UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 20-F

|

o |

REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934 |

|

|

|

|

OR | |

|

|

|

|

x |

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15 (d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

|

|

|

|

OR | |

|

|

|

|

o |

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15 (d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

|

|

|

|

OR | |

|

|

|

|

o |

SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15 (d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Commission file number 1-14878

|

GERDAU S.A. |

|

(Exact name of Registrant as specified in its charter) |

|

|

|

N/A |

|

(Translation of Registrant’s name into English) |

|

|

|

Federative Republic of Brazil |

|

(Jurisdiction of incorporation or organization) |

|

|

|

Av. Farrapos 1811 Porto Alegre, Rio Grande do Sul - Brazil CEP 90220-005 |

|

(Address of principal executive offices) (Zip code) |

Securities registered pursuant to Section 12(b) of the Act:

|

Title of each class |

|

Name of each exchange in which registered |

|

Preferred Shares, no par value per share, each represented by American Depositary Shares |

|

New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act: None

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act: None

The total number of issued shares of each class of stock of GERDAU S.A. as of December 31, 2012 was:

|

|

573,627,483 Common Shares, no par value per share |

|

|

1,146,031,245 Preferred Shares, no par value per share |

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

x Yes o No

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934.

o Yes x No

Note — Checking the box above will not relieve any registrant required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 from their obligations under those Sections.

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

x Yes o No

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

o Yes x No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See definition of “accelerated filer and large accelerated filer” in Rule 12b-2 of the Exchange Act. (Check one):

|

Large accelerated filer x |

|

Accelerated filer o |

|

Non-accelerated filer o |

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

|

U.S. GAAP o |

|

International Financial Reporting Standards as issued |

|

Other o |

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow.

o Item 17 o Item 18

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

o Yes x No

|

|

|

Page |

|

|

|

|

|

|

3 | |

|

|

|

|

|

|

4 | |

|

|

|

|

|

4 | ||

|

4 | ||

|

5 | ||

|

14 | ||

|

46 | ||

|

46 | ||

|

77 | ||

|

87 | ||

|

91 | ||

|

96 | ||

|

102 | ||

|

QUANTITATIVE AND QUALITATIVE DISCLOSURES REGARDING MARKET RISK |

116 | |

|

118 | ||

|

|

|

|

|

|

118 | |

|

|

|

|

|

118 | ||

|

MATERIAL MODIFICATIONS TO THE RIGHTS OF SECURITY HOLDERS AND USE OF PROCEEDS |

119 | |

|

119 | ||

|

120 | ||

|

120 | ||

|

120 | ||

|

120 | ||

|

121 | ||

|

PURCHASES OF EQUITY SECURITIES BY THE ISSUER AND AFFILIATED PURCHASERS |

121 | |

|

122 | ||

|

122 | ||

|

123 | ||

|

|

|

|

|

|

123 | |

|

|

|

|

|

123 | ||

|

123 | ||

|

124 |

Unless otherwise indicated, all references herein to:

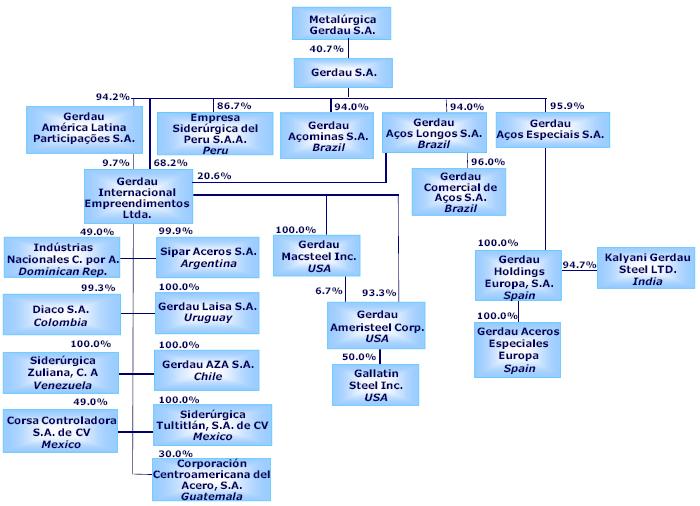

(i) the “Company”, “Gerdau”, “we” or “us” are references to Gerdau S.A., a corporation organized under the laws of the Federative Republic of Brazil (“Brazil”) and its consolidated subsidiaries;

(ii) “Açominas” is a reference to Aço Minas Gerais S.A. — Açominas prior to November 2003 whose business was to operate the Ouro Branco steel mill. In November 2003 the company underwent a corporate reorganization, receiving all of Gerdau’s Brazilian operating assets and liabilities and being renamed Gerdau Açominas S.A.;

(iii) “Gerdau Açominas” is a reference to Gerdau Açominas S.A. after November 2003 and to Açominas before such date. In July 2005, certain assets and liabilities of Gerdau Açominas were spun-off to four other newly created entities: Gerdau Aços Longos, Gerdau Aços Especiais, Gerdau Comercial de Aços and Gerdau América do Sul Participações. As a result of such spin-off, as from July 2005, the activities of Gerdau Açominas only comprise the operation of the Açominas steel mill;

(iv) “Chaparral Steel” or to “Chaparral” are references to Chaparral Steel Company, a corporation organized under the laws of the State of Delaware, and its consolidated subsidiaries;

(v) “Preferred Shares” and “Common Shares” refer to the Company’s authorized and outstanding preferred stock and common stock, designated as ações preferenciais and ações ordinárias, respectively, all without par value. All references herein to the “real”, “reais” or “R$” are to the Brazilian real, the official currency of Brazil. All references to (i) “U.S. dollars”, “dollars”, “U.S.$” or “$” are to the official currency of the United States, (ii) “Canadian dollars” or “Cdn$” are to the official currency of Canada, (iii) “Euro” or “€” are to the official currency of members of the European Union, (iv) “billions” are to thousands of millions, (v) “km” are to kilometers, and (vi) “tonnes” are to metric tonnes;

(vi) “Installed capacity” means the annual projected capacity for a particular facility (excluding the portion that is not attributable to our participation in a facility owned by a jointly-controlled entity), calculated based upon operations for 24 hours each day of a year and deducting scheduled downtime for regular maintenance;

(vii) “Tonne” means a metric tonne, which is equal to 1,000 kilograms or 2,204.62 pounds;

(viii) “Consolidated shipments” means the combined volumes shipped from all our operations in Brazil, Latin America, North America and Europe, excluding our jointly-controlled entities and associate companies;

(ix) “worldsteel” means World Steel Association, “IABr” means Brazilian Steel Institute (Instituto Aço Brasil) and “AISI” means American Iron and Steel Institute;

(x) “CPI” means consumer price index, “CDI” means Interbanking Deposit Rates (Certificados de Depósito Interfinanceiro), “IGP-M” means Consumer Prices Index (Índice Geral de Preços do Mercado), measured by FGV (Fundação Getulio Vargas), “LIBOR” means London Interbank Offered Rate, “GDP” means Gross Domestic Product;

(xi) “Brazil BO” means Brazil Business Operation, “North America BO” means North America Business Operation, “Latin America BO” means Latin America Business Operation, “Specialty Steel BO” means Specialty Steel Business Operation.

