|

Pricing Supplement No. ELN-23 Prospectus Supplement dated June 30, 2017 and |

Filed Pursuant to Rule 424(b)(2) Registration Statement No. 333-218604-02 May 20, 2020 |

Financial Products

|

$72,000,000 Equity-Linked Notes due May 28, 2027 Linked to the Performance of the Common Stock of McDonald’s Corporation |

| • | The securities do not provide for the regular payment of interest. |

| • | If the product of the Final Level and the Conversion Ratio is greater than $1,000, at maturity you will receive, for each $1,000 principal amount of securities, a cash payment equal to the Final Level multiplied by the Conversion Ratio. However, if the product of the Final Level and the Conversion Ratio is equal to or less than $1,000, you will receive, for each $1,000 principal amount of securities, a cash payment equal to $1,000. |

| • | The Conversion Ratio reflects the Premium of 27.50% over the Initial Level by which the level of the Underlying must rise before you begin to participate in any appreciation of the Underlying. For more information, see “Risk Factors—The securities will pay less than the full appreciation of the Underlying, if any” herein. |

| • | Senior unsecured obligations of Credit Suisse maturing May 28, 2027. Any payment on the securities is subject to our ability to meet our obligations as they become due. |

| • | Minimum purchase of $1,000. Minimum denominations of $1,000 and integral multiples in excess thereof. |

| • | The offering price for the securities was determined on May 20, 2020 (the “Trade Date”) and the securities are expected to settle on May 28, 2020 (the “Settlement Date”). Delivery of the securities in book-entry form only will be made through The Depository Trust Company. |

| • | The securities will not be listed on any exchange. |

Investing in the securities involves a number of risks. See “Selected Risk Considerations” beginning on page 7 of this pricing supplement and “Risk Factors” beginning on page PS-3 of the accompanying product supplement.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of the securities or passed upon the accuracy or the adequacy of this pricing supplement or the accompanying product supplement, the prospectus supplement and the prospectus. Any representation to the contrary is a criminal offense.

| Price to Public | Underwriting Discounts and Commissions(1) | Proceeds to Issuer | |

| Per security | $1,000 | $0 | $1,000 |

| Total | $72,000,000 | $0 | $72,000,000 |

(1) For more detailed information, please see “Supplemental Plan of Distribution (Conflicts of Interest)” in this pricing supplement.

The agent for this offering, Credit Suisse Securities (USA) LLC (“CSSU”), is our affiliate. For more information, see “Supplemental Plan of Distribution (Conflicts of Interest)” in this pricing supplement.

Credit Suisse currently estimates the value of each $1,000 principal amount of the securities on the Trade Date is $965 (as determined by reference to our pricing models and the rate we are currently paying to borrow funds through issuance of the securities (our “internal funding rate”)). See “Selected Risk Considerations” in this pricing supplement.

The securities are not deposit liabilities and are not insured or guaranteed by the Federal Deposit Insurance Corporation or any other governmental agency of the United States, Switzerland or any other jurisdiction.

Credit Suisse

May 20, 2020

Key Terms

| Issuer: | Credit Suisse AG (“Credit Suisse”), acting through its Nassau branch |

| Reference Share Issuer: | The issuer of the Underlying. |

| Underlying: | The securities are linked to the performance of the common stock of McDonald’s Corporation. The ticker symbol is MCD UN <Equity>. For additional information on the Underlying, see “The Underlying” herein. |

| Reference Value: | The product of the Final Level multiplied by the Conversion Ratio. |

| Conversion Ratio: | 4.26803, which is a number equal to $1,000 / [(1 + Premium) × Initial Level], rounded to 5 decimal places. |

| Premium: | 27.50% |

| Redemption Amount: | At maturity, for each $1,000 principal amount of securities, the Redemption Amount will be: |

|

if the Reference Value is greater than $1,000, the Reference Value.

The return on the securities will increase by less than 1% for every 1% increase in the level of the Underlying beyond the Premium.

| |

| if the Reference Value is equal to or less than $1,000, $1,000. | |

| Any payment on the securities is subject to our ability to meet our obligations as they become due. | |

| Adjustments: |

The share adjustment factor will be adjusted to reflect any Ordinary Cash Dividend (as defined below) on the Underlying that is different (higher or lower) than the Base Dividend or if no Ordinary Cash Dividend is declared for a quarter, as set forth below.

An “Ordinary Cash Dividend Adjustment Event” will occur if (i) an ex-dividend date for the Underlying occurs in respect of an Ordinary Cash Dividend that is different (higher or lower) than the Base Dividend or (ii) other than in connection with a Payment Period Adjustment, the Reference Share Issuer declares that it will pay no Ordinary Cash Dividend (or the calculation agent determines that no Ordinary Cash Dividend will be paid) in respect of any quarter.

If an Ordinary Cash Dividend Adjustment Event occurs, the share adjustment factor will be adjusted on the ex-dividend date for such Ordinary Cash Dividend or the date that the calculation agent determines based on the last expected ex-dividend date reported by Bloomberg would have been the ex-dividend date for the Ordinary Cash Dividend but for the non-payment of such Ordinary Cash Dividend in such quarter, as applicable.

The new share adjustment factor will equal the product of (i) the prior share adjustment factor and (ii) a fraction, the numerator of which will be the current market price of the Underlying minus the Base Dividend, and the denominator of which will be the current market price of the Underlying minus the amount of the Ordinary Cash Dividend per share, which, in the case no Ordinary Cash Dividend is paid in such quarter, will be deemed to be zero.

