SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 6-K

REPORT OF FOREIGN PRIVATE ISSUER

PURSUANT TO RULE 13a-16 or 15d-16 OF

THE SECURITIES EXCHANGE ACT OF 1934

Report on Form 6-K dated

27 MARCH 2003

AngloGold Limited

_

(Name of Registrant)

11 Diagonal Street

Johannesburg, 2001

(P O Box 62117)

Marshalltown, 2107

South Africa____

(Address of Principal Executive Offices)

Indicate by check mark whether the registrant files or will file annual reports under cover of Form 20-F or Form 40-F:

Form 20-F: Form 40-F:

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(1):

Yes:

No:

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(7):

Yes:

No:

Indicate by check mark whether the registrant by furnishing the information contained in this form is also thereby furnishing the information to the Commission pursuant to Rule 12g3-2(b) under the Securities Exchange Act of 1934.

Yes:

No:

Enclosures:

2002 ANNUAL REPORT TO SHAREHOLDERSTOGETHER WITH NOTICE OF MEETING

1

ANGLO GOLD LIMITED ANNUAL REPORT 2002

Key features - 2002

THE FOLLOWING EXCHANGE RATES WERE USED AS A BASIS FOR CALCULATIONS IN THIS DOCUMENT

2

ANGLO GOLD LIMITED ANNUAL REPORT 2002

Corporate

profile

Brazil

Argentina

Serra Grande

Cerro Vanguardia

Morro Velho

USA

Jerritt

Canyon

Cripple Creek

& Victor

Mali

Tanzania

Namibia

Geita

Sadiola

Yatela

Morila

Navachab

SA operations

South Africa

Union Reefs

Sunrise Dam

Australia

3

ANGLO GOLD LIMITED ANNUAL REPORT 2002

Contents

4

Letter from the Chairman and Deputy Chairman Chairman Russell Edey and Deputy Chairman James Motlatsi share their views with shareholders.

6

Delivering on our promises

7

One-year forecast 2003

8

Interview with the CEO Journalist Alec Hogg interviews CEO Bobby Godsell on AngloGold, gold and other issues.

12

Group value-added statement

13

Review of the gold market Marketing Director Kelvin Williams discusses the renewed support for gold, its performance during 2002 and the outlook for 2003.

14

Financial review

17

Group operating and financial results

18

Review of operations A solid performance for the year reviewed by region.

46

Marketing AngloGold believes in gold and is committed to growing this market.

48

Exploration Focused, yet extensive exploration in 10 countries. Read more.

52

Mineral Resources and Ore Reserves

54

Directors and executive management

56

Directors' approval Secretary's certificate Report of the independent auditors

57

Corporate governance AngloGold is committed to attaining the highest levels of corporate governance.

63

Remuneration report

64

Directors' report

74

Group financial statements

112

Company financial statements

131

Investment in principal subsidiaries and joint venture interests

132

US GAAP consolidated financial statements For the first time, an analysis in terms of US GAAP.

138

Glossary of terms

140

Shareholders' information

143

Directorate and administration

144

Contact information

Inside back cover

Other reports and sources of information

"The best news of 2002 is that the higher

Rand gold price has liberated a whole

lot of reserves in South Africa.

We are looking at six new projects

contributing 11Moz."

BOBBY GODSELL, ANGLOGOLD CEO Page 8

4.5Moz of new production at Moab Khotsong Page 28

Russell Edey, Chairman

James Motlatsi, Deputy Chairman

Letter from the

Chairman and Deputy Chairman

ANGLO GOLD LIMITED ANNUAL REPORT 2002

4

(Clockwise from top left) Tshepo Shale, a loco driver, Projek Katleho Great Noligwa, South Africa; Jannie Schnaar and Kobus Jacobs, Great Noligwa,

South Africa; Waltinho Correina Gonzaga and Leoncio Jos Arajo Costa at Serra Grande in Brazil, South America; Nolast Marebexeni is an onsetter's assistant

at Savuka, South Africa; Stuart Foya, a geochemist with the East and West Africa region, in the Morila pit; Heidi van Wyk, Moab Khotsong, South Africa.

A

Delivering

on our promises

ANGLO GOLD LIMITED ANNUAL REPORT 2002

6

What we promised for 2002

Commitment to long-term target of eliminating all accidents at work.

Growing the company into the gold equity of choice and an investment that offers its shareholders competitive returns:

* Drive the company down the cost curve

* Seek organic growth

* Continue near-mine or brownfields exploration

* Develop new greenfields exploration projects

* Apply a disciplined acquisition strategy

* Seek value down the gold chain

Reducing Rand-price cover by restructuring the hedge book

What we delivered in 2002

Long-term trend in lost time injuries decreased to 8.86 per million man hours, the lowest ever for AngloGold.

During 2002, AngloGold was one of the top-performing resource stocks in the world. The company consistently rewards shareholders with a strong dividend flow. Its performance during 2002 represents a total return to shareholders a combination of share price performance and dividend of 98% in Dollar terms.

Total cash costs continued to decline from $178/oz by 10% to $161/oz despite the impact of the strengthening Rand on the South African operations.

Three new South Africa projects, at Moab Khotsong, TauTona and Mponeng are on schedule. Sunrise Dam Expansion is complete, with the CC&V project nearing completion.

The AngloGold growth story continues, with 11.4Moz of new resources added at a cost of $1.60/oz and 3.2Moz of new reserves at a cost of $4.40/oz.

Exploration is continuing in countries in which AngloGold has operations, namely Argentina, Brazil, Tanzania, Mali, South Africa and the United States, as well as in prospective areas in Alaska, Canada and Peru. Some $19m was spent during the year.

AngloGold increased its stake from 46.25% to 92.5% in Cerro Vanguardia in Argentina during the year and continues to identify value-adding merger and acquisition opportunities.

AngloGold remains committed to developing the gold market. Following a number of notable successes during 2002 the Afridesia campaign, OroAfrica design centre, Riches of Brazil and Africa competitions, and the GoldAvenue catalogue development the company will continue its work with the World Gold Council but will also operate independently in the spheres where it has strategic influence.

AngloGold reduced its hedging contracts by some 133t during the year. The continuing strength of the gold price and the company's solid operating performance, has reduced the need to manage revenue through forward pricing and the hedge book will continue to be managed, restructured and reduced.

(The above figures are the year-on-year differences in reserves, including the effect of depletion)

Growing reserves

Some of the significant increases in ore reserves include:

Mponeng

increased by 4.6Moz mainly due to the inclusion of the Mponeng CLR and VCR below 120 level

Moab Khotsong

increased by 4.3Moz due to the inclusion of the Phase 2 project which will exploit the Vaal reef below 101 level

TauTona

increased by 0.8Moz due to the inclusion of the CLR below 120 level, the area East of the Bank Dyke on 116 level and the VCR area "A"

Savuka and Tau Lekoa

increased by 1.2Moz and 0.7Moz respectively owing to changes in mine design leading to additional life at both operations

Geita

increased by 0.8Moz due to the redesign of the Nyankanga, Geita Hill and Lone Cone pits, as well as the inclusion of the Chipaka, Area 3W and Roberts pits

Cerro Vanguardia

increased by 1.1Moz mainly as a result of AngloGold's increase in ownership to 92.5%.

7

ANGLO GOLD LIMITED ANNUAL REPORT 2002

One-year forecast - 2003

South

East and

South

North

Forecast

Actual

Forecast

Africa

West Africa

America

America

Australia

2003

2002

2002

Gold

Underground operations

Metric tonnes milled - 000

11,611

1,224

214

6

13,055

13,426

13,646

Yield

- g/t 8.16

7.18

7.64

5.11

8.06

8.27

8.29

Production

- oz 000

3,047

283

53

1

3,384

3,569

3,639

Productivity

g/employee

- actual 214

1,043

1,884

1,126

232

238

247

Surface and dump reclamation

Metric tonnes treated - 000

38,325

38,325

38,366

40,239

Yield

- g/t 0.23

0.23

0.30

0.23

Production

- oz 000

285

285

365

294

Open-pit operations

Metric tonnes treated - 000

8,727

1,057

18,416

5,332

33,532

27,186

30,378

Yield

- g/t

3.67

8.00

0.70

2.53

1.99

2.29

1.89

Production

- oz 000

1,031

272

414

433

2,150

2,005

1,848

Total

Production

- oz 000

3,332

1,031

555

467

434

5,819

5,939

5,781

Total cash costs

- $/oz produced

209

152

108

190

203

187

161

154

Capital

expenditure

- $ m

188

25

39

27

24

303

268

268

Rand/US Dollar average exchange rate

9.00

10.48

11.15

Alec Hogg: Surely the most relevant aspect of the year was the way the gold price improved, starting at under $280/oz and ending at $345/oz. Subsequent to year-end we have seen $390/oz. Is this sustainable?

