|

Pricing Supplement No. U737

To the Underlying Supplement dated March 23, 2012,

Product Supplement No. U-I dated March 23, 2012,

Prospectus Supplement dated March 23, 2012 and

Prospectus dated March 23, 2012

|

Filed Pursuant to Rule 424(b)(2)

Registration Statement No. 333-180300-03

November 30, 2012

|

|

Financial

Products

|

$726,000

High/Low Coupon Callable Yield Notes due March 5, 2014

Linked to the Performance of the S&P 500® Index and the Russell 2000® Index

|

||

General

|

•

|

The securities are designed for investors who are mildly bearish, neutral or mildly bullish on the Underlyings. Investors should be willing to lose some or all of their investment if a Knock-In Event occurs with respect to either Underlying. Any payment on the securities is subject to our ability to pay our obligations as they become due.

|

|

•

|

Interest will be paid quarterly in arrears at a rate per annum that will depend on whether a Knock-In Event occurs. If a Knock-In Event does not occur, interest will be paid at an Applicable Rate per annum of 7.50%. If a Knock-In Event occurs during any Observation Period, interest for that quarterly period and each subsequent quarterly interest period will be paid at an Applicable Rate per annum of 1.0%. Interest will be calculated on a 30/360 basis, subject to Early Redemption.

|

|

•

|

The Issuer may redeem the securities, in whole but not in part, on any Interest Payment Date scheduled to occur on or after June 5, 2013. No interest will accrue or be payable following an Early Redemption.

|

|

•

|

Senior unsecured obligations of Credit Suisse AG, acting through its Nassau Branch, maturing March 5, 2014.†

|

|

•

|

Minimum purchase of $1,000. Minimum denominations of $1,000 and integral multiples of $1,000 in excess thereof.

|

|

•

|

The securities priced on November 30, 2012 (the “Trade Date”) and are expected to settle on December 5, 2012 (the “Settlement Date”). Delivery of the securities in book-entry form only will be made through The Depository Trust Company.

|

Key Terms

|

Issuer:

|

Credit Suisse AG (“Credit Suisse”), acting through its Nassau Branch

|

|||||

|

Underlyings:

|

Each Underlying is identified in the table below, together with its Bloomberg ticker symbol, Initial Level and Knock-In Level:

|

|||||

|

Underlying

|

Ticker

|

Initial Level

|

Knock-In Level

|

|||

|

S&P 500® Index (“SPX”)

|

SPX

|

1416.18

|

920.517

|

|||

|

Russell 2000® Index (“RTY”)

|

RTY

|

821.92

|

534.248

|

|||

|

Applicable Rate:

|

•

|

If a Knock-In Event does not occur, the Applicable Rate will be 7.50% per annum.

|

||||

|

•

|

If a Knock-In Event occurs during any Observation Period, the Applicable Rate for the corresponding interest period and each subsequent interest period will be 1.0% per annum.

|

|||||

|

Interest will be calculated on a 30/360 basis.

|

||||||

|

Interest Payment Dates:

|

Unless redeemed earlier, interest will be paid quarterly in arrears at the Applicable Rate per annum on March 5, 2013, June 5, 2013, September 5, 2013, December 5, 2013 and the Maturity Date, subject to the modified following business day convention. No interest will accrue or be payable following an Early Redemption.

|

|||||

|

Redemption Amount:

|

The Redemption Amount you will be entitled to receive will depend on the individual performance of each Underlying and whether a Knock-In Event occurs. If the securities are not subject to Early Redemption, the Redemption Amount will be determined as follows:

|

|||||

|

•

|

If a Knock-In Event occurs, the Redemption Amount will equal the principal amount of the securities you hold multiplied by the sum of one plus the Underlying Return of the Lowest Performing Underlying. In this case, the maximum Redemption Amount will equal the principal amount of the securities. Therefore, unless the Final Level of each of the Underlyings is greater than or equal to its Initial Level, the Redemption Amount will be less than the principal amount of the securities. You could lose your entire investment.

|

|||||

|

•

|

If a Knock-In Event does not occur, the Redemption Amount will equal the principal amount of the securities you hold.

|

|||||

|

Any payment on the securities is subject to our ability to pay our obligations as they become due.

|

||||||

|

Early Redemption:

|

Prior to the Maturity Date, the Issuer may redeem the securities in whole, but not in part, on any Interest Payment Date scheduled to occur on or after June 5, 2013, upon notice on or before the relevant Early Redemption Notice Date at 100% of the principal amount of the securities, together with the interest payable on that Interest Payment Date.

|

|||||

|

Early Redemption Notice Dates:

|

Notice of Early Redemption will be provided prior to the relevant Interest Payment Date on or before May 31, 2013, August 30, 2013 or December 2, 2013, as applicable.

|

|||||

|

Knock-In Event:

|

A Knock-In Event will occur if, on any trading day during any Observation Period, the closing level of either Underlying is equal to or less than its Knock-In Level.

|

|||||

|

Knock-In Level:

|

For each Underlying, as set forth in the table above.

|

|||||

|

Lowest Performing Underlying:

|

The Underlying with the lowest Underlying Return.