If the Reference Share Issuer effects a change in the periodicity of its Ordinary Cash Dividend payments (e.g., from quarterly payments to semi-annual payments) (a “Payment Period Adjustment”), then the calculation agent will make corresponding adjustments to the Base Dividend and references in this pricing supplement to a quarter or a quarterly dividend shall be deemed to refer instead to such other period or periodic dividend, as appropriate.

A dividend or other distribution consisting exclusively of cash to all, or substantially all, holders of the Underlying (the “Relevant Dividend”) will be deemed to be an “Ordinary Cash Dividend” if the calculation agent determines that the Relevant Dividend is declared and paid within the normal |

1

|

dividend policy or is materially similar to the historical dividend, or that the Reference Share Issuer announces will be an ordinary dividend. For the avoidance of doubt, the Relevant Dividend may be all or only a portion of any cash dividend or other cash distribution and Relevant Dividends may occur contemporaneously on any given date.

In the event that a dividend or other distribution is declared on any class of the Reference Share Issuer’s capital stock (or on the capital stock of any surviving entity or subsequent surviving entity of the Reference Share Issuer (a “reference issuer survivor”)) payable in shares of the Underlying (or the common stock of any reference issuer survivor) then, once the Underlying is trading ex-dividend, the share adjustment factor will be adjusted to equal the product of (i) the prior share adjustment factor and (ii) a fraction, the numerator of which will be the number of shares of the Underlying (or the common stock of any reference issuer survivor) outstanding on the trading day immediately preceding the ex-dividend date plus the number of shares constituting such distribution, and the denominator of which shall be the number of shares of the Underlying (or dividend or common stock of any reference issuer survivor) outstanding on the trading day immediately preceding the ex-dividend date.

A dividend or other distribution, other than an Ordinary Cash Dividend, consisting exclusively of cash to all or substantially all holders of the Underlying will be deemed to be an extraordinary cash dividend. If an extraordinary cash dividend occurs, the share adjustment factor will be adjusted so that the new share adjustment factor equals the product of (i) the prior share adjustment factor and (ii) a fraction, the numerator of which will be the closing price of the Underlying on the trading day immediately preceding the ex-dividend date and the denominator of which will be the closing price of the Underlying on the trading day immediately preceding the ex-dividend date minus the extraordinary cash dividend.

There are other adjustment provisions you should carefully review described in the relevant product supplement under “Description of the Securities—Adjustments.” For the avoidance of doubt, the provisions set forth above shall supersede the provisions set forth in “Description of the Securities—Adjustments—For equity securities of a reference share issuer” in the relevant product supplement, as applicable. | |

| Base Dividend: | $1.25 per calendar quarter, subject to adjustment by the calculation agent when appropriate to reflect adjustments to the Share Adjustment Factor. For example, if the Underlying is subject to a 1-for-2 reverse stock split, then the calculation agent will double the Base Dividend, and if the Underlying is subject to a 2-for-1 stock split then the calculation agent will reduce the Base Dividend by half. |

| Initial Level: | $183.765 |

| Final Level: | The closing level of the Underlying on the Valuation Date. |

| Events of Default and Acceleration: | In case an event of default (as described in the accompanying prospectus) with respect to any issuance of securities shall have occurred and be continuing, the amount declared due and payable upon any acceleration of the securities will be determined by the calculation agent and will equal, for each security, the amount to be received on the Maturity Date, calculated as though the date of acceleration were the Valuation Date. For the avoidance of doubt, these provisions shall supersede the provisions set forth in “Description of the Securities—Events of default and acceleration” in any accompanying product supplement. |

| Valuation Date: | May 25, 2027, subject to postponement as set forth in any accompanying product supplement under “Description of the Securities—Postponement of calculation dates.” |

| Maturity Date: | May 28, 2027, subject to postponement as set forth in any accompanying product supplement under “Description of the Securities—Postponement of calculation dates.” If the Maturity Date is not a business day, the Redemption Amount will be payable on the first following business day, unless that business day falls in the next calendar month, in which case payment will be made on the first preceding business day. |

2

| CUSIP/ISIN: | 22552W4L6/US22552W4L67 |

3

Additional Terms Specific to the Securities

You should read this pricing supplement together with the product supplement dated June 30, 2017, the prospectus supplement dated June 30, 2017 and the prospectus dated June 30, 2017, relating to our Medium-Term Notes of which these securities are a part. You may access these documents on the SEC website at www.sec.gov as follows (or if such address has changed, by reviewing our filings for the relevant date on the SEC website):

| • | Product Supplement No. I–G dated October 4, 2017: |

https://www.sec.gov/Archives/edgar/data/1053092/000095010317009709/dp81337_424b2-psg.htm

| • | Prospectus Supplement and Prospectus dated June 30, 2017: |

http://www.sec.gov/Archives/edgar/data/1053092/000104746917004364/a2232566z424b2.htm

In the event the terms of the securities described in this pricing supplement differ from, or are inconsistent with, the terms described in any product supplement, the prospectus supplement or prospectus, the terms described in this pricing supplement will control.

Our Central Index Key, or CIK, on the SEC website is 1053092. As used in this pricing supplement, “we,” “us,” or “our” refers to Credit Suisse.

