First

BanCorp Investor Presentation

November 2013

Exhibit 99.1 |

Disclaimer

1

This presentation contains “forward-looking statements” concerning First

BanCorp’s (the “Corporation”) future economic performance. The words or phrases “would

be,” “will allow,” “intends to,” “will likely result,”

“are expected to,” “expect,” “anticipate,” “look forward,” “should,” “believes” and similar expressions are meant to

identify “forward-looking statements” within the meaning of Section 27A of the

Private Securities Litigation Reform Act of 1995, and are subject to the safe harbor

created by such section. The Corporation wishes to caution readers not to place undue reliance

on any such “forward-looking statements,” which speak only as of the date

made, and to advise readers that various factors, including, but not limited to, uncertainty about whether the Corporation and FirstBank Puerto Rico (“FirstBank”

or “the Bank”) will be able to fully comply with the written agreement dated

June 3, 2010 that the Corporation entered into with the Federal Reserve Bank of New York

(the “FED”) and the order dated June 2, 2010 (the “Order”) that

FirstBank entered into with the FDIC and the Office of the Commissioner of Financial Institutions of

Puerto Rico that, among other things, require FirstBank to maintain certain capital levels and

reduce its special mention, classified, delinquent and non-performing assets; the

risk of being subject to possible additional regulatory actions; uncertainty as to the availability of certain funding sources, such as retail brokered CDs; the

Corporation’s reliance on brokered CDs and its ability to obtain, on a periodic basis,

approval from the FDIC to issue brokered CDs to fund operations and provide liquidity

in accordance with the terms of the Order; the risk of not being able to fulfill the Corporation’s cash obligations or resume paying dividends to the

Corporation’s stockholders in the future due to the Corporation’s inability to

receive approval from the FED to receive dividends from FirstBank or FirstBank’s failure to

generate sufficient cash flow to make a dividend payment to the Corporation; the strength or

weakness of the real estate markets and of the consumer and commercial credit sectors

and their impact on the credit quality of the Corporation’s loans and other assets, including the Corporation’s construction and commercial real estate

loan portfolios, which have contributed and may continue to contribute to, among other things,

the high levels of non-performing assets, charge-offs and the provision expense

and may subject the Corporation to further risk from loan defaults and foreclosures; adverse changes in general economic conditions in the United States and

in Puerto Rico, including the interest rate scenario, market liquidity, housing absorption

rates, real estate prices and disruptions in the U.S. capital markets, which may reduce

interest margins, impact funding sources and affect demand for all of the Corporation’s products and services and the value of the Corporation’s assets; an

adverse change in the Corporation’s ability to attract new clients and retain existing

ones; a decrease in demand for the Corporation’s products and services and lower

revenues and earnings because of the continued recession in Puerto Rico and the current fiscal

problems and budget deficit of the Puerto Rico government; uncertainty about regulatory

and legislative changes for financial services companies in Puerto Rico, the United States and the U.S. and British Virgin Islands, which could affect the

Corporation’s financial performance and could cause the Corporation’s actual results

for future periods to differ materially from prior results and anticipated or projected

results; uncertainty about the effectiveness of the various actions undertaken to stimulate the United States economy and stabilize the United States’

financial markets, and the impact such actions may have on the Corporation’s business,

financial condition and results of operations; changes in the fiscal and monetary

policies and regulations of the federal government, including those determined by the Federal

Reserve System, the FDIC, government-sponsored housing agencies and regulators in

Puerto Rico and the U.S. and British Virgin Islands; the risk of possible failure or circumvention of controls and procedures and the risk that the

Corporation’s risk management policies may not be adequate; the risk that the FDIC may

further increase the deposit insurance premium and/or require special assessments to

replenish its insurance fund, causing an additional increase in the Corporation’s non-interest expense; risks of not being able to recover the assets

pledged to Lehman Brothers Special Financing, Inc.; the impact on the Corporation’s

results of operations and financial condition associated with acquisitions and

dispositions; a need to recognize additional impairments on financial instruments or goodwill

relating to acquisitions; risks that downgrades in the credit ratings of the

Corporation’s long-term senior debt will adversely affect the Corporation’s

ability to access necessary external funds; the impact of the Dodd-Frank Wall Street Reform

and Consumer Protection Act on the Corporation’s businesses, business practices and cost

of operations; and general competitive factors and industry consolidation. The

Corporation does not undertake, and specifically disclaims any obligation, to update any “forward-looking statements” to reflect occurrences or unanticipated

events or circumstances after the date of such statements except as required by the federal

securities laws. Investors should refer to the Corporation’s Annual Report on Form

10-K for the year ended December 31, 2012 for a discussion of such factors and certain risks and uncertainties to which the Corporation is subject.

|

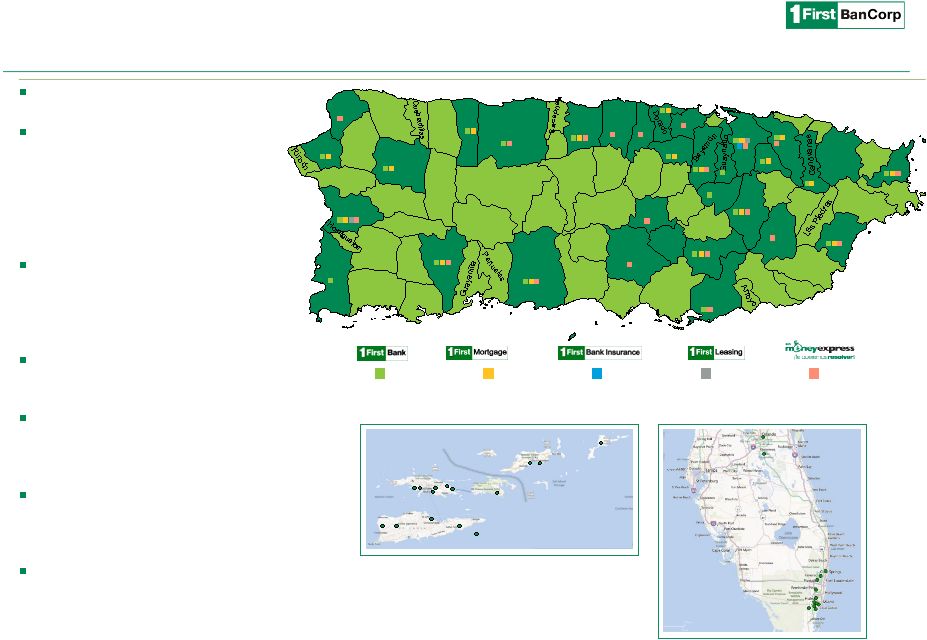

Eastern

Caribbean:

