Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, DC 20549

FORM 10-K

(Mark One)

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15 (d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended June 30, 2010

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15 (d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to .

Commission file number 0-25259

BOTTOMLINE TECHNOLOGIES (de), INC.

(Exact Name of Registrant as Specified in Its Charter)

| Delaware | 02-0433294 | |

| (State or Other Jurisdiction of Incorporation or Organization) |

(I.R.S. Employer Identification No.) | |

| 325 Corporate Drive Portsmouth, New Hampshire |

03801 | |

| (Address of Principal Executive Offices) | (Zip Code) | |

Registrant’s telephone number, including area code: (603) 436-0700

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class: |

Name of each exchange on which registered: | |

| Common Stock, $.001 par value per share | The NASDAQ Global Market |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No x

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15 (d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 229.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ¨ No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large Accelerated Filer ¨ | Accelerated Filer x | |||||

| Non-Accelerated Filer ¨ | Smaller Reporting Company ¨ | |||||

| (Do not check if a smaller reporting company) |

||||||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act.): Yes ¨ No x

The aggregate market value of the voting stock held by non-affiliates of the registrant, based on the last sale price of the registrant’s common stock at the close of business on December 31, 2009 was $426,659,320 (reference is made to Part II, Item 5 herein for a statement of assumptions upon which this calculation is based). The registrant has no non-voting stock.

There were 32,219,347 shares of common stock, $.001 par value per share, of the registrant outstanding as of August 31, 2010.

DOCUMENTS INCORPORATED BY REFERENCE

Items 10, 11, 12, 13 and 14 of Part III (except for information required with respect to our executive officers, which is set forth under “Part I—Executive Officers and Other Key Employees of the Registrant”) have been omitted from this report, as we expect to file with the Securities and Exchange Commission, not later than 120 days after the close of our fiscal year ended June 30, 2010, a definitive proxy statement for our 2010 annual meeting of stockholders. The information required by Items 10, 11, 12, 13 and 14 of Part III of this report, which will appear in our definitive proxy statement, is incorporated by reference into this report.

Table of Contents

2

Table of Contents

This Annual Report on Form 10-K contains forward-looking statements that involve risks and uncertainties. Any statements (including statements to the effect that we “believe,” “expect,” “anticipate,” “plan” and similar expressions) that are not statements relating to historical matters should be considered forward-looking statements. Our actual results may differ materially from the results discussed in the forward-looking statements as a result of numerous important factors, including those discussed in “Item 1A. Risk Factors.”

| Item 1. | Business. |

Our Company

We provide electronic payment, invoice and document management solutions to corporations, financial institutions and banks around the world. Our solutions are used to streamline, automate and manage processes and transactions involving global payments, invoice receipt and approval, collections, cash management, risk mitigation, document management, reporting and document archive. We offer software designed to run on-site at the customer’s location as well as hosted or Software as a Service (SaaS) solutions. Historically, our software has been sold predominantly on a perpetual license basis. Today however, a growing portion of our offerings are being sold as SaaS and paid for on a subscription and transaction basis.

Our corporate customers rely on our solutions to automate their payment and accounts payable processes and to streamline and manage the production and retention of electronic documents. We offer Legal eXchange®, a SaaS offering that receives, manages and controls legal invoices and the related spend management for insurance companies and other large corporate consumers of outside legal services. We also offer Paymode-X, a SaaS offering that facilitates the exchange of electronic payments and invoices between organizations and suppliers and which is offered to customers of Bank of America and Bottomline. Our offerings also include software solutions that banks use to provide web-based payment and reporting capabilities to their corporate customers.

Our solutions complement and leverage our customers’ existing information systems, accounting applications and banking relationships. As a result, our solutions can be deployed quickly and efficiently. To help our customers receive the maximum value from our products and meet their own particular needs, we also provide professional services for installation, training, consulting and product enhancement.

Bottomline was originally organized as a New Hampshire corporation in 1989 and was reincorporated as a Delaware corporation in August 1997. We maintain our corporate headquarters in Portsmouth, New Hampshire and our international headquarters in Reading, England. We maintain a website with the address www.bottomline.com. Our website includes links to our Code of Business Conduct and Ethics, and our Audit Committee, Compensation Committee, and Nominating and Corporate Governance Committee charters. We are not including the information contained in our website as part of, or incorporating it by reference into, this Annual Report on Form 10-K. We make available free of charge, through our website, our annual reports on Form 10-K, quarterly reports on Form 10-Q, and current reports on Form 8-K, and amendments to these reports, as soon as reasonably practical after such material is electronically filed with, or furnished to, the Securities and Exchange Commission (SEC).

Unless the context requires otherwise, references to “we,” “us,” “our,” “Bottomline” and the “Company” refer to Bottomline Technologies (de), Inc. and its subsidiaries.

Our Strategy

Our objective is to be the leading global provider of business payment, invoice and document automation software solutions and services. Key elements of our strategy include the following:

| • | Continuing to add customers and functionality to our growing Paymode-X and Legal eXchange networks; |

3

Table of Contents

| • | Providing software and services which enable banks to offer their corporate customers leading global payment capability and functionality; |

| • | Leveraging our leading payment and document automation software solutions for enterprise customers; |

| • | Increasing the deployment of our SaaS solutions, as well as subscription and transaction based pricing, in order to increase our recurring revenue contribution; |

| • | Continuing to enhance the capabilities and functionality of our Paymode-X solution to capitalize on the significant market opportunity for that offering; |

| • | Continuing to expand our presence outside of North America and Europe by leveraging our experience with changing global payment standards; |

| • | Broadening our relationships with our customer base by selling existing applications, as well as new product offerings, into that base; |

| • | Continuing to develop and broaden strategic relationships that enhance our global position; and |

| • | Pursuing strategic acquisitions that expand our geographical footprint or complement our product functionality. |

Our Products and Services

Payment and Document Automation

The payments automation capabilities inherent in our WebSeries® and PayBase® solutions can generate a wide variety of domestic and international payment instructions along with consolidated bank reporting of cash activity including automated clearing house (ACH), electronic data interchange (EDI), Fedwire transfer, BACSTEL-IP and SWIFT messaging and paper checks in most currencies. Through our payment automation capabilities, customers can reduce administrative expenses and strengthen compliance and anti-fraud controls. Users are able to gather and access data via the Internet on payment and bank account information, including account totals and detailed transaction data, providing improved workflow, financial reporting and bank communications.

To help augment financial document composition and delivery we also offer a number of solutions for automating a wide variety of business documents and financial transaction processes as well as related web-based delivery and document archive. Our products offer advanced design, output formatting and delivery capabilities that enable customers to replace paper-based forms (such as invoices, purchase orders and shipping notices) with more efficient and cost-effective electronic documents. With the capabilities of these product suites, users can centrally manage, distribute and archive business and transaction documents and then distribute them via email, print, fax or the Internet.

Order-to-Pay Solutions

Our Paymode-X solution is designed to simplify the conversion from paper to electronic payments, foster collaboration between buyers and suppliers and streamline business processes for cost reduction and working capital optimization. Paymode-X is a SaaS solution that enables organizations to send electronic payments and remittance details to vendors. Paymode-X also offers electronic invoicing functionality to allow for the automation of the complete order-to-pay process.

