Filed Pursuant to Rule 424(b)(2)

Registration Statement No. 333-238458-02

The information in this preliminary pricing supplement is not complete and may be changed. This preliminary pricing supplement is not an offer to sell, nor does it seek an offer to buy, these notes in any jurisdiction where the offer or sale is not permitted.

Subject to Completion. Dated January 6, 2022.

Pricing Supplement No. A400 to the Underlying Supplement dated June 18, 2020, the Product Supplement No. I-B dated June 18, 2020, the Prospectus Supplement and Prospectus dated June 18, 2020

_________________________________________________________

$

Leveraged Basket-Linked Medium-Term Notes due

The notes will not bear interest. The amount that you will be paid on your notes on the stated maturity date (expected to be the second scheduled business day after the determination date) is based on the performance of a weighted basket comprised of the EURO STOXX 50® Index (36.00% weighting), the TOPIX® (29.00% weighting), the FTSE® 100 Index (16.00% weighting), the Swiss Market Index® (11.00% weighting) and the S&P/ASX 200 Index (8.00% weighting) as measured from and including the trade date to and including the determination date (expected to be between 18 and 21 months after the trade date). The initial basket level is 100 and the final basket level will equal the sum of the products, as calculated for each basket underlier, of: (i) the final index level divided by (ii) the initial index level (set on the trade date and which may be higher or lower than the actual closing level of such basket underlier on the trade date) multiplied by (iii) the applicable initial weighted value for each basket underlier. If the final basket level on the determination date is greater than the initial basket level, the return on your notes will be positive, subject to the maximum settlement amount (expected to be between $1,256.80 and $1,301.40 for each $1,000 face amount of your notes). If the final basket level is less than the initial basket level, the return on your notes will be negative. You could lose your entire investment in the notes. Any payment on the notes is subject to our ability to pay our obligations as they become due.

To determine your payment at maturity, we will calculate the basket return, which is the percentage increase or decrease in the final basket level from the initial basket level. On the stated maturity date, for each $1,000 face amount of your notes, you will receive an amount in cash equal to:

| ● | if the basket return is positive (i.e., the final basket level is greater than the initial basket level), the sum of (i) $1,000 plus (ii) the product of (a) $1,000 times (b) 200% times (c) the basket return, such sum subject to the maximum settlement amount; or |

| ● | if the basket return is zero or negative (i.e., the final basket level is equal to or less than the initial basket level), the sum of (i) $1,000 plus (ii) the product of (a) $1,000 times (b) the basket return. |

Declines in one basket underlier may offset increases in the other basket underliers. Due to the unequal weighting of each basket underlier, the performance of each basket underlier will have varying impact on your return on the notes. For example, the performances of the EURO STOXX 50® Index, the TOPIX® and the FTSE® 100 Index will have a significantly larger impact on your return on the notes than the performance of the Swiss Market Index® and the S&P/ASX 200 Index.

Investing in the notes involves a number of risks. See “Additional Risk Factors Specific To Your Notes” beginning on page PS-14 of this pricing supplement and “Risk Factors” beginning on page PS-3 of the accompanying product supplement.

| Original issue date: | , 2022 | Original issue price: | 100% of the face amount |

| Underwriting discount: | % of the face amount | Net proceeds to the issuer: | % of the face amount |

We or one of our affiliates will pay an underwriting discount of up to $15.10 per $1,000 face amount of the notes ($ in the aggregate), resulting in net proceeds to the issuer of between $984.90 and $1,000 per $1,000 face amount of the notes ($ in the aggregate).

For more detailed information, please see “Supplemental plan of distribution (conflicts of interest)” on page PS-7 of this pricing supplement.

The agent for this offering, Credit Suisse Securities (USA) LLC (“CSSU”), is our affiliate. For more information, see “Supplemental plan of distribution (conflicts of interest)” on page PS-7 of this pricing supplement.

Neither the Securities and Exchange Commission nor any other regulatory body has approved or disapproved of these notes or passed upon the accuracy or adequacy of this pricing supplement, the accompanying product supplement, the accompanying underlying supplement, the accompanying prospectus supplement or the accompanying prospectus. Any representation to the contrary is a criminal offense.

Credit Suisse currently estimates the value of each $1,000 face amount of the notes on the trade date will be between $950.80 and $980.80 (as determined by reference to our pricing models and the rate we are currently paying to borrow funds through issuance of the notes (our “internal funding rate”)). This range of estimated values reflects terms that are not yet fixed. A single estimated value reflecting final terms will be determined on the trade date. See “Additional Risk Factors Specific To Your Notes” in this pricing supplement.

The notes are not deposit liabilities and are not insured or guaranteed by the Federal Deposit Insurance Corporation or any other governmental agency of the United States, Switzerland or any other jurisdiction.

Credit Suisse

Pricing Supplement dated January , 2022.

The original issue price, underwriting discount and net proceeds to the issuer listed above relate to the notes we sell initially. We may decide to sell additional notes after the date of this pricing supplement, at issue prices and with underwriting discounts and net proceeds that differ from the amounts set forth above. The return (whether positive or negative) on your investment in the notes will depend in part on the issue price you pay for such notes.

We may use this pricing supplement in the initial sale of the notes. In addition, CSSU or any other affiliate of ours may use this pricing supplement in a market-making transaction in a note after its initial sale. Unless Credit Suisse or its agent informs the purchaser otherwise in the confirmation of sale, this pricing supplement is being used in a market-making transaction.

SUMMARY INFORMATION

You may revoke your offer to purchase the notes at any time prior to the time at which we accept such offer on the date the notes are priced. We reserve the right to change the terms of, or reject any offer to purchase the notes prior to their issuance. In the event of any changes to the terms of the notes, we will notify you and you will be asked to accept such changes in connection with your purchase. You may also choose to reject such changes in which case we may reject your offer to purchase.

We refer to the notes we are offering by this pricing supplement as the “offered notes” or the “notes”. Each of the offered notes, including your notes, has the terms described below.

You should read this pricing supplement together with the underlying supplement dated June 18, 2020, the product supplement dated June 18, 2020, the prospectus supplement dated June 18, 2020 and the prospectus dated June 18, 2020, relating to our Medium-Term Notes of which these notes are a part. You may access these documents on the SEC website at www.sec.gov as follows (or if such address has changed, by reviewing our filings for the relevant date on the SEC website):

| ● | Underlying Supplement dated June 18, 2020: https://www.sec.gov/Archives/edgar/data/1053092/000095010320011950/dp130454_424b2-eus.htm |

| ● | Product Supplement No. I-B dated June 18, 2020: https://www.sec.gov/Archives/edgar/data/1053092/000095010320011955/dp130588_424b2-ps1b.htm |

| ● | Prospectus Supplement and Prospectus dated June 18, 2020: https://www.sec.gov/Archives/edgar/data/1053092/000110465920074474/tm2019510-8_424b2.htm |

In the event the terms of the notes described in this pricing supplement differ from, or are inconsistent with, the terms described in the underlying supplement, product supplement, prospectus supplement or prospectus, the terms described in this pricing supplement will control.

Our Central Index Key, or CIK, on the SEC website is 1053092. As used in this pricing supplement, “we,” “us,” or “our” refers to Credit Suisse.

This pricing supplement, together with the documents listed above, contains the terms of the notes and supersedes all other prior or contemporaneous oral statements as well as any other written materials including preliminary or indicative pricing terms, fact sheets, correspondence, trade ideas, structures for implementation, sample structures, brochures or other educational materials of ours. We may, without the consent of the registered holder of the notes and the owner of any beneficial interest in the notes, amend the notes to conform to its terms as set forth in this pricing supplement and the documents listed above, and the trustee is authorized to enter into any such amendment without any such consent. You should carefully consider, among other things, the matters set forth in “Additional Risk Factors Specific To Your Notes” in this pricing supplement and “Risk Factors” in the accompanying product supplement, “Foreign Currency Risks” in the accompanying prospectus, and any risk factors we describe in the combined Annual Report on Form 20-F of Credit Suisse Group AG and us incorporated by reference therein, and any additional risk factors we describe in future filings we make with the SEC under the Securities Exchange Act of 1934, as amended, as the notes involve risks not associated with conventional debt securities. You should consult your investment, legal, tax, accounting and other advisors before deciding to invest in the notes.