Bobby Godsell: An element of it is sustainable. What pleases me is that the ghosts around the gold price have gone away. For over a decade-and-a-half people have argued that gold has lost its glister, that gold is no longer a store of value, that gold is something that only primitive people want and hold, that the Dollar will be strong forever, that US equity markets will grow by 30% a year forever. That has gone away.

To be truthful, I don't know what the equilibrium price is.I think it is still finding its place. I think the negative sentiment has gone away and that there's more upside than downside in the price. We never predict it.

Alec: Does a higher gold price change the way you run the business?

Bobby: The most immediate change is that our need for revenue and price certainty has diminished. That comes from two sources. At really low prices, you've got to secure particularly your marginal operations. At plus $300/oz, we have less need for hedging, so we've taken 300t out of our hedge and are more exposed to the upside. Equally our operations are running well and so we need less insurance.

The second major change and the best news of 2002 is that the higher Rand gold price has liberated a whole lot of reserves in South Africa. South African orebodies are more defined by exchange rates and gold prices than by geology. We are looking at six new projects contributing 11Moz. Suddenly our guys in South Africa are walking tall again, they can see expansion and growth. We've come to the end of contracting, selling and closing and are planning major, new 20-year long projects.

Bobby: I don't think we're ever going to become theological anti- hedgers. When we started five years ago it was a very gloomy time for a gold company. We said to investors, "give us your money and we'll make you rich". One of our arguments was that we were going to pay a decent dividend. Throughout that period, we paid a dividend that has fluctuated in Dollar yield terms between 4% and 7%. So anybody holding AngloGold shares has got a yield of at least 4% in cash, plus capital appreciation. To do this we needed a certain amount of revenue certainty.

I do think that excessive hedging has contributed to price weakness. Australian producers have hedged up to 100% of their reserves. That is excessive.

We don't want to be excessive hedgers; we don't want to sell everything at the spot perhaps somewhere in between.

Bobby: From a management perspective we ask ourselves two simple questions: What can we manage? What can't we manage?

Bobby: When we started seven years ago, we had two revolutionary ideas.

Interview with

Bobby Godsell

Chief Executive Officer

V

ANGLO GOLD LIMITED ANNUAL REPORT 2002

For over a decade-and-a-half people have argued that gold has lost its glister, that gold is no longer a store of value, that gold is something that only primitive people want and hold, that the Dollar will be strong forever, that US equity markets will grow by 30% a year forever. That has gone away.

8

We can't manage the price. We can't manage the exchange rate. What we can manage are the costs and so our target is that we will keep our cost increases in South Africa to two-thirds of the country's inflation rate.

INTERVIEW WITH THE CHIEF EXECUTIVE OFFICER

9

ANGLO GOLD LIMITED ANNUAL REPORT 2002

First, that people should make money out of owning gold stocks in bad times as well as good. We say that at low gold prices we are going to generate cash, make profits and pay dividends. At high gold prices we are going to generate more cash, make more profit and pay better dividends. Last year our dividend was up by about 68% in Dollar terms.

We then said that to do this we are going to focus on making money rather than on size.

So we went from being the biggest producer to being the second or third biggest. We very consciously sold off and shut down low-margin, high-risk producers. This took a third of South African production out of our hands from 4.7Moz to 3.4Moz. Last year we produced 15% less gold and made 20% better headline earnings.

So it was a shift from volume to value. And it was very necessary. We had an asset portfolio that was exceedingly high risk, with very old mines, remnant mining, and variable grades. We now have a more stable asset base with diversity in mining type 40% outside of South Africa and 40% from surface and shallow operations.

Now we are looking at growth and it is still growth in earnings. What is true is that if you want to grow your earnings, you have also got to grow your volume of mining.

Alec: The strategy, though, must have taken some kind of a diversion with the disappointment of not being able to acquire Normandy? Bobby: Normandy would have been a company character- changing transaction. I regret very much we couldn't get it. The appeal for me of Normandy is that it would have combined the leading Australian and South African companies into one of such size, such robustness, with such a strong balance sheet and such good assets, that any North American investor would have had to take notice of it.

This is against a background where everybody says most mergers and acquisitions destroy wealth rather that create it. We certainly got to the point where, had we gone another five cents on our offer, we would have been destroying wealth.

What does please me is that since then our company has done

well. Our share has traded very well in the United States we now trade there in value terms, at five times what we do in Johannesburg. And our Johannesburg values haven't gone down; it's the US value that has gone up.

Alec:

An issue that affected all mining companies in South

Africa over the past year was the Mining Charter. You were

pretty involved.

Bobby: To achieve an industry that is broadly representative of

our country, that looks like South Africa, is a good thing. I have

been concerned that empowerment should be broad rather than

narrow, benefiting many rather than a few, and that it should be

real. You can put somebody's name on a transaction, but if they

don't really have anything at risk, then they aren't, in truth,

owners. We have to make more money in South Africa, not

merely redistribute it. So ownership as a generator of wealth

is important.

Against those criteria, the Charter looks to me to be very good. It covers a wide range of issues, things incidentally that AngloGold has been doing for a long time.

What the Charter is turning out to be is a test of the social licence. A business will only survive if it benefits all of its stakeholders over time if people, the community, customers, employees and shareholders are left better off having an association with the company. I think it's a very good document and is going to make the South African industry more competitive, not less, and lead to greater wealth creation, not less. To draw on the gene pool of 100% of South Africa, not just white males, has got to be a good thing.

Alec:

Out-and-out capitalists would disagree with the assertion that

inclusivity will make you more competitive.

Bobby: With respect, I think that out-and-out capitalists, unless

they're racists, have no reason to do this. Read the Charter,

sentence by sentence, and ask yourself the question: If this is

done well, if it's done in a real way, if it's done with integrity, will

this create more wealth or less wealth?

It's quite clear from the Charter that assets should change hands at fair market value. That phrase is used repeatedly. We have done three major empowerment transactions and sold off about a quarter of our production ounces. We haven't lost one cent in terms of value. There is no Father Christmas in this Charter, there's no giving things away.

Also, as we move to many more black managers, I expect those managers to perform. You can't put somebody in charge of a deep level gold mine unless he's really competent. Frankly, to have half of our managers able to speak fluent seSotho or Xhosa has got to lead to greater productivity. We know that when we combine literacy and new job structures, we see a 25% increase in the output of those teams.

Alec: What about the cost or the value of ounces in the ground? South African gold ounces have made progress compared to other parts of the world. But they do still lag?

Bobby: Gold companies trade at a premium to their net asset value. It's true that some of the North Americans trade at a larger premium. That premium is one of two things. It's either a bet on the gold price or it's the view that management is smart enough to buy new mines, prove up new reserves.

I am happy to accept the challenge for AngloGold that we will grow the company in terms of profitable ounces into the future. I am not terribly worried about competing with the North Americans.

Alec: Last year you said you were going to significantly increase your investment in exploration.

Bobby: We have, through two different strategies. Brownfields exploration means you are drilling for ounces where you already have infrastructure. They are very nice ounces because if you find more, you don't have to spend capital to sink the shaft or build the plant. Particularly with open-pit mining, companies often starve the brownfields budget and only drill to have the certainty for another six or 12 months of production. Every Dollar we spend in brownfields exploration wins reserve ounces. Our exploration budget is about $60m - two thirds of that is brownfields.

Greenfields is different. I can only explain it in non-technical terms. It's about God's sense of humour, because God put gold in interesting places. He didn't put it in Switzerland or Singapore. So we look for gold in new and interesting places we have just opened an office in Mongolia.

We have a map that tells us in terms of basic geological theory where you could expect major gold mineralisation through different mineralisation processes. It's a disappointing map, because a large part of the world is prospective. It would be super if you could only concentrate on two or three places. China

and India ought to be very prospective. Places that have been poorly surveyed, poorly explored, obviously hold quite a lot of potential. We are very excited about Peru, about the Great Lakes area of Africa.

