|

Reopening Supplement 1 to Pricing Supplement No. DRN-1

To the Underlying Supplement dated May 24, 2013,

Product Supplement No. RN-I dated May 24, 2013,

Prospectus Supplement dated March 23, 2012 and

Prospectus dated March 23, 2012

|

Filed Pursuant to Rule 424(b)(2)

Registration Statement No. 333-180300-03

November 8, 2013

|

|

$5,000,000*

Daily Redeemable Notes (“DRNs”) Linked to the Performance of the S&P 500 VIX Futures Variable Long/Short Index TR – Short Term due June 4, 2018

|

||

General

|

·

|

The DRNs are designed for investors who seek exposure to the performance of the S&P 500 VIX Futures Variable Long/Short Index TR – Short Term (the “index”). Investors should be willing to forgo coupon payments and, if the index declines or does not increase sufficiently to offset the impact of fees and charges (as described below), be willing to lose up to 100% of their investment. Any payment on the DRNs is subject to our ability to pay our obligations as they become due.

|

|

·

|

The DRNs are senior medium-term notes of Credit Suisse AG, acting through its Nassau Branch, maturing June 4, 2018.**

|

|

·

|

The purpose of this Reopening Supplement 1 to Pricing Supplement DRN-1 is to offer additional DRNs with an aggregate principal amount of $5,000,000, which we refer to as the “reopened securities.” $11,676,000 aggregate principal amount of the DRNs were originally priced on June 3, 2013 (the “original issue trade date”) and issued on June 6, 2013, which we refer to as the “original securities.” The reopened securities will constitute a further issuance of, and will be consolidated with and form a single tranche with the original securities and will have the same CUSIP. Delivery of the securities in book-entry form only will be made through The Depository Trust Company (“DTC”). References to the “securities” will collectively refer to the reopened securities and the original securities.

|

|

·

|

The reopened securities priced on November 8, 2013 (the “reopening trade date”) and are expected to settle on November 14, 2013 (the “reopening settlement date”).

|

|

·

|

The denomination and stated principal amount of each DRN is $1,000. Any future issuances of the DRNs may be issued at a price that is higher or lower than the stated principal amount, based on the most recent closing indicative value of the DRNs at that time.

|

|

·

|

An investment in the DRNs involves significant risks and is not appropriate for every investor. Investing in the DRNs is not equivalent to investing directly in the index. Accordingly, the DRNs should be purchased only by knowledgeable investors who understand the terms of the investment in the DRNs and are familiar with the behavior of the index and volatility markets generally. Investors should consider potential transaction costs when evaluating an investment in the DRNs and should regularly monitor their holdings of the DRNs to ensure that they remain consistent with their investment strategies.

|

|

·

|

The DRNs are subject to early redemption at your option (subject to the applicable early redemption charge) and at our option, in each case subject to the requirements specified below and in the accompanying product supplement.

|

|

·

|

The DRNs are subject to a daily investor fee and investor fee factor specified below.

|

Key Terms

|

Issuer:

|

Credit Suisse AG (“Credit Suisse”), acting through its Nassau Branch

|

|

CUSIP/ISIN:

|

22547Q2V7/US22547Q2V77

|

|

Index:

|

The return on the DRNs will be based on the performance of the index during the term of the DRNs. The index is reported on Bloomberg under ticker symbol “SPVXVST <Index>.” The index provides a way of investing in volatility. In particular, it provides exposure to a variable volatility profile through a series of thirteen portfolios. Each portfolio is composed of a 2x long position (a “leveraged leg”) and an inverse position (an “inverse leg”) in the S&P 500 VIX Short-Term Futures™ Index ER (the “base index”), both of which rebalance daily. Once every quarter, each portfolio is rebalanced so that the leveraged leg is weighted at 1/3 of the portfolio and the inverse leg is weighted at 2/3 of the portfolio. As a result, upon each rebalancing day for a portfolio, the exposure to the base index in the leveraged leg initially offsets the exposure to the base index in the inverse leg.

The index is designed to achieve positive returns from trending decreases or increases in the prices futures contracts on the CBOE Volatility Index® (the “VIX Index”) with a constant weighted average maturity of one month. If the base index trend ups, the exposure in the leveraged position should increase and the exposure in the inverse position should decrease, resulting in a net increase in long exposure. If the base index trends down, the opposite should occur, with the result being a net increase in short exposure. This dynamic leads the net exposure to be increasing when the base index moves up and decreasing when the base index moves down. The weighted average of the performance of each portfolio’s leveraged leg and inverse leg will determine the change (which may be positive or negative) in the level of each portfolio on a given day.The weighted average of the performance of the thirteen portfolios will then determine the change (which may be positive or negative) in the level of the index on a given day. For more information on the index, see “The Index” in the accompanying underlying supplement.

|

|

Redemption Amount:

|

If your DRNs have not previously been redeemed by Credit Suisse, at maturity you will receive, for each DRN you hold, a cash payment equal to the closing indicative value of your DRNs on the final valuation date. Any payment on the DRNs is subject to our ability to pay our obligations as they become due.

|

|

Closing Indicative Value:

|

The closing indicative value for the DRNs on the reopening trade date was $969.60. The closing indicative value of the DRNs on each calendar day following the reopening trade date will be equal to (1)(a) the closing indicative value on the calendar day immediately preceding such calendar day times (b) the daily index factor on such calendar day minus (2) the daily investor fee on such calendar day. The closing indicative value will never be less than zero. If the closing indicative value is equal to zero on any trading day, the closing indicative value on that day, and on all future days, will be zero.

|

|

Listing:

|

The securities will not be listed on any securities exchange. We may redeem the DRNs pursuant to the early redemption right at your option or our option, set forth below, but we will not purchase the DRNs in the secondary market.

|

Investing in the DRNs involves a number of risks. See “Selected Risk Considerations” beginning on page PS-3 of this reopening supplement and “Risk Factors beginning on US-2 of the accompanying underlying supplement and PS-4 of the accompanying product supplement.

