| ITEM 1. | REPORTS TO STOCKHOLDERS. |

(a) The Registrant’s annual report transmitted to shareholders pursuant to Rule

30e-1

under the Investment Company Act of 1940 is as follows:

Annual Report to Shareholders |

February 29, 2024 | |

Invesco Senior Income Trust

NYSE:

VVR

Managed Distribution Plan Disclosure

On September 19, 2023, the Board of Trustees (the “Board”) of Invesco Senior Income Trust (the “Trust”) approved an amendment to the Trust’s Managed Distribution Plan (the “Plan”) whereby the Trust will pay its monthly dividend to common shareholders at a stated fixed monthly distribution amount of $0.043 per share. Previously, on January 19, 2023 and September 20, 2022, the Board approved amendments whereby the Trust paid its monthly dividends to common shareholders at a stated fixed monthly distribution amount of $0.039 per share and $0.032 per share, respectively. Prior to these changes under the Plan, the Trust paid a monthly dividend to common shareholders at a stated fixed monthly distribution amount of $0.026 per share. The effective date of the Plan is October 1, 2020.

The Plan is intended to provide shareholders with a consistent, but not guaranteed, periodic cash payment from the Trust, regardless of when or whether income is

earned or capital gains are realized. If sufficient investment income is not available for a monthly distribution, the Trust will distribute long-term capital gains and/or return of capital in order to maintain its managed distribution level under the Plan. A return of capital may occur, for example, when some or all of the money that shareholders invested in the Trust is paid back to them. A return of capital distribution does not necessarily reflect the Trust’s investment performance and should not be confused with “yield” or “income.” No conclusions should be drawn about the Trust’s investment performance from the amount of the Trust’s distributions or from the terms of the Plan. The Plan will be subject to periodic review by the Board, and the Board may amend the terms of the Plan or terminate the Plan at any time without prior notice to the Trust’s shareholders. The amendment or termination of the Plan could have an adverse effect on the market price of the Trust’s common shares.

The Trust will provide its shareholders of record on each distribution record date with a Section 19 Notice disclosing the sources of its dividend payment when a distribution includes anything other than net investment income. The amounts and sources of distributions reported in Section 19 Notices are only estimates and are not being provided for tax reporting purposes. The actual amounts and sources of the amounts for tax reporting purposes will depend upon the Trust’s investment experience during its full fiscal year and may be subject to changes based on tax regulations. The Trust will send shareholders a Form

1099-DIV

for the calendar year that will tell them how to report these distributions for federal income tax purposes. Please refer to “Distributions” under Note 1 of the Notes to Financial Statements for information regarding the tax character of the Trust’s distributions. 2 Invesco Senior Income Trust

Management’s Discussion of Trust Performance

Performance summary | ||

For the fiscal year ended February 29, 2024, Invesco Senior Income Trust (the Trust), at net asset value (NAV), outperformed its benchmark, the Credit Suisse Leveraged Loan Index. The Trust’s return can be calculated based on either the market price or the NAV of its shares. NAV per share is determined by dividing the value of the Trust’s portfolio securities, cash and other assets, less all liabilities and preferred shares, by the total number of common shares outstanding. Market price reflects the supply and demand for Trust shares. As a result, the two returns can differ, as they did during the fiscal year. | ||

Performance |

||

Total returns, 2/28/23 to 2/29/24 |

||

Trust at NAV |

12.65% | |

Trust at Market Value |

18.93 | |

Credit Suisse Leveraged Loan Index q |

11.37 | |

Market Price Premium to NAV as of 2/29/24 |

1.47 | |

Source(s): q |

||

The performance data quoted represent past performance and cannot guarantee comparable future results; current performance may be lower or higher. Investment return, NAV and common share market price will fluctuate so that you may have a gain or loss when you sell shares. Please visit invesco.com/us for the most recent month-end performance. Performance figures reflect Trust expenses, the reinvestment of distributions (if any) and changes in NAV for performance based on NAV and changes in market price for performance based on market price. Since the Trust is a closed-end management investment company, shares of the Trust may trade at a discount or premium from the NAV. This characteristic is separate and distinct from the risk that NAV could decrease as a result of investment activities and may be a greater risk to investors expecting to sell their shares after a short time. The Trust cannot predict whether shares will trade at, above or below NAV. The Trust should not be viewed as a vehicle for trading purposes. It is designed primarily for risk-tolerant long-term investors. | ||