PS-3

Key Terms

Issuer: Credit Suisse AG (“Credit Suisse”), acting through its London Branch.

Basket underliers: the EURO STOXX 50® Index (Bloomberg symbol, <SX5E Index>), as published by STOXX Limited (“STOXX”); the TOPIX® (Bloomberg symbol, <TPX Index>), as maintained by the Tokyo Stock Exchange, Inc. (“TSE”); the FTSE® 100 Index (Bloomberg symbol, <UKX Index>), as published by FTSE Russell (“FTSE”); the Swiss Market Index® (Bloomberg symbol, <SMI Index>), as published by SIX Group Ltd. (“SIX Group”); and the S&P/ASX 200 Index (Bloomberg symbol, <AS51 Index>), as published by S&P Dow Jones Indices LLC (“S&P”). For more information on the basket underliers, see “The Reference Indices—The STOXX Indices—The EURO STOXX 50® Index,” “The Reference Indices—The Tokyo Stock Price Index,” “The Reference Indices—The FTSE Russell Indices—The FTSE® 100 Index,” “The Reference Indices—The Swiss Market Index®” and “The Reference Indices—The S&P Dow Jones Indices—The S&P/ASX 200 Index” in the accompanying underlying supplement.

Specified currency: U.S. dollars (“$”)

Face amount: each note will have a face amount of $1,000; $ in the aggregate for all the offered notes; the aggregate face amount of the offered notes may be increased if the issuer, at its sole option, decides to sell an additional amount of the offered notes on a date subsequent to the date of this pricing supplement.

Purchase at amount other than face amount: the amount we will pay you at the stated maturity date for your notes will not be adjusted based on the issue price you pay for your notes, so if you acquire notes at a premium (or discount) to face amount and hold them to the stated maturity date, it could affect your investment in a number of ways. The return on your investment in such notes will be lower (or higher) than it would have been had you purchased the notes at face amount. Also, the cap level would be triggered at a lower (or higher) percentage return relative to your initial investment than indicated below. See “Additional Risk Factors Specific to Your Notes — If You Purchase Your Notes at a Premium to Face Amount, the Return on Your Investment Will Be Lower Than the Return on Notes Purchased at Face Amount and the Impact of Certain Key Terms of the Notes Will be Negatively Affected” on page PS-15 of this pricing supplement.

United States Federal Income Tax Consequences of Investing in the Notes: please refer to “Material U.S. Federal Income Tax Considerations” herein for a discussion of certain United States federal income tax considerations for making an investment in the notes.

Cash settlement amount (on the stated maturity date): for each $1,000 face amount of your notes, we will pay you on the stated maturity date an amount in cash equal to:

| ● | if the final basket level is greater than or equal to the cap level, the maximum settlement amount; |

| ● | if the final basket level is greater than the initial basket level but less than the cap level, the sum of (1) $1,000 plus (2) the product of (i) $1,000 times (ii) the upside participation rate times (iii) the basket return; or |

| ● | if the final basket level is equal to or less than the initial basket level, the sum of (1) $1,000 plus (2) the product of (i) $1,000 times (ii) the basket return. |

Initial basket level: 100

Initial weighted value: the initial weighted value for each of the basket underliers is expected to equal the product of the initial weight of such basket underlier times the initial basket level. The initial weight of each basket underlier is shown in the table below:

| Basket Underlier | Initial Weight in Basket |

| EURO STOXX 50® Index | 36.00% |

| TOPIX® | 29.00% |

| FTSE® 100 Index | 16.00% |

| Swiss Market Index® | 11.00% |

| S&P/ASX 200 Index | 8.00% |

PS-4

Initial EURO STOXX 50® Index level: the closing level or an intraday level of such basket underlier to be set on the trade date, as determined by the calculation agent in its sole discretion, and which may be higher or lower than the actual closing level of such basket underlier on the trade date.

Initial TOPIX® level: the closing level or an intraday level of such basket underlier to be set on the trade date, as determined by the calculation agent in its sole discretion, and which may be higher or lower than the actual closing level of such basket underlier on the trade date.

Initial FTSE® 100 Index level: the closing level or an intraday level of such basket underlier to be set on the trade date, as determined by the calculation agent in its sole discretion, and which may be higher or lower than the actual closing level of such basket underlier on the trade date.

Initial Swiss Market Index® level: the closing level or an intraday level of such basket underlier to be set on the trade date, as determined by the calculation agent in its sole discretion, and which may be higher or lower than the actual closing level of such basket underlier on the trade date.

Initial S&P/ASX 200 Index level: the closing level or an intraday level of such basket underlier to be set on the trade date, as determined by the calculation agent in its sole discretion, and which may be higher or lower than the actual closing level of such basket underlier on the trade date.

We refer to each of the Initial EURO STOXX 50® Index level, Initial TOPIX® level, Initial FTSE® 100 Index level, Initial Swiss Market Index® level and Initial S&P/ASX 200 Index level as an initial underlier level, as applicable.

Final EURO STOXX 50® Index level: the closing level of such basket underlier on the determination date, except in the circumstances described under “Description of the Securities — Postponement of calculation dates” on page PS-22 of the accompanying product supplement and subject to adjustment as provided under “Description of the Securities — Changes to the calculation of an underlying” on page PS-24 of the accompanying product supplement.

Final TOPIX® level: the closing level of such basket underlier on the determination date, except in the circumstances described under “Description of the Securities — Postponement of calculation dates” on page PS-22 of the accompanying product supplement and subject to adjustment as provided under “Description of the Securities — Changes to the calculation of an underlying” on page PS-24 of the accompanying product supplement.

Final FTSE® 100 Index level: the closing level of such basket underlier on the determination date, except in the circumstances described under “Description of the Securities — Postponement of calculation dates” on page PS-22 of the accompanying product supplement and subject to adjustment as provided under “Description of the Securities — Changes to the calculation of an underlying” on page PS-24 of the accompanying product supplement.

Final Swiss Market Index® level: the closing level of such basket underlier on the determination date, except in the circumstances described under “Description of the Securities — Postponement of calculation dates” on page PS-22 of the accompanying product supplement and subject to adjustment as provided under “Description of the Securities — Changes to the calculation of an underlying” on page PS-24 of the accompanying product supplement.

Final S&P/ASX 200 Index level: the closing level of such basket underlier on the determination date, except in the circumstances described under “Description of the Securities — Postponement of calculation dates” on page PS-22 of the accompanying product supplement and subject to adjustment as provided under “Description of the Securities — Changes to the calculation of an underlying” on page PS-24 of the accompanying product supplement.

PS-5

We refer to each of the Final EURO STOXX 50® Index level, Final TOPIX® level, Final FTSE® 100 Index level, Final Swiss Market Index® level and Final S&P/ASX 200 Index level as a final underlier level, as applicable.

Final basket level: the sum of the following: (1) the final EURO STOXX 50® Index level divided by the initial EURO STOXX 50® Index level, multiplied by the initial weighted value of the EURO STOXX 50® Index plus (2) the final TOPIX® level divided by the initial TOPIX® level, multiplied by the initial weighted value of the TOPIX® plus (3) the final FTSE® 100 Index level divided by the initial FTSE® 100 Index level, multiplied by the initial weighted value of the FTSE® 100 Index plus (4) the final Swiss Market Index® level divided by the initial Swiss Market Index® level, multiplied by the initial weighted value of the Swiss Market Index® plus (5) the final S&P/ASX 200 Index level divided by the initial S&P/ASX 200 Index level, multiplied by the initial weighted value of the S&P/ASX 200 Index.

Basket return: the quotient of (1) the final basket level minus the initial basket level divided by (2) the initial basket level, expressed as a percentage

Upside participation rate: 200%

Cap level (to be set on the trade date): expected to be between 112.84% and 115.07% of the initial basket level.