Legal Spend Management

Legal eXchange, a SaaS offering, integrates with claims management and time and billing systems to automate legal invoice management processes and to provide insight into all areas of a company’s outside legal spend. Legal eXchange’s combination of automated invoice routing and a sophisticated rules engine allows

4

Table of Contents

corporate legal and insurance claims departments to create more efficient processes for managing invoices generated by outside law firms and other service providers, while offering access to important legal spend factors including budgeting, expense monitoring and outside counsel performance.

Electronic Banking

Our WebSeries Electronic Banking Platform allows banks and financial institutions to deploy Internet-based cash management services for their corporate clients. Based on patented technology and complementary existing systems, our banking platform enables users to leverage a single Internet-based interface for the origination and processing of all types of inbound and outbound domestic and international payments. The software architecture of our banking platform allows banks and financial institutions to configure highly specialized solution sets for enterprise cash management, wholesale banking and retail branch payments using modules for ACH, international payments, check management, information reporting, unattended payment and file transmission, and distributed document printing.

Professional Services

Our teams of service professionals draw on extensive experience to provide consulting, project implementation and training services to our clients. By easing the implementation of our products, these services help our customers accelerate the time to value. By improving the overall customer experience, these services help us retain customers and drive future revenue generating arrangements from existing customers.

Equipment and Supplies

We offer consumable products for laser check printing, including magnetic ink character recognition toner and blank-paper check stock. We also provide printers and printer-related equipment, primarily through arrangements with our hardware vendors, to complement our software product offerings.

Our Customers

Our customers are in diverse industries including financial services, insurance, health care, technology, communications, education, media, manufacturing and government. We provide our products and services to approximately 80 of the Fortune 100 companies and approximately 75 of the FTSE (Financial Times) 100 companies. Our customers include leading organizations such as Australia and New Zealand Banking Group (ANZ), Bank of America, British Airways, Cigna Corporation, Deere and Company, The Hartford Insurance Group, Inc., Johnson Controls, Inc., Liberty Mutual and Vodafone.

Our Competition

The markets in which we participate are highly competitive. We believe our ability to compete depends on factors within and beyond our control, including:

| • | the performance, reliability, features, price and ease of use of our offerings as compared to competitor alternatives; |

| • | our industry knowledge and expertise; |

| • | the execution of our sales and services organizations; |

| • | our ability to attract and retain employees with the requisite domain knowledge and technical skill set necessary to develop and support our products; and |

| • | the timing and market acceptance of new products as well as enhancements to existing products, by us and by our current and future competitors. |

5

Table of Contents

Our payment and document automation products compete primarily with companies that provide solutions to create, publish, manage and archive electronic documents, such as Adobe, StreamServe and Xerox and companies that offer electronic payment and laser check printing software and services, such as Payformance (now a division of SunGard), MHC Software, and ACOM Solutions in the US and Microgen, Albany Software and Experian in Europe. Our products also compete with companies that provide a diverse array of accounts payable automation and workflow capabilities, such as Xign (now part of JP Morgan Chase), BasWare, 170 Systems (now part of Kofax), Open Text, and ReadSoft. We also compete with providers of enterprise resource planning solutions and providers of traditional payment products, including check stock and check printing software and services. In addition, some financial institutions compete with us as outsourced check printing and electronic payment service providers.

For Electronic Banking, we primarily compete with companies such as S1, CoCoNet, Clear2Pay, Fundtech and ACI Worldwide that offer a wide range of financial services including electronic banking applications. We also encounter competition to a lesser degree from Dovetail Software, Infosys Technologies and Oracle Financial Services Software (i-flex), as well as companies that provide traditional treasury workstation solutions.

For our Legal eXchange solution, we compete with a number of companies, including Serengeti Law, DataCert, CT TyMetrix, LexisNexis CounselLink and Allegient Systems.

For our Paymode-X solution, we compete with companies such as Xign (now a part of JP Morgan Chase) and Syncada.

Although we believe that we compete favorably in each of the markets in which we participate, the markets for our products and services are intensely competitive and characterized by rapid technological change and a number of factors could adversely affect our ability to compete in the future, including those discussed in “Item 1A. Risk Factors.”

Our Operating Segments

Operating segments are defined as components of an enterprise for which separate financial information is available that is evaluated regularly by the chief operating decision maker, or decision making group, in deciding how to allocate resources and in assessing performance.

Our operating segments are organized principally by the type of product or service offered and by geography; similar operating segments have been aggregated into three reportable segments as follows:

Payments and Transactional Documents. Our Payments and Transactional Documents segment is a supplier of software products that provide a range of financial business process management solutions including making and collecting payments, sending and receiving invoices, and generating and storing business documents. This segment also provides a range of standard professional services and equipment and supplies that complement and enhance our core software products. Revenue associated with this segment is typically recorded upon delivery or, if extended payment terms have been granted to the customer, as payments become contractually due. This segment incorporates our check printing solutions in the UK, revenue for which is typically recorded on a per transaction basis or ratably over the expected life of the customer relationship, as well as certain solutions that are licensed on a subscription basis, revenue for which is typically recorded ratably over the contractual term.

Banking Solutions. The Banking Solutions segment provides solutions that are specifically designed for banking and financial institution customers. These solutions typically involve longer implementation periods and a significant level of professional resources. Due to the customized nature of these products, revenue is generally recognized over the period of project performance, on a percentage of completion basis. Periodically, we license these solutions on a subscription basis which has the effect of contributing to recurring revenue and the revenue predictability of future periods, but which also delays revenue recognition over a period that is longer than the period of project performance.

6

Table of Contents

Outsourced Solutions. The Outsourced Solutions segment provides customers with outsourced and hosted solution offerings that facilitate invoice receipt and presentment and spend management. Our Legal eXchange solution, which provides the opportunity to create more efficient processes for managing invoices generated by outside law firms while offering access to important legal spend factors such as budgeting, expense monitoring and outside counsel performance, is included within this segment. This segment also incorporates our hosted and outsourced accounts payable automation solutions, including Paymode-X. Revenue within this segment is generally recognized on a subscription or transaction basis or proportionately over the estimated life of the customer relationship.

Each operating segment has separate sales forces and periodically a sales person in one operating segment will sell products and services that are typically sold within a different operating segment. In such cases, the transaction is generally recorded by the operating segment to which the sales person is assigned. Accordingly, segment results can include the results of transactions that have been allocated to a specific segment based on the contributing sales resources, rather than the nature of the product or service. Conversely, a transaction can be recorded by the operating segment primarily responsible for delivery to the customer, even if the sales person is assigned to a different operating segment.

Our chief operating decision maker assesses segment performance based on a variety of factors that can include segment revenue and a segment measure of profit or loss. Each segment’s measure of profit or loss is on a pre-tax basis and excludes stock compensation expense, acquisition-related expenses, impairment losses on equity investments, amortization of intangible assets and restructuring related charges. There are no inter-segment sales; accordingly, the measure of segment revenue and profit or loss reflects only revenues from external customers. The costs of certain corporate level expenses, primarily general and administrative expenses, are allocated to our operating segments at predetermined rates that approximate cost.