|

|||||

|

Underlying Return:

|

For each Underlying, the Underlying Return will be calculated as follows:

|

|||||

|

Final Level − Initial Level

Initial Level

|

, subject to a maximum of zero

|

|||||

|

Initial Level:

|

For each Underlying, as set forth in the table above.

|

|||||

|

Final Level:

|

For each Underlying, the closing level of such Underlying on the Valuation Date.

|

|||||

|

Observation Periods:

|

There are five quarterly Observation Periods. The first Observation Period will be from but excluding the Trade Date to and including the first Observation Date. Each subsequent Observation Period will be from but excluding an Observation Date to and including the next following Observation Date.

|

|||||

|

Observation Dates:†

|

February 28, 2013, May 31, 2013, August 30, 2013, December 2, 2013 and the Valuation Date.

|

|||||

|

Valuation Date:†

|

February 28, 2014

|

|||||

|

Maturity Date:†

|

March 5, 2014

|

|||||

|

Listing:

|

The securities will not be listed on any securities exchange.

|

|||||

|

CUSIP:

|

22546TF89

|

|||||

† The determination of the closing level for each Underlying on each Observation Date, other than the Valuation Date, is subject to postponement if such date is not a trading day for such Underlying or as a result of a market disruption event in respect of such Underlying, as described herein under “Market Disruption Events.” The Valuation Date is subject to postponement in respect of each Underlying if such date is not an underlying business day for such Underlying or as a result of a market disruption event in respect of such Underlying, as described in the accompanying product supplement under “Description of the Securities—Market disruption events.” The Interest Payment Dates including the Maturity Date are subject to postponement, each as described herein, if such date is not a business day or if the determination of the closing level for any Underlying on the corresponding Observation Date or the Valuation Date, as applicable, is postponed because such date is not a trading day or an underlying business day for any Underlying, as applicable, or as a result of a market disruption event in respect of any Underlying.

Investing in the securities involves a number of risks. See “Selected Risk Considerations” in this pricing supplement and “Risk Factors” beginning on page PS-3 of the accompanying product supplement.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of the securities or passed upon the accuracy or the adequacy of this pricing supplement or the accompanying underlying supplement, the product supplement, the prospectus supplement and the prospectus. Any representation to the contrary is a criminal offense.

|

Price to Public

|

Underwriting Discounts and Commissions(1)

|

Proceeds to Issuer

|

|

|

Per security

|

$1,000.00

|

$2.50

|

$997.50

|

|

Total

|

$726,000.00

|

$37.50

|

$725,962.50

|

(1) We or one of our affiliates will pay varying discounts and commissions of up to $2.50 per $1,000 principal amount of securities, for total underwriting discounts and commissions of $37.50, and may pay referral fees of up to $5.50 per $1,000 principal amount of securities. For more detailed information, please see “Supplemental Plan of Distribution (Conflicts of Interest)” on the last page of this pricing supplement.

The agent for this offering, Credit Suisse Securities (USA) LLC (“CSSU”), is our affiliate. For more information, see “Supplemental Plan of Distribution (Conflicts of Interest)” on the last page of this pricing supplement.The securities are not deposit liabilities and are not insured or guaranteed by the Federal Deposit Insurance Corporation or any other governmental agency of the United States, Switzerland or any other jurisdiction.

CALCULATION OF REGISTRATION FEE

|

Title of Each Class of Securities Offered

|

Maximum Aggregate Offering Price

|

Amount of Registration Fee

|

|

Notes

|

$726,000.00

|

$99.03

|

Credit Suisse

November 30, 2012

Additional Terms Specific to the Securities

You should read this pricing supplement together with the underlying supplement dated March 23, 2012, the product supplement dated March 23, 2012, the prospectus supplement dated March 23, 2012 and the prospectus dated March 23, 2012, relating to our Medium-Term Notes of which these securities are a part. You may access these documents on the SEC website at www.sec.gov as follows (or if such address has changed, by reviewing our filings for the relevant date on the SEC website):

|

•

|

Underlying supplement dated March 23, 2012:

|

|

•

|

Product supplement No. U-I dated March 23, 2012:

|

|

•

|

Prospectus supplement and Prospectus dated March 23, 2012:

|

Our Central Index Key, or CIK, on the SEC website is 1053092. As used in this pricing supplement, the “Company,” “we,” “us,” or “our” refers to Credit Suisse.

This pricing supplement, together with the documents listed above, contains the terms of the securities and supersedes all other prior or contemporaneous oral statements as well as any other written materials including preliminary or indicative pricing terms, fact sheets, correspondence, trade ideas, structures for implementation, sample structures, brochures or other educational materials of ours. You should carefully consider, among other things, the matters set forth in “Risk Factors” in the product supplement and “Selected Risk Considerations” in this pricing supplement, as the securities involve risks not associated with conventional debt securities. You should consult your investment, legal, tax, accounting and other advisors before deciding to invest in the securities.