Market conditions and your Trust

During the fiscal year covered by this report, the senior loan market was characterized by concerns around geopolitical instability and global macroeconomic health, along with the related interest rate uncertainty. The combination of these various pressures continued to drive flows out of capital markets and cause risk premia to widen for the first half of the fiscal year. This sentiment shifted towards the end of the fiscal year as improving economic outlooks, the subsequent pause in interest rate hikes and the potential for interest rate cuts on the horizon reversed the trend, pushing risk premia tighter and rerouting flows back into the capital markets. Despite these uncertain circumstances, senior loans outperformed other risk assets through the end of the fiscal year.

1,2

Senior loans’ defensive positioning at the top of the capital structure and floating rate feature benefited the asset class during these bouts of risk aversion and interest rate jitters that caused duration to act as a double-edged sword. Senior loans, as represented by the Credit Suisse Leveraged Loan Index, returned 11.37% during the Fund’s fiscal year,1

with total returns primarily driven by contributions from coupons, and further supplemented by principal returns/price gains. These two drivers worked hand in hand to push overall returns for the fiscal year to their highest level since fiscal year end 2017, all while exhibiting less monthly performance volatility than longer duration assets such as high yield and investment grade US corporate.

1,2

The robust coupon income – currently near

all-time

highs – grew throughout both the fiscal and 2023 calendar year, thanks to rising base rates and, to a lesser extent, wider new issue spreads. Over the course of calendar year 2023, CME Term SOFR increased from 4.59% to 5.38%3

while nominal loan spreads increased from 3.69% to 3.98% during the same time.1

Together with the delayed realization of Secured Overnight Financing Rate (SOFR) increases during late 2022, which had not yet reflected in loan contract resets, loan market coupon grew from 8.14% to 9.36% during the calendar year 2023, ending the fiscal year at 9.28%. Meanwhile, a largely benign credit environment supported broad based price appreciation across the loan market despite central bank efforts to tighten financial conditions and a consistent (but diminishing) trend of rating agency net downgrades. Better-than-expected economic performance in calendar year 2023 underpinned healthy earnings progression for most borrowers, supporting their ability to service debt amid rising interest expense and facilitating access to capital markets for many to extend near-term maturities. Broad loan market issuer interest coverage ratios ended the calendar year at 3.1 times coverage, while leverage levels have remained at pre-pandemic

levels. As of December 31, 2023, only ~7% of outstanding loans mature in 2024 or 2025, so there is minimal refinancing risk in the market.

1

Both the broadly syndicated and private credit markets provided options for issuers to address liquidity shortfalls or extend/refinance near-term maturities during the calendar year. Given these current fundamentals, the par weighted default rate at the end of the fiscal year remained not far from cycle lows, at 1.41%,4

while the percentage of loans trading below 80 declined to just 3.35%,4

a good signal that credit stress in the market is contained. That being said, the loan market is expected to experience moderately increasing levels of defaults, with most forecasts between a 3.0% to 4.0% trailing twelve months default rate by year-end

2024, on par with the long-term average default rates.4,5

The surprisingly constructive macroeconomic backdrop enabled lower rated loans to outperform higher rated loans in both price advances and total returns during the fiscal year, with the average loan price increasing from $91.89 at the start of the calendar year ($93.49 at the start of the fiscal year) to $95.74 at the end of the fiscal year, with gains most pronounced amongst the B and CCC cohorts.