We do not track or assign our assets by operating segment.

The following represents a summary of our reportable segments for the years ended June 30, 2010, 2009 and 2008.

| Fiscal Year Ended June 30, | |||||||||||

| 2010 | 2009 | 2008 | |||||||||

| (in thousands) | |||||||||||

| Segment revenue: |

|||||||||||

| Payments and Transactional Documents |

$ | 93,449 | $ | 90,786 | $ | 84,962 | |||||

| Banking Solutions |

33,129 | 22,936 | 22,107 | ||||||||

| Outsourced Solutions |

31,412 | 24,292 | 24,172 | ||||||||

| $ | 157,990 | $ | 138,014 | $ | 131,241 | ||||||

| Segment measure of profit (loss): |

|||||||||||

| Payments and Transactional Documents |

$ | 21,766 | $ | 14,662 | $ | 14,052 | |||||

| Banking Solutions |

4,508 | (1,739 | ) | 1,150 | |||||||

| Outsourced Solutions |

3,030 | 2,349 | (2,610 | ) | |||||||

| Total measure of segment profit |

$ | 29,304 | $ | 15,272 | $ | 12,592 | |||||

7

Table of Contents

A reconciliation of the measure of segment profit to our GAAP income (loss) for 2010, 2009 and 2008, before the provision for income taxes, is as follows:

| Fiscal Year Ended June 30, | ||||||||||||

| 2010 | 2009 | 2008 | ||||||||||

| (in thousands) | ||||||||||||

| Segment measure of profit |

$ | 29,304 | $ | 15,272 | $ | 12,592 | ||||||

| Less: |

||||||||||||

| Amortization of intangible assets |

(13,214 | ) | (15,563 | ) | (11,399 | ) | ||||||

| Stock compensation expense |

(8,956 | ) | (9,498 | ) | (8,803 | ) | ||||||

| Acquisition related expenses |

(585 | ) | (581 | ) | (269 | ) | ||||||

| Restructuring charges |

52 | (1,548 | ) | — | ||||||||

| Add: |

||||||||||||

| Other (expense) income, net |

(93 | ) | 443 | 3,082 | ||||||||

| Income (loss) before provision for income taxes |

$ | 6,508 | $ | (11,475 | ) | $ | (4,797 | ) | ||||

Financial Information About Geographic Areas

We have presented geographic information about our revenues below. This presentation allocates revenue based on the point of sale, not the location of the customer. Accordingly, we derive revenues from geographic locations, based on the location of the customer, that would vary from the geographic areas listed here; particularly in respect of a financial institution customer located in Australia for which the point of sale was the United States. Revenues based on the point of sale were as follows:

| Fiscal Year Ended June 30, | ||||||||||||||||||

| 2010 | 2009 | 2008 | ||||||||||||||||

| (in thousands) | ||||||||||||||||||

| United States |

$ | 105,433 | 66.7 | % | $ | 85,698 | 62.1 | % | $ | 74,846 | 57.0 | % | ||||||

| Europe |

50,702 | 32.1 | % | 50,826 | 36.8 | % | 54,673 | 41.7 | % | |||||||||

| Australia |

1,855 | 1.2 | % | 1,490 | 1.1 | % | 1,722 | 1.3 | % | |||||||||

| Total |

$ | 157,990 | 100.0 | % | $ | 138,014 | 100.0 | % | $ | 131,241 | 100.0 | % | ||||||

Long-lived assets, which are based on geographical designation, were as follows:

| Fiscal Year Ended June 30, | ||||||

| 2010 | 2009 | |||||

| (in thousands) | ||||||

| Long-lived assets: |

||||||

| United States |

$ | 13,593 | $ | 12,160 | ||

| Europe |

2,464 | 2,313 | ||||

| Australia |

121 | 137 | ||||

| Total long-lived assets |

$ | 16,178 | $ | 14,610 | ||

A significant percentage of our revenues have been generated by our international operations and our future growth rates and success are in part dependent on continued growth and success in international markets. As is the case with most international operations, the success and profitability of these operations is subject to numerous risks and uncertainties including exchange rate fluctuations. We do not currently hedge against exchange rate fluctuations. A number of other factors could also have a negative effect on our business and results from operations outside the US, including different regulatory and industry standards and certification requirements, reduced protection for intellectual property rights in some countries, import or export licensing requirements, the complexities of foreign tax jurisdictions and difficulties and costs of staffing and managing our foreign operations.

8

Table of Contents

For the fiscal year ended June 30, 2010, we had one customer that accounted for approximately 10% of our consolidated revenues. The revenue from this customer is a component of our Banking Solutions segment.

Sales and Marketing

As of June 30, 2010, we employed 165 sales and marketing employees worldwide, of whom 94 were focused on the Americas markets, 68 were focused on European markets and 3 were focused on Asia Pacific markets. We market and sell our products directly through our sales force and indirectly through a variety of channel partners and reseller relationships. We market and sell our products domestically and internationally, with an international focus on Europe and Australia. We also maintain an inside sales group which provides a lower-cost channel into maintaining existing customers and expanding our customer base.

Product Development and Engineering

Our product development and engineering organization includes employees as well as offshore development resources who provide a flexible supplement to our internal resources. We have three primary development groups: software engineering, quality assurance and technical writing. We spent $18.9 million, $20.1 million, and $17.4 million on product development and engineering costs in fiscal years 2010, 2009 and 2008. These expenditures include the impact of stock compensation expense.

Our software engineers have substantial experience in advanced software development techniques as well as extensive knowledge of the complex processes involved in business document, payment, and invoicing systems. Our engineers participate in the Microsoft Developer Network, IBM Partner World for Developers, and the Oracle Partner Developer Program. They maintain extensive knowledge of software development trends and best practices. Our technology focuses on providing business solutions utilizing industry standards, providing a path for extendibility and scalability of our products. Security, control and fraud prevention, as well as performance, data management and information reporting, are priorities in the technology we develop and deploy.

Our quality assurance engineers have extensive knowledge of our products and expertise in software quality assurance techniques. The quality assurance team participates in all phases of our product development processes. Members of the quality assurance group make use of both manual and automated software testing techniques to ensure high quality software is being delivered to our customers. The quality assurance group members participate in alpha and beta releases, testing of new product releases as well as customizations to our clients, and provide initial training materials for customer support and service.

Our technical support group provides all product documentation as well as technical support for released products. The technical writers are versed in current document technology and work closely with the software engineers to create and maintain documentation that is clear, current and complete. The technical support engineers are responsible for the analysis of reported software problems and work closely with customer support staff as well as other internal groups to provide the highest quality of support to our customers. The group’s broad knowledge of our products, our technology, and our customers’ infrastructure allows it to rapidly respond to customer support needs.

Backlog

At the end of fiscal year 2010, our backlog was $68.1 million, including deferred revenues of $40.2 million. At the end of fiscal year 2009, our backlog was $83.9 million, including deferred revenues of $43.2 million. We do not believe that backlog is a meaningful indicator of sales that can be expected for any future period, and there can be no assurance that backlog at any point in time will translate into revenue in any specific subsequent period.

