United States

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

☒ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended: July 31, 2019

☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from: ________________ to _______________

Commission File No. 000-29169

Generex Biotechnology _Corporation

(Exact name of registrant as specified in its charter)

| Delaware | 98-0178636 |

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification Number) |

10102 USA Today Way, Miramar, Florida 33025

(Address of principal executive office)

Registrant's telephone number: (416) 364-2551

| Title of each class | Trading Symbol | Name of each exchange on which traded |

| Common voting shares | GNBT | OTC |

Indicate by check mark if the registrant is a well known seasoned issuer, as defined in Rule 405 of the Securities Act:

☐ Yes ☒ NO

Indicate by check mark if the registrant not required to file reports pursuant to Section 13 or Section 15 (d) of the Act:

☐ Yes ☒ NO

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

☒ YES ☐ No

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

☒ YES ☐ No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act:

| Large accelerated filer ☐ | Accelerated filer ☐ |

| Non-accelerated filer ☐ | Smaller reporting company ☒ |

| Emerging Growth Company ☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13 (a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

☐ YES ☒ NO

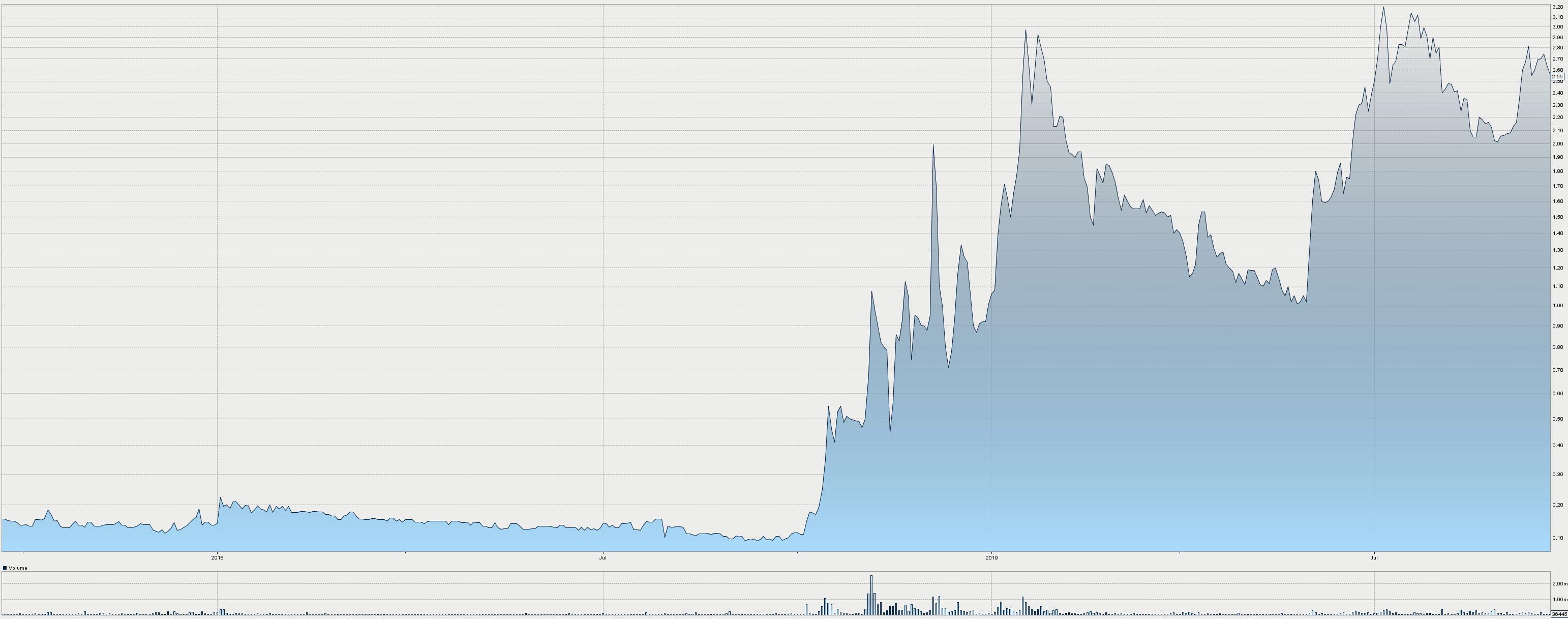

State the aggregate market value of the voting and non-voting common equity held by non-affiliates computed by reference to the price at which the common equity was last sold, or the average bid and asked price of such common equity, as of the last business day of the registrant’s most recently completed second fiscal quarter.

| Non Affiliate Float | Closing price as of Second Quarter January 31, 2019 | Market Capitalization |

| 22,543,206 | $2.13 | $48,017,029 |

Indicate the number of the number of shares outstanding of each of the registrant’s classes of common stock, as of the latest practicable date.

| As of Date | Outstanding |

| October 18, 2019 | 44,177,973 |

| 1 |

Table of Contents

| PART I | 4 |

| Item 1. Business. | 4 |

| Corporate History | 6 |

| Business Overview | 6 |

| Historical Business | 7 |

| Treatment of Legacy Assets | 7 |

| NuGenerex Therapeutics | 7 |

| NuGenerex Immuno-Oncology (NGIO, formerly Antigen Express) | 10 |

| NuGenerex Diagnostics (formerly Hema Diagnostic Systems LLC) | 12 |

| The “New” Generex & The NuGenerex Family of Subsidiary Companies | 14 |

| NuGenerex Regenerative Medicine | 16 |

| Regentys Corporation | 17 |

| NuGenerex Surgical Products | 20 |

| NuGenerex Health, LLC | 21 |

| NuGenerex Health HMO | 22 |

| Contemplated Product Positioning and Plan Design | 22 |

| GOVERNMENT REGULATION | 22 |

| MARKETING AND DISTRIBUTION | 30 |

| Manufacturing | 31 |

| RAW MATERIAL SUPPLIES | 33 |

| Intellectual Property | 34 |

| Competition | 37 |

| Environmental Compliance | 40 |

| Research and Development Expenditures | 40 |

| Employees | 40 |

| Item 1A. Risk Factors. | 41 |

| Item 1B. Unresolved Staff Comments. | 61 |

| Item 2. Properties. | 61 |

| Item 3. Legal Proceedings. | 62 |

| Item 4. Mine Safety Disclosures. | 63 |

| PART II | 64 |

| Item 5. Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities. | 64 |

| Market Information | 64 |

| Holders | 65 |

| Dividends | 65 |

| Equity Compensation Plan Information | 65 |

| Recent sales of unregistered securities; use of proceeds from registered securities | 65 |

| Purchases of equity securities by the issuer and affiliated purchasers. | 66 |

| Item 6. Selected Financial Data. | 66 |

| Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations. | 66 |

| Executive Summary | 66 |

| Financial Condition, Liquidity and Resources | 70 |

| Funding Requirements and Commitments | 74 |

| Off-Balance Sheet Arrangements | 77 |

| Tabular Disclosure of Contractual Obligations | 77 |

| Accounting for Research and Development Projects | 77 |

| Critical Accounting Policies | 78 |

| Item 7A. Quantitative and Qualitative Disclosures About Market Risk. | 78 |

| Item 8. Financial Statements and Supplementary Data. | 79 |

| Item 9. Changes in and Disagreements With Accountants on Accounting and Financial Disclosure. | 114 |

| Item 9A. Controls and Procedures. | 114 |

| Preliminary Note | 114 |

| Evaluation of Disclosure Controls and Procedures | 115 |

| Changes in Internal Control over Financial Reporting | 115 |

| MANAGEMENT’S REPORT ON INTERNAL CONTROL OVER FINANCIAL REPORTING | 115 |

| PART III | 117 |

| Item 10. Directors, Executive Officers and Corporate Governance. | 117 |

| Family Relationships | 117 |

| Involvement in Certain Legal Proceedings | 121 |

| Code of Ethics | 122 |

| Corporate Governance | 122 |

| Item 11. Executive Compensation. | 123 |

| Compensation, Discussion & Analysis | 123 |

| Summary Compensation Table | 126 |

| Outstanding Equity Awards at Fiscal Year-End | 127 |

| OUTSTANDING EQUITY AWARDS AT JULY 31, 2019 | 127 |

| Director Compensation | 127 |

| DIRECTOR COMPENSATION | 127 |

| Item 12. Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | 128 |

| Security Ownership of certain Beneficial Holders and Management | 128 |

| Item 13. Certain Relationships and Related Transactions, and Director Independence. | 129 |

| Item 14. Principal Accounting Fees and Services. | 130 |

| PART IV | 130 |

| Item 15. Exhibits, Financial Statement Schedules. | 130 |

| 2 |

As used herein, the terms the “Company,” “Generex,” “we,” “us,” or “our” refer to Generex Biotechnology Corporation, a Delaware corporation.

