UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, DC 20549

FORM 10-K

(Mark One)

| ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the fiscal year ended: April 30 , 2023

OR

| TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the transition period from _________ to _________

Commission file number 001-11507

(Exact name of Registrant as specified in its charter)

| State or other jurisdiction of incorporation or organization | I.R.S. Employer Identification No. | |||||||

| Address of principal executive offices | Zip Code | |||||||

( | ||

| Registrant’s telephone number including area code | ||

| Securities registered pursuant to Section 12(b) of the Act: Title of each class | Trading Symbol | Name of each exchange on which registered | ||||||

| Securities registered pursuant to Section 12(g) of the Act: | ||||||||

| None | ||||||||

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes x No o

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

Yes o No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No o

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes x No o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Accelerated filer o | |||||

Non-accelerated filer o | |||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. o

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. x

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. o

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). o

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes o No x

The aggregate market value of the voting stock held by non-affiliates of the registrant, computed by reference to the closing price as of the last business day of the registrant’s most recently completed second fiscal quarter, October 31, 2022, was approximately $1,821 million. The registrant has no non-voting common stock.

The number of shares outstanding of the registrant’s Class A and Class B Common Stock as of May 31, 2023 was 46,255,091 and 9,026,142 respectively.

DOCUMENTS INCORPORATED BY REFERENCE

JOHN WILEY & SONS, INC. AND SUBSIDIARIES

FORM 10-K

FOR THE FISCAL YEAR ENDED APRIL 30, 2023

INDEX

| PAGE | ||||||||

2

Cautionary Notice Regarding Forward-Looking Statements “Safe Harbor” Statement under the Private Securities Litigation Reform Act of 1995:

This report contains “forward-looking statements” within the meaning of the safe harbor provisions of the Private Securities Litigation Reform Act of 1995 concerning our business, consolidated financial condition and results of operations. The Securities and Exchange Commission (SEC) encourages companies to disclose forward-looking information so that investors can better understand a company’s prospects and make informed investment decisions. Forward-looking statements are subject to risks and uncertainties, many of which are outside our control, which could cause actual results to differ materially from these statements. Therefore, you should not rely on any of these forward-looking statements. Forward-looking statements can be identified by such words as “anticipates,” “believes,” “plan,” “assumes,” “could,” “should,” “estimates,” “expects,” “intends,” “potential,” “seek,” “predict,” “may,” “will” and similar references to future periods. All statements other than statements of historical facts included in this report regarding our strategies, prospects, financial condition, operations, costs, plans and objectives are forward-looking statements. Examples of forward-looking statements include, among others, statements we make regarding our fiscal year 2024 outlook, anticipated restructuring charges and savings, operations, performance, and financial condition. Reliance should not be placed on forward-looking statements, as actual results may differ materially from those described in any forward-looking statements. Any such forward-looking statements are based upon many assumptions and estimates that are inherently subject to uncertainties and contingencies, many of which are beyond our control, and are subject to change based on many important factors. Such factors include, but are not limited to (i) the level of investment by Wiley in new technologies and products; (ii) subscriber renewal rates for our journals; (iii) the financial stability and liquidity of journal subscription agents; (iv) the consolidation of book wholesalers and retail accounts; (v) the market position and financial stability of key retailers; (vi) the seasonal nature of our educational business and the impact of the used book market; (vii) worldwide economic and political conditions; (viii) our ability to protect our copyrights and other intellectual property worldwide; (ix) our ability to successfully integrate acquired operations and realize expected opportunities; (x) the ability to realize operating savings over time and in fiscal year 2024 in connection with our multiyear Business Optimization Program and our Fiscal Year 2023 Restructuring Program; and (xi) other factors detailed from time to time in our filings with the SEC. We undertake no obligation to update or revise any such forward-looking statements to reflect subsequent events or circumstances.

Please refer to Part I, Item 1A, “Risk Factors,” of our Annual Report on Form 10-K for important factors that we believe could cause actual results to differ materially from those in our forward-looking statements. Any forward-looking statement made by us in this report is based only on information currently available to us and speaks only as of the date on which it is made. We undertake no obligation to publicly update any forward-looking statement, whether written or oral, that may be made from time to time, whether as a result of new information, future developments or otherwise.

Non-GAAP Financial Measures:

We present financial information that conforms to Generally Accepted Accounting Principles in the United States of America (US GAAP). We also present financial information that does not conform to US GAAP, which we refer to as non-GAAP.

In this report, we may present the following non-GAAP performance measures:

•Adjusted Earnings Per Share (Adjusted EPS);

•Free Cash Flow less Product Development Spending;

•Adjusted Revenue;

•Adjusted Contribution to Profit and margin;

•Adjusted Operating Income and margin;

•Adjusted Income Before Taxes;

•Adjusted Income Tax Provision;

•Adjusted Effective Tax Rate;

•EBITDA, Adjusted EBITDA and margin;

•Organic revenue; and

•Results on a constant currency basis.

3

Management uses these non-GAAP performance measures as supplemental indicators of our operating performance and financial position as well as for internal reporting and forecasting purposes, when publicly providing our outlook, to evaluate our performance and calculate incentive compensation. We present these non-GAAP performance measures in addition to US GAAP financial results because we believe that these non-GAAP performance measures provide useful information to certain investors and financial analysts for operational trends and comparisons over time. The use of these non-GAAP performance measures may also provide a consistent basis to evaluate operating profitability and performance trends by excluding items that we do not consider to be controllable activities for this purpose.

The performance metric used by our chief operating decision maker to evaluate performance of our reportable segments is Adjusted Contribution to Profit. We present both Adjusted Contribution to Profit and Adjusted EBITDA for each of our reportable segments as we believe Adjusted EBITDA provides additional useful information to certain investors and financial analysts for operational trends and comparisons over time. It removes the impact of depreciation and amortization expense, as well as presents a consistent basis to evaluate operating profitability and compare our financial performance to that of our peer companies and competitors.

For example:

•Adjusted EPS, Adjusted Revenue, Adjusted Contribution to Profit, Adjusted Operating Income, Adjusted Income Before Taxes, Adjusted Income Tax Provision, Adjusted Effective Tax Rate, Adjusted EBITDA, and organic revenue (excluding acquisitions) provide a more comparable basis to analyze operating results and earnings and are measures commonly used by shareholders to measure our performance.

•Free Cash Flow less Product Development Spending helps assess our ability, over the long term, to create value for our shareholders as it represents cash available to repay debt, pay common stock dividends, and fund share repurchases and acquisitions.

•Results on a constant currency basis remove distortion from the effects of foreign currency movements to provide better comparability of our business trends from period to period. We measure our performance excluding the impact of foreign currency (or at constant currency), which means that we apply the same foreign currency exchange rates for the current and equivalent prior period.

In addition, we have historically provided these or similar non-GAAP performance measures and understand that some investors and financial analysts find this information helpful in analyzing our operating margins and net income, and in comparing our financial performance to that of our peer companies and competitors. Based on interactions with investors, we also believe that our non-GAAP performance measures are regarded as useful to our investors as supplemental to our US GAAP financial results, and that there is no confusion regarding the adjustments or our operating performance to our investors due to the comprehensive nature of our disclosures. We have not provided our fiscal year 2024 outlook for the most directly comparable US GAAP financial measures, as they are not available without unreasonable effort due to the high variability, complexity, and low visibility with respect to certain items, including restructuring charges and credits, gains and losses on foreign currency, and other gains and losses. These items are uncertain, depend on various factors, and could be material to our consolidated results computed in accordance with US GAAP.

