UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 6-K

REPORT OF FOREIGN PRIVATE ISSUER PURSUANT TO RULE 13a-16 OR 15d-16 UNDER THE SECURITIES EXCHANGE ACT OF 1934

February 9, 2023

Commission File Number 001-15244

Credit Suisse Group AG

(Translation of registrant’s name into English)

Paradeplatz 8, 8001 Zurich, Switzerland

(Address of principal executive office)

Commission File Number 001-33434

Credit Suisse AG

(Translation of registrant’s name into English)

Paradeplatz 8, 8001 Zurich, Switzerland

(Address of principal executive office)

Indicate by check mark whether the registrant files or will file annual reports under cover of Form 20-F or Form 40-F.

Form 20-F  Form 40-F

Form 40-F

Form 40-F

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(1):

Note: Regulation S-T Rule 101(b)(1) only permits the submission in paper of a Form 6-K if submitted solely to provide an attached annual report to security holders.

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(7):

Note: Regulation S-T Rule 101(b)(7) only permits the submission in paper of a Form 6-K if submitted to furnish a report or other document that the registrant foreign private issuer must furnish and make public under the laws of the jurisdiction in which the registrant is incorporated, domiciled or legally organized (the registrant’s “home country”), or under the rules of the home country exchange on which the registrant’s securities are traded, as long as the report or other document is not a press release, is not required to be and has not been distributed to the registrant’s security holders, and, if discussing a material event, has already been the subject of a Form 6-K submission or other Commission filing on EDGAR.

This report includes the media release and the slides for the presentation to investors in connection with the 4Q22 results.

|

Media Release

Zurich, February 9, 2023

|

|

Ad hoc announcement pursuant to Art. 53 LR

Credit Suisse makes strong progress on Group strategic priorities; reports net revenues of CHF 3.1 bn and pre-tax loss of CHF 1.3 bn along

with a CET1 ratio of 14.1% in 4Q22

“2022 was a crucial year for Credit Suisse. We announced our strategic plan to create a simpler, more focused bank, built around client needs and since October we have been executing at pace. We successfully raised CHF ~4 billion in equity

capital, accelerated the delivery of our ambitious cost targets, and are making strong progress on the radical restructuring of our Investment Bank. Today’s announcement of our acquisition of the M. Klein & Company investment banking business marks another milestone in the carveout of CS First Boston as a leading independent capital markets and advisory business. The transaction should further strengthen CS First Boston’s advisory and capital

markets capabilities.

We have a clear plan to create a new Credit Suisse and intend to continue to deliver on our three-year strategic transformation by re-shaping our portfolio, reallocating capital, right-sizing our cost base, and building on our leading

franchises.”

Ulrich Körner, Chief Executive Officer of Credit Suisse Group AG

_______________________________________________________________________________________________________________________________________________________________________________________________________________________________

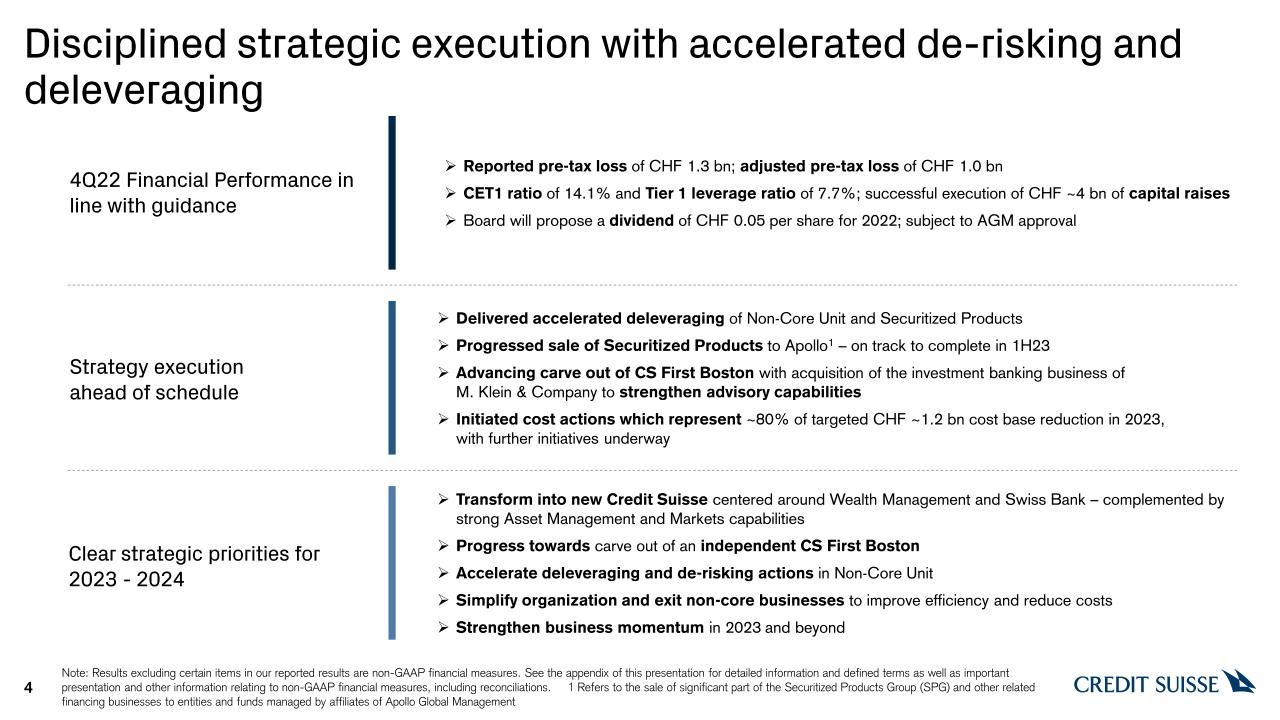

Disciplined strategic execution and accelerated de-risking and deleveraging

|

4Q22 financial performance in line with guidance

|

▪ Reported pre-tax loss of CHF 1.3 bn; adjusted* pre-tax loss of

CHF 1.0 bn

▪ CET1 ratio of 14.1%, Tier 1 leverage ratio of 7.7%

▪ Improved average Liquidity

Coverage Ratio (LCR) of 144%1 at the end of 4Q22 from lower levels in the quarter

▪ Board will propose a cash dividend of CHF 0.05 per share for

2022; subject to shareholder approval at the 2023 Annual General Meeting

|

|

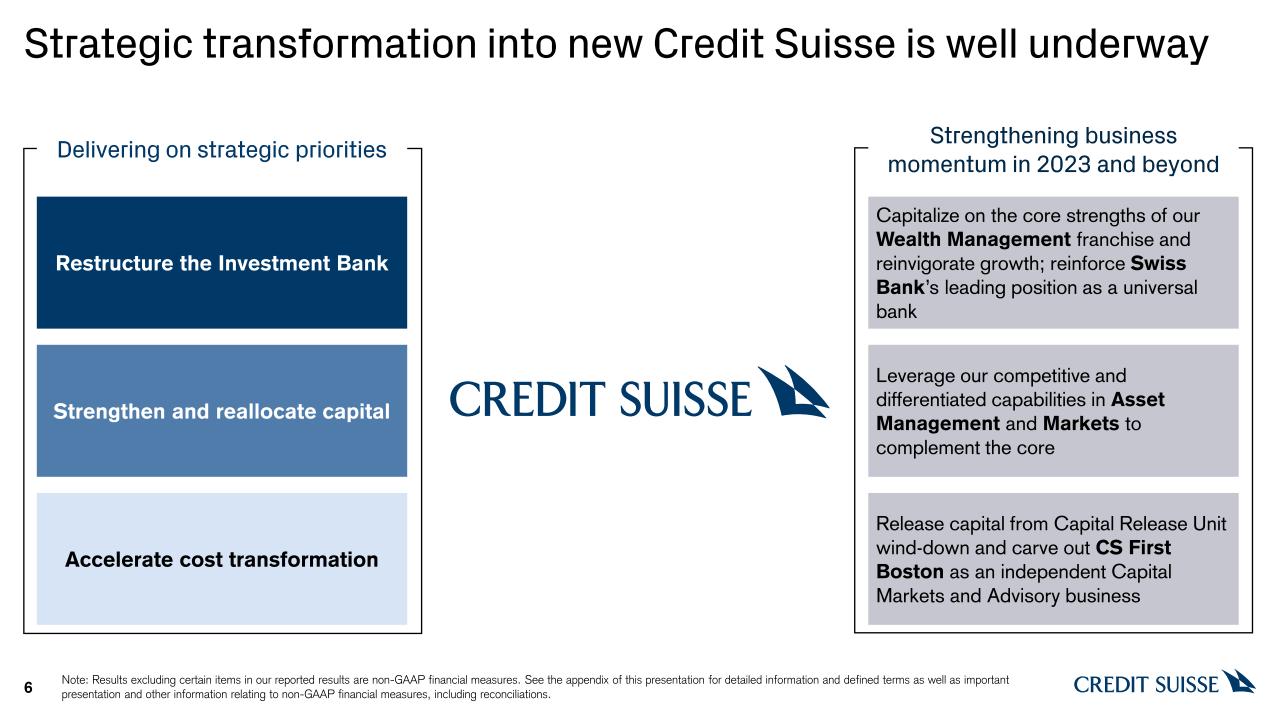

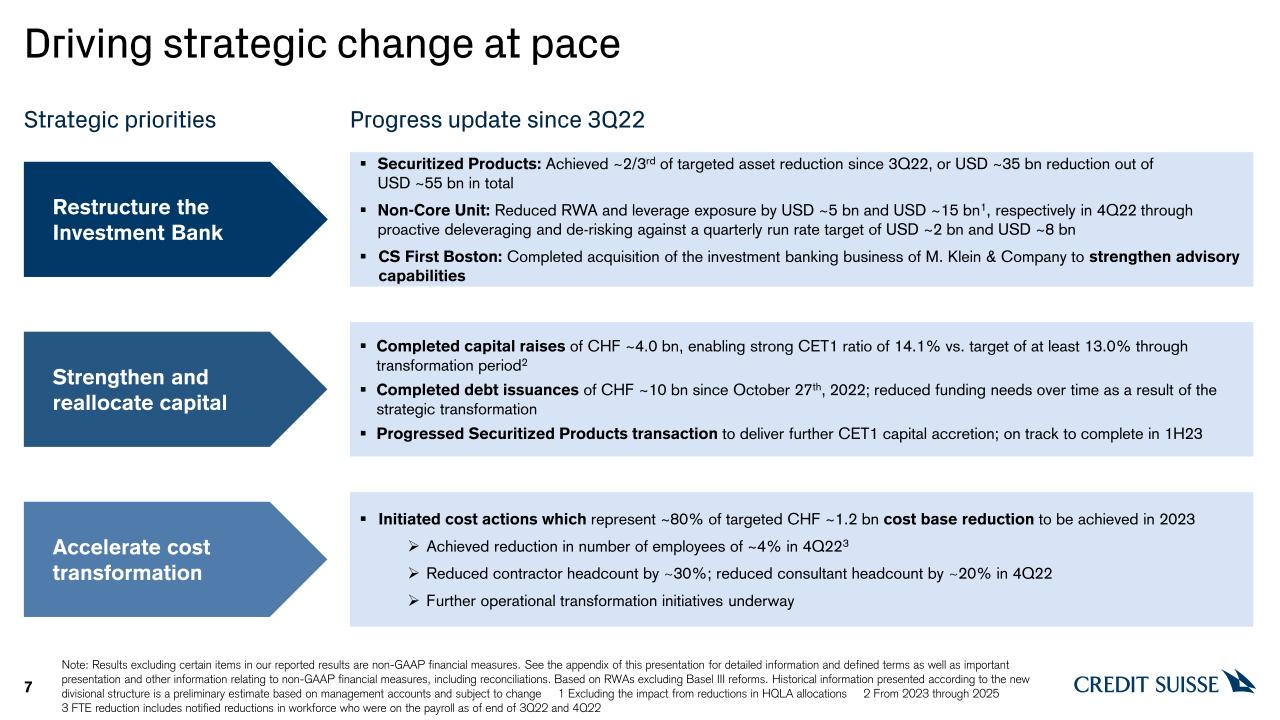

Strategy execution ahead of schedule

|

▪ Strong execution of strategic

actions from a position of capital strength; successful execution of CHF ~4 bn of capital raises

▪ Delivered accelerated deleveraging

of Non-Core Unit (NCU)2 and Securitized Products Group (SPG)

▪ Progressed sale of SPG to Apollo

Global Management3 with first closing of the sale completed on February 8, 2023. On track to complete in 1H23

▪ Announced next milestone in the

carveout of CS First Boston with acquisition of The Klein Group LLC4, the investment banking business of M. Klein & Company LLC to strengthen advisory

and capital markets capabilities

▪ Initiated cost transformation actions in 4Q22, which are

expected to represent ~80% of targeted CHF ~1.2 bn cost base reduction to be achieved in FY23, with further initiatives underway

|

|

Clear strategic priorities for 2023-2024

|

▪ Transform into new Credit Suisse centered around Wealth

Management and Swiss Bank complemented by strong Asset Management and Markets capabilities

▪ Progress towards the carveout of an independent CS First Boston

▪ Accelerate deleveraging and de-risking actions in Non-Core Unit

▪ Simplify organization and exit non-core businesses to improve

efficiency and reduce costs

▪ Strengthen business momentum in 2023 and beyond

|

|

Media Release

Zurich, February 9, 2023

|

|

Credit Suisse Group results for 4Q22 and FY22

|

Reported (CHF mn)

|

4Q22

|

3Q22

|

4Q21

|

Δ3Q22

|

Δ4Q21

|

FY22

|

FY21

|

ΔFY21

|

|

Net revenues

|

3,060

|

3,804

|

4,582

|

(20)%

|

(33)%

|

14,921

|

22,696

|

(34)%

|

|

Provision for credit losses

|

41

|

21

|

(20)

|

-

|

-

|

16

|

4,205

|

-

|

|

Total operating expenses

|

4,334

|

4,125

|

6,266

|

5%

|

(31)%

|

18,163

|

19,091

|

(5)%

|

|

Pre-tax income/(loss)

|

(1,315)

|

(342)

|

(1,664)

|

-

|

-

|

(3,258)

|

(600)

|

-

|

|

Income tax expense/(benefit)

|

82

|

3,698

|

416

|

(98)%

|

(80)%

|

4,048

|

1,026

|

-

|

|

Net income/(loss) attributable to shareholders

|

(1,393)

|

(4,034)

|

(2,085)

|

-

|

-

|

(7,293)

|

(1,650)

|

-

|

|

Return on tangible equity

|

(13.5)%

|

(38.3)%

|

(20.9)%

|

-

|

-

|

(17.6)%

|

(4.2)%

|

-

|

|

Cost/income ratio

|

142%

|

108%

|

137%

|

-

|

-

|

122%

|

84%

|

-

|

|

Net New Assets (NNA)/Net Asset Outflows - CHF bn

|

(110.5)

|

(12.9)

|

1.6

|

-

|

-

|

(123.2)

|

30.9

|

-

|

|

Assets under Management (AuM) - CHF bn

|

1,294

|

1,401

|

1,614

|

-

|

-

|

1,294

|

1,614

|

-

|

|

|

||||||||

|

Adjusted* (CHF mn)

|

4Q22

|

3Q22

|

4Q21

|

Δ3Q22

|

Δ4Q21

|

FY22

|

FY21

|

ΔFY21

|

|

Net revenues

|

2,964

|

3,798

|

4,384

|

(22)%

|

(32)%

|

15,164

|

22,544

|

(33)%

|

|

Provision for credit losses

|

41

|

21

|

(15)

|

-

|

-

|

171

|

(102)

|

-

|

|

Total operating expenses

|

3,938

|

3,869

|

4,071

|

2%

|

(3)%

|

16,242

|

16,047

|

1%

|

|

Pre-tax income/(loss)

|

(1,015)

|

(92)

|

328

|

-

|

-

|

(1,249)

|

6,599

|

-

|

|

Capital ratios

|

4Q22

|

3Q22

|

4Q21

|

Δ3Q22

|

Δ4Q21

|

FY22

|

FY21

|

ΔFY21

|

|

CET1 ratio

|

14.1%

|

12.6%

|

14.4%

|

-

|

-

|

14.1%

|

14.4%

|

-

|

|

Tier 1 leverage ratio

|

7.7%

|

6.0%

|

6.1%

|

-

|

-

|

7.7%

|

6.1%

|

-

|

|

CET1 leverage ratio

|

5.4%

|

4.1%

|

4.3%

|

-

|

-

|

5.4%

|

4.3%

|

-

|

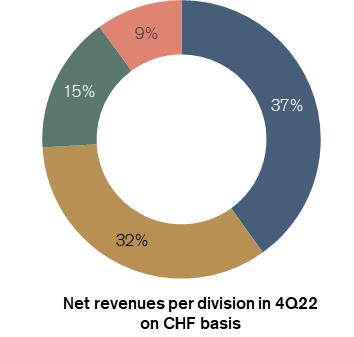

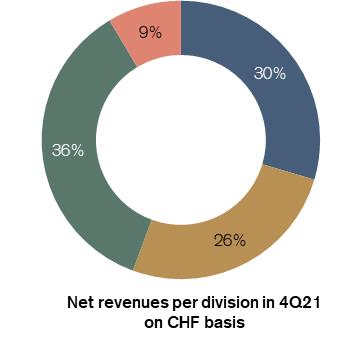

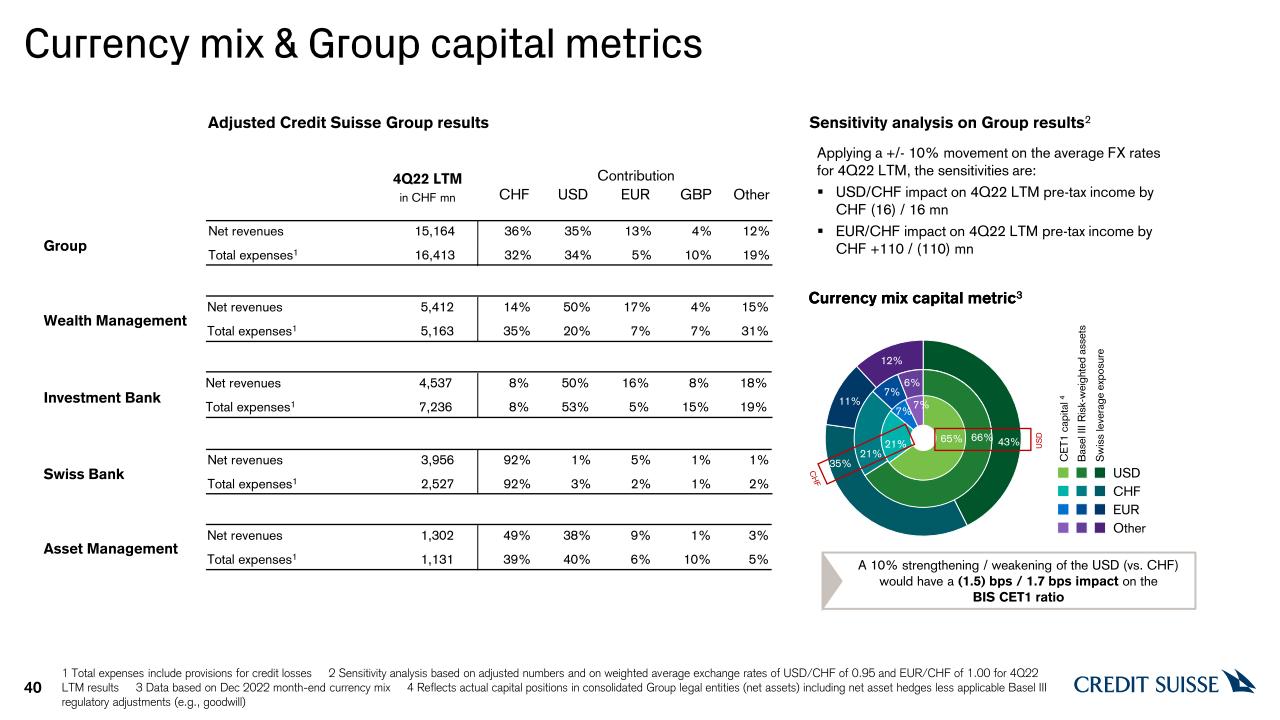

Net revenues for 4Q22 versus 4Q21 by division

The below charts exclude the Corporate Center, which account for 7% of net revenues for 4Q22 and (2)% of net revenues for 4Q21.