The Company has prepared the consolidated financial statements included herein in accordance with International Financial Reporting Standards (IFRS) as issued by the International Accounting Standards Board (IASB). The following investments are accounted for following the equity method: in Gallatin Steel Co. (“Gallatin”), Bradley Steel Processor and MRM Guide Rail, all in North America, of which Gerdau Ameristeel holds 50% of the total capital, through the date of obtention of control in July 2012 the investment in Kalyani Gerdau Steel Ltd, the investment in Armacero Industrial y Comercial Limitada, in Chile, in which the Company holds a 50% stake, the investment in the holding company Multisteel Business Holdings Corp., in which the Company holds a 49% stake, which in turn holds 99.13% of the capital stock of Industrias Nacionales, C. por A. (INCA), in the Dominican Republic, the investment in the holding company Corsa Controladora, S.A. de C.V., in which the Company holds a 49% stake, which in turn holds the capital stock of Aceros Corsa S.A. de C.V., in Mexico, the investment in the holding company Corporacion Centroamericana del Acero S.A., in which the Company holds a 30% stake, which in turn holds the capital stock of Aceros de Guatemala S.A., in Guatemala, the investment in Gerdau Corsa S.A.P.I. de C.V., in Mexico, in which the Company holds a 50% stake and the investment in Dona Francisca Energética S.A, in Brazil, in which the Company holds a 51.82% stake.

Unless otherwise indicated, all information in this Annual Report is stated as of December 31, 2012. Subsequent developments are discussed in Item 8.B - Financial Information - Significant Changes.

CAUTIONARY STATEMENT WITH RESPECT TO FORWARD-LOOKING STATEMENTS

This Annual Report contains forward-looking statements within the meaning of the Private Securities Litigation Act of 1995. These statements relate to our future prospects, developments and business strategies.

Statements that are predictive in nature, that depend upon or refer to future events or conditions or that include words such as “expects,” “anticipates,” “intends,” “plans,” “believes,” “estimates” and similar expressions are forward-looking statements. Although we believe that these forward-looking statements are based upon reasonable assumptions, these statements are subject to several risks and uncertainties and are made in light of information currently available to us.

It is possible that our future performance may differ materially from our current assessments due to a number of factors, including the following:

· general economic, political and business conditions in our markets, both in Brazil and abroad, including demand and prices for steel products;

· interest rate fluctuations, inflation and exchange rate movements of the real in relation to the U.S. dollar and other currencies in which we sell a significant portion of our products or in which our assets and liabilities are denominated;

· our ability to obtain financing on satisfactory terms;

· prices and availability of raw materials;

· changes in international trade;

· changes in laws and regulations;

· electric energy shortages and government responses to them;

· the performance of the Brazilian and the global steel industries and markets;

· global, national and regional competition in the steel market;

· protectionist measures imposed by steel-importing countries; and

· other factors identified or discussed under “Risk Factors.”

Our forward-looking statements are not guarantees of future performance, and actual results or developments may differ materially from the expectations expressed in the forward-looking statements. As for the forward-looking statements that relate to future financial results and other projections, actual results will be different due to the inherent uncertainty of estimates, forecasts and projections. Because of these uncertainties, potential investors should not rely on these forward-looking statements.

We undertake no obligation to publicly update any forward-looking statement, whether as a result of new information, future events or otherwise.

ITEM 1. IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS

Not applicable, as the Company is filing this Form 20-F as an annual report.

ITEM 2. OFFER STATISTICS AND EXPECTED TIMETABLE

Not applicable, as the Company is filing this Form 20-F as an annual report.

A. SELECTED FINANCIAL DATA

The selected financial information for the Company included in the following tables should be read in conjunction with, and is qualified in its entirety by, the IFRS financial statements of the Company and “Operating and Financial Review and Prospects” appearing elsewhere in this Annual Report. The consolidated financial data of the Company as of and for each of the years ended on December 31, 2012, 2011, 2010, 2009 and 2008 are derived from the financial statements prepared in accordance with IFRS and presented in Brazilian Reais.

IFRS Summary Financial and Operating Data

|

|

|

(Expressed in thousands of Brazilian Reais - R$ except quantity of shares and amounts per share) |

| ||||||||

|

|

|

2012 |

|

2011 |

|

2010 |

|

2009 |

|

2008 |

|

|

NET SALES |

|

37,981,668 |

|

35,406,780 |

|

31,393,209 |

|

26,540,050 |

|

41,907,845 |

|

|

Cost of sales |

|

(33,234,102 |

) |

(30,298,232 |

) |

(25,873,476 |

) |

(22,305,550 |

) |

(31,228,035 |

) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

GROSS PROFIT |

|

4,747,566 |

|

5,108,548 |

|

5,519,733 |

|

4,234,500 |

|

10,679,810 |

|

|

Selling expenses |

|

(587,369 |

) |

(603,747 |

) |

(551,547 |

) |

(429,612 |

) |

(479,551 |

) |

|

General and administrative expenses |

|

(1,884,306 |

) |

(1,797,937 |

) |

(1,805,914 |

) |

(1,714,494 |

) |

(2,284,857 |

) |

|

Reversal of impairment (impairment) of assets |

|

— |

|

— |

|

336,346 |

|

(1,072,190 |

) |

— |

|

|

Restructuring costs |

|

— |

|

— |

|

— |

|

(150,707 |

) |

— |

|

|

Other operating income |

|

244,414 |

|

195,015 |

|

207,320 |

|

190,157 |

|

205,676 |

|

|

Other operating expenses |

|

(180,453 |

) |

(85,533 |

) |

(100,840 |

) |

(101,810 |

) |

(116,064 |

) |

|

Equity in earnings (losses) of unconsolidated companies, net |

|

8,353 |

|

62,662 |

|

39,454 |

|

(108,957 |

) |

122,808 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

INCOME BEFORE FINANCIAL INCOME (EXPENSES) AND TAXES |

|

2,348,205 |

|

2,879,008 |

|

3,644,552 |

|

846,887 |

|

8,127,822 |

|

|

Financial income |

|

316,611 |

|

455,802 |

|

295,563 |

|

436,236 |

|

484,046 |

|

|

Financial expenses |

|

(952,679 |

) |

(970,457 |

) |

(1,097,633 |

) |

(1,286,368 |

) |

(1,620,782 |

) |

|

Exchange variations, net |

|

(134,128 |

) |

51,757 |

|

104,364 |

|

1,060,883 |

|

(1,035,576 |

|

|

Gains and losses on financial instruments, net |

|

(18,547 |

) |

(65,438 |

) |

12,392 |

|

(26,178 |

) |

(62,396 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

INCOME BEFORE TAXES |

|

1,559,462 |

|

2,350,672 |

|

2,959,238 |

|

1,031,460 |

|

5,893,114 |

|

|

Income and social contribution taxes |

|

|

|

|

|

|

|

|

|

|

|

|

Current |

|

(316,271 |

) |

(519,843 |

) |

(642,306 |

) |

(303,272 |

) |

(1,423,660 |

) |

|

Deferred |

|

253,049 |

|

266,747 |

|

140,447 |

|

276,320 |

|

475,444 |

) |

|

NET INCOME |

|

1,496,240 |

|

2,097,576 |

|

2,457,379 |

|

1,004,508 |

|

4,944,898 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

ATRIBUTABLE TO: |

|

|

|

|

|

|

|

|

|

|

|

|

Owners of the parent |

|

1,425,633 |

|

2,005,727 |

|

2,142,488 |

|

1,121,966 |

|

3,940,505 |

|

|

Non-controlling interests |

|

70,607 |

|

91,849 |

|

314,891 |

|

(117,458 |

) |

1,004,393 |

|

|

|

|

1,496,240 |

|

2,097,576 |

|

2,457,379 |

|

1,004,508 |

|

4,944,898 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Basic earnings per share — in R$ |

|

|

|

|

|

|

|

|

|

|

|

|

Common |

|

0.84 |

|

1.22 |

|

1.50 |

|

0.79 |

|

2.83 |

|

|

Preferred |

|

0.84 |

|

1.22 |

|

1.50 |

|

0.79 |

|

2.83 |

|

|

Diluted earnings per share — in R$ |

|

|

|

|

|

|

|

|

|

|

|

|

Common |

|

0.84 |

|

1.22 |

|

1.50 |

|

0.79 |

|

2.75 |

|

|

Preferred |

|

0.84 |

|

1.22 |

|

1.50 |

|

0.79 |

|

2.75 |

|

|

Cash dividends declared per share — in R$ |

|

|

|

|

|

|

|

|

|

|

|

|

Common |

|

0.24 |

|

0.35 |

|

0.44 |

|

0.25 |

|

0.79 |

|

|

Preferred |

|

0.24 |

|

0.35 |

|

0.44 |

|

0.25 |

|

0.79 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Weighted average Common Shares outstanding during the year (1) |

