance that returns from large- and mid-capitalization value stocks will trail returns from the overall stock market. Large- and mid-cap stocks each tend to go through cycles of doing better—or worse—than other segments of the stock market or the stock market in general. These periods have, in the past, lasted for as long as several years. Historically, mid-cap stocks have been more volatile in price than large-cap stocks because, among other things, mid-size companies are more sensitive to changing economic conditions.

Security Selection

The Fund uses multiple investment advisors. Each advisor independently selects and maintains a portfolio of common stocks for the Fund.

Each advisor employs active investment management methods, which means that securities are bought and sold according to the advisor’s evaluations of companies and their financial prospects, the prices of the securities, and the stock market and the economy in general. Each advisor will sell a security when, in the view of the advisor, it is no longer as attractive as an alternative investment or if the advisor deems it to be in the best interest of the Fund‘s. Different advisors may reach different conclusions on the same security.

8

Although each advisor uses a different process to select securities, each is committed to investing in large- and mid-cap stocks that, in the advisor’s opinion, are undervalued. Undervalued stocks are generally those that are out of favor with investors and that the advisor believes are trading at prices that are below average in relation to measures such as earnings and book value.

Wellington Management Company LLP (Wellington Management) relies on the depth and experience of its investment team and supporting global industry analysts to identify stocks that the advisor believes are undervalued by the market. The portfolio typically offers prospective growth of earnings plus a dividend yield comparable with broad market averages, while at the same time being undervalued relative to the market.

Pzena Investment Management, LLC (Pzena) utilizes a fundamental, bottom-up, deep-value-oriented investment strategy. Pzena seeks to buy good businesses at low prices, focusing exclusively on companies that are underperforming their historically demonstrated earnings power.

Pzena conducts intensive fundamental research, investing in companies only when all three of the following criteria are generally met: (1) the company’s identified problems, if any, are temporary; (2) the company’s management has a viable strategy to generate a recovery in earnings; and (3) there is meaningful downside protection in case the earnings recovery does not materialize.

The Fund is subject to manager risk, which is the chance that poor security selection will cause the Fund to underperform relevant benchmarks or other funds with a similar investment objective. In addition, significant investment in the financial sector subjects the Fund to proportionately higher exposure to the risks of this sector.

Other Investment Policies and Risks

In addition to investing in undervalued common stocks, the Fund may make other kinds of investments to achieve its objective.

The Fund typically invests a limited portion, up to 30%, of its assets in foreign securities, which may include depositary receipts. Foreign securities may be traded on U.S. or foreign markets. To the extent that it owns foreign securities, the Fund is subject to country risk and currency risk. Country risk is the chance that world events—such as political upheaval, financial troubles, or natural disasters—will adversely affect the value of securities issued by companies in foreign countries. In addition, the prices of foreign stocks and the prices of U.S. stocks have, at times, moved in opposite directions. Currency risk is the chance that the value of a foreign investment, measured in U.S. dollars, will decrease because of unfavorable changes in currency exchange rates.

9

The Fund may invest in money market instruments; fixed income securities; convertible securities; and other equity securities, such as preferred stocks. The Fund may invest up to 15% of its net assets in illiquid securities.

The Fund may invest, to a limited extent, in derivatives. Generally speaking, a derivative is a financial contract whose value is based on the value of a financial asset (such as a stock, a bond, or a currency), a physical asset (such as gold, oil, or wheat), a market index (such as the S&P 500 Index), or a reference rate (such as LIBOR). Investments in derivatives may subject the Fund to risks different from, and possibly greater than, those of investments directly in the underlying securities, assets, or market indexes. The Fund will not use derivatives for speculation or for the purpose of leveraging (magnifying) investment returns.

The Fund may enter into foreign currency exchange forward contracts, which are a type of derivative. A foreign currency exchange forward contract is an agreement to buy or sell a currency at a specific price on a specific date, usually 30, 60, or 90 days in the future. In other words, the contract guarantees an exchange rate on a given date. Advisors of funds that invest in foreign securities can use these contracts to guard against unfavorable changes in currency exchange rates. These contracts, however, would not prevent the Fund‘s securities from falling in value as a result of risks other than unfavorable currency exchange movements.

| Plain Talk About Derivatives |

| Derivatives can take many forms. Some forms of derivatives—such as exchange- |

| traded futures and options on securities, commodities, or indexes—have been |

| trading on regulated exchanges for decades. These types of derivatives are |

| standardized contracts that can easily be bought and sold and whose market |

| values are determined and published daily. Non-exchange-traded derivatives (such |

| as certain swap agreements and foreign currency exchange forward contracts), |

| on the other hand, tend to be more specialized or complex and may be more |

| difficult to accurately value. |

The Vanguard Group, Inc. (Vanguard) administers a small portion of the Fund‘s assets to facilitate cash flows to and from the Fund‘s advisors. Vanguard typically invests these assets in stock index futures, which are a type of derivative, and/or shares of exchange-traded funds (ETFs), including ETF Shares issued by Vanguard stock funds. These stock index futures and ETFs typically provide returns similar to those of common stocks. Vanguard may also purchase futures or ETFs when doing so will reduce the Fund‘s transaction costs or add value because the instruments are favorably priced. Vanguard receives no additional revenue from Fund assets invested

10

in ETF Shares of other Vanguard funds. Fund assets invested in ETF Shares are excluded when allocating to the Fund its share of the costs of Vanguard operations.

Cash Management

The Fund‘s daily cash balance may be invested in one or more Vanguard CMT Funds, which are very low-cost money market funds. When investing in a Vanguard CMT Fund, the Fund bears its proportionate share of the at-cost expenses of the CMT Fund in which it invests. Vanguard receives no additional revenue from Fund assets invested in a Vanguard CMT Fund.

Temporary Investment Measures

The Fund may temporarily depart from its normal investment policies and strategies when an advisor believes that doing so is in the Fund‘s best interest, so long as the alternative is consistent with the Fund‘s investment objective. For instance, the Fund may invest beyond its normal limits in derivatives or exchange-traded funds that are consistent with the Fund‘s objective when those instruments are more favorably priced or provide needed liquidity, as might be the case if the Fund is transitioning assets from one advisor to another or receives large cash flows that it cannot prudently invest immediately.