|

Wealth Management

|

|

Wealth Management

|

|

|||

|

Investment Bank

|

Investment Bank

|

|||||

|

Swiss Bank

|

Swiss Bank

|

|||||

|

Asset Management

|

Asset Management

|

|||||

|

Media Release

Zurich, February 9, 2023

|

|

Summary of 4Q22 performance

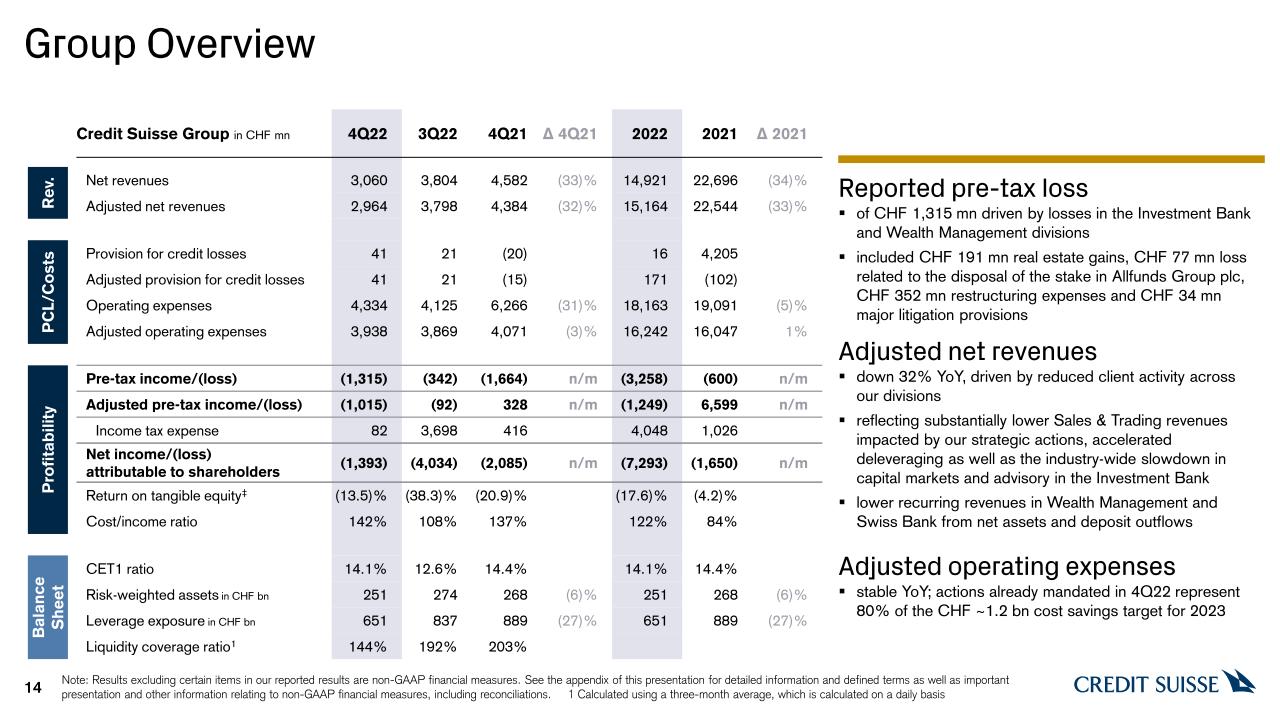

Credit Suisse’s performance in 4Q22 was impacted by the challenging economic and market environment, significant deposit and net asset outflows at the beginning of the quarter and the execution of our strategic actions.

Following the Group’s strategy announcement on October 27, 2022, Credit Suisse commenced rapid implementation of actions throughout 4Q22 to build the foundation for the new Credit Suisse. We announced decisive measures to radically restructure the

Investment Bank, accelerate cost transformation, and strengthen and reallocate capital, each of which are progressing at pace. Additional detail on the strategic progress made is outlined in a separate section: ‘Executing our

strategic transformation – the new Credit Suisse’.

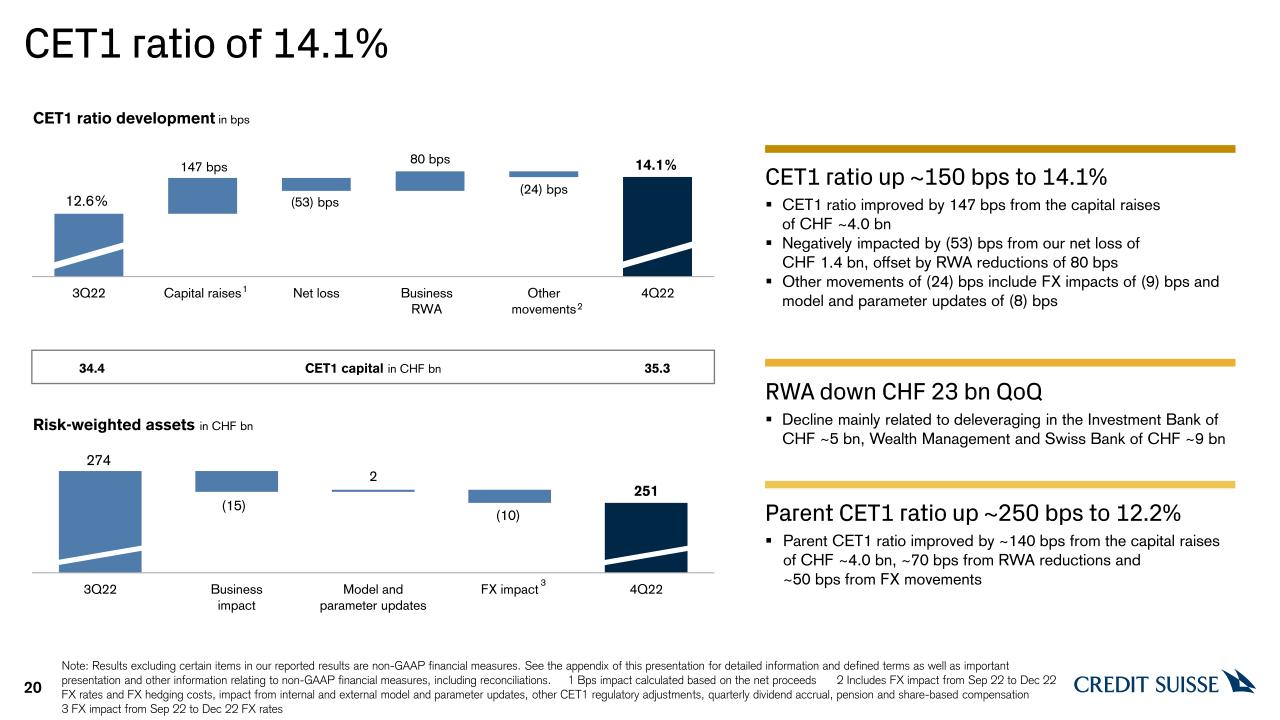

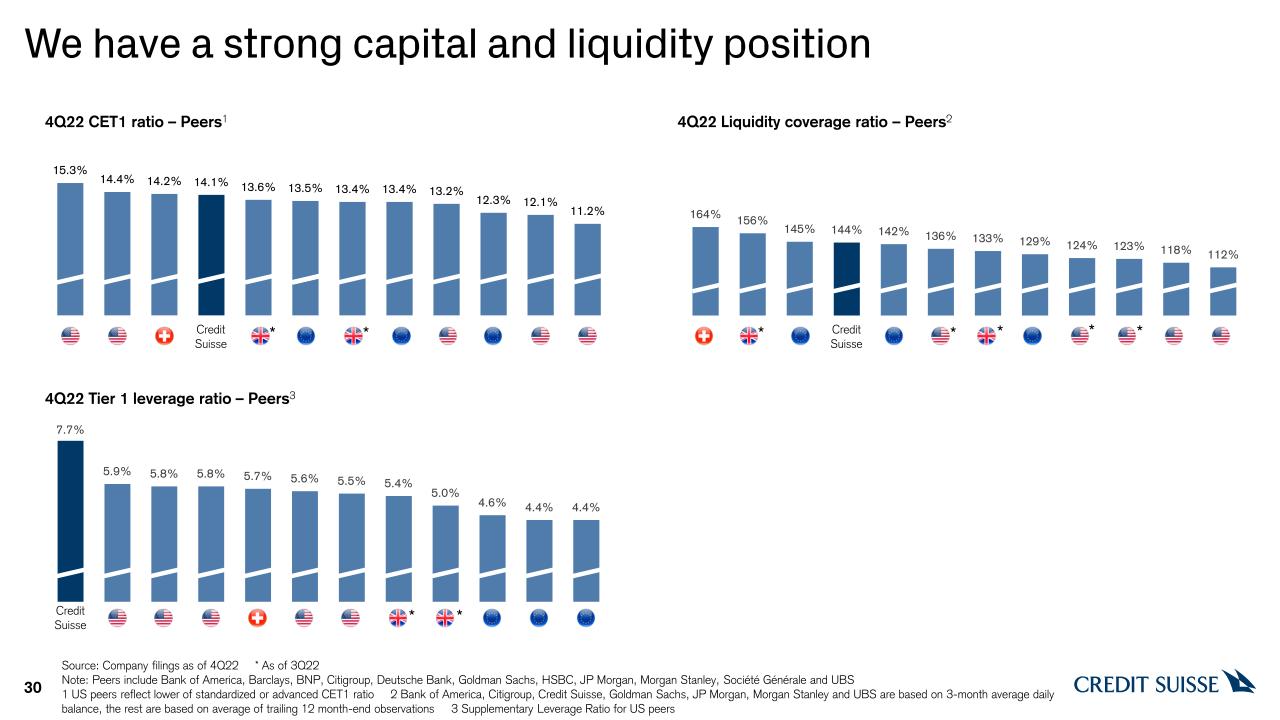

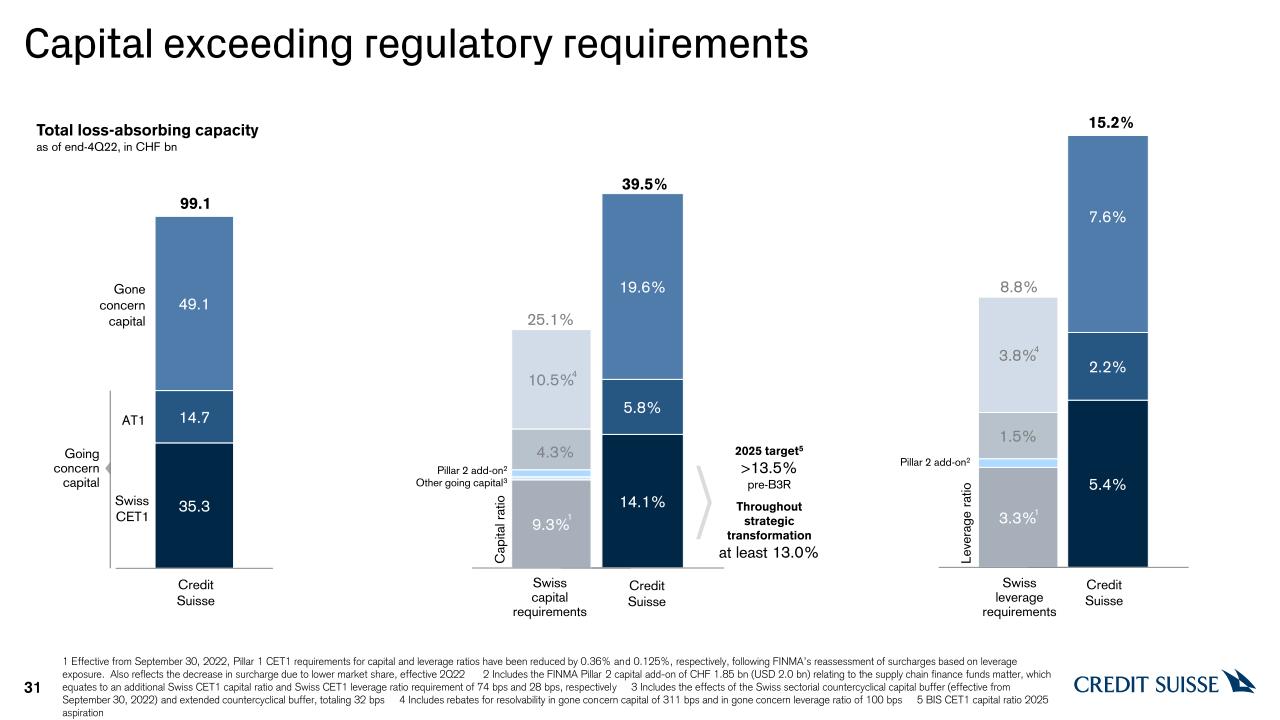

We continue to execute on our strategic actions from a position of capital strength. Our CET1 capital ratio was 14.1% as of the end of 4Q22, up from 12.6% at the end of 3Q22, mainly driven by the capital raises with gross proceeds of CHF ~4.0 bn

as well as Risk Weighted Asset (RWA) reductions, partially offset by our net loss. Our Tier 1 leverage ratio and our CET1 leverage ratio increased to 7.7% and 5.4%, respectively, as of the end of 4Q22; this was due to significantly lower leverage

exposure, mainly in our Investment Bank (IB), Wealth Management (WM) and Swiss Bank (SB) businesses.

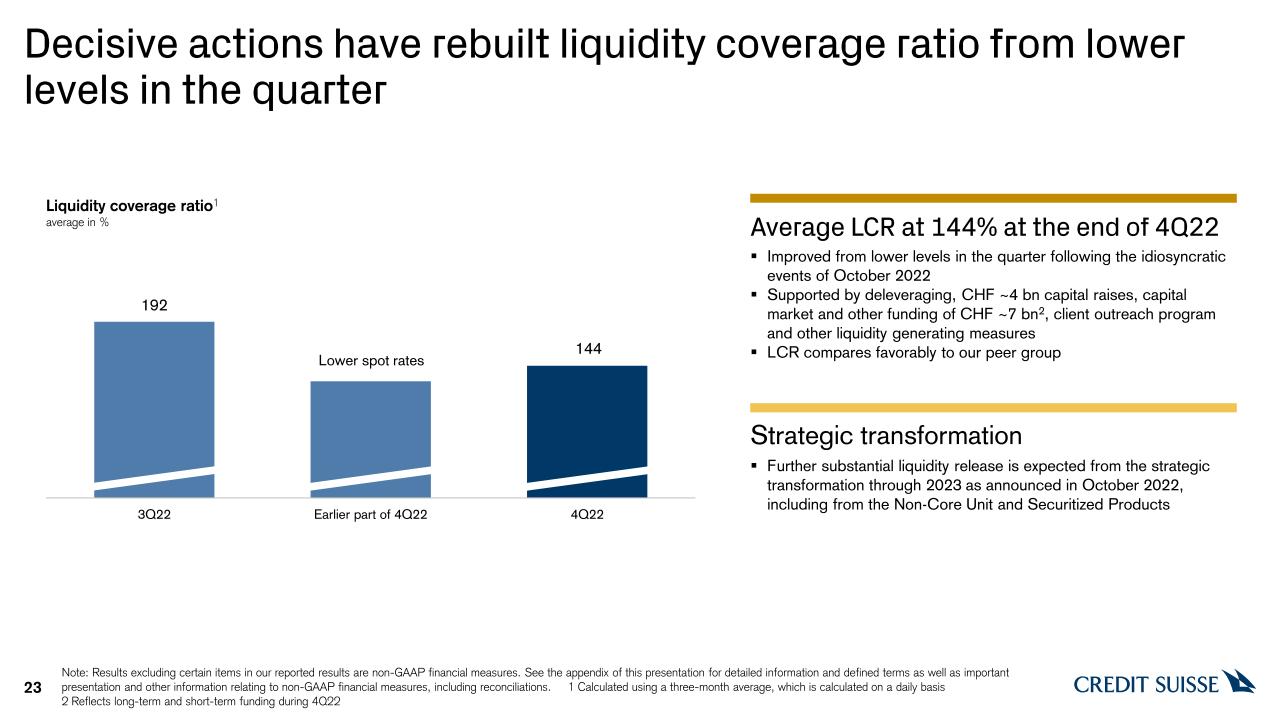

Our average Liquidity Coverage Ratio (LCR) as of the end of 4Q22 improved from lower levels in the quarter to 144%5, compared to an average LCR of 192% as of the end

of 3Q22. As previously disclosed, the lower LCR was largely driven by idiosyncratic events at the beginning of the quarter. The LCR has improved from lower levels in the quarter, supported by deleveraging, capital raises, capital market and other

funding of CHF ~7 bn6, our client outreach program and other liquidity generating measures.

As previously disclosed, Credit Suisse experienced deposit and net asset outflows in 4Q22 at levels that substantially exceeded the rates incurred in 3Q22. Approximately two thirds of the net asset outflows in the quarter were concentrated in

October 2022 and had reduced substantially for the rest of the quarter. Deposit outflows in 4Q22 contributed to ~60% of WM and SB net asset outflows. We have taken comprehensive measures to further increase our client engagement and regain deposits

as well as Assets under Management (AuM).