Maximum settlement amount (to be set on the trade date): for each $1,000 face amount of the notes, expected to be between $1,256.80 and $1,301.40.

Trade date:

Original issue date (to be set on the trade date): a specified date that is expected to be the fifth scheduled business day following the trade date.

Determination date (to be set on the trade date): a specified date that is expected to be between 18 and 21 months after the trade date, subject to postponement as described under “Description of the Securities—Postponement of calculation dates” on page PS-22 of the accompanying product supplement.

Stated maturity date (to be set on the trade date): a specified date that is expected to be the second scheduled business day after the determination date, subject to postponement as described under “Description of the Securities — Postponement of calculation dates” on page PS-22 of the accompanying product supplement. If the stated maturity date is not a business day, the stated maturity date will be postponed to the next following business day. Notwithstanding anything to the contrary set forth in the accompanying product supplement, if the determination date is postponed as provided under “Determination date” above, the stated maturity date will be postponed to the second business day following the determination date as postponed.

No interest: the offered notes will not bear interest.

No listing: the offered notes will not be listed on any securities exchange or interdealer quotation system.

No redemption: the offered notes will not be subject to redemption.

Closing level: as described under “Description of the Securities — Certain definitions” on page PS-19 of the accompanying product supplement.

Business day: as described under “Description of the Securities — Certain definitions” on page PS-19 of the accompanying product supplement.

Trading day: as described under “Description of the Securities — Certain definitions” on page PS-19 of the accompanying product supplement.

Use of proceeds and hedging: as described under “Supplemental Use of Proceeds and Hedging” on page PS-16 of the accompanying product supplement.

ERISA: as described under “ERISA Considerations” on page PS-45 of the accompanying product supplement.

PS-6

Supplemental plan of distribution (conflicts of interest): under the terms and subject to the conditions contained in a distribution agreement dated May 7, 2007, as amended, which we refer to as the distribution agreement, we have agreed to sell the notes to CSSU.

The distribution agreement provides that CSSU is obligated to purchase all of the notes if any are purchased.

Credit Suisse AG expects to agree to sell to CSSU, and CSSU expects to agree to purchase from Credit Suisse AG, the aggregate face amount of the offered notes specified on the front cover of this pricing supplement. CSSU proposes initially to offer the notes to the public at the original issue price set forth on the cover page of this pricing supplement, and to certain unaffiliated securities dealers at such price less a concession not in excess of 1.51% of the face amount.

We expect to deliver the notes against payment for the notes on the original issue date indicated herein, which may be a date that is greater than two business days following the trade date. Under Rule 15c6-1 of the Securities Exchange Act of 1934, as amended, trades in the secondary market generally are required to settle in two business days, unless the parties to a trade expressly agree otherwise. Accordingly, if the original issue date is more than two business days after the trade date, purchasers who wish to transact in the notes more than two business days prior to the original issue date will be required to specify alternative settlement arrangements to prevent a failed settlement.

The agent for this offering, CSSU, is our affiliate. In accordance with FINRA Rule 5121, CSSU may not make sales in this offering to any of its discretionary accounts without the prior written approval of the customer. A portion of the net proceeds from the sale of the notes will be used by CSSU or one of its affiliates in connection with hedging our obligations under the notes.

For further information, please refer to “Underwriting (Conflicts of Interest)” in the accompanying product supplement.

Calculation agent: Credit Suisse International

Events of Default: With respect to these notes, the first bullet of the first sentence of “Description of Debt Securities— Events of Default” in the accompanying prospectus is amended to read in its entirety as follows:

| · | a default in payment of the principal or any premium on any debt security of that series when due, and such default continues for 30 days; |

CUSIP no.: 22553PEL9

ISIN no.: US22553PEL94

FDIC: the notes are not deposit liabilities and are not insured

or guaranteed by the Federal Deposit Insurance Corporation or any other governmental agency of the United States, Switzerland or any other

jurisdiction.

PS-7

Supplemental Terms of the Notes

For purposes of the notes offered by this pricing supplement, all references to each of the following defined terms used in the accompanying product supplement will be deemed to refer to the corresponding defined term used in this pricing supplement, as set forth in the table below:

| Product Supplement Defined Term | Pricing Supplement Defined Term |

| Maturity date | Stated maturity date |

| Valuation date | Determination date |

| Securities | Notes or offered notes |

| Principal amount | Face amount |

| Redemption amount | Cash settlement amount |

| Underlying | Basket underlier |

In addition, with respect to the Leveraged Basket-Linked Medium-Term

Notes, please refer to Key Terms above for the following terms: upside participation rate and maximum settlement amount.

PS-8

HYPOTHETICAL EXAMPLES

The following table and chart are provided for purposes of illustration only. They should not be taken as an indication or prediction of future investment results and are intended merely to illustrate the impact that the various hypothetical final basket levels or hypothetical final underlier levels of the basket underliers, as applicable, on the determination date could have on the cash settlement amount at maturity assuming all other variables remain constant.

The examples below are based on a range of final basket levels and final underlier levels of the basket underliers that are entirely hypothetical; no one can predict what the basket level will be on any day throughout the life of your notes, and no one can predict what the final basket level will be on the determination date. The basket underliers have been highly volatile in the past — meaning that the levels of the basket underliers have changed considerably in relatively short periods — and their performances cannot be predicted for any future period.

The following examples reflect hypothetical rates of return on the offered notes assuming that they are purchased on the original issue date at the face amount and held to the stated maturity date. If you sell your notes in a secondary market prior to the stated maturity date, your return will depend upon the market value of your notes at the time of sale, which may be affected by a number of factors that are not reflected in the table below such as interest rates, the volatility of the basket underliers and our creditworthiness. The information in the table also reflects the key terms and assumptions in the box below.

| Key Terms and Assumptions | |

| Face amount | $1,000.00 per note |

| Upside participation rate | 200% |

| Cap level | 112.84% of the initial basket level |

| Maximum settlement amount | $1,256.80 per note |

| Initial basket level | 100 |

| A market disruption event does not occur with respect to any basket underlier on the originally scheduled determination date and the originally scheduled determination date is a trading day. | |

| During the term of the notes, no change in or affecting any of the basket underliers or the methods by which any of the basket underlier sponsors calculates the EURO STOXX 50® Index, the TOPIX®, the FTSE® 100 Index, the Swiss Market Index® or the S&P/ASX 200 Index, respectively. | |

| Notes purchased on the original issue date at the face amount and held to the stated maturity date. | |

Moreover, we have not yet set the initial EURO STOXX 50® Index level, the initial TOPIX® level, the initial FTSE® 100 Index level, the initial Swiss Market Index® level or the initial S&P/ASX 200 Index level that will serve as the baselines for determining the basket return and the amount that we will pay on your notes, if any, at maturity. We will not do so until the trade date. The actual initial EURO STOXX 50® Index level, the initial TOPIX® level, the initial FTSE® 100 Index level, the initial Swiss Market Index® level and the initial S&P/ASX 200 Index level may differ substantially from the level of such basket underlier prior to the trade date and may be higher or lower than the closing level of each basket underlier on the trade date.

For these reasons, the actual performance of the basket over the life of your notes, as well as the amount payable at maturity, if any, may bear little relation to the hypothetical examples shown below or to the historical level of each basket underlier shown elsewhere in this pricing supplement. For information about the historical level of each basket underlier during recent periods, see “The Basket and the Basket Underliers — Historical Closing Levels of the Basket Underliers” below. Before investing in the offered notes, you should consult publicly available information to determine the levels of the basket underliers between the date of this pricing supplement and the date of your purchase of the offered notes.