9

Table of Contents

Proprietary Rights

We rely upon a combination of patents, copyrights, trademarks and trade-secret laws to establish and maintain proprietary rights in our technology and products. We had 8 active patent applications relating to our products as of June 30, 2010. We have been awarded 18 patents and expect to receive others. The earliest year of expiration for our awarded patents is 2015.

We intend to continue to file patent applications as we develop new technologies. There can be no assurance, however, that our existing patent applications, or any others that may be filed in the future, will issue or will be of sufficient scope and strength to provide meaningful protection of our technology or any commercial advantage to us, or that the issued patents will not be challenged, invalidated or circumvented. In addition, we rely upon a combination of copyright and trademark laws and non-disclosure and other intellectual property contractual arrangements to protect our proprietary rights. Given the rapidly changing nature of the industry’s technology, the creative abilities of our development, marketing and service personnel may be as or more important to our competitive position as the legal protections and rights afforded by patents. We also enter into agreements with our employees and clients that seek to limit and protect our intellectual property and the distribution of proprietary information. However, there can be no assurance that the steps we have taken to protect our intellectual property will be adequate to deter misappropriation of proprietary information, and we may not be able to detect unauthorized use and take appropriate steps to enforce our proprietary rights.

Government Regulation

Although our operations and products have not been subject to any material industry-specific government regulation to-date, some of our existing and potential customers are subject to extensive federal and state regulations. In addition, government regulation in the financial services industry is evolving, particularly with respect to information security, payment technology and payment methodologies and we or our customers may become subject to new or increased regulation in the future. Accordingly, our products and services must be designed to work within the regulatory constraints under which our customers operate.

Employees

As of June 30, 2010, we had 747 full-time employees, 165 of whom were in sales and marketing, 363 of whom were in professional services and customer support, 118 of whom were in development and 101 of whom were in administration and finance. None of our employees are represented by a labor union. We have not experienced any work stoppages and we believe that employee relationships are good. Our future success will depend in part on our continued ability to attract, retain and motivate highly qualified technical and managerial personnel in a highly competitive market.

| Item 1A. | Risk Factors. |

Investing in our common stock involves a high degree of risk. You should carefully consider the risks and uncertainties described below before making an investment decision involving our common stock. The risks and uncertainties described below are not the only ones facing our company. Additional risks and uncertainties may also impair our business operations.

If any of the following risks actually occur, our business, financial condition or results of operations would likely suffer. In that case, the trading price of our common stock could fall, and you may lose all or part of the money you paid to buy our common stock.

10

Table of Contents

Continuing weakness or further deterioration in domestic and global economic conditions could have a significant adverse impact on our business, financial condition and operating results

Our business and operating results could be significantly affected by general economic conditions. The US and global economies have experienced a significant prolonged downturn and prospects for sustained economic recovery remain uncertain. Prolonged economic weakness or a further downturn in the US and global economies could result in a variety of risks to our business, including:

| • | increased volatility in our stock price; |

| • | increased volatility in foreign currency exchange rates; |

| • | delays in, or curtailment of, purchasing decisions by our customers or potential customers either as a result of continuing economic uncertainty or anxiety or as a result of their inability to access the liquidity necessary to engage in purchasing initiatives; |

| • | increased credit risk associated with our customers or potential customers, particularly those that may operate in industries most affected by the economic downturn, such as financial services; and |

| • | impairment of our goodwill or other assets. |

During the fiscal year ended June 30, 2010, we experienced a slight decline in the foreign currency exchange rates associated with the British Pound Sterling which negatively impacted our overall revenue growth. We have observed that, in some cases, closing new business is taking somewhat longer and, in some cases, customer buying decisions are being postponed. To the extent that the current economic downturn worsens or persists, or any of the above risks occur, our business and operating results could be significantly and adversely affected.

Our common stock has experienced and may continue to undergo extreme market price and volume fluctuations

The NASDAQ Global Market often experiences extreme price and volume fluctuations. Broad market fluctuations of this type may adversely affect the market price of our common stock. The stock prices for many companies in the technology sector have experienced wide fluctuations that often have been unrelated to their operating performance. The market price of our common stock has experienced and may continue to undergo extreme fluctuations due to a variety of factors, including:

| • | general and industry-specific business, economic and market conditions; |

| • | changes in or our failure to meet analysts’ or investors’ estimates or expectations; |

| • | actual or anticipated fluctuations in operating results, including those arising as a result of any impairment of goodwill or other intangible assets related to past or future acquisitions; |

| • | public announcements concerning us, including announcements of litigation, our competitors or our industry; |

| • | introductions of new products or services or announcements of significant contracts by us or our competitors; |

| • | acquisitions, divestitures, strategic partnerships, joint ventures, or capital commitments by us or our competitors; |

| • | adverse developments in patent or other proprietary rights; and |

| • | announcements of technological innovations by our competitors. |

Our business and operating results are subject to fluctuations in foreign currency exchange rates

We conduct a substantial portion of our operations outside of the US, principally in Europe and Australia. During the fiscal year ended June 30, 2010, approximately 44% of our revenues and 31% of our operating

11

Table of Contents

expenses, respectively, were attributable to customers or operations located outside of North America. During fiscal 2010, the foreign currency exchange rates of the British Pound to the US Dollar declined slightly. We anticipate that foreign currency exchange rates may continue to fluctuate in the near term. As we experienced in fiscal 2010, continued appreciation of the US Dollar against the British Pound or future appreciation of the US Dollar against the European Euro and Australian Dollar will have the impact of reducing both our revenues and operating expenses.

Our future financial results will be affected by our success in selling new products in a subscription and transaction based revenue model

A substantial portion of our revenues and profitability were historically generated from perpetual software license revenues. We are offering a growing number of our products under a subscription and transaction based revenue model, which we believe has certain advantages over a perpetual license model, including better predictability of revenue.

A subscription and transaction based revenue model typically results in no up-front revenue. Additionally, there can be no assurance that our customers, or the markets in which we compete, will respond favorably to the approach we have taken with our newer offerings. To the extent that our subscription and transaction based offerings do not receive general marketplace acceptance our financial results could be materially and adversely affected.

An increasing number of large and more complex customer contracts, or contracts that involve the delivery of services over contractually committed periods, generally delays the timing of our revenue recognition and, in the short-term, may adversely affect our operating results, financial condition and the market price of our stock

Due to an increasing number of large and more complex customer contracts, particularly in our Banking Solutions segment, we have experienced, and will likely continue to experience, delays in the timing of our revenue recognition. These arrangements generally require significant implementation work, product customization and modification and user acceptance and systems integration testing, resulting in the recognition of revenue over the period of project completion which normally spans several quarters. Delays in revenue recognition on these contracts, including delays that result from customer decisions to halt or otherwise slow down a long-term project due to their own staffing or other challenges, could affect our operating results, financial condition and the market price of our common stock. Similarly, if we are unable to continue to generate new large orders on a regular basis, our business operating results and financial condition could be adversely affected.

