Registration No. 333-218604-02

Dated April 19, 2018

Securities Act of 1933, Rule 424(b)(2)

UNDERLYING

SUPPLEMENT TO THE PROSPECTUS SUPPLEMENT DATED JUNE 30, 2017, THE PROSPECTUS

SUPPLEMENT DATED JUNE 30, 2017 AND PROSPECTUS DATED JUNE 30, 2017

Credit Suisse AG

Medium-Term Notes and Warrants

Underlying Supplement for Indices

As part of our Medium-Term Notes and Warrants program, Credit Suisse AG (“Credit Suisse”) from time to time may offer certain securities (the “securities”) linked to the performance of one or more indices, each of which we refer to as a “reference index,” or to a weighted basket of reference indices. We refer to such weighted basket as the “basket” and to each reference index included in the basket as a “basket component.” We refer generally to any reference index and basket component as an “underlying.” References to a “reference index,” “basket component” and “underlying” are deemed to include reference to any relevant successor underlying.

This prospectus supplement, which we refer to as an “underlying supplement,” describes some of the underlyings to which the securities may be linked. The specific terms of each security offered will be described in the applicable pricing supplement and product supplement.

With respect to any notes, you should read this underlying supplement, the related prospectus dated June 30, 2017, the related prospectus supplement dated June 30, 2017, any applicable product supplement, the applicable pricing supplement and any applicable free writing prospectus (each, an “offering document”) carefully before you invest. With respect to any warrants, you should read this underlying supplement, the related prospectus dated June 30, 2017, the related prospectus supplement dated June 30, 2017, any applicable product supplement, the applicable pricing supplement and any applicable free writing prospectus (each, also an “offering document”) carefully before you invest. If the terms described in the applicable pricing supplement are different or inconsistent with those described herein (or with those described in the prospectus, prospectus supplement, any applicable product supplement or any applicable free writing prospectus), the terms described in the applicable pricing supplement will control.

This underlying supplement describes only select reference indices to which the securities may be linked. We do not guarantee that we will offer securities linked to any of the reference indices described herein. In addition, we may offer securities linked to one or more reference indices that are not described herein. In such case, we will describe any such additional reference index or reference indices in the applicable pricing supplement or any applicable product supplement or in another underlying supplement.

For risks related to an investment in the securities, please refer to the “Risk Factors” section in any accompanying product supplement and the “Selected Risk Considerations” or “Key Risks” section, as applicable, in the applicable pricing supplement.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of the securities or determined if this underlying supplement or any other offering document to which it relates are truthful or complete. Any representation to the contrary is a criminal offense.

Credit Suisse

The date of this underlying supplement is April 19, 2018.

table of contents

Page

| The Securities | US-1 |

| The Reference Indices | US-2 |

| The NYSE Arca Gold Miners Index | US-2 |

| The NYSE Arca Hong Kong 30 Index | US-5 |

| The DAX Indices | US-6 |

| The DAX | US-6 |

| The MDAX | US-7 |

| The FTSE Russell Indices | US-14 |

| The FTSE 100 Index | US-14 |

| The FTSE China 50™ Index | US-15 |

| The Russell 2000® Index | US-18 |

| The Hang Seng® Indices | US-31 |

| The Hang Seng® Index | US-31 |

| The Hang Seng® China Enterprises Index | US-35 |

| The JPX-Nikkei Index 400 | US-38 |

| The Korea Stock Price Index 200 | US-42 |

| The MVIS® Global Junior Gold Miners Index | US-44 |

| The MSCI Indices | US-50 |

| The MSCI Australia Index | US-51 |

| The MSCI Brazil Index | US-51 |

| The MSCI Brazil 25/50 Index | US-51 |

| The MSCI Canada Index | US-52 |

| The MSCI Germany Index | US-52 |

| The MSCI Emerging Markets Index | US-52 |

| The MSCI EAFE® Index | US-52 |

| The MSCI EASEA® Index | US-53 |

| The MSCI Japan Index | US-53 |

| The MSCI Korea Index | US-53 |

| The MSCI Korea 25/50 Index | US-53 |

| The MSCI Singapore Free Index | US-54 |

| The MSCI Taiwan Index | US-54 |

| The MSCI All Country (AC) Asia Ex Japan Index | US-54 |

| The MSCI All Country (AC) Far East Ex Japan Index | US-54 |

| The MSCI ACWI Index | US-55 |

| The NASDAQ-100 Index | US-66 |

| The NIFTY 50 Index | US-70 |

| The Nikkei 225 Index | US-74 |

| The S&P Dow Jones Indices | US-76 |

| The Dow Jones Industrial Average™ | US-76 |

| The Dow Jones U.S. Financials and Real Estate Indices | US-77 |

| The Dow Jones U.S. Financials Index | US-77 |

| The Dow Jones U.S. Real Estate Index | US-78 |

| The S&P 500® Index | US-82 |

| The S&P MidCap 400® Index | US-82 |

| The S&P 100® Index | US-82 |

| The S&P Select Industry Indices | US-87 |

| The S&P® Homebuilders Select IndustryTM Index | US-87 |

| The S&P® Metals & Mining Select IndustryTM Index | US-87 |

| The S&P® Oil & Gas Exploration & Production Select IndustryTM Index | US-87 |

| The S&P/ASX 200 Index | US-91 |

| The S&P Select Sector Indices | US-93 |

| The Consumer Discretionary Select Sector Index | US-93 |

| The Consumer Staples Select Sector Index | US-94 |

| The Energy Select Sector Index | US-94 |

| The Financial Select Sector Index | US-94 |

| The Health Care Select Sector Index | US-94 |

| The Industrials Select Sector Index | US-94 |

| The Materials Select Sector Index | US-94 |

| The Real Estate Select Sector Index | US-94 |

| The Technology Select Sector Index | US-94 |

| The Utilities Select Sector Index | US-95 |

| The STOXX Indices | US-97 |

| The STOXX® Europe 600 Index | US-97 |

| The EURO STOXX 50® Index | US-98 |

| The EURO STOXX® Banks Index | US-99 |

| The STOXX® Europe 600 Basic Resources Index | US-100 |

| The Swiss Market Index | US-104 |

| The Tokyo Stock Price Index | US-107 |

ii

The Securities

We are responsible for the information contained and incorporated by reference in this underlying supplement. As of the date of this underlying supplement, we have not authorized anyone to provide you with different information, and we take no responsibility for any other information others may give you. We are not making an offer of these securities in any state where the offer is not permitted. You should not assume that the information in this document or the accompanying product supplement, prospectus supplement and prospectus is accurate as of any date other than the date on the front of this document.

We are offering securities for sale in those jurisdictions in the United States where it is lawful to make such offers. The distribution of this underlying supplement or the accompanying pricing supplement, product supplement, prospectus supplement or prospectus and the offering of securities in some jurisdictions may be restricted by law. If you possess this underlying supplement and the accompanying pricing supplement, product supplement, prospectus supplement and prospectus, you should find out about and observe these restrictions. This underlying supplement and the accompanying pricing supplement, product supplement, prospectus supplement and prospectus are not an offer to sell the securities and are not soliciting an offer to buy the securities in any jurisdiction where the offer or sale is not permitted or where the person making the offer or sale is not qualified to do so or from any person to whom such offer or sale is not permitted. We refer you to the “Underwriting (Conflicts of Interest)” or “Supplemental Plan of Distribution” section, as the case may be, of the applicable product supplement and the “Supplemental Plan of Distribution (Conflicts of Interest),” “Supplement to the Plan of Distribution” or “Supplemental Plan of Distribution” section, as the case may be, of the applicable pricing supplement for additional information. If the terms described in the applicable pricing supplement are different or inconsistent with those described herein, the terms described in the applicable pricing supplement will control.

In this underlying supplement and accompanying pricing supplement, product supplement, prospectus supplement and prospectus, unless otherwise specified or the context otherwise requires, references to “we,” “us” and “our” are to Credit Suisse and its consolidated subsidiaries, and references to “dollars” and “$” are to U.S. dollars.