1

As loan market conditions improved, access to the primary market expanded but remained most accommodating for higher quality issuers. For the calendar year, 62.3% of gross issuance came from issuers rated B† or below, versus 75.4% the prior year.5

Refinancing activity was the dominant transaction type, growing 168% versus the prior year,5

however, new issuance for uses beyond managing maturities was limited by the dearth of acquisition activity in the private equity and corporate realms. Net new issuance (ex-refinancing/repricing)

of $81.8 billion (bn) was down 50% versus prior year.5

Reflective of the selective funding environment, leveraged buyouts financed with loans during 2023 calendar year featured the lowest leverage levels since 2010 and the highest sponsor equity contributions on record.6

Despite sparse new issuance, collateralized loan obligation (CLO) origination remained strong with US CLOs having priced $139.3bn (or $116.2bn ex-refinancings)

across 322 structures during the calendar year.5

Of that, $108.1bn (or $88.4bn ex-refinancings)

came from structures that purchase broadly syndicated loans (BSL) while the remainder came from structures that purchase middle market/private credit loans. CLO formation served as a critical pillar of support for loan demand during 2023 both for the fiscal and calendar years. At fiscal

year-end,

yields remain robust on both a historical and relative value basis, with average loan coupons continuing to outyield the average coupon for high-yield bonds.1,2

Given the price of senior loans at the end of the fiscal year, they provided a 9.39% yield (represented by the yield to 3-year

life).1

During the fiscal year, the Trust employed leverage, which allowed us to enhance the Trust’s yield while keeping credit standards

3 Invesco Senior Income Trust

high relative to the benchmark. As of the close of the fiscal year, leverage accounted for approximately 31% of the Trust’s total assets. Leverage involves borrowing at a floating short-term rate and reinvesting the proceeds at a higher rate. Unlike other fixed-income asset classes, using leverage in conjunction with senior loans does not involve the same degree of risk from rising short-term interest rates since the income from senior loans generally adjusts to changes in interest rates, as do the rates which determine the Trust’s borrowing costs. (Similarly, should short-term rates fall, borrowing costs also would decline.) For more information about the Trust’s use of leverage and the associated risks, see the Notes to Financial Statements later in this report.

During the fiscal year ended February 29, 2024, , and were the largest contributors to the Fund’s absolute performance, while , and were the largest detractors from absolute performance. On an industry basis, the service, transportation, and manufacturing industries provided the largest contributors to absolute return, while broadcasting was the only detractor from absolute performance.

Commercial Barge Line

My Alarm Center

Teasdale Foods

MLN US

IAP Worldwide Services

NAC Aviation 8

In managing the Trust, we take a multi-strategy approach to private credit – allocating across direct lending, broadly syndicated loans and special situations, seeking to take advantage of market opportunities and potential market inefficiencies. We seek to efficiently allocate risk within the portfolio in order to maximize risk-adjusted returns through five different considerations consisting of credit selection, sector migration, risk positioning, asset selection and trading.

The common thread across the Trust’s strategies (broadly syndicated loans, direct lending and special situations) is its focus on senior secured floating rate loans. We believe this aspect provides capital preservation potential given these loans are senior and secured in the capital structure which has historically resulted in lower volatility with higher recovery rates versus unsecured high-yield bonds and equity.

5

Meanwhile, the loan coupons are floating rate, meaning they have very little interest rate risk relative to traditional fixed income investments and sensitivity in rising rate environments, as was the case during the fiscal year.1

The senior loan asset class behaves differently from many traditional fixed-income investments. The interest income generated by a portfolio of senior loans is usually determined by a fixed credit spread over a reference rate. Because senior loans generally have a very short duration and the coupons, or interest rates, are usually adjusted every 30 to 90 days as the reference rate changes, the yield on the portfolio adjusts. Interest rate risk refers to the tendency for traditional fixed-income prices to decline when interest rates rise. For senior loans, however, interest rates and income are variable, and the prices of loans are therefore less sensitive to interest

rate changes than traditional fixed-income bonds. As a result, senior loans can provide a natural hedge against volatile interest rates.

We are monitoring interest rates, the market, economic and geopolitical factors that may impact the direction, speed and magnitude of changes to interest rates across the maturity spectrum, including the potential impact of monetary policy changes by the US Federal Reserve and other central banks. If interest rates rise or fall faster than expected, markets may experience increased volatility, which may affect the value and/or liquidity of certain of the Trust’s investments and the market price of the Trust’s shares.