Neither the Securities and Exchange Commission (the “SEC”) nor any state securities commission has approved or disapproved of the DRNs or passed upon the accuracy or the adequacy of this reopening supplement or the accompanying prospectus supplement and the prospectus. Any representation to the contrary is a criminal offense.

|

Price to Public

|

Underwriting Discounts and Commissions

|

Proceeds to Issuer

|

|

|

Per DRN

|

$970.00

|

$0.00

|

$970.00

|

|

Total

|

$4,850,000.00

|

$0.00

|

$4,850,000.00

|

After the initial public offering of any DRNs, the public offering price, concession and discount of such DRNs may be changed. In exchange for providing certain services relating to the distribution of the DRNs, Credit Suisse Securities (USA) LLS (‘CSSU”), a member of the Financial Industry Regulatory Authority (“FINRA”), or another member may receive all or a portion of the investor fee. In addition, CSSU may charge investors the applicable early redemption charge as specified herein. For more detailed information, please see “Supplemental Plan of Distribution (Conflicts of Interest)” on the last page of this reopening supplement.

The agent for this offering, CSSU, is our affiliate. For more information, see “Supplemental Plan of Distribution (Conflicts of Interest)” on the last page of this reopening supplement.

The DRNs are not deposit liabilities and are not insured or guaranteed by the Federal Deposit Insurance Corporation or any other governmental agency of the United States, Switzerland or any other jurisdiction.

CALCULATION OF REGISTRATION FEE

|

Title of Each Class of Securities Offered

|

Maximum Aggregate Offering Price

|

Amount of Registration Fee

|

|

Notes

|

$4,850,000.00

|

$624.68

|

Credit Suisse

|

November 8, 2013

|

(cover continued on next page)

|

(continued from previous page)

|

Daily Index Factor:

|

The daily index factor on any trading day will be equal to (1) the closing level of the index on such trading day divided by (2) the closing level of the index on the immediately preceding trading day. The daily index factor is deemed to be one on any day that is not a trading day.

|

|

Daily Investor Fee:

|

On any calendar day (each a “calculation day”), the daily investor fee will be equal to the product of (1) the closing indicative value on the immediately preceding calendar day times (2) the daily index factor on such calculation day times (3)(a) the investor fee factor divided by (b) 365.

Because the daily investor fee reduces the amount of your return at maturity or upon early redemption by Credit Suisse, the level of the index must increase by an amount sufficient to offset the impact of the daily investor fee (and the applicable early redemption charge for DRNs redeemed at your option, if you elect to have Credit Suisse redeem your DRNs prior to maturity, as described herein) in order for you to receive at least the principal amount of your investment at maturity or upon early redemption. If the level of the index decreases or does not increase sufficiently, you will receive less, and possibly significantly less, than the principal amount of your investment at maturity or upon early redemption.

|

|

Investor Fee Factor:

|

The investor fee factor is 1.25%.

|

|

Early Redemption of the DRNs at Your Option:

|

Subject to the requirements described below and in the accompanying product supplement, you may offer the applicable minimum number or stated principal amount of the DRNs (the “minimum early redemption quantity”) or more of your DRNs to Credit Suisse for early redemption on any business day during the term of the DRNs until May 25, 2018. The minimum early redemption quantity will be equal to $1,000 stated principal amount of DRNs (1 DRN) (for both the original securities and reopening securities). The trading day immediately succeeding the date you offer your DRNs for early redemption will be the valuation date applicable to such early redemption. If you elect to offer your DRNs for early redemption and the requirements for acceptance by Credit Suisse are met, you will receive, for each DRN you hold, a cash payment on the applicable early redemption date in an amount equal to the daily early redemption value. CSSU may charge investors the applicable early redemption charge for DRNs redeemed at the investor’s option.

Unless the scheduled early redemption date is postponed because it is not a business day or because there is a market disruption event on the scheduled valuation date, the final day on which Credit Suisse will redeem your DRNs at your option will be June 1, 2018. As such, you must offer your DRNs for early redemption no later than May 25, 2018.

Please see “Description of the DRNs—Early Redemption Procedures—Early Redemption at Your Option” in the accompanying product supplement for more information.

|

|

Early Redemption Charge:

|

On any valuation date, the early redemption charge will be equal to the product of (1) daily early redemption value times (2) the greater of (a) 1.25% times the number of calendar days remaining until June 3, 2014 divided by 365 and (b) 0.05%. If you elect to offer your DRNs for early redemption before June 3, 2014 and the requirements for acceptance by Credit Suisse are met, you should expect to pay the early redemption charge, which was $12.50 per $1,000 principal amount of DRNs on the original issue trade date. The early redemption charge on the reopening trade date is $7.09 per $1,000 principal amount of DRNs, which will decline on a straight-line basis to $0.50 per $1,000 principal amount of DRNs.

|

|

Early Redemption of the DRNs at Our Option:

|

We will have the right to redeem the DRNs, in whole but not in part, on any business day during the term of the DRNs. The trading day immediately succeeding the date of our notice of early redemption will be the valuation date applicable to such early redemption. Upon such early redemption, you will receive, for each DRN you hold, a cash payment on the applicable early redemption date in an amount equal to the daily early redemption value

Unless the scheduled early redemption date is postponed because it is not a business day or because there is a market disruption event on the scheduled valuation date, the final day on which we can deliver an early redemption notice is May 25, 2018.

