Table of Contents

REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934 |

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Title of each class |

Trading Symbol(s) |

Name of each exchange on which registered | ||

Ordinary Shares* |

* |

Not for trading, but only in connection with the registration of American Depositary Shares. |

U.S. GAAP ☐ |

by the International Accounting Standards Board ☒ |

Other |

☐ |

Table of Contents

TABLE OF CONTENTS

Table of Contents

FORWARD-LOOKING STATEMENTS

This Annual Report on Form 20-F includes forward-looking statements, which involve a number of risks and uncertainties. These forward-looking statements can generally be identified as such because the context of the statement will include words such as “may,” “will,” “intend,” “plan,” “believe,” “anticipate,” “expect,” “estimate,” “predict,” “potential,” “continue,” “likely,” or “opportunity,” the negative of these words or other similar words. Similarly, statements that describe our future plans, strategies, intentions, expectations, objectives, goals or prospects and other statements that are not historical facts are also forward-looking statements. Discussions containing these forward-looking statements may be found, among other places, in “Business Overview” and “Operating and Financial Review and Prospects” in this Annual Report on Form 20-F. For such statements, we claim the protection of the Private Securities Litigation Reform Act of 1995 and section 27A of the Securities Act and Section 21E of the Exchange Act. Readers of this Annual Report on Form 20-F are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the time this Annual Report on Form 20-F was filed with the Securities and Exchange Commission, or SEC. These forward-looking statements are based largely on our expectations and projections about future events and future trends affecting our business and are subject to risks and uncertainties that could cause actual results to differ materially from those anticipated in the forward-looking statements. These risks and uncertainties include, without limitation, those discussed in “Risk Factors” and in “Operating and Financial Review and Prospects” of this Annual Report on Form 20-F. In addition, past financial or operating performance is not necessarily a reliable indicator of future performance, and you should not use our historical performance to anticipate results or future period trends. We can give no assurances that any of the events anticipated by the forward-looking statements will occur or, if any of them do, what impact they will have on our results of operations and financial condition. Except as required by law, we undertake no obligation to update publicly or revise our forward-looking statements to reflect events or circumstances that arise after the filing of this Annual Report on Form 20-F.

In this Annual Report on Form 20-F, “Kazia,” “Company,” “we,” “us” and “our” refer to Kazia Therapeutics Limited and its wholly owned subsidiaries on a consolidated basis, unless the context otherwise provides.

PART I

| Item 1. | Identity of Directors, Senior Management and Advisors |

Item 1 details are not required to be disclosed as part of the Annual Report.

| Item 2. | Offer Statistics and Expected Timetable |

Item 2 details are not required to be disclosed as part of the Annual Report.

| Item 3. | Key Information |

A. Reserved

B. Capitalization and Indebtedness.

Not applicable.

C. Reasons for the Offer and Use of Proceeds.

Not applicable.

D. Risk factors

Investment in our securities involves a high degree of risk. You should consider carefully the risks described below, together with other information in this Annual Report on Form 20-F and our other public filings, before making investment decisions regarding our securities. If any of the following events actually occur, our business, operating results, prospects or financial condition could be materially and adversely affected. This could cause the trading price of our common stock to decline and you may lose all or part of your investment. Moreover, the risks described below are not the only ones that we face. Additional risks not presently known to us or that we currently deem immaterial may also affect our business, operating results, prospects or financial condition.

1

Table of Contents

Risks Related to Our Financial Condition and Capital Requirement

We have incurred significant net losses since our inception. We expect to incur significant net losses for the foreseeable future and may never achieve or maintain profitability.

We have incurred significant net losses. We anticipate that we will continue to incur significant net losses for the foreseeable future and we may never achieve or maintain profitability. We are a biotechnology company and have not yet generated significant revenue. We have incurred losses of A$8,419,484, A$25,014,055 and A$20,465,180 for the fiscal years ended June 30, 2021 (restated), 2022 (restated) and 2023, respectively. We have not generated any revenues from sales of any of our product candidates in prior financial years, however in the fiscal year ended June 30, 2021 we did generate revenues of A$15.2 million from the licensing of our development stage drug candidates.

As of 30 June 2023, we had accumulated losses of A$89,082,571. We have devoted most of our financial resources to research and development, including our clinical development activities. To date, we have financed our operations primarily through the issuance of equity securities, research and development grants from the Australian government and payments from our collaboration partners. While we have generated significant revenue in recent fiscal years from license transactions, the nature of such revenue is irregular and unpredictable, and is based upon achievement of milestones over which we have limited or no control. As a consequence, we expect to continue to incur significant operating losses for the foreseeable future due to the cost of research and development including clinical trials and the regulatory approval process for product candidates. The amount of our future net losses is uncertain and will depend, in part, on the rate of our future expenditures. Our ability to continue operations will depend on, among other things, our ability to obtain funding through equity or debt financings, strategic collaborations or grants.

We anticipate that our expenses will increase substantially if and as we:

| • | continue our research and clinical development of our product candidates; |

| • | expand the scope of our current clinical studies for our product candidates or initiate additional clinical or other studies for product candidates; |

| • | seek regulatory and marketing approvals for any of our product candidates that successfully complete clinical trials; |

| • | further develop the manufacturing process for our product candidates; |

| • | change or add additional manufacturers or suppliers; |

| • | seek to identify and validate additional product candidates; |

| • | acquire or in-license other product candidates and technologies; |

| • | maintain, protect and expand our intellectual property portfolio; |

| • | create additional infrastructure to support our operations as a public company in the United States and our product development and future commercialization efforts; and |

| • | experience any delays or encounter issues with any of the above. |

The net losses we incur may fluctuate significantly from year to year, such that a period-to-period comparison of our results of operations may not be a good indication of our future performance.

We have never generated any revenue from product sales and may never be profitable.

Our ability to generate significant revenue and achieve profitability depends on our ability, alone or with strategic collaboration partners, to successfully complete the development of and obtain the regulatory approvals for our product candidates, to manufacture sufficient supply of our product candidates, to establish a sales and marketing organization or suitable third-party alternative for the marketing of any approved products and to successfully commercialize any approved products on commercially reasonable terms. All of these activities will require us to raise sufficient funds to finance business activities. In addition, we do not anticipate generating revenue from commercializing product candidates for the foreseeable future, if ever. Our ability to generate future revenues from commercializing product candidates depends heavily on:

| • | successfully initiating and completing clinical trials of our product candidates; |

| • | the timing of the initiation and completion of preclinical studies and clinical trials; |

| • | the timing of patient enrollment and dosing in any future clinical trials; |

| • | the timing of the availability of data from clinical trials; |

| • | expectations about the successful completion of clinical trials; |

| • | obtaining regulatory and marketing approvals for product candidates for which we complete clinical trials; |

| • | the timing of expected regulatory filings; |

| • | expectations about approval by regulatory authorities of our drug candidates; |