The Reference Indices

The securities may be linked to the performance of one or more of the following reference indices. We have derived all information contained in this underlying supplement regarding each reference index, including, without limitation, its composition, its method of calculation and changes in its components and its historical closing values, from publicly available information. We have not participated in the preparation of, or verified, such publicly available information. Such information reflects the policies of, and is subject to change by, the sponsor(s) of each such reference index.

If any Bloomberg symbol for a particular reference index differs from, or is more precise than, any Bloomberg symbol referenced below, we will set forth the different, or more precise, Bloomberg symbol in the relevant pricing supplement. We have not participated in the preparation of, or independently verified, the information obtained from Bloomberg Financial Markets.

Each reference index is developed, calculated and maintained by its respective sponsor(s) and/or publisher. Neither we nor any of the agents have participated in the preparation of such information or made any due diligence inquiry with respect to any reference index, sponsor(s) or publisher. We cannot give any assurance that all events occurring prior to the date of the applicable pricing supplement (including events that would affect the accuracy or completeness of the publicly available information described in the preceding paragraph) that may affect the level of any reference index (and therefore the level of any such reference index at the time we price the securities, as applicable) have been publicly disclosed. Subsequent disclosure of any such events or the disclosure of or failure to disclose material future events concerning the sponsor of any reference index could affect the interest, payment at maturity or any other amounts payable, if any, on the securities, as applicable, and therefore the market value of the securities in the secondary market, if any.

You, as an investor in the securities, should make your own investigation into any relevant reference index, sponsor(s) or publisher. The sponsors and publishers are not involved in the offer of the securities in any way and have no obligation to consider your interests as a holder of the securities. The sponsors and/or publishers have no obligation to continue to publish the reference indices, and may discontinue or suspend publication of any reference index at any time in their sole discretion.

The historical performance of a reference index is not an indication of its future performance and future performance may differ significantly from historical performance, either positively or negatively.

Information contained on certain websites mentioned below is not incorporated by reference in, and should not be considered part of, this underlying supplement or the accompanying prospectus supplement and prospectus.

The NYSE Arca Gold Miners Index

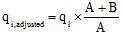

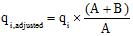

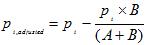

The NYSE Arca Gold Miners Index is a modified market capitalization weighted index composed of publicly traded companies involved primarily in the mining of gold and silver. The NYSE Arca Gold Miners Index includes common stocks, American depositary receipts (“ADRs”) and Global depositary receipts (“GDRs”) of selected companies that are involved in mining for gold and silver ore and that are listed for trading on the NYSE or the NYSE Arca, Inc. (“NYSE Arca”) or quoted on The NASDAQ Stock Market. Only companies with market capitalization greater than $750 million that have a daily average trading volume of at least 50,000 shares over the past three months are eligible for inclusion in the NYSE Arca Gold Miners Index. If a company has more than one listing, the listing representing the company’s ordinary shares is generally used. The index compiler has discretion not to include all companies that meet the minimum levels for inclusion.

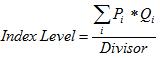

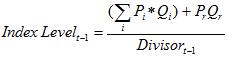

The NYSE Arca Gold Miners Index is calculated on a price return basis using a modified market capitalization divided by the divisor. The divisor was set on December 20, 2002 to obtain a base level of 500.00 at the base market capitalization. As described below, the divisor is continually adjusted as a result of corporate actions and composition changes to maintain continuity in the index. More specifically, the index is calculated using the following formula:

US-2

|

Where:

| t | day of calculation | |

| N | number of constituent equities in index | |

| Qi,t | number of shares of equity i on day t | |

| Mi,t | multiplier of equity i | |

| Ci,t | price of equity i on day t | |

| DIV | current index divisor on day t |

Quarterly Review of the NYSE Arca Gold Miners Index

The NYSE Arca Gold Miners Index is reviewed quarterly so that at least 90% of the index weight is accounted for by index components that continue to meet the initial eligibility requirements. The NYSE Arca may at any time and from time to time change the number of securities comprising the group by adding or deleting one or more securities, or replacing one or more securities contained in the group with one or more substitute securities of its choice, if in the NYSE Arca’s discretion such addition, deletion or substitution is necessary or appropriate to maintain the quality and/or character of the NYSE Arca Gold Miners Index. Components will be removed from the index during the quarterly review if their market capitalization falls below $450 million, or the traded average daily shares for the previous three months is lower than 30,000 shares and the traded average daily value for the previous three months is lower than $600,000.

Changes to the NYSE Arca Gold Miners Index compositions and/or the component share weights in the NYSE Arca Gold Miners Index typically take effect after the close of trading on the third Friday of each calendar quarter month, in connection with the quarterly index rebalance. An index announcement on the website of NYSE Euronext will announce such changes. The inclusion of companies in the index will be announced at least three trading days before the actual inclusion. The component to be removed will be announced no later than 3 p.m. ET on the business day before the effective date of removal.

The NYSE Arca Gold Miners Index is weighted based on the market capitalization of each of the component securities, modified to conform to the following asset diversification requirements, which are applied in conjunction with the scheduled quarterly adjustments to the NYSE Arca Gold Miners Index:

(1) the weight of any single component security may not account for more than 20% of the total value of the NYSE Arca Gold Miners Index;

(2) the component securities are split into two subgroups—large and small—which are ranked by market capitalization weight in the NYSE Arca Gold Miners Index. Large securities are defined as having a NYSE Arca Gold Miners Index weight greater than or equal to 5%. Small securities are defined as having an index weight below 5%; and

(3) the aggregate weight of those component securities that individually represent more than 4.5% of the total value of the NYSE Arca Gold Miners Index may not account for more than 45% of the total NYSE Arca Gold Miners Index value.

During the scheduled quarterly adjustments to the index, the component weights are adjusted using the following process to maintain the above three asset diversification requirements:

(1) If any component stock exceeds 20% of the total value of the index, then all stocks greater than 20% of the index are reduced to represent 20% of the value of the index. The aggregate amount by which all component stocks are reduced is redistributed proportionately across the remaining stocks that represent less than 20% of the index value. After this redistribution, if any other stock then exceeds 20%, the stock is set to 20% of the index value and the redistribution is repeated.

(2) The components are sorted into two groups, large and small. Large components are components with a starting index weight of 5% or greater and small components are those that are under 5% (after any adjustments for

US-3

Diversification Rule 1). The large and small group in aggregate will represent 45% and 55%, respectively, of the final index weight.

(3) The weight of each of the large stocks will be scaled down proportionately (with a floor of 5%) so that the aggregate weight of the large components will be reduced to represent 45% of the index. If any large component stock falls below a weight equal to the product of 5% and the proportion by which the stocks were scaled down following this distribution, then the weight of the stock is set equal to 5% and the components with weights greater than 5% will be reduced proportionately.

(4) Finally, the weight of each of the small components will be scaled up proportionately from the redistribution of the large components. If any small component stock exceeds a weight equal to the product of 4.5% and the proportion by which the stocks were scaled down following this distribution, then the weight of the stock is set equal to 4.5%. The redistribution of weight to the remaining stocks is repeated until the entire amount has been redistributed.

Corporate Action-Related Adjustments

The index may be adjusted in order to maintain the continuity of the index level and the composition. The underlying aim is that the index continues to reflect as closely as possible the value of the underlying portfolio. Adjustments take place in reaction to events that occur with constituents, in order to mitigate or eliminate the effect of that event on the index.

(1) Removal of constituents. Any stock deleted from the index as a result of a corporate action such as a merger, acquisition, spin-off, delisting or bankruptcy is not replaced by any new stock. The total number of stocks in the index is reduced by one every time a company is deleted. If a company is removed from the index, the divisor will be adapted to maintain the index level.

