Filed Pursuant to Rule 433

Registration Statement Number 333-180300-03

Fact Sheet (J443)

March 3, 2015

Credit Suisse – Dual Directional Capped Knock-Out Notes due September 14, 2016 Linked to the

Performance of the S&P 500® Index

(continued on the next page)

J.P. Morgan

Placement Agent

* Credit Suisse may act through its Nassau Branch or its London Branch.

** In the event that the closing level of the Underlying is not available on the Pricing Date, the Initial Level will be determined on the immediately following trading day on which a closing level is available.

† Subject to postponement as described in the applicable pricing supplement and product supplement.

Product Risks (continued)

|

|

·

|

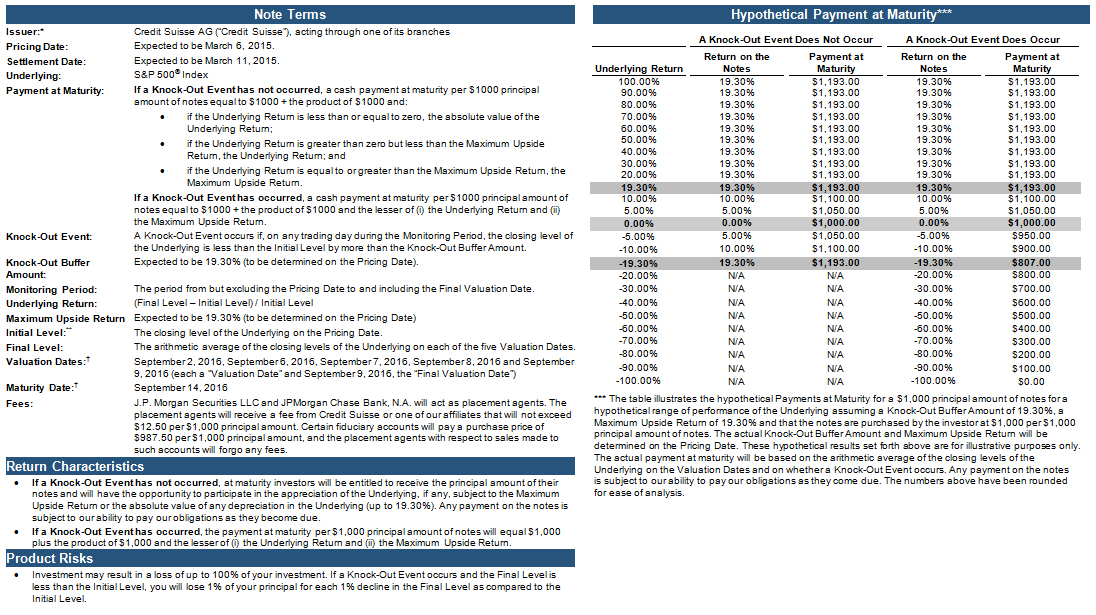

Regardless of whether a Knock-Out Event occurs, if the Final Level is greater than the Initial Level, for each $1,000 principal amount of notes, you will receive at maturity $1,000 plus an additional return that will not exceed a predetermined percentage of the principal amount, regardless of the appreciation of in the Underlying, which may be significant. We refer to this predetermined percentage as the Maximum Upside Return, which will be set on the Pricing Date and will not be less than 19.30%*. Accordingly, if the Underlying Return is greater than zero, the maximum amount payable at maturity is expected to be $1,193 per $1,000 principal amount of notes. Additionally, if a Knock-Out Event has not occurred and the Final Level is less than the Initial Level, you will receive at maturity $1,000 plus an additional return equal to the absolute value of the Underlying Return, up to 19.30%*. Because a Knock-Out Event will occur if the closing level of the Underlying is less than the Initial Level by more than the Knock-Out Buffer Amount of 19.30%* on any trading day during the Monitoring Period, the maximum amount payable on the notes is expected to be $1,193 per $1,000 principal amount of notes (to be determined on the Pricing Date).

|

* The actual Maximum Upside Return on the notes and the actual Knock-Out Buffer Amount will be set on the Pricing Date and will not be less than 19.30% and 19.30%, respectively.

|

|

·

|

The notes do not pay interest.

|

|

|

·

|

Although the return on the notes will be based on the performance of the Underlying, the payment of any amount due on the notes is subject to the credit risk of Credit Suisse. Investors are dependent on our ability to pay all amounts due on the notes and, therefore, investors are subject to our credit risk.

|

|

|

·

|

Your investment in the notes may not perform as well as an investment in an instrument that measures the point-to-point performance of the Underlying from the Pricing Date to the Final Valuation Date. Your ability to participate in the appreciation of the Underlying, if any, may be limited by the 5-day-end-of-term averaging used to calculate the Final Level, especially if there is a significant increase in the closing level of the Underlying on the Final Valuation Date. Accordingly, you may not receive the benefit of the full appreciation of the Underlying, if any, between the Pricing Date and the Final Valuation Date.

|

|

|

·

|

The original issue price of the notes includes the agent’s commission and the cost of hedging our obligations under the notes through one or more of our affiliates. As a result, the price, if any, at which Credit Suisse (or its affiliates), will be willing to purchase notes from you in secondary market transactions, if at all, will likely be lower than the original issue price, and any sale prior to the Maturity Date could result in a substantial loss to you. You should be willing and able to hold your notes to maturity.

|

|

|

·

|

As a holder of the notes, you will not have voting rights or rights to receive cash dividends or other distributions or other rights with respect to the equity securities included in the Underlying.