1

Hypothetical Redemption Amounts and Total Payments on the Securities

The tables and examples below illustrate hypothetical Redemption Amounts payable at maturity and, in the case of the tables, total payments over the term of the securities (which include both payments at maturity and the total interest paid on the securities) on a $1,000 investment in the securities for a range of Underlying Returns of the Lowest Performing Underlying, both in the event a Knock-In Event does not occur and in the event a Knock-In Event does occur. The tables and examples reflect that the Applicable Rate is 7.50% per annum if a Knock-In Event does not occur and 1.0% per annum for the corresponding quarterly interest period and each subsequent quarterly interest period if a Knock-In Event occurs and assume that (i) the securities are not redeemed prior to maturity, (ii) the term of the securities is exactly 15 months and (iii) the Knock-In Level for each Underlying is 65.0% of the Initial Level of such Underlying. In addition, the examples below assume that the Initial Level is 1410 for SPX and 810 for RTY. The examples are intended to illustrate hypothetical calculations of only the Redemption Amount and do not illustrate the calculation or payment of any individual interest payment. The Redemption Amounts and total payment amounts set forth below are provided for illustration purposes only. The actual Redemption Amounts and total payments applicable to a purchaser of the securities will depend on several variables, including, but not limited to (a) whether on any trading day during any Observation Period the closing level of either Underlying is equal to or less than its Knock-In Level and (b) the Final Level of the Lowest Performing Underlying determined on the Valuation Date. It is not possible to predict whether a Knock-In Event will occur and in the event that there is a Knock-In Event, whether and by how much the Final Level of the Lowest Performing Underlying will decrease in comparison to its Initial Level. Any payment on the securities is subject to our ability to pay our obligations as they become due. The numbers appearing in the following tables and examples have been rounded for ease of analysis.

TABLE 1: A Knock-In Event DOES NOT occur during any Observation Period.

|

Principal

Amount

of Securities

|

Percentage Change from the Initial Level to the Final Level of the Lowest Performing Underlying

|

Underlying Return of the Lowest Performing Underlying

|

Redemption

Amount

(Knock-In Event

does not occur)

|

Total Interest

Payment on

the Securities

|

Total Payment

on the Securities

|

|

$1,000.00

|

50.00%

|

0.00%

|

$1,000.00

|

$93.75

|

$1,093.75

|

|

$1,000.00

|

40.00%

|

0.00%

|

$1,000.00

|

$93.75

|

$1,093.75

|

|

$1,000.00

|

30.00%

|

0.00%

|

$1,000.00

|

$93.75

|

$1,093.75

|

|

$1,000.00

|

20.00%

|

0.00%

|

$1,000.00

|

$93.75

|

$1,093.75

|

|

$1,000.00

|

10.00%

|

0.00%

|

$1,000.00

|

$93.75

|

$1,093.75

|

|

$1,000.00

|

0.00%

|

0.00%

|

$1,000.00

|

$93.75

|

$1,093.75

|

|

$1,000.00

|

−10.00%

|

−10.00%

|

$1,000.00

|

$93.75

|

$1,093.75

|

|

$1,000.00

|

−20.00%

|

−20.00%

|

$1,000.00

|

$93.75

|

$1,093.75

|

|

$1,000.00

|

−30.00%

|

−30.00%

|

$1,000.00

|

$93.75

|

$1,093.75

|

|

$1,000.00

|

−34.99%

|

−34.99%

|

$1,000.00

|

$93.75

|

$1,093.75

|

2

TABLE 2: A Knock-In Event OCCURS during an Observation Period.

|

Principal

Amount

of Securities

|

Percentage Change from the Initial Level to the Final Level of the Lowest Performing Underlying

|

Underlying Return of the Lowest Performing Underlying

|

Redemption Amount (Knock-In Event occurs)

|

Total Interest Payments on the Securities

|

|

$1,000.00

|

50.00%

|

0.00%

|

$1,000.00

|

(See table below)

|

|

$1,000.00

|

40.00%

|

0.00%

|

$1,000.00

|

|

|

$1,000.00

|

30.00%

|

0.00%

|

$1,000.00

|

|

|

$1,000.00

|

20.00%

|

0.00%

|

$1,000.00

|

|

|

$1,000.00

|

10.00%

|

0.00%

|

$1,000.00

|

|

|

$1,000.00

|

0.00%

|

0.00%

|

$1,000.00

|

|

|

$1,000.00

|

−10.00%

|

−10.00%

|

$900.00

|

|

|

$1,000.00

|

−20.00%

|

−20.00%

|

$800.00

|

|

|

$1,000.00

|

−30.00%

|

−30.00%

|

$700.00

|

|

|

$1,000.00

|

−40.00%

|

−40.00%

|

$600.00

|

|

|

$1,000.00

|

−50.00%

|

−50.00%

|

$500.00

|

|

|

$1,000.00

|

−60.00%

|

−60.00%

|

$400.00

|

|

|

$1,000.00

|

−70.00%

|

−70.00%

|

$300.00

|

|

|

$1,000.00

|

−80.00%

|

−80.00%

|

$200.00

|

|

|

$1,000.00

|

−90.00%

|

−90.00%

|

$100.00

|

|

|

$1,000.00

|

−100.00%

|

−100.00%

|

$0.00

|

Assuming the securities are not redeemed prior to the Maturity Date, expected total interest payments will depend on whether and when a Knock-In Event occurs.

|

Time of First Knock-In Event

|

Total Interest Payment on the Securities

|

|

|

From Trade Date to first Observation Date

|

$12.50

|

|

|

From first Observation Date to second Observation Date

|

$28.75

|

|

|

From second Observation Date to third Observation Date

|

$45.00

|

|

|

From third Observation Date to fourth Observation Date

|

$61.25

|

|

|

From fourth Observation Date to Valuation Date

|

$77.50

|

3

The total payment on the securities will be equal to the Redemption Amount applicable to an investor plus the applicable total interest payments on the securities.

