EXHIBIT 99.1

Management’s Discussion and Analysis

This management’s discussion and analysis is designed to provide you with a narrative explanation through the eyes of our management of our financial condition and results of operations. We recommend that you read this in conjunction with our consolidated interim financial statements for the three and six months ended June 30, 2015, our 2014 annual consolidated financial statements and our 2014 annual management’s discussion and analysis. This management’s discussion and analysis is dated as of July 28, 2015. This management’s discussion and analysis contains forward-looking statements, which are subject to risks and uncertainties that could cause our actual results to differ materially from the forward-looking statements. Forward-looking statements include, but are not limited to, our 2015 outlook and our expectations related to general economic conditions and market trends and their anticipated effects on our business segments. For additional information related to forward-looking statements and material risks associated with them, please see the “Cautionary Note Concerning Factors That May Affect Future Results” section of this management’s discussion and analysis.

We have organized our management’s discussion and analysis in the following key sections:

| • |

Overview – a brief discussion of our business | 2 | ||||

| • |

Results of Operations – a comparison of our current and prior-year period results | 5 | ||||

| • |

Liquidity and Capital Resources – a discussion of our cash flow and debt | 15 | ||||

| • |

Outlook – our current financial outlook for 2015 | 20 | ||||

| • |

Related Party Transactions – a discussion of transactions with our principal and controlling shareholder, The Woodbridge Company Limited (Woodbridge), and others | 22 | ||||

| • |

Subsequent Events – a discussion of material events occurring after June 30, 2015 and through the date of this management’s discussion and analysis | 22 | ||||

| • |

Changes in Accounting Policies – a discussion of changes in our accounting policies and recent accounting pronouncements | 22 | ||||

| • |

Critical Accounting Estimates and Judgments – a discussion of critical estimates and judgments made by our management in applying accounting policies | 22 | ||||

| • |

Additional Information – other required disclosures | 22 | ||||

| • |

Appendix – supplemental information and discussion | 24 | ||||

We prepare our consolidated financial statements in accordance with International Financial Reporting Standards (IFRS), as issued by the International Accounting Standards Board (IASB). This management’s discussion and analysis also includes certain non-IFRS financial measures which we use as supplemental indicators of our operating performance and financial position as well as for internal planning purposes.

References in this discussion to “$” and “US$” are to U.S. dollars and references to “C$” are to Canadian dollars. In addition, “bp” means “basis points” and “n/a” and “n/m” refer to “not applicable” and “not meaningful”, respectively. Unless otherwise indicated or the context otherwise requires, references in this discussion to “we,” “our,” “us” and “Thomson Reuters” are to Thomson Reuters Corporation and our subsidiaries. When we refer to “net sales,” we are referring to new sales less cancellations.

Page 1

OVERVIEW

Our company

We are the leading source of intelligent information for businesses and professionals. We combine industry expertise with innovative technology to deliver critical information to enable our customers to operate in a dynamic business environment. The exponential growth in the volume of data, the impact of technology, and an increasingly complex legal and regulatory environment create challenges for our customers as well as opportunities for our businesses. The breadth and depth of our offerings, our global footprint, and the trust and credibility built by the world’s most trusted news organization uniquely position our company at the confluence of content and technology. We bring in-depth understanding of our customers’ needs, flexible technology platforms, proprietary content and scale. We believe our ability to embed our solutions into customers’ workflows is a significant competitive advantage as it leads to strong customer retention.

We derive the majority of our revenues from selling solutions to our customers, primarily electronically and on a subscription basis. Over the years, this has proven to be capital efficient and cash flow generative, and it has enabled us to maintain leading and scalable positions in our chosen markets.

We are organized in four strategic business units supported by a corporate center:

|

Financial & Risk, a provider of critical news, information and analytics, enabling transactions and bringing together financial communities. Financial & Risk also provides regulatory and operational risk management solutions. | |

|

|

Legal, a provider of critical online and print information, decision tools, software and services that support legal, investigation, business and government professionals around the world. | |

|

|

Tax & Accounting, a provider of integrated tax compliance and accounting information, software and services for professionals in accounting firms, corporations, law firms and government. | |

|

|

Intellectual Property & Science, a provider of comprehensive intellectual property and scientific information, decision support tools and services that enable the lifecycle of innovation for governments, academia, publishers, corporations and law firms to discover, protect and commercialize new ideas and brands. | |

We also have a Global Growth & Operations (GGO) organization which works across our business units to combine our global capabilities and to expand our local presence and development in countries and regions where we believe the greatest growth opportunities exist. Our GGO organization is focused on supporting our businesses in the following geographic areas: Latin America, China, India, the Middle East, Africa, the Association of Southeast Asian Nations/North Asia, Russia and countries comprising the Commonwealth of Independent States and Turkey. We do not report GGO as a separate business unit, but rather include its results within our strategic business units.

We operate Reuters, which is a provider of real-time, high-impact, multimedia news and information services to newspapers, television and cable networks, radio stations and websites around the globe. Our Reuters News business is managed and reported within our corporate center.

Page 2

Key Highlights

Second quarter performance:

| Non-IFRS Financial Measures(1) (millions of U.S. dollars, except per share amounts and margins) |

2015 | 2014 | CHANGE | CHANGE IN CONSTANT CURRENCY | ||||||||||

| Revenues from ongoing businesses |

3,038 | 3,158 | (4%) | 2% | ||||||||||

| Adjusted EBITDA |

856 | 877 | (2%) | 3% | ||||||||||

| Adjusted EBITDA margin |

28.2% | 27.8% | 40bp | 50bp | ||||||||||

| Underlying operating profit |

576 | 581 | (1%) | 7% | ||||||||||

| Underlying operating profit margin |

19.0% | 18.4% | 60bp | 100bp | ||||||||||

| Adjusted earnings per share (adjusted EPS) |

$0.52 | $0.51 | 2% | 14% |

Our second quarter results were consistent with our expectations, and we reaffirmed our full-year business outlook in connection with announcing those results. Given the significant impact that changes in foreign exchange rates continue to have on our results, we are providing additional information in this management’s discussion and analysis about our performance at constant currency rates.

Revenues from ongoing businesses increased in constant currency, reflecting growth across all of our business units. The increase was entirely from existing businesses. On a combined basis, revenues from our Legal, Tax & Accounting and Intellectual Property & Science businesses grew 2% and revenues from our Financial & Risk business grew 1%.

| SECOND QUARTER 2015 REVENUES FROM ONGOING BUSINESSES

| ||

|

• Financial & Risk’s revenues increased 1%, all from existing businesses. This was the first time Financial & Risk had positive growth in more than three years. The performance was driven by positive net sales in each of the last five quarters and an annual price increase. These factors were partly offset by the lower price realization resulting from the migration of some of Financial & Risk’s foreign exchange and buy-side customers to new products on the unified technology platform. Financial & Risk’s major product and platform migration programs remain on schedule and its EBITDA margin continues to improve.

• Legal’s revenues increased 2%, all from existing businesses, as Legal Solutions businesses growth of 5% more than offset a 5% decline in U.S. print. U.S. online legal information revenues grew slightly in the quarter.

• Tax & Accounting revenues grew 6% (5% from existing businesses), despite a decline in the Government business.

• Intellectual Property & Science revenues increased 1%, all from existing businesses, as recurring revenue growth of 4% was partly offset by lower transaction revenues. |

|

Adjusted EBITDA and underlying operating profit declined due to the impact of foreign currency on our results. In constant currency, adjusted EBITDA, underlying operating profit and the related margins increased as higher revenues offset a modest increase in operating expenses. Adjusted EPS increased slightly, but included a $0.06 negative impact from foreign currency. In constant currency, adjusted EPS increased primarily due to higher underlying operating profit.

In 2015, we plan to capitalize on our position to help our customers navigate the information age. Specifically, we are focused on further improving execution across our company by:

| • | investing in sales and marketing expertise, as well as customer service capabilities; |

| • | implementing several key product and platform migrations in our Financial & Risk business, which we believe will improve service levels to our customers and drive cost savings; and |

| • | delivering strong and consistent cash flow to reinvest in our growth businesses while returning capital to our shareholders through dividends and share repurchases. |

We have returned over $3.8 billion to shareholders through share repurchases and dividends since we announced our capital strategy program in October 2013.

| (1) | Refer to Appendix A for additional information on non-IFRS financial measures. |

Page 3

2015 Outlook:

We recently reaffirmed our 2015 full-year business outlook that we originally communicated in February. For 2015, we continue to expect positive revenue from existing businesses (organic), adjusted EBITDA margin between 27.5% and 28.5%, underlying operating profit margin between 18.5% and 19.5%, and free cash flow between $1.55 billion and $1.75 billion.

