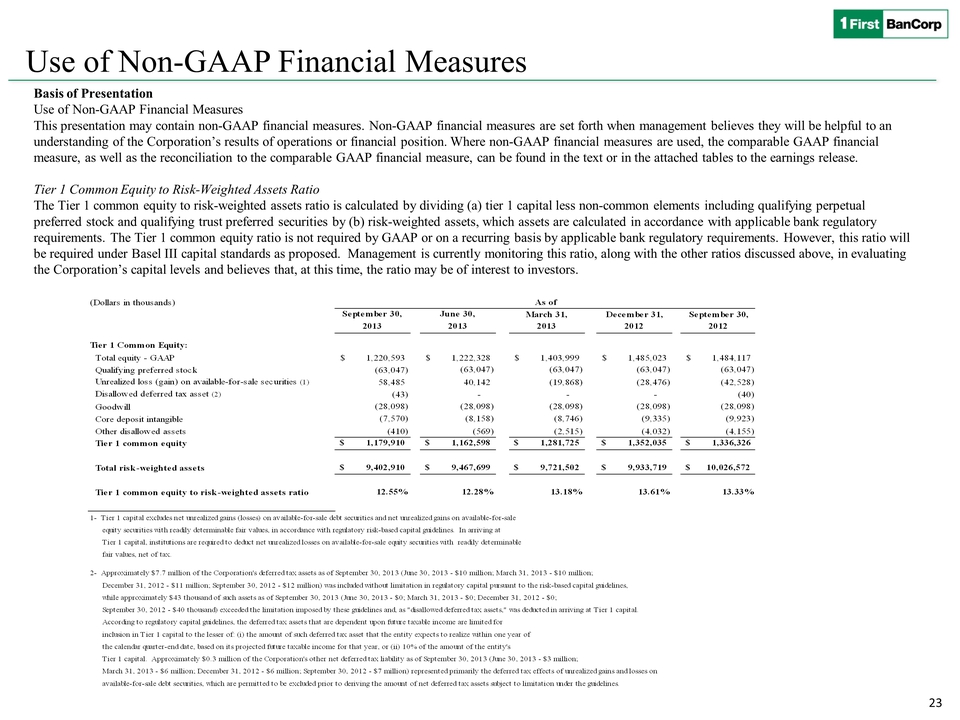

Exhibit 99.1

First

BanCorp. Announces Earnings for the Quarter Ended September 30, 2013

2013

Third Quarter Highlights and Comparison with Second Quarter

SAN JUAN, Puerto Rico--(BUSINESS WIRE)--October 23, 2013--First BanCorp.

(NYSE: FBP):

-

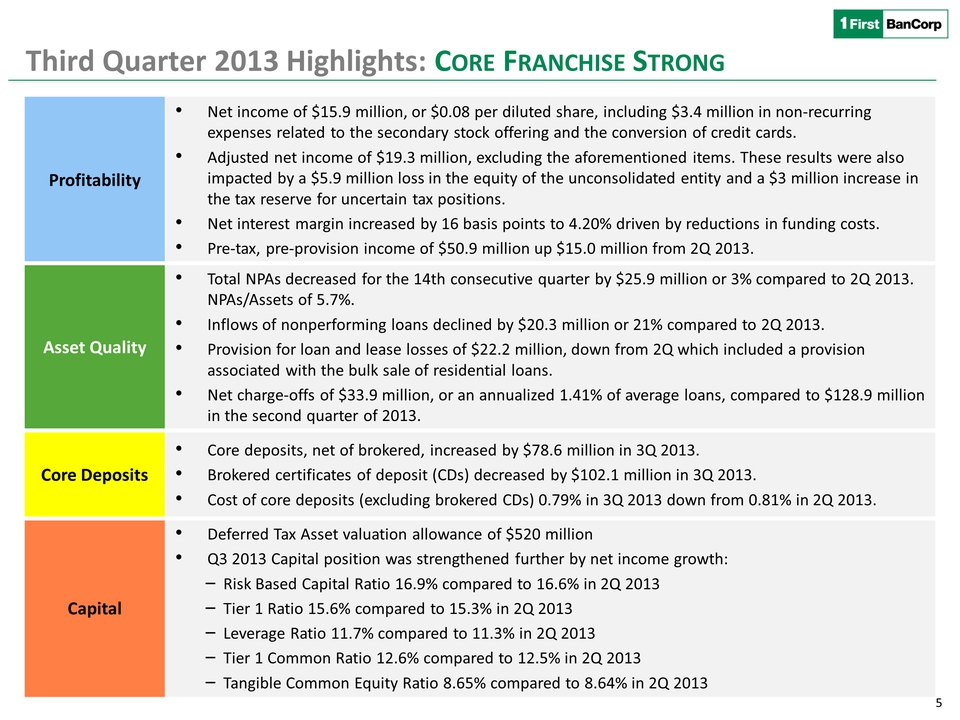

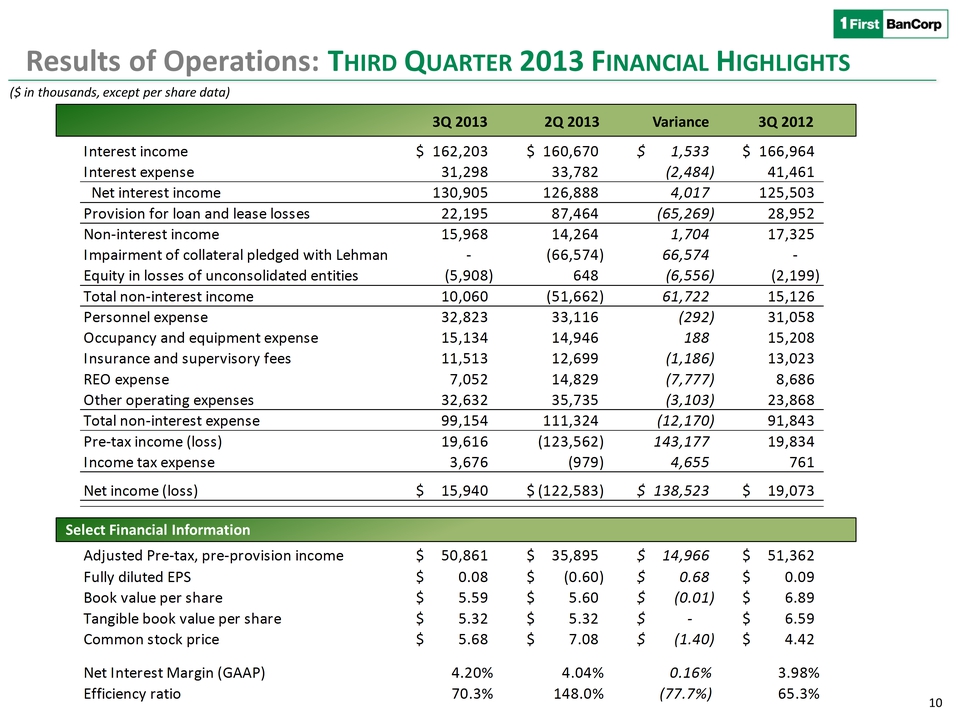

Net income of $15.9 million, or $0.08 per diluted share, compared to a

net loss of $122.6 million, or $0.60 per diluted share, for the second

quarter of 2013. The results for the second quarter included a $72.9

million loss on the bulk sale of non-performing residential assets and

a $66.6 million loss related to the write-off of assets pledged as

collateral to Lehman Brothers, Inc. (“Lehman”).

-

Adjusted net income of $19.3 million, or $0.09 per diluted share,

excluding $1.7 million in costs associated with the secondary offering

of the Corporation’s common stock by certain of the existing

stockholders and $1.7 million in costs associated with the conversion

of the credit card processing platform, compared to an adjusted net

income of $16.8 million, or $0.08 per diluted share, for the second

quarter of 2013, excluding the effects of the bulk sale of

non-performing residential assets and the Lehman collateral write-off.

-

Pre-tax, pre-provision income of $50.9 million, compared to $35.9

million for the second quarter of 2013.

-

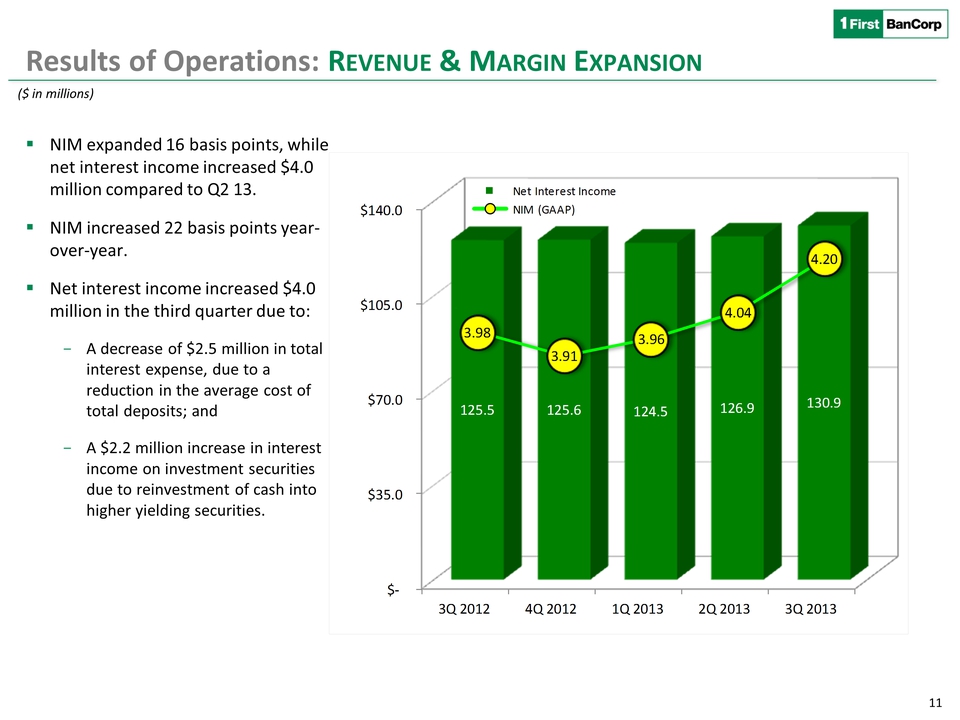

Adjusted net interest income, excluding fair value adjustments of

derivative instruments, increased by $4.5 million to $130.7 million,

and the related adjusted net interest margin expanded to 4.19% from

4.02% in the second quarter of 2013.