|

571,929,945 |

|

550,305,197 |

|

494,888,956 |

|

494,888,956 |

|

485,403,980 |

(1) |

|

Weighted average Preferred Shares outstanding during the year (1) |

|

1,130,398,618 |

|

1,092,338,207 |

|

930,434,530 |

|

925,676,955 |

|

905,257,476 |

(1) |

|

Number of Common Shares outstanding at year end (2) |

|

573,627,483 |

|

573,627,483 |

|

505,600,573 |

|

496,586,494 |

|

496,586,494 |

(2) |

|

Number of Preferred Shares outstanding at year end (2) |

|

1,146,031,245 |

|

1,146,031,245 |

|

1,011,201,145 |

|

934,793,732 |

|

934,793,732 |

(2) |

(1) The information on the numbers of shares presented above corresponds to the weighted average quantity during each year.

(2) The information on the numbers of shares presented above corresponds to the shares at the end of the year

|

|

|

On December 31, |

| ||||||||

|

|

|

2012 |

|

2011 |

|

2010 |

|

2009 |

|

2008 |

|

|

|

|

(Expressed in thousands of Brazilian Reais - R$) |

| ||||||||

|

Balance sheet selected information |

|

|

|

|

|

|

|

|

|

|

|

|

Cash and cash equivalents |

|

1,437,235 |

|

1,476,599 |

|

1,061,034 |

|

2,091,944 |

|

2,026,609 |

|

|

Short-term investments (1) |

|

1,059,605 |

|

3,101,649 |

|

1,115,461 |

|

2,677,714 |

|

3,386,637 |

|

|

Current assets |

|

16,410,397 |

|

17,319,149 |

|

12,945,944 |

|

14,164,686 |

|

20,775,540 |

|

|

Current liabilities |

|

7,823,182 |

|

6,777,001 |

|

5,021,900 |

|

4,818,521 |

|

8,475,437 |

|

|

Net working capital (2) |

|

8,587,215 |

|

10,542,148 |

|

7,924,044 |

|

9,346,165 |

|

12,300,103 |

|

|

Property, plant and equipment, net |

|

19,690,181 |

|

17,295,071 |

|

16,171,560 |

|

16,731,101 |

|

20,054,747 |

|

|

Net assets (3) |

|

28,797,917 |

|

26,519,803 |

|

20,147,615 |

|

22,004,793 |

|

25,043,578 |

|

|

Total assets |

|

53,093,158 |

|

49,981,794 |

|

42,891,260 |

|

44,583,316 |

|

59,050,514 |

|

|

Short-term debt (including “Current Portion of Long-Term Debt”) |

|

2,324,374 |

|

1,715,305 |

|

1,577,968 |

|

1,356,781 |

|

3,788,085 |

|

|

Long-term debt, less current portion |

|

11,725,868 |

|

11,182,290 |

|

12,360,056 |

|

12,563,155 |

|

18,595,002 |

|

|

Debentures - short term |

|

257,979 |

|

41,688 |

|

115,069 |

|

— |

|

145,034 |

|

|

Debentures - long term |

|

360,334 |

|

744,245 |

|

616,902 |

|

600,979 |

|

705,715 |

|

|

Equity |

|

28,797,917 |

|

26,519,803 |

|

20,147,615 |

|

22,004,793 |

|

25,043,578 |

|

|

Capital stock |

|

19,249,181 |

|

19,249,181 |

|

15,651,352 |

|

14,184,805 |

|

14,184,805 |

|

(1) Includes held for trading and available for sale.

(2) Total current assets less total current liabilities.

(3) Total assets less total current liabilities and less total non-current liabilities.

Exchange rates between the United States Dollar and Brazilian Reais

The following table presents the exchange rates, according to the Brazilian Central Bank, for the periods indicated between the United States dollar and the Brazilian real which is the currency in which we prepare our financial statements included in this Annual Report on Form 20-F.

Exchange rates from U.S. dollars to Brazilian reais

|

|

|

Period- |

|

|

|

|

|

|

|

|

Period |

|

end |

|

Average |

|

High |

|

Low |

|

|

March-2013 (through March 26) |

|

2.0081 |

|

1.9791 |

|

2.0140 |

|

1.9528 |

|

|

February-2013 |

|

1.9754 |

|

1.9733 |

|

1.9893 |

|

1.9570 |

|

|

January-2013 |

|

1.9883 |

|

2.0311 |

|

2.0471 |

|

1.9883 |

|

|

December-2012 |

|

2.0435 |

|

2.0778 |

|

2.1121 |

|

2.0435 |

|

|

November-2012 |

|

2.1074 |

|

2.0678 |

|

2.1074 |

|

2.0312 |

|

|

October - 2012 |

|

2,0308 |

|

2,0299 |

|

2,0382 |

|

2.0224 |

|

|

September - 2012 |

|

2.0306 |

|

2.0281 |

|

2.0392 |

|

2.0139 |

|

|

2012 |

|

2.0435 |

|

1.9550 |

|

2.1121 |

|

1.7024 |

|

|

2011 |

|

1.8758 |

|

1.6746 |

|

1.9016 |

|

1.5345 |

|

|

2010 |

|

1.6662 |

|

1.7593 |

|

1.8811 |

|

1.6554 |

|

|

2009 |

|

1.7412 |

|

1.9935 |

|

2.4218 |

|

1.7024 |

|

|

2008 |

|

2.3370 |

|

1.8375 |

|

2.5004 |

|

1.5593 |

|

Dividends

The Company’s total authorized capital stock is composed of common and preferred shares. As of December 31, 2012, the Company had 571,929,945 common shares and 1,128,534,345 non-voting preferred shares outstanding (excluding treasury stock).

The following table details dividends and interest on equity paid to holders of common and preferred stock since 2008. The figures are expressed in Brazilian reais and U.S. dollars. The exchange rate used for conversion to U.S. dollars was based on the date of the resolution approving the dividend. Dividends per share figures have been retroactively adjusted for all periods to reflect the stock dividend of one share for every share held (April 2008).

Dividends per share information has been computed by dividing dividends and interest on equity by the number of shares outstanding, which excludes treasury stock. The table below presents the quarterly dividends paid per share, except where stated otherwise:

|

Period |

|

Date of |

|

R$ per Share |

|

$ per Share |

|

|

1st Quarter 2008 (1) |

|

05/12/2008 |

|

0.2050 |

|

0.1224 |

|

|

2nd Quarter 2008 |

|

08/06/2008 |

|

0.3600 |

|

0.2281 |

|

|

3rd Quarter 2008 |

|

11/05/2008 |

|

0.1800 |

|

0.0849 |

|

|

4th Quarter 2008 |

|

02/19/2009 |

|

0.0400 |

|

0.0172 |

|

|

3rd Quarter 2009 (1) |

|

11/05/2009 |

|

0.0750 |

|

0.0435 |

|

|

4th Quarter 2009 (1) |

|

12/23/2009 |

|

0.1800 |

|

0.1013 |

|

|

1st Quarter 2010 (1) |

|

05/06/2010 |

|

0.1200 |

|

0.0654 |

|

|

2st Quarter 2010 |

|

08/05/2010 |

|

0.1400 |

|

0.0798 |

|

|

3st Quarter 2010 (1) |

|

11/05/2010 |

|

0.1200 |

|

0.0714 |

|

|

4st Quarter 2010 |

|

03/03/2011 |

|

0.0600 |

|

0.0363 |

|

|

1st Quarter 2011 |

|

05/05/2011 |

|

0.0600 |

|

0.0370 |

|

|

2nd Quarter 2011 (1) |

|

08/04/2011 |

|

0.0900 |

|

0.0571 |

|

|

3rd Quarter 2011 |

|

11/10/2011 |

|

0.1200 |

|

0.0681 |

|

|

4th Quarter 2011 |

|

02/15/2012 |

|

0.0800 |

|

0.0466 |

|

|

1st Quarter 2012 |

|

05/02/2012 |

|

0.0600 |

|

0.0313 |

|

|

2nd Quarter 2012 |

|

08/02/2012 |

|

0.0900 |

|

0.0440 |

|

|

3rd Quarter 2012 |

|

11/01/2012 |

|

0.0700 |

|

0.0345 |

|

|

4th Quarter 2012 |

|

02/21/2013 |

|

0.0200 |

|

0.0101 |

|

(1) Payment of interest on equity.

