Use these links to rapidly review the document

TABLE OF CONTENTS

ITEM 8. FINANCIAL STATEMENTS AND SUPPLEMENTARY DATA

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

| ý | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

For the fiscal year ended: December 30, 2012 |

||

or |

||

o |

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

|

For the transition period from to |

||

Commission file number: 1-9824

The McClatchy Company

(Exact name of registrant as specified in its charter)

| Delaware (State or other jurisdiction of incorporation or organization) |

52-2080478 (I.R.S. Employer Identification No.) |

|

2100 "Q" Street, Sacramento, CA (Address of principal executive offices) |

95816 (Zip Code) |

| 916-321-1844 Registrant's telephone number, including area code |

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Name of each exchange on which registered | |

| Class A Common Stock, par value $.01 per share | New York Stock Exchange |

Securities registered pursuant to Section 12 (g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

o Yes ýNo

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

o Yes ýNo

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

ýYes o No

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

ýYes o No

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of "large accelerated filer," "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer o | Accelerated filer ý | Non-accelerated filer o (Do not check if a smaller reporting company) |

Smaller reporting company o |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). o Yes ý No

Based on the closing price of the registrant's Class A Common Stock on the New York Stock Exchange on June 22, 2012 the last business day of the registrant's second fiscal quarter, the aggregate market value of the voting and non-voting common equity held by non-affiliates was approximately $135.3 million. For purposes of the foregoing calculation only, as required by Form 10-K, the Registrant has included in the shares owned by affiliates, the beneficial ownership of Common Stock of officers and directors of the Registrant and members of their families, and such inclusion shall not be construed as an admission that any such person is an affiliate for any purpose.

Shares outstanding as of February 22, 2013:

Class A Common Stock |

61,170,502 | |||

Class B Common Stock |

24,800,962 |

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant's Definitive Proxy Statement to be delivered to shareholders in connection with the Annual Meeting of Shareholders to be held on May 14, 2013, are incorporated by reference in Part III of this Annual Report on Form 10-K.

Note About Forward-Looking Statements:

This annual report on Form 10-K contains forward-looking statements within the meaning of Section 27A of the Securities Exchange Act of 1934, as amended, including statements relating to future financial performance and operations. These statements are based upon our current expectations and knowledge of factors impacting our business and are generally preceded by, followed by or are a part of sentences that include the words "believes," "expects," "anticipates," "estimates" or similar expressions. All statements, other than statements of historical fact, are statements that could be deemed forward-looking statements. For all of those statements, we claim the protection of the safe harbor for forward-looking statements contained in the Private Securities Litigation Reform Act of 1995. Such statements are subject to risks, trends and uncertainties. A detailed discussion of these and other risks and uncertainties that could cause actual results and events to differ materially from such forward-looking statements is included in the section entitled "Risk Factors" (refer to Part I, Item 1A). We undertake no obligation to revise or update any forward-looking statements except as required under applicable law.

Overview

The McClatchy Company (the "Company," "we," "us" or "our") is a leading local media company that provides both print and digital news and advertising services in the markets we serve. We have more than a century and a half of experience in mass and targeted media with our origins in the California Gold Rush era of 1857. Originally incorporated in California as McClatchy Newspapers, Inc., our three original California newspapers – The Sacramento Bee, The Fresno Bee and The Modesto Bee – were the core of our business until 1979, when we began to diversify geographically outside of California. At that time, we purchased two newspapers in the Northwest, the Anchorage Daily News and the Tri-City Herald in southeastern Washington. In 1986, we purchased The (Tacoma) News Tribune and in 1987, we reincorporated in Delaware. We expanded into the Carolinas when we purchased newspapers in South Carolina in 1990 and The News and Observer Publishing Company in North Carolina in 1995. In 2006, we acquired Knight-Ridder, Inc., retaining 20 daily papers and significant digital assets.

As the third largest newspaper company in the country, based upon daily circulation, our operations include 30 daily newspapers, community newspapers, websites, mobile news and advertising, niche publications, direct marketing and direct mail services. Our newspapers range from large dailies serving metropolitan areas to non-daily newspapers serving small communities. For the year ended December 30, 2012 ("fiscal year 2012"), we had an average paid daily circulation of 2.0 million and Sunday circulation of 2.7 million. We also operate local websites in each of our markets that complement our newspapers and extend our audience reach. Our owned newspapers include, among others, the Fort Worth Star-Telegram, The Sacramento Bee, The Kansas City Star, The Miami Herald, The Charlotte Observer, and The (Raleigh) News & Observer.

Our newspapers are located in 29 diverse, growth markets across the United States. The business is operated across six operating regions: California, Florida, Texas, Southeast, Midwest and Northwest. For the year ended December 30, 2012, no region represented more than 29% of total advertising revenue and no single newspaper represented more than 12.4% of total newspaper revenues. Overall, our markets are expected to achieve household growth faster than the national average from 2013-2015.

We also own a portfolio of premium digital assets, including 15.0% of CareerBuilder, LLC, which operates the nation's largest online job website, CareerBuilder.com; 25.6% of Classified Ventures, LLC, a company that offers classified websites such as the auto website Cars.com and the rental site Apartments.com; 33.3% of HomeFinder, LLC, which operates the online real estate website HomeFinder.com; and 11.4% of Wanderful Media (formerly ShopCo, LLC), owner of Find n Save®, a digital shopping portal that

1

provides advertisers with a common platform to reach online audiences with digital circulars, coupons and display advertising.

McClatchy is listed on the New York Stock Exchange under the symbol MNI.

Strategy

We are committed to a three-pronged strategy to grow our media and advertising business as a leading local media company:

- •

- First, to operate high-quality newspapers in growth markets;

- •

- Second, to operate the leading local digital business in each of our daily newspaper markets, including websites,

e-mail products, mobile services and other electronic media; and

- •

- Third, to extend these franchises by supplementing the mass reach of the newspaper with direct marketing and direct mail products so that advertisers can capture both mass and targeted audiences with one-stop shopping.

Business Initiatives

Our local media businesses have undergone a period of tremendous structural and cyclical change. In order to maintain our position as a leading local media company and implement our strategy, we are focused on the following five major business initiatives:

Increasing Advertising Revenues

Advertising revenues comprise the vast majority of our revenues, making the quality of our sales force of utmost importance. Advertising revenues were approximately 74% of consolidated net revenues in fiscal year 2012 and 75% in the year ended December 25, 2011 ("fiscal year 2011"). Circulation revenues approximated 21% of consolidated net revenues in fiscal years 2012 and 2011.

We have a local sales force in each of our markets and believe that these sales forces are generally larger than those of other local media outlets and websites in those markets. Our sales forces are responsible for delivering to advertisers the broad array of our advertising products, including print, digital and direct marketing products. Our advertisers range from large national retail chains to local automobile dealerships to small businesses and classified advertisers. To reach national advertisers, our newspapers work with national advertising representation firms and our corporate advertising department to develop relationships and make it easier for those large advertisers to place orders.

Increasingly, our emphasis has been on growing the breadth of products offered to advertisers, particularly our digital products, while expanding our relationships with smaller advertisers. Over the last several years we have expanded our "Sunday Select" program, which delivers a package of preprinted advertisements on Sunday to non-newspaper subscribers upon their request. Also we have expanded our popular "Print and Deliver" program, which helps small advertisers create preprinted advertising inserts to reach customers near their stores.

We are also focused on developing new digital advertising products and expanding our digital business as discussed further below.