-

Non-interest income of $10.1 million, compared to a non-interest loss

of $51.7 million for the second quarter of 2013. The non-interest

income for the third quarter was adversely impacted by the equity in

loss of unconsolidated entity of $5.9 million. The non-interest loss

for the second quarter included the $66.6 million impact of the Lehman

collateral write-off.

-

Non-interest expenses of $99.2 million, compared to $111.3 million for

the second quarter of 2013. Adjusted non-interest expenses of $95.8

million, excluding costs associated with the secondary offering and

the conversion of the credit card processing platform, compared to

adjusted non-interest expenses of $104.7 million for the second

quarter of 2013, excluding $5.0 million of expenses specifically

related to the bulk sale of non-performing residential assets and the

$1.7 million retroactive effect of the national gross receipts tax

that corresponded to the first quarter of 2013.

-

Credit quality remained stable:

-

Non-performing assets decreased for the 14th

consecutive quarter, declining by $25.9 million, or 3%, from the

second quarter of 2013 to $726.0 million.

-

Non-performing loans, including non-performing loans held for

sale, declined by $22.5 million, or 4%, from the second quarter of

2013 to $578.6 million.

-

Inflows of non-performing loans held for investment declined by

$20.3 million, or 21%, compared to inflows for the second quarter

of 2013.

-

Provision for loan and lease losses of $22.2 million compared to

$87.5 million in the second quarter of 2013. The results for the

second quarter included a provision of $67.9 million associated

with the bulk sale of non-performing residential assets.

-

Net charge-offs of $33.9 million, or an annualized 1.41% of

average loans, compared to $128.9 million in the second quarter of

2013. Net charge-offs in the second quarter included $98.0 million

related to the bulk sale of non-performing residential assets.

-

Income tax expense of $3.7 million, compared to an income tax benefit

of $1.0 million for the second quarter of 2013, mainly related to the

increase in reserves for uncertain tax positions.

-

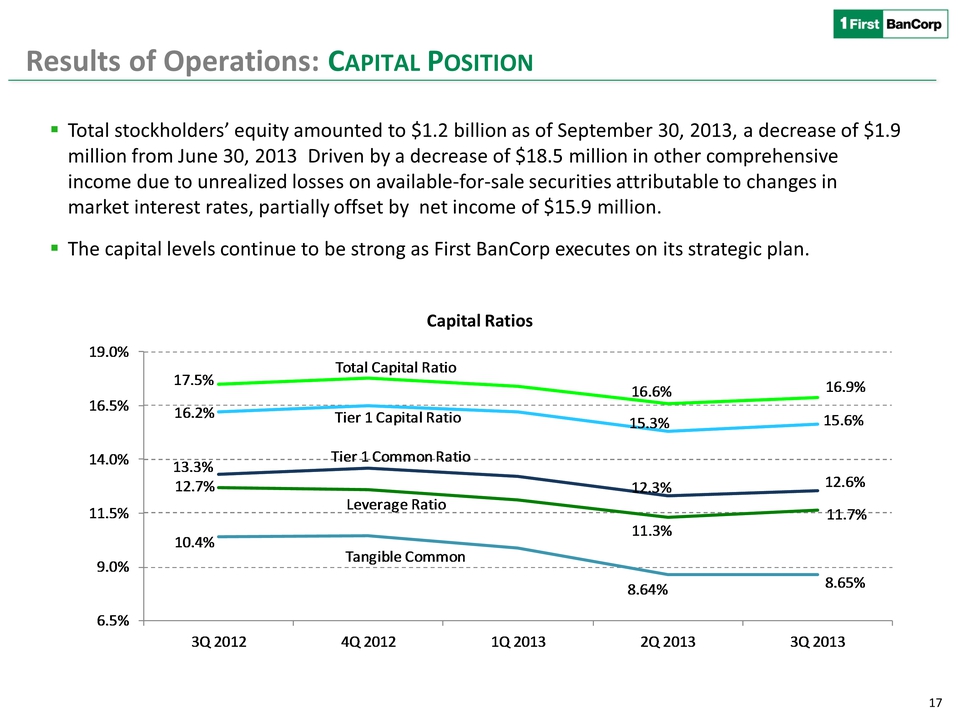

Total capital, Tier 1 capital, and leverage ratios of 16.89%, 15.61%,

and 11.65%, respectively, as of September 30, 2013. Common equity Tier

1 capital ratio of 12.55% and Tangible common equity ratio of 8.65% as

of September 30, 2013.

-

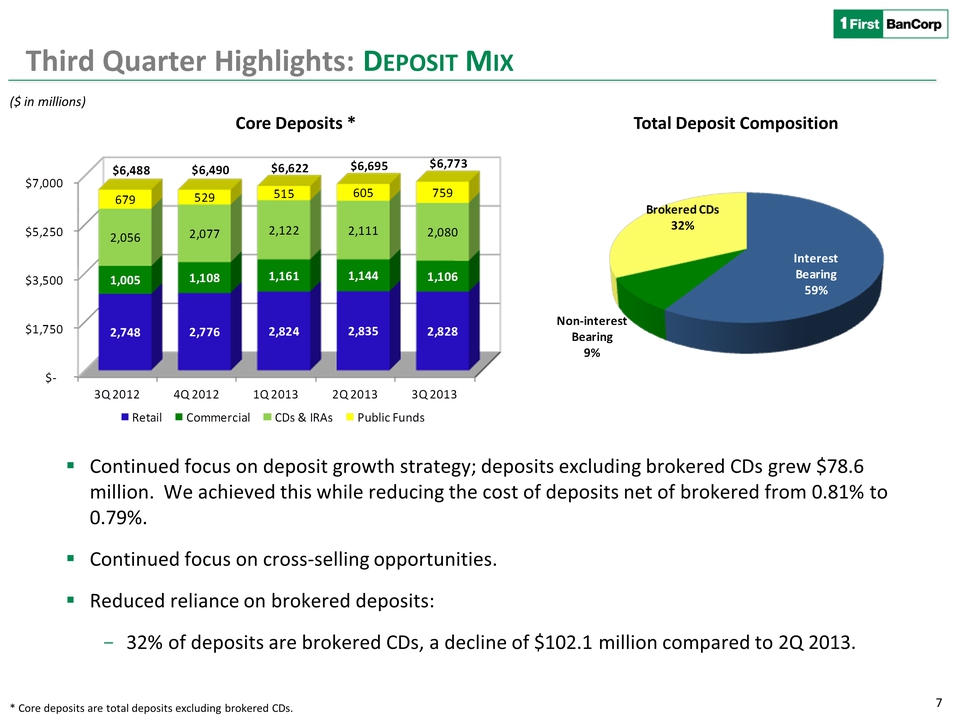

Non-brokered deposits increased by $78.6 million to $6.8 billion as of

September 30, 2013 from $6.7 billion as of June 30, 2013.

-

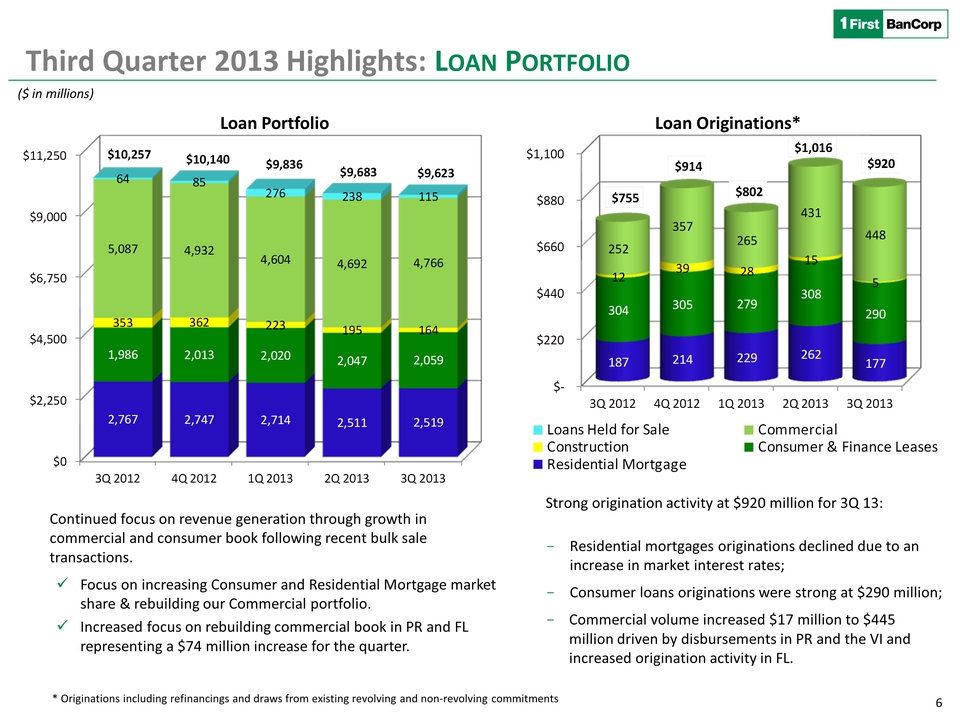

Total loan originations (excluding credit cards utilization activity)

of $836.7 million for the third quarter of 2013.

First BanCorp. (the “Corporation”) (NYSE: FBP), the bank holding company

for FirstBank Puerto Rico (“FirstBank” or “the Bank”), today reported

net income of $15.9 million for the third quarter of 2013, or $0.08 per

diluted share, compared to a net loss of $122.6 million, or $0.60 per

diluted share, for the second quarter of 2013 and net income of $19.1

million, or $0.09 per diluted share, for the third quarter of 2012.