The Group’s overall performance was mainly driven by significantly lower year on year IB revenues. These were impacted by the industry-wide slowdown in capital markets, reduced activity in our sales & trading businesses and reflect the cost of

reducing risk and accelerated deleveraging in light of our strategic actions and in response to the Group’s significant deposit outflows in 4Q22. Performance in WM and SB was impacted by lower recurring revenues from lower deposit levels and lower

AuM. Asset Management’s (AM) performance year on year was adversely impacted by the challenging macroeconomic environment.

In 4Q22, we saw net revenues decrease by 33% year on year. This was driven by a decline in IB net revenues, down 74%, on a USD basis; a reduction in WM net revenues, down 17%; a decline in AM revenues, down 28%; as well as a decrease in SB net

revenues, down 20%. The Corporate Center’s performance in 4Q22 improved year on year with adjusted* net revenues of CHF 186 mn driven by improved Treasury revenue performance.

Reported operating expenses of CHF 4.3 bn were down 31% year on year driven by the goodwill impairment charge in 4Q21 of CHF 1.6 bn and by lower litigation provisions year on year. Reported operating expenses included restructuring expenses of CHF

352 mn and CHF 34 mn of major litigation provisions. Our adjusted* operating expenses of CHF 4.0 bn were down 3% year on year.

We reported a pre-tax loss of CHF 1.3 bn compared to a pre-tax loss of CHF 1.7 bn in 4Q21. Our reported pre-tax loss in 4Q22 included CHF 191 mn of real estate gains, a loss of CHF 77 mn related to our equity investment in Allfunds Group, and a

loss of CHF 20 mn related to our equity investment in SIX Group. Our stake in Allfunds Group was sold in October 2022. Our adjusted* pre-tax loss for 4Q22 was CHF 1.0 bn, down compared to adjusted* pre-tax income of CHF 328 mn in 4Q21.

We reported a net loss attributable to shareholders of CHF 1.4 bn, compared to net loss attributable to shareholders of CHF 2.1 bn in 4Q21.

Group AuM stood at CHF 1.3 trn at the end of 4Q22, down CHF 107 bn or 8% from CHF 1.4 trn at the end of 3Q22, due to net asset outflows and adverse FX impact, partly offset by favorable market movements. Group

net asset outflows in 4Q22 were CHF 110.5 bn, compared to NNA of CHF 1.6 bn in 4Q21.

_______________________________________________________________________________________________________________________________________________________________________________________________________________________________

Summary of FY22 performance

Our performance in 2022 underscores the importance of our forward focus on radically transforming the bank, efficiently reducing risk, lowering our cost base, strengthening our capital position and playing to our strengths and core franchises. The

Group continues to execute on the decisive strategic actions detailed on October 27, 2022, to create a simpler, more focused, stable bank built around the needs of our clients – a new Credit Suisse.

For the full year ending December 31, 2022, we saw net revenues decrease by 34% year on year, driven by a decline in IB net revenues, down 55% on a USD basis, and a decline in WM net revenues, down 30%. We also saw a decrease in AM net revenues,

down 14% year on year and in SB revenues which were down 5% year on year. Our reported net revenues of CHF 14.9 bn included real estate gains of CHF 368 mn and a valuation loss of CHF 586 mn related to our equity investment in Allfunds Group.

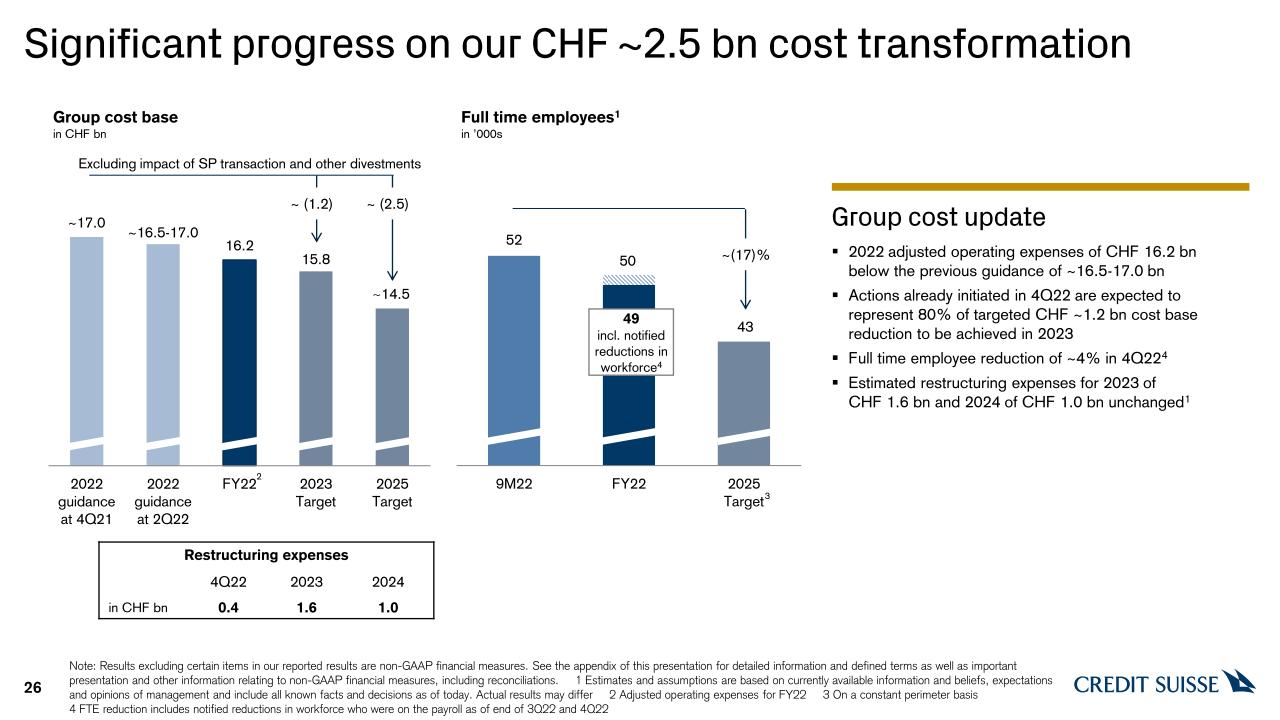

We reported operating expenses of CHF 18.2 bn, down 5% year on year, which included major litigation provisions of CHF 1.3 bn and restructuring expenses CHF 533 mn. Our FY22 adjusted* operating expenses of CHF 16.2 bn were below previous guidance

of CHF ~16.5-17.0 bn, and up 1% year-on-year. The full impact of the cost transformation actions taken in 4Q22 are expected to be seen in FY23.

We reported a pre-tax loss of CHF 3.3 bn for FY22, compared to a pre-tax loss of CHF 600 mn for FY21. Our adjusted* pre-tax loss for FY22 was CHF 1.3 bn, which compares to an exceptionally strong adjusted* pre-tax income of CHF 6.6 bn for FY21.

Our reported net loss attributable to shareholders for FY22 is CHF 7.3 bn, compared to a net loss attributable to shareholders of CHF 1.7 bn in FY21. The net loss attributable to shareholders for FY22 included an impairment of deferred tax assets

related to our strategic review of CHF 3.7 bn taken in 3Q22.

Our Group net asset outflows for FY22 were CHF 123.2 bn, compared to NNA of CHF 30.9 bn for the same period in 2021.

|

Media Release

Zurich, February 9, 2023

|

|

|

Outlook

|

|

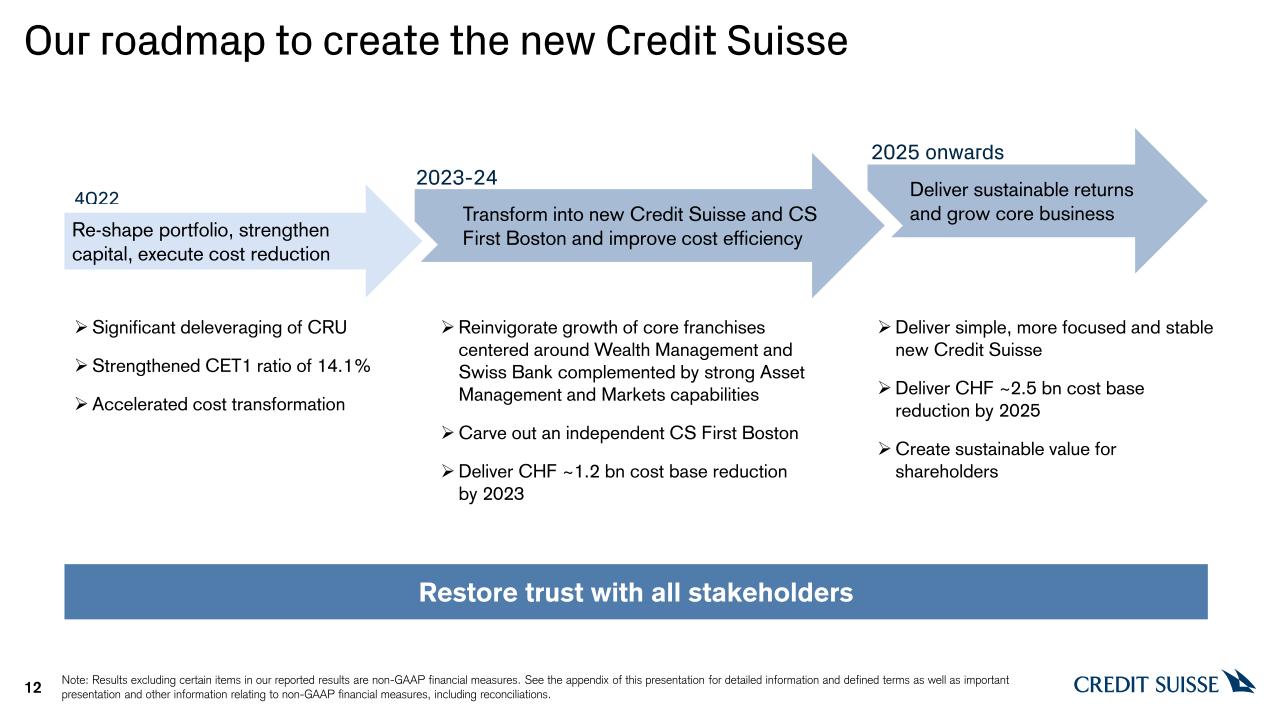

Credit Suisse continues to execute on its strategic transformation at pace and confirms the targets announced at the October 2022 strategy update. We have strengthened our capital position with a 4Q22 CET1

ratio of 14.1%. We have improved our average Liquidity Coverage Ratio to 144% from lower levels in the quarter7. We have also accelerated our cost

transformation program and continued to execute on the decisive strategic actions announced on October 27, 2022. We have accelerated the proactive deleveraging of non-core businesses and exposures as well as progressed on the announced sale

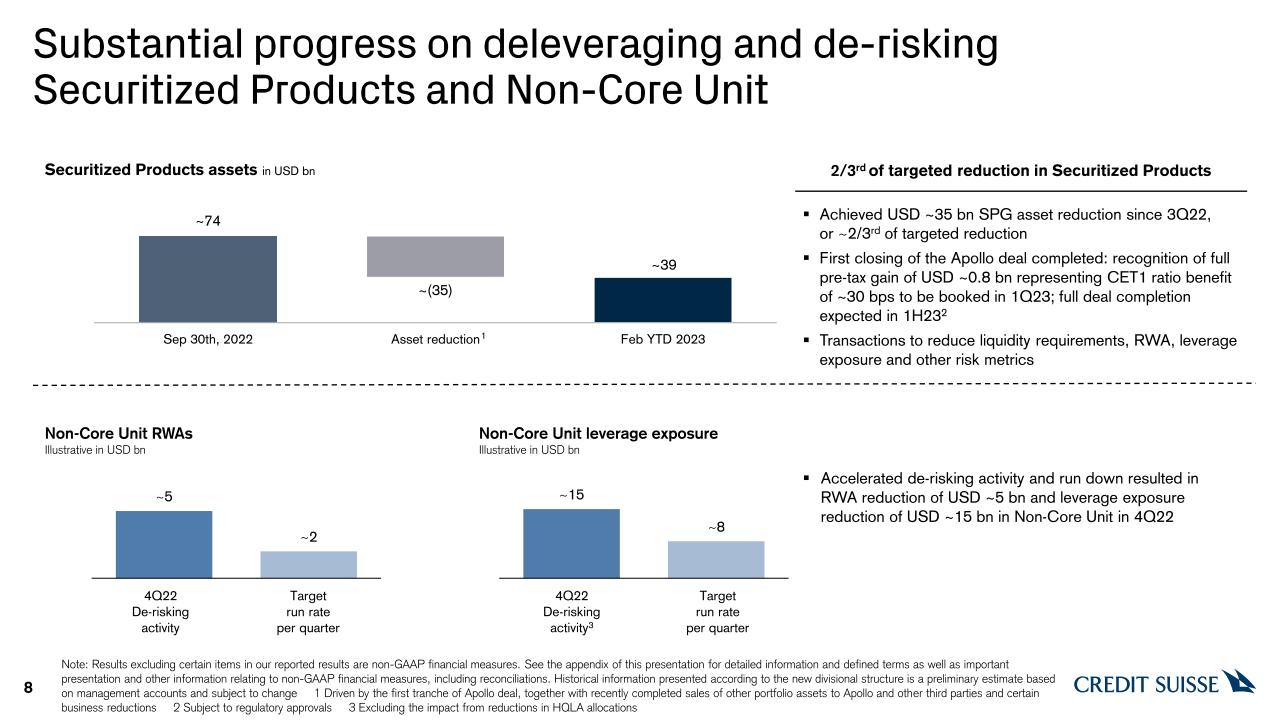

of a significant part of our Securitized Products Group (SPG) to entities and funds managed by affiliates of Apollo Global Management. The reduction in the SPG portfolio has already achieved approximately two-thirds of its targeted asset

reduction since 3Q22, with the first closing of the transaction with Apollo Global Management completed on February 8, 2023, subject to regulatory approvals. After this first closing, Credit Suisse is expecting to recognize the full pre-tax

gain on the sale of approximately USD 0.8 bn, representing a CET1 ratio benefit of ~30 basis points to be booked in 1Q23. The sale is expected to be completed in 1H23. The actions we are taking are expected to further strengthen liquidity

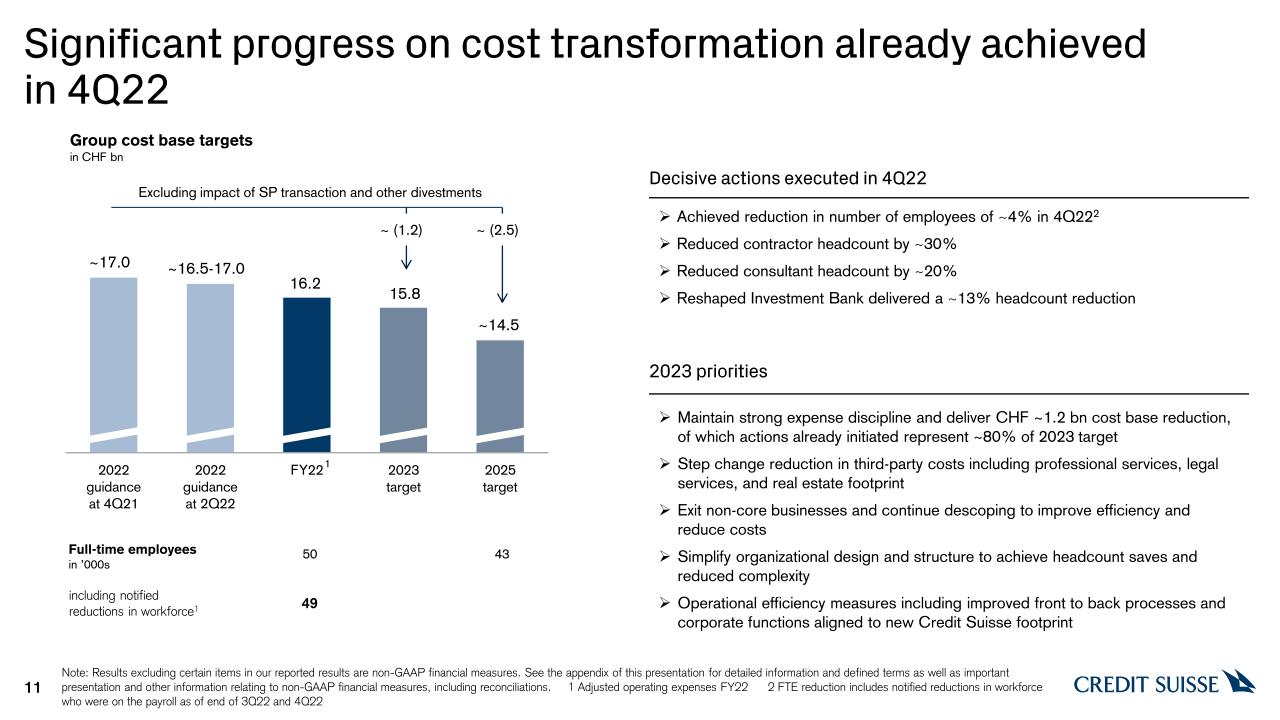

ratios and reduce the funding requirements of the Group. The bank’s cost transformation is well under way and actions already initiated by Credit Suisse in 4Q22 are expected to represent ~80% of the 2023 cost base reduction target of

approximately CHF 1.2 bn, with further initiatives underway.

Our financial results for 2022 were significantly affected by the challenging macro and geopolitical environment with market uncertainty and client risk aversion. This environment has had an adverse impact

on client activity across all our divisions. While we would expect these market conditions to continue in the coming months, we have taken comprehensive measures to further increase our client engagement, regain deposits as well as AuM and

improve cost efficiencies.

As previously disclosed, Credit Suisse experienced deposit and net asset outflows in 4Q22. While these outflows were significant, approximately two thirds of the outflows in the quarter were concentrated in

October and had reduced substantially for the rest of the quarter. While the bank continues to take proactive actions to regain client inflows, lower deposits and AuM are expected to lead to reduced net interest income and recurring

commissions and fees. While this is likely to lead to a loss for WM in the 1Q23, performance for the remainder of 2023 will depend on our ability to execute our strategy, net asset flows and market conditions.

