Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

SCHEDULE 14A

Proxy Statement Pursuant to Section 14(a) of the

Securities Exchange Act of 1934

(Amendment No. )

Filed by the Registrant x Filed by a Party other than the Registrant ¨

Check the appropriate box:

| ¨ | Preliminary Proxy Statement | |||

| ¨ | Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2)) | |||

| x | Definitive Proxy Statement | |||

| ¨ | Definitive Additional Materials | |||

| ¨ | Soliciting Material Pursuant to §240.14a-12 | |||

CAPITAL TRUST, INC. | ||||

| (Name of Registrant as Specified In Its Charter) | ||||

| (Name of Person(s) Filing Proxy Statement, if other than the Registrant) | ||||

| Payment of Filing Fee (Check the appropriate box): | ||||

| x | No fee required. | |||

| ¨ | Fee computed on table below per Exchange Act Rules 14a-6(i)(1) and 0-11. | |||

| (1) | Title of each class of securities to which transaction applies:

| |||

|

| ||||

| (2) | Aggregate number of securities to which transaction applies:

| |||

|

| ||||

| (3) | Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11 (set forth the amount on which the filing fee is calculated and state how it was determined):

| |||

|

| ||||

| (4) | Proposed maximum aggregate value of transaction:

| |||

|

| ||||

| (5) | Total fee paid: | |||

|

| ||||

| ¨ | Fee paid previously with preliminary materials. | |||

| ¨ | Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the Form or Schedule and the date of its filing. | |||

| (1) | Amount Previously Paid:

| |||

|

| ||||

| (2) | Form, Schedule or Registration Statement No.:

| |||

|

| ||||

| (3) | Filing Party:

| |||

|

| ||||

| (4) | Date Filed:

| |||

|

| ||||

Table of Contents

CAPITAL TRUST, INC.

410 Park Avenue, 14th Floor

New York, New York 10022

November 12, 2012

Dear Stockholders:

You are cordially invited to attend a special meeting of stockholders of Capital Trust, Inc., a Maryland corporation, which we refer to as Capital Trust, which will be held at 10:00 a.m., New York City time, on December 19, 2012, at the offices of Paul Hastings LLP, 75 East 55th Street, New York, New York 10022.

As previously announced, on September 27, 2012 we entered into a purchase and sale agreement, which we refer to as the Purchase Agreement, with Huskies Acquisition LLC, which we refer to as the Purchaser, an affiliate of The Blackstone Group L.P., pursuant to which, among other things, the Purchaser has agreed to purchase our investment management and special servicing business and make an equity investment in us. We are seeking our stockholders’ approval of four related and interdependent proposals related to the Purchase Agreement.

If the transactions contemplated by the Purchase Agreement, which we refer to as the Transactions, are completed, we will pay a special cash dividend of $2.00 per share to all holders of record of our class A common stock, par value $0.01 per share, which we refer to as our Common Stock, as of the close of business on November 12, 2012, the record date for the special meeting.

At the special meeting, you are being asked to consider and vote on proposals, which we refer to as the Proposals, to approve:

| 1. | the Purchase Agreement, including the sale of our investment management and special servicing business, including our subsidiary, CT Investment Management Co., LLC, and related private investment fund co-investments, to the Purchaser for a purchase price of $20,629,004; |

| 2. | the issuance and sale of 5,000,000 shares of our Common Stock to the Purchaser for a purchase price of $10,000,000, or $2.00 per share (these shares will not be entitled to the $2.00 per share special dividend); |

| 3. | the entry by Capital Trust into a new management agreement with an affiliate of The Blackstone Group L.P., which we refer to as the New CT Manager; and |

| 4. | certain amendments to our charter contemplated by the Purchase Agreement, which provides, among other things, subject to certain exceptions, that none of The Blackstone Group L.P. or its affiliates (as such term is defined in the charter amendments), our directors or any person our directors control shall have any duty to refrain, directly or indirectly, from engaging in business opportunities or competing with us. |

The Proposals comprise a group of related and interdependent proposals for stockholder action. Implementation of each such Proposal is contingent upon the implementation of each of the other Proposals. Accordingly, we will not implement any of the Proposals unless all of the Proposals are approved by our stockholders by the affirmative vote of the holders of a majority of the shares of our Common Stock outstanding and entitled to vote at the special meeting.

Following completion of the Transactions, we will remain publicly traded and listed on the New York Stock Exchange under the external management of the New CT Manager, and our existing stockholders will retain their investment in our Common Stock held by them on such date. We will retain our interest in CT Legacy REIT

Table of Contents

Mezz Borrower, Inc., a vehicle formed to finance certain legacy assets in connection with our March 31, 2011 comprehensive debt restructuring, our existing cash balances (as reduced to fund the expenses of the Transactions and the special dividend), our carried interest in CT Opportunity Partners I, LP, a private investment fund under our management that will be managed by the New CT Manager following consummation of the Transactions, and our interests in three collateralized debt obligations sponsored by us.

After careful consideration, our board of directors has determined that the Transactions are advisable and in the best interests of Capital Trust. Our board of directors recommends that you vote “FOR” each of the Proposals.

Only stockholders who hold shares of our Common Stock at the close of business on November 12, 2012 will be entitled to vote at the special meeting. Whether or not you expect to attend the special meeting in person, we urge you to submit your proxy as promptly as possible (1) through the Internet, (2) by telephone or (3) by marking, signing and dating the enclosed proxy card and returning it in the postage-paid envelope provided. If you hold your shares in “street name,” you should instruct your broker how to vote in accordance with your voting instruction card. If you do not submit your proxy, do not instruct your broker how to vote your shares or do not vote in person at the special meeting, it will have the same effect as a vote “AGAINST” each of the Proposals. If you have any questions about any of the proposals described in the accompanying proxy statement, please call MacKenzie Partners, Inc., toll-free at (800) 322-2885 or call collect at (212) 929-5500.

You are encouraged to read carefully the accompanying proxy statement in its entirety, including the annexes and the section titled “Risk Factors” beginning on page 12.

If you have questions about any of the Proposals or need to obtain proxy cards or other information related to the proxy solicitation, you may contact MacKenzie Partners, Inc., our proxy solicitor, at the address and telephone numbers listed below.

MacKenzie Partners, Inc.

105 Madison Avenue

New York, New York 10016

Tel: (800) 322-2885 (toll free) or (212) 929-5500 (call collect)

Email: proxy@mackenziepartners.com

Thank you for your cooperation and your continued support of Capital Trust.

| Sincerely, |

| /s/ Samuel Zell |

| Samuel Zell |

| Chairman of the Board |

Neither the Securities and Exchange Commission nor any state securities regulatory agency has approved or disapproved the Transactions, passed upon the merits or fairness of the Transactions or passed upon the adequacy of the disclosure in the proxy statement. Any representation to the contrary is a criminal offense.

Table of Contents

CAPITAL TRUST, INC.