As always, we appreciate your continued participation in Invesco Senior Income Trust.

| 1 | Source: Credit Suisse Leveraged Loan Index |

| 2 | Source: Credit Suisse High Yield Index represents High Yield, and the Bloomberg US Corporate Investment Grade Index represents US Corporate |

| 3 | Source: Bloomberg as of December 4, 2023 |

| 4 | Source: Morningstar LSTA US Leveraged Loan Index |

| 5 | Source: JP Morgan Research |

| 6 | Source: Pitchbook Data Inc. |

† Standard & Poor’s, Fitch Ratings, Moody’s. A credit rating is an assessment provided by a nationally recognized statistical rating organization (NRSRO) of the creditworthiness of an issuer with respect to debt obligations, including specific securities, money market instruments or other debts. Ratings are measured on a scale that generally ranges from AAA (highest) to D (lowest); ratings are subject to change without notice.

“Non-Rated”

indicates the debtor was not rated and should not be interpreted as indicating low quality. For more information on rating methodology, please visit spglobal.com, fitchratings.com and ratings.moodys.com. Portfolio manager(s):

Scott Baskind

Thomas Ewald - Lead

Philip Yarrow

The views and opinions expressed in management’s discussion of Trust performance are those of Invesco Advisers, Inc. and its affiliates. These views and opinions are subject to change at any time based on factors such as market and economic conditions. These views and opinions may not be relied upon as investment advice or recommendations, or as an offer for a particular security. The information is not a complete analysis of every aspect of any market, country, industry, security or the Trust. Statements of fact are from sources considered reliable, but Invesco Advisers, Inc. makes no representation or warranty as to their completeness or accuracy. Although historical performance is no guarantee of future results, these insights may help you understand our investment management philosophy.

See important Trust and, if applicable, index disclosures later in this report.

4 Invesco Senior Income Trust

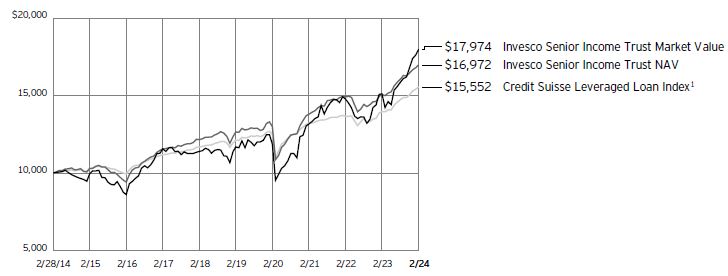

Your Trust’s Long-Term Performance

Results of a $10,000 Investment

Trust and index data from 2/28/14

1 Source: Bloomberg LP

Past performance cannot guarantee future results.

Performance shown in the chart does not reflect deduction of taxes a shareholder would pay on Trust distributions or sale of Trust shares.

5 Invesco Senior Income Trust

Average Annual Total Returns |

||||||||

As of 2/29/24 |

||||||||

NAV |

Market |

|||||||

10 Years |

5.43 | % | 6.04 | % | ||||

5 Years |

6.06 | 8.99 | ||||||

1 Year |

12.65 | 18.93 | ||||||

The performance data quoted represent past performance and cannot guarantee future results; current performance may be lower or higher. Please visit invesco.com/performance for the most recent

month-end

performance. Performance figures do not reflect deduction of taxes a shareholder would pay on Trust distributions or sale of Trust shares. Investment return and principal value will fluctuate so that you may have a gain or loss when you sell shares.

6 Invesco Senior Income Trust

Supplemental Information

∎ |

Unless otherwise stated, information presented in this report is as of February 29, 2024, and is based on total net assets applicable to common shares. |

∎ |

Unless otherwise noted, all data is provided by Invesco. |

∎ |

To access your Trust’s reports, visit invesco.com/fundreports. |

About indexes used in this report

∎ |

The Credit Suisse Leveraged Loan Index US-dollar-denominated, non-investment grade loans. |

∎ |

The Trust is not managed to track the performance of any particular index, including the index(es) described here, and consequently, the performance of the Trust may deviate significantly from the performance of the index(es). |