This pricing supplement, together with the documents listed above, contains the terms of the securities and supersedes all other prior or contemporaneous oral statements as well as any other written materials including preliminary or indicative pricing terms, fact sheets, correspondence, trade ideas, structures for implementation, sample structures, brochures or other educational materials of ours. We may, without the consent of the registered holder of the securities and the owner of any beneficial interest in the securities, amend the securities to conform to its terms as set forth in this pricing supplement and the documents listed above, and the trustee is authorized to enter into any such amendment without any such consent. You should carefully consider, among other things, the matters set forth in “Selected Risk Considerations” in this pricing supplement and “Risk Factors” in any accompanying product supplement, “Foreign Currency Risks” in the accompanying prospectus, and any risk factors we describe in the combined Annual Report on Form 20-F of Credit Suisse Group AG and us incorporated by reference therein, and any additional risk factors we describe in future filings we make with the SEC under the Securities Exchange Act of 1934, as amended, as the securities involve risks not associated with conventional debt securities. You should consult your investment, legal, tax, accounting and other advisors before deciding to invest in the securities.

Prohibition of Sales to EEA Retail Investors

The securities may not be offered, sold or otherwise made available to any retail investor in the European Economic Area. For the purposes of this provision:

(a) the expression “retail investor” means a person who is one (or more) of the following:

(i) a retail client as defined in point (11) of Article 4(1) of Directive 2014/65/EU (as amended, “MiFID II”); or

(ii) a customer within the meaning of Directive 2002/92/EC, where that customer would not qualify as a professional client as defined in point (10) of Article 4(1) of MiFID II; or

(iii) not a qualified investor as defined in Directive 2003/71/EC; and

(b) the expression “offer” includes the communication in any form and by any means of sufficient information on the terms of the offer and the securities offered so as to enable an investor to decide to purchase or subscribe the securities.

4

Hypothetical Redemption Amounts

The table and examples below illustrate, for a $1,000 investment in the securities, hypothetical Redemption Amounts payable at maturity for a hypothetical range of performance of the Underlying. The table and examples below assume (i) a hypothetical Initial Level of $183.765, (ii) a Premium of 27.50%, (iii) a Conversion Ratio of 4.26803 per $1,000 principal amount of securities (derived from the hypothetical Initial Level and Premium set forth in (i) and (ii) in this paragraph) and (iv) a share adjustment factor of 1.0. The actual Initial Level, Premium and Conversion Ratio are set forth in “Key Terms” herein. Under these assumptions, you will not be entitled to participate in any appreciation of the Underlying unless the level of the Underlying increases by at least 27.50% from the Initial Level to the Final Level.

The Redemption Amounts set forth below are for illustrative purposes only. The actual Redemption Amount applicable to a purchaser of the securities will depend on the Final Level. You should consider carefully whether the securities are suitable to your investment goals. Any payment on the securities is subject to our ability to meet our obligations as they become due. The numbers appearing in the tables and examples below have been rounded for ease of analysis.

Table: Hypothetical Redemption Amounts

|

Final Level |

Percentage

Change |

Reference Value (Final Level × Conversion Ratio) |

Return on the Securities |

Redemption Amount |

| $367.53 | 100% | $1,568.63 | 56.863% | $1,568.63 |

| $349.154 | 90% | $1,490.20 | 49.02% | $1,490.20 |

| $330.777 | 80% | $1,411.77 | 41.177% | $1,411.77 |

| $312.401 | 70% | $1,333.34 | 33.334% | $1,333.34 |

| $294.024 | 60% | $1,254.90 | 25.49% | $1,254.90 |

| $275.648 | 50% | $1,176.47 | 17.647% | $1,176.47 |

| $257.271 | 40% | $1,098.04 | 9.804% | $1,098.04 |

| $238.895 | 30% | $1,019.61 | 1.961% | $1,019.61 |

| $234.30 | 27.50% | $1,000 | 0% | $1,000 |

| $220.518 | 20% | $941.18 | 0% | $1,000 |

| $202.142 | 10% | $862.75 | 0% | $1,000 |

| $183.765 | 0% | $784.31 | 0% | $1,000 |

| $165.389 | -10% | $705.89 | 0% | $1,000 |

| $147.012 | -20% | $627.45 | 0% | $1,000 |

| $128.636 | -30% | $549.02 | 0% | $1,000 |

| $110.259 | -40% | $470.59 | 0% | $1,000 |

| $91.883 | -50% | $392.16 | 0% | $1,000 |

| $73.506 | -60% | $313.73 | 0% | $1,000 |

| $55.13 | -70% | $235.30 | 0% | $1,000 |

| $36.753 | -80% | $156.86 | 0% | $1,000 |

| $18.377 | -90% | $78.43 | 0% | $1,000 |

| $0 | -100% | $0.00 | 0% | $1,000 |

5

Examples:

The following examples illustrate how the Redemption Amount is calculated.

Example 1: The level of the Underlying increases by 70% from the Initial Level to the Final Level. The Reference Value is calculated as follows:

| Reference Value | = | Conversion Ratio × Final Level |

| = | 4.26803 × $312.401 | |

| = | $1,333.34 |

Because the Reference Value is greater than $1,000, you will receive at maturity an amount equal to the Reference Value. The Redemption Amount will equal $1,333.34 for each $1,000 principal amount of securities. Because the level of the Underlying increases from the Initial Level to the Final Level by more than 27.50%, the Redemption Amount on the Valuation Date is greater than $1,000.

Example 2: The level of the Underlying increases by 10% from the Initial Level to the Final Level. The Reference Value is calculated as follows:

| Reference Value | = | Conversion Ratio × Final Level |

| = | 4.26803 × $202.142 | |

| = | $862.75 |

Because the level of the Underlying increases from the Initial Level to the Final Level by less than 27.50%, the Reference Value is less than $1,000. Therefore, the Redemption Amount is equal to the principal amount. You will receive at maturity a payment in cash equal to $1,000 per $1,000 principal amount of securities.