410 Park Avenue, 14th Floor

New York, New York 10022

NOTICE OF SPECIAL MEETING OF STOCKHOLDERS

TO BE HELD ON DECEMBER 19, 2012

To our Stockholders:

We hereby notify you that we are holding a special meeting of stockholders of Capital Trust, Inc., a Maryland corporation, which we refer to as Capital Trust, at the offices of Paul Hastings LLP, 75 East 55th Street, New York, New York 10022, on December 19, 2012, at 10:00 a.m., New York City time, for the following purposes:

| 1. | to consider and vote upon a proposal to approve the purchase and sale agreement, dated September 27, 2012, by and between Capital Trust and Huskies Acquisition LLC, which we refer to as the Purchaser, an affiliate of The Blackstone Group L.P., including the sale of our investment management and special servicing business, including our subsidiary, CT Investment Management Co., LLC, and our related private investment fund co-investments, to the Purchaser, for a purchase price of $20,629,004, pursuant to the terms and subject to the conditions contained in the purchase and sale agreement, as more fully described in the accompanying proxy statement. A copy of the purchase and sale agreement is attached to the accompanying proxy statement as Annex A, which we refer to as the Purchase Agreement. We refer to this proposal as the Investment Management Business Sale Proposal; |

| 2. | to consider and vote upon a proposal to approve the issuance and sale of 5,000,000 shares of our class A common stock, par value $0.01 per share, which we refer to as our Common Stock, to the Purchaser for a purchase price of $10,000,000, or $2.00 per share, pursuant to the terms and subject to the conditions contained in the Purchase Agreement, as more fully described in the accompanying proxy statement. These 5,000,000 shares will represent approximately 17.1% of our outstanding Common Stock after such issuance based on the number of shares outstanding as of the date of this proxy statement. We refer to this proposal as the Purchaser Investment Proposal; |

| 3. | to consider and vote upon a proposal to approve the entry by us into a new management agreement with an affiliate of The Blackstone Group L.P., which we refer to as the New CT Manager, in substantially the form attached to the accompanying proxy statement as Annex B, pursuant to which we will become externally managed by the New CT Manager, as more fully described in the accompanying proxy statement. We refer to the new management agreement with the New CT Manager as the New Management Agreement and to this proposal as the Management Agreement Proposal; |

| 4. | to consider and vote upon a proposal to approve certain amendments to our charter contemplated by the Purchase Agreement in the form attached to the accompanying proxy statement as Annex C, which provides, among other things, subject to certain exceptions, that none of The Blackstone Group L.P. or its affiliates (as such term is defined in the charter amendments), our directors or any person our directors control shall have any duty to refrain, directly or indirectly, from engaging in business opportunities or competing with us, as more fully described in the accompanying proxy statement. We refer to this proposal as the Charter Amendment Proposal; and |

| 5. | to consider and vote upon a proposal to approve the adjournment of the special meeting if necessary or appropriate to solicit additional proxies if there are insufficient votes to approve the Investment Management Business Sale Proposal, the Purchaser Investment Proposal, the Management Agreement Proposal or the Charter Amendment Proposal. We refer to this proposal as the Adjournment Proposal. |

Table of Contents

The Investment Management Business Sale Proposal, the Purchaser Investment Proposal, the Management Agreement Proposal and the Charter Amendment Proposal, which we refer to collectively as the Proposals and each individually as a Proposal, comprise a group of related and interdependent proposals for stockholder action. Implementation of each such Proposal is contingent upon the implementation of each of the other Proposals. Accordingly, we will not implement any of the foregoing Proposals unless all of the Proposals are approved by our stockholders. Approval of the Adjournment Proposal is not a requirement for implementation of the other Proposals.

You can vote your shares of our Common Stock if our records show that you were a stockholder as of the close of business on November 12, 2012, the record date for the special meeting of stockholders, which we refer to as the record date.

If all of the Proposals are approved by our stockholders and the transactions contemplated by the Purchase Agreement are consummated, we will pay a special cash dividend of $2.00 per share to all holders of record of our Common Stock as of the close of business on the record date. The Purchaser will not be entitled to participate in the special dividend.

All Capital Trust, Inc. stockholders are cordially invited to attend the special meeting in person. However, to assure your representation at the special meeting, please submit your proxy as promptly as possible using one of the following methods: (1) through the Internet, (2) by telephone or (3) by marking, signing and dating the enclosed proxy card and returning it in the postage-paid envelope provided. Any stockholder attending the special meeting may vote in person even if he or she has authorized a proxy to vote his or her shares using the Internet, telephone or proxy card.

| By Order of the Board of Directors, |

| /s/ Geoffrey G. Jervis |

| Geoffrey G. Jervis |

| Secretary |

November 12, 2012

Table of Contents

CAPITAL TRUST, INC.

410 Park Avenue, 14th Floor

New York, New York 10022

PROXY STATEMENT FOR

SPECIAL MEETING OF STOCKHOLDERS

TO BE HELD ON DECEMBER 19, 2012

This proxy statement is being furnished by and on behalf of our board of directors in connection with the solicitation of proxies to be voted at the special meeting of stockholders, which we refer to as the special meeting. This proxy statement is first being mailed to our stockholders on or about November 13, 2012.

The date, time and place of the special meeting are:

Date: December 19, 2012

Time: 10:00 a.m., New York City time

Place: The law offices of Paul Hastings LLP

75 East 55th Street, New York, New York 10022

At the special meeting, stockholders will be asked to:

| 1. | consider and vote upon a proposal to approve the purchase and sale agreement, dated September 27, 2012, by and between Capital Trust, Inc. and Huskies Acquisition LLC, which we refer to as the Purchaser, an affiliate of The Blackstone Group L.P., including the sale of our investment management and special servicing business, including our subsidiary, CT Investment Management Co., LLC, which we refer to as CTIMCO, and our related private investment fund co-investments, to the Purchaser for a purchase price of $20,629,004, pursuant to the terms and subject to the conditions contained in the purchase and sale agreement, as more fully described in this proxy statement. A copy of the purchase and sale agreement is attached to this proxy statement as Annex A, which we refer to as the Purchase Agreement. We refer to this proposal as the Investment Management Business Sale Proposal; |

| 2. | consider and vote upon a proposal to approve the issuance and sale of 5,000,000 shares of our class A common stock, par value $0.01 per share, which we refer to as our Common Stock, to the Purchaser for a purchase price of $10,000,000, or $2.00 per share, pursuant to the terms and subject to the conditions contained in the Purchase Agreement, as more fully described in this proxy statement. These 5,000,000 shares will represent approximately 17.1% of our outstanding Common Stock after such issuance based on the number of shares outstanding as of the date of this proxy statement. We refer to the shares to be issued to the Purchaser as the New CT Shares and this proposal as the Purchaser Investment Proposal; |

| 3. | consider and vote upon a proposal to approve the entry by us into a new management agreement with an affiliate of The Blackstone Group L.P., which we refer to as the New CT Manager, in substantially the form attached to the accompanying proxy statement as Annex B, pursuant to which we will become externally managed by the New CT Manager, as more fully described in this proxy statement. We refer to the new management agreement with the New CT Manager as the New Management Agreement and to this proposal as the Management Agreement Proposal; |

| 4. | consider and vote upon a proposal to approve certain amendments to our charter contemplated by the Purchase Agreement in the form attached to the accompanying proxy statement as Annex C, which provides, among other things, subject to certain exceptions, that none of The Blackstone Group L.P. or its affiliates (as such term is defined in the charter amendments), our directors and any person our |

Table of Contents

| directors control shall have any duty to refrain, directly or indirectly, from engaging in business opportunities or competing with us, as more fully described in this proxy statement. We refer to this proposal as the Charter Amendment Proposal; and |

| 5. | consider and vote upon a proposal to approve the adjournment of the special meeting if necessary or appropriate to solicit additional proxies if there are insufficient votes to approve the Investment Management Business Sale Proposal, the Purchaser Investment Proposal, the Management Agreement Proposal and the Charter Amendment Proposal. We refer to this proposal as the Adjournment Proposal. |

The transactions contemplated to be consummated by the Purchase Agreement are referred to in this proxy statement as the Transactions.

If all of the Proposals are approved by our stockholders and the Transactions are completed, we will pay a special cash dividend of $2.00 per share to all holders of record of our Common Stock as of the close of business on the record date, which we refer to as the special dividend. The Purchaser will not be entitled to participate in the special dividend.