Non-GAAP performance measures do not have standardized meanings prescribed by US GAAP and therefore may not be comparable to the calculation of similar measures used by other companies and should not be viewed as alternatives to measures of financial results under US GAAP. The adjusted metrics have limitations as analytical tools, and should not be considered in isolation from, or as a substitute for, US GAAP information. It does not purport to represent any similarly titled US GAAP information and is not an indicator of our performance under US GAAP. Non-GAAP financial metrics that we present may not be comparable with similarly titled measures used by others. Investors are cautioned against placing undue reliance on these non-GAAP measures.

4

PART I

Item 1. Business

The Company, founded in 1807, was incorporated in the state of New York on January 15, 1904. Throughout this report, when we refer to “Wiley,” the “Company,” “we,” “our,” or “us,” we are referring to John Wiley & Sons, Inc. and all of our subsidiaries, except where the context indicates otherwise.

Please refer to Part II, Item 8, “Financial Statements and Supplementary Data,” for financial information about the Company and its subsidiaries, which is incorporated herein by reference. Also, when we cross reference to a “Note,” we are referring to our “Notes to Consolidated Financial Statements,” in Part II, Item 8, “Financial Statements and Supplementary Data” unless the context indicates otherwise.

Wiley is a global leader in scientific research and career-connected education, unlocking human potential by enabling discovery, powering education, and shaping workforces. For over 200 years, Wiley has fueled the world’s knowledge ecosystem. Today, our high-impact content, platforms, and services help researchers, learners, institutions, and corporations achieve their goals in an ever-changing world. Wiley is a predominantly digital company with approximately 85% of revenue generated by digital products and tech-enabled services. For the year ended April 30, 2023, approximately 57% of our revenue is recurring which includes revenue that is contractually obligated or set to recur with a high degree of certainty.

We have reorganized our Education lines of business into two new customer-centric segments. The Academic segment addresses the university customer group and includes Academic Publishing and University Services. The Talent segment addresses the corporate customer group and is focused on delivering training, sourcing, and upskilling solutions. Prior period segment results have been revised to the new segment presentation. There were no changes to our consolidated financial results. Our new segment reporting structure consists of three reportable segments, as well as a Corporate expense category (no change), which includes certain costs that are not allocated to the reportable segments:

•Research includes Research Publishing and Research Solutions, and no changes were made as a result of this realignment;

•Academic includes the Academic Publishing and University Services lines. Academic Publishing is the combination of the former Education Publishing line and professional publishing offerings;

•Talent is the combination of the former Talent Development line, and our assessments (corporate training) and corporate learning offerings.

Through the Research segment, we provide peer-reviewed scientific, technical, and medical (STM) publishing, content platforms, and related services to academic, corporate, and government customers, academic societies, and individual researchers. The Academic segment provides scientific, professional, and education print and digital books, digital courseware, and test preparation services, as well as engages in the comprehensive management of online degree programs for universities. The Talent segment services include sourcing, training, and preparing aspiring students and professionals to meet the skill needs of today’s technology careers and placing them with large companies and government agencies. It also includes assessments (corporate training) and corporate learning offerings. Our operations are primarily located in the United States (US), United Kingdom (UK), India, Sri Lanka, and Germany. In the year ended April 30, 2023, approximately 45% of our consolidated revenue was from outside the US.

Wiley’s business strategies are tightly aligned with long term growth trends, including open research, career-connected education, and workforce optimization. Research strategies include driving publishing output to meet the global demand for peer-reviewed research and expanding platform and service offerings for corporations and societies. Education strategies include expanding online degree programs and driving online enrollment for university partners, scaling digital content and courseware, and expanding IT talent placement and reskilling programs for corporate partners.

5

Business Segments

We report financial information for the following reportable segments, as well as a Corporate expense category, which includes certain costs that are not allocated to the reportable segments:

•Research

•Academic

•Talent

Research:

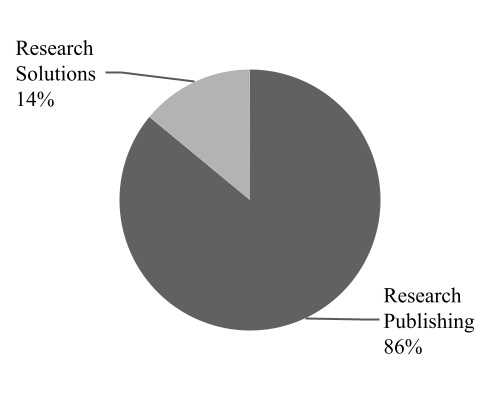

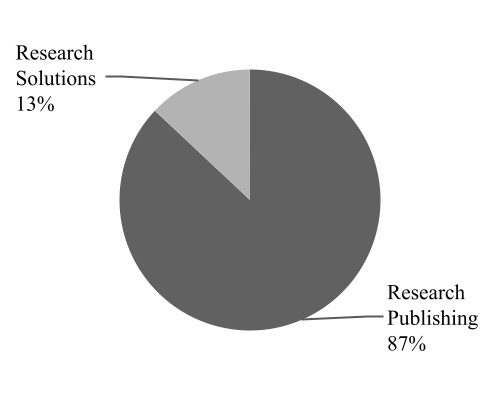

Research’s mission is to support researchers, professionals and learners in the discovery and use of research knowledge to help them achieve their goals. Research provides scientific, technical, medical, and scholarly journals, as well as related content and services, to academic, corporate, and government libraries, learned societies, and individual researchers and other professionals. Journal publishing categories include the physical sciences and engineering, health sciences, social sciences and humanities, and life sciences. Research also includes Atypon Systems, Inc. (Atypon), a publishing software and service provider that enables scholarly and professional societies and publishers to deliver, host, enhance, market, and manage their content on the web through the Literatum™ platform. Research customers include academic, corporate, government, and public libraries, funders of research, researchers, scientists, clinicians, engineers and technologists, scholarly and professional societies, and students and professors. Research products are sold and distributed globally through multiple channels, including research libraries and library consortia, independent subscription agents, direct sales to professional society members, and other customers. Publishing centers include Australia, China, Germany, India, the UK, and the US. Research revenue accounted for approximately 54% of our consolidated revenue in the year ended April 30, 2023, with a 34.9% Adjusted EBITDA margin. See Part II, Item 7, "Management’s Discussion and Analysis of Financial Condition and Results of Operations" in the section "Segment Operating Results" of this Annual Report on Form 10-K for further details. Approximately 95% of Research revenue is generated by digital and online products, and services.

Research revenue by product type includes Research Publishing and Research Solutions. The graphs below present revenue by product type for the years ended April 30, 2023 and 2022:

2023

2022

Key growth strategies for the Research segment include evolving and developing new licensing models for our institutional customers (“pay to read and publish”), developing new open access journals and revenue streams (“pay to publish”), focusing resources on high-growth and emerging markets, and developing new digital products, services, and workflow solutions to meet the needs of researchers, authors, societies, and corporate customers.