Our 2015 outlook assumes constant currency rates relative to 2014 and is based on the expected performance of our existing businesses and does not factor in the impact of any acquisitions or divestitures that may occur during the year. In light of increased volatility recently experienced in the foreign exchange markets, we continue to believe that currency is having a higher than usual impact on our results in 2015. Additional information is provided in the “Outlook” section of this management’s discussion and analysis. The information in this section is forward-looking and should also be read in conjunction with the section of this management’s discussion and analysis entitled “Cautionary Note Concerning Factors That May Affect Future Results”.

Seasonality

Our revenues and operating profit on a consolidated basis do not tend to be significantly impacted by seasonality as we record a large portion of our revenues ratably over a contract term and our costs are generally incurred evenly throughout the year. However, our non-recurring revenues can cause changes in our performance from quarter to consecutive quarter. Additionally, the release of certain print-based offerings can be seasonal as can certain product releases for the regulatory markets, which tend to be concentrated at the end of the year. Our quarterly performance may also be impacted by the timing of certain product migrations we are in the process of executing, as well as by volatile foreign currency exchange rates, as we have recently experienced. As a consequence, the results of certain of our segments can be impacted by seasonality to a greater extent than our consolidated revenues and operating profit.

Use of non-IFRS financial measures

In addition to our results reported in accordance with IFRS, we use certain non-IFRS financial measures as supplemental indicators of our operating performance and financial position, as well as for internal planning purposes. These non-IFRS financial measures include:

| • | Revenues from ongoing businesses; |

| • | Revenue changes at constant currency (before currency or revenues excluding the effects of foreign currency); |

| • | Underlying operating profit and the related margin; |

| • | Adjusted EBITDA and the related margin; |

| • | Adjusted EBITDA less capital expenditures and the related margin; |

| • | Adjusted earnings and adjusted earnings per share; |

| • | Net debt; |

| • | Free cash flow; and |

| • | Free cash flow from ongoing businesses. |

Given the increased volatility recently experienced in the foreign exchange markets, currency has had a significant impact on our results for the three and six months ended June 30, 2015. We believe analysis of our results excluding the effects of foreign currency improves comparability. Accordingly, we have supplemented our analysis in this management’s discussion and analysis with the following non-IFRS measures:

| • | Changes in underlying operating profit and the related margin at constant currency (before currency or changes in underlying operating profit and the related margin excluding the effects of foreign currency); |

| • | Changes in adjusted EBITDA and the related margin at constant currency (before currency or changes in adjusted EBITDA and the related margin excluding the effects of foreign currency); and |

| • | Changes in adjusted earnings per share at constant currency (before currency or changes in adjusted earnings per share excluding the effects of foreign currency). |

We report non-IFRS financial measures as we believe their use provides more insight into and understanding of our performance. See Appendix A of this management’s discussion and analysis for a description of our non-IFRS financial measures, including an explanation of why we believe they are useful measures of our performance, including our ability to generate cash flow. Refer to the sections of this management’s discussion and analysis entitled “Results of Operations”, “Liquidity and Capital Resources” and Appendix B for reconciliations of these non-IFRS financial measures to the most directly comparable IFRS financial measures.

Page 4

RESULTS OF OPERATIONS

Basis of presentation

In this management’s discussion and analysis, we discuss our results of operations on both an IFRS and non-IFRS basis. Both bases exclude discontinued operations and include the performance of acquired businesses from the date of purchase.

Consolidated results

We discuss our consolidated results from continuing operations on an IFRS basis, as reported in our consolidated income statement. Additionally, we discuss our consolidated results on a non-IFRS basis using the measures described within the “Use of Non-IFRS Financial Measures” section of this management’s discussion and analysis. Among other adjustments, our non-IFRS revenue and profitability measures as well as free cash flow from ongoing businesses exclude Other Businesses, which is an aggregation of businesses that have been or are expected to be exited through sale or closure that did not qualify for discontinued operations classification.

Segment results

We discuss the results of our four reportable segments as presented in our consolidated interim financial statements for the three and six months ended June 30, 2015: Financial & Risk, Legal, Tax & Accounting and Intellectual Property & Science.

We also provide information on “Corporate & Other” and “Other Businesses”. These categories neither qualify as a component of another reportable segment nor as a separate reportable segment.

| • | Corporate & Other includes expenses for corporate functions, certain share-based compensation costs and the Reuters News business, which is comprised of the Reuters News Agency and consumer publishing; and |

| • | Other Businesses is an aggregation of businesses that have been or are expected to be exited through sale or closure that did not qualify for discontinued operations classification. The results of Other Businesses are not comparable from period to period as the composition of businesses changes due to the timing of completed divestitures. |

See note 3 of our consolidated interim financial statements for the three and six months ended June 30, 2015 which includes a reconciliation of results from our reportable segments to consolidated results as reported in our consolidated income statement.

In analyzing our revenues from ongoing businesses, at both the consolidated and segment levels, we identify the impact of foreign currency changes. Additionally, we separately measure revenue growth from existing businesses and from acquired businesses on a constant currency basis.

Consolidated results

| THREE MONTHS ENDED JUNE 30, | SIX MONTHS ENDED JUNE 30, | |||||||||||||||||||||||||||||||

| CHANGE | CHANGE | |||||||||||||||||||||||||||||||

| (millions of U.S. dollars, except per share amounts and margins) | 2015 | 2014 | Total | Constant currency |

2015 | 2014 | Total | Constant currency |

||||||||||||||||||||||||

| IFRS Financial Measures |

||||||||||||||||||||||||||||||||

| Revenues |

3,038 | 3,159 | (4%) | 6,082 | 6,289 | (3%) | ||||||||||||||||||||||||||

| Operating profit |

405 | 381 | 6% | 812 | 740 | 10% | ||||||||||||||||||||||||||

| Diluted earnings per share |

$0.33 | $0.31 | 6% | $0.71 | $0.65 | 9% | ||||||||||||||||||||||||||

| Non-IFRS Financial Measures |

||||||||||||||||||||||||||||||||

| Revenues from ongoing businesses |

3,038 | 3,158 | (4%) | 2% | 6,082 | 6,287 | (3%) | 2% | ||||||||||||||||||||||||

| Adjusted EBITDA |

856 | 877 | (2%) | 3% | 1,659 | 1,697 | (2%) | 4% | ||||||||||||||||||||||||

| Adjusted EBITDA margin |

28.2% | 27.8% | 40bp | 50bp | 27.3% | 27.0% | 30bp | 50bp | ||||||||||||||||||||||||

| Adjusted EBITDA less capital expenditures |

633 | 652 | (3%) | 1,133 | 1,224 | (7%) | ||||||||||||||||||||||||||

| Adjusted EBITDA less capital expenditures margin |

20.8% | 20.6% | 20bp | 18.6% | 19.5% | (90)bp | ||||||||||||||||||||||||||

| Underlying operating profit |

576 | 581 | (1%) | 7% | 1,091 | 1,109 | (2%) | 6% | ||||||||||||||||||||||||

| Underlying operating profit margin |

19.0% | 18.4% | 60bp | 100bp | 17.9% | 17.6% | 30bp | 80bp | ||||||||||||||||||||||||

| Adjusted earnings per share |

$0.52 | $0.51 | 2% | 14% | $0.96 | $0.97 | (1%) | 10% | ||||||||||||||||||||||||

Foreign currency effects. With respect to the average foreign exchange rates that we use to report our results, the U.S. dollar strengthened significantly against the Euro, the British pound sterling, the Japanese yen and the Canadian dollar in the second quarter and six-month period ended June 30, 2015 compared to the same periods in 2014. Given our currency mix of revenues and expenses around the world, these fluctuations had a negative impact on our consolidated revenues, as well as on our consolidated adjusted EBITDA and underlying operating profit margins. The revenues of each of our segments were negatively impacted by foreign currency movements. However, certain of our segments experienced benefits to their related margins, reflecting their specific currency profiles.