∎ |

A direct investment cannot be made in an index. Unless otherwise indicated, index results include reinvested dividends, and they do not reflect sales charges. Performance of the peer group, if applicable, reflects fund expenses; performance of a market index does not. |

| NOT FDIC INSURED | MAY LOSE VALUE | NO BANK GUARANTEE |

7 Invesco Senior Income Trust

Dividend Reinvestment Plan

The dividend reinvestment plan (the Plan) offers you a prompt and simple way to reinvest your dividends and capital gains distributions (Distributions) into additional shares of your Invesco

closed-end

Trust (the Trust). Under the Plan, the money you earn from Distributions will be reinvested automatically in more shares of the Trust, allowing you to potentially increase your investment over time. All shareholders in the Trust are automatically enrolled in the Plan when shares are purchased. Plan benefits

∎ |

Add to your account: |

You may increase your shares in your Trust easily and automatically with the Plan.

∎ |

Low transaction costs: |

Shareholders who participate in the Plan may be able to buy shares at below-market prices when the Trust is trading at a premium to its net asset value (NAV). In addition, transaction costs are low because when new shares are issued by the Trust, there is no brokerage fee, and when shares are bought in blocks on the open market, the per share fee is shared among all participants.

∎ |

Convenience: |

You will receive a detailed account statement from Computer share Trust Company, N.A. (the Agent), which administers the Plan. The statement shows your total Distributions, date of investment, shares acquired, and price per share, as well as the total number of shares in your reinvestment account. You can also access your account

at invesco.com/closed-end.

∎ |

Safekeeping: |

The Agent will hold the shares it has acquired for you in safekeeping.

Who can participate in the Plan

If you own shares in your own name, your purchase will automatically enroll you in the Plan. If your shares are held in “street name” – in the name of your brokerage firm, bank, or other financial institution – you must instruct that entity to participate on your behalf. If they are unable to participate on your behalf, you may request that they reregister your shares in your own name so that you may enroll in the Plan.

How to enroll

If you haven’t participated in the Plan in the past or chose to opt out, you are still eligible to participate. Enroll by visiting

invesco.com/closed-end,

by calling toll-free 800 341 2929 or by notifying us in writing at Invesco Closed-End

Funds, Computer-share Trust Company, N.A., P.O. Box 43078, Providence, RI 02940-3078. If you are writing to us, please include the Trust name and account number and ensure that all shareholders listed on the account sign these written instructions. Your participation in the Plan will begin with the next Distribution payable after the Agent receives your authorization, as long as they receive it before the “record date,” which is generally 10 business days before the Distribution is paid. If your authorization arrives after such record date, your participation in the Plan will begin with the following Distribution. How the Plan works

If you choose to participate in the Plan, your Distributions will be promptly reinvested for you, automatically increasing your shares. If the Trust is trading at a share price that is equal to its NAV, you’ll pay that amount for your reinvested shares. However, if the Trust is trading above or below NAV, the price is determined by one of two ways:

| 1. | Premium: If the Trust is trading at a premium – a market price that is higher than its NAV – you’ll pay either the NAV or 95 percent of |

the market price, whichever is greater. When the Trust trades at a premium, you may pay less for your reinvested shares than an investor purchasing shares on the stock exchange. Keep in mind, a portion of your price reduction may be taxable because you are receiving shares at less than market price. |

| 2. | Discount: If the Trust is trading at a discount – a market price that is lower than its NAV – you’ll pay the market price for your reinvested shares. |

Costs of the Plan

There is no direct charge to you for reinvesting Distributions because the Plan’s fees are paid by the Trust. If the Trust is trading at or above its NAV, your new shares are issued directly by the Trust and there are no brokerage charges or fees. However, if the Trust is trading at a discount, the shares are purchased on the open market, and you will pay your portion of any per share fees. These per share fees are typically less than the standard brokerage charges for individual transactions because shares are purchased for all participants in blocks, resulting in lower fees for each individual participant. Any service or per share fees are added to the purchase price. Per share fees include any applicable brokerage commissions the Agent is required to pay.