7% of Assets

14 bank branches

3 First Express branches

Franchise Overview

Founded in 1948

Headquartered in San Juan, Puerto

Rico with operations in PR, Eastern

Caribbean (Virgin Islands) and

Florida

–

~2,500 FTE employees

(1)

2nd largest financial holding

company in Puerto Rico with

attractive business mix and

substantial loan market share

Florida presence with focus on

serving south Florida region

The largest depository institution

in the Virgin Islands with

approximately 40% market share

146 ATM machines and largest

ATM network in the Eastern

Caribbean Region

(2)

A well diversified operation with

over 650,000 retail & commercial

customers

Well diversified with significant competitive strengths

2

Total Assets -

$12.8B

Total Loans -

$9.6B

Total Deposits -

$10.0B

Naguabo

Fajardo

Ceiba

Luquillo

Juncos

Río

Grande

Loíza

Trujillo

Alto

Carolina

Gurabo

Toa Baja

Cataño

San Juan

Aguas

Buenas

Caguas

Comerío

Naranjito

Corozal

Toa Alta

San

Germán

Mayagüez

Barranquitas

San

Lorenzo

Cayey

Patillas

Humacao

Hatillo

Cabo

Rojo

Maunabo

Guayama

Vega

Baja

Isabela

San

Sebastián

Aguadilla

Sabana

Grande

Yauco

Ciales

Jayuya

Juana

Díaz

Santa

Isabel

Adjuntas

Aguada

Aibonito

Añasco

Arecibo

Camuy

Cidra

Coamo

Florida

Guánica

Lajas

Lares

Las Marías

Manatí

Maricao

Moca

Morovis

Orocovis

Ponce

Salinas

Utuado

Villalba

Yabucoa

47 Branches

35 Branches

5 Branches

2 Branches

26 Branches

12 bank branches

1 Loan Production Office

SE Florida:

7% of Assets

30% of core

deposits

(3)

15% of core

deposits

(3)

As of September 30, 2013.

1) FTE = Full Time Equivalent. 2) Eastern

Caribbean Region or ECR includes United States and British Virgin Islands.

3) Data as of December 31, 2012. Core deposits excludes brokered deposits allocated to Puerto

Rico. |

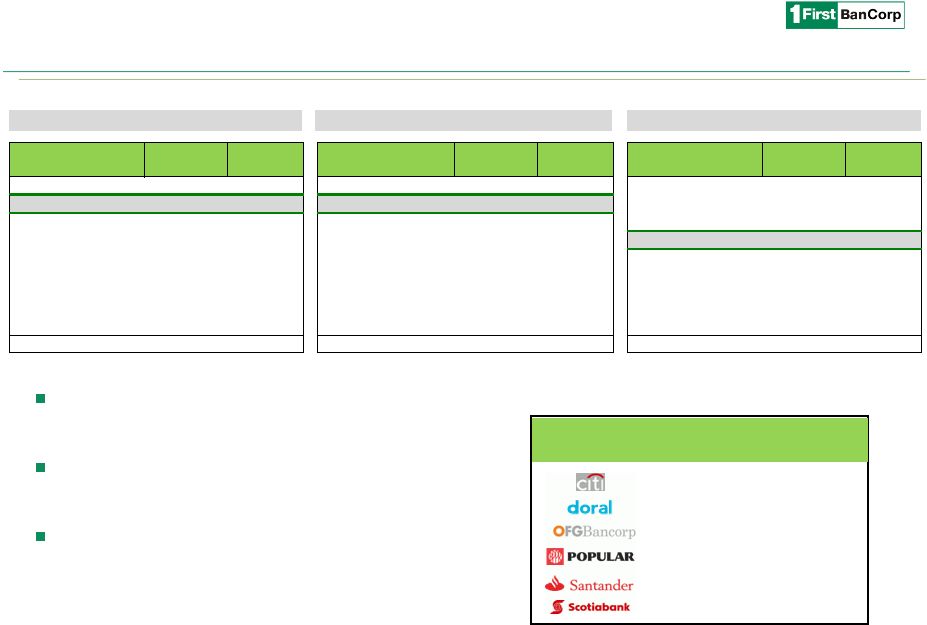

Franchise

Overview ($ in millions)

Well positioned Puerto Rico institution in a consolidating market

Source: PR Market Share Report prepared with data provided by the Commissioner of Financial

Institutions of Puerto Rico as of 6/30/13. 1) Puerto Rico only.

2) Calculated as institution bank branches within a mile of an FBP branch as a percentage of

total institution branches. 3) Alphabetical order.

3

Puerto Rico Total Assets

(1)

Puerto Rico Total Loans

(1)

Puerto

Rico

Deposits,

Net

of

Brokered

(1)

Strong and uniquely positioned franchise in

densely populated regions of core operating

footprint

Strong market share in loan portfolios

facilitates customer relationship expansion and

cross-sell to increase deposit share

Long-term opportunity for additional

consolidation

Branch overlap of greater than 40% with six

Puerto Rico institutions

(2)

1-mile

branch

overlap

(3)

64

42

80%

42

47

44

Portfolio

Balance

Market

Share

Portfolio

Balance

Market

Share

Portfolio

Balance

Market

Share

1

Banco Popular

$26,132

39.9%

1

Banco Popular

$19,212

38.8%

1

Banco Popular

$17,852

44.1%

2

FirstBank

9,662

14.8%

2

FirstBank

8,123

16.4%

2

Banco Santander

5,694

14.1%

3

Oriental Bank

7,405

11.3%

3

Banco Santander

5,413

10.9%

3

Oriental Bank

4,908

12.1%

4

Banco Santander

7,031

10.7%

4

Scotiabank

5,146

10.4%

4

FirstBank

3,858

9.5%

5

Scotiabank

7,002

10.7%

5

Oriental Bank

5,083

10.3%

5

Scotiabank

3,427

8.5%

6

Doral Bank

5,477

8.4%

6

Doral Bank

2,839

5.7%

6

Citibank

2,227

5.5%

7

Citibank

2,223

3.4%

7

Other

2,692

5.4%

7

Doral Bank

2,031

5.0%

8

Banco Cooperativo

518

0.8%

8

Citibank

755

1.5%

8

Banco Cooperativo

437

1.1%

9

BBU

20

0.0%

9

Banco Cooperativo

193

0.4%

9

BBU

25

0.1%

Total

$65,469

100%

Total

$49,456

100%

Total

$40,460

100%

Institutions

Institutions

Institutions

– |

2009

Today (3Q 2013)

Change ('09-3Q'13)

% improvement

NPAs

$1,711

$726

$985

58%

NPAs/assets

8.7%

5.7%

303 bps

Tier 1 Common

4.1%

12.6%

845 bps

101%

TCE / TA

3.2

8.7

545 bps

76%

Core deposits

$5,108

$6,773

$1,665

33%

NIM

2.69%

4.20%

151 bps

Our turnaround story

Franchise Overview

($ in millions)

De-Risking of Balance Sheet

Capital

Enhanced Franchise Value

4

1) Represents change in dollar amount.