Following completion of the Transactions, we will remain publicly traded and listed on the New York Stock Exchange, which we refer to as the NYSE, under the external management of the New CT Manager, and our existing stockholders will retain their investment in our Common Stock held by them on such date. We will retain our interest in CT Legacy REIT Mezz Borrower, Inc., which we refer to as CT Legacy REIT, a vehicle formed to finance certain legacy assets that were refinanced in connection with our March 31, 2011 comprehensive debt restructuring, our existing cash balances (as reduced to fund the expenses of the Transactions and the special dividend discussed below), our carried interest in CT Opportunity Partners I, LP, which we refer to as CTOPI, a private investment fund under our management that will be managed by the New CT Manager following consummation of the Transactions, and our interests in three collateralized debt obligations, which we refer to as CDOs, sponsored by us.

The Investment Management Business Sale Proposal, the Purchaser Investment Proposal, the Management Agreement Proposal and the Charter Amendment Proposal, which we refer to collectively as the Proposals and each individually as a Proposal, comprise a group of related and interdependent proposals for stockholder action. Implementation of each such Proposal is contingent upon the implementation of each of the other Proposals. Accordingly, we will not implement any of the foregoing Proposals unless all of the Proposals are approved by our stockholders. Approval of the Adjournment Proposal is not a requirement for implementation of the other Proposals.

You can vote your shares of our Common Stock if our records show that you were a stockholder as of the close of business on November 12, 2012, the record date for the special meeting of stockholders, which we refer to as the record date.

Our principal offices are located at 410 Park Avenue, 14th Floor, New York, New York 10022 and our telephone number is (212) 655-0220.

Table of Contents

i

Table of Contents

The following is a summary that highlights information contained elsewhere in this proxy statement and the annexes hereto. This summary may not contain all of the information that may be important to you. For a more complete description of the Purchase Agreement and the Transactions, we encourage you to read carefully this proxy statement, including the attached annexes, in its entirety. References herein to “we,” “us,” “our,” “Capital Trust” or “the company” refer to Capital Trust, Inc., a Maryland corporation, and its subsidiaries unless the context specifically requires otherwise. References herein to “Blackstone” refer to The Blackstone Group L.P., a Delaware limited partnership, and its subsidiaries, including the Purchaser, unless the context specifically requires otherwise.

The Parties

Huskies Acquisition LLC

c/o The Blackstone Group L.P.

345 Park Avenue

New York, New York 10154

(212) 583-5000

Huskies Acquisition LLC is a Delaware limited liability company formed in connection with the Transactions by affiliates of Blackstone.

About Blackstone

Blackstone is one of the world’s leading investment and advisory firms. Our alternative asset management businesses include the management of private equity funds, real estate funds, hedge fund solutions, credit-oriented funds and closed-end funds. The Blackstone Group also provides various financial advisory services, including financial and strategic advisory, restructuring and reorganization advisory and fund placement services. Through its different businesses, Blackstone had total fee-earning assets under management of approximately $157.6 billion as of June 30, 2012. Blackstone is traded on the NYSE under the symbol “BX,” and is headquartered in New York City.

Capital Trust, Inc.

410 Park Avenue

14th Floor

New York, New York 10022

(212) 655-0220

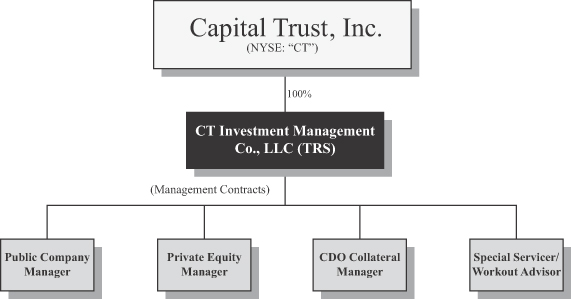

Capital Trust is a real estate finance company that specializes in credit sensitive financial products. To date, our investment programs have focused on loans and securities backed by commercial real estate assets. We invest for our own account directly on our balance sheet and for third parties through a series of investment funds and managed separate accounts. From the inception of our finance business in 1997 through June 30, 2012, we have completed over $12.0 billion of commercial real estate investments. We conduct our operations as a real estate investment trust, or REIT, for federal income tax purposes. Capital Trust is traded on the NYSE under the symbol “CT,” and is headquartered in New York City.

The Transactions

Our entry into the Purchase Agreement and our agreement to consummate the Transactions represent the culmination of a review of strategic alternatives undertaken by our board of directors. The Transactions achieve

1

Table of Contents

our board’s goal of maximizing stockholder value with a strategic transaction that provides a meaningful and current cash return for our stockholders and allows our stockholders to continue to participate in the recovery of our legacy assets with the benefit of ongoing asset management provided by our senior management team. Following consummation of the Transactions, we will remain publicly traded and will be externally managed by an affiliate of Blackstone, and as a result our stockholders will continue to hold an ongoing investment in Capital Trust and can benefit from any potential opportunities developed in the future.

The Purchase Agreement contemplates two principal transactions:

| • | the sale of our investment management and special servicing business, including the sale of CTIMCO and our private investment fund co-investments, to the Purchaser, for a purchase price of $20,629,004, which we refer to as the CT Investment Management Interests Purchase Price, pursuant to the terms and subject to the conditions contained in the Purchase Agreement, which are described in this proxy statement under “Proposal 1—Investment Management Business Sale Proposal” beginning on page 82; and |

| • | the issuance and sale of 5,000,000 shares of our Common Stock to the Purchaser for a purchase price of $10,000,000, or $2.00 per share, which we refer to as the New CT Shares Purchase Price, pursuant to the terms and subject to the conditions contained in the Purchase Agreement, which are described in this proxy statement under “Proposal 2—Purchaser Investment Proposal” beginning on page 85. |

We refer to the sale of our investment management and special servicing business contemplated in Proposal 1 as the Investment Management Business Sale, the Purchaser’s investment in our Common Stock contemplated in Proposal 2 as the Purchaser Investment and these transactions together as the Principal Transactions. We refer to the CT Investment Management Interests Purchase Price and the New CT Shares Purchase Price together as the Purchase Price.

The consummation of the Principal Transactions is subject to the satisfaction of a number of closing conditions as described under “Purchase Agreement—Conditions to Closing” beginning on page 57. These closing conditions include the following, for which we are also seeking the approval of our stockholders at the special meeting:

| • | the entry by Capital Trust into the New Management Agreement with the New CT Manager, in substantially the form attached to this proxy statement as Annex B, pursuant to which we will become externally managed by the New CT Manager, which is described in this proxy statement under “Proposal 3—Management Agreement Proposal” beginning on page 87; and |

| • | adoption of the amendments to our charter contemplated by the Purchase Agreement in substantially the form attached to this proxy statement as Annex C, which provides, among other things, subject to certain exceptions, that none of Blackstone or its affiliates (as such term is defined in the charter amendments), our directors and any person our directors control shall have any duty to refrain, directly or indirectly, from engaging in business opportunities or competing with us, as more fully described in this proxy statement under “Proposal 4—Charter Amendment Proposal” beginning on page 88. |

Upon consummation of the Transactions, we will no longer be engaged in the investment management and special servicing businesses, but will retain our interest in CT Legacy REIT, our existing cash balances (as reduced to fund the expenses of the Transactions and the special dividend), our carried interest in CTOPI and our retained interests in three CDOs sponsored by us. We will remain publicly traded and listed on the NYSE under the external management of the New CT Manager, an affiliate of Blackstone, pursuant to the New Management Agreement, and our existing stockholders will retain their investment in our Common Stock held by them on such date subject to the dilution experienced from the issuance of 5,000,000 shares of our Common Stock to the Purchaser. Based on the 24,205,573 shares of Common Stock outstanding as of the record date for the special meeting upon the consummation of the Purchaser Investment, the Purchaser will own 17.1% of our outstanding Common Stock.