2

Table of Contents

| • | the clinical utility and potential attributes and benefits of our product candidates, including the potential duration of treatment effects; |

| • | potential licenses of intellectual property and collaborations; |

| • | the commercialization of our product candidates, if approved; |

| • | expectations regarding expenses, ongoing losses, future revenue and capital needs; |

| • | our financial performance; |

| • | the length of time over which we expect our cash and cash equivalents to be sufficient; |

| • | our intellectual property position and the duration of our patent portfolio; |

| • | maintaining, protecting and expanding our intellectual property portfolio, and avoiding infringing on intellectual property of third parties; |

| • | establishing and maintaining successful licenses, collaborations and alliances with third parties; |

| • | developing a sustainable, scalable, reproducible and transferable manufacturing process for our product candidates; |

| • | establishing and maintaining supply and manufacturing relationships with third parties that can provide products and services adequate, in amount and quality, to support clinical development and commercialization of our product candidates, if approved; |

| • | launching and commercializing any product candidates for which we obtain regulatory and marketing approval, either by collaborating with a partner or, if launched independently, by establishing a sales, marketing and distribution infrastructure; |

| • | obtaining market acceptance of any product candidates that receive regulatory approval as viable treatment options; |

| • | the outcome of corresponding endeavors in respect of competitive or potentially competitive product candidates by other drug development companies; |

| • | obtaining favorable coverage and reimbursement rates for our products from third-party payers; |

| • | addressing any competing technological and market developments; |

| • | identifying and validating new product candidates; and |

| • | negotiating favorable terms in any collaboration, licensing or other arrangements into which we may enter. |

Even if one or more of our product candidates is approved for commercial sale, we may incur significant costs associated with commercializing any approved product candidate. As one example, our expenses could increase beyond expectations if we are required by the U.S. Food and Drug Administration (“FDA”) or other regulatory agencies, domestic or foreign, to perform clinical and other studies in addition to those that we currently anticipate. Even if we are able to generate revenues from the sale of any approved products, we may not become profitable and may need to obtain additional funding to continue operations, which could have an adverse effect on our business, financial condition, results of operations and prospects.

The Company has two product candidates currently in clinical trials. Failure of one or both of these product candidates to show benefit to patients could materially and adversely affect the continuity of our business and our financial condition.

The Company’s lead programs include paxalisib (formerly GDC-0084), a small molecule inhibitor of the PI3K/Akt/mTOR pathway, and EVT801, a small molecule selective inhibitor of vascular endothelial growth factor receptor 3 (VEGFR3). However, even though progress has been made, such as the clinical validation of the PI3K/Akt/mTOR pathway as a target for oncology therapies, development of our product candidates may prove unsuccessful, after completion of clinical trials, due to any failure to provide adequate beneficial effect to cancer patients. It is possible that either or both product candidates may fail to show sufficient benefit as an intended treatment for the specific cancer indication to become commercially viable products, which could materially and adversely affect the continuity of our business and our financial condition.

The Company has ongoing clinical trials in which experimental therapies are administered to human subjects. If profound and unexpected safety concerns are encountered in clinical trials, it may materially and adversely affect the continuity of our business and our financial condition.

Despite all applicable efforts to characterize the safety profile of our drug development candidates through animal studies and other mechanisms, the possibility of unexpected safety concerns remains. If one or both of our clinical stage candidates were found to be associated with profound and unexpected toxicity or other safety concerns, the Company may be required to cease development of one or both candidates, and may additionally incur other impairments to the business including reputational damage, which may materially and adversely affect the continuity of our business and our financial condition.

The Company relies on third-party contract manufacturing organizations to manufacture its drug product candidates. If one or more of these vendors were unable to meet the Company’s needs, it may materially and adversely impact our business.

Manufacture of pharmaceutical material for human administration is technically complex and highly regulated. If one or more of the Company’s vendors failed to produce drug product to the requisite standard, the continuity of the Company’s operations may be severely disrupted. Even if a vendor was found deficient in respect of another product, it may impair the confidence of regulatory agencies in our product candidates, thereby disrupting our operations.

Global contract manufacturing capacity is limited, and the manufacturing process is not readily portable. As a result, the Company’s ability to manufacture its product candidates in a timely manner is dependent on the availability of suitable capacity at its vendors.

The manufactured drug products, and their intermediaries, are of significant financial value. Loss, damage, or theft of this material, for example while in storage or transit, may result in significant detriment to the Company, which may be incompletely cured by insurance.

3

Table of Contents

There is substantial doubt about our ability to continue as a going concern, which may hinder our ability to obtain future financing.

The Company has limited cash resources and will periodically need additional funds to maintain the planned level of R&D activity. We expect to consume cash and incur operating losses for the foreseeable future as the Company continues developing its oncology drug candidates. The impact on cash resources and results from operations will vary with the extent and timing of future clinical trial programs. While it is not possible to make accurate predictions of future operating results, we expect existing cash and cash equivalents, including the capital raised in July 2023, will be sufficient to enable us to continue our research and development activities until approximately November 2023.

As at 30 June 2023, we had cash on hand at the bank of A$5.2 million. The financial statements have been prepared on a going concern basis, which contemplates continuity of normal activities and realization of assets and settlement of liabilities in the normal course of business. As is often the case with drug development companies, our ability to continue as a going concern is dependent upon our ability to derive sufficient cash from investors, from licensing and partnering and collaboration activities and from other sources of revenue such as grant funding.

Furthermore, we are limited by General Instruction I.B.5 to Form F-3 (the “Baby Shelf Rule”) as of the filing of this Annual Report, until such time as our non-affiliate public float exceeds $75 million. The amount of funds we can raise through primary non-affiliate public offerings of securities in any 12-month period using our registration statement on Form F-3 is limited to one-third of the aggregate market value of the ordinary shares held by non-affiliates of the Company, which limitation may change over time based on our stock price, number of ordinary shares outstanding and the percentage of ordinary shares held by non-affiliates. These factors raise substantial doubt about our ability to continue as a going concern within one year after the date that the financial statements are issued. The independent auditor’s report for the fiscal year ended 30 June 2023 included an explanatory paragraph in relation to the going concern uncertainty.

If the Company is unable to obtain additional funds on favorable terms or at all, it may be required to cease or reduce its operations. Our future success is dependent upon our ability to obtain additional funding. There can be no assurance, however, that we will be successful in obtaining such funding in sufficient amounts, on terms acceptable to us, or at all. Also, if the Company raises more funds by selling additional securities, the ownership interests of holders of its securities will be diluted.

Global economic uncertainty caused by rising inflation, political instability, and conflicts and other events of geopolitical significance, such as the conflict between Russia and Ukraine, and the recent conflict between Israel and Gaza, could adversely affect our business and financial performance.

Negative global economic conditions may pose challenges to the Company’s business strategy, which relies on access to capital from financial markets and/or investment by other companies. Failure to obtain sufficient funding on acceptable terms could have a material adverse effect on our business, results of operations and financial condition. Negative conditions in the global economy, including credit markets and the financial services industry, have generally made equity and debt financing more difficult to obtain, and may negatively impact the Company’s ability to complete financing transactions. We are currently operating in a period of economic uncertainty and capital markets disruption, which has been significantly impacted by the geopolitical instability due to the ongoing military conflict between Russia and Ukraine and the recently erupted conflict between Israel and Gaza. Our business, financial condition, and results of operations may be materially adversely affected by the negative impact on the global economy and capital markets resulting from the conflict in Ukraine or any other geopolitical tensions. U.S. and global markets are experiencing volatility and disruption following the escalation of geopolitical tensions, including the military conflict between Russia and Ukraine and the recent conflict between Israel and Gaza as well as any additional escalations that may develop in the Middle East region. Although the length and impact of these ongoing military conflicts are highly unpredictable, the conflict in Ukraine and the recent conflict between Israel and Gaza have led to market disruptions, including significant volatility in commodity prices, credit and capital markets, as well as supply chain disruptions.