Research Publishing

Research Publishing generates the majority of its revenue from contracts with its customers in the following revenue streams:

•Journal Subscriptions (“pay to read”), Open Access (“pay to publish”), and Transformational Models (“pay to read and publish”); and

•Licensing, Backfiles, and Other.

6

Journal Subscriptions, Open Access, and Transformational Models

As of April 30, 2023, we publish over 1,900 academic research journals. We sell journal subscriptions directly to thousands of research institutions worldwide through our sales representatives, indirectly through independent subscription agents, through promotional campaigns, and through memberships in professional societies for those journals that are sponsored by societies. Journal subscriptions are primarily licensed through contracts for digital content available online through our Wiley Online Library platform. Contracts are negotiated by us directly with customers or their subscription agents. Subscription periods typically cover calendar years. Subscription revenue is generally collected in advance. Approximately 53% of Journal Subscription revenue is derived from publishing rights owned by Wiley. Long-term publishing alliances also play a major role in Research Publishing’s success. Approximately 47% of Journal Subscriptions revenue is derived from publication rights that are owned by professional societies and other publishing partners such as charitable organizations or research institutions, and are published by us pursuant to long-term contracts or owned jointly with such entities. These alliances bring mutual benefit: The partners gain Wiley’s publishing, marketing, sales, and distribution expertise, while Wiley benefits from being affiliated with prestigious organizations and their members. Societies that sponsor or own such journals generally receive a royalty and/or other financial consideration. We may procure editorial services from such societies on a prenegotiated fee basis. We also enter into agreements with outside independent editors of journals that define their editorial duties and the fees and expenses for their services. Contributors of articles to our journal portfolio transfer publication rights to us or a professional society, as applicable. We publish the journals of many prestigious societies, including the American Cancer Society, the American Heart Association, the American Anthropological Association, the American Geophysical Union, and the German Chemical Society.

Wiley Online Library, which is delivered through our Literatum platform, provides the user with intuitive navigation, enhanced discoverability, expanded functionality, and a range of personalization options. Access to abstracts is free and full content is accessible through licensing agreements or as individual article purchases. Large portions of the content are provided free or at nominal cost to developing nations through partnerships with certain nonprofit organizations. Our online publishing platforms provide revenue growth opportunities through new applications and business models, online advertising, deeper market penetration, and individual sales and pay-per-view options.

Wiley’s performance in the 2021 release of Clarivate Analytics’ Journal Citation Reports (JCR) remains strong, maintaining its top 3 position in terms of citations received and sits in 4th place for journals indexed and articles published. Wiley has 7% of titles, 8% of articles, and 11% of citations.

A total of 1,540 Wiley journals were included in the reports. Wiley journals ranked #1 in 19 categories across 17 of its titles and achieved 270 top-10 category rankings.

The annual JCR are one of the most widely used sources of citation metrics used to analyze the performance of peer-reviewed journals. The most famous of these metrics, the Impact Factor, is based on the frequency with which an average article is cited in the JCR report year. Alongside other metrics, this makes it an important tool for evaluating a journal’s impact on ongoing research.

Under the Open Access business model, accepted research articles are published subject to payment of Article Publication Charges (APCs) and then all open articles are immediately free to access online. Contributors of open access articles retain many rights and typically license their work under terms that permit reuse.

Open Access offers authors choices in how to share and disseminate their work, and it serves the needs of researchers who may be required by their research funder to make articles freely accessible without embargo. APCs are typically paid by the individual author or by the author’s funder, and payments are often mediated by the author’s institution. We provide specific workflows and infrastructure to authors, funders, and institutions to support the requirements of Open Access.

We offer two Open Access publishing models. The first of these is Hybrid Open Access where authors publishing in the majority of our paid subscription journals, after article acceptance, are offered the opportunity to make their individual research article openly available online.

The second offering of the Open Access model is a growing portfolio of fully open access journals, also known as Gold Open Access Journals. All Open Access articles are subject to the same rigorous peer-review process applied to our subscription-based journals. As with our subscription portfolio, a number of the Gold Open Access Journals are published under contract for, or in partnership with, prestigious societies, including the American Geophysical Union, the American Heart Association, the European Molecular Biology Organization, and the British Ecological Society. The Open Access portfolio spans life, physical, medical, and social sciences and includes a choice of high impact journals and broad-scope titles that offer a responsive, author-centered service.

7

Transformational agreements (“read and publish”), are an innovative model that blends Journal Subscription and Open Access offerings. Essentially, for a single fee, a national or regional consortium of libraries pays for and receives full read access to our journal portfolio and the ability to publish under an open access arrangement. Like subscriptions, transformational agreements involve recurring revenue under multiyear contracts. Transformational models accelerate the transition to open access while maintaining subscription access.

Licensing, Backfiles, and Other

Licensing, Backfiles, and Other includes backfile sales, the licensing of publishing rights, and individual article sales. A backfile license provides access to a historical collection of Wiley journals, generally for a one-time fee. We also engage with international publishers and receive licensing revenue from reproductions, translations, and other digital uses of our content. Through the Article Select and PayPerView programs, we provide fee-based access to non-subscribed journal articles, content, book chapters, and major reference work articles. The Research Publishing business is also a provider of content and services in evidence-based medicine (EBM). Through our alliance with The Cochrane Collaboration, we publish The Cochrane Library, a premier source of high-quality independent evidence to inform healthcare decision-making. EBM facilitates the effective management of patients through clinical expertise informed by best practice evidence that is derived from medical literature.

Research Solutions

Research Solutions is principally comprised of our Atypon platforms business and our corporate and society services offerings, including advertising, career-centers, knowledge hubs, databases, consulting, and reprints.

Atypon Platforms and Services

Literatum, our online publishing platform for societies and other research publishers, delivers integrated access to more than 10 million articles from approximately 2,100 publishers and societies, as well as over 27,000 online books and hundreds of multivolume reference works, laboratory protocols and databases.

Corporate and Society Service Offerings

Corporate and society service offerings include advertising, spectroscopy software and spectral databases, and job board software and career center services, which includes the products and services from our acquisition of Madgex Holdings Limited (Madgex) and Bio-Rad Laboratories Inc.’s Informatics products (Informatics). In addition, it also includes product and service offerings related to recent acquisitions such as J&J Editorial Services, LLC. (J&J) on October 1, 2021, and the eJournalPress business (EJP) on November 30, 2021. J&J is a publishing services company providing expert offerings in editorial operations, production, copyediting, system support and consulting. EJP is a technology platform company with an established journal submission and peer-review management system.

We generate advertising revenue from print and online journal subscription and controlled circulation products, our online publishing platform, Literatum, online events such as webinars and virtual conferences, community interest websites such as analyticalscience.wiley.com, and other websites. Journal and article reprints are primarily used by pharmaceutical companies and other industries for marketing and promotional purposes.