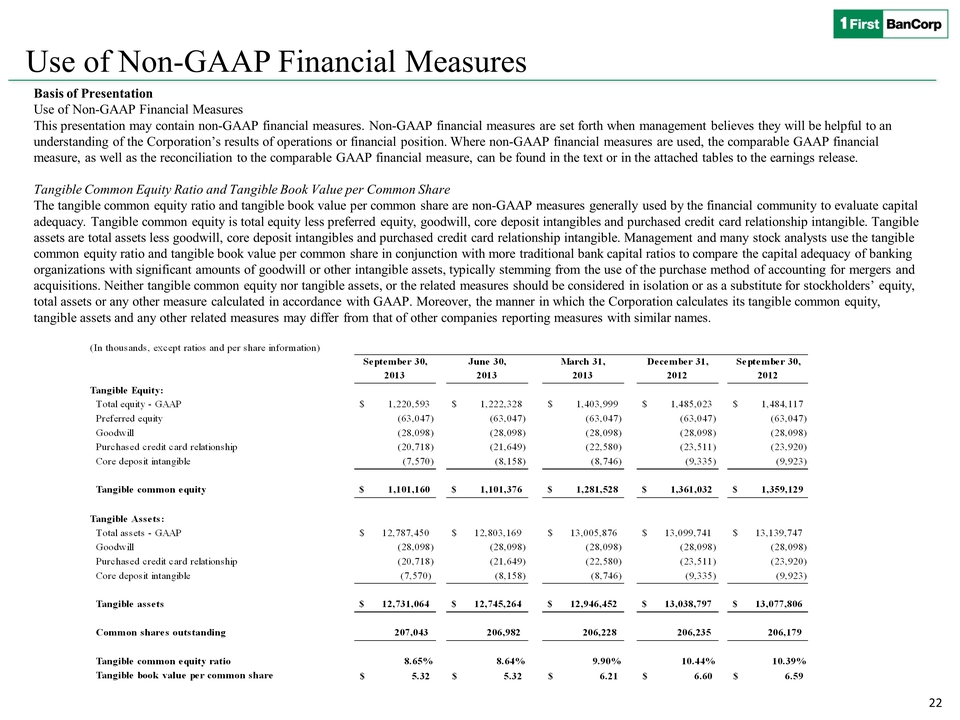

This press release includes certain non-GAAP financial measures,

including adjusted pre-tax, pre-provision income, adjusted net interest

income and margin, certain capital ratios, non-interest income adjusted

to exclude the Lehman collateral write-off and equity in (loss) earnings

of unconsolidated entity, and certain other financial measures adjusted

to exclude the effects of the secondary offering costs, the credit card

processing platform conversion costs, and the bulk sale of

non-performing residential assets, and should be read in conjunction

with the accompanying tables (Exhibit A), which are an integral part of

this press release.

Aurelio Alemán, President and Chief Executive Officer of First BanCorp.,

commented, “The results for the third quarter continue to show

improvements associated with the execution of our business strategies.

Net income for the quarter amounted to $15.9 million, including $3.4

million in non-recurring expenses related to the secondary stock

offering and the conversion of the credit card processing platform, both

completed during the quarter. Excluding these items, net income amounted

to $19.3 million. Furthermore, the results were impacted by a $5.9

million loss in the equity of the unconsolidated entity to which we sold

loans in 2011 and a $3 million increase in the tax reserve for uncertain

tax positions. The quarter showed improvement in pre-tax pre-provision

income, which increased to $50 million, expansion of the net interest

margin to 4.19% and growth of $78.6 million in non-brokered deposits and

$63 million in loans held in portfolio. Loan originations were

approximately $836 million for the quarter.

Mr. Alemán continued, “Despite the negative market headwinds, we have

stayed the course in the execution of our strategies. We are pleased

with the steps taken by the Puerto Rico government with regard to the

fiscal situation and their efforts to address investor concerns and

remain unwavering in our commitment to the Puerto Rico market. We will

continue to focus on enhancing franchise value through the organic

reduction of nonperforming loans and earnings generation.”

RECENT EVENTS

Secondary Offering

On August 16, 2013, a secondary offering of the Corporation’s common

stock was completed by certain of the Corporation’s existing

stockholders. The United States Department of the Treasury (“Treasury”)

sold 12 million shares of common stock, funds affiliated with Thomas H.

Lee Partners (“THL”) sold 8 million shares of common stock, and funds

managed by Oaktree Capital Management, L.P. (“Oaktree”) sold 8 million

shares of common stock. On September 11, 2013, the underwriters

exercised their option to purchase an additional 2.9 million shares of

common stock from the selling stockholders. The Corporation did not

receive any proceeds from the offering. Non-interest expenses for the

third quarter of 2013 included approximately $1.7 million in costs

associated with the secondary offering, including $1.1 million paid by

the Corporation for underwriting discounts and commissions. As of

September 30, 2013, each of THL and Oaktree owns 20.22% of the

Corporation’s outstanding common stock and the U.S. Treasury owns 9.51%

of such stock.

ADJUSTED PRE-TAX, PRE-PROVISION INCOME TRENDS

One metric that management believes is useful in analyzing performance

is the level of earnings adjusted to exclude tax expense, the provision

for loan and lease losses, securities gains or losses, fair value

adjustments on derivatives measured at fair value and equity in earnings

or loss of unconsolidated entity, which is a non-GAAP financial measure.

In addition, from time to time, earnings are adjusted also for items

judged by management to be outside of ordinary banking activities and/or

for items that, while these may be associated with ordinary banking

activities, are so unusually large that management believes that a

complete analysis of the Corporation’s performance requires

consideration also of results that exclude such amounts (for additional

information about these non-GAAP financial measure, see “Adjusted

Pre-Tax, Pre-Provision Income” in “Basis of Presentation”).

The following table shows adjusted pre-tax, pre-provision income of

$50.9 million in the third quarter of 2013, up $15.0 million from the

prior quarter:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(Dollars in thousands)

|

|

Quarter Ended

|

|

|

|

September 30,

|

|

June 30,

|

|

March 31,

|

|

December 31,

|

|

September 30,

|

|

|

|

2013

|

|

2013

|

|

2013

|

|

2012

|

|

2012

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Income (loss) before income taxes

|

|

$

|

19,616

|

|

|

$

|

(123,562

|

)

|

|

$

|

(71,011

|

)

|

|

$

|

16,028

|

|

|

$

|

19,834

|

|

|

Add: Provision for loan and lease losses

|

|

|

22,195

|

|

|

|

87,464

|

|

|

|

111,123

|

|

|

|

30,466

|

|

|

|

28,952

|

|

|

Add: Net loss on investments and impairments

|

|

|

-

|

|

|

|

42

|

|

|

|

117

|

|

|

|

69

|

|

|

|

547

|

|

|

Less: Unrealized gain on derivative instruments and liabilities

measured at fair value

|

|

|

(232

|

)

|

|

|

(708

|

)

|

|

|

(400

|

)

|

|

|

(432

|

)

|

|

|

(170

|

)

|

|

Add: Bulk sales related expenses and other professional fees

related to the terminated preferred stock exchange offer

|

|

|

-

|

|

|

|

3,198

|

|

|

|

5,096

|

|

|

|

-

|

|

|

|

-

|

|

|

Add: Loss on certain OREO properties sold as part of the bulk sale

of non-performing residential mortgage assets

|

|

|

-

|

|

|

|

1,879

|

|

|

|

-

|

|

|

|

-

|

|

|

|

-

|

|

|

Add: Secondary offering costs

|

|

|

1,669

|

|

|

|

-

|

|

|

|

-

|

|

|

|

-

|

|

|

|

-

|

|

|

Add: Credit card processing platform conversion costs

|

|

|

1,715

|

|

|

|

-

|

|

|

|

-

|

|

|

|

-

|

|

|

|

-

|

|

|

Add: National gross receipt tax (1)

|

|

|

-

|

|

|

|

1,656

|

|

|

|

-

|

|

|

|

-

|

|

|

|

-

|

|

|

Add: Write-off collateral pledged to Lehman

|

|

|

-

|

|

|

|

66,574

|

|

|

|

-

|

|

|

|

-

|

|

|

|

-

|

|

|

Add/Less: Equity in loss (earnings) of unconsolidated entity

|

|

|

5,908

|

|

|

|

(648

|

)

|

|

|

5,538

|

|

|

|

8,330

|

|

|

|

2,199

|

|

|

Adjusted pre-tax, pre-provision income (2)

|

|

$

|

50,871

|

|

|

$

|

35,895

|

|

|

$

|

50,463

|

|

|

$

|

54,461

|

|

|

$

|

51,362

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Change from most recent prior quarter-amount

|

|

$

|

14,976

|

|

|

$

|

(14,568

|

)

|

|

$

|

(3,998

|

)

|

|

$

|

3,099

|

|

|

$

|

13,449

|

|

|

Change from most recent prior quarter-percentage

|

|

|

41.7

|

%

|

|

|

-28.9

|

%

|

|

|

-7.3

|

%

|

|

|

6.0

|

%

|

|

|

35.5

|

%

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(1) Represents the impact of the national gross receipts tax

corresponding to the first quarter of 2013, recorded during the

second quarter after enactment.

|

|

(2) See "Basis of Presentation" for definition.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

The increase in adjusted pre-tax, pre-provision income from the 2013

second quarter primarily reflected:

-

An $8.9 million decrease in adjusted non-interest expenses mainly due

to lower losses on other real estate owned (“OREO”) operations. This

reduction reflects a $4.9 million decrease in write-downs on OREO

properties, as the prior quarter was impacted by a $5.3 million charge

against the value of certain commercial OREO properties in the Virgin

Islands, and a $1.7 million decrease in operating costs of the

Corporation’s OREO properties. See Non-Interest Expenses

section below for additional information.