Example 3: The level of the Underlying decreases by 50% from the Initial Level to the Final Level. The Reference Value is calculated as follows:

| Reference Value | = | Conversion Ratio × Final Level |

| = | 4.26803 × $91.883 | |

| = | $392.16 |

Because the Reference Value is less than $1,000, the Redemption Amount is equal to the principal amount. You are entitled to receive at maturity a payment in cash equal to $1,000 per $1,000 principal amount of securities.

Although the Final Level is less than the Initial Level, the Redemption Amount is equal to $1,000.

6

Selected Risk Considerations

An investment in the securities involves significant risks. Investing in the securities is not equivalent to investing directly in the Underlying. These risks are explained in more detail in the “Risk Factors” section of any accompanying product supplement.

| • | THE SECURITIES WILL PAY LESS THAN THE FULL APPRECIATION OF THE UNDERLYING, IF ANY — If the level of the Underlying appreciates over the term of the securities, you will not participate in such appreciation unless the Underlying has appreciated by an amount sufficient to offset the Premium of 27.50%. This is because the Conversion Ratio reflects the Premium over the Initial Level. As a result, the return on your securities in the case of an increase in the level of the Underlying will not equal the return of a direct investment in the Underlying and will increase by less than 1% for every 1% increase in the level of the Underlying beyond the Premium. The Underlying would need to appreciate by 27.50% before you would begin to participate in any appreciation of the Underlying. Any payment on the securities is subject to our ability to meet our obligations as they become due. |

| · | REGARDLESS OF THE AMOUNT OF ANY PAYMENT YOU RECEIVE ON THE SECURITIES, YOUR ACTUAL YIELD MAY BE DIFFERENT IN REAL VALUE TERMS— Inflation may cause the real value of any payment you receive on the securities to be less at maturity than it is at the time you invest. An investment in the securities also represents a forgone opportunity to invest in an alternative asset that generates a higher real return. You should carefully consider whether an investment that may result in a return that is lower than the return on alternative investments is appropriate for you. |

| • | THE SECURITIES ARE SUBJECT TO THE CREDIT RISK OF CREDIT SUISSE — Investors are dependent on our ability to pay all amounts due on the securities, and therefore, investors are subject to our credit risk. Any decline in our credit ratings, any adverse changes in the market’s view of our creditworthiness or any increase in our credit spreads is likely to adversely affect the value of the securities prior to maturity. |

| • | THE SECURITIES DO NOT PAY INTEREST — We will not pay interest on the securities. You may receive less at maturity than you could have earned on ordinary interest-bearing debt securities with similar maturities, including other of our debt securities, since the Redemption Amount is based on the performance of the Underlying. Because the Redemption Amount may be less than the amount originally invested in the securities, the return on the securities (the effective yield to maturity) may be negative. Even if it is positive, the return payable on each security may not be enough to compensate you for any loss in value due to inflation and other factors relating to the value of money over time. |

| • | THE PROBABILITY THAT THE FINAL LEVEL WILL BE GREATER THAN THE INITIAL LEVEL BY LESS THAN THE PREMIUM WILL DEPEND ON THE VOLATILITY OF THE UNDERLYING — “Volatility” refers to the frequency and magnitude of changes in the level of the Underlying. The greater the expected volatility with respect to the Underlying on the Trade Date, the higher the expectation as of the Trade Date that the level of the Underlying will not appreciate by an amount sufficient to offset the Premium (as described under “The securities will pay less than the full appreciation of the Underlying, if any” above), indicating a higher probability that you will not participate in any appreciation of the Underlying. The terms of the securities are set, in part, based on expectations about the volatility of the Underlying as of the Trade Date. The volatility of the Underlying can change significantly over the term of the securities. The level of the Underlying could fall sharply, which could result in a return of principal and no participation in any appreciation of the Underlying. |

| • | NO AFFILIATION WITH THE REFERENCE SHARE ISSUER — We are not affiliated with the Reference Share Issuer. You should make your own investigation into the Underlying and the Reference Share Issuer. In connection with the offering of the securities, neither we nor our affiliates have participated in the preparation of any publicly available documents or made any due diligence inquiry with respect to the Reference Share Issuer. |

| • | HEDGING AND TRADING ACTIVITY — We or any of our affiliates may carry out hedging activities related to the securities, including in the Underlying or instruments related to the Underlying. We or our affiliates may also trade in the Underlying or instruments related to the Underlying from time to time. Any of these hedging or trading activities on or prior to the Trade Date and during the term of the securities could adversely affect our payment to you at maturity. |

7

| • | THE ESTIMATED VALUE OF THE SECURITIES ON THE TRADE

DATE IS LESS THAN THE PRICE TO PUBLIC — The initial estimated value of your securities on the Trade Date (as

determined by reference to our pricing models and our internal funding rate) is less than the original Price to Public. The Price

to Public of the securities includes any discounts or commissions as well as transaction costs such as expenses incurred to create,

document and market the securities and the cost of hedging our risks as issuer of the securities through one or more of our affiliates