(a) Mergers and acquisitions. In the event that a merger or acquisition occurs between members of the index, the acquired company is deleted and its market capitalization moves to the acquiring company’s stock. In the event that only one of the parties to a merger or acquisition is a member of the index, an acquiring member of the index continues as a member of the index and its shares will be adjusted at the next rebalance while an acquired member of the index is removed from the index and the acquiring company may be considered for inclusion at the next rebalance.

(b) Suspensions and company distress. Immediately upon a company’s bankruptcy announcement, the stock is removed from the index at the closing price of the first trading day following the announcement. If the stock does not trade on the relevant exchange between the bankruptcy announcement and the next rebalance effective date, the stock may be deleted from the index with a presumed market value of $0.

(c) Split-up / spin-off. The closing price of the index constituent is adjusted by the value of the spin-off. Spun-off companies will not be automatically added into the index at the time of the event.

(2) Dividends. The price index will be adjusted for dividends that are special. To determine whether a dividend should be considered a special dividend, the compiler will use the following criteria: (a) the declaration of a dividend additional to those dividends declared as part of a company’s normal results and dividend reporting cycle; or (b) the identification of an element of a dividend paid in line with a company’s normal results and dividend reporting cycle as an element that is unambiguously additional to the company’s normal payment.

(3) Rights issues and other rights. In the event of a rights issue, the price is adjusted for the value of the right on the ex date, and the shares are increased according to the terms of the offering. The value of the right is determined from the market value of the right. The compiler shall only effect adjustments if the rights represent a positive value.

(4) Bonus issues, stock splits and reverse stock splits. For bonus issues, stock splits and reverse stock splits, the number of shares included in the index will be adjusted in accordance with the ratio given in the corporate action. Since the event won’t change the value of the company included in the index, the divisor will not be changed because of this.

(5) Changes in number of shares. Changes in the number of shares in issue will not be reflected in the index until the next review unless the change is related to a specific corporate action.

US-4

The NYSE Arca Hong Kong 30 Index

The NYSE Arca Hong Kong 30 Index (“NYSE Arca Hong Kong 30 Index”) is a broad-market index that measures the composite price performance of 30 stocks actively traded on the Stock Exchange of Hong Kong (“SEHK”) and is designed to reflect the movement of the Hong Kong stock market as a whole. The NYSE Arca Hong Kong 30 Index was established on June 25, 1993 with a benchmark value of 350.00. The NYSE Arca Hong Kong 30 Index is calculated and disseminated each New York business day based on the most recent official closing price of each of the component stocks as reported by the SEHK and a fixed HK$/US$ exchange rate. The NYSE Arca Hong Kong 30 Index is calculated, maintained and published by the NYSE Arca, an indirect, wholly owned subsidiary of the American Stock Exchange LLC (“AMEX” or the “American Stock Exchange”), which completed its merger with NYSE Euronext on October 1, 2008. The combined entity is referred to herein as the “Exchange.” The NYSE Arca Hong Kong 30 Index is reported by Bloomberg under the ticker symbol “HKX.”

Eligibility Standards for the Inclusion and Maintenance of Component Stocks in the NYSE Arca Hong Kong 30 Index

NYSE Arca states that it selects securities comprising the NYSE Arca Hong Kong 30 Index based on their market weight, trading liquidity and representativeness of the business industries reflected on the SEHK. NYSE Arca will require that each NYSE Arca Hong Kong 30 Index component security be one issued by an entity with major business interests in Hong Kong, listed for trading on the SEHK, and have its primary trading market located in a country with which NYSE Arca has an effective surveillance sharing agreement. NYSE Arca will remove any NYSE Arca Hong Kong 30 Index component security that fails to meet any of the foregoing listing and maintenance criteria within 30 days after such a failure occurs. To ensure that the NYSE Arca Hong Kong 30 Index does not consist of a number of thinly-capitalized, low-priced securities with small public floats and low trading volumes, NYSE Arca has established additional listing and maintenance criteria:

| · | All component securities selected for inclusion in the NYSE Arca Hong Kong 30 Index must have, and thereafter maintain, an average daily capitalization, as calculated by the total number of shares outstanding times the latest price per share (in Hong Kong dollars), measured over the prior six-month period, of at least HK$3 billion (approximately US$380 million); |

| · | All component securities selected for inclusion in the NYSE Arca Hong Kong 30 Index must have, and thereafter maintain, a minimum free float value (total freely tradable outstanding shares less insider holdings), based on a monthly average measured over the prior three-month period, of US$238 million, although up to, but no more than, three NYSE Arca Hong Kong 30 Index component securities may have a free float value of less than US$238 million but in no event less than US$150 million, measured over the same period; |

| · | All component securities selected for inclusion in the NYSE Arca Hong Kong 30 Index must have, and thereafter maintain, an average daily closing price, measured over the prior six-month period, not lower than HK$2.50; and |

| · | All component securities selected for inclusion in the NYSE Arca Hong Kong 30 Index must have, and thereafter maintain, an average daily trading volume, measured over the prior six-month period, of more than one million shares per day, although up to, but no more than, three component securities may have an average daily trading volume, measured over the prior six-month period, of less than one million shares per day but in no event less than 500,000 shares per day. |

NYSE Arca reviews the NYSE Arca Hong Kong 30 Index’s component securities on a quarterly basis, conducted on the last business day in January, April, July and October. Any component security failing to meet the above listing and maintenance criteria is reviewed on the second Friday of the second month following the quarterly review again to determine compliance with the above criteria. Any NYSE Arca Hong Kong 30 Index component stock failing this second review is replaced by a “qualified” NYSE Arca Hong Kong 30 Index component stock, effective upon the close of business on the following Friday, provided, however, that if such Friday is not a business day, the replacement will be effective at the close of business on the first preceding business day. NYSE Arca will notify its membership immediately after it determines to replace an NYSE Arca Hong Kong 30 Index component stock.

US-5

The NYSE Arca Hong Kong 30 Index is maintained by NYSE Arca and contains at least thirty component stocks at all times. NYSE Arca may change the composition of the NYSE Arca Hong Kong 30 Index at any time in order to reflect more accurately the composition and track the movement of the Hong Kong stock market. Any replacement component stock must also meet the component stock listing and maintenance standards as discussed above. If the number of NYSE Arca Hong Kong 30 Index component securities in the NYSE Arca Hong Kong 30 Index falls below thirty, no new option series based on the NYSE Arca Hong Kong 30 Index will be listed for trading unless and until the Securities and Exchange Commission approves a rule filing pursuant to section 19(b) of the Exchange Act of 1934 reflecting such change.

License Agreement with the Exchange

We have entered into an agreement with the Exchange, providing us and certain of our affiliates or subsidiaries identified in that agreement with a non-exclusive license and, for a fee, with the right to use the NYSE Arca Hong Kong 30 Index, which is owned and published by the Exchange, in connection with certain securities.

The securities are not sponsored, endorsed, sold or promoted by the Exchange (including its affiliates). The Exchange has not passed on the legality or suitability of, or the accuracy or adequacy of descriptions and disclosures relating to the securities. The Exchange makes no representation or warranty, express or implied to the owners of the securities or any member of the public regarding the advisability of investing in securities generally or in the securities particularly, or the ability of the NYSE Arca Hong Kong 30 Index to track general stock market performance. The Exchange has no relationship to Credit Suisse with respect to the NYSE Arca Hong Kong 30 Index other than the licensing of the NYSE Arca Hong Kong 30 Index and the related trademarks for use in connection with the securities, which index is determined, composed and calculated by the Exchange without regard to Credit Suisse or the securities. The Exchange has no obligation to take the needs of Credit Suisse or the owners of the securities into consideration in determining, composing or calculating the NYSE Arca Hong Kong 30 Index. The Exchange is not responsible for and has not participated in the determination of the timing of, prices at, or quantities of the securities to be issued or in the determination or calculation of the equation by which the securities are to be converted into cash. The Exchange has no liability in connection with the administration, marketing or trading of the securities.

