UNITED STATES SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

________________________________________________________

FORM 10-Q

________________________________________________________

QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | ||||||||

For the quarterly period ended March 31, 2024

OR

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | ||||||||

Commission file number 1-3932

WHIRLPOOL CORPORATION

(Exact name of registrant as specified in its charter)

| (State of Incorporation) | (I.R.S. Employer Identification No.) | ||||||||||

| (Address of principal executive offices) | (Zip Code) | ||||||||||

Registrant's telephone number, including area code (269 ) 923-5000

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading symbol(s) | Name of each exchange on which registered | ||||||||||||||||||

| and | ||||||||||||||||||||

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of "large accelerated filer," "accelerated filer," "smaller reporting company," and "emerging growth company" in Rule 12b-2 of the Exchange Act.

| ☒ | Accelerated filer | ☐ | |||||||||

| Non-accelerated filer | ☐ | Smaller reporting company | |||||||||

| Emerging growth company | |||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

Number of shares outstanding of each of the issuer's classes of common stock, as of the latest practicable date:

| Class of common stock | Shares outstanding at April 19, 2024 | |||||||

| Common stock, par value $1.00 per share | ||||||||

WHIRLPOOL CORPORATION

QUARTERLY REPORT ON FORM 10-Q

Three Months Ended March 31, 2024

TABLE OF CONTENTS

| PAGE | ||||||||

PART I | ||||||||

| Item 1. | ||||||||

| Item 2. | ||||||||

| Item 3. | ||||||||

| Item 4. | ||||||||

| Item 1. | ||||||||

| Item 1A. | ||||||||

| Item 2. | ||||||||

| Item 3. | ||||||||

| Item 4. | ||||||||

| Item 5. | ||||||||

| Item 6. | ||||||||

FORWARD-LOOKING STATEMENTS

The Private Securities Litigation Reform Act of 1995 provides a safe harbor for forward-looking statements made by us or on our behalf. Certain statements contained in this quarterly report, including those within the forward-looking perspective section within the Management's Discussion and Analysis section, and other written and oral statements made from time to time by us or on our behalf do not relate strictly to historical or current facts and may contain forward-looking statements that reflect our current views with respect to future events and financial performance. As such, they are considered "forward-looking statements" which provide current expectations or forecasts of future events. Such statements can be identified by the use of terminology such as "may," "could," "will," "should," "possible," "plan," "predict," "forecast," "potential," "anticipate," "estimate," "expect," "project," "intend," "believe," "may impact," "on track," "guarantee," "seek," and the negative of these words and words and terms of similar substance. Our forward-looking statements generally relate to our growth strategies, financial results, product development, and sales efforts. These forward-looking statements should be considered with the understanding that such statements involve a variety of risks and uncertainties, known and unknown, and may be affected by inaccurate assumptions. Consequently, no forward-looking statement can be guaranteed and actual results may vary materially.

This document contains forward-looking statements about Whirlpool Corporation and its consolidated subsidiaries ("Whirlpool") that speak only as of this date. Whirlpool disclaims any obligation to update these statements. Forward-looking statements in this document may include, but are not limited to, statements regarding future financial results, long-term value creation goals, restructuring expectations, productivity, raw material prices and related costs, supply chain, portfolio transformation expectations, asset impairment, litigation, ESG efforts, debt repayment expectations, and the impact of COVID-19 and the Russia/Ukraine, Israel and Red Sea conflicts on our operations. Many risks, contingencies and uncertainties could cause actual results to differ materially from Whirlpool's forward-looking statements. Among these factors are: (1) intense competition in the home appliance industry, and the impact of the changing retail environment, including direct-to-consumer sales; (2) Whirlpool's ability to maintain or increase sales to significant trade customers; (3) Whirlpool's ability to maintain its reputation and brand image; (4) the ability of Whirlpool to achieve its business objectives and leverage its global operating platform, and accelerate the rate of innovation; (5) Whirlpool’s ability to understand consumer preferences and successfully develop new products; (6) Whirlpool's ability to obtain and protect intellectual property rights; (7) acquisition, divestiture, and investment-related risks, including risks associated with our past acquisitions; (8) the ability of suppliers of critical parts, components and manufacturing equipment to deliver sufficient quantities to Whirlpool in a timely and cost-effective manner; (9) COVID-19 pandemic, other public health emergency-related business disruptions and economic uncertainty; (10) Whirlpool's ability to navigate risks associated with our presence in emerging markets; (11) risks related to our international operations; (12) Whirlpool's ability to respond to unanticipated social, political and/or economic events; (13) information technology system failures, data security breaches, data privacy compliance, network disruptions, and cybersecurity attacks; (14) product liability and product recall costs; (15) Whirlpool's ability to attract, develop and retain executives and other qualified employees; (16) the impact of labor relations; (17) fluctuations in the cost of key materials (including steel, resins, base metals) and components and the ability of Whirlpool to offset cost increases; (18) Whirlpool's ability to manage foreign currency fluctuations; (19) impacts from goodwill impairment and related charges; (20) triggering events or circumstances impacting the carrying value of our long-lived assets; (21) inventory and other asset risk; (22) health care cost trends, regulatory changes and variations between results and estimates that could increase future funding obligations for pension and postretirement benefit plans; (23) litigation, tax, and legal compliance risk and costs; (24) the effects and costs of governmental investigations or related actions by third parties; (25) changes in the legal and regulatory environment including environmental, health and safety regulations, data privacy, and taxes and tariffs; (26) Whirlpool's ability to respond to the impact of climate change and climate change regulation; and (27) the uncertain global economy and changes in economic conditions.

We undertake no obligation to update any forward-looking statement, and investors are advised to review disclosures in our filings with the SEC. It is not possible to foresee or identify all factors that could cause actual results to differ from expected or historic results. Therefore, investors should not consider the foregoing factors to be an exhaustive statement of all risks, uncertainties, or factors that could potentially cause actual results to differ from forward-looking statements.

Additional information concerning these and other factors can be found in the "Risk Factors" section of our Annual Report on Form 10-K, as updated in Part II, Item 1A of our Quarterly Reports on Form 10-Q.

2

Unless otherwise indicated, the terms "Whirlpool," "the Company," "we," "us," and "our" refer to Whirlpool Corporation and its consolidated subsidiaries.

Website Disclosure

We routinely post important information for investors on our website, whirlpoolcorp.com, in the "Investors" section. We also intend to update the Hot Topics Q&A portion of this webpage as a means of disclosing material, non-public information and for complying with our disclosure obligations under Regulation FD. Accordingly, investors should monitor the "Investors" section of our website, in addition to following our press releases, SEC filings, public conference calls, presentations and webcasts. The information contained on, or that may be accessed through, our webpage is not incorporated by reference into, and is not a part of, this document.

3

| PART I. FINANCIAL INFORMATION | ||

| ITEM 1. | FINANCIAL STATEMENTS | ||||

TABLE OF CONTENTS

| PAGE | |||||

| FINANCIAL STATEMENTS AND SUPPLEMENTARY DATA | |||||

| PAGE | ||||||||

| NOTES TO THE CONSOLIDATED CONDENSED FINANCIAL STATEMENTS (UNAUDITED) | ||||||||

| 1. | ||||||||

| 2. | ||||||||

| 3. | ||||||||

| 4. | ||||||||

| 5. | ||||||||

| 6. | ||||||||

| 7. | ||||||||

| 8. | ||||||||

| 9. | ||||||||

| 10. | ||||||||

| 11. | ||||||||

| 12. | ||||||||

| 13. | ||||||||

| 14. | ||||||||

4

WHIRLPOOL CORPORATION

CONSOLIDATED CONDENSED STATEMENTS OF COMPREHENSIVE INCOME (LOSS) (UNAUDITED)