Expanding McClatchy's Digital Business

Our advertising revenues from digital advertising have increased every year for at least the past 10 years, notwithstanding weak economic conditions and structural changes in the delivery of advertising products to digital media. Our newspaper websites, e-mail projects, podcasts, mobile services and other electronic media enable us to engage our readers with real-time news and information that matters to them. For the year ended December 30, 2012, our newspaper websites attracted an average of approximately 39 million unique visitors per month, of which approximately 25% were utilizing mobile devices.

2

We continue to be a newspaper industry leader in digital advertising revenues from newspaper websites as a percent of total advertising with 21.8% of advertising coming from digital products in fiscal year 2012, compared to 19.9% in fiscal year 2011. For fiscal year 2012, 54.3% of our digital advertising revenues came from advertisements placed only online; that is, they were not tied to a joint print buy, compared to 48.4% in fiscal year 2011. We believe this independent advertising revenue stream bodes well for the future of our digital business and is evidence of its importance as a delivery channel for advertisers.

Beginning in September 2012, five of our newspapers introduced new subscription packages for digital content that ended free, unlimited access to the newspapers' websites and certain mobile content. We expanded this model to our other markets in November and December 2012. The new program ("Plus Program") offers both a combined digital and print subscription and a digital-only subscription. Existing home delivery subscribers are given full access to the digital content and rolled into a bundled print and digital package for an additional fee when their subscription renews. Subscribers may "opt out" of the package and will be charged for print circulation only. A metered paywall on each of the newspaper websites requires users (generally non-subscribers) to pay for content after accessing a limited number of pages or news articles for free each month.

Our websites offer classified digital advertising products provided by companies in which we hold minority investment (as discussed above), including CareerBuilder.com for employment, Cars.com for autos and Apartments.com in the rental category.

We continue to pursue additional new digital products and offerings. In July 2012, we launched the initial phase of impressLOCAL®, our proprietary comprehensive digital marketing solution for local small- and medium-size businesses, which was rolled out to our Forth Worth, Texas and Kansas City, Missouri markets. By offering advertisers integrated packages including website customization, search engine marketing and optimization, social media presence and marketing services, and other multi-platform advertising opportunities, impressLOCAL® helps businesses improve the effectiveness of their marketing and advertising efforts. We expect to continue to roll out impressLOCAL® across certain of our other markets in 2013.

In August 2011, we completed the launch of dealsaver®, our proprietary daily deals service, across all of our markets. Unlike competitors, dealsaver® benefits from the promotional power of our local papers, their related websites and local sales forces. Since late 2010 we have been introducing Find n Save® across our markets. Find n Save® is a digital shopping portal that provides advertisers with a common platform to reach online audiences with digital circulars, coupons and display advertising. We have also partnered with several other leading media and publishing companies to form Wanderful Media, which provides Find n Save® with significant scale. Other investors currently include, among others, Gannett Co., Inc., The Washington Post Company and the Hearst Corporation.

Maintaining Commitment to Public Service Journalism

We believe that high-quality news content is the foundation of the mass reach necessary for the press to play its role in a democratic society. It is also the underpinning of our success in the marketplace.

We are committed to developing best-in-class journalism and local content. Our newspapers have received many national and regional awards from their peers for outstanding journalism, including 52 Pulitzer Prizes and the Robert F. Kennedy Journalism Award for coverage of human rights and social justice in each of the last four years. In February 2013, we were awarded a prestigious George Polk Award for our coverage of the civil war in Syria.

We deliver breaking news as our websites and news delivered on mobile devices compete with television and radio broadcasters for news headlines that can subsequently be expanded in our newspapers. Our news organizations can provide both targeted information and in-depth coverage as needed through newspapers, websites, mobile devices and other developing technologies.

3

We believe our newspapers and digital operations are well-equipped to discover, produce and distribute premium quality content in ways that leverage our size and use technology to find efficiencies in newsgathering and distribution.

Broadening Newspapers' Audiences in Their Local Markets

Each of our daily newspapers has the largest circulation of any newspaper serving its particular community, and coupled with a local website and other digital platforms, reaches a broad audience in each market. We believe that our broad reach in each market is of primary importance in attracting advertising, which is our principal source of revenues.

Daily newspaper paid circulation was down 5.6% and Sunday circulation was down 3.1% in fiscal year 2012 compared with fiscal year 2011, reflecting, in part, print subscription price increases at about half of our newspapers during fiscal year 2012. Circulation volumes are also impacted by fragmentation of audiences faced by all media as available media outlets proliferate and readership trends change. As discussed above, during fiscal year 2012, we introduced the Plus Program digital packages at our daily newspapers. Marketing of the new model was intended, in part, to encourage print readers to take advantage of our content in digital formats. The Plus Program includes subscriptions for both combined digital and print readers and digital-only readers.

Our digital audience continues to show growth, with average local daily unique visitors at our newspapers' websites in fiscal year 2012 up 2.6% from fiscal year 2011. In addition, all our websites now offer mobile-friendly versions for smartphones, and our newspapers' content is available on e-readers, tablets and other mobile devices.

To remain the leading local media company for the communities we serve and a must-buy for advertisers, we are focused on maintaining a broad reach of print and digital audiences in each market we serve. We will continue to refine and strengthen our print platform, but our growth increasingly comes from our digital products and the beneficial impact those products have on the total audience we deliver for our advertisers.

Focusing on Cost Controls

The ongoing structural and cyclical changes in our markets demands that we respond by reengineering and restructuring our operations to achieve an efficient and sustainable cost structure. Over the past five years, we have substantially lowered our cost structure through workforce reductions, optimizing technology and maximizing printing, and distribution and content efficiencies, all while maintaining profitability at each of our newspapers.

Compensation expense is the largest component of our cash operating expenses. Technology increasingly is giving us the ability to operate more efficiently and reduce staff and related compensation expense. We actively look for opportunities to realize efficiencies by outsourcing and centralizing certain functions such as production, circulation, finance, information systems, customer call centers and advertising operations. For instance, 12 of our newspapers are now printed through outsourcing arrangements with nearby newspapers owned by us or other companies. We also believe using technology is an important component of our ability to continue to operate cost-effectively.

Our newspaper operations have emphasized restructuring moves that are generally preferred or acceptable to our audiences and advertisers, such as reducing the width of newspapers or reducing unprofitable circulation that reaches areas outside of a newspaper's core market. We are focusing our efforts on quality content production, effective sales efforts and growth in digital operations.

4

Other Operational Information

Each of our newspapers is largely autonomous in our local advertising and editorial operations in order to meet most effectively the needs of the particular community it serves.

We have two operating segments. Each segment consists primarily of a group of newspapers and related businesses reporting to segment managers that are aggregated into a single reportable segment. One operating segment consists primarily of our newspaper operations in California, the Northwest and Texas while the other operating segment consists primarily of newspaper operations in the Southeast, the Gulf Coast and the Midwest. Publishers of each of the newspapers make the day-to-day decisions and report to vice presidents (segment managers). The segment managers are responsible for implementing the operating and financial plans at each of the newspapers within their respective operating segment. The corporate managers, including executive officers, set the basic business, accounting, financial and reporting policies.

Our newspapers also work together to consolidate functions and share resources regionally and across operational segments that lend themselves to such efficiencies, such as certain regional or national sales efforts, accounting functions, digital publishing systems and products, information technology functions and others. Our corporate advertising department is headed by a vice president of advertising who works with our largest advertisers in placing advertising across our operating segments' newspapers and online products. These efforts are often coordinated through the segment managers and corporate personnel.