Additionally, various of Russia’s actions have led to sanctions and other penalties being levied by the U.S., Australia, the European Union, and other countries, as well as other public and private actors and companies, against Russia and certain other geographic areas, including agreement to remove certain Russian financial institutions from the Society for Worldwide Interbank Financial Telecommunication payment system and restrictions on imports of Russian oil, liquified natural gas and coal. Additional potential sanctions and penalties have also been proposed and/or threatened. Russian military actions and the resulting sanctions could further adversely affect the global economy and financial markets and lead to instability and lack of liquidity in capital markets, potentially making it more difficult for us to obtain additional funds.

The duration and severity of these conditions is uncertain, as is the extent to which they may adversely affect the Company’s business and the business of current and prospective vendors and collaborators. If negative global economic conditions persist or worsen, the Company may be unable to secure additional funding to sustain its operations or to find suitable collaborators to advance its internal programs, even if positive results are achieved from research and development efforts.

Any of the above-mentioned factors could affect our business, prospects, financial condition, and operating results. The extent and duration of the military action, sanctions, and resulting market disruptions are impossible to predict, but could be substantial.

If we are unable to raise sufficient funding on acceptable terms due to these or other factors, we may be unable to continue to operate. There is no assurance that we will be successful in obtaining sufficient financing on acceptable terms and conditions to fund continuing operations, if at all. Our failure to obtain sufficient funds on acceptable terms when needed could have a material adverse effect on our business, results of operations and financial condition.

4

Table of Contents

Risks Related to Our Business Operations

We may not successfully engage in strategic transactions or enter into new collaborations, which could adversely affect our ability to develop and commercialize product candidates, impact our cash position, increase our expenses and present significant distractions to our management.

From time to time, we may consider additional strategic transactions, such as collaborations, acquisitions, asset purchases or sales

and out- or in-licensing of product candidates or technologies. In particular we will evaluate and, if strategically attractive, seek to enter into additional collaborations, including with major biotechnology or pharmaceutical companies. The competition for collaborators is significant, and the negotiation process is time-consuming and complex. Any new collaboration may be on terms that are not optimal for us, and we may not be able to maintain any new or existing collaboration if, for example, development or approval of a product candidate is delayed, sales of an approved product candidate do not meet expectations or the collaborator discontinues the collaboration. Any such collaboration, or other strategic transaction, may require us to

incur non-recurring or other charges, increase our expenditures, pose significant integration or implementation challenges or disrupt our management or business.

These transactions would entail numerous operational and financial risks, including exposure to unknown liabilities, incurrence of substantial debt or dilutive issuances of equity securities to pay transaction consideration or costs, higher than expected collaboration, acquisition or integration costs, write-downs of assets or goodwill or impairment charges, increased amortization expenses, difficulty and cost in facilitating the collaboration or combining the operations and personnel of any acquired business, impairment of relationships with key suppliers, manufacturers or customers of any acquired business due to changes in management and ownership and the inability to retain key employees of any acquired business.

Accordingly, although there can be no assurance that we will undertake or successfully complete any additional transactions of the nature described above, any transactions that we do complete may be subject to the foregoing or other risks and have a material adverse effect on our business, results of operations, financial condition and prospects. Conversely, any failure to enter any collaboration or other strategic transaction that would be beneficial to us could delay and make more expensive the development and potential commercialization of our product candidates and have a negative impact on the competitiveness of any product candidate that reaches market.

Any inability to attract and retain qualified key management and technical personnel would impair our ability to implement our business plan.

Our success largely depends on the continued service of key management and other specialized personnel. The loss of one or more members of our management team or other key employees or advisors could delay or increase the cost of our research and development programs and materially harm our business, financial condition, results of operations and prospects. The relationships that our key managers have cultivated within our industry make us particularly dependent upon their continued employment with us. We are dependent on the continued service of our technical personnel because of the highly technical nature of our product candidates and the specialized nature of the regulatory approval process for our product candidates. Because our management team and key employees are not obligated to provide us with continued service, they could terminate their employment with us at any time without penalty. We do not maintain key person life insurance policies on any of our management team members or key employees. Our future success will depend in large part on our continued ability to attract and retain other highly qualified scientific, technical and management personnel, as well as personnel with expertise in clinical testing, manufacturing, governmental regulation and commercialization. We face competition for personnel from other companies, universities, public and private research institutions, government entities and other organizations.

Our collaborations with outside scientists and consultants may be subject to restriction and change.

We work with medical experts, chemists, biologists and other scientists at academic and other institutions, and consultants who assist us in our research, development and regulatory efforts, including the members of our scientific advisory board. In addition, these scientists and consultants have provided, and we expect that they will continue to provide, valuable advice regarding our programs and regulatory approval processes. These scientists and consultants are not our employees and may have other commitments that would limit their future availability to us. If a conflict of interest arises between their work for us and their work for another entity, we may lose their services. In addition, we are limited in our ability to prevent them from establishing competing businesses or developing competing products. For example, if a key scientist acting as a principal investigator in any of our future clinical trials identifies a potential product or compound that is more scientifically interesting to professional interests, their availability to remain involved in any future clinical trials could be restricted or eliminated.

5

Table of Contents

We face potential product liability claims, and, if successful claims are brought against us, we may incur substantial liability and costs. If the use of our product candidates harms patients, or is perceived to harm patients even when such harm is unrelated to our product candidates, our regulatory approvals could be revoked or otherwise negatively impacted and we could be subject to costly and damaging product liability claims.

The use of our product candidates in clinical trials and the sale of any products for which we may in the future obtain marketing approval exposes us to the risk of product liability claims. Product liability claims might be brought against us by consumers, healthcare providers, pharmaceutical companies or others selling or otherwise coming into contact with our product candidates. There is a risk that our product candidates may induce adverse events. If we cannot successfully defend against product liability claims, we could incur substantial liability and costs. In addition, regardless of merit or eventual outcome, product liability claims may result in:

| • | impairment of our business reputation; |

| • | withdrawal of clinical trial participants; |

| • | costs due to related litigation; |

| • | distraction of management’s attention from our primary business; |

| • | substantial monetary awards to patients or other claimants; |

| • | the inability to commercialize our product candidates; |

| • | decreased demand for our product candidates, if approved for commercial sale; and |

| • | increased cost, or impairment of our ability, to obtain or maintain product liability insurance coverage. |

We may use our limited financial and human resources to pursue a particular research program or product candidate and fail to capitalize on programs or product candidates that may be more profitable or for which there is a greater likelihood of success.