(which includes a projected profit). These costs will be effectively borne by you as an investor in the securities. These amounts

will be retained by Credit Suisse or our affiliates in connection with our structuring and offering of the securities (except to

the extent discounts or commissions are reallowed to other broker-dealers or any costs are paid to third parties). On the Trade Date, we value the components of the securities in accordance with our pricing models. These include a fixed income component valued using our internal funding rate, and individual option components valued using mid-market pricing. As such, the payout on the securities can be replicated using a combination of these components and the value of these components, as determined by us using our pricing models, will impact the terms of the securities at issuance. Our option valuation models are proprietary. Our pricing models take into account factors such as interest rates, volatility and time to maturity of the securities, and they rely in part on certain assumptions about future events, which may prove to be incorrect. |

Because Credit Suisse’s pricing models may differ from other issuers’ valuation models, and because funding rates taken into account by other issuers may vary materially from the rates used by Credit Suisse (even among issuers with similar creditworthiness), our estimated value at any time may not be comparable to estimated values of similar securities of other issuers.

| • | EFFECT OF INTEREST RATE USED IN STRUCTURING THE SECURITIES — The internal funding rate we use in structuring notes such as these securities is typically lower than the interest rate that is reflected in the yield on our conventional debt securities of similar maturity in the secondary market (our “secondary market credit spreads”). If on the Trade Date our internal funding rate is lower than our secondary market credit spreads, we expect that the economic terms of the securities will generally be less favorable to you than they would have been if our secondary market credit spread had been used in structuring the securities. We will also use our internal funding rate to determine the price of the securities if we post a bid to repurchase your securities in secondary market transactions. See “—Secondary Market Prices” below. |

| • | SECONDARY MARKET PRICES — If Credit Suisse (or an affiliate) bids for your securities in secondary

market transactions, which we are not obligated to do, the secondary market price (and the value used for account statements or

otherwise) may be higher or lower than the Price to Public and the estimated value of the securities on the Trade Date. The estimated

value of the securities on the cover of this pricing supplement does not represent a minimum price at which we would be willing

to buy the securities in the secondary market (if any exists) at any time. The secondary market price of your securities at any

time cannot be predicted and will reflect the then-current estimated value determined by reference to our pricing models and other

factors. These other factors include our internal funding rate, customary bid and ask spreads and other transaction costs, changes

in market conditions and any deterioration or improvement in our creditworthiness. In circumstances where our internal funding

rate is lower than our secondary market credit spreads, our secondary market bid for your securities could be more favorable than

what other dealers might bid because, assuming all else equal, we use the lower internal funding rate to price the securities and

other dealers might use the higher secondary market credit spread to price them. Furthermore, assuming no change in market conditions

from the Trade Date, the secondary market price of your securities will be lower than the Price to Public because it will not include

any discounts or commissions and hedging and other transaction costs. If you sell your securities to a dealer in a secondary market

transaction, the dealer may impose an additional discount or commission, and as a result the price you receive on your securities

may be lower than the price at which we may repurchase the securities from such dealer. We (or an affiliate) may initially post a bid to repurchase the securities from you at a price that will exceed the then-current estimated value of the securities. That higher price reflects our projected profit and costs that were included in the Price to Public, and that higher price may also be initially used for account statements or otherwise. We (or our affiliate) may offer to pay this higher price, for your benefit, but the amount of any excess over the then-current estimated value will be temporary and is expected to decline over a period of approximately six to nine months. |

8

The securities are not designed to be short-term trading instruments and any sale prior to maturity could result in a substantial loss to you. You should be willing and able to hold your securities to maturity.

| • | CREDIT SUISSE IS SUBJECT TO SWISS REGULATION — As a Swiss bank, Credit Suisse is subject to regulation by governmental agencies, supervisory authorities and self-regulatory organizations in Switzerland. Such regulation is increasingly more extensive and complex and subjects Credit Suisse to risks. For example, pursuant to Swiss banking laws, the Swiss Financial Market Supervisory Authority (FINMA) may open resolution proceedings if there are justified concerns that Credit Suisse is over-indebted, has serious liquidity problems or no longer fulfills capital adequacy requirements. FINMA has broad powers and discretion in the case of resolution proceedings, which include the power to convert debt instruments and other liabilities of Credit Suisse into equity and/or cancel such liabilities in whole or in part. If one or more of these measures were imposed, such measures may adversely affect the terms and market value of the securities and/or the ability of Credit Suisse to make payments thereunder and you may not receive any amounts owed to you under the securities. |

| • | LACK OF LIQUIDITY — The securities will not be listed on any securities exchange. Credit Suisse (or its affiliates) intends to offer to purchase the securities in the secondary market but is not required to do so. Even if there is a secondary market, it may not provide enough liquidity to allow you to trade or sell the securities when you wish to do so. Because other dealers are not likely to make a secondary market for the securities, the price at which you may be able to trade your securities is likely to depend on the price, if any, at which Credit Suisse (or its affiliates) is willing to buy the securities. If you have to sell your securities prior to maturity, you may not be able to do so or you may have to sell them at a substantial loss. |

| • | POTENTIAL CONFLICTS — We and our affiliates play a variety of roles in connection with the issuance of the securities, including acting as calculation agent and as agent of the issuer for the offering of the securities, hedging our obligations under the securities and determining their estimated value. In performing these duties, the economic interests of us and our affiliates are potentially adverse to your interests as an investor in the securities. Further, hedging activities may adversely affect any payment on or the value of the securities. Any profit in connection with such hedging activities will be in addition to any other compensation that we and our affiliates receive for the sale of the securities, which creates an additional incentive to sell the securities to you. We and/or our affiliates may also currently or from time to time engage in business with the Reference Share Issuer, including extending loans to, or making equity investments in, the Reference Share Issuer or providing advisory services to the Reference Share Issuer. In addition, one or more of our affiliates may publish research reports or otherwise express opinions with respect to the Reference Share Issuer and these reports may or may not recommend that investors buy or hold shares of the Underlying. As a prospective purchaser of the securities, you should undertake an independent investigation of the Reference Share Issuer that in your judgment is appropriate to make an informed decision with respect to an investment in the securities. |