Adjusted non-interest expenses exclude costs associated with the

secondary offering and the conversion of the credit card processing

platform completed in the third quarter as well as expenses related to

the bulk sale of non-performing residential assets completed in the

second quarter, and the impact of the national gross receipts tax that

corresponded to the first quarter of 2013 but was recorded in the second

quarter after enactment of the 2013 Tax Burden Adjustment and

Redistribution Act (“Act 40”). See Basis of Presentation

section below for reconciliation of this non-GAAP financial measure to

the corresponding GAAP measure.

-

A $4.5 million increase in net interest income, excluding fair value

adjustments, mainly due to further reductions in the cost of funding

as well as the decrease in mortgage-backed securities (“MBS”)

prepayment activity levels that resulted in a higher yield on U.S.

agency MBS held by the Corporation. See Net Interest Income discussion

below for additional information.

-

A $1.7 million increase in adjusted non-interest income reflecting the

adverse impact in the previous quarter of a $3.4 million loss related

to the restructuring of a commercial mortgage loan held for sale in

which the Corporation entered into an agreement to receive foreclosed

real estate in partial satisfaction of a debt arrangement and modified

the terms of the remaining balance. This was partially offset by a

$1.3 million decrease in revenues from the mortgage banking business.

Adjusted non-interest income excludes the Lehman collateral write-off

recorded in the second quarter and equity in earnings (loss) of

unconsolidated entity. See Basis of Presentation section below

for reconciliation of this non-GAAP financial measure to the

corresponding GAAP measure.

NET INTEREST INCOME

Net interest income, excluding fair value adjustments on derivatives and

financial liabilities measured at fair value (“valuations”), and net

interest income on a tax-equivalent basis are non-GAAP measures. (See “Basis

of Presentation – Net Interest Income, Excluding Valuations and on a

Tax-Equivalent Basis” below for additional information.)

The following table reconciles net interest income in accordance with

GAAP to net interest income, excluding valuations, and net interest

income on a tax-equivalent basis. The table also reconciles net interest

spread and net interest margin on a GAAP basis to these items excluding

valuations and on a tax-equivalent basis.

|

(Dollars in thousands)

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Quarter Ended

|

|

|

|

September 30,

|

|

June 30,

|

|

March 31,

|

|

December 31,

|

|

September 30,

|

|

|

|

2013

|

|

2013

|

|

2013

|

|

2012

|

|

2012

|

|

Net Interest Income

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Interest Income - GAAP

|

|

$

|

162,203

|

|

|

$

|

160,670

|

|

|

$

|

160,225

|

|

|

$

|

165,054

|

|

|

$

|

166,964

|

|

|

Unrealized (gain) loss on derivative instruments

|

|

|

(232

|

)

|

|

|

(708

|

)

|

|

|

(400

|

)

|

|

|

(432

|

)

|

|

|

(170

|

)

|

|

Interest income excluding valuations

|

|

|

161,971

|

|

|

|

159,962

|

|

|

|

159,825

|

|

|

|

164,622

|

|

|

|

166,794

|

|

|

Tax-equivalent adjustment

|

|

|

4,420

|

|

|

|

3,038

|

|

|

|

1,595

|

|

|

|

1,451

|

|

|

|

1,463

|

|

|

Interest income on a tax-equivalent basis excluding valuations

|

|

|

166,391

|

|

|

|

163,000

|

|

|

|

161,420

|

|

|

|

166,073

|

|

|

|

168,257

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Interest Expense - GAAP

|

|

|

31,298

|

|

|

|

33,782

|

|

|

|

35,732

|

|

|

|

39,423

|

|

|

|

41,461

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net interest income - GAAP

|

|

$

|

130,905

|

|

|

$

|

126,888

|

|

|

$

|

124,493

|

|

|

$

|

125,631

|

|

|

$

|

125,503

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net interest income excluding valuations

|

|

$

|

130,673

|

|

|

$

|

126,180

|

|

|

$

|

124,093

|

|

|

$

|

125,199

|

|

|

$

|

125,333

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net interest income on a tax-equivalent basis excluding valuations

|

|

$

|

135,093

|

|

|

$

|

129,218

|

|

|

$

|

125,688

|

|

|

$

|

126,650

|

|

|

$

|

126,796

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Average Balances

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Loans and leases

|

|

$

|

9,639,612

|

|

|

$

|

9,820,781

|

|

|

$

|

10,077,907

|

|

|

$

|

10,199,808

|

|

|

$

|

10,297,835

|

|

|

Total securities and other short-term investments

|

|

|

2,719,973

|

|

|

|

2,768,659

|

|

|

|

2,675,755

|

|

|

|

2,576,421

|

|

|

|

2,238,701

|

|

|

Average Interest-Earning Assets

|

|

$

|

12,359,585

|

|

|

$

|

12,589,440

|

|

|

$

|

12,753,662

|

|

|

$

|

12,776,229

|

|

|

$

|

12,536,536

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Average Interest-Bearing Liabilities

|

|

$

|

10,409,792

|

|

|

$

|

10,583,702

|

|

|

$

|

10,652,144

|

|

|

$

|

10,700,868

|

|

|

$

|

10,518,169

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Average Yield/Rate

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Average yield on interest-earning assets - GAAP

|

|

|

5.21

|

%

|

|

|

5.12

|

%

|

|

|

5.10

|

%

|

|

|

5.14

|

%

|

|

|

5.30

|

%

|

|

Average rate on interest-bearing liabilities - GAAP

|

|

|

1.19

|

%

|

|

|

1.28

|

%

|

|

|

1.36

|

%

|

|

|

1.47

|

%

|

|

|

1.57

|

%

|

|

Net interest spread - GAAP

|

|

|

4.02

|

%

|

|

|

3.84

|

%

|

|

|

3.74

|

%

|

|

|

3.67

|

%

|

|

|

3.73

|

%

|

|

Net interest margin - GAAP

|

|

|

4.20

|

%

|

|

|

4.04

|

%

|

|

|

3.96

|

%

|

|

|

3.91

|

%

|

|

|

3.98

|

%

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Average yield on interest-earning assets excluding valuations

|

|

|

5.20

|

%

|

|

|

5.10

|

%

|

|

|

5.08

|

%

|

|

|

5.13

|

%

|

|

|

5.29

|

%

|

|

Average rate on interest-bearing liabilities excluding valuations

|

|

|

1.19

|

%

|

|

|

1.28

|

%

|

|

|

1.36

|

%

|

|

|

1.47

|

%

|

|

|

1.57

|

%

|

|

Net interest spread excluding valuations

|

|

|

4.01

|

%

|

|

|

3.82

|

%

|

|

|

3.72

|

%

|

|

|

3.66

|

%

|

|

|

3.72

|

%

|

|

Net interest margin excluding valuations

|

|

|

4.19

|

%

|

|

|

4.02

|

%

|

|

|

3.95

|

%

|

|

|

3.90

|

%

|

|

|

3.98

|

%

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Average yield on interest-earning assets on a tax-equivalent basis

and excluding valuations

|

|

|

5.34

|

%

|

|

|

5.19

|

%

|

|

|

5.13

|

%

|

|

|

5.17

|

%

|

|

|

5.34

|

%

|

|

Average rate on interest-bearing liabilities excluding valuations

|

|

|

1.19

|

%

|

|

|

1.28

|

%

|

|

|

1.36

|

%

|

|

|

1.47

|

%

|

|

|

1.57

|

%

|

|

Net interest spread on a tax-equivalent basis and excluding

valuations

|

|

|

4.15

|

%

|

|

|

3.91

|

%

|

|

|

3.77

|

%

|

|

|

3.70

|

%

|

|

|

3.77

|

%

|

|

Net interest margin on a tax-equivalent basis and excluding

valuations

|

|

|

4.34

|

%

|

|

|

4.12

|

%

|

|

|

4.00

|

%

|

|

|

3.94

|

%

|

|

|

4.02

|

%

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

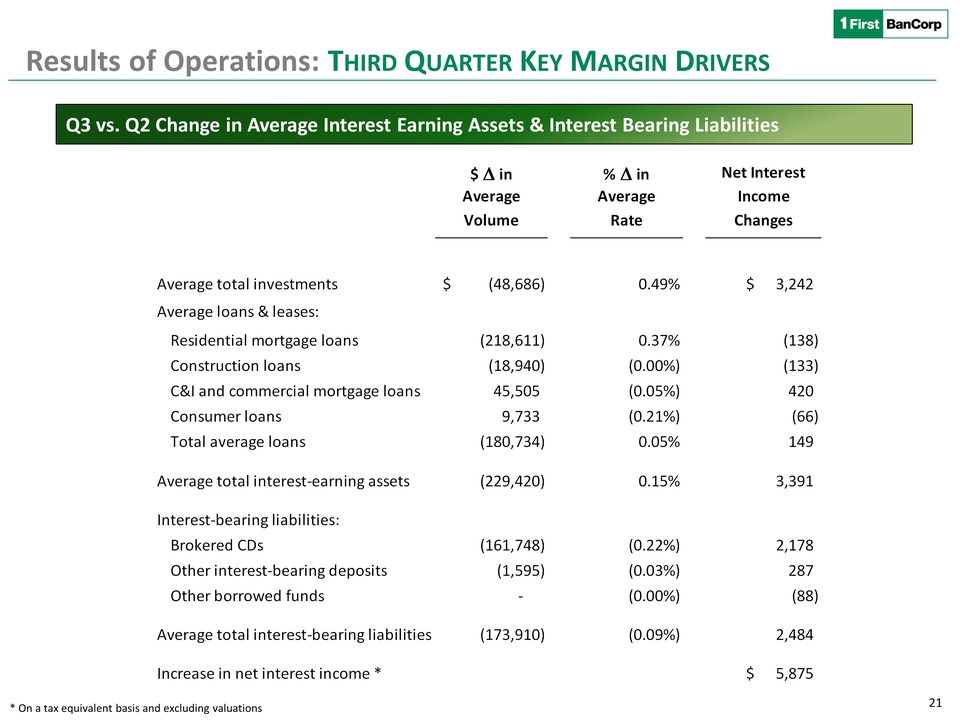

Net interest income, excluding valuations, amounted to $130.7 million,

an increase of $4.5 million when compared to the second quarter of 2013.