Academic:

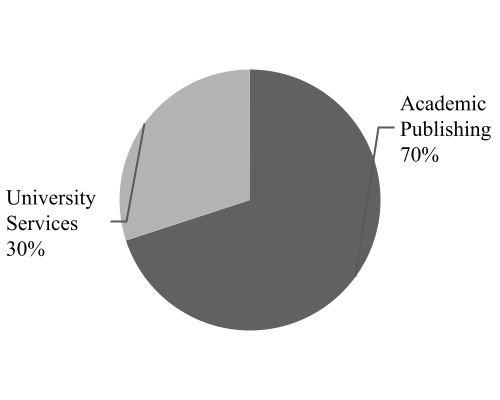

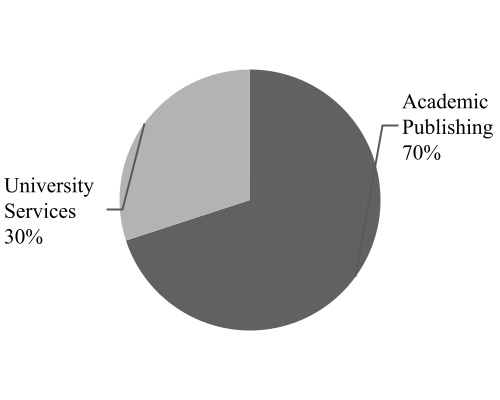

Our Academic segment includes Academic Publishing and University Services, whose products and services include scientific, professional, and education print and digital books, and digital courseware to support libraries, corporations, students, professionals, and researchers, as well as online program management or OPM services for higher education institutions. Communities served include business, finance, accounting, management, leadership, computer science, data science, technology, behavioral health, engineering and architecture, mathematics, science and medicine, and education. Products are developed for worldwide distribution through multiple channels, including brick-and-mortar and online retailers, libraries, colleges and universities, corporations, direct-to-consumer, distributor networks, and through other channels. Publishing centers include Australia, Germany, India, the UK, and the US. Academic accounted for approximately 34% of our consolidated revenue in the year ended April 30, 2023, with a 21.4% Adjusted EBITDA margin. See Part II, Item 7, "Management’s Discussion and Analysis of Financial Condition and Results of Operations" in the section "Segment Operating Results" of this Annual Report on Form 10-K for further details. Approximately 65% of Academic revenue is from digital and online products and services.

8

Academic revenue by product type includes Academic Publishing and University Services. The graphs below present revenue by product type for the years ended April 30, 2023 and 2022:

2023

2022

Key strategies for the Academic business include developing high-impact, career-aligned courseware, products, brands, franchises, and solutions to meet the evolving needs of global learners and university partners while expanding global discoverability and distribution. We continue to implement strategies to efficiently and effectively manage print revenue declines while driving growth in our digital lines of business.

Book sales for Academic Publishing are generally made on a returnable basis with certain restrictions. We provide for estimated future returns on sales made during the year based on historical return experience and current market trends.

Materials for book publications are obtained from authors throughout most of the world, utilizing the efforts of a best-in-class internal editorial staff, external editorial support, and advisory boards. Most materials originate by the authors themselves or as the result of suggestions or solicitations by editors. We enter into agreements with authors that state the terms and conditions under which the materials will be published, the name in which the copyright will be registered, the basis for any royalties, and other matters. Author compensation models include royalties, which vary depending on the nature of the product and work-for-hire. We may make advance royalty payments against future royalties to authors of certain publications. Royalty advances are reviewed for recoverability and a reserve for loss is maintained, if appropriate.

We continue to add new titles, revise existing titles, and discontinue the sale of others in the normal course of our business. We also create adaptations of original content for specific markets based on customer demand. Our general practice is to revise our textbooks every 3-5 years, as warranted, and to revise other titles as appropriate. Subscription-based products are updated on a more frequent basis.

We generally contract independent printers and binderies globally for their services, using a variety of suppliers and materials to support our range of needs.

We have an agreement to outsource our US-based book distribution operations to Cengage Learning, with the continued aim of improving efficiency in our distribution activities and moving to a more variable cost model. As of April 30, 2023, we had one global warehousing and distribution facility remaining, which is in the UK.

Academic Publishing

Academic Publishing generates the majority of its revenue from contracts with its customers in the following revenue streams:

•Print and Digital Publishing

•Digital Courseware

•Test Preparation and Certification

•Licensing and Other

9

Print and Digital Publishing

Education textbooks, related supplementary material, and digital products are sold primarily to bookstores and online retailers serving both for-profit and nonprofit educational institutions (primarily colleges and universities), and direct-to-students. We employ sales representatives who call on faculty responsible for selecting books to be used in courses and on the bookstores that serve such institutions and their students. The textbook business is seasonal, with the majority of textbook sales occurring during the July-through-October and December-through-February periods. There are various channels to drive affordability for print and digital materials within the higher education market, including used, rental, and inclusive access.

STM books (Reference) are sold and distributed globally in digital and print formats through multiple channels, including research libraries and library consortia, independent subscription agents, direct sales to professional society members, bookstores, online booksellers, and other customers.

Professional books, which include business and finance, technology, professional development for educators, and other professional categories, as well as the For Dummies® brand, are sold to brick-and-mortar and online retailers, wholesalers who supply such bookstores, college bookstores, individual practitioners, corporations, and government agencies. We employ sales representatives who call upon independent bookstores, national and regional chain bookstores, wholesalers, and corporations globally. Sales of professional books also result from direct marketing outreach, conferences, and other industry-relevant outreach.

We also promote active and growing custom professional and education publishing programs. Professional organizations use our custom professional publications for marketing outreach. This outreach includes customized digital and print books written for a specific customer and includes custom cover art, such as imprints, messages, and slogans. More specific are customized For Dummies® publications, which leverage the power of this well-known brand to meet the specific information needs of a wide range of organizations around the world.

We develop content in a digital format that can be used for both digital and print products, resulting in productivity and efficiency savings and enabling print-on-demand delivery. Book content is available online through Wiley Online Library (delivered through our Literatum platform), WileyPLUS, zyBooks®, alta™, and other proprietary platforms. Digital books are delivered to intermediaries, including Amazon, Apple, and Google, for sale to individuals in various industry-standard formats. These are now the preferred deliverable for licensees of all types, including foreign language publishers. Digital books are also licensed to libraries through aggregators. Specialized formats for digital textbooks go to distributors servicing the academic market, and digital book collections are sold by subscription through independent third-party aggregators servicing distinct communities. Custom deliverables are provided to corporations, institutions, and associations to educate their employees, generate leads for their products, and extend their brands. Digital content is also used to create online articles, mobile apps, newsletters, and promotional collateral. Continually reusing content improves margins, speeds delivery, and helps satisfy a wide range of evolving customer needs. Our online presence not only enables us to deliver content online, but also to sell more books. The growth of online booksellers benefits us because they provide unlimited virtual “shelf space” for our entire backlist. Publishing alliances and franchise products are important to our strategy. Education and STM publishing alliance partners include IEEE, American Institute of Chemical Engineers, and many others. The ability to join Wiley’s product development, sales, marketing, distribution, and technology with a partner’s content, technology, and/or brand name has contributed to our success.

Digital Courseware

We offer high-quality online learning solutions, including WileyPLUS, a research-based online environment for effective teaching and learning that is integrated with a complete digital textbook. WileyPLUS improves student learning through instant feedback, personalized learning plans, and self-evaluation tools, as well as a full range of course-oriented activities, including online planning, presentations, study, homework, and testing. In selected courses, WileyPLUS includes a personalized adaptive learning component.