We continue to make significant investments in existing products and new product offerings which can adversely affect our operating results; these investments may not be successful

We operate in a highly competitive and rapidly evolving technology environment and believe that it is important to enhance existing product offerings and to develop new product offerings to meet strategic opportunities as they evolve. Our operating results have recently been affected by increases in product development expenses as we have continued to make investments in our hosted, banking and accounts payable automation products, principally Paymode-X. We may at any time, based on product needs or marketplace demands, decide to significantly increase our product development expenditures. We expect to continue to make significant investments in Paymode-X during fiscal year 2011. Investments in existing products and new product offerings can have a negative impact on our operating results, and any existing product enhancements or new product offerings may not be accepted in the marketplace or generate material revenues.

12

Table of Contents

Integration of acquisitions could interrupt our business and our financial condition could be harmed

Part of our operating strategy is to identify and pursue strategic acquisitions that can expand our geographical footprint or complement our existing product functionality. We may in the future continue to acquire or make investments in other businesses, products or technologies. Any acquisition or strategic investment we have made in the past or may make in the future may entail numerous risks, including the following:

| • | difficulties integrating acquired operations, personnel, technologies or products; |

| • | inability to retain key personnel of the acquired company; |

| • | inadequacy of existing operating, financial and management information systems to support the combined organization or new operations; |

| • | write-offs related to impairment of goodwill and other acquired assets; |

| • | entrance into markets in which we have no or limited prior experience or knowledge; |

| • | diversion of management’s focus from our core business concerns; |

| • | dilution to existing stockholders and our earnings per share; |

| • | incurrence of substantial debt; and |

| • | exposure to litigation from third parties, including claims related to intellectual property or other assets acquired or liabilities assumed. |

Any such difficulties encountered as a result of any merger, acquisition or strategic investment could have a material adverse effect on our business, operating results and financial condition.

As a result of our acquisitions, we could be subject to significant future write-offs with respect to intangible assets, which may adversely affect our future operating results

We review our intangible assets periodically for impairment. At June 30, 2010, the carrying value of our goodwill and our other intangible assets was approximately $64.3 million and $31.2 million, respectively. While we reviewed our goodwill and our other intangible assets during the fourth quarter of fiscal year 2010 and concluded that there was no impairment, we could be subject to future impairment charges with respect to these intangible assets or intangible assets arising as a result of acquisitions in future periods. Any such charges, to the extent occurring, would likely have a material adverse effect on our operating results.

Our fixed costs may lead to operating results below analyst or investor expectations if our revenues are below anticipated levels, which could adversely affect the market price of our common stock

A significant percentage of our expenses, particularly personnel and facilities costs, are relatively fixed and based in part on anticipated revenue levels. In recent years, we have experienced slowing growth rates with certain of our licensed software products. During the fiscal year ended June 30, 2010, we experienced a decline in the foreign currency exchange rates applicable to our UK based revenues which negatively impacted our overall revenue growth. A decline in revenues without a corresponding and timely slowdown in expense growth could negatively affect our business. Significant revenue shortfalls in any quarter may cause significant declines in operating results since we may be unable to reduce spending in a timely manner.

Quarterly or annual operating results that are below the expectations of public market analysts could adversely affect the market price of our common stock. Factors that could cause fluctuations in our operating results include the following:

| • | economic conditions, which may affect our customers’ and potential customers’ budgets for information technology expenditures; |

| • | the timing of orders and longer sales cycles; |

13

Table of Contents

| • | the timing of product implementations, which are highly dependent on customers’ resources and discretion; |

| • | the incurrence of costs relating to the integration of software products and operations in connection with acquisitions of technologies or businesses; and |

| • | the timing and market acceptance of new products or product enhancements by either us or our competitors. |

Because of these factors, we believe that period-to-period comparisons of our results of operations are not necessarily meaningful.

Our mix of products and services could have a significant effect on our financial condition, results of operations and the market price of our common stock

The gross margins for our products and services vary considerably. Our software revenues generally yield significantly higher gross margins than do our subscription and transaction, service and maintenance and equipment and supplies revenue streams. During the fiscal year ended June 30, 2010, we experienced a slight increase in our overall software license revenues. If software license revenues were to significantly decline in any future period, or if the mix of our products and services in any given period did not match our expectations, our results of operations and the market price of our common stock could be significantly adversely affected.

We face risks associated with our international operations that could harm our financial condition and results of operations

A significant percentage of our revenues have been generated by our international operations, and our future growth rates and success are in part dependent on our continued growth and success in international markets. We have operations in the US, UK, Australia, France and Germany. As is the case with most international operations, the success and profitability of these operations are subject to numerous risks and uncertainties that include, in addition to the risks our business as a whole faces, the following:

| • | currency exchange rate fluctuations; |

| • | difficulties and costs of staffing and managing foreign operations; |

| • | differing regulatory and industry standards and certification requirements; |

| • | the complexities of foreign tax jurisdictions; |

| • | reduced protection for intellectual property rights in some countries; and |

| • | import or export licensing requirements. |

A significant percentage of our revenues to date have come from our payment and document management offerings and our future performance will depend on continued market acceptance of these solutions

A significant percentage of our revenues to date have come from the license and maintenance of our payment and document management offerings and sales of associated products and services. Any significant reduction in demand for our payment and document management offerings could have a material adverse effect on our business, operating results and financial condition. Our future performance could depend on the following factors:

| • | retaining our software maintenance customer base, which is a significant source of our recurring revenue; |

| • | continued market acceptance of our payment and document management offerings; |

| • | our ability to introduce enhancements to meet the market’s evolving needs for secure payments and cash management solutions; and |

| • | acceptance of software solutions offered on a SaaS basis. |

14

Table of Contents

A growing number of our customer arrangements involve selling our products and services on a SaaS basis, which may have the effect of delaying revenue recognition and increasing development or start-up expenses

An increasing number of our customer arrangements involve offering certain of our products and services on a SaaS basis. Such arrangements typically include a contractually defined service period as well as performance criteria that our products or services are required to meet over the duration of the service period. Arrangements entered into on a SaaS basis generally delay the timing of revenue recognition and often require the incurrence of up-front costs, which can be significant. We are continuing to make investments in many of our offerings, particularly Paymode-X, and there can be no assurance that these products will ultimately gain broad market acceptance. Additionally, we might be unable to consistently maintain the performance requirements or service levels called for under any such arrangements. Any such events, to the extent occurring, could have a material and adverse effect on our operating results.

A growing portion of our revenue is derived from subscription and transaction based revenue arrangements

A growing portion of our revenue is being derived from subscription and transaction based arrangements. We believe that these arrangements have several advantages over perpetual license arrangements, including better predictability of revenue. However, there are also certain risks inherent with these transactions. For example, there is a risk that customers may elect not to renew these arrangements upon expiration or that they may aggressively attempt to renegotiate pricing or other significant contractual terms, either at or prior to the point of renewal, based on economic conditions that exist at that time. Further, in respect of our hosted and SaaS product offerings, customers often negotiate contractual termination rights in the event of a contractual breach by us which, to the extent occurring, might permit the customer to exit the contract prior to the end of its term, generally without additional compensation to us. Our future revenue and overall growth rates depend significantly upon customer retention. To the extent we were unable to achieve desired customer retention rates, or in the event we were unable to retain or renew customers on favorable economic terms, our business, operating results and financial condition could be adversely affected.