Our newspaper business is somewhat seasonal, with peak revenues and profits generally occurring in the second and fourth quarters of each year reflecting the Spring and Thanksgiving and Christmas holidays, respectively. The first and third quarters, when holidays are not prevalent, are historically the slowest quarters for revenues and profits.

5

The following table summarizes the circulation of each of our daily newspapers. These circulation figures are reported on our fiscal year basis and are not meant to reflect Alliance for Audited Media ("AAM") (formerly Audit Bureau of Circulations) reported figures. Some of our fiscal year 2011 circulation volumes have been updated to reflect additional publications, which are now allowed under AAM reporting rules.

| |

2012 | 2011 | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Circulation by Newspaper | Daily | Sunday | Daily | Sunday | |||||||||

Fort Worth Star-Telegram |

201,584 | 271,876 | 204,175 | 233,300 | |||||||||

The Sacramento Bee |

196,519 | 259,957 | 204,638 | 270,171 | |||||||||

The Kansas City (Missouri) Star |

192,304 | 286,200 | 201,140 | 304,547 | |||||||||

The Charlotte Observer |

142,871 | 200,241 | 151,828 | 214,159 | |||||||||

The Miami Herald |

138,148 | 194,548 | 159,123 | 212,875 | |||||||||

The (Raleigh) News & Observer |

124,981 | 184,982 | 131,126 | 192,416 | |||||||||

The Fresno Bee |

107,815 | 165,137 | 109,935 | 141,117 | |||||||||

Lexington Herald-Leader |

84,715 | 108,430 | 91,031 | 116,417 | |||||||||

The (Tacoma) News Tribune |

74,968 | 98,155 | 79,534 | 103,096 | |||||||||

The Wichita Eagle |

66,072 | 91,621 | 69,318 | 101,281 | |||||||||

The (Columbia, SC) State |

65,883 | 120,687 | 72,450 | 129,072 | |||||||||

The Modesto Bee |

58,040 | 69,933 | 60,595 | 72,680 | |||||||||

El Nuevo Herald (Miami, FL) |

53,237 | 68,492 | 56,453 | 71,960 | |||||||||

Idaho Statesman (Boise) |

47,328 | 70,335 | 49,023 | 76,197 | |||||||||

Belleville (Illinois) News-Democrat |

43,901 | 55,769 | 47,347 | 56,880 | |||||||||

Anchorage Daily News |

42,293 | 46,354 | 43,954 | 49,321 | |||||||||

The (Macon, GA) Telegraph |

40,342 | 60,554 | 45,483 | 65,778 | |||||||||

The (Myrtle Beach, SC) Sun News |

34,219 | 46,860 | 36,723 | 51,708 | |||||||||

The (San Luis Obispo, CA) Tribune |

32,948 | 36,783 | 34,046 | 38,408 | |||||||||

(Biloxi, MS) Sun Herald |

31,939 | 36,860 | 35,768 | 41,300 | |||||||||

The Bradenton (Florida) Herald |

30,707 | 41,768 | 32,691 | 44,423 | |||||||||

(Columbus, GA) Ledger-Enquirer |

30,091 | 38,614 | 32,128 | 41,730 | |||||||||

Tri-City (Washington) Herald |

28,272 | 34,194 | 32,046 | 37,409 | |||||||||

The Olympian (Washington) |

22,271 | 27,201 | 24,055 | 29,212 | |||||||||

The (Rock Hill, SC) Herald |

19,420 | 23,477 | 21,491 | 25,776 | |||||||||

The Island Packet (Hilton Head, SC) |

18,992 | 21,881 | 18,655 | 21,526 | |||||||||

(State College, PA) Centre Daily Times |

18,043 | 24,467 | 19,217 | 26,306 | |||||||||

The Bellingham (Washington) Herald |

16,328 | 20,246 | 16,919 | 21,216 | |||||||||

Merced (California) Sun-Star |

12,401 | – | 12,935 | – | |||||||||

The Beaufort (South Carolina) Gazette |

9,224 | 9,477 | 9,747 | 10,105 | |||||||||

Our newspapers are generally delivered by independent contractors, and subscription revenues are recorded net of direct delivery costs.

Other Operations

We also have ownership interests and investments in unconsolidated companies and joint ventures. This includes ownership in premium digital assets, including 15.0% of CareerBuilder, LLC, which operates the nation's largest online job website, CareerBuilder.com; 25.6% of Classified Ventures, LLC, a company that offers classified websites such as the auto website Cars.com and the rental site Apartments.com; and 33.3% of HomeFinder, LLC, which operates the online real estate website HomeFinder.com. In 2011, we became an 11.4% owner of Wanderful Media (formerly ShopCo, LLC), owner of Find n Save®, a digital shopping portal that provides advertisers with a common platform to reach online audiences with digital circulars, coupons and display advertising.

6

We capture significant value from our digital investments, including Classified Ventures and CareerBuilder, which along with other important investments provided us with an additional $38.6 million of cash distributions in fiscal year 2012.

We and the Tribune Company have a joint venture in the McClatchy-Tribune Information Service ("MCT"), which offers stories, graphics, illustrations, photos and paginated pages for print publishers and web-ready content for online publishers. All our newspapers, Washington, D.C. staff and foreign bureaus produce MCT editorial material. Content is also supplied by Tribune Company newspapers and a number of other member newspapers.

We own 49.5% of the voting stock and 70.6% of the nonvoting stock of The Seattle Times Company. The Seattle Times Company owns The Seattle Times newspaper, weekly newspapers in Puget Sound and daily newspapers located in Walla Walla and Yakima, Washington.

In addition, we own a 27.0% interest in Ponderay Newsprint Company ("Ponderay"), a general partnership, which owns and operates a newsprint mill in the state of Washington.

Raw Materials

During fiscal year 2012, we consumed approximately 159,000 metric tons of newsprint compared to 167,000 metric tons in fiscal year 2011 for our operations. The decrease in tons consumed was primarily due to lower advertising sales and circulation volumes. We currently obtain a majority of our supply of newsprint from Ponderay and SP Fiber Technologies (successor to SP Newsprint Co.), as well as a number of other suppliers, primarily under long-term contracts. We have a purchase commitment for 2013 of 81,648 metric tons of newsprint from SP Fiber Technologies.

Our earnings are sensitive to changes in newsprint prices. Newsprint expense accounted for 9.9% of total operating expenses in fiscal year 2012 and 10.3% in fiscal year 2011. However, because we have an ownership interest in Ponderay, an increase in newsprint prices, while negatively affecting our operating expenses, would increase the earnings from our share of this investment, therefore partially offsetting the increase in our newsprint expense. A decline in newsprint prices would have the opposite effect. Ponderay is also impacted by fluctuations in the cost of energy and fiber used in the paper-making process.

We estimate that we will use approximately 142,000 metric tons of newsprint in fiscal 2013, depending on the level of print advertising, circulation volumes and other business considerations. We purchased approximately 131,000 metric tons of newsprint from Ponderay and SP Fiber Technologies in 2012. See the discussion below; Item 7, "Management's Discussion and Analysis of Financial Condition and Results of Operations"; and the financial statements and accompanying notes for further discussion of the impact of these investments on our business.

We fully support recycling efforts. In fiscal year 2012, 97.8% of the newsprint used by our newspapers was made up of some recycled fiber; the average content was 61.8% recycled fiber. This translates into an overall recycled newsprint average of 60.5%. During fiscal year 2012, all of our newspapers collected and recycled press waste, newspaper returns and printing plates.