The levels in the left column of the table below represent hypothetical final basket levels and are expressed as percentages of the initial basket level. The amounts in the right column represent the

PS-9

hypothetical cash settlement amounts per $1,000 face amount of notes, based on the corresponding hypothetical final basket level and the assumptions noted above.

|

Hypothetical Final Basket Level (as Percentage of Initial Basket Level) |

Hypothetical Cash Settlement Amount (per $1,000 Face Amount of Notes) | ||

| 200.00% | $1,256.80 | ||

| 175.00% | $1,256.80 | ||

| 150.00% | $1,256.80 | ||

| 125.00% | $1,256.80 | ||

| 120.00% | $1,256.80 | ||

| 112.84% | $1,256.80 | ||

| 110.00% | $1,200.00 | ||

| 105.00% | $1,100.00 | ||

| 103.00% | $1,060.00 | ||

| 100.00% | $1,000.00 | ||

| 95.00% | $950.00 | ||

| 90.00% | $900.00 | ||

| 85.00% | $850.00 | ||

| 75.00% | $750.00 | ||

| 50.00% | $500.00 | ||

| 25.00% | $250.00 | ||

| 0.00% | $0.00 | ||

If, for example, the final basket level were determined to be 25.00% of the initial basket level, the cash settlement amount that we would deliver on your notes at maturity would be $250.00 per $1,000 face amount of your notes, as shown in the table above. As a result, if you purchased your notes on the original issue date at the face amount and held them to the stated maturity date, you would lose 75.00% of your investment (if you purchased your notes at a premium to face amount you would lose a correspondingly higher percentage of your investment). Alternatively, if the final basket level were determined to be 200.00% of the initial basket level, the cash settlement amount that we would deliver on your notes at maturity would be capped at the maximum settlement amount of $1,256.80 per $1,000 face amount of your notes, as shown in the table above. As a result, if you held your notes to the stated maturity date, you would not benefit from any increase in the final basket level over 112.84% of the initial basket level.

The following chart shows a graphical illustration of the hypothetical cash settlement amounts that we would pay on your notes on the stated maturity date, if the final basket level (expressed as a percentage of the initial basket level) were any of the hypothetical levels shown on the horizontal axis. The chart shows that any hypothetical final basket level (expressed as a percentage of the initial basket level) of less than the initial basket level (the section left of the 100.00% marker on the horizontal axis) would result in a hypothetical cash settlement amount of less than $1,000 per $1,000 face amount of your notes (the section below the $1,000 marker on the vertical axis). The chart also shows that any hypothetical final basket level (expressed as a percentage of the initial basket level) of greater than or equal to the cap level (the section right of the cap level marker on the horizontal axis) would result in a capped return on your investment.

PS-10

The following examples illustrate the hypothetical cash settlement amount at maturity, for each $1,000 face amount of notes, based on hypothetical final underlier levels of the basket underliers, calculated based on the key terms and assumptions above. The percentages in Column A represent hypothetical final underlier levels for each basket underlier expressed as percentages of their respective hypothetical initial underlier levels. The amounts in Column B represent the applicable initial weighted value for each basket underlier, and the amounts in Column C represent the products of the percentages in Column A times the corresponding amounts in Column B. The final basket level for each example is shown beneath each example, and will equal the sum of the products shown in Column C. The basket return for each example is shown beneath the final basket level for such example, and will equal the quotient of (i) the final basket level for such example minus the initial basket level divided by (ii) the initial basket level, expressed as a percentage. The values below have been rounded for ease of analysis.

Example 1: The final basket level is greater than the cap level. The cash settlement amount equals the maximum settlement amount.

| Column A | Column B | Column C | ||||

| Basket Underlier |

Hypothetical Final underlier level (as percentage of Initial underlier level) |

Initial Weighted Value |

Column A × Column B | |||

| EURO STOXX 50® Index | 180.00% | 36.00 | 64.80 | |||

| TOPIX® | 180.00% | 29.00 | 52.20 | |||

| FTSE® 100 Index | 180.00% | 16.00 | 28.80 | |||

| Swiss Market Index® | 180.00% | 11.00 | 19.80 | |||

| S&P/ASX 200 Index | 180.00% | 8.00 | 14.40 | |||

| Final Basket Level: | 180.00 | |||||

| Basket Return: | 80.00% | |||||

PS-11

In this example, all of the hypothetical final underlier levels for the basket underliers are greater than the applicable hypothetical initial underlier levels, which results in the hypothetical final basket level being greater than the initial basket level of 100.00. Since the hypothetical final basket level was determined to be 180.00, the hypothetical cash settlement amount that we would deliver on your notes at maturity would be capped at the maximum settlement amount of $1,256.80 for each $1,000 face amount of your notes (i.e. 125.68% of each $1,000 face amount of your notes).

Example 2: The final basket level is greater than the initial basket level but less than the cap level.

| Column A | Column B | Column C | ||||

| Basket Underlier |

Hypothetical Final underlier level (as percentage of Initial underlier level) |

Initial Weighted Value |

Column A × Column B | |||

| EURO STOXX 50® Index | 101.00% | 36.00 | 36.36 | |||

| TOPIX® | I | 102.00% | 29.00 | 29.58 | ||

| FTSE® 100 Index | 103.00% | 16.00 | 16.48 | |||

| Swiss Market Index® | 110.00% | 11.00 | 12.10 | |||

| S&P/ASX 200 Index | 115.00% | 8.00 | 9.20 | |||

| Final Basket Level: | 103.72 | |||||

| Basket Return: | 3.72% | |||||

In this example, all of the hypothetical final underlier levels for the basket underliers are greater than the applicable hypothetical initial underlier levels, which results in the hypothetical final basket level being greater than the initial basket level of 100.00. Since the hypothetical final basket level was determined to be 103.72, the hypothetical cash settlement amount for each $1,000 face amount of your notes will equal:

Cash settlement amount = $1,000 + ($1,000 × 200% × 3.72%) = $1,074.40

Example 3: The final basket level is less than the initial basket level. The cash settlement amount is less than the $1,000 face amount.

| Column A | Column B | Column C | ||||

| Basket Underlier |

Hypothetical Final underlier level (as percentage of Initial underlier level) |

Initial Weighted Value |

Column A × Column B | |||

| EURO STOXX 50® Index | 50.00% | 36.00 | 18.00 | |||

| TOPIX® | 100.00% | 29.00 | 29.00 | |||

| FTSE® 100 Index | 100.00% | 16.00 | 16.00 | |||

| Swiss Market Index® | 135.00% | 11.00 | 14.85 | |||

| S&P/ASX 200 Index | 135.00% | 8.00 | 10.80 | |||

| Final Basket Level: | 88.65 | |||||

| Basket Return: | -11.35% | |||||

In this example, the hypothetical final underlier level of the EURO STOXX 50® Index is less than its hypothetical initial underlier level, while the hypothetical final underlier levels of the TOPIX® and the FTSE® 100 Index are equal to their applicable hypothetical initial underlier levels and the hypothetical final underlier levels of the Swiss Market Index® and the S&P/ASX 200 Index are greater than their applicable initial underlier levels.

Because the basket is unequally weighted, increases in the lower weighted basket underliers will be offset by decreases in the more heavily weighted basket underliers. In this example, the large decline in the EURO STOXX 50® Index results in the hypothetical final basket level being less than the initial basket level of 100.00 even though the TOPIX® and the FTSE® 100 Index remained flat and the Swiss Market Index® and the S&P/ASX 200 Index increased.

PS-12

Since the hypothetical final basket level of 88.65 is less than the initial basket level of 100.00, the hypothetical cash settlement amount for each $1,000 face amount of your notes will equal:

Cash settlement amount = $1,000 + ($1,000 × -11.35%) = $886.50

Example 4: The final basket level is less than the initial basket level. The cash settlement amount is less than the $1,000 face amount.

| Column A | Column B | Column C | ||||

| Basket Underlier |

Hypothetical Final underlier level (as percentage of Initial underlier level) |

Initial Weighted Value |

Column A × Column B | |||

| EURO STOXX 50® Index | 50.00% | 36.00 | 18.00 | |||

| TOPIX® | 60.00% | 29.00 | 17.40 | |||

| FTSE® 100 Index | 60.00% | 16.00 | 9.60 | |||

| Swiss Market Index® | 65.00% | 11.00 | 7.15 | |||

| S&P/ASX 200 Index | 55.00% | 8.00 | 4.40 | |||

| Final Basket Level: | 56.55 | |||||

| Basket Return: | -43.45% | |||||

In this example, the hypothetical final underlier levels for all of the basket underliers are less than the applicable hypothetical initial underlier levels, which results in the hypothetical final basket level being less than the initial basket level of 100.00.