Tax implications

The automatic reinvestment of Distributions does not relieve you of any income tax that may be due on Distributions. You will receive tax information annually to help you prepare your federal income tax return.

Invesco does not offer tax advice. The tax information contained herein is general and is not exhaustive by nature. It was not intended or written to be used, and it cannot be used, by any taxpayer for avoiding penalties that may be imposed on the taxpayer under US federal tax laws. Federal and state tax laws are complex and constantly changing. Shareholders should always consult a legal or tax adviser for information concerning their individual situation.

How to withdraw from the Plan

You may withdraw from the Plan at any time by calling 800 341 2929, by visiting invesco.com/

closed-end

or by writing to Invesco Closed-End

Funds, Computer share Trust Company, N.A., P.O. Box 43078, Providence, RI 02940-3078. Simply indicate that you would like to withdraw from the Plan, and be sure to include your Trust name and account number. Also, ensure that all shareholders listed on the account sign these written instructions. If you withdraw, you have three options with regard to the shares held in the Plan: | 1. | If you opt to continue to hold your non- certificated whole shares (Investment Plan Book Shares), they will be held by the Agent electronically as Direct Registration Book- Shares (Book-Entry Shares) and fractional shares will be sold at the then-current market price. Proceeds will be sent via check to your address of record after deducting applicable fees, including per share fees such as any applicable brokerage commissions the Agent is required to pay. |

| 2. | If you opt to sell your shares through the Agent, we will sell all full and fractional shares and send the proceeds via check to your address of record after deducting $2.50 per account and a brokerage charge. |

| 3. | You may sell your shares through your financial adviser through the Direct Registration System (DRS). DRS is a service within the securities industry that allows Trust shares to be held in your name in electronic format. You retain full ownership of your shares, without having to hold a share certificate. You should contact your financial adviser to learn more about any restrictions or fees that may apply. |

The Trust and Computer share Trust Company, N.A. may amend or terminate the Plan at any time. Participants will receive at least 30 days written notice before the effective date of any amendment. In the case of termination, Participants will receive at least 30 days written notice before the record date for the payment of any such Distributions by the Trust. In the case of amendment or termination necessary or appropriate to comply with applicable law or the rules and policies of the Securities and Exchange Commission or any other regulatory authority, such written notice will not be required.

To obtain a complete copy of the current Dividend Reinvestment Plan, please call our Client Services department at 800 341 2929 or visit

invesco.com/closed-end.

8 Invesco Senior Income Trust

Fund Information

Portfolio Composition*

By credit quality |

% of total investments | |

BBB- |

0.80% | |

BB+ |

1.93 | |

BB |

6.15 | |

BB- |

3.38 | |

B+ |

7.17 | |

B |

13.80 | |

B- |

10.40 | |

CCC+ |

5.29 | |

CCC |

2.88 | |

CCC- |

0.15 | |

CC |

0.33 | |

D |

0.78 | |

Not Rated |

39.66 | |

Equity |

7.28 |

| * | Source: Standard & Poor’s. A credit rating is an assessment provided by a nationally recognized statistical rating organization (NRSRO) of the creditworthiness of an issuer with respect to debt obligations, including specific securities, money market instruments or other debts. Ratings are measured on a scale that generally ranges from AAA (highest) to D (lowest); ratings are subject to change without notice. “Non-Rated” indicates the debtor was not rated, and should not be interpreted as indicating low quality. For more information on Standard & Poor’s rating methodology, please visit standardandpoors.com and select “Understanding Ratings” under Rating Resources on the homepage. |

Top Five Debt Issuers*

% of total net assets | ||||

1. |

Keg Logistics LLC | 4.09% | ||

2. |

FDH Group Acquisition, Inc. | 3.44 | ||

3. |

CV Intermediate Holdco Corp. (Class Valuation) | 3.19 | ||

4. |

SDB Holdco LLC (Specialty Dental Brands) | 3.12 | ||

5. |

Lightning Finco Ltd. (LiveU) | 3.02 | ||

The Trust’s holdings are subject to change, and there is no assurance that the Trust will continue to hold any particular security.

| * | Excluding money market fund holdings, if any. |

Data presented here are as of February 29, 2024.