(1)

(1)

(1)

(1)

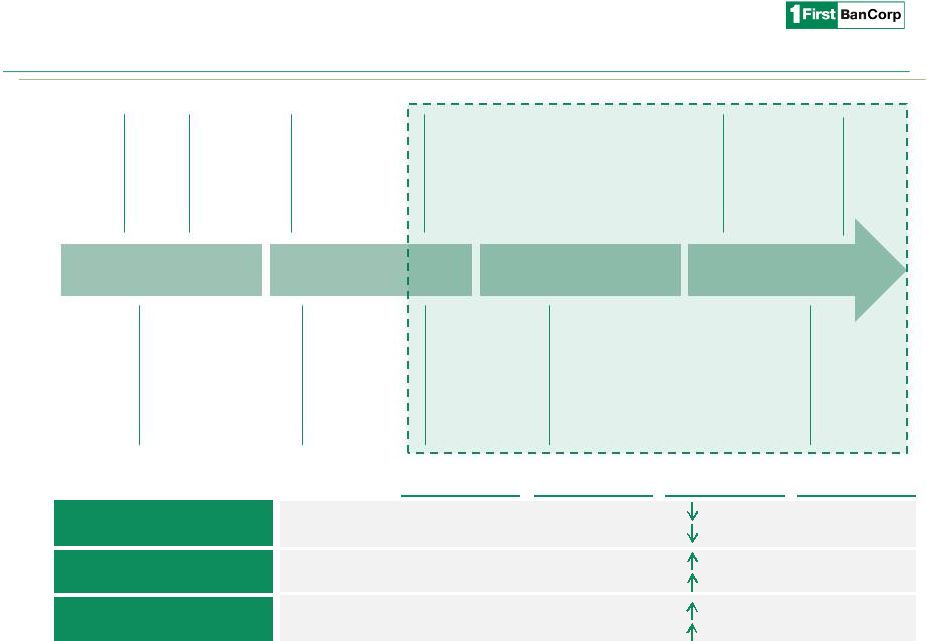

June 2010:

Written

Agreement

with the FED

and Consent

Order with

FDIC

July 2010:

The U.S.

Treasury

exchanged

TARP for

convertible

preferred

August 2010:

Exchange of 89%

Perpetual

Preferred Stock

for Common

February 2011:

Sale of non-

performing

loans with a

book value of

$269 million

Feb-April 2011:

Sale of $330

million of MBS

and $518

million of

performing

residential

mortgages

March 2013:

Sale of non-performing

loans with a book value

of $217.7 million and

entered two separate

agreements for sale of

NPLs with a book value

of $99 million

2010

2011

2013

October 2011:

Conversion of

the shares held

by the U.S.

Treasury into

32.9 million

shares of

common stock

May 2012:

Acquisition of a $406

million portfolio of

FirstBank-branded

credit cards from FIA

June 2013:

Write-off of $66.6

million collateral

pledged to

Lehman, sale of

NPLs with book

value of $203.8

million and $19.2

million of OREO

October 2011:

Private placement

of $525 million in

common stock.

Lead investors

included Thomas H.

Lee & Oaktree

2012

August 2013:

Completed

secondary

offering reducing

ownership

interest of U S

Treasury and PE

Investors |

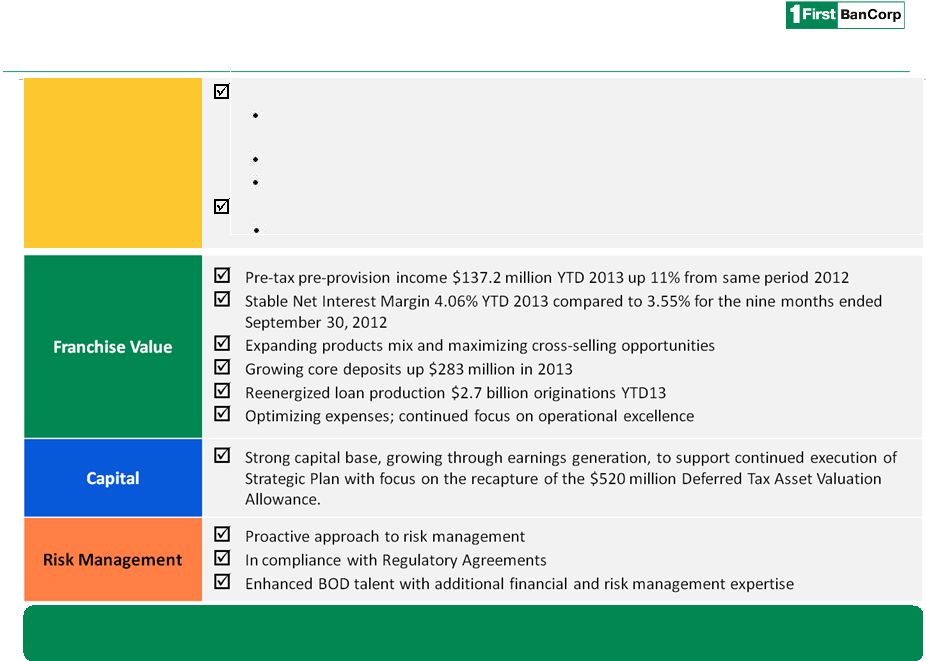

Core Franchise is

Strong Effectively executing Strategic Plan towards Profitability

5

Management focused on continued strengthening of the franchise and

executing on profitability levers

Balance Sheet

Improving risk profile; current focus on organic reduction of NPAs

Executing on opportunities to reduce cost of funds

$797 million brokered CDs maturing over the next six months at an average rate of 0.94%