FOR THE PERIODS ENDED MARCH 31

(Millions of dollars, except per share data)

| Three Months Ended | |||||||||||

| 2024 | 2023 | ||||||||||

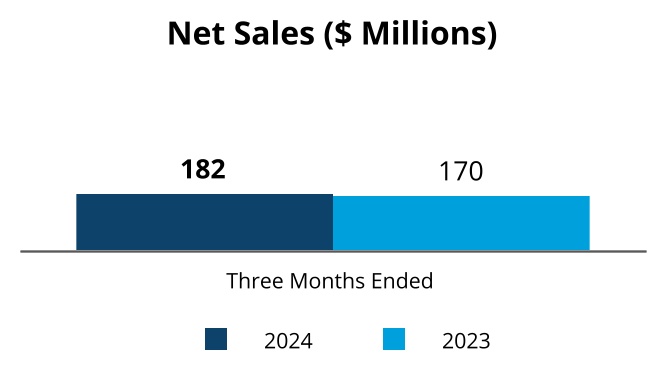

| Net sales | $ | $ | |||||||||

| Expenses | |||||||||||

| Cost of products sold | |||||||||||

| Gross margin | |||||||||||

| Selling, general and administrative | |||||||||||

| Intangible amortization | |||||||||||

| Restructuring costs | |||||||||||

| Loss (gain) on sale and disposal of businesses | |||||||||||

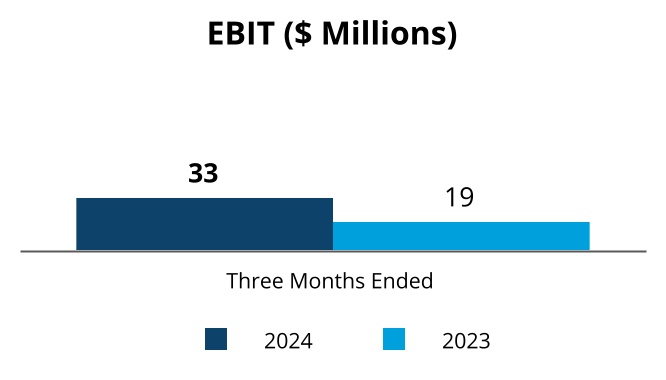

| Operating (loss) profit | ( | ||||||||||

| Other (income) expense | |||||||||||

| Interest and sundry (income) expense | ( | ||||||||||

| Interest expense | |||||||||||

| Earnings (loss) before income taxes | ( | ( | |||||||||

| Income tax expense (benefit) | |||||||||||

| Equity method investment income (loss), net of tax | |||||||||||

| Net earnings (loss) | ( | ( | |||||||||

| Less: Net earnings (loss) available to noncontrolling interests | |||||||||||

| Net earnings (loss) available to Whirlpool | $ | ( | $ | ( | |||||||

| Per share of common stock | |||||||||||

| Basic net earnings (loss) available to Whirlpool | $ | ( | $ | ( | |||||||

| Diluted net earnings (loss) available to Whirlpool | $ | ( | $ | ( | |||||||

| Dividends declared | $ | $ | |||||||||

| Weighted-average shares outstanding (in millions) | |||||||||||

| Basic | |||||||||||

| Diluted | |||||||||||

| Comprehensive income (loss) | $ | ( | $ | ( | |||||||

The accompanying notes are an integral part of these Consolidated Condensed Financial Statements.

5

WHIRLPOOL CORPORATION

CONSOLIDATED CONDENSED BALANCE SHEETS

(Millions of dollars, except share data)

| (Unaudited) | |||||||||||

| March 31, 2024 | December 31, 2023 | ||||||||||

| Assets | |||||||||||

| Current assets | |||||||||||

| Cash and cash equivalents | $ | $ | |||||||||

Accounts receivable, net of allowance of $ | |||||||||||

| Inventories | |||||||||||

| Prepaid and other current assets | |||||||||||

| Assets held for sale | |||||||||||

| Total current assets | |||||||||||

Property, net of accumulated depreciation of $ | |||||||||||

| Right of use assets | |||||||||||

| Goodwill | |||||||||||

Other intangibles, net of accumulated amortization of $ | |||||||||||

| Deferred income taxes | |||||||||||

| Other noncurrent assets | |||||||||||

| Total assets | $ | $ | |||||||||

| Liabilities and stockholders' equity | |||||||||||

| Current liabilities | |||||||||||

| Accounts payable | $ | $ | |||||||||

| Accrued expenses | |||||||||||

| Accrued advertising and promotions | |||||||||||

| Employee compensation | |||||||||||

| Notes payable | |||||||||||

| Current maturities of long-term debt | |||||||||||

| Other current liabilities | |||||||||||

| Liabilities held for sale | |||||||||||

| Total current liabilities | |||||||||||

| Noncurrent liabilities | |||||||||||

| Long-term debt | |||||||||||

| Pension benefits | |||||||||||

| Postretirement benefits | |||||||||||

| Lease liabilities | |||||||||||

| Other noncurrent liabilities | |||||||||||

| Total noncurrent liabilities | |||||||||||

| Stockholders' equity | |||||||||||

Common stock, $ | |||||||||||

| Additional paid-in capital | |||||||||||

| Retained earnings | |||||||||||

| Accumulated other comprehensive loss | ( | ( | |||||||||

Treasury stock, | ( | ( | |||||||||

| Total Whirlpool stockholders' equity | |||||||||||

| Noncontrolling interests | |||||||||||

| Total stockholders' equity | |||||||||||

| Total liabilities and stockholders' equity | $ | $ | |||||||||

The accompanying notes are an integral part of these Consolidated Condensed Financial Statements.

6

WHIRLPOOL CORPORATION

CONSOLIDATED CONDENSED STATEMENTS OF CASH FLOWS (UNAUDITED)

FOR THE PERIODS ENDED MARCH 31

(Millions of dollars)

| Three Months Ended | |||||||||||

| 2024 | 2023 | ||||||||||

| Operating activities | |||||||||||

| Net earnings (loss) | $ | ( | $ | ( | |||||||

| Adjustments to reconcile net earnings to cash provided by (used in) operating activities: | |||||||||||

| Depreciation and amortization | |||||||||||

| Loss (gain) on sale and disposal of businesses | |||||||||||

| Changes in assets and liabilities: | |||||||||||

| Accounts receivable | ( | ( | |||||||||

| Inventories | ( | ( | |||||||||

| Accounts payable | ( | ( | |||||||||

| Accrued advertising and promotions | ( | ( | |||||||||

| Accrued expenses and current liabilities | ( | ||||||||||

| Taxes deferred and payable, net | |||||||||||

| Accrued pension and postretirement benefits | ( | ( | |||||||||

| Employee compensation | ( | ||||||||||

| Other | ( | ( | |||||||||

| Cash provided by (used in) operating activities | ( | ( | |||||||||

| Investing activities | |||||||||||

| Capital expenditures | ( | ( | |||||||||

| Acquisition of businesses, net of cash acquired | ( | ||||||||||

| Cash provided by (used in) investing activities | ( | ( | |||||||||

| Financing activities | |||||||||||

| Net proceeds from borrowings of long-term debt | |||||||||||

| Net proceeds (repayments) of long-term debt | ( | ( | |||||||||

| Net proceeds (repayments) from short-term borrowings | |||||||||||

| Dividends paid | ( | ( | |||||||||

| Repurchase of common stock | ( | ||||||||||

| Sale of minority interest in subsidiary | |||||||||||

| Common stock issued | |||||||||||

| Other | ( | ||||||||||

| Cash provided by (used in) financing activities | ( | ||||||||||

| Effect of exchange rate changes on cash, cash equivalents and restricted cash | ( | ||||||||||

| Less: change in cash classified as held for sale | ( | ( | |||||||||

| Increase (decrease) in cash, cash equivalents and restricted cash | ( | ( | |||||||||

| Cash, cash equivalents and restricted cash at beginning of year | |||||||||||

| Cash, cash equivalents and restricted cash at end of period | $ | $ | |||||||||

The accompanying notes are an integral part of these Consolidated Condensed Financial Statements.

7

NOTES TO THE CONSOLIDATED CONDENSED FINANCIAL STATEMENTS (UNAUDITED)

(1) BASIS OF PRESENTATION

General Information

The accompanying unaudited Consolidated Condensed Financial Statements have been prepared in accordance with accounting principles generally accepted in the United States of America ("GAAP") for interim financial information, and with the instructions to Form 10-Q and Article 10 of Regulation S-X. Accordingly, they do not include all information or footnotes required by U.S. GAAP for complete financial statements. As a result, this Form 10-Q should be read in conjunction with the Consolidated Financial Statements and accompanying Notes in our Form 10-K for the year ended December 31, 2023.

Management believes that the accompanying Consolidated Condensed Financial Statements reflect all adjustments, including normal recurring items, considered necessary for a fair presentation of the interim periods.

We are required to make estimates and assumptions that affect the amounts reported in the Consolidated Condensed Financial Statements and accompanying Notes. Actual results could differ materially from those estimates.

We have eliminated all material intercompany transactions in our Consolidated Condensed Financial Statements. We do not consolidate the financial statements of any company in which we have an ownership interest of 50% or less, unless that company is deemed to be a variable interest entity ("VIE") of which we are the primary beneficiary. VIEs are consolidated when the company is the primary beneficiary of these entities and has the ability to directly impact the activities of these entities.

Risks and Uncertainties

Macroeconomic volatility, as well as ongoing international conflicts, continues to impact countries across the world, and the duration and severity of the effects are currently unknown. During the quarter, we continued experiencing some disruption from these conflicts, primarily in Europe due to the conflict in Ukraine. The duration and severity of the effects on our business and the global economy are inherently unpredictable. We have some sales and distribution operations in Ukraine; however, the revenues and net assets are not material to our Major Domestic Appliances Europe ("MDA Europe") operating segment and consolidated results. Our Ukraine business was part of the major domestic appliance European transaction, which was completed on April 1, 2024. For additional information, see Note 14 to the Consolidated Condensed Financial Statements.

The Consolidated Condensed Financial Statements presented herein reflect estimates and assumptions made by management at March 31, 2024.