| • | UNPREDICTABLE ECONOMIC AND MARKET FACTORS WILL AFFECT THE VALUE OF THE SECURITIES — The payout on the securities can be replicated using a combination of the components described in “The estimated value of the securities on the Trade Date is less than the Price to Public.” Therefore, in addition to the level of the Underlying on any trading day, the terms of the securities at issuance and the value of the securities prior to maturity may be influenced by factors that impact the value of fixed income securities and options in general, such as: |

| o | the expected and actual volatility of the Underlying; |

| o | the time to maturity of the securities; |

| o | the dividend rate on the Underlying; |

| o | interest and yield rates in the market generally; |

| o | investors’ expectations with respect to the rate of inflation; |

| o | events affecting companies engaged in the industry of the Reference Share Issuer; |

9

| o | geopolitical conditions and economic, financial, political, regulatory or judicial events that affect the Reference Share Issuer or markets generally and which may affect the level of the Underlying; and |

| o | our creditworthiness, including actual or anticipated downgrades in our credit ratings. |

Some or all of these factors may influence the price that you will receive if you choose to sell your securities prior to maturity. The impact of any of the factors set forth above may enhance or offset some or all of any change resulting from another factor or factors.

| • | NO OWNERSHIP RIGHTS IN THE UNDERLYING — Your return on the securities will not reflect the return you would realize if you actually owned shares of the Underlying. The return on your investment is not the same as the total return based on a purchase of shares of the Underlying. |

| • | NO DIVIDEND PAYMENTS OR VOTING RIGHTS — As a holder of the securities, you will not have any ownership interest or rights in the Underlying, such as voting rights or dividend payments. In addition, the issuer of the Underlying will not have any obligation to consider your interests as a holder of the securities in taking any corporate action that might affect the value of the Underlying and therefore, the value of the securities. |

| • | ANTI-DILUTION PROTECTION IS LIMITED — The calculation agent will make anti-dilution adjustments for certain events affecting the Underlying. However, an adjustment will not be required in response to all events that could affect the Underlying. If an event occurs that does not require the calculation agent to make an adjustment, or if an adjustment is made but such adjustment does not fully reflect the economics of such event, the value of the securities may be materially and adversely affected. See “Adjustment for Ordinary Dividend” in “Key Terms” herein and “Description of the Securities—Adjustments—For equity securities of a reference share issuer” in the relevant product supplement. |

Supplemental Use of Proceeds and Hedging

We intend to use the proceeds of this offering for our general corporate purposes, which may include the refinancing of existing debt outside Switzerland. Some or all of the proceeds we receive from the sale of the securities may be used in connection with hedging our obligations under the securities through one or more of our affiliates. Such hedging or trading activities on or prior to the Trade Date and during the term of the securities (including on the Valuation Date) could adversely affect the value of the Underlying and, as a result, could decrease the amount you may receive on the securities at maturity. For additional information, see “Supplemental Use of Proceeds and Hedging” in any accompanying product supplement.

10

The Underlying

Companies with securities registered under the Securities Exchange Act of 1934 (the “Exchange Act”) are required to periodically file certain financial and other information specified by the SEC. Information provided to or filed with the SEC by the Reference Share Issuer pursuant to the Exchange Act can be located by reference to the SEC file number provided below.

According to its publicly available filings with the SEC, McDonald’s Corporation franchises and operates McDonald’s restaurants, which serve a broad menu at various price points. The common stock of McDonald’s Corporation is listed on the New York Stock Exchange. McDonald’s Corporation’s SEC file number is 001-05231 and can be accessed through www.sec.gov.

This pricing supplement relates only to the securities offered hereby and does not relate to the Underlying or other securities of the Reference Share Issuer. We have derived all disclosures contained in this pricing supplement regarding the Underlying and the Reference Share Issuer from the publicly available documents described in the preceding paragraph. In connection with the offering of the securities, neither we nor our affiliates have participated in the preparation of such documents or made any due diligence inquiry with respect to the Reference Share Issuer.

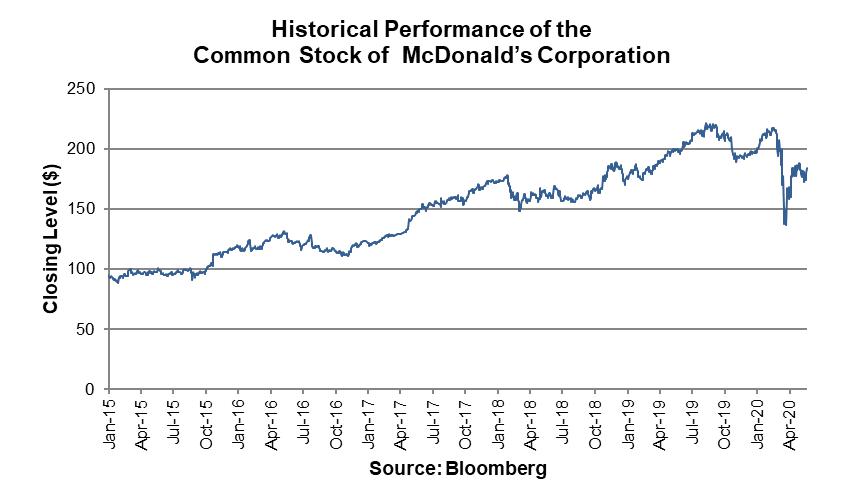

Historical Information

The following graph sets forth the historical performance of the Underlying based on the closing level of the Underlying from January 2, 2015 through May 20, 2020. We obtained the historical information below from Bloomberg, without independent verification.