Forward-Looking Statements

Certain matters in this Annual Report on Form 10-K, including, without limitation, certain matters discussed under Item 7 - Management’s Discussion and Analysis of Financial Condition and Results of Operations, constitute “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. All statements, other than statements of historical facts, included in this Annual Report that address activities, events or developments that we expect or anticipate will or may occur in the future, including such matters as our projections, future capital expenditures, business strategy, competitive strengths, goals, expansion, market and industry developments and the growth of our businesses and operations, are forward-looking statements. These statements can be identified by introductory words such as "expects," “anticipates,” "plans," "intends," "believes," "will," "estimates," "projects" or words of similar meaning, and by the fact that they do not relate strictly to historical or current facts. Our forward-looking statements address, among other things:

| • | our expectations of future revenues, expenditures, capital or other funding requirements, |

| • | the adequacy of our cash and working capital to fund present and planned operations and growth, |

| • | the timing of our expansion plans, |

| • | our expectations concerning product candidates for our technologies; |

| • | our expectations concerning existing or potential development and license agreements for third-party collaborations and joint ventures; |

| • | our expectations of when different phases of clinical activity may commence and conclude; |

| • | the effect of governmental regulations generally, |

| • | our expectations of when regulatory submissions may be filed or when regulatory approvals may be received; and |

| • | our expectations of when commercial sales of our products may commence and when actual revenue from the product sales may be received. |

Any or all of our forward-looking statements may turn out to be wrong. They may be affected by inaccurate assumptions that we might make or by known or unknown risks and uncertainties. Actual outcomes and results may differ materially from what is expressed or implied in our forward-looking statements. Among the factors that could affect future results are:

| • | the inherent uncertainties of product development based on our new and as yet not fully proven technologies; |

| • | the risks and uncertainties regarding the actual effect on humans of seemingly safe and efficacious formulations and treatments when tested clinically; |

| • | the inherent uncertainties associated with clinical trials of product candidates; |

| • | the inherent uncertainties associated with the process of obtaining regulatory approval to market product candidates; |

| • | the inherent uncertainties associated with commercialization of products that have received regulatory approval; |

| • | economic and industry conditions generally and in our specific markets. |

| • | the volatility of, and decline in, our stock price; and |

| • | our current lack of financing for operations and our ability to obtain the necessary financing to fund our operations and effect our strategic development plan. |

Additional factors that could affect future results are set forth below under Item 1A. Risk Factors. We caution investors that the forward-looking statements contained in this Annual Report must be interpreted and understood in light of conditions and circumstances that exist as of the date of this Annual Report. We expressly disclaim any obligation or undertaking to update or revise forward-looking statements made in this Annual Report to reflect any changes in management's expectations resulting from future events or changes in the conditions or circumstances upon which such expectations are based.

| 3 |

PART I

Item 1. Business.

Corporate History

Generex Biotechnology Corporation (the “Company,” “Generex,” “we,” “us” or “our”) is based in Miramar, Florida, with offices in Dallas, Texas, Toronto, Canada and Wellesley, Massachusetts. The Company was originally incorporated in the state of Delaware on September 4, 1997, for the purpose of acquiring Generex Pharmaceuticals Inc., a Canadian (Province of Ontario) corporation formed in November 1995 to engage in pharmaceutical and biotechnological research and development and other activities. The Company’s acquisition of Generex Pharmaceuticals Inc. was completed in October 1997 in a transaction in which the holders of all outstanding shares of Generex Pharmaceuticals Inc. exchanged their shares for shares of Generex common stock.

In January 1998, Generex participated in a “reverse acquisition” with Green Mt. P.S., Inc, (“Green Mt.”), an inactive Idaho corporation formed in 1983. As a result of this transaction, the shareholders of Generex (the former shareholders of Generex Pharmaceuticals Inc.) acquired a majority (approximately 90%) of the outstanding capital stock of Green Mt., and Generex became a wholly-owned subsidiary of Green Mt.; Green Mt. changed its corporate name to Generex Biotechnology Corporation ("Generex Idaho"), and Generex changed its corporate name to GBC - Delaware, Inc. Because the reverse acquisition resulted in GBC - Delaware, Inc. shareholders (formally Generex shareholders) becoming the majority holders of Generex Idaho, GBC Delaware, Inc. was treated as the acquiring corporation in the transaction for accounting purposes. Thus, our, GBC - Delaware, Inc. (formally Generex), historical financial statements, which essentially represented the historical financial statements of Generex Pharmaceuticals Inc., were deemed to be the historical financial statements of Generex Idaho.

In April 1999, we completed a reorganization in which GBC - Delaware, Inc. merged with Generex Idaho. In this transaction, all outstanding shares of Generex Idaho were converted into shares of GBC - Delaware, Inc.; Generex Idaho ceased to exist as a separate entity, and we, GBC - Delaware, Inc., changed our corporate name back to "Generex Biotechnology Corporation." This reorganization did not result in any material change in our historical financial statements or current financial reporting.

Following our reorganization in 1999, Generex Pharmaceuticals Inc., which was incorporated in Ontario, Canada, remained as our wholly-owned subsidiary. All of our Canadian operations are performed by Generex Pharmaceuticals Inc.; Generex Pharmaceuticals Inc. is the 100% owner of 1097346 Ontario Inc., which was also incorporated in Ontario, Canada. In August 2003, we acquired Antigen Express, Inc. (“Antigen”), a Delaware incorporated company. Antigen is engaged in the research and development of technologies and immunomedicines for the treatment of malignant, infectious, autoimmune and allergic diseases. Antigen also does business under the name NuGenerex Immuno-Oncology. On February 28, 2019 Generex issued a dividend of Antigen to Generex shareholders in the amount of 1 share of Antigen for every 4 shares of Generex common stock. Generex still maintains majority control of Antigen.

We formed Generex (Bermuda), Inc., which is organized in Bermuda, in January 2001 in connection with a joint venture with Elan International Services, Ltd., a wholly-owned subsidiary of Elan Corporation, plc, (“Elan”) to pursue the application of certain of our and Elan's drug delivery technologies, including our platform technology for the buccal delivery of pharmaceutical products. In December 2004, we and Elan agreed to terminate the joint venture. Under the termination agreement, we retained all of our intellectual property rights and obtained full ownership of Generex (Bermuda), Inc.; Generex (Bermuda), Inc. does not currently conduct any business activities. We have additional subsidiaries incorporated in the U.S. and Canada which are dormant and do not carry on any business activities.

| 4 |

On January 18, 2017, we acquired a majority of the equity interests in Hema Diagnostic Systems, LLC (“HDS”). In December 2018, we acquired the remaining interest in HDS. The company, now a wholly-owned subsidiary of Generex, has been renamed NuGenerex Diagnostics, LLC (NGDx), and is managed by President Harold Haines, PhD.

On October 3, 2018, our wholly owned subsidiary, NuGenerex Distribution Solutions, LLC (“NuGenerex”), entered into an asset purchase agreement (the “Veneto Asset Purchase Agreement”) with Veneto Holdings, L.L.C. (“Veneto”), pursuant to which NuGenerex purchased certain assets of Veneto and its subsidiaries (the “Assets”). The Veneto Asset Purchase Agreement contains provisions regarding payment terms, confidentiality and indemnification, as well as other customary provisions.

Effective as at October 3, 2018, NuGenerex assigned the Veneto Asset Purchase Agreement to NuGenerex Distribution Solutions 2, LLC. The sole member of NuGenerex Distribution Solutions 2, LLC is NuGenerex Management Services, Inc., a wholly-owned subsidiary of Generex Biotechnology Corporation.

On October 3, 2018, we acquired certain assets from Veneto (the “First Closing Assets”), primarily consisting of the operating assets of (a) system dispensing pharmacies, (b) a central adjudicating pharmacy, (c) a wholesale pharmaceutical purchasing company, and (d) an in-network laboratory.