Page 5

Revenues

| THREE MONTHS ENDED JUNE 30, | PERCENTAGE CHANGE: | |||||||||||||||||||

| (millions of U.S. dollars) |

2015 | 2014 | Existing businesses |

Acquired businesses |

Constant currency |

Foreign currency |

Total | |||||||||||||

| Revenues from ongoing businesses |

3,038 | 3,158 | 2% | - | 2% | (6%) | (4%) | |||||||||||||

| Other Businesses |

- | 1 | n/m | n/m | n/m | n/m | n/m | |||||||||||||

| Revenues |

3,038 | 3,159 | n/m | n/m | n/m | n/m | (4%) | |||||||||||||

| SIX MONTHS ENDED JUNE 30, | PERCENTAGE CHANGE: | |||||||||||||||||||

| (millions of U.S. dollars) |

2015 | 2014 | Existing businesses |

Acquired businesses |

Constant currency |

Foreign currency |

Total | |||||||||||||

| Revenues from ongoing businesses |

6,082 | 6,287 | 1% | 1% | 2% | (5%) | (3%) | |||||||||||||

| Other Businesses |

- | 2 | n/m | n/m | n/m | n/m | n/m | |||||||||||||

| Revenues |

6,082 | 6,289 | n/m | n/m | n/m | n/m | (3%) | |||||||||||||

Revenues from ongoing businesses increased on a constant currency basis in the second quarter reflecting growth across all of our business segments. In the six-month period, the increase in revenues from ongoing businesses was driven by combined growth of 3% from our Legal, Tax & Accounting and Intellectual Property & Science segments, as our Financial & Risk segment revenues were essentially unchanged. Revenues from acquired businesses, primarily from our Tax & Accounting segment, contributed to revenue growth in the six-month period.

Revenues from our GGO organization comprised approximately 10% of our revenues in both the second quarter and six-month period. On a constant currency basis, revenues grew 6% and 7% (6% and 5% from existing businesses) in the second quarter and six-month period, respectively.

Operating profit, underlying operating profit, adjusted EBITDA and adjusted EBITDA less capital expenditures

| THREE MONTHS ENDED JUNE 30, | SIX MONTHS ENDED JUNE 30, | |||||||||||||||||||||||||||||||

| CHANGE | CHANGE | |||||||||||||||||||||||||||||||

| (millions of U.S. dollars, except margins) | 2015 | 2014 | Total | Constant currency |

2015 | 2014 | Total | Constant currency |

||||||||||||||||||||||||

| Operating profit |

405 | 381 | 6% | 812 | 740 | 10% | ||||||||||||||||||||||||||

| Adjustments to remove: |

||||||||||||||||||||||||||||||||

| Amortization of other identifiable intangible assets |

147 | 165 | 296 | 328 | ||||||||||||||||||||||||||||

| Fair value adjustments |

59 | 33 | 6 | 35 | ||||||||||||||||||||||||||||

| Other operating (gains) losses, net |

(35) | 2 | (23) | 5 | ||||||||||||||||||||||||||||

| Operating loss from Other Businesses |

- | - | - | 1 | ||||||||||||||||||||||||||||

| Underlying operating profit |

576 | 581 | (1%) | 7% | 1,091 | 1,109 | (2%) | 6% | ||||||||||||||||||||||||

| Remove: depreciation and amortization of computer software (excluding Other Businesses) |

280 | 296 | 568 | 588 | ||||||||||||||||||||||||||||

| Adjusted EBITDA(1) |

856 | 877 | (2%) | 3% | 1,659 | 1,697 | (2%) | 4% | ||||||||||||||||||||||||

| Deduct: capital expenditures, less proceeds from disposals (excluding Other Businesses) |

223 | 225 | 526 | 473 | ||||||||||||||||||||||||||||

| Adjusted EBITDA less capital expenditures(1) |

633 | 652 | (3%) | 1,133 | 1,224 | (7%) | ||||||||||||||||||||||||||

| Underlying operating profit margin |

19.0% | 18.4% | 60bp | 100bp | 17.9% | 17.6% | 30bp | 80bp | ||||||||||||||||||||||||

| Adjusted EBITDA margin |

28.2% | 27.8% | 40bp | 50bp | 27.3% | 27.0% | 30bp | 50bp | ||||||||||||||||||||||||

| Adjusted EBITDA less capital expenditures margin |

20.8% | 20.6% | 20bp | 18.6% | 19.5% | (90)bp | ||||||||||||||||||||||||||

| (1) | See Appendix B for a reconciliation of net earnings to adjusted EBITDA and adjusted EBITDA less capital expenditures. |

Operating profit increased in both periods due to higher revenues(2) and a gain on the sale of the Fiduciary Services and Competitive Intelligence unit of our Lipper business (Lipper Services), which were partly offset by a modest increase in operating expenses(2) and the impact of unfavorable foreign currency movements. Additionally, in the six-month period, operating profit increased due to lower unfavorable fair value adjustments.

| (2) | On a constant currency basis. |

Page 6

In both periods, adjusted EBITDA and underlying operating profit declined due to foreign currency. On a constant currency basis, adjusted EBITDA, underlying operating profit and the related margins increased primarily due to higher revenues, which more than offset a modest increase in expenses. Underlying operating profit and the related margins also benefited from lower depreciation and amortization expense.

Adjusted EBITDA less capital expenditures decreased in the second quarter due to lower adjusted EBITDA. The decline in the six-month period reflected lower adjusted EBITDA and higher capital expenditures.

Operating expenses

| THREE MONTHS ENDED JUNE 30, |

SIX MONTHS ENDED JUNE 30, |

|||||||||||||||||||||||||

| (millions of U.S. dollars) | 2015 | 2014 | CHANGE | 2015 | 2014 | CHANGE | ||||||||||||||||||||

| Operating expenses |

2,241 | 2,315 | (3%) | 4,429 | 4,628 | (4%) | ||||||||||||||||||||

| Adjustments to remove: |

||||||||||||||||||||||||||

| Fair value adjustments(1) |

(59) | (33) | (6) | (35) | ||||||||||||||||||||||

| Other Businesses |

- | (1) | - | (3) | ||||||||||||||||||||||

| Operating expenses, excluding fair value adjustments and Other Businesses |

2,182 | 2,281 | (4%) | 4,423 | 4,590 | (4%) | ||||||||||||||||||||

| (1) | Fair value adjustments primarily represent non-cash accounting adjustments from the revaluation of embedded foreign exchange derivatives within certain customer contracts due to fluctuations in foreign exchange rates and mark-to-market adjustments from certain share-based awards. |

In both periods, operating expenses, excluding fair value adjustments and Other Businesses decreased due to the impact of foreign currency. On a constant currency basis, operating expenses, excluding fair value adjustments and Other Businesses, increased slightly. The increase reflected higher investments in certain growth businesses, and timing of our annual salary increases for employees that came into effect in the second quarter of this year compared to the third quarter of last year. These increases were mitigated by lower expenses from earlier efficiency initiatives, primarily in our Financial & Risk segment. Expenses in the second quarter and six-month period of 2014 included $30 million and $40 million, respectively, of efficiency-related charges, which were primarily severance.

Depreciation and amortization

| THREE MONTHS ENDED JUNE 30, |

SIX MONTHS ENDED JUNE 30, |

|||||||||||||||||||||||||

| (millions of U.S. dollars) | 2015 | 2014 | CHANGE | 2015 | 2014 | CHANGE | ||||||||||||||||||||

| Depreciation |

87 | 99 | (12%) | 182 | 197 | (8%) | ||||||||||||||||||||

| Amortization of computer software |

193 | 197 | (2%) | 386 | 391 | (1%) | ||||||||||||||||||||

| Subtotal |

280 | 296 | (5%) | 568 | 588 | (3%) | ||||||||||||||||||||

| Amortization of other identifiable intangible assets |

147 | 165 | (11%) | 296 | 328 | (10%) | ||||||||||||||||||||

| • | Depreciation and amortization of computer software on a combined basis decreased in both periods as the impact of foreign currency and the completion of depreciation and amortization of assets acquired in previous years more than offset higher expenses associated primarily with product development initiatives across our business. |

| • | Amortization of other identifiable intangible assets decreased in both periods, primarily due to the impact of foreign currency, and the completion of amortization for certain identifiable intangible assets acquired in previous years. |

Other operating gains (losses), net

| THREE MONTHS ENDED JUNE 30, |

SIX MONTHS ENDED JUNE 30, |

|||||||||||||||||

| (millions of U.S. dollars) | 2015 | 2014 | 2015 | 2014 | ||||||||||||||

| Other operating gains (losses), net |

35 | (2) | 23 | (5) | ||||||||||||||

In the second quarter and six months ended June 30, 2015, other operating gains, net, were primarily comprised of a gain from the sale of our Lipper Services business.

Page 7

Net interest expense

| THREE MONTHS ENDED JUNE 30, |

SIX MONTHS ENDED JUNE 30, |

|||||||||||||||||||||||||

| (millions of U.S. dollars) | 2015 | 2014 | CHANGE | 2015 | 2014 | CHANGE | ||||||||||||||||||||

| Net interest expense |

107 | 111 | (4%) | 212 | 219 | (3%) | ||||||||||||||||||||

The decrease in net interest expense in both periods was primarily due to lower interest on our debt obligations reflecting the refinancing of certain debt obligations during 2014 and lower interest on certain tax liabilities. These decreases were partly offset by higher pension-related interest costs driven by a higher valuation of our net pension obligations. As over 95% of our long-term debt obligations paid interest at fixed rates (after swaps), the net interest expense on the balance of our debt was relatively unchanged.