Examples of Calculation of Redemption Amounts at Maturity

Example 1: A Knock-In Event occurs because on a trading day during an Observation Period, the closing level of one Underlying is equal to or less than its Knock-In Level; and the Final Level of the Lowest Performing Underlying is less than its Initial Level.

|

Underlying

|

Initial Level

|

Lowest closing level of the Underlying

during any Observation Period

|

Final Level

|

|

SPX

|

1410

|

1410.00 (100% of Initial Level)

|

1551.00 (110% of Initial Level)

|

|

RTY

|

810

|

526.50 (65% of Initial Level)

|

526.50 (65% of Initial Level)

|

Since the closing level of RTY on a trading day during an Observation Period is equal to or less than its Knock-In Level, a Knock-In Event occurs. RTY is also the Lowest Performing Underlying.

Therefore, the Underlying Return of the Lowest Performing Underlying will equal:

|

Final Level of RTY – Initial Level of RTY

Initial Level of RTY

|

; subject to a maximum of 0.00

|

= (526.50 – 810) / 810 = −0.35

The Redemption Amount = principal amount of the securities × (1 + Underlying Return of the Lowest Performing Underlying)

= $1,000 × (1 – 0.35) = $650

Example 2: A Knock-In Event occurs because on a trading day during an Observation Period, the closing level of one Underlying is equal to or less than its Knock-In Level; the closing level of the Lowest Performing Underlying on any trading day during every Observation Period is never equal to or less than its Knock-In Level; and the Final Level of the Lowest Performing Underlying is less than its Initial Level.

|

Underlying

|

Initial Level

|

Lowest closing level of the Underlying

during any Observation Period

|

Final Level

|

|

SPX

|

1410

|

916.50 (65% of Initial Level)

|

1551.00 (110% of Initial Level)

|

|

RTY

|

810

|

704.70 (87% of Initial Level)

|

704.70 (87% of Initial Level)

|

Since the closing level of SPX on a trading day during an Observation Period is equal to or less than its Knock-In Level, a Knock-In Event occurs. RTY is the Lowest Performing Underlying, even though its closing level on any trading day during any Observation Period is never equal to or less than its Knock-In Level.

Therefore, the Underlying Return of the Lowest Performing Underlying will equal:

|

Final Level of RTY – Initial Level of RTY

Initial Level of RTY

|

; subject to a maximum of 0.00

|

= (704.70 – 810) / 810 = −0.13

The Redemption Amount = principal amount of the securities × (1 + Underlying Return of the Lowest Performing Underlying)

= $1,000 × (1 – 0.13) = $870

4

Example 3: A Knock-In Event occurs because on a trading day during an Observation Period, the closing level of one Underlying is equal to or less than its Knock-In Level; and the Final Level of the Lowest Performing Underlying is greater than its Initial Level.

|

Underlying

|

Initial Level

|

Lowest closing level of the Underlying

during any Observation Period

|

Final Level

|

|

SPX

|

1410

|

916.50 (65% of Initial Level)

|

1551.00 (110% of Initial Level)

|

|

RTY

|

810

|

729.00 (90% of Initial Level)

|

972.00 (120% of Initial Level)

|

Since the closing level of SPX on a trading day during an Observation Period is equal to or less than its Knock-In Level, a Knock-In Event occurs. SPX is also the Lowest Performing Underlying.

Therefore, the Underlying Return of the Lowest Performing Underlying will equal:

|

Final Level of SPX – Initial Level of SPX

Initial Level of SPX

|

; subject to a maximum of 0.00

|

= (1551.00 – 1410) / 1410 = 0.10

BUT 0.10 is greater than the maximum of 0.00, so the Underlying Return of the Lowest Performing Underlying is 0.00.

The Redemption Amount = principal amount of the securities × (1 + Underlying Return of the Lowest Performing Underlying)

= $1,000 × (1 + 0.00) = $1,000

Example 4: A Knock-In Event does not occur during any Observation Period.

|

Underlying

|

Initial Level

|

Lowest closing level of the Underlying

during any Observation Period

|

Final Level

|

|

SPX

|

1410

|

1226.70 (87% of Initial Level)

|

1551.00 (110% of Initial Level)

|

|

RTY

|

810

|

712.80 (88% of Initial Level)

|

891.00 (110% of Initial Level)

|

Since the closing level of each Underlying on any trading day during every Observation Period was never equal to or less than its Knock-In Level, a Knock-In Event does not occur.

Therefore, the Redemption Amount equals $1,000.