Strategic actions taken to significantly reduce the Group’s risk profile are expected to be reflected in our financial results and given the challenging market backdrop, we would expect the IB to report a

loss in 1Q23. In light of the adverse revenue impact from the previously disclosed exit from non-core businesses and exposures as well as, in particular restructuring charges related to our cost transformation, Credit Suisse would also

expect the Group to report a substantial loss before taxes in 2023. The Group’s actual results will depend on a number of factors including the performance of the IB and WM divisions, the continued exit of non-core positions, any goodwill

impairments, litigation, regulatory actions, credit spreads and related funding costs, and the outcome of certain other items, including potential real estate sales. We estimate restructuring expenses for 2023 of CHF ~1.6 bn and 2024 of CHF

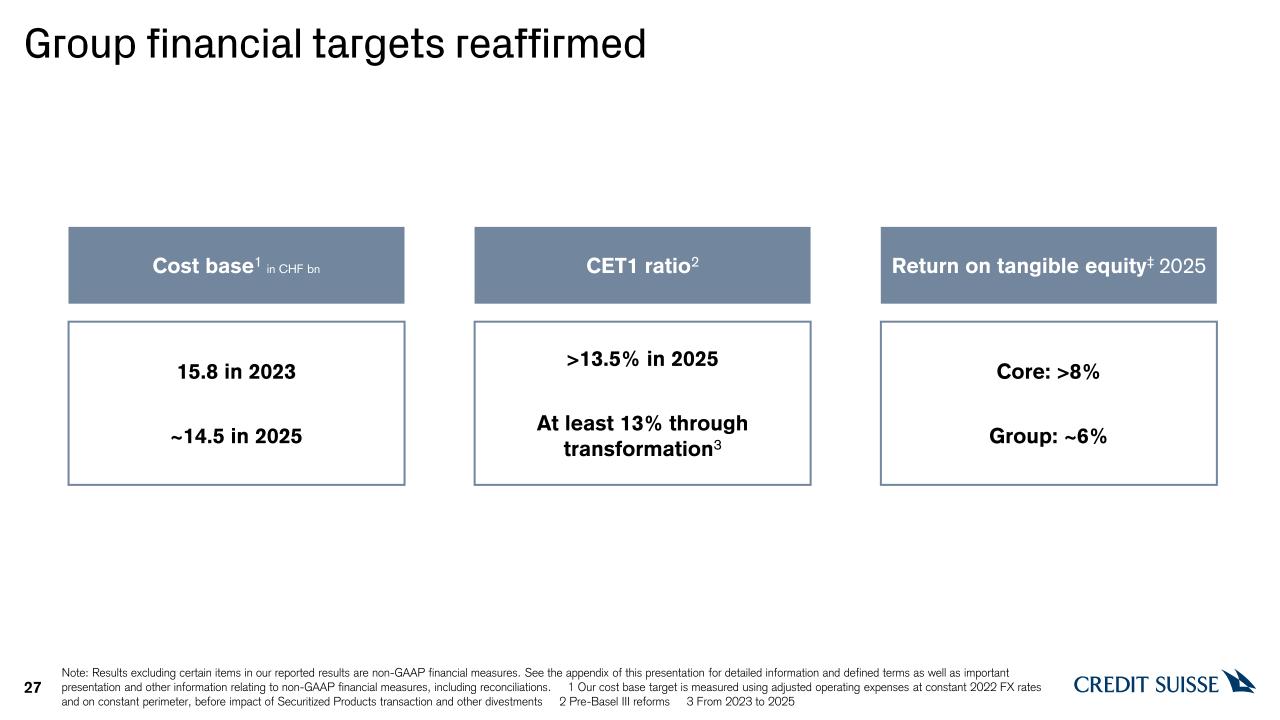

~1.0 bn, unchanged from previous guidance8. In respect of regulatory capital, the Group continues to target a 2025 pre-Basel III reform CET1 ratio of more than

13.5%, while expecting to maintain a pre-Basel III reform CET1 ratio of at least 13% throughout the transformation period through 2025.

|

|

Media Release

Zurich, February 9, 2023

|

|

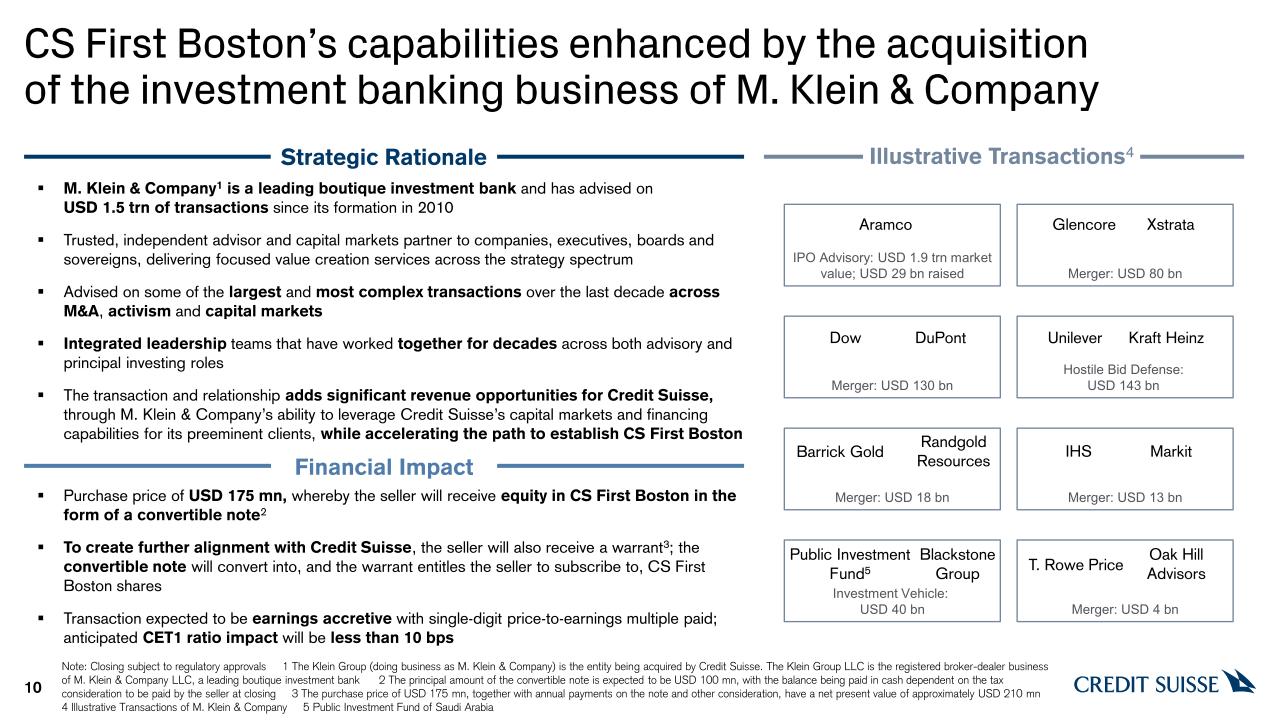

Credit Suisse is executing on its three-year strategic plan to establish a new Credit Suisse with a more integrated business model that is a trustworthy partner and delivers value for all stakeholders. Since October 27, 2022, when we announced the

strategic transformation of the Group, we have taken steps to strengthen our balance sheet and reduce risk; we continue to engage clients proactively and access the public and private markets. The Group plans to continue to execute on the decisive

strategic actions to return to the bank’s core strengths. We will build on our leading WM and SB franchises, with strong AM and Markets capabilities.

Summary of strategic achievements in 4Q22 and early 2023:

| ▪ |

Completed our capital raises with gross proceeds of CHF ~4 bn, marking a significant milestone on our transformation journey. Through the capital raises we strengthened our CET1 ratio by approximately 147 bps9, enabling us to progress with our strategic actions from a position of capital strength. Our CET1 capital ratio was 14.1% as of the end of 4Q22, up from 12.6% at the end of 3Q22

|

| ▪ |

Announced that we have entered into definitive transaction agreements to sell a significant part of SPG to entities and funds managed by affiliates of Apollo Global Management. With the execution of the first closing of the transaction,

we have achieved USD ~35 bn asset reduction in SPG and other related financing businesses since the end of 3Q22, or approximately two-thirds of the targeted asset reduction

|

| ▪ |

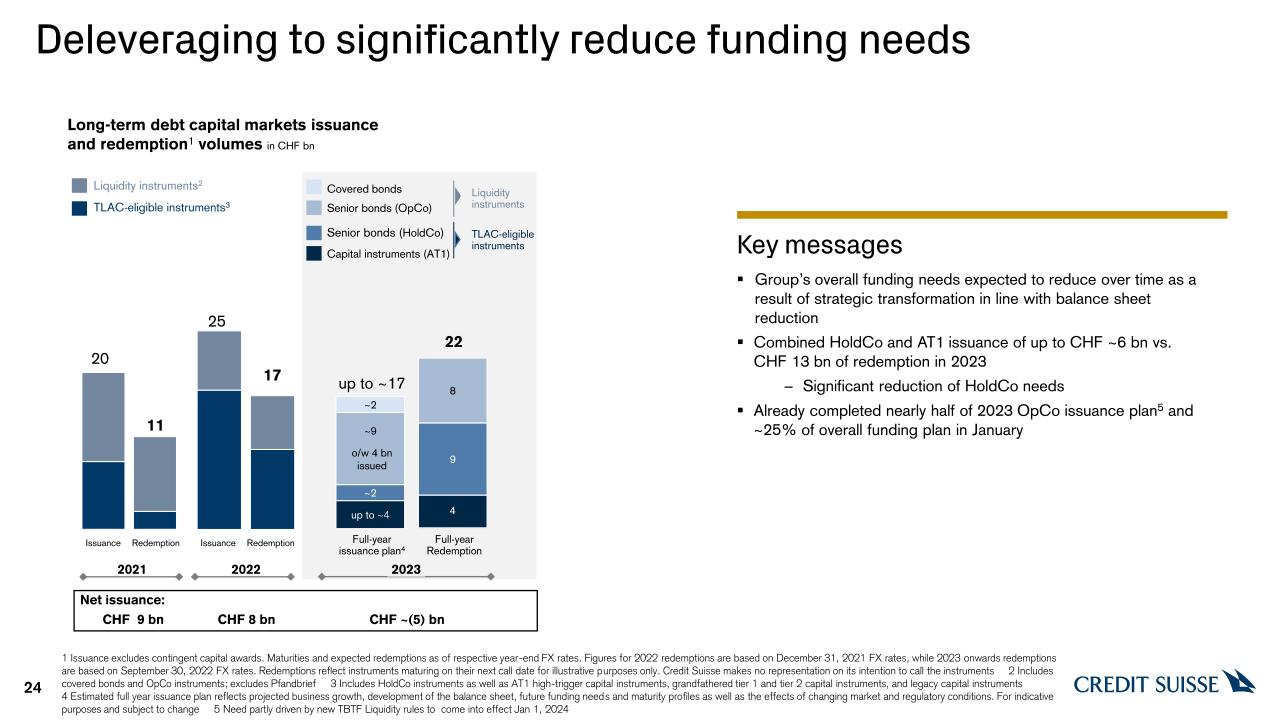

Successfully executed our funding plan for 2022; completed debt issuances of CHF ~10 bn since October 27, 2022, including issuance of over USD 5 bn through three bond sales in November and December 2022, which saw strong investor demand

|

| ▪ |

Accelerated cost transformation is well under way. The cost actions already initiated as of December 2022, are expected to represent ~80% of the 2023 cost base reduction target of approximately CHF ~1.2 bn, with

further initiatives in progress. The number of employees reduced by ~4% in 4Q22, including notified reductions in workforce10. We have also reduced contractor

headcount by ~30% and consultant headcount by ~20% in 4Q22

|

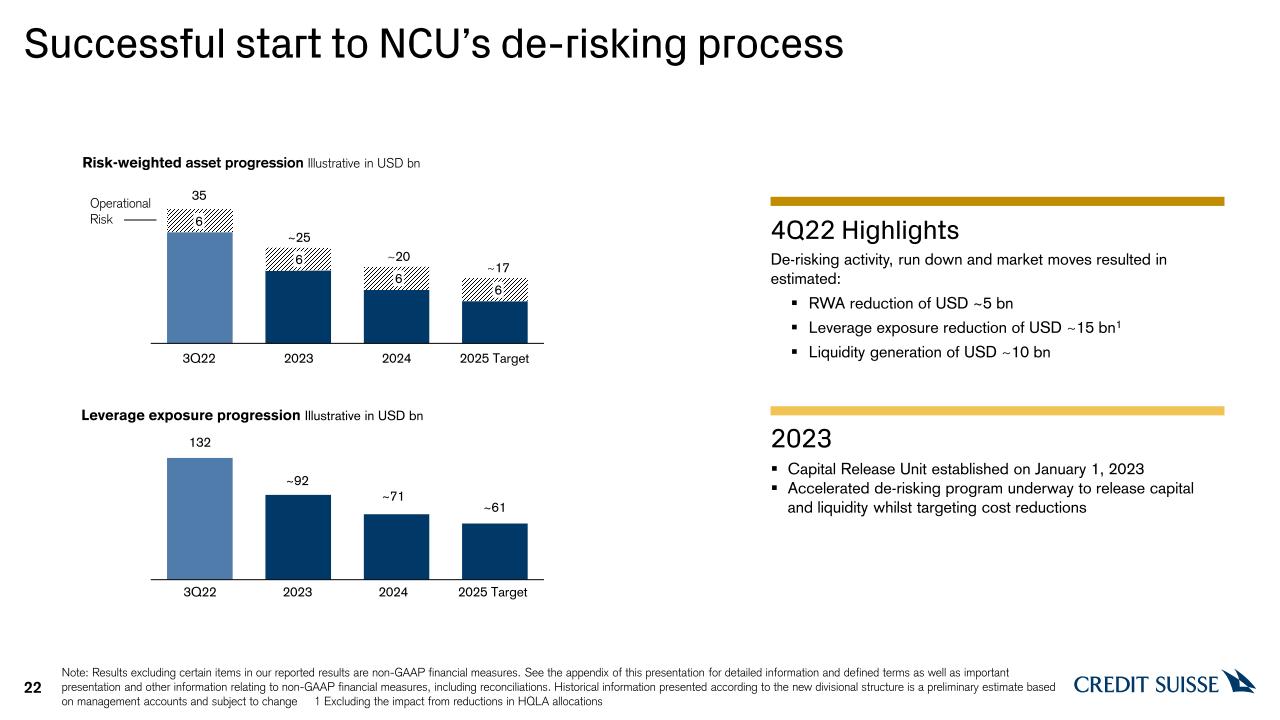

| ▪ |

Total RWA reduced QoQ by CHF 23 bn in 4Q22. The decline is mainly related to deleveraging in the Investment Bank of CHF ~5 bn and CHF ~9 bn in WM and SB, in light of our strategic actions and in response to the Group’s significant

deposit outflows in 4Q22

|

| ▪ |

Successful establishment of our Capital Release Unit, on January 1, 2023, which includes the NCU. Progressing the Group’s de-risking activity with RWA reduction of USD ~5 bn and leverage reduction of USD ~15 bn11 in 4Q22. De-risking activity generated USD ~10 bn of liquidity in 4Q22

|

Throughout 2023, it is our intention to continue to deliver on strategic actions by:

| ▪ |

Capitalizing on the strength of our WM franchise and reinvigorating growth; reinforcing SB’s leading position as a universal bank. Leveraging our strong and differentiated capabilities in AM and Markets to

complement the core

|

| ▪ |

The full SPG transaction with Apollo Global Management12 is expected to

close in 1H23, subject to regulatory approvals. Following the first closing, we are now expecting to recognize the full pre-tax gain on the sale of USD ~0.8 bn, representing CET1 ratio benefit

~30 basis points to be booked in 1Q23. We expect that the transaction will reduce liquidity requirements, RWA, leverage exposure and other risk metrics and expect to deliver further CET1 accretion.

|

| ▪ |

As we reduce residential mortgage-backed securities (RMBS) exposures and activity as part of our announced strategy towards a managed exit from the SPG business and to de-risk the bank, we anticipate, based on

ongoing regulatory discussions, that operational risk RWA associated with historical RMBS activity will decrease

|

| ▪ |

Advancing on the carveout of CS First Boston as a distinct, leading independent capital markets and advisory business. Acquisition of The Klein Group LLC13, the investment banking business of M. Klein & Company LLC to strengthen CS First Boston’s advisory and capital markets capabilities; additional revenue opportunities from Credit Suisse’s complementary

strengths

|

| ▪ |

Maintaining strong expense discipline by continuing our cost transformation measures throughout 2023, with an aim to deliver CHF ~1.2 bn reduction in the cost base for FY23. We estimate restructuring expenses for