The Exchange is under no obligation to continue the calculation and dissemination of the NYSE Arca Hong Kong 30 Index and the method by which the NYSE Arca Hong Kong 30 Index is calculated and the name “NYSE Arca Hong Kong 30 Index” may be changed at the discretion of the Exchange. No inference should be drawn from the information contained in this underlying supplement that the Exchange makes any representation or warranty, implied or express, to you or any member of the public regarding the advisability of investing in securities generally or in the securities in particular or the ability of the NYSE Arca Hong Kong 30 Index to track general stock market performance. The Exchange has no obligation to take into account your interest, or that of anyone else having an interest in determining, composing or calculating the NYSE Arca Hong Kong 30 Index. The use of and reference to the NYSE Arca Hong Kong 30 Index in connection with the securities have been consented to by the Exchange.

The Exchange disclaims all responsibility for any inaccuracies in the data on which the NYSE Arca Hong Kong 30 Index is based, or any mistakes or errors or omissions in the calculation or dissemination of the NYSE Arca Hong Kong 30 Index.

The DAX Indices

The DAX

The DAX® Index (the “DAX”) comprises the 30 largest and most actively traded companies listed on the Frankfurt Stock Exchange. These companies are selected from the continuously traded companies in the Prime Standard Segment that meet certain selection criteria. To be listed in the Prime Standard, a company must meet minimum statutory requirements, which include the regular publication of financial reports, and must satisfy additional transparency requirements. The reference date of the DAX is December 30, 1987. The DAX is reported by Bloomberg under the ticker symbol “DAX.”

The DAX is capital-weighted, meaning the weight of any individual issue is proportionate to its respective share in the overall capitalization of all index component issuers. The weight of any single company is capped at 10% of the DAX capitalization, measured quarterly. Weighting is based exclusively on the free float portion of the issued share capital of any class of shares involved. Both the number of shares included in the issued share capital and the

US-6

free float factor are updated on one day each quarter (the “chaining date”). The DAX is a performance (i.e., total return) index, which reinvests all income from dividend and bonus payments in the DAX portfolio. For information concerning the methodology of the DAX, please refer to “Methodology of the DAX Indices” below.

The MDAX

The MDAX® Index (the “MDAX”) comprises 50 issuers based in Germany from classic sectors (i.e., sectors other than technology sectors) which, in terms of size and turnover, follow after the DAX companies. These companies are selected from the continuously traded companies in the Prime Standard Segment that meet certain selection criteria. To be listed in the Prime Standard, a company must meet minimum statutory requirements, which include the regular publication of financial reports, and must satisfy additional transparency requirements. The reference date of the MDAX is December 30, 1987. The MDAX is reported by Bloomberg under the ticker symbol “MDAX.”

The MDAX is capital-weighted, meaning the weight of any individual issue is proportionate to its respective share in the overall capitalization of all index component issuers. The weight of any single company is capped at 10% of the MDAX capitalization, measured quarterly. Weighting is based exclusively on the free float portion of the issued share capital of any class of shares involved. Both the number of shares included in the issued share capital and the free float factor are updated on one day each quarter (the “chaining date”). The MDAX is a performance (i.e., total return) index, which reinvests all income from dividend and bonus payments in the MDAX portfolio. For information concerning the methodology of the MDAX, please refer to “Methodology of the DAX Indices” below.

Methodology of the DAX Indices

The Working Committee for Equity Indices and the Management Board of Deutsche Börse

The Working Committee for Equity Indices (the “Committee”) advises Deutsche Börse AG (“Deutsche Börse” or the “DAX Index Sponsor”) on all issues related to the DAX and the MDAX (each a “DAX Index,” and together the “DAX Indices”), recommending measures that are necessary in order to ensure the relevance of the DAX Indices range and the correctness and transparency of the DAX Indices calculation process. In accordance with the various rules, the Committee pronounces recommendations in respect of the composition of the DAX Indices. However, any decisions on the composition of and possible modifications to the DAX Indices are exclusively taken by the Management Board of Deutsche Börse (the “Board”). Such decisions are published in a press release and on Deutsche Börse’s publicly available website in the evening after the Committee has concluded its meeting. We have not participated in the preparation of, or independently verified, the information contained on Deutsche Börse’s website.

The Committee’s meetings usually take place on the fifth trading day in each of March, June, September and December. The date for the respective next meeting is announced via a press release on Deutsche Börse’s website on the evening of the current meeting.

The so-called “equity index ranking” is published monthly by Deutsche Börse, containing all relevant data in respect of the key criteria order book turnover and market capitalization. This publication also serves the Committee as a basis for decision-making at its quarterly meetings. It is produced at the beginning of each month and published via the Internet.

Free Float

For the determination of the free float portion used to weight a company’s class of shares in the DAX Indices and for the ranking lists, the following definition applies:

1. All shareholdings of an owner which, on an accumulated basis, account for at least 5% of a company’s share capital attributed to a class of shares are considered to be non-free float. Shareholdings of an owner also include shareholdings:

US-7

| · | held by the family of the owner as defined by section §15a of the German Securities Trading Act (“WpHG”); |

| · | for which a pooling has been arranged in which the owner has an interest; |

| · | managed or kept in safe custody by a third party for account of the owner; and |

| · | held by a company which the owner controls as defined by section 22(3) of the WpHG. |

2. The definition of “non-free float”—irrespective of the size of a shareholding—covers any shareholding of an owner that is subject to a statutory or contractual qualifying period of at least six months with regard to its disposal by the owner. This applies only during the qualifying period. Shareholdings as defined by No. 1 above are counted as shareholdings for the calculation according to No. 1. Shares held by the issuing company (treasury shares) are always considered as block holdings and are not part of the free float of the share class.

3. As long as the size of such a shareholding does not exceed 25% of a company’s share capital, the definition of free float includes all shareholdings held by:

| · | asset managers and trust companies; |

| · | funds and pension funds; and |

| · | investment companies or foreign investment companies in their respective special fund assets |

with the purpose of pursuing short-term investment strategies. Such shares, for which the acquirer has at the time of purchase clearly and publicly stated that strategic goals are being pursued and that the intention is to actively influence the company policies and ongoing business of the company, are not considered as such a short-term investment. In addition, shares having been acquired through a public purchase offer are not considered as short-term investment. This does not apply to shareholdings managed or held in safe custody according to No. 1, or to venture capital companies, or other assets serving similar purposes. The shareholdings as defined by No. 1 above are not counted as shareholdings for the calculation according to No. 1.

4. In the case of an ongoing takeover, shares that are under the control of the overtaking companies via derivatives will also be considered for the determination of the stock’s free float. The derivatives need to be subject to registration according to legislation in WpHG and the German Securities Acquisition and Takeover Act (“WpÜG”).

The various criteria in Nos. 1 to 4 are also fully applied to classes of shares that are subject to restrictions of ownership.

Index Composition

Selection Criteria

To be included or to remain in the DAX Indices, companies have to satisfy certain prerequisites. All classes of the company’s shares must:

| · | be listed in the Prime Standard Segment on the Frankfurt Stock Exchange; |

| · | be traded continuously on Deutsche Börse’s electronic trading system Xetra®; |

| · | show a free float portion of at least 10%; |

| · | have their legal headquarters or operating headquarters in Germany; and |

| · | for inclusion in the MDAX, belong to a sector or subsector that is assigned to the “Classic” (i.e., non-technology) area. |

Companies that are first listed at Xetra® have additionally to be listed for a minimum of at least 30 trading days.

US-8

If, for any company, more than one class of shares fulfills the above criteria, only the respective larger or more liquid class can be included in the DAX Indices. Moreover, companies must either:

| · | have a registered office in Germany or their operating headquarters in Germany; or |

| · | have their focus of trading volume on Xetra® and their legal headquarters in the European Union or in a European Free Trade Association country (“EFTA”). |

Operating headquarters is defined as the location of management or company administration, in part or in full. If a company has its operating headquarters in Germany, but not its registered office, this must be publicly identified by the company. The major trading turnover requirement is met if at least 33% of aggregate turnover inside the EU/EFTA over the past twelve months took place on the Frankfurt Stock Exchange, including Xetra®.