Our future financial results will depend on our ability to manage growth effectively

Our ability to manage growth effectively will depend in part on our ability to continue to enhance our operating, financial and management information systems. If we are unable to manage growth effectively, the quality of our services, our ability to retain key personnel and our business, operating results and financial condition could be materially adversely affected.

We face significant competition in our targeted markets, including competition from companies with significantly greater resources

In recent years, we have encountered increasing competition in our targeted markets. We compete with a wide range of companies ranging from small start-up enterprises with limited resources, which compete principally on the basis of technology features or specific customer relationships, to large companies which can leverage significant customer bases and financial resources. Given the size and nature of the markets we target, the implementation of our growth strategy and our success in competing for market share is dependent on our ability to grow our sales and marketing capabilities and maintain an appropriate level of financial resources.

We depend on key employees who are skilled in e-commerce, payment, cash and document management and invoice presentment methodology and Internet and other technologies

Our success depends upon the efforts and abilities of our executive officers and key technical and sales employees who are skilled in e-commerce, payment methodology and regulation, and Internet, database and network technologies. Our key employees are in high demand within the marketplace and many competitors,

15

Table of Contents

customers and industry organizations are able to offer considerably higher compensation packages than we currently provide. The loss of one or more of these individuals could have a material adverse effect on our business. In addition, we currently do not maintain “key man” life insurance policies on any of our employees. While some of our executive officers have employment or retention agreements with us, the loss of the services of any of our executive officers or other key employees could have a material adverse effect on our business, operating results and financial condition.

Increased competition may result in price reductions and decreased demand for our products

The markets in which we compete are intensely competitive and characterized by rapid technological change. Some competitors in our targeted markets have longer operating histories, significantly greater financial, technical, and marketing resources, greater brand recognition and a larger installed customer base than we do. We expect to face additional competition as other established and emerging companies enter the markets we address. In addition, current and potential competitors may make strategic acquisitions or establish cooperative relationships to expand their product offerings and to offer more comprehensive solutions. This growing competition may result in price reductions of our products and services, reduced revenues and gross margins and loss of market share, any one of which could have a material adverse effect on our business, operating results and financial condition.

Our success depends on our ability to develop new and enhanced products, services and strategic partner relationships

The markets in which we compete are subject to rapid technological change and our success is dependent on our ability to develop new and enhanced products, services and strategic partner relationships that meet evolving market needs. Trends that could have a critical impact on us include:

| • | evolving industry standards, mandates and laws, such as those mandated by the National Automated Clearing House Association and the Association for Payment Clearing Services; |

| • | rapidly changing technology, which could cause our software to become suddenly outdated or could require us to make our products compatible with new database or network systems; |

| • | developments and changes relating to the Internet that we must address as we maintain existing products and introduce any new products; and |

| • | the loss of any of our key strategic partners who serve as a valuable network from which we can leverage industry expertise and respond to changing marketplace demands. |

There can be no assurance that technological advances will not cause our products to become obsolete or uneconomical. If we are unable to develop and introduce new products or enhancements to existing products in a timely and successful manner, our business, operating results and financial condition could be materially adversely affected. Similarly, if our new products do not receive general marketplace acceptance, or if the sales cycle of any of our new products significantly delays the timing of revenue recognition, our results could be negatively affected.

Our products could be subject to future legal or regulatory actions, which could have a material adverse effect on our operating results

Our software products and SaaS offerings facilitate the transmission of business documents and information including, in some cases, confidential financial data related to payments, invoices and cash management. Our web-based software products, and certain of our SaaS offerings, transmit this data electronically. While we believe that all of our product and service offerings comply with current regulatory and security requirements, there can be no assurance that future legal or regulatory actions will not impact our product and service offerings. To the extent that current or future regulatory or legal developments mandate a change in any of our products or

16

Table of Contents

services, require us to comply with any industry specific licensing or compliance requirements or alter the demand for or the competitive environment of our products and services, we might not be able to respond to such requirements in a timely or cost effective manner. If this were to occur, our business, operating results and financial condition could be materially adversely affected.

Any unanticipated performance problems or bugs in our product offerings could have a material adverse effect on our future financial results

If the products that we offer and continue to introduce do not sustain marketplace acceptance, our future financial results could be adversely affected. Since certain of our offerings are still in early stages of adoption and since most of our products are continually being enhanced or further developed in response to general marketplace demands, any unanticipated performance problems or bugs that we have not been able to detect could result in additional development costs, diversion of technical and other resources from our other development efforts, negative publicity regarding us and our products, harm to our customer relationships and exposure to potential liability claims. In addition, if our products do not enjoy wide commercial success, our long-term business strategy will be adversely affected, which could have a material adverse effect on our business, operating results and financial condition.

Catastrophic events may disrupt our business

We are a highly automated business and we rely on our network infrastructure, various software applications and many internal technology systems and data networks for our customer support, development, sales and marketing and accounting and finance functions. Further, our SaaS offerings rely on certain of these systems from the perspective of the ongoing provision of services to our customers and potential customers. A disruption or failure of these systems in the event of a natural disaster, telecommunications failure, cyber-attack, war, terrorist attack, or other catastrophic event could cause system interruptions, reputational harm, delays in product development, breaches of data security and loss of critical data. Such an event could also prevent us from fulfilling our customer orders or maintaining certain service level requirements, particularly in respect of our SaaS offerings. While we have developed certain disaster recovery plans and backup systems to reduce the potentially adverse effect of such events, a catastrophic event that resulted in the destruction or disruption of any of our data centers or our critical business or information technology systems could severely affect our ability to conduct normal business operations and, as a result, our business, operating results and financial condition could be adversely affected.

Security breaches or computer viruses could harm our business by disrupting the delivery of services, damaging our reputation, or resulting in material liability to us

Our products, particularly our SaaS or web-based offerings, may be vulnerable to unauthorized access, computer viruses and other disruptive problems. In the course of providing services to our customers, we may collect, store, process or transmit sensitive and confidential information. A security breach affecting us could damage our reputation and result in the loss of customers and potential customers. Such an event could also result in material financial liability to us.

Privacy, security, and compliance concerns have continued to increase as technology has evolved to facilitate e-commerce. We may need to spend significant capital or other resources to ensure ongoing protection against the threat of security breaches or to alleviate problems caused by security concerns. Additionally, computer viruses could infiltrate our systems and disrupt our business and our provision of services, particularly our SaaS offerings. Any such event could have an adverse effect on our business, operating results, and financial condition.

We could incur substantial costs resulting from warranty claims or product liability claims

Our product agreements typically contain provisions that afford customers a degree of warranty protection in the event that our products fail to conform to written specifications. These agreements typically contain

17

Table of Contents

provisions intended to limit the nature and extent of our risk of warranty and product liability claims. A court, however, might interpret these terms in a limited way or conclude that part or all of these terms were unenforceable. Furthermore, some of our agreements are governed by non-US law, and there is a risk that foreign law might provide us less or different protection. While we maintain general liability insurance, including coverage for errors and omissions, we cannot be sure that our existing coverage will continue to be available on reasonable terms or will be available in amounts sufficient to cover one or more large claims.