2023 of CHF ~1.6 bn and 2024 of CHF ~1.0 bn, unchanged from previous guidance14

|

| ▪ |

Group-wide review of Credit Suisse’s organizational set up to reduce layers and duplication across divisions and functions, which we expect will support a more effective, less complex design

|

| ▪ |

Detailed review of all aspects of third party spend to drive further efficiencies across divisions and functions including but not limited to real estate footprint and procurement

|

| ▪ |

Group’s overall funding needs expected to reduce over time as a result of strategic transformation in line with balance sheet reduction; 2023 funding plan of up to CHF ~17 bn against CHF 22 bn of redemptions

|

| ▪ |

Strengthening capital and leverage ratios through planned divestments as well as RWA and leverage exposure reductions from the NCU

|

|

Media Release

Zurich, February 9, 2023

|

|

Divisional summaries

|

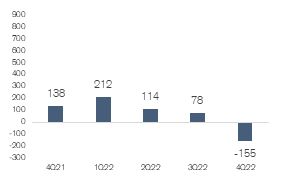

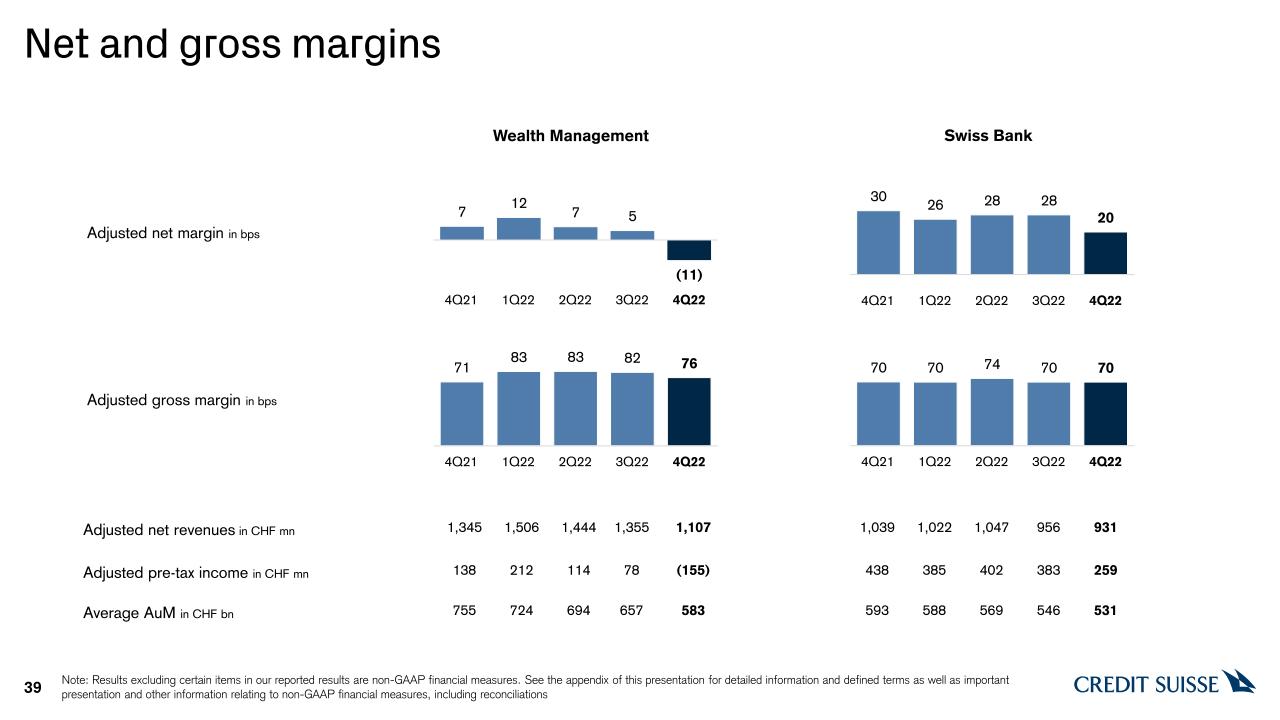

Wealth Management (WM)

|

|||

Adjusted* pre-tax income/loss QoQ in CHF million

|

4Q22

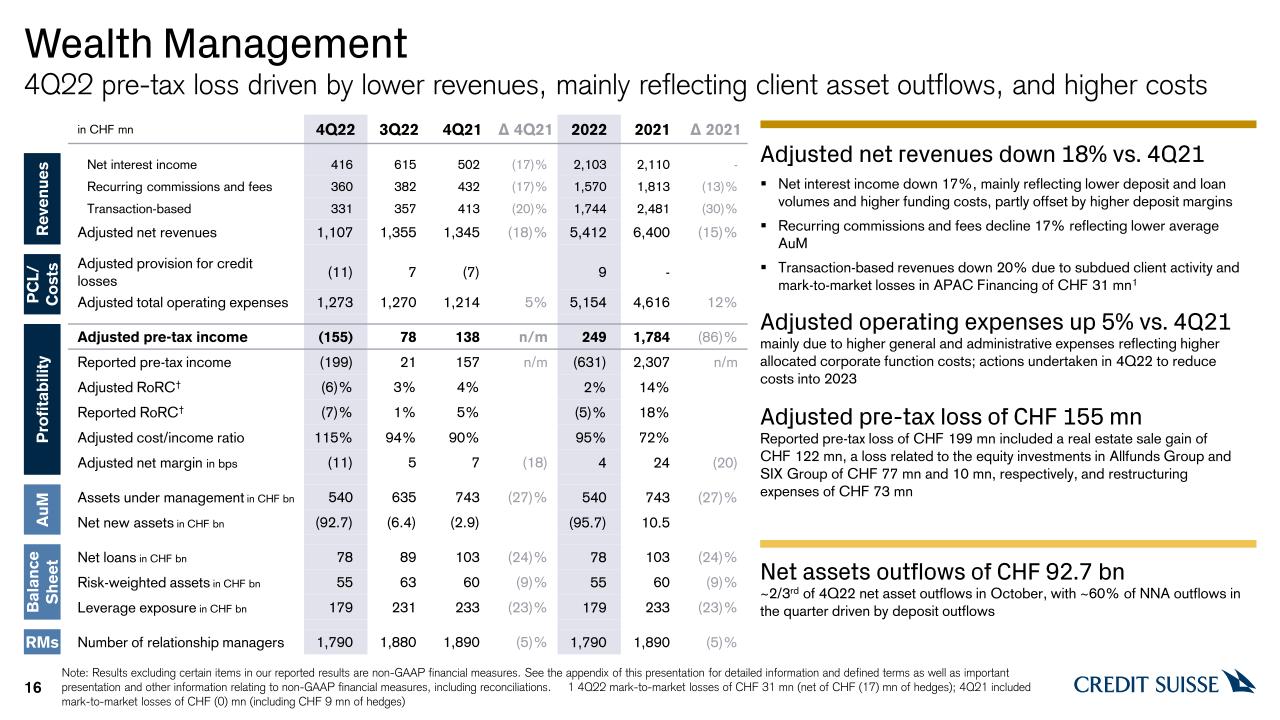

On an adjusted* basis, WM had a pre-tax loss of CHF 155 mn, down year on year from a pre-tax income of CHF 138 mn, as client asset outflows and sentiment weighed on revenues, combined with higher costs. The

reported pre-tax loss for the quarter of CHF 199 mn, included a real estate sale gain of CHF 122 mn, losses related to the equity investments in Allfunds Group and SIX Group of CHF 77 mn and CHF 10 mn, respectively, as well as

restructuring expenses of CHF 73 mn.

WM had reported net revenues of CHF 1.1 bn, down 17% year on year. Adjusted* net revenues of CHF 1.1 bn were down 18%. Net interest income was down 17% year on year, mainly reflecting lower volumes for deposits and loans, including the

related adverse impacts of lower funding benefits, and interest rate management costs. Recurring commissions and fees were also down 17%, mainly reflecting lower average AuM. Finally, transaction and performance-based revenues were down 20%

year on year, mainly due to subdued client activity, lower corporate advisory fees and mark-to-market losses in APAC Financing of CHF 31 mn15.

WM had higher adjusted* operating expenses of CHF 1.3 bn, up 5%, mainly due to higher general and administrative expenses, reflecting higher allocated corporate function costs.

WM had net asset outflows of CHF 92.7 bn in 4Q22. Approximately two thirds of net asset outflows for the quarter were in October 2022, with ~60% of net asset outflows driven by deposit outflows. WM reported AuM of CHF 540 bn, compared to

CHF 743 bn as of the end of 4Q21 and CHF 635 bn as of the end of 3Q22. The decrease in AuM quarter on quarter was mainly driven by net asset outflows across all regions.

|

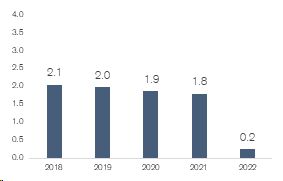

||

Adjusted* pre-tax income YoY in CHF billion

|

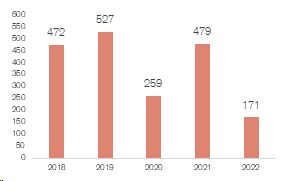

FY22

On an adjusted* basis, WM had a pre-tax income of CHF 249 mn, down 86% year on year. This was driven by lower revenues across transaction- and performance-based revenues, recurring commissions and fees, the revenue impact of the outflows

in 4Q22, as well as higher operating expenses. WM’s adjusted* pre-tax income was adversely impacted by an impairment of IT-related assets of CHF 183 mn, following a review of WM’s technology and platform

strategy throughout 2022, and mark-to-market losses in APAC Financing Group of CHF 121 mn16. The

reported pre-tax loss for FY22 of CHF 631 mn, included a real estate sale gain of CHF 147 mn, losses related to the equity investment in Allfunds Group and SIX Group of CHF 588 mn and CHF 17 mn, respectively, as well as major litigation

provisions of CHF 306 mn and restructuring expenses of CHF 109 mn.

WM had reported net revenues of CHF 5.0 bn, down 30% year on year. Adjusted* net revenues of CHF 5.4 bn were down 15%. Transaction- and performance-based revenues were down 30% year on year, mainly due to lower brokerage and product

issuing fees and lower Global Trading Solutions (GTS) revenues. Recurring commissions and fees were down 13%, mainly reflecting lower average AuM. Net interest income was flat year on year, as higher margin on deposits offset the impact of

lower volumes for deposits and loans and the adverse impact of higher funding and higher interest rate management costs.

WM had higher adjusted* operating expenses, up 12%, mainly due to higher general and administrative expenses.

WM had net asset outflows of CHF 95.7 bn in FY22 driven by outflows across all regions, reflecting significant outflows in 4Q22. AuM was down CHF 202 bn year on year, mainly driven by net asset outflows, unfavorable market movements and

structural effects, including reclassifications of CHF 17.6 bn related to the sanctions imposed in connection with Russia’s invasion of Ukraine.

|

||

|

Media Release

Zurich, February 9, 2023

|

|

|

Swiss Bank (SB)

|

||

Adjusted* pre-tax income QoQ in CHF million

|

4Q22

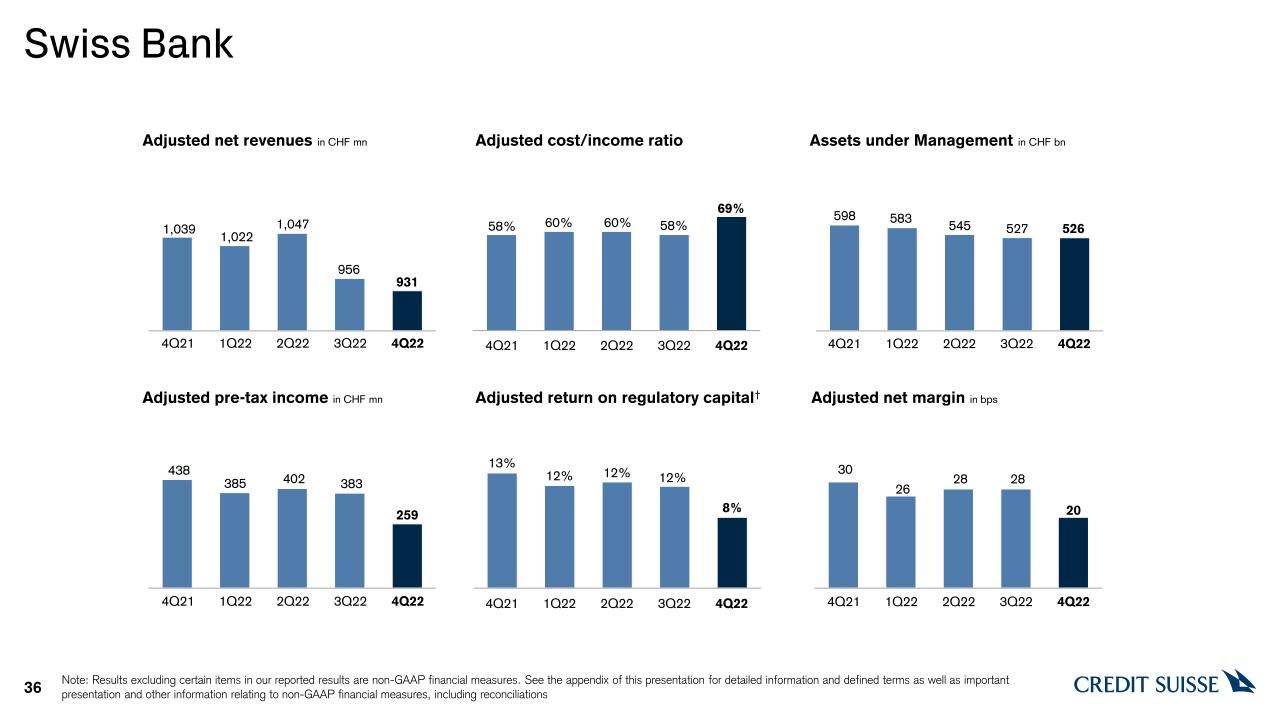

SB had a resilient 4Q22 despite being negatively impacted by normalizing provisions and compensation expenses. On an adjusted* basis, SB had a pre-tax income of CHF 259 mn, down 41% year on year, reflecting decreased net revenues, higher

operating expenses and normalizing provision for credit losses of CHF 28 mn, at 7 basis points of our net loans. SB had higher adjusted* operating expenses, up 6%, due to increased compensation expenses, mainly reflecting higher deferral of

compensation in 4Q21. SB’s adjusted* cost to income ratio was 69%.

SB’s reported net revenues were CHF 972 mn, down 20% year on year; adjusted* net revenues were down 10%. Net interest income decreased by 11% year on year with higher deposit income more than offset by decreased income from loans and

lower SNB threshold benefits from the SNB increase of interest rates; on a QoQ basis, net interest income is stable. Recurring commissions and fees were down 10% reflecting lower average AuM. Transaction-based revenues were down 18%, mainly

driven by equity investments17; excluding those, transaction-based revenues would have been down 8% due to lower client activity.

SB had net asset outflows of CHF 8.3 bn mainly driven by outflows in private clients. The division’s AuM as of the end of 4Q22 were CHF 526 bn, stable compared to CHF 527 bn at the end of 3Q22, mainly reflecting net asset outflows and

unfavorable foreign exchange-related movements, offset by favorable market movements.

|

|

Adjusted* pre-tax income YoY in CHF billion

|

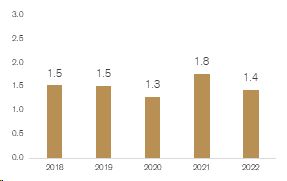

FY22

On an adjusted* basis, SB had a pre-tax income of CHF 1.4 bn, down 19% year on year, mainly driven by lower net revenues down 4% and provision for credit losses of CHF 90 mn. Adjusted* operating expenses were up 2%, reflecting Group-wide

risk, compliance and technology costs, higher occupancy expenses as well as targeted advertising and marketing campaigns, while compensation expenses were stable. SB’s adjusted* cost to income ratio was 62%.

SB’s reported net revenues were CHF 4.1 bn, down 5% year on year; adjusted* net revenues were down 4% mainly driven by lower net interest income, down 5%, primarily reflecting lower SNB threshold benefits from the SNB increase of

interest rates, and lower loan income, partially offset by higher deposit income. Transaction-based revenues were down 9%, mainly driven by equity investments18

and gains related to IBOR transition19, excluding those, transaction-based revenues would have been down 3%. Recurring commissions and fees were flat year on

year.

SB had net asset outflows of CHF 5.4 bn for FY22 driven by outflows in private clients, partially offset by inflows in institutional clients. SB’s AuM were CHF 72 bn lower year on year, mainly driven by unfavorable market movements and

net asset outflows.

|

|

Media Release

Zurich, February 9, 2023

|

|

|

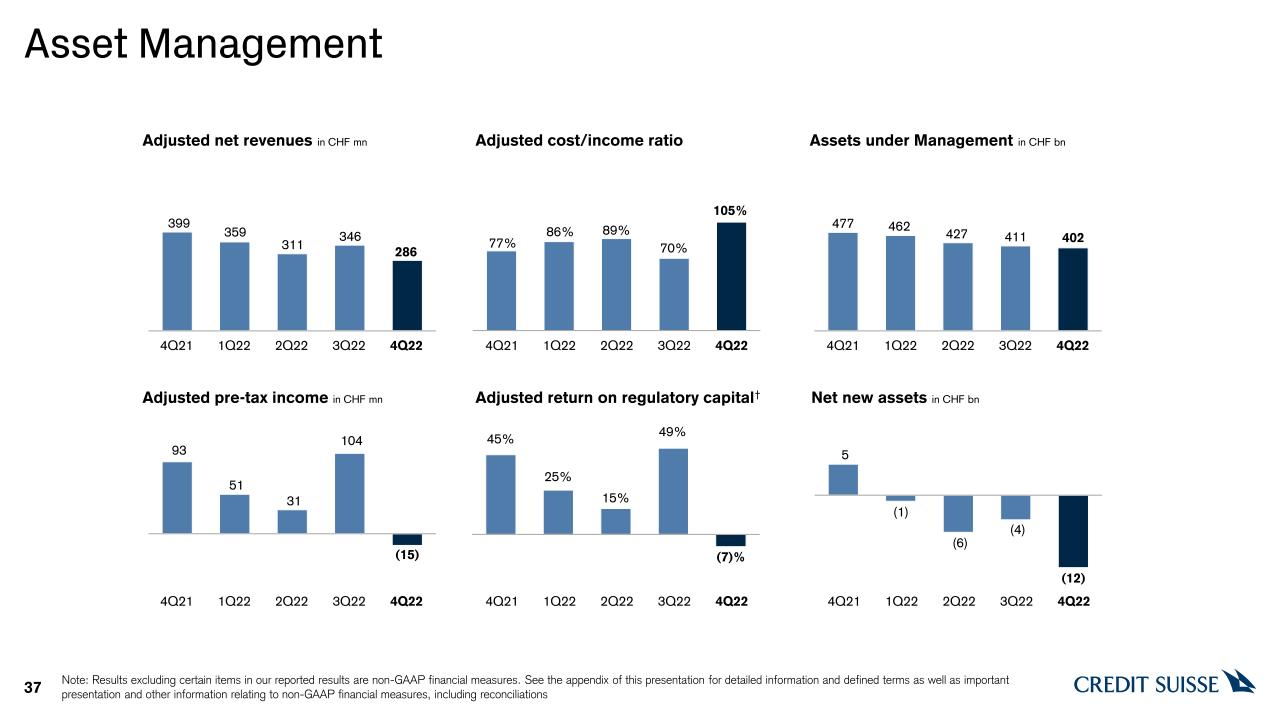

Asset Management (AM)

|

||

Adjusted* pre-tax income QoQ in CHF million

|

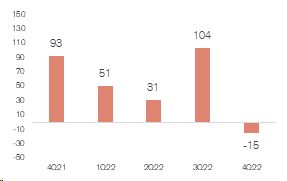

4Q22

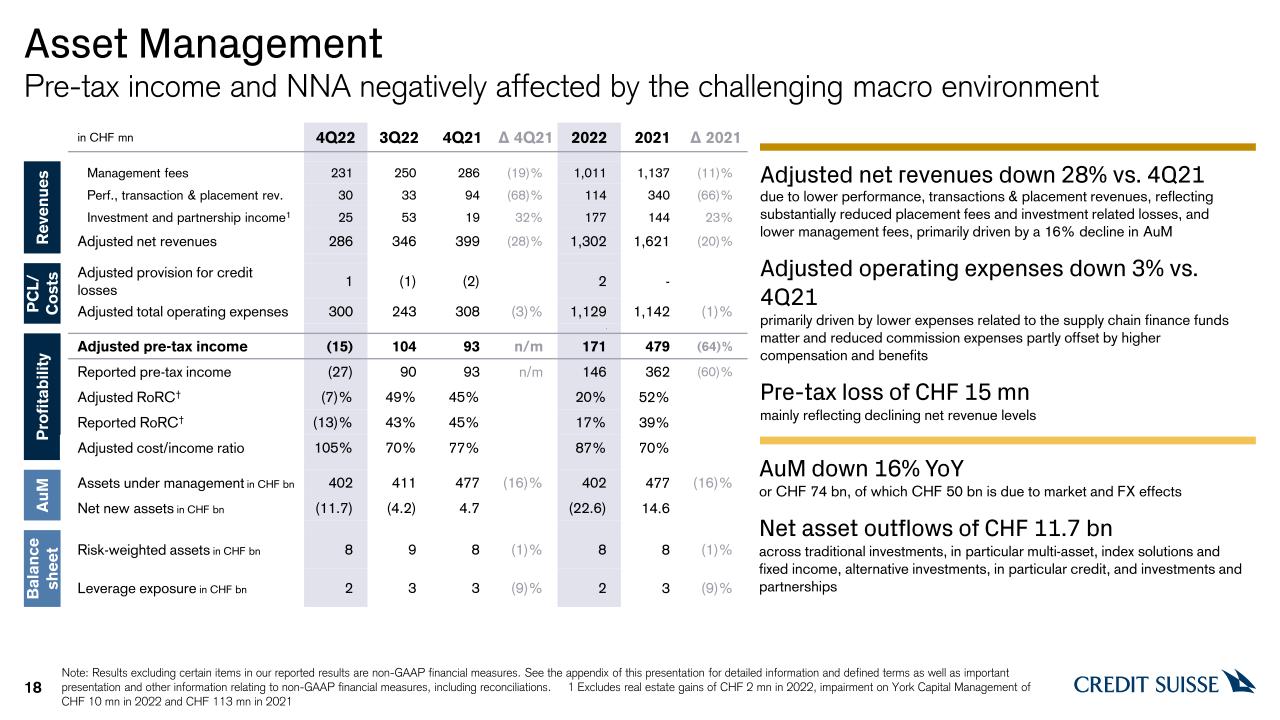

AM’s performance continued to be adversely affected by the challenging macro-environment. On an adjusted* basis, AM had a pre-tax loss of CHF 15 mn for 4Q22, down year on year compared to a pre-tax income of CHF 93 mn in 4Q21. The

adjusted* pre-tax loss was driven by lower net revenues. Adjusted* operating expenses were down 3% mainly reflecting lower expenses related to the Supply Chain Finance Funds matter and reduced commission expenses, partly offset by an

increase in compensation and benefits.