Because we have limited resources, we may forego or delay pursuit of opportunities with certain programs or product candidates or for indications that later prove to have greater commercial potential. Our resource allocation decisions may cause us to fail to capitalize on viable commercial products or profitable market opportunities. Our spending on current and future research and development programs for product candidates may not yield any commercially viable products. If we do not accurately evaluate the commercial potential or target market for a particular product candidate, we may relinquish valuable rights to that product candidate through strategic collaboration, licensing or other royalty arrangements in cases in which it would have been more advantageous for us to retain sole development and commercialization rights to such product candidate, or we may allocate internal resources to a product candidate in a therapeutic area in which it would have been more advantageous to enter into a collaboration arrangement.

Our internal computer and information technology systems, or those of our collaborators and other development partners, third-party Contract Research Organizations (CROs) or other contractors or consultants, may fail or suffer security breaches, which could result in a disruption of our product development programs.

Despite the implementation of security measures, our internal computer and information technology systems and those of our current and any future CROs and other contractors, consultants and collaborators are vulnerable to damage from computer viruses, cyber-attacks, unauthorized access, natural disasters, terrorism, war and telecommunication and electrical failures. Such events could cause interruptions of our operations. While we have not experienced any material system failure, accident or security breach to date, if such an event were to occur and cause interruptions in our operations, it could result in a disruption of our development programs and our business operations, whether due to a loss of our trade secrets or other similar disruptions. One of our major suppliers did experience a cyber attack in April 2023 but it did not result in any material system failure and had no long term impact on our business. For example, the loss of clinical trial data from ongoing or future clinical trials or data from preclinical studies could result in delays in our regulatory approval efforts and significantly increase our costs to recover or reproduce the data. Likewise, we rely on third parties to manufacture our product candidates and will rely on third parties to conduct future clinical trials, and similar events relating to their computer systems could also have similar consequences to our business. To the extent that any disruption or security breach were to result in a loss of, or damage to, our data or applications, or inappropriate disclosure of confidential or proprietary information, we could incur liability and the further development and commercialization of our product candidates could be delayed and become more expensive.

Our ability to utilize our net operating losses and certain other tax attributes may be limited.

We have substantial carried forward tax losses which may not be available to offset any future assessable income. In order for an Australian corporate taxpayer to carry forward and utilize tax losses, the taxpayer must pass either the continuity of ownership test, or, if it fails the COT, the same business test (“SBT”), or similar business test, in respect of relevant tax losses.

We have not carried out any formal analysis as to whether we have met the COT or, failing the COT, the SBT or similar business test over relevant periods. In addition, future shareholding changes may result in a significant ownership change for us. It is therefore uncertain as to whether any of our tax losses carried forward as of 30 June 2023 will be available to be carried forward and available to offset our assessable income, if any, in future periods.

6

Table of Contents

Risks Related to the Product Development and Regulatory Approval of Our Product Candidates

We may not be able to obtain orphan drug exclusivity, where relevant, in all markets for our product candidates.

Regulatory authorities in some jurisdictions, including the United States, may designate drugs for relatively small patient populations as orphan drugs. Under the Orphan Drug Act, the FDA may designate a product as an orphan drug if it is a product intended to treat a rare disease or condition, which is generally defined as a patient population of fewer than 200,000 individuals annually in the United States. The FDA may also designate a product as an orphan drug if it is intended to treat a disease or condition of more than 200,000 individuals in the United States and there is no reasonable expectation that the cost of developing and making a drug or biological product available in the United States for this type of disease or condition will be recovered from sales of the product candidate.

Generally, if a product with an orphan drug designation subsequently receives the first marketing approval for the indication for which it has such designation, the product is entitled to a period of marketing exclusivity, which precludes the FDA from approving another marketing application for the same drug for such indication for that time period. The applicable period is seven years in the United States. Orphan drug exclusivity may be lost if the FDA determines that the request for designation was materially defective or if the manufacturer is unable to assure sufficient quantity of the drug to meet the needs of patients with the rare disease or condition.

Paxalisib (formerly GDC-0084) was granted orphan drug designation by the FDA in February 2018 for the treatment of glioblastoma, in August 2020 for the treatment of malignant glioma, which includes DIPG, a rare and highly aggressive childhood brain cancer, and in June 2022 for the treatment of atypical rhabdoid / teratoid tumors (AT/RT). However, even if we obtain orphan drug exclusivity for additional products in the United States or other jurisdictions, that exclusivity may not effectively protect the product from competition because different drugs can be approved for the same condition, and the same drug could be approved for a different condition. Moreover, even after an orphan drug is approved, the FDA can subsequently approve the same drug, made by a competitor, for the same condition if the FDA concludes that the competitive product is clinically superior in that it is shown to be safer, more effective or makes a major contribution to patient care.

Positive results from preclinical studies of our product candidates are not necessarily predictive of the results of our planned clinical trials of our product candidates.

Positive results in preclinical proof of concept and animal studies of our product candidates may not result in positive results in clinical trials in humans. Many companies in the pharmaceutical and biotechnology industries have suffered significant setbacks in clinical trials after achieving positive results in preclinical development or early-stage clinical trials, and we cannot be certain that we will not face similar setbacks. These setbacks have been caused by, among other things, preclinical findings made while clinical trials were underway or safety or efficacy observations made in clinical trials, including adverse events. Moreover, preclinical and clinical data are often susceptible to varying interpretations and analyses, and many companies that believed their product candidates performed satisfactorily in preclinical studies and clinical trials nonetheless failed to obtain FDA or other regulatory authority approval. If we fail to produce positive results in our clinical trials of our product candidates, the development timeline and regulatory approval and commercialization prospects for our product candidates, and, correspondingly, our business and financial prospects, would be negatively impacted.

Even if the Company receives regulatory approval to commercialize its drug candidates, the ability to generate revenues from any resulting products will be subject to a variety of risks, many of which are out of the Company’s control.

Regardless of regulatory approval, products arising from the development process may not gain market acceptance among physicians, patients, healthcare payers or the medical community. The Company believes that the degree of market acceptance and its ability to generate revenues from such products will depend on a number of factors, including, but not limited to:

| • | advancements in the treatment of cancer that make our treatments obsolete; |

| • | market exclusivity and competitor products; |

| • | timing of market introduction of the Company’s drugs and competitive drugs; |

| • | actual and perceived efficacy and safety of the Company’s drug candidates; |

7

Table of Contents

| • | prevalence and severity of any side effects; |

| • | potential or perceived advantages or disadvantages over alternative treatments; |

| • | strength of sales, marketing and distribution support; |

| • | price of future products, both in absolute terms and relative to alternative treatments; |

| • | the effect of current and future healthcare laws on the Company’s drug candidates; and |

| • | availability of coverage and reimbursement from government and other third-party payers. |

If any of the Company’s drugs are approved and fail to achieve market acceptance, the Company may not be able to generate significant revenue to achieve or sustain profitability.

Risks Related to Commercialization of Our Product Candidates

The Company may not be able to establish the contractual arrangements necessary to develop, market and distribute the product candidates. Our failure to do so may adversely affect our business, results of operations and financial condition.

The Company has been successful in executing contractual agreements with strategic partners. This remains a key part of the Company’s business plan and the Company must continue to partner with third parties to manufacture clinical grade drug product and conduct key pre-clinical and clinical investigations. Strategic agreements around packaging, branding, market access and distribution for its drug products will also eventually be required.