Other finance (costs) income

| THREE MONTHS ENDED JUNE 30, |

SIX MONTHS ENDED JUNE 30, |

|||||||||||||||||

| (millions of U.S. dollars) | 2015 | 2014 | 2015 | 2014 | ||||||||||||||

| Other finance (costs) income |

(5) | 29 | 37 | 57 | ||||||||||||||

Other finance (costs) income primarily included gains or losses realized from changes in foreign currency exchange rates on certain intercompany funding arrangements and certain gains or losses related to foreign exchange contracts.

Tax expense

| THREE MONTHS ENDED JUNE 30, |

SIX MONTHS ENDED JUNE 30, |

|||||||||||||||||

| (millions of U.S. dollars) | 2015 | 2014 | 2015 | 2014 | ||||||||||||||

| Tax expense |

14 | 40 | 42 | 27 | ||||||||||||||

The tax expense in each period reflected the mix of taxing jurisdictions in which pre-tax profits and losses were recognized. Because the geographical mix of pre-tax profits and losses in interim periods may be different from that for the full-year, tax expense or benefit in interim periods is not necessarily indicative of tax expense for the full-year.

Additionally, the comparability of our tax expense was impacted by various transactions and accounting adjustments during each period. The following table sets forth certain components within income tax expense that impact comparability from period-to-period, including tax expense (benefit) associated with items that are removed from adjusted earnings:

| TAX EXPENSE (BENEFIT) | THREE MONTHS ENDED JUNE 30, |

SIX MONTHS ENDED JUNE 30, |

||||||||||||||||

| (millions of U.S. dollars) | 2015 | 2014 | 2015 | 2014 | ||||||||||||||

| Tax items impacting comparability: |

||||||||||||||||||

| Corporate tax rates(1) |

6 | - | 5 | (2) | ||||||||||||||

| Other tax adjustments(2) |

(2) | 14 | (7) | 2 | ||||||||||||||

| Subtotal |

4 | 14 | (2) | - | ||||||||||||||

| Tax related to: |

||||||||||||||||||

| Fair value adjustments |

(11) | (8) | 5 | (7) | ||||||||||||||

| Other items |

- | 4 | (2) | 3 | ||||||||||||||

| Subtotal |

(11) | (4) | 3 | (4) | ||||||||||||||

| Total |

(7) | 10 | 1 | (4) | ||||||||||||||

| (1) | Relates to the net changes of deferred tax liabilities due to changes in U.S. state apportionment factors and changes in corporate tax rates that were substantively enacted in certain jurisdictions. |

| (2) | Relates primarily to changes in the recognition of deferred tax assets in various jurisdictions due to acquisitions, assumptions regarding future profitability, and adjustments for indefinite-lived assets and liabilities that are not expected to reverse. |

Because the items described above impact the comparability of our tax expense for each period, we remove them from our calculation of adjusted earnings, along with the pre-tax items to which they relate.

Page 8

The computation of our adjusted tax expense is set forth below:

| THREE MONTHS ENDED JUNE 30, |

SIX MONTHS ENDED JUNE 30, |

|||||||||||||||||

| (millions of U.S. dollars) | 2015 | 2014 | 2015 | 2014 | ||||||||||||||

| Tax expense (benefit) |

14 | 40 | 42 | 27 | ||||||||||||||

| Remove: Items from above impacting comparability |

7 | (10) | (1) | 4 | ||||||||||||||

| Other adjustments: |

||||||||||||||||||

| Interim period effective tax rate normalization(1) |

(2) | (7) | (3) | 5 | ||||||||||||||

| Tax charge amortization(2) |

21 | 21 | 43 | 43 | ||||||||||||||

| Total tax expense on adjusted earnings |

40 | 44 | 81 | 79 | ||||||||||||||

| (1) | Adjustment to reflect income taxes based on estimated full-year effective tax rate. Reported earnings or loss for interim periods reflect income taxes based on the estimated effective tax rates of each of the jurisdictions in which we operate. The adjustment reallocates estimated full-year income taxes between interim periods, but has no effect on full-year income taxes. |

| (2) | In 2013, we recorded $604 million of deferred tax charges associated with the consolidation of the ownership and management of our technology and content assets. Within our tax expense on adjusted earnings, we amortize these deferred charges on a straight-line basis over seven years. We believe this treatment more appropriately reflects our tax position because these charges are expected to be paid over seven years from the date of the original transaction, in varying annual amounts, in conjunction with the repayments of interest-bearing notes that were issued as consideration in the original transactions. |

Net earnings and earnings per share

| THREE MONTHS ENDED JUNE 30, |

SIX MONTHS ENDED JUNE 30, |

|||||||||||||||||||||||||

| (millions of U.S. dollars, except per share amounts) | 2015 | 2014 | CHANGE | 2015 | 2014 | CHANGE | ||||||||||||||||||||

| Net earnings |

281 | 260 | 8% | 601 | 552 | 9% | ||||||||||||||||||||

| Diluted earnings per share |

$0.33 | $0.31 | 6% | $0.71 | $0.65 | 9% | ||||||||||||||||||||

Net earnings and diluted earnings per share increased in the second quarter as higher operating profit and lower tax expense were partly offset by higher net finance costs and adverse currency movements. The increase in net earnings and diluted earnings per share in the six-month period reflected the same factors, except for higher tax expense.

Adjusted earnings and adjusted earnings per share

| THREE MONTHS ENDED JUNE 30, |

SIX MONTHS ENDED JUNE 30, |

|||||||||||||||||||||||||||||||||

| CHANGE | CHANGE | |||||||||||||||||||||||||||||||||

| (millions of U.S. dollars, except per share amounts and share data) | 2015 | 2014 | Total | Constant currency |

2015 | 2014 | Total | Constant currency |

||||||||||||||||||||||||||

| Earnings attributable to common shareholders |

262 | 249 | 5% | 567 | 531 | 7% | ||||||||||||||||||||||||||||

| Adjustments to remove: |

||||||||||||||||||||||||||||||||||

| Operating loss from Other Businesses |

- | - | - | 1 | ||||||||||||||||||||||||||||||

| Fair value adjustments |

59 | 33 | 6 | 35 | ||||||||||||||||||||||||||||||

| Other operating (gains) losses, net |

(35) | 2 | (23) | 5 | ||||||||||||||||||||||||||||||

| Other finance costs (income) |

5 | (29) | (37) | (57) | ||||||||||||||||||||||||||||||

| Share of post-tax earnings in equity method investments |

(2) | (1) | (6) | (1) | ||||||||||||||||||||||||||||||

| Tax on above items(1) |

(11) | (4) | 3 | (4) | ||||||||||||||||||||||||||||||

| Tax items impacting comparability(1) |

4 | 14 | (2) | - | ||||||||||||||||||||||||||||||

| Amortization of other identifiable intangible assets |

147 | 165 | 296 | 328 | ||||||||||||||||||||||||||||||

| Interim period effective tax rate normalization(1) |

2 | 7 | 3 | (5) | ||||||||||||||||||||||||||||||

| Tax charge amortization(1) |

(21) | (21) | (43) | (43) | ||||||||||||||||||||||||||||||

| Dividends declared on preference shares |

- | - | (1) | (1) | ||||||||||||||||||||||||||||||

| Adjusted earnings |

410 | 415 | (1%) | 763 | 789 | (3%) | ||||||||||||||||||||||||||||

| Adjusted earnings per share (adjusted EPS) |

$0.52 | $0.51 | 2% | 14% | $0.96 | $0.97 | (1%) | 10% | ||||||||||||||||||||||||||

| Diluted weighted-average common shares (millions) |

788.9 | 813.4 | 793.2 | 817.3 | ||||||||||||||||||||||||||||||

| (1) | See the “Tax expense” section above for additional information. |

Page 9

In the second quarter, adjusted earnings decreased while the related per share amount slightly increased. Both adjusted earnings and adjusted earnings per share included a negative impact from foreign currency, which amounted to $0.06 on a per share basis. In the six-month period, both adjusted earnings and adjusted earnings per share decreased due to a negative impact from foreign currency, which amounted to $0.11 on a per share basis. On a constant currency basis, adjusted earnings and the related per share amounts increased in both periods primarily due to higher underlying operating profit. Additionally, adjusted earnings per share benefited from lower diluted weighted-average common shares due to share repurchases (see the “Liquidity and Capital Resources—Share Repurchases” section of this management’s discussion and analysis for additional information).