9 Invesco Senior Income Trust

Consolidated Schedule of Investments

February 29, 2024

Interest Rate |

Maturity Date |

Principal Amount (000) (a) |

Value | |||||||||||||||

Variable Rate Senior Loan Interests–132.63% (b)(c) |

||||||||||||||||||

Aerospace & Defense–6.02% |

||||||||||||||||||

ADB Safegate (ADBAS/CEP IV) (Luxembourg), Term Loan B (3 mo. EURIBOR + 4.75%) |

8.71 | % | 10/05/2026 | EUR | 1,414 | $ 1,465,041 | ||||||||||||

Barnes Group, Inc., Term Loan (1 mo. Term SOFR + 3.00%) |

8.43 | % | 09/03/2030 | $ | 455 | 456,760 | ||||||||||||

Brown Group Holding LLC (Signature Aviation US Holdings, Inc.), Incremental Term Loan B-2 (1 mo. Term SOFR + 3.00%) |

8.31 | % | 07/02/2029 | 1,348 | 1,347,856 | |||||||||||||

Castlelake Aviation Ltd., Incremental Term Loan (3 mo. Term SOFR + 2.50%) |

8.13 | % | 10/22/2027 | 4,661 | 4,664,920 | |||||||||||||

FDH Group Acquisition, Inc., Term Loan A (d)(e) |

12.00 | % | 10/01/2025 | 21,776 | 21,558,070 | |||||||||||||

Gogo Intermediate Holdings LLC, Term Loan (1 mo. Term SOFR + 3.75%) |

9.19 | % | 04/30/2028 | 980 | 977,630 | |||||||||||||

NAC Aviation 8 Ltd. (Ireland) |

||||||||||||||||||

Revolver Loan (e)(f) |

0.00 | % | 12/31/2026 | 1,826 | 1,826,168 | |||||||||||||

Term Loan (e) |

9.44 | % | 12/31/2026 | 2,135 | 0 | |||||||||||||

Term Loan (e) |

9.44 | % | 12/31/2026 | 2,181 | 0 | |||||||||||||

Peraton Corp., Second Lien Term Loan (3 mo. Term SOFR + 7.75%) |

13.18 | % | 02/01/2029 | 2,389 | 2,394,342 | |||||||||||||

Propulsion (BC) Finco S.a.r.l. (Spain), Term Loan (3 mo. Term SOFR + 4.00%) |

9.10 | % | 09/14/2029 | 3 | 2,586 | |||||||||||||

Rand Parent LLC (Atlas Air), Term Loan B (1 mo. Term SOFR + 4.25%) |

9.60 | % | 03/17/2030 | 1,533 | 1,533,845 | |||||||||||||

Titan Acquisition Holdings L.P., Term Loan (1 mo. Term SOFR + 4.00%) (e) |

9.32 | % | 06/14/2030 | 590 | 591,387 | |||||||||||||

TransDigm, Inc., Term Loan I (1 mo. Term SOFR + 3.25%) |

8.60 | % | 08/24/2028 | 898 | 901,072 | |||||||||||||

| 37,719,677 | ||||||||||||||||||

Air Transport–3.24% |

||||||||||||||||||

AAdvantage Loyality IP Ltd. (American Airlines, Inc.), Term Loan (3 mo. Term SOFR + 4.75%) |