In addition, the Fund may take temporary defensive positions that are inconsistent with its normal investment policies and strategies—for instance, by allocating substantial assets to cash equivalent investments or other less volatile instruments—in response to adverse or unusual market, economic, political, or other conditions. In doing so, the Fund may succeed in avoiding losses but may otherwise fail to achieve its investment objective.

Frequent Trading or Market-Timing

Background. Some investors try to profit from strategies involving frequent trading of mutual fund shares, such as market-timing. For funds holding foreign securities, investors may try to take advantage of an anticipated difference between the price of the fund’s shares and price movements in overseas markets, a practice also known as time-zone arbitrage. Investors also may try to engage in frequent trading of funds holding investments such as small-cap stocks and high-yield bonds. As money is shifted into and out of a fund by a shareholder engaging in frequent trading, the fund incurs costs for buying and selling securities, resulting in increased brokerage and administrative costs. These costs are borne by all fund shareholders, including the long-term investors who do not generate the costs. In addition, frequent trading may interfere with an advisor’s ability to efficiently manage the fund.

Policies to address frequent trading. The Vanguard funds (other than money market funds and short-term bond funds, but including Vanguard Short-Term Inflation-

11

Protected Securities Index Fund) do not knowingly accommodate frequent trading. The board of trustees of each Vanguard fund (other than money market funds and short-term bond funds, but including Vanguard Short-Term Inflation-Protected Securities Index Fund) has adopted policies and procedures reasonably designed to detect and discourage frequent trading and, in some cases, to compensate the fund for the costs associated with it. These policies and procedures do not apply to Vanguard ETF® Shares because frequent trading in ETF Shares generally does not disrupt portfolio management or otherwise harm fund shareholders. Although there is no assurance that Vanguard will be able to detect or prevent frequent trading or market-timing in all circumstances, the following policies have been adopted to address these issues:

• Each Vanguard fund reserves the right to reject any purchase request—including exchanges from other Vanguard funds—without notice and regardless of size. For example, a purchase request could be rejected because the investor has a history of frequent trading or if Vanguard determines that such purchase may negatively affect a fund’s operation or performance.

• Each Vanguard fund (other than money market funds and short-term bond funds, but including Vanguard Short-Term Inflation-Protected Securities Index Fund) generally prohibits, except as otherwise noted in the Investing With Vanguard section, an investor’s purchases or exchanges into a fund account for 30 calendar days (60 calendar days for participants in employer-sponsored defined contribution plans recordkept directly by Vanguard) after the investor has redeemed or exchanged out of that fund account.

• Certain Vanguard funds charge shareholders purchase and/or redemption fees on transactions.

See the Investing With Vanguard section of this prospectus for further details on Vanguard’s transaction policies.

Each Vanguard fund (other than money market funds), in determining its net asset value, will use fair-value pricing when appropriate, as described in the Share Price section. Fair-value pricing may reduce or eliminate the profitability of certain frequent-trading strategies.

Do not invest with Vanguard if you are a market-timer.

12

Turnover Rate

Although the Fund generally seeks to invest for the long term, it may sell securities regardless of how long they have been held. The Financial Highlights section of this prospectus shows historical turnover rates for the Fund. A turnover rate of 100%, for example, would mean that the Fund had sold and replaced securities valued at 100% of its net assets within a one-year period. The average turnover rate for large-cap value funds was approximately 56%, as reported by Morningstar, Inc., on October 31, 2015.

| Plain Talk About Turnover Rate |

| Before investing in a mutual fund, you should review its turnover rate. This gives |

| an indication of how transaction costs, which are not included in the fund’s |

| expense ratio, could affect the fund’s future returns. In general, the greater the |

| volume of buying and selling by the fund, the greater the impact that brokerage |

| commissions and other transaction costs will have on its return. Also, funds with |

| high turnover rates may be more likely to generate capital gains, including short- |

| term capital gains, that must be distributed to shareholders as taxable income. |

The Fund and Vanguard

The Fund is a member of The Vanguard Group, a family of more than 190 mutual funds holding assets of approximately $3.1 trillion. All of the funds that are members of The Vanguard Group (other than funds of funds) share in the expenses associated with administrative services and business operations, such as personnel, office space, and equipment.

Vanguard Marketing Corporation provides marketing services to the funds. Although shareholders do not pay sales commissions or 12b-1 distribution fees, each fund (other than a fund of funds) or each share class of a fund (in the case of a fund with multiple share classes) pays its allocated share of the Vanguard funds’ marketing costs.

| Plain Talk About Vanguard’s Unique Corporate Structure |

| The Vanguard Group is truly a mutual mutual fund company. It is owned jointly by |

| the funds it oversees and thus indirectly by the shareholders in those funds. |

| Most other mutual funds are operated by management companies that may be |

| owned by one person, by a private group of individuals, or by public investors |

| who own the management company’s stock. The management fees charged by |

| these companies include a profit component over and above the companies’ cost |

| of providing services. By contrast, Vanguard provides services to its member |

| funds on an at-cost basis, with no profit component, which helps to keep the |

| funds’ expenses low. |

13

Investment Advisors

The Fund uses a multimanager approach. Each advisor independently manages its assigned portion of the Fund’s assets, subject to the supervision and oversight of Vanguard and the Fund’s board of trustees. The board of trustees designates the proportion of Fund assets to be managed by each advisor and may change these proportions at any time.

• Pzena Investment Management, LLC, 320 Park Avenue, 8th Floor, New York, NY

10022, is a global investment management firm founded in 1995. Pzena focuses exclusively on a deep value investment approach. The members of the firm’s executive committee and other employees collectively own a majority of the firm. As of October 31, 2015, Pzena managed approximately $25.5 billion in assets.