Completed two bulk sales of adversely classified loans and OREO properties with

total book value of $441 million in first half of 2013

NPAs decreased for the 14

th

consecutive quarter

NPAs down 41% or $512 million YTD 2013 |

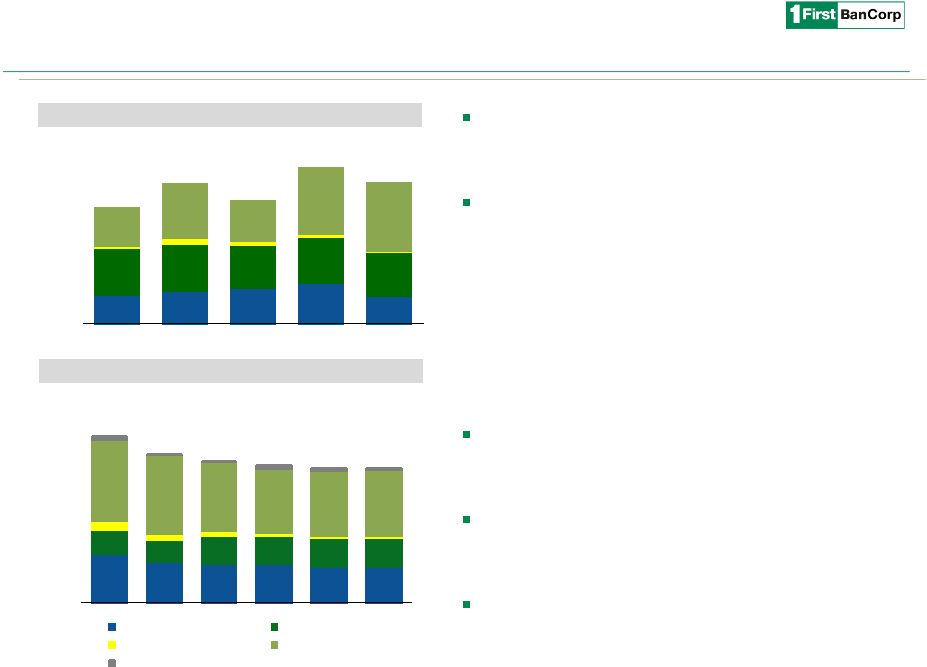

Core deposit

growth strategy continues producing positive results; $1.7 billion since 2009

Florida continues to be a strong funding source

Focus remains on cross-selling opportunities

Cost of deposits, net of brokered CDs, decreased to

0.79%

Reduced reliance on brokered CDs

$3.2 billion (32% of deposits) today vs. $7.4

billion (60%) in 2009

6

Core Deposits

(1)

Total Deposit Composition

Cost of Deposits

(1)

Brokered CDs

32%

Non-interest

bearing

9%

Interest

bearing

59%

3Q 2013

1) Total Deposits excluding Brokered CDs.

Opportunity for Earnings Growth

Successful deposit growth over recent years

Brokered CDs

60%

Non-interest

bearing

6%

Interest

bearing

34%

4Q 2009

2,381

2,477

2,654

2,776

2,828

774

763

915

1,108

1,106

1,505

2,090

2,126

2,077

2,080

448

470

481

529

759

$5,108

$5,800

$6,176

$6,490

$6,773

$0

$1,500

$3,000

$4,500

$6,000

2009

2010

2011

2012

3Q 2013

Retail

Commercial

CDs & IRA

Public Funds

($ in millions)

1.87%

1.56%

1.34%

0.88%

0.79%

0.00%

1.00%

2.00%

3.00%

2009

2010

2011

2012

3Q 2013

Total Deposits, Net of Brokered CDs |

3,417

2,874

2,747

2,714

2,511

2,519

1,716

1,562

2,013

2,020

2,047

2,059

701

428

362

223

195

164

5,822

5,695

4,932

4,604

4,692

4,766

301

16

85

276

238

115

$11,957

$10,575

$10,140

$9,836

$9,683

$9,623

$0

$5,000

$10,000

$15,000

2010

2011

2012

1Q 2013

2Q 2013

3Q 2013

Residential

Consumer & Finance Leases

Construction

Commercial

Loans Held for Sale

187

214

229

262

177

304

305

279

308

290

12

39

28

15

5

252

357

265

431

448

$755

$914

$802

$1,016

$920

$0

$220

$440

$660

$880

$1,100

3Q 2012

4Q 2012

1Q 2013

2Q 2013

3Q 2013

Continued focus on revenue generation through

growth in commercial and consumer book following

recent bulk sale transactions.

Focus on increasing Consumer and Residential

Mortgage market share & rebuilding our Commercial

portfolio.

–

3Q 2013 Consumer originations were strong at

$290 million; and

–

Residential mortgage originations declined in 3Q

2013 primarily driven by an increase in market

interest rates and new housing demand.

Consumer book should benefit from marketing

efforts on credit card portfolio with systems

conversion complete in 3Q 2013.

Increased focus on rebuilding commercial book in PR

and FL representing a $74 million increase for the 3Q

2013.

Continue executing on Florida growth opportunities

7

Loan Portfolio

1) Originations include purchases, refinancings, and draws from existing revolving and

non-revolving commitments. Strong Origination Capabilities

Loan

Originations

(1)

($ in millions)

Rebuilding & replacing to achieve higher yielding portfolio |

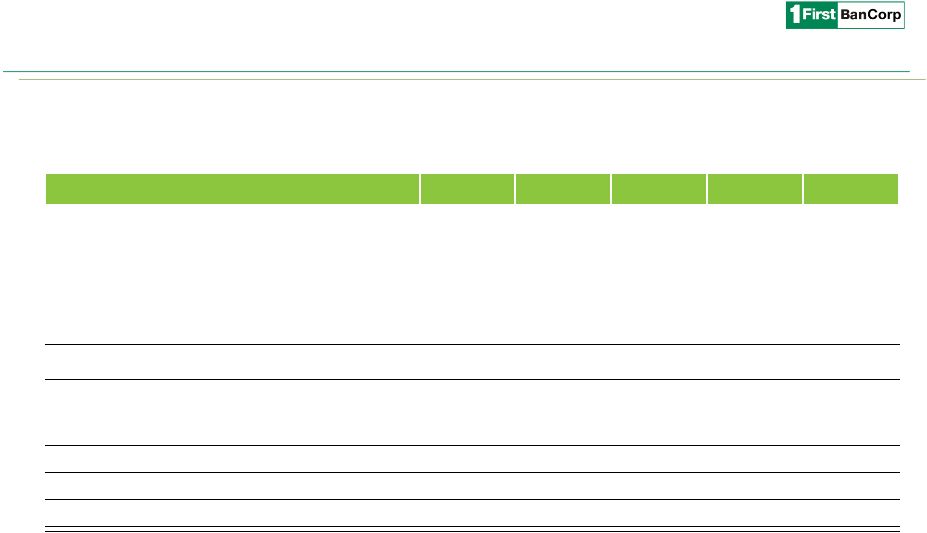

Product

Book Value

Accumulated

Charge-offs

Reserves

Net Carrying

Amount

C&I

$127.6

$46.0

$28.3

57.2%

CRE

114.1

94.8

15.4

47.2%

Construction

157.8

47.7

23.5

65.4%

Total

$399.4

$188.5

$67.2

56.5%

Commercial Non-performing Loans (includes HFS)

Continuing De-risking of the Balance Sheet

8

Net Charge-offs (NCO)

(1)

Non-performing Assets (NPA)

2010

2011

2012

2013

(2)