The highly interactive zyBooks platform enables learners to learn by doing while allowing professors to be more efficient and devote more time to teaching. The platform maximizes learner engagement and retention through demonstration and hands-on learning experiences using interactive question sets, animations, tools, and embedded labs. The zyBooks platform will become an essential component of Wiley’s differentiated digital learning experience and, when combined with alta’s adaptive learning technology and WileyPLUS, powers high-impact education across Wiley’s Academic segment.

10

Test Preparation and Certification

The Test Preparation and Certification business represents learning solutions, training activities, and print and digital formats that are delivered to customers directly through online digital delivery platforms, bookstores, online booksellers, and other customers. Products include CPAExcel®, a modular, digital platform comprised of online self-study, videos, mobile apps, and sophisticated planning tools to help professionals prepare for the CPA exam, and test preparation products for the GMAT™, ACT®, CFA®, CMA®, CIA®, CMT®, FRM®, FINRA®, Banking, and PMP® exams. In the last quarter of fiscal year 2023 we sold a portion of our test preparation and certification products referred to as Wiley's Efficient Learning test prep portfolio which focused on test prep for finance, accounting and business certifications. See Note 4, "Acquisitions and Divestitures" of the Notes to Consolidated Financial Statements for further details.

Licensing and Other

Licensing and distribution services are made available to other publishers under agency arrangements. We also engage in co-publishing titles with international publishers and receive licensing revenue from photocopies, reproductions, translations, and digital uses of our content and use of the Knewton® adaptive engine. Wiley also realizes advertising revenue from branded websites (e.g., Dummies.com) and online applications.

University Services

Our University Services business offers institutions and their students a rich portfolio of education technology and student and faculty support services, allowing the institutions to reach more students online with their own quality academic programs.

Many of Wiley’s client institutions are regional state universities or small liberal arts colleges. Our resources, expertise and innovations meaningfully impact their ability to increase access to their programs online, as many students now seek these types of flexible offerings. University Services provides institutions with a bespoke suite of services that each institution has determined it needs to serve students, including market research, marketing and recruitment, program development, online platform technology, student retention support, instructional design, faculty development and support, and access to the Engage Learning Management System, which facilitates the online education experience. Graduate degree programs include Business Administration, Finance, Accounting, Healthcare, Engineering, Communications, and others. Revenue is derived from pre-negotiated contracts with institutions that provide for a share of revenue generated after students have enrolled and demonstrated initial persistence. While the majority of our contracts are revenue-share arrangements, we also offer the opportunity to contract on a fee-for-service basis, unlike many other third-party online providers. As of April 30, 2023, the University Services business had 64 university partners under contract.

Talent:

Our Talent segment consists of talent development (Wiley Edge, formerly mthree) for professionals and businesses, assessments (corporate training) and corporate learning offerings. Our key growth strategy includes bridging the IT skills gap through talent development for corporations around the world. Talent accounted for approximately 12% of our consolidated revenue in the year ended April 30, 2023, with a 21.1% Adjusted EBITDA margin. See Part II, Item 7, "Management’s Discussion and Analysis of Financial Condition and Results of Operations" in the section "Segment Operating Results" of this Annual Report on Form 10-K for further details. Talent generated 98% of its revenue from digital and online products and services.

On January 1, 2020, Wiley acquired mthree, a talent placement provider that addresses the IT skills gap by finding, training, and placing job-ready technology talent in roles with leading corporations worldwide. In late May 2022, Wiley renamed mthree as Wiley Edge. Wiley Edge sources, trains, and prepares aspiring students and professionals to meet the skill needs of today’s technology and banking services careers, and then places them with some of the world’s largest financial institutions, technology companies, and government agencies. Wiley Edge also works with its clients to retrain and retain existing employees so they can continue to meet the changing demands of today’s technology landscape. In fiscal year 2023, Wiley Edge signed 15 new corporate clients and expanded into new industry verticals beyond financial services, such as technology and consumer goods.

11

Our assessments (corporate training) offerings include high-demand soft-skills training solutions that are delivered to organizational clients through online digital delivery platforms, either directly or through an authorized distributor network of independent consultants, trainers, and coaches. Wiley’s branded assessment solutions include Everything DiSC®, The Five Behaviors® based on Patrick Lencioni’s perennial bestseller The Five Dysfunctions of a Team, and Leadership Practices Inventory® from Kouzes and Posner’s bestselling The Leadership Challenge®, as well as PXT Select™, a pre-hire selection tool. Our solutions help organizations hire and develop effective managers, leaders, and teams.

We also offer online learning and training solutions for global corporations and small and medium-sized enterprises, which are sold on a subscription or fee basis. Learning experiences, formats and modules on topics such as leadership development, value creation, client orientation, change management, and corporate strategy are delivered on a cloud-based CrossKnowledge Learning Management System (LMS) platform that hosts more than 20,000 content assets (videos, digital learning modules, written files, etc.) in 18 languages. Its offering includes a collaborative e-learning publishing and program creation system. In addition, learning experiences, content, and LMS offerings are continuously refreshed and expanded to serve a wider variety of customer needs. These digital learning solutions are either sold directly to corporate customers or through our global partners’ network.

Fiscal Year 2024 Dispositions, Segment Realignment, and Restructuring

On June 1, 2023, Wiley’s Board of Directors approved a plan to dispose of certain education businesses. Those businesses are University Services (formerly Online Program Management) in our Academic segment, and Wiley Edge (formerly Talent Development) and CrossKnowledge in our Talent segment. These dispositions are expected to be completed in fiscal year 2024, and will be reported as held for sale in the first quarter of fiscal year 2024. In fiscal year 2023, these businesses, combined with the two dispositions disclosed in Note 4, "Acquisitions and Divestitures" generated approximately $393 million of revenue (approximately 19% of our consolidated revenue) and $43 million of Adjusted EBITDA (approximately 10% of our consolidated Adjusted EBITDA). We are evaluating the financial statement impact of these planned dispositions. During fiscal year 2024, it is anticipated that additional restructuring actions will be undertaken to rightsize the Company’s expenses. The timing of much of these restructuring actions will be influenced by the completion of the dispositions. The amount of such charges has not yet been determined.

In the first quarter of fiscal year 2024, we are realigning our segments. Our new segment structure will consist of two reportable segments which includes (1) Research (no change) and (2) Learning, as well as a Corporate expense category (no change), which includes certain costs that are not allocated to the reportable segments. Research will continue to have reporting lines of Research Publishing and Research Solutions. Learning will include reporting lines of Academic (education publishing) and Professional (professional publishing and assessments).

Human Capital

As of April 30, 2023, we employed approximately 8,800 colleagues, including 1,800 placement candidates in the Wiley Edge product offering, on a full-time equivalent basis worldwide.