To preserve the character of the DAX Indices, the Board reserves the right to exclude certain companies from the DAX Indices in coordination with the Committee. One possible reason for such an exclusion could be that the applicable company is a foreign holding company with headquarters in Germany, but a clear focus on business activities abroad.

For companies already part of the DAX Indices, the above paragraph does not apply.

Companies that satisfied the prerequisites listed above are selected for inclusion in the DAX Indices according to the following two key criteria:

| · | order book turnover on Xetra® and in Frankfurt floor trading (within the preceding twelve months); and |

| · | free float market capitalization (determined using the average of the volume-weighted average price (“VWAP”) of the last 20 trading days prior to the last day of the month) on the last trading day of each month. |

In addition, for the MDAX, the following factors influence the decision-making process:

| · | the free float; |

| · | market availability (measured on the basis of trading volumes, frequency of price determination, exchange turnover or the Xetra® Liquidity Measure); |

| · | sector affiliation; and |

| · | the period during which a company has met the criteria for inclusion in, or elimination from, the MDAX (retroactive view). |

Taking these criteria into account, the Committee submits proposals to the Board to leave the current composition of the DAX Indices unchanged or to effect changes. The final decision as to whether or not to replace an index component issue is taken by the Board. In the case of the DAX, such decisions will be directly reflected by the respective rankings.

Adjustments to Index Composition

The index composition of the DAX Indices is reviewed quarterly based on the Fast Exit and Fast Entry rules. The index composition of the DAX is reviewed every September based on the Regular Exit and Regular Entry rules, while the index composition of the MDAX is reviewed semiannually based on the Regular Exit and Regular Entry rules.

The purpose of the review on the basis of the Fast Exit and Fast Entry rules is to account for significant changes in rankings. These changes may occur when companies no longer possess the required size (free float market capitalization) or liquidity (order book volume), which may arise due to large issues (e.g., major changes in the free float or a steep price drop) and should be taken into consideration promptly in the index.

The “Overview of rules” table shows when and how the rules detailed below apply.

US-9

Overview of rules

FF MCap: free float market capitalization

OB volume: Order book volume

| DAX | Candidate rank FF MCap/OB volume | Alternate candidate rank FF MCap/OB volume | Mar | Jun | Sep | Dec |

| Fast Exit | 45/45 | 35/35; 35/40; 35/45 | X | X | X | X |

| Fast Entry | 25/25 | 35/35 | X | X | X | X |

| Regular Exit | 40/40 | 35/35 | X | |||

| Regular Entry | 30/30 | 35/35 | X | |||

| MDAX | Candidate rank FF MCap/OB volume | Alternate candidate rank FF MCap/OB volume | Mar | Jun | Sep | Dec |

| Fast Exit | 65/65 | 55/55; 55/60; 55/65 | X | X | X | X |

| Fast Entry | 45/45 | 55/55 | X | X | X | X |

| Regular Exit | 60/60 | 55/55 | X | X | ||

| Regular Entry | 50/50 | 55/55 | X | X |

The selection of companies in the DAX Indices is based on the quantitative criteria of free float market capitalization and order book volume. The currently valid ranking list always forms the basis for the application of the rules outlined below. The four rules are applied successively.

1. Fast Exit: A company in the index is replaced if it has a worse rank than the “candidate rank” in one of the two criteria of free float market capitalization or order book volume (see the “Overview of rules” table; for example, greater than 45 in free float market capitalization criterion or greater than 45 in the order book volume criterion in the DAX ranks). It is replaced by the company with the highest free float market capitalization that has the corresponding ranking positions for both criteria in the “alternate candidate rank” stated in the “Overview of rules” table for the respective DAX Index (e.g., less than or equal to 35 in the DAX ranks). If there are no companies that meet these conditions, the successor is determined by relaxing the order book volume criterion twice gradually, each time by five ranks (e.g., 35/40, then 35/45 in the DAX ranks). If there is still no company that meets the criteria, the company with the highest free float market capitalization is determined as the successor.

2. Fast Entry: A company is included in the index if it has the same or better rank than the candidate rank in both the free float market capitalization and order book volume criteria (e.g., less than or equal to rank 25 for the free float market capitalization criterion and less than or equal to rank 25 in the order book volume criterion in the DAX ranks). The company with the lowest free float market capitalization that is ranked worse than the alternate candidate rank in one of the criteria is excluded (e.g., greater than 35 in one of the two criteria in the DAX ranks). If there are no companies in the index that meet these criteria, the company with the lowest free float market capitalization is removed from the index.

3. Regular Exit: A company in the index may be replaced if it has a worse rank than the candidate rank in one of the two criteria of free float market capitalization or order book volume (for example, greater than 40 in the free float market capitalization criterion or greater than 40 in the order book volume criterion in the DAX ranks). It may be replaced by the company with the highest free float market capitalization that has the corresponding ranking positions for both criteria in the alternate candidate rank stated in the “Overview of rules” table for the respective index (e.g., less than or equal to 35 in the DAX ranks). If no successor can be determined, no change takes place.

4. Regular Entry: A company may be included in the index if it has the same or better rank than the candidate rank in both the free float market capitalization and order book volume criteria (e.g., less than or equal to rank 30 for the free float market capitalization criterion and less than or equal to rank 30 in the order book volume criterion in the DAX ranks). The company with the lowest free float market capitalization that is ranked worse than the alternate candidate rank in one of the criteria may be excluded (e.g., greater than 35 in one of the two criteria in the DAX ranks). If no alternate candidate can be determined, no exchange takes place.

In principle, the following applies to all four rules: if there are several companies that fulfill the criteria, the best/worst candidate in terms of free float market capitalization is included/replaced.

US-10

In exceptional cases, for example, takeovers announced at short notice or significant changes in the free float, Deutsche Börse may deviate from rules 1 – 4 mentioned above. The Committee can be consulted as an advisory council. Furthermore, Deutsche Börse may also decide to undertake a market consultation.

Actions in case of shortfalls in the DAX Indices

It may be the case that there is a shortfall in the relevant DAX Index during the index review. This may occur when a company no longer meets the basic criteria (see “Index Composition—Selection Criteria” above). An example would be a company publicly announcing the discontinuation of the Prime Standard listing. Remaining in the relevant DAX Index is therefore no longer justified; however, this will only take effect in the next regular review. In this case, the company would be removed during the regular review before the application of the four rules above. Consequently there would be a shortfall in the relevant DAX Index.

If there is a shortfall during the regular review before the four rules of the DAX Indices are applied, a check is performed to see whether there is a relegation candidate from a superior index (e.g., a shortfall may occur in the MDAX due to an exit from DAX and the simultaneous promotion of an MDAX company). In this case, a review using the Regular Exit rule for the respective DAX Index will be performed for the exit candidate, reviewing the eligibility for acceptance into the subordinate DAX Index.

a. If the company meets the Regular Exit rule, the relegation candidate is directly accepted into the relevant DAX Index in which the shortfall occurred.

b. If the Regular Exit rule is not met, the relegation candidate is not accepted directly into the relevant DAX Index with the shortfall.

c. If there are no other relegation candidates and a shortfall continues to exist in the relevant DAX Index, this shortfall in the relevant DAX Index is treated as a Fast Exit. Consequently, the Fast Exit rule of the respective DAX Index with the shortfall is applied. In this case, the company which caused the shortfall is considered the Fast Exit candidate. A company that in turn could be accepted into the relevant DAX Index with the shortfall is found using the Fast Exit rule.