Segment results

A discussion of the operating results of our Financial & Risk, Legal, Tax & Accounting and Intellectual Property & Science reportable segments follows:

| • | Results from the Reuters News business are included in “Corporate & Other”. These results as well as Other Businesses are both excluded from our reportable segments as neither of them qualify as a component of our four reportable segments, nor as a separate reportable segment. |

| • | We use segment operating profit to measure the operating performance of our reportable segments. |

| — | The costs of centralized support services such as technology, editorial, real estate, accounting, procurement, legal and human resources are allocated to each segment based on usage or other applicable measures. |

| — | We define segment operating profit as operating profit before (i) amortization of other identifiable intangible assets; (ii) other operating gains and losses; (iii) certain asset impairment charges; (iv) corporate-related items; and (v) fair value adjustments. We use this measure because we do not consider these excluded items to be controllable operating activities for purposes of assessing the current performance of our reportable segments. |

| — | We also use segment operating profit margin, which we define as segment operating profit as a percentage of revenues. |

| — | Our definition of segment operating profit may not be comparable to that of other companies. |

| • | As a supplemental measure of segment operating performance, we add back depreciation and amortization of computer software to segment operating profit to arrive at each segment’s EBITDA and the related margin as a percentage of revenues. See Appendix B of this management’s discussion and analysis for additional information. |

Financial & Risk

| THREE MONTHS ENDED JUNE 30, | PERCENTAGE CHANGE: | |||||||||||||||||||||||||||||

| (millions of U.S. dollars, except margins) | 2015 | 2014 |

|

Existing businesses |

|

|

Acquired businesses |

|

|

Constant currency |

|

|

Foreign currency |

|

Total | |||||||||||||||

| Revenues |

1,552 | 1,655 | 1% | - | 1% | (7%) | (6%) | |||||||||||||||||||||||

| EBITDA |

430 | 426 | 1% | |||||||||||||||||||||||||||

| EBITDA margin |

27.7% | 25.7% | 200bp | |||||||||||||||||||||||||||

| Segment operating profit |

274 | 266 | 3% | |||||||||||||||||||||||||||

| Segment operating profit margin |

17.7% | 16.1% | 160bp | |||||||||||||||||||||||||||

| SIX MONTHS ENDED JUNE 30, | PERCENTAGE CHANGE: | |||||||||||||||||||||||||||||

| (millions of U.S. dollars, except margins) | 2015 | 2014 |

|

Existing businesses |

|

|

Acquired businesses |

|

|

Constant currency |

|

|

Foreign currency |

|

Total | |||||||||||||||

| Revenues |

3,104 | 3,313 | - | - | - | (6%) | (6%) | |||||||||||||||||||||||

| EBITDA |

831 | 825 | 1% | |||||||||||||||||||||||||||

| EBITDA margin |

26.8% | 24.9% | 190bp | |||||||||||||||||||||||||||

| Segment operating profit |

515 | 506 | 2% | |||||||||||||||||||||||||||

| Segment operating profit margin |

16.6% | 15.3% | 130bp | |||||||||||||||||||||||||||

Page 10

Revenues on a constant currency basis increased during the second quarter, all from existing businesses. This was the first quarter in more than three years that Financial & Risk reported growth on this basis. The increase in revenues was driven by positive net sales in each of the last five quarters, an annual price increase and higher transactions revenues. Net sales have now improved year-over-year in 10 of the last 11 quarters. These factors were partly offset by the lower price realization resulting from the migration of some of Financial & Risk’s foreign exchange and buy-side customers to new products on its unified platform, as well as a 1% decline in Recoveries revenues. However, we expect the decline in Recoveries revenues will increase over the second half of the year as more third parties move to direct billing. Accordingly, we do not expect incremental improvement in Financial & Risk’s revenue growth rate in the second half of the year. In the six-month period, revenues on a constant currency basis were essentially unchanged, but reflected similar dynamics as the second quarter.

By geographic area, second quarter revenues in the Americas and Asia Pacific increased 1%, while revenues in Europe, Middle East and Africa (EMEA) were essentially unchanged. For the six-month period, revenues increased in the Americas, decreased in EMEA, and were essentially unchanged in Asia Pacific. In both periods, net sales were positive in all regions.

Financial & Risk’s revenue performance in the second quarter of 2015 was positively impacted by two favorable trends.

| • | First, Financial & Risk’s business mix has been evolving as higher growth businesses, such as feeds and non-desktop products (such as Elektron Managed Services and Governance, Risk & Compliance solutions) are becoming a greater proportion of the segment’s revenue base. In the second quarter, feeds and non-desktop product revenues collectively represented 36% of Financial & Risk’s revenues (Q2 2014 - 34%) and grew 6% and 5%, respectively. |

| • | Second, we believe Financial & Risk now offers better desktop products and as a result, it has improved desktop retention rates. Desktop revenues, which represented 41% of the segment’s revenue base in the second quarter (Q2 2014–42%) had a 3% decline, which reflected the impact of the migration activity and resulting lower price realization. However, excluding the negative impact of the lower price realization, desktop revenues grew slightly. |

The major product and platform migrations that Financial & Risk has planned in 2015 are on schedule. We have converted approximately half of the revenue base associated with the migration of our remaining buy-side and foreign exchange customers. Further, relative to the closure of our legacy real time platform, we have moved over 90% of customers to the new Elektron platform, with approximately 85% of those customers entirely off the legacy platform. We expect to continue incurring some dual running costs until the legacy platform is closed in the fourth quarter.

|

Results by type were:

• Subscription revenues increased 1% in the second quarter reflecting the impact of positive net sales in each of the last five quarters and a benefit from an annual price increase. These factors were partly offset by the commercial impacts associated with the migration of some customers to Financial & Risk’s unified technology platform. Revenues for the six-month period were essentially unchanged;

• Transactions revenues increased 3% in both the second quarter and the six-month period, as contributions from the FXall, Tradeweb and BETA businesses were partly offset by lower FX matching transaction revenues; and

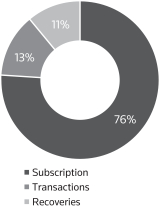

• Recoveries revenues (low-margin revenues that we collect and largely pass-through to a third party provider, such as stock exchange fees) decreased 1% in the second quarter and were essentially unchanged for the six-month period. We expect the Recoveries revenue decline in the second quarter to increase over the second half of the year. |

SECOND QUARTER 2015 REVENUES BY TYPE | |

|

|

EBITDA, segment operating profit and the related margins increased in both periods as higher revenues and savings from efficiency initiatives offset expenses associated with dual running costs, the timing of annual salary increases, as well as the unfavorable impact of foreign currency. The annual salary increase occurred in the second quarter of this year compared to the third quarter of last year. The prior-year periods also included the impact of charges, primarily severance, associated with the efficiency initiatives. Excluding the impacts of currency and prior-year severance charges, EBITDA and segment operating profit increased 5% and 8%, respectively, in the second quarter and 7% and 11%, respectively, in the six-month period. We previously stated that we have targeted an EBITDA margin nearing 30% by the end of 2015 for our Financial & Risk business. As an indication of how we are progressing toward this target, the segment’s EBITDA margin in the second quarter was 28.7%, excluding the impact of foreign currency.

Page 11

Legal

| THREE MONTHS ENDED JUNE 30, | PERCENTAGE CHANGE: | |||||||||||||||||||||||||||||

| (millions of U.S. dollars, except margins) | 2015 | 2014 |

|

Existing businesses |

|

|

Acquired businesses |

|

|

Constant currency |

|

|

Foreign currency |

|

Total | |||||||||||||||

| Revenues |

840 | 850 | 2% | - | 2% | (3%) | (1%) | |||||||||||||||||||||||

| EBITDA |

314 | 331 | (5%) | |||||||||||||||||||||||||||

| EBITDA margin |

37.4% | 38.9% | (150)bp | |||||||||||||||||||||||||||

| Segment operating profit |

251 | 261 | (4%) | |||||||||||||||||||||||||||

| Segment operating profit margin |

29.9% | 30.7% | (80)bp | |||||||||||||||||||||||||||

| SIX MONTHS ENDED JUNE 30, | PERCENTAGE CHANGE: | |||||||||||||||||||||||||||||

| (millions of U.S. dollars, except margins) | 2015 | 2014 |

|

Existing businesses |

|

|

Acquired businesses |

|

|

Constant currency |

|

|

Foreign currency |

|

Total | |||||||||||||||

| Revenues |

1,650 | 1,653 | 2% | - | 2% | (2%) | - | |||||||||||||||||||||||

| EBITDA |

593 | 615 | (4%) | |||||||||||||||||||||||||||

| EBITDA margin |

35.9% | 37.2% | (130)bp | |||||||||||||||||||||||||||

| Segment operating profit |

464 | 476 | (3%) | |||||||||||||||||||||||||||

| Segment operating profit margin |

28.1% | 28.8% | (70)bp | |||||||||||||||||||||||||||

Revenues on a constant currency basis increased during the second quarter, all from existing businesses. Subscription revenues, which represented 71% of Legal’s business, increased 2%. Transaction revenues (13% of Legal’s business) increased 10% driven by its legal enterprise solutions business including Elite and Serengeti, Pangea3 legal managed services, and our Latin America businesses. Legal’s U.S. print revenues (16% of Legal’s business) decreased 5%. Excluding U.S. print, Legal’s revenues increased 3%.