Since the hypothetical final basket level of 56.55 is less than the initial basket level of 100.00, the hypothetical cash settlement amount for each $1,000 face amount of your notes will equal:

Cash settlement amount = $1,000 + ($1,000 × -43.45%) = $565.50

The cash settlement amounts shown above are entirely hypothetical; they are based on hypothetical levels for the basket underliers on the determination date and on assumptions that may prove to be inaccurate. The actual market value of your notes on the stated maturity date or at any other time, including any time you may wish to sell your notes, may bear little relation to the hypothetical cash settlement amounts shown above, and these amounts should not be viewed as an indication of the financial return on an investment in the offered notes. The hypothetical cash settlement amounts on notes held to the stated maturity date in the examples above assume you purchased your notes at their face amount and have not been adjusted to reflect the actual issue price you pay for your notes. The return on your investment (whether positive or negative) in your notes will be affected by the amount you pay for your notes. If you purchase your notes for a price other than the face amount, the return on your investment will differ from, and may be significantly lower than, the hypothetical returns suggested by the above examples. Please read “Risk Factors—Unpredictable economic and market factors may affect the value of the securities prior to maturity” on page PS-8 of the accompanying product supplement.

| We cannot predict the actual final basket level or what the market value of your notes will be on any particular trading day, nor can we predict the relationship between the level of each basket underlier and the market value of your notes at any time prior to the stated maturity date. The actual amount that you will receive, if any, at maturity and the rate of return on the offered notes will depend on the actual initial underlier level of each basket underlier, the cap level and maximum settlement amount, which we will set on the trade date, and the actual basket return determined by the calculation agent as described above. Moreover, the assumptions on which the hypothetical returns are based may turn out to be inaccurate. Consequently, the amount of cash to be paid in respect of your notes, if any, on the stated maturity date may be very different from the information reflected in the table and chart above. |

PS-13

ADDITIONAL RISK FACTORS SPECIFIC TO YOUR NOTES

| An investment in the notes is subject to the risks described below, as well as the risks described under “Risk Factors” in the accompanying product supplement. You should carefully review these risks as well as the terms of the notes described herein and in the accompanying prospectus as supplemented by the accompanying prospectus supplement, the accompanying product supplement, and the accompanying underlying supplement of Credit Suisse. Your notes are a riskier investment than ordinary debt securities. Also, your notes are not equivalent to investing directly in the stocks comprising the basket underliers. You should carefully consider whether the offered notes are suited to your particular circumstances. |

Risks Relating to the Notes Generally

The Stated Maturity Date of the Notes Is a Pricing Term and Will Be Determined by the Issuer on the Trade Date

We will not determine the stated maturity date until the trade date, so you will not know the exact term of, or the determination date for, the notes at the time that you make your investment decision. The term of the notes could be as short as the shorter end of the stated maturity date range described in “Key Terms” herein, and as long as the longer end of the stated maturity date range. You should be willing to hold your notes until the latest possible stated maturity date contemplated by the range. The stated maturity date selected by us could have an impact on the value of the notes. Assuming no changes in other economic terms of the notes, the value of the notes would likely be lower if the term of the notes is at the longer end of the stated maturity date range, rather than the shorter end of the stated maturity date range.

The Amount Payable on Your Notes Is Not Linked to the Level of the Basket Underliers at Any Time Other than the Determination Date

The final basket level will be based on the closing levels of the basket underliers on the determination date (subject to postponement as described elsewhere in the accompanying product supplement). Therefore, if the closing level of one or more of the basket underliers dropped precipitously on the determination date, the cash settlement amount for your notes may be significantly less than it would have been had the cash settlement amount been linked to the closing levels of the basket underliers prior to such drop in the levels of the basket underliers. Although the actual levels of the basket underliers on the stated maturity date or at other times during the life of your notes may be higher than the closing levels of the basket underliers on the determination date, you will not benefit from the closing levels of the basket underliers at any time other than on the determination date.

You May Lose Your Entire Investment in the Notes

You can lose your entire investment in the notes. The cash payment on your notes, if any, on the stated maturity date will be based on the performance of a weighted basket comprised of the EURO STOXX 50® Index, the TOPIX®, the FTSE® 100 Index, the Swiss Market Index® and the S&P/ASX 200 Index as measured from the initial basket level of 100 to the final basket level on the determination date. If the final basket level is less than the initial basket level, you will have a loss, for each $1,000 of the face amount of your notes, equal to the product of (a) $1,000 times (b) the basket return. Thus, you may lose your entire investment in the notes, which would include any premium to face amount you paid when you purchased the notes.

Also, the market price of your notes prior to the stated maturity date may be significantly lower than the purchase price you pay for your notes. Consequently, if you sell your notes before the stated maturity date, you may receive far less than the amount of your investment in the notes.

Furthermore, regardless of the amount of any payment you receive on the notes, you may nevertheless suffer a loss on your investment in the notes in real value terms. This is because inflation may cause the real value of the amount of any payment you receive on the notes to be less at maturity than it is at the time you invest, and because an investment in the notes represents a forgone opportunity to invest in an

PS-14

alternative asset that does generate a positive real return. You should carefully consider whether an investment that may result in a return that is lower than the return on alternative investments is appropriate for you.

Regardless of the Amount of Any Payment You Receive on the Notes, Your Actual Yield May Be Different in Real Value Terms

Inflation may cause the real value of any payment you receive on the notes to be less at maturity than it is at the time you invest. An investment in the notes also represents a forgone opportunity to invest in an alternative asset that generates a higher real return. You should carefully consider whether an investment that may result in a return that is lower than the return on alternative investments is appropriate for you.

Your Notes Will Not Bear Interest

You will not receive any interest payments on your notes. As a result, even if the cash settlement amount payable for your notes on the stated maturity date exceeds the face amount of your notes, the overall return you earn on your notes may be less than you would have earned by investing in a non-indexed debt security of comparable maturity, including our other debt securities, that bears interest at a prevailing market rate.

The Probability that the Final Basket Level Will Be Less Than the Initial Basket Level Will Depend on the Volatility of the Basket Underliers

“Volatility” refers to the frequency and magnitude of changes in the levels of the basket underliers. The greater the expected volatility with respect to the basket underliers on the trade date, the higher the expectation as of the trade date that the final basket level could be less than the initial basket level, indicating a higher expected risk of loss on the notes. The terms of the notes are set, in part, based on expectations about the volatility of the underlier as of the trade date. The volatility of the basket can change significantly over the term of the notes. The levels of the basket underliers could fall sharply, which could result in a significant loss of principal. You should be willing to accept the downside market risk of the basket underliers and the potential to lose a significant amount of your principal at maturity.

Your Maximum Gain on the Notes Is Limited to the Maximum Settlement Amount

If the final basket level is greater than the initial basket level, for each $1,000 face amount of the notes, you will receive at maturity a payment that will not exceed the maximum settlement amount, regardless of the appreciation in the basket underliers, which may be significant. Accordingly, the amount payable on your notes may be significantly less than it would have been had you invested directly in each basket underlier.

We May Sell Additional Notes at a Different Issue Price

At our sole option, we may decide to sell an additional aggregate face amount of the notes subsequent to the date of this pricing supplement at issue prices and with underwriting discounts and net proceeds that differ from the amounts set forth on the cover page. The issue price of the notes in the subsequent sale may differ substantially (higher or lower) from the original issue price you paid as provided on the cover of this pricing supplement.