• Wellington Management Company LLP, 280 Congress Street, Boston, MA 02210, a Delaware limited liability partnership, is an investment counseling firm that provides investment services to investment companies, employee benefit plans, endowments, foundations, and other institutions. Wellington Management and its predecessor organizations have provided investment advisory services for over 80 years. Wellington Management is owned by the partners of Wellington Management Group LLP, a Massachusetts limited liability partnership. As of October 31, 2015, Wellington Management had investment management authority with respect to approximately $898 billion in client assets.

The Fund pays each of its investment advisors a base fee plus or minus a performance adjustment. Each base fee, which is paid quarterly, is a percentage of average daily net assets managed by the advisor during the most recent fiscal quarter. The base fee has breakpoints, which means that the percentage declines as assets go up. The performance adjustment, also paid quarterly, is based on the cumulative total return of each advisor’s portion of the Fund relative to that of the Russell 1000 Value Index (for Pzena) or the S&P 500 Index (for Wellington Management) over the preceding 36-month period. When the performance adjustment is positive, the Fund’s expenses increase; when it is negative, expenses decrease.

For the fiscal year ended October 31, 2015, the aggregate advisory fee represented an effective annual rate of 0.13% of the Fund’s average net assets before a performance-based increase of 0.03%.

14

Under the terms of an SEC exemption, the Fund’s board of trustees may, without prior approval from shareholders, change the terms of an advisory agreement or hire a new investment advisor—either as a replacement for an existing advisor or as an additional advisor. Any significant change in the Fund’s advisory arrangements will be communicated to shareholders in writing. In addition, as the Fund’s sponsor and overall manager, Vanguard may provide investment advisory services to the Fund, on an at-cost basis, at any time. Vanguard may also recommend to the board of trustees that an advisor be hired, terminated, or replaced or that the terms of an existing advisory agreement be revised.

For a discussion of why the board of trustees approved the Fund’s investment advisory agreements, see the most recent semiannual report to shareholders covering the fiscal period ended April 30.

The managers primarily responsible for the day-to-day management of the Fund are:

Richard Pzena, Managing Principal and co-Chief Investment Officer of Pzena. He has worked in investment management since 1984, has managed investment portfolios for Pzena since 1996, and has co-managed a portion of the Fund since 2012. Education: B.S. and M.B.A., The Wharton School of the University of Pennsylvania.

John P. Goetz, Managing Principal and co-Chief Investment Officer of Pzena. He has worked in investment management since 1979, has managed investment portfolios for Pzena since 1996, and has co-managed a portion of the Fund since 2012. Education: B.A., Wheaton College; M.B.A., the Kellogg School at Northwestern University.

Benjamin S. Silver, CFA, CPA, Principal, co-Director of Research, and Portfolio Manager at Pzena. He has worked in investment management since 1999, has been with Pzena since 2001, has managed investment portfolios since 2006, and has co-managed a portion of the Fund since 2015. Education: B.S., Yeshiva University.

James N. Mordy, Senior Managing Director and Equity Portfolio Manager at Wellington Management. He has been with Wellington Management and has worked on the Windsor Fund investment team since 1985, has managed investment portfolios since 1997, and has managed a portion of the Fund since 2008. Education: B.A., Stanford University; M.B.A., The Wharton School of the University of Pennsylvania.

The Statement of Additional Information provides information about each portfolio manager’s compensation, other accounts under management, and ownership of shares of the Fund.

15

Dividends, Capital Gains, and Taxes

Fund Distributions

The Fund distributes to shareholders virtually all of its net income (interest and dividends, less expenses) as well as any net short-term or long-term capital gains realized from the sale of its holdings. Income dividends generally are distributed semiannually in June and December; capital gains distributions, if any, generally occur annually in December. In addition, each Fund may occasionally make a supplemental distribution at some other time during the year. You can receive distributions of income or capital gains in cash, or you can have them automatically reinvested in more shares of the Fund.

| Plain Talk About Distributions |

| As a shareholder, you are entitled to your portion of a fund’s income from interest |

| and dividends as well as capital gains from the fund’s sale of investments. |

| Income consists of both the dividends that the fund earns from any stock |

| holdings and the interest it receives from any money market and bond |

| investments. Capital gains are realized whenever the fund sells securities for |

| higher prices than it paid for them. These capital gains are either short-term or |

| long-term, depending on whether the fund held the securities for one year or less |

| or for more than one year. |

Basic Tax Points

Vanguard will send you a statement each year showing the tax status of all of your distributions. In addition, investors in taxable accounts should be aware of the following basic federal income tax points:

• Distributions are taxable to you whether or not you reinvest these amounts in additional Fund shares.

• Distributions declared in December—if paid to you by the end of January—are taxable as if received in December.

• Any dividend distribution or short-term capital gains distribution that you receive is taxable to you as ordinary income. If you are an individual and meet certain holding-period requirements with respect to your Fund shares, you may be eligible for reduced tax rates on “qualified dividend income,” if any, distributed by the Fund.

• Any distribution of net long-term capital gains is taxable to you as long-term capital gains, no matter how long you have owned shares in the Fund.

• Capital gains distributions may vary considerably from year to year as a result of the Fund‘s normal investment activities and cash flows.

16

- A sale or exchange of Fund shares is a taxable event. This means that you may have

- capital gain to report as income, or a capital loss to report as a deduction, when you

complete your tax return.

• Any conversion between classes of shares of the same fund is a nontaxable event. By contrast, an exchange between classes of shares of different funds is a taxable event.

Individuals, trusts, and estates whose income exceeds certain threshold amounts are subject to a 3.8% Medicare contribution tax on “net investment income.” Net investment income takes into account distributions paid by the Fund and capital gains from any sale or exchange of Fund shares.

Dividend distributions and capital gains distributions that you receive, as well as your gains or losses from any sale or exchange of Fund shares, may be subject to state and local income taxes.