On November 1, 2018, we consummated the acquisition of Veneto assets (the “Second Closing Assets”), consisting primarily of Veneto’s management services organization business and other assets. The aggregate price for the First Closing Assets and the Second Closing Assets was $30,000,000. We issued a promissory note in the principal amount of $35,000,000 (the “New Note”) consisting of the $30,000,000 purchase price and a $5,000,000 original issue discount, as the sole consideration payable on the Second Closing Date. On January 15, 2019, the parties entered into an amendment to the Asset Purchase Agreement (the “Amendment”) restructuring payment of the New Note.

On March 28, 2019, the Company entered into an amendment, a “Restructuring Agreement” with Veneto and the equity owners of Veneto to restructure the payment of the New Note that provided, in lieu of any cash payments, the Company delivered on May 23, 2019 8,400,000 shares of our common stock; plus an aggregate 5,500,000 shares of the common stock of our subsidiary, Antigen. The Veneto assets acquired by Generex included management services operations, systems, facilities, and other services.

On January 7, 2019, we acquired a majority interest in Regentys Corporation (“Regentys”) for an aggregate of $15,000,000, among which $400,000 was paid in cash and the remainder was paid by the issuance of a promissory note with a fair value of $14,342,414 for a total net purchase price of $14,742,414. The total fair value of the assets acquired totaled $907,883 and goodwill of $13,834,581. Installments payable under the note were tied to specific business development objectives and dates. As of October 26, 2019, an additional $850,000 was paid for a total of $1,250,000 against the note. Regentys is developing a non-surgical treatment for inflammatory bowel diseases such as ulcerative colitis and Crohn’s disease.

On January 7, 2019, we acquired a majority interest in Olaregen Therapeutix Inc. (“Olaregen”) for an aggregate of $12,000,000, among which $400,000 was paid in cash and the remainder was paid by the issuance of a promissory note with a fair value of $11,472,334 for a total net purchase price of $11,872,663. The total fair value of the assets acquired totaled $2,461,439 and goodwill of $9,411,224. $1,291,500 principal was paid against the note as of July 31, 2019 and an additional $500,000 was paid subsequently for a total aggregate of $1,791,500 of principal payments in addition to the $400,000 initial payment. Olaregen is launching an FDA-510(k) cleared wound care product.

On May 10, 2019, we acquired from a third party the outstanding Series A Preferred Stock in Olaregen in exchange for 4 million shares of the Company’s common stock, plus the issuance of a $2 million promissory note increasing our interest in Olaregen to approximately 62% of the Olaregen’s outstanding voting shares.

| 5 |

Business Overview

Our management team has embarked upon a complete strategic reorganization and transformation of the entire corporate structure, leveraging our legacy assets which have applied over $400 million dollars in developmental activities over the years, providing the Company with net operating loss (“NOL”) carryforwards from both United States and Canadian sources. As of July 31, 2019, the Company has significant NOL carryforwards that are described in detail in the Notes to our Financial Statements included in this 10-K. We have also formulated an acquisition strategy and identified targets to build a specialized healthcare platform with both scalability and the ability to leverage across the organization in an effort to achieve higher profit margins.

Since the new management team has taken over in January 2017, Generex has been reorganized as a strategic, diversified life science holding company that is actively involved in building a modern organizational platform for the financing, development, commercialization, and distribution of promising devices, biologics, therapeutic, and diagnostic products to improve human health and return value to its investors. As the foundation for the reorganization, we are acquiring operating companies that provide multiple and significant revenue streams through delivery of patient-focused healthcare products and services, including specialty pharmacy, orthopedic implants, surgical supplies, biologics, medical devices, and regenerative medicines. These foundational acquisitions service unique market channels that provide end-to-end healthcare solutions in partnerships with patients, physicians, health systems, and payors. The synergistic business models of the combined organization offer cross channel sales opportunities for rapid growth, with significant revenues and profits projected going forward.

Details of the Generex business strategy are provided following the discussion of the Generex historical business and our legacy assets.

Historical Business

Historically, we have been a research and development company focused on the commercialization of Oral-lyn buccal insulin spray for diabetes. Additionally, through our wholly-owned subsidiary Antigen Express, we have a deep intellectual property portfolio of immunotherapy assets relating to the “Ii-Key” technology that activates the immune response for the treatment of cancer and infectious diseases. We have completed a Phase IIb clinical trial of AE37 immunotherapeutic peptide vaccine with the Ii-Key technology in over 300 women with breast cancer.

In 2017, we acquired HDS (now NuGenerex Diagnostics) and their diagnostic product portfolio of rapid point-of-care EXPRESS test kits and cassettes for infectious disease testing.

We believe that these legacy diagnostics, diabetes and cancer assets are may have significant value which is not being recognized due to missteps in the clinical development process by previous management, resulting inability to raise capital necessary to fund further development. We think the products and IP portfolio retain significant value. A recently signed co-development deal with a major pharmaceutical company for AE37 in triple negative breast cancer, and a licensing deal in China for AE37 in prostate cancer illustrate the potential for AE37 immunotherapeutic vaccine. Additionally, Oral-lyn has been reformulated to enter clinical trials for Type II diabetes. The HDS EXPRESS diagnostic technology has been expanded with the new, patent-pending EXPRESS II technology and a new product pipeline. We filled our first international commercial order for 40,000 units of its NGDx -Malaria PF/PV Cassette Test Kit to Imres, BV, a Netherlands-based medical distribution company, and was recently granted a CE Mark Certification under the European Medical Devices Directive (MDD) for its The Express II Syphilis Treponemal Assay, a rapid point-of-care diagnostic assay for the detection of syphilis antibodies in primary and secondary syphilis. As part of the reorganization plan, we placed our legacy assets into separate subsidiaries under the NuGenerex family of companies, including NuGenerex Diagnostics, Nugenerex Immuno-Oncology (Antigen Express), and NuGenerex Therapeutics (Oral-Lyn and RapidMist buccal delivery technology). Our strategy is to spin out NuGenerex Immuno-Oncology as a separately traded public company, to reignite the Oral-Lyn development program with a reformulated buccal insulin spray, and to build out the diagnostics business, as detailed in the following paragraphs, however there are no assurances that we will be able to accomplish our strategic objectives.

| 6 |

Treatment of Legacy Assets

Generex and its subsidiary companies have extensive patent portfolios, with intellectual property for composition of matter, formulation, design, and use in a number of therapeutic areas, across multiple indications. As described, we plan to build our legacy assets with the ultimate goal to spin-out such assets at the appropriate time, which have been incorporated into NuGenerex subsidiary companies in an effort to unlock the potential unrealized value of the intellectual property and commercial opportunities for these development companies in major markets for immuno-oncology, diabetes, and infectious disease testing:

- NuGenerex Therapeutics: Oral-lyn (Buccal Insulin) and RaidMist Buccal delivery technology

- NuGenerex Immuno-Oncology: Phase II AE37 + Keytruda in TNBC; Antigen Express (Ii-Key), Licensing, Partnerships, investor dividend paid (1:4) for spin-out

- NuGenerex Diagnostics: NGDx Express II rapid diagnostic tests for infectious disease

NuGenerex Therapeutics

NuGenerex Therapeutics houses the legacy diabetes assets, Oral-Lyn and RapidMist buccal delivery technology. We believe that our buccal delivery technology is a platform technology that has application to many large molecule drugs and designed to provide a convenient, non-invasive, accurate and cost-effective way to administer such drugs. We have identified several large molecule drugs as possible candidates for development, including cannabinoid medicines. To that end we have entered into a licensing agreement with Scientus Pharmaceuticals for the use of the RapidMist technology for the administration of cannabinoids.

Buccal Delivery Technology and Products

Our buccal delivery technology involves the preparation of proprietary formulations in which an active pharmaceutical agent is placed in a solution with a combination of absorption enhancers and other excipients classified “generally recognized as safe” ("GRAS") by the U.S. Food and Drug Administration (“FDA”) when used in accordance with specified quantities and other limitations. The resulting formulations are aerosolized with a pharmaceutical grade chemical propellant and are administered to patients using our proprietary RapidMist™ brand metered dose inhaler. The device is a small, lightweight, hand-held, easy-to-use aerosol applicator comprised of a container for the formulation, a metered dose valve, an actuator and dust cap. Using the device, patients self-administer the formulations by spraying them into the mouth. The device contains multiple applications, the number being dependent, among other things, on the concentration of the formulation. Absorption of the pharmaceutical agent occurs in the buccal cavity, principally through the inner cheek walls. In clinical studies of our flagship oral insulin product Generex Oral-lyn™, insulin absorption in the buccal cavity has been shown to be efficacious and safe.