These estimates and assumptions affect, among other things, the Company’s goodwill, long-lived asset and indefinite-lived intangible asset valuation; inventory valuation; assessment of the annual effective tax rate; valuation of deferred income taxes and income tax contingencies; and the allowance for expected credit losses and bad debt. Events and changes in circumstances arising after April 25, 2024, including those resulting from the impacts of macroeconomic volatility, as well as the ongoing international conflicts, will be reflected in management’s estimates for future periods.

Goodwill and Indefinite-lived Intangible Assets

We continue to monitor the significant global economic uncertainty to assess the outlook for demand for our products and the impact on our business and our overall financial performance. Our Maytag and InSinkErator trademarks continue to be at risk at March 31, 2024. The goodwill in our reporting units or other indefinite-lived intangible assets are not presently at risk for future impairment.

The potential impact of demand disruptions, production impacts or supply constraints along with a number of other factors could negatively affect revenues for the Maytag and InSinkErator trademarks, but we remain committed to the strategic actions necessary to realize the long-term forecasted revenues and profitability of these trademarks.

8

A lack of recovery or further deterioration in market conditions, a sustained trend of weaker than expected financial performance for our Maytag and InSinkErator trademarks, among other factors, as a result of the macroeconomic factors or other unforeseen events could result in an impairment charge in future periods which could have a material adverse effect on our financial statements.

As a result of our analysis, and in consideration of the totality of events and circumstances, there were no triggering events of impairment identified during the first quarter of 2024.

Income taxes

Under U.S. GAAP, the Company calculates its quarterly tax provision based on an estimated effective tax rate for the year and then adjusts this amount by certain discrete items each quarter. Potential changing and volatile macro-economic conditions could cause fluctuations in forecasted earnings before income taxes. As such, the Company's effective tax rate could be subject to volatility as forecasted earnings before income taxes are impacted by events which cannot be predicted.

Other Accounting Matters

Synthetic Lease Arrangements

We have a number of synthetic lease arrangements with financial institutions for non-core properties. The leases contain provisions for options to purchase, extend the original term for additional periods or return the property. As of March 31, 2024 and December 31, 2023, these arrangements include residual value guarantees of up to approximately $378 million and $378 million, respectively, that could potentially come due in future periods. We do not believe it is probable that any material amounts will be owed under these guarantees. Therefore, no material amounts related to the residual value guarantees are included in the lease payments used to measure the right-of-use assets and lease liabilities.

Supply Chain Financing Arrangements

The Company has ongoing agreements globally with various third-parties to provide certain suppliers the opportunity to sell receivables due from us to participating financial institutions at the sole discretion of both the suppliers and the financial institutions. Under these agreements, the average payment terms range from 120 to 180 days and are based on industry standards and best practices within each of our global regions. Whirlpool has no assets pledged as part of our global programs.

9

| Millions of dollars | Outstanding Obligations | ||||

| Confirmed obligations outstanding as of December 31, 2023 | $ | ||||

| Invoices confirmed during the period | |||||

| Confirmed invoices paid during the period | ( | ||||

| Impact of foreign currency | ( | ||||

| Confirmed obligations outstanding as of March 31, 2024 | $ | ||||

Obligations outstanding and activities during the period related to our European major domestic appliance business have been excluded from the table above. The obligations outstanding amounted to $395 million and $393 million as of March 31, 2024 and December 31, 2023, respectively.

A downgrade in our credit rating or changes in the financial markets could limit the financial institutions’ willingness to commit funds to, and participate in, the programs. We do not believe such risk would have a material impact on our working capital or cash flows.

Equity Method Investments

| Millions of dollars | March 31, 2024 | December 31, 2023 | |||||||||||||||

| Other noncurrent assets | Carrying value of equity interest | $ | $ | ||||||||||||||

| Accounts payable | Outstanding amounts due | $ | $ | ||||||||||||||

| Millions of dollars | Three Months Ended March 31, | |||||||||||||

| 2024 | 2023 | |||||||||||||

| Purchases from Whirlpool China | $ | $ | ||||||||||||

The licensing revenue and outstanding accounts receivable from Whirlpool China and its subsidiaries are not material for the periods presented.

The market value of our 20 % investment in Whirlpool China, based on the quoted market price, is $177 million as of March 31, 2024. Management has concluded that there are currently no indicators for an other-than-temporary impairment.

Related Parties

The Company has a controlling equity ownership of 87 % in Elica PB India which is consolidated in Whirlpool Corporation's financial statements and is reported within our MDA Asia reportable segment. Elica PB India is a VIE for which the Company is the primary beneficiary. The carrying amount of customer relationships, which are included in Other intangible assets, net of accumulated amortization, amounts to $28 million as of March 31, 2024 and $29 million as of December 31, 2023, respectively. Other assets or liabilities of Elica PB India are not material to the Consolidated Condensed Financial Statements of the Company for the periods presented.

Both Whirlpool India and the non-controlling interest shareholders retain an option for Whirlpool India to purchase the remaining equity interest in Elica PB India for fair value, which could be material to the financial statements of the Company, depending on the performance of the business.

10

Accounting Pronouncements Issued But Not Yet Effective

In November 2023, the FASB issued Update 2023-07, "Segment Reporting (Topic 280): Improvements to Reportable Segment Disclosures". This Update applies to all public entities that are required to report segment information in accordance with Topic 280. The amendments in this Update revise reportable segment disclosure requirements, primarily through enhanced disclosures about significant segment expenses. The amendments in this Update do not change how a public entity identifies its operating segments, aggregates those operating segments, or applies the quantitative thresholds to determine its reportable segments. The new standard is effective for fiscal years beginning after December 15, 2023, and interim periods within fiscal years beginning after December 15, 2024. Early adoption is permitted. The standard should be applied retrospectively to all prior periods presented in the financial statements. The Company is currently evaluating the impact of adopting this new standard.

In December 2023, the FASB issued Update 2023-09, "Income Taxes (Topic 740): Improvements to Income Tax Disclosures". This Update applies to all entities that are subject to Topic 740. The amendments in this Update revise income tax disclosures primarily related to the rate reconciliation and income taxes paid information as well as the effectiveness of certain other income tax disclosures. The new standard is effective for annual periods beginning after December 15, 2024. Early adoption is permitted. The standard should be applied on a prospective basis, but retrospective application is permitted. The Company is currently evaluating the impact of adopting this new standard.

All other issued and not yet effective accounting standards are not relevant or material to the Company.

(2) REVENUE RECOGNITION

Disaggregation of Revenue

The following table presents our disaggregated revenues by revenue source. For additional information on the disaggregated revenues by operating segment, see Note 13 to the Consolidated Condensed Financial Statements.

Three Months Ended March 31, | |||||||||||

| Millions of dollars | 2024 | 2023 | |||||||||

| Major product categories: | |||||||||||

| Laundry | $ | $ | |||||||||

| Refrigeration | |||||||||||

| Cooking | |||||||||||

| Dishwashing | |||||||||||

| Total major product category net sales | $ | $ | |||||||||

| Spare parts and warranties | |||||||||||

| Other | |||||||||||

| Total net sales | $ | $ | |||||||||

Other revenue sources include primarily the revenues from the InSinkErator business, subscription arrangements and licenses.

The impact to revenue related to prior period performance obligations is less than 1% of global consolidated revenues for the three months ended March 31, 2024.

Allowance for Expected Credit Losses and Bad Debt Expense

We estimate our expected credit losses and bad debt expense primarily by using an aging methodology and establish customer-specific reserves for higher risk trade customers. Our expected credit losses and bad debt expense are evaluated and controlled within each geographic region considering the unique credit risk specific to the country, marketplace and economic environment. We take into account past events, current conditions and reasonable and supportable forecasts in developing the reserve.

11

The following table summarizes our allowance for expected credit losses and bad debt expense by operating segment for the three months ended March 31, 2024:

| Millions of dollars | December 31, 2023 (1) | Charged to Earnings | Write-offs | Foreign Currency | March 31, 2024 | ||||||||||||

| Accounts receivable allowance | |||||||||||||||||

| MDA North America | $ | $ | $ | $ | $ | ||||||||||||

| MDA Latin America | ( | ||||||||||||||||

| MDA Asia | |||||||||||||||||

| SDA Global | |||||||||||||||||

| Consolidated | $ | $ | $ | ( | $ | $ | |||||||||||

| Financing receivable allowance | |||||||||||||||||

| MDA Latin America | $ | $ | $ | $ | ( | $ | |||||||||||

| Consolidated | $ | $ | $ | ( | $ | $ | |||||||||||

(1) Effective January 1, 2024, we reorganized our operating segment structure. All prior period amounts have been reclassified to conform with current period presentation. For additional information, see Note 13 to the Consolidated Condensed Financial Statements.