This prospectus provides general tax information only. If you are investing through a tax-deferred retirement account, such as an IRA, special tax rules apply. Please consult your tax advisor for detailed information about any tax consequences for you.

| Plain Talk About Buying a Dividend |

| Unless you are investing through a tax-deferred retirement account (such as an |

| IRA), you should consider avoiding a purchase of fund shares shortly before the |

| fund makes a distribution, because doing so can cost you money in taxes. This is |

| known as “buying a dividend.” For example: On December 15, you invest $5,000, |

| buying 250 shares for $20 each. If the fund pays a distribution of $1 per share on |

| December 16, its share price will drop to $19 (not counting market change). You |

| still have only $5,000 (250 shares x $19 = $4,750 in share value, plus 250 shares |

| x $1 = $250 in distributions), but you owe tax on the $250 distribution you |

| received—even if you reinvest it in more shares. To avoid buying a dividend, check |

| a fund’s distribution schedule before you invest. |

17

General Information

Backup withholding. By law, Vanguard must withhold 28% of any taxable distributions or redemptions from your account if you do not:

- Provide us with your correct taxpayer identification number.

- Certify that the taxpayer identification number is correct.

- Confirm that you are not subject to backup withholding.

Similarly, Vanguard must withhold taxes from your account if the IRS instructs us to do so.

Foreign investors. Vanguard funds offered for sale in the United States (Vanguard U.S. funds), including the Fund offered in this prospectus, are not widely available outside the United States. Non-U.S. investors should be aware that U.S. withholding and estate taxes and certain U.S. tax reporting requirements may apply to any investments in Vanguard U.S. funds. Foreign investors should visit the Non-U.S. Investors page on our website at vanguard.com for information on Vanguard’s non-U.S. products.

Invalid addresses. If a dividend distribution or capital gains distribution check mailed to your address of record is returned as undeliverable, Vanguard will automatically reinvest the distribution and all future distributions until you provide us with a valid mailing address. Reinvestments will receive the net asset value calculated on the date of the reinvestment.

Share Price

Share price, also known as net asset value (NAV), is calculated each business day as of the close of regular trading on the New York Stock Exchange (NYSE), generally 4 p.m., Eastern time. Each share class has its own NAV, which is computed by dividing the total assets, minus liabilities, allocated to the share class by the number of Fund shares outstanding for that class. On U.S. holidays or other days when the NYSE is closed, the NAV is not calculated, and the Fund does not sell or redeem shares. However, on those days the value of the Fund’s assets may be affected to the extent that the Fund holds securities that change in value on those days (such as foreign securities that trade on foreign markets that are open).

Stocks held by a Vanguard fund are valued at their market value when reliable market quotations are readily available from the principal exchange or market on which they are traded. Such securities are generally valued at their official closing price, the last reported sales price, or if there were no sales that day, the mean between the closing bid and asking prices. Certain short-term debt instruments used to manage a fund’s cash may be valued at amortized cost when it approximates fair value. The values of any foreign securities held by a fund are converted into U.S. dollars using an exchange rate obtained from an independent third party as of the close of regular trading on the

18

NYSE. The values of any mutual fund shares held by a fund are based on the NAVs of the shares. The values of any ETF or closed-end fund shares held by a fund are based on the market value of the shares.

When a fund determines that market quotations either are not readily available or do not accurately reflect the value of a security, the security is priced at its fair value (the amount that the owner might reasonably expect to receive upon the current sale of the security). A fund also will use fair-value pricing if the value of a security it holds has been materially affected by events occurring before the fund’s pricing time but after the close of the principal exchange or market on which the security is traded. This most commonly occurs with foreign securities, which may trade on foreign exchanges that close many hours before the fund’s pricing time. Intervening events might be company-specific (e.g., earnings report, merger announcement) or country-specific or regional/global (e.g., natural disaster, economic or political news, act of terrorism, interest rate change). Intervening events include price movements in U.S. markets that exceed a specified threshold or that are otherwise deemed to affect the value of foreign securities. Fair-value pricing may be used for domestic securities—for example, if (1) trading in a security is halted and does not resume before the fund’s pricing time or a security does not trade in the course of a day and (2) the fund holds enough of the security that its price could affect the NAV.

Fair-value prices are determined by Vanguard according to procedures adopted by the board of trustees. When fair-value pricing is employed, the prices of securities used by a fund to calculate the NAV may differ from quoted or published prices for the same securities.

Vanguard fund share prices are published daily on our website at vanguard.com/prices.

19

Financial Highlights

The following financial highlights tables are intended to help you understand the Fund’s financial performance for the periods shown, and certain information reflects financial results for a single Fund share. The total returns in each table represent the rate that an investor would have earned or lost each period on an investment in the Fund (assuming reinvestment of all distributions). This information has been obtained from the financial statements audited by PricewaterhouseCoopers LLP, an independent registered public accounting firm, whose report—along with the Fund’s financial statements—is included in the Fund‘s most recent annual report to shareholders. You may obtain a free copy of the latest annual or semiannual report by visiting vanguard.com or by contacting Vanguard by telephone or mail.

| Plain Talk About How to Read the Financial Highlights Tables |

| This explanation uses the Fund’s Investor Shares as an example. The |

| Investor Shares began fiscal year 2015 with a net asset value (share price) of |

| $21.98 per share. During the year, each Investor Share earned $0.356 from |

| investment income (interest and dividends) and $0.026 from investments that |

| had appreciated in value or that were sold for higher prices than the Fund paid |

| for them. |

| Shareholders received $1.302 per share in the form of dividend and capital gains |

| distributions. A portion of each year’s distributions may come from the prior |

| year’s income or capital gains. |

| The share price at the end of the year was $21.06, reflecting earnings of $0.382 |

| per share and distributions of $1.302 per share. This was a decrease of $0.92 per |

| share (from $21.98 at the beginning of the year to $21.06 at the end of the year). |

| For a shareholder who reinvested the distributions in the purchase of more |

| shares, the total return was 1.76% for the year. |

| As of October 31, 2015, the Investor Shares had approximately $5.4 billion in net |

| assets. For the year, the expense ratio was 0.39% ($3.90 per $1,000 of net |

| assets), and the net investment income amounted to 1.64% of average net |

| assets. The Fund sold and replaced securities valued at 28% of its net assets. |