Net interest margin expanded to 4.19% for the third quarter of 2013 from

4.02% for the second quarter of 2013. The increase in net interest

income and margin was mainly due to:

-

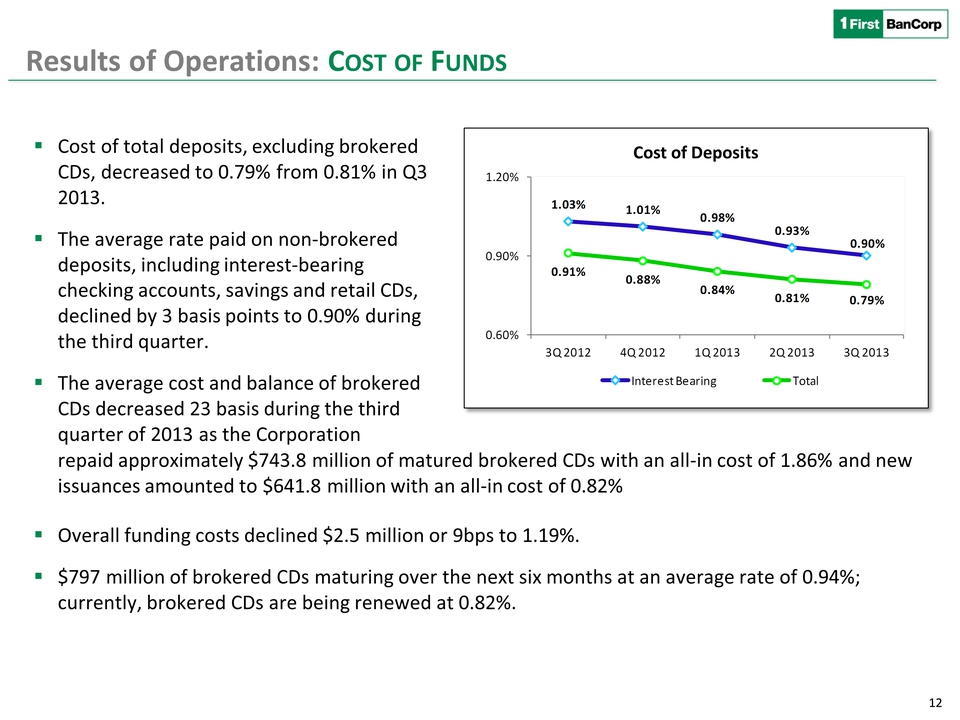

A decrease of $2.5 million, or 9 basis points, in total interest

expense, of which approximately $2.4 million was due to a reduction in

the average cost of total deposits with the remaining decrease

primarily related to the maturities of Federal Home Loan Bank

advances. The average cost and balance of brokered certificates of

deposit (“CDs”) decreased 23 basis points during the third quarter of

2013 as the Corporation repaid approximately $743.8 million of matured

brokered CDs with an all-in cost of 1.86% and new issuances amounted

to $641.8 million with an all-in cost of 0.82%. The Corporation

expects its cost of funding to remain stable for the remainder of 2013.

-

A $2.2 million increase in interest income on investment securities

mainly due to the decrease in MBS prepayment activity levels that

resulted in a higher yield on U.S. agency MBS bought at a premium.

-

The net interest margin also improved due to the $71.3 million

reduction in the average balance of low-yielding cash balances, mainly

balances maintained at the Federal Reserve, as the Corporation

deployed some of its liquidity into higher yielding U.S. agency MBS

investments and used cash balances to repay maturing brokered CDs.

Also contributing to the expanded margin was the decrease in the

average balance of non-performing loans due to, among other things,

the full effect of the sale of non-performing residential mortgage

loans completed in the second quarter.

These increases were partially offset by:

-

A $0.2 million decrease in interest income on loans.

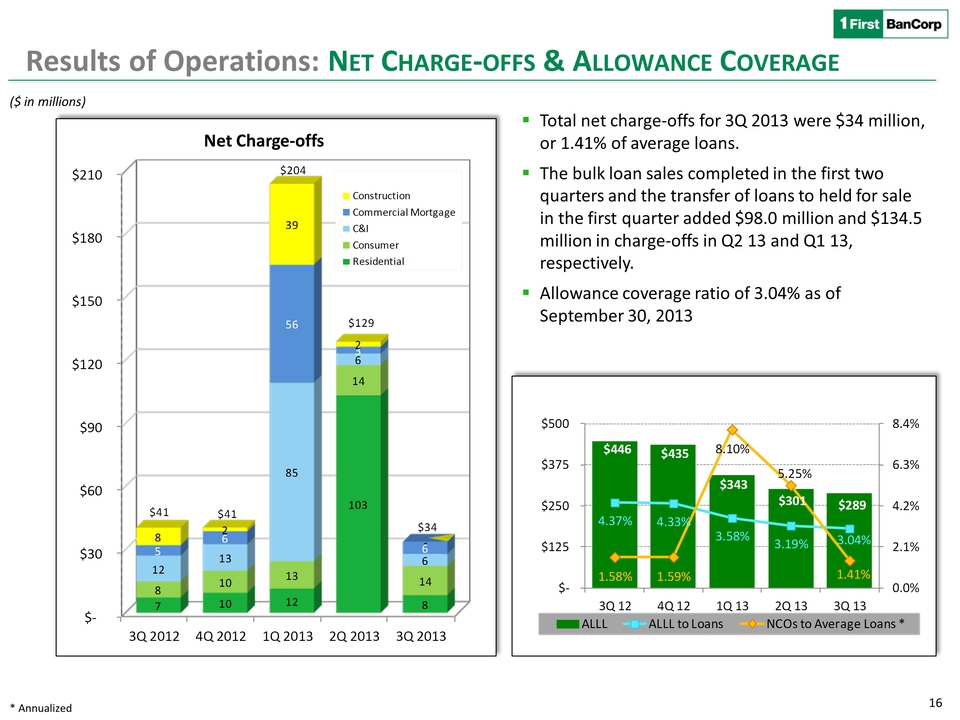

PROVISION FOR LOAN AND LEASE LOSSES

The provision for loan and lease losses for the third quarter of 2013

was $22.2 million, compared to $87.5 million for the second quarter of

2013, which includes $67.9 million related to the bulk sale of

non-performing residential assets. Excluding the impact of the bulk sale

of non-performing residential assets, the provision for loan and lease

losses of $22.2 million for the third quarter was $2.6 million higher

than the provision recorded for the second quarter of 2013. The increase

was mainly related to the construction and consumer loan portfolios. The

provision for construction loans in the third quarter amounted to $1.3

million compared to a reserve release of $6.7 million for the second

quarter that was driven by updated appraisals for certain collateral

dependent loans. The provision for consumer loans increased by $3.1

million, compared to the provision for the second quarter, mainly

related to the increase in the general reserve for auto and credit card

loans. These increases were partially offset by lower provisions for

commercial loans reflecting a lower migration of loans into adversely

classified categories and lower underlying losses on these portfolios.

See Credit Quality discussion below for additional information

regarding the allowance for loan and lease losses.

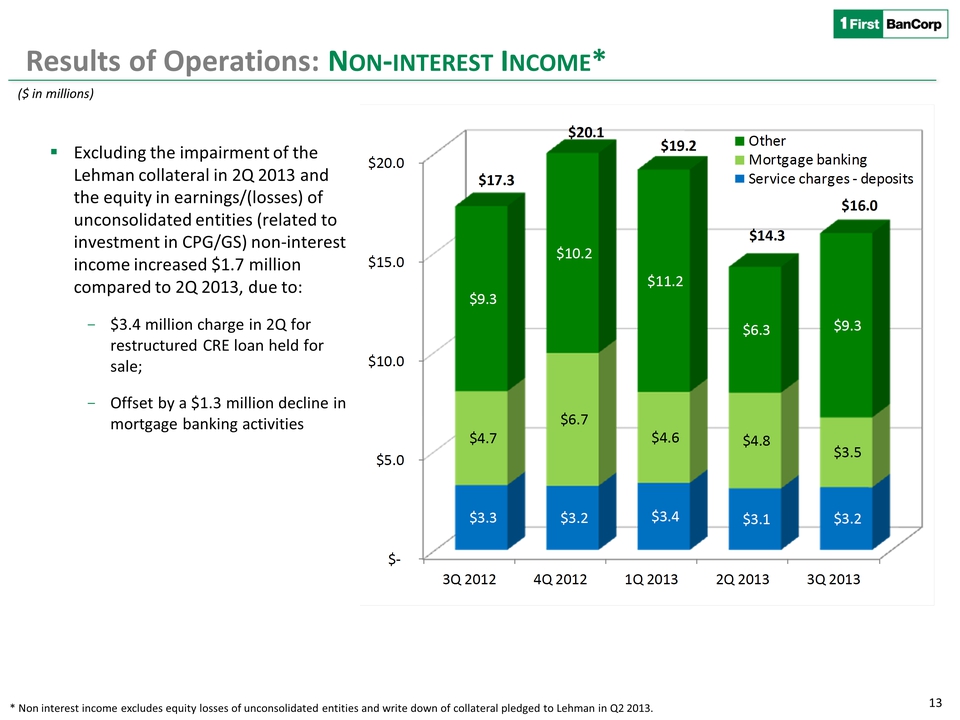

NON-INTEREST INCOME (LOSS)

|

|

Quarter Ended

|

|

|

September 30,

|

|

June 30,

|

|

March 31,

|

|

December 31,

|

|

September 30,

|

|

(In thousands)

|

2013

|

|

2013

|

|

2013

|

|

2012

|

|

2012

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Service charges on deposit accounts

|

$

|

3,157

|

|

|

$

|

3,098

|

|

|

$

|

3,380

|

|

|

$

|

3,228

|

|

|

$

|

3,267

|

|

|

Mortgage banking activities

|

|

3,521

|

|

|

|

4,823

|

|

|

|

4,580

|

|

|

|

6,700

|

|

|

|

4,728

|

|

|

Net loss on investments and impairments

|

|

-

|

|

|

|

(42

|

)

|

|

|

(117

|

)

|

|

|

(69

|

)

|

|

|

(547

|

)

|

|

Broker-dealer income

|

|

-

|

|

|

|

-

|

|

|

|

-

|

|

|

|

-

|

|

|

|

20

|

|

|

Impairment - collateral pledged to Lehman

|

|

-

|

|

|

|

(66,574

|

)

|

|

|

-

|

|

|

|

-

|

|

|

|

-

|

|

|

Other operating income

|

|

9,290

|

|

|

|

6,384

|

|

|

|

11,324

|

|

|

|

10,239

|

|

|

|

9,857

|

|

|

Equity in (loss) earnings of unconsolidated entity

|

|

(5,908

|

)

|

|

|

648

|

|

|

|

(5,538

|

)

|

|

|

(8,330

|

)

|

|

|

(2,199

|

)