If You Purchase Your Notes at a Premium to Face Amount, the Return on Your Investment Will Be Lower Than the Return on Notes Purchased at Face Amount and the Impact of Certain Key Terms of the Notes Will be Negatively Affected

The cash settlement amount will not be adjusted based on the issue price you pay for the notes. If you purchase the notes at a price that differs from the face amount of the notes, then the return on your investment in such notes held to the stated maturity date will differ from, and may be substantially less than, the return on the notes purchased at face amount. If you purchase your notes at a premium to face

PS-15

amount and hold them to the stated maturity date the return on your investment in the notes will be lower than it would have been had you purchased the notes at face amount or a discount to face amount. In addition, the impact of the cap level on the return on your investment will depend upon the price you pay for your notes relative to face amount. For example, if you purchase your notes at a premium to face amount, the cap level will permit a lower percentage increase in your investment in the notes than would have been the case for notes purchased at face amount or a discount to face amount.

The U.S. Federal Tax Consequences of an Investment in the Notes Are Unclear

There is no direct legal authority regarding the proper U.S. federal tax treatment of the notes, and we do not plan to request a ruling from the Internal Revenue Service (the “IRS”). Consequently, significant aspects of the tax treatment of the notes are uncertain, and the IRS or a court might not agree with the treatment of the notes as prepaid financial contracts that are treated as “open transactions.” If the IRS were successful in asserting an alternative treatment of the notes, the tax consequences of the ownership and disposition of the notes, including the timing and character of income recognized by U.S. investors and the withholding tax consequences to non-U.S. investors, might be materially and adversely affected. Moreover, future legislation, Treasury regulations or IRS guidance could adversely affect the U.S. federal tax treatment of the notes, possibly retroactively.

Risks Relating to the Basket Underliers

The Initial Underlier Level of Each Basket Underlier Will Be Determined at the Discretion of the Calculation Agent

The initial underlier level of each basket underlier will be the closing level or an intraday level of such basket underlier on the trade date, as determined by the calculation agent in its sole discretion. As such, the initial underlier level of each basket underlier may not be based on the closing level of such basket underlier on the trade date. The initial underlier level of each basket underlier may be higher or lower than the actual closing level of such basket underlier on the trade date.

You Have No Shareholder Rights or Rights to Receive Any of the Equity Securities Comprising the Basket Underliers

Investing in the notes will not make you a holder of any of the equity securities comprising the basket underliers. Neither you nor any other holder or owner of the notes will have any voting rights, any right to receive dividends or other distributions, any rights to make a claim against the issuers of, or any other rights with respect to, the equity securities comprising the basket underliers. The cash settlement amount will be paid in cash and you will have no right to receive delivery of any equity securities comprising the basket underliers.

The Lower Performance of One Basket Underlier May Offset an Increase in the Other Basket Underliers

Declines in the level of one basket underlier may offset increases in the level of the other basket underliers. As a result, any return on the basket — and thus on your notes — may be reduced or eliminated, which will have the effect of reducing the amount payable in respect of your notes at maturity. Because the amount payable on the notes, if any, depends on the performance of the basket underliers, you will bear the risk that any of the basket underliers will perform poorly. In addition, because the basket underliers are not equally weighted, increases in the lower weighted basket underliers may be offset by even small decreases in the more heavily weighted basket underliers.

Except to the Extent that Credit Suisse is Included in the Swiss Market Index®, We Do Not Control Any Companies Included in Any Basket Underlier

While we or our affiliates may from time to time own securities of companies included in the basket, we and our affiliates do not control any company included in any basket underlier. Except to the extent that

PS-16

Credit Suisse is included in the Swiss Market Index®, we are not responsible for any disclosure made by any other company.

The SMI is Concentrated in a Small Number of Constituents

The SMI consists of 20 issuer constituents included in the Swiss Performance Index (“SPI”), which generally tracks all Swiss exchange traded equity securities. Depending on the weightings of each SMI constituent at the time, the level of the SMI may be heavily dependent on just few constituents at any given time, which means that those constituents will disproportionately and significantly affect the performance of the SMI. As of December 29, 2017, the weighting of the single top constituent of the SMI composed over 18% of the SMI, and the weightings of the top three constituents combined composed over 53% of the SMI. As a result, you may be exposed to concentration risk in a small number of SPI issuers.

The Closing Levels of the Basket Underliers Will Not Be Adjusted For Changes in Exchange Rates Relative to the U.S. Dollar Even Though the Equity Securities Included in the Basket Underliers Are Traded in Foreign Currencies and the Notes Are Denominated in U.S. Dollars

The value of your notes will not be adjusted for exchange rate fluctuations between the U.S. dollar and the currencies in which the equity securities included in each of the basket underliers are based. Therefore, if the applicable currencies appreciate or depreciate relative to the U.S. dollar over the term of the notes, you will not receive any additional payment or incur any reduction in your return, if any, at maturity.

Foreign Securities Markets Risk

Some or all of the assets included in the basket underliers are issued by foreign companies and trade in foreign securities markets. Investments in the notes therefore involve risks associated with the securities markets in those countries, including risks of volatility in those markets, government intervention in those markets and cross shareholdings in companies in certain countries. Also, foreign companies are generally subject to accounting, auditing and financial reporting standards and requirements and securities trading rules different from those applicable to U.S. reporting companies. The equity securities included in the basket underliers may be more volatile than domestic equity securities and may be subject to different political, market, economic, exchange rate, regulatory and other risks, including changes in foreign governments, economic and fiscal policies, currency exchange laws or other laws or restrictions. Moreover, the economies of foreign countries may differ favorably or unfavorably from the economy of the United States in such respects as growth of gross national product, rate of inflation, capital reinvestment, resources and self-sufficiency. These factors may adversely affect the values of the equity securities included in the basket underliers, and therefore the performance of the basket and the value of the notes.

Government Regulatory Action, Including Legislative Acts and Executive Orders, Could Result in Material Changes to the Basket Underliers and Could Negatively Affect Your Return on the Notes

Government regulatory action, including legislative acts and executive orders, could materially affect the basket underliers. For example, in response to recent executive orders, stocks of companies that are determined to be linked to the People's Republic of China military, intelligence and security apparatus may be delisted from a U.S. exchange, removed as a component in indices or exchange traded funds, or transactions in, or holdings of, securities with exposure to such stocks may otherwise become prohibited under U.S. law. If government regulatory action results in such consequences, there may be a material and negative effect on the notes.

Risks Relating to the Issuer

The Notes Are Subject to the Credit Risk of Credit Suisse

PS-17

Investors are dependent on our ability to pay all amounts due on the notes and, therefore, if we were to default on our obligations, you may not receive any amounts owed to you under the notes. In addition, any decline in our credit ratings, any adverse changes in the market’s view of our creditworthiness or any increase in our credit spreads is likely to adversely affect the value of your notes prior to maturity.

Credit Suisse Is Subject to Swiss Regulation

As a Swiss bank, Credit Suisse is subject to regulation by governmental agencies, supervisory authorities and self-regulatory organizations in Switzerland. Such regulation is increasingly more extensive and complex and subjects Credit Suisse to risks. For example, pursuant to Swiss banking laws, the Swiss Financial Market Supervisory Authority (FINMA) may open resolution proceedings if there are justified concerns that Credit Suisse is over-indebted, has serious liquidity problems or no longer fulfills capital adequacy requirements. FINMA has broad powers and discretion in the case of resolution proceedings, which include the power to convert debt instruments and other liabilities of Credit Suisse into equity and/or cancel such liabilities in whole or in part. If one or more of these measures were imposed, such measures may adversely affect the terms and market value of the notes and/or the ability of Credit Suisse to make payments thereunder and you may not receive any amounts owed to you under the notes.

Risks Relating to Conflicts of Interest

Hedging and Trading Activity

We, any dealer or any of our or their respective affiliates may carry out hedging activities related to the notes, including in instruments related to the basket underliers. We, any dealer or any of our or their respective affiliates may also trade in instruments related to the basket underliers from time to time. Any of these hedging or trading activities on or prior to the Trade Date and during the term of the notes could adversely affect our payment to you at maturity.