Please see “Description of the DRNs—Early Redemption Procedures—Early Redemption at Our Option” in the accompanying product supplement for more information.

|

|

Daily Early Redemption Value:

|

With respect to any early redemption, for each DRN you hold, the daily early redemption value is the closing indicative value of the DRNs on the applicable valuation date.

|

|

Valuation Date: †

|

May 30, 2018 or, if such date is not a trading day, the next following trading day (the “final valuation date”), and any valuation date for an early redemption of the DRNs.

|

|

Maturity Date: **

|

June 4, 2018

|

|

Early Redemption Date: **

|

An early redemption date is the third business day following the applicable valuation date.

|

|

Further Issuances: ***

|

We may, without your consent, issue and sell additional DRNs after the reopening trade date at our sole discretion. Any further issuances of DRNs will form a single tranche with the offered DRNs, will have the same CUSIP number and will be fungible with the offered DRNs of such tranche upon settlement.

|

|

Calculation Agent:

|

Credit Suisse International

|

† Each valuation date (including the final valuation date) is subject to postponement if a market disruption event occurs on such date, as described in “Market Disruption Events” in the accompanying underlying supplement.

* As of the reopening settlement date, the aggregate stated principal amount of DRNs is expected to be $16,676,000.

** Any applicable early redemption date and the maturity date is subject to postponement if such date is not a business day. The early redemption date is also subject to postponement if a market disruption event occurs on the applicable valuation date. The maturity date is also subject to postponement if the scheduled final valuation date is postponed because it is not a trading day or because a market disruption event occurs, as described in “Market Disruption Events” in the accompanying underlying supplement.

***Additional DRNs may be issued and sold from time to time through CSSU and one or more dealers at a price that is higher or lower than the stated principal amount, based on the most recent closing indicative value of the DRNs. Any further issuances will increase the outstanding aggregate principal amount of the DRNs. If there is a substantial demand for the DRNs, we may issue additional DRNs frequently. However, we are under no obligation to issue or sell additional DRNs at any time, and if we do sell additional DRNs, we may limit or restrict such sales, and we may stop selling additional DRNs at any time.

TABLE OF CONTENTS

Page

|

Hypothetical Examples

|

PS-1

|

|

Selected Risk Considerations

|

PS-3

|

|

Supplemental Use of Proceeds and Hedging

|

PS-8

|

|

Historical Information

|

PS-9

|

|

Material U.S. Federal Income Tax Considerations

|

PS-10

|

|

Supplemental Plan of Distribution (Conflicts of Interest)

|

PS-11

|

|

Annex A

|

A-1

|

You should read this Reopening Supplement 1 to Pricing Supplement DRN-1 together with the accompanying underlying supplement dated May 24, 2013, the product supplement dated May 24, 2013, the prospectus supplement dated March 23, 2012 and the prospectus dated March 23, 2012, relating to our Medium-Term Notes of which these DRNs are a part. You may access these documents on the SEC website at www.sec.gov as follows (or if such address has changed, by reviewing our filings for the relevant date on the SEC website):

|

·

|

Underlying supplement dated May 24, 2013:

|

|

·

|

Product supplement No. RN-1 dated May 24, 2013:

|

|

·

|

Prospectus supplement and Prospectus dated March 23, 2012:

|

Our Central Index Key, or CIK, on the SEC website is 1053092. As used in this reopening supplement, the “Company,” “we,” “us,” or “our” refers to Credit Suisse.

This reopening supplement, together with the documents listed above, contains the terms of the DRNs and supersedes all other prior or contemporaneous oral statements as well as any other written materials including preliminary or indicative pricing terms, fact sheets, correspondence, trade ideas, structures for implementation, sample structures, brochures or other educational materials of ours. You should carefully consider, among other things, the matters set forth in “ Selected Risk Considerations” in this reopening supplement and “Risk Factors” in the accompanying product supplement, as the DRNs involve risks not associated with conventional debt securities. You should consult your investment, legal, tax, accounting and other advisors before deciding to invest in the DRNs.

i

HYPOTHETICAL EXAMPLES

The following examples show how the DRNs would perform in hypothetical circumstances, assuming (i) a closing level of the index on the original issue trade date of 350.00 and reflecting the $1,000 stated principal amount of each DRN. We have included five examples: (1) an example in which the level of the index increases at a constant rate of 10% each year, (2) an example in which the level of the index increases at an accelerating rate, (3) an example in which the level of the index decreases at an accelerating rate, (4) an example in which the level of the index increases and then decreases over the term of the DRNs and (5) an example in which the level of the index fluctuates between negative and positive annualized index returns during the term of the DRNs. These examples highlight the behavior of the closing indicative value of the DRNs at the end of each year in different circumstances. The figures in these examples have been rounded for convenience. Although your payment upon early redemption would be based on the closing indicative value of the DRNs on the applicable valuation date, which is calculated in the manner illustrated in the examples below, you should be aware that CSSU, our agent for any early redemption at your option, may charge the applicable early redemption charge for DRNs redeemed at the request of an investor prior to maturity. Any payment on the DRNs is subject to our ability to pay our obligations as they become due.

The figures set forth in the examples below are for purposes of illustration only (including for periods of time that have elapsed since the original issue trade date for the DRNs) and are not actual historical results. For information relating to the historical performance of the index, please refer to “Historical Information” below in this reopening supplement.

For purposes of the calculations in these tables, each year is assumed to have 365 days. The rate of return on your investment in the DRNs will depend on the price at which you purchased the DRNs.