($ in millions)

(4)

(3)

(5)

63

39

37

25

54

38

35

41

142

118

67

62

186

101

41

7

$445

$295

$180

$134

$0

$200

$400

$600

2010

2011

2012

2013 YTD

Construction

Commercial

Consumer

Residential

1,639

1,551

1,506

1,239

1,233

1,208

1,184

1,138

1,119

1,066

1,008

976

683

506

498

150

150

163

163

172

176

188

194

213

242

251

260

256

151

147

159

148

95

80

$1,790

$1,701

$1,669

$1,562

$1,410

$1,390

$1,377

$1,337

$1,332

$1,308

$1,259

$1,238

$1,087

$752

$726

9.5%

10.0%

9.3%

10.2%

10.2%

9.6%

8.4%

5.7%

$0

$400

$800

$1,200

$1,600

$2,000

1Q

2Q

3Q

4Q

1Q

2Q

3Q

4Q

1Q

2Q

3Q

4Q

1Q

2Q

3Q

NPLs Held for Sale

Repossessed Assets & Other

Loans Held for Investment

NPAs / Assets

Proactively managing asset quality

Transferred $182m of loans to held for sale resulting in NCOs of $36m

Focus remains on organic reductions of nonperforming assets including the

disposition of $227million of HFS and OREO

1) Excludes bulk sales.

2) Excludes $165 million of net charge-offs associated with the bulk sale to CPG in

2010. 3) Excludes $232 million of net-charge offs associated with the bulk

asset sales and transfer of loans in 2013. 4) September 30, 2013.

5) Net Carrying Amount = % of carrying value net of reserves and accumulated charge-offs.

NPAs are down over $1 billion, or 59%, since the peak in 1Q 2010

Recent actions (2013):

Bulk sale of NPAs ($441m book value), resulting in NCOs of $197m

Non-cash charge of $67m due to write-off of securities pledged to

Lehman |

Focus on

Strategic Plan 3Q 2013 Highlights

Net income of $15.9 million, or $0.08 per diluted share, including $3.4 million in

non-recurring expenses related to the secondary stock offering and the conversion

of credit cards. Adjusted net income of $19.3 million, excluding the aforementioned

items. These results were also impacted by a $5.9 million loss in the equity of the

unconsolidated entity and a $3 million increase in the tax reserve for uncertain tax positions.

Net interest margin increased by 16 basis points to 4.20% driven

by reductions in funding costs.

Pre-tax, pre-provision income of $50.9 million up $15.0 million from 2Q 2013.

Strong capital position with total capital ratio, tier 1 and leverage of 16.9%, 15.6% and

11.7%, respectively (2)

Rebuild earnings and de-risk balance sheet

($ in millions, except per share results)

9

1) See reconciliation on page 20.

2) First Bancorp cannot be considered well-capitalized because of the regulatory

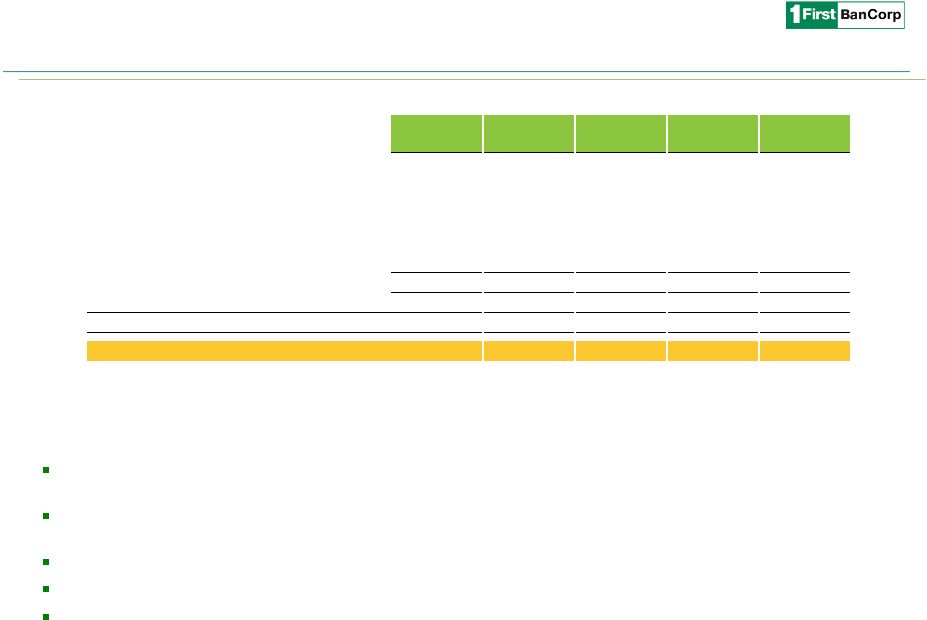

agreements. Income Statement

3Q 2012

4Q 2012

1Q 2013

2Q 2013

3Q 2013

GAAP Net Interest Income

125.5

$

125.6

$

124.5

$

126.9

$

130.9

$

Provision for loan and lease losses

29.0

30.5

111.1

87.5

22.2

Non-interest income

17.3

20.1

19.1

14.3

16.0

Impairment of collateral pledged to Lehman

(66.6)

-

Equity in (losses) gains of unconsolidated entities

(2.2)

(8.3)

(5.5)

0.6

(5.9)

Non-interest expense

91.8

90.9

98.0

111.3

99.2

Pre-tax net income (loss)

19.8

16.0

(71.0)

(123.6)

19.6

Income tax (expense) benefit

(0.8)

(1.5)

(1.6)

1.0

(3.7)

Net income (loss)

19.1

$

14.5

$

(72.6)

$

(122.6)

$

15.9

$

Adjusted

Pre-tax

pre-provision

earnings

(1)

51.4

$

54.5

$

50.5

$

35.9

$

50.9

$

Net Interest Margin, (GAAP) (%)

3.98%

3.91%

3.96%

4.04%

4.20%

Net income (loss) per common share-basic

0.09

$

0.07

$

(0.35)

$

(0.60)

$

0.08

$

|

Opportunity

for Earnings Growth

Targeted strategies for growth

1) Source: Office of the Commissioner of Financial Institutions of Puerto Rico as of 6/30/13

and internal reports. 10

Puerto

Rico

Market

Share

(1)