However, potential partners could be discouraged by the Company’s limited operating history. There is no assurance that the Company will be able to negotiate commercially acceptable licensing or other agreements for the future exploitation of its drug product candidates including continued clinical development, manufacture or marketing. If the Company is unable to successfully contract for these services, or if arrangements for these services are terminated, the Company may have to delay the commercialization program which will adversely affect its ability to generate operating revenues.

The Company’s commercial opportunity will be reduced or eliminated if competitors develop and market products, devices or other treatments that are more effective, have fewer side effects or are less expensive than its drug candidates.

The development of drug candidates is highly competitive and is high risk. A number of other companies have products or drug candidates in various stages of pre-clinical or clinical development that are intended for the same therapeutic indications for which the Company’s drug candidates are being developed. Some of these potential competing drugs are further advanced in development than the Company’s drug candidates and may be commercialized sooner. Even if the Company is successful in developing effective drugs, its compounds may not compete successfully with products produced by its competitors.

The Company’s competitors include pharmaceutical companies and biotechnology companies, as well as universities and public and private research institutions. In addition, companies active in different but related fields represent substantial competition. Many of the Company’s competitors developing oncology drugs have significantly greater capital resources, larger R&D staff and facilities and greater experience in drug development, regulation, manufacturing and marketing. These organizations also compete with the Company and its service providers, to recruit qualified personnel, and to attract partners for joint ventures and to license technologies. As a result, the Company’s competitors may be able to develop technologies and products that would render the Company’s technologies or its drug candidates obsolete or non-competitive.

Risks Related to Our Intellectual Property

If we are unable to protect intellectual property rights related to our product candidates, we may not be able to obtain exclusivity for our product candidates or prevent others from developing similar competitive products.

We rely upon a combination of patents, know-how, trade secret protection and confidentiality agreements to protect the intellectual property related to our product candidates. The strength of patents in the biotechnology and pharmaceutical field involves complex legal and scientific questions and can be uncertain. The patent applications that we own or in-license may fail to result in issued patents with claims that cover our product candidates in the United States or other jurisdictions. In addition, we cannot guarantee that any patents will issue from any pending or future patent applications owned by or licensed to us. There is no assurance that all of the potentially relevant prior art relating to our patents and patent applications has been found. If such prior art exists, it can invalidate a patent or prevent a patent from issuing from a pending patent application. Even if patents do successfully issue and even if such patents cover our product candidates, third parties may initiate opposition, interference, re-examination, post-grant review, inter partes review, nullification or derivation action in court or before patent offices or similar proceedings challenging the validity, enforceability or scope of such patents, which may result in the patent claims being narrowed or invalidated. Furthermore, even if our patents and patent applications are unchallenged, they may not adequately protect our intellectual property, provide exclusivity for our product candidates or prevent others from designing around our claims. Any of these outcomes could impair our ability to prevent competition from third parties.

8

Table of Contents

If the patent applications we hold or have in-licensed with respect to our programs or product candidates fail to issue, or are revoked, if the breadth or strength of our patent protection is threatened, or if our patent portfolio fails to provide meaningful exclusivity for our product candidates, it could dissuade companies from collaborating with us to develop product candidates and threaten our ability to commercialize future products. Any successful opposition to any patents owned by or licensed to us could deprive us of rights necessary for the successful commercialization of any product candidates that we may develop. Further, if we encounter delays in regulatory approvals, the period of time during which we could market a product candidate under patent protection could be reduced. Even where we have a valid and enforceable patent, we may not be able to exclude others from practicing our invention where the other party can show that they used the invention in commerce before our filing date or the other party benefits from a compulsory license. In addition, patents have a limited lifespan. In the United States, the natural expiration of a patent is generally 20 years after it is filed. Various extensions may be available, but the life of a patent, and the protection it affords, is limited. Even if patents covering our product candidates are obtained, once the patent life has expired for a product, we may be open to competition from competitive medications, including biosimilar or generic medications. This risk is material in light of the length of the development process of our products and lifespan of our current patent portfolio.

In addition to the protection afforded by patents, we rely on trade secret protection and confidentiality agreements to protect proprietary know-how that is not patentable or that we elect not to patent, processes for which patents are difficult to enforce and any other elements of our product candidate discovery and development processes that involve proprietary know-how, information or technology that is not covered by patents. However, trade secrets can be difficult to protect. What constitutes a trade secret and what protections are available for trade secrets varies from state to state in the United States and country by country worldwide. We seek to protect our proprietary technology and processes, in part, by entering into confidentiality agreements with our employees, consultants, scientific advisors and contractors. We also seek to preserve the integrity and confidentiality of our data and trade secrets by maintaining physical security of our premises and physical and electronic security of our information technology systems. Security measures may be breached, and we may not have adequate remedies for any breach. In addition, our trade secrets may otherwise become known or be independently discovered by competitors. Although we expect all of our employees and consultants to assign their inventions to us, and all of our employees, consultants, advisors and any third parties who have access to our proprietary know-how, information or technology to enter into confidentiality agreements, we cannot provide any assurances that all such agreements have been duly executed or that our trade secrets and other confidential proprietary information will not be disclosed or that competitors will not otherwise gain access to our trade secrets or independently develop substantially equivalent information and techniques.

Obtaining and maintaining our patent protection depends on compliance with various procedural, document submission, fee payment and other requirements imposed by governmental patent agencies, and our patent protection could be reduced or eliminated for non-compliance with these requirements.

Periodic maintenance fees, renewal fees, annuity fees and various other governmental fees on patents and applications are required to be paid to the USPTO and various governmental patent agencies outside of the United States in several stages over the lifetime of the patents and applications. The USPTO and various corresponding governmental patent agencies outside of the United States require compliance with a number of procedural, documentary, fee payment and other similar provisions during the patent application process and after a patent has issued. There are situations in which non-compliance can result in abandonment or lapse of the patent or patent application, resulting in partial or complete loss of patent rights in the relevant jurisdiction.

Our success depends, in part, on our ability to protect our intellectual property and our technologies.

Our commercial success depends, in part, on our ability to obtain and maintain patent and trade secret protection for our technologies, our traits, and their uses, as well as our ability to operate without infringing upon the proprietary rights of others. If we do not adequately protect our intellectual property, competitors may be able to use our technologies and erode or negate any competitive advantage we may have, which could harm our business and ability to achieve profitability.

Filing, prosecuting and defending patents on product candidates in all countries around the world would be prohibitively expensive. In addition, we may at times in-license third-party technologies for which limited international patent protection exists and for which the time period for filing international patent applications has passed. Consequently, we may not be able to prevent third parties from practicing our inventions, or from selling or importing products made using our inventions. Potential competitors may use our technologies in jurisdictions where we have not obtained patent protection to develop their own products and further, may export otherwise infringing products to territories where we have patent protection but enforcement is difficult. These products may compete with our product candidates, if approved, and our patents or other intellectual property rights may not be effective or sufficient to prevent them from competing.