We view our colleagues as one of our most significant assets and investments to deliver on our mission to unlock human potential and to champion and advocate for our customers who want to make impacts in their fields, their workplaces, and their lives, through knowledge creation, use and dissemination. Our success depends on our ability to develop, attract, reward, and retain a diverse population of talented, qualified, and highly skilled colleagues at all levels of our organization and across our global workforce so that they can deliver on our promise to our customers to clear the way to their successes. This includes programs, policies, and initiatives that promote diversity, equity, and inclusion (DEI); talent acquisition; ongoing employee learning and development; competitive compensation and benefits; health and well-being; and emphasis on employee satisfaction and engagement.

Our culture differentiates us as an organization and our core values define how we work together. We ask colleagues to embody our three values—Learning Champion, Needle Mover, and Courageous Teammate—and assess their performance against these in addition to what they achieve against their goals. These values define who we are as a company and what we stand for.

12

Our human capital metrics summary (excluding placement candidates in Wiley Edge) as of April 30, 2023:

| CATEGORY | METRIC | ||||||||||

| EMPLOYEES | By Region | Americas | 48 | % | |||||||

| APAC | 20 | % | |||||||||

| EMEA | 32 | % | |||||||||

| DIVERSITY AND INCLUSION | Global Gender Representation | % Female Colleagues | 59 | % | |||||||

| % Female Senior Leaders (Vice President and Above) | 43 | % | |||||||||

| US Person of Color (POC) Representation* | % POC | 27 | % | ||||||||

| % POC Senior Leaders (Vice President and Above) | 19 | % | |||||||||

* US POC includes employees who self-identify as Hispanic or Latino, Black or African American, Asian, American Indian or Alaskan Native, Native Hawaiian or other Pacific Islander, Other, or two or more races.

Health & Well-Being

Safeguarding and promoting colleague well-being is central to what we do, as it is critical we provide tools and resources to help colleagues be healthy, and an environment that allows us to be at our best. We support our colleagues in maintaining their physical, emotional, social, and financial well-being through working practices, education, and benefit programs.

Our recently implemented post pandemic hybrid work model provides the majority of our colleagues the flexibility to work remotely at least some of the time. The hybrid work model is intended to support colleague health and well-being, while maintaining a culture of innovation and collaboration.

Diversity, Equity & Inclusion

Through our DEI strategy, we are operationalizing critical priorities. We are focused on four DEI Strategic Pillars—Fostering an Inclusive Community, Enhancing our Foundation, Understanding our People, and Creating Impact Through our Business.

These pillars reflect our DEI near-term priorities to propel a sustainable, inclusive organization that embodies diversity and equity throughout our policies, programs, and processes, and fosters an inclusive culture that celebrates the unique contributions of our colleagues and supports human connectivity. In addition, we develop partnerships and launch pilot programs to support communities that are underrepresented in higher education, the workforce, and the field of publishing.

Our Employee Resource Groups help amplify our DEI priorities through learning, community engagement, and allyship and advocacy. As a member of the CEO Action for Diversity and Inclusion, Wiley demonstrates its commitment to sustained, concrete actions that advance diversity and inclusive thinking, behavior, and business practices in the workplace.

Careers & Engagement

Investment in colleague development and growth for current and future roles is central to our culture. Our goal is to provide colleagues with learning opportunities and experiences at every stage of their journey at Wiley. We help colleagues upskill and thrive by leveraging the power of our internal products and tapping into our external partnerships. We focus on delivering quality curated resources, customized learning paths, and comprehensive development programs. We offer interactive development programs that allow our colleagues to share lessons learned, adopt best practices, and have interactive opportunities with their peers. Through our Champion Your Career program, our colleagues get practical advice on updating their resumes and honing their interviewing skills, and have career conversations with our Talent team. Leveraging Wiley's Everything DiSC assessment tools and resources, our colleagues can better understand themselves and others, creating a common language that makes interactions more collaborative and effective.

13

Through our Pay@Wiley journey, we enhanced our colleague and manager understanding of pay through our education programs, and raised transparency by sharing segment in range and publishing our first global equitable pay study. We introduced Achievers, our recognition platform that was designed so our colleagues can recognize each other to create a culture of recognition and celebrate success.

We conduct our Talent Review annually, focusing on high-performing and high-potential talent, diversity, and succession for our most critical roles. We are committed to identifying, growing, and retaining top talent and ensuring we have the right skills for the future. We establish key development action planning opportunities for each colleague to build bench strength and review development progress and mobility regularly.

Environment

We continue our journey to support the sustainability of our planet. We believe environmental responsibility and business objectives are fundamentally connected and essential to our operations. This is why we are acting now to protect the environment by making informed choices and limiting our impact on natural resources.

For the fourth consecutive year, we are a CarbonNeutral® certified company across our global operations, in accordance with the CarbonNeutral Protocol. Our locations use 100% renewable energy through green tariffs and energy attribute certificates (EACs). Most of our global office real estate is leased and, whenever possible, we work with property owners to optimize sustainability.

This year, we furthered our commitment by setting a science-based target with the Science Based Targets Initiative (SBTi). We set a near and long-term company-wide emissions target, including being net zero by 2040. We are responding to the SBTi’s urgent call for corporate climate action by aligning with 1.5°C and net-zero through the Business Ambition for 1.5°C campaign.

We also work with publishing partners, where possible, to reduce print production and consumption, reduce excess inventory through print-on-demand, and encourage digital consumption of our products. We begun implementing measures to ensure our subcontractors who assist us in providing material aspects of the products and services are held to the same high standards as we hold ourselves.

In July 2022, we submitted to Carbon Disclosure Project (CDP) Climate for the first time. We continue to track and trace our paper usage and submitted a CDP Forests disclosure for the second year. Our commitment to sustainably sourced paper is supported by our Paper Selection and Use Policy. We continually evaluate climate and environmental reporting and plan to expand our disclosures in the coming years.

Our partnership with Trees for the Future continues. We plant a tree for every copy of a journal we actively stop printing, up to one million trees, resulting in more than 600,000 trees to date.

We are always seeking opportunities to improve environmental performance. We comply with environmental laws and regulations, thoughtfully investing resources toward managing environmental affairs and raising awareness of global environmental issues through education and research.

Financial Information About Business Segments

The information set forth in Part II, Item 8, “Financial Statements and Supplementary Data” in Note 3, “Revenue Recognition, Contracts with Customers,” and Note 20, “Segment Information,” of the Notes to Consolidated Financial Statements and Item 7, “Management’s Discussion and Analysis of Financial Condition and Results of Operations” of this Annual Report on Form 10-K are incorporated herein by reference.

Available Information

Our investor site is investors.wiley.com. Our internet address is www.wiley.com. We make available, free of charge, on or through our investors.wiley.com website, our Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K, and amendments to those reports that we file or furnish pursuant to Sections 13(a) or 15(d) of the Securities Exchange Act of 1934, or the Exchange Act, as soon as reasonably practicable after we electronically file these materials with, or furnish them to, the SEC. The information contained on, or that may be accessed through our website is not incorporated by reference into, and is not a part of, this Annual Report on Form 10-K.