20

| Windsor Fund Investor Shares | |||||

| Year Ended October 31, | |||||

| For a Share Outstanding Throughout Each Period | 2015 | 2014 | 2013 | 2012 | 2011 |

| Net Asset Value, Beginning of Period | $21.98 | $19.50 | $14.66 | $12.92 | $12.56 |

| Investment Operations | |||||

| Net Investment Income | .356 1 | .279 | .255 | .252 | .184 |

| Net Realized and Unrealized Gain (Loss) | |||||

| on Investments | .026 | 2.467 | 4.839 | 1.729 | .346 |

| Total from Investment Operations | .382 | 2.746 | 5.094 | 1.981 | .530 |

| Distributions | |||||

| Dividends from Net Investment Income | (.339) | (.266) | (.254) | (.241) | (.170) |

| Distributions from Realized Capital Gains | (.963) | — | — | — | — |

| Total Distributions | (1.302) | (.266) | (.254) | (.241) | (.170) |

| Net Asset Value, End of Period | $21.06 | $21.98 | $19.50 | $14.66 | $12.92 |

| Total Return2 | 1.76% | 14.14% | 35.17% | 15.56% | 4.15% |

| Ratios/Supplemental Data | |||||

| Net Assets, End of Period (Millions) | $5,379 | $7,179 | $7,126 | $6,711 | $6,736 |

| Ratio of Total Expenses to Average Net Assets3 | 0.39% | 0.38% | 0.37% | 0.35% | 0.39% |

| Ratio of Net Investment Income to Average | |||||

| Net Assets | 1.64%1 | 1.33% | 1.49% | 1.80% | 1.34% |

| Portfolio Turnover Rate | 28% | 38% | 40% | 68% | 49% |

| 1 Net investment income per share and the ratio of net investment income to average net assets include $0.052 and 0.24%, | |||||

| respectively, resulting from income received from Covidien Ltd. in January 2015. | |||||

| 2 Total returns do not include account service fees that may have applied in the periods shown. | |||||

| 3 Includes performance-based investment advisory fee increases (decreases) of 0.03%, 0.03%, 0.02%, (0.01%), and 0.03%. | |||||

21

| Windsor Fund Admiral Shares | |||||

| Year Ended October 31, | |||||

| For a Share Outstanding Throughout Each Period | 2015 | 2014 | 2013 | 2012 | 2011 |

| Net Asset Value, Beginning of Period | $74.17 | $65.81 | $49.47 | $43.59 | $42.37 |

| Investment Operations | |||||

| Net Investment Income | 1.2911 | 1.016 | .924 | .900 | .664 |

| Net Realized and Unrealized Gain (Loss) | |||||

| on Investments | .062 | 8.314 | 16.329 | 5.844 | 1.171 |

| Total from Investment Operations | 1.353 | 9.330 | 17.253 | 6.744 | 1.835 |

| Distributions | |||||

| Dividends from Net Investment Income | (1.235) | (.970) | (.913) | (.864) | (.615) |

| Distributions from Realized Capital Gains | (3.248) | — | — | — | — |

| Total Distributions | (4.483) | (.970) | (.913) | (.864) | (.615) |

| Net Asset Value, End of Period | $71.04 | $74.17 | $65.81 | $49.47 | $43.59 |

| Total Return2 | 1.85% | 14.24% | 35.32% | 15.71% | 4.26% |

| Ratios/Supplemental Data | |||||

| Net Assets, End of Period (Millions) | $12,206 | $10,884 | $9,144 | $5,795 | $4,994 |

| Ratio of Total Expenses to Average Net Assets3 | 0.29% | 0.28% | 0.27% | 0.25% | 0.29% |

| Ratio of Net Investment Income to Average | |||||

| Net Assets | 1.74%1 | 1.43% | 1.59% | 1.90% | 1.44% |

| Portfolio Turnover Rate | 28% | 38% | 40% | 68% | 49% |

| 1 Net investment income per share and the ratio of net investment income to average net assets include $0.177 and 0.24%, | |||||

| respectively, resulting from income received from Covidien Ltd. in January 2015. | |||||

| 2 Total returns do not include account service fees that may have applied in the periods shown. | |||||

| 3 Includes performance-based investment advisory fee increases (decreases) of 0.03%, 0.03%, 0.02%, (0.01%), and 0.03%. | |||||

22

Investing With Vanguard

This section of the prospectus explains the basics of doing business with Vanguard. Vanguard fund shares can be held directly with Vanguard or indirectly through an intermediary, such as a bank, a broker, or an investment advisor. If you hold Vanguard fund shares directly with Vanguard, you should carefully read each topic within this section that pertains to your relationship with Vanguard. If you hold Vanguard fund shares indirectly through an intermediary (including shares held through a Vanguard brokerage account), please see Investing With Vanguard Through Other Firms, and also refer to your account agreement with the intermediary for information about transacting in that account. Vanguard reserves the right to change the following policies without notice. Please call or check online for current information. See

Contacting Vanguard.

For Vanguard fund shares held directly with Vanguard, each fund you hold in an account is a separate “fund account.” For example, if you hold three funds in a nonretirement account titled in your own name, two funds in a nonretirement account titled jointly with your spouse, and one fund in an individual retirement account, you have six fund accounts—and this is true even if you hold the same fund in multiple accounts. Note that each reference to “you” in this prospectus applies to any one or more registered account owners or persons authorized to transact on your account.

Purchasing Shares

Vanguard reserves the right, without notice, to increase or decrease the minimum amount required to open, convert shares to, or maintain a fund account or to add to an existing fund account.

Investment minimums may differ for certain categories of investors.

Account Minimums for Investor Shares To open and maintain an account. $3,000.

To add to an existing account. Generally $1.

Account Minimums for Admiral Shares

To open and maintain an account. $50,000. If you request Admiral Shares when you open a new account but the investment amount does not meet the account minimum for Admiral Shares, your investment will be placed in Investor Shares of the Fund. Institutional, financial intermediary, and Vanguard retail managed clients should contact Vanguard for information on special eligibility rules that may apply to them.