9

Table of Contents

Many companies have encountered significant problems in protecting and defending intellectual property rights around the world. The legal systems of certain countries, particularly certain developing countries, do not favor the enforcement of patents, trade secrets and other intellectual property protection, particularly those relating to biotechnology products, which could make it difficult for us to stop the infringement of our patents or marketing of competing products in violation of our proprietary rights generally. Proceedings to enforce our patent rights could result in substantial costs and divert our efforts and attention from other aspects of our business, could put our patents at risk of being invalidated or interpreted narrowly and our patent applications at risk of not issuing and could provoke third parties to assert claims against us. We may not prevail in any lawsuits that we initiate and the damages or other remedies awarded, if any, may not be commercially meaningful. Accordingly, our efforts to enforce our intellectual property rights around the world may be inadequate to obtain a significant commercial advantage from the intellectual property that we develop or license.

Risks Related to Our Reliance on Third Parties

The Company relies on third parties to conduct its pre-clinical studies and clinical trials. If those parties do not successfully carry out their contractual duties or meet expected deadlines, the Company’s drug candidates may not advance in a timely manner or at all.

In the course of discovery, pre-clinical testing and clinical trials, the Company relies on third parties, including laboratories, investigators, clinical contract research organizations (“CROs”), and manufacturers, to perform critical services. For example, the Company relies on third parties to conduct all of its pre-clinical and clinical studies. These third parties may not be available when the Company needs them or, if they are available, may not comply with all regulatory and contractual requirements or may not otherwise perform their services in a timely or acceptable manner, and the Company may need to enter into new arrangements with alternative third parties and the studies may be extended, delayed or terminated. These independent third parties may also have relationships with other commercial entities, some of which may compete with the Company. As a result of the Company’s dependence on third parties, it may face delays or failures outside of its direct control. These risks also apply to the development activities of collaborators, and the Company does not control their research and development, clinical trial or regulatory activities.

The Company has no direct control over the cost of manufacturing its drug candidates. Increases in the cost of manufacturing the Company’s drug candidates would increase the costs of conducting clinical trials and could adversely affect future profitability.

The Company does not intend to manufacture the drug product candidates in-house, and it will rely on third parties for drug supplies both for clinical trials and for commercial quantities in the future. The Company has taken the strategic decision not to manufacture active pharmaceutical ingredients (“API”) for the drug candidates, as these can be more economically supplied by third parties with particular expertise in this area. The Company outsources the manufacture of its drug products and their testing to FDA requirements. The Company uses contract facilities that are registered with the FDA, have a track record of large-scale API manufacture, and have already invested in capital and equipment. The Company has no direct control over the cost of manufacturing its product candidates. If the cost of manufacturing increases, or if the cost of the materials used increases, these costs may be passed on, making the cost of conducting clinical trials more expensive. Increases in manufacturing costs could adversely affect the Company’s future profitability if it was unable to pass all of the increased costs along to its customers.

Risks Related to our Securities

Enforceability of civil liabilities under the federal securities laws against the Company or the Company’s officers and directors may be difficult.

The Company is a public company limited by shares and is registered and operates under the Australian Corporations Act 2001. Half of the Company’s directors and officers reside outside of the United States. In addition, a substantial portion of the directly owned assets of the Company are located outside of the United States. As a result, it may be difficult or impossible for investors to effect service of process within the United States against the Company or its directors and officers or to enforce against them any of the judgments, including those obtained in original actions or in actions to enforce judgments of the U.S. courts, predicated upon the civil liability provisions of the federal or state securities laws of the United States. There is doubt as to the enforceability in the Commonwealth of Australia, in original actions or in actions for enforcement of judgments of U.S. courts, of civil liabilities predicated solely upon federal or state securities laws of the U.S., especially in the case of enforcement of judgments of U.S. courts where the defendant has not been properly served in Australia.

10

Table of Contents

Our failure to meet the continued listing requirements of Nasdaq could result in a delisting of our common stock, which could negatively impact the market price and liquidity of our common shares and our ability to access the capital markets.

Our common stock is listed on the Nasdaq Capital Market. If we fail to satisfy the continued listing requirements of Nasdaq, such as the corporate governance requirements or the minimum closing bid price requirement, Nasdaq may take steps to delist our common stock. Such a delisting would have a negative effect on the price of our common stock, impair the ability to sell or purchase our common stock when persons wish to do so, and any delisting materially adversely affect our ability to raise capital or pursue strategic restructuring, refinancing or other transactions on acceptable terms, or at all. Delisting from the Nasdaq Capital Market could also have other negative results, including the potential loss of institutional investor interest and fewer business development opportunities. In the event of a delisting, we would attempt to take actions to restore our compliance with Nasdaq’s listing requirements, but we can provide no assurance that any such action taken by us would allow our common stock to become listed again, stabilize the market price or improve the liquidity of our common stock, prevent our common stock from dropping below the Nasdaq minimum bid price requirement or prevent future non-compliance with Nasdaq’s listing requirements.

On December 9, 2022, we received a notice from the Nasdaq Listing Qualifications Department of The Nasdaq Capital Market (“Nasdaq”) informing us that because the closing bid price of our common stock had been below $1.00 per share for 30 consecutive business days, we no longer complied with the minimum bid price requirement for continued listing on The Nasdaq Capital Market. Nasdaq Listing Rule 5550(a)(2) (the “Rule”) requires listed securities to maintain a minimum bid price of $1.00 per share, and Listing Rule 5810(c)(3)(A) provides that a failure to meet the minimum bid price requirement exists if the deficiency continues for a period of 30 consecutive business days. The notice had no immediate effect on the listing or the trading of our common stock on The Nasdaq Capital Market. Pursuant to Nasdaq Marketplace Rule 5810(c)(3)(A), the notice letter stated that we had an initial compliance period of 180 calendar days to regain compliance with the minimum bid price requirement. To regain compliance, the closing bid price of our common stock must meet or exceed $1.00 per share for a minimum of 10 consecutive business days during the 180 calendar day grace period. If at any time during this period the bid price of the company’s ADSs closes at or above US$1.00 per share for a minimum of ten consecutive business days, the company will regain compliance with the minimum bid requirement.

On April 13, 2023, we received a letter from the Listing Qualifications Staff (the “Staff”) of Nasdaq confirming the Company had regained compliance with Nasdaq’s minimum bid price requirement under Listing Rule 5550(a)(2). In the letter received on April 13, 2023, the Staff determined that, during the ten consecutive business days from March 29, 2023 to April 12, 2023, the closing bid price of the Company’s ADSs has been at $1.00 per share or greater and accordingly, the Company has regained compliance with Listing Rule 5550(a)(2). The Company also issued an ASX announcement titled, “Kazia Regains Compliance with Nasdaq Minimum Bid Price Requirement” and filed a Form 6-K with the SEC announcing that the Company had regained compliance.

The trading price of the Company’s ordinary shares and American Depositary Shares (“ADSs”) is highly volatile. Your investment could decline in value and the Company may incur significant costs from class action litigations.