14

Item 1A. Risk Factors

Introduction

The risks described below should be carefully considered before making an investment decision. You should carefully consider all the information set forth in this Annual Report on Form 10-K, including the following risk factors, before deciding to invest in any of our securities. This Annual Report on Form 10-K also contains, or may incorporate by reference, forward-looking statements that involve risks and uncertainties. See the “Cautionary Notice Regarding Forward-Looking Statements,” immediately preceding Part I of this Annual Report on Form 10-K. The risks below are not the only risk factors we face. Additional risks not currently known to us or that we presently deem insignificant could impact our consolidated financial position and results of operations. Our businesses, consolidated financial position, and results of operations could be materially adversely affected by any of these risks. The trading price of our securities could decline due to any of these risks, and investors may lose all or part of their investment.

Strategic Risks

We may not be able to realize the expected benefits of our growth strategies, which are described in Item 1. Business, including successfully integrating acquisitions, which could adversely impact our consolidated financial position and results of operations.

Our growth strategy includes business acquisitions, including knowledge-enabled services, which complement our existing businesses. Acquisitions may have a substantial impact on our consolidated financial position and results of operations. Acquisitions involve risks and uncertainties, including difficulties in integrating acquired operations and in realizing expected opportunities, cost synergies, diversions of management resources, loss of key employees, challenges with respect to operating new businesses, and other uncertainties.

We have announced our intent to explore the sale of certain of our businesses, and such proposed divestitures may introduce significant risks and uncertainties.

We have initiated a strategic review of our non-core education businesses which could result in the future divestiture of certain assets or businesses that no longer fit with our strategic direction or growth targets. Divestitures involve significant risks and uncertainties that could adversely affect our business, consolidated financial position and consolidated results of operations. These include, among others, the inability to find potential buyers on favorable terms, disruption to our business and/or diversion of management attention from other business concerns, the potential loss of key employees, difficulties in separating the operations of the divested business, and retention of certain liabilities related to the divested business. Significant time and expenses could be incurred to divest these non-core businesses which may adversely affect operations as dispositions may require our continued financial involvement, such as through transition service agreements, guarantees, and indemnities or other current or contingent financial obligations and liabilities.

The demand for digital and lower cost books could impact our sales volumes and pricing in an adverse way.

A common trend facing each of our businesses is the digitization of content and proliferation of distribution channels through the Internet and other electronic means, which are replacing traditional print formats. This trend towards digital content has also created contraction in the print book retail market which increases the risk of bankruptcy for certain retail customers, potentially leading to the disruption of short-term product supply to consumers, as well as potential bad debt write-offs. New distribution channels, such as digital formats, the Internet, online retailers, and growing delivery platforms (e.g., tablets and e-readers), combined with the concentration of retailer power, present both risks and opportunities to our traditional publishing models, potentially impacting both sales volumes and pricing.

As the market has shifted to digital products, customer expectations for lower-priced products have increased due to customer awareness of reductions in production costs and the availability of free or low-cost digital content and products. As a result, there has been pressure to sell digital versions of products at prices below their print versions. Increased customer demand for lower prices could reduce our revenue.

15

We publish educational content for undergraduate, graduate, and advanced placement students, lifelong learners, and, in Australia, for secondary school students. Due to growing student demand for less expensive textbooks, many college bookstores, online retailers, and other entities, offer used or rental textbooks to students at lower prices than new textbooks. The Internet has made the used and rental textbook markets more efficient and has significantly increased student access to used and rental textbooks. Further expansion of the used and rental textbook markets could further adversely affect our sales of print textbooks, subsequently affecting our consolidated financial position and results of operations.

A reduction in enrollment at colleges and universities could adversely affect the demand for our higher education products.

Enrollment in US colleges and universities can be adversely affected by many factors, including changes in government and private student loan and grant programs, uncertainty about current and future economic conditions, increases in tuition, general decreases in family income and net worth, and record low unemployment due to an active job market. In addition, enrollment levels at colleges and universities outside the US are influenced by global and local economic factors, local political conditions, and other factors that make predicting foreign enrollment levels difficult. Reductions in expected levels of enrollment at colleges and universities both within and outside the US could adversely affect demand for our higher education offerings, which could adversely impact our consolidated financial position and results of operations.

If we are unable to retain key talent and other colleagues, our consolidated financial condition or results of operations may be adversely affected.

The Company and industry are highly dependent on the loyal engagement of key leaders and colleagues. Loss of talent due to inadequate skills and career path development or maintaining competitive salaries and benefits could have a significant impact on Company performance.

We are highly dependent on the continued services of key talent who have in-depth market and business knowledge and/or key relationships with business partners. The loss of the services of key talent for any reason and our inability to replace them with suitable candidates quickly or at all, as well as any negative market perception resulting from such loss, could have a material adverse effect on our business, consolidated financial position, and results of operations.

We have a significant investment in our colleagues around the world. We offer competitive salaries and benefits in order to attract and retain the highly skilled workforce needed to sustain and develop new products and services required for growth. Employment costs are affected by competitive market conditions for qualified individuals and factors such as healthcare and retirement benefit costs.

The competitive pressures we face in our business, as well as our ability to retain our business relationships with our authors and professional societies, could adversely affect our consolidated financial position and results of operations.

The contribution of authors and their professional societies is one of the more important elements of the highly competitive publishing business. Success and continued growth depend greatly on developing new products and the means to deliver them in an environment of rapid technological change. Attracting new authors and professional societies while retaining our existing business relationships is critical to our success. If we are unable to retain our existing business relationships with authors and professional societies, this could have an adverse impact on our consolidated financial position and results of operations.

16

Information Technology Systems and Cybersecurity Risks

Our company is highly dependent on information technology systems and their business management and customer-facing capabilities critical for the long-term competitive sustainability of the business. If we fail to innovate in response to rapidly evolving technological and market developments, our competitive position may be negatively impacted.

We must continue to invest in technology and other innovations to adapt and add value to our products and services to remain competitive. This is particularly true in the current environment, where investment in new technology is ongoing and there are rapid changes in the products competitors are offering, the products our customers are seeking, and our sales and distribution channels. In some cases, investments will take the form of internal development; in others, they may take the form of an acquisition. There are uncertainties whenever developing or acquiring new products and services, and it is often possible that such new products and services may not be launched, or, if launched, may not be profitable or as profitable as existing products and services. If we are unable to introduce new technologies, products, and services, our ability to be profitable may be adversely affected.

In addition, our ability to effectively compete, may be affected by our ability to anticipate and respond effectively to the opportunity and threat presented by new technology disruption and developments, including generative artificial intelligence (GAI). We may be exposed to competitive risks related to the adoption and application of new technologies by established market participants or new entrants, and others.

We cannot predict the effect of technological changes on our business. Failure to keep pace with these technological developments or otherwise bring to market products that reflect these technologies could have a material adverse impact on our overall business and results of operations. We may not be successful in anticipating or responding to these developments on a timely and cost-effective basis. Additionally, the effort to gain technological expertise and develop new technologies in our business requires us to incur significant expenses. If we cannot offer new technologies as quickly as our competitors, or if our competitors develop more cost-effective technologies or product offerings, we could experience a material adverse effect on our operating results, growth and financial condition.

We may be susceptible to information technology risks that may adversely impact our business, consolidated financial position and results of operations.