To add to an existing account. Generally $1.

23

How to Initiate a Purchase Request

Be sure to check Exchanging Shares, Frequent-Trading Limitations, and Other Rules You Should Know before placing your purchase request.

Online. You may open certain types of accounts, request a purchase of shares, and request an exchange through our website or our mobile application if you are registered for online access.

By telephone. You may call Vanguard to begin the account registration process or request that the account-opening forms be sent to you. You may also call Vanguard to request a purchase of shares in your account or to request an exchange. See

Contacting Vanguard.

By mail. You may send Vanguard your account registration form and check to open a new fund account. To add to an existing fund account, you may send your check with an Invest-by-Mail form (from a transaction confirmation or your account statement), with a deposit slip (available online), or with a written request. You may also send a written request to Vanguard to make an exchange. For a list of Vanguard addresses, see Contacting Vanguard.

How to Pay for a Purchase

By electronic bank transfer. You may purchase shares of a Vanguard fund through an electronic transfer of money from a bank account. To establish the electronic bank transfer service on an account, you must designate the bank account online, complete a special form, or fill out the appropriate section of your account registration form. After the service is set up on your account, you can purchase shares by electronic bank transfer on a regular schedule (Automatic Investment Plan) or upon request. Your purchase request can be initiated online (if you are registered for online access), by telephone, or by mail.

By wire. Wiring instructions vary for different types of purchases. Please call Vanguard for instructions and policies on purchasing shares by wire. See Contacting Vanguard.

By check. You may make initial or additional purchases to your fund account by sending a check or by utilizing our mobile application if you are registered for online access. Also see How to Initiate a Purchase Request. Make your check payable to Vanguard and include the appropriate fund number (e.g., Vanguard—xx). For a list of Fund numbers (for share classes in this prospectus), see Additional Information.

By exchange. You may purchase shares of a Vanguard fund using the proceeds from the simultaneous redemption of shares of another Vanguard fund. You may initiate an exchange online (if you are registered for online access), by telephone, or by mail. See

Exchanging Shares.

24

Trade Date

The trade date for any purchase request received in good order will depend on the day and time Vanguard receives your request, the manner in which you are paying, and the type of fund you are purchasing. Your purchase will be executed using the net asset value (NAV) as calculated on the trade date. NAVs are calculated only on days that the New York Stock Exchange (NYSE) is open for trading (a business day).

For purchases by check into all funds other than money market funds and for purchases by exchange, wire, or electronic bank transfer (not using an Automatic Investment Plan) into all funds: If the purchase request is received by Vanguard on a business day before the close of regular trading on the NYSE (generally 4 p.m., Eastern time), the trade date for the purchase will be the same day. If the purchase request is received on a business day after the close of regular trading on the NYSE, or on a nonbusiness day, the trade date for the purchase will be the next business day.

For purchases by check into money market funds: If the purchase request is received by Vanguard on a business day before the close of regular trading on the NYSE (generally 4 p.m., Eastern time), the trade date for the purchase will be the next business day. If the purchase request is received on a business day after the close of regular trading on the NYSE, or on a nonbusiness day, the trade date for the purchase will be the second business day following the day Vanguard receives the purchase request. Because money market instruments must be purchased with federal funds and it takes a money market mutual fund one business day to convert check proceeds into federal funds, the trade date for the purchase will be one business day later than for other funds.

For purchases by electronic bank transfer using an Automatic Investment Plan: Your trade date generally will be the date you selected for withdrawal of funds from your designated bank account. Your bank account generally will be debited on the business day after your trade date. If the date you selected for withdrawal of funds from your bank account falls on a weekend, holiday, or other nonbusiness day, your trade date generally will be the previous business day. For retirement accounts, if the date you selected for withdrawal of funds from your designated bank account falls on the last business day of the year, your trade date will be the first business day of the following year. Please note that if you select the first of the month for automated withdrawals from your designated bank account, trades designated for January 1 will receive the next business day’s trade date.

If your purchase request is not accurate and complete, it may be rejected. See Other Rules You Should Know—Good Order.

For further information about purchase transactions, consult our website at vanguard.com or see Contacting Vanguard.

25

Other Purchase Rules You Should Know

Admiral Shares. Admiral Shares generally are not available for SIMPLE IRAs, Vanguard Individual 401(k) Plans, and Vanguard retail-serviced Individual 403(b)(7) Custodial Accounts.

Check purchases. All purchase checks must be written in U.S. dollars and must be drawn on a U.S. bank. Vanguard does not accept cash, traveler’s checks, or money orders. In addition, Vanguard may refuse “starter checks” and checks that are not made payable to Vanguard.

New accounts. We are required by law to obtain from you certain personal information that we will use to verify your identity. If you do not provide the information, we may not be able to open your account. If we are unable to verify your identity, Vanguard reserves the right, without notice, to close your account or take such other steps as we deem reasonable. Certain types of accounts may require additional documentation.

Refused or rejected purchase requests. Vanguard reserves the right to stop selling fund shares or to reject any purchase request at any time and without notice, including, but not limited to, purchases requested by exchange from another Vanguard fund. This also includes the right to reject any purchase request because the investor has a history of frequent trading or because the purchase may negatively affect a fund’s operation or performance.

Large purchases. Call Vanguard before attempting to invest a large dollar amount.

No cancellations. Vanguard will not accept your request to cancel any purchase request once processing has begun. Please be careful when placing a purchase request.

Converting Shares

When a conversion occurs, you receive shares of one class in place of shares of another class of the same fund. At the time of conversion, the dollar value of the “new” shares you receive equals the dollar value of the “old” shares that were converted. In other words, the conversion has no effect on the value of your investment in the fund at the time of the conversion. However, the number of shares you own after the conversion may be greater than or less than the number of shares you owned before the conversion, depending on the NAVs of the two share classes.

Vanguard will not accept your request to cancel any self-directed conversion request once processing has begun. Please be careful when placing a conversion request.