Buccal Insulin Product – Generex Oral-Lyn™

Insulin is a hormone that is naturally secreted by the pancreas to regulate the level of glucose, a type of sugar, in the bloodstream. The term “diabetes” refers to a group of disorders that are characterized by the inability of the body to properly regulate blood glucose levels. When glucose is abundant, it is converted into fat and stored for use when food is not available. When glucose is not available from food, these facts are broken down into free fatty acids that stimulate glucose production. Insulin acts by stimulating the use of glucose as fuel and by inhibiting the production of glucose. In a healthy individual, a balance is maintained between insulin secretion and glucose metabolism.

| 7 |

According to the Centers for Disease Control (CDC), there are two major types of diabetes. Type 1 diabetes (juvenile onset diabetes or insulin dependent diabetes) refers to the condition where the pancreas produces little or no insulin. Type 1 diabetes accounts for 5-10 percent of diabetes cases (CDC). It often occurs in children and young adults. Type 1 diabetics must take daily insulin injections, typically three to five times per day, to regulate blood glucose levels. Generex Oral-lyn™ provides a needle-free means of delivering insulin for these patients.

According to the American Diabetes Association, in Type 2 diabetes (adult onset or non-insulin dependent diabetes mellitus), the body does not produce enough insulin, or cannot properly use the insulin produced. Type 2 diabetes is the most common form of the disease and accounts for 90-95 percent of diabetes cases, according to the American Diabetes Association. In addition to insulin therapy, Type 2 diabetics may take oral drugs that stimulate the production of insulin by the pancreas or that help the body to more effectively use insulin. Generex Oral-lyn™ provides a simple means of delivering needed insulin to this major cohort of individuals.

Studies in diabetes have identified a condition closely related to and preceding diabetes, called impaired glucose tolerance (IGT). People with IGT do not usually meet the criteria for the diagnosis of diabetes mellitus. They have normal fasting glucose levels but two hours after a meal their blood glucose level is far above normal. With the increase use of glucose tolerance tests the number of people diagnosed with this pre-diabetic condition is expanding exponentially. Per the 2017 Diabetes Atlas Update, published by the International Diabetes Federation (IDF), approximately 40 million people in the United States and more than 425 million people world-wide suffer from IGT. Generex Oral-lyn™ is an ideal solution to providing meal-time insulin to the millions of IGT sufferers. This therapeutic area is currently being investigated.

There is no known cure for diabetes. The IDF estimates that there are currently approximately 382 million diabetics worldwide per their 2017 Diabetes Atlas Update and is expected to affect over 592 million people by the year 2035. There are estimated to be over 37 million people suffering from diabetes in North America alone and diabetes is the second largest cause of death by disease in North America.

A substantial number of large molecule drugs (i.e., drugs composed of molecules with a high molecular weight and fairly complex and large spatial orientation) have been approved for sale in the United States or are presently undergoing clinical trials as part of the process to obtain such approval, including various proteins, peptides, monoclonal antibodies, hormones and vaccines. Unlike small molecule drugs, which generally can be administered by various methods, large molecule drugs historically have been administered predominately by injection. The principal reasons for this have been the vulnerability of large molecule drugs to digestion and the relatively large size of the molecule itself, which makes absorption into the blood stream through the skin inefficient or ineffective. The RapidMist technology provides a recognized and proven drug delivery system for the delivery of large molecules directly into the blood stream with the attendant advantages.

Oral-lyn History

In May 2005, we received approval from the Ecuadorian Ministry of Public Health for the commercial marketing and sale of Generex Oral-lyn™ for treatment of Type 1 and Type 2 diabetes. We have successfully completed the delivery and installation of a turnkey Generex Oral-lyn™ production operation at the facilities of PharmaBrand in Quito, Ecuador. The first commercial production run of Generex Oral-lyn™ in Ecuador was completed in May 2006. While Ecuador production capability may be sufficient to meet the needs of South America, it is believed to be insufficient for worldwide production for future commercial sales and clinical trials.

On the basis of the test results in Ecuador and other pre-clinical data, we made an Investigational New Drug (“IND”) submission to Health Canada (Canada's equivalent to the FDA) in July 1998, and received permission from the Canadian regulators to proceed with clinical trials in September 1998. We filed an IND application with the FDA in October 1998, and received FDA approval to proceed with human trials in November 1998.

| 8 |

We began our clinical trial programs in Canada and the United States in January 1999. Between January 1999 and September 2000, we conducted clinical trials of our insulin formulation involving approximately 200 subjects with Type 1 and Type 2 diabetes and healthy volunteers. The study protocols in most trials involved administration of two different doses of our insulin formulation following either a liquid Sustacal meal or a standard meal challenge. The objective of these studies was to evaluate our insulin formulation's efficacy in controlling post-prandial (meal related) glucose levels. These trials demonstrated that our insulin formulation controlled post-prandial hyperglycemia in a manner comparable to injected insulin. In April 2003, a Phase II-B clinical trial protocol was approved in Canada. In September 2006, a Clinical Trial Application relating to our Generex Oral-lyn™ protocol for late-stage trials was approved by Health Canada. The FDA’s review period for the protocol lapsed without objection in July 2007.

In late April 2008, we initiated Phase III clinical trials in North America for Generex Oral-lyn™ with the first subject screening in Texas. Other clinical sites participating in the study were located in the United States (Texas, Maryland, Minnesota and California), Canada (Alberta), European Union (Romania, Poland and Bulgaria), Eastern Europe (Russia and Ukraine),) and Ecuador. Approximately 450 subjects were enrolled in the program at approximately 70 clinical sites around the world. The Phase III protocol called for a six-month trial with a six-month follow-up with the primary objective to compare the efficacy of Generex Oral-lyn™ and the RapidMist™ Diabetes Management System with that of standard regular injectable human insulin therapy as measured by HbA1c, in patients with Type-1 diabetes mellitus. The final subjects completed the trial in August 2011. After appropriate validation, the data from approximately 450 patients was tabulated, reviewed and analyzed. Those results from the Phase III trial along with a comprehensive review and supplemental analyses of approximately 40 prior Oral-lyn clinical studies were compiled and submitted to the FDA in late December 2011 in a comprehensive package including a composite metanalysis of all safety data. We do not currently plan to expend significant resources on additional clinical trials of Oral-lyn™ until after such time that we secure additional financing. However, we have undertaken a formulation enhancement project with the University Health Network at the University of Toronto and the University of Guelph, Ontario to increase the amount of insulin reaching the blood stream. We believe that the preliminary results from an animal study are encouraging,

In the past, we engaged a global clinical research organization to provide many study related site services, including initiation, communication with sites, project management and documentation; a global central lab service company to arrange for the logistics of kits and blood samples shipment and testing; an Internet-based clinical electronic data management company to assist us with global data entry, project management and data storage/processing of the Phase III clinical trial and regulatory processes. In the past, we have contracted with third-party manufacturers to produce sufficient quantities of the RapidMist™ components, the insulin, and the raw material excipients required for the production of clinical trial batches of Generex Oral-lyn™.

Future Plans

We have reformulated the original Oral-Lyn buccal insulin as a new patentable Oral-Lyn 2 that requires only 2 - 3 pre-prandial (before meal) sprays for the treatment of Type II diabetes. The reformulated Oral-lyn 2 was made possible by new techniques in protein chemistry and pharmaceutical formulation science, that with minimal changes in the production process and content of the components, allow the development of a new and improved, concentrated insulin formulation for improved diabetes management.

NuGenerex has engaged the University of Toronto’s Center for Molecular Design and Pre-formulations (CMDP) through the University Health Network with the goal of enhancing the Oral-lyn™ 2 formulation to make it more attractive to patients and prospective commercialization partners by increasing the bioavailability of insulin in the product and reducing the number of sprays required to achieve effective prandial metabolic control for patients with diabetes. Under the supervision of NuGenerex consultant Dr. Lakshmi P. Kotra, B.Pharm. (Hons), Ph.D., of CMDP, preliminary efforts succeeded in increasing the insulin concentration in the product by approximately 400 - 500% as confirmed by a variety of in vitro testing procedures, while preserving the solubility, stability, biologic activity, and potency of the insulin in the formulation.