2

Table of Contents

New Management Agreement

Upon completion of the Transactions, we will enter into the New Management Agreement with the New CT Manager, pursuant to which we will become externally managed by the New CT Manager. While Blackstone has not yet determined the persons who will serve as officers and employees of the New CT Manager, it is expected that the New CT Manager will be managed (including with respect to investment decisions to be made on behalf of CT) by senior professionals of Blackstone and certain of our current executive officers.

For pro forma information relating to the fees we would have paid to the New CT Manager pursuant to the New Management Agreement had it been in effect during the six months ended June 30, 2012 and the year ended December 31, 2011, please see “New Management Agreement—Pro Forma New Management Agreement Fees” beginning on page 69.

Board Designation Rights

The Purchase Agreement provides the Purchaser with the right to designate two individuals for election to our board of directors, one of whom will be appointed as chairman of our board of directors. This right will be effective upon the completion of the Transactions and for so long as certain ownership thresholds are maintained by Blackstone and its affiliates. See “Purchase Agreement—Covenants—Board Designation Rights” beginning on page 56. Upon the consummation of the Transactions, it is expected that Samuel Zell, chairman of our board of directors, will resign from our board of directors.

Capital Trust Is Prohibited From Soliciting Others

The Purchase Agreement contains detailed provisions that prohibit us and our subsidiaries, directors, officers, employees and representatives from, among other things, directly or indirectly, soliciting, initiating, or knowingly encouraging or inducing or taking any action which would reasonably be expected to lead to a third party making an acquisition proposal (as defined in the Purchase Agreement). The Purchase Agreement does not, however, prohibit our board of directors from considering and recommending to our stockholders an unsolicited acquisition proposal from a third party if specified conditions are met. If our board of directors changes its recommendation in favor of the Transactions, the Purchaser will be able to terminate the Purchase Agreement, and we would be required to reimburse the Purchaser for its expenses in connection with the contemplated Transactions and the Purchaser’s pursuit thereof, up to a maximum of $1.5 million. For additional information regarding the non-solicitation provisions in the Purchase Agreement, see “Purchase Agreement—Covenants—No Solicitation” beginning on page 52.

Termination of the Purchase Agreement

The Purchase Agreement may be terminated prior to the successful completion of the Transactions:

| (i) | upon the mutual written consent of both us and the Purchaser; |

| (ii) | by either us or the Purchaser, if the closing shall not have occurred on or prior to 5:00 p.m., New York time, on June 27, 2013, which we refer to as the outside date; provided, however, that a breach of the Purchase Agreement by the party seeking to terminate is not the cause of the failure of the closing to occur by such time; |

| (iii) | by either us or the Purchaser, if any law or governmental authority prohibits the consummation of the Transactions; provided, however, that a breach of the Purchase Agreement by the party seeking to terminate is not the cause; |

| (iv) | by either us or the Purchaser, if approval by our stockholders of the Proposals is not obtained at the special meeting; |

3

Table of Contents

| (v) | by the Purchaser, if our board of directors has changed its recommendation that our stockholders approve the Proposals or takes certain other actions that reflect a lack of support for the Transactions, in either case, prior to the special meeting; and |

| (vi) | by either us or the Purchaser, if the other party shall have breached any representation, warranty, covenant or agreement under the Purchase Agreement, which breach cannot be or has not been cured within thirty (30) days after being given written notice thereof, and which breach would give rise to the failure of a mutual closing condition or a Purchaser/Capital Trust closing condition. |

For additional information regarding the termination provisions in the Purchase Agreement, see “Purchase Agreement—Termination” beginning on page 60.

Expense Reimbursement

We have agreed to reimburse Blackstone for all fees and expenses incurred by or on behalf of Blackstone and its affiliates in connection with the Transactions and the pursuit and negotiation thereof, subject to a cap of $1.5 million under certain circumstances and if specified conditions are met in connection with a termination of the Purchase Agreement. Blackstone has agreed to reimburse us for all fees and expenses incurred after July 3, 2012 by or on behalf of us and our affiliates in connection with the Transactions and the pursuit and negotiation thereof, subject to a cap of $1.5 million in the aggregate if we terminate the Purchase Agreement due to a breach by the Purchaser of the Purchase Agreement as described under item (vi) under “—Termination of the Purchase Agreement” above. For additional information regarding the expense reimbursement provisions in the Purchase Agreement, see “Purchase Agreement—Expense Reimbursement” beginning on page 60.

Effects If the Transactions Are Not Completed

If any of the Proposals are not approved by our stockholders, or if the Transactions are not completed for any other reason, our stockholders will not receive the $2.00 per share special dividend and we will continue to operate our businesses as we have in the past. In addition, we may pursue strategic alternatives with others if the Transactions are not completed.

Unaudited Pro Forma Financial Information

Selected unaudited pro forma financial information giving effect to the Investment Management Business Sale, including the entry into the New Management Agreement, and the Purchaser Investment is set forth in “Unaudited Pro Forma Financial Information” beginning on page 24.

Voting Agreement

Concurrently with the execution and delivery of the Purchase Agreement, the Purchaser entered into a voting agreement with W. R. Berkley Corporation, which we refer to as W. R. Berkley, and several of its affiliates, which own in the aggregate 3,843,413 shares, or approximately 15.9%, of our outstanding Common Stock as of the record date for the special meeting. Pursuant to the terms of the voting agreement, such stockholders agreed to, among other things, vote their respective shares of our Common Stock in favor of the Proposals and against the approval of any acquisition proposal (as defined in the Purchase Agreement). Such stockholders have also agreed not to sell or transfer their respective shares of our Common Stock, subject to certain exceptions, or to solicit any acquisition transaction. The voting agreement will terminate upon, among other things, the closing of the Investment Management Business Sale and the Purchaser Investment, consummation of the Transactions contemplated by the Purchase Agreement and a change in Capital Trust’s board of directors’ recommendations with respect to the approval of the Proposals. For additional information on the voting agreement, please see “Voting Agreement” beginning on page 74.

4

Table of Contents

Letter Agreement with W. R. Berkley

As an inducement to W. R. Berkley to enter into the voting agreement, we entered into a letter agreement with W. R. Berkley pursuant to which we agreed not to engage in certain offerings of our equity securities following the closing of the Transactions without the approval of a majority of our independent directors. The letter agreement will lapse once approval of a majority of our independent directors has been obtained with respect to the first applicable offering. For additional information on the letter agreement with W. R. Berkley, please see “Voting Agreement—Letter Agreement with W. R. Berkley” beginning on page 75.