Note: the Company did not make interim dividend payments in the 1st and 2nd quarter of 2009.

Brazilian Law 9,249 of December 1995 provides that a company may, at its sole discretion, pay interest on equity in addition to or instead of dividends (See Item 8 — “Financial Information - Interest on Equity”). A Brazilian corporation is entitled to pay its shareholders interest on equity up to the limit based on the application of the TJLP rate (Long-Term Interest Rate) to its shareholders’ equity or 50% of the net income in the fiscal year, whichever is lower. This payment is considered part of the mandatory dividend required by Brazilian Corporation Law for each fiscal year. The payment of interest on equity described herein is subject to a 15% withholding tax. See Item 10. “Additional Information — Taxation”.

Gerdau has a Dividend Reinvestment Plan (DRIP), a program that allows the holders of Gerdau ADRs to reinvest dividends to purchase additional ADRs in the Company, with no issuance of new shares. Gerdau also provides its shareholders with a similar program in Brazil that allows for the reinvestment of dividends in additional shares, with no issuance of new shares.

B. CAPITALIZATION AND INDEBTEDNESS

Not required, as the Company is filing this Form 20-F as an annual report.

C. REASONS FOR THE OFFER AND USE OF PROCEEDS

Not required, as the Company is filing this Form 20-F as an annual report.

D. RISK FACTORS

The Company may not successfully integrate its businesses, management, operations or products, or achieve any of the benefits anticipated from future acquisitions.

Over the years, the Company has expanded its presence mainly through acquisitions in the North American and Latin American markets. The integration of the business and opportunities stemming from entities recently acquired and those that may be acquired by the Company in the future may involve risks. The Company may not successfully integrate acquired businesses, managements, operations, products and services with its current operations. The diversion of management’s attention from its existing businesses, as well as problems that can arise in connection with the integration of the new operations may have an impact on revenue and operating results. The integration of acquisitions may result in additional expenses that could reduce profitability. The Company may not succeed in addressing these risks or any other problems encountered in connection with past and future acquisitions.

All these acquisitions generated goodwill, which is stated in the Company’s balance sheet. The Company evaluates the recoverability of this goodwill on investments annually and uses accepted market practices, including discounted cash flow for business segments which have goodwill. A downturn in the steel market could negatively impact expectations for futures earnings, leading to the need to recognize an expense in its statement of income regarding the impairment in goodwill.

The Company may be unable to reduce its financial leverage, which could increase its cost of capital, in turn adversely affecting its financial condition or operating results.

In 2007, the international rating agencies, Fitch Ratings and Standard & Poor’s, classified the Company’s credit risk as “investment grade”, which gave the Company access to financing at lower borrowing rates. In the beginning of December 2011, Moody’s assigned the Investment Grade rating “Baa3” for all of Gerdau’s ratings, with a stable perspective. With this upgrade from Moody’s, Gerdau currently has the Investment Grade of the three of principal rating agencies: Fitch Ratings, Moody’s and Standard & Poor’s.

The efforts to maintain operating cash generation and to reduce the indebtedness level helped the Company to maintain its credit risk, so that in 2012 the three agencies have issued reports reiterating the investment grade rating, with a stable outlook.

If the Company is unable to maintain its operating and financial results, it may lose its “investment grade” rating, which could increase its cost of capital and consequently adversely affect its financial condition and operating results.

The Company’s level of indebtedness could adversely affect its ability to raise additional capital to fund operations, limit the ability to react to changes in the economy or the industry and prevent it from meeting its obligations under its debt agreements.

The Company’s degree of leverage could have important consequences, including the following:

· it may limit the ability to obtain additional financing for working capital, additions to fixed assets, product development, debt service requirements, acquisitions and general corporate or other purposes;

· it may limit the ability to declare dividends on its shares and ADSs;

· a portion of the cash flows from operations must be dedicated to the payment of interest on existing indebtedness and is not available for other purposes, including operations, additions to fixed assets and future business opportunities;

· it may limit the ability to adjust to changing market conditions and place the Company at a competitive disadvantage compared to its competitors that have less debt;

· the Company may be vulnerable in a downturn in general economic conditions;

· the Company may be required to adjust the level of funds available for additions to fixed assets; and

· Pursuant to the Company’s financial agreements, the penalty for non-compliance with prescribed financial covenants can lead to a declaration of default by the creditors of the relevant loans. Furthermore, R$10.5 billion of the Company’s total indebtedness as of December 31, 2012 was subject to cross-default provisions, with threshold amounts varying from US$10.0 million to US$100.0 million, depending on the agreement. Thus, there is a risk that an event of default in one single debt agreement can potentially trigger events of default in other debt agreements.

Under the terms of its existing indebtedness, the Company is permitted to incur additional debt in certain circumstances but doing so could increase the risks described above.

Unexpected equipment failures may lead to production curtailments or shutdowns.

The Company operates several steel plants in different sites. Nevertheless, interruptions in the production capabilities at the Company’s principal sites would increase production costs and reduce shipments and earnings for the affected period. In addition to periodic equipment failures, the Company’s facilities are also subject to the risk of catastrophic loss due to unanticipated events such as fires, explosions or violent weather conditions. The Company’s manufacturing processes are dependent upon critical pieces of steelmaking equipment, such as its electric arc furnaces, continuous casters, gas-fired reheat furnaces, rolling mills and electrical equipment, including high-output transformers, and this equipment may, on occasion, incur downtime as a result of unanticipated failures. The Company has experienced and may in the future experience material plant shutdowns or periods of reduced production as a result of such equipment failures. Unexpected interruptions in production capabilities would adversely affect the Company’s productivity and results of operations. Moreover, any interruption in production capability may require the Company to make additions to fixed assets to remedy the problem, which would reduce the amount of cash available for operations. The Company’s insurance may not cover the losses. In addition, long-term business disruption could harm the Company’s reputation and result in a loss of customers, which could materially adversely affect the business, results of operations, cash flows and financial condition.

The interests of the controlling shareholder may conflict with the interests of the non-controlling shareholders.

Subject to the provisions of the Company´s By-Laws, the controlling shareholder has powers to:

· elect a majority of the directors and nominate executive officers, establish the administrative policy and exercise full control of the Company´s management;

· sell or otherwise transfer the Company´s shares; and

· approve any action requiring the approval of shareholders representing a majority of the outstanding capital stock, including corporate reorganization, acquisition and sale of assets, and payment of any future dividends.

By having such power, the controlling shareholder can make decisions that may conflict with the interest of the Company and other shareholders.

Non-controlling shareholders may have their stake diluted in an eventual capital increase.

If the Company decides to make a capital increase through issuance of securities, there may be a dilution of the interest of the non-controlling shareholders in the current composition of the Company’s capital.

Participation in other activities related to the steel industry may conflict with the interest of subsidiaries and affiliates.