Example 1. This example assumes that the level of the index has increased by approximately 61.05% over the term of the DRNs.

|

A

|

B

|

C

|

D

|

E

|

|

Year

|

Index

Level

|

Closing

Indicative Value

|

Annualized

Index Return

|

Annualized

Product Return

|

|

0

|

350.00

|

$1,000.00

|

n/a

|

n/a

|

|

1

|

385.00

|

$1,086.34

|

10.00%

|

8.63%

|

|

2

|

423.50

|

$1,180.13

|

10.00%

|

8.63%

|

|

3

|

465.85

|

$1,282.02

|

10.00%

|

8.63%

|

|

4

|

512.44

|

$1,392.71

|

10.00%

|

8.63%

|

|

5

|

563.68

|

$1,512.95

|

10.00%

|

8.63%

|

Example 2. This example assumes that the level of the index has increased by approximately 14.21% over the term of the DRNs.

|

A

|

B

|

C

|

D

|

E

|

|

Year

|

Index

Level

|

Closing

Indicative Value

|

Annualized

Index Return

|

Annualized

Product Return

|

|

0

|

350.00

|

$1,000.00

|

n/a

|

n/a

|

|

1

|

354.62

|

$1,000.61

|

1.32%

|

0.06%

|

|

2

|

363.01

|

$1,011.56

|

2.37%

|

1.09%

|

|

3

|

372.28

|

$1,024.51

|

2.55%

|

1.28%

|

|

4

|

382.49

|

$1,039.53

|

2.74%

|

1.47%

|

|

5

|

399.73

|

$1,072.89

|

4.51%

|

3.21%

|

Example 3. This example assumes that the level of the index has decreased by approximately 6.99% over the term of the DRNs.

PS-1

|

A

|

B

|

C

|

D

|

E

|

|

Year

|

Index

Level

|

Closing

Indicative Value

|

Annualized

Index Return

|

Annualized

Product Return

|

|

0

|

350.00

|

$1,000.00

|

n/a

|

n/a

|

|

1

|

345.87

|

$975.92

|

-1.18%

|

-2.41%

|

|

2

|

341.39

|

$951.32

|

-1.30%

|

-2.52%

|

|

3

|

336.52

|

$926.10

|

-1.43%

|

-2.65%

|

|

4

|

331.24

|

$900.24

|

-1.57%

|

-2.79%

|

|

5

|

325.52

|

$873.70

|

-1.73%

|

-2.95%

|

Example 4. This example assumes that the level of the index has increased by approximately 23.83% over the term of the DRNs.

|

A

|

B

|

C

|

D

|

E

|

|

Year

|

Index

Level

|

Closing Indicative Value

|

Annualized

Index

Return

|

Annualized

Product

Return

|

|

0

|

350.00

|

$1,000.00

|

n/a

|

n/a

|

|

1

|

375.33

|

$1,059.05

|

7.24%

|

5.91%

|

|

2

|

394.61

|

$1,099.62

|

5.14%

|

3.83%

|

|

3

|

407.98

|

$1,122.76

|

3.39%

|

2.10%

|

|

4

|

421.87

|

$1,146.56

|

3.40%

|

2.12%

|

|

5

|

433.41

|

$1,163.29

|

2.74%

|

1.46%

|

Example 5. This example assumes that the level of the index has decreased by approximately 40.95% over the term of the DRNs.

|

A

|

B

|

C

|

D

|

E

|

|

Year

|

Index

Level

|

Closing

Indicative Value

|

Annualized

Index Return

|

Annualized

Product Return

|

|

0

|

350.00

|

$1,000.00

|

n/a

|

n/a

|

|

1

|

315.00

|

$888.82

|

-10.00%

|

-11.12%

|

|

2

|

283.50

|

$790.00

|

-10.00%

|

-11.12%

|

|

3

|

255.15

|

$702.17

|

-10.00%

|

-11.12%

|

|

4

|

229.64

|

$624.11

|

-10.00%

|

-11.12%

|

|

5

|

206.68

|

$554.74

|

-10.00%

|

-11.12%

|

PS-2

SELECTED RISK CONSIDERATIONS

The DRNs are senior unsecured debt obligations of Credit Suisse. The DRNs are senior medium-term notes as described in the accompanying prospectus supplement and prospectus and are riskier than ordinary unsecured debt securities. The return on the DRNs is linked to the performance of the index. Investing in the DRNs is not equivalent to investing directly in the index or any instrument tracked by the index. See “The Index” in the accompanying underlying supplement for more information.

This section describes some of the most significant risks relating to an investment in the DRNs. In addition, please see the accompanying underlying supplement for a description of the risks relating to the index and the accompanying product supplement for the risks related to DRNs generally. We urge you to read the following information about these risks, together with the other information in this reopening supplement and the accompanying underlying supplement, product supplement, prospectus supplement and prospectus before investing in the DRNs.

The DRNs are subject to the risks relating to the index

Because the DRNs are linked to the index, the DRNs are subject to the risks relating to the index. These include, without limitation:

|

|

·

|

the DRNs are not linked to the VIX Index;

|

|

|

·

|

we cannot give you any assurance that future market conditions will be favorable to the index;

|

|

|

·

|

the index is rebalanced daily and is exposed to path dependency risk and market volatility risk;

|

|

|

·

|

past performance of the index is no guide to future performance, and the index, the base index and VIX futures have limited historical information;

|

|

|

·

|

concentration risks associated with the base index may adversely affect the value of your DRNs;

|

|

|

·

|

trading and other transactions by us, our affiliates, or third parties with whom we transact, in securities or financial instruments related to the index may impair the value of your DRNs;

|

|

|

·

|

suspension or disruptions of market trading in futures contracts may adversely affect the value of your DRNs;

|

|

|

·

|

the DRNs do not give you rights in the underlying futures or the component securities of the S&P 500® Index;

|

|

|

·

|

the calculation agent may modify the index; and

|

|

|

·

|

the policies of the index sponsor or the Chicago Board Options Exchange and changes that affect the S&P 500® Index, the VIX Index, the base index or the index could affect the applicable redemption amount of your DRNs and their value.

|

For more information on these and other risks relating to the index, please see “Risk Factors” starting on US-2 of the accompanying underlying supplement.