(3) INVENTORIES

The following table summarizes our inventories at March 31, 2024 and December 31, 2023:

| Millions of dollars | March 31, 2024 | December 31, 2023 | ||||||||||||

| Finished products | $ | $ | ||||||||||||

| Raw materials and work in process | ||||||||||||||

| Total Inventories | $ | $ | ||||||||||||

(4) PROPERTY, PLANT AND EQUIPMENT

The following table summarizes our property, plant and equipment at March 31, 2024 and December 31, 2023:

| Millions of dollars | March 31, 2024 | December 31, 2023 | ||||||||||||

| Land | $ | $ | ||||||||||||

| Buildings | ||||||||||||||

| Machinery and equipment | ||||||||||||||

| Accumulated depreciation | ( | ( | ||||||||||||

| Property, plant and equipment, net | $ | $ | ||||||||||||

During the three months ended March 31, 2024, we disposed of land, buildings, machinery and equipment with a net book value of $2 million, compared to $1 million in the same period of 2023. The net gain on the disposals was no

(5) FINANCING ARRANGEMENTS

Debt Offering

On February 22, 2024, the Company entered into an Underwriting Agreement (the "Underwriting Agreement") with SMBC Nikko Securities America, Inc., BNP Paribas Securities Corp., ING Financial Markets LLC, Mizuho Securities USA LLC, Scotia Capital (USA) Inc. and SG Americas Securities, LLC, as representatives of the several underwriters named therein, relating to the offering by the Company of $300 million aggregate principal amount of 5.750 % Senior Notes due 2034 (the "Notes"), in a public offering pursuant to a registration statement on Form S-3 (File No. 333-276169), and a preliminary prospectus supplement and prospectus

12

supplement related to the offering of the Notes, each as previously filed with the Securities and Exchange Commission (the "Commission"). On February 27, 2024, the Company closed its offering of the Notes. The Notes contain covenants that limit the Company's ability to incur certain liens or enter into certain sale and lease-back transactions. In addition, if we experience a specific kind of change of control, we are required to make an offer to purchase all of the notes at a purchase price of 101 % of the principal amount thereof, plus accrued and unpaid interest. The Company used the net proceeds from the sale of the Notes, together with cash on hand, to repay, at maturity, all $300 million aggregate principal amount of the Company's 4.000 % Notes due March 1, 2024.

On February 22, 2023, the Company completed its offering of $300 million aggregate principal amount of 5.500 % Senior Notes due 2033 (the “2033 Notes”), in a public offering pursuant to a registration statement on Form S-3 (File No. 333-255372). The 2033 Notes were issued under an indenture (the “Indenture”), dated March 20, 2000, between the Company, as issuer, and U.S. Bank Trust Company, National Association (as successor to U.S. Bank, National Association and Citibank, N.A.), as trustee. The sale of the 2033 Notes was made pursuant to the terms of an Underwriting Agreement, dated February 14, 2023, with BNP Paribas Securities Corp., ING Financial Markets LLC, Mizuho Securities USA LLC, SMBC Nikko Securities America, Inc. and SG Americas Securities, LLC, as representatives of the several underwriters in connection with the offering and sales of the 2033 Notes. The 2033 Notes contain covenants that limit the Company's ability to incur certain liens or enter into certain sale and lease-back transactions. In addition, if we experience a specific kind of change of control, we are required to make an offer to purchase all of the notes at a purchase price of 101 % of the principal amount thereof, plus accrued and unpaid interest. The Company used the net proceeds from the sale of the 2033 Notes to repay $250 million aggregate principal amount of 3.700 % Notes which were paid on March 1, 2023, and for general corporate purposes.

Term Loan Agreement

On September 23, 2022, the Company entered into a Term Loan Agreement by and among the Company, Sumitomo Mitsui Banking Corporation (“SMBC”), as Administrative Agent and Syndication Agent and as lender, and certain other financial institutions as lenders. SMBC, BNP Paribas, ING Bank N.V., Dublin Branch, Mizuho Bank, Ltd., and Societe Generale acted as Joint Lead Arrangers and Syndication Agents; The Bank of Nova Scotia and Bank of China, Chicago Branch acted as Documentation Agents; and SMBC acted as Sole Bookrunner for the Term Loan Agreement. The Term Loan Agreement provides for an aggregate lender commitment of $2.5 billion. The Company utilized proceeds from the term loan facility on a delayed draw basis to fund a majority of the $3.0 billion purchase price consideration for the Company’s acquisition from Emerson Corporation (“Emerson”) of Emerson’s InSinkErator business, as set forth in the Asset and Stock Purchase Agreement between Whirlpool and Emerson dated as of August 7, 2022 (the “Acquisition Agreement”).

The outstanding amount for this term loan at March 31, 2024 is $2.0 billion, of which $500 million is classified in current liabilities on the Consolidated Condensed Balance Sheet. The term loan facility is divided into two tranches: a $1 billion tranche with a maturity date of April 30, 2024, of which $500 million was repaid in December 2023 and the remaining $500 million was repaid in April 2024; and a $1.5 billion tranche with a maturity date of October 31, 2025.

The interest and fee rates payable with respect to the term loan facility based on the Company's current debt rating are as follows: (1) the spread over secured overnight financing rate ("SOFR") for the 18-month tranche (fully repaid as of April 2024) is 0.975 %; (2) the spread over SOFR for the 3-year tranche is 1.225 %; (3) the spread over prime for both tranches is zero ; and (4) the ticking fee for both tranches is 0.125 %, as of the date hereof.

The Term Loan Agreement contains customary covenants and warranties including, among other things, a rolling twelve month interest coverage ratio required to be greater than or equal to 3.0 for each fiscal quarter. In addition, the covenants limit the Company's ability to (or to permit any subsidiaries to), subject to various exceptions and limitations: (i) merge with other companies; (ii) create liens on its property; and (iii) incur debt at the subsidiary level. We were in compliance with our interest coverage ratio under the term loan agreement as of March 31, 2024.

13

Credit Facilities

On May 3, 2022, the Company entered into a Fifth Amended and Restated Long-Term Credit Agreement (the “Amended Long-Term Facility”) by and among the Company, certain other borrowers, the lenders referred to therein, JPMorgan Chase Bank, N.A. as Administrative Agent, and Citibank, N.A., as Syndication Agent. BNP Paribas, Mizuho Bank, Ltd. and Wells Fargo Bank, National Association acted as Documentation Agents. JPMorgan Chase Bank, N.A., BNP Paribas Securities Corp., Citibank, N.A., Mizuho Bank, Ltd. and Wells Fargo Securities, LLC acted as Joint Lead Arrangers and Joint Bookrunners for the Amended Long-Term Facility. Consistent with the Company’s prior credit agreement, the Amended Long-Term Facility provides an aggregate borrowing capacity of $3.5 billion. The facility has a maturity date of May 3, 2027, unless earlier terminated.

The interest rate payable with respect to the Amended Long-Term Facility is based on the Company’s current debt rating, Term SOFR (Secured Overnight Financing Rate) + 1.125 % interest rate margin per annum (with a 0.10 % SOFR spread adjustment) or the Alternate Base Rate + 0.125 % per annum, at the Company’s election.

The Amended Long-Term Facility contains customary covenants and warranties, such as, among other things, a rolling four quarter interest coverage ratio required to be greater than or equal to 3.0 as of the end of each fiscal quarter. The Amended Long-Term Facility also includes limitations on the Company’s ability to (or to permit any subsidiaries to), subject to various exceptions and limitations: (i) merge with other companies; (ii) create liens on its property; and (iii) incur debt at the subsidiary level. We were in compliance with our interest coverage ratio under the Amended Long-Term Facility as of March 31, 2024.

In addition to the committed $3.5 billion Amended Long-Term Facility and the committed $2.0 billion term loan, we have committed credit facilities in Brazil and India. These committed credit facilities provide borrowings up to approximately $212 million at March 31, 2024 and $218 million at December 31, 2023, based on exchange rates then in effect, respectively. These committed credit facilities have maturities that run through 2025.

We had $2.0 billion and $2.0 billion drawn on the committed credit facilities (representing amounts outstanding on the term loan facility) at March 31, 2024 and December 31, 2023, respectively.

Notes Payable

Notes payable, which consist of short-term borrowings payable to banks or commercial paper, are generally used to fund working capital requirements. The fair value of our notes payable approximates the carrying amount due to the short maturity of these obligations.

The following table summarizes the carrying value of notes payable at March 31, 2024 and December 31, 2023:

| Millions of dollars | March 31, 2024 | December 31, 2023 | ||||||||||||

| Commercial paper | $ | $ | ||||||||||||

| Short-term borrowings due to banks | ||||||||||||||

| Total notes payable | $ | $ | ||||||||||||

Transfers and Servicing of Financial Assets

In an effort to manage economic and geographic trade customer risk, from time to time, the Company will transfer, primarily without recourse, accounts receivable balances of certain customers to financial institutions resulting in a nominal impact recorded in interest and sundry (income) expense. These transactions are accounted for as sales of the receivables resulting in the receivables being de-recognized from the Consolidated Condensed Balance Sheets. These transfers do not require continuing involvement from the Company.