Potential Conflicts

We and our affiliates play a variety of roles in connection with the issuance of the notes, including acting as calculation agent and as an agent of the offering of the notes, hedging our obligations under the notes and determining their estimated value. In addition, the distributor from which you purchase the notes may conduct hedging activities in connection with the notes. In performing these duties, the economic interests of us, our affiliates and the distributor are potentially adverse to your interests as an investor in the notes. Further, hedging activities may adversely affect any payment on or the value of your notes. Any profit in connection with such hedging activities will be in addition to any other compensation that we and our affiliates or the distributor receives for the sale of the notes, which creates an additional incentive to sell the notes to you.

Risks Relating to the Estimated Value and Secondary Market Prices of the Notes

Unpredictable Economic and Market Factors Will Affect the Value of the Notes

The payout on the notes can be replicated using a combination of the components described in “The estimated value of the notes on the trade date may be less than the price to public.” Therefore, in addition to the level of the basket, the terms of the notes at issuance and the value of the notes prior to maturity may be influenced by factors that impact the value of fixed income securities and options in general such as:

| · | the expected and actual volatility of the basket underliers; |

| · | the expected and actual correlation, if any, between the basket underliers; |

| · | the time to maturity of the notes; |

| · | the dividend rate on the equity securities included in the basket underliers; |

PS-18

| · | interest and yield rates in the markets generally; |

| · | investors’ expectations with respect to the rate of inflation; |

| · | geopolitical conditions and economic, financial, political, regulatory, judicial or other events that affect the equity securities included in the basket underliers or markets generally and which may affect the level of the basket underliers; and |

| · | our creditworthiness, including actual or anticipated downgrades in our credit ratings. |

Some or all of these factors may influence the price that you will receive if you choose to sell your notes prior to maturity. The impact of any of the factors set forth above may enhance or offset some or all of any change resulting from another factor or factors.

The Estimated Value of the Notes on the Trade Date May Be Less Than the Price to Public

The initial estimated value of your notes on the trade date (as determined by reference to our pricing models and our internal funding rate) may be significantly less than the original issue price. The original issue price of the notes includes any discounts or commissions as well as transaction costs such as expenses incurred to create, document and market the notes and the cost of hedging our risks as issuer of the notes through one or more of our affiliates (which includes a projected profit). These costs will be effectively borne by you as an investor in the notes. These amounts will be retained by Credit Suisse or our affiliates in connection with our structuring and offering of the notes (except to the extent discounts or commissions are reallowed to other broker-dealers or any costs are paid to third parties).

On the trade date, we value the components of the notes in accordance with our pricing models. These include a fixed income component valued using our internal funding rate, and individual option components valued using proprietary pricing models dependent on inputs such as volatility, correlation, dividend rates, interest rates and other factors, including assumptions about future market events and/or environments. These inputs may be market-observable or may be based on assumptions made by us in our discretionary judgment. As such, the payout on the notes can be replicated using a combination of these components, and the value of these components, as determined by us using our pricing models, will impact the terms of the notes at issuance. Our option valuation models are proprietary. Our pricing models take into account factors such as interest rates, volatility and time to maturity of the notes, and they rely in part on certain assumptions about future events, which may prove to be incorrect.

Because Credit Suisse’s pricing models may differ from other issuers’ valuation models, and because funding rates taken into account by other issuers may vary materially from the rates used by Credit Suisse (even among issuers with similar creditworthiness), our estimated value at any time may not be comparable to estimated values of similar notes of other issuers. A fee will also be paid to SIMON Markets LLC, an electronic platform affiliated with Goldman Sachs & Co. LLC. Goldman Sachs & Co. LLC is acting as a dealer in connection with the distribution of the notes.

Effect of Interest Rate Used in Estimating Value

The internal funding rate we use in structuring notes such as these notes is typically lower than the interest rate that is reflected in the yield on our conventional debt securities of similar maturity in the secondary market (our “secondary market credit spreads”). If on the trade date our internal funding rate is lower than our secondary market credit spreads, we expect that the economic terms of the notes will generally be less favorable to you than they would have been if our secondary market credit spread had been used in structuring the notes. We will also use our internal funding rate to determine the price of the notes if we post a bid to repurchase your notes in secondary market transactions. See “—Secondary Market Prices” below.

PS-19

Secondary Market Prices

If Credit Suisse (or an affiliate) bids for your notes in secondary market transactions, which we are not obligated to do, the secondary market price (and the value used for account statements or otherwise) may be higher or lower than the original issue price and the estimated value of the notes on the trade date. The estimated value of the notes on the cover of this pricing supplement does not represent a minimum price at which we would be willing to buy the notes in the secondary market (if any exists) at any time. The secondary market price of your notes at any time cannot be predicted and will reflect the then-current estimated value determined by reference to our pricing models, the related inputs and other factors, including our internal funding rate, customary bid and ask spreads and other transaction costs, changes in market conditions and deterioration or improvement in our creditworthiness. In circumstances where our internal funding rate is higher than our secondary market credit spreads, our secondary market bid for your notes could be less favorable than what other dealers might bid because, assuming all else equal, we use the higher internal funding rate to price the notes and other dealers might use the lower secondary market credit spread to price them. Furthermore, assuming no change in market conditions from the trade date, the secondary market price of your notes will be lower than the original issue price because it will not include any discounts or commissions and hedging and other transaction costs. If you sell your notes to a dealer in a secondary market transaction, the dealer may impose an additional discount or commission, and as a result the price you receive on your notes may be lower than the price at which we may repurchase the notes from such dealer.

We (or an affiliate) may initially post a bid to repurchase the notes from you at a price that will exceed the then-current estimated value of the notes. That higher price reflects our projected profit and costs, which may include discounts and commissions that were included in the original issue price, and that higher price may also be initially used for account statements or otherwise. We (or our affiliate) may offer to pay this higher price, for your benefit, but the amount of any excess over the then-current estimated value will be temporary and is expected to decline over a period of approximately three months.

The notes are not designed to be short-term trading instruments and any sale prior to maturity could result in a substantial loss to you. You should be willing and able to hold your notes to maturity.

Lack of Liquidity

The notes will not be listed on any securities exchange. Credit Suisse (or its affiliates) intends to offer to purchase the notes in the secondary market but is not required to do so. Even if there is a secondary market, it may not provide enough liquidity to allow you to trade or sell the notes when you wish to do so. Because other dealers are not likely to make a secondary market for the notes, the price at which you may be able to trade your notes is likely to depend on the price, if any, at which Credit Suisse (or its affiliates) is willing to buy the notes. If you have to sell your notes prior to maturity, you may not be able to do so or you may have to sell them at a substantial loss.

PS-20

THE BASKET UNDERLIERS

The historical levels of the basket or the basket underliers should not be taken as an indication of future performance, and no assurance can be given as to the closing level of the basket underliers on any trading day during the term of the notes, including on the determination date. We cannot give you assurance that the future performance of the basket underliers will result in any return of your investment. Any payment on the notes is subject to our ability to pay our obligations as they become due.

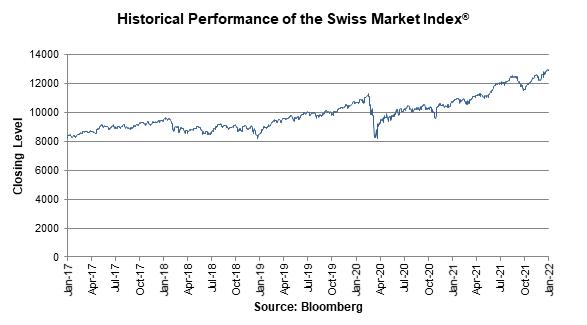

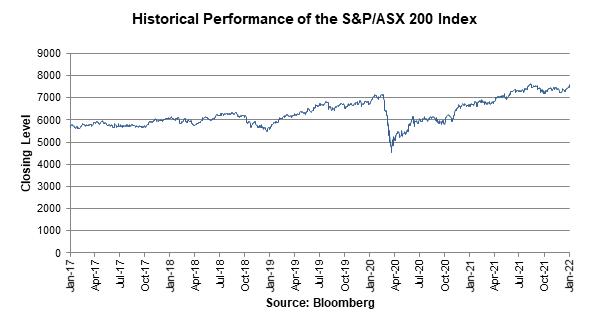

The graphs below show the daily historical closing levels, for each Basket Component from January 3, 2017 through January 4, 2022. The graphs are for illustrative purposes only. We obtained the closing levels in the graphs below from Bloomberg Financial Services, without independent verification.