5

Selected Risk Considerations

An investment in the securities involves significant risks. Investing in the securities is not equivalent to investing directly in the Underlyings. These risks are explained in more detail in the “Risk Factors” section of the accompanying product supplement.

|

|

•

|

YOU MAY RECEIVE LESS THAN THE PRINCIPAL AMOUNT AT MATURITY — You may receive less at maturity than you originally invested in the securities, or you may receive nothing, excluding any accrued or unpaid interest. If a Knock-In Event occurs and the Final Level of the Lowest Performing Underlying is less than its Initial Level, you will not receive the maximum amount of interest payable on the securities and you will be fully exposed to any depreciation in the Lowest Performing Underlying. In this case, the Redemption Amount you will be entitled to receive will be less than the principal amount of the securities and you could lose your entire investment. It is not possible to predict whether a Knock-In Event will occur and, in the event that there is a Knock-In Event, whether and by how much the Final Level of the Lowest Performing Underlying will decrease in comparison to its Initial Level. Any payment on the securities is subject to our ability to pay our obligations as they become due.

|

|

|

•

|

THE SECURITIES WILL NOT PAY MORE THAN THE PRINCIPAL AMOUNT, PLUS ACCRUED AND UNPAID INTEREST AT THE APPLICABLE RATE, AT MATURITY OR UPON EARLY REDEMPTION — The securities will not pay more than the principal amount, plus accrued and unpaid interest at the Applicable Rate, at maturity or upon early redemption. If the Final Level of each Underlying is greater than its respective Initial Level (regardless of whether a Knock-In Event has occurred), you will not receive the appreciation of either Underlying. Assuming the securities are held to maturity and the term of the securities is exactly 15 months, the maximum amount payable with respect to the securities will not exceed $1,093.75 for each $1,000 principal amount of the securities.

|

|

|

•

|

THE SECURITIES ARE SUBJECT TO THE CREDIT RISK OF CREDIT SUISSE — Although the return on the securities will be based on the performance of the Underlyings, the payment of any amount due on the securities, including any applicable interest payments, early redemption payment or payment at maturity, is subject to the credit risk of Credit Suisse. Investors are dependent on our ability to pay all amounts due on the securities and, therefore, investors are subject to our credit risk. In addition, any decline in our credit ratings, any adverse changes in the market’s view of our creditworthiness or any increase in our credit spreads is likely to adversely affect the value of the securities prior to maturity.

|

|

|

•

|

IF A KNOCK-IN EVENT OCCURS DURING ANY OBSERVATION PERIOD, THE APPLICABLE RATE FOR THE CORRESPONDING QUARTERLY INTEREST PERIOD AND EACH SUBSEQUENT INTEREST PERIOD WILL BE 1.0% PER ANNUM — If a Knock-In Event occurs during any Observation Period, the Applicable Rate for the corresponding quarterly interest period and each subsequent interest period will be 1.0% per annum. For example, if a Knock-In Event occurs during the period from the Trade Date to the first Observation Date, the Applicable Rate per annum for each interest period will be 1.0% and the maximum amount of interest you will be entitled to receive, assuming the term of the securities is exactly 15 months, will not exceed $12.50 per $1,000 principal amount of the securities.

|

|

|

•

|

THE REDEMPTION AMOUNT PAYABLE AT MATURITY WILL BE LESS THAN THE PRINCIPAL AMOUNT OF THE SECURITIES EVEN IF A KNOCK-IN EVENT OCCURS WITH RESPECT TO ONLY ONE UNDERLYING AND THE FINAL LEVEL OF ONLY ONE UNDERLYING IS LESS THAN ITS INITIAL LEVEL — Even if on a trading day during any Observation Period the closing level of only one Underlying is equal to or less than its Knock-In Level, a Knock-In Event will have occurred. In this case, the Redemption Amount payable at maturity will be less than the principal amount of the securities if, in addition to the occurrence of a Knock-In Event, the Final Level of at least one Underlying is less than its Initial Level. This will be true even if on any trading day during every Observation Period the closing level of the Lowest Performing Underlying was never equal to or less than its Knock-In Level.

|

|

|

•

|

THE SECURITIES ARE SUBJECT TO A POTENTIAL EARLY REDEMPTION, WHICH WOULD LIMIT YOUR ABILITY TO ACCRUE INTEREST OVER THE FULL TERM OF THE SECURITIES —

|

6

The securities are subject to a potential early redemption. Prior to maturity, the securities may be redeemed on any Interest Payment Date scheduled to occur on or after June 5, 2013, upon notice on or before the relevant Early Redemption Notice Date. If the securities are redeemed prior to the Maturity Date, you will be entitled to receive the principal amount of your securities and any accrued but unpaid interest payable at the Applicable Rate on such Interest Payment Date. In this case, you will lose the opportunity to continue to accrue and be paid interest from the date of Early Redemption to the scheduled Maturity Date. If the securities are redeemed prior to the Maturity Date, you may be unable to invest in other securities with a similar level of risk that yield as much interest as the securities.