In greenfields exploration you have to take some risks - you have got to try 20 things and expect 19 of them to fail.

Alec: Could there be another Wits Basin out there?

Bobby: It's hard to believe that it's entirely unique. We do understand the Basin extremely well. We have looked in other parts of the world; we understand the palaeontological and ageing-of-the-earth signmarks. It would be wonderful to find another. We are delighted to find any decent orebody that we can make money out of.

Alec: What about Australia? Do you think there could be a big find waiting there?

Bobby: We are very excited about two orebodies that we have interests in.

At Sunrise Dam mine, we have dramatically expanded the size of that open-pit operation and are immensely excited about the brownfields potential. Every time we put the drill down we come up with excellent results. I would be very surprised if we didn't significantly extend its life going forward.

The Boddington project is one of the largest and longest life

gold orebodies in the world. We share that with Newmont, who succeeded Normandy in ownership, and Newcrest, and we are trying to find the right model to expand it.

Alec: An area where you do have a distinct advantage that you have already turned to account is on the continent of Africa.

Bobby: It's our continent, it's our home. The great thing about South Africans is that they understand about cultural diversity. We are a world in one country and no manager can assume that he knows what the people who work with him think. He's got to take the effort to find out. It's been wonderful to see Afrikaners from the Free State go to Morila in Mali, an Islamic country, French-speaking, and turn out to be very good leaders of people.

Equally, we are completely committed to developing talent

from those countries. Mali has had no modern mining history. We are running three world-class mines there with overwhelmingly local people.

Alec: There's been criticism of South African gold companies for decades about not beneficiating. A couple of years ago you made a move into this field by the acquisition of a company called OroAfrica - a reconnaissance investment. How has that turned out?

Bobby: It has done pretty well. This was part of the journey we started on seven years ago.

It's very interesting that the first sentence of every conversation about gold is a conversation about price. It's indicative of an industry that hasn't grown up, because industries don't do well because of price, they do well because of profit. The auto industry and other industries are not fascinated by price. They are interested in sales, consumers and customers.

INTERVIEW WITH THE CHIEF EXECUTIVE OFFICER

ANGLO GOLD LIMITED ANNUAL REPORT 2002

10

INTERVIEW WITH THE CHIEF EXECUTIVE OFFICER

11

ANGLO GOLD LIMITED ANNUAL REPORT 2002

The gold industry is not very customer oriented. An industry that forgets its customers will, and deserves to, go out of business. The customers of gold are overwhelmingly people who buy jewellery - 80% of 4,000t of annual production goes into jewellery.

For the last five years we have been looking at the customer and we would like to be part of modernising gold jewellery. This is an industry that got stuck in the 19th century. Going into OroAfrica was to find out about the customer. Here we had a modern factory located in our own country, making particularly gold chain and other machine-initiated gold jewellery, earrings and pendants, in alliance with the leading Italian gold jewellery manufacturer (Filk). OroAfrica uses about 5t of gold a year; Filk uses about 70t of gold. It's huge business.

It's still early days. What we'd like to do for gold is to be the Benetton of the gold industry, to be the Starbucks of jewellery. Coffee drinking was in decline in the United States. People thought it was unhealthy. But Starbucks has come along and persuaded people to pay $3 for a cup of coffee with foam in it, when they could have the same thing for 50 cents. That completely changed the market and consumption is going up. That's what we want to do, we want to revolutionise what we offer our customers.

Alec: Starbucks has branded coffee. Can AngloGold brand gold?

Bobby: Starbucks has also reinvigorated the entire category. If you go to to any modern city, you will find 15 Starbucks look-alikes - a place that looks nice, where you can pay a very high price for a fancy cup of coffee and where you have to learn a new language to order it. They've invented a new experience.

We think we can re-invent gold jewellery, whether it is the AngloGold brand or anything else. Coming from where we do, we would very much like to have an African brand. But equally we have been experimenting with Brazilian jewellery.

Gold is about people, particularly in Africa, it's about peasant life, it's about kings, the country, something that has been around for 5,000 to 7,000 years; part of the earth; part of the rich cultural heritage. If we draw on that, we think we can put a jewellery offer in the marketplace which is distinctly different to the dull, 19th century jewellery store offer that we have had.

Alec: Looking ahead, is it a year when AngloGold shareholders can expect similar progress as in the year behind. Bobby: We have never been in the business of predicting the gold price and to some extent, inevitably, our equity price is linked to the gold price.

We are going to mine 6Moz of gold, we are going to mine it at a good cost, we are going to generate a lot of profit and we would be hoping to pay a really decent dividend. We hope that our price reflects the benefit of that, particularly over time.

We listed on the New York Stock Exchange in 1998 at $16 we - are now trading at around $32 so there has been good capital appreciation. Last year a holder of an AngloGold share would have seen a total return, including dividends, of close to 100%. Whether we are going to see the gold price shoot up as dramatically this year as it did last, I don't know. But what we can say to our shareholders is, "hold our shares, over time and at any moment in time, you have made good money". And at the very least, we are going to pay a good dividend.

Alec: If we speak in a year's time, strategically what milestones would you like to have behind you.

Bobby: Two major things:

I am assuming operational excellence; I am assuming we will mine gold very profitably.

Over and above that I would hope that we would be further

down the road in growing our ounces. We want to say to shareholders that this is not a wasting-asset industry. Your piece of AngloGold paper is worth something today, it will be worth something to you in five or 10 years' time, we would like you to leave it to your kids. We have got to grow our earnings.

Then I would love to have something dramatic and interesting to say about going downstream, modernising the customer base and finding ways to expand the jewellery market, maybe even making some money out of that side of the business.

Alec: And mergers and acquisitions?

Bobby: All the time and ongoing, but only if they add value. We haven't had a year where we haven't done something, but it is opportunistic. I hope that we have the courage to go after every deal and I hope we have the wisdom only to do those deals that make money for our shareholders.

The full interview is available in video, audio and transcript form on the AngloGold website

at www.anglogold.com

We are going to mine 6Moz of gold, we are going to mine it at a good cost, we are going to generate a lot of profit and we would be hoping to pay a really decent dividend. We hope that our price reflects the benefit of that, particularly over time.