NuGenerex subsequently entered into a Research Services Agreement with the University of Guelph pursuant to which Dr. Dana Allen, DVM, MSc. and Dr. Ron Johnson, DVM, Ph.D. of the Ontario Veterinary College of the University of Guelph conducted a study of the relative bioavailability of the enhanced formulation in dogs in the University’s Comparative Clinical Research Facility. The University had previously conducted the studies of the original formulation of Generex Oral-lyn™ for proof of concept, safety, and toxicity.

| 9 |

In the new studies, the enhanced NuGenerex Oral-lyn™ 2 formulation was compared with the original formulation in a blinded, parallel controlled study involving fasted, awake, healthy mature beagle dogs. Each dog received three sprays of either the enhanced formulation or the original formulation. Each dog was observed with assessments of serum insulin and glucose measured over a two-hour period. There were no adverse events observed in any of the animals.

In the dogs given the enhanced Generex Oral-lyn™ formulation (5X), there was a greater than 20-fold increase in serum insulin at 15 minutes (excluding one dog who had little response at any time point; (with dog included it was greater than 5-fold)) and almost 500% greater absorption of insulin over the two-hour test period compared to dogs given the original formulation (1X). There was a 33% decrease in serum glucose at 30 minutes in dogs treated with the enhanced Generex Oral-lyn™ formulation, compared to a 12% increase in serum glucose in dogs treated with the original formulation.

The results of the dog studies coupled with the positive findings from the in vitro work provide support and confidence to move forward with the remaining clinical and regulatory work necessary to achieve FDA approval of the enhanced NuGenerex Oral-lyn™ formulation through a 505(b)2 NDA.

The combined results provide evidence that the enhanced NuGenerex Oral-lyn™ 2 will be able to be used by people with either type 1 or type 2 diabetes mellitus as a safe, simple, fast, flexible, and effective alternative to pre-prandial insulin injections with dosing of only two to four sprays required before meals.

The Oral-lyn Safety Database contains information on 1,496 subjects. Eight hundred sixty-nine (869) subjects were exposed to Oral-lyn, while 627 served as Control subjects and were exposed to commercially available oral antihyperglycemics, injected insulin, or Oral-lyn placebo. There were 695 subjects in pK/pD studies (368, Oral-lyn; 327, Control) and 801 subjects in efficacy trials (501, Oral-lyn; 300, Control).

Two hundred seventy-two (272) Oral-lyn subjects reported at least one adverse event (132 in pK/pD studies; 140 in efficacy studies) while 278 Control subjects reported at least one adverse event (111 in pK/pD studies; 167 in efficacy studies). With respect to adverse events by Maximum Severity there appeared to be no significant differences between Oral-lyn and the Control groups in either the Efficacy or the pK studies.

In summary, there appear to be no indications of any significant unexpected adverse events. The expected events of hypoesthesia oral, throat irritation, dry throat, and cough were for the most part mild and could be consistent with the Oral-lyn therapy especially during the learning phase of administration. There was an indication of overlap of some of these events with multiple event terms in the constellation of upper respiratory tract infection that appeared to be balanced across therapy groups.

Our strategy is to revitalize our diabetes program by advancing the reformulated buccal spray Oral-lyn 2 for the treatment of Type II diabetes, and to integrate Oral-Lyn 2 therapy into our end-to-end solution for disease management through our MSO model.

Beyond Oral-lyn 2 for Type II diabetes, NuGenerex Drug Delivery Solutions will advance the RapidMist buccal delivery technology with additional small and large molecule drugs which will benefit from an alternative route of administration.

NuGenerex Immuno-Oncology (NGIO, formerly Antigen Express)

NuGenerex Immuno-Oncology is developing immunotherapeutic products and vaccines based on our proprietary, patented platform technology, Ii-Key. The Ii-Key is a peptide derived from the major histocompatibility complex (MHC) Class II associated invariant chain (Ii) that regulates the formation, trafficking, and antigen-presenting functions of MHC class II complexes, essential for the activation of T cells in the immune response. T cells recognize antigenic epitopes when they are 'presented' to them by specific molecules, termed (MHC) on the surface of infected or malignant cells. This interaction activates the T cells, stimulating a multicellular cascade of actions that eliminates the diseased cell and protects against future disease recurrence.

| 10 |

When the Ii-Key peptide is linked to an antigenic epitope, it can bind to MHC Class II molecules, displacing resident antigens from the antigen binding groove, essentially 'hijacking' the MHC class II complex to present the Ii-Key epitope to selectively activate T-Cell Th1 responses, thereby increasing the intensity and duration of the immune response.

NuGenerex Immuno-Oncology has developed a number of Ii-Key Hybrid peptides for the immunotherapeutic targeting of tumor associated antigens (TAAs) in cancer and for vaccines against infectious diseases.

Ii-Key hybrid peptides can also be used to selectively activate Th2 responses and thereby induce tolerance to antigens involved in harmful immune reactions, e.g. autoimmunity, allergy, and transplant rejection.

AE37 – Ii-Key/HER2/neu Hybrid Immunotherapeutic Vaccine

Our most advanced immunotherapy vaccine is AE37, an Ii-Key-Hybrid molecule that contains the HER2/neu antigenic peptide linked to the Ii-Key to enhance immune stimulation against HER2, which is expressed in numerous cancers, including breast, prostate, and bladder cancers. We have completed a Phase I clinical trial of AE37 in breast cancer: A phase Ib safety and immunology study of AE37 and GM-CSF in 16 breast cancer patients who had completed all first-line therapies and who were disease-free at the time of enrollment to the study (Holmes et al. Results of the first phase I clinical trial of the novel Ii-Key hybrid preventive HER-2/neu peptide (AE37) vaccine. J Clin Oncol 2008;26:3426-33). Furthermore, we completed a Phase IIb trial of AE37 in the prevention of cancer recurrence in women who were at high risk of recurrence after undergoing successful primary standard of care breast cancer therapies and were disease free at time of enrollment. Though the study enrolled 300 subjects, the results were not statistically significant due to a complete lack of recurrence in the 160 women with HER2-3+ positive tumors who were treated with Herceptin during primary therapy. Though the trial was not powered to evaluate the prevention of recurrence in subgroups, the trial indicated efficacy in the subset of patients diagnosed with HER2 1+, 2+, and triple negative breast cancer.

Based on the results from this trial, NuGenerex has entered into a collaborative agreement with Merck Sharpe & Dohme B.V. (Merck) and the National Surgical Adjuvant Breast and Prostate Program (NSABP) to conduct a Phase II trial to evaluate the safety and efficacy of AE37 in combination with the anti-PD-1 therapy, KEYTRUDA (pembrolizumab) in patients with metastatic triple-negative breast cancer. The trial is scheduled to begin enrolling patients in the second quarter of 2019.

In addition to the breast cancer program, NuGenerex has conducted a Phase I clinical trial in prostate cancer, enrolling thirty-two HER-2/neu+, castrate-sensitive, and castrate-resistant prostate cancer patients to demonstrate safety and strong immunological response to AE37. We are advancing AE37 for the treatment of prostate cancer through a licensing and research agreement with Shenzhen BioScien Pharmaceuticals Co., Ltd., for which NuGenerex has received a $700,000 upfront payment, with additional future milestone and royalty payments.

In exchange for exclusive rights to AE37 for prostate cancer in China, Shenzen is financing and conducting the Phase II trials in the European Union and Phase III trials globally under International Commission on Harmonisation (“ICH”) guidelines, with NuGenerex retaining the rights to all clinical data for regulatory submissions and commercialization in the rest of the world outside China.

Future Plans

NuGenerex Immuno-Oncology has been established to not only to advance the NuGenerex Immuno-Oncology core technology, but also to expand our portfolio in the field of immunotherapy and personalized medicine through partnerships and acquisitions. As part of our strategy, we are planning to spin-out NuGenerex Immuno-Oncology as a separate, publicly traded entity to unlock the true value of the Ii-Key technology for our stockholders as it creates a pure play in immunotherapy, which will foster investment and collaboration.

| 11 |

As an initial step in accomplishing the spin-out of NGIO, on February 25, 2019, we issued a stock dividend to our shareholders, whereby our shareholders received 1 share of NGIO for every 4 shares of our stock held on the dividend date. The stock dividends will enable our stockholders to directly participate in the potentially promising future of NGIO, while creating a large shareholder base with the potential for substantial liquidity immediately upon spin-out to a national exchange, which will provide NGIO with ready access to the capital markets to finance its on-going clinical and regulatory initiatives.

Additionally, we are in discussions with multiple academic institutions and biotechnology development companies to acquire products and technologies to augment the NGIO development pipeline and product portfolio.

We plan to finalize our corporate acquisition strategy and to initiate the spin-out process for NGIO in the second quarter of 2020.