Puerto Rico

Opportunities for ongoing market share gains

Largest opportunity on deposit products, electronic

banking & transaction services

Growth in selected loan products for balanced risk/return

to manage risk concentration and diversify income

sources

Recently acquired FirstBank-branded credit card portfolio

Diversifies revenue stream and loan portfolio

composition

Opportunity to broaden and deepen relationships

SE Florida

Continue focus in core deposit growth, commercial and

transaction banking and conforming residential

mortgages

Virgin Islands

Current

Market

Share

Jun-13

Rank

Auto / leasing

19%

2

Commercial

20%

2

Credit cards

18%

2

Mortgage

originations

15%

3

Personal

8%

4

ACH Transactions

11%

6

ATM Terminals

8%

3

Debit Cards

7%

4

POS Terminals

11%

2

Branches

12%

4

Deposits

10%

4

Expansion prospects in Florida given long-term

demographic trends

Solidify leadership position by further increasing customer

share of wallet |

Opportunity for

Earnings Growth 11

Path to improved profitability

Net Interest

Income

Improvement

Cost of funds

reduction

$797 million brokered

CDs maturing over the

next six months at an

average rate of 0.94%

Cash liquidity re-

investment

$700MM currently

yielding 28 bps

Replacement of NPLs

for performing loans

Additional loan

growth as economy

recovers across our

geographies

Provision

Reduction

Currently 120bps of

loans (excluding

bulk sales)

2000-2008

weighted average

provision of 98bps

on loans

Deposit fee income

from expansion of

transaction deposit base

Non-interest bearing

represents only 9% of

deposit base

POS Terminals, Debit

cards, ACH transactions,

ATM Terminals

Credit costs of

$37MM

(1)

for the first

9 months of 2013

compared to 2008

annual expense of

$23MM

Fee Income

Opportunities

Operating Expense

Reduction

Long-term Efficiency Ratio Target of 55%

1) Represents net loss on REO operations and professional fees from collections, appraisals

and other credit related fees. Market share

expansion of

transaction processing

FDIC Cost reduction

with credit profile

improvement ($15 –

20 million annually) |

Tier 1 Common of $1.2bn or 12.6% and Tier 1 capital of 15.6% Tangible

Book Value of $1.1bn or $5.32 / share

Deferred

Tax

Asset

Valuation

Allowance

of

$520m;

Adjusted

Tangible

Book

Value

(3)

of

$7.83

/

share

Key Investment Highlights

12

As of September 30, 2013.

1) See reconciliation to net income on page 20.

2) See reconciliation to total equity on page 21.

3) Assuming 100% reversal of Deferred Tax Asset Valuation Allowance of $520m; shares

outstanding of 207m. See reconciliation to adjusted tangible book value on page 21.

Improving core operating performance

Healthy capital levels

Continuing de-risking of the balance sheet

Opportunity for revenue expansion and earnings growth

Total NPAs declined for the 14 consecutive quarter, down over $1bn or 59%

since peak in 1Q 2010

Focus remains on organic reductions of non-performing assets

th

Average pre-tax pre-provision income for the last five quarters of approximately $49m NIM expanded 151 bps since 2009 to 4.20% in 3Q 2013

Stabilization of non-interest expenses; expected reduction in credit-related expense

(1)

(2)

Strong loan origination capabilities ($2.7bn YTD 2013) Potential for NIM expansion through reduction in cost of deposits and replacement of

performing for NPLs

Expected reduction in credit-related and other expenses (e.g., FDIC insurance) Increasing market share in fee generating products and services, consumer and mortgage loan

originations

Opportunity for commercial loan growth in SE Florida Long-term potential for value

creation from consolidation in Puerto Rico |

This Page Intentionally Left Blank |

Appendix

|

Outlook on

economic growth projections in PR –

GNP: -0.03% for FY 2013 and -0.76% for FY 2014 (PR

Planning

Board)

–

Real GDP: 1.0%

for 2013 and 1.9% for 2014 (Global Insight)

August 2013 unemployment rate of 13.9% compared to August

2012 of 14.0% (United States Department of Labor. Bureau of

Labor Statistics, Household Survey. Seasonally Adjusted.) Increased

tourist activity in first eleven months of fiscal 2013 –

Hotel occupancy rate of 72.1% for 2013 YTD compared to

average occupancy rate of 69.6% during the same period

2012 (P.R. Tourism Company).

Evaluation of priority infrastructure projects moving forward

Government targeting 65% reduction in fiscal 2014 budget

deficit

Act 154 excise tax fixed to its original level of 4% for five years

commencing on July 1, 2013

Corporate income tax rate increased from 30% to 39%

Tax of approximately 0.5% levied on gross income

Pension plan reform

Privatization of Luis Muñoz Marín International Airport

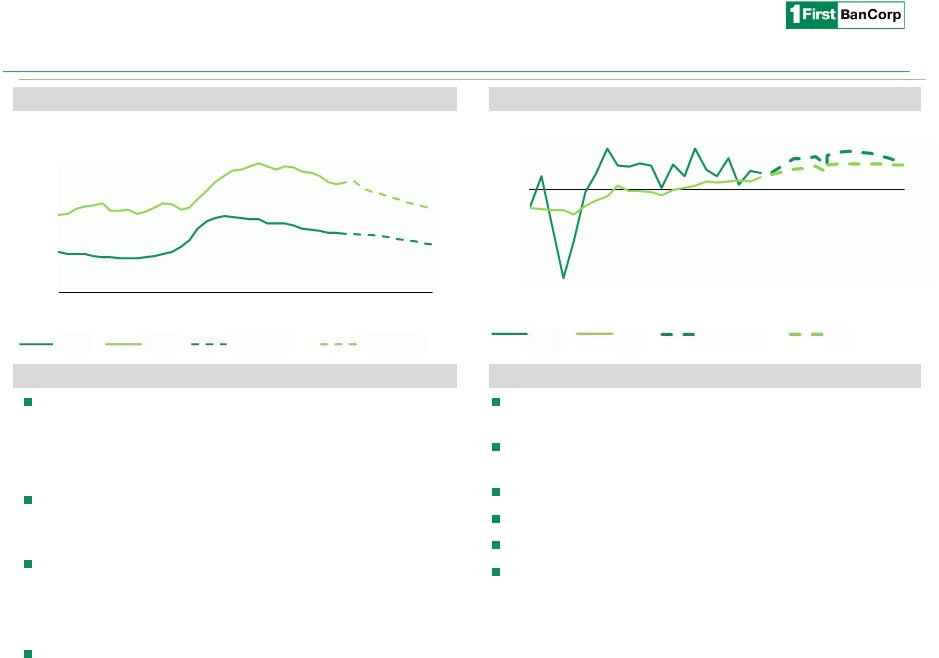

Puerto Rico economic update

Unemployment

(1)

Economic Activity

Recent Changes

15

Real GDP

(1)

1) Source: Global Insight’s Comparative World Overview, Quarterly data.

10.0%

10.5%

5.3%

6.1%

2.4%

3.0%

1.2%

1.6%

(2.1%)

(3.7%)

PR has lagged the US recovery coming out of the credit crisis

–

5.0%

10.0%

15.0%

20.0%

2005

2007

2009

2011

2013

2015

U.S.