12

ANGLO GOLD LIMITED ANNUAL REPORT 2002

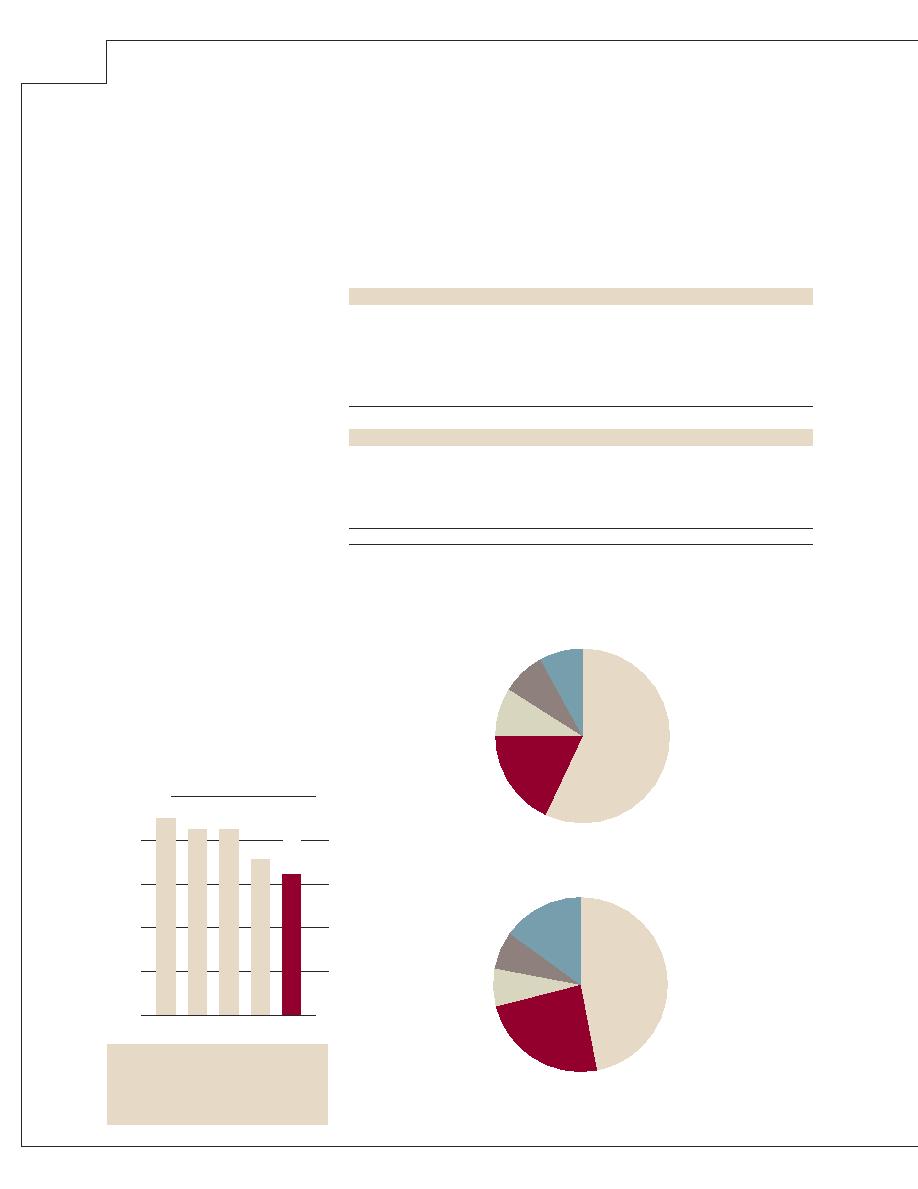

Group value-added statement

for the year ended 31 December 2002

Figures in US Dollars millions

Notes

%

2002

%

2001*

Value added Turnover

2

1,761

2,041

Less: Purchases of goods and services in order to operate mines and produce refined metal, including market development costs net of other income

(611)

(746)

Value added by operations

90

1,150

98

1,295

Non-hedge derivatives

7

92

(5)

Income from investments and interest received

6

3

43

2

26

100

1,285

100

1,316

Value distributed Employees Salaries, wages and other benefits

10

35

443

48

627

Government

11

13

165

8

111

- Current taxation

14

177

8

103

- Deferred taxation

(1)

(12)

8

Providers of capital

- Finance costs

8

3

44

5

72

- Dividends

13

20

251

13

167

- Minorities

1

15

1

8

Other

- Loss on disposal of mines

31

1

13

4

Total value distributed

73

931

75

989

Re-invested in the Group

- Amortisation and depreciation

14, 15 & 16

21

273

19

249

- Retained income

6

81

6

78

100

1,285

100

1,316

* Includes Free State assets

State for taxes

$111m or 8%

Providers

of capital

$247m or 19%

Re-invested

in the group

$327m or 25%

Employees for

remuneration

$627m or 48%

Other $4m or 0%

2001 Distribution of wealth*

Employees for

remuneration

$443m or 35%

State for taxes $165m or 13%

Providers of capital

$310m or 24%

Re-invested

in the group

$354m or 27%

Other $13m or 1%

2002 Distribution of wealth

13

ANGLO GOLD LIMITED ANNUAL REPORT 2002

The factors which drove the gold price during 2002 had a particularly strong impact in the final quarter. These factors included US Dollar weakness, international political tension, equity market declines and a halt to the dismantling of producer hedging. This last factor had the effect of both lowering gold producer selling in the spot market, and introducing some buying in the market. During the final quarter of the year, the price was influenced most significantly by Dollar weakness and by escalating conflict over Iraq. Over the past year, the spot price has responded almost perfectly to the Dollar's fall against the Euro (see graph). The additional tension in the Middle East provided the lift to take gold up further. All of the factors that have been positive for gold in 2002 remain firmly in play, and there is good reason to expect higher gold prices in the year ahead.

Under the favourable price performance of gold, the physical market continued to show weakness throughout 2002. There has been a general decline in physical demand for gold in both the jewellery and the investment sectors, with exceptions in only a few countries. Compounding the effects of this lower demand, scrap sales and gold recycling have increased sharply in the face of higher gold prices. The negative impact of these factors in the physical market was mitigated to a degree by slightly lower new mine production, and by the reduction in supply occasioned by the run-down in gold producer hedging referred to above. As is the case in all periods of rising gold prices and gold price volatility, the physical market should revive once the price returns to a stable trading range for a period of time. However, with further gold price volatility expected in 2003, a resurgence of physical demand should not be expected immediately.

A critical factor in the strength of the gold market in 2002 has been the return of investor and speculator interest in the metal. This interest has not translated particularly into demand for physical gold, but can most certainly be seen in the derivative markets, and particularly in the futures and options positions on the New York Comex and, from time to time, on the Tokyo Comex. There is no doubt also a considerable over-the-counter derivative trade in gold, although this is not easily measured. The importance of this gold buying in the derivatives markets for the

gold price can be seen from the graph, showing gold trading positions on New York Comex from the beginning of 2000, and the US Dollar spot price of gold. Buying in the derivatives markets is directly influenced by the factors referred to above, and is directly responsible for moving the price of gold.

Review of the

gold market

T

14

Results for the year

• Headline earnings before unrealised

non-hedge derivatives increased by 29% to $368m or 166 US cps (2001: $286m or 133 US cps).

• Return on capital improved from

13% to 15%.

• Return on equity increased from

16% to 21%.

• Gold production was down 15% to

5.9Moz, mainly due to the sale of the Free State assets.

• Total cash costs declined by 10%

to $161/oz.

Dividends

A final dividend of R6.75 per share ($0.82 per share) was paid, bringing the total dividend for the year to R13.50 per share ($1.46 per share). This dividend represents a yield of 4.4% calculated on a share price of R305 on 30 January 2003. This level of dividend is consistent with AngloGold's established practice of paying out a high proportion of its earnings to shareholders, once it has provided for its organic growth objectives.

Gold production

Gold production was down 15% (1.04Moz) to 5.9Moz. This is mainly due to the South Africa region's sale of the Free State assets, Elandsrand and Deelkraal. If these are excluded, the group's production would have increased by 3% or 190,000oz.

The Free State contributed 1.2Moz and Elandsrand and Deelkraal contributed 35,000oz in the prior year.

With reference to the disposals mentioned above, South Africa's production is 27% lower than 2001 at 3.4Moz.

Production in the East and West Africa region increased by 25% or 217,000oz to 1.08Moz. The main contributors were at Morila (+169,000oz) due to a 74% increase in recovered grade to 11.96g/t; Yatela (+55,000oz) as 2002 was the first year of full production; and at Geita (+17,000oz) arising from increased tonnage throughput. Decreased production was recorded at Sadiola (-22,000oz) where there was lower grade and tonnage throughput.

The North America region's production decreased by 7% or 34,000oz to 462,000oz. Cripple Creek's production was 11,000oz up on the prior year due to the expansion of the crusher and absorption circuit. Jerritt Canyon's production was 45,000oz below that reported in the prior year, because of adverse weather conditions, and completion of the Cortez tolling agreement and lower recovery issues.

South America's production increased by 37,000oz to 478,000oz. This is mainly attributable to the additional 46.25% interest acquired in Cerro Vanguardia. If the additional interest were ignored, production would be 5% lower than the prior year due to production problems at Cerro Vanguardia arising from recurrent underground water in the pits causing mining of wet ore with a very high level of clay.

Australia's production decreased by 6,000oz to 502,000oz. This is mainly as a result of the closure of operations at Boddington and Tanami, which was partially offset by a 29% or 87,000oz increase in production at Sunrise Dam made possible by the mill upgrade.

Gold income

The average gold price received increased by 6% to $303/oz in 2002. See Review of Gold Market on page 13.

Gold income together with realised non-hedge derivative income declined by 10% or $205m during the 2002 financial year to $1,841m ($2,046m). This is in line with lower production, but partially offset by a higher price received. The current year's received price is $16/oz higher than that for the previous year at $303/oz and compares to an average spot price of $310/oz.

Cost of sales

Cost of sales, comprising total cash costs, retrenchment and rehabilitation costs, changes in gold inventories and amortisation of mining assets, went down from $1,519m in 2001 to $1,203m in 2002, a decrease of 21%, analysed as follows:

Total cash costs decreased from $1,255m in 2001 to $967m in 2002 (or $178/oz to $161/oz), following the reduction in gold produced from 6.983Moz in 2001 to 5.939Moz in 2002. Of the $17/oz reduction in cash costs year on year, $24/oz related to the weakening of the SA Rand against the US Dollar. Excluding the Free State operations in the prior year, total cash costs decreased by 5% from $170/oz to $161/oz.