The closing level of the EURO STOXX 50® Index on January 4, 2022 was 4367.62.

The closing level of the TOPIX® on January 4, 2022 was 2030.22.

PS-21

The closing level of the FTSE® 100 Index on January 4, 2022 was 7505.15.

The closing level of the Swiss Market Index® on January 4, 2022 was 12900.97.

PS-22

The closing level of the S&P/ASX 200 Index on January 4, 2022 was 7589.757.

EURO STOXX 50® Index

For additional information on the EURO STOXX 50® Index, see “The Reference Indices—The STOXX Indices—The EURO STOXX 50® Index” in the accompanying underlying supplement.

In addition, information about the EURO STOXX 50® Index may be obtained from other sources including, but not limited to, the basket underlier sponsor’s website (including information regarding the EURO STOXX 50® Index’s (i) top ten constituents and weightings, (ii) sector weightings and (iii) country weightings). We are not incorporating by reference into this pricing supplement the website or any material it includes. Neither we nor any agent or dealer for this offering makes any representation that this publicly available information regarding the basket underliers is accurate or complete.

TOPIX®

For additional information on the Tokyo Stock Price Index, see “The Reference Indices —The Tokyo Stock Price Index” in the accompanying underlying supplement.

In addition, information about the TOPIX® Index may be obtained from other sources including, but not limited to the basket underlier sponsor’s website (including information regarding the TOPIX® Index’s sector weightings). We are not incorporating by reference into this pricing supplement the website or any material it includes. Neither we nor any agent or dealer for this offering makes any representation that this publicly available information regarding the basket underliers is accurate or complete.

FTSE® 100 Index

For additional information on the FTSE® 100 Index, see “The Reference Indices —The FTSE Russell Indices—The FTSE 100 Index” in the accompanying underlying supplement.

In addition, information about the FTSE® 100 Index may be obtained from other sources including, but not limited to, the basket underlier sponsor’s website (including information regarding the FTSE® 100 Index’s (i) top five constituents and weightings and (ii) sector weightings). We are not incorporating by reference into this pricing supplement the website or any material it includes. Neither we nor any agent or dealer for this offering makes any representation that this publicly available information regarding the basket underliers is accurate or complete.

PS-23

Swiss Market Index® (SMI)

For additional information on the Swiss Market Index, see “The Reference Indices — The Swiss Market Index” in the accompanying underlying supplement.

In addition, information about the Swiss Market Index may be obtained from other sources including, but not limited to, the basket underlier sponsor’s website (including information regarding the Swiss Market Index’s (i) constituents and weightings and (ii) sector weightings). We are not incorporating by reference into this pricing supplement the website or any material it includes. Neither we nor any agent or dealer for this offering makes any representation that this publicly available information regarding the basket underliers is accurate or complete.

S&P/ASX 200 Index

For additional information on the S&P/ASX 200 Index, see “The Reference Indices — The S&P Dow Jones Indices – The S&P/ASX Index” in the accompanying underlying supplement.

In addition, information about the S&P/ASX 200 Index may be obtained from other sources including, but not limited to, the basket underlier sponsor’s website (including information regarding the S&P/ASX 200 Index’s (i) top ten constituents, (ii) sector weightings and (iii) country weightings). We are not incorporating by reference into this pricing supplement the website or any material it includes. Neither we nor any agent or dealer for this offering makes any representation that this publicly available information regarding the basket underliers is accurate or complete.

For more information on the EURO STOXX 50® Index, the Tokyo Stock Price Index, the FTSE® 100 Index, the Swiss Market Index® and the S&P/ASX 200 Index, see “The Reference Indices—The STOXX Indices—The EURO STOXX 50® Index,” “The Reference Indices—The Tokyo Stock Price Index,” “The Reference Indices—The FTSE Russell Indices—The FTSE® 100 Index,” “The Reference Indices—The Swiss Market Index®” and “The Reference Indices—The S&P Dow Jones Indices—The S&P/ASX 200 Index” in the accompanying underlying supplement.

HISTORICAL BASKET LEVELS

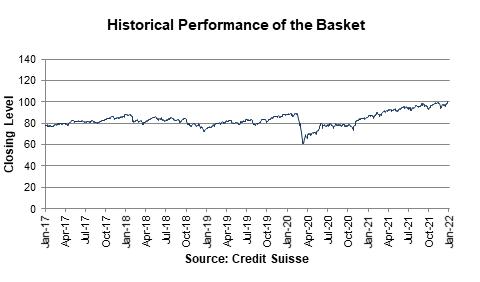

The following graph is based on the basket closing level for the period from January 3, 2017 through January 4, 2022 assuming that the basket closing level was 100 on January 4, 2022. We derived the basket closing levels based on the method to calculate the basket closing level as described in this pricing supplement and on actual closing levels of the relevant basket underliers on the relevant date. The basket closing level has been normalized such that its hypothetical level on January 4, 2022 was 100. As noted in this Pricing Supplement, the initial basket level will be set at 100 on the trade date. The basket closing level can increase or decrease due to changes in the levels of the basket underliers.

PS-24

UNITED STATES FEDERAL TAX CONSIDERATIONS

This discussion supplements and, to the extent inconsistent therewith, supersedes the discussion in the accompanying product supplement under “United States Federal Tax Considerations.”

There are no statutory, judicial or administrative authorities that address the U.S. federal income tax treatment of the notes or instruments that are similar to the notes. In the opinion of our counsel, Davis Polk & Wardwell LLP, a note should be treated as a prepaid financial contract that is an “open transaction” for U.S. federal income tax purposes. However, there is uncertainty regarding this treatment. Moreover, our counsel’s opinion is based on market conditions as of the date of this preliminary pricing supplement and is subject to confirmation on the trade date.

Assuming this treatment of the notes is respected and subject to the discussion in “United States Federal Tax Considerations” in the accompanying product supplement, the following U.S. federal income tax consequences should result:

| · | You should not recognize taxable income over the term of the notes prior to maturity, other than pursuant to a sale or other disposition. |

| · | Upon a sale or other disposition (including retirement) of a note, you should recognize capital gain or loss equal to the difference between the amount realized and your tax basis in the note. Such gain or loss should be long-term capital gain or loss if you held the note for more than one year. |

We do not plan to request a ruling from the IRS regarding the treatment of the notes, and the IRS or a court might not agree with the treatment described herein. In particular, the IRS could treat the notes as contingent payment debt instruments, in which case the tax consequences of ownership and disposition of the notes, including the timing and character of income recognized, could be materially and adversely affected. Moreover, the U.S. Treasury Department and the IRS have requested comments on various issues regarding the U.S. federal income tax treatment of “prepaid forward contracts” and similar financial instruments and have indicated that such transactions may be the subject of future regulations or other guidance. In addition, members of Congress have proposed legislative changes to the tax treatment of derivative contracts. Any legislation, Treasury regulations or other guidance promulgated after consideration of these issues could materially and adversely affect the tax consequences of an investment in the notes, possibly with retroactive effect. You should consult your tax advisor regarding possible alternative tax treatments of the notes and potential changes in applicable law.

Non-U.S. Holders. Subject to the discussions in the next paragraph and in “United States Federal Tax Considerations—Tax Consequences to Non-U.S. Holders” and “United States Federal Tax Considerations—FATCA” in the accompanying product supplement, if you are a Non-U.S. Holder (as defined in the accompanying product supplement) of the notes, you generally should not be subject to U.S. federal withholding or income tax in respect of any amount paid to you with respect to the notes, provided that (i) income in respect of the notes is not effectively connected with your conduct of a trade or business in the United States, and (ii) you comply with the applicable certification requirements.