AM’s reported net revenues were down 28% year on year at CHF 286 mn. The decrease in net revenues was due to lower performance, transaction and placement revenues, down 68% year on year, mainly reflecting lower placement fees and

investment-related losses. Management fees were down 19%, reflecting a combination of the 16% decline in AuM year on year as well as increased investor bias towards passive products. AM saw higher investment and partnership income, up 32%

year on year, mainly due to equity participation gains, including the gain from the disposal of the Group’s interest in Energy Infrastructure Partners AG, partially offset by reduced performance fees.

AM had net asset outflows of CHF 11.7 bn for the quarter across driven by outflows from traditional investments, primarily related to outflows in multi-asset solutions, index solutions and fixed income; from investments and partnerships,

primarily related to an emerging markets joint venture; and from alternative investments, primarily related to outflows in credit. AM had AuM of CHF 402 bn at the end of 4Q22, down 16% year on year or CHF 75 bn, of which CHF ~50 bn was due

to market and FX-related movements.

|

|

Adjusted* pre-tax income YoY in CHF million

|

FY22

On adjusted* basis, AM had a pre-tax income of CHF 171 mn for FY22, down 64% year on year, primarily driven by lower net revenues. Adjusted* operating expenses were down 1% primarily due to reduced professional services fees related to

the wind down and administration of the Supply Chain Finance Funds as well as reduced commission expenses.

AM’s reported net revenues were down 14% year on year at CHF 1.3 bn driven by decreased performance, transaction and placement revenues and declining management fees, partially offset by higher investment and partnership income. The

decrease in net revenues was due to lower performance, transaction and placement revenues, down 66% year on year, reflecting primarily investment related losses as opposed to gains in 2021, reduced placement fees and decreasing performance

fees. Net revenues also reflected reduced management fees, down 11%, due to lower average AuM and increased investor bias towards passive products. These were partly offset by higher investment and partnerships income, primarily driven by

an impairment of CHF 113 mn related to our non-controlling interest in York Capital Management in FY21. Adjusted* net revenues were down 20% year on year.

AM had net asset outflows of CHF 22.6 bn for FY22 across traditional investments and alternative investments, partially offset by investments and partnerships.

|

|

Media Release

Zurich, February 9, 2023

|

|

|

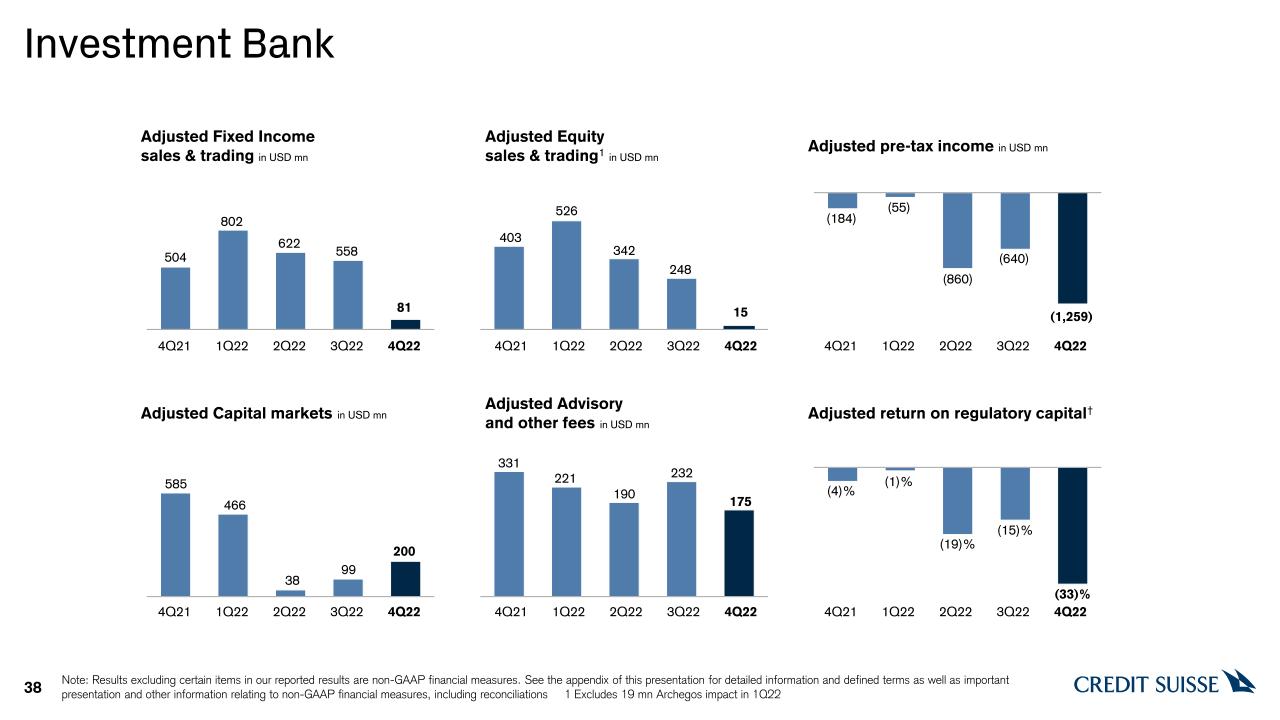

Investment Bank (IB)

|

||

Adjusted* pre-tax income/loss QoQ in USD million

|

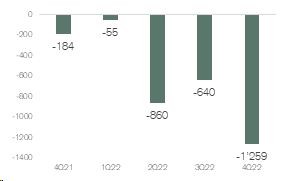

4Q22

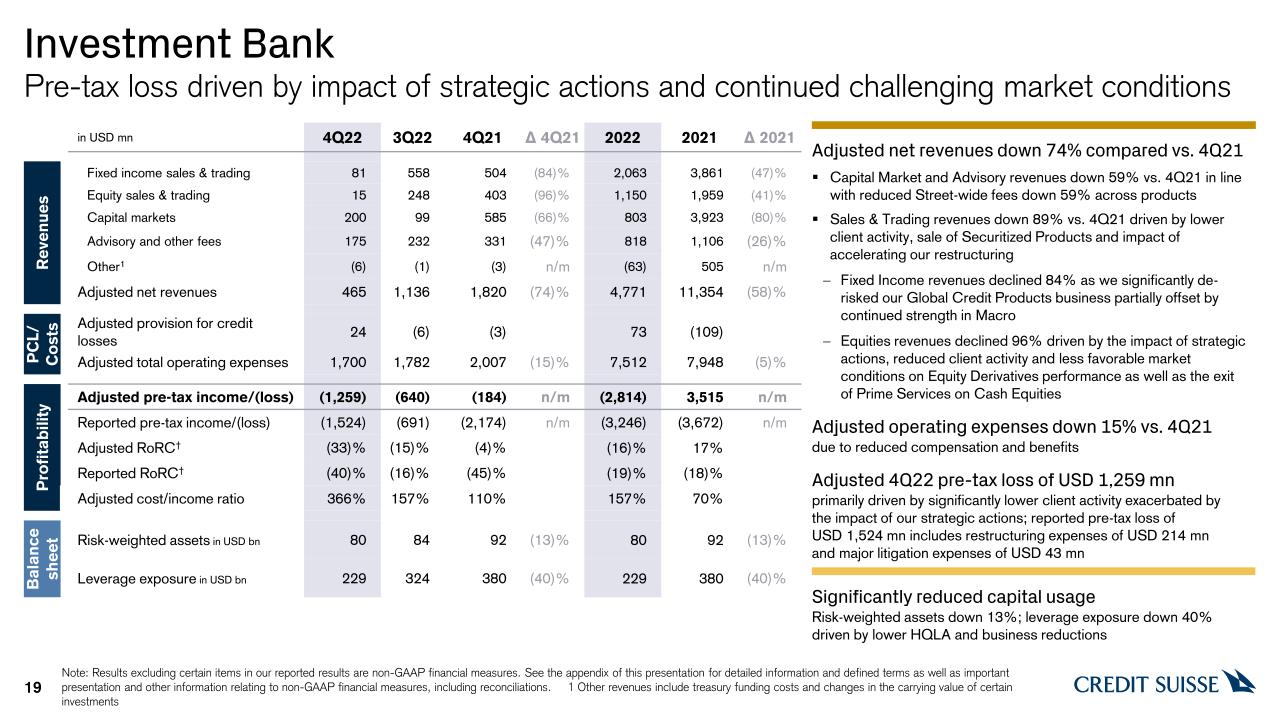

On an adjusted* basis, the IB posted a pre-tax loss of USD 1.3 bn, up compared to a pre-tax loss of USD 184 mn in 4Q21, reflecting lower net revenues of USD 465 mn, down 74% year on year, amid challenging market

conditions driven by higher volatility as well as muted primary issuance and widened credit spreads. IB’s performance also reflected the impact of accelerated deleveraging in light of our strategic actions and in response to the Group’s

significant deposit outflows in 4Q22. The reported pre-tax loss was USD 1.5 bn, compared to a reported pre-tax loss of USD 2.2 bn in 4Q21. Reported operating expenses were down 51% year on year, as 4Q21 included a goodwill impairment charge

of USD 1.8 bn. Adjusted* operating expenses were down 15% year on year, primarily due to lower compensation and benefits as well as lower revenue-related expenses.

Capital Markets revenues decreased 66% year on year as muted primary issuance and macro conditions continued to weigh on client sentiment. Advisory revenues were down 47% year on year in line with reduced

industry-wide deal closings. Combined, Capital Markets and Advisory revenues decreased 59% year on year, in line with the reduced street-wide fees across products20.

Revenues in our Fixed Income Sales & Trading business were down 84%, as continued strength in Macro was offset by a substantial decline in Securitized Products and Global Credit Products largely due to the strategic actions taken in the

quarter. Equity Sales & Trading revenues declined by 96% year on year reflecting less favorable market conditions compared to 4Q21. Results also reflect the impact of our strategic actions, a slowdown in client activity due in part to

the Group’s credit rating downgrades and the exit of Prime Services on Equity Derivatives and Cash Equities.

For 4Q22, we significantly reduced capital usage in the IB. Risk-weighted assets were down 13% year on year at USD 80 bn and Leverage Exposure was down 40% year on year, at USD 229 bn, due to lower high-quality

liquid assets (HQLA) reflecting reductions in cash held at central banks and reductions in non-cash HQLA relating to the significant deposit outflows the Group experienced in 4Q22 and business reductions.

|

|

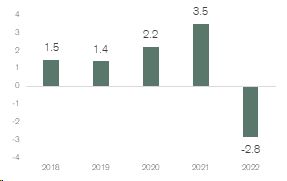

Adjusted* pre-tax income/loss YoY in USD billion

|

FY22

On an adjusted* basis, the IB posted a significant pre-tax loss of USD 2.8 bn, down significantly year on year, reflecting extremely challenging market conditions, particularly in our capital markets business and

the impact of our restructuring of the IB. The reported pre-tax loss was USD 3.3 bn, mainly driven by significantly lower revenues. The division’s reported net revenues were USD 4.8 bn for FY22, down 55% year on year; on an adjusted* basis,

net revenues were down 58%, largely due to significantly lower capital markets and fixed income sales and trading revenues as well as lower equity sales and trading revenues. Reported operating expenses were down 18%, mainly reflecting the

goodwill impairment of USD 1.8 bn in FY21. Adjusted* operating expenses were down 5% year on year, primarily due to lower compensation and benefits.

Capital Markets revenues decreased 80% year on year, impacted by significantly challenged primary issuance. Advisory revenues were down 26% year on year due to lower announced deals in the year. Revenues in our

Fixed Income Sales & Trading business were down 47% from FY21 and reflected the impact of our strategic actions to de-risk the business and reduce capital in light of our announced strategy. On an adjusted* basis, Equity Sales &

Trading21 revenues declined by 54% driven by lower revenues across all products, particularly in Equity Derivatives, and also reflecting the exit of Prime

Services22.

|

|

Media Release

Zurich, February 9, 2023

|

|

Progress on our sustainability ambitions and strategy

Credit Suisse has continued to focus on its sustainability strategy, driving activity across divisions and functions in 4Q22. The bank continues to emphasize the importance of

sustainability as a core element of its value proposition for its clients, shareholders, employees and society.

Summary of recent sustainability-related activity:

| ▪ |

4Q22 AuM, classified under Credit Suisse’s Sustainable Investment Framework as Exclusion, Integration, Thematic or Impact, of CHF 132 bn, compared to CHF 150 bn in 4Q21, on the same basis, resulting in a penetration of 10.2% of total AuM

as of December 31, 2022, compared to 9.3% as of the end of 4Q21

|

| ▪ |

Number of WM funds classified according to Credit Suisse’s Sustainable Investment Framework23 increased to 171 as of the end of 4Q22

compared to 156 at the end of 4Q21

|

| ▪ |

Credit Suisse’s bond for The Nature Conservancy's blue loan for Belize, won Capital Monitor’s Most Innovative Sustainable Bond category in their inaugural Sustainable Banking Awards in December 2022

|

| ▪ |

In December we published a dedicated Climate Action Plan for Credit Suisse AM and Investment Solutions & Sustainability within WM, which details the divisions’ goal to achieve net zero across their investment

portfolios by 2050, as well as a 2030 interim goal for a 50% reduction in investment-associated emissions in intensity terms compared to 2019. We continue to review our policies and approach

|

| ▪ |

The 2022 Sustainability Report, which is scheduled for publication on March 9, 2023, will provide further highlights for FY22 such as our progress towards the previously communicated Sustainable Finance, Net Zero

and Diversity & Inclusion ambitions

|

Contact details

Kinner Lakhani, Investor Relations, Credit Suisse

Tel: +41 44 333 71 49

Email: investor.relations@credit-suisse.com

Dominik von Arx, Corporate Communications, Credit Suisse

Tel: +41 844 33 88 44

Email: media.relations@credit-suisse.com

The Earnings Release and Presentation for 4Q22 and FY22 are available to download from 06:45 CET today at:

www.credit-suisse.com/results

Presentation of 4Q22 and FY22 results

Thursday, February 9, 2023

|

Event

|

4Q22 Analyst and Investor Call

|

4Q22 Media Call

|

|

Time

|

08:15 CET (Zurich)

07:15 GMT (London)

02:15 EST (New York)

|

10:30 CET (Zurich)

09:30 GMT (London)

04:30 EST (New York)

|

|

Language

|

English

|

English

|

|

Access

|

Switzerland: +41 58 310 51 26

Europe: +44 121 281 80 12

US: +1 631 232 79 97

Reference:

Credit Suisse Analysts and Investors Call

Conference ID:

20220714

Please dial in 10 minutes before the start

of the call. When dialing in please enter

the Passcode/Conference ID and leave

your first, last name and company name

after the tone. You will be joined

automatically to the conference.

Webcast link here.

|

Switzerland: +41 (0) 583105126

UK: +44 (0) 1212 818 012

US: +1 631 232 7997

Reference:

Credit Suisse Media Call

Conference ID:

20220715

Please dial in 10 minutes before the start

of the call. When dialing in please enter

the Passcode/Conference ID and leave

your first, last name and company name

after the tone. You will be joined

automatically to the conference.

Webcast link here.

|

|

Q&A Session

|

Following the presentation, you will have

the opportunity to ask the speakers

questions if you are an analyst or investor

|

Following the presentation, you will have

the opportunity to ask the speakers

questions

|

|

Playback

|

Replay available at our website.

|

Replay available our website.

|

Abbreviations

AM – Asset Management; APAC – Asia Pacific; AuM – assets under management; bn – billion; CET1 – common equity tier 1; CHF – Swiss francs; ESG – Environmental, Social and Governance; FINMA – Swiss Financial Market

Supervisory Authority FINMA; FTE – Full time equivalent; FX – Foreign Exchange; GAAP – Generally accepted accounting principles; GTS – Global Trading Solutions; HQLA – high-quality liquid assets; IB – Investment Bank; IBOR – interbank offered rates;

IT – Information Technology; LCR – Liquidity Coverage Ratio; mn – million; M&A – Mergers & Acquisitions; NCU – Non-Core Unit; NNA – net new assets; QoQ – Quarter on Quarter; RMBS – Residential mortgage-backed securities; RWA – risk-weighted

assets; SB – Swiss Bank; SNB – Swiss National Bank; SCFF – Supply Chain Finance Funds; SEC – US Securities and Exchange Commission; SIX – SIX Group; SPG – Securitized Product Group; trn – trillion; UK – United Kingdom; US – United States; USD – US

dollar; WM – Wealth Management; YoY – Year on Year

Important information

This document contains select information from the full 4Q22 Earnings Release and 4Q22 Results Presentation slides that Credit Suisse believes is of particular interest to media professionals. The complete 4Q22 Earnings

Release and 4Q22 Results Presentation slides, which have been distributed simultaneously, contain more comprehensive information about our results and operations for the reporting quarter, as well as important information about our reporting

methodology and some of the terms used in these documents. The complete 4Q22 Earnings Release and 4Q22 Results Presentation slides are not incorporated by reference into this document.

Credit Suisse has not finalized restated historical information according to its new divisional structure and Credit Suisse’s independent registered public accounting firm has not reviewed such information. Accordingly, the

preliminary information contained in this presentation is subject to completion of ongoing procedures, which may result in changes to that information, and you should not place undue reliance on this preliminary information.