|

|

|

·

|

If the closing level of the Underlying on any trading day during the Monitoring Period is less than the Initial Level by more than the Knock-Out Buffer Amount of 19.30%*, you will not be entitled to receive the absolute value of the Underlying Return on the notes and you will be fully exposed at maturity to any depreciation in the Underlying. We refer to this as a contingent buffer. Under these circumstances, if the Final Level is less than the Initial Level, you will lose 1% of the principal amount of your investment for every 1% decrease in the Final Level as compared to the Initial Level. You will be subject to this potential loss of principal even if the closing level of the Underlying subsequently increases such that the Final Level of the Underlying is less than the Initial Level by not more than the Knock-Out Buffer Amount, or is equal to or greater than the Initial Level. If these notes had a non-contingent buffer feature, under the same scenario, you would have received the full principal amount of your notes plus a return equal to the absolute value of the Underlying Return if the Final Level is less than the Initial Level by up to the Knock-Out Buffer Amount of 19.30%*. As a result, your investment in the notes may not perform as well as an investment in a security with a return that includes a non-contingent buffer.

|

* The actual Knock-Out Buffer Amount will be set on the Pricing Date and will not be less than 19.30%.

|

|

·

|

Credit Suisse currently anticipates that the value of the notes on the Pricing Date will be less than the price the investor pays for the notes, reflecting the deduction of underwriting discounts and commissions and other costs of creating and marketing the notes. Prior to maturity, costs such as concessions and hedging may affect the value of the notes.

|

|

|

·

|

The notes will not be listed on any securities exchange. Credit Suisse (or its affiliates) intends to offer to purchase the notes in the secondary market but is not required to do so. Even if there is a secondary market, it may not provide enough liquidity to allow you to trade or sell the notes when you wish to do so. Because other dealers are not likely to make a secondary market for the notes, the price at which you may be able to trade your notes is likely to depend on the price, if any, at which Credit Suisse (or its affiliates) is willing to buy the notes.

|

|

|

·

|

We and our affiliates play a variety of roles in connection with the issuance of the notes, including acting as calculation agent, hedging our obligations under the notes and determining their estimated value. In performing these duties, the economic interests of us and our affiliates are potentially adverse to your interests as an investor in the notes. Further, hedging activities may adversely affect any payment on or the value of the notes. Any profit in connection with such hedging activities will be in addition to any other compensation that we and our affiliates receive for the sale of the notes, which creates an additional incentive to sell the notes to you.

|

|

|

·

|

In addition to the closing level of the Underlying during the Monitoring Period, the value of the notes will be affected by a number of economic and market factors that may either offset or magnify each other, including whether the closing level of the Underlying has decreased, as compared to the Initial Level by more than the Knock-Out Buffer Amount, the expected volatility of the Underlying, the time to maturity of the notes, the dividend rate on the equity securities included in the Underlying, interest and yield rates in the market generally, investors’ expectations with respect to the rate of inflation, geopolitical conditions and a variety of economic, financial, political, regulatory and judicial events that affect the stocks comprising the Underlying or markets generally and which may affect the level of the Underlying, and our creditworthiness, including actual or anticipated downgrades in our credit ratings. Some or all of these factors may influence the price that you will receive if you choose to sell your notes prior to maturity. The impact of any of the factors set forth above may enhance or offset some or all of any change resulting from another factor or factors.

|

The risks set forth in the section entitled “Product Risks” above are only intended as summaries of some of the risks relating to an investment in the notes. Prior to investing in the notes, you should, in particular, review the “Product Risks” above, the “Selected Risk Considerations” section in the applicable pricing supplement and the “Risk Factors” section of the product supplement, which set forth risks relating to an investment in the notes.

You may revoke your offer to purchase the notes at any time prior to the time at which we accept such offer on the date the notes are priced. We reserve the right to change the terms of, or reject any offer to purchase the notes prior to their issuance. In the event of any changes to the terms of the notes, we will notify you and you will be asked to accept such changes in connection with your purchase. You may also choose to reject such changes in which case we may reject your offer to purchase.

Additional Information

Credit Suisse and its affiliates do not provide tax advice. Accordingly, any discussion of U.S. tax matters contained herein (including any attachments) is not intended or written to be used and cannot be used, in connection with the promotion, marketing or recommendation by anyone unaffiliated with Credit Suisse of any of the matters addressed herein or for the purpose of avoiding U.S. tax-related penalties.

This document is a summary of the terms of the notes and factors that you should consider before deciding to invest in the notes. Credit Suisse has filed a registration statement (including pricing supplement, underlying supplement, product supplement, prospectus supplement and prospectus) with the Securities and Exchange Commission, or SEC, for the offering to which this offering summary relates. Before you invest, you should read this summary together with the Preliminary Pricing Supplement dated March 3, 2015, Underlying Supplement dated July 29, 2013, Product Supplement No. JPM-I dated March 23, 2012, Prospectus Supplement dated March 23, 2012 and Prospectus dated March 23, 2012, to understand fully the terms of the notes and other considerations that are important in making a decision about investing in the notes. You may get these documents without cost by visiting EDGAR on the SEC Web site at www.sec.gov. Alternatively, Credit Suisse, any agent or any dealer participating in this offering will arrange to send you the pricing supplement, underlying supplement, product supplement, prospectus supplement and prospectus if you so request by calling toll-free 1-(800)-221-1037.

You may access the pricing supplement related to the offering summarized herein on the SEC website at:

You may access the underlying supplement, product supplement, prospectus supplement and prospectus on the SEC website at www.sec.gov or by clicking on the hyperlinks to each of the respective documents incorporated by reference in the pricing supplement.