P.R.

U.S. projected

P.R. projected

(10.0%)

(5.0%)

–

5.0%

2008

2010

2012

2014

2016

U.S.

P.R.

U.S. projected

P.R. projected |

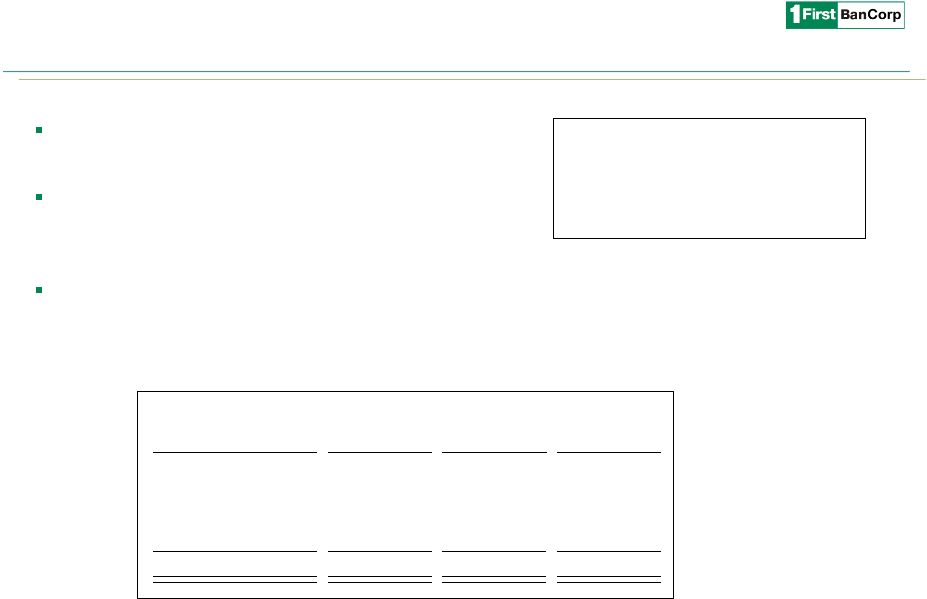

Puerto Rico

Government Exposure 16

As of September 30, 2013

Total asset exposure to the Puerto Rico Government

as of September 30, 2013 was just over $395 million

In addition, there is $199 million of indirect exposure

to the Tourism Development Fund supporting hotel

projects.

Investment Portfolio

71.0

$

Central Government

48.1

Public Corporations

79.6

Municipalities

199.0

Time

Deposits

Transaction

Accounts

Total

Federal Funds

-

$

12.9

$

12.9

$

Municipalities

35.4

104.6

140.0

Public Agencies

5.0

184.5

189.4

Public Corporations

240.1

1.5

241.6

Total

280.4

$

303.5

$

584.0

$

Total Government Deposits as of September 30, 2013 were $584 million.

($ in millions) |

Stock

Profile 17

Trading Symbol:

•

FBP

Exchange:

•

NYSE

Share

Price

(11/8/13):

•

$6.28

Shares

Outstanding

(as

of

September 30,

2013):

•

207,042,785

Market Capitalization

(11/8/13):

•

$1.30bn

1 Yr. Average Daily

Volume:

•

654,555

Price

(11/8/13)

to

Tangible

Book

(9/30/13):

•

1.18x

Price

(11/8/13)

to

Adjusted

Tangible Book

(1)

(9/30/13):

•

0.80x

5% or more Beneficial Ownership

Beneficial Owner

Amount

Percent of

Class

Entities affiliated with Thomas H. Lee

Partners, L.P.

41,854,770

20.2%

Entities managed by Oaktree Capital

Management, L.P.

41,854,769

20.2

United States Department of the

Treasury

(2)

20,996,340

10.1

Wellington Management Company, LLP

19,887,328

9.6

1) Assuming 100% reversal of Deferred Tax Valuation Allowance of $520m; shares outstanding of

207m. 2) Includes

the U.S. Treasury warrant that entitles it to purchase up to 1,285,899 shares of Common Stock at an exercise price of $3.29 per share, as adjusted as a result of the

issuance of shares of Common Stock in the Corporation’s $525m private placement of Common

Stock completed in October 2011. The exercise price and the number of shares issuable

upon exercise of the warrant are subject to further adjustments under certain circumstances to prevent dilution. The warrant has a 10-year term from its issue date and is

exercisable in whole or in part at any time. |

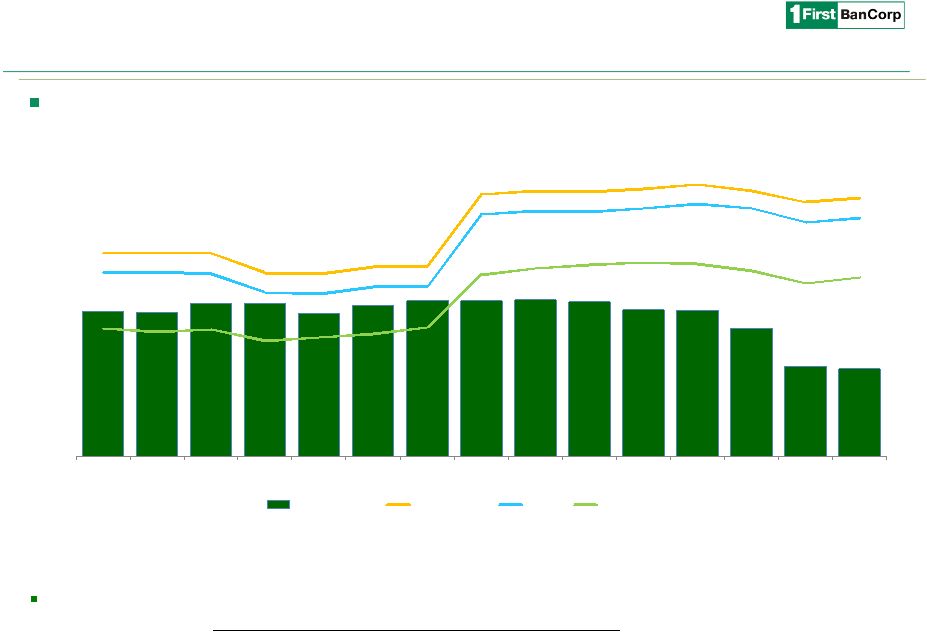

Capital Position

and Asset Quality 18

Asset

quality

remains

our

number

one

focus,

while

preserving

and

growing

capital

Strong capital position: Total capital, Tier 1 capital and Leverage ratios of the

Corporation of 16.9%, 15.6% and 11.7%,

respectively.