Credit Suisse has not finalized its 2022 Annual Report and Credit Suisse’s independent registered public accounting firm has not completed its audit of the consolidated financial statements for the period. Accordingly, the

financial information contained in this document is subject to completion of year-end procedures, which may result in changes to that information.

This document contains certain unaudited interim financial information for the first quarter of 2023. This information has been derived from management accounts, is preliminary in nature, does not reflect the complete

results of the first quarter of 2023 and is subject to change, including as a result of any normal quarterly adjustments in relation to the financial statements for the first quarter of 2023. This information has not been subject to any review by our

independent registered public accounting firm. There can be no assurance that the final results for these periods will not differ from these preliminary results, and any such differences could be material. Quarterly financial results for the first

quarter of 2023 will be included in our 1Q23 Financial Report. These interim results of operations are not necessarily indicative of the results to be achieved for the remainder of or the full first quarter of 2023.

Our cost base target is measured using adjusted operating expenses at constant 2022 FX rates and on constant perimeter, before impact of Securitized Products transaction and other divestments.

We may not achieve all of the expected benefits of our strategic initiatives, such as in relation to intended reshaping of the bank, cost reductions and strengthening and reallocating capital. Factors beyond our control,

including but not limited to the market and economic conditions (including macroeconomic and other challenges and uncertainties, for example, resulting from Russia’s invasion of Ukraine), customer reaction to our proposed initiatives, enhanced risks

to our businesses during the contemplated transitions, changes in laws, rules or regulations and other challenges discussed in our public filings, could limit our ability to achieve some or all of the expected benefits of these initiatives. Our

ability to implement our strategy objectives could also be impacted by timing risks, obtaining all required approvals and other factors.

In particular, the terms “Estimate”, “Illustrative”, “Ambition”, “Objective”, “Outlook”, “Goal”, “Commitment” and “Aspiration” are not intended to be viewed as targets or projections, nor are they considered to be Key

Performance Indicators. All such estimates, illustrations, ambitions, objectives, outlooks, goals, commitments and aspirations, as well as any other forward-looking statements described as targets or projections, are subject to a large number of

inherent risks, assumptions and uncertainties, many of which are completely outside of our control. These risks, assumptions and uncertainties include, but are not limited to, general market conditions, market volatility, increased inflation,

interest rate volatility and levels, global and regional economic conditions, challenges and uncertainties resulting from Russia’s invasion of Ukraine, political uncertainty, changes in tax policies, scientific or technological developments, evolving

sustainability strategies, changes in the nature or scope of our operations, including as a result of our recently announced strategy initiatives, changes in carbon markets, regulatory changes, changes in levels of client activity as a result of any

of the foregoing and other factors. Accordingly, these statements, which speak only as of the date made, are not guarantees of future performance and should not be relied on for any purpose. We do not intend to update these estimates, illustrations,

ambitions, objectives, outlooks, goals, commitments, aspirations, targets, projections or any other forward-looking statements. For these reasons, we caution you not to place undue reliance upon any forward-looking statements.

Unless otherwise noted, all such estimates, illustrations, expectations, ambitions, objectives, outlooks, goals, commitments, aspirations, targets and projections are for the full year indicated or as of the end of the year

indicated, as applicable.

In preparing this document, management has made estimates and assumptions that affect the numbers presented. Actual results may differ. Annualized numbers do not take into account variations in operating results,

seasonality and other factors and may not be indicative of actual, full-year results. Figures throughout this document may also be subject to rounding adjustments. All opinions and views constitute good faith judgments as of the date of writing

without regard to the date on which the reader may receive or access the information. This information is subject to change at any time without notice and we do not intend to update this information.

Our estimates, ambitions, objectives, aspirations and targets often include metrics that are non-GAAP financial measures and are unaudited. A reconciliation of the estimates, ambitions, objectives, aspirations and targets

to the nearest GAAP measures is unavailable without unreasonable efforts. Results excluding certain items included in our reported results do not include items such as goodwill impairment, major litigation provisions, real estate gains, impacts from

foreign exchange and other revenue and expense items included in our reported results, all of which are unavailable on a prospective basis. Such estimates, ambitions, objectives, aspirations and targets are calculated in a manner that is consistent

with the accounting policies applied by us in preparing our financial statements.

Return on tangible equity, a non-GAAP financial measure, is calculated as annualized net income attributable to shareholders divided by average tangible shareholders’ equity. Tangible shareholders’ equity, a non-GAAP

financial measure, is calculated by deducting goodwill and other intangible assets from total shareholders’ equity as presented in our balance sheet. Management believes that return on tangible equity is meaningful as it is a measure used and relied

upon by industry analysts and investors to assess valuations and capital adequacy. Adjusted return on tangible equity excluding certain items included in our reported results is calculated using results excluding such items, applying the same

methodology. For end 4Q22, tangible shareholders’ equity excluded goodwill of CHF 2,903 million and other intangible assets of CHF 458 million from total shareholders’ equity of CHF 45,129 million as presented in our balance sheet. For end-3Q22,

tangible shareholders’ equity excluded goodwill of CHF 3,018 million and other intangible assets of CHF 424 million from total shareholders’ equity of CHF 43,267 million as presented in our balance sheet. For end 4Q21, tangible shareholders’ equity

excluded goodwill of CHF 2,917 million and other intangible assets of CHF 276 million from total shareholders’ equity of CHF 43,954 million as presented in our balance sheet.

Credit Suisse is subject to the Basel framework, as implemented in Switzerland, as well as Swiss legislation and regulations for systemically important banks, which include capital, liquidity, leverage and large exposure

requirements and rules for emergency plans designed to maintain systemically relevant functions in the event of threatened insolvency. Credit Suisse has adopted the Bank for International Settlements (BIS) leverage ratio framework, as issued by the

Basel Committee on Banking Supervision (BCBS) and implemented in Switzerland by the Swiss Financial Market Supervisory Authority FINMA (FINMA).

Unless otherwise noted, all CET1 ratio, CET1 leverage ratio, Tier-1 leverage ratio, risk-weighted assets and leverage exposure figures in this document are as of the end of the respective period.

Unless otherwise noted, leverage exposure is based on the BIS leverage ratio framework and consists of period-end balance sheet assets and prescribed regulatory adjustments. The tier 1 leverage ratio and CET1 leverage ratio

are calculated as BIS tier 1 capital and CET1 capital, respectively, divided by period end leverage exposure.

Investors and others should note that we announce important company information (including quarterly earnings releases and financial reports as well as our annual sustainability report) to the investing public using press

releases, SEC and Swiss ad hoc filings, our website and public conference calls and webcasts. We also routinely use our Twitter account @creditsuisse (https://twitter.com/creditsuisse), our LinkedIn account

(https://www.linkedin.com/company/credit-suisse/), our Instagram accounts (https://www.instagram.com/creditsuisse_careers/ and https://www.instagram.com/creditsuisse_ch/), our Facebook account (https://www.facebook.com/creditsuisse/) and other social

media channels as additional means to disclose public information, including to excerpt key messages from our public disclosures. We may share or retweet such messages through certain of our regional accounts, including through Twitter at @csschweiz

(https://twitter.com/csschweiz) and @csapac (https://twitter.com/csapac). Investors and others should take care to consider such abbreviated messages in the context of the disclosures from which they are excerpted. The information we post on these

social media accounts is not a part of this document.

Information referenced in this document, whether via website links or otherwise, is not incorporated into this document.

Certain material in this document has been prepared by Credit Suisse on the basis of publicly available information, internally developed data and other third-party sources believed to be reliable. Credit Suisse has not

sought to independently verify information obtained from public and third-party sources and makes no representations or warranties as to accuracy, completeness, reasonableness or reliability of such information.

In various tables, use of “–” indicates not meaningful or not applicable.

The English language version of this document is the controlling version.

*Refers to results excluding certain items included in our reported results. These are non-GAAP financial measures. For a reconciliation to the most directly comparable US GAAP measures, see the Appendix

of this Media Release.

1 Calculated using a three-month average, which is calculated on a daily basis

2 The Non-Core Unit was established on January 1, 2023; Credit Suisse is providing historical information under the new divisional

structure, which is a preliminary estimate based on management accounts and is subject to change

3 Refers to entities and funds managed by affiliates of Apollo Global Management

4 The registered broker-dealer business of M. Klein & Company LLC

5 Calculated using a three-month average, which is calculated on a daily basis

6 Reflects long-term and short-term funding during 4Q22

7 Average Liquidity Ratio is calculated a three-month average, which is calculated on a daily basis

8 Estimates and assumptions are based on currently available information, beliefs and expectations of management and the actuals may

differ

9 Basis points impact calculated based on the net proceeds

10 FTE reduction includes notified reductions in workforce who were on the payroll as end of 4Q22

11 Excluding the impact from reductions in HQLA allocations

12 Refers to entities and funds managed by affiliates of Apollo Global Management

13 The registered broker-dealer business of M. Klein & Company LLC

14 Estimates and assumptions are based on currently available information, beliefs and expectations of management and the actuals may

differ

15 4Q22 mark-to-market losses of CHF 31 mn (net of CHF (17) mn of hedges)

16 FY22 mark-to-market losses of CHF 121 mn (net of CHF (11) mn of hedges)

17 Gain/(loss) on equity investments of CHF (8) mn in 4Q22 and CHF 6 mn in 4Q21

18 Gain/(loss) on equity investments of CHF (13) mn in 2022 and CHF 7 mn in 2021

19 Gain related to IBOR transition of CHF 1 mn in 2022 and CHF 16 mn in 2021

20 Source: Dealogic (Global) as of December 31, 2022

21 Excludes Archegos gains of USD 19 mn and losses of USD 518 mn from Equity Sales & Trading revenues in 2022 and 2021

22 Includes Index Access and APAC Delta One

23 Includes funds of our Wealth Management Lead Offering, that as of December 31 2022, have been classified under Credit Suisse’s

Sustainable Investment Framework as Exclusion, Integration, Thematic or Impact

|

Appendix

|

|

| Key metrics | |||||||||||||||||

| in / end of | % change | in / end of | % change | ||||||||||||||

| 4Q22 | 3Q22 | 4Q21 | QoQ | YoY | 2022 | 2021 | YoY | ||||||||||

| Credit Suisse Group results (CHF million) | |||||||||||||||||

| Net revenues | 3,060 | 3,804 | 4,582 | (20) | (33) | 14,921 | 22,696 | (34) | |||||||||

| Provision for credit losses | 41 | 21 | (20) | 95 | – | 16 | 4,205 | (100) | |||||||||

| Compensation and benefits | 2,062 | 1,901 | 2,145 | 8 | (4) | 8,813 | 8,963 | (2) | |||||||||

| General and administrative expenses | 1,710 | 1,919 | 2,182 | (11) | (22) | 7,782 | 7,159 | 9 | |||||||||

| Commission expenses | 210 | 250 | 283 | (16) | (26) | 1,012 | 1,243 | (19) | |||||||||

| Goodwill impairment | 0 | – | 1,623 | – | (100) | 23 | 1,623 | (99) | |||||||||

| Restructuring expenses | 352 | 55 | 33 | – | – | 533 | 103 | 417 | |||||||||

| Total other operating expenses | 2,272 | 2,224 | 4,121 | 2 | (45) | 9,350 | 10,128 | (8) | |||||||||

| Total operating expenses | 4,334 | 4,125 | 6,266 | 5 | (31) | 18,163 | 19,091 | (5) | |||||||||

| Loss before taxes | (1,315) | (342) | (1,664) | 285 | (21) | (3,258) | (600) | 443 | |||||||||

| Income tax expense | 82 | 3,698 | 416 | (98) | (80) | 4,048 | 1,026 | 295 | |||||||||

| Loss attributable to shareholders | (1,393) | (4,034) | (2,085) | (65) | (33) | (7,293) | (1,650) | 342 | |||||||||

| Balance sheet statistics (CHF million) | |||||||||||||||||

| Total assets | 531,358 | 700,358 | 755,833 | (24) | (30) | 531,358 | 755,833 | (30) | |||||||||

| Risk-weighted assets | 250,540 | 273,598 | 267,787 | (8) | (6) | 250,540 | 267,787 | (6) | |||||||||

| Leverage exposure | 650,551 | 836,881 | 889,137 | (22) | (27) | 650,551 | 889,137 | (27) | |||||||||

| Assets under management and net new assets (CHF billion) | |||||||||||||||||

| Assets under management | 1,293.6 | 1,400.6 | 1,614.0 | (7.6) | (19.9) | 1,293.6 | 1,614.0 | (19.9) | |||||||||

| Net new assets/(net asset outflows) | (110.5) | (12.9) | 1.6 | – | – | (123.2) | 30.9 | – | |||||||||

| Basel III regulatory capital and leverage statistics (%) | |||||||||||||||||

| CET1 ratio | 14.1 | 12.6 | 14.4 | – | – | 14.1 | 14.4 | – | |||||||||

| CET1 leverage ratio | 5.4 | 4.1 | 4.3 | – | – | 5.4 | 4.3 | – | |||||||||

| Tier 1 leverage ratio | 7.7 | 6.0 | 6.1 | – | – | 7.7 | 6.1 | – | |||||||||

Page A-1

|

Appendix

|

|

Results excluding certain items included in our reported results are non-GAAP financial measures. Following the reorganization implemented at the beginning of 2022, we have amended the presentation of our adjusted results. Management believes that such results provide a useful presentation of our operating results for purposes of assessing our Group and divisional performance consistently over time, on a basis that excludes items that management does not consider representative of our underlying performance. Provided below is a reconciliation to the most directly comparable US GAAP measures.

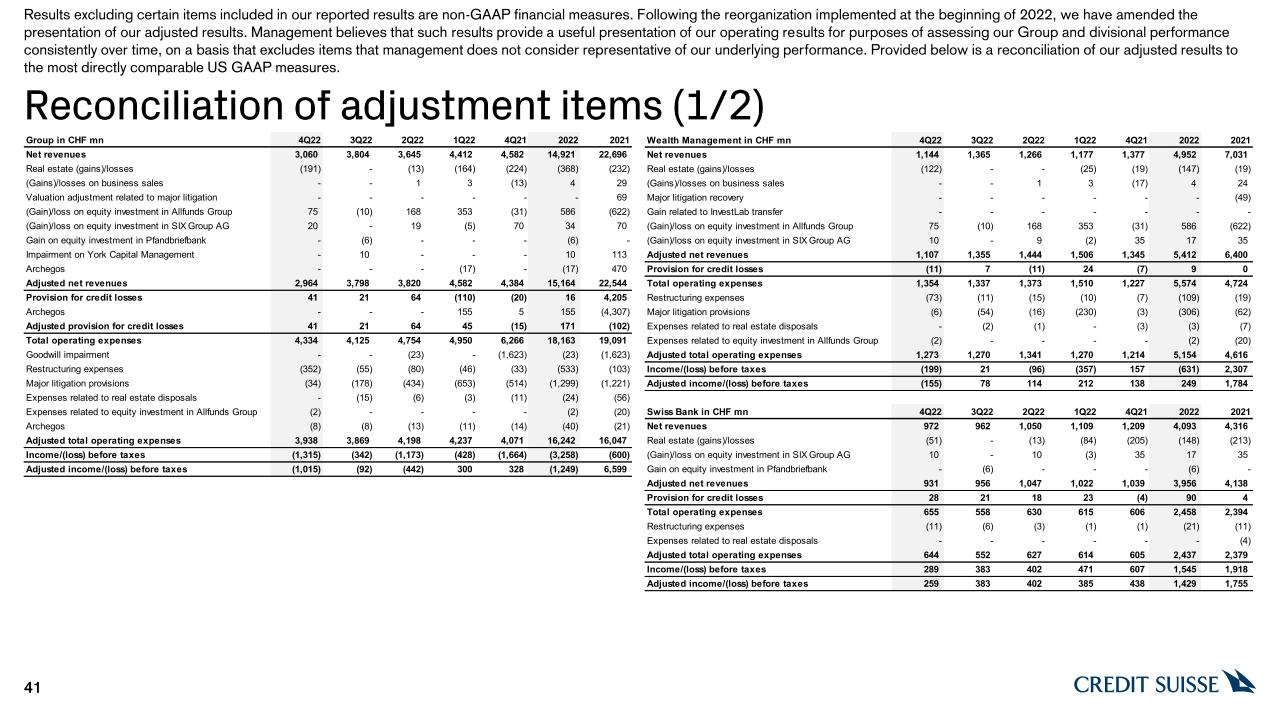

| Reconciliation of adjustment items | |||||||||||

| Group | |||||||||||

| in | 4Q22 | 3Q22 | 4Q21 | 2022 | 2021 | ||||||

| Results (CHF million) | |||||||||||

| Net revenues | 3,060 | 3,804 | 4,582 | 14,921 | 22,696 | ||||||

| Real estate (gains)/losses | (191) | 0 | (224) | (368) | (232) | ||||||

| (Gains)/losses on business sales | 0 | 0 | (13) | 4 | 29 | ||||||

| Major litigation recovery | 0 | 0 | 0 | 0 | (49) | ||||||

| Valuation adjustment related to major litigation | 0 | 0 | 0 | 0 | 69 | ||||||

| (Gain)/loss on equity investment in Allfunds Group | 75 | (10) | (31) | 586 | (622) | ||||||

| (Gain)/loss on equity investment in SIX Group AG | 20 | 0 | 70 | 34 | 70 | ||||||

| (Gain)/loss on equity investment in Pfandbriefbank | 0 | (6) | 0 | (6) | 0 | ||||||

| Impairment on York Capital Management | 0 | 10 | 0 | 10 | 113 | ||||||

| Archegos | 0 | 0 | 0 | (17) | 470 | ||||||

| Adjusted net revenues | 2,964 | 3,798 | 4,384 | 15,164 | 22,544 | ||||||

| Provision for credit losses | 41 | 21 | (20) | 16 | 4,205 | ||||||

| Archegos | 0 | 0 | 5 | 155 | (4,307) | ||||||

| Adjusted provision for credit losses | 41 | 21 | (15) | 171 | (102) | ||||||

| Total operating expenses | 4,334 | 4,125 | 6,266 | 18,163 | 19,091 | ||||||

| Goodwill impairment | – | 0 | (1,623) | (23) | (1,623) | ||||||

| Restructuring expenses | (352) | (55) | (33) | (533) | (103) | ||||||

| Major litigation provisions | (34) | (178) | (514) | (1,299) | (1,221) | ||||||

| Expenses related to real estate disposals | 0 | (15) | (11) | (24) | (56) | ||||||

| Expenses related to equity investment in Allfunds Group | (2) | 0 | 0 | (2) | (20) | ||||||

| Archegos | (8) | (8) | (14) | (40) | (21) | ||||||

| Adjusted total operating expenses | 3,938 | 3,869 | 4,071 | 16,242 | 16,047 | ||||||

| Income/(loss) before taxes | (1,315) | (342) | (1,664) | (3,258) | (600) | ||||||

| Adjusted income/(loss) before taxes | (1,015) | (92) | 328 | (1,249) | 6,599 | ||||||

| Adjusted economic profit | (1,798) | (1,122) | (842) | (5,089) | 808 | ||||||

| Adjusted return on tangible equity (%) | (9.6) | (35.2) | (1.0) | (12.3) | 11.2 | ||||||