Interests of Certain Persons in the Proposals

In considering the recommendation of our board of directors, our stockholders should be aware that our largest stockholder, W. R. Berkley, the chairman of our board of directors, and certain of our executive officers have certain interests in the Proposals that are in addition to the interests of our stockholders generally. Our board of directors was aware of these interests and considered them in approving the Purchase Agreement and the Transactions governed thereby and recommending that our stockholders approve the Proposals. As a result of the consummation of the Transactions:

| • | our executive officers are expected to receive offers of employment with Blackstone upon consummation of the Transactions; |

| • | certain incentive awards granted to our executive officers in the form of restricted stock will become 100% vested as a result of the consummation of the Transactions; |

| • | restricted stock awards held by our executive officers that would otherwise vest in the future, if at all, will become 100% vested as a result of the consummation of the Transactions; |

| • | annual performance-based bonuses for 2012 will be paid based on the higher of “target” or actual performance as a result of the consummation of the Transactions, if the Transactions are consummated before December 31, 2012; |

| • | certain performance based incentive compensation awards held by our executive officers will be modified; |

| • | our directors and executive officers will continue to be indemnified and covered by directors’ and officers’ insurance following consummation of the Transactions; |

| • | CTIMCO, which will be owned by Blackstone following consummation of the Transactions, will continue to manage certain separate accounts for affiliates of W. R. Berkley; and |

| • | a subsidiary of CTIMCO, which will be owned by Blackstone following consummation of the Transactions, will continue to manage a private fund in which an affiliate of the chairman of our board of directors is invested. |

It is expected that Mr. Steven Plavin, our chief executive officer, Mr. Geoffrey Jervis, our chief financial officer, and Mr. Thomas Ruffing, our chief credit officer, will continue in such roles as our executive officers following consummation of the Transactions.

Please see “Interest of Certain Persons in the Transactions” beginning on page 42 for further information concerning these interests.

Recommendation of Our Board of Directors

Our board of directors has unanimously determined to recommend a vote in favor of approval of each of the Proposals and the Adjournment Proposal (excluding one director who could not attend the meeting at which the Transactions were approved but who subsequently confirmed his approval of the Proposals and the Transactions). Our board of directors believes that the Transactions are fair to, and in the best interests of, Capital Trust. For a discussion of the factors considered by our board of directors in reaching its decision to recommend approval of the Transactions, please see “Background of the Transactions and Recommendation” beginning on page 31.

5

Table of Contents

Opinion of Capital Trust’s Financial Advisor

In connection with the Transactions, Evercore Group L.L.C., which we refer to as Evercore, delivered to a special committee of our board of directors a written opinion, dated September 27, 2012, as to the fairness, from a financial point of view and as of the date of the opinion, of the Purchase Price (as such term is defined in “Opinion of Capital Trust’s Financial Advisor” beginning on page 76) to be received by Capital Trust in connection with the Principal Transactions. The full text of the written opinion, which describes, among other things, the assumptions made, procedures followed, factors considered and limitations on the review undertaken, is attached as Annex F to this proxy statement and is incorporated by reference herein in its entirety. Evercore provided its opinion to the special committee for the information and benefit of the committee in connection with its evaluation of the Principal Transactions. Evercore’s opinion does not address any other aspect of the Transactions and does not constitute a recommendation to any stockholder as to how to vote in connection with the Proposals. For further information regarding Evercore’s financial opinion, please see “Opinion of Capital Trust’s Financial Advisor” beginning on page 76.

Special Dividend

In accordance with the Purchase Agreement, our board of directors has authorized and we have declared a special dividend of $2.00 per share, which dividend will be decreased by the aggregate per share amount of any dividends we declare or pay to our stockholders after September 27, 2012 and prior to the closing of the Transactions, payable to stockholders of record on the record date for the special meeting, November 12, 2012. Payment of the special dividend is contingent upon the consummation of the Transactions and accordingly will not be paid unless all the Proposals are approved by the required affirmative vote of holders of a majority of the shares of Common Stock outstanding and entitled to vote at the special meeting. We will pay the special dividend as soon as practicable following the closing of the Transactions. The Purchaser, in its capacity as the holder of the New CT Shares to be purchased pursuant to the Purchase Agreement, will not be entitled to participate in the special dividend, as it will not be a stockholder of record on the record date for the special meeting.

As required by the NYSE’s procedures, from November 7, 2012 (three business days prior to the special meeting and special dividend record date) through the special dividend payment date, our Common Stock will trade with “due-bills” representing an assignment of the right to receive the special dividend, and our Common Stock will not trade ex-dividend until the first business day after the special dividend payment date. The payment date for the special dividend is expected to be as soon as practicable following the special meeting and the completion of the Transactions. Stockholders who sell their shares on or before the special dividend payment date will not be entitled to receive the special dividend. Due-bills obligate a seller to deliver the dividend to the buyer. The due-bill obligations are settled customarily between the brokers representing the buyers and sellers of the stock. Capital Trust has no obligations for either the amount of the due-bill or the processing of the due-bill. Buyers and sellers of our common stock should consult their broker before trading in our Common Stock to be sure they understand the effect of the NYSE’s due-bill procedures.

Regulatory Matters

The consummation of the Transactions does not require the consent or approval of any government or regulatory agency. However, the sale of CTIMCO, a Securities and Exchange Commission, which we refer to as the SEC, registered investment adviser, to the Purchaser as part of the Investment Management Business Sale requires CTIMCO to file an amendment to its current Form ADV on file with the SEC promptly following the closing of such sale to reflect changes relating to the ownership and persons in control of CTIMCO post-closing.

6

Table of Contents

Certain United States Federal Income Tax Considerations

Our stockholders will not recognize gain or loss for federal income tax purposes as a result of the Transactions (excluding the $2.00 per share special dividend, the consequences of which are addressed under “Certain United States Federal Income Tax Considerations” beginning on page 91).

Amendment of Rights Agreement

Pursuant to the Purchase Agreement, on September 27, 2012, we entered into an amendment to our Tax Benefits Preservation Rights Agreement dated as of March 31, 2011, which we refer to as the Rights Agreement, by and between us and American Stock Transfer & Trust Company, LLC, which, among other things, exempted the Transactions from application of the triggering provisions of the Rights Agreement. For additional information on the amendment to the Rights Agreement, please see “Purchase Agreement—Amendment of the Tax Benefits Preservation Rights Agreement” beginning on page 61.

Registration Rights

As a condition to the consummation of Transactions, we will upon closing of the Transactions enter into a registration rights agreement pursuant to which we will agree, upon demand, subject to certain terms and conditions, to register for resale under the Securities Act of 1933, as amended, which we refer to as the Securities Act, the New CT Shares sold to the Purchaser and assist in the facilitation of certain sales of such shares by Purchaser. For additional information on the registration rights agreements, please see “Purchase Agreement—Registration Rights Agreement” beginning on page 61 and “Proposal 2—Purchaser Investment Proposal” beginning on page 85.

No Appraisal Rights

Under Maryland law, stockholders are not entitled to any dissenters’ appraisal rights in connection with the Transactions. Please see “Risk Factors—Risk Factors Related to the Transactions—Our stockholders will not have the right to appraisal of their investment in our Common Stock in connection with the Transactions” beginning on page 14.

7

Table of Contents

QUESTIONS AND ANSWERS ABOUT THE SPECIAL MEETING AND VOTING

The following are some questions that you, as a stockholder of Capital Trust, may have regarding the Proposals and the special meeting and brief answers to those questions. We urge you to read carefully the remainder of this proxy statement because the information in this section may not provide all the information that might be important to you with respect to the Transactions and the special meeting. Additional important information is also contained in the annexes to this proxy statement.

Where and when will the special meeting be held?

The date, time and place of the meeting are:

December 19, 2012

10:00 a.m. (New York City time)

The law offices of Paul Hastings LLP

75 East 55th Street

New York, New York 10022

Why am I receiving this proxy statement?

Our board of directors is furnishing this proxy statement to you in connection with the solicitation of proxies to be voted at the special meeting of stockholders or at any adjournments of the special meeting because our records show that you were a stockholder as of the record date.

What Proposals will the stockholders vote on at the special meeting?