•

While retrenchment costs were $22m in 2001 (with most of the costs being associated with the Free State) they decreased to $3m in 2002.

•

Rehabilitation and other non-cash costs decreased by $1m on the previous year whilst amortisation of mining assets increased by 11% to

Financial

review

A

ANGLO GOLD LIMITED ANNUAL REPORT 2002

15

$245m. South Africa's amortisation of mining assets reduced $15m to $61m, mainly due to the sale of the Free State operations and the devaluation of the SA Rand. The lower amortisation charge in South Africa was offset by the higher amortisation charges in East and West Africa due to increased levels of production, and in North America as a result of accelerated amortisation charges on the old crusher assets.

Inventory movement was a $9m charge in 2001 compared to a credit of $24m in 2002. The increase in inventory levels on the previous year is mainly due to the increase in gold in process in the North America region. This is as a result of the ongoing problems with extracting gold from the heap leach pad resulting in a build up of inventory.

Operating profit

Operating profit excluding unrealised non-hedge derivatives is 21% up on the previous year at $638m. This is mainly due to a 6% increase in the received Dollar gold price, and a weaker average Rand/Dollar exchange rate. Included in this operating profit is an amount of $80m relating to realised gains on non- hedge derivatives.

The main reason for the $111m increase in operating profit is the weaker Rand/Dollar exchange rate ($143m), offset by $24m caused by lower grades.

The operating margin for the AngloGold group was 35% for 2002 and 26% for 2001. The EBITDA margin was 43% in 2002 compared to 33% in 2001. These margins vary from operation to operation and are summarised on page 16.

Net profit

Net profit of $332m (2001: $245m) is arrived at after making, amongst others, the following adjustments to operating profit:

Corporate and other administration expenses increased by $3m on the previous year to $25m.

Market development costs amounted to $17m for the year of which some 80% was paid to the World Gold Council.

Total exploration expenditure was $51m (2001: $44m) of which $28m (2001: $26m) was expensed.

Interest received increased from $20m to $36m, mainly as a result of the improved gold price and improved cash position with the sale of shares acquired in the aborted bid of Normandy and the proceeds from the Free State sale.

Other net expenses amounted to $16m for the year and included the unwinding of the decommissioning obligation, foreign exchange losses on transactions other than sales, and post-retirement medical expenses relating to mines sold.

Finance costs decreased by $28m to $44m, due to lower interest rates and the rearrangement of the loan facility debt. The proceeds on the sale of the Normandy investment were utilised to repay debt.

An abnormal item relating to thesettlement of a legal claim in the amount of $10m $5m net of tax.

Goodwill amortised remained fairlyconstant at $28m compared to 2001.

A loss on disposal of the Free State

assets of $13m was recognised in 2002. During 2001, a loss of $4m was recognised in respect of the sale of assets at the Deelkraal and Elandsrand mines.

The taxation charge increased by $54m to $165m in 2002, owing mainly to an increase in earnings for the year. The effective tax rate is 32% compared to 30% in 2001.

The minorities share of earnings has increased to $15m compared to $8m in the prior year. This is due to the increase of minorities in Cerro Vanguardia from 3.75% to 7.5%.

Cash flow

OPERATING ACTIVITIES

Cash generated from operations was derived from profits on ordinary activities before taxation of $512m per the income statement, adjusted for changes in working capital and non-cash flow items. The most significant non-cash flow item was the amortisation of mining assets of $245m.

Finance costs of $40m; and

Mining and normal taxes of $131m.

INVESTING ACTIVITIES

Funds of $605m generated from operating activities were utilised to grow the group by investing in capital projects amounting to $271m. Major project expenditure in 2002 comprised:

Moab Khotsong $36m;

Mponeng $33m;

TauTona $11m;

Cripple Creek & Victor Expansion

$66m; and

Sunrise Dam Project $26m.

The funds generated from operating

activities were further adjusted by:

$164m which was received for the disposal of the Free State assets, of which $24m was paid for contractual obligations;

$34m which was paid for investments, the major portion of this being Normandy;

$158m which was the proceeds on the sale of the Normandy investment;

$97m which was the net cash consideration paid for the 46.25% additional interest in Cerro Vanguardia.

FINANCING ACTIVITIES

During the year, $585m was drawn and $120m was repaid on the three- year $600m syndicated loan facility. On the existing $400m syndicated loan facility, $175m was drawn.

Major loans repaid include $121m to Credit Agricole, $355m on the matured syndicated loan facility and $128m on the $400m syndicated loan facility. Other repayments comprise normal scheduled payments in terms of loan agreements.

FINANCIAL REVIEW

ANGLO GOLD LIMITED ANNUAL REPORT 2002

16

With effect from 1 January 2002, the Free State assets were sold to a joint venture

On 3 October 2002, the President of South Africa signed the Mineral and Petroleum Resources Development Act 2002. The provisions of this law will come into operation on dates to be specified by the President, who may stipulate different dates for different provisions. It is

FINANCIAL REVIEW

ANGLO GOLD LIMITED ANNUAL REPORT 2002

2002

Gold

Operating

Operating

income

profit*

margin

EBITDA

EBITDA

$m

$m

%

$m

margin %

South Africa

930

389

38.8

373

37.2

East and West Africa

329

129

39.2

190

57.8

South America

195

84

42.1

118

59.2

North America

152

3

1.9

59

38.1

Australia

155

33

21.3

55

35.5

Total

1,761

638

34.7

795

43.2

2001

Gold

Operating

Operating

income

profit*

margin

EBITDA

EBITDA

$m

$m

%

$m

margin %

South Africa

1,298

341

26.1

351

26.9

East and West Africa

250

87

34.8

134

53.6

South America

177

65

36.1

98

54.4

North America

161

16

9.9

58

36.0

Australia

155

18

12.2

38

25.7

Total

2,041

527

25.8

679

33.2

*

Operating profit excludes unrealised non-hedge derivatives.

17

FINANCIAL REVIEW

ANGLO GOLD LIMITED ANNUAL REPORT 2002

2002

2001

2000

1999

1998

Underground operations Area mined

- m

2

000

2,116

3,043

3,900

3,880

4,275

Metric tonnes milled

- 000

total

13,426

17,954

21,293

21,704

23,396

Yield

- g/t average

8.27

8.20

7.96

8.09

8.08

Production

- oz 000

total

3,569

4,734

5,451

5,643

5,821

Productivity g/employee

target

247

219

209

222

174

actual

238

214

193

210

184

Surface and dump reclamation Metric tonnes treated

- 000

38,366

50,355

50,289

54,354

57,511

Yield

- g/t

0.30

0.32

0.32

0.30

0.30

Production

- oz 000

365

514

510 520

547

Open-pit operations Metric tonnes mined

- 000

109,987

85,790

49,121 47,880

7,525

Stripping ratio

- t (mined-treated)/t treated

3.05

2.17

1.08 2.51

1.63

Metric tonnes treated

- 000

27,186

27,042

23,601 13,630

2,863

Yield

- g/t

2.29

2.00

1.69 1.72

2.54

Production

- oz 000

2,005

1,735

1,28 2 755

234

Total Production

- oz 000

5,939

6,983

7,24 3 6,918

6,602

- South Africa

- oz 000

3,412

4,670

5,418

5,746

6,368

- East and West Africa

- oz 000

1,085

868

366

262

234

- North America

- oz 000

462

496

496

485 -

- South America

- oz 000

478

441

439

425 -

- Australia

- oz 000

502

508

524 - -

Price received*

- $/oz sold

303

287

308

315

333

Total cash costs

- $/oz produced

161

178

213

213

225

Total production costs

- $/oz produced

203

213

245 244

259

Monthly average number of employees

53,097

70,380

84,036 86,120

93,316

LTIFR

8.86

10.55

11.58 13.91

14.52

Rand/US Dollar average exchange rate

10.48

8.62 6.78 6.11

5.53

Financial results $m Operating profit

650

517

468

505

469

Operating profit excluding unrealised non-hedge derivatives

638

527

468

505

469

Net profit

332

245

166 434

318

EBITDA

795

679

608 614

566

Headline earnings

376

281

254 325

277

Headline earnings before unrealised non-hedge derivatives

368

286

254 325

277

Capital expenditure

271

298

304 220

174

Financial ratios Capital employed

- $m

2,994

2,550

3,119 3,354

2,149

Return on capital

- %

15

13

10 15

13

Equity - $m

2,082

1,559

2,006 2,576

2,057

Return on equity

- %

21

16

11 16

12

Debt - $m

926

987

1,156 828

184

Cash - $m

413

191

195 493

254

Net debt (cash)

- $m

513

796

961 335

(70)

Net debt (cash) to capital employed

- %

17

31

31 10

(3)

Net debt (cash) to equity

- %

25

51

48 13

(3)

Interest cover

- times

18

9

9

12

23

Operating margin

- %

35

26

21

23

21

EBITDA margin

- %

43

33

28

28

25

Glossary of terms on page 138. * Including realised non-hedge derivatives

Group operating and financial results

The safety and health of employees remains a key area of focus for the company. Performance on the safety and health front was encouraging in some areas and disappointing in others.