Through its subsidiaries and affiliates, the Company also engages in other activities related to production and sale of steel products, including reforestation projects; power generation; production of coking coal, iron ore and pig iron; and fab shops and downstream operations. For having the management control in these companies, the Company’s interests may conflict with the interest of these subsidiaries and affiliates, which can even lead to new strategic direction for these businesses.

Higher steel scrap prices or a reduction in supply could adversely affect production costs and operating margins.

The main metal input for the Company’s mini-mills, which mills accounted for 76.2% of total crude steel output in 2012 (in volume), is steel scrap. Although international steel scrap prices are determined essentially by scrap prices in the U.S. local market, because the United States is the main scrap exporter, scrap prices in the Brazilian market are set by domestic supply and demand. The price of steel scrap in Brazil varies from region to region and reflects demand and transportation costs. Should scrap prices increase significantly without a corresponding increase in finished steel selling prices, the Company’s profits and margins could be adversely affected. An increase in steel scrap prices or a shortage in the supply of scrap to its units would affect production costs and potentially reduce operating margins and revenues.

Increases in iron ore and coal prices, or reductions in market supply, could adversely affect the Company’s operations.

When the prices of raw materials, particularly iron ore and coking coal, increase, and the Company needs to produce steel in its integrated facilities, the production costs in its integrated facilities also increase. The Company uses iron ore to produce liquid pig iron at its Ouro Branco mill, and at its Barão de Cocais and Divinópolis mills in the state of Minas Gerais, as well as Siderperu mill, in Peru. Iron ore is also used to produce sponge iron at the Usiba mill in the state of Bahia.

The Ouro Branco mill is the Company’s largest mill in Brazil, and its main metal input for the production of steel is iron ore. In 2012, this unit represented 51.0% of the total crude steel output (in volume) of the Brazil Business Operation. A shortage of iron ore in the domestic market may adversely affect the steel producing capacity of the Brazilian units, and an increase in iron ore prices could reduce profit margins.

The Company has iron ore mines in the state of Minas Gerais, Brazil. To reduce the exposure to iron ore price volatility, the Company invested in the expansion of the production capacity of these mines, and at the end of 2012, reached 100% of the iron ore requirements of the Ouro Branco mill.

All of the Company’s coking coal requirements for its Brazilian units are imported due to the low quality of Brazilian coal. Coking coal is the main energy input at the Ouro Branco mill and is used at the coking facility. Although this mill is not dependent on coke supplies, a contraction in the supply of coking coal could adversely affect the integrated operations at this site, since the Ouro Branco mill requires coking coal to produce coke in its coking facility. The coking coal used in this mill is imported from Canada, the United States, Australia and Colombia. A shortage of coking coal in the international market would adversely affect the steel producing capacity of the Ouro Branco mill, and an increase in prices could reduce profit margins. The Company does not have relevant long-term supply contracts for the raw materials it uses.

The Company’s operations are energy-intensive, and energy shortages or higher energy prices could have an adverse affect.

Steel production is an energy-intensive process, especially in melt shops with electric arc furnaces. Electricity represents an important cost component at these units, as also does natural gas, although to a lesser extent. Electricity cannot be replaced at the Company’s mills and power rationing or shortages, like those that occurred in Brazil in 2001, could adversely affect production at those units.

Natural gas is used in the reheating furnaces of the Company’s rolling mills. In the case of shortages in the supply of natural gas, the Company could in some instances use fuel oil, diesel or LPG.

Global crises and subsequent economic slowdowns like those that occurred during 2008 and 2009 may adversely affect global steel demand. As a result, the Company’s financial condition and results of operations may be adversely affected.

Historically, the steel industry has been highly cyclical and deeply impacted by economic conditions in general, such as world production capacity and fluctuations in steel imports/exports and the respective import duties. After a steady period of growth between 2004 and 2008, the marked drop in demand resulting from the global economic crisis of 2008-2009 once again demonstrated the vulnerability of the steel market to volatility of international steel prices and raw materials. That crisis was caused by the dramatic increase of high risk real estate financing defaults and foreclosures in the United States, with serious consequences for bank and financial markets throughout the world. Developed markets, such as North America and Europe, experienced a strong recession due to the collapse of real estate financings and the shortage of global credit. As a result, the demand for steel products suffered a decline in 2009, but since 2010 has been experiencing a gradual recovery, principally in the developing economies.

The economic downturn and unprecedented turbulence in the global economy can negatively impact the consuming markets, affecting the business environment with respect to the following:

· Decrease in international steel prices;

· Slump in international steel trading volumes;

· Crisis in automotive industry and infrastructure sectors; and

· Lack of liquidity, mainly in the U.S. economy.

If the Company is not able to remain competitive in these shifting markets, our profitability, margins and income may be negatively affected. Although the demand for steel products from 2010 to 2012 had been experiencing gradual improvements, no assurance can be given that these improvements will continue through the next years. A decline in this trend could result in a decrease in Gerdau shipments and revenues.

Brazil’s political and economic conditions and the Brazilian government’s economic and other policies may negatively affect demand for the Company’s products as well as its net sales and overall financial performance.

The Brazilian economy has been characterized by frequent and occasionally extensive intervention by the Brazilian government. The Brazilian government has often changed monetary, taxation, credit, tariff and other policies to influence the course of the country’s economy. The Brazilian government’s actions to control inflation and implement other policies have involved hikes in interest rates, wage and price controls, devaluation of the currency, freezing of bank accounts, capital controls and restrictions on imports.

The Company’s operating results and financial condition may be adversely affected by the following factors and the government responses to them:

· exchange rate controls and fluctuations;

· interest rates;

· inflation;

· tax policies;

· energy shortages;

· liquidity of domestic and foreign capital and lending markets; and

· other political, diplomatic, social and economic developments in or affecting Brazil.

Uncertainty over whether the Brazilian government will change policies or regulations affecting these or other factors may contribute to economic uncertainty in Brazil and to heightened volatility in Brazilian securities markets and securities issued abroad by Brazilian issuers. These and other developments in Brazil’s economy and government policies may adversely affect the Company and its business.

Inflation and government actions to combat inflation may contribute significantly to economic uncertainty in Brazil and could adversely affect the Company’s business.

Brazil has experienced high inflation in the past. Since the implementation of the Real Plan in 1994, the annual rate of inflation has decreased significantly, as measured by the National Broad Consumer Price Index (Índice Nacional de Preços ao Consumidor Amplo, or IPCA). Inflation measured by the IPCA index was 5.8% in 2008, 4.3% in 2009, 5.8% in 2010, 6.3% in 2011 and 5.7% in 2012. If Brazil were to experience high levels of inflation once again, the country’s rate of economic growth could slow, which would lead to lower demand for the Company’s products in Brazil. Inflation is also likely to increase some costs and expenses which the Company may not be able to pass on to its customers and, as a result, may reduce its profit margins and net income. In addition, high inflation generally leads to higher domestic interest rates, which could lead the cost of servicing the Company’s debt denominated in Brazilian reais to increase. Inflation may also hinder its access to capital markets, which could adversely affect its ability to refinance debt. Inflationary pressures may also lead to the imposition of additional government policies to combat inflation that could adversely affect its business.

Variations in the foreign exchange rates between the U.S. dollar and the currencies of countries in which the Company operates may increase the cost of servicing its debt denominated in foreign currency and adversely affect its overall financial performance.

The Company’s operating results are affected by fluctuations in the foreign exchange rates between the Brazilian real, the currency in which the Company prepares its financial statements, and the currencies of the countries in which it operates.

Significant depreciation in the Brazilian real in relation to the U.S. dollar or other currencies could reduce the Company’s ability to service its obligations denominated in foreign currencies, particularly since a significant part of its net sales revenue is denominated in Brazilian reais.

For example, the North America Business Operation reports its results in U.S. dollars. Therefore, fluctuations in the exchange rate between the U.S. dollar and the Brazilian real could affect its operating results. The same occurs with all other businesses located outside Brazil with respect to the exchange rate between the local currency of the respective subsidiary and the Brazilian real.