In the six-month period, revenues increased on a constant currency (substantially all from existing businesses). Subscription revenues increased 2%, transaction revenues increased 13% (12% from existing businesses) and U.S. print declined 6%. Excluding U.S. print, Legal’s revenues increased 4%. We expect Legal’s full-year 2015 revenue growth rate to be comparable to its revenue growth rate for the first half of the year.

Results by line of business were:

|

• Solutions business revenues include non-U.S. legal information and global software and services businesses. Our Solutions business revenues increased 5% and 7% in the second quarter and six-month period, respectively, with substantially all revenue growth coming from existing businesses. Revenue growth in both periods was driven by higher transactional revenues and growth in U.K. Practical Law and our Investigations and Public Records business;

• U.S. online legal information revenues increased slightly in both periods, all from existing businesses, due to growth in U.S. Practical Law and an improved revenue performance by Westlaw. This was the second consecutive quarter of revenue growth for this business; and

• U.S. print revenues decreased 5% and 6%, all from existing businesses in the second quarter and six-month period, respectively. |

SECOND QUARTER 2015 REVENUES BY LINE OF BUSINESS | |

|

EBITDA, segment operating profit and the related margins decreased in the second quarter and six-month period due to the timing of expenses, particularly the timing of our annual salary increase, which occurred in the second quarter of this year compared to the third quarter of last year. Segment operating profit and the related margin benefited from lower depreciation and amortization expense. Foreign exchange benefited EBITDA and segment operating profit margin by 60bp and 50bp in the second quarter, respectively, and by 50bp and 40bp in the six-month period, respectively, compared to the prior-year periods.

We continue to expect that Legal’s full-year EBITDA margin will be comparable to 2014.

Page 12

Tax & Accounting

| THREE MONTHS ENDED JUNE 30, | PERCENTAGE CHANGE: | |||||||||||||||||||||||||||||

| (millions of U.S. dollars, except margins) | 2015 | 2014 |

|

Existing businesses |

|

|

Acquired businesses |

|

|

Constant currency |

|

|

Foreign currency |

|

Total | |||||||||||||||

| Revenues |

327 | 324 | 5% | 1% | 6% | (5%) | 1% | |||||||||||||||||||||||

| EBITDA |

90 | 98 | (8%) | |||||||||||||||||||||||||||

| EBITDA margin |

27.5% | 30.2% | (270)bp | |||||||||||||||||||||||||||

| Segment operating profit |

63 | 65 | (3%) | |||||||||||||||||||||||||||

| Segment operating profit margin |

19.3% | 20.1% | (80)bp | |||||||||||||||||||||||||||

| SIX MONTHS ENDED JUNE 30, | PERCENTAGE CHANGE: | |||||||||||||||||||||||||||||

| (millions of U.S. dollars, except margins) | 2015 | 2014 |

|

Existing businesses |

|

|

Acquired businesses |

|

|

Constant currency |

|

|

Foreign currency |

|

Total | |||||||||||||||

| Revenues |

700 | 672 | 6% | 2% | 8% | (4%) | 4% | |||||||||||||||||||||||

| EBITDA |

216 | 213 | 1% | |||||||||||||||||||||||||||

| EBITDA margin |

30.9% | 31.7% | (80)bp | |||||||||||||||||||||||||||

| Segment operating profit |

161 | 149 | 8% | |||||||||||||||||||||||||||

| Segment operating profit margin |

23.0% | 22.2% | 80bp | |||||||||||||||||||||||||||

In both periods, revenues increased on a constant currency basis reflecting contributions from both existing and acquired businesses. Recurring revenues, which comprised approximately 80% of our Tax & Accounting business, increased 7% (primarily from existing businesses) in the second quarter and 9% (7% from existing businesses) in the six-month period. Transaction revenues decreased 1%, all from existing businesses, in the second quarter, but increased 3% (2% from existing businesses) in the six-month period.

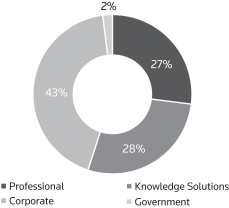

Results by line of business were:

|

• Professional revenues from accounting firms increased 10% and 11%, all from existing businesses, in the second quarter and six-month period, respectively, primarily from our CS Professional Suite and Enterprise Suite solutions for accounting firms;

• Knowledge Solutions revenues increased 3% and 1%, all from existing businesses, in the second quarter and for the six-month period, respectively;

• Corporate revenues increased 11%, primarily from existing businesses, in the second quarter and 14% (10% from existing businesses) for the six-month period, primarily from ONESOURCE software and services and strong growth in solutions revenues in Latin America; and

• Government revenues, which represent a relatively small revenue base, decreased significantly in the second quarter and six-month period due to timing of revenues associated with certain contracts. Revenues for the Government business are less predictable in nature, and growth rates could vary significantly from quarter to quarter. |

SECOND QUARTER 2015 REVENUES BY LINE OF BUSINESS | |

|

|

In the second quarter, EBITDA and the related margin decreased. The decrease reflected the decline in Government business revenues, investments in growth businesses, and timing of expenses including our annual salary increase which occurred in the second quarter of this year compared to the third quarter of last year. These decreases were partly offset by higher revenues in the Professional, Corporate and Knowledge Solutions businesses. The decline in segment operating profit and the related margin was mitigated by lower depreciation and amortization expense. Foreign exchange benefited EBITDA and segment operating profit margins by 100bp and 110bp, respectively, compared to the prior-year period. In the six-month period, EBITDA, segment operating profit and segment operating profit margin all increased while EBITDA margin declined slightly. The stronger performance in the six-month period (compared to the second quarter) was due to the benefit of higher revenue growth from the first quarter. Foreign exchange benefited both EBITDA and segment operating profit margins by 80bp, compared to the prior-year period.

Page 13

Tax & Accounting is a seasonal business with a significant percentage of its operating profit historically generated in the fourth quarter. Small movements in the timing of revenues and expenses can impact quarterly margins. Full-year margins are more reflective of the segment’s performance.

Intellectual Property & Science

| THREE MONTHS ENDED JUNE 30, | PERCENTAGE CHANGE: | |||||||||||||||||||||||||||||

| (millions of U.S. dollars, except margins) | 2015 | 2014 |

|

Existing businesses |

|

|

Acquired businesses |

|

|

Constant currency |

|

|

Foreign currency |

|

Total | |||||||||||||||

| Revenues |

248 | 251 | 1% | - | 1% | (2%) | (1%) | |||||||||||||||||||||||

| EBITDA |

81 | 85 | (5%) | |||||||||||||||||||||||||||

| EBITDA margin |

32.7% | 33.9% | (120)bp | |||||||||||||||||||||||||||

| Segment operating profit |

58 | 62 | (6%) | |||||||||||||||||||||||||||

| Segment operating profit margin |

23.4% | 24.7% | (130)bp | |||||||||||||||||||||||||||

| SIX MONTHS ENDED JUNE 30, |

|

PERCENTAGE CHANGE: |

| |||||||||||||||||||||||||||

| (millions of U.S. dollars, except margins) | 2015 | 2014 |

|

Existing businesses |

|

|

Acquired businesses |

|

|

Constant currency |

|

|

Foreign currency |

|

Total | |||||||||||||||

| Revenues |

485 | 494 | 1% | - | 1% | (3%) | (2%) | |||||||||||||||||||||||

| EBITDA |

141 | 157 | (10%) | |||||||||||||||||||||||||||

| EBITDA margin |

29.1% | 31.8% | (270)bp | |||||||||||||||||||||||||||

| Segment operating profit |

96 | 113 | (15%) | |||||||||||||||||||||||||||

| Segment operating profit margin |

19.8% | 22.9% | (310)bp | |||||||||||||||||||||||||||

In both periods, revenues increased on a constant currency basis, all from existing businesses, as growth in recurring revenues was partly offset by a decline in transactional revenues.