You should not take the historical levels of the Underlying as an indication of future performance of the Underlying or the securities. Any historical trend in the level of the Underlying during any period set forth below is not an indication that the level of the Underlying is more or less likely to increase or decrease at any time over the term of the securities.

For additional information about the Underlying, see the information set forth under “The Underlying” herein.

The closing level of the Underlying on May 20, 2020 was $184.10.

11

United States Federal Tax Considerations

This discussion supplements and, to the extent inconsistent therewith, supersedes the discussion in the accompanying product supplement under “Material United States Federal Income Tax Considerations.” The discussions below and in the accompanying product supplement do not address the consequences to taxpayers subject to special tax accounting rules under Section 451(b) of the Internal Revenue Code.

In the opinion of our counsel, Davis Polk & Wardwell LLP, the securities should be treated as “contingent payment debt instruments” for U.S. federal income tax purposes, as described in the section of the accompanying product supplement called “Material United States Federal Income Tax Considerations—U.S. Holders—Contingent Payment Debt Instruments,” and the remaining discussion assumes that this treatment of the securities is respected.

If you are a U.S. Holder, you will be required to recognize interest income during the term of the securities at the “comparable yield,” which generally is the yield at which we could issue a fixed-rate debt instrument with terms similar to those of the securities, including the level of subordination, term, timing of payments and general market conditions, but excluding any adjustments for the riskiness of the contingencies or the liquidity of the securities. We are required to construct a “projected payment schedule” in respect of the securities representing a payment the amount and timing of which would produce a yield to maturity on the securities equal to the comparable yield. Assuming you hold the securities until their maturity, the amount of interest you include in income based on the comparable yield in the taxable year in which the securities mature will be adjusted upward or downward to reflect the difference, if any, between the actual and projected payment on the securities at maturity as determined under the projected payment schedule.

Upon the sale, exchange or retirement of the securities prior to maturity, you generally will recognize gain or loss equal to the difference between the proceeds received and your adjusted tax basis in the securities. Your adjusted tax basis will equal your purchase price for the securities, increased by interest previously included in income on the securities. Any gain generally will be treated as ordinary income, and any loss generally will be treated as ordinary loss to the extent of prior interest inclusions on the security and as capital loss thereafter.

We have determined that the comparable yield for a security is a rate of 1.92%, compounded semi-annually, and that the projected payment schedule with respect to a security is as follows:

| Payment Dates | Projected payment (per $1,000) | OID deemed to accrue during accrual period (per $1,000) | Total OID deemed to have accrued from original issue date as of end of accrual period |

| November 28, 2020 | $0.00 | $9.58 | $9.58 |

| May 28, 2021 | $0.00 | $9.68 | $19.26 |

| November 28, 2021 | $0.00 | $9.77 | $29.03 |

| May 28, 2022 | $0.00 | $9.86 | $38.89 |

| November 28, 2022 | $0.00 | $9.96 | $48.85 |

| May 28, 2023 | $0.00 | $10.05 | $58.90 |

| November 28, 2023 | $0.00 | $10.15 | $69.05 |

| May 28, 2024 | $0.00 | $10.25 | $79.30 |

| November 28, 2024 | $0.00 | $10.34 | $89.64 |

| May 28, 2025 | $0.00 | $10.44 | $100.09 |

| November 28, 2025 | $0.00 | $10.54 | $110.63 |

| May 28, 2026 | $0.00 | $10.64 | $121.27 |

| November 28, 2026 | $0.00 | $10.75 | $132.02 |

| May 28, 2027 | $1,142.87 | $10.85 | $142.87 |

Neither the comparable yield nor the projected payment schedule constitutes a representation by us regarding the actual amount that we will pay on the securities.

12

Non-U.S. Holders. Subject to the discussions in the next paragraph and in “Material United States Federal Income Tax Considerations” in the accompanying product supplement, if you are a Non-U.S. Holder (as defined in the accompanying product supplement) of the securities, you generally will not be subject to U.S. federal withholding or income tax in respect of any amount paid to you with respect to the securities, provided that (i) income in respect of the securities is not effectively connected with your conduct of a trade or business in the United States, and (ii) you comply with the applicable certification requirements. See “Material United States Federal Income Tax Considerations —Non-U.S. Holders Generally” in the accompanying product supplement for a more detailed discussion of the rules applicable to Non-U.S. Holders of the securities.

As discussed under “Material United States Federal Income Tax Considerations—Non-U.S. Holders Generally—Substitute Dividend and Dividend Equivalent Payments” in the accompanying product supplement, Section 871(m) of the Internal Revenue Code generally imposes a 30% withholding tax on “dividend equivalents” paid or deemed paid to Non-U.S. Holders with respect to certain financial instruments linked to U.S. equities or indices that include U.S. equities. Treasury regulations under Section 871(m), as modified by an Internal Revenue Service (the “IRS”) notice, exclude from their scope financial instruments issued prior to January 1, 2023 that do not have a “delta” of one with respect to any U.S. equity. Based on the terms of the securities and representations provided by us, our counsel is of the opinion that the securities should not be treated as transactions that have a “delta” of one within the meaning of the regulations with respect to any U.S. equity and, therefore, should not be subject to withholding tax under Section 871(m).