There is still a possibility for a shortfall in the relevant DAX Index. This may occur when a company that so far had not been included in a DAX Index as it failed to meet the base criteria (see “Index Composition—Selection Criteria” above) qualifies for the new index composition and replaces a company. An example of this would be if a company has only recently been listed (IPO). If two companies are exchanged and the example above or a similar situation applies, this may lead to a surplus in the subordinate DAX Index. If, for example, a recently listed company qualifies directly for the DAX, the replaced company could be included into the MDAX and cause a surplus there.

If a company changes from a DAX Index into a subordinate DAX Index without a security from the subordinated DAX Index being promoted at the same time, this may lead to a surplus of companies (e.g., a recently listed company is promoted to the DAX following the regular review. At first the composition of the DAX is finalized. As soon as the review of the DAX is complete, the review of the exchanged candidate for acceptance into the MDAX is carried out using the Regular Exit rule). In this case, a check using the Regular Exit rule for the respective DAX Index is performed for the exit candidate, reviewing the eligibility for acceptance into the subordinated DAX Index.

a. If the company does not violate the Regular Exit rule, the relegation candidate is directly accepted into the subordinated DAX Index.

b. If the Regular Exit rule is not met, the relegation candidate is not accepted directly into the subordinated DAX Index with the shortfall.

c. If there are no other relegation candidates and there is still a shortfall in the relevant DAX Index, this surplus is treated as a Fast Entry. Consequently, the Fast Entry rule of the respective DAX Index is applied. In this case, the company that caused the surplus is considered as the Fast Entry candidate. A company that, in turn, could be removed from the relevant DAX Index with the surplus is found using the Fast Entry rule.

US-11

The relevant DAX Index is restored to the fixed number of companies before the four rules for the relevant DAX Index are applied (Fast Exit, Fast Entry, Regular Exit and Regular Entry). The aim of this is to ensure that the relevant DAX Index contains the designated number of companies before the review of the index is performed.

Extraordinary Index Review

Extraordinary adjustments to the index composition have to be performed, regardless of the “fast-exit” or “fast-entry” rules, upon occurrence of specific events, such as insolvency. In addition, a company can be removed immediately if its index weight based on the actual market capitalization exceeds 10% and its annualized 30-day volatility exceeds 250%. The relevant figures are published by Deutsche Börse on a daily basis. The Board, in agreement with the Committee, may decide on the removal and may replace the company two full trading days after the announcement.

Adjustments are also necessary in two scenarios in the mergers and acquisitions context:

| · | if an absorbing or emerging company meets basis criteria for inclusion in the applicable DAX Index, as soon as the free float of the absorbed company falls below 10%, the company is removed from the applicable DAX Index under the ordinary or extraordinary adjustments described above. The absorbed company is replaced by the absorbing or emerging company on the same date; and |

| · | if an absorbing company is already included in the applicable DAX Index or does not meet the basis criteria for inclusion in the applicable DAX Index, as soon as the free float of the absorbed company falls below 10%, the company is removed from the applicable DAX Index under the ordinary or extraordinary adjustments described above. On the same date, the absorbed company is replaced by a new company determined by the Fast Exit Rule (for the DAX) or after recommendation of the Committee (for the MDAX). |

The weight of the company represented in the applicable DAX Index is adjusted to the new number of shares on the quarterly date after the merger has taken place.

Index Calculation

The DAX Indices are weighted by market capitalization; however, only freely available and tradable shares (“free float”) are taken into account. The DAX Indices are performance (i.e., total return) indices, which reinvests all income from dividend and bonus payments in the applicable DAX Index portfolio.

The DAX Indices Formula

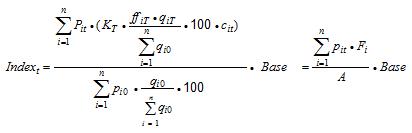

The DAX Indices are conceived according to the Laspeyres formula set out below:

whereby:

| cit | = | Adjustment factor of company i at time t |

| ffiT | = | Free float factor of share class i at time T |

| n | = | Number of shares in the applicable DAX Index |

| pi0 | = | Closing price of share i on the trading day before the first inclusion in the applicable DAX Index |

| piT | = | Price of share i at time t |

| qi0 | = | Number of shares of company i on the trading day before the first inclusion in the applicable DAX Index |

| qiT | = | Number of shares of company i at time T |

| t | = | Calculation time of the applicable DAX Index |

US-12

| KT | = | Applicable DAX Index chaining factor valid as of chaining date T |

| T | = | Date of the last chaining |

The formula set out below is equivalent in analytic terms, but designed to achieve relative weighting:

Index calculation can be reproduced in simplified terms by using the expression Fi:

| · | multiply the current price by the respective Fi weighting factor; |

| · | take the sum of these products; and |

| · | divide this by the base value (A) which remains constant until a modification in the applicable DAX Index composition occurs. |

The Fi factors provide information on the number of shares required from each company to track the underlying Index portfolio.

Calculation Frequency

Index calculation is performed on every exchange trading day in Frankfurt, using prices traded on Deutsche Börse’s electronic trading system Xetra®, whereby the last determined prices are used. The DAX Indices are calculated continuously once a second. The DAX is distributed as soon as current prices are available for all 30 index components included in the DAX (but no later than 9:06 a.m.). As long as opening prices for individual shares are not available, the particular closing prices of the previous day are taken instead for calculating the indices.

In the event of a suspension during trading hours, the last price determined before such a suspension is used for all subsequent computations. If such suspension occurs before the start of trading, the closing price of the previous day is taken instead. The “official” closing index level is calculated using the respective closing prices (or last prices) established on Xetra®.

Adjustments

The DAX Indices are adjusted for exogenous influences (e.g., price-relevant capital changes) by means of certain correction factors, assuming a reinvestment according to the “opération blanche.” If the absolute amount of the accumulated distributions (dividends, bonus and special distributions, spin-offs or subscription rights on other security classes) between two regular chaining dates accounts for more than 10% of the market capitalization of the

US-13

distributing company on the day before the first distribution, the part of the distribution exceeding the 10% will not be reinvested in a single stock but in the overall index portfolio per unscheduled chaining date.

Licensing Agreement with Deutsche Börse

The DAX Indices are a registered trademark of Deutsche Börse. The securities are neither sponsored nor promoted, distributed or in any other manner supported by Deutsche Börse (the “licensor”). Neither the publication of the DAX Indices by the licensor nor the granting of a license regarding the DAX Indices as well as the DAX and MDAX trademarks for the utilization in connection with the securities or other securities or financial products that are derived from the DAX Indices, represents a recommendation by the licensor for a capital investment or contains in any manner a warranty or opinion by the licensor with respect to the attractiveness on an investment in the securities.

The FTSE Russell Indices

The FTSE 100 Index, the FTSE China 50™ Index and the Russell 2000® Index (together, the “FTSE Russell Indices”) are maintained by FTSE Russell. Since 2015, “FTSE Russell” is a trading name of FTSE International Limited, Frank Russell Company, and FTSE TMX Global Debt Capital Markets Limited and its subsidiaries (including MTSNext Limited).

The FTSE 100 Index

The FTSE 100 Index is a free float-adjusted index that measures the composite price performance of stocks of the largest 100 blue-chip companies (determined on the basis of market capitalization) traded on the London Stock Exchange PLC (“LSE”). The 100 stocks included in the FTSE 100 Index (the “FTSE Underlying Stocks”) were selected from a reference group of stocks trading on the LSE which were selected by excluding certain stocks that have low liquidity based on public float, accuracy and reliability of prices, size and number of trading days. The FTSE Underlying Stocks were selected from this reference group by selecting 100 stocks with the largest market value. A list of the issuers of the FTSE Underlying Stocks is available from FTSE International Limited (“FTSE”), a company owned equally by the LSE and the Financial Times Limited (the “FT”). The FTSE 100 Index is reported by Bloomberg under the ticker symbol “UKX.”