Our products are used to facilitate the transmission of sensitive business documents and other confidential data related to payments, cash management and invoices. Further, some of our products facilitate the transfer of cash or transmit instructions that initiate cash transfer. Although we have not experienced any material warranty or product liability claims to date, a warranty or product liability claim, whether or not meritorious, could result in substantial costs and a diversion of management’s attention and our resources, which could have an adverse effect on our business, operating results and financial condition.

We could be adversely affected if we are unable to protect our proprietary technology and could be subject to litigation regarding our intellectual property rights, causing serious harm to our business

We rely upon a combination of patent, copyright and trademark laws and non-disclosure and other intellectual property contractual arrangements to protect our proprietary rights. However, we cannot assure you that our patents, pending applications for patents that may issue in the future, or other intellectual property will be of sufficient scope and strength to provide meaningful protection to our technology or any commercial advantage to us, or that the patents will not be challenged, invalidated or circumvented. We enter into agreements with our employees and customers that seek to limit and protect the distribution of proprietary information. Despite our efforts to safeguard and maintain our proprietary rights, there can be no assurance that such rights will remain protected or that we will be able to detect unauthorized use and take appropriate steps to enforce our intellectual property rights.

In recent years, there has been significant litigation in the United States involving patents and other intellectual property rights. We may be a party to litigation in the future to protect our intellectual property rights or as a result of an alleged infringement of the intellectual property rights of others. Any such claims, whether or not meritorious, could require us to spend significant sums in litigation, pay damages, delay product implementations, develop non-infringing intellectual property or acquire licenses to intellectual property that is the subject of the infringement claim. These claims could have a material adverse effect on our business, operating results and financial condition.

We engage off-shore development resources which may not be successful and which may put our intellectual property at risk

In order to optimize our research and development capabilities and to meet development timeframes, we contract with off-shore third party vendors in India and elsewhere for certain development activities. While our experience to date with these resources has been positive, there are a number of risks associated with off-shore development activities that include, but are not limited to, the following:

| • | less efficient and less accurate communication and information flow as a consequence of time, distance and language barriers between our primary development organization and the off-shore resources, resulting in delays or deficiencies in development efforts; |

| • | disruption due to political or military conflicts around the world; |

| • | misappropriation of intellectual property from departing personnel, which we may not readily detect; and |

| • | currency exchange rate fluctuations that could adversely impact the cost advantages intended from these agreements. |

To the extent that these or unforeseen risks occur, our operating results and financial condition could be adversely impacted.

18

Table of Contents

Some anti-takeover provisions contained in our charter and under Delaware law could hinder a takeover attempt

We are subject to the provisions of Section 203 of the General Corporation Law of the State of Delaware prohibiting, under some circumstances, publicly-held Delaware corporations from engaging in business combinations with some stockholders for a specified period of time without the approval of the holders of substantially all of our outstanding voting stock. Such provisions could delay or impede the removal of incumbent directors and could make more difficult a merger, tender offer or proxy contest involving us, even if such events could be beneficial, in the short-term, to the interests of our stockholders. In addition, such provisions could limit the price that some investors might be willing to pay in the future for shares of our common stock. Our certificate of incorporation and bylaws contain provisions relating to the limitations of liability and indemnification of our directors and officers, dividing our board of directors into three classes of directors serving three-year terms and providing that our stockholders can take action only at a duly called annual or special meeting of stockholders.

We may incur significant costs from class action litigation as a result of expected volatility in our common stock

In the past, companies that have experienced market price volatility of their stock have been the targets of securities class action litigation. In August 2001, we were named as a party in one of the so-called “laddering” securities class action suits relating to the underwriting of our initial public offering. In April 2008, we acquired Optio Software, which is also a party in a “laddering” securities class action suit. We could incur substantial costs and experience a diversion of our management’s attention and resources in connection with any such litigation, which could have a material adverse effect on our business, financial condition and results of operations.

| Item 1B. | Unresolved Staff Comments. |

There are no material unresolved written comments from the staff of the SEC regarding our periodic or current reports received not less than 180 days before the end of our fiscal year to which this Form 10-K relates.

| Item 2. | Properties. |

As of June 30, 2010, we lease approximately 60,000 square feet of office space at our corporate headquarters in Portsmouth, New Hampshire under a lease that expires in 2022. We also occupy approximately 71,000 square feet of leased domestic offices in Portland, Maine; Alpharetta, Georgia; Great Neck, New York and Morrisville, North Carolina.

We own approximately 16,000 square feet of office space in Reading, England, and this facility serves as our European headquarters. Additionally, we lease approximately 23,000 square feet of office space throughout the UK. We also lease approximately 5,000 square feet of office space in Melbourne and Sydney, Australia.

Our New Hampshire facility serves as our corporate headquarters and is used by employees associated with all of our operating segments in addition to our management, administrative, sales and marketing and customer support teams. Our Portland, Maine facility is used by personnel who support our Paymode-X solution, which is a component of our outsourced solutions segment. Our New York facility is used to support the product development initiatives of all of our operating segments. Our North Carolina and Georgia facilities, and all of our European facilities, are used predominantly by personnel associated with our payments and transactional documents operating segment. Our Australian facilities are used by personnel associated with both our payment and transactional documents and banking solutions operating segments.

| Item 3. | Legal Proceedings. |

On August 10, 2001, a class action complaint was filed against the Company in the United States District Court for the Southern District of New York: Paul Cyrek v. Bottomline Technologies, Inc.; Daniel M. McGurl;

19

Table of Contents

Robert A. Eberle; FleetBoston Robertson Stephens, Inc.; Deutsche Banc Alex Brown Inc.; CIBC World Markets; and J.P. Morgan Chase & Co. A consolidated amended class action complaint, In re Bottomline Technologies Inc. Initial Public Offering Securities Litigation, was filed on April 20, 2002.

On November 13, 2001, a class action complaint was filed against Optio in the United States District Court for the Southern District of New York: Kevin Dewey v. Optio Software, Inc.; Merrill Lynch, Pierce, Fenner & Smith, Inc.; Bear, Stearns & Co., Inc.; Fleetboston Robertson Stephens, Inc.; Deutsche Bank Securities, Inc.; Dain Rauscher Inc.; U.S. Bancorp Piper Jaffray, Inc.; C. Wayne Cape; and F. Barron Hughes. A consolidated amended class action complaint, In re Optio Software, Inc. Initial Public Offering Securities Litigation, was filed on April 22, 2002.

The amended complaints filed in both the actions against the Company and Optio assert claims under Sections 11, 12(2) and 15 of the Securities Act of 1933, as amended, and Sections 10(b) and 20(a) of the Securities Exchange Act of 1934, as amended. The amended complaints assert, among other things, that the descriptions in the Company’s and Optio’s prospectuses for their initial public offerings were materially false and misleading in describing the compensation to be earned by the underwriters of the offerings, and in not describing certain alleged arrangements among underwriters and initial purchasers of the common stock from the underwriters. The amended complaints seek damages (or, in the alternative, tender of the plaintiffs’ and the class’s common stock and rescission of their purchases of the common stock purchased in the initial public offering), costs, attorneys’ fees, experts’ fees and other expenses.