The DRNs do not have a minimum redemption amount or daily early redemption value and you may lose all or a significant portion of your investment in the DRNs

The DRNs do not have a minimum redemption amount or daily early redemption value. You may receive less, and possibly significantly less, at maturity or upon early redemption than the amount you originally invested. Our cash payment on your DRNs at maturity or upon early redemption will be based primarily on any increase or decrease in the closing levels of the index, and will be reduced by the daily investor fee (and the early redemption charge of up to 1.25% times the daily early redemption value per DRN if you offer your DRNs for early redemption). You may lose some or all of your investment in the DRNs if the level of the index decreases or does

PS-3

not increase sufficiently to offset the impact of the daily investor fee (and the early redemption charge for any DRNs redeemed at your option). Any payment on the DRNs is subject to our ability to pay our obligations as they become due.

You will not receive coupon payments on the DRNs

We will not make coupon payments on the DRNs. You may receive less at maturity or upon early redemption than you could have earned on ordinary interest-bearing debt securities with similar maturities, including other of our debt securities, since the redemption amount and the daily early redemption value are based on the appreciation or depreciation of the index. Because the payment due at maturity and the daily early redemption value may be less than the amount originally invested in the DRNs, the return on the DRNs (the effective yield to maturity) may be negative. Even if it is positive, the return payable on the DRNs may not be enough to compensate you for any loss in value due to inflation and other factors relating to the value of money over time.

The DRNs are subject to the credit risk of Credit Suisse

Although the return on the DRNs will be based on the performance of the index, the payment of any amount due on the DRNs, including at maturity or upon early redemption, is subject to the credit risk of Credit Suisse. Investors are dependent on Credit Suisse’s ability to pay all amounts due on the DRNs, and therefore investors are subject to our credit risk. In addition, any decline in our credit ratings, any adverse changes in the market’s view of our creditworthiness or any increase in our credit spreads is likely to adversely affect the value of the DRNs prior to maturity.

Your return at maturity or upon early redemption will be reduced by the daily investor fee

The daily investor fee reduces the amount of your return at maturity or upon early redemption by Credit Suisse, and therefore the level of the index must increase by an amount sufficient to offset the impact of the daily investor fee (and the applicable early redemption charge of up to 1.25% times the daily early redemption value per DRN if you offer your DRNs for early redemption) in order for you to receive at least the principal amount of your investment at maturity or upon early redemption. If the level of the index decreases or does not increase sufficiently to offset the impact of these adjustments, you will receive less, and possibly significantly less, than the principal amount of your investment at maturity or upon early redemption of the DRNs by Credit Suisse.

If the closing indicative value is equal to zero on any trading day, you will lose all of your investment

If the closing indicative value is equal to zero on any trading day, the closing indicative value on that day, and on all future days, will be zero and you will lose all of your investment in the DRNs. Due to the application of the daily investor fee, among other factors, the closing indicative value may be equal to zero on any trading when the level of the index is above zero on that day.

An early redemption charge may be charged upon an early redemption at your option

CSSU will act as our agent in connection with any early redemption at your option and may charge the applicable early redemption charge for DRNs redeemed at your option, if you elect to have us redeem your DRNs prior to maturity. The imposition of this fee will mean that you will not receive the full amount of the daily early redemption value upon an early redemption at your option. If you elect to offer your DRNs for early redemption before May 28, 2014 and the requirements for acceptance by Credit Suisse are met, you should expect to pay the early redemption charge, which was $12.50 per $1,000 principal amount of DRNs on the original issue trade date. The early redemption charge on the reopening trade date is $7.09 per $1,000 principal amount of DRNs, which will decline on a straight-line basis to $0.50 per $1,000 principal amount of DRNs.

There are certain procedures you must follow to offer your DRNs to Credit Suisse for early redemption

Credit Suisse will redeem your DRNs at your election prior to maturity only if you have followed the procedures for early redemption detailed in the accompanying product supplement. The procedures involved in the offer of any early redemption represent substantial restrictions on your ability to cause Credit Suisse to redeem your DRNs prior to the maturity date. If your irrevocable offer for early redemption is received after 4:00 p.m., New

PS-4

York City time on a business day, you will be deemed to have made your offer for early redemption on the following business day. Additionally, unless the scheduled early redemption date is postponed because it is not a business day or because there is a market disruption event on the scheduled valuation date, the final day on which Credit Suisse will redeem your DRNs prior to maturity will be June 1, 2018. As such, you must offer your DRNs for early redemption no later than May 25, 2018.

You will not know the daily early redemption value you will receive at the time an election is made to redeem your DRNs prior to maturity

You will not know the daily early redemption value at the time you elect to have us redeem your DRNs or at the time we elect to redeem your DRNs prior to the maturity date. You will not know the daily early redemption value until the applicable valuation date, which will be the trading day immediately following the business day on which either you deliver the redemption offer to Credit Suisse or on which we deliver the relevant notice to DTC. We will pay you the daily early redemption value, if any (in the case of early redemption at your option, less the applicable early redemption charge), on the applicable early redemption date, which is the third business day following the applicable valuation date. The determination of the closing level of the index for a valuation date, and the related early redemption date, will be postponed if a market disruption event exists on such scheduled valuation date. See “Market Disruption Events” in the accompanying underlying supplement. As a result, you will be exposed to market risk in the event that the market fluctuates between the time either you deliver the early redemption offer to Credit Suisse or on which we deliver the relevant notice to DTC and the applicable valuation date.

Credit Suisse may redeem your DRNs at its option at any time

We have the right to redeem your DRNs, in whole but not in part, on any business day during the term of the DRNs. The amount you may receive upon an early redemption by Credit Suisse may be less than the amount you would receive on your investment at maturity or if you had elected to have Credit Suisse redeem your DRNs at a time of your choosing. If Credit Suisse exercises its right to redeem your DRNs prior to the maturity date, you will receive, for each DRN you hold, a cash payment in an amount equal to the daily early redemption value, which is the closing indicative value of the DRN on the applicable valuation date. Credit Suisse has no obligation to take your interests into account when deciding whether to call the DRNs. The payment of any amount due on the DRNs, including any redemption amount or upon early redemption, is subject to the credit risk of Credit Suisse.