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Non-interest income (loss)

|

$

|

10,060

|

|

|

$

|

(51,663

|

)

|

|

$

|

13,629

|

|

|

$

|

11,768

|

|

|

$

|

15,126

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Non-interest income for the third quarter of 2013 amounted to $10.1

million, compared to non-interest loss of $51.7 million for the second

quarter of 2013. The results for the second quarter included the $66.6

million write-off of the collateral pledged to Lehman. Non-interest

income, excluding the Lehman collateral write-off, decreased $4.9

million from the 2013 second quarter primarily due to:

-

A $6.6 million negative variance in the equity in earnings (loss) of

unconsolidated entity. The Corporation recorded a loss of $5.9 million

on its investment in unconsolidated entity for the third quarter

compared to earnings of $0.6 million for the second quarter of 2013.

This adjustment is related to the Bank’s investment in CPG/GS PR NPL,

LLC (“CPG/GS”), the entity that purchased $269.2 million of loans from

FirstBank in 2011. The Bank holds a 35% subordinated ownership

interest in CPG/GS. This investment is accounted for under the equity

method and following the hypothetical liquidation book value method to

determine the Bank’s share of CPG/GS earnings or losses.

-

A $1.3 million decrease in revenues from the mortgage banking business

mainly related to: (i) a decrease of $1.2 million in the net realized

gain on loan sales and securitization activities, and (ii) a $0.2

million decrease in servicing fees due to the expiration of the

interim servicing on loans included in the bulk sales of assets

completed in the first half of 2013.

-

A $0.2 million decrease in revenues from the insurance agency

activities, included as part of “Other operating income” in the table

above.

These decreases were partially offset by:

-

The impact in the previous quarter of a $3.4 million loss related to

the restructuring of a commercial mortgage loan held for sale in which

the Corporation received foreclosed real estate in partial

satisfaction of a debt arrangement and modified the terms of the

remaining balance. This loss was included as part of “Other operating

income” in the table above.

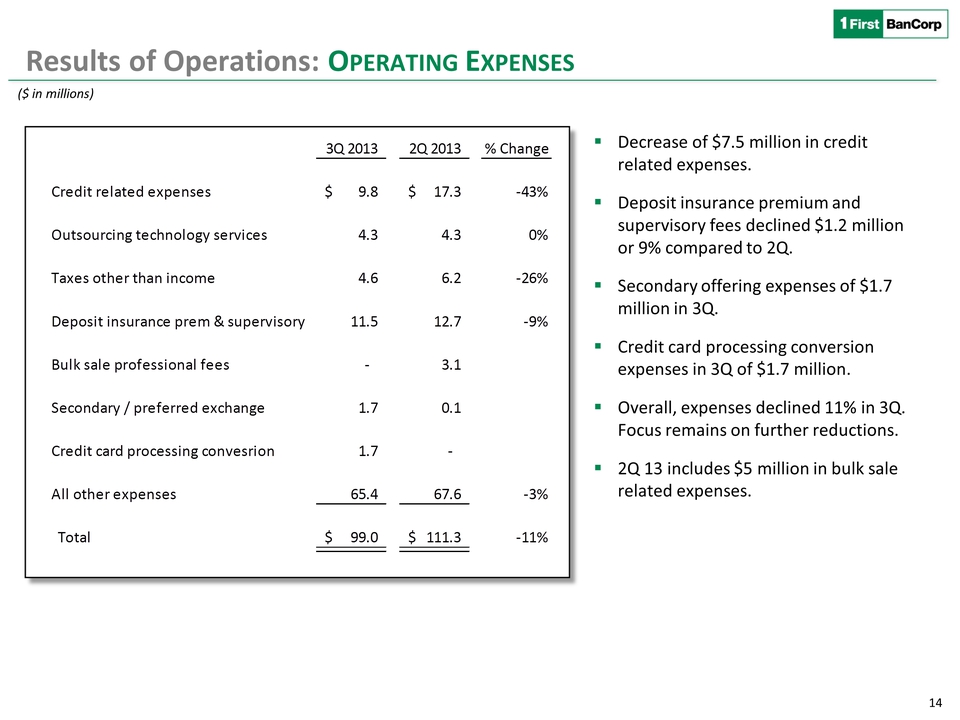

NON-INTEREST EXPENSES

|

|

|

Quarter Ended

|

|

|

|

September 30,

|

|

June 30,

|

|

March 31,

|

|

December 31,

|

|

September 30,

|

|

(In thousands)

|

|

2013

|

|

2013

|

|

2013

|

|

2012

|

|

2012

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Employees' compensation and benefits

|

|

$

|

32,823

|

|

$

|

33,116

|

|

$

|

33,554

|

|

$

|

31,840

|

|

$

|

31,058

|

|

Occupancy and equipment

|

|

|

15,134

|

|

|

14,946

|

|

|

15,070

|

|

|

14,972

|

|

|

15,208

|

|

Deposit insurance premium

|

|

|

10,479

|

|

|

11,430

|

|

|

11,517

|

|

|

11,897

|

|

|

11,657

|

|

Other insurance and supervisory fees

|

|

|

1,034

|

|

|

1,269

|

|

|

1,289

|

|

|

1,366

|

|

|

1,366

|

|

Taxes, other than income taxes

|

|

|

4,693

|

|

|

6,239

|

|

|

2,989

|

|

|

3,013

|

|

|

3,499

|

|

Professional fees:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Collections, appraisals and other credit related fees

|

|

|

2,780

|

|

|

2,520

|

|

|

1,924

|

|

|

1,127

|

|

|

2,250

|

|

Outsourcing technology services

|

|

|

4,338

|

|

|

4,258

|

|

|

1,346

|

|

|

1,557

|

|

|

1,311

|

|

Bulk sales professional fees

|

|

|

-

|

|

|

3,060

|

|

|

3,878

|

|

|

-

|

|

|

-

|

|

Terminated preferred stock exchange offer professional fees

|

|

|

-

|

|

|

115

|

|

|

1,081

|

|

|

-

|

|

|

-

|

|

Secondary offering professional fees

|

|

|

390

|

|

|

-

|

|

|

-

|

|

|

-

|

|

|

-

|

|

Other professional fees

|

|

|

4,332

|

|

|

3,782

|

|

|

2,903

|

|

|

4,275

|

|

|

3,908

|

|

Business promotion

|

|

|

3,478

|

|

|

3,831

|

|

|

3,357

|

|

|

4,067

|

|

|

4,004

|

|

Net loss on OREO operations

|

|

|

7,052

|

|

|

14,829

|

|

|

7,310

|

|

|

6,201

|

|

|

8,686

|

|

Secondary offering other costs

|

|

|

1,279

|

|

|

-

|

|

|

-

|

|

|

-

|

|

|

-

|

|

Other

|

|

|

11,342

|

|

|

11,928

|

|

|

11,792

|

|

|

10,590

|

|

|

8,896

|

|

Total

|

|

$

|

99,154

|

|

$

|

111,323

|

|

$

|

98,010

|

|

$

|

90,905

|

|

$

|

91,843

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Non-interest expenses in the third quarter of 2013 amounted to $99.2

million, a decrease of $12.2 million from $111.3 million for the second

quarter of 2013. Non-interest expenses for the third quarter included

approximately $1.7 million in costs associated with the secondary

offering and $1.7 million in costs associated with the conversion of the

credit card processing platform. Results for the second quarter included

$5.0 million of expenses specifically related to the bulk sale of

non-performing residential assets ($3.1 million of professional fees and

$1.9 million as part of OREO losses) as well as $1.7 million of the

national gross receipts tax that corresponded to the first quarter of

2013 but was recorded in the second quarter after enactment of Act 40

which amended the Puerto Rico Internal Revenue Code of 2011 (the “2011

PR Code”).

Adjusted non-interest expenses, which exclude the aforementioned items,

amounted to $95.8 million for the third quarter of 2013, down $8.9

million compared to the second quarter. The main drivers of the decrease

were:

-

A lower net loss on OREO operations, mainly reflecting a $4.9 million

decrease in write-downs on OREO properties. The previous quarter was

adversely impacted by $5.3 million in write-downs to the value of

certain commercial OREO properties in the Virgin Islands region. Also

contributing to the lower net loss on OREO operations was a $1.7

million decrease in operating expenses for, among other things,

repairs and maintenance costs as well as legal-related fees.

-

A $0.3 million reduction in employees’ compensation and benefit

expenses as the previous quarter included certain non-periodic

employee compensation-related expenses such as employees’ lump-sum and

severance payments.

-

A $1.2 million decrease in the Federal Deposit Insurance Corporation

(“FDIC”) insurance premium and other local regulatory fees included as

part of “Other insurance and supervisory fees” in the table above.

-

A $0.3 million increase to legal reserves in the previous quarter,

included as part of “Other” in the table above.