Proposal 1—Investment Management Business Sale Proposal. At the special meeting, stockholders will be asked to approve the Purchase Agreement, including the sale of our investment management and special servicing business and the sale of CTIMCO and related private investment fund co-investments, to the Purchaser, for a purchase price of $20,629,004, pursuant to the terms and subject to the conditions contained in the Purchase Agreement.

Pursuant to the Purchase Agreement, we will sell to the Purchaser our entire ownership interest in CTIMCO, through which we operate our investment management and special servicing businesses, and certain related private fund co-investments and other interests. As result of this sale, we will no longer be engaged in the investment management and special servicing businesses and upon entry into the New Management Agreement (as discussed below), we will no longer have our own employees and will be externally managed by the New CT Manager.

The Investment Management Business Sale Proposal is described more specifically herein under “Proposal 1—Investment Management Business Sale Proposal” beginning on page 82.

Proposal 2—Purchaser Investment Proposal. At the special meeting, our stockholders will be asked to approve the issuance and sale of 5,000,000 shares of our Common Stock (representing approximately 17.1% of our outstanding Common Stock after such issuance based on the number of shares outstanding as of the date of this proxy statement) to the Purchaser for a purchase price of $10,000,000, or $2.00 per share, pursuant to the terms and subject to the conditions contained in the Purchase Agreement. These newly issued shares will not be entitled to the $2.00 per share special dividend to be paid upon consummation of the Transactions.

The Purchaser Investment Proposal is described more specifically herein under “Proposal 2—Purchaser Investment Proposal” beginning on page 85.

Proposal 3—Management Agreement Proposal. At the special meeting, our stockholders will be asked to approve the entry by Capital Trust into the New Management Agreement, pursuant to which we will become externally managed by the New CT Manager.

8

Table of Contents

Upon consummation of the Transactions, it is expected that our executive officers and other key employees will become employed by Blackstone, and we will no longer have any employees. The day-to-day management of our business and affairs will be delegated to the New CT Manager pursuant to the terms of the New Management Agreement. It is expected that the New CT Manager will be managed by senior professionals of Blackstone and certain of our current executive officers and that our former employees, who will be employed by the New CT Manager, will carry out functions similar to those carried out for us when they were employed by us, such that we will benefit from a continuity in the management of our business and affairs. There may, however, be certain conflicts between these former employees and/or the New CT Manager and us which did not exist prior to the Transactions (see “Risk Factors” beginning on page 12).

The Management Agreement Proposal is described more specifically herein under “Proposal 3—Management Agreement Proposal” beginning on page 87.

Proposal 4—Charter Amendment Proposal. At the special meeting, our stockholders will be asked to approve certain amendments to our charter contemplated by the Purchase Agreement. The charter amendments provide, among other things, subject to certain exceptions, that none of Blackstone or its affiliates (as such term is defined in the charter amendments), our directors or any person our directors control shall have any duty to refrain, directly or indirectly, from engaging in business opportunities or competing with us.

The Charter Amendment Proposal is described more specifically herein under “Proposal 4—Charter Amendment Proposal” beginning on page 88.

Proposal 5—Adjournment Proposal. At the special meeting our stockholders will be asked to approve the adjournment of the special meeting if necessary or appropriate to solicit additional proxies if there are insufficient votes to approve the Proposals.

Are the Proposals contingent upon one another?

Yes. All of the Proposals comprise a group of related and interdependent proposals for stockholder action. Implementation of each Proposal is contingent upon the implementation of the other Proposals. Accordingly, we will not implement any of the Proposals unless each of the Proposals is approved by our stockholders. Implementation of the Adjournment Proposal is not contingent upon the implementation of the Proposals.

How does the board of directors recommend that I vote?

Our board of directors recommends that our stockholders vote to approve each of the Proposals and the Adjournment Proposal.

When are the Transactions expected to be completed?

The parties currently expect to close the Transactions in late 2012 or early 2013.

You can vote your shares of our Common Stock if our records show that you were the owner of the shares as of the close of business on November 12, 2012, the record date for determining the stockholders entitled to vote at the special meeting and any adjournments or postponements thereof. As of November 12, 2012, there were a total of 24,205,573 shares of our Common Stock outstanding and entitled to vote at the special meeting. You have one vote for each share of our Common Stock that you own.

We will convene the special meeting if stockholders representing the required quorum of shares of Common Stock entitled to vote either sign and return their paper proxy cards, authorize a proxy to vote electronically or telephonically or attend the meeting. A majority of the shares of Common Stock entitled to vote at the special meeting, present in person or by proxy, will constitute a quorum. If you sign and return your paper proxy card or

9

Table of Contents

authorize a proxy to vote electronically or telephonically, your shares will be counted to determine whether we have a quorum even if you abstain or fail to vote as indicated in the proxy materials. Broker non-votes (which occur when a brokerage firm has not received voting instructions from the beneficial owner on a non-routine matter, as defined by the NYSE), if any, will also be considered present for the purpose of determining whether we have a quorum.

What vote is required to approve each of the Proposals?

We cannot complete the Transactions unless each of the Proposals is approved by the affirmative vote of the holders of a majority of our outstanding shares of Common Stock entitled to vote on each such Proposal at the special meeting. The Adjournment Proposal must be approved by the affirmative vote of a majority of the votes cast, whether in person or by proxy, at the special meeting.

What will happen if I abstain from voting or fail to vote?

Your abstention or failure to submit a proxy or vote in person at the special meeting, will have the same effect as a vote “AGAINST” each of the Proposals. Your abstention or failure to submit a proxy or vote in person at the special meeting, will have no effect on the Adjournment Proposal.

You may vote by proxy or in person at the special meeting.

Voting by Proxy. If you hold your shares as stockholder of record, you may authorize a proxy to vote your shares by mail, on the Internet or by telephone. If you submit a proxy on the Internet or by telephone, you should not return the proxy card accompanying this proxy statement.

| • | Voting by Mail. You may authorize a proxy to vote your shares by mail by marking the proxy card accompanying this proxy statement, dating and signing it, and returning it in the postage-paid envelope provided. Please allow sufficient time for mailing if you decide to submit a proxy for your shares by mail. |

| • | Vote on the Internet. You may also authorize a proxy to vote your shares on the Internet, by going to the www.proxyvote.com website and follow the instructions. Please have your proxy card in hand when accessing the website, as it contains a 12-digit control number required to authorize your proxy. |

| • | Vote by Telephone. You may also authorize a proxy to vote your shares by telephone, by calling the toll-free number reflected on the proxy card. Please have your proxy card in hand when calling the toll-free number, as it contains a 12-digit control number required to authorize your proxy. |

You can authorize a proxy to vote by telephone or via the Internet at any time prior to 11:59 p.m., New York City time, on December 18, 2012.

Voting in Person. If you hold shares as a stockholder of record and plan to attend the special meeting and wish to vote in person, you will be given a ballot at the special meeting. Alternatively, you may provide us with a signed proxy card at the special meeting before voting is closed. If you would like to vote in person, please bring proof of identification with you to the special meeting. Even if you plan to attend the special meeting, we strongly encourage you to submit a proxy for your shares in advance as described above, so your vote will be counted if you are not able to attend. If your shares are held in street name, you must bring to the special meeting a proxy from the record holder of the shares (your broker, bank or other nominee) authorizing you to vote at the special meeting. To do this, you should contact your broker, bank or other nominee as soon as possible.

If I hold my shares in street name through my broker, will my broker vote these shares for me?

If you hold your shares in street name, you must provide your broker, bank or other nominee with instructions in order to vote those shares. To do so, you should follow the voting instructions provided to you by

10

Table of Contents

your bank, broker or other nominee. If your bank, broker or nominee holds your shares in its name and you do not instruct it how to vote, it will not have discretion to vote on any of the Proposals or the Adjournment Proposal at the special meeting.