The value of the DRNs is expected to be influenced by many unpredictable factors

The value of your DRNs is expected to fluctuate between the date you purchase them and the applicable valuation date. You may sustain a significant loss if you sell the DRNs prior to maturity. Several factors, many of which are beyond our control, will influence the value of the DRNs. We expect that generally the level of the index will affect the value of the DRNs more than any other factor. Other factors that may influence the value of the DRNs include:

|

|

·

|

the time remaining to the maturity of the DRNs;

|

|

|

·

|

our early redemption right, which is likely to limit the value of the DRNs;

|

|

|

·

|

interest and yield rates in the market generally;

|

|

|

·

|

the volatility of any option or futures contracts relating to the index, the base index, the VIX Index, the S&P 500® Index, the component securities of the S&P 500® Index or the underlying futures;

|

|

|

·

|

the liquidity of any option or futures contracts relating to the Index, the base index, the VIX Index, the S&P 500® Index, the component securities of the S&P 500® Index or the underlying futures;

|

|

|

·

|

geopolitical conditions and a variety of economic, financial, political, regulatory or judicial events that affect stock markets generally, the Index, the base index, the equity securities included in the S&P 500® Index, the VIX Index or the relevant futures contracts on the VIX Index; and

|

|

|

·

|

our creditworthiness, including actual or anticipated downgrades in our credit ratings.

|

PS-5

These factors interrelate in complex ways, and the effect of one factor on the value of your DRNs may offset or enhance the effect of another factor.

Lack of liquidity of the DRNs

The DRNs will not be listed on any securities exchange. We may redeem the DRNs pursuant to the early redemption right at your option or our option, but we will not purchase the DRNs in the secondary market. Also, the number of DRNs outstanding or held by person other than our affiliates could be reduced at any time due to early redemptions of the DRNs. There may be little or no secondary market for the DRNs. Even if there is a secondary market, it may not provide enough liquidity to allow you to trade or sell the DRNs when you wish to do so. Because other dealers are not likely to make a secondary market for the DRNs, the price at which you may be able to sell your DRNs (other than by effecting an early redemption at your option) is likely to depend on the closing indicative value of the DRNs on the applicable valuation date. If you have to sell your DRNs in the secondary market, you may not be able to do so or you may have to sell them at a substantial loss.

We are under no obligation to issue or sell additional DRNs at any time, and if we do sell additional DRNs, we may limit or restrict such sales, and we may stop selling additional DRNs at any time

At our sole discretion, we may decide to issue and sell additional DRNs from time to time at a price that is higher or lower than the stated principal amount, based on the most recent closing indicative value of the DRNs. The price of the DRNs in any subsequent sale may differ substantially (higher or lower) from the issue price paid in connection with any other issuance of the DRNs. However, we are under no obligation to issue or sell additional DRNs at any time, and if we do sell additional DRNs, we may limit or restrict such sales, and we may stop selling additional DRNs at any time.

The index has limited history and may perform in unexpected ways. Any historical or retrospectively calculated performance of the index should not be taken as an indication of the future performance of the index.

The index began publishing on November 3, 2011 and therefore has a limited history. We have calculated hypothetical historical performance data to illustrate how the index may have performed had it been created in the past, but those calculations are subject to many limitations. Unlike actual historical performance, such calculations do not reflect actual trading, liquidity constraints, fees and other costs. In addition, the models used to calculate these hypothetical returns are based on certain data, assumptions and estimates. Different models or models using different data assumptions, and estimates might result in materially different hypothetical performance. Furthermore, any hypothetical historical performance or actual historical performance is not an indication of how the index will perform in the future.

Potential conflicts

We and our affiliates play a variety of roles in connection with the issuance of the DRNs, including acting as calculation agent and hedging our obligations under the DRNs. In performing these duties, the economic interests of the calculation agent and other affiliates of ours are potentially adverse to your interests as an investor in the DRNs. In addition, we are a minority investor in VelocityShares LLC (“VelocityShares”) and we have customary rights to nominate a director of such affiliate. VelocityShares worked with the index sponsor in developing the guidelines and policies governing the composition and calculation of the index. The policies and judgments for which VelocityShares was responsible could have an impact, positive or negative, on the level of the index. Please see “Risk Factors—There may be potential conflicts of interest” in the accompanying product supplement.

You will not have any rights in the instruments tracked by the index

As an owner of the DRNs, you will not own or have any beneficial or other legal interest in, and will not be entitled to any rights with respect to, any instrument tracked by the index. Additionally, the return on an investment in the DRNs, if any, may be less than the return on a similar investment in other instruments tracking the index due to the daily investor fee (and the applicable early redemption charge for DRNs redeemed at your option, if you elect to have us redeem your DRNs prior to maturity). The return on the DRNs may also differ from the results of the index for the reasons described under “—The DRNs are subject to the credit risk of Credit Suisse.”

PS-6

The United States federal income tax treatment of an investment in the DRNs is uncertain