INCOME TAXES

The income tax expense for the third quarter of 2013 amounted to $3.7

million compared to an income tax benefit of $1.0 million for the second

quarter of 2013, primarily reflecting an increase in reserves for

uncertain tax positions and the impact in the previous quarter of

amendments to the 2011 PR Code enacted on June 30, 2013. The increase in

the reserve for uncertain tax positions was mainly related to changes in

management judgment given the lengthy administrative appeals process and

expectations as to resolution resulting in an increase of $3.0 million

to current Unrecognized Tax Positions.

Some of the amendments of Act 40 were retroactive to January 1, 2013,

including the new national gross receipt tax. In the case of financial

institutions, the national gross receipts tax was imposed as an

additional tax at a flat rate of 1%. This charge was recorded as part of

non-interest expenses in the Corporation’s Statement of Income. However,

financial institutions may claim a credit equal to 50% of the national

gross receipts tax against their regular tax liabilities or AMT

liabilities. During the second quarter of 2013, after enactment of Act

40, the Corporation recorded $1.6 million as a credit against its

provision for income taxes, of which $0.8 million corresponded to the

first quarter of 2013.

In addition, Act 40 effectively increased the maximum statutory tax rate

of corporations from 30% to 39%. This provision was also retroactive to

January 1, 2013, and resulted in a net benefit of approximately $0.5

million recorded in the second quarter mainly due to the increase in the

deferred tax asset of profitable subsidiaries. As of September 30, 2013,

the deferred tax asset, net of a valuation allowance of $519.8 million,

amounted to $7.4 million.

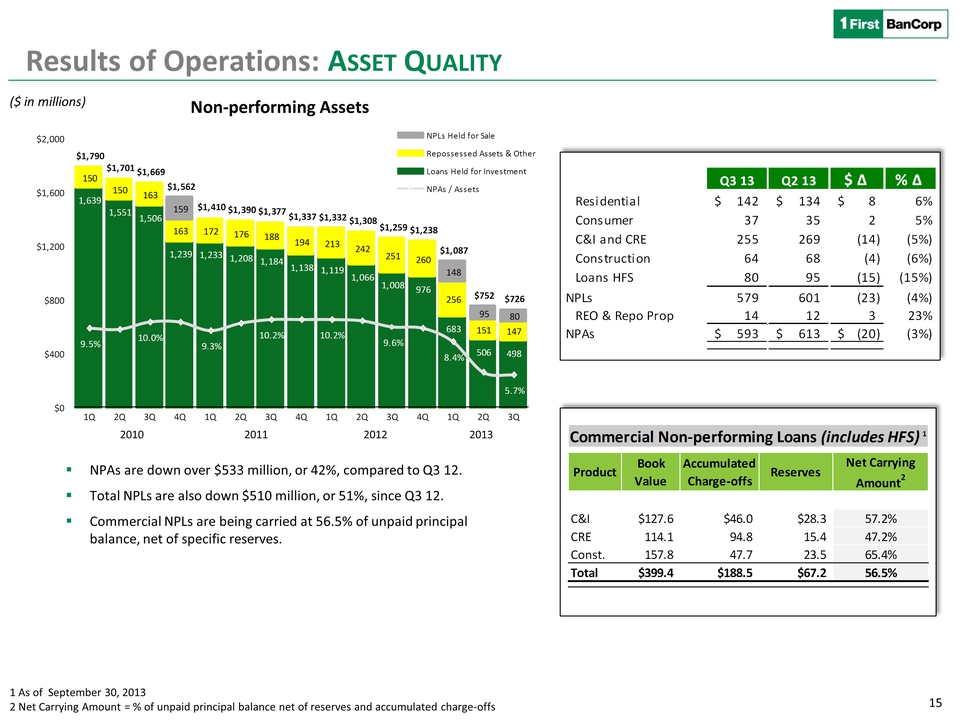

CREDIT QUALITY

Non-Performing Assets

|

(Dollars in thousands)

|

|

September 30,

|

|

June 30,

|

|

March 31,

|

|

December 31,

|

|

September 30,

|

|

|

|

2013

|

|

2013

|

|

2013

|

|

2012

|

|

2012

|

|

Non-performing loans held for investment:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Residential mortgage

|

|

$

|

142,002

|

|

|

$

|

133,937

|

|

|

$

|

311,495

|

|

|

$

|

313,626

|

|

|

$

|

320,913

|

|

|

Commercial mortgage

|

|

|

127,374

|

|

|

|

136,737

|

|

|

|

136,708

|

|

|

|

214,780

|

|

|

|

231,163

|

|

|

Commercial and Industrial

|

|

|

127,584

|

|

|

|

131,906

|

|

|

|

141,045

|

|

|

|

230,090

|

|

|

|

230,459

|

|

|

Construction

|

|

|

64,241

|

|

|

|

68,204

|

|

|

|

59,810

|

|

|

|

178,190

|

|

|

|

189,458

|

|

|

Consumer and Finance leases

|

|

|

37,184

|

|

|

|

35,416

|

|

|

|

33,652

|

|

|

|

38,875

|

|

|

|

36,051

|

|

|

Total non-performing loans held for investment

|

|

|

498,385

|

|

|

|

506,200

|

|

|

|

682,710

|

|

|

|

975,561

|

|

|

|

1,008,044

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

REO

|

|

|

133,284

|

|

|

|

139,257

|

|

|

|

181,479

|

|

|

|

185,764

|

|

|

|

177,001

|

|

|

Other repossessed property

|

|

|

14,125

|

|

|

|

11,503

|

|

|

|

9,913

|

|

|

|

10,107

|

|

|

|

9,775

|

|

|

Other assets (1)

|

|

|

-

|

|

|

|

-

|

|

|

|

64,543

|

|

|

|

64,543

|

|

|

|

64,543

|

|

|

Total non-performing assets, excluding loans held for sale

|

|

$

|

645,794

|

|

|

$

|

656,960

|

|

|

$

|

938,645

|

|

|

$

|

1,235,975

|

|

|

$

|

1,259,363

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Non-performing loans held for sale

|

|

|

80,234

|

|

|

|

94,951

|

|

|

|

147,995

|

|

|

|

2,243

|

|

|

|

-

|

|

|

Total non-performing assets, including loans held for sale (2)

|

|

$

|

726,028

|

|

|

$

|

751,911

|

|

|

$

|

1,086,640

|

|

|

$

|

1,238,218

|

|

|

$

|

1,259,363

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Past-due loans 90 days and still accruing

|

|

$

|

127,735

|

|

|

$

|

113,061

|

|

|

$

|

125,384

|

|

|

$

|

142,012

|

|

|

$

|

141,028

|

|

|

Non-performing loans held for investment to total loans held for

investment

|

|

|

5.24

|

%

|

|

|

5.36

|

%

|

|

|

7.14

|

%

|

|

|

9.70

|

%

|

|

|

9.89

|

%

|

|

Non-performing loans to total loans

|

|

|

6.01

|

%

|

|

|

6.21

|

%

|

|

|

8.45

|

%

|

|

|

9.64

|

%

|

|

|

9.83

|

%

|

|

Non-performing assets, excluding non-performing loans held for

sale, to total assets, excluding non-performing loans held for sale

|

|

|

5.08

|

%

|

|

|

5.17

|

%

|

|

|

7.30

|

%

|

|

|

9.44

|

%

|

|

|

9.58

|

%

|

|

Non-performing assets to total assets

|

|

|

5.68

|

%

|

|

|

5.87

|

%

|

|

|

8.35

|

%

|

|

|

9.45

|

%

|

|

|

9.58

|

%

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(1) Collateral pledged to Lehman Brothers, Inc.

|

|

(2)Amount excludes purchased credit impaired loans with a carrying

value as of September 30, 2013, of approximately $6.0 million

acquired as part of the credit card portfolio acquired from FIA

Card Services ("FIA").

|

|

|

Credit quality metrics remained relatively stable:

-

Total non-performing assets decreased by $25.9 million, or 3%, from

the second quarter of 2013 to $726.0 million. Total non-performing

loans, including non-performing loans held for sale, decreased by

$22.5 million, or 4%, from the second quarter of 2013. The decrease

was primarily due to charge-offs of $7.8 million against two

non-performing commercial loan relationships, the completion of the

transfer to OREO of one of the properties amounting to $6.7 million in

connection with the aforementioned commercial mortgage loan held for

sale relationship restructured in the second quarter on which the

Corporation received foreclosed real estate in partial satisfaction of

a debt arrangement, $6.4 million related to construction loan held for

sale participations paid off during the third quarter, and a $6.8

million commercial mortgage troubled debt restructured loan restored

to accrual status.

-

Inflows of non-performing loans decreased by $20.3 million, or 21%,

compared to inflows in the second quarter. This reduction was

primarily reflected in the residential mortgage loans portfolio. The

largest individual relationship that entered into non-performing

status during the third quarter amounted to $2.3 million.

-

Adversely classified commercial and construction loans held for

investment decreased by $32.1 million to $632.5 million, or 5%, from

the second quarter of 2013. Non-performing commercial and construction

loans held for sale decreased by $14.7 million.

-

The OREO balance decreased by $6.0 million, driven by sales and fair

value adjustments.

-

Total troubled debt restructured loans (“TDRs”) held for investment

were $636.9 million at September 30, 2013, up $23.8 million, or 4%,

from June 30, 2013. Approximately $427.1 million of total TDRs held

for investment were in accrual status as of September 30, 2013.