In July 2002, the Company and Optio joined in an omnibus motion to dismiss, which challenged the legal sufficiency of plaintiffs’ claims. The motion was filed on behalf of hundreds of issuer and individual defendants named in similar lawsuits. On February 19, 2003, the court issued an order denying the motion to dismiss as to Bottomline and denying in part the motion to dismiss as to Optio. In addition, in October 2002, Daniel M. McGurl, Robert A. Eberle, C. Wayne Cape and F. Barron Hughes were dismissed from this case without prejudice. Both Bottomline and Optio authorized the negotiation of a settlement of the pending claims, and the parties negotiated a settlement, which was subject to approval by the court. On August 31, 2005, the court issued an order preliminarily approving the settlement. On December 5, 2006, the United States Court of Appeals for the Second Circuit overturned the District Court’s certification of the class of plaintiffs who are pursuing the claims that would be settled in the settlement against the underwriter defendants. Plaintiffs filed a Petition for Rehearing and Rehearing En Banc with the Second Circuit on January 5, 2007 in response to the Second Circuit’s decision. On April 6, 2007, plaintiffs’ Petition for Rehearing of the Second Circuit’s decision was denied. On June 25, 2007, the District Court signed an order terminating the settlement. On September 27, 2007, plaintiffs filed a motion for class certification in certain designated “focus cases” in the District Court. That motion was withdrawn. Neither Bottomline nor Optio’s cases are part of the designated focus case group. On November 13, 2007, the issuer defendants in the designated focus cases filed a motion to dismiss the second consolidated amended class action complaints that were filed in those cases. On March 26, 2008, the District Court issued an Opinion and Order denying, in large part, the motions to dismiss the amended complaints in these focus cases. On April 2, 2009, the plaintiffs filed a motion for preliminary approval of a new proposed settlement between plaintiffs, the underwriter defendants, the issuer defendants and the insurers for the issuer defendants. On June 10, 2009, the Court issued an opinion preliminarily approving the proposed settlement, and scheduling a settlement fairness hearing for September 10, 2009. On August 25, 2009, the plaintiffs filed a motion for final approval of the proposed settlement, approval of the plan of distribution of the settlement fund, and certification of the settlement classes. The settlement fairness hearing was held on September 10, 2009. On October 5, 2009, the Court issued an opinion granting plaintiffs’ motion for final approval of the settlement, approval of the plan of distribution of the settlement fund, and certification of the settlement classes. An order and final judgment was entered on November 25, 2009. Various notices of appeal of the Court’s order have been filed.

The Company, and its subsidiary Optio, intend to vigorously defend themselves in these actions. Bottomline does not currently believe that the outcome of these proceedings will have a material adverse impact on its financial condition, results of operations or cash flows.

20

Table of Contents

| Item 4. | [Removed and Reserved] |

Executive Officers and Other Key Employees of the Registrant

Our executive officers and other key employees and their respective ages as of August 31, 2010, are as follows:

| Name |

Age | Positions | ||

| Robert A. Eberle |

49 | President, Chief Executive Officer and Director | ||

| Kevin M. Donovan |

40 | Chief Financial Officer and Treasurer | ||

| Nigel K. Savory |

43 | Managing Director, Europe | ||

| Richard A. Bell |

45 | Senior Vice President and General Manager, Financial Process Solutions, North America | ||

| Eric A. Campbell |

53 | Chief Technology Officer | ||

| Paul J. Fannon |

42 | Group Sales Director, Europe | ||

| Thomas D. Gaillard |

47 | Senior Vice President and General Manager, Transactional Services, North America | ||

| Marcus G.R. Hughes |

52 | Director of Global Marketing | ||

| Michael Lane |

47 | Senior Vice President and General Manager, Global Banking and Financial Services | ||

| Andrew Mintzer |

48 | Senior Vice President, Product Strategy and Delivery | ||

| Chris W. Peck |

45 | Managing Director, Banking Europe |

Robert A. Eberle has served as a director since September 2000 and as Chief Executive Officer since November 2006. Mr. Eberle has served as President since August 2004.

Kevin M. Donovan has served as Chief Financial Officer since August 2004 and as Treasurer since May 2001.

Nigel K. Savory has served as Managing Director, Europe since December 2003.

Richard A. Bell has served as Senior Vice President and General Manager, Financial Process Solutions, North America since September 2005.

Eric A. Campbell has served as Chief Technology Officer since May 2000.

Paul J. Fannon has served as Group Sales Director, Europe since October 2008. From December 2003 through October 2008, Mr. Fannon served as Managing Director, Transactional Services Europe.

Thomas D. Gaillard has served as Senior Vice President and General Manager, Transactional Services, North America since July 2003.

Marcus G.R. Hughes has served as Director of Global Marketing since March 2009. From January 2009 to March 2009, Mr. Hughes served as a consultant to the Company. From March 2007 to January 2009, Mr. Hughes served as Managing Director, Global Head of Trade Services at Banco Santander. From May 2002 to March 2007, Mr. Hughes served as Head of Banking, Europe for Bottomline Technologies Europe.

Michael Lane has served as Senior Vice President and General Manager, Global Banking and Financial Services since March 2008. From May 2005 to February 2008, Mr. Lane served as Managing Director, Financial Services for Pegasystems, Inc.

Andrew Mintzer has served as Senior Vice President, Product Strategy and Delivery since November 2007. From June 2003 to November 2007, Mr. Mintzer served as Vice President of Development.

Christopher W. Peck has served as Managing Director, Banking Europe since October 2008. From July 2003 through October 2008, Mr. Peck served as Managing Director, Group Sales Europe.

21

Table of Contents

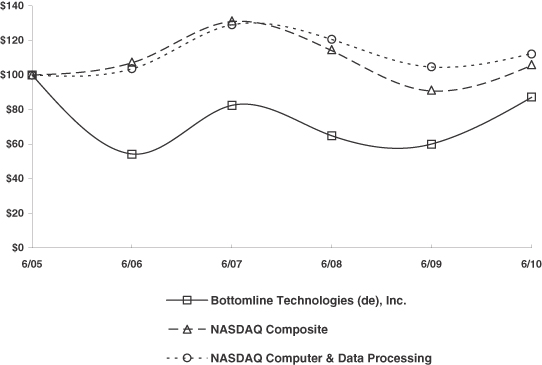

| Item 5. | Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities. |

Our common stock is traded on The NASDAQ Global Market under the symbol EPAY. The following table sets forth, for the periods indicated, the high and low sale prices of our common stock, as quoted on The NASDAQ Global Market.

| Period |

High | Low | ||||

| Fiscal 2009 |

||||||

| First quarter |

$ | 13.00 | $ | 9.61 | ||

| Second quarter |

$ | 10.46 | $ | 4.46 | ||

| Third quarter |

$ | 7.67 | $ | 4.66 | ||

| Fourth quarter |

$ | 10.31 | $ | 6.43 | ||

| Fiscal 2010 |

||||||

| First quarter |

$ | 13.34 | $ | 8.26 | ||

| Second quarter |

$ | 18.50 | $ | 12.07 | ||

| Third quarter |

$ | 18.49 | $ | 15.25 | ||

| Fourth quarter |