Results by type were:

|

• Recurring revenues increased 4% in the second quarter and in the six-month period as growth from our MarkMonitor online brand protection solution and Web of Science subscriptions was partly offset by softness in Asset Management revenues; and

• Transactional revenues decreased 8% in the second quarter and decreased 9% in the six-month period due to lower sales within the Government and Academia business. |

SECOND QUARTER 2015 REVENUES BY TYPE | |

|

|

EBITDA, segment operating profit and the related margins decreased in both periods due to timing of expenses, including our annual salary increase which occurred in the second quarter of this year compared to the third quarter of last year, as well as a lower margin revenue mix compared to the prior-year periods. Foreign exchange benefited EBITDA and segment operating profit margin by 80bp and 100bp in the second quarter, respectively, and by 70bp and 90bp in the six-month period, respectively, compared to the prior-year periods.

Quarterly revenue growth for Intellectual Property & Science can be uneven due to the impact of large sales in the Government and Academia business. Small movements in the timing of revenues and expenses can impact quarterly margins. Full-year revenues and margins are more reflective of the segment’s performance.

Page 14

Corporate & Other

| THREE MONTHS ENDED JUNE 30, |

SIX MONTHS ENDED JUNE 30, |

|||||||||||||||||

| (millions of U.S. dollars) | 2015 | 2014 | 2015 | 2014 | ||||||||||||||

| Revenues – Reuters News |

74 | 82 | 148 | 161 | ||||||||||||||

| Reuters News |

(2) | 4 | (5) | 4 | ||||||||||||||

| Core corporate expenses |

(68) | (77) | (140) | (139) | ||||||||||||||

| Total |

(70) | (73) | (145) | (135) | ||||||||||||||

In both periods, revenues from our Reuters News business declined due to unfavorable foreign currency.

Core corporate expenses were lower in the second quarter due to timing and were largely unchanged in the six-month period.

LIQUIDITY AND CAPITAL RESOURCES

Our capital strategy is aligned with our business strategy to drive revenue growth from existing businesses, achieve savings from our efficiency initiatives, and to reinvest in our growth businesses.

Our disciplined capital management strategy remains focused on:

| • | Growing free cash flow and balancing cash generated between reinvestment in the business and returns to shareholders; and |

| • | Maintaining a strong balance sheet, solid credit ratings and ample financial flexibility to support the execution of our business strategy. |

Our principal sources of liquidity are cash on hand, cash provided by our operations, our $2.0 billion commercial paper programs and our $2.5 billion credit facility. From time to time, we also issue debt securities. Our principal uses of cash are for debt repayments, debt servicing costs, dividend payments, capital expenditures, share repurchases and acquisitions. We believe that our existing sources of liquidity will be sufficient to fund our expected cash requirements in the normal course of business for the next 12 months.

Cash flow

Summary of consolidated statement of cash flow

| THREE MONTHS ENDED JUNE 30, |

SIX MONTHS ENDED JUNE 30, |

|||||||||||||||||||||||||

| (millions of U.S. dollars) | 2015 | 2014 | $ CHANGE | 2015 | 2014 | $ CHANGE | ||||||||||||||||||||

| Net cash provided by operating activities |

931 | 876 | 55 | 1,168 | 989 | 179 | ||||||||||||||||||||

| Net cash used in investing activities |

(154) | (349) | 195 | (463) | (596) | 133 | ||||||||||||||||||||

| Net cash used in financing activities |

(421) | (486) | 65 | (587) | (1,009) | 422 | ||||||||||||||||||||

| Increase (decrease) in cash and bank overdrafts |

356 | 41 | 315 | 118 | (616) | 734 | ||||||||||||||||||||

| Translation adjustments |

3 | 3 | - | (9) | 3 | (12) | ||||||||||||||||||||

| Cash and bank overdrafts at beginning of period |

765 | 655 | 110 | 1,015 | 1,312 | (297) | ||||||||||||||||||||

| Cash and bank overdrafts at end of period |

1,124 | 699 | 425 | 1,124 | 699 | 425 | ||||||||||||||||||||

| Cash and bank overdrafts at end of period comprised of: |

||||||||||||||||||||||||||

| Cash and cash equivalents |

1,127 | 704 | 423 | 1,127 | 704 | 423 | ||||||||||||||||||||

| Bank overdrafts |

(3) | (5) | 2 | (3) | (5) | 2 | ||||||||||||||||||||

Operating activities. The increase in net cash provided by operating activities in the second quarter and six-month period was primarily due to lower severance payments associated with our earlier efficiency initiatives and favorable movements in working capital, partly offset by higher tax payments.

Investing activities. The decrease in net cash used in investing activities in the second quarter and six-month period was primarily due to 2015 proceeds from the sale of our Lipper Services business and reduced acquisition spending. In 2014, our acquisition spending included Dominio Sistemas, a Brazilian provider of accounting and software solutions to accounting firms. In the six-month period, the decreases in net cash used in investing activities were partly offset by higher capital expenditures.

Page 15

Financing activities. The decrease in net cash used in financing activities for the second quarter and six-month period was primarily attributable to 2015 commercial paper borrowings, partly offset by a 2014 contribution from the non-controlling interests of Tradeweb of $115 million in exchange for additional shares. This contribution is reflected within “Other financing activities” in the consolidated statement of cash flow. We returned $0.6 billion (2014 – $0.6 billion) and $1.2 billion (2014 – $1.1 billion) to our shareholders through dividends and share repurchases in the second quarter and six-month period, respectively. Additional information about our debt, dividends and share repurchases is as follows:

| • | Commercial paper programs. Our $2.0 billion commercial paper programs provide cost-effective and flexible short-term funding to balance the timing of dividend payments, debt repayments, share repurchases, and completed acquisitions. Issuances of commercial paper reached a peak of $0.6 billion during the six-month period of 2015, all of which remained outstanding at June 30, 2015. |

| • | Credit facility. We have a $2.5 billion syndicated credit facility agreement which matures in May 2018. The facility may be utilized to provide liquidity for general corporate purposes (including support for our commercial paper programs). There were no borrowings under the credit facility during the six-month period of 2015. |

We may request an increase, subject to approval by applicable lenders, in the lenders’ commitments up to a maximum amount of $3.0 billion.

Based on our current credit ratings, the cost of borrowing under the agreement is priced at LIBOR/EURIBOR plus 100 basis points. If our long-term debt rating were downgraded by Moody’s or Standard & Poor’s, our facility fee and borrowing costs may increase, although availability would be unaffected. Conversely, an upgrade in our ratings may reduce our facility fee and borrowing costs. We monitor the lenders that are party to our facility and believe they continue to be able to lend to us.

We guarantee borrowings by our subsidiaries under the credit facility. We must also maintain a ratio of net debt as of the last day of each fiscal quarter to EBITDA as defined in the credit agreement (earnings before interest, income taxes, depreciation and amortization and other modifications described in the credit agreement) for the last four quarters ended of not more than 4.5:1. We were in compliance with this covenant at June 30, 2015.

| • | Debt shelf prospectus. We have a debt shelf prospectus under which we may issue up to $3.0 billion principal amount of debt securities from time to time through April 2016. As of June 30, 2015, we have issued $1.5 billion principal amount of debt securities under the prospectus. |

| • | Credit ratings. Our access to financing depends on, among other things, suitable market conditions and the maintenance of suitable long-term credit ratings. Our credit ratings may be adversely affected by various factors, including increased debt levels, decreased earnings, declines in customer demand, increased competition, a further deterioration in general economic and business conditions and adverse publicity. Any downgrades in our credit ratings may impede our access to the debt markets or result in significantly higher borrowing rates. |

The following table sets forth the credit ratings that we have received from rating agencies in respect of our outstanding securities as of the date of this management’s discussion and analysis:

| MOODY’S | STANDARD & POOR’S | DBRS LIMITED | FITCH | |||||

| Long-term debt |

Baa2 | BBB+ | BBB (high) | BBB+ | ||||

| Commercial paper |

P-2 | A-2 | R-2 (high) | F2 | ||||

| Trend/Outlook |

Stable | Stable | Stable | Stable | ||||

These credit ratings are not recommendations to purchase, hold, or sell securities and do not address the market price or suitability of a specific security for a particular investor. Credit ratings may not reflect the potential impact of all risks on the value of securities. We cannot assure you that our credit ratings will not be lowered in the future or that rating agencies will not issue adverse commentaries regarding our securities.

| • | Dividends. In February 2015, we announced a $0.02 per share increase in the annualized dividend rate to $1.34 per common share. Dividends paid on our common shares were as follows for the periods presented: |

| THREE MONTHS ENDED JUNE 30, |

SIX MONTHS ENDED JUNE 30, |

|||||||||||||||||

| (millions of U.S. dollars) | 2015 | 2014 | 2015 | 2014 | ||||||||||||||

| Dividends declared |

262 | 266 | 528 | 536 | ||||||||||||||

| Dividends reinvested |

(8) | (8) | (16) | (16) | ||||||||||||||

| Dividends paid |

254 | 258 | 512 | 520 | ||||||||||||||

Page 16

| • | Share repurchases. We may buy back shares (and subsequently cancel them) from time to time as part of our capital strategy. In July 2014, we announced a plan to repurchase up to $1.0 billion of our common shares by the end of 2015. We completed these repurchases in the second quarter of 2015. |

In May 2015, we renewed our current normal course issuer bid (NCIB) for an additional 12 months and we announced a new plan to repurchase up to an additional $1.0 billion of our common shares by the end of 2016. Under the renewed NCIB, we may repurchase up to 30 million common shares between May 28, 2015 and May 27, 2016 in open market transactions on the Toronto Stock Exchange (TSX), the New York Stock Exchange (NYSE) and/or other exchanges and alternative trading systems, if eligible, or by such other means as may be permitted by the TSX and/or NYSE or under applicable law, including private agreement purchases if we receive an issuer bid exemption order in the future from applicable securities regulatory authorities in Canada for such purchases.