|

|

•

|

SINCE THE SECURITIES ARE LINKED TO THE PERFORMANCE OF MORE THAN ONE UNDERLYING, YOU WILL BE FULLY EXPOSED TO THE RISK OF FLUCTUATIONS IN THE LEVEL OF EACH UNDERLYING — Since the securities are linked to the performance of more than one Underlying, the securities will be linked to the individual performance of each Underlying. Because the securities are not linked to a basket, in which the risk is mitigated and diversified among all of the components of a basket, you will be exposed to the risk of fluctuations in the levels of the Underlyings to the same degree for each Underlying. For example, in the case of securities linked to a basket, the return would depend on the weighted aggregate performance of the basket components as reflected by the basket return. Thus, the depreciation of any basket component could be mitigated by the appreciation of another basket component, to the extent of the weightings of such components in the basket. However, in the case of securities linked to the lowest performing Underlying, the individual performance of each Underlying is not combined to calculate your return and the depreciation of any Underlying is not mitigated by the appreciation of any other Underlying. Instead, the Redemption Amount payable at maturity depends on the lowest performing of the Underlyings to which the securities are linked.

|

|

|

•

|

THE SECURITIES ARE LINKED TO THE RUSSELL 2000® INDEX AND ARE SUBJECT TO THE RISKS ASSOCIATED WITH SMALL-CAPITALIZATION COMPANIES — The Russell 2000® Index is composed of equity securities issued by companies with relatively small market capitalization. These equity securities often have greater stock price volatility, lower trading volume and less liquidity than the equity securities of large-capitalization companies, and are more vulnerable to adverse business and economic developments than those of large-capitalization companies. In addition, small-capitalization companies are typically less established and less stable financially than large-capitalization companies. These companies may depend on a small number of key personnel, making them more vulnerable to loss of personnel. Such companies tend to have smaller revenues, less diverse product lines, smaller shares of their product or service markets, fewer financial resources and less competitive strengths than large-capitalization companies and are more susceptible to adverse developments related to their products. Therefore, the Russell 2000® Index may be more volatile than it would be if it were composed of equity securities issued by large-capitalization companies.

|

|

|

•

|

CERTAIN BUILT-IN COSTS ARE LIKELY TO ADVERSELY AFFECT THE VALUE OF THE SECURITIES PRIOR TO MATURITY — While the payment at maturity described in this pricing supplement is based on the full principal amount of your securities, the original issue price of the securities includes the agent’s commission and the cost of hedging our obligations under the securities through one or more of our affiliates. As a result, the price, if any, at which Credit Suisse (or its affiliates), will be willing to purchase securities from you in secondary market transactions, if at all, will likely be lower than the original issue price, and any sale prior to the Maturity Date could result in a substantial loss to you. The securities are not designed to be short-term trading instruments. Accordingly, you should be able and willing to hold your securities to maturity.

|

|

|

•

|

LACK OF LIQUIDITY — The securities will not be listed on any securities exchange. Credit Suisse (or its affiliates) intends to offer to purchase the securities in the secondary market but is not required to do so. Even if there is a secondary market, it may not provide enough liquidity to allow you to trade or sell the securities when you wish to do so. Because other dealers are not likely to make a secondary market for the securities, the price at which you may be able to trade your securities is likely to depend on the price, if any, at which Credit Suisse (or its affiliates) is willing to buy the securities. If you have to sell your securities prior to maturity, you may not be able to do so or you may have to sell them at a substantial loss.

|

7

|

|

•

|

POTENTIAL CONFLICTS — We and our affiliates play a variety of roles in connection with the issuance of the securities, including acting as calculation agent and hedging our obligations under the securities. In performing these duties, the economic interests of the calculation agent and other affiliates of ours are potentially adverse to your interests as an investor in the securities.

|

|

|

•

|

MANY ECONOMIC AND MARKET FACTORS WILL AFFECT THE VALUE OF THE SECURITIES — In addition to the levels of the Underlyings on any trading day during any Observation Period, the value of the securities will be affected by a number of economic and market factors that may either offset or magnify each other, including:

|

|

|

o

|

the expected volatility of the Underlyings;

|

|

|

o

|

the time to maturity of the securities;

|

|

|

o

|

the Early Redemption feature, which would limit the value of the securities;

|

|

|

o

|

interest and yield rates in the market generally;

|

|

|

o

|

investors’ expectations with respect to the rate of inflation;

|

|

|

o

|

geopolitical conditions and a variety of economic, financial, political, regulatory or judicial events that affect the components comprising the Underlyings, or markets generally and which may affect the levels of the Underlyings; and

|

|

|

o

|

our creditworthiness, including actual or anticipated downgrades in our credit ratings.

|

Some or all of these factors may influence the price that you will receive if you choose to sell your securities prior to maturity. The impact of any of the factors set forth above may enhance or offset some or all of any change resulting from another factor or factors.

|

|

•

|

NO OWNERSHIP RIGHTS RELATING TO THE UNDERLYINGS — Your return on the securities will not reflect the return you would realize if you actually owned the equity securities comprising Underlyings. The return on your investment, which is based on the percentage change in the Underlyings, is not the same as the total return you would receive based on the purchase of the equity securities that comprise the Underlyings.

|

|

|

•

|

NO DIVIDEND PAYMENTS OR VOTING RIGHTS — As a holder of the securities, you will not have voting rights or rights to receive cash dividends or other distributions or other rights with respect to the equity securities that comprise the Underlyings.

|

Supplemental Use of Proceeds and Hedging

We intend to use the proceeds of this offering for our general corporate purposes, which may include the refinancing of existing debt outside Switzerland. Some or all of the proceeds we receive from the sale of the securities may be used in connection with hedging our obligations under the securities through one or more of our affiliates. Such hedging or trading activities on or prior to the Trade Date and during the term of the securities (including on the Valuation Date) could adversely affect the value of the Underlyings and, as a result, could decrease the amount you may receive on the securities at maturity. For additional information, see “Supplemental Use of Proceeds and Hedging” in the accompanying product supplement.