A determination that the securities are not subject to Section 871(m) is not binding on the IRS, and the IRS may disagree with this determination. Moreover, Section 871(m) is complex and its application may depend on your particular circumstances, including your other transactions. You should consult your tax advisor regarding the potential application of Section 871(m) to the securities.

We will not be required to pay any additional amounts with respect to U.S. federal withholding taxes.

FATCA. You should review the section entitled “Material United States Federal Income Tax Considerations—Securities Held Through Foreign Entities” in the accompanying product supplement regarding withholding rules under the “FATCA” regime. The discussion in that section is hereby modified to reflect regulations proposed by the U.S. Treasury Department indicating an intent to eliminate the requirement under FATCA of withholding on gross proceeds of the disposition of affected financial instruments. The U.S. Treasury Department has indicated that taxpayers may rely on these proposed regulations pending their finalization.

You should read the section entitled “Material United States Federal Income Tax Considerations” in the accompanying product supplement.

You should also consult your tax advisor regarding all aspects of the U.S. federal income and estate tax consequences of an investment in the securities and any tax consequences arising under the laws of any state, local or non-U.S. taxing jurisdiction.

13

Supplemental Plan of Distribution (Conflicts of Interest)

Under the terms and subject to the conditions contained in a distribution agreement dated May 7, 2007, as amended, which we refer to as the distribution agreement, we have agreed to sell the securities to CSSU.

The distribution agreement provides that CSSU is obligated to purchase all of the securities if any are purchased.

CSSU will offer the securities at the offering price set forth on the cover page of this pricing supplement and will not receive a commission in connection with the distribution of the securities. CSSU may re-allow some or all of the discount on the principal amount per security on sales of such securities by other brokers or dealers. If all of the securities are not sold at the initial offering price, CSSU may change the public offering price and other selling terms.

An affiliate of Credit Suisse has paid or may pay in the future a fixed amount to broker-dealers in connection with the costs of implementing systems to support these securities.

We expect to deliver the securities against payment for the securities on the Settlement Date indicated herein, which may be a date that is greater than two business days following the Trade Date. Under Rule 15c6-1 of the Securities Exchange Act of 1934, as amended, trades in the secondary market generally are required to settle in two business days, unless the parties to a trade expressly agree otherwise. Accordingly, if the Settlement Date is more than two business days after the Trade Date, purchasers who wish to transact in the securities more than two business days prior to the Settlement Date will be required to specify alternative settlement arrangements to prevent a failed settlement.

The agent for this offering, CSSU, is our affiliate. In accordance with FINRA Rule 5121, CSSU may not make sales in this offering to any of its discretionary accounts without the prior written approval of the customer. A portion of the net proceeds from the sale of the securities will be used by CSSU or one of its affiliates in connection with hedging our obligations under the securities.

For further information, please refer to “Underwriting (Conflicts of Interest)” in any accompanying product supplement.

14

Validity of the Securities

In the opinion of Davis Polk & Wardwell LLP, as United States counsel to Credit Suisse, when the securities offered by this pricing supplement have been executed and issued by Credit Suisse and authenticated by the trustee pursuant to the indenture, and delivered against payment therefor, such securities will be valid and binding obligations of Credit Suisse, enforceable against Credit Suisse in accordance with their terms, subject to (i) applicable bankruptcy, insolvency and similar laws affecting creditors’ rights generally, (ii) possible judicial or regulatory actions giving effect to governmental actions or foreign laws affecting creditors’ rights and (iii) concepts of reasonableness and equitable principles of general applicability (including, without limitation, concepts of good faith, fair dealing and the lack of bad faith), provided that such counsel expresses no opinion as to the effect of fraudulent conveyance, fraudulent transfer or similar provision of applicable law on the conclusions expressed above. This opinion is given as of the date of this pricing supplement and is limited to the laws of the State of New York, except that such counsel expresses no opinion as to the application of state securities or Blue Sky laws to the securities. Insofar as this opinion involves matters governed by Swiss law, Davis Polk & Wardwell LLP has relied, without independent inquiry or investigation, on the opinion of Homburger AG, dated May 6, 2020 and filed by Credit Suisse as an exhibit to a Current Report on Form 6-K on May 6, 2020. The opinion of Davis Polk & Wardwell LLP is subject to the same assumptions, qualifications and limitations with respect to such matters as are contained in the opinion of Homburger AG. In addition, the opinion of Davis Polk & Wardwell LLP is subject to customary assumptions about the establishment of the terms of the securities, the trustee’s authorization, execution and delivery of the indenture and its authentication of the securities, and the validity, binding nature and enforceability of the indenture with respect to the trustee, all as stated in the opinion of Davis Polk & Wardwell LLP dated May 6, 2020, which was filed by Credit Suisse as an exhibit to a Current Report on Form 6-K on May 6, 2020. Davis Polk & Wardwell LLP expresses no opinion as to waivers of objections to venue, the subject matter or personal jurisdiction of a United States federal court or the effectiveness of service of process other than in accordance with applicable law. In addition, such counsel notes that the enforceability in the United States of Section 10.08(c) of the indenture is subject to the limitations set forth in the United States Foreign Sovereign Immunities Act of 1976.

15

Credit Suisse