Can I change my vote after I have submitted my proxy?

Yes. If your shares are held in “street name” you must contact your broker, bank or other nominee to change your vote. If you are a holder of record, you can change your vote at any time before your proxy is voted at the special meeting by:

| • | delivering a signed written notice revoking your proxy card to the Secretary of Capital Trust at the following address: Capital Trust, Inc., 410 Park Avenue, 14th Floor, New York, New York 10022, Attention: Secretary |

| • | signing and delivering a new, valid proxy bearing a later date; |

| • | submitting another proxy by telephone or on the Internet by 11:59 p.m. New York City time on December 18, 2012 (your latest telephone or Internet voting instructions will be followed); or |

| • | attending the special meeting and voting your proxy in person, although your attendance alone will not revoke your proxy. |

What should I do if I receive more than one set of voting materials for the special meeting?

You may receive more than one set of voting materials for the special meeting, including multiple copies of this proxy statement and multiple proxy cards or voting instruction forms. For example, if you hold your shares in more than one brokerage account, you will receive a separate voting instruction form for each brokerage account in which you hold shares. If you are a holder of record and your shares are registered in more than one name, you will receive more than one proxy card. Please complete, sign, date and return each proxy card and voting instruction form that you receive.

What if I do not specify a choice for a matter when returning a proxy?

If you hold your shares of record, proxies that are signed and returned without voting instructions will be voted “FOR” each of the Proposals and the Adjournment Proposal.

Who pays for this proxy solicitation?

We do. In addition to sending you these proxy materials, some of our employees may contact you by telephone, by mail or in person. None of these employees will receive any extra compensation for doing this. We have engaged Mackenzie Partners, Inc., an outside proxy solicitation firm, to solicit votes and the cost to us of engaging such a firm is estimated to be $40,000 plus reasonable out-of-pocket expenses.

11

Table of Contents

In addition to the other information included in this proxy statement, including the matters addressed in the section of the proxy statement entitled “Special Note Regarding Forward-Looking Information,” you should carefully consider the following risks before deciding how to vote on the proposals presented at the special meeting. The risk factors related to the Transactions present risks directly related to the Transactions. We have also included risks associated with Capital Trust as a result of the externalization of our management with the New CT Manager following the consummation of the Transactions. The risks and uncertainties described below are not the only risks and uncertainties that we face. Additional risks and uncertainties not presently known to us or that we currently deem immaterial may also impair our business operations. The risks below also include forward-looking information, and our actual results may differ substantially from those discussed in this forward-looking information. See “Special Note Regarding Forward-Looking Information” beginning on page 21.

Risk Factors Related to the Transactions

The market price of our Common Stock may decline as a result of the Transactions.

We may fail to realize all of the benefits anticipated in the Transactions or our operations may be impacted by unanticipated factors. Any of these factors could adversely affect our business and results of operations and contribute to a decrease in the price of our Common Stock. In addition, the market price of our Common Stock may decline when it begins to trade ex-dividend with respect to the special dividend.

We will become externally managed and advised as result of the Transactions and will no longer have employees to manage our day-to-day activities.

Upon consummation of the Transactions, we will become externally managed and advised by the New CT Manager, an affiliate of Blackstone. We will no longer have employees and all of our officers will be employees of Blackstone or its affiliates. We will have no separate facilities and will be completely reliant on the New CT Manager, which has significant discretion as to the implementation of our investment and operating policies and strategies.

Our success will depend to a significant extent upon the efforts, experience, diligence, skill and network of business contacts of the executive officers and key personnel of the New CT Manager and its affiliates. Blackstone has not yet determined the persons who will serve as the officers and employees of the New CT Manager, but it is expected that the New CT Manager will be managed by senior professionals of Blackstone and certain of our current executive officers. These individuals will evaluate, negotiate, execute and monitor our investments; therefore, our success will depend on their continued service with the New CT Manager and its affiliates. The departure of one or more of the executive officers or key personnel from the New CT Manager and its affiliates could have a material adverse effect on our performance.

In addition, we can offer no assurance that the New CT Manager will remain our investment manager or that we will continue to have access to the New CT Manager’s officers and key personnel. The initial term of the New Management Agreement only extends until the third anniversary of the closing of the Transactions. Thereafter, the New Management Agreement will be renewable for one-year terms; provided, however, that the New CT Manager may terminate the New Management Agreement annually upon 180 days’ prior notice. If the New Management Agreement is terminated and no suitable replacement is found to manage us, we may not be able to execute our business plan. Furthermore, we may incur certain costs in connection with a termination of the New Management Agreement. See “—Termination of the New Management Agreement would be costly.” below.

Blackstone will have the ability to influence our affairs and the outcome of matters submitted to a vote of stockholders.

The 5,000,000 shares of our Common Stock acquired by the Purchaser upon consummation of the Transactions will represent approximately 17.1% of our outstanding Common Stock following such issuance

12

Table of Contents

(based on the number of shares outstanding as of the date of this proxy statement). The Purchaser will also be entitled to designate two individuals for election to our board of directors, one of whom will be appointed as chairman of our board of directors. The voting power associated with this ownership along with its board designation rights will provide Blackstone the ability to influence our affairs and the outcome of matters required to be submitted to stockholders for approval.

In the event we experience an “ownership change” for purposes of Section 382 of the Internal Revenue Code of 1986, as amended, our ability to utilize our net operating losses and net capital losses against future taxable income will be limited, increasing our dividend distribution requirement for which we may not have sufficient cash flow.

We have substantial net operating and net capital loss carry forwards which we use to offset our taxable income and thereby reduce our tax liability and/or our distribution requirements. In the event that we experience an “ownership change” for purposes of Section 382 of the Internal Revenue Code of 1986, as amended, which we refer to as the Internal Revenue Code, our ability to use these losses could be effectively eliminated. We would experience an “ownership change” if, over a rolling three-year testing period, the percentage of our Common Stock owned by one or more persons who own, directly or constructively, 5% or more of our Common Stock, which we refer to as Five-Percent Stockholders, has increased by more than 50 percentage points over the lowest percentage of our Common Stock owned by such Five-Percent Stockholders during the three-year testing period. Increased ownership by Five-Percent Stockholders can occur as a result of an issuance of stock, such as pursuant to the Purchaser Investment Proposal, as well as by regular trading activity in our Common Stock. Following the Transactions, and assuming the full cashless exercise of the warrants to purchase our Common Stock that we issued in connection with the March 2009 restructuring of our debt obligations at an assumed fair market value of our Common Stock of $4.00 per share, Five-Percent Stockholders would have experienced a net increase in their percentage ownership of our Common Stock of approximately 26 percentage points over the three-year testing period, leaving less than 25 percentage points of increased ownership by Five-Percent Stockholders until we would experience an ownership change. The issuance of our preferred stock purchase rights pursuant to our Rights Agreement deters but does not prevent such an ownership change. We have also exempted Blackstone and its affiliates from certain provisions of the Rights Agreement. See “Purchase Agreement—Amendment of the Tax Benefits Preservation Rights Agreement” beginning on page 61. In addition, if we decide to take steps to preserve these tax benefits, our ability to raise additional capital through offerings of our Common Stock or other classes of our participating stock could be substantially constrained.

We have agreed to exempt the Purchaser, Blackstone and their respective affiliates from certain statutory anti-takeover protections.