Export revenue and margins are also affected by fluctuations in the exchange rate of the U.S. dollar and other local currencies of the countries where the Company produces in relation to the Brazilian real. The Company’s production costs are denominated in local currency but its export sales are generally denominated in U.S. dollars. Revenues generated by exports denominated in U.S.

dollars are reduced when they are translated into Brazilian real in periods during which the Brazilian currency appreciates in relation to the U.S. dollar.

The Brazilian real appreciated against the U.S. dollar by 4.3% in 2010. On December 31, 2011, the U.S. dollar/Brazilian real exchange rate was $1.00 per R$ 1.88, resulting in depreciation of 12.6% when compared to December 31, 2010. By the end of 2012 the Brazilian real had depreciated 8.9% against the U.S. dollar.

Depreciation in the Brazilian real in relation to the U.S. dollar could also result in additional inflationary pressures in Brazil, by generally increasing the price of imported products and services and requiring recessionary government policies to curb demand. In addition, depreciation in the Brazilian real could weaken investor confidence in Brazil.

The Company held debt denominated in foreign currency, mainly U.S. dollars, in an aggregate amount of R$ 11.8 billion at December 31, 2012, representing 80.3% of its gross indebtedness on a consolidated basis. On December 31, 2012, the Company held R$ 880 million in cash equivalents and short-term investments denominated in currencies different from the Brazilian real, intended to be invested in maintenance capital expenditure, new production capacity or working capital, in the same countries in which such amount is available, considering the Company´s significant foreign operations. Due to its tax planning policy, the Company does not intend to transfer material amounts between countries, using different currencies. Additionally, the Company does not have any material restriction on the transfer of cash and short-term investments held by foreign subsidiaries and the funds are readily convertible into other foreign currencies, including the Brazilian real.

Demand for steel is cyclical and a reduction in prevailing world prices for steel could adversely affect the Company’s operating results.

The steel industry is highly cyclical. Consequently, the Company is exposed to substantial swings in the demand for steel products, which in turn causes volatility in the prices of most of its products and eventually could cause write-downs of its inventories. In addition, the demand for steel products, and hence the financial condition and operating results of companies in the steel industry, including the Company itself, are generally affected by macroeconomic changes in the world economy and in the domestic economies of steel-producing countries, including general trends in the steel, construction and automotive industries. Since 2003, demand for steel products from developing countries (particularly China), the strong euro compared to U.S. dollar and world economic growth have contributed to a historically high level of prices for the Company’s steel products. However, these relatively high prices may not last, especially due to expansion in world installed capacity or a new level of demand. In the second half of 2008, and especially in the beginning of 2009, the U.S. and European economies experienced a significant slow down, in turn affecting many other countries. Since the end of 2009, world steel demand and prices have been improving and the Company believes that this trend will continue throughout 2013. A material decrease in demand for steel or exports by countries not able to consume their production, could have a significant adverse effect on the Company’s operations and prospects.

Less expensive imports from other countries into Brazil may adversely affect the Company’s operating results.

Steel imports in Brazil caused downward pressure on steel prices in 2010, adversely affecting shipments and profit margins, especially in the fourth quarter. Competition from foreign steel producers is a threat and may grow due to an increase in foreign installed steel capacity, depreciation of the U.S. dollar and a reduction of domestic steel demand in other markets, with these factors leading to higher levels of steel imports into Brazil at lower prices. Any change in the factors mentioned above, as well as in duties or protectionist measures could result in a higher level of imports into Brazil, resulting in pressures on the domestic prices that could adversely impact our business. During 2011 and 2012, as a result of higher international prices, the domestic price premium compared to the international price was reduced, avoiding thereby the importation of long steel products and permitting a recovery in the domestic market prices which had been pressured by increased raw material costs.

New Entrants into the Brazilian market can affect the Company’s competitiveness.

Since 2009, the intention of installing new steel production capacity in Brazil has been announced by a number of players in the industry. If effected, these installations could result in a possible loss of market share, reduction of prices and shortage of raw materials with the resulting increase in their prices.

Our mineral resource estimates may materially differ from mineral quantities that we may be able to actually extract.

Our mining resources are estimated quantities of ore and minerals. There are numerous uncertainties inherent in estimating quantities of resources, including many factors beyond our control. Reserve engineering involves estimating deposits of minerals that cannot be measured in an exact manner, and the accuracy of any reserve estimate is a function of the quality of available data, engineering and geological interpretation and judgment. In addition, estimates of different engineers may vary. As a result, no assurance can be given that the amount of mining resources will be extracted or that they can be extracted at commercially viable rates.

An increase in China’s steelmaking capacity or a slowdown in China’s steel consumption could have a material adverse effect on domestic and global steel pricing and could result in increased steel imports into the markets in which we operate.

A significant factor in the worldwide strengthening of steel pricing over the past several years has been the significant growth in steel consumption in China, which at times has outpaced that country’s manufacturing capacity to produce enough steel to satisfy its own needs. At times this has resulted in China being a net importer of steel products, as well as a net importer of raw materials and supplies required in the steel manufacturing process. A reduction in China’s economic growth rate with a resulting reduction of steel consumption, coupled with China’s expansion of steel-making capacity, could have the effect of a substantial weakening of both domestic and global steel demand and steel pricing. Moreover, many Asian and European steel producers that had previously shipped their output to China may ship their steel products to other markets in the world, which could cause a material erosion of margins through a reduction in pricing.

Restrictive measures on trade in steel products may affect the Company’s business by increasing the price of its products or reducing its ability to export.

The Company is a steel producer that supplies both the domestic market in Brazil and a number of international markets. The Company’s exports face competition from other steel producers, as well as restrictions imposed by importing countries in the form of quotas, ad valorem taxes, tariffs or increases in import duties, any of which could increase the costs of products and make them less competitive or prevent the Company from selling in these markets. There are no assurances that importing countries will not impose quotas, ad valorem taxes, tariffs or increase import duties.

Costs related to compliance with environmental regulations could increase if requirements become stricter, which could have a negative effect on the Company’s operating results.

The Company’s industrial units and other activities must comply with a series of federal, state and municipal laws and regulations regarding the environment and the operation of plants in the countries in which they operate. These regulations include procedures relating to control of air emissions, disposal of liquid effluents and the handling, processing, storage, disposal and reuse of solid waste, hazardous or not, as well as other controls necessary for a steel company.

Moreover, environmental legislation establishes that the regular functioning of operations that pollute, have the potential to pollute or that cause any form of environmental degradation, is subject to environmental licensing. This licensing is required for initial installation and operation of the project, as well as any expansions performed, and the licenses must be renewed periodically. Each of the licenses is issued according to the phase of the project’s implementation. In order for the license to remain valid, the project must comply with conditions established by the environmental licensing body.

Non-compliance with environmental laws and regulations could result in administrative or criminal sanctions and closure orders, in addition to the obligation of repairing damage caused to third parties and the environment, such as clean-up of contamination. If current and future laws become stricter, spending on fixed assets and costs to comply with legislation could increase and negatively affect the Company’s financial situation. Moreover, future acquisitions could subject the Company to additional spending and costs in order to comply with environmental legislation.

Laws and regulations to reduce greenhouse gases and other atmospheric emissions could be enacted in the near future, with significant, adverse effects on the results of the Company’s operations, cash flows and financial situation.

One of the possible effects of the expansion of greenhouse gas reduction requirements is an increase in costs, mainly resulting from the demand for renewable energy and the implementation of new technologies in the productive chain. On the other hand, demand is expected to grow constantly for recyclable materials such as steel, which, being a product that could be recycled numerous times without losing its properties, results in lower emissions during the lifecycle of the product.