A conversion between share classes of the same fund is a nontaxable event.

26

Trade Date

The trade date for any conversion request received in good order will depend on the day and time Vanguard receives your request. Your conversion will be executed using the NAVs of the different share classes on the trade date. NAVs are calculated only on days that the NYSE is open for trading (a business day).

For a conversion request received by Vanguard on a business day before the close of regular trading on the NYSE (generally 4 p.m., Eastern time), the trade date will be the same day. For a conversion request received on a business day after the close of regular trading on the NYSE, or on a nonbusiness day, the trade date will be the next business day. See Other Rules You Should Know.

Conversions From Investor Shares to Admiral Shares

Self-directed conversions. If your account balance in the Fund is at least $50,000, you may ask Vanguard to convert your Investor Shares to Admiral Shares. You may request a conversion through our website (if you are registered for online access), by telephone, or by mail. Institutional, financial intermediary, and Vanguard retail managed clients should contact Vanguard for information on special eligibility rules that may apply to them. See Contacting Vanguard.

Automatic conversions. Vanguard conducts periodic reviews of account balances and may, if your account balance in the Fund exceeds $50,000, automatically convert your Investor Shares to Admiral Shares. You will be notified before an automatic conversion occurs and will have an opportunity to instruct Vanguard not to effect the conversion. Institutional, financial intermediary, and Vanguard retail managed clients should contact Vanguard for information on special eligibility rules that may apply to them.

Mandatory Conversions to Investor Shares

If an account no longer meets the balance requirements for Admiral Shares, Vanguard may automatically convert the shares in the account to Investor Shares. A decline in the account balance because of market movement may result in such a conversion. Vanguard will notify the investor in writing before any mandatory conversion occurs.

Redeeming Shares

How to Initiate a Redemption Request

Be sure to check Exchanging Shares, Frequent-Trading Limitations, and Other Rules You Should Know before placing your redemption request.

Online. You may request a redemption of shares or request an exchange through our website or our mobile application if you are registered for online access.

27

By telephone. You may call Vanguard to request a redemption of shares or an exchange. See Contacting Vanguard.

By mail. You may send a written request to Vanguard to redeem from a fund account or to make an exchange. See Contacting Vanguard.

How to Receive Redemption Proceeds

By electronic bank transfer. You may have the proceeds of a fund redemption sent directly to a designated bank account. To establish the electronic bank transfer service on an account, you must designate a bank account online, complete a special form, or fill out the appropriate section of your account registration form. After the service is set up on your account, you can redeem shares by electronic bank transfer on a regular schedule (Automatic Withdrawal Plan) or upon request. Your redemption request can be initiated online (if you are registered for online access), by telephone, or by mail.

By wire. To receive your proceeds by wire, you may instruct Vanguard to wire your redemption proceeds ($100 minimum) to a previously designated bank account. To establish the wire redemption service, you generally must designate a bank account online, complete a special form, or fill out the appropriate section of your account registration form.

By exchange. You may have the proceeds of a Vanguard fund redemption invested directly in shares of another Vanguard fund. You may initiate an exchange online (if you are registered for online access), by telephone, or by mail. See Exchanging Shares.

By check. If you have not chosen another redemption method, Vanguard will mail you a redemption check, generally payable to all registered account owners, normally within two business days of your trade date, and generally to the address of record.

Trade Date

The trade date for any redemption request received in good order will depend on the day and time Vanguard receives your request and the manner in which you are redeeming. Your redemption will be executed using the NAV as calculated on the trade date. NAVs are calculated only on days that the NYSE is open for trading (a business day).

For redemptions by check, exchange, or wire: If the redemption request is received by Vanguard on a business day before the close of regular trading on the NYSE (generally 4 p.m., Eastern time), the trade date will be the same day. If the redemption request is received on a business day after the close of regular trading on the NYSE, or on a nonbusiness day, the trade date will be the next business day.

• Note on timing of wire redemptions from money market funds: For telephone requests received by Vanguard on a business day before 10:45 a.m., Eastern time

28

(2 p.m., Eastern time, for Vanguard Prime Money Market Fund), the redemption proceeds generally will leave Vanguard by the close of business the same day. For telephone requests received by Vanguard on a business day after those cut-off times, or on a nonbusiness day, and for all requests other than by telephone, the redemption proceeds generally will leave Vanguard by the close of business on the next business day.

• Note on timing of wire redemptions from all other funds: For requests received by Vanguard on a business day before the close of regular trading on the NYSE (generally 4 p.m., Eastern time), the redemption proceeds generally will leave Vanguard by the close of business on the next business day. For requests received by Vanguard on a business day after the close of regular trading on the NYSE, or on a nonbusiness day, the redemption proceeds generally will leave Vanguard by the close of business on the second business day after Vanguard receives the request.

For redemptions by electronic bank transfer using an Automatic Withdrawal Plan: Your trade date generally will be the date you selected for withdrawal of funds (redemption of shares) from your Vanguard account. Proceeds of redeemed shares generally will be credited to your designated bank account two business days after your trade date. If the date you selected for withdrawal of funds from your Vanguard account falls on a weekend, holiday, or other nonbusiness day, your trade date generally will be the previous business day. For retirement accounts, if the date you selected for withdrawal of funds from your Vanguard account falls on the last day of the year and if that date is a holiday, your trade date will be the first business day of the following year. Please note that if you designate the first of the month for automated withdrawals, trades designated for January 1 will receive the next business day’s trade date.

For redemptions by electronic bank transfer not using an Automatic Withdrawal Plan: If the redemption request is received by Vanguard on a business day before the close of regular trading on the NYSE (generally 4 p.m., Eastern time), the trade date will be the same day. If the redemption request is received on a business day after the close of regular trading on the NYSE, or on a nonbusiness day, the trade date will be the next business day.