Pursuant to the Purchase Agreement, our board of directors has (i) amended our bylaws to render the application of Maryland Control Share Acquisition Act inapplicable to any acquisition of Common Stock by (a) the Purchaser and its present affiliates and (b) Blackstone and its present and future affiliates and (ii) irrevocably resolved that the Maryland Business Combination Act will not apply to any “business combination” (as defined in the Maryland Business Combination Act) of Capital Trust with (a) the Purchaser or its present affiliates or (b) Blackstone and any of its present or future affiliates; provided, however, that the Purchaser or any of its present affiliates and Blackstone and any of its present or future affiliates, shall not enter into any “business combination” with Capital Trust without the prior approval of at least a majority of the directors who are not affiliates or associates of the Purchaser or Blackstone. The Maryland Control Share Acquisition Act and the Maryland Business Combination Act provide protections that are designed to deter unsolicited takeover attempts and, as a result of these exemptions, those statutory provisions will not be available to deter any transaction involving the Purchaser, Blackstone or their respective affiliates, unless the Purchase Agreement is terminated.

13

Table of Contents

Shares eligible for sale in the near future may cause the market price for our Common Stock to decline.

The Purchaser will own 5,000,000 shares of our Common Stock following the closing of the Transactions for which we have granted registration rights that, beginning on the first anniversary of the closing, will facilitate the resale of such shares in the public market, and any such resale would increase the number of shares of our Common Stock available for public trading. Sales of a substantial number of shares of our Common Stock in the public market, or the perception that such sales might occur, could have a material adverse effect on the price of our Common Stock and may also impair our ability to raise additional capital through the sale of our equity securities in the future.

Our stockholders will not have the right to appraisal of their investment in our Common Stock in connection with the Transactions.

There are no appraisal or dissenters’ rights that are available to our stockholders under Maryland law or our charter or bylaws in connection with the Transactions. As a result, our stockholders will not be able to have the fair value of their investment in our Common Stock judicially appraised and paid to them in cash in connection with the Transactions.

The amendments to our charter reflected in the Charter Amendment Proposal contain provisions that reduce or eliminate duties of Blackstone and our directors with respect to corporate opportunities and competitive activities.

The amendments to our charter reflected in the Charter Amendment Proposal effectively eliminate the duties of Blackstone and its affiliates (as such term is defined in the charter amendments), and our directors or any person our directors control to present to us business opportunities or to refrain from competing with us that otherwise may exist in the absence of such amended charter provisions. Under the charter amendments, Blackstone and its affiliates and our directors or any person our directors control will not be obligated to present to us opportunities unless they are expressly offered to such person in his or her capacity as a director or officer of Capital Trust and will be able to engage in competing activities without any restriction imposed as a result of Blackstone’s or its affiliates’ status as a stockholder or Blackstone’s affiliates’ status as officers or directors of Capital Trust.

Risk Factors Related to Capital Trust as a Result of the Externalization of Management

The personnel of the New CT Manager, as our external manager, will not be required to dedicate a specific portion of their time to the management of our business.

Except as expressly required by the New Management Agreement, neither the New CT Manager nor any other Blackstone affiliate will be obligated to dedicate any specific personnel exclusively to us, nor are they or their personnel obligated to dedicate any specific portion of their time to the management of our business. As a result, we cannot provide any assurances regarding the amount of time the New CT Manager or its affiliates will dedicate to the management of our business and the New CT Manager may have conflicts in allocating its time, resources and services among our business and any other investment vehicles and accounts the New CT Manager (or its personnel) may manage. It is expected that each of our officers following consummation of the Transactions will also be an employee of the New CT Manager or another Blackstone affiliate, who has now or may be expected to have significant responsibilities for other investment vehicles currently managed by Blackstone and its affiliates. Consequently, we may not receive the level of support and assistance that we otherwise might receive if we were internally managed. The New CT Manager and its affiliates are not restricted from entering into other investment advisory relationships or from engaging in other business activities.

The New CT Manager manages our portfolio pursuant to very broad investment guidelines and our board of directors will not approve each investment decision made by the New CT Manager, which may result in our making riskier investments with which you may not agree and which could cause our operating results and the value of our Common Stock to decline.

The New CT Manager will be authorized to follow very broad investment guidelines. Our board of directors will periodically review our investment guidelines and our investment portfolio but will not, and will not be

14

Table of Contents

required to, review and approve in advance all of our proposed investments. In addition, in conducting periodic reviews, our directors may rely primarily on information provided to them by the New CT Manager or its affiliates. Subject to maintaining our REIT qualification and our exemption from regulation under the Investment Company Act of 1940, as amended, which we refer to as the Investment Company Act, the New CT Manager has significant latitude within the broad investment guidelines in determining the types of investments it makes for us, which could result in investment returns that are substantially below expectations or that result in losses, which would cause our operating results and the value of our Common Stock to decline.

The New CT Manager’s fee structure may not create proper incentives or may induce the New CT Manager and its affiliates to make certain investments, including speculative investments, which increase the risk of our investment portfolio.

We will pay the New CT Manager base management fees regardless of the performance of our portfolio. The New CT Manager’s entitlement to a base management fee, which is not based upon performance metrics or goals, might reduce its incentive to devote its time and effort to seeking investments that provide attractive risk-adjusted returns for our portfolio. Because the base management fees are also based in part on our outstanding equity, the New CT Manager may also be incentivized to advance strategies that increase our equity, and there may be circumstances where increasing our equity will not optimize the returns for our stockholders. Consequently, we may be required to pay the New CT Manager base management fees in a particular quarter despite experiencing a net loss or a decline in the value of our portfolio during that quarter. In connection with the Transactions, we also entered into a letter agreement with W. R. Berkley pursuant to which we agreed not to engage in certain offerings of our equity securities following the closing of the Transactions without the approval of a majority of our independent directors. See “Voting Agreement—Letter Agreement with W. R. Berkley” beginning on page 75.

In addition, the New CT Manager has the ability to earn incentive fees each quarter based on our excess earnings, which may create an incentive for the New CT Manager to invest in assets with higher yield potential, which are generally riskier or more speculative, or sell an asset prematurely for a gain, in an effort to increase our short-term net income and thereby increase the incentive fees to which it is entitled. If our interests and those of the New CT Manager are not aligned, the execution of our business plan and our results of operations could be adversely affected, which could materially and adversely affect our ability to make distributions to our stockholders and the market price of our Common Stock.

We may compete with existing and future private and public investment vehicles established and/or managed by Blackstone or its affiliates, which may present various conflicts of interest that restrict our ability to pursue certain investment opportunities or take other actions that are beneficial to our business and result in decisions that are not in the best interests of our stockholders.

Following the consummation of the Transactions, we will be subject to conflicts of interest arising out of our relationship with Blackstone, including the New CT Manager and its affiliates. Blackstone will be entitled to appoint two nominees to serve on our board of directors (one of whom will be appointed as chairman of our board of directors), and Stephen D. Plavin, who will continue as our chief executive officer and a member of our board, Geoffrey G. Jervis, who will continue as our chief financial officer, and Thomas C. Ruffing, who will continue as our chief credit officer, will be executives of Blackstone and/or one or more of its affiliates, and we will be managed by the New CT Manager, a Blackstone affiliate. There is no guarantee that the policies and procedures adopted by us, the terms and conditions of the New Management Agreement or the policies and procedures adopted by the New CT Manager, Blackstone and their affiliates, will enable us to identify, adequately address or mitigate these conflicts of interest.

Some examples of conflicts of interest that may arise following consummation of the Transactions by virtue of our relationship with the New CT Manager and Blackstone include:

| • | Broad and Wide-Ranging Activities. The New CT Manager, Blackstone and their affiliates engage in a broad spectrum of activities, including a broad range of activities relating to investments in the real |

15

Table of Contents