18

Review

of

operations

A

ANGLO GOLD LIMITED ANNUAL REPORT 2002

AngloGold's Lost Time Injury Frequency Rate

(per million man hours)

(Clockwise from top left) Metallurgical test work pouring fused material from a gold fire assay in Kayes laboratory in Mali, East and West Africa region;

Severe weather conditions at Jerritt Canyon caused a slow start to the year in the North America region; This flotation tank at Ergo, South Africa, has the

capacity to treat 100,000t of slimes a day; Hydro-powered rockdrill operated by Ephraim Mabeia at Tau Lekoa mine, South Africa region; Stream sampling by

geologists in the Peru exploration division; Gold production rose significantly at Sunrise Dam, Australia region, during the year.

2002

2001

South Africa

9.98

11.58

East & West Africa

2.93

1.30

South America

4.21

8.16

North America

4.95

1.58

Australia

11.22

13.47

Group

8.86

10.55

0

2

4

6

8

10

12

14

16

1998 1999 2000 2001 2002

8.86

20

The massive fridge plant at Moab Khotsong in South Africa.

and developing a safety mindset. To assist in creating this safety mindset, an external consultant DuPont has completed an assessment of the company's operations and an in-house team has been established to tackle the implementation of this campaign. AngloGold's HIV/AIDS programme is dealt with on page 23.

Performance

Highlights for the year from an operational perspective include the sterling performance of the East and West Africa region, which increased attributable production by 25% to 1,085,000oz, at a total cash cost of $126/oz.

Further progress was made in AngloGold's drive for geographical and orebody diversity. Gold production from outside South Africa, principally from low-cost surface and shallow mines, rose to 42% of production, 39% of operating profit and 53% of EBITDA.

Overall, attributable production decreased to 5.94Moz, mainly as a result of the impact of the sale of the Free State assets. This was partially offset by an increase in production from the remaining operations of about 3%.

Good cost control was undermined to some extent by the strong performance of the SA Rand in the second half of the year. Nonetheless, total cash costs in Dollar terms decreased still further by 10% to $161/oz. As a result, operating profit increased by 21% to $638m.

Capital expenditure during the year amounted to $271m of which $95m was attributable to maintenance and $176m to expansion.

Outlook

Looking ahead, production is expected to remain unchanged in 2003 at 6Moz, while

total cash costs are expected to rise to $187/oz, largely due to the strengthening of the South African currency and the lower average grade being mined. The latter is directly related to the fact that lower grade areas have become profitable as a result of a rise in the gold price. Capital expenditure is forecast at $303m.

REVIEW OF OPERATIONS

ANGLO GOLD LIMITED ANNUAL REPORT 2002

$/oz

0

50

100

150

200

250

1998 1999 2000 2001 2002

Total cash costs over time

Total cash costs have declined steadily

over the past five years. However, an

increase is expected in 2003 to $187/oz.

TOTAL CASH COSTS PER REGION ($/oz)

2002

2001 Variance %

South Africa

158

184

(14)

East and West Africa

126

129

(2)

South America

126

134

(6)

North America

222

211

5

Australia

193

194

(1)

Group

161

178

(10)

ATTRIBUTABLE PRODUCTION (000oz)

2002

2001 Variance %

South Africa

3,412

4,670

(27)

East and West Africa

1,085

868

25

South America

478

441

8

North America

462

496

(7)

Australia

502

508

(1)

Group

5,939

6,983

(15)

South Africa 58%

East & West Africa 18%

Australia 8%

South America 8%

North America 8%

Contribution to production (oz) by region

South Africa 47%

Australia 7%

South America 15%

North America 7%

East & West Africa 24%

Contribution to EBITDA by region

161/oz

22

REVIEW OF OPERATIONS

ANGLO GOLD LIMITED ANNUAL REPORT 2002

Safety and health

Tragically, 39 employees lost their lives in mine accidents during the year. This include 11 employees who lost their lives in three multiple fatal seismic accidents at Great Noligwa and Savuka. As a result, the FIFR rose to 0.34 in 2002 from 0.28 the previous year.

The primary cause of fatal accidents remains falls of ground, which caused 57% of fatal accidents during the year. A high- profile Fall of Ground Safety Campaign was launched during the first quarter of the year in an attempt to increase awareness associated with particularly non-seismic falls of ground, and this campaign has largely been successful. Transport-related accidents were the second biggest problem

* TauTona mine, despite operating at ultra-deep levels, has not had a rockfall-related accident since September 2001, and continues to post accident frequency rates similar to those of AngloGold's surface operations. TauTona

Ergo

West Wits TauTona Savuka Mponeng

Vaal River Tau Lekoa Kopanang Great Noligwa Moab Khotsong

South Africa

AngloGold's operations in South Africa

Key statistics

2002

2001

Tonnes treated (Mt) Underground

11.3

15.3

Surface (incl Ergo)

38.4

50.3

Average grade (g/t) Underground

8.40

8.20

158

184

R/kg

53,146

50,065

Number of employees*

Efficiencies g/TEC

223

206

m

2

/TEC

4.58

4.42

Capex $m

105

101

Rm

1,150

875

* Including contractors

Inundation

Slip and fall

Explosives

5%

2%

2%

Causes of fatal accidents - 2002

The primary cause of fatal accidents on the South African operations is falls of ground.

A major campaign to address this was initiated during the year.

23

REVIEW OF OPERATIONS

also won the South Africa region Safety Shield Competition for the best improvement in serious injury rates over the past five years.

* After the tragic multiple fatal accidents in May and June, Great Noligwa mine went on to achieve a million fatality- free shifts on 27 November 2002.

Occupational health

The primary concerns in respect of occupational health in the South African operations are noise-induced hearing loss (NIHL), occupational lung diseases (OLD) and tuberculosis (TB).

Occupational health services are provided to employees at two fully- equipped regional occupational health centres. These are staffed by occupational medical practitioners, professional nurses, audiologists and other support staff.

In addition, each mine has an occupational health nurse on site.

During the year, 52,742 occupational medical surveillance examinations (initial, periodical, transfer and exit) were performed. There were 1,087 new cases of NIHL in 2002. This translates into a rate of 26 per 1,000 employees, compared with 12 per 1,000 in 2001. Regarding OLD, 186 employees were diagnosed, reflecting a rate of 4 per 1,000 employees, the same rate as in 2001; 983 new cases of TB were treated in 2002, a rate of 23 per 1,000 employees, also the same rate as in 2001.

Stricter screening for NIHL, in preparation for a new compensation rule requiring base-lining of all employees, has meant an increase in the NIHL rates, which are now expected to fall off. No increase in liability is anticipated.

AngloGold continues to make advances in the control of underground dust. New and more accurate measuring methods have been introduced; better engineering practices are evident; a more standard approach to respiratory protective equipment has been implemented and employees detected as having very early OLD are moved to lower risk areas.

TB remains an area of focus in the sphere of occupational health. More effective detection methods are resulting in earlier diagnosis and treatment, which is limiting the onward transmission of the disease.

HIV is the major factor contributing to increased TB rates in South Africa. It is expected that the HIV Wellness Programme and introduction of anti- retroviral therapy (ART) by AngloGold (see HIV below) will have a positive impact on the TB problem and a project aimed at preventing transmission of TB, through mass prophylaxis, is planned for 2003.

HIV/AIDS

The prevention of HIV/AIDS infections

and the compassionate care of those

afflicted with the disease remains a

priority for the South Africa region.