10.33 | % | 04/20/2028 | 5,831 | 5,951,541 | |||||||||||||

Air Canada (Canada), Term Loan (3 mo. Term SOFR + 3.50%) |

8.93 | % | 08/11/2028 | 1,166 | 1,169,638 | |||||||||||||

American Airlines, Inc. |

||||||||||||||||||

Term Loan (1 mo. Term SOFR + 2.75%) |

8.60 | % | 02/15/2028 | 1,679 | 1,673,703 | |||||||||||||

Term Loan (1 mo. Term SOFR + 3.50%) |

8.87 | % | 06/04/2029 | 3,076 | 3,078,076 | |||||||||||||

Avolon TLB Borrower 1 (US) LLC, Term Loan B-6 (1 mo. Term SOFR + 2.00%) |

7.32 | % | 06/22/2028 | 195 | 195,599 | |||||||||||||

United AirLines, Inc., Term Loan B (1 mo. Term SOFR + 2.75%) |

8.08 | % | 02/22/2031 | 4,855 | 4,858,402 | |||||||||||||

WestJet Airlines Ltd. (Canada) |

||||||||||||||||||

Term Loan (3 mo. Term SOFR + 3.00%) |

8.43 | % | 12/11/2026 | 144 | 144,387 | |||||||||||||

Term Loan (1 mo. Term SOFR + 3.75%) |

9.06 | % | 02/14/2031 | 3,269 | 3,246,540 | |||||||||||||

| 20,317,886 | ||||||||||||||||||

Automotive–9.80% |

||||||||||||||||||

Adient PLC, Term Loan B-2 (1 mo. Term SOFR + 2.75%) |

8.08 | % | 01/31/2031 | 668 | 670,073 | |||||||||||||

Autokiniton US Holdings, Inc., Term Loan B (1 mo. Term SOFR + 4.00%) |

9.44 | % | 04/06/2028 | 946 | 948,507 | |||||||||||||

Constellation Auto (CONSTE/BCA) (United Kingdom) |

||||||||||||||||||

First Lien Term Loan B-2 |

9.94 | % | 07/28/2028 | GBP | 305 | 357,721 | ||||||||||||

Second Lien Term Loan B-1 |

12.69 | % | 07/27/2029 | GBP | 800 | 737,129 | ||||||||||||

DexKo Global, Inc. |

||||||||||||||||||

Incremental First Lien Term Loan (1 mo. Term SOFR + 4.25%) |

9.60 | % | 10/04/2028 | 806 | 807,802 | |||||||||||||

Revolver Loan (e)(f) |

0.00 | % | 10/05/2026 | 1,224 | 1,214,416 | |||||||||||||

Driven Holdings LLC, Term Loan (1 mo. Term SOFR + 3.00%) |

8.44 | % | 12/17/2028 | 1,080 | 1,072,802 | |||||||||||||

Engineered Components & Systems LLC, Term Loan (1 mo. Term SOFR + 6.00%) |

11.33 | % | 08/30/2030 | 1,197 | 1,196,588 | |||||||||||||

First Brands Group LLC |

||||||||||||||||||

First Lien Term Loan (6 mo. Term SOFR + 5.00%) |

10.57 | % | 03/30/2027 | 3,473 | 3,485,430 | |||||||||||||

First Lien Term Loan (1 mo. Term SOFR + 5.00%) |

10.57 | % | 03/30/2027 | 3,314 | 3,323,885 | |||||||||||||

Second Lien Term Loan (g) |

- | 03/30/2028 | 934 | 926,447 | ||||||||||||||

Highline Aftermarket Acquisition LLC, Term Loan (1 mo. Term SOFR + 4.50%) |

9.93 | % | 11/09/2027 | 2,499 | 2,502,064 | |||||||||||||

Les Schwab Tire Centers, Term Loan (1 mo. Term SOFR + 3.25%) |

8.69 | % | 11/02/2027 | 1,542 | 1,542,770 | |||||||||||||

M&D Distributors |

||||||||||||||||||

Delayed Draw Term Loan (d)(e)(f) |

0.00 | % | 08/31/2028 | 1,102 | 1,097,423 | |||||||||||||

Delayed Draw Term Loan (d)(e) |

11.01 | % | 08/31/2028 | 1,256 | 1,251,428 | |||||||||||||

Revolver Loan (d)(e)(f) |

0.00 | % | 08/31/2028 | 759 | 755,689 | |||||||||||||

Revolver Loan (d)(e) |

13.00 | % | 08/31/2028 | 424 | 421,804 | |||||||||||||

Term Loan A (d)(e) |

10.99 | % | 08/31/2028 | 6,678 | 6,651,068 | |||||||||||||

Mavis Tire Express Services Topco Corp., First Lien Term Loan (1 mo. Term SOFR + 3.75%) |

9.08 | % | 05/04/2028 | 2,961 | 2,967,107 | |||||||||||||