14

(6) COMMITMENTS AND CONTINGENCIES

BEFIEX Credits and Other Brazil Tax Matters

In previous years, our Brazilian operations earned tax credits under the Brazilian government's export incentive program (BEFIEX). These credits reduced Brazilian federal excise taxes on domestic sales. Our Brazilian operations have received tax assessments for income and social contribution taxes associated with certain monetized BEFIEX credits. We do not believe BEFIEX credits are subject to income or social contribution taxes. We have not provided for income or social contribution taxes on these BEFIEX credits, and based on the opinions of tax and legal advisors, we have not accrued any amount related to these assessments at March 31, 2024. The total amount of outstanding tax assessments received for income and social contribution taxes relating to the BEFIEX credits, including interest and penalties, is approximately 2.3 billion Brazilian reais (approximately $461 million at March 31, 2024).

Relying on existing Brazilian legal precedent, in 2003 and 2004, we recognized tax credits in an aggregate amount of $26 million, adjusted for currency, on the purchase of raw materials used in production ("IPI tax credits"). The Brazilian tax authority subsequently challenged the recording of IPI tax credits. No such credits have been recognized since 2004. In 2009, we entered into a Brazilian government program ("IPI Amnesty") which provided extended payment terms and reduced penalties and interest to encourage taxpayers to resolve this and certain other disputed tax credit amounts. As permitted by the program, we elected to settle certain debts through the use of other existing tax credits and recorded charges of approximately $34 million in 2009 associated with these matters. In July 2012, the Brazilian revenue authority notified us that a portion of our proposed settlement was rejected and we received tax assessments of 287 million Brazilian reais (approximately $58 million at March 31, 2024), reflecting interest and penalties to date. The government's assessment in this case relies heavily on its arguments regarding taxability of BEFIEX credits for certain years, which we are disputing in one of the BEFIEX government assessment cases cited in the prior paragraph. Because the IPI Amnesty case is moving faster than the BEFIEX taxability case, we could be required to pay the IPI Amnesty assessment before obtaining a final decision in the BEFIEX taxability case.

We have received tax assessments from the Brazilian federal tax authorities relating to amounts allegedly due regarding insurance taxes (PIS/COFINS) for tax credits recognized since 2007. These credits were recognized for inputs to certain manufacturing and other business processes. These assessments are being challenged at the administrative and judicial levels in Brazil. The total amount of outstanding tax assessments received for credits recognized for PIS/COFINS inputs is approximately 338 million Brazilian reais (approximately $68 million at March 31, 2024). Based on the opinion of our tax and legal advisors, we have no t accrued any amount related to these assessments.

In addition to the BEFIEX, IPI tax credit and PIS/COFINS inputs matters noted above, other assessments issued by the Brazilian tax authorities related to indirect and income tax matters, and other matters, are at various stages of review in numerous administrative and judicial proceedings. We are vigorously defending our positions related to BEFIEX credits and other Brazil Tax Matters. The amounts related to these assessments will continue to be increased by monetary adjustments at the Selic rate, which is the benchmark rate set by the Brazilian Central Bank. In accordance with our accounting policies, we routinely assess these matters and, when necessary, record our best estimate of a loss.

Litigation is inherently unpredictable and the conclusion of these matters may take many years to ultimately resolve. Amounts at issue in potential future litigation could increase as a result of interest and penalties in future periods. Accordingly, it is possible that an unfavorable outcome in these proceedings could have a material adverse effect on our financial statements in any particular reporting period.

Legacy MDA Europe Legal Matters

Competition Investigation

In 2013, the French Competition Authority ("FCA") commenced an investigation of appliance manufacturers and retailers in France, including Whirlpool and Indesit. The FCA investigation was split into two parts, and in December 2018, we finalized a settlement with the FCA on the first part of the investigation. The second part of the FCA investigation, which is focused primarily on manufacturer interactions with retailers, is ongoing. The Company has agreed to a preliminary settlement range with the FCA and recorded a charge of approximately $69 million in the first half of 2023. The Company expects the settlement amount to be finalized in the first half of 2024, and for payment to be made to the FCA in 2024.

15

Although it is currently not possible to assess the impact, if any, that matters related to the FCA investigation may have on our financial statements, matters related to the FCA investigation could have a material adverse effect on our financial statements in any particular reporting period.

Grenfell Tower

On June 23, 2017, London's Metropolitan Police Service released a statement that it had identified a Hotpoint–branded refrigerator as the initial source of the Grenfell Tower fire in West London. U.K. authorities are conducting investigations, including regarding the cause and spread of the fire. The model in question was manufactured by Indesit Company between 2006 and 2009, prior to Whirlpool's acquisition of Indesit in 2014. We are fully cooperating with the investigating authorities. Whirlpool was named as a defendant in a product liability suit in Pennsylvania federal court related to this matter. The federal court dismissed the case with prejudice in September 2020 and the dismissal was affirmed on appeal in July 2022. Plaintiffs filed a petition with the U.S. Supreme Court in January 2023 which was subsequently denied. In December 2020, lawsuits related to Grenfell Tower were filed in the U.K. against approximately 20 defendants, including Whirlpool Corporation and certain Whirlpool subsidiaries. In the fourth quarter of 2022, we accrued an immaterial amount related to these claims in our financial statements. Additional claims may be filed related to this incident.

Latin America Tax Review

In the first quarter of 2023, we accrued an immaterial amount in our Consolidated Condensed Financial Statements related to prior-period Value Added Tax (VAT) remittances in our Latin America region. We resolved certain aspects of this matter in the second quarter of 2023 and the overall financial statement impact of such resolution was immaterial. We continue to review tax matters within the region for any potential additional impacts, if any; certain matters could have a material adverse effect on our financial statements in any particular reporting period.

Other Litigation

We are currently vigorously defending a number of other lawsuits related to the manufacture and sale of our products which include class action allegations, and may become involved in similar actions. These lawsuits allege claims which include negligence, breach of contract, breach of warranty, product liability and safety claims, false advertising, fraud, and violation of federal and state regulations, including consumer protection laws. In general, we do not have insurance coverage for class action lawsuits. We are also involved in various other legal actions arising in the normal course of business, for which insurance coverage may or may not be available depending on the nature of the action. We dispute the merits of these suits and actions, and intend to vigorously defend them. Management believes, based upon its current knowledge, after taking into consideration legal counsel's evaluation of such suits and actions, and after taking into account current litigation accruals, that the outcome of these matters currently pending against Whirlpool should not have a material adverse effect, if any, on our financial statements.

16

Product Warranty Reserves

Product warranty reserves are included in other current and other noncurrent liabilities in our Consolidated Condensed Balance Sheets. The following table summarizes the changes in total product warranty liability reserves for the periods presented:

| Product Warranty | ||||||||||||||

| Millions of dollars | 2024 | 2023 | ||||||||||||

Balance at January 1 (1) | $ | $ | ||||||||||||

| Issuances/accruals during the period | ||||||||||||||

| Settlements made during the period/other | ( | ( | ||||||||||||

Liabilities classified to held for sale (1) | ||||||||||||||

Balance at March 31 | $ | $ | ||||||||||||

| Current portion | $ | $ | ||||||||||||

| Non-current portion | ||||||||||||||

| Total | $ | $ | ||||||||||||

In the normal course of business, we engage in investigations of potential quality and safety issues. As part of our ongoing effort to deliver quality products to consumers, we are currently investigating certain potential quality and safety issues globally. As necessary, we undertake to effect repair or replacement of appliances in the event that an investigation leads to the conclusion that such action is warranted.

Guarantees

We have guarantee arrangements in a Brazilian subsidiary. For certain creditworthy customers, the subsidiary guarantees customer lines of credit at commercial banks to support purchases following its normal credit policies. If a customer were to default on its line of credit with the bank, our subsidiary would be required to assume the line of credit and satisfy the obligation with the bank. At March 31, 2024 and December 31, 2023, the guaranteed amounts totaled 1.2 billion Brazilian reais (approximately $246 million at March 31, 2024) and 1.3 billion Brazilian reais (approximately $273 million at December 31, 2023), respectively. The fair value of these guarantees were nominal at March 31, 2024 and December 31, 2023. Our subsidiary insures against a significant portion of this credit risk for these guarantees, under normal operating conditions, through policies purchased from high-quality underwriters.

We provide guarantees of indebtedness and lines of credit for various consolidated subsidiaries. The maximum contractual amount of indebtedness and lines of credit available under these lines for consolidated subsidiaries totaled approximately $2.9 billion at March 31, 2024 and $3.0 billion at December 31, 2023, respectively. Our total short-term outstanding bank indebtedness under guarantees (excluding those related to the European major domestic appliance business) was $25 million and $17 million at March 31, 2024 and December 31, 2023, respectively.