Allowance for Loan and Lease Losses

The following table sets forth an analysis of the allowance for loan and

lease losses during the periods indicated:

|

|

|

Quarter Ended

|

|

(Dollars in thousands)

|

|

September 30,

|

|

June 30,

|

|

|

|

March 31,

|

|

|

|

December 31,

|

|

September 30,

|

|

|

|

2013

|

|

2013

|

|

|

|

2013

|

|

|

|

2012

|

|

2012

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Allowance for loan and lease losses, beginning of period

|

|

$

|

301,047

|

|

|

$

|

342,531

|

|

|

|

|

$

|

435,414

|

|

|

|

|

$

|

445,531

|

|

|

$

|

457,153

|

|

|

Provision for loan and lease losses

|

|

|

22,195

|

|

|

|

87,464

|

|

(1

|

)

|

|

|

111,123

|

|

(5

|

)

|

|

|

30,466

|

|

|

|

28,952

|

|

|

Net charge-offs of loans:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Residential mortgage

|

|

|

(8,457

|

)

|

|

|

(103,418

|

)

|

(2

|

)

|

|

|

(11,580

|

)

|

(6

|

)

|

|

|

(9,555

|

)

|

|

|

(7,358

|

)

|

|

Commercial mortgage

|

|

|

(5,918

|

)

|

|

|

(3,253

|

)

|

|

|

|

|

(56,036

|

)

|

(7

|

)

|

|

|

(6,101

|

)

|

|

|

(5,002

|

)

|

|

Commercial and Industrial

|

|

|

(5,718

|

)

|

|

|

(5,520

|

)

|

|

|

|

|

(84,829

|

)

|

(8

|

)

|

|

|

(12,601

|

)

|

|

|

(12,261

|

)

|

|

Construction

|

|

|

71

|

|

|

|

(2,368

|

)

|

(3

|

)

|

|

|

(38,515

|

)

|

(9

|

)

|

|

|

(1,837

|

)

|

|

|

(8,326

|

)

|

|

Consumer and finance leases

|

|

|

(13,841

|

)

|

|

|

(14,389

|

)

|

|

|

|

|

(13,046

|

)

|

|

|

|

|

(10,489

|

)

|

|

|

(7,627

|

)

|

|

Net charge-offs

|

|

|

(33,863

|

)

|

|

|

(128,948

|

)

|

(4

|

)

|

|

|

(204,006

|

)

|

(10

|

)

|

|

|

(40,583

|

)

|

|

|

(40,574

|

)

|

|

Allowance for loan and lease losses, end of period

|

|

$

|

289,379

|

|

|

$

|

301,047

|

|

|

|

|

$

|

342,531

|

|

|

|

|

$

|

435,414

|

|

|

$

|

445,531

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Allowance for loan and lease losses to period end total loans held

for investment

|

|

|

3.04

|

%

|

|

|

3.19

|

%

|

|

|

|

|

3.58

|

%

|

|

|

|

|

4.23

|

%

|

|

|

4.37

|

%

|

|

Net charge-offs (annualized) to average loans outstanding during the

period

|

|

|

1.41

|

%

|

|

|

5.25

|

%

|

|

|

|

|

8.10

|

%

|

|

|

|

|

1.59

|

%

|

|

|

1.58

|

%

|

|

Net charge-offs (annualized), excluding charge-offs related to

loans sold and loans transferred to held for sale, to average

loans outstanding during the period

|

|

|

1.41

|

%

|

|

|

1.29

|

%

|

|

|

|

|

2.87

|

%

|

|

|

|

|

1.59

|

%

|

|

|

1.58

|

%

|

|

Provision for loan and lease losses to net charge-offs during the

period

|

|

|

0.66x

|

|

|

|

0.68x

|

|

|

|

|

|

0.54x

|

|

|

|

|

|

0.75x

|

|

|

|

0.71x

|

|

|

Provision for loan and lease losses to net charge-offs during the

period, excluding impact of loans sold and loans transferred to

held for sale

|

|

|

0.66x

|

|

|

|

0.63x

|

|

|

|

|

|

0.68x

|

|

|

|

|

|

0.75x

|

|

|

|

0.71x

|

|

|

|

|

(1) Includes provision of $67.9 million associated with the bulk

sale of non-performing residential assets.

|

|

(2) Includes net charge-offs totaling $97.9 million associated with

the bulk sale of non-performing residential assets.

|

|

(3) Includes net charge-offs totaling $31 thousand associated with

the bulk sale of non-performing residential assets.

|

|

(4) Includes net charge-offs totaling $98.0 million associated with

the bulk sale of non-performing residential assets.

|

|

(5) Includes provision of $64.1 million associated with the bulk

sale of adversely classified commercial assets and the transfer of

loans to held for sale.

|

|

(6) Includes net charge-offs totaling $1.0 million associated with

the bulk sale of adversely classified commercial assets.

|

|

(7) Includes net charge-offs of $54.6 million associated with the

bulk sale of adversely classified commercial assets and the transfer

of loans to held for sale.

|

|

(8) Includes net charge-offs totaling $44.7 million associated with

the bulk sale of adversely classified commercial assets.

|

|

(9) Includes net charge-offs of $34.2 million associated with the

bulk sale of adversely classified commercial assets and the transfer

of loans to held for sale.

|

|

(10) Includes net charge-offs of $134.5 million associated with the

bulk sale of adversely classified commercial assets and the transfer

of loans to held for sale.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

-

The ratio of the allowance for loan and lease losses to loans held for

investment was 3.04% as of September 30, 2013, compared to 3.19% as of

June 30, 2013, primarily due to charge-offs of impaired commercial

loans with previously established adequate reserves and lower

underlying losses on commercial mortgage loans. The ratio of the

allowance to non-performing loans held for investment of 58.06% as of

September 30, 2013 decreased from 59.47% as of June 30, 2013.

The following table sets forth information concerning the composition of

the Corporation’s allowance for loan and lease losses as of September

30, 2013 and June 30, 2013 by loan category and by whether the allowance

and related provisions were calculated individually for impairment

purposes or through a general valuation allowance:

|

(Dollars in thousands)

|

|

Residential Mortgage Loans

|

|

Commercial (including Commercial Mortgage, C&I, and Construction

loans)

|

|

Consumer and Finance Leases

|

|

Total

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

As of September 30, 2013

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Impaired loans:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Principal balance of loans, net of charge-offs

|

|

$

|

397,025

|

|

|

$

|

479,421

|

|

|

$

|

28,063

|

|

|

$

|

904,509

|

|

|

Allowance for loan and lease losses

|

|

|

17,982

|

|

|

|

84,539

|

|

|

|

3,655

|

|

|

|

106,176

|

|

|

Allowance for loan and lease losses to principal balance

|

|

|

4.53

|

%

|

|

|

17.63

|

%

|

|

|

13.02

|

%

|

|

|

11.74

|

%

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

PCI loans:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Carrying value of PCI loans

|

|

|

-

|

|

|

|

-

|

|

|

|

5,963

|

|

|

|

5,963

|

|

|

Allowance for PCI loans

|

|

|

-

|

|

|

|

-

|

|

|

|

-

|

|

|

|

-

|

|

|

Allowance for PCI loans to carrying value

|

|

|

-

|

|

|

|

-

|

|

|

|

-

|

|

|

|

-

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Loans with general allowance:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Principal balance of loans

|

|

|

2,122,432

|

|

|

|

4,450,330

|

|

|

|

2,025,400

|

|

|

|

8,598,162

|

|

|

Allowance for loan and lease losses

|

|

|

13,805

|

|

|

|

116,649

|

|

|

|

52,749

|

|

|

|

183,203

|

|

|

Allowance for loan and lease losses to principal balance

|

|

|

0.65

|

%

|

|

|

2.62

|

%

|

|

|

2.60

|

%

|

|

|

2.13

|

%

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total loans held for investment:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Principal balance of loans

|

|

$

|

2,519,457

|

|

|

$

|

4,929,751

|

|

|

$

|

2,059,426

|

|

|

$

|

9,508,634

|

|

|

Allowance for loan and lease losses

|

|

|

31,787

|

|

|

|

201,188

|

|

|

|

56,404

|

|

|

|

289,379

|

|

|

Allowance for loan and lease losses to principal balance

|

|

|

1.26

|

%

|

|

|

4.08

|

%

|

|

|

2.74

|

%

|

|

|

3.04

|

%

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

As of June 30, 2013

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Impaired loans:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Principal balance of loans, net of charge-offs

|

|

$

|

384,062

|

|

|

$

|

496,398

|

|

|

$

|

27,785

|

|

|

$

|

908,245

|

|

|

Allowance for loan and lease losses

|

|

|

20,406

|

|

|

|

91,606

|

|

|

|

2,941

|

|

|

|

114,953

|

|

|

Allowance for loan and lease losses to principal balance

|

|

|

5.31

|

%

|

|

|

18.45

|

%

|

|

|

10.58

|

%

|

|

|

12.66

|

%

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

PCI loans:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Carrying value of PCI loans

|

|

|

-

|

|

|

|

-

|

|

|

|

8,285

|

|

|

|

8,285

|

|

|

Allowance for PCI loans

|

|

|

-

|

|

|

|

-

|

|

|

|

-

|

|

|

|

-

|

|

|

Allowance for PCI loans to carrying value

|

|

|

-

|

|

|

|

-

|

|

|

|

-

|

|

|

|

-

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Loans with general allowance:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Principal balance of loans

|

|

|

2,127,144

|

|

|

|

4,390,814

|

|

|

|

2,011,298

|

|

|

|

8,529,256

|

|

|

Allowance for loan and lease losses

|

|

|

15,175

|

|

|

|

118,812

|

|

|

|

52,107

|

|

|

|

186,094

|

|

|

Allowance for loan and lease losses to principal balance

|

|

|

0.71

|

%

|

|

|

2.71

|

%

|

|

|

2.59

|

%

|

|

|

2.18

|

%

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total loans held for investment:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Principal balance of loans

|

|

$

|

2,511,206

|

|

|

$

|

4,887,212

|

|

|

$

|

2,047,368

|

|

|

$

|

9,445,786

|

|

|

Allowance for loan and lease losses

|

|

|

35,581

|

|

|

|

210,418

|

|

|

|

55,048

|

|

|

|

301,047

|

|

|

Allowance for loan and lease losses to principal balance

|

|

|

1.42

|

%

|

|

|

4.31

|

%

|

|

|

2.69

|

%

|

|

|

3.19