The trading price of the Company’s ordinary shares and ADSs is highly volatile in response to various factors, many of which are beyond the Company’s control, including:

| • | unacceptable toxicity findings in animals and humans; |

| • | lack of efficacy in human trials at Phase II stage or beyond; |

| • | announcements of technological innovations by the Company and its competitors; |

| • | new products introduced or announced by the Company or its competitors; |

| • | changes in financial estimates by securities analysts; |

| • | actual or anticipated variations in operating results; |

| • | expiration or termination of licenses, research contracts or other collaboration agreements; |

| • | conditions or trends in the regulatory climate in the biotechnology, pharmaceutical and genomics industries; |

| • | changes in the market values of similar companies; |

| • | changes in the broader macroeconomic environment; |

| • | the liquidity of any market for the Company’s securities; and |

| • | additional sales by the Company of its shares. |

11

Table of Contents

In addition, equity markets in general and the market for biotechnology and life sciences companies in particular, have experienced substantial price and volume fluctuations that have often been unrelated or disproportionate to the operating performance of the companies traded in those markets. Further changes in economic conditions in Australia, the U.S., EU, or globally, could impact the Company’s ability to grow profitably. Adverse economic changes are outside the Company’s control and may result in material adverse effects on the Company’s business or results of operations. These broad market and industry factors may materially affect the market price of the Company’s ordinary shares and ADSs regardless of its development and operating performance. In the past, following periods of volatility in the market price of a company’s securities, securities class action litigation has

often been instituted against that company. Such litigation, if instituted against the Company, could cause it to incur substantial costs and divert management’s attention and resources.

If the market price of the Company’s ADSs falls and remains below US$5.00 per share, under stock exchange rules, the Company’s stockholders will not be able to use such ADSs as collateral for borrowing in margin accounts. This inability to use ADSs as collateral may depress demand as certain institutional investors are restricted from investing in securities priced below US$5.00 and may lead to sales of such ADSs, creating downward pressure on and increased volatility in the market price of the Company’s ordinary shares and ADSs.

A decrease in the trading price of our ADSs could cause their delisting from Nasdaq.

Under Nasdaq rules, companies listed on the Nasdaq Capital Market are required to maintain a share price of at least US$1.00 per share to avoid delisting of their shares. If the share price declines below US$1.00 for a period of 30 consecutive business days, then that listed company would have 180 days to regain compliance with the US$1.00 per share minimum. In the event that the Company’s share price declines below US$1.00, it may be required to take action in order to comply with the Nasdaq rules that may be in effect at the time.

The delisting of our ordinary shares on the ASX may adversely affect the price, liquidity and value of the ADSs.

On 11 October 2023, we announced our intention to delist from the ASX, which is anticipated to become effective on or around 14 November 2023. If the proposed delisting is completed, our ordinary shares will no longer be quoted or traded on the ASX and only the ADSs will be listed on the Nasdaq Stock Market, and as a result, shareholders will no longer be able to trade their ordinary shares on the ASX. Following the completion of the delisting, the Company’s ordinary shares will only be capable of being traded on Nasdaq in the form of ADSs, which will require shareholders to transfer their ordinary shares to ADSs to trade on Nasdaq and engage a suitably qualified Australian broker or a U.S. based broker who is able to trade on Nasdaq, or by off-market, private transactions, which will require shareholders to identify and agree terms with potential purchasers of ordinary shares. In addition, following the completion of the delisting, the Company will no longer be subject to the ASX Listing Rules. We cannot predict the effect of the proposed delisting on the value of our ADSs, however the delisting may restrict the liquidity of these securities by providing only one market on which to trade our securities, which may impair the development or liquidity of an active trading market for the ADSs in the U.S.

You are reliant on the depositary to exercise your voting rights and to receive distributions on ADSs and, as a result, you may be unable to exercise your voting rights on a timely basis or you may not receive certain distributions.

In certain circumstances, holders of ADSs may have limited rights relative to holders of ordinary shares. The rights of holders of ADSs with respect to the voting of ordinary shares and the right to receive certain distributions may be limited in certain respects by the deposit agreement entered into by us and The Bank of New York Mellon. For example, although ADS holders are entitled under the deposit agreement, subject to any applicable provisions of Australian law and of our Constitution, to instruct the depositary as to the exercise of the voting rights pertaining to the ordinary shares represented by the ADSs, and the depositary has agreed that it will try, as far as practical, to vote the ordinary shares so represented in accordance with such instructions, ADS holders may not receive notices sent by the depositary in time to ensure that the depositary will vote the ordinary shares. This means that, from a practical point of view, the holders of ADSs may not be able to exercise their right to vote. In addition, under the deposit agreement, the depositary has the right to restrict distributions to holders of the ADSs in the event that it is unlawful or impractical to make such distributions. We have no obligation to take any action to permit distributions to holders of our ADSs. As a result, holders of ADSs may not receive distributions.

If we are, a passive foreign investment company, or PFIC, there could be adverse U.S. federal income tax consequences to U.S. investors.

Based on the composition of our assets and income, we believe that we were not a PFIC for U.S. federal income tax purposes with respect to our 2022 taxable year. However, there can be no assurance that we will not be considered a PFIC in the current year or for any future taxable year. Our treatment as a PFIC could result in a reduction in the after-tax return to the U.S. holders of our ordinary shares or ADSs and would likely cause a reduction in the value of such ordinary shares or ADSs. For U.S. federal income tax purposes, we will be classified as a PFIC for any taxable year in which either (i) 75% or more of our gross income is passive income, or (ii) at least 50% of the average quarterly value of all of our assets for the taxable year produce or are held for the production of passive income. If we are classified as a PFIC for U.S. federal income tax purposes, highly complex rules will apply to U.S. holders owning ordinary shares or ADSs. Accordingly, you are urged to consult your tax advisors regarding the application of such rules. See Item 10—Additional Information—Taxation, United States Federal Income Tax Consequences for a more complete discussion of the U.S. federal income tax risks related to owning and disposing of our ordinary shares or ADSs.

Currency fluctuations may adversely affect the price of our ordinary shares, ADSs.

Our ordinary shares are quoted in Australian dollars on the ASX and the ADSs are quoted in U.S. dollars on Nasdaq. Movements in the Australian dollar/U.S. dollar exchange rate may adversely affect the U.S. dollar price of the ADSs. In the past year the Australian dollar has generally weakened against the U.S. dollar. However, this trend may not continue and may be reversed.

We may lose our foreign private issuer status, which would then require us to comply with the Exchange Act’s domestic reporting regime and cause us to incur significant legal, accounting and other expenses.

We are a foreign private issuer. In order to maintain our current status as a foreign private issuer, at least 50% of our outstanding ordinary shares must continue to be either directly or indirectly owned of record by non-residents of the United States. If more than 50% of our outstanding ordinary shares are instead held by U.S. residents, then in order to continue to maintain our foreign private issuer status, (i) a majority of our executive officers or directors must not be U.S. citizens or residents, (ii) more than 50% of our assets must not be located in the United States, and (iii) our business must be administered principally outside the United States.

Losing our status as a foreign private issuer would require us to comply with all of the periodic disclosure and current reporting requirements of the Exchange Act applicable to U.S. domestic issuers. We also will be required to make changes in our corporate governance practices in accordance with various SEC and Nasdaq rules. The regulatory and compliance costs to us under U.S. securities laws, if we are required to comply with the reporting requirements applicable to a U.S. domestic issuer, would be significantly higher than the cost we would incur as a foreign private issuer. As a result, we would expect that a loss of foreign private issuer status will increase our legal and financial compliance costs and will make some activities highly time consuming and costly. We also expect that if we will be required to comply with the rules and regulations applicable to U.S. domestic issuers, it will make it more difficult and expensive for us to obtain director and officer liability insurance; we may therefore be required to accept reduced coverage or incur substantially higher costs to obtain coverage. These rules and regulations could also make it more difficult for us to attract and retain qualified members of our board of directors.