If your redemption request is not accurate and complete, it may be rejected. If we are unable to send your redemption proceeds by wire or electronic bank transfer because the receiving institution rejects the transfer, Vanguard will make additional efforts to complete your transaction. If Vanguard is still unable to complete the transaction, we may send the proceeds of the redemption to you by check, generally payable to all registered account owners, or use your proceeds to purchase new shares of the fund from which you sold shares for the purpose of the wire or electronic bank transfer transaction. See Other Rules You Should Know—Good Order.

29

For further information about redemption transactions, consult our website at vanguard.com or see Contacting Vanguard.

Other Redemption Rules You Should Know

Documentation for certain accounts. Special documentation may be required to redeem from certain types of accounts, such as trust, corporate, nonprofit, or retirement accounts. Please call us before attempting to redeem from these types of accounts.

Potentially disruptive redemptions. Vanguard reserves the right to pay all or part of a redemption in kind—that is, in the form of securities—if we reasonably believe that a cash redemption would negatively affect the fund’s operation or performance or that the shareholder may be engaged in market-timing or frequent trading. Under these circumstances, Vanguard also reserves the right to delay payment of the redemption proceeds for up to seven calendar days. By calling us before you attempt to redeem a large dollar amount, you may avoid in-kind or delayed payment of your redemption. Please see Frequent-Trading Limitations for information about Vanguard’s policies to limit frequent trading.

Recently purchased shares. Although you can redeem shares at any time, proceeds may not be made available to you until the fund collects payment for your purchase. This may take up to seven calendar days for shares purchased by check or by electronic bank transfer. If you have written a check on a fund with checkwriting privileges, that check may be rejected if your fund account does not have a sufficient available balance.

Share certificates. Share certificates are no longer issued for Vanguard funds. Shares currently held in certificates cannot be redeemed, exchanged, converted, or transferred (reregistered) until you return the certificates (unsigned) to Vanguard by registered mail. For the correct address, see Contacting Vanguard.

Address change. If you change your address online or by telephone, there may be up to a 14-day restriction on your ability to request check redemptions online and by telephone. You can request a redemption in writing at any time. Confirmations of address changes are sent to both the old and new addresses.

Payment to a different person or address. At your request, we can make your redemption check payable, or wire your redemption proceeds, to a different person or send it to a different address. However, this generally requires the written consent of all registered account owners and may require additional documentation, such as a signature guarantee or a notarized signature. You may obtain a signature guarantee from some commercial or savings banks, credit unions, trust companies, or member firms of a U.S. stock exchange.

30

No cancellations. Vanguard will not accept your request to cancel any redemption request once processing has begun. Please be careful when placing a redemption request.

Emergency circumstances. Vanguard funds can postpone payment of redemption proceeds for up to seven calendar days. In addition, Vanguard funds can suspend redemptions and/or postpone payments of redemption proceeds beyond seven calendar days at times when the NYSE is closed or during emergency circumstances, as determined by the SEC.

Exchanging Shares

An exchange occurs when you use the proceeds from the redemption of shares of one Vanguard fund to simultaneously purchase shares of a different Vanguard fund. You can make exchange requests online (if you are registered for online access), by telephone, or by mail. See Purchasing Shares and Redeeming Shares.

If the NYSE is open for regular trading (generally until 4 p.m., Eastern time, on a business day) at the time an exchange request is received in good order, the trade date generally will be the same day. See Other Rules You Should Know—Good Order for additional information on all transaction requests.

Vanguard will not accept your request to cancel any exchange request once processing has begun. Please be careful when placing an exchange request.

Please note that Vanguard reserves the right, without notice, to revise or terminate the exchange privilege, limit the amount of any exchange, or reject an exchange, at any time, for any reason. See Frequent-Trading Limitations for additional restrictions on exchanges.

Frequent-Trading Limitations

Because excessive transactions can disrupt management of a fund and increase the fund’s costs for all shareholders, the board of trustees of each Vanguard fund places certain limits on frequent trading in the funds. Each Vanguard fund (other than money market funds and short-term bond funds, but including Vanguard Short-Term Inflation-Protected Securities Index Fund) limits an investor’s purchases or exchanges into a fund account for 30 calendar days (60 calendar days for participants in employer-sponsored defined contribution plans recordkept directly by Vanguard) after the investor has redeemed or exchanged out of that fund account. ETF Shares are not subject to these frequent-trading limits.

For Vanguard Retirement Investment Program pooled plans, the limitations apply to exchanges made online or by telephone.

31

These frequent-trading limitations do not apply to the following:

• Purchases of shares with reinvested dividend or capital gains distributions.

• Transactions through Vanguard’s Automatic Investment Plan, Automatic Exchange Service, Direct Deposit Service, Automatic Withdrawal Plan, Required Minimum Distribution Service, and Vanguard Small Business Online®.

• Discretionary transactions through Vanguard Asset Management Services™, Vanguard Personal Advisor Services®, and Vanguard Institutional Advisory Services®.

• Redemptions of shares to pay fund or account fees.

• Redemptions of shares to remove excess shareholder contributions to certain types of retirement accounts (including, but not limited to, IRAs, certain Individual 403(b)(7) Custodial Accounts, and Vanguard Individual 401(k) Plans).

• Transaction requests submitted by mail to Vanguard from shareholders who hold their accounts directly with Vanguard or through a Vanguard brokerage account. (Transaction requests submitted by fax, if otherwise permitted, are subject to the limitations.)

• Transfers and reregistrations of shares within the same fund.

• Purchases of shares by asset transfer or direct rollover.

• Conversions of shares from one share class to another in the same fund.

• Checkwriting redemptions.

• Section 529 college savings plans.

• Certain approved institutional portfolios and asset allocation programs, as well as trades made by funds or trusts managed by Vanguard or its affiliates that invest in other Vanguard funds. (Please note that shareholders of Vanguard’s funds of funds are subject to the limitations.)

For participants in employer-sponsored defined contribution plans,* the frequent-trading limitations do not apply to:

• Purchases of shares with participant payroll or employer contributions or loan repayments.

• Purchases of shares with reinvested dividend or capital gains distributions.

• Distributions, loans, and in-service withdrawals from a plan.

• Redemptions of shares as part of a plan termination or at the direction of the plan.