Page A-2

|

Appendix

|

|

| Wealth Management | |||||||||||||||||

| in / end of | % change | in / end of | % change | ||||||||||||||

| 4Q22 | 3Q22 | 4Q21 | QoQ | YoY | 2022 | 2021 | YoY | ||||||||||

| Results (CHF million) | |||||||||||||||||

| Net revenues | 1,144 | 1,365 | 1,377 | (16) | (17) | 4,952 | 7,031 | (30) | |||||||||

| Provision for credit losses | (11) | 7 | (7) | – | 57 | 9 | 0 | – | |||||||||

| Total operating expenses | 1,354 | 1,337 | 1,227 | 1 | 10 | 5,574 | 4,724 | 18 | |||||||||

| Income/(loss) before taxes | (199) | 21 | 157 | – | – | (631) | 2,307 | – | |||||||||

| Metrics | |||||||||||||||||

| Economic profit (CHF million) | (316) | (168) | (68) | 88 | 365 | (1,186) | 969 | – | |||||||||

| Cost/income ratio (%) | 118.4 | 97.9 | 89.1 | – | – | 112.6 | 67.2 | – | |||||||||

| Assets under management (CHF billion) | 540.5 | 635.4 | 742.6 | (14.9) | (27.2) | 540.5 | 742.6 | (27.2) | |||||||||

| Net new assets/(net asset outflows) (CHF billion) | (92.7) | (6.4) | (2.9) | – | – | (95.7) | 10.5 | – | |||||||||

| Gross margin (annualized) (bp) | 79 | 83 | 73 | – | – | 75 | 94 | – | |||||||||

| Net margin (annualized) (bp) | (14) | 1 | 8 | – | – | (10) | 31 | – | |||||||||

| Reconciliation of adjustment items | |||||||||||

| Wealth Management | |||||||||||

| in | 4Q22 | 3Q22 | 4Q21 | 2022 | 2021 | ||||||

| Results (CHF million) | |||||||||||

| Net revenues | 1,144 | 1,365 | 1,377 | 4,952 | 7,031 | ||||||

| Real estate (gains)/losses | (122) | 0 | (19) | (147) | 1 | (19) | |||||

| (Gains)/losses on business sales | 0 | 0 | (17) | 4 | 24 | ||||||

| Major litigation recovery | 0 | 0 | 0 | 0 | (49) | ||||||

| (Gain)/loss on equity investment in Allfunds Group | 75 | (10) | (31) | 586 | (622) | ||||||

| (Gain)/loss on equity investment in SIX Group AG | 10 | 0 | 35 | 17 | 35 | ||||||

| Adjusted net revenues | 1,107 | 1,355 | 1,345 | 5,412 | 6,400 | ||||||

| Provision for credit losses | (11) | 7 | (7) | 9 | 0 | ||||||

| Total operating expenses | 1,354 | 1,337 | 1,227 | 5,574 | 4,724 | ||||||

| Restructuring expenses | (73) | (11) | (7) | (109) | (19) | ||||||

| Major litigation provisions | (6) | (54) | (3) | (306) | (62) | ||||||

| Expenses related to real estate disposals | 0 | (2) | (3) | (3) | (7) | ||||||

| Expenses related to equity investment in Allfunds Group | (2) | 0 | 0 | (2) | (20) | ||||||

| Adjusted total operating expenses | 1,273 | 1,270 | 1,214 | 5,154 | 4,616 | ||||||

| Income/(loss) before taxes | (199) | 21 | 157 | (631) | 2,307 | ||||||

| Adjusted income/(loss) before taxes | (155) | 78 | 138 | 249 | 1,784 | ||||||

| Adjusted economic profit | (282) | (126) | (82) | (526) | 578 | ||||||

| Adjusted return on regulatory capital (%) | (5.5) | 2.5 | 4.5 | 2.1 | 14.2 | ||||||

|

1

Of which CHF 142 million is reflected in other revenues and CHF 5 million is reflected in transaction- and performance-based revenues.

|

|||||||||||

Page A-3

|

Appendix

|

|

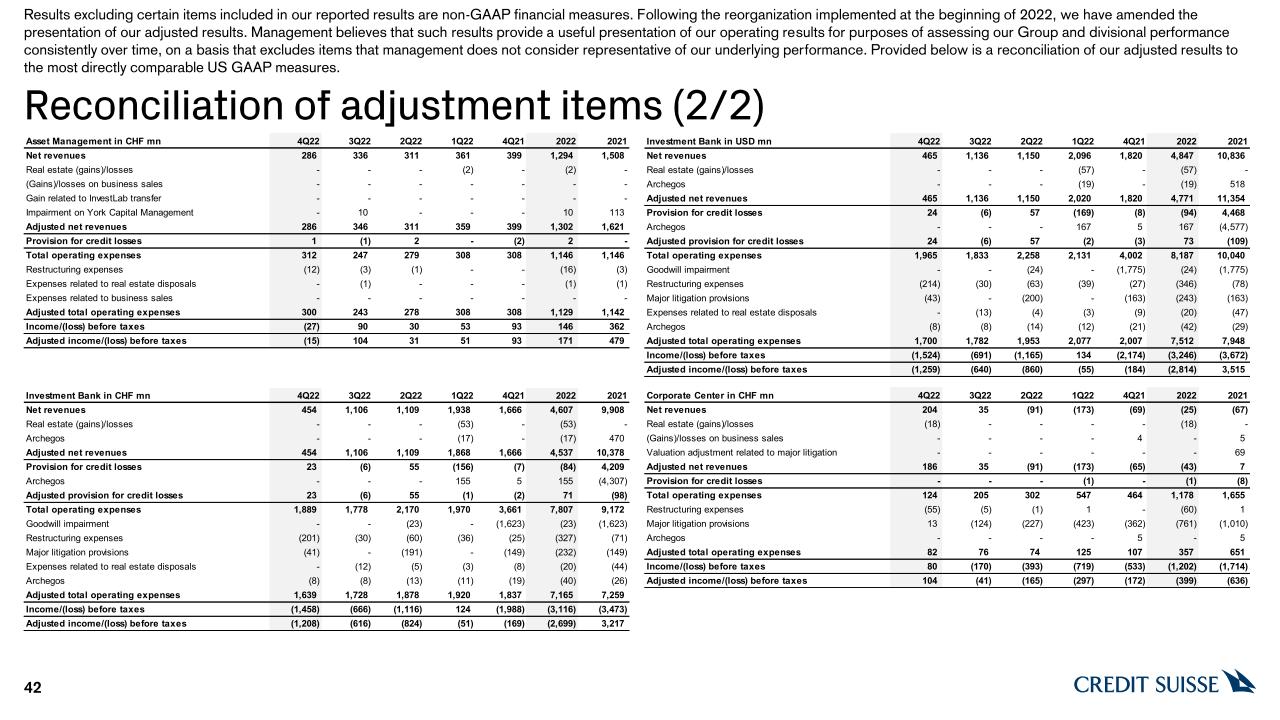

| Investment Bank | |||||||||||||||||

| in / end of | % change | in / end of | % change | ||||||||||||||

| 4Q22 | 3Q22 | 4Q21 | QoQ | YoY | 2022 | 2021 | YoY | ||||||||||

| Results (CHF million) | |||||||||||||||||

| Net revenues | 454 | 1,106 | 1,666 | (59) | (73) | 4,607 | 9,908 | (54) | |||||||||

| Provision for credit losses | 23 | (6) | (7) | – | – | (84) | 4,209 | – | |||||||||

| Total operating expenses | 1,889 | 1,778 | 3,661 | 6 | (48) | 7,807 | 9,172 | (15) | |||||||||

| Loss before taxes | (1,458) | (666) | (1,988) | 119 | (27) | (3,116) | (3,473) | (10) | |||||||||

| Metrics | |||||||||||||||||

| Economic profit (CHF million) | (1,420) | (873) | (1,897) | 63 | (25) | (3,810) | (4,347) | (12) | |||||||||

| Cost/income ratio (%) | 416.1 | 160.8 | 219.7 | – | – | 169.5 | 92.6 | – | |||||||||

| Results (USD million) | |||||||||||||||||

| Net revenues | 465 | 1,136 | 1,820 | (59) | (74) | 4,847 | 10,836 | (55) | |||||||||

| Provision for credit losses | 24 | (6) | (8) | – | – | (94) | 4,468 | – | |||||||||

| Total operating expenses | 1,965 | 1,833 | 4,002 | 7 | (51) | 8,187 | 10,040 | (18) | |||||||||

| Loss before taxes | (1,524) | (691) | (2,174) | 121 | (30) | (3,246) | (3,672) | (12) | |||||||||

| Net revenue detail | |||||||||||

| in / end of | 4Q22 | 3Q22 | 4Q21 | 2022 | 2021 | ||||||

| Net revenue detail (USD million) | |||||||||||

| Fixed income sales and trading | 81 | 558 | 504 | 2,063 | 3,861 | ||||||

| Equity sales and trading | 15 | 248 | 403 | 1,150 | 1,959 | ||||||

| Capital markets | 200 | 99 | 585 | 803 | 3,923 | ||||||

| Advisory and other fees | 175 | 232 | 331 | 818 | 1,106 | ||||||

| Other revenues | (6) | (1) | (3) | 13 | (13) | ||||||

| Net revenues | 465 | 1,136 | 1,820 | 4,847 | 10,836 | ||||||

Page A-4

|

Appendix

|

|

| Reconciliation of adjustment items | |||||||||||

| Investment Bank | |||||||||||

| in | 4Q22 | 3Q22 | 4Q21 | 2022 | 2021 | ||||||

| Results (CHF million) | |||||||||||

| Net revenues | 454 | 1,106 | 1,666 | 4,607 | 9,908 | ||||||

| Real estate (gains)/losses | 0 | 0 | 0 | (53) | 0 | ||||||

| Archegos | 0 | 0 | 0 | (17) | 470 | ||||||

| Adjusted net revenues | 454 | 1,106 | 1,666 | 4,537 | 10,378 | ||||||

| Provision for credit losses | 23 | (6) | (7) | (84) | 4,209 | ||||||

| Archegos | 0 | 0 | 5 | 155 | (4,307) | ||||||

| Adjusted provision for credit losses | 23 | (6) | (2) | 71 | (98) | ||||||

| Total operating expenses | 1,889 | 1,778 | 3,661 | 7,807 | 9,172 | ||||||

| Goodwill impairment | 0 | 0 | (1,623) | (23) | (1,623) | ||||||

| Restructuring expenses | (201) | (30) | (25) | (327) | (71) | ||||||

| Major litigation provisions | (41) | 0 | (149) | (232) | (149) | ||||||

| Expenses related to real estate disposals | 0 | (12) | (8) | (20) | (44) | ||||||

| Archegos | (8) | (8) | (19) | (40) | (26) | ||||||

| Adjusted total operating expenses | 1,639 | 1,728 | 1,837 | 7,165 | 7,259 | ||||||

| Income/(loss) before taxes | (1,458) | (666) | (1,988) | (3,116) | (3,473) | ||||||

| Adjusted income/(loss) before taxes | (1,208) | (616) | (169) | (2,699) | 3,217 | ||||||

| Adjusted economic profit | (1,233) | (835) | (533) | (3,497) | 670 | ||||||

| Adjusted return on regulatory capital (%) | (33.0) | (14.9) | (3.8) | (16.4) | 16.9 | ||||||

| Reconciliation of adjustment items | |||||||||||

| Investment Bank | |||||||||||

| in | 4Q22 | 3Q22 | 4Q21 | 2022 | 2021 | ||||||

| Results (USD million) | |||||||||||

| Net revenues | 465 | 1,136 | 1,820 | 4,847 | 10,836 | ||||||

| Real estate (gains)/losses | 0 | 0 | 0 | (57) | 0 | ||||||

| Archegos | 0 | 0 | 0 | (19) | 518 | ||||||

| Adjusted net revenues | 465 | 1,136 | 1,820 | 4,771 | 11,354 | ||||||

| Provision for credit losses | 24 | (6) | (8) | (94) | 4,468 | ||||||

| Archegos | 0 | 0 | 5 | 167 | (4,577) | ||||||

| Adjusted provision for credit losses | 24 | (6) | (3) | 73 | (109) | ||||||

| Total operating expenses | 1,965 | 1,833 | 4,002 | 8,187 | 10,040 | ||||||

| Goodwill impairment | – | – | (1,775) | (24) | (1,775) | ||||||

| Restructuring expenses | (214) | (30) | (27) | (346) | (78) | ||||||

| Major litigation provisions | (43) | 0 | (163) | (243) | (163) | ||||||

| Expenses related to real estate disposals | 0 | (13) | (9) | (20) | (47) | ||||||

| Archegos | (8) | (8) | (21) | (42) | (29) | ||||||

| Adjusted total operating expenses | 1,700 | 1,782 | 2,007 | 7,512 | 7,948 | ||||||

| Income/(loss) before taxes | (1,524) | (691) | (2,174) | (3,246) | (3,672) | ||||||

| Adjusted income/(loss) before taxes | (1,259) | (640) | (184) | (2,814) | 3,515 | ||||||

| Adjusted economic profit | (1,286) | (866) | (579) | (3,671) | 751 | ||||||

| Adjusted return on regulatory capital (%) | (33.0) | (14.9) | (3.8) | (16.4) | 16.9 | ||||||

Page A-5

|

Appendix

|

|

| Swiss Bank | |||||||||||||||||

| in / end of | % change | in / end of | % change | ||||||||||||||

| 4Q22 | 3Q22 | 4Q21 | QoQ | YoY | 2022 | 2021 | YoY | ||||||||||

| Results (CHF million) | |||||||||||||||||

| Net revenues | 972 | 962 | 1,209 | 1 | (20) | 4,093 | 4,316 | (5) | |||||||||

| Provision for credit losses | 28 | 21 | (4) | 33 | – | 90 | 4 | – | |||||||||

| Total operating expenses | 655 | 558 | 606 | 17 | 8 | 2,458 | 2,394 | 3 | |||||||||

| Income before taxes | 289 | 383 | 607 | (25) | (52) | 1,545 | 1,918 | (19) | |||||||||

| Metrics | |||||||||||||||||

| Economic profit (CHF million) | 24 | 88 | 256 | (73) | (91) | 367 | 629 | (42) | |||||||||

| Cost/income ratio (%) | 67.4 | 58.0 | 50.1 | – | – | 60.1 | 55.5 | – | |||||||||

| Assets under management (CHF billion) | 525.8 | 527.1 | 597.9 | (0.2) | (12.1) | 525.8 | 597.9 | (12.1) | |||||||||

| Net new assets/(net asset outflows) (CHF billion) | (8.3) | (1.5) | 1.0 | – | – | (5.4) | 5.9 | – | |||||||||

| Gross margin (annualized) (bp) | 73 | 71 | 82 | – | – | 73 | 74 | – | |||||||||

| Net margin (annualized) (bp) | 22 | 28 | 41 | – | – | 28 | 33 | – | |||||||||

| Reconciliation of adjustment items | |||||||||||

| Swiss Bank | |||||||||||

| in | 4Q22 | 3Q22 | 4Q21 | 2022 | 2021 | ||||||

| Results (CHF million) | |||||||||||

| Net revenues | 972 | 962 | 1,209 | 4,093 | 4,316 | ||||||

| Real estate (gains)/losses | (51) | 0 | (205) | (148) | (213) | ||||||

| (Gain)/loss on equity investment in SIX Group AG | 10 | 0 | 35 | 17 | 35 | ||||||

| (Gain)/loss on equity investment in Pfandbriefbank | 0 | (6) | 0 | (6) | 0 | ||||||

| Adjusted net revenues | 931 | 956 | 1,039 | 3,956 | 4,138 | ||||||

| Provision for credit losses | 28 | 21 | (4) | 90 | 4 | ||||||

| Total operating expenses | 655 | 558 | 606 | 2,458 | 2,394 | ||||||

| Restructuring expenses | (11) | (6) | (1) | (21) | (11) | ||||||

| Expenses related to real estate disposals | 0 | 0 | 0 | 0 | (4) | ||||||

| Adjusted total operating expenses | 644 | 552 | 605 | 2,437 | 2,379 | ||||||

| Income before taxes | 289 | 383 | 607 | 1,545 | 1,918 | ||||||

| Adjusted income before taxes | 259 | 383 | 438 | 1,429 | 1,755 | ||||||

| Adjusted economic profit | 1 | 88 | 129 | 280 | 506 | ||||||

| Adjusted return on regulatory capital (%) | 8.1 | 11.5 | 13.2 | 10.9 | 13.0 | ||||||

Page A-6

|

Appendix

|

|

| Asset Management | |||||||||||||||||

| in / end of | % change | in / end of | % change | ||||||||||||||

| 4Q22 | 3Q22 | 4Q21 | QoQ | YoY | 2022 | 2021 | YoY | ||||||||||

| Results (CHF million) | |||||||||||||||||

| Net revenues | 286 | 336 | 399 | (15) | (28) | 1,294 | 1,508 | (14) | |||||||||

| Provision for credit losses | 1 | (1) | (2) | – | – | 2 | 0 | – | |||||||||

| Total operating expenses | 312 | 247 | 308 | 26 | 1 | 1,146 | 1,146 | 0 | |||||||||

| Income/(loss) before taxes | (27) | 90 | 93 | – | – | 146 | 362 | (60) | |||||||||

| Metrics | |||||||||||||||||

| Economic profit (CHF million) | (32) | 55 | 57 | – | – | 60 | 215 | (72) | |||||||||

| Cost/income ratio (%) | 109.1 | 73.5 | 77.2 | – | – | 88.6 | 76.0 | – | |||||||||

| Reconciliation of adjustment items | |||||||||||

| Asset Management | |||||||||||

| in | 4Q22 | 3Q22 | 4Q21 | 2022 | 2021 | ||||||

| Results (CHF million) | |||||||||||

| Net revenues | 286 | 336 | 399 | 1,294 | 1,508 | ||||||

| Real estate (gains)/losses | 0 | 0 | 0 | (2) | 0 | ||||||

| Impairment on York Capital Management | 0 | 10 | 0 | 10 | 113 | ||||||

| Adjusted net revenues | 286 | 346 | 399 | 1,302 | 1,621 | ||||||

| Provision for credit losses | 1 | (1) | (2) | 2 | 0 | ||||||

| Total operating expenses | 312 | 247 | 308 | 1,146 | 1,146 | ||||||