Details of share repurchases were as follows:

| THREE MONTHS ENDED JUNE 30, |

SIX MONTHS ENDED JUNE 30, |

|||||||||||||||||

| 2015 | 2014 | 2015 | 2014 | |||||||||||||||

| Share repurchases (millions of U.S. dollars) |

348 | 353 | 696 | 617 | ||||||||||||||

| Shares repurchased (millions) |

8.5 | 10.1 | 17.3 | 17.6 | ||||||||||||||

| Share repurchases – average price per share |

$40.67 | $35.17 | $40.20 | $35.16 | ||||||||||||||

Decisions regarding any future repurchases will be based on market conditions, share price and other factors including opportunities to invest capital for growth. We may elect to suspend or discontinue our share repurchases at any time, in accordance with applicable laws. From time to time when we do not possess material nonpublic information about ourselves or our securities, we may enter into a pre-defined plan with our broker to allow for the repurchase of shares at times when we ordinarily would not be active in the market due to our own internal trading blackout periods, insider trading rules or otherwise. Any such plans entered into with our broker will be adopted in accordance with applicable Canadian securities laws and the requirements of Rule 10b5-1 under the U.S. Securities Exchange Act of 1934, as amended. We entered into such plans with our broker on June 30, 2015 and on December 31, 2014. As a result, we recorded a $65 million liability in “Other financial liabilities” within current liabilities at June 30, 2015 ($115 million at December 31, 2014) with a corresponding amount recorded in equity in the consolidated statement of financial position in both periods. The liability recorded on December 31, 2014 was settled in the first quarter of 2015.

Free cash flow

| THREE MONTHS ENDED JUNE 30, |

SIX MONTHS ENDED JUNE 30, |

|||||||||||||||||

| (millions of U.S. dollars) | 2015 | 2014 | 2015 | 2014 | ||||||||||||||

| Net cash provided by operating activities |

931 | 876 | 1,168 | 989 | ||||||||||||||

| Capital expenditures, less proceeds from disposals |

(223) | (225) | (526) | (473) | ||||||||||||||

| Other investing activities |

1 | 1 | 3 | 2 | ||||||||||||||

| Dividends paid on preference shares |

- | - | (1) | (1) | ||||||||||||||

| Free cash flow |

709 | 652 | 644 | 517 | ||||||||||||||

| Remove: Other Businesses |

- | 1 | - | 1 | ||||||||||||||

| Free cash flow from ongoing businesses |

709 | 653 | 644 | 518 | ||||||||||||||

Free cash flow and free cash flow from ongoing businesses increased in the second quarter and six-month period primarily due to higher cash from operating activities. The six-month period also reflected higher capital expenditures.

Financial position

Our total assets were $30.0 billion at June 30, 2015, a decrease of $0.6 billion compared to December 31, 2014. The decrease was primarily due to changes in foreign currency, depreciation of fixed assets, and amortization of computer software and other identifiable intangible assets. These decreases were partially offset by capital expenditures.

Page 17

As of June 30, 2015, the carrying amounts of our total current liabilities exceeded the carrying amounts of our total current assets primarily because current liabilities include deferred revenue, which arises from the sale of information and services delivered electronically on a subscription basis, for which many customers pay in advance. The cash received from these advance payments is used to currently fund the operating, investing and financing activities of our business. However, for accounting purposes, these advance payments must be deferred and recognized over the term of the subscription. As such, we typically reflect a negative working capital position in our balance sheet. In the ordinary course of business, deferred revenue does not represent a cash obligation, but rather an obligation to perform services or deliver products. Therefore, we believe that our negative working capital position as at June 30, 2015, was not indicative of a liquidity issue, but rather an outcome of the required accounting for our business model.

Additionally, as of June 30, 2015, our current liabilities increased due to the reclassification of $500 million principal amount of 0.875% notes due in May 2016 from long-term indebtedness to current indebtedness. As previously stated in this “Liquidity and Capital Resources” section, we believe our existing sources of liquidity will be sufficient to fund our expected cash requirements in the normal course of business for the next 12 months. Additionally, in July 2015, we repaid our C$600 million principal amount of 5.70% notes for $593 million (after swaps).

Net debt(1)

| June 30, | December 31, | |||||||

| (millions of U.S. dollars) | 2015 | 2014 | ||||||

| Current indebtedness |

1,564 | 534 | ||||||

| Long-term indebtedness |

6,971 | 7,576 | ||||||

| Total debt |

8,535 | 8,110 | ||||||

| Swaps |

335 | 207 | ||||||

| Total debt after swaps |

8,870 | 8,317 | ||||||

| Remove fair value adjustments for hedges(2) |

27 | 6 | ||||||

| Total debt after currency hedging arrangements |

8,897 | 8,323 | ||||||

| Remove transaction costs and discounts included in the carrying value of debt |

73 | 78 | ||||||

| Less: cash and cash equivalents(3) |

(1,127) | (1,018) | ||||||

| Net debt |

7,843 | 7,383 | ||||||

| (1) | Net debt is a non-IFRS financial measure, which we define in Appendix A. |

| (2) | Represents the interest-related fair value component of hedging instruments that are removed to reflect net cash outflow upon maturity. |

| (3) | Includes cash and cash equivalents of $100 million and $105 million at June 30, 2015 and December 31, 2014, respectively, held in subsidiaries, which have regulatory restrictions, contractual restrictions or operate in countries where exchange controls and other legal restrictions apply and are therefore not available for general use by our company. |

The maturity dates for our debt are well balanced with no significant concentration in any one year. Our next scheduled debt maturities occur in July 2015 (repaid on maturity—see “Subsequent Events”) and in May 2016. At June 30, 2015, the average maturity of our term debt was approximately eight years at an average interest rate (after swaps) of less than 5%.

Additional information

| • | We monitor the financial strength of financial institutions with which we have banking and other commercial relationships, including those that hold our cash and cash equivalents as well as those which are counterparties to derivative financial instruments and other arrangements; and |

| • | We expect to continue to have access to funds held by our subsidiaries outside the U.S. in a tax efficient manner to meet our liquidity requirements. |

Off-balance sheet arrangements, commitments and contractual obligations

For a summary of our other off-balance sheet arrangements, commitments and contractual obligations please see our 2014 annual management’s discussion and analysis. There were no material changes to these arrangements, commitments and contractual obligations during the six months ended June 30, 2015.

Page 18

Contingencies

Lawsuits and legal claims

We are engaged in various legal proceedings, claims, audits and investigations that have arisen in the ordinary course of business. These matters include, but are not limited to, intellectual property infringement claims, employment matters and commercial matters. The outcome of all of the matters against us is subject to future resolution, including the uncertainties of litigation. Based on information currently known to us and after consultation with outside legal counsel, management believes that the ultimate resolution of any such matters, individually or in the aggregate, will not have a material adverse impact on our financial condition taken as a whole.

Uncertain tax positions

We are subject to taxation in numerous jurisdictions and we are routinely under audit by many different taxing authorities in the ordinary course of business. There are many transactions and calculations during the course of business for which the ultimate tax determination is uncertain, as taxing authorities may challenge some of our positions and propose adjustments or changes to our tax filings. As a result, we maintain provisions for uncertain tax positions that we believe appropriately reflect our risk. These provisions are made using our best estimate of the amount expected to be paid based on a qualitative assessment of all relevant factors. We review the adequacy of these provisions at the end of each reporting period and adjust them based on changing facts and circumstances. Due to the uncertainty associated with tax audits, it is possible that at some future date, liabilities resulting from such audits or related litigation could vary significantly from our provisions. However, based on currently enacted legislation, information currently known to us and after consultation with outside tax advisors, management believes that the ultimate resolution of any such matters, individually or in the aggregate, will not have a material adverse impact on our financial condition taken as a whole.