The Company expects operations overseas to be affected by future federal, state and provincial laws related to climate change, seeking to deal with the question of greenhouse gas (GHG) and other atmospheric emissions. Thus, one of the possible effects of this increase in legal requirements could be an upturn in energy costs.

Layoffs in the Company’s labor force could generate costs or negatively affect the Company’s operations.

A substantial number of our employees are represented by labor unions and are covered by collective bargaining or other labor agreements, which are subject to periodic negotiation. Strikes or work stoppages have occurred in the past and could reoccur in connection with negotiations of new labor agreements or during other periods for other reasons, including the risk of layoffs during a down cycle that could generate severance costs. Moreover, we could be adversely affected by labor disruptions involving unrelated parties that may provide us with goods or services. Strikes and other labor disruptions at any of our operations could adversely affect the operation of facilities and the timing of completion and the cost of capital of our projects.

Developments and the perception of risks in other countries, especially in the United States and emerging market countries, may adversely affect the market prices of our preferred shares and ADSs.

The market for securities issued by Brazilian companies is influenced, to varying degrees, by economic and market conditions in the United States and emerging market countries, especially other Latin American countries. Although economic conditions are different in each country, the reaction of investors to economic developments in one country may cause the capital markets in other countries to fluctuate. Developments or adverse economic conditions in other emerging market countries have at times resulted in significant outflows of funds from, and declines in the amount of foreign currency invested in Brazil.

The Brazilian economy is also affected by international economic and market conditions, especially economic and market conditions in the United States. Share prices on the BM&FBOVESPA, for example, have historically been sensitive to fluctuations in United States interest rates as well as movements of the major United States stocks indexes.

Economic developments in other countries and securities markets could adversely affect the market prices of our preferred shares or the ADSs, could make it more difficult for us to access the capital markets and finance our operations in the future on acceptable terms or at all, and could also have a material adverse effect on our operations and prospects.

Less expensive imports from other countries into North America and Latin America may adversely affect the Company’s operating results.

Steel imports in North America and Latin America have forced a reduction in steel prices in the last several years, adversely affecting shipments and profit margins. The competition of foreign steel producers is strong and may increase due to the increase in their installed capacity, the depreciation of the U.S. dollar and the reduced domestic demand for steel in other markets, with those factors leading to higher levels of steel imports into North and Latin America at lower prices. In the past, the United States government adopted temporary protectionist measures to control the import of steel by means of quotas and tariffs. Some Latin American countries have adopted similar measures. These protectionist measures may not be adopted and, despite efforts to regulate trade, imports at unfair prices may be able to enter into the North American and Latin American markets, resulting in pricing pressures that may adversely affect the Company’s results.

A. HISTORY AND DEVELOPMENT OF THE COMPANY

Gerdau S.A. is a Brazilian corporation (Sociedade Anônima) that was incorporated on November 20, 1961 under the laws of Brazil. Its main registered office is located at Av. Farrapos, 1811, Porto Alegre, Rio Grande do Sul, Brazil, and the telephone number is +55 (51) 3323 2000.

History

The current Company is the product of a number of corporate acquisitions, mergers and other transactions dating back to 1901. The Company began operating in 1901 as the Pontas de Paris nail factory controlled by the Gerdau family based in Porto Alegre, who is still the Company’s indirect controlling shareholder. In 1969, Pontas de Paris was renamed Metalúrgica Gerdau S.A., which today is the holding company controlled by the Gerdau family through intermediate holding companies that in turn controls what is today Gerdau S.A.

From 1901 to 1969, the Pontas de Paris nail factory grew and expanded its business into a variety of steel-related products and services. At the end of World War II, the Company acquired Siderúrgica Riograndense S.A., a steel producer also located in Porto

Alegre, in an effort to broaden its activities and provide it with greater access to raw materials. In February 1948, the Company initiated its steel operations, which foreshadowed the successful mini-mill model of producing steel in electric arc furnaces using steel scrap as the main raw material. At that time the Company adopted a regional sales strategy to ensure more competitive operating costs. In 1957, the Company installed a second unit in the state of Rio Grande do Sul in the city of Sapucaia do Sul, and in 1962, steady growth in the production of nails led to the construction of a larger and more advanced factory in Passo Fundo, also in Rio Grande do Sul.

In 1967, the Company expanded into the Brazilian state of São Paulo, purchasing Fábrica de Arames São Judas Tadeu, a producer of nails and wires, which was later renamed Comercial Gerdau and ultimately became the Company’s Brazilian distribution channel for steel products. In June 1969, the Company expanded into the Northeast of Brazil, producing long steel at Siderúrgica Açonorte in the state of Pernambuco. In December 1971, the Company acquired control of Siderúrgica Guaíra, a long steel producer in the state of Paraná in Brazil’s South Region. The Company also established a new company, Seiva S.A. Florestas e Indústrias, to produce lumber on a sustainable basis for the furniture, pulp and steel industries. In 1979, the Company acquired control of the Cosigua mill in Rio de Janeiro, which currently operates the largest mini-mill in Latin America. Since then, the Company has expanded throughout Brazil with a series of acquisitions and new operations, and today owns 15 steel units in Brazil.

In 1980, the Company began to expand internationally with the acquisition of Gerdau Laisa S.A., the only long steel producer in Uruguay, followed in 1989 by the purchase of the Canadian company Gerdau Ameristeel Cambridge, a producer of common long rolled steel products located in Cambridge, Ontario. In 1992, the Company acquired control of Gerdau AZA S.A., a producer of crude steel and long rolled products in Chile. Over time, the Company increased its international presence by acquiring a non-controlling interest in a rolling mill in Argentina, a controlling interest in Diaco S.A. in Colombia, and, most notably, additional interests in North America through the acquisition of Gerdau Ameristeel MRM Special Sections, a producer of special sections such as elevator guide rails and super light beams, and the former Ameristeel Corp., a producer of common long rolled products. In October 2002, through a series of transactions, the Company merged its North American steel production assets with those of the Canadian company Co-Steel, a producer of long steel, to create Gerdau Ameristeel, which is currently the second largest long steel producer in North America based on steel production volume. Gerdau Ameristeel itself has a number of operations throughout Canada and the United States, including its 50% jointly-controlled entity interest in Gallatin Steel, a manufacturer of flat steel, and also operates 20 steel units and 62 fabrication shops and downstream operations.

In September 2005, Gerdau acquired 36% of the stock issued by Sipar Aceros S.A., a long steel rolling mill, located in the Province of Santa Fé, Argentina. This interest, added to the 38% already owned by Gerdau represents 74% of the capital stock of Sipar Aceros S.A. At the end of the third quarter of 2005, Gerdau concluded the acquisition of a 57% interest in Diaco S.A., the largest rebar manufacturer in Colombia. In January 2008, the Company purchased an additional interest of 40%, for $107.2 million (R$ 188.7 million on the acquisition date).

In January 2006, through its subsidiary Gerdau Hungria Holdings Limited Liability Company, Gerdau acquired 40% of the capital stock of Corporación Sidenor S.A. for $219.2 million (R$ 493.2 million), the largest long special steel producer, forged parts manufacturer and foundry in Spain, and one of the major producers of forged parts using the stamping process in that country. In December 2008, Gerdau Hungria Holding Limited Liability Company acquired for $288.0 million (R$ 674.0 million) from LuxFin Participation S.L., its 20% interest in Corporación Sidenor. With this acquisition, Gerdau became the majority shareholder (60%) in Corporación Sidenor. In December 2006, Gerdau announced that its Spanish subsidiary Corporación Sidenor, S.A., had completed the acquisition of all outstanding shares issued by GSB Acero, S.A., a subsidiary of CIE Automotive for $143.0 million (R$ 313.8 million).

In March 2006, the assets of two industrial units were acquired in the United States. The first was Callaway Building Products in Knoxville, Tennessee, a supplier of fabricated rebar to the construction industry. The second was Fargo Iron and Metal Company located in Fargo, North Dakota, a storage and scrap processing facility and service provider to manufacturers and construction companies.