The U.S. federal income tax consequences of an investment in the DRNs are uncertain, and may be adverse to a holder of the DRNs. No statutory, judicial, or administrative authority directly addresses the characterization of the DRNs or instruments similar to the DRNs for U.S. federal income tax purposes. As a result, significant aspects of the U.S. federal income tax consequences of an investment in the DRNs are not certain. Under the terms of the DRNs, you will have agreed with us to treat the securities as prepaid financial contracts, with respect to the underlying, as described under “Material U.S. Federal Income Tax Considerations—Characterization of the Securities” in the accompanying underlying supplement. If the U.S. Internal Revenue Service (the “IRS”) were successful in asserting an alternative characterization for the DRNs, the timing and character of income, gain or loss with respect to the DRNs may differ. No assurance can be given that the IRS will agree with the statements made in the section entitled “Material U.S. Federal Income Tax Considerations” in the accompanying underlying supplement. Additionally, in Notice 2008-2, the IRS and the Treasury Department stated they are considering issuing new regulations or other guidance on whether holders of an instrument such as the DRNs should be required to accrue income during the term of the instrument. Accordingly, it is possible that regulations or other guidance may be issued that require holders of the DRNs to recognize income in respect of the DRNs prior to receipt of any payments thereunder or redemption, sale or exchange thereof. Any regulations or other guidance that may be issued could result in income and gain (either at maturity or upon redemption, sale or exchange) in respect of the DRNs being treated as ordinary income. It is also possible that a Non-U.S. Holder of the DRNs could be subject to U.S. withholding tax in respect of the DRNs under such regulations or other guidance. It is not possible to determine whether such regulations or other guidance will apply to your DRNs (possibly on a retroactive basis). More recently, on January 24, 2013, the House Ways and Means Committee released in draft form certain proposed legislation relating to financial instruments. If enacted as proposed, the effect of that legislation generally would be to require instruments such as the DRNs to be marked to market on an annual basis with all gains and losses to be treated as ordinary, subject to certain exceptions. Finally, the IRS could assert that each rebalancing of the underlying is a significant modification of the DRNs and, therefore, a taxable event to you. If the IRS were to prevail in treating each rebalancing of the underlying as a taxable event, you would recognize capital gain or, possibly, loss on the DRNs on the date of each rebalancing to the extent of the difference between the fair market value of the DRNs and your adjusted basis in the DRNs at the time of rebalancing. Such gain or loss generally would be short-term capital gain or loss.

YOU ARE URGED TO CONSULT WITH YOUR OWN TAX ADVISOR REGARDING ALL ASPECTS OF THE U.S. FEDERAL INCOME TAX CONSEQUENCES OF INVESTING IN THE DRNS.

PS-7

SUPPLEMENTAL USE OF PROCEEDS AND HEDGING

We intend to use the proceeds of this offering for our general corporate purposes, which may include the refinancing of existing debt outside Switzerland. Some or all of the proceeds we receive from the sale of the DRNs may be used in connection with hedging our obligations under the securities through one or more of our affiliates. Such hedging or trading activities on or prior to the reopening trade date and during the term of the securities (including on the applicable valuation date) could adversely affect the value of the index and, as a result, could decrease the amount you may receive on the DRNs at maturity or upon early redemption. For additional information, see “Supplemental Use of Proceeds and Hedging” in the accompanying product supplement.

PS-8

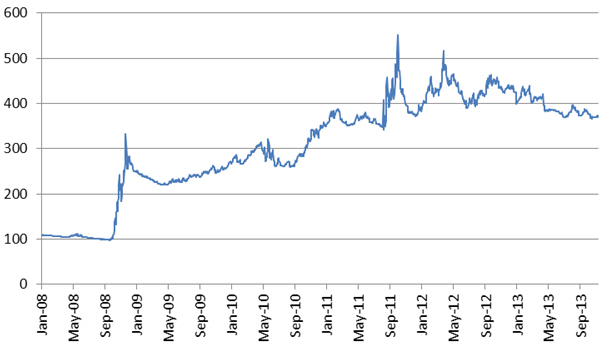

HISTORICAL INFORMATION

The graph below sets forth the hypothetical historical performance of the index from January 1, 2008 through November 2, 2011 and the actual historical performance of the index from November 3, 2011, through November 8, 2013. The closing level of the index on November 8, 2013, was 373.83. Because the index was only launched on November 3, 2011, S&P Dow Jones Indices, the index sponsor, has retrospectively calculated the index performance on all dates prior to its launch. Although we believe that the retrospective calculation of the index performance represents accurately and fairly how the index would have performed from January 1, 2008 through November 3, 2011, the index did not, in fact, exist during that period and certain assumptions were made in performing the retrospective calculation that may have affected the index’s hypothetical performance for this period. We obtained the actual historical performance below from Bloomberg, without independent verification.

The hypothetical and historical index performance should not be taken as an indication of future performance of the index, and no assurance can be given as to the closing level of the index on any trading day, including on any applicable valuation date. We cannot give you assurance that the performance of the index will result in the return of any of your initial investment.

For additional information on the index, see information set forth under “The Index” in the accompanying underlying supplement.

PS-9

MATERIAL U.S. FEDERAL INCOME TAX CONSIDERATIONS

Please see the discussion of certain United States federal income tax considerations in “Material U.S. Federal Income Tax Considerations” in the accompanying underlying supplement.

PS-10

SUPPLEMENTAL PLAN OF DISTRIBUTION (CONFLICTS OF INTEREST)

Under the terms and subject to the conditions contained in a distribution agreement dated May 7, 2007, as amended, which we refer to as the distribution agreement, we have agreed to sell the DRNs to CSSU. We will not make a secondary market in the DRNs.

The distribution agreement provides that CSSU is obligated to purchase all of the DRNs if any are purchased.

CSSU proposes to offer the DRNs at the offering price set forth on the cover page of this reopening supplement and will not receive a commission in connection with the distribution of the DRNs. After the initial public offering of any DRNs, the public offering price, concession and discount of such DRNs may be changed. Any future issuances of the DRNs may be issued at a price that is higher or lower than the stated principal amount, based on the most recent closing indicative value of the DRNs at that time. In exchange for providing certain services relating to the distribution of the DRNs, CSSU, a member of the Financial Industry Regulatory Authority (“FINRA”), or another member may receive all or a portion of the investor fee. In addition, CSSU may charge investors the applicable early redemption charge as specified herein.

We expect to deliver the DRNs against payment for the DRNs on the reopening settlement date indicated herein, which may be a date that is greater than three business days following the reopening trade date. Under Rule 15c6-1 of the Securities Exchange Act of 1934, as amended, trades in the secondary market generally are required to settle in three business days, unless the parties to a trade expressly agree otherwise. Accordingly, if the reopening settlement date is more than three business days after the reopening trade date, purchasers who wish to transact in the DRNs more than three business days prior to the reopening settlement date will be required to specify alternative settlement arrangements to prevent a failed settlement.