8

The Underlying

The S&P 500® Index, published by Standard & Poor’s Financial Services LLC (“S&P”), is intended to provide a performance benchmark for the U.S. equity markets. The calculation of the level of the S&P 500® Index is based on the relative value of the aggregate market value of the common stocks of 500 companies as of a particular time as compared to the aggregate average market value of the common stocks of 500 similar companies during the base period of the years 1941 through 1943.

The S&P 500® Index is a float-adjusted index. Under float adjustment, the share counts used in calculating the S&P 500® Index reflect only those shares that are available to investors, not all of a company’s outstanding shares. Float adjustment excludes shares that are closely held by control groups, other publicly traded companies or government agencies.

Beginning on September 21, 2012, all share-holdings with a position greater than 5% of a stock’s outstanding shares, other than holdings by “block owners,” were removed from the float for purposes of calculating the S&P 500® Index. Generally, these “control holders” will include officers and directors, private equity, venture capital & special equity firms, other publicly traded companies that hold shares for control, strategic partners, holders of restricted shares, ESOPs, employee and family trusts, foundations associated with the company, holders of unlisted share classes of stock or government entities at all levels (other than government retirement/pension funds) and any individual person who controls a 5% or greater stake in a company as reported in regulatory filings. Holdings by block owners, such as depositary banks, pension funds, mutual funds & ETF providers, 401(k) plans of the company, government retirement/pension funds, investment funds of insurance companies, asset managers and investment funds, independent foundations and savings and investment plans, will ordinarily be considered part of the float. Shares held in a trust to allow investors in countries outside the country of domicile (e.g., ADRs, CDIs and Canadian exchangeable shares) are normally part of the float unless those shares form a control block. If a company has more than one class of stock outstanding, shares in an unlisted or non-traded class are treated as a control block.

For each stock, an investable weight factor (“IWF”) is calculated by dividing the available float shares by the total shares outstanding. Beginning on September 21, 2012, available float shares are defined as total shares outstanding less shares held by control holders. The S&P 500® Index is calculated by dividing the sum of the IWF multiplied by both the price and the total shares outstanding for each stock by the index divisor.

For additional information on the Underlying, see information set forth under “The Reference Indices—The S&P Indices—The S&P 500® Index” in the accompanying underlying supplement.

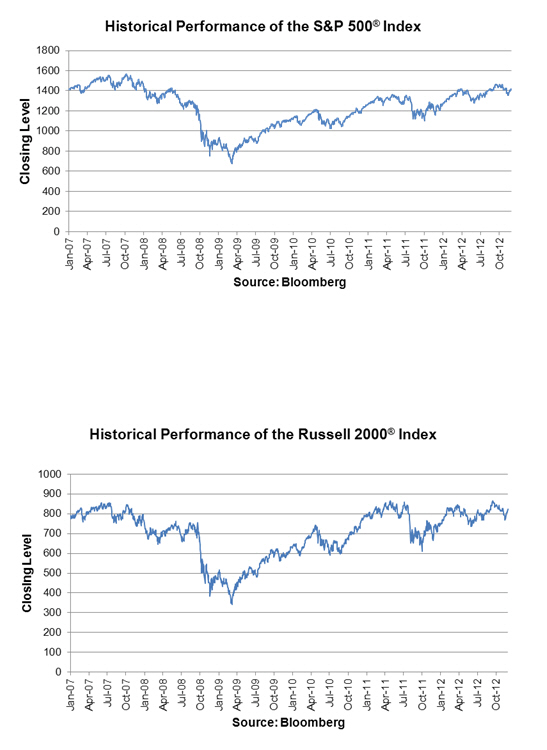

Historical Information

The following graphs set forth the historical performance of the Underlyings based on the closing level of each Underlying from January 1, 2007 through November 30, 2012. The closing level of the S&P 500® Index on November 30, 2012 was 1416.18. The closing level of the Russell 2000® Index on November 30, 2012 was 821.92. We obtained the closing levels below from Bloomberg, without independent verification. We make no representation or warranty as to the accuracy or completeness of the information obtained from Bloomberg. You should not take the historical levels of the Underlyings as an indication of future performance of the Underlyings or the securities. The levels of either of the Underlyings may decrease so that a Knock-In Event occurs and at maturity you will receive a Redemption Amount equal to less than the principal amount of the securities. Any payment on the securities is subject to our ability to pay our obligations as they become due. We cannot give you any assurance that the closing levels of the Underlyings will remain above their respective Knock-In Levels during any Observation Period. If on any trading day during any Observation Period, the closing level of either Underlying is equal to or less than its Knock-In Level, and the Final Level of the Lowest Performing Underlying is less than its Initial Level, you will lose money on your investment.