In June 2006, Gerdau acquired for $103.0 million (R$ 224.5 million) Sheffield Steel Corporation in Sand Springs, Oklahoma in the USA. Sheffield is a mini-mill producer of common long steel, namely concrete reinforcement bars and merchant bars. It has one melt shop and one rolling mill in Sand Springs, Oklahoma, one rolling mill in Joliet, Illinois and three downstream units in Kansas City and Sand Springs.

In the same month, Gerdau S.A. won the bid for 50% plus one share of the capital stock of Empresa Siderúrgica Del Perú S.A.A. (Siderperú) located in the city of Chimbote in Peru for $60.6 million (R$ 134.9 million). In November 2006, Gerdau also won the bid for 324,327,847 shares issued by Siderperú, which represented 33% of the total capital stock, for $40.5 million, totaling $101.1 million (R$ 219.8 million). This acquisition added to the interest already acquired earlier in the year, for an interest of 83% of the capital stock of Siderperú. Siderperú operates a blast furnace, a direct reduction unit, a melt shop with one electric arc furnaces and two LD converters and three rolling mills.

In November 2006, the Company completed the acquisition of a 55% controlling interest in Pacific Coast Steel (“PCS”), for $104.0 million (R$ 227.4 million). The company operates rebar fabrication plants in San Diego, San Bernardino, Fairfield, and Napa, California. Additionally, in April, 2008 Gerdau increased its stake in PCS to 84% paying $82.0 million (R$ 138.4 million). The acquisition of PCS expanded the Company’s operations to the West Coast of the United States and also added rebar placing capability.

In March 2007, Gerdau acquired Siderúrgica Tultitlán, a mini mill located in the Mexico City metropolitan area that produces rebar and profiles. The price paid for the acquisition was $259.0 million (R$ 536.0 million).

In May 2007, Gerdau acquired an interest of 30% in Multisteel Business Holdings Corp., a holding of Indústrias Nacionales, C. por A. (“INCA”), a company located in Santo Domingo, Dominican Republic, that produces rolled products. This partnership allowed the Company to access the Caribbean market. The total cost of the acquisition was $42.9 million (R$ 82.0 million). In July 2007, the Company acquired an additional interest of 19% in Multisteel Business Holdings Corp., bringing its total interest in the Company to 49%. The total cost of this second acquisition was $72.0 million (R$ 135.2 million).

In June 2007, Gerdau acquired 100% of the capital stock of Siderúrgica Zuliana C.A., a Venezuelan company operating a steel mill in the city of Ojeda, Venezuela. The total cost of the acquisition was $92.5 million (R$ 176.2 million).

In the same month, Gerdau and the Kalyani Group from India initiated an agreement to establish a jointly-controlled entity for an investment in Tadipatri, India. The jointly-controlled entity included an interest of 45% in Kalyani Gerdau Steel Ltd., a producer of steel with two LD converters, one continuous casting unit and facilities for the production of pig iron. The agreement provides for shared control of the jointly-controlled entity, and the purchase price was $73.0 million (R$ 127.3 million). In May 2008, Gerdau announced the conclusion of this acquisition. On July 7, 2012, the Company obtained control of Kalyani Gerdau Steel Ltds (KGS), which the Company had an interest of 91.28% as of the control acquisition date. In 2012, until the date the Company acquired control over KGS, the Company made capital increases in KGS, which resulted in an increase of shareholding interest held on December 31, 2011 from 80.57% to 91.28%.

In September 2007, Gerdau Ameristeel concluded the acquisition of Chaparral Steel Company, increasing the Company’s portfolio of products and including a comprehensive line of structural steel products. Chaparral operates two mills, one located in Midlothian, Texas, and the other located in Petersburg, Virginia. The total cost of the acquisition was $4.2 billion (R$ 7.8 billion), plus the assumption of certain liabilities.

In October 2007, Gerdau Ameristeel acquired 100% of Enco Materials Inc., a leading company in the market of commercial materials headquartered in Nashville, Tennessee. Enco Materials Inc. has eight units located in Arkansas, Tennessee and Georgia. The purchase price for this acquisition was $46 million (R$ 84.9 million) in cash, plus the assumption of certain liabilities of the acquired company.

In the same month, Gerdau executed a letter of intent for the acquisition of an interest of 49% in the capital stock of the holding company Corsa Controladora, S.A. de C.V., headquartered in Mexico City, Mexico. The holding company owns 100% of the capital stock of Aceros Corsa, S.A. de C.V. and its distributors. Aceros Corsa, located in the city of Tlalnepantla in the Mexico City metropolitan area, is a mini-mill responsible for the production of long steel (light commercial profiles). The acquisition price was $110.7 million (R$ 186.3 million). In February 2008, the Company announced the conclusion of this acquisition.

In November 2007, Gerdau entered into a binding agreement for the acquisition of the steel company MacSteel from Quanex Corporation. MacSteel is the second largest producer of Special Bar Quality (SBQ) in the United States and operates three mini-mills located in Jackson, Michigan; Monroe, Michigan; and Fort Smith, Arkansas. The Company also operates six downstream operations in the states of Michigan, Ohio, Indiana and Wisconsin. The agreement did not include the Building Products business of Quanex, which is an operation not related to the steel market. The purchase price for this acquisition was $1.5 billion (R$ 2.4 billion) in addition to the assumption of their debts and some liabilities. Gerdau concluded the acquisition in April 2008.

In January 2008, Gerdau acquired an additional interest of 40% in the capital of Diaco S.A. for $107.2 million (R$ 188.7 million on the date of the acquisition), increasing its interest to 99% of the capital stock, a figure that also takes into consideration the dilution of the non-controlling interests, which explains the higher percentage in comparison with the percentages of the two major acquisitions made.

In February 2008, Gerdau invested in the verticalization of its businesses and acquired an interest of 51% in Cleary Holdings Corp. for $ 73.0 million (R $ 119.3 million). The Company controls a metallurgical coke producer and coking coal reserves in Colombia. In August 2010, Gerdau S.A. concluded the acquisition of an additional 49% of the total capital of Cleary Holdings Corp. for $ 57 million.

In April 2008, Gerdau entered into a strategic partnership with Corporación Centroamericana del Acero S.A., assuming a 30.0% interest in the capital of this company. The Company owns assets in Guatemala and Honduras as well as distribution centers in El Salvador, Nicaragua and Belize. The price of the acquisition was $180 million (R$ 303.7 million).

In June, 2008, the parent company Metalúrgica Gerdau S.A. acquired a 29% stake of voting and total capital in Aços Villares S.A. from BNDESPAR for R$ 1.3 billion. As a payment, Metalúrgica Gerdau S.A. issued debentures to be exchanged for Gerdau S.A.’s common shares. In December, 2009 the Company’s stake in Aços Villares S.A. owned through its subsidiary Corporación Sidenor S.A. was transferred to direct control of Gerdau S.A., for US$ 218 million (R$ 384 million), which then owned a total 59% stake in Aços Villares S.A. In December 30, 2010, Gerdau S.A. and Aços Villares S.A. shareholders approved the merger into Gerdau S.A. of Aços Villares S.A.

In December 2008, Gerdau Hungria Holding Limited Liability Company acquired Lux Fin Participation S.L. for $288.0 million (R$ 674.0 million), which indirectly holds a 20% interest in Corporación Sidenor. As a result of this acquisition, Gerdau became the majority shareholder (60%) of Corporación Sidenor.

On August 30, 2010, Gerdau S.A. concluded the acquisition of all outstanding common shares issued by Gerdau Ameristeel that it did not yet hold either directly or indirectly, for $11.00 per share in cash, corresponding to a total of $1.6 billion (R$ 2.8 billion). With the acquisition, Gerdau Ameristeel was delisted from the New York and Toronto stock exchanges.