AngloGold's core intervention comprises

four elements, namely:

Moab Khotsong

6.82

4.65

0.19

0.17

SAFETY STATISTICS

2002

2001

2000

1999

1998

FIFR

0.34

0.28

0.24

0.38

0.41

LTIFR

9.98

11.58

11.98

14.35

15.18

The South African operations performed

creditably in the year under review, despite a

slow start. If the Free State operations are

excluded from last year's production numbers,

production for the South Africa region

decreased by 1%.

ANGLO GOLD LIMITED ANNUAL REPORT 2002

24

The South African operations performed well for the year under review, despite a slow start at the beginning of the year and significant seismic events at Great Noligwa mine. Overall gold production declined by 27% to 3,412,000oz, a result of the once-off decrease of 1,232,000oz (26% on last year) attributable to the sale of the Free State assets. If the Free State operations are excluded from last year's production numbers, production decreased by 1% due to the drop in production at Ergo. Total cash costs decreased by 14% to $158/oz, and even in Rand terms were well controlled to a 6% increase to R53,146/kg. This was despite an inflation rate of approximately 12% during the year. Productivity, in terms of the two main indices used namely g/TEC and m /TEC improved by 8% to 223 and 4% to 4.58, respectively.

REVIEW OF OPERATIONS

ANGLO GOLD LIMITED ANNUAL REPORT 2002

GREAT NOLIGWA

REVIEW OF OPERATIONS

ANGLO GOLD LIMITED ANNUAL REPORT 2002

TauTona 25%

Kopanang 14%

25

26

REVIEW OF OPERATIONS

TAU TONA

TauTona continued with its strong performance during the year, with gold production rising by 3% to 643,000oz, or 19,997kg. Total cash costs decreased to $132/oz. In Rand terms, however, this reflected an increase of 5% to R44,465/kg.

Performance at Mponeng improved significantly during the year, with volumes mined increasing by 21% and yields rose to 8.63g/t. Although newly equipped raise lines had an impact on costs during the year, the

As anticipated, gold production decreased by 20% to 264,000oz, or 8,215kg, following the closure of the Daggafontein plant in December 2001. During the year, the operation was affected by higher- than-expected rainfall, environmental clean-up activities and power failures. The effects were offset by improved headgrades and increased metallurgical efficiency. Total cash costs decreased by 15% to $184/oz. In Rand terms, total cash costs increased by 5% to R61,810/kg.

Moab Khotsong

The largest project under development in the

South Africa region is the Moab Khotsong

mine, located in the Vaal River area.

Production is scheduled to commence in late

2003 , with full production expected in 2006.

The mine will add 4.5Moz to the region's

production to 2015, at an average cash

cost of $129/oz.

ANGLO GOLD LIMITED ANNUAL REPORT 2002

27

REVIEW OF OPERATIONS

ANGLO GOLD LIMITED ANNUAL REPORT 2002

project team. The project scope includes rehabilitation, social aspects and other liabilities associated with the closure of the operation.

Growth

Three major growth projects are currently

in progress in South Africa at Mponeng,

TauTona and Moab Khotsong at a total

capital cost of approximately R5.6bn

($649.7m at current year's closing

exchange rate).

MPONENG SHAFT DEEPENING PROJECT

Good progress has been made during the year with the Mponeng Shaft Deepening Project. The project involves the development of ore reserves from the Ventersdorp Contact Reef (VCR) on 113, 116 and 120 levels at Mponeng mine (ranging from 3,172m to 3,372m below surface). The project will add some 2.8Moz to production and extend the LOM by five years to 2012. Total capex for the project is R1.3bn ($159.3m at current year's closing exchange rate) with some R318.7m remaining ($37.2m at current year's closing exchange rate). Average project cash costs over the LOM should be in the region of R55,200/kg ($180/oz at current year's closing exchange rate). In-circle development is in progress and will be completed by February 2003.

Access development on 113 level has been completed and permanent equipping began in January 2003. At 116 and 120 levels, access development is scheduled for completion in May 2003.

TauTona

VCR shaft pillar and 66 level

0.3Moz

2005

Tau Lekoa

Above 900 level

0.2Moz

2006

Great Noligwa

Great Noligwa mine contributed 26% to the South Africa region's production. This was despite

several major seismic events at the mine during the year. The underground locomotive seen here is

known as "Big Momma". Its introduction is part of the mine's Hypermine project.

28

REVIEW OF OPERATIONS

ANGLO GOLD LIMITED ANNUAL REPORT 2002

Since the South Africa region employs by far the most people, and has the largest number of operations, its community and environmental impact is greater here than anywhere else. The aim of the South Africa region is to create a balance between the impact on the natural and social environments in which it operates while at the same time ensuring that it delivers significant and lasting benefits to employees, their communities and other stakeholders, in partnership with government, international agencies, labour, health and non-governmental organisations. As a result of historical and current socio- economic imperatives, the role played by the company in social issues is significant.

An amended Environmental Management Programme Report for the West Wits and Vaal River operations was submitted to the Department of Minerals and Energy in November 2002. It is anticipated that feedback will be received on this early in 2003.

(From left to right) A pre-schooler enjoying the outside play area at the Shiloh Marabian Mission Station School in Whittlesea (a Khululeka project); Noncedile Mozondi, one of the Mabhongo villagers who was given chickens as a part of the Masikhanyise sustainable development project. Coleth du Plessis and her pupils in the new cookery centre at the North West Secondary School for the deaf in Leeudoringstad. All these projects were supported by the AngloGold Fund.

REVIEW OF OPERATIONS

29

ANGLO GOLD LIMITED ANNUAL REPORT 2002

* Klerksdorp Methodist Primary School is one of the few English-medium primary schools in one of AngloGold's key operational areas. The school's intake has grown exponentially over the past few years, to the point where new learners had to be turned away due to the lack of space. AngloGold's donation of $118,000 will enable a block of five classrooms to be added to the complex.

* The Boyden Observatory is home to the second largest optical telescope in Africa. The observatory, part of the University of the Free State's Science Block, recently initiated a project to upgrade its facilities to make them more relevant to the school curriculum and accessible to previously disadvantaged communities in the area. The long-term aim is to foster greater interest in the study of science, engineering and technology.

(From left to right) A Grade 6 pupil doing his homework in the aftercare centre at the Methodist Primary School in Klerksdorp; Ayanda Matha a pre-grade pupil enjoying the playground equipment that AngloGold sponsored for the Winterberg School Trust, Tarkastad; Elisabeth Ganakgomo preparing a quilted bedspread that will be sold to raise funds for the Mohau AIDS centre.

* Goldfields Hospice in the Free State has received a grant of $15,000. This valuable facility provides extensive community- based homecare for terminally ill patients in the Welkom area in the Free State.

* Siphumezulwazi Secondary School in Alice in the Eastern Cape has been awarded grant from the AngloGold Fund for the construction of five classrooms, a store room, an office and ablution facilities.

* The National Association of Childcare Workers in the

Eastern Cape was awarded $27,500 for the Isibindi project in Cala, in the Eastern Cape. The project provides accredited training, support and development for child and youth care workers and is aimed at assisting children and youths who have been placed at risk as a result of abuse, HIV/AIDS or criminal involvement.

* Khululeka Community Education Development Centre in Queenstown, Eastern Cape, is another project that was supported during the year. A $25,000 grant to this leading early childhood development centre will enable a comprehensive training programme to be developed to empower other early childhood development practitioners with skills, resources and values to provide quality education and care for young children. The materials developed by Khululeka are already used by many other non-governmental organisations (NGOs) who do not have the resources or infrastructure to develop their own materials.

* The African Medical Mission in the Eastern Cape received

a grant of $27,000. The hospital which is situated in the town of Bedford, caters for a third of the people in the province many of whom live in rural areas and cannot afford alternative medical facilities and care.

* Carletonville Technical College was awarded some $23,000 to purchase computers for an engineering laboratory. The college is one of only six technical colleges in the country offering mining-related subjects and the only facility offering surface and hard-rock courses. Improved facilities will better equip locals with the knowledge, resources and skills to be employed by mines in the surrounding areas.

* Another project which received support is the St Bernard's

Hospice in the Eastern Cape. One of the best managed hospices in the region, St Bernard's provides a safe haven for terminally ill patients. A grant of $25,000 has assisted this organisation in improving and extending its homecare programme and to extend specialist care to patients, many of whom suffer from HIV/AIDS.