NuGenerex Diagnostics (formerly Hema Diagnostic Systems LLC)

Our wholly-owned subsidiary, NuGenerex Diagnostics (formerly Hema Diagnostic Systems LLC or HDS) is in the business of developing, manufacturing, and distributing rapid point-of-care in-vitro medical diagnostics for infectious diseases. These are commonly referred as rapid diagnostic tests (“RDTs”). We manufacture and sell RDTs based upon our own proprietary EXPRESS platforms as well as standard “cassette” devices.

Since its founding, NuGenerex Diagnostics has been developing and continues to develop an expanding line of RDTs for infectious disease diagnosis. These include products for human immunodeficiency virus (HIV), tuberculosis, malaria, hepatitis B, hepatitis C, syphilis, and others. These assays are all qualitative in nature and provide a simple positive or negative result directly at the clinical site. They can be used for definitive diagnosis, triage or in combination with other assays depending on which disease is being considered.

Each device incorporates a test strip containing reagent lines (stripes) that have been impregnated with specific antigens or antibodies that detect the target molecules specific to an infectious disease. The test strips are incorporated into our proprietary EXPRESS platforms which are easy-to-use and user-friendly diagnostic devices. There are two EXPRESS platforms; the EXPRESS and the EXPRESS II. The EXPRESS II is an upgraded version of the original EXPRESS and its use involves fewer operator steps, making it of higher clinical utility value. The Express II platform is designed to be used in a broad range of clinical and laboratory medical settings and for direct use by consumers in the home. It is simple to use, with fewer steps of operation than other rapid point-of-care tests. A single drop of blood taken by a simple finger stick is added directly to the device and the assay is activated by placing a pod of buffer solution onto the device. Results can be read in as early as 5 minutes, and no longer than 30 minutes. The accuracy of the Express II Syphilis Treponemal Assay is equal to or better than standard laboratory assays for syphilis antibodies with sensitivities and specificities of over 99%.

We believe that each system delivers its own advantages which enhance the use, application and performance of each diagnostic. This ease of use in the EXPRESS delivery systems is designed to ensure that our RDTs perform efficiently and effectively providing the most accurate and repeatable test results available while, at the same time, minimizing the transference of a potentially infected blood sample. The EXPRESS and cassette diagnostic kits for infectious disease testing are designed for use in resource-poor countries throughout the world, especially in sub-Saharan Africa, where the World Health Organization coordinates population screening for infectious diseases. We recently filled our first international commercial order for 40,000 units of its NGDx -Malaria PF/PV Cassette Test Kit to Imres, BV, a Netherlands-based medical distribution company.

NuGenerex Diagnostics was recently granted a CE Mark Certification under the European Medical Devices Directive (MDD) for its The Express II Syphilis Treponemal Assay, a rapid point-of-care diagnostic assay for the detection of syphilis antibodies in primary and secondary syphilis. The assay is based upon NuGenerex Diagnostic’s innovative patent pending point-of-care diagnostic platform, the Express II. The accuracy of the Express II Syphilis Treponemal Assay is equal to or better than standard laboratory assays for syphilis antibodies with sensitivities and specificities of over 99%.

| 12 |

With the receipt of the CE Mark Certification for its rapid point-of-care Express II Syphilis Treponemal Assay, we believe NuGenerex Diagnostics is well situated to enter into this growing syphilis testing market and will now pursue marketing efforts in Europe and, in parallel, begin plans for the filing of a 510k application with the United States FDA for marketing clearance in the United States. To this end, NuGenerex Diagnostics is fully qualified as a diagnostic test developer and manufacturer under FDA Good Manufacturing Procedures (GMP) and is certified by the International Standards Organization for the manufacture of medical devices under ISO 13485-2016 regulations.

NuGenerex Diagnostics has just begun a new initiative which revolves around the development of quantitative rapid diagnostic assays. These assays allow laboratory personnel and clinicians to assess the absolute amount of specific target molecules in blood or serum samples as opposed to “yes” or “no” results of qualitative RDTs. The first assay to be developed is a multiplex biomarker test for the diagnosis of sepsis and the potential differentiation of infectious sepsis from systemic immune response syndrome (SIRS).

We maintain an FDA registered facility in Miramar, Florida and are certified under both ISO9001 and ISO13485 for the Design, Development, Production and Distribution of the in-vitro devices. Approval of our HIV rapid test has been issued by the United States Agency for International Development (USAID). Additionally, some of our products qualified for and carry the European Union “CE” Mark, which allows us to enter into CE Member countries subject to individual country requirements. Currently, we have two malaria rapid tests approved under World Health Organization (WHO) guidelines. This process allows expedited approval of rapid tests, reducing the current 24 -30-month process down to approximately 6-9 months. WHO approval is necessary for our products to be used in those countries which rely upon the expertise of the WHO, as well as for non-governmental organizations (“NGO”) funding for the purchase of diagnostic products.

We maintain current U.S. Certificates of Exportability that are issued by two FDA divisions-CBER and CDRH. CBER (Center for Biologicals Evaluation and Research) is the FDA regulatory division that oversees infectious disease diagnostic devices, including our HIV, Hepatitis B and Hepatitis C EXPRESS and EXPRESS II kits. The other division, Center for Devices and Radiological Health (CDRH), is responsible for the oversight of other HDS devices which include Tuberculosis, Syphilis, and the remaining product line. Our HDS facility maintains FDA Establishment Registration status and is in accord with GMP (Good Manufacturing Practice) as confirmed by the FDA.

We do not currently have FDA clearance to sell our products in the United States. We intend to submit selected devices to the FDA under a Pre-Market Approval Application (PMA) or through the 510K process. The 510K would require the appropriate regulatory administrative submissions as well as a limited scientific review by the FDA to determine completeness (acceptance and filing reviews); in-depth scientific, regulatory, and Quality System review by appropriate FDA personnel (substantive review); review and recommendation by the appropriate advisory committee (panel review); and final deliberations, documentation, and notification of the FDA decision. The PMA process is more extensive, requiring clinical trials to support the application. We expect to apply to the FDA for clearance of our first RDT (Express II Syphilis Treponemal Assay) for FDA 510K approval in early 2020. We anticipate the FDA process will be completed within 9 months after submission. During this timeline, we will be preparing documentation for additional rapid tests to undergo either the FDA PMA or 510k process.

Future Plans

Generex plans to use the NuGenerex Diagnostics subsidiary to build a multi-faceted diagnostics business focused on personalized medicine. To that end, we are exploring opportunities in multiplex assays for point-of-care infectious disease testing, pharmacogenomic testing for medication management, and biomarker analysis for personalized cancer treatment, including immunotherapy.

| 13 |

The “New” Generex & The NuGenerex Family of Subsidiary Companies

Through reorganization and acquisition, we are building the family of NuGenerex subsidiary companies to provide end-to-end solutions for physicians and patients. To that end, our subsidiary NuGenerex Distribution Solutions (NDS) has established a network of physicians, ancillary service providers, and patients through a Management Services Organization (MSO). As the MSO network currently consists of orthopedic surgeons and podiatrists, we have acquired and/or have agreements to acquire a number of revenue-generating companies that manufacture, market and distribute surgical and wound healing products. The acquisitions include Olaregen Therapeutix, a regenerative medicine company that has recently launched Excellagen wound conforming gel, which is FDA-cleared for the management of 17 wound healing indications, and Regentys, a clinical-stage development company with regenerative medicine technology for the treatment of inflammatory bowel diseases; Pantheon Medical, a manufacturer of patented, FDA-cleared foot & ankle kits with surgical plates, screws, and tools; and MediSource Partners, a licensed distributor of surgical supplies, orthopedic implants, and biologics, including human placental derived tissue products for regenerative medicine applications. Additionally, NDS will be launching a new software as a service (SaaS) business called DME-IQ that enables orthopedic surgeons to manage in-house programs for orthopedic durable medical equipment, including inventory controls, insurance adjudication, and patient billing. Together, under the banner of these subsidiary companies offer a range of products and services to meet the needs of our proprietary distribution channels. Cross selling of products and services will enhance the revenue opportunities for the entire family of NuGenerex subsidiaries.

Our corporate mission is to provide end-to-end solutions for physicians and patients through geographic expansion of our MSO model, diversification of management services offerings, the establishment of an HMO in partnership with Dr. Kiran Patel, and the proposed acquisition of an Accountable Care Organization for complex care.