17

(7) PENSION AND OTHER POSTRETIREMENT BENEFIT PLANS

The following table summarizes the components of net periodic pension cost and the cost of other postretirement benefits for the periods presented:

| Three Months Ended March 31, | ||||||||||||||||||||||||||||||||||||||

| United States Pension Benefits | Foreign Pension Benefits | Other Postretirement Benefits | ||||||||||||||||||||||||||||||||||||

| Millions of dollars | 2024 | 2023 | 2024 | 2023 | 2024 | 2023 | ||||||||||||||||||||||||||||||||

| Service cost | $ | $ | $ | $ | $ | $ | ||||||||||||||||||||||||||||||||

| Interest cost | ||||||||||||||||||||||||||||||||||||||

| Expected return on plan assets | ( | ( | ( | ( | ||||||||||||||||||||||||||||||||||

| Amortization: | ||||||||||||||||||||||||||||||||||||||

| Actuarial loss | ||||||||||||||||||||||||||||||||||||||

| Prior service credit | ( | |||||||||||||||||||||||||||||||||||||

| Settlement and curtailment (gain) loss | ||||||||||||||||||||||||||||||||||||||

| Net periodic benefit cost (credit) | $ | ( | $ | $ | $ | $ | $ | ( | ||||||||||||||||||||||||||||||

The following table summarizes the net periodic cost recognized in operating profit and interest and sundry (income) expense for the periods presented:

| Three Months Ended March 31, | ||||||||||||||||||||||||||||||||||||||

| United States Pension Benefits | Foreign Pension Benefits | Other Postretirement Benefits | ||||||||||||||||||||||||||||||||||||

| Millions of dollars | 2024 | 2023 | 2024 | 2023 | 2024 | 2023 | ||||||||||||||||||||||||||||||||

| Operating profit (loss) | $ | $ | $ | $ | $ | $ | ||||||||||||||||||||||||||||||||

| Interest and sundry (income) expense | ( | ( | ||||||||||||||||||||||||||||||||||||

| Net periodic benefit cost | $ | ( | $ | $ | $ | $ | $ | ( | ||||||||||||||||||||||||||||||

401(k) Defined Contribution Plan

During the first quarter of 2024, we announced that the Company matching contributions for our 401(k) defined contribution plan, equal to up to 7 % of participants' eligible compensation, covering substantially all U.S. employees will be contributed in company stock starting from March 2024.

(8) HEDGES AND DERIVATIVE FINANCIAL INSTRUMENTS

Derivative instruments are accounted for at fair value based on market rates. Derivatives where we elect hedge accounting are designated as either cash flow, fair value or net investment hedges. Derivatives that are not accounted for based on hedge accounting are marked to market through earnings. If the designated cash flow hedges are highly effective, the gains and losses are recorded in other comprehensive income (loss) and subsequently reclassified to earnings to offset the impact of the hedged items when they occur. In the event it becomes probable the forecasted transaction to which a cash flow hedge relates will not occur, the derivative would be terminated and the amount in accumulated other comprehensive income (loss) would be recognized in earnings. The fair value of the hedge asset or liability is presented in either other current assets / liabilities or other noncurrent assets / liabilities on the Consolidated Condensed Balance Sheets and in other within cash provided by (used in) operating activities in the Consolidated Condensed Statements of Cash Flows.

Using derivative instruments means assuming counterparty credit risk. Counterparty credit risk relates to the loss we could incur if a counterparty were to default on a derivative contract. We generally deal with investment grade counterparties and monitor the overall credit risk and exposure to individual counterparties. We do not anticipate nonperformance by any counterparties. The amount of counterparty credit exposure is limited to the unrealized gains, if any, on such derivative contracts. We do not require nor do we post collateral on such contracts.

18

Hedging Strategy

In the normal course of business, we manage risks relating to our ongoing business operations including those arising from changes in commodity prices, foreign exchange rates and interest rates. Fluctuations in these rates and prices can affect our operating results and financial condition. We use a variety of strategies, including the use of derivative instruments, to manage these risks. We do not enter into derivative financial instruments for trading or speculative purposes.

Commodity Price Risk

We enter into commodity derivative contracts on various commodities to manage the price risk associated with forecasted purchases and sales of material used in our manufacturing process. The objective of these hedges is to reduce the variability of cash flows associated with the forecasted purchases and sales of commodities.

Foreign Currency and Interest Rate Risk

We incur expenses associated with the procurement and production of products in a limited number of countries, while we sell in the local currencies of a large number of countries. Our primary foreign currency exchange exposures result from cross-currency sales of products. As a result, we enter into foreign exchange contracts to hedge certain firm commitments and forecasted transactions to acquire products and services that are denominated in foreign currencies. We enter into certain undesignated non-functional currency asset and liability hedges that relate primarily to short-term payables, receivables, intercompany loans and dividends. When we hedge a foreign currency denominated payable or receivable with a derivative, the effect of changes in the foreign exchange rates are reflected currently in interest and sundry (income) expense for both the payable/receivable and the derivative. Therefore, as a result of the economic hedge, we do not elect hedge accounting.

We also enter into hedges to mitigate currency risk primarily related to forecasted foreign currency denominated expenditures, intercompany financing agreements and royalty agreements and designate them as cash flow hedges. Gains and losses on derivatives designated as cash flow hedges, to the extent they are included in the assessment of effectiveness, are recorded in other comprehensive income (loss) and subsequently reclassified to earnings to offset the impact of the hedged items when they occur.

We may enter into cross-currency interest rate swaps to manage our exposure relating to cross-currency debt. Outstanding notional amounts of cross-currency interest rate swap agreements were $618

We may enter into interest rate swap agreements to manage interest rate risk exposure. Our interest rate swap agreements, if any, effectively modify our exposure to interest rate risk, primarily through converting certain floating rate debt to a fixed rate basis, or certain fixed rate debt to a floating rate basis. These agreements involve either the receipt or payment of floating rate amounts in exchange for fixed rate interest payments or receipts, respectively, over the life of the agreements without an exchange of the underlying principal amounts. We may enter into swap rate lock agreements to effectively reduce our exposure to interest rate risk by locking in interest rates on probable long-term debt issuances. There were no

We may enter into instruments that are designated and qualify as a net investment hedge to manage our exposure related to foreign currency denominated investments. The effective portion of the instruments' gain or loss is reported as a component of other comprehensive income (loss) and recorded in accumulated other comprehensive loss. The gain or loss will be subsequently reclassified into net earnings when the underlying net investment is either sold or substantially liquidated. The remaining change in fair value of the hedge instruments represents the ineffective portion, which is immediately recognized in interest and sundry (income) expense on our Consolidated Condensed Statements of Comprehensive Income (Loss). There were no

19

The following table summarizes our outstanding derivative contracts and their effects in our Consolidated Condensed Balance Sheets at March 31, 2024 and December 31, 2023. Hedge assets and liabilities of our European major domestic appliance business have been classified as held for sale and are excluded from the table below.

| Fair Value of | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Notional Amount | Hedge Assets | Hedge Liabilities | Maximum Term (Months) | |||||||||||||||||||||||||||||||||||||||||||||||||||||

| Millions of dollars | 2024 | 2023 | 2024 | 2023 | 2024 | 2023 | 2024 | 2023 | ||||||||||||||||||||||||||||||||||||||||||||||||

Derivatives accounted for as hedges(1) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Commodity swaps/options | $ | $ | $ | $ | $ | $ | (CF) | |||||||||||||||||||||||||||||||||||||||||||||||||

| Foreign exchange forwards/options | (CF/NI) | |||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Cross-currency swaps | (CF) | |||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Total derivatives accounted for as hedges | $ | $ | $ | $ | ||||||||||||||||||||||||||||||||||||||||||||||||||||

| Derivatives not accounted for as hedges | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Commodity swaps/options | $ | $ | $ | $ | $ | $ | N/A | |||||||||||||||||||||||||||||||||||||||||||||||||

| Foreign exchange forwards/options | N/A | |||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Total derivatives not accounted for as hedges | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Total derivatives | $ | $ | $ | $ | ||||||||||||||||||||||||||||||||||||||||||||||||||||

| Current | $ | $ | $ | $ | ||||||||||||||||||||||||||||||||||||||||||||||||||||

| Noncurrent | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Total derivatives | $ | $ | $ | $ | ||||||||||||||||||||||||||||||||||||||||||||||||||||

(1)Derivatives accounted for as hedges are considered cash flow (CF) hedges.