* The AngloGold Fund also awarded a grant of $20,000 to

the Triest Training Centre in North West Province. The centre provides care, rehabilitation and the integration of intellectually handicapped people into mainstream society.

The Morifi Community Secondary School was opened in September 2002. The school, granted R2.5m from the AngloGold Fund and situated in rural Lesotho not far from Mohale's Hoek, is the first in the area to cater for pupils in the post-primary phase. It was built following extensive consultation and planning with both the community and the Lesotho Ministry of Education. As almost a fifth of employees are from Lesotho, this is in line with the strategy to contribute to those communities from where AngloGold's employees come. The first intake of 160 pupils has been enrolled and there are five teachers on the staff. The number of pupils is expected to increase to 475 within three years.

REVIEW OF OPERATIONS

30

(From left to right) Songo Ndungane and Popama Mokopane, Grade 2

pupils, taking a break from a literacy class, Ginsberg Primary,

King William's Town.

32

REVIEW OF OPERATIONS

ANGLO GOLD LIMITED ANNUAL REPORT 2002

Safety and health

Safety has been an issue of concern in the East and West Africa region during the year, with 45 lost time injuries. One fatal accident occurred at Morila and three fatal accidents at Geita. The main contributing factors were identified and action plans were implemented to address the deficiencies. The LTIFR and the FIFR for the region were 2.93 and 0.26 respectively.

During the year, Geita maintained its NOSA 4-star rating, while Navachab retained its NOSA 5-star rating.

Malaria

With the ever-present threat of malaria at most of the African operations, prevention and treatment programmes are running effectively at the Malian and Tanzanian operations The focus is on education, malaria vector control, the issuing of mosquito nets and early detection and treatment.

HIV/AIDS

HIV/AIDS programmes have been implemented in the region with the

Mali

Tanzania

Namibia

Geita

Sadiola

Yatela

Morila

Navachab

WHO OWNS AND MANAGES THE OPERATIONS

Key statistics

2002

2001

Tonnes treated (Mt) (attributable)

8.0

7.3

Average grade (g/t)

4.22

3.71

Gold production (000 oz) (attributable)

1,085

868

Total cash cost $/oz

126

129

Number of employees* 2,275

1,600

Efficiencies (g/TEC)

1,855

1,884

Capex ($m) (attributable)

27

34

* Including contractors

East and West Africa

AngloGold's operations in East and West Africa

The East and West Africa region (formerly known as the Africa region) comprises five operations,

located in three African countries other than South Africa. These are the Yatela, Sadiola and Morila

mines in Mali, the Navachab mine in Namibia and the Geita mine in Tanzania.

Navachab

3.05

2.98

0.00

0.00

Yatela

2.07

2.52

0.00

0.00

33

REVIEW OF OPERATIONS

ANGLO GOLD LIMITED ANNUAL REPORT 2002

primary focus on prevention through education and awareness. At all operations, education programmes have been conducted in the local communities and throughout the workforce. Peer educators have been identified and have received professional training. Partnerships have been formed with NGOs and other stakeholders in the local communities. Awareness programmes and condom distribution initiatives are ongoing.

Performance and outlook

Overall, the East and West Africa region

delivered an excellent performance for

the year and produced over a million

attributable ounces for the first time,

largely owing to the exceptional high-

grade ore at Morila. Attributable

production increased by 25% to

1,085,000oz, while total cash costs

decreased by 2% to $126/oz. Operating

profit, excluding unrealised non-hedge

derivatives, increased to $129m.

MORILA

Gold production at Morila increased by 67% to 421,000oz, largely as a result of the interception of exceptionally high-grade zones of ore during July to October. The average recovered grade for the year rose by 74% to 11.96g/t. As a result, total cash costs for the year improved by 28% to $74/oz and operating profit, excluding unrealised non-hedge derivatives, rose by 190% to $70m.

Attributable production at Morila should decrease by 19% to 343,000oz for 2003, while total cash costs will be $93/oz with the return to average mine grades. Drilling to identify other possible high- grade zones is underway. Capital expenditure of $4m is anticipated in 2003.

GEITA

Geita experienced another good year. Production rose by 6% to 290,000oz, despite a 2% decline in the average grade for the year to 3.62g/t. Total cash costs increased by 19% to $175/oz, as a result of increased stripping requirements, increased mining from the Kukuluma pit, and greater distances to the Geita plant. Operating profit, excluding unrealised non-hedge derivatives, fell by 20% to $20m.

During the second quarter, Geita successfully concluded its 90-day project completion testing, as required by loan covenants, resulting in the release of the AngloGold loan guarantees.

Approval was granted for the first phase of the Geita expansion project during the first quarter of the year. This followed encouraging results from exploration drilling in the Nyankanga pit, which increased the total remaining ore reserve to 33.5Mt. To realise the full potential of this increased reserve, plant throughput is being raised from 4.5Mtpa to 6Mtpa in two phases over the next two years. By year-end, Phase 1 of this project

increasing throughput to 5.6Mtpa had been completed and commissioned.

During 2003, attributable production should increase by 17% to 339,000oz. Total cash costs should increase by 1% to $176/oz. Capital expenditure of $12m is planned in 2003.

SADIOLA

Tonnage throughput at Sadiola was adversely affected by mineral sizer downtime in the first quarter, the low availability of high-grade oxide ore during the year and problems with the treatment of higher-grade soft sulphide ore. This resulted in a 5% decrease in the average recovered grade for the year to 2.96g/t. Consequently, gold production of 182,000oz was 10% lower than the previous year. Total cash costs increased by 25% to $163/oz as a result of the lower production and treatment of sulphide ores. Operating profit, excluding unrealised non-hedge derivatives, decreased by 42% to $12m.

The plant conversion project to improve gold recovery from the treatment of soft sulphide ore was completed on schedule by the end of February 2002. High cyanide values in the final residue prevented the treatment of soft sulphide ore, which required high cyanide addition to maintain acceptable recoveries. A cyanide destruction plant was designed and commissioned in the third quarter and

Expansion at Geita

The first phase of the Geita gold plant

expansion was approved during the first

quarter following encouraging results from

exploration in the Nyankanga pit, which

increased the total remaining reserve to

33.5Mt. Plant throughput is being increased

from 4.5Mtpa to 6Mtpa in two phases.

Phase 1, which was completed in

December 2002, involved the installation of

secondary crushers and modification to the

ball mill to cater for the increased throughput,

raising the treatment rate to 5.6Mtpa at a

capital cost of $3m.

34

REVIEW OF OPERATIONS

ANGLO GOLD LIMITED ANNUAL REPORT 2002

As a result of the successful brownfields drilling programme at Geita during

AngloGold's aim of ensuring sustainable development is particularly pertinent in Africa where mining operations are frequently located in inaccessible areas, largely untouched by industry and economic development. Sensible mining practices, with the full involvement of local communities and governments, can ensure that long-term benefits accrue to the regions, even after mining has been completed.

35

AngloGold's philosophy of ensuring

sustainable development is particularly

pertinent in Africa where mining operations

are frequently located in inaccessible areas,

largely untouched by industry and economic

development. Sensible mining practices,

with the full involvement of local

government and communities such

as here at Sadiola in Mali can ensure that

long-term benefits accrue to the region,

even after mining has been completed.

REVIEW OF OPERATIONS

ANGLO GOLD LIMITED ANNUAL REPORT 2002

36

Brazil

Argentina

Serra Grande

Cerro Vanguardia

Morro Velho

AngloGold's operations

in South America

The South America region comprises three

operations, Morro Velho and Serra Grande

(50%) in Brazil and Cerro Vanguardia

(92.5% as of July 2002) in Argentina.

Key statistics

2002

2001

Tonnes treated (Mt) (attributable)

1.9

1.7

Average grade (g/t)

7.8

7.8

Gold production (oz) (attributable)

478,000

441,000

Total cash cost ($/oz)

126

134

Number of employees *

2,660

2,300

Efficiencies (g/TEC)

684

611

Capex ($m) (attributable)

24

20

* Excludes contractors for the Cuiab

Expansion and contractors for the implementation phase of Crrego do Stio mine

South America

Safety and health

Safety performance in the region was good, with the overall LTIFR - at 4.21 - below the Ontario benchmark of 6.5. Regrettably, a fatal accident occurred at

Cerro Vanguardia on 17 July.

Following a complete review of risk management procedures in November 2002, Cerro Vanguardia was re-audited and maintained a NOSA 5-star rating and ISO14001 Certification.