The FTSE 100 Index was first calculated on January 3, 1984 with an initial base level index value of 1,000 points. Publication of the FTSE 100 Index began in February 1984. The FTSE 100 Index is calculated on systems managed by Reuters. Prices and FX rates used are supplied by Reuters. The FTSE 100 Index is calculated, published and disseminated by FTSE, and calculated in association with the Institute and Faculty of Actuaries.

Security Inclusion Criteria

Companies that are large enough to be constituents of the FTSE 100 Index but do not pass the liquidity test are excluded.

Where there are multiple lines of equity capital in a company, all are included and priced separately, provided that the secondary line’s full market capitalization (i.e., before the application of any investability weightings) is greater than 25% of the full market capitalization of the company’s principal line and the secondary line satisfies the eligibility rules and screens in its own right in all respects.

Companies are required to have greater than 5% of the company’s voting rights (aggregated across all of its equity securities, including, where identifiable, those that are not listed or trading) in the hands of unrestricted shareholders or they will be deemed ineligible for index inclusion. Existing constituents who do not currently meet this requirement have a five-year grandfathering period to comply.

At the next annual review, the companies are retested against all eligibility screens.

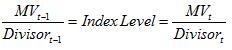

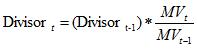

Calculation of the FTSE 100 Index

The FTSE 100 Index level is the summation of the free float-adjusted market values (or capitalizations) of all companies within the FTSE 100 Index divided by the divisor. The price movement of a larger company (say,

US-14

representing 5% of the value of the FTSE 100 Index) will therefore have a larger effect on the FTSE 100 Index than a smaller company (say, representing 1% of the value of the FTSE 100 Index).

The FTSE 100 Index is reviewed quarterly by the FTSE Russell Europe, Middle East & Africa Regional Equity Advisory Committee (the “Regional Committee”) in order to maintain continuity in the level. Changes to the constituents can be prompted by new listings on the exchange, corporate actions (e.g., mergers and acquisitions) or an increase or decrease in a market capitalization. The Regional Committee undertakes the reviews of the FTSE 100 Index and ensures that constituent changes and index calculations are made in accordance with the ground rules of the FTSE 100 Index. The meetings to review the constituents are held on a quarterly basis in March, June, September and December. Each review is based on data from the close of business on the Tuesday before the first Friday of the review month. Any constituent changes are implemented after the close of business on the third Friday of the review month (i.e., effective Monday), following the expiry of the ICE Futures Europe futures and options contracts.

The FTSE Underlying Stocks may be replaced, if necessary, in accordance with deletion/addition rules which provide generally for the removal and replacement of a stock from the FTSE 100 Index if such stock is delisted or its issuer is subject to a takeover offer that has been declared unconditional or it has ceased, in the opinion of the Regional Committee, to be a viable component of the FTSE 100 Index. To maintain continuity, a stock will be added at the quarterly review if it has risen to 90th place or above and a stock will be deleted if at the quarterly review it has fallen to 111th place or below, in each case ranked on the basis of market capitalization. A constant number of constituents will be maintained for the FTSE 100 Index. Where a greater number of companies qualify to be interested in the FTSE 100 Index than those qualifying to be deleted, the lowest-ranking constituents presently included in the FTSE 100 Index will be deleted to ensure that an equal number of companies are inserted and deleted at the periodic review. Likewise, where a greater number of companies qualify to be deleted than those qualifying to be inserted, the securities of the highest-ranking companies which are presently not included in the index will be inserted to match the number of companies being deleted at the periodic review.

For more information on the FTSE 100 Index, see “Methodology of the FTSE Russell Indices” below.

License Agreement with FTSE

We have entered into an agreement with FTSE providing us and certain of our affiliates or subsidiaries with a non-exclusive license and, for a fee, with the right to use the FTSE 100 Index, which is owned and published by the FTSE, in connection with certain securities, including the securities.

All rights to the FTSE 100 Index are owned by the FTSE, the publisher of the FTSE 100 Index. None of the LSE, the Financial Times and FTSE has any relationship to Credit Suisse or the securities. None of the LSE, the Financial Times and the FTSE sponsors, endorses, authorizes, sells or promotes the securities, or has any obligation or liability in connection with the administration, marketing or trading of the securities.

The securities are not in any way sponsored, endorsed, sold or promoted by FTSE or by the LSE or by the FT and none of FTSE, the LSE or FT makes any warranty or representation whatsoever, expressly or impliedly, either as to the results to be obtained from the use of the FTSE 100 Index and/or the figure at which the FTSE 100 Index stands at any particular time on any particular day or otherwise. The FTSE 100 Index is compiled and calculated solely by FTSE. However, none of FTSE, the LSE or FT shall be liable (whether in negligence or otherwise) to any person for any error in the FTSE 100 Index and none of FTSE, the LSE or FT shall be under any obligation to advise any person of any error therein.

“FTSE™” and “Footsie™” are trademarks of LSE and FT and are used by FTSE under license.

The FTSE China 50™ Index

The FTSE China 50™ Index (the “FTSE China 50 Index”) is a stock index calculated, published and disseminated by FTSE Index Limited (“FXI”), a joint venture of FTSE Russell and Xinhua Financial Network Limited (“Xinhua”), and is designed to represent the performance of the mainland Chinese market that is available to international investors and comprises 50 of the largest and most liquid Chinese stocks (H Shares, Red Chips and P Chips) listed and traded on the Stock Exchange of Hong Kong (“SEHK”).

US-15

The FTSE China 50 Index is calculated and published in Hong Kong and U.S. dollars. “H” shares are securities of companies incorporated in the People’s Republic of China and nominated by the Chinese government for listing and trading on the SEHK. “Red Chip” shares are securities of companies incorporated outside of the People’s Republic of China, which are substantially owned, directly or indirectly, by Chinese state-owned enterprises and have the majority of their revenue or assets derived from mainland China. “P Chip” companies are incorporated outside the People’s Republic of China, which are controlled by mainland China individuals, with the establishment and origin of the company in mainland China and the majority of their revenue or assets derived from mainland China. FTSE Index Limited has no obligation to continue to publish, and may discontinue publication of, the FTSE China 50 Index. The FTSE China 50 Index is reported by Bloomberg under the ticker symbol “XIN0I.”

Methodology of the FTSE China 50 Index

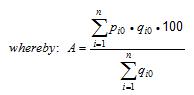

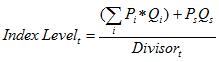

The FTSE China 50 Index is calculated using the free float index calculation methodology of FTSE Russell. The FTSE China 50 Index is calculated using the following algorithm:

where:

| (i) | is 1, 2, … , N; |

| (N) | is the number of securities in the FTSE China 50 Index; |

| (p) | is the latest trade price of the component security (or the price at the close of the FTSE China 50 Index on the previous day); |

| (e) | is the exchange rate required to convert the security’s currency into the FTSE China 50 Index’s base currency; |

| (s) | is the number of shares in issue used by the FTSE China 50 Index for the security; |

| (f) | is the investability weighting, a factor to be applied to each security to allow amendments to its weighting, expressed as a number between 0 and 1, where 1 represents a 100% free float. The investability weighting for each security is published by FTSE; |

| (c) | is the capping factor to be applied to a security to correctly weight that security in the FTSE China 50 Index. The factor maps the investable market capitalization of each stock to a notional market capitalization for inclusion in the FTSE China 50 Index; |

| (d) | is the divisor, a figure that represents the total issued share capital of the FTSE China 50 Index at the base date, which can be adjusted to allow changes in the issued share capital of individual securities to be made without distorting the FTSE China 50 Index. |

The FTSE China 50 Index uses actual trade prices for securities with local stock exchange quotations and Reuters real-time spot currency rates for its calculations.