Competition

Our newspapers, direct marketing programs, websites and mobile content compete for advertising revenues and readers' time with television, radio, other websites, direct mail companies, free shoppers, suburban neighborhood and national newspapers and other publications, and billboard companies, among others. In some of our markets, our newspapers also compete with other newspapers published in nearby cities and towns. Competition for advertising is generally based upon print readership levels and demographics, advertising rates, internet usage and advertiser results, while competition for circulation and readership is generally based upon the content, journalistic quality, service and the price of the newspaper.

7

Our major daily newspapers are the primary general circulation newspaper in each of their respective markets. However, in recent years, newspapers have experienced difficulty maintaining or increasing print circulation levels because of a number of factors, including increased competition from other publications and other forms of media technologies available in various markets, including the internet and other new media formats that are often free for users and the proliferation of news outlets that fragments audiences. In addition, while our newspaper internet sites are generally the leading local sites in each of our major daily newspaper markets, based upon research conducted by us and various independent sources, we have noted changes in readership trends, including a shift of readers to the internet and mobile devices, and have experienced a continued shift of advertising to digital advertising. We face greater competition, particularly in the areas of employment, automotive and real estate advertising, from online competitors. To address the structural shift to digital media, our daily newspapers provide editorial content on a wide variety of platforms and formats – from our daily newspaper to leading local websites; on social network sites such as Facebook and Twitter; on smartphones and on e-readers; on websites and blogs; in niche online publications and in e-mail newsletters; through RSS (rich site summary) feeds and mobile applications. In addition, our websites offer leading digital classified products such as CareerBuilder.com, Cars.com and Apartments.com and retail and national advertising on Find n Save® portals. We also operate dealsaver®, our proprietary daily deals service, in all of our markets.

Employees – Labor

As of December 30, 2012, we had approximately 7,400 full and part-time employees (equating to approximately 6,640 full-time equivalent employees), of whom approximately 6.1% were represented by unions. Most of our union-represented employees are currently working under labor agreements with expiration dates through 2014. We have no unions at 21 of our 30 daily papers.

While our newspapers have not had a strike for decades, and we do not currently anticipate a strike occurring, we cannot preclude the possibility that a strike may occur at one or more of our newspapers when future negotiations occur. We believe that in the event of a newspaper strike we would be able to continue to publish and deliver to subscribers, a capability which is critical to retaining revenues from advertising and circulation, although there can be no assurance that we will be able to continue to publish in the event of a strike.

Compliance with Environmental Laws

We use appropriate waste disposal techniques for items such as ink and other toxic fluids. As of December 30, 2012, we have $1.0 million in letters of credit shared among various state environmental agencies and the U.S. Environmental Protection Agency to provide collateral related to existing or previously removed storage tanks. However, we do not currently have any significant environmental issues and in fiscal years 2012, 2011 and 2010 had no significant expenses or capital expenditures related to environmental control facilities.

Available Information

Our Annual Report on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K, and amendments to reports filed pursuant to Sections 13(a) and 15(d) of the Securities Exchange Act of 1934, as amended (the "Exchange Act"), are filed with the U.S. Securities and Exchange Commission (the "SEC"). We are subject to the informational requirements of the Exchange Act and file or furnish reports, proxy statements and other information with the SEC. Other information includes, among other things, our Corporate Governance Guidelines, charters for each committee of the Board of Directors, Code of Business Conduct and Ethics, and Senior Officers Code of Ethics. Such reports and other information we file with the SEC are available free of charge on our website at www.mcclatchy.com/investor_relations/ and such reports are available on the SEC's website. The public may read and copy any materials we file with the SEC at the SEC's Public Reference Room at 100 F Street, NE, Room 1580, Washington, D.C. 20549. The public may obtain information on the operation of the Public Reference Room by calling the SEC at

8

1-800-SEC-0330. The SEC maintains an internet site that contains reports, proxy and information statements and other information regarding issuers that file electronically with the SEC at www.sec.gov. Paper copies of any such filings and corporate governance documents are available free of charge upon request to The McClatchy Company, 2100 Q Street, Sacramento, CA 95816, Attn: Investor Relations. The contents of these websites are not incorporated into this filing. Further, our references to the URLs for these websites are intended to be an inactive textual reference only.

We have significant competition in the market for news and advertising, which may reduce our advertising and circulation revenues in the future.

Our primary source of revenues is advertising, followed by circulation. In recent years, the advertising industry generally has experienced a secular shift toward internet advertising and away from other traditional media. In addition, our circulation has declined, reflecting general trends in the newspaper industry, including consumer migration toward the internet and other media for news and information. We face increasing competition from other digital sources for both advertising and circulation revenues. This competition has intensified as a result of the continued developments of digital media technologies. Distribution of news, entertainment and other information over the internet, as well as through mobile phones, tablets and other devices, continues to increase in popularity. These technological developments are increasing the number of media choices available to advertisers and audiences. As media audiences fragment, we expect advertisers to continue to allocate larger portions of their advertising budgets to digital media, which through pay-for-performance and keyword-targeted advertising can offer advertisers more directly measurable returns on investment than traditional print media. This increased competition has had and is expected to continue to have an adverse effect on our business and financial results, including negatively impacting revenues and operating income.

Our advertising revenues may decline due to weak general economic and business conditions.

The U. S. economy continues to be in a period of uncertainty. Certain aspects of the economy, including housing, employment and consumer confidence, remain challenging. These challenging economic conditions have had and are expected to continue to have an adverse effect on our advertising revenues. To the extent these economic conditions continue or worsen our business and advertising revenues will be further adversely affected, which could negatively impact our operations and cash flows and our ability to meet the covenants in our debt agreements. Our advertising revenues will be particularly adversely affected if advertisers respond to weak and uneven economic conditions by reducing their budgets or shifting spending patterns or priorities, or if they are forced to consolidate or cease operations. Consolidation across various industries, particularly large department stores and telecommunications companies, may also reduce our overall advertising revenues. In addition, seasonal variations in consumer spending cause our quarterly advertising revenues to fluctuate. Advertising revenues in the second and fourth quarters are typically higher than in the first and third quarters, reflecting the slower economic activity in those quarters and the stronger fourth-quarter holiday season. If general economic conditions and other factors cause a decline in revenues, particularly during the second or fourth quarters, we may not be able to increase or maintain our revenues for the year, which would have an adverse effect on our business and financial results.

In September 2012, we began introducing subscription packages for digital content that ended free, unlimited access to our newspapers' websites and certain mobile content. If we are not successful in the implementation of our digital subscription packages, our ability to produce anticipated circulation revenues and sustain our print and/or digital audiences may be negatively impacted.

Beginning in September 2012, five of our newspapers introduced new subscription packages, our Plus Program, for digital content that ended free, unlimited access to the newspapers' websites and certain mobile content. We expanded this model to our other markets in November and December 2012. The Plus

9

Program includes both a combined digital and print subscription and a digital-only subscription. Existing home delivery subscribers are given full access to the digital content and are automatically enrolled in a bundled print and digital package for an additional fee when their subscription renews. Subscribers who do not wish to take the new package may "opt out" of the package and will be charged for print circulation only. Further, a metered paywall on each of the newspaper websites requires users to pay for content after accessing a limited number of pages or news articles for free each month. Our ability to build a subscriber base on our digital platforms through these packages depends on market acceptance, consumer habits, pricing, an adequate online infrastructure, terms of delivery platforms and other factors. If our print subscribers opt out of the packages in greater numbers than we anticipate, we may not generate expected circulation revenues. In addition, the price increases may result in a loss of print readers, and the paywall may result in fewer page views or unique visitors to our websites if digital viewers are unwilling to pay to gain access to our digital content. Stagnation or a decline in website traffic levels may adversely affect our advertiser base and advertising rates and result in a decline in digital revenues.