Information technology is a key part of our business strategy and operations. As a business strategy, Wiley’s technology enables us to provide customers with new and enhanced products and services and is critical to our success in migrating from print to digital business models. Information technology is also a fundamental component of all our business processes, collecting and reporting business data, and communicating internally and externally with customers, suppliers, employees, and others. We face technological risks associated with digital products and service delivery in our businesses, including with respect to information technology capability, reliability, security, enterprise resource planning, system implementations, and upgrades. Across our businesses, we hold personal data, including that of employees and customers. Failures of our information technology systems and products (including operational failure, natural disaster, computer virus, or cyberattacks) could interrupt the availability of our digital products and services, result in corruption or loss of data or breach in security, and result in liability or reputational damage to our brands and/or adversely impact our consolidated financial position and results of operations.

Management has designed and implemented policies, processes, and controls to mitigate risks of information technology failure and to provide security from unauthorized access to our systems. In addition, we have disaster recovery plans in place to maintain business continuity for our key financial systems. While key financial systems have backup and tested disaster recovery systems, other applications and services have limited backup and recovery procedures which may delay or prevent recovery in case of disaster. The size and complexity of our information technology and information security systems, and those of our third-party vendors with whom we contract, make such systems potentially vulnerable to cyberattacks common to most industries from inadvertent or intentional actions by employees, vendors, or malicious third parties. While we have taken steps to address these risks, there can be no assurance that a system failure, disruption, or data security breach would not adversely affect our business and could have an adverse impact on our consolidated financial position and results of operations.

17

We are continually improving and upgrading our computer systems and software. We have implemented a global Enterprise Resource Planning (ERP) system as part of a multiyear plan to integrate and upgrade our operational and financial systems and processes. We have also implemented record-to-report, purchase-to-pay, and several other business processes within all locations. We implemented order-to-cash for certain businesses and have continued to roll out additional processes and functionality of the ERP system in phases. Implementation of an ERP system involves risks and uncertainties. Any disruptions, delays, or deficiencies in the design or implementation of a new system could result in increased costs, disruptions in operations, or delays in the collection of cash from our customers, as well as having an adverse effect on our ability to timely report our financial results, all of which could materially adversely affect our business, consolidated financial position, and results of operations. We currently use out of support systems for order management for certain businesses. While we have contingency support available, any major disruptions, while unlikely, may require longer remediation time. This could impact our ability to process and fulfill orders for those businesses. We currently use a legacy platform with limited support for order management of the global Academic business. Any defects and disruptions in the legacy systems which cannot be addressed in a timely manner could impact our ability to process orders and reconcile financial statements.

Cyber risk and the failure to maintain the integrity of our operational or security systems or infrastructure, or those of third parties with which we do business, could have a material adverse effect on our business, consolidated financial condition, and results of operations.

The cybersecurity risks we face range from cyberattacks common to most industries, such as the development and deployment of malicious software to gain access to our networks and attempt to steal confidential information, launch distributed denial of service attacks, or attempt other coordinated disruptions, to more advanced threats that target us because of our prominence in the global research and advisory field. As a result of the COVID-19 pandemic, most of our employees continue to work remotely, at least some of the time, which magnifies the importance of the integrity of our remote access security measures.

Like many multinational corporations, we, and some third parties upon which we rely, have experienced cyberattacks on our computer systems and networks in the past and may experience them in the future, likely with more frequency and sophistication and involving a broader range of devices and modes of attack, all of which will increase the difficulty of detecting and successfully defending against them. To date, none have resulted in any material adverse impact to our business, operations, products, services, or customers. Wiley has invested heavily in Cybersecurity tools and resources to keep our systems safe. We have implemented various security controls to meet our security obligations, while also defending against constantly evolving security threats. Our security controls help to secure our information systems, including our computer systems, intranet, proprietary websites, email and other telecommunications and data networks, and we scrutinize the security of outsourced website(s) and service providers prior to retaining their services. However, the security measures implemented by us or by our outside service providers may not be effective, and our systems (and those of our outside service providers) may be vulnerable to theft, loss, damage and interruption from a number of potential sources and events, including unauthorized access or security breaches, cyber-attacks, computer viruses, power loss, or other disruptive events.

The security compliance landscape continues to evolve, requiring us to stay apprised of changes in cybersecurity, privacy laws and regulations, such as the European Union General Data Protection Regulation (GDPR), the California Consumer Privacy Act (CCPA), the Brazilian General Data Protection Law (LGPD), the Chinese Cybersecurity, Data Security and Personal Information Protection laws (PIPL). The United Kingdom ceased to be an EU Member State on January 31, 2020, but enacted the UK data protection law. It is unclear how UK data protection laws will continue to develop; however, contractual clauses have been established regulating data transfers to and from the United Kingdom. Some countries also are considering or have enacted legislation requiring local storage and processing of data that could increase the cost and complexity of delivering our services.

In addition, to new and proposed data protection laws, we also stay apprised and adopt certain security standards required by our clients, such as International Organization for Standardization (ISO), National Institute of Standards and Technology (NIST) and Center for Internet Security (CIS). Recent well-publicized security breaches at other companies have led to enhanced government and regulatory scrutiny of the measures taken by companies to protect against cyberattacks and may in the future result in heightened cybersecurity requirements, including additional regulatory expectations for oversight of vendors and service providers.

18

A cyberattack could cause delays in initiating or completing sales, impede delivery of our products and services to our clients, disrupt other critical client-facing or business processes, or dislocate our critical internal functions. Additionally, any material breaches or other technology-related catastrophe, or media reports of perceived security vulnerabilities to our systems or those of our third parties, even if no breach has been attempted or has occurred, could cause us to experience reputational harm, loss of customers and revenue, fines, regulatory actions and scrutiny, sanctions or other statutory penalties, litigation, liability for failure to safeguard our customers information, or financial losses that are either not insured against or not fully covered through any insurance maintained by us.

Operational Risks

We may not realize the anticipated cost savings and benefits from, or our business may be disrupted by, our business transformation and restructuring efforts.

We continue to transform our business from a traditional publishing model to a global provider of content-enabled solutions with a focus on digital products and services. We have made several acquisitions over the past few years that represent examples of strategic initiatives that were implemented as part of our business transformation. We will continue to explore opportunities to develop new business models and enhance the efficiency of our organizational structure. The rapid pace and scope of change increases the risk that not all our strategic initiatives will deliver the expected benefits within the anticipated timeframes. In addition, these efforts may disrupt our business activities, which could adversely affect our consolidated financial position and results of operations.

We continue to restructure and realign our cost base with current and anticipated future market conditions, including our Business Optimization Program and Fiscal Year 2023 Restructuring Program. Significant risks associated with these actions that may impair our ability to achieve the anticipated cost savings or that may disrupt our business, include delays in the implementation of anticipated workforce reductions in highly regulated locations outside of the US, decreases in employee morale, the failure to meet operational targets due to the loss of key employees, and disruptions of third parties to whom we have outsourced business functions. In addition, our ability to achieve the anticipated cost savings and other benefits from these actions within the expected timeframe is subject to many estimates and assumptions. These estimates and assumptions are subject to significant economic, competitive, and other uncertainties, some of which are beyond our control. If these estimates and assumptions are incorrect, if we experience delays, or if other unforeseen events occur, our business and consolidated financial position and results of operations could be adversely affected.

We may not realize the anticipated cost savings and processing efficiencies associated with the outsourcing of certain business processes.