20

The following tables summarize the effects of derivative instruments on our Consolidated Condensed Statements of Comprehensive Income (Loss) for the periods presented:

| Three Months Ended March 31, | ||||||||||||||||||||||||||

Gain (Loss) Recognized in OCI (Effective Portion ) (2) | ||||||||||||||||||||||||||

| Millions of dollars | 2024 | 2023 | ||||||||||||||||||||||||

| Cash flow hedges | ||||||||||||||||||||||||||

| Commodity swaps/options | $ | $ | ||||||||||||||||||||||||

| Foreign exchange forwards/options | ( | |||||||||||||||||||||||||

| Cross-currency swaps | ( | |||||||||||||||||||||||||

| Interest rate derivatives | ( | |||||||||||||||||||||||||

| $ | $ | ( | ||||||||||||||||||||||||

| Three Months Ended March 31, | ||||||||||||||||||||||||||

| Location of Gain (Loss) Reclassified from OCI into Earnings (Effective Portion) | Gain (Loss) Reclassified from OCI into Earnings (Effective Portion)(3) | |||||||||||||||||||||||||

| Cash Flow Hedges - Millions of dollars | 2024 | 2023 | ||||||||||||||||||||||||

| Commodity swaps/options | Cost of products sold | $ | ( | $ | ||||||||||||||||||||||

| Foreign exchange forwards/options | Net sales | |||||||||||||||||||||||||

| Foreign exchange forwards/options | Cost of products sold | ( | ( | |||||||||||||||||||||||

| Foreign exchange forwards/options | Interest and sundry (income) expense | |||||||||||||||||||||||||

| Cross-currency swaps | Interest and sundry (income) expense | ( | ||||||||||||||||||||||||

| $ | $ | ( | ||||||||||||||||||||||||

| Three Months Ended March 31, | ||||||||||||||||||||||||||

| Location of Gain (Loss) Recognized on Derivatives not Accounted for as Hedges | Gain (Loss) Recognized on Derivatives not Accounted for as Hedges | |||||||||||||||||||||||||

| Derivatives not Accounted for as Hedges - Millions of dollars | 2024 | 2023 | ||||||||||||||||||||||||

| Foreign exchange forwards/options | Interest and sundry (income) expense | $ | ( | $ | ||||||||||||||||||||||

(2)Change in gain (loss) recognized in OCI (effective portion) for the three months ended March 31, 2024 is primarily driven by fluctuations in currency and commodity prices and interest rates compared to prior year. The tax impact of the cash flow hedges was $(9 ) million and $5 million for the three months ended March 31, 2024 and 2023, respectively.

(3)Change in gain (loss) reclassified from OCI into earnings (effective portion) for the three months ended March 31, 2024 was primarily driven by fluctuations in currency and commodity prices and interest rates compared to prior year.

For cash flow hedges, the amount of ineffectiveness recognized in interest and sundry (income) expense was nominal for the periods ended March 31, 2024 and 2023. There were no hedges designated as fair value for the periods ended March 31, 2024 and 2023. The net amount of unrealized gain or loss on derivative instruments included in accumulated OCI related to contracts maturing and expected to be realized during the next twelve months is a loss of $7 million at March 31, 2024.

(9) FAIR VALUE MEASUREMENTS

21

The following table summarizes the valuation of our assets and liabilities measured at fair value on a recurring basis at March 31, 2024 and December 31, 2023:

| Fair Value | ||||||||||||||||||||||||||||||||||||||||||||||||||

| Millions of dollars | Total Cost Basis | Level 1 | Level 2 | Total | ||||||||||||||||||||||||||||||||||||||||||||||

| Measured at fair value on a recurring basis: | 2024 | 2023 | 2024 | 2023 | 2024 | 2023 | 2024 | 2023 | ||||||||||||||||||||||||||||||||||||||||||

Short-term investments (1) | $ | $ | $ | $ | $ | $ | $ | $ | ||||||||||||||||||||||||||||||||||||||||||

| Net derivative contracts | ( | ( | ( | ( | ||||||||||||||||||||||||||||||||||||||||||||||

The non-recurring fair values represent only those assets whose carrying values were adjusted to fair value during the reporting period.

European Major Domestic Appliance Business Held for Sale

On January 16, 2023, the Company entered into a contribution agreement with Arçelik A.Ş (“Arcelik”). Under the terms of the agreement, Whirlpool will contribute its European major domestic appliance business, and Arcelik will contribute its European major domestic appliance, consumer electronics, air conditioning, and small domestic appliance businesses into the newly formed entity of which Whirlpool will own 25 % and Arcelik 75 %.

On December 20, 2022, the Company's board authorized the transaction with Arcelik and the European major domestic appliance business was classified as held for sale during the fourth quarter of 2022. The disposal group was measured at fair value less cost to sell. We used a discounted cash flow analysis and multiple market data points in our analysis to determine fair value (Level 3 input) of the 25 % interest retained, resulting in an estimated fair value of $139 million. The discounted cash flow analysis utilized a discount rate of 16.5 % at December 31, 2022.

During the first quarter of 2024, the fair value of the disposal group was updated based on working capital adjustments, cash flow assumptions and changes in discount rates. This updated assessment resulted in an estimated fair value of $227 million at March 31, 2024. The discounted cash flow analysis utilized a discount rate of 15.5 %.

During the three months ended March 31, 2024, we recorded a loss of $247 million to the loss on sale and disposal of businesses. The adjustment reflects ongoing reassessment of the fair value less costs to sell of the disposal group and transaction costs. The transaction closed on April 1, 2024 and no further fair value adjustments are expected in subsequent quarters related to the contribution of our European major domestic appliance business.

During the three months ended March 31, 2023, we recorded an increase of $222 million to the loss on sale and disposal of businesses.

See Note 14 to the Consolidated Condensed Financial Statements for additional information.

Other Fair Value Measurements

The fair value of long-term debt (including current maturities) was $6.8 billion and $6.9 billion at March 31, 2024 and December 31, 2023, respectively, and was estimated using discounted cash flow analysis based on incremental borrowing rates for similar types of borrowing arrangements (Level 2 input).

22

(10) STOCKHOLDERS' EQUITY

The following table summarizes the changes in stockholders' equity for the periods presented:

| Whirlpool Stockholders' Equity | ||||||||||||||||||||||||||||||||||||||

| Total | Retained Earnings | Accumulated Other Comprehensive Income (Loss) | Treasury Stock / Additional Paid-In-Capital | Common Stock | Non-Controlling Interest | |||||||||||||||||||||||||||||||||

| Balances, December 31, 2023 | $ | $ | $ | ( | $ | ( | $ | $ | ||||||||||||||||||||||||||||||

| Comprehensive income (loss) | ||||||||||||||||||||||||||||||||||||||

| Net earnings (loss) | ( | ( | — | — | — | |||||||||||||||||||||||||||||||||

| Other comprehensive income | — | — | — | — | ||||||||||||||||||||||||||||||||||

| Comprehensive income (loss) | ( | ( | — | — | ||||||||||||||||||||||||||||||||||

| Stock issued (repurchased) | ( | — | — | ( | — | — | ||||||||||||||||||||||||||||||||

| Sale of minority interest in subsidiary | — | — | ||||||||||||||||||||||||||||||||||||

| Dividends declared | ( | ( | — | — | — | |||||||||||||||||||||||||||||||||

| Balances, March 31, 2024 | $ | $ | $ | ( | $ | ( | $ | $ | ||||||||||||||||||||||||||||||

| Whirlpool Stockholders' Equity | ||||||||||||||||||||||||||||||||||||||

| Total | Retained Earnings | Accumulated Other Comprehensive Income (Loss) | Treasury Stock / Additional Paid-In-Capital | Common Stock | Non-Controlling Interest | |||||||||||||||||||||||||||||||||

| Balances, December 31, 2022 | $ | $ | $ | ( | $ | ( | $ | $ | ||||||||||||||||||||||||||||||

| Comprehensive income (loss) | ||||||||||||||||||||||||||||||||||||||

| Net earnings (loss) | ( | ( | — | — | — | |||||||||||||||||||||||||||||||||

| Other comprehensive income | ( | — | ( | — | — | — | ||||||||||||||||||||||||||||||||

| Comprehensive income (loss) | ( | ( | ( | — | — | |||||||||||||||||||||||||||||||||

| Stock issued (repurchased) | — | — | — | — | ||||||||||||||||||||||||||||||||||

| Dividends declared | ( | ( | — | — | — | — | ||||||||||||||||||||||||||||||||

| Balances, March 31, 2023 | $ | $ | $ | ( | $ | ( | $ | $ | ||||||||||||||||||||||||||||||

Other Comprehensive Income (Loss)

The following table summarizes our other comprehensive income (loss) and related tax effects for the periods presented:

| Three Months Ended March 31, | ||||||||||||||||||||||||||

| 2024 | 2023 | |||||||||||||||||||||||||

| Millions of dollars | Pre-tax | Tax Effect | Net | Pre-tax | Tax Effect | Net | ||||||||||||||||||||

| Currency translation adjustments | $ | ( | $ | $ | ( | $ | ( | $ | $ | ( | ||||||||||||||||

| Cash flow hedges | ( | ( | ( | |||||||||||||||||||||||

| Pension and other postretirement benefits plans | ( | ( | ||||||||||||||||||||||||

| Other comprehensive income (loss) | ( | ( | ( | |||||||||||||||||||||||

| Less: Other comprehensive income (loss) available to noncontrolling interests | ||||||||||||||||||||||||||

| Other comprehensive income (loss) available to Whirlpool | $ | $ | ( | $ | $ | ( | $ | $ | ( | |||||||||||||||||

23

Reclassifications Out of Accumulated Other Comprehensive Income (Loss)

There were no material net impacts of the reclassification adjustments out of accumulated other comprehensive income (loss) included in net earnings (loss) for the three months ended March 31, 2024.