Increasing popularity of digital media and the shift in consumer habits and advertising expenditures from traditional print to digital media have adversely affected and may continue to adversely affect our operating revenues and may require significant capital investments due to changes in technology.

Technology in the media industry continues to evolve rapidly. Advances in technology have led to an increasing number of methods for delivery of news and other content and have resulted in a wide variety of consumer demands and expectations, which are also rapidly evolving. If we are unable to exploit new and existing technologies to distinguish our products and services from those of our competitors or adapt to new distribution methods that provide optimal user experiences, our business and financial results may be adversely affected.

Technological developments also pose other challenges that could adversely affect our revenues and competitive position. New delivery platforms may lead to pricing restrictions, the loss of distribution control and the loss of a direct relationship with consumers. We may also be adversely affected if the use of technology developed to block the display of advertising on websites proliferates.

Technological developments and any changes we make to our business model may require significant capital investments. We may be limited in our ability to invest funds and resources in digital products, services or opportunities and we may incur costs of research and development in building and maintaining the necessary and continually evolving technology infrastructure. Some of our existing competitors and new entrants may have greater operational, financial and other resources or may otherwise be better positioned to compete for opportunities and as a result, our digital businesses may be less successful, which could adversely affect our business and financial results.

Our quarterly financial results have fluctuated in the past and will fluctuate in the future. As a result, you should not rely upon past quarterly financial results as indicators of future performance.

Our financial results in any given quarter can be influenced by numerous factors, many of which we are unable to predict or are outside of our control, including:

- •

- the timing of investments, restructuring plans and capital expenditures;

- •

- expenses associated with long-term plans, including our construction of and relocation to a new production

facility and offices in Miami;

- •

- our ability to implement cost controls; and

- •

- the effect of the overall economy on revenues, particularly advertising revenues related to employment, real estate and consumer goods.

Accordingly, our quarterly and annual financial results may vary significantly in the future. The results of prior periods should not be relied upon as an indication of future performance. We cannot provide any

10

assurance that in future quarters, our revenue or operating results will not be below our projections or the expectations of stock market analysts or investors which could cause our stock price to decline.

Our lease for our existing Miami facilities requires that we vacate the existing facilities by the end of May 2013. If the construction of our new facilities for our Miami newspaper operations is not completed by the end of May 2013, we may incur substantial unscheduled additional costs associated with the relocation of the Miami operations.

On May 27, 2011, we sold 14.0 acres of land in Miami, including the building holding the operations of one of our subsidiaries, The Miami Herald Media Company. In connection with the sale, The Miami Herald Media Company entered into a lease agreement with the buyer pursuant to which we have continued to operate our Miami newspaper operations rent free from the existing location through May 2013, while our new facilities are being constructed. We must vacate the facilities by the end of May 2013.

If we are unable to complete the construction of new facilities and move our Miami newspaper operations to the new facilities by May 2013, or if the relocation is otherwise delayed, we may incur substantial costs to produce our newspapers using third-party vendors, or we may not be able to conduct a portion or all of our business until the relocation occurs. In addition, there could be substantial penalties required as a result of breaching our obligation under the lease to vacate our existing facilities by the May 2013 deadline. Any additional costs would adversely affect our results of operations.

If we are unable to execute cost-control measures successfully, our total operating costs may be greater than expected, which may adversely affect our profitability.

As a result of adverse general economic and business conditions and our operating results, we have taken steps to lower operating costs by reducing workforce and implementing general cost-control measures. If we do not achieve expected savings from these initiatives, or if our operating costs increase as a result of these initiatives, our total operating costs may be greater than anticipated. These cost-control measures may also affect our business and our ability to generate future revenue. Because portions of our expenses are fixed costs that neither increase nor decrease proportionately with revenues, we are limited in our ability to reduce costs in the short-term to offset any declines in revenues. If these cost-control efforts do not reduce costs sufficiently or otherwise adversely affect our business, income from continuing operations may decline.

An economic downturn and the impact on our business may result in goodwill and masthead impairment charges.

Due to the economic downturn and the decline in the price of our publicly traded common stock, we recorded masthead impairment charges of $2.8 million in fiscal year 2011 and $59.6 million in fiscal year 2008 and $3.0 billion of goodwill and masthead impairment charges in fiscal year 2007. We currently have goodwill of $1.0 billion. Further erosion of general economic, market or business conditions could have a negative impact on our business and stock price, which may require that we record additional impairment charges in the future.

Our business, reputation and results of operations could be negatively impacted by data security breaches and other security threats and disruptions.

Certain network and information systems are critical to our business activities. Network and information systems may be affected by cyber security incidents that can result from deliberate attacks or system failures. Threats include, but are not limited to, computer hackings, computer viruses, worms or other destructive or disruptive software, or other malicious activities. Our security measures may also be breached due to employee error, malfeasance, or otherwise. As a result of these breaches, an unauthorized party may obtain access to our data or our users' data or our systems may be compromised. These events evolve quickly and often are not recognized until launched against a target, so we may be unable to anticipate these techniques or to implement adequate preventative measures. Our network and information systems may also be compromised by power outages, fire, natural disasters, terrorist attacks, war or other similar events. There can be no assurance that the actions, measures and controls we have

11

implemented will be sufficient to prevent disruptions to mission critical systems, the unauthorized release of confidential information or corruption of data. Although we have experienced cyber security incidents, to date none had a material impact on our financial condition, results of operations or liquidity. Nonetheless, these types of events are likely to occur in the future and such events could disrupt our operations or other third party information technology systems in which we are involved. A significant breakdown, invasion, corruption, destruction or interruption of critical information technology systems, or infrastructure by employees, others with authorized access to our systems, or unauthorized persons could result in legal or financial liability or otherwise negatively impact our operations. They also could require significant management attention and resources, and could negatively impact our reputation among our customers, advertisers and the public, which could have a negative impact on our financial condition, results of operations or liquidity.

We are subject to significant financial risk as a result of our $1.6 billion in total consolidated debt.

As of December 30, 2012, we had approximately $1.7 billion in total principal indebtedness outstanding, including current portion of long-term debt of $83.6 million in 11.50% senior secured notes, resulting from our commitment to redeem these notes by January 17, 2013. In February 2013, we purchased $48.5 million aggregate principal amount of our outstanding debt, in the open market, which consisted of $37.5 million aggregate principal amount of our 4.625% notes due in 2014 and $11.0 million aggregate principal amount of our 5.750% notes due in 2017. As a result of the redemptions and purchases, we reduced our total consolidated debt to $1.6 billion as of the filing of this annual report on Form 10-K. Additionally, after the purchases in February 2013 we have $304.1 million aggregate principal amounts with scheduled maturity dates in 2014 and 2017. This level of debt increases our vulnerability to general adverse economic and industry conditions and we will likely need to refinance our debt prior to its scheduled maturity. Higher leverage ratios, our credit ratings or other factors outside of our control could adversely affect our future ability to refinance maturing debt on commercially acceptable terms, or at all, or the ultimate structure of such refinancing.

Covenants in the indenture governing the notes and our other existing debt agreements will restrict our business in many ways.