Free float is calculated using available published information rounded to 12 decimal places. Companies with a free float of 5% or below are excluded from the FTSE China 50 Index. Following the application of an initial free float restriction, a constituent’s free float will only be changed if its rounded free float moves to more than 3 percentage points above or below the existing rounded free float. Where a company’s actual free float moves to above 99%, it will not be subject to the 3 percentage point threshold and will be rounded to 100%. A constituent with a free float of 15% or below will not be subject to the 3 percentage point threshold. Foreign ownership limits, if any, are applied after calculating the free float restriction. If the foreign ownership limit is more restrictive than the free float restriction, the precise foreign ownership limit is applied. If the foreign ownership limit is less restrictive or equal to the free float restriction, the free float restriction is applied.

The FTSE China 50 Index is periodically reviewed for changes in free float. These reviews coincide with the quarterly reviews undertaken of the FTSE China 50 Index. The constituents will be reviewed using data from the

US-16

close of business on the Monday following the third Friday in February, May, August and November. Where there is a market holiday in either China or Hong Kong on the Monday following the third Friday, the close of business on the last trading day prior to the Monday after the third Friday, where both markets are open, will be used. Implementation of any changes takes place after the close of the index calculation on the third Friday in March, June, September and December. A stock’s free float is also reviewed and adjusted if necessary following certain corporate events. If the corporate event includes a corporate action which affects the FTSE China 50 Index, any change in free float is implemented at the same time as the corporate action.

Securities must be sufficiently liquid to be traded. The following criteria, among others, are used to ensure that illiquid securities are excluded:

| · | Price. FXI must be satisfied that an accurate and reliable price exists for the purposes of determining the market value of a company. FXI may exclude a security from the FTSE China 50 Index if it considers that an “accurate and reliable” price is not available. |

| · | Liquidity. Securities in the FTSE China 50 Index will be reviewed semiannually for liquidity in March and September. Securities which do not turn over at least 0.05% of their shares in issue, after the application of any free float restrictions and based on their median daily trading volume per month for ten of the twelve months prior to the quarterly review will not be eligible for inclusion in the FTSE China 50 Index. An existing constituent failing to turn over at least 0.04% of its shares in issue, after the application of any free float restrictions and based on its median daily trading volume per month for more than eight of the twelve months prior to the quarterly review, will be removed after close of the index calculation on the next trading day following the third Friday in January, April, July and October. Any period when a share is suspended will be excluded from the calculation. |

| · | New Issues. New issues must have a minimum trading record of at least three months prior to the date of the review and turnover of a minimum of 0.05% of their shares in issue, after the application of any free float restrictions and based on the median daily trading volume each month, on a pro rata basis, except in certain circumstances. When testing liquidity, the free float weight as at the last date in the testing period will be used for the calculation for the whole of that period. |

| · | The FTSE China 50 Index, like other indices of FXI, is governed by an independent advisory committee that ensures that the FTSE China 50 Index is operated in accordance with its published ground rules, and that the rules remain relevant to the FTSE China 50 Index. |

Changes to Constituent Weightings

Changes in Free Float. The FTSE China 50 Index will be reviewed quarterly for changes in free float. Implementation of any changes will happen at close of trading on the third Friday in March, June, September and December. A constituent’s free float will also be reviewed and adjusted if necessary:

| · | by identifying information which necessitates a change in free float weighting; |

| · | following a corporate event; or |

| · | expiry of a lock-in clause. |

If a corporate event includes a corporate action which affects the FTSE China 50 Index, any change in free float will be implemented at the same time as the corporate action.

New Issues. Where an eligible non-constituent of the FTSE China 50 Index undertakes an Initial Public Offering of a new equity security, that security will be eligible for fast entry inclusion to the FTSE China 50 Index providing it meets the following conditions: (a) if it is a Fast Entry into the FTSE All-World Index and (b) if its full market capitalization (shares in issue * price) when ranked in descending order is in 20th position or higher. The full market capitalization will be based on the closing price on the first day of trading and the security’s inclusion will be implemented after the close of business on the fifth day of trading. Where a fast entrant is added to the FTSE China 50 Index the lowest ranking constituent by full market capitalization of the FTSE China 50 Index will be selected for removal using the closing prices on the first day of trading and implemented after the close of business on the fifth day of trading. In the event of the fifth day of trading being

US-17

in close proximity to an index review, FTSE Russell may use its discretion to include a fast entrant at the index review date following advance notice. Following the announcement of a Fast Entry constituent, the FTSE China 50 Index is capped using prices adjusted for corporate events as at the close of business on the fourth day of official trading based on the constituents, shares in issue and free float on the next trading day following the fifth day of official trading. Newly issued securities which do not qualify for early entry will be eligible for inclusion at the next quarterly review, if large enough to become a constituent of the FTSE China 50 Index at that time. The security may also qualify for inclusion in the FTSE China 50 Index Reserve List. If FTSE Russell decides to include a new security as a constituent security other than as part of the normal periodic review procedure, this decision will be publicly announced at the earliest practicable time.

Suspended Companies. Where the company is removed from the FTSE China 50 Index it will be replaced with the highest-ranking company, by full market capitalization, on the Reserve List eligible to be included in the index as at the close of the index calculation on the day preceding the inclusion of the replacement company. This change will be effected after the close of the index calculation and prior to the start of the index calculation on the following day.

For more information on the FTSE China 50 Index, see “Methodology of the FTSE Russell Indices” below.

License Agreement with FTSE Index Limited

The securities are not in any way sponsored, endorsed, sold or promoted by FXI, FTSE Russell or Xinhua or by the LSE or by FT and neither FXI, FTSE Russell, Xinhua nor the LSE nor FT makes any warranty or representation whatsoever, expressly or impliedly, either as to the results to be obtained from the use of the FTSE China 50 Index and/or the figure at which the FTSE China 50 Index stands at any particular time on any particular day or otherwise. The FTSE China 50 Index is compiled and calculated by or on behalf of FXI. However, neither FXI or FTSE Russell or Xinhua or the LSE or FT shall be liable (whether in negligence or otherwise) to any person for any error in the FTSE China 50 Index and neither FXI, FTSE Russell, Xinhua or the LSE or FT shall be under any obligation to advise any person of any error therein.

The FTSE China 50 Index is calculated by or on behalf of FXI. FXI does not sponsor, endorse or promote the securities.

All copyright in the FTSE China 50 Index values and constituent list vest in FXI. Credit Suisse has obtained full license from FXI to use such copyright in connection with the securities.

“FTSE™” is a trademark jointly owned by LSE and FT. “FTSE” is a trademark of FTSE Russell. “Xinhua” is a service mark and trademark of Xinhua Financial Network Limited. All marks are licensed for use by FXI.

The Russell 2000® Index

The Russell 2000® Index is intended to track the performance of the small-cap segment of the U.S. equity market. The Russell 2000® Index is reconstituted annually and eligible initial public offerings (“IPOs”) are added to the Russell 2000® Index quarterly. The Russell 2000® Index is a subset of the Russell 3000E Index, which contains the largest 4,000 companies incorporated in the U.S. and its territories and represents approximately 99% of the U.S. equity market. The Russell 2000® Index measures the composite price performance of stocks of approximately 2,000 U.S. companies ranked from 1,001 to 3,000 (based on descending total market capitalization) within the Russell 3000E Index members. As of November 30, 2017, the largest five sectors represented by the Russell 2000® Index were Financial Services, Health Care, Producer Durables, Technology, and Consumer Discretionary. Real-time dissemination of the value of the Russell 2000® Index by Reuters began on December 31, 1986. The Russell 2000® Index was developed by Russell Investments and is calculated, maintained and published by FTSE Russell. The Russell 2000® Index is reported by Bloomberg under ticker symbol “RTY.”

Methodology for the Russell U.S. Indices

Companies which FTSE Russell assigns to the U.S. equity market are included in the Russell U.S. indices. If a company incorporates, has a stated headquarters location, and also trades in the same country (ADRs and ADSs are not eligible), the company is assigned to the equity market of its country of incorporation. If any of the three do not match, FTSE Russell then defines three Home Country Indicators (“HCI”): (a) country of Incorporation, (b) country of Headquarters, and (c) country of the most liquid exchange as defined by two-year average daily dollar trading

US-18