Net earnings (loss) per Share

Diluted net earnings (loss) per share of common stock include the dilutive effect of stock options and other share-based compensation plans. Basic and diluted net earnings (loss) per share of common stock for the periods presented were calculated as follows:

| Three Months Ended March 31, | ||||||||||||||

| Millions of dollars and shares | 2024 | 2023 | ||||||||||||

| Numerator for basic and diluted earnings per share - Net earnings (loss) available to Whirlpool | $ | ( | $ | ( | ||||||||||

| Denominator for basic earnings per share - weighted-average shares | ||||||||||||||

| Denominator for diluted earnings per share - adjusted weighted-average shares | ||||||||||||||

| Anti-dilutive stock options/awards excluded from earnings per share | ||||||||||||||

Share Repurchase Program

On April 19, 2021, our Board of Directors authorized a share repurchase program of up to $2 billion, which has no expiration date. On February 14, 2022, the Board of Directors authorized an additional $2 billion in share repurchases under the Company's ongoing share repurchase program. During the three months ended March 31, 2024, we repurchased 456 thousand shares under the share repurchase program at an aggregate price of approximately $50 million. At March 31, 2024, there were approximately $2.5 billion in remaining funds authorized under this program.

(11) RESTRUCTURING CHARGES

We periodically take action to improve operating efficiencies, typically in connection with business acquisitions or changes in the economic environment. Our footprint and headcount reductions and organizational integration actions relate to discrete, unique restructuring events, primarily reflected in the following plans.

In March 2024, the Company committed to workforce reduction plans in the United States and globally, in an effort to reduce complexity and simplify our organizational model after the European major domestic appliance transaction. The workforce reduction plans included involuntary severance actions as of the end of the first quarter of 2024. Total expected costs for these actions is $23 million, of which we have incurred $14 million in employee termination costs and $9 million other associated costs within the first quarter. All of these costs will result in cash settlements primarily in 2024. The Company is currently evaluating certain follow-on restructuring actions for the remainder of 2024.

The following table summarizes the changes to our restructuring liability during the three months ended March 31, 2024:

| Millions of Dollars | December 31, 2023 | Charge to Earnings | Cash Paid | Non-Cash and Other | March 31, 2024 | ||||||||||||

| Employee Termination | $ | $ | $ | ( | $ | $ | |||||||||||

| Other exit costs | |||||||||||||||||

| Total | $ | $ | $ | ( | $ | $ | |||||||||||

The following table summarizes the restructuring charges by operating segment and Corporate for the periods presented:

24

| Millions of dollars | Three Months Ended March 31 | |||||||

| 2024 | 2023 | |||||||

| MDA North America | $ | $ | ||||||

| MDA Latin America | ||||||||

| MDA Asia | ||||||||

| Corporate/Other | ||||||||

| Total | $ | $ | ||||||

(12) INCOME TAXES

Income tax expense was $76 million for the three months ended March 31, 2024, compared to income tax expense of $68 million for the same period of 2023. The increase in tax expense is primarily due to the sale of minority shares in Whirlpool of India and related capital gains, and legal entity restructuring tax impacts.

The following table summarizes the difference between income tax expense (benefit) at the U.S. statutory rate of 21% and the income tax expense (benefit) at effective worldwide tax rates for the respective periods:

| Three Months Ended March 31, | |||||||||||

| Millions of dollars | 2024 | 2023 | |||||||||

| Earnings (Loss) before income taxes | $ | ( | $ | ( | |||||||

| Income tax expense (benefit) computed at United States statutory tax rate | ( | ( | |||||||||

| State and local taxes, net of federal tax benefit | ( | ||||||||||

| Valuation allowances | |||||||||||

| Audit and Settlements | |||||||||||

| U.S. foreign income items, net of credits | ( | ||||||||||

| Sale of minority shares and capital gains | |||||||||||

| Legal Entity restructuring tax impact | ( | ||||||||||

| Non deductible impairments | |||||||||||

| Non deductible fines and penalties | |||||||||||

| Other | |||||||||||

| Income tax expense (benefit) computed at effective worldwide tax rates | $ | $ | |||||||||

At the end of each interim period, we estimate the effective tax rate expected to be applicable for the full fiscal year and the impact of discrete items, if any, and adjust the quarterly rate as necessary.

Subsequent Events

On April 1, 2024, the Company completed its transaction with Arcelik related to its European and MENA businesses. The disposal group has been classified as held for sale starting from the fourth quarter of 2022, resulting in a cumulative loss from disposal of businesses of approximately $1.9 billion through the first quarter of 2024. For income tax purposes, some of these losses were not realizable by the Company until the transaction closed in the second quarter of 2024. In addition to income tax recorded to date, the Company estimates that it will record additional deferred tax assets of between $100 and $300 million, net of applicable reserves and valuation allowances, in the second quarter of 2024, as a result of closing the transaction with Arcelik. For additional information, see Note 14 to the Consolidated Condensed Financial Statements.

25

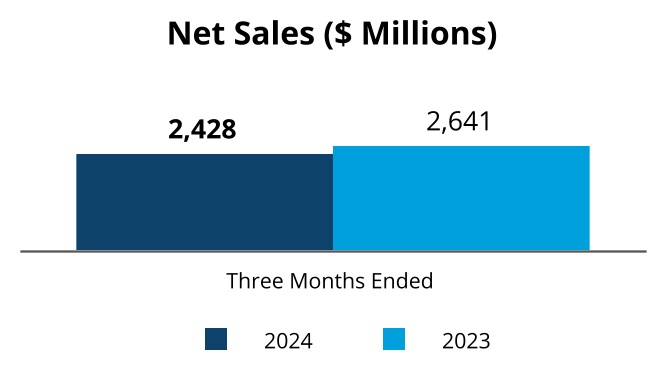

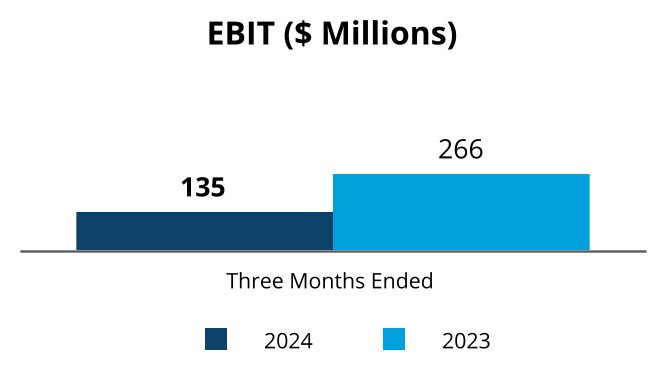

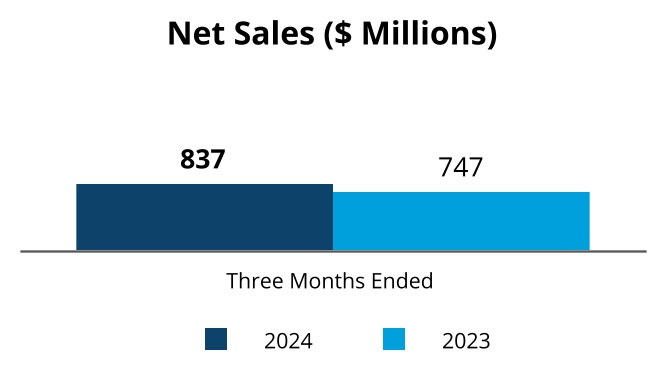

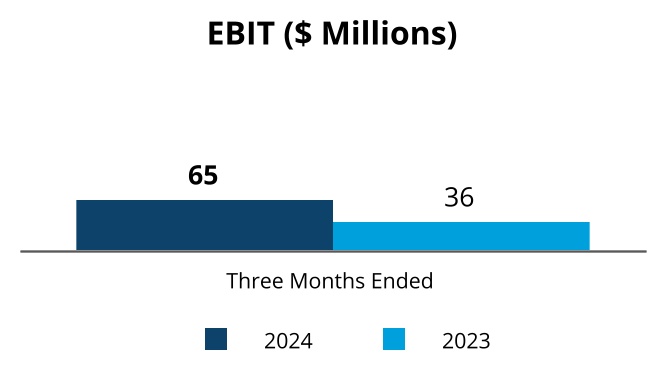

(13) SEGMENT INFORMATION

Beginning January 1, 2024, we reorganized our operating segment structure to better represent the revised structure within our portfolio transformation, including a greater focus on our strong value creating small domestic appliance business. The Company implemented this change to align with the Company's new operating structure, consistent with how the Company’s Chief Operating Decision Maker evaluates performance and allocates resources in accordance with ASC 280, Segment Reporting. Our reportable segments consist of Major Domestic Appliances ("MDA") North America; MDA Europe, MDA Latin America; MDA Asia; and Small Domestic Appliances ("SDA") Global. All prior period amounts have been reclassified to conform with current period presentation.