The indenture governing our 9.00% Senior Secured Notes due in 2022 (the "9.00% Notes") and our secured credit agreement contain various covenants that limit, subject to certain exceptions, our ability and/or our restricted subsidiaries' ability to, among other things:

- •

- incur or assume liens;

- •

- incur additional debt or provide guarantees in respect of obligations of other persons;

- •

- issue redeemable stock and preferred stock;

- •

- pay dividends or make distributions on capital stock, repurchase, redeem or make payments on capital stock or prepay,

repurchase, redeem, retire, defease, acquire or cancel certain of our existing notes or debentures prior to the stated maturity thereof;

- •

- make loans, investments or acquisitions;

- •

- create or permit restrictions on the ability of our subsidiaries to pay dividends or make other distributions to us or to

guarantee our debt, limit our or any of our subsidiaries' ability to create liens, or make or pay intercompany loans or advances;

- •

- enter into certain transactions with affiliates;

- •

- sell, transfer, license, lease or dispose of our or our subsidiaries' assets, including the capital stock of our subsidiaries; and

12

- •

- dissolve, liquidate, consolidate or merge with or into, or sell substantially all the assets of us and our subsidiaries, taken as a whole, to, another person

The restrictions contained in the indenture governing the 9.00% Notes and the secured credit agreement could adversely affect our ability to:

- •

- finance our operations;

- •

- make needed capital expenditures;

- •

- make strategic acquisitions or investments or enter into alliances;

- •

- withstand a future downturn in our business or the economy in general;

- •

- refinance our outstanding indebtedness prior to maturity;

- •

- engage in business activities, including future opportunities, that may be in our interest; and

- •

- plan for or react to market conditions or otherwise execute our business strategies.

Our ability to comply with covenants contained in the indenture for the 9.00% Notes and our secured credit agreement may be affected by events beyond our control, including prevailing economic, financial and industry conditions. Even if we are able to comply with all of the applicable covenants, the restrictions on our ability to manage our business in our sole discretion could adversely affect our business by, among other things, limiting our ability to take advantage of financings, mergers, acquisitions and other corporate opportunities that we believe would be beneficial to us. In addition, our obligations under the 9.00% Notes and the secured credit agreement are secured, subject to permitted liens, on a first-priority basis, and such security interests could be enforced in the event of default by the collateral agent for the secured credit agreement. In the event of such an enforcement, we cannot assure you that the proceeds from an enforcement would be sufficient to pay our obligations under the 9.00% Notes or secured credit agreement or at all.

In the future, we will need to repay our existing indebtedness and meet our obligations, and the failure to do so will adversely affect our business.

We may not be able to generate sufficient cash internally to repay all of our indebtedness at maturity or to meet our other obligations. As of December 30, 2012, we had approximately $1.7 billion of total indebtedness outstanding, which was reduced to $1.6 billion by the end of February 2013, with our redemption of the then-outstanding 11.50% senior secured notes and the purchases of additional notes. As of the end of fiscal year 2012, the projected benefit obligations of our qualified defined benefit pension plan ("Plan") exceeded plan assets by $587.9 million. While amounts of future contributions are subject to numerous assumptions, including, among others, changes in interest rates, returns on assets in the Plan and future government regulations, we estimate that a total of approximately $25 million will be required to be contributed to the Plan in fiscal year 2014. In addition, we have a limited number of supplemental retirement plans, which provide certain key employees with additional retirement benefits. These plans have no assets; however as of December 30, 2012, our projected benefit obligations of these plans was $126.4 million. These plans are on a pay-as-you-go basis. Our ability to make payments on and to refinance our indebtedness, including the 9.00% Notes and our other series of outstanding notes, to make required contributions to the Plan, fund the supplemental retirement plans and to fund working capital needs and planned capital expenditures will depend on our ability to generate cash in the future. Our ability to generate cash, to a certain extent, is subject to general economic, financial, competitive, business, legislative, regulatory and other factors that are beyond our control.

If our business does not generate sufficient cash flow from operations or if future borrowings are not available to us in an amount sufficient to enable us to pay our indebtedness, including the 9.00% Notes and our other series of outstanding notes or to fund our other liquidity needs, we may need to refinance all or a portion of our indebtedness, on or before the maturity thereof, reduce or delay capital investments or seek

13

to raise additional capital, any of which could have a material adverse effect on our operations. In addition, we may not be able to effect any of these actions, if necessary, on commercially reasonable terms or at all. Our ability to restructure or refinance our indebtedness will depend on the condition of the capital markets and our financial condition at such time. Any refinancing of our debt could be at higher interest rates and may require us to comply with more onerous covenants, which could further restrict our business operations or our ability to refinance our existing debt. The terms of existing or future debt instruments, including the indenture governing the 9.00% Notes offered hereby, may limit or prevent us from taking any of these actions. In addition, any failure to make scheduled payments of interest and principal on our outstanding indebtedness would likely result in a reduction of our credit rating, which could harm our ability to incur additional indebtedness on commercially reasonable terms or at all. Our inability to generate sufficient cash flow to satisfy our debt service obligations, or to refinance or restructure our obligations on commercially reasonable terms or at all, would have an adverse effect, which could be material, on our business, financial condition and results of operations, as well as on our ability to satisfy our obligations in respect of our outstanding debt.

As of December 30, 2012, we had approximately $36.1 million in face amount of letters of credit outstanding under the secured credit agreement and a current portion due on long-term debt of $83.6 million of 11.50% senior secured notes. The remaining $83.6 million of 11.50% senior secured notes was redeemed by January 17, 2013. In February 2013, we purchased $48.5 million aggregate principal amount of our outstanding debt, in the open market, which consisted of $37.5 million aggregate principal amount of our 4.625% notes due in 2014 and $11.0 million aggregate principal amount of our 5.750% notes due in 2017. As a result of the redemptions and purchases in early 2013, we reduced our total outstanding indebtedness to $1.6 billion. Of the $1.6 billion, we have approximately $28.9 million of notes with an interest rate of 4.625% due in 2014; approximately $275.1 million of notes with an interest rate of 5.750% due in 2017; $910 million of 9.00% Notes; approximately $89.2 million of debentures with an interest rate of 7.150% due in 2027 and approximately $276.2 million of debentures with an interest rate of 6.875% due in 2029.

We may not be able to pay for or refinance existing obligations or raise any required additional capital or do so on favorable terms. Borrowing costs related to future capital raising activities may be significantly higher than our current borrowing costs, and we may not be able to raise additional capital on favorable terms, or at all, if unsettled conditions in financial markets continue to exist. We may be forced to cancel or scale back our business activities, and we may be unable to refinance our debt.

We require newsprint for operations and, therefore, our operating results may be adversely affected if the price of newsprint increases or if we experience disruptions in our newsprint supply chain.

Newsprint is the major component of our cost of raw materials. Newsprint accounted for 9.9% of our operating expenses in the year ended December 30, 2012. Accordingly, our earnings are sensitive to changes in newsprint prices. The price of newsprint has historically been volatile and may increase as a result of various factors, including:

- •

- declining newsprint supply from mill closures;

- •

- reduction in newsprint suppliers because of consolidation in the newsprint industry;

- •

- paper mills reducing their newsprint supply because of switching their production to other paper grades; and

- •

- a decline in the financial situation of newsprint suppliers.