For additional information on the S&P 500® Index, see “The Reference Indices—The S&P® Indices—The S&P 500® Index” in the accompanying underlying supplement, and for additional information on the Russell 2000® Index, see “The Reference Indices—The Russell 2000® Index” in the accompanying underlying supplement.

9

10

Market Disruption Events

If the calculation agent determines that on any Observation Date, other than the Valuation Date, a market disruption event (as defined in the accompanying product supplement under “Description of the Securities—Market disruption events—For an equity-based reference index”) exists in respect of any Underlying or if such day is not a trading day (as defined in the accompanying product supplement under “Description of the Securities—Certain definitions”) for any Underlying, then the determination of the closing level for such Underlying on such Observation Date will be postponed to the first succeeding trading day for such Underlying on which the calculation agent determines that no market disruption event exists in respect of such Underlying, unless the calculation agent determines that a market disruption event exists in respect of such Underlying on each of the five trading days for such Underlying immediately following such Observation Date. In that case, the closing level for such Underlying on such Observation Date will be determined as of the fifth succeeding trading day for such Underlying following such Observation Date (such fifth trading day, the “calculation date”), notwithstanding the market disruption event in respect of such Underlying, and the calculation agent will determine the closing level for such Underlying on that calculation date in accordance with the formula for and method of calculating such Underlying last in effect prior to the commencement of the market disruption event in respect of such Underlying using exchange traded prices on the relevant exchanges (as determined by the calculation agent in its sole discretion) or, if trading in any component comprising such Underlying has been materially suspended or materially limited, its good faith estimate of the prices that would have prevailed on such exchanges (as determined by the calculation agent in its sole discretion) but for the suspension or limitation, as of the valuation time on that calculation date, of each component comprising the Underlying (subject to the provisions described under “Description of the Securities—Changes to the calculation of a reference index” in the accompanying product supplement).

The determination of the closing level for any Underlying not affected by a market disruption event on an Observation Date (other than the Valuation Date) or by an Observation Date (other than the Valuation Date) not being a trading day for such Underlying will occur on such Observation Date. The Valuation Date for any Underlying not affected by a market disruption event will be the scheduled Valuation Date for such Underlying.

If the determination of the closing level for any Underlying on an Observation Date other than the Valuation Date is postponed as a result of a market disruption event as described above to a date on or after the corresponding Interest Payment Date, then such corresponding Interest Payment Date will be postponed to the business day following the latest date to which such determination is so postponed for any Underlying.

If the Valuation Date for any Underlying is postponed as a result of a market disruption event as described in the accompanying product supplement or because the scheduled Valuation Date is not an underlying business day for any Underlying, then the Maturity Date will be postponed to the fifth business day following the latest Valuation Date for any Underlying.

11

Material U.S. Federal Income Tax Considerations

The amount of the stated interest rate on the security that constitutes interest on the Deposit (as defined in the accompanying product supplement) equals 0.3352%, and the remaining balance constitutes the Put Premium (as defined in the accompanying product supplement). Please refer to "Material United States Federal Income Tax Considerations" in the accompanying product supplement for a discussion summarizing material U.S. federal income tax consequences of owning and disposing of the securities that may be relevant to holders of the securities that acquire the securities as part of the original issuance of the securities.

Supplemental Plan of Distribution (Conflicts of Interest)

Under the terms and subject to the conditions contained in a distribution agreement dated May 7, 2007, as amended, which we refer to as the distribution agreement, we have agreed to sell the securities to CSSU. The distribution agreement provides that CSSU is obligated to purchase all of the securities if any are purchased.

CSSU proposes to offer the securities at the offering price set forth on the cover page of this pricing supplement and will receive varying underwriting discounts and commissions of up to $2.50 per $1,000 principal amount of securities, for total underwriting discounts and commissions of $37.50. CSSU may re-allow some or all of the discount on the principal amount per security on sales of such securities by other brokers or dealers. If all of the securities are not sold at the initial offering price, CSSU may change the public offering price and other selling terms.

In addition, Credit Suisse International, an affiliate of Credit Suisse, may pay referral fees of up to $5.50 per $1,000 principal amount of securities in connection with the distribution of the securities. An affiliate of Credit Suisse has paid or may pay in the future a fixed amount to broker dealers in connection with the costs of implementing systems to support these securities.

We expect to deliver the securities against payment for the securities on the Settlement Date indicated above, which may be a date that is greater than three business days following the Trade Date. Under Rule 15c6-1 of the Securities Exchange Act of 1934, as amended, trades in the secondary market generally are required to settle in three business days, unless the parties to a trade expressly agree otherwise. Accordingly, if the Settlement Date is more than three business days after the Trade Date, purchasers who wish to transact in the securities more than three business days prior to the Settlement Date will be required to specify alternative settlement arrangements to prevent a failed settlement.

The agent for this offering, CSSU, is our affiliate. In accordance with FINRA Rule 5121, CSSU may not make sales in this offering to any of its discretionary accounts without the prior written approval of the customer. A portion of the net proceeds from the sale of the securities will be used by CSSU or one of its affiliates in connection with hedging our obligations under the securities.

For further information, please refer to “Underwriting (Conflicts of Interest)” in the accompanying product supplement.

12

Credit Suisse