12

Table of Contents

Australian takeover laws may discourage takeover offers being made for us or may discourage the acquisition of a significant position in our ordinary shares and ADSs.

We are incorporated in Australia and are subject to the takeover laws of Australia. Among other things, we are subject to the Australian Corporations Act 2001, or the Corporations Act. Subject to a range of exceptions, the Corporations Act prohibits the acquisition of a direct or indirect interest in our issued voting shares if the acquisition of that interest will lead to a person’s voting power in us increasing to more than 20%, or increasing from a starting point that is above 20% and below 90%. Australian takeover laws may discourage takeover offers being made for us or may discourage the acquisition of a significant position in our ordinary shares. This may have the ancillary effect of entrenching our board of directors and may deprive or limit our shareholders’ and ADS holders’ opportunity to sell their ordinary shares and ADSs and may further restrict the ability of our shareholders and ADS holders to obtain a premium from such transactions. See Item 10.B “Additional Information – Memorandum and Articles of Association.”

| Item 4. | Information on the Company |

A. History and development of the Company

Kazia Therapeutics Limited (“Kazia”), a public company limited by shares, was incorporated in March 1994 and registered in New South Wales, Australia. Kazia is registered and operates under the Australian Corporations Act 2001.

Kazia has its registered office at Three International Towers, Level 24, 300 Barangaroo Avenue, Sydney, NSW 2000, Australia. Its telephone number and other contact details are: Phone +61-2-9472 4101; email info@kaziatherapeutics.com; and website, www.kaziatherapeutics.com (the information contained in the website does not form part of the Annual Report). Our agent for service of process in the United States is Vcorp Services, LLC, 25 Robert Pitt Drive, Suite 204, Monsey, New York 10952.

The Company’s Ordinary Shares are listed on the Australian Securities Exchange (“ASX”) under the symbol ‘KZA’ and its ADSs, each representing ten Ordinary Shares, trade on the Nasdaq Capital Market under the symbol ‘KZIA’. The Depositary for the Company’s ADSs is The Bank of New York Mellon, 240 Greenwich Street, New York, NY 10286. All information we file with the SEC is available through the SEC’s Electronic Data Gathering, Analysis and Retrieval system, which may be accessed through the SEC’s website at www.sec.gov.

Resignation of Chairman

Kazia announced that Dr John Friend joined the Kazia Board as Managing Director on 1 August 2023. Kazia announced the resignation of Mr. Iain Ross as Chairman and non-executive director on 11 August 2023. The Board of Directors elected Dr John Friend as Interim Chairman on 11 August 2023.

Kazia announces voluntary delisting from ASX

On 11 October 2023 Kazia announced that it submitted a formal application to the ASX to be removed from the official list of the ASX (Official List) in accordance with ASX Listing Rule 17.11 (Delist or the Delisting). This formal request follows the receipt of in-principle advice from the ASX in relation to the proposed Delisting, subject to the satisfaction of certain conditions. The Board has ultimately determined that the costs, administrative burden and commercial disadvantages of remaining listed on ASX outweigh any benefits of a continued ASX listing. Following the Delisting, the Company will maintain its listing on the Nasdaq and the fully paid ordinary shares of the Company will no longer be quoted on the ASX.

B. Business overview

The ongoing principal business of the Company has been pharmaceutical drug development. The Company is an emerging oncology-focused biotechnology company that has a portfolio of development candidates, diversified across several distinct technologies, with the potential to yield first-in-class and best-in-class agents in a range of oncology indications.

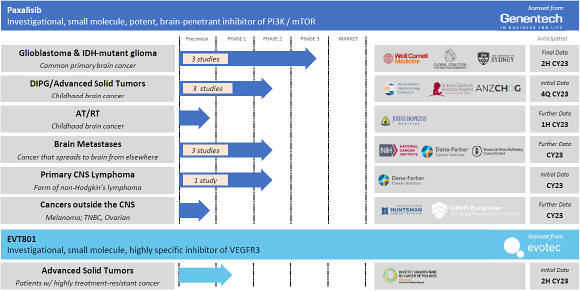

Paxalisib

Kazia’s lead program is paxalisib, (formerly known as GDC-0084), an investigational brain-penetrant inhibitor of the PI3K / Akt / mTOR pathway, that was specifically designed to treat brain cancer.

Paxalisib was developed by Genentech, Inc (South San Francisco, California) and the company entered into a worldwide exclusive license for the asset in October 2016. Prior to this transaction, Genentech had completed an extensive preclinical development program that provided convincing validation for paxalisib as a potential drug for brain cancer. Genentech also completed a phase I clinical trial in 47 patients with advanced recurrent grade III and grade IV glioma (NCT01547546). The most common adverse events were oral mucositis and hyperglycemia. Per RANO criteria, 40% of patients exhibited a best observable response of stable disease, and 26% demonstrated a metabolic partial response on FDG-PET.

The development candidate was granted the International Non-Proprietary Name (INN) ‘paxalisib’ by the World Health Organisation in December 2019. This was confirmed as the United States Adopted Name (USAN) by the USAN Council in April 2020. Paxalisib is orally administered and is presented in a 15mg capsule formulation. The development candidate is the subject of IND 112,608 with the U.S. Food and Drug Administration (“FDA”).

Paxalisib is a potent and selective inhibitor of all four isoforms of phosphoinositide-3-kinase (PI3K) and a moderate inhibitor of the mammalian target of rapamycin (mTOR). The PI3K / Akt / mTOR signaling axis has been shown to be dysregulated in approximately 85-90% of cases of glioblastoma, per Cancer Genome Atlas, and is considered a promising target in this disease. More generally, five PI3K inhibitors have thus far been approved by FDA, for a range of hematological malignancies and solid tumors, making this a well-validated target in cancer. Paxalisib is distinguished from these products by the fact that it is the only PI3K inhibitor in mainstream clinical development which is known to cross the blood-brain barrier, a crucial prerequisite for any novel treatment in brain cancer.

13

Table of Contents

Paxalisib’s mechanism is therefore entirely distinct from that of temozolomide, the existing FDA-approved standard of care treatment. Temozolomide functions primarily by alkylating guanine residues in DNA, thereby inhibiting cell division in the rapidly-growing tumor. Paxalisib, by contrast, inhibits a biochemical control signal, and is therefore associated with a very different resistance and toxicity profile.

Paxalisib is the subject of granted or pending composition-of-matter patents in all key territories. In general, the expiry of these patents is in December 2031. However, the company expects that it will be able to secure patent term extensions in the most substantial markets, including US, EU, China, Japan, and Korea, and that these extensions will provide effective protection until 2036. In addition, the company has recently received notice of grant for a patent protecting the manufacturing process associated with paxalisib, and this will provide an additional layer of protection in relevant territories until 2036.