We have not attempted to hedge price fluctuations in the normal purchases of newsprint or enter into contracts with embedded derivatives for the purchase of newsprint other than the natural hedge created by our ownership interest in Ponderay. If the price of newsprint increases materially, operating results could be adversely affected. In addition, we rely on a limited number of suppliers for deliveries of newsprint. If

14

newsprint suppliers experience labor unrest, transportation difficulties or other supply disruptions, our ability to produce and deliver newspapers could be impaired and/or the cost of the newsprint could increase, both of which would negatively affect our operating results.

A portion of our employees are members of unions, and if we experience labor unrest, our ability to produce and deliver newspapers could be impaired.

If we experience labor unrest, our ability to produce and deliver newspapers could be impaired in some locations. In addition, the results of future labor negotiations could harm our operating results. Our newspapers have not experienced a labor strike for decades. However, we cannot ensure that a strike will not occur at one or more of our newspapers in the future. As of December 30, 2012, approximately 6.1% of full-time and part-time employees were represented by unions. Most of our union-represented employees are currently working under labor agreements, with expiration dates through 2014. We face collective bargaining upon the expirations of these labor agreements. Even if our newspapers do not suffer a labor strike, our operating results could be harmed if the results of labor negotiations restrict our ability to maximize the efficiency of our newspaper operations. In addition, our ability to make short-term adjustments to control compensation and benefits costs, rebalance our portfolio of businesses or otherwise adapt to changing business needs may be limited by the terms and duration of our collective bargaining agreements.

We may be required to make greater contributions to our qualified defined benefit pension plans in the next several years than previously required, placing greater liquidity needs upon our operations.

The adverse conditions in the capital markets in 2008 had a significantly negative impact on the investment funds in our qualified defined benefit pension plan ("Plan"), which has been partially offset by returns in the capital markets since the end of 2008. The projected benefit obligations of the Plan exceeded plan assets by $587.9 million as of December 30, 2012, an increase of $165.4 million from December 25, 2011. In January 2013, we contributed $7.5 million to the Plan, reducing the underfunded obligation to $580.4 million.

The excess of benefit obligations over pension assets is expected to give rise to required pension contributions over the next several years. Legislation enacted in the second quarter of 2012 mandated a change in the discount rates used to calculate the projected benefit obligations for purposes of funding pension plans. The new legislation and calculation uses historical averages of long-term highly-rated corporate bonds (within ranges as defined in the legislation) which have an impact of applying a higher discount rate to determine the projected benefit obligations for funding and current long-term interest rates. Also, the Pension Relief Act of 2010 ("PRA") provided relief in the funding requirements of the Plan, and we have elected an option that allows the funding related to our 2009 and 2011 plan years required contributions to be paid over 15 years. However, even with the relief provided by these legislative rules, we expect future contributions to be required. In addition, adverse conditions in the capital markets and/or lower long-term interest rates may result in greater annual contribution requirements. In addition, adverse conditions in the capital markets and/or lower long-term interest rates may result in greater annual contribution requirements, placing greater liquidity needs upon our operations.

We have invested in certain digital ventures, but such ventures may not be as successful as expected, which could adversely affect our results of operations.

We continue to evaluate our business and make strategic investments in digital ventures, either alone or with partners, to further our digital growth. We have, among others, investments with other partners in CareerBuilder LLC, which operates the nation's largest online job site, CareerBuilder.com, Classified Ventures, LLC, which operates Cars.com, Apartments.com and other classified websites, and HomeFinder LLC, which operates the real estate website HomeFinder.com. The success of these ventures may be dependent to an extent on the efforts of our partners. Further, our ability to monetize the investments and/or the value we may receive upon any disposition may depend on the actions of our

15

partners. As a result, our ability to control the timing or process relating to a disposition may be limited, which could adversely affect the liquidity of these investments or the value we may ultimately attain upon disposition. If the value of the companies in which we invest declines, we may be required to record a charge to earnings. There can be no assurances that we will receive a return on these investments or that they will result in advertising growth or will produce equity income or capital gains in future years.

If we are not successful in growing and managing our digital businesses, our business, financial condition and prospects will be adversely affected.

Our future growth depends to a significant degree upon the development and management of our digital businesses. The growth of our digital businesses over the long term depends on various factors, including, among other things, the ability to:

- •

- continue to increase digital audiences;

- •

- attract advertisers to our websites;

- •

- maintain or increase the advertising rates on our websites;

- •

- exploit new and existing technologies to distinguish our products and services from those of competitors and develop new

content, products and services; and

- •

- invest funds and resources in digital opportunities.

In addition, we expect that our digital business will continue to increase as a percentage of our total revenues in future periods. For the year ended December 30, 2012, digital advertising revenues comprised 21.8% of total advertising revenues, as compared to 19.9% for fiscal year 2011. As our digital business becomes a greater portion of our overall business, we will face a number of increased risks from managing our digital operations, including, but not limited, to the following:

- •

- restructuring our sales force to effectively sell advertising in the digital advertising arena versus our historical print

advertising business;

- •

- attracting and retaining employees with skill sets and knowledge base needed to successfully operate in digital business;

and

- •

- managing the transition to a digital business from a historical print focused business and the need to concurrently reduce the physical infrastructure, distribution infrastructure and related fixed costs associated with the historical print business.

The proliferation of digital media options on the internet provides consumers with a large number of alternative news choices that compete with traditional media companies and could adversely impact our operating results.

The increasing number of digital media options available on the internet, through social networking tools and through mobile and other devices distributing news and other content, is expanding consumer choice significantly. Faced with a multitude of media choices and a dramatic increase in accessible information, consumers may place greater value on when, where, how and at what price they consume digital content than they do on the source or reliability of such content. News aggregation websites and customized news feeds (often free to users) may reduce our traffic levels by creating a disincentive for the audience to visit our websites or use our digital applications. Online traffic is also driven by internet search results. Search engines frequently update and change the methods for directing search queries to web pages or change methodologies and metrics for valuing the quality and performance of internet traffic on delivering cost-per-click advertisements. The failure to successfully manage search engine optimization efforts across our businesses could result in significant decreases in traffic to our various websites, which could result in substantial decreases in conversion rates and repeat business, as well as increased costs if we were to replace free traffic with paid traffic, any or all of which could adversely affect our business, financial condition and results of operations. If traffic levels stagnate or decline, we may not be able to create

16

sufficient advertiser interest in our digital businesses or to maintain or increase the advertising rates of the inventory on our digital platforms.

Circulation declines could adversely affect our circulation and advertising revenues and circulation price increases could exacerbate declines in circulation volumes.

Advertising and circulation revenues are affected by circulation and readership levels of our newspapers. In recent years, newspapers have experienced difficulty maintaining or increasing print circulation levels because of a number of factors, including:

- •

- increased competition from other publications and other forms of media technologies available in various markets,

including the internet and other new media formats that are often free for users;

- •

- continued fragmentation of media audiences;

- •

- a growing preference among some consumers to receive all or a portion of their news other than from a newspaper;

- •

- increases in subscription and newsstand rates; and

- •

- declining discretionary spending by consumers affected by negative economic conditions.

These factors could also affect our newspapers' ability to institute circulation price increases for print products. Also, print price increases have historically had an initial negative impact on circulation volumes that may not be mitigated with additional marketing and promotion. A prolonged reduction in circulation would have a material adverse effect on advertising revenues. To maintain our circulation base, we may be required to incur additional costs that we may not be able to recover through circulation and advertising revenues.

Developments in the laws and regulations to which we are subject, may result in increased costs and lower advertising revenues from our digital businesses.