The NuGenerex family of subsidiary companies offer a broad range of products and services to meet the needs of physicians and patients, including:

| • | NuGenerex Distribution Solutions: MSO, Ancillary Services, , DME-IQ, and Surgical Products. |

| • | NuGenerex Regenerative Medicine: Olaregen Therapeutix, Regentys. |

| • | NuGenerex Surgical Products: Pantheon Medical – Foot & Ankle, LLC and MediSource Partners, LLC. |

| • | NuGenerex Health: MSO/HMO with Dr. Kiran Patel: Ancillary health management services for chronic conditions – 65,000 + Patient population with Diabetes; Ophthalmology, Podiatry, Chronic Care Management (CCM). |

Services and Products

NuGenerex Distribution Solutions

Generex Biotechnology established NuGenerex Distribution Solutions (NDS) in 2018 as the foundational piece in the transformation of the Company into an integrated healthcare holding company that provides end-to-end solutions for physicians and patients. Part of the NDS model includes a physician-owned MSO which is positioned to procure our new products and services as made available. NDS will also continue to provide inventory selection and management, as well as management services for legal and regulatory compliance, accounting, HR, IT and customer support services through the MSO networks.

We serve as the General Partner of the MSO which is 99% owned by over 50 entities. The entities included orthopedic and podiatric surgery centers with over 100 Physicians in 5 states and this MSO structure creates the foundation of our future alternative distribution channel with an open sales channel for products and services. The company plans to expand its geographic footprint nationally where appropriate.

| 14 |

NuGenerex Distribution Solutions Corporate Mission NDS benefits the medical community by providing cost effective ancillary services that ultimately deliver better outcomes and enhance the doctor-patient relationship. NDS will make available numerous best of class products and services using a patient centric approach that enables ancillary service providers, physicians, and patients to better coordinate healthcare services from diagnosis through treatment and follow-up.

NDS Expansion

The NuGenerex MSO network has operated in five states and is configuring a roll out which will be compliant and take costs out of healthcare through better outcomes. Those organizations which invest in our new MSO model will be aligned solely with our GNBT shareholders and will receive discount codes to procure our products such as Excellagen.

DME-IQ

NuGenerex Distribution Solutions is planning a launch DME-IQ, a novel software as a service (SaaS) solution for physicians to manage in-office distribution of durable medical equipment (DME). DME-IQ supports the development and management of compliant and profitable in-office DME programs. DME-IQ focuses on several key areas which include negotiating on behalf of the physicians with key vendors to decrease the COGS (Cost of Goods Sold), increasing insurance collections by providing oversight of the coding during the billing process, providing the necessary personnel to manage the appeals processes, and ensuring compliance with state and federal regulations.

DME-IQ will automate and provide the orthopedic practices with a proprietary, tablet-based software package that immediately verifies patient benefits and eligibility. This unique system manages DME inventory, collects patient copays and deductibles, and links patient information with the DME products and necessary patient forms all in one easy to use platform.

The DME Market

The US market for DME is large and growing, a result of several factors including the rising prevalence of chronic diseases requiring long-term care, the rapidly growing geriatric population, and the trend toward home healthcare services. Chronic disorders such as diabetes, diabetic foot & pressure ulcers, chronic pain, and cancer that require long-term patient care and postoperative recovery are driving demand for DME. According to a 2018 market report by Grand View Research, Inc., the US DME market is expected to reach $70.8 billion by 2025, growing at a 6.0% CAGR during the forecast period.

DME-IQ tracks and maintains DME inventory to ensure an adequate supply and product mix for orthopedic patient populations, and the system facilitates insurance claim submissions and adjudication to help achieve optimal reimbursements. With the DME-IQ system, the practice gains control of their DME program from an operations and financial perspective, while patients gain access to a wider variety of DME products that are custom fitted for their needs.

The explosion of high deductible insurance plans has resulted in a dramatic increase of patient out-of-pocket payments for care, and the subsequent requirement that physicians spend more time as collection agents rather than doctors. DME-IQ provides practice workflow solutions for DME with custom, tablet-based software that removes the administrative burden from the practice, facilitating patient eligibility review, collection of patient co-pay and deductibles, centralized insurance adjudication, DME product procurement, and other support services that allow physician practices to increase revenue and service quality. The launch of DME-IQ advances the mission of NDS to provide physicians with end-to-end solutions for patient centric care.”

| 15 |

NuGenerex Regenerative Medicine

Olaregen Therapeutix, Inc.

Our majority-owned subsidiary, Olaregen Therapeutix, Inc. is a regenerative medicine company focused on the development, manufacturing and commercialization of products that fill unmet needs in the current wound care market. We aim to provide advanced healing solutions that substantially improve medical outcomes while lowering the overall cost of care. Olaregen’s first product, Excellagen® (wound conforming matrix) is a topically applied product for dermal wounds and other indications. Excellagen is a FDA 510(k) cleared device for of a broad array of dermal wounds, including partial and full thickness wounds, pressure ulcers, venous ulcers, diabetic ulcers, chronic vascular ulcers, tunneled/undermined wounds, surgical wounds (donor sites/ grafts, post-Mohs surgery, post-laser surgery, podiatric, wound dehiscence), trauma wounds (abrasions, lacerations, second-degree burns and skin tears) and draining wounds, enabling Olaregen to market Excellagen in multiple vertical markets.

The Wound Care Market

Total Global Wound Care Industry is expected to reach $22.01 billion by 2022, according to Markets and Markets; Bioactive Wound Care Market (i.e. skin substitute) is valued at $7.8 billion; In the U.S. There are 6.5 million patients in the U.S. with chronic wounds (NIH estimate).

Olaregen Highlights

| • | Received FDA 510(k) clearance on October 3, 2013, for 17 indications; |

| • | Obtained Intellectual properties and global rights of Excellagen® except China, Russia and CIS. |

| • | Received Patent on October 10, 2017; |

| • | Has a unique Healthcare Common Procedure Coding System (HCPCS) Code - Q4149 |

| • | Clinical data show significant tissue growth and positive wound closure (PDGF) |

| • | Ease of use – No grafting |

| • | Low cost provider with High profit margins; |

| • | Low execution risk (seasoned management team with product launch experience); |

| • | No development risk (over $20 million invested and completed); |

| • | No regulatory risk (FDA cleared). |

| 16 |

Excellagen is an advanced, wound care management platform:

| • | Formulated fibrillar Type I bovine collagen (2.6%) |

| • | High molecular weight |

| • | Viscosity optimized for dripless wound coverage |

| • | Flowable with no staples or sutures required |

| • | Pre-filled, ready to use syringes |

| • | One syringe covers up to 5.0 cm2 wound |

| • | Refrigerated storage only with no thawing or mixing |

| • | Treatment at only one-week intervals |

| • | Activates human platelets |

| • | Triggers the release of Platelet-Derived Growth Factor (PDGF) |

| • | Accelerates granulation tissue growth in “non-healing wounds” |

Additionally, Excellagen can serve as an Enabling Delivery Platform for pluripotent stem cells, antimicrobial agents, small molecule drugs, DNA-Based Biologics, conditioned cell media and peptides. Olaregen's initial focus will be in advanced wound care including diabetic foot ulcers (DFU), venous leg ulcers and pressure ulcers. Future products focusing on innovative therapies in bone and joint regeneration comprise the current pipeline.

Excellagen® History

Olaregen Therapeutix Inc. acquired the intellectual properties and global rights of Excellagen® except in China, Russia and CIS, from Taxus Cardium, Inc. (OTC: CRXM), and its wholly owned subsidiaries Activation Therapeutics, Inc. and Gene Biotherapeutics, Inc.

On August 2018, Olaregen acquired the IP for a total consideration is $4,200,000 and is broken down as follows: 1) $650,000 upfront payment, 2) $200,000 sales credit for collagen solution, and 3) $3,350,000 payable at 10% of net sales, which is defined as total sales less allowances, including hub fees, sales concessions, co-promote fees, cost of goods sold and other charges.

Regentys Corporation

Our majority-owned subsidiary, Regentys Corporation (formerly Asana Medical, Inc.) is a regenerative medicine company developing a tissue engineered therapy for the treatment of Ulcerative Colitis.

Overview

In January 2019, we acquired a majority interest in Regentys Corporation, a Florida corporation, a development-stage regenerative medicine company. Since its formation in May 2013 as Asana Medical Inc., Regentys has been developing a first-in-class tissue engineered therapies for the treatment of Ulcerative Colitis (UC) and other inflammatory bowel diseases.

| 17 |

Ulcerative Colitis

According to an article that was published in The Lancet on December 23, 2018 named worldwide incidence and prevalence of inflammatory bowel disease in the 21st century: a systematic review of population-based studies. (2018 Dec 23;390(10114):2769-2778), Ulcerative Colitis affects an estimated 3.2 million patients in Europe, the United States and Japan. It is a chronic, inflammatory disease that causes sores or ulcers in the lining of the large intestine (the colon). Immunological in nature, UC is thought to be facilitated by a variety of hereditary, genetic and environmental factors and it is increasingly being diagnosed in more urbanized areas. Symptoms, including urgency, bleeding, and diarrhea, that substantially affect quality of life.