$520

million

Deferred

Tax

Asset

Valuation

Allowance.

9.5%

9.4%

10.0%

10.0%

9.3%

9.8%

10.2%

10.2%

10.2%

10.1%

9.6%

9.5%

8.4%

5.9%

5.7%

13.3%

13.4%

13.3%

12.0%

12.0%

12.4%

12.4%

17.1%

17.4%

17.3%

17.5%

17.8%

17.4%

16.6%

16.9%

12.0%

12.1%

12.0%

10.7%

10.7%

11.1%

11.1%

15.8%

16.0%

16.0%

16.2%

16.5%

16.2%

15.3%

15.6%

8.4%

8.1%

8.3%

7.6%

7.8%

8.0%

8.4%

11.9%

12.3%

12.5%

12.7%

12.6%

12.1%

11.3%

11.7%

0.0%

6.0%

12.0%

18.0%

Q1 '10

Q2 '10

Q3 '10

Q4 '10

Q1 '11

Q2 '11

Q3 '11

Q4 '11

Q1 '12

Q2 '12

Q3 '12

Q4 '12

Q1 '13

Q2 '13

Q3 '13

NPAs / Assets

Total Capital

Tier 1

Leverage

Core franchise is strong |

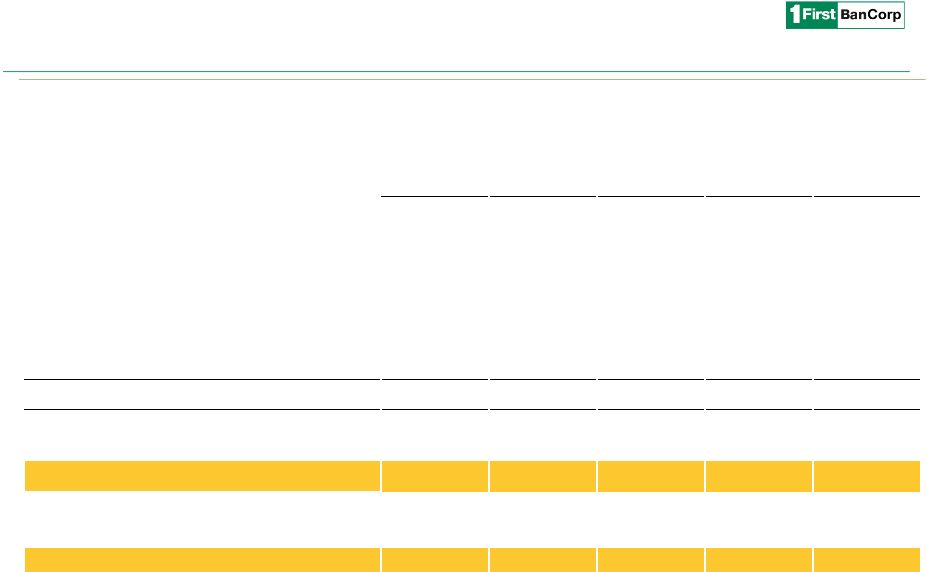

Non-performing Assets

($ in millions)

1) Collateral pledged with Lehman Brothers Special Financing, Inc.

19

2009

2010

2011

2012

9/30/2013

Non-performing loans held for investment:

Residential mortgage

441,642

$

392,134

$

338,208

$

313,626

$

142,002

$

Commercial mortgage

196,535

217,165

240,414

214,780

127,374

Commercial & industrial

241,316

317,243

270,171

230,090

127,584

Construction

634,329

263,056

250,022

178,190

64,241

Consumer & finance leases

50,041

49,391

39,547

38,875

37,184

Total non-performing loans held for investment

1,563,863

1,238,989

1,138,362

975,561

498,385

OREO

69,304

84,897

114,292

185,764

133,284

Other repossessed property

12,898

14,023

15,392

10,107

14,125

Other assets

(1)

64,543

64,543

64,543

64,543

-

Total non-performing assets, excluding loans

held for sale 1,710,608

1,402,452

1,332,589

1,235,975

645,794

Non-performing loans held for sale

-

159,321

4,764

2,243

80,234

Total non-performing assets

1,710,608

$

1,561,773

$

1,337,353

$

1,238,218

$

726,028

$ |

Adjusted

Pre-tax, Pre-provision Income Reconciliation 20

($ in thousands)

3Q 2012

4Q 2012

1Q 2013

2Q 2013

3Q 2013

Income (loss) before income taxes

19,834

$

16,028

$

(71,011)

$

(123,562)

$

19,616

$

Add: Provision for loan and lease losses

28,952

30,466

111,123

87,464

22,195

Add: Net loss on investments and impairments

547

69

117

42

-

Less: Unrealized gain (loss) on derivatives instruments and

liabilities measured at fair value

(170)

(432)

(400)

(708)

(232)

Add: Bulk sales related expenses and other professional fees related

to the terminated preferred stock exchange offer

-

-

5,096

3,198

-

Add: Loss on certain OREO properties sold as part of the bulk sale

of non-performing residential mortgage assets

-

-

-

1,879

-

Add: Secondary offering costs

-

-

-

-

1,669

Add: Credit card processing platform conversion costs

-

-

-

-

1,715

Add: National gross tax receipts tax corresponding to Q1 2013

recorded during Q2 2013 after enactment

-

-

-

1,656

-

Add: write-off of collateral pledged to Lehman

-

-

-

66,574

-

Add: Equity in losses (earnings) of unconsolidated entities

2,199

8,330

5,538

(648)

5,908

Adjusted Pre-tax, pre-provision income

51,362

$

54,461

$

50,463

$

35,895

$

50,871

$

Quarter Ended |

Tangible Book Value

Per Share Reconciliation 21

($ in millions, except for per share data)

3Q 2012

4Q 2012

1Q 2013

2Q 2013

3Q 2013

Tangible equity:

Total equity - GAAP

1,484

$

1,485

$

1,404

$

1,222

$

1,221

$

Preferred equity

(63)

(63)

(63)

(63)

(63)

Goodwill

(28)

(28)

(28)

(28)

(28)

Purchased credit card relationship

(24)

(24)

(23)

(22)

(21)

Core deposit intangible

(10)

(9)

(9)

(8)

(8)

Tangible common equity

1,359

$

1,361

$

1,282

$

1,101

$

1,101

$

Common shares outstanding

206

206

206

207

207

Tangible book value per common share

6.59

$

6.60

$

6.21

$

5.32

$

5.32

$

Deferred tax valuation allowance

360

$

360

$

384

$

523

$

520

$

Deferred tax valuation allowance per share

1.75

1.75

1.86

2.53

2.51

Adjusted tangible book value per share

8.34

$

8.34

$

8.08

$

7.85

$

7.83

$

|

|