We are generally subject to government regulation in the jurisdictions in which we operate. In addition, our websites are available worldwide and are subject to laws regulating the internet both within and outside the United States. We may incur increased costs necessary to comply with existing and newly adopted laws and regulations or penalties for any failure to comply. Advertising revenues from our digital businesses could be adversely affected, directly or indirectly, by existing or future laws and regulations relating to the use of consumer data in digital media.

Adverse results from litigation or governmental investigations can impact our business practices and operating results.

From time to time, we and our subsidiaries are parties to litigation and regulatory, environmental and other proceedings with governmental authorities and administrative agencies. Adverse outcomes in lawsuits or investigations could result in significant monetary damages or injunctive relief that could adversely affect our operating results or financial condition as well as our ability to conduct our business as it is presently being conducted.

ITEM 1B. UNRESOLVED STAFF COMMENTS

None

Our corporate headquarters are located at 2100 "Q" Street, Sacramento, California. At December 30, 2012, we had newspaper production facilities in 17 markets in 13 states. Our facilities vary in size and in total occupy about 7.0 million square feet. Approximately 2.4 million of the total square footage is leased

17

from others, while we own the properties for the remaining square footage. We own substantially all of our production equipment, although certain office equipment is leased.

We maintain our properties in good condition and believe that our current facilities are adequate to meet the present needs of our newspapers.

We are subject to a variety of legal proceedings (including libel, employment, wage and hour, independent contractor and other legal actions) and government proceedings (including environmental matters) that arise from time to time in the ordinary course of our business. Litigation is inherently unpredictable, and outcomes are typically uncertain, and our past experience does not provide any additional visibility or predictability to estimate the range of loss that may occur because the costs, outcome and status of these types of claims and proceedings have varied significantly in the past. Accordingly, we are unable to estimate the amount or range of reasonably possible losses. Historically, such claims and proceedings have not had a material adverse effect upon our consolidated results of operations or financial condition.

ITEM 4. MINE SAFETY DISCLOSURES

None

18

ITEM 5. MARKET FOR REGISTRANT'S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY

SECURITIES.

The McClatchy Company's (the "Company," "we," "us" or "our") Class A Common Stock is listed on the New York Stock Exchange ("NYSE") under the symbol "MNI". A small amount of Class A Common Stock is also traded on other exchanges. Our Class B Common Stock is not publicly traded. As of February 22, 2013, there were approximately 5,355 and 20 record holders of our Class A and Class B Common Stock, respectively. The following table lists the high and low prices of our Class A Common Stock as reported by the NYSE for each fiscal quarter of 2012 and 2011:

| Fiscal Year 2012 Quarters Ended: | High | Low | |||

|---|---|---|---|---|---|

March 25, 2012 |

$3.04 | $2.22 | |||

June 24, 2012 |

$2.96 | $1.98 | |||

September 23, 2012 |

$2.42 | $1.50 | |||

December 30, 2012 |

$3.45 | $2.18 |

| Fiscal Year 2011 Quarters Ended: | High | Low | |||

|---|---|---|---|---|---|

March 27, 2011 |

$5.61 | $3.21 | |||

June 26, 2011 |

$3.75 | $2.30 | |||

September 25, 2011 |

$2.91 | $1.25 | |||

December 25, 2011 |

$2.41 | $1.05 |

Dividends:

During fiscal year 2009, we suspended our quarterly dividend and therefore we did not pay any cash dividends in the fiscal years 2012 or 2011. The payment and amount of future dividends remain within the discretion of the Board of Directors and will depend upon our future earnings, financial condition, and other factors considered relevant by the Board of Directors. Also, the amount of future dividends is governed by reaching certain leverage levels of earnings before interest, taxes, depreciation and amortization under our debt agreements.

Equity Securities:

During the year ended December 30, 2012, we did not sell any equity securities of the Company, which were not registered under the Securities Act of 1933, as amended. During the year ended December 30, 2012, we did not repurchase any equity securities.

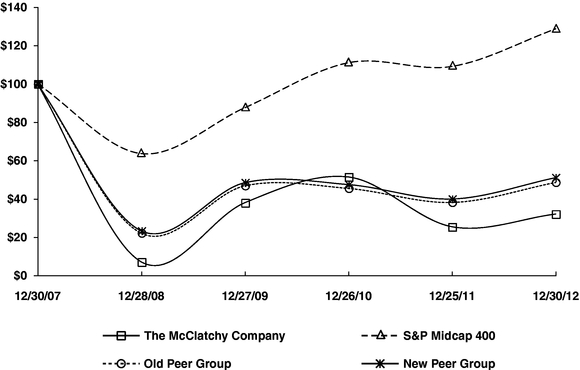

Performance Graph:

The following graph compares the cumulative five-year total return attained by shareholders on The McClatchy Company's common stock versus the cumulative total returns of the S&P Midcap 400 index, a customized peer group composed of six companies ("New Peer Group") and a customized peer group composed of nine companies used during the fiscal year ended December 25, 2011 ("Old Peer Group").

Our New Peer Group is customized to include six companies that are publicly traded with at least 40% of their revenues from newspaper publishing. This peer group includes: A. H. Belo Corp., E.W. Scripps Company, Gannett Co., Journal Communications Inc., Lee Enterprises Inc. and New York Times Company. In customizing the New Peer Group we removed three companies that were included in Old Peer Group: Gatehouse Media Inc., Media General Inc., and Sun-Times Media Group, Inc. These companies were removed because they are no longer publicly traded or are smaller reporting companies.

19

COMPARISON OF 5 YEAR CUMULATIVE TOTAL RETURN*

Among The McClatchy Company, the S&P Midcap 400 Index,

Old Peer Group, and New Peer Group

*$100 invested on 12/30/07 in stock or 12/31/07 in index, including reinvestment of dividends.

Index calculated on month-end basis.

Copyright© 2013 S&P, a division of The McGraw-Hill Companies Inc. All rights reserved.

| |

Fiscal Years Ended: | ||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| |

12/30/07 | 12/28/08 | 12/27/09 | 12/26/10 | 12/25/11 | 12/30/12 | |||||||||||||

The McClatchy Company |

$ | 100 | $ | 7 | $ | 38 | $ | 51 | $ | 25 | $ | 32 | |||||||

S&P Midcap 400 |

$ | 100 | $ | 64 | $ | 88 | $ | 111 | $ | 109 | $ | 129 | |||||||

Old Peer Group |

$ | 100 | $ | 22 | $ | 47 | $ | 46 | $ | 38 | $ | 49 | |||||||

New Peer Group |

$ | 100 | $ | 23 | $ | 49 | $ | 48 | $ | 40 | $ | 51 | |||||||

20

ITEM 6. SELECTED FINANCIAL DATA

The selected financial data set forth below should be read in conjunction with Item 7 – "Management's Discussion and Analysis of Financial Condition and Results of Operations," our consolidated financial statements and the related notes, and other financial data included elsewhere in this annual report. Historical results are not necessarily indicative of the results to be expected in future periods.

| (in thousands, except per share amounts) |

December 30, 2012 (1) |

December 25, 2011 |

December 26, 2010 |

December 27, 2009 |

December 28, 2008 |

|||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

REVENUES – NET: |

||||||||||||||||

Advertising |

$ | 914,738 | $ | 956,305 | $ | 1,049,964 | $ | 1,143,129 | $ | 1,568,766 | ||||||

Circulation |

263,286 | 262,335 | 272,776 | 278,256 | 265,584 | |||||||||||

Other |

52,700 | 51,000 | 52,492 | 50,199 | 66,106 | |||||||||||

|