Regentys™ Extracellular Matrix Hydrogel (“ECMH”)

Regentys’ initial product, ECMH™ Rectal Solution, is a first-in-class, non-pharmacologic, non-surgical treatment option for millions of patients suffering from mild to moderate Ulcerative Colitis. Its product candidate is a powder that is reconstituted with saline and delivered as a liquid via enema. As ECMH reaches body temperature, it gels and coats the mucosal lining of the GI tract.

The core technology is derived from ECM, a safe and effective FDA-approved base now extensively used for surgical applications and wound treatment. ECMH acts as a bio-scaffold, separating the damaged tissue from waste flow, covering ulcerations to limit the inflammatory response, and facilitating a healing environment using endogenous (the body’s own) stem cells.

Pre-Clinical Results

Published pre-clinical results in the Journal of Crohn’s and Colitis highlight the promise of Regentys technology. Animal data show the ECMH therapy can both alleviate clinical symptoms and facilitate healing in UC patients. Previous pre-clinical ECM animal data for approved products has been shown to have a high correlation with human data.

Competition

Currently four biologics are FDA-approved, including top-selling antibody medicines Humira® (adalimumab), Simponi® (golimumab), Remicade® (infliximab) and Entyvio® (vedolizumab), all of which act to suppress the pro-inflammatory protein, TNF-a (Tumor Necrosis Factor Alpha), a leading cause of the proliferation of ulcerative colis and other forms of IDB. However, even with these options, more than half of all UC patients do not achieve long-term remission. Moreover, 20-30% of non-responsive patients will undergo colon removal surgery in an attempt to remediate the disease.

Regentys Advantages

We expect our product to offer a true alternative to patients non-responsive to first line therapies such as 5-ASA. Unresponsive patients will then need to choose among therapies that alter the body’s immune system or pose long term health risks or perhaps both. Regentys’ technology is expected to enable targeted tissue healing but pose none of the health risks of more expensive market-leading biologics that generally suppress the immune system. We expect to provide our therapy at a cost less than other therapies.

Market

| 18 |

In 2023, when we expect to receive approval, the projected drug costs for UC alone are expected to exceed $7.5B globally according to a 2017 report by Allied Market Research; including other inflammatory bowel disease indications, the global market is expected to be double the UC market. Based upon the nature of IBD, and the characteristics of Regentys’ technology, management believes variations of Regentys’ core technology will also be effective in treating IBD diseases such as Crohn’s, rectal mucositis, proctitis and anal fissures.

Intellectual Property

Regentys in-licensed patents and co-developed its technology platform with the University of Pittsburgh. It now holds patent rights in US and foreign jurisdictions, and has other global filings pending; as well, it has patent applications pending for similar indications predicated on its existing technology in other major global markets.

Regulatory Path

The FDA has affirmed our approach to file a 510(k) de novo application on its ECM hydrogel. We have developed a protocol and has engaged a clinical research organization to manage the conduct of its first-in-human clinical trials expected to start in Q2/Q3 2020 in Australia. Additionally, we have engaged consultants to assist in managing the trials and regulatory approval process in Australia, the US and Europe, jurisdictions in which we initially expect to undertake clinical trials and, among other markets, where it will first seek governmental approval to promote and sell medical devices.

Product Development

Since 2013, we have maintained a research and development agreement with the University of Pittsburgh supplemented with personnel from the affiliated McGowan Institute of Regenerative Medicine. In February 2018, Regentys entered into a development agreement with (and has received a co-investment by) Cook Biotech, Inc., a global leader in ECM manufacturing technology (CookBio). Product batches now on hand are expected to be sufficient for additional development and testing. A larger clinical batch with finalized specifications will be generated in the coming months for use in clinical trials. There are alternate providers of development services who can assist with product development activities. Notwithstanding these options, management believes that because of the nature of ongoing development activities, and the reliance upon certain bench and manufacturing processes and ECM product expertise and technology, any interruption in the development relationship with CookBio would subject the Company to substantial expenditures of time and cost to duplicate the product.

Manufacturing

Regentys has an exclusive manufacturing agreement with CookBio for the production of biomaterial and use of its proprietary technology conditioned upon the completion of final product development work. Management has negotiated an agreement with a third-party manufacturer for product components and kitting. We believe that there are alternate sources of these manufacturing and supply services. However, because of the nature of regulation in the medical device industry, and the reliance upon the collection, reporting and management of medical device manufacturing data, a change of manufacturer would substantially impact the time and cost required for clinical product production and regulatory compliance.

Financing

In January 2019, Regentys was acquired by Generex for an aggregate purchase price of $15,000,000, with $400,000 paid in upfront cash up-front and a promissory note of $14,600,000. Installments payable under the note were tied to specific business development objectives and dates. As October 3, 2019, an additional $850,000 was paid for a total of $1,250,000 against the note. Regentys entered into an accommodation agreement dated March 14, 2019 with Generex to provide longer time to pay. While Generex has not timely made the required payments as of the date this 10-K is filed, Management believes that payments now due will provide sufficient and timely funding to undertake and finalize its first-in-human clinical trials and to acquire one or more regulatory approvals to market and sell our products in Australia, the US and/or the EU.

| 19 |

Operations

Currently, Regentys employs four full-time contract employee and several part-time consultants. We supplement our business operations by engaging external legal (intellectual property, corporate and health care), accounting and tax professionals. We also have contracted with information services, regulatory and clinical trial companies who make available professionals to manage the information services, regulatory, clinical, and compliance aspects of the business. Upon payment of the interim note, Regentys will formally add two contract employees, additional administrative staff and a third-party provider to assist with employee payroll and benefits as well as undertake clinical trial activities suing external support.

NuGenerex Surgical Products

Pantheon Medical – Foot & Ankle, LLC and MediSource Partners, LLC

Pantheon Medical is a manufacturer of orthopedic foot & ankle surgery kits that offer physician friendly “all-in-one,” integrated surgical kits that include plates, screws, and tools required for orthopedic surgeons and podiatrists conducting foot and ankle surgeries.

MediSource Partners is a 10-year old private company that is an FDA registered distributor of surgical, medical, and biologic supplies, with over 25 vendor contracts for nationwide distribution of implants and devices for spine, hips, knees, foot, ankle, hand, and wrist surgeries. Additional product lines include biologics (blood, bone, tissue, stem cells), durable medical equipment, and soft goods. We maintain partnerships and contracts with hospital systems for ordering, billing and inventory management.

The acquisitions of Pantheon and MediSource were finalized on August 1, 2019, immediately subsequent to the end of our 2019 fiscal year. MediSource Partners has contracts with over 25 vendors (including Pantheon Medical) for distribution of:

| • | Implants and devices |

| • | Biologics (blood, bone, tissue, and stem cells) |

| • | Durable medical equipment |

| • | Soft Goods |

| • | Kits to process bone marrow aspirates and platelet rich plasma biologics |

Historical Background

MediSource Partners was founded in 2009 and designed to be unique amongst its competitors by operating as a service-focused, “one stop shop” for the healthcare professionals it serves. With over 25,000 products in its catalogue, including thirteen (13) lines dedicated to spine, MediSource prides itself on its ability to service everything from small private practices across several disciplines, to entire hospital systems. The large and broad-based inventory allows our client physicians to “customize” their operating environment by selecting and implementing the hardware, biologics, soft goods and ancillary tools they feel most confident in and comfortable with. In addition, the “one stop shop” model reduces the burden placed on support staff tasked with managing multiple reps from multiple vendors and shortens the distribution chain to reduce costs and potential redundancies. The success of this model is demonstrated in MediSource’s ability to offer this client-focused, low-impact service at a pricing matrix often below even standard GPO pricing, thus increasing client profitability and productivity.

Pantheon Medical was founded in 2014 to build a manufacturing company with proprietary product lines that offer convenience and cost effectiveness to physicians. Pantheon is contracted with MediSource Partners for nationwide distribution of its proprietary “All-in-One” Foot & Ankle Surgery Kit.

| 20 |

Product Development