The agent for this offering, CSSU, is our affiliate. In accordance with FINRA Rule 5121, CSSU may not make sales in this offering to any of its discretionary accounts without the prior written approval of the customer. A portion of the net proceeds from the sale of the securities will be used by CSSU or one of its affiliates in connection with hedging our obligations under the securities. For further information, please refer to “Underwriting (Conflicts of Interest)” in the accompanying product supplement.

PS-11

Annex A

FORM OF OFFER FOR EARLY REDEMPTION

PART A: TO BE COMPLETED BY THE BENEFICIAL OWNER

|

Dated:

|

___________

|

|||

|

[insert date]

|

||||

Credit Suisse AG (“Credit Suisse”)

list.etndesk@credit-suisse.com

|

|

Re: Daily Redeemable Notes Linked to the Performance of the S&P 500 VIX Futures Variable Long/Short Index TR—Short Term due June 4, 2018

|

CUSIP No. 22547Q2V7

Ladies and Gentlemen:

The undersigned beneficial owner hereby irrevocably offers to Credit Suisse the right to redeem the DRNs, as described in the applicable pricing supplement, in the amounts and on the date set forth below.

|

Name of beneficial holder:

|

|

|

[insert name of beneficial owner]

|

At least the applicable minimum early redemption quantity for early redemption must be offered at one time for the offer to be valid, as set forth in the applicable pricing supplement. The trading day immediately succeeding the date the DRNs are offered for early redemption will be the valuation date applicable to such early redemption.

|

Stated principal amount of DRNs offered for early redemption:

|

||||

|

[insert principal amount of DRNs offered for early redemption by Credit Suisse]

|

||||

|

Applicable valuation date:

|

,

|

20

|

||

|

Applicable early redemption date:

|

,

|

20

|

||

|

[insert a date that is three business days following the applicable valuation date]

|

||||

|

Contact Name:

|

|

|

[insert the name of a person or entity to be contacted with respect to this Offer for Early Redemption]

|

|

|

Telephone #:

|

|

|

[insert the telephone number at which the contact person or entity can be reached]

|

A-1

My DRNs are held in the following DTC Participant’s Account (the following information is available from the broker through which you hold your DRNs):

Name:

DTC Account Number (and any relevant sub-account):

Contact Name:

Telephone Number:

Acknowledgement: In addition to any other requirements specified in the Reopening Supplement being satisfied, I acknowledge that the DRNs specified above will not be redeemed unless (i) this Offer for Early Redemption, as completed and signed by the DTC Participant through which my DRNs are held (the “DTC Participant”), is delivered to Credit Suisse, (ii) the DTC Participant has booked a “delivery vs. payment” (“DVP”) trade on the applicable valuation date facing Credit Suisse, and (iii) the DTC Participant instructs DTC to deliver the DVP trade to Credit Suisse as booked for settlement via DTC at or prior to 10:00 a.m., New York City time, on the applicable early redemption date. I also acknowledge that if this Offer for Early Redemption is received after 4:00 p.m., New York City time, on a business day, I will be deemed to have made this Offer for Early Redemption on the following business day.

The undersigned acknowledges that Credit Suisse will not be responsible for any failure by the DTC Participant through which such undersigned’s DRNs are held to fulfill the requirements for early redemption set forth above.

|

[Beneficial Holder]

|

||

PART B OF THIS NOTICE IS TO BE COMPLETED BY THE DTC PARTICIPANT IN WHOSE ACCOUNT THE DRNs ARE HELD AND DELIVERED TO CREDIT SUISSE BY 4:00 P.M., NEW YORK CITY TIME, ON THE BUSINESS DAY IMMEDIATELY PRECEDING THE APPLICABLE VALUATION DATE

A-2

BROKER’S CONFIRMATION OF EARLY REDEMPTION

[PART B: TO BE COMPLETED BY BROKER]

|

Dated:

|

|||

|

[insert date]

|

|||

Credit Suisse AG (“Credit Suisse”)

|

|

Re: Daily Redeemable Notes Linked to the Performance of the S&P 500 VIX Futures Variable Long/Short Index TR—Short Term due June 4, 2018

|

|

|

Ladies and Gentlemen:

|

CUSIP No. 22547Q2V7

The undersigned holder of Daily Redeemable Notes Linked to the Performance of the S&P 500 VIX Futures Variable Long/Short Index TR – Short Term due June 4, 2018 issued by Credit Suisse AG, acting through its Nassau Branch, CUSIP 22547Q2V7 hereby irrevocably offers to Credit Suisse the right to early redemption, on the early redemption date

of , with respect to the number of the DRNs indicated below as described in the applicable pricing supplement. Terms not defined herein have the meanings given to such terms in the applicable pricing supplement.

The undersigned certifies to you that it will (i) book a delivery vs. payment trade on the valuation date with respect to the stated principal amount of DRNs specified below at a price per DRN equal to the daily early redemption value, facing Credit Suisse AG, DTC #355 and (ii) deliver the trade as booked for settlement via DTC at or prior to 10:00 a.m., New York City time, on the early redemption date.

Very truly yours,

[NAME OF DTC PARTICIPANT HOLDER]

Contact Name:

Title:

Telephone:

Fax:

E-mail:

At least the applicable minimum early redemption quantity for early redemption must be offered at one time for the offer to be valid, as set forth in the applicable pricing supplement. The trading day immediately succeeding the date the DRNs are offered for early redemption will be the valuation date applicable to such early redemption.

|

Stated principal amount of DRNs offered for early redemption:

|

|

|

[insert principal amount of DRNs offered for early redemption by Credit Suisse]

|

DTC # (and any